Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Franklin Covey 2003 Annual Report Financial Highlights 1

Financial Highlights

AUGUST 31, 2003 2002 2001 2000 1999

In thousands, except per share data

Income Statement DataNet sales $307,160 $332,998 $439,781 $522,630 $509,351 Net loss from continuing

operations (45,253) (96,466) (13,196) (7,472) (14,689) Net loss attributable to

common shareholders (53,988) (109,266) (19,236) (12,414) (10,647) Diluted loss per share (2.69) (5.49) (0.95) (0.61) (0.51)

Balance Sheet DataTotal assets $259,741 $304,738 $536,480 $592,479 $623,303 Long-term obligations of

continuing operations 5,116 4,923 92,858 65,139 5,602 Shareholders’ equity 185,800 234,555 309,882 374,053 378,434

Common Stock FIRST SECOND THIRD FOURTHPrice Range QUARTER QUARTER QUARTER QUARTER

Fiscal 2003High $ 2.41 $ 1.79 $ 1.09 $ 2.00Low .90 .75 .65 1.05

Fiscal 2002High $ 7.00 $ 6.30 $ 3.70 $ 3.10Low 2.04 3.10 2.18 1.95

2 Letter from the Chairmen Franklin Covey 2003 Annual Report

To ourShareholders:

hortly after President John F. Kennedy’s speech to Congress in 1961 in which he committed the

nation, “to achieving the goal, before this decade is out, of landing a man on the moon and

returning him safely to the earth,” he gave another lesser-known speech in which he explained

what a stretch the achievement of that goal would be. He said:

“We choose to go to the moon not because [it] is easy, but because [it is]

hard, because that goal will serve to organize and measure the best of our

energies and skills …I realize that this is, in some measure, an act of faith

and vision, for we do not know what benefits await us. But if I were to say,

my fellow citizens, that we shall send to the moon, 240,000 miles away from

the control station in Houston, a giant rocket more than 300 feet tall, the

length of [a] football field, made of new metal alloys, some of which have not

yet been invented, capable of standing heat and stresses several times more

than have ever been experienced, fitted together with a precision better than

that of the finest watch, carrying all the equipment needed for propulsion,

guidance, control, communications, food and survival, on an untried mission,

to an unknown celestial body, and then return it safely to earth, re-entering

atmosphere at speeds of over 25,000 miles per hour, causing heat about half

that of the temperature of the sun and do all this, and do it right, and do it

first before this decade is out, then we must be bold.”

As audacious as that goal was, and as many setbacks as those pursuing it encountered, on July 21, 1969, twomen stood on the moon, and on July 24, they returned safely to the earth!

FranklinCovey’s Bold Goal. A little more than two years ago: the events of September 11th had justoccurred; the economy was experiencing a significant slowdown; we had more than $97 million in debt; ourrevenues had been declining due to a dramatic decline in sales of handheld devices and to organizations’slashing their investments in both our training and tools; and we had a heavy cost structure relative to ourrevenues. At this critical time, we set three seemingly bold goals for ourselves: (1) to put the Company on afirm financial foundation, and return to profitability; (2) to reposition ourselves in the marketplace; and (3) tobecome a prime example of the kind of performance culture which we help other organizations to achieve.Like NASA, however, the achievement of these goals would require us to do a number of things we had neverdone before.

S

Thanks to the focus, hard work, discipline, and bound-less energy, talent, and creativity of our associates, wemade significant progress toward achieving these goalsduring our fiscal year 2003:

1) Financially – After having implemented significantcost reductions in fiscal 2002, operating costs werereduced by an additional $89 million in fiscal 2003,and additional cost reduction actions were takenwhich will result in substantial additional costreductions during fiscal 2004; (2) after having paid-off substantially all of our debt in fiscal 2002, wemaintained high levels of liquidity during fiscal2003; (3) programs to improve our gross marginswere initiated, resulting in a small improvement ingross margin percentage for fiscal 2003, andestablished the foundation for additional improve-ments during fiscal 2004; and (4) revenues in ourOrganizational Solutions Business Unit and ourConsumer Business Unit moderated from acombined 24.3% rate of decline in fiscal 2002 to a7.7% decline in fiscal 2003.

2) Strategically – During fiscal 2003, we developed andlaunched new research-based individual andorganizational effectiveness training and facilitatedprocess offerings to appeal to line leaders whocontrol the strategic and operating agendas (and thetraining budgets) for their organizations. Sales ofthese offerings exceeded projections, and we estab-lished a significant pipeline of “pilot” engagementswith major organizations. We also expanded ournetwork of international licensees, entering into newagreements with high quality local training organiza-tions. Through the establishment or expansion ofdistribution relationships with major office super-store chains, FranklinCovey products are nowavailable in more than 2,000 office superstores,including: Staples, Office Depot, and Office Max,and we introduced a new sub-brand, “365 byFranklinCovey,” in more than 1,000 Target Stores.The impact of these strategic repositioning effortson revenues is expected to be felt beginning in thesecond quarter of fiscal 2004.

3) Organizationally – As a result of implementing ournew offerings, processes, and tools throughoutFranklinCovey, we achieved significant increases (as measured by our new “xQ” measurementinstrument) in the levels of clarity and enthusiasmfor our key goals, and in the extent to whichindividuals and teams throughout the organizationare focused on our key priorities.

As we now begin our 2004 fiscal year, we are morecommitted than ever to keeping our transformationgoing, and to achieving our financial, strategic, andorganizational goals:

Financial. Profitability, cash flow, and growth are thelife-blood of any business. They provide opportunitiesand growth for all stakeholders. In fiscal 2004, ourfinancial goals are to achieve all three. Specifically, weexpect to:

• Achieve significant improvements in year-over-yearoperating results in every quarter. The combinationof stabilizing revenue, increasing gross margins, anddeclining expenses is expected to result in significantimprovements in operating results for the year as awhole, and in each quarter.

• Achieve top line revenue growth in comparable unitsby the third quarter. With significant challenges toour core business over the past few years (compoundedby the long economic slowdown), it has been morethan 5 years since we have achieved top-line revenuegrowth on a truly “apples-to-apples” basis. By the thirdquarter of fiscal 2004, we expect to achieve comparable-operations revenue growth in most units.

• Generate positive cash flow and generate anoperating profit. A central objective has been toposition ourselves for a return to profitability as acompany. During fiscal 2003, we made significantprogress toward this objective, with a more than $70million reduction in operating losses. During fiscal2004, our goal is to generate positive cash flow and,with a small increase in revenue, to generate anoperating profit.

• Increase our liquidity to even higher levels. Twoyears ago, we committed to pay-off debt and tobuild cash reserves so that we would have a “longenough runway” to allow our restructuring andrepositioning efforts to gel, and to get the company“off the ground and into the air.” While we havemaintained high levels of liquidity over the past twoyears, the substantial improvement in operatingresults expected in fiscal 2004, together withimprovements in our inventory and receivables’ levelsand the possible sale of our real estate holdings,should substantially increase our liquidity levels byfiscal year-end.

Franklin Covey 2003 Annual Report Letter from the Chairmen 3

• Set the stage for achieving our targeted businessmodel in fiscal 2005. While we are encouraged bythe improvements in operating results achievedduring fiscal 2003, and by those expected to beachieved during fiscal 2004, our ultimate objective isto generate sufficient levels of profitability, that ourbusiness model is truly attractive. Through acombination of revenue stabilization, gross marginimprovement, and continued focus on expense levelsduring fiscal 2004, we expect to establish thefoundation for achieving attractive levels ofprofitability in fiscal 2005.

Strategic. The strength of any organization’s strategicposition in the marketplace is ultimately determined byits importance to its key customers. And, while ourstrategic repositioning efforts will be hard, and will taketime, we are confident that as we are successful inhelping others to achieve their own great missions, wewill develop deep, pervasive, ongoing relationships withthem. During fiscal 2004, our strategic goals are:

• To get 20, industry-leading organizations in fullrollout with our new solutions. Our clients havesome of the most worthy missions imaginable: fromattempting to cure the world’s major healthproblems, to making housing affordable to asignificantly greater share of the population, toproviding third-world countries with an increase intheir standard of living, to defending the free world.Our goal during fiscal 2004 is to build a solid,document-able, reference-able, track record ofhelping at least 20 of these major, industry-leadingorganizations to achieve their mission-criticalobjectives, and to leverage these relationships andresults to accelerate growth.

