The Chartered Institute of Management Accountants 2003 Examination Question and Answer Book Write here your full examination number Centre Code: Hall Code: Desk Number: Foundation Level Financial Accounting Fundamentals 1 FAFN 21 May 2003 Wednesday morning INSTRUCTIONS TO CANDIDATES Read this page before you look at the questions THIS QUESTION PAPER BOOKLET IS ALSO YOUR ANSWER BOOKLET. Sufficient space has been provided for you to write your answers, and also for workings where questions require them. For section B questions, you must write your answers in the shaded space provided. Please note that you will NOT receive marks for your workings. Do not exceed the stated number of words. Do NOT remove any sheets from this booklet: cross through neatly any work that is not to be marked. Avoid the use of correction fluid. You are allowed three hours to answer this question paper. All questions are compulsory. Answer the ONE question in section A (this has 25 sub-questions and is on pages 2-12) Answer the THREE questions in section B (these are on pages 13-19) You are advised to spend 10 minutes reading through the paper before starting to answer the questions. You should spend no more than 85 minutes in total answering the ONE question in section A, which has 25 sub-questions. You should spend no more than 85 minutes in total answering the THREE questions in section B. Hand this entire booklet to the invigilators at the end of the examination. You are NOT permitted to leave the examination hall with this booklet. Do NOT write your name or your student registration number anywhere on this booklet.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Chartered Institute of Management Accountants 2003

ExaminationQuestion andAnswer Book

Write here your full examination number

Centre Code:

Hall Code:

Desk Number:

Foundation Level Financial Accounting Fundamentals

1 FAFN21 May 2003

Wednesday morning

INSTRUCTIONS TO CANDIDATES

Read this page before you look at the questions

THIS QUESTION PAPER BOOKLET IS ALSO YOUR ANSWER BOOKLET.Sufficient space has been provided for you to write your answers, and also for workings where questionsrequire them. For section B questions, you must write your answers in the shaded space provided. Pleasenote that you will NOT receive marks for your workings. Do not exceed the stated number of words. DoNOT remove any sheets from this booklet: cross through neatly any work that is not to be marked. Avoidthe use of correction fluid.

You are allowed three hours to answer this question paper. All questions are compulsory.

Answer the ONE question in section A (this has 25 sub-questions and is on pages 2-12)

Answer the THREE questions in section B (these are on pages 13-19)

You are advised to spend 10 minutes reading through the paper before starting to answer the questions.

You should spend no more than 85 minutes in total answering the ONE question in section A, which has25 sub-questions.

You should spend no more than 85 minutes in total answering the THREE questions in section B.

Hand this entire booklet to the invigilators at the end of the examination. You are NOT permitted to leavethe examination hall with this booklet.

Do NOT write your name or your student registration number anywhere on this booklet.

FAFN 2 May 2003

SECTION A — 50 MARKS

ANSWER ALL TWENTY-FIVE SUB-QUESTIONS – 2 MARKS EACH

Question One

Do not write in thesecolumns below

For useby the

firstmarker

For useby thesecondmarker

After the profit and loss account for Z Ltd had been prepared, it was found thataccrued expenses of $1,500 had been omitted and that closing stock had beenovervalued by $500.

The effect of these errors is an

1.1

A overstatement of net profit of $1,000

B overstatement of net profit of $2,000

C understatement of net profit of $1,000

D understatement of net profit of $2,000

Each of the sub-questions numbered from 1.1 to 1.25 inclusive, given below, has only ONE correctanswer.

REQUIRED:Place a circle “O” around the letter A, B, C or D that gives the correct answer to each sub-question.

If you wish to change your mind about an answer, block out your first answer completely and then circleanother letter. You will NOT receive marks if more than one letter is circled.

Please note that you will NOT receive marks for any workings to these sub-questions. Sufficient spacehas been provided for you to do your workings where these sub-questions require them.