• Grow average “revenue per organizational client” inour top 100 accounts. As organizations adopt ourprinciples, tools, and processes pervasively, it changestheir work places. It helps redefine how individualswork, and how they work together with others toaccomplish common objectives. One of the mosttangible measures of our success in developing deep,pervasive, ongoing relationships with our clients willbe the growth in our revenue in our top 100 accounts.

• Increasing the number of committed users of theFranklinCovey Planning System and tools. At theindividual level, our experience and data indicatesthat no single thing increases personal focus andproductivity more than the consistent usage of theplanning methodologies and tools we offer. Over thepast years, however, changes in technology and inthe channels of distribution for paper-basedplanning systems have resulted in declines in oursales of planning tools. With expected increases in

the number of individuals trained, improvedcoordination between our major business units toassure that trained individuals remain committedusers of the planning methodologies and tools, ouraddition of software-based planning tools, and ourexpansion into office superstore and third-partyretail channels, we expect to arrest and begin toreverse the decline in sales of our paper-based andsoftware-based planning tools during fiscal 2004.

Organizational. Organizationally, we need to be amodel of the kind of high performance, value-creating,principle-centered culture which our clients can hope toachieve when they fully implement the solutions weoffer. As described earlier, during fiscal 2003, we madesubstantial gains (as measured by the xQ) in increasingour associates’ understanding of, and enthusiasm forachieving FranklinCovey’s dominant priorities. We alsoincreased the extent to which teams and individualsthroughout the organization are focusing their time andcollective efforts toward achieving these priorities.During fiscal 2004, each manager throughout thecompany will be responsible for implementing a specificpersonalized plan for further improving the focus andexecution ability of his/her team.

As with the space program 34 years ago, achieving thegoals we have set for ourselves will not be easy, it will behard. However, if we are going to accomplish thingsnever done before, “we must be bold.” We know that wewill face many challenges in our pursuit of these goals.However, as we focus the collective power, talent, andenergy of our associates and the resources of thecompany on implementing these changes, we areconfident in our ability to meet these challenges andaccomplish our goals.

We are grateful for your support, and look forward torealizing these goals together.

Sincerely,

Robert A. WhitmanChairman of the Board of Directors

Stephen R. CoveyVice-Chairman of the Board of Directors

Hyrum W. SmithVice-Chairman of the Board of Directors

4 Letter from the Chairmen Franklin Covey 2003 Annual Report

Form 10-K

6 Form 10-K Franklin Covey 2003 Annual Report

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K�� ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934 FOR THE FISCAL YEAR ENDED AUGUST 31, 2003

OR

�� TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGEACT OF 1934 FOR THE TRANSITION PERIOD FROM ______________ TO ______________

FRANKLIN COVEY CO.(Exact name of registrant as specified in its charter)

Utah 1-11107 87-0401551(State or other jurisdiction (Commission File No.) (IRS Employer

of incorporation) Identification No.)

2200 West Parkway BoulevardSalt Lake City, Utah 84119-2331

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (801) 817-1776

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class Name of Each Exchange on Which RegisteredCommon Stock, $.05 Par Value New York Stock Exchange

�� Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) ofthe Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.YES �� NO ��

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not containedherein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ��

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Act).YES �� NO ��

As of February 28, 2003, the aggregate market value of the Registrant’s Common Stock held by non-affiliates of theRegistrant was $14,087,150.

As of November 21, 2003, the Registrant had 19,926,837 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCEParts of the Registrant’s Proxy Statement for the Registrant’s Annual Meeting of Shareholders, which is scheduled

to be held on January 9, 2004, are incorporated by reference in Part III of this Form 10-K.

�

�

�

INDEX TO FORM 10-K

PART I 8Item 1. Business 8

General 8Franklin Covey Products 9

Paper Planners 9Electronic Solutions 9Binders 10Personal Development Products 10

Training and Productivity Solutions for Organizations 10

Training and EducationPrograms 11

Segment Information 12Retail Stores 12Catalog/e-Commerce 13Other Channels 13Organizational Solutions Group 13International Sales 14

Strategic Distribution Alliances 14Clients 14Competition 14

Training 14Products 15

Manufacturing and Distribution 15Trademarks, Copyrights and

Intellectual Property 16Employees 16Available Information 16

Item 2. Properties 17

Item 3. Legal Proceedings 17

Item 4. Submission of Matters to a Vote of Security Holders 17

PART II 68Item 5. Market for the Registrant’s

Common Equity and Related Shareholder Matters 68

Item 6. Selected Financial Data 68

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations 68

Item 7a. Quantitative and QualitativeDisclosures About Market Risk 69

Item 8. Financial Statements and Supplementary Data 69

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure 69

Item 9a. Controls and Procedures 69

PART III 70Item 10. Directors and Executive Officers

of the Registrant 70

Item 11. Executive Compensation 70

Item 12. Security Ownership of Certain BeneficialOwners and Management andRelated Stockholder Matters 70

Item 13. Certain Relationships and Related Transactions 71

Item 14. Principal Accountant Fees and Services 71

PART IV 72Item 15. Exhibits, Financial Statement Schedules

and Reports on Form 8-K 72(a) Documents Filed 72

1. Financial Statements 722. Exhibit List 72

(b) Reports on Form 8-K 73(c) Exhibits 73(d) Financial Statement Schedules 73

SIGNATURES 74

CERTIFICATIONS OF THE CEO & CFO 75-76

Franklin Covey 2003 Annual Report Form 10-K 7

PART I

Item 1. Business

GENERAL

Franklin Covey Co. (the “Company”, “we”, “us”, “our”or “FranklinCovey”) is an international learning andperformance solutions company dedicated to helpingorganizations and individuals focus on and execute theirhighest priorities. To achieve that goal, we providetraining and education programs, educational materials,publications, assessment and measurement instruments,implementation processes and tools. We have organizedour business to serve two main customer segments:organizations and individual consumers. We offersolutions for organizations through a combination ofassessment instruments, including the xQ (ExecutionQuotient™) Profile and the 7 Habits Profile, trainingcourses including FOCUS: Achieving Your HighestPriorities; Aligning Goals for Results; 7 Habits of HighlyEffective People, and implementation tools based onthe FranklinCovey Planning System including theFranklinCovey Planner, PDA (Personal Digital Assistants)devices like Palm®, PlanPlus for Microsoft Outlook®,wireless communication organizers, the Tablet PC andother tools. We measure the impact of training invest-ments for our clients through pre- and post- assessmentprofiles and return on investment analysis.

As noted above, one of our mainstay tools that assistsour clients in implementing effectiveness training is theFranklinCovey Planning System. The FranklinCoveyPlanning System implements our principle-basedtraining and learning by using tools such as theFranklinCovey Planner. The original FranklinCoveyPlanner consists of a paper-based, two-pages-per-dayplanning pages combined with a seven-ring binder, avariety of planning aids, monthly and annual calendarsand a personal management section. FranklinCoveyPlanning Pages can also be purchased in a variety offormats, including one-page-per-day and two-pages-per-week versions. We also offer a variety of forms andaccessories that allow our clients to expand and customizetheir FranklinCovey Planning System. A significantpercentage of FranklinCovey Planner users continue topurchase new planning pages each year, creatingsubstantial recurring sales.

We have developed additional FranklinCovey PlanningSystem tools to address the needs of more technology-oriented workers as well as those who require bothgreater mobility and ready access to large quantities ofdata. New FranklinCovey planning tools includePlanPlus™ for Microsoft Outlook software for desktopand handheld device usage, and TabletPlanner softwarefor Tablet PCs, both of which have won awards andcritical acclaim from the media. PlanPlus™ incorporatesFranklinCovey Planning productivity principles into theOutlook calendar and email system. TabletPlanner,developed in cooperation with Agilix Labs, includesscreen views similar to the paper-based FranklinCoveyPlanner, natural handwriting interface, the fullFranklinCovey Planning System with appointmentscheduling, prioritized daily and master tasks and dailynotes, digital note-taking and synchronization withOutlook Exchange and an e-Binder concept allowingthe collection of all important documents into one place.

We offer a selection of top-selling PDAs, including,several PalmOne™ (merger of Palm and Handspring)handheld wireless communication and planning devices,Hewlett-Packard’s® iPAQ™ Pocket PC®, and the newconverged devices that offer the best of both wirelessand handheld functionality. FranklinCovey markets the FranklinCovey Planning System componentsdirectly to organizations and individuals, through itscatalog, its retail stores, its e-commerce Internet site atwww.franklincovey.com and through third-partychannels. The FranklinCovey Planning System is nowalso available for the recently introduced Tablet PCthrough FranklinCovey TabletPlanner software.

The principles we teach in our curriculum have alsobeen published in book, audiotape and CD formats.Books sold by the Company include The 7 Habits ofHighly Effective People®, Principle-Centered Leadership,First Things First, The 7 Habits of Highly EffectiveFamilies, Nature of Leadership and Living the 7 Habits, allby Stephen R. Covey, The 10 Natural Laws of Time andLife Management, What Matters Most and The ModernGladiator by Hyrum W. Smith, The Power Principle byBlaine Lee, The 7 Habits of Highly Effective Teens bySean Covey and Business Think by Dave Marcum andSteve Smith. These books, as well as audiotape and CD audio versions of many of these products, are soldthrough general retail channels, as well as through our own catalog, our e-commerce Internet site atwww.franklincovey.com and our more than 150 retail stores.

8 Form 10-K Franklin Covey 2003 Annual Report

As noted above, we provide effectiveness solutions toorganizations in business, industry, government entities,communities, to schools and educational institutions,and to individuals. We sell services to organizations andschools through our own direct sales forces. We thendeliver training services to organizations, schools andindividuals in one of four ways:

1. FranklinCovey consultants provide on-site consultingor training classes for organizations and schools. Inthese situations, our consultant can tailor the curricu-lum to our client’s specific business and objectives.

2. We conduct public seminars in more than 130 citiesthroughout the United States, where organizationscan send their employees in smaller numbers.These public seminars are also marketed directly to individuals through our catalog, e-commerce web-site, retail stores, and by direct mail.

3. Our programs are also designed to be facilitated bylicensed professional trainers and managers in clientorganizations, reducing dependence on our profes-sional presenters, and creating continuing revenuethrough royalties and as participant materials arepurchased for trainees by these facilitators.

4. We also offer The 7 Habits of Highly Effective People®training course in online and CD-ROM formats.This self-paced e-learning alternative provides theflexibility that many organizations need to meet theneeds of various groups, managers or supervisorswho can’t get away for extended classroom trainingand executives who need a series of working sessionsover several weeks.

In fiscal 2003, we provided products and services to 90of the Fortune 100 companies and more than 75percent of the Fortune 500 companies. We also provideproducts and services to a number of U.S. and foreigngovernmental agencies, including the U.S. Departmentof Defense, as well as numerous educational institu-tions. More than 350,000 individuals were trainedduring the year ended August 31, 2003.

We also provide products, consulting and trainingservices internationally, either through directly operatedoffices, or through licensed providers. At August 31,2003, we had direct operations in Canada, Japan,Australia, Mexico, Brazil and the United Kingdom.We also had licensed operations in 55 countries.

Unless the context requires otherwise, all references tothe “Company”, “we”, “us”, “our” or to “FranklinCovey”herein refer to Franklin Covey Co. and each of itsoperating divisions and subsidiaries. The Company’sprincipal executive offices are located at 2200 WestParkway Boulevard, Salt Lake City, Utah 84119-2331and its telephone number is (801) 817-1776.

FRANKLINCOVEY PRODUCTS

An important principle taught in our productivitytraining is to have only one personal productivity systemand to have all of ones’ information in that one system.Based upon that principle, we developed theFranklinCovey Planner as one of the basic tools forimplementing the principles of our time managementsystem. The original FranklinCovey Planner consists ofa paper-based FranklinCovey planning system, a binderin which to carry it, various planning aids, weekly,monthly and annual calendars as well as personalmanagement sections. We offer a broad line of renewalplanners, forms and binders for the FranklinCoveyPlanner in various sizes and styles. For those clientswho use digital or electronic productivity systems, wealso offer a wide variety of electronic solutionsincorporating the same principles as the originalFranklinCovey Planner.

Paper Planners. Paper planning page refills areavailable for the FranklinCovey Planner in various sizesand styles and consist of daily or weekly formats, withAppointment Schedules, Prioritized Daily Task Lists,Monthly Calendars, Daily Notes, and personalmanagement pages for an entire year. FranklinCoveyPlanning Pages are offered in a number of designs toappeal to various customer segments. The Starter Pack,which includes personal management tabs and pages, aguide to using the planner, a pagefinder and weeklycompass cards, combined with a binder and storagebinder completes the FranklinCovey Planning System.

Electronic Solutions. We also offer time and lifemanagement methodology within a complete PersonalInformation Management (“PIM”) system through theFranklinCovey Planning Software program. This systemcan be used in conjunction with the paper-basedFranklinCovey Planner, electronic handheld organizersor used as a stand-alone planning and informationmanagement system. The FranklinCovey PlanningSoftware permits users to generate and print data onFranklinCovey paper that can be inserted directly intothe FranklinCovey Planner. The program operates inthe Windows® 95, 98, 2000 and NT operating systems.The FranklinCovey Planning Software includes all neces-sary software, related tutorials and reference manuals.

Franklin Covey 2003 Annual Report Form 10-K 9

We also offer PlanPlus™ for Microsoft® Outlook®software designed to operate as an extension toMicrosoft’s Outlook® software. This is intendedespecially for our corporate clients that have alreadystandardized on Microsoft® for group scheduling, butwish to make the FranklinCovey Planning Systemavailable to their employees without creating the needto support two separate systems. As this kind of exten-sion proves its value in the market, the FranklinCoveyPlanning Software extension model may be expanded toother platforms.

We are an OEM provider of the PalmOne™ hand-helds, which has become another successful planningtool that uses the FranklinCovey Planning Software andis sold through our FranklinCovey channels. In aneffort to combine the functionality of paper and thecapabilities of the Palm®, we introduced products thatcan add paper-based planning to these electronicplanners as well as binders and carrying cases specific tothe PalmOne™ product line. We have also expandedthe handheld line to include other electronic organizerswith the FranklinCovey Planning Software such as theiPAQ™ Pocket PC from Hewlett-Packard® and theTrio™ by Handspring®, now part of PalmOne™.

We also provide The 7 Habits of Highly Effective People®training course in online and CD-ROM versions. Thisedition delivers the rich, compelling content from the3-day classroom workshop in a flexible self-pacedversion via the Internet or CD-ROM that is availablewhen and where employees need it. The Online Editionis presented in a multi-media format with videosegments, voiceovers, a learning journal, interactiveexercises, and other techniques. Included with thecourse is a 360-Degree profile and e-Coaching.

The FranklinCovey Planning System is now alsoavailable for the recently introduced Tablet PC throughFranklinCovey TabletPlanner software. The softwarewas developed in cooperation with Agilix Labs andincludes the following features: screen views similar tothe paper-based FranklinCovey Planner, naturalhandwriting interface, the full FranklinCovey PlanningSystem with appointment scheduling, prioritized dailyand master tasks and daily notes, digital note-takingand synchronization with Outlook Exchange and an e-Binder concept allowing the collection of allimportant documents into one place.

Binders. To further customize the FranklinCoveyPlanning System, we offer binders and electronicorganizer accessories (briefcases, portfolios, businesstotes, messenger bags, etc.) in a variety of materials,styles and sizes. These materials include high qualityleathers, fabrics, synthetics and vinyl in a variety of colorand design options. Binder styles include zipperclosures, snap closures, and open formats with pocketconfigurations to accommodate credit cards, businesscards, checkbooks, electronic devices and writinginstruments. Most of the leather items are proprietaryFranklinCovey designs. However, we also offer productsfrom such leading manufacturers as Kenneth Cole.

Personal Development and Accessory Products.To supplement our principal products, we offer anumber of accessories and related products, includingbooks, videotapes and audio cassettes focused on timemanagement, leadership, personal improvement andother topics. We also market a variety of content-basedpersonal development products. These products includebooks, audio learning systems such as multi-tape, CDsand workbook sets, CD-ROM software products,calendars, posters and other specialty name brand items.We offer numerous accessory forms through our FormsWizard software, which allows customization of forms,including check registers, spreadsheets, stationery,mileage logs, maps, menu planners, shopping lists andother information management and project planningforms. Our accessory products and forms are generallyavailable in all the FranklinCovey Planner sizes.