May 2003 3 FAFN

Do not write in thesecolumns below

1.2 The cashier is reconciling his company’s cash book with the bank statement at31 March 2003.

For useby the

firstmarker

For useby thesecondmarker

$The firm’s cash book shows a debit balance of 12,350

The following information is available:

Bank charges not entered in the cash book 170Unpresented cheques 4,600Direct debit payment on the bank statement not entered in thecash book

230

Sales receipts banked, but not credited by the bank 9,400A cheque from a customer which had previously been entered inthe cash book when received, has been returned by the bank as“dishonoured”, and this has not been recorded in the cash book

110

What should be stated as the bank balance in the company’s balance sheet at31 March 2003?

A $11,840

B $12,060

C $12,860

D $16,640

For useby the

firstmarker

For useby thesecondmarker

1.3 Which ONE of the following is true?

A External auditors normally check all purchase invoices.

B External auditors should prepare the accounts.

C External auditors must follow the audit procedures prepared by the internalauditors.

D External auditors check the internal control system.

FAFN 4 May 2003

Do not write in thesecolumns below

D is preparing the accounts for A Ltd for the year ended 31 March 2003. Themost recent gas bill received by A Ltd was dated 6 February 2003 and relatedto the quarter 1 November 2002 to 31 January 2003, and the amount of the billwas $2,100.

For useby thefirst

marker

For useby thesecondmarker

1.4

Which ONE of the following ledger entries should be made in A Ltd’s books at31 March 2003?

Debit CreditA Accruals NIL Gas expense NIL

B Gas expense $1,400 Accruals $1,400

C Accruals $1,400 Gas expense $1,400

D Gas expense $2,100 Accruals $2,100

1.5 The following information related to Q plc for the year ended 28 February 2003: For useby thefirst

marker

For useby the

secondmarker

$Prime cost 122,000Factory overheads 185,000Opening work-in-progress at 1 March 2002 40,000Factory cost of goods completed 300,000

The closing work-in-progress at 28 February 2003 was

A $33,000

B $40,000

C $47,000

D $54,000

1.6 N Ltd, which is registered for VAT, received an invoice from an advertisingagency for $4,000 plus VAT. The rate of VAT on the goods was 17⋅5%. Thecorrect ledger entries are:

For useby thefirst

marker

For useby the

secondmarker

Debit $ Credit $A Advertising expense 4,000 Creditors 4,000

B Advertising expense 4,700 Creditors 4,700

C Advertising expense 4,700 Creditors 4,000VAT account 700

D Advertising expense 4,000 Creditors 4,700VAT account 700

May 2003 5 FAFN

Do not write in thesecolumns below

1.7 E Ltd received an invoice for the purchase of fixed asset equipment which wascredited to the correct supplier’s ledger account, but debited to the equipmentrepairs account, instead of the equipment account.

For useby thefirst

marker

For useby the

secondmarker

The effect of not correcting this error on the financial statements would be:

A Profit would be overstated and fixed assets would be understated.

B Profit would be overstated and fixed assets would be overstated.

C Profit would be understated and capital would be overstated.

D Profit would be understated and fixed assets would be understated.

1.8 H Ltd began trading on 1 July 2001. The company is now preparing itsaccounts for the accounting year ended 30 June 2002. Rates are charged for atax year, which runs from 1 April to 31 March, and were $1,800 for the yearended 31 March 2002 and $2,000 for the year ended 31 March 2003. Ratesare payable quarterly in advance, plus any arrears, on 1 March, 1 June,1 September and 1 December.

For useby thefirst

marker

For useby the

secondmarker

The charge to H Ltd’s profit and loss account for rates for the year ended 30June 2002 is

A $1,650

B $1,700

C $1,850

D $1,900

1.9 The return on capital employed for S plc is 24% and the net asset turnover ratiois 3 times.

For useby thefirst

marker

For useby the

secondmarker

What is the net profit margin?

A 8%

B 28%

C 72%

D It cannot be calculated.

FAFN 6 May 2003

1.10 Which ONE of the following would NOT help detect errors in a computerisedaccounting system?

For useby thefirst

marker

For useby the

secondmarker

A The use of coding systems.

B The use of batch processing.

C The use of passwords.