TRAINING AND PRODUCTIVITYSOLUTIONS FOR ORGANIZATIONS

FranklinCovey is a leading provider of effectivenesstraining, productivity tools and assessment services fororganizations including corporations, Government, edu-cation and non-profit firms. These services are marketedand delivered world-wide through our OrganizationalSolutions Business Unit (OSBU), which consists oftalented consultants, selected through a competitive anddemanding process, and sales professionals.

10 Form 10-K Franklin Covey 2003 Annual Report

FranklinCovey currently employs 94 training consult-ants in major metropolitan areas of the United States,with an additional 19 training consultants outside of theUnited States. Our training consultants are selectedfrom a large number of experienced applicants. Theseconsultants generally have several years of trainingand/or consulting experience and are known for theirexcellent presentation skills. Once selected, the trainingconsultant goes through a rigorous training programincluding multiple live presentations. The trainingprogram ultimately results in the Company’s certifica-tion of the consultant. FranklinCovey believes that thecaliber of its training consultants has helped build itsreputation for providing high quality seminars. TheOSBU can also help organizational clients diagnoseinefficiencies in their organization and design the corecomponents of a client’s organizational solutions. Thenew xQ Survey is an exclusive FranklinCovey assess-ment tool that gathers information, from an employeeperspective, on how well organizational goals areunderstood and are being carried out. The surveyquestions, administered through a Web-based system,probe for details to uncover underlying focus andteamwork barriers or issues.

FranklinCovey’s OSBU is organized in geographicregional sales teams in order to assure that both theconsultant and the client sales professional participate inthe development of new business and the assessment ofclient needs. Consultants are then entrusted with theactual delivery of content, seminars, processes and othersolutions. Consultants follow up with client serviceteams, working with them to develop lasting clientimpact and ongoing business opportunities.

Training and Education Programs. We offer a range oftraining programs designed to measurably improve theeffectiveness of individuals and organizations. Ourprograms are oriented to address personal, interper-sonal, managerial and organizational needs. In addition,we believe that our learning process provides anengaging and behavior-changing experience, whichfrequently generates additional business. During fiscalyear 2003, more than 350,000 individuals were trainedusing the Company’s curricula in its single andmultiple-day workshops and seminars.

Our single-day FOCUS: Achieving Your HighestPriorities workshop teaches productivity skills integratedwith a powerful planning system to help individualsclarify, focus on, and execute their highest priorities,both personally and professionally. This seminar isconducted by our training consultants for employees ofclients and in public seminars throughout the UnitedStates and in many foreign countries. The single-dayAligning Goals for Results workshop helps managersidentify the highest priorities for their teams and thenlead those teams to execute tasks day-after-day.

We also deliver multiple-day workshops, primarily inthe Leadership area. Included in these offerings is thethree-day 7 Habits workshop based upon the materialpresented in The 7 Habits of Highly Effective People®.The 7 Habits workshop provides the foundation forcontinued client relationships and generates morebusiness as the content and application tools aredelivered deeper into the client’s organization.Additionally, a three-day 4 Roles of Leadership course isoffered, which focuses on the managerial aspects ofclient needs. FranklinCovey Leadership Week consistsof a five-day session focused on materials fromFranklinCovey’s The 7 Habits of Highly Effective People®and The 4 Roles of Leadership courses. FranklinCoveyLeadership Week is reserved for supervisory levelmanagement of our corporate clients. As a part of theweek’s agenda, executive participants plan and designstrategies to successfully implement key organizationalgoals or initiatives.

In addition to providing consultants and presenters, wealso train and certify client facilitators to teach selectedFranklinCovey workshops within their organizations.We believe client-facilitated training is important to ourfundamental strategy of creating pervasive on-goingclient impact and revenue streams. After having beencertified, client facilitators can purchase manuals,profiles, planners and other products to conducttraining workshops within their organization, generallywithout us repeating the sales process. This createsprograms which have an on-going impact on ourcustomers and which generate annuity-type revenues.This is aided by the fact that curriculum content in onecourse leads the client to additional participation inother Company courses. Since 1988, we have trainedmore than 20,000 client facilitators. Client facilitatorsare certified only after graduating from one of ourcertification workshops and completing post-coursecertification requirements.

Franklin Covey 2003 Annual Report Form 10-K 11

We regularly sponsor public seminars in cities through-out the United States and in several foreign countries.The frequency of seminars in each city or countrydepends on the concentration of our clients and thelevel of promotion and resulting demand, and generallyranges from semi-monthly to quarterly. Our smallerinstitutional clients often utilize the public seminars totrain their employees.

In April 2002, we introduced The 7 Habits of HighlyEffective People® training course in online and CD-ROM versions. The need for reaching more employeesfaster and more inexpensively are the key drivers behindthe growth of e-learning in the marketplace. The 7Habits Online Edition addresses that need, offering aflexible alternative to classroom training.

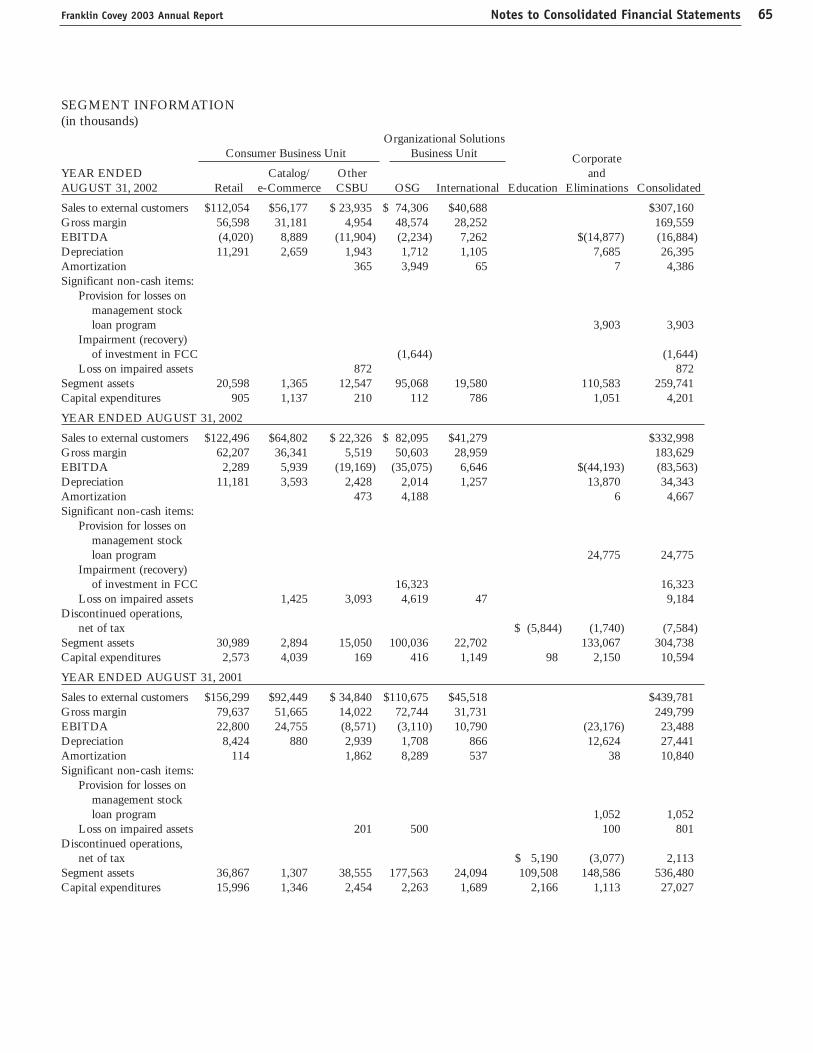

SEGMENT INFORMATION

The following table sets forth, for the periods indicated,the Company’s revenue from external customers foreach of its operating segments:

2003 2002 2001

Consumer Business Unit Retail Stores $112,054 $122,496 $156,299Catalog / e-commerce 56,177 64,802 92,449Other 23,935 22,326 34,840

Total CBU 192,166 209,624 283,588

Organizational Solutions Business UnitOrganizational Solutions

Group 74,306 82,095 110,675International 40,688 41,279 45,518

Total OSBU 114,994 123,374 156,193

Total $307,160 $332,998 $439,781

We market products and services to organizations,schools and individuals both domestically andinternationally through FranklinCovey retail stores,catalogs, www.franklincovey.com, our organizationaland educational sales forces and other distributionchannels. Additional financial information related toour operating segments, as well as geographical infor-mation can be found in the notes to our consolidatedfinancial statements (Note 20).

Retail Stores. Beginning in late 1985, we began a retailstrategy by opening retail stores in areas of high clientdensity. The initial stores were generally located inlower traffic destination locations. We have since revisedour strategy by locating retail stores in high-traffic retailcenters, primarily large shopping centers and malls, toserve existing clients and to attract increased numbersof walk-in clients. Our retail stores average approxi-mately 1,900 square feet. Our retail strategy focuses on providing high quality client service at the point ofsale. We believe this approach increases clientsatisfaction as well as the frequency and volume ofpurchases. At August 31, 2003, FranklinCovey had 153 domestic retail stores located in 37 states and theDistrict of Columbia.

We believe that our retail stores serve as attractivedistribution centers for existing clients and alsoencourage walk-in traffic and impulse buying. Storeclients are also an excellent source of participants forFranklinCovey’s public seminars. The stores alsoprovide the opportunity to assess client reaction to newproduct offerings and to test-market new products.

We believe that our retail stores have an upscale imageconsistent with our marketing strategy. Products areattractively presented and displayed with an emphasison integration of related products and accessories.Stores are staffed with a manager, an assistant managerand additional sales personnel as needed. These salesassociates have been trained to use the originalFranklinCovey Planning System, as well as the variouselectronic versions we offer, enabling them to assist andadvise clients in selection and use of our products.During peak periods, additional personnel are added topromote prompt and courteous client service.

We closed 22 retail stores in the United States and 10in international locations during fiscal year 2003 andintend to close additional stores during fiscal 2004.These closures are comprised of unprofitable stores andstores located in markets where the Company hasmultiple retail operations. The Company may also closeadditional retail store locations if future analysisdemonstrates that operating performance may beimproved through further retail store closures.

12 Form 10-K Franklin Covey 2003 Annual Report

Catalog/e-Commerce. We periodically mail catalogs toour clients, including a fall catalog, holiday catalogs,spring and summer catalogs timed to coincide withplanner renewals and catalogs related to special events,such as store openings or new product offerings. Catalogsmay be targeted to specific geographic areas or usergroups as appropriate. Catalogs are typically printed infull color with an attractive selling presentation high-lighting product benefits and features. We also marketthe FranklinCovey Planning System through our e-commerce Internet site at www.franklincovey.com.Customers may order catalogs and other marketingmaterials as well as the Company’s product line throughthis Internet portal.

During fiscal 2001, we entered into a long-termcontract with EDS of Dallas, Texas, to provide a largepart of our customer relationship management (CRM)in servicing our Catalog and e-Commerce customers.We use EDS to maintain a client service department,which clients may call toll-free, 24 hours a day, Mondaythrough Saturday, to inquire about a product or to placean order. Through a computerized order entry system,client representatives have access to client preferences,prior orders, billings, shipments and other informationon a real-time basis. Each of the more than 125customer service representatives has the authority toimmediately solve client service problems.

The integrated CRM system provided by EDS allowsorders from our customers to be processed through itswarehousing and distribution systems. Clientinformation stored within the order entry system is alsoused for additional purposes, including target marketingof specific products to existing clients and site selectionfor Company retail stores. We believe that the orderentry system helps assure client satisfaction throughboth rapid delivery and accurate order shipment.

Other Channels. We have an alliance with theMeadWestvaco to sell our products through thecontract stationer channel. MeadWestvaco wholesalesproducts to contract stationer businesses such as BoiseCascade, Office Express and Staples, which then selloffice products through catalog order entry systems tobusinesses and organizations. MeadWestvaco alsorepresents FranklinCovey in the office superstorecategory by wholesaling the FranklinCovey PlanningSystem to Staples, Office Depot and OfficeMax. Wealso recently entered into an agreement with TargetStores, in which we designed a new line of paperplanning products branded under the “365 byFranklinCovey” under-brand label.

Organizational Solutions Group. Our sales professionalsmarket training, consulting and measurement services toinstitutional clients and public seminar clients.

We employ 100 sales professionals and business devel-opers located in six major metropolitan areas throughoutthe United States who sell integrated offerings toinstitutional clients. We also employ an additional 54sales professionals and business developers outside ofthe United States in six countries. Our sales profes-sionals have selling experience prior to employment bythe Company and are trained and evaluated in theirrespective sales territories. Sales professionals typicallycall upon persons responsible for corporate employeetraining, such as corporate training directors or humanresource officers. Increasingly, sales professionals alsocall upon line leaders. Our sales professionals workclosely with training consultants in their territories toschedule and tailor seminars and workshops to meetspecific objectives of institutional clients.

We also employ 94 training consultants throughout the United States, who present institutional and public seminars in their respective territories, and anadditional 19 training consultants outside of the United States. Training consultants work with salesprofessionals and institutional clients to incorporate aclient’s goals, policies and objectives in seminars andpresent ways that employee goals may be aligned withthose of the institution.

Public seminars are planned, implemented and coor-dinated with training consultants by a staff of marketingand administrative personnel at the Company’scorporate offices. These seminars provide training fororganizations and the general public and are also usedas a marketing tool for attracting corporate and otherinstitutional clients. Corporate training directors areoften invited to attend public seminars to preview theseminar content prior to engaging FranklinCovey totrain in-house employees. Smaller institutional clientsoften enroll their employees in public seminars when aprivate seminar is not cost effective. In the publicseminars, attendees are also invited to provide names ofpotential persons and companies who may be interestedin our seminars and products. These referrals aregenerally used as prospects for our sales professionals.

Franklin Covey 2003 Annual Report Form 10-K 13

We also provide The 7 Habits of Highly EffectiveTeens as a workshop or as a year-long curriculum toschools and school districts and other organizationsworking with youth. Based on the 7 Habits of HighlyEffective Teens book, it helps to teach students andteachers better studying skills, learning habits, andinterpersonal development. In December 2001, we soldthe stock of Premier Agendas to School Specialty.Pursuant to a license from FranklinCovey, Premier isexpected to continue to expose over 20 million K-12students to FranklinCovey’s world-renowned 7 Habitscontent. We retained the educator leadership andeffectiveness training portion of Premier’s business.

International Sales. We provide products, training andprinting services internationally through Company-owned and licensed operations. We have Company-owned operations and offices in Australia, Brazil,Canada, Japan, Mexico and the United Kingdom. Wealso have licensed operations in Argentina, Bahamas,Belgium, Bermuda, Bulgaria, Chile, China, Colombia,Croatia, Czech Republic, Denmark, Ecuador, Egypt,Estonia, Finland, France, Germany, Greece, Greenland,Hong Kong, Hungary, India, Indonesia, Israel, Italy,Korea, Latvia, Lebanon, Lithuania, Luxembourg, Malaysia,Netherlands, Nigeria, Norway, Panama, Philippines,Poland, Portugal, Puerto Rico, Russia, Saudi Arabia,Singapore, Slovak Republic, Slovenia, South Africa,Spain, Sri Lanka, Sweden, Taiwan, Thailand, Trinidad/Tobago, Turkey, UAE, Uruguay, and Venezuela. Thereare also licensee retail operations in Hong Kong, Japan,Singapore and Taiwan. Our seven most popular books,The 7 Habits of Highly Effective People®, Principle-Centered Leadership, The 10 Natural Laws of Timeand Life Management, First Things First, The PowerPrinciple, The 7 Habits of Highly Effective Familiesand The 7 Habits of Highly Effective Teens arecurrently published in multiple languages.

STRATEGIC DISTRIBUTION ALLIANCES

We have created strategic alliances with innovative andrespected organizations in an effort to develop effectivedistribution of our products and services. The principaldistribution alliances currently maintained by FranklinCoveyare: Simon & Schuster and Saint Martin’s Press inpublishing books for the Company; Lumicore topromote and facilitate Dr. Covey’s personal appearancesand teleconferences; Nightingale-Conant to market anddistribute audio and video tapes of the Company’s booktitles; MeadWestvaco to market and distribute selectedFranklinCovey Planners and accessories through theAt-A-Glance catalog office supply channels and in theoffice superstores channel; PalmOne(TM)to serve asthe official training organization for its PalmOne™products; distribution agreements with Hewlett Packardand Acer in connection with the Tablet PC; Agilix Labsin development of the TabletPlanner Software; andMicrosoft in conjunction with the Tablet PC training,PlanPlus and TabletPlanner marketing.