D The use of control accounts.

1.11 The total cost of salaries charged to a limited company’s profit and loss accountis

For useby thefirst

marker

For useby the

secondmarker

A cash paid to employees.

B net pay earned by employees.

C gross pay earned by employees.

D gross pay earned by employees, plus employer’s national insurancecontributions.

1.12 Which ONE of the following statements is TRUE? For useby thefirst

marker

For useby the

secondmarker

A Internal auditors report to the directors.

B External auditors report to the directors.

C Internal auditors are employed by the shareholders.

D External auditors are employees of a company.

May 2003 7 FAFN

1.13 The following is the aged debtors analysis for J Ltd at 30 April 2003: For useby thefirst

marker

For useby the

secondmarker

Age of debt Less than 1month

1-2 months 2-3 months Over 3months

Amount ($) 12,000 24,000 8,000 6,000

The company provides for doubtful debts as follows:

Provision 0% 1% 10% 30%

The doubtful debt provision at 1 May 2002 brought forward was $2,880.

The entry for doubtful debts in the profit and loss account for the year ended 30April 2003 and the net debtors figure in the balance sheet at that date shouldbe:

Profit and loss account Balance sheetA $40 credit $47,160

B $40 debit $47,160

C $2,840 debit $50,000

D $2,840 credit $47,160

1.14 The following information relates to companies Q plc and R plc, who arecompetitors selling widgets:

For useby thefirst

marker

For useby the

secondmarker

Q plc R plcGross profit percentage 30% 25%Fixed asset turnover ratio 4 5

A director at Q plc believes that these ratios indicate that:

(i) Q plc has a higher selling price.

(ii) Q has lower purchasing costs.

(iii) R plc has lower sales volume.

(iv) R plc has fewer fixed assets.

Which of the above are possibly true based on the information provided?

A (i) only.

B (i) and (ii) only.

C (i), (ii) and (iii) only.

D (i), (ii), (iii) and (iv).

FAFN 8 May 2003

1.15 The prime cost of goods manufactured is the total of For useby thefirst

marker

For useby the

secondmarker

A raw materials consumed.

B raw materials consumed and direct wages.

C raw materials consumed, direct wages and direct expenses.

D raw materials consumed, direct wages, direct expenses and productionoverheads.

1.16 On 1 May 2003, E Ltd owed a supplier $1,200. During the month of May, E Ltd: For useby thefirst

marker

For useby the

secondmarker

• purchased goods for $1,700 and the supplier offered a 5% discount forpayment within the month.

• returned goods valued at $100 which had been purchased in April 2003.

• sent a cheque to the supplier for payment of the goods delivered in May.

The balance on the supplier’s account at the end of May 2003 is

A $1,015

B $1,100

C $1,185

D $1,300

1.17 The main advantage of using a sales ledger control account is that For useby thefirst

marker

For useby the

secondmarker

A double entry book-keeping is not necessary.

B it helps in detecting errors.

C it helps with credit control.

D it ensures that the trial balance will always balance.