CLIENTS

We have a relatively broad base of institutional andindividual clients. We have more than 2,000 institu-tional clients consisting of corporations, governmentalagencies, educational institutions and other organiza-tions. We believe our products, workshops and seminarsencourage strong client loyalty. Employees in each ofour distribution channels focus on providing timely andcourteous responses to client requests and inquiries.Institutional clients may choose to receive assistance indesigning and developing customized forms, tabs, page-finders and binders necessary to satisfy specific needs.

COMPETITION

Training. Competition in the performance skillsorganizational training and education industry is highlyfragmented with few large competitors. We estimatethat the industry represents more than $6 billion inannual revenues and that the largest traditional organi-zational training firms have sales in the $100 million to$150 million range. Based upon FranklinCovey’s fiscal2003 organizational sales of approximately $115million, we believe we are a leading competitor in theorganizational training and education market. Othersignificant competitors in the training market areDevelopment Dimensions International, AchieveGlobal (formerly Zenger Miller), OrganizationalDynamics Inc., Provant, Forum Corporation, EPSSolutions and the Center for Creative Leadership.

14 Form 10-K Franklin Covey 2003 Annual Report

Products. The paper-based time management andpersonal organization products market is intenselycompetitive and subject to rapid change. FranklinCoveycompetes directly with other companies that manufac-ture and market calendars, planners, personal organizers,appointment books, diaries and related products throughretail, mail order and other direct sales channels. In thismarket, several competitors have strong name recogni-tion. We believe our principal competitors includeDayTimer, At-A-Glance and Day Runner. We alsocompete with companies that market substitutes forpaper-based products, such as electronic organizers,software PIMs and handheld computers. OurFranklinCovey Planning Software competes directlywith numerous other PIMs. Many FranklinCoveycompetitors have significant marketing, productdevelopment, financial and other resources. Anemerging potential source of competition is theappearance of calendars and event-planning servicesavailable at no charge on the Web. There is no indica-tion that the current level of features has proven to beattractive to the traditional planner customer as a stand-alone service, but as these products evolve and improve,they could pose a competitive threat.

Given the relative ease of entry in FranklinCovey’sproduct and training markets, the number of competi-tors could increase, many of whom may imitate ourmethods of distribution, products and seminars, or offersimilar products and seminars at lower prices. Some ofthese companies may have greater financial and otherresources than us. We believe that the FranklinCoveyPlanner and related products compete primarily on thebasis of user appeal, client loyalty, design, productbreadth, quality, price, functionality and client service.We also believe that the FranklinCovey Planner hasobtained market acceptance primarily as a result of theconcepts embodied in the FranklinCovey Planner, thehigh quality of materials, innovative design, our atten-tion to client service, and the strong loyalty and referralsof our existing clients. We believe that our integrationof training services with products has become a com-petitive advantage. Moreover, we believe that we are amarket leader in the United States among a smallnumber of integrated providers of productivity and timemanagement products and services. Increased competi-tion from existing and future competitors could, however,have a material adverse effect on our sales and profitability.

MANUFACTURING AND DISTRIBUTION

The manufacturing operations of FranklinCovey consistprimarily of printing, collating, assembling and packag-ing components used in connection with our paperproduct lines. We operate our central manufacturingservices out of Salt Lake City. We have also developedpartner printers, both domestically and internationally,who can meet our quality standards, thereby facilitatingefficient delivery of product in a global market. Webelieve this has positioned us for greater flexibility andgrowth capacity. Automated production, assembly andmaterial handling equipment are used in the manufac-turing process to ensure consistent quality of productionmaterials and to control costs and maintain efficiencies.By operating in this fashion, we have gained greatercontrol of production costs, schedules and qualitycontrol of printed materials.

During fiscal 2001, we entered into a long-termcontract with EDS to provide warehousing anddistribution services of our product line. EDS maintainsa facility at the Company’s headquarters as well as atother locations throughout North America.

Binders used for our products are produced from eitherleather, simulated leather, tapestry or vinyl materials.These binders are produced by multiple and alternativeproduct suppliers. We currently enjoy good relationswith our suppliers and vendors and do not anticipateany difficulty in obtaining the required binders andmaterials needed for our business. We have imple-mented special procedures to ensure a high standard ofquality for binders, most of which are manufactured bysuppliers in the United States, Europe, Canada, Korea,Mexico and China.

We also purchase numerous accessories, including pens,books, videotapes, calculators and other products, fromvarious suppliers for resale to our clients. These itemsare manufactured by a variety of outside contractorslocated in the United States and abroad. We do notbelieve that we are entirely dependent on any one ormore of such contractors and consider our relationshipswith such suppliers to be good.

Franklin Covey 2003 Annual Report Form 10-K 15

TRADEMARKS, COPYRIGHTS ANDINTELLECTUAL PROPERTY

We seek to protect our intellectual property through acombination of trademarks, copyrights and confiden-tiality agreements. We claim rights for more 120trademarks in the United States and have obtainedregistration in the United States and many foreigncountries for many of our trademarks, includingFranklinCovey, The 7 Habits of Highly Effective People®,Principle-Centered Leadership, Aligning Goals for Results,FOCUS: Achieving Your Highest Priorities, FranklinCoveyPlanner, PlanPlus, and The Seven Habits. We considerour trademarks and other proprietary rights to beimportant and material to our business. Each of themarks set forth in italics above is a registered mark or amark for which protection is claimed.

We own all copyrights on our planners, books, manuals,text and other printed information provided in ourtraining seminars, the programs contained withinFranklinCovey Planner Software and its instructionalmaterials, and our software and electronic products,including audio tapes and video tapes. We license,rather than sell, all facilitator workbooks and otherseminar and training materials in order to limit itsdistribution and use. FranklinCovey places trademarkand copyright notices on its instructional, marketingand advertising materials. In order to maintain theproprietary nature of our product information,FranklinCovey enters into written confidentialityagreements with certain executives, product developers,sales professionals, training consultants, other employeesand licensees. Although we believe the protectivemeasures with respect to our proprietary rights areimportant, there can be no assurance that such measureswill provide significant protection from competitors.

EMPLOYEES

As of August 31, 2003, FranklinCovey had 1,425 fulland part-time associates, including 300 in sales,marketing and training; 700 in customer service andretail; 141 in production operations and distribution;and 284 in administration and support staff. Duringfiscal 2002, the Company outsourced a significant partof its information technology services, customer service,distribution and warehousing operations to EDS. Anumber of the Company’s former employees involved inthese operations are now employed by EDS to providethose services to FranklinCovey. None of FranklinCovey’sassociates are represented by a union or other collectivebargaining group. Management believes that its rela-tions with its associates are satisfactory. FranklinCoveydoes not currently foresee a shortage in qualifiedpersonnel needed to operate the Company’s business.

AVAILABLE INFORMATION

The Company’s principal executive offices are located at2200 West Parkway Boulevard, Salt Lake City, Utah84119-2331 and its telephone number is (801) 817-1776.

We regularly file reports with the Securities ExchangeCommission (SEC). These reports include, but are notlimited to, Annual Reports on Form 10-K, QuarterlyReports on Form 10-Q, current reports on Form 8-K,and security transaction reports on Forms 3, 4, or 5.The public may read and copy any materials that theCompany files with the SEC at the SEC’s PublicReference Room located at 450 Fifth Street, NW,Washington, DC 20549. The public may obtaininformation on the operation of the Public ReferenceRoom by calling the SEC at 1-800-SEC-0330. TheSEC also maintains electronic versions of theCompany’s reports on its website at www.sec.gov.

The Company makes our Annual Report on Form 10K,Quarterly Reports on Form 10Q, current reports onForm 8K, and other reports filed or furnished with theSEC available to the public, free of charge, through ourwebsite at www.franklincovey.com. These reports areprovided through our website as soon as reasonablypracticable after we file or furnish these reports with the SEC.

16 Form 10-K Franklin Covey 2003 Annual Report

Item 2. Properties

Franklin Covey’s principal business operations andexecutive offices are located in Salt Lake City, Utah.The following is a summary of our owned and leasedproperties. Our facility lease agreements are accountedfor as operating leases, which expire at various datesthrough the year 2016.

United States Administrative Offices:Salt Lake City, Utah (7 locations) – 2 leasedProvo, Utah (1 location) – leased

International Administrative Offices:Canada (1 location)Latin America (3 locations) – all leasedAsia Pacific (2 locations) – both leasedEurope (1 location) – leased

Regional Sales Offices:United States (7 locations) – all leased

Distribution Facilities:Asia Pacific (2 locations) – both leasedCanada (1 location)Latin America (1 location) – leasedEurope (1 location) – leased

Manufacturing Facilities:United States (1 location)

Retail Stores:United States (153 locations) – all leased

We consider our existing facilities sufficient for ourcurrent and anticipated level of operations in theupcoming fiscal year. However, we are actively seekingto sell our administrative offices located in Salt LakeCity, Utah and to execute a sale-leaseback agreement onall five buildings. During fiscal 2003, we closed 22 retailstore locations in the United States as well as 10 inter-national store locations located in Canada and Mexico.We have also closed two stores in fiscal 2004 and expectto close additional retail locations during fiscal 2004.

Item 3. Legal Proceedings

During fiscal 2002, the Company received a subpoenafrom the Securities and Exchange Commission (the“SEC”) seeking documents and information relating tothe Company’s management stock loan program andpreviously announced, and withdrawn, tender offer. TheCompany has provided the documents and informationrequested by the SEC, including the testimonies of itsChief Executive Officer, Chief Financial Officer, andother key employees. The Company has cooperated, andwill continue to fully cooperate, in providing requestedinformation to the SEC. The SEC has stated that theformal inquiry is not an indication that the SEC hasconcluded that there has been a violation of any law orregulation. The Company believes that it has compliedwith the laws and regulations applicable to its manage-ment stock loan program and withdrawn tender offer.

The Company is also the subject of certain legalactions, which we consider routine to our businessactivities. At August 31, 2003, management believesthat, after consultation with legal counsel, any potentialliability to the Company under such actions will notmaterially affect our financial position, liquidity, orresults of operations.

Item 4. Submission of Mattersto a Vote of Security Holders

No matters were submitted to a vote of security holdersduring the fourth quarter of our fiscal year endedAugust 31, 2003.

Franklin Covey 2003 Annual Report Form 10-K 17

PART II

Management’s Discussion andAnalysis of Financial Conditionand Results of Operations

OVERVIEW

The following management’s discussion and analysis isintended to provide a summary of the principal factorsaffecting the results of operations, liquidity and capitalresources, contractual obligations, and the criticalaccounting policies of Franklin Covey Co. (also referredto as the “Company”, “we”, “us”, and “our”, unlessotherwise indicated) and subsidiaries. This discussionand analysis should be read together with our consoli-dated financial statements and related notes, whichcontain additional information regarding the accountingpolicies and estimates underlying the Company’sfinancial statements. Our consolidated financialstatements and related notes begin on page 36 of thisreport on Form 10-K.

Franklin Covey Co. seeks to improve the effectivenessof organizations and individuals and is a worldwideleader in providing integrated learning and performancesolutions to organizations and individuals that are designedto enhance productivity, leadership, sales performance,communication, and other skills. Each performancesolution may include products and services that encom-pass training and consulting, assessment, and variousapplication tools that are generally available in electronicor paper-based formats. Our products and services areavailable through professional consulting services, publicworkshops, retail stores, catalogs, and the Internet atwww.franklincovey.com. The Company’s best-knownofferings include the Franklin Covey Planner™, ourproductivity workshop entitled “Focus: Achieving YourHighest Priorities,” and courses based on the best-selling book, The 7 Habits of Highly Effective People.

Our fiscal year ends on August 31, and unless otherwiseindicated, fiscal 2003, fiscal 2002, and fiscal 2001, referto the twelve-month periods ended August 31, 2003,2002, and 2001.

Key factors that influence our operating results includethe number of organizations that are active customers;the number of people trained within those organiza-tions; the sale of personal productivity tools (includingFranklin Covey Planners, personal digital assistants or“PDAs”, binders, and other related products); and ourability to manage operating costs necessary to providetraining and products to our clients.

The following is a summary of our recent businessacquisitions and divestitures:

Agilix Labs, Inc. – During the first quarter of fiscal2003, we purchased approximately 20 percent of thecapital stock (on a fully diluted basis) of Agilix Labs,Inc. (“Agilix”), a Delaware corporation, for cashpayments totaling $1.0 million. Agilix is a developmentstage enterprise that develops software applications,including software for “Tablet PCs.” Although thesoftware developed by Agilix continues to be sold withTablet PCs, uncertainties surrounding Agilix’s businessplan developed during fiscal 2003 and their potentialadverse effects on Agilix’s operations and future cashflows were significant. As a result, we determined thatour ability to recover the carrying value of ourinvestment in Agilix was remote. Accordingly, weimpaired and expensed our remaining investment inAgilix, which totaled $0.9 million, during the quarterended March 1, 2003.

Premier Agendas – During fiscal 2002, we sold PremierAgendas, a wholly owned subsidiary located inBellingham, Washington, and Premier School AgendasLtd., a wholly owned subsidiary organized in Ontario,Canada, (collectively, “Premier”) to School Specialty,Inc., a company that specializes in providing productsand services to students and schools. The sale price was$152.5 million in cash plus the retention of Premier’sworking capital, which was received in the form of a$4.0 million promissory note from the purchaser. TheCompany received full payment on the promissory noteplus accrued interest during June 2002. Prior to the saleclosing, the Company also received cash distributionsfrom Premier’s working capital that totaled approxi-mately $7 million. For further information regardingthe sale of Premier, refer to Note 13 in our consolidatedfinancial statements.

18 Management’s Discussion and Analysis Franklin Covey 2003 Annual Report

FranklinPlanner.com – During fiscal 2002, wediscontinued the on-line planning services provided at franklinplanner.com. The Company acquiredfranklinplanner.com during fiscal 2000 and intended tosell on-line planning as a component of our productivitysolutions for both organizations and individuals. However,due to competitors that offered free on-line planning andother related factors, we were not able to create a profitablebusiness model for the operations of franklinplanner.com.Although we were unable to generate revenue from theon-line planning services offered at franklinplanner.com,an on-line planning tool was considered a key com-ponent of our overall product and services offerings andfranklinplanner.com continued to operate during fiscal2001 and fiscal 2002. However, due to lack of demandfor its services and the need to reduce operatingexpenses, we terminated franklinplanner.com during thefourth quarter of fiscal 2002.

Franklin Covey Coaching, LLC – Effective September1, 2000, the Company entered into a joint ventureagreement with American Marketing Systems (“AMS”)to form Franklin Covey Coaching, LLC (“FCC”). Eachpartner owned 50 percent of the joint venture andparticipated equally in FCC’s management. The FCCjoint venture agreement required our coaching programsto achieve specified earnings thresholds beginning infiscal 2002 or the existing joint venture agreement couldbe terminated at the option of AMS. Due to unfavor-able economic conditions and other factors, theCompany’s coaching programs did not produce therequired earnings during fiscal 2002. As a result, AMSexercised its option to terminate the existing jointventure agreement effective August 31, 2002. Under the provisions of a new partnership agreement thatterminated our interest in FCC in October 2003, wereceived payments totaling $2.6 million, of which $2.0million was received in fiscal 2003. Refer to Note 4 inour consolidated financial statements for furtherinformation on the new partnership agreement withFranklin Covey Coaching, LLC.

Project Consulting Group – During April 2001, theCompany purchased the Project Consulting Group for$1.5 million in cash. The Project Consulting Groupprovides project consulting, project management, andproject methodology training services.

RESULTS OF OPERATIONS

Segment Review

Following the sale of Premier during fiscal 2002, wenow have two reporting segments: the ConsumerBusiness Unit (the “CBU”) and the OrganizationalSolutions Business Unit (the “OSBU”). The operatingresults of Premier and our other products and servicesdesigned for teachers and students were previouslyreported in the Education Business Unit, which wasdissolved during fiscal 2002. Our remaining student andteacher programs and products are now classified withOSBU results of operations.

Consumer Business Unit – This business unit isprimarily focused on sales to individual customers andincludes the results of the Company’s 153 domesticretail stores, 10 international retail stores (which wereclosed at August 31, 2003), catalog and eCommerceoperations, and other related distribution channels,including wholesale, the government, and officesuperstores. The CBU results of operations also includethe financial results of our paper planner manufacturingoperations. Although CBU sales primarily consist ofproducts such as planners, binders, software, and hand-held electronic planning devices, virtually any componentof the Company’s leadership and productivity solutionscan be purchased through CBU channels.

Organizational Solutions Business Unit – The OSBUis primarily responsible for the development, marketing,sale, and delivery of productivity, leadership, salesperformance, and communication training solutionsdirectly to organizational clients, including othercompanies, the government, and educational institu-tions. The OSBU includes the financial results of theOrganizational Solutions Group (“OSG”) andinternational operations, except for international retailstores. The OSG is responsible for the domestic saleand delivery of productivity, leadership, sales perform-ance, and communication training solutions tocorporations and includes sales of training seminars toteachers and students, which were previously reportedas part of the Education Business Unit. The OSG isalso responsible for consulting services that complimentour productivity and leadership training solutions. TheCompany’s international sales group includes theoperating results of our directly owned foreign officesand royalty revenues from licensees.

Franklin Covey 2003 Annual Report Management’s Discussion and Analysis 19

The following table sets forth selected segment salesand consolidated operational data from continuingoperations for the years indicated. For further informa-tion regarding our reporting segments and othergeographic information, refer to Note 20 in ourconsolidated financial statements (in thousands).

YEAR ENDEDAUGUST 31, 2003 2002 2001

Consumer Business Unit:Retail stores $112,054 $ 122,496 $156,299 Catalog and

eCommerce 56,177 64,802 92,449 Other CBU 23,935 22,326 34,840

192,166 209,624 283,588

Organizational Solutions Business Unit:OSG 74,306 82,095 110,675International 40,688 41,279 45,518

114,994 123,374 156,193

Total sales 307,160 332,998 439,781Cost of sales 137,601 149,369 189,982

Gross margin 169,559 183,629 249,799

Selling, general, and administrative 183,312 216,910 224,458

Provision for losses on management stock loan program 3,903 24,775 1,052

Impairment (recovery) of investment in

unconsolidated subsidiary (1,644) 16,323

Loss on impaired assets 872 9,184 801

Depreciation 26,395 34,343 27,441Amortization 4,386 4,667 10,840

Loss from continuing operations $ (47,665) $(122,573) $ (14,793)

FISCAL 2003 COMPARED TO FISCAL 2002

Sales

Product Sales - Product sales, which primarily consistof planners, binders, software, and handheld electronicplanning devices, decreased $19.4 million, or ninepercent, compared to the prior year. The decline inproduct sales was primarily attributable to declines inretail and catalog sales. These declines were partiallyoffset by increased sales from our eCommerce andwholesale channels. Retail store sales declined $10.4million, or nine percent, primarily due to reducedtraffic. The unfavorable retail sales trend was reflectedin a 10 percent decline in comparable store salesperformance (comparable stores represent retail storesthat have been open longer than one year) compared tofiscal 2002. As a result of unfavorable operatingperformance in certain of our retail stores, we closed 22retail stores in the United States and 10 internationallocations during fiscal 2003. These closures areprimarily comprised of unprofitable stores and storeslocated in markets where the Company has multipleretail operations. We may also close additional retaillocations if future analysis demonstrates that ouroperating performance may be improved throughfurther store closures. We anticipate that a portion ofthe sales from these closed stores will transition to otherretail store locations or to one of our other productchannels. At August 31, 2003, we were operating 153domestic retail stores compared to 173 domestic and 10international stores at August 31, 2002.

Catalog sales declined $13.5 million, compared to fiscal2002, reflecting continuing trends of lower call volumethrough our catalog call center. However, decreasedcatalog sales were partially offset by $4.9 million ofincreased sales through our Internet web site located atwww.franklincovey.com. Although total sales from thecatalog and eCommerce channel are down, the shift ofsales from the catalog call center to the Internetproduced improved operating results for this channeldue to the lower operating costs per transaction of oureCommerce operations. Other CBU sales improvedprimarily due to increased wholesale sales through ourcontract stationer channel, which produced a $1.3million sales increase compared to fiscal 2002.

20 Management’s Discussion and Analysis Franklin Covey 2003 Annual Report

Training and Services Sales – Training solution andrelated services sales during fiscal 2003 decreased by$6.4 million, or six percent, compared to fiscal 2002.The Company offers a variety of training solutions,training related products, and consulting servicesfocused on productivity, leadership, sales performance,and communication training programs which areprovided through our OSBU channels. The decrease inOSG sales, which are primarily domestic training andtraining-product sales, was primarily attributable todecreased sales of customized training products, theelimination of our organizational change consultinggroup, decreased public seminar sales, and reducedgovernment training sales. Partially offsetting these salesdecreases were increases in client-facilitated workshopsand productivity programs, including our newproductivity workshop entitled, “Focus: Achieving YourHighest Priorities.”

International sales decreased $0.6 million, or onepercent, compared to the prior year. Decreased sales inMexico, Canada, and Europe were partially offset byincreased sales in Japan, the United Kingdom, Australia,and increased licensee royalty revenue.

Gross Margin

Gross margin consists of sales less cost of sales. Ourcost of sales includes materials used in the production ofplanners and related products, assembly andmanufacturing labor costs, direct costs of conductingseminars, freight, and certain other overhead costs.Gross margin may be affected by, among other things,prices of materials, labor rates, product sales mix,changes in product discount levels, productionefficiency, and freight costs.

Our overall gross margin for fiscal 2003 improvedslightly to 55.2 percent of sales compared to 55.1percent in the prior year. Gross margin on product salesdecreased to 49.0 percent compared to 50.0 percent inthe prior year. The decline in our product gross marginwas chiefly attributable to the following three factors:1) the substantial discounting of a number of slowermoving products in order to liquidate this merchandise;2) a shift in our product mix toward technologyproducts, including tablet PCs and handheld electronicdevices, which generally have lower gross margins thanthe majority of our other products; and 3) in responseto general market trends, significant promotionaldiscounts were used on certain products to enhancesales. Partially offsetting these factors during fiscal 2003were the favorable results from focused cost-cuttinginitiatives aimed at reducing our production costs forpaper-related products and decreasing the purchaseprice of our binder products.

Training solution and services gross margin, as a percentof sales, improved to 67.2 percent in fiscal 2003,compared to 65.4 percent in the prior year. Theimprovement in training solutions gross margin wasprimarily due to decreased sales of customized trainingproducts and the elimination of our organizationalchange consulting practice, both of which typically havelower gross margins than the majority of our othertraining solution and training product related sales.Additionally, higher-margin facilitator sales continuedto improve and had a favorable impact on our grossmargin percentage in fiscal 2003.

Operating Expenses

Selling, General, and Administrative – Our selling,general, and administrative (“SG&A”) expensesdecreased $33.6 million, or 15 percent, compared tofiscal 2002. SG&A expenses decreased as a percentageof sales to 59.7 percent in fiscal 2003 compared to 65.1percent in fiscal 2002. Decreased SG&A expenses werethe result of initiatives specifically designed to reduceour overall operating costs. These successful cost-cuttinginitiatives resulted in associate expense reductionstotaling $17.7 million, reductions in other SG&Aexpenses, including outsourcing, consulting, anddevelopment, that totaled $10.3 million, and advertisingand promotional expense reductions totaling $9.0 million,compared to the prior year. Partially offsetting these costreduction efforts were additional expenses generated fromclosing stores in fiscal 2003, as discussed below. As aresult of changing administrative space needs and cost-cutting efforts, we also vacated a portion of our corporatecampus in Salt Lake City, Utah and are actively seekingto lease the vacant space. In order to further improveour financial results and reduce operating costs, ourmanagement regularly evaluates our business activitiesand operating segment financial results and mayimplement additional cost-cutting initiatives.

Franklin Covey 2003 Annual Report Management’s Discussion and Analysis 21

We regularly assess the operating performance of ourretail stores, including previous operating performancetrends and projected future profitability. During thisassessment process, judgments are made as to whetherunder-performing or unprofitable stores should beclosed. As a result of this evaluation process, we decidedto close certain stores during fiscal 2003 and fiscal2004. These store closures are comprised of stores thatwere unprofitable or were located in markets where theCompany has multiple retail locations. The costs asso-ciated with closing retail stores are typically comprisedof charges related to vacating the premises, which mayinclude a provision for the remaining term on the lease,and severance and other personnel costs. During fiscal2003, the Company closed 22 stores in the UnitedStates and 10 international retail stores that werelocated in Canada and Mexico. In connection withthese store closures, we incurred and expensed $3.6million, which was recorded in selling, general, andadministrative expenses in fiscal 2003. Subsequent toAugust 31, 2003, we have closed 2 stores and intend toclose additional stores through the end of the thirdquarter of fiscal 2004.