May 2003 9 FAFN

Do not write in thesecolumns below

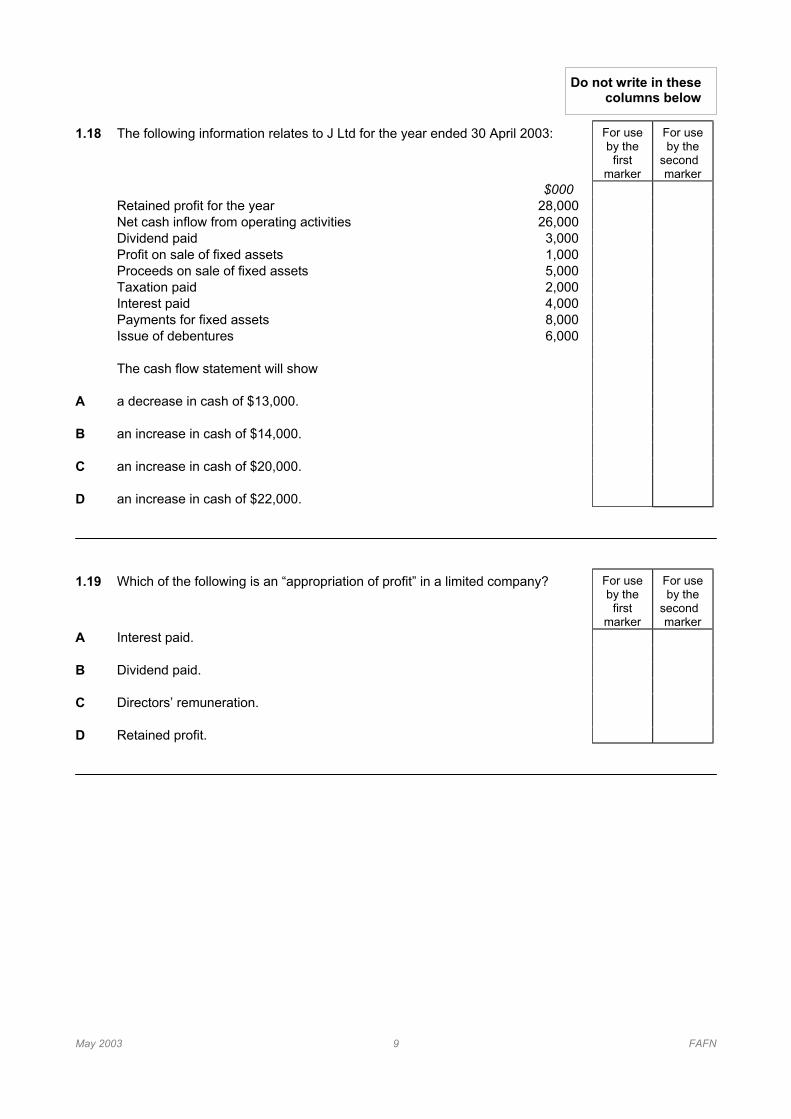

1.18 The following information relates to J Ltd for the year ended 30 April 2003: For useby thefirst

marker

For useby the

secondmarker

$000Retained profit for the year 28,000Net cash inflow from operating activities 26,000Dividend paid 3,000Profit on sale of fixed assets 1,000Proceeds on sale of fixed assets 5,000Taxation paid 2,000Interest paid 4,000Payments for fixed assets 8,000Issue of debentures 6,000

The cash flow statement will show

A a decrease in cash of $13,000.

B an increase in cash of $14,000.

C an increase in cash of $20,000.

D an increase in cash of $22,000.

1.19 Which of the following is an “appropriation of profit” in a limited company? For useby thefirst

marker

For useby the

secondmarker

A Interest paid.

B Dividend paid.

C Directors’ remuneration.

D Retained profit.

FAFN 10 May 2003

1.20 N operates an imprest system for petty cash. On 1 February 2003, the floatwas $300. It was decided that this should be increased to $375 at the end ofFebruary 2003.

For useby thefirst

marker

For useby the

secondmarker

During February, the cashier paid $20 for window cleaning, $100 for stationeryand $145 for coffee and biscuits. The cashier received $20 from staff for theprivate use of the photocopier and $60 for a miscellaneous cash sale.

What amount was drawn from the bank account for petty cash at the end ofFebruary 2003?

A $185

B $260

C $315

D $375

1.21 An audit trail in a computerised accounting system is For useby thefirst

marker

For useby the

secondmarker

A information regarding all transactions in a period.

B a history of all transactions on a ledger account.

C a list of all transactions checked by the internal auditor.

D a list of all transactions automatically posted from day books to ledgers.

1.22 The following are extracts from the financial statements for the year ended 31January 2003 of M plc:

For useby thefirst

marker

For useby the

secondmarker

$000Issued Ordinary shares of $1 200Share premium account 50Profit and loss account 25Debenture 80Profit before interest for the year ended 31 January 2003 60

What is the return on total capital employed?

A 17%

B 22%

C 24%

D 30%

May 2003 11 FAFN

Do not write in thesecolumns below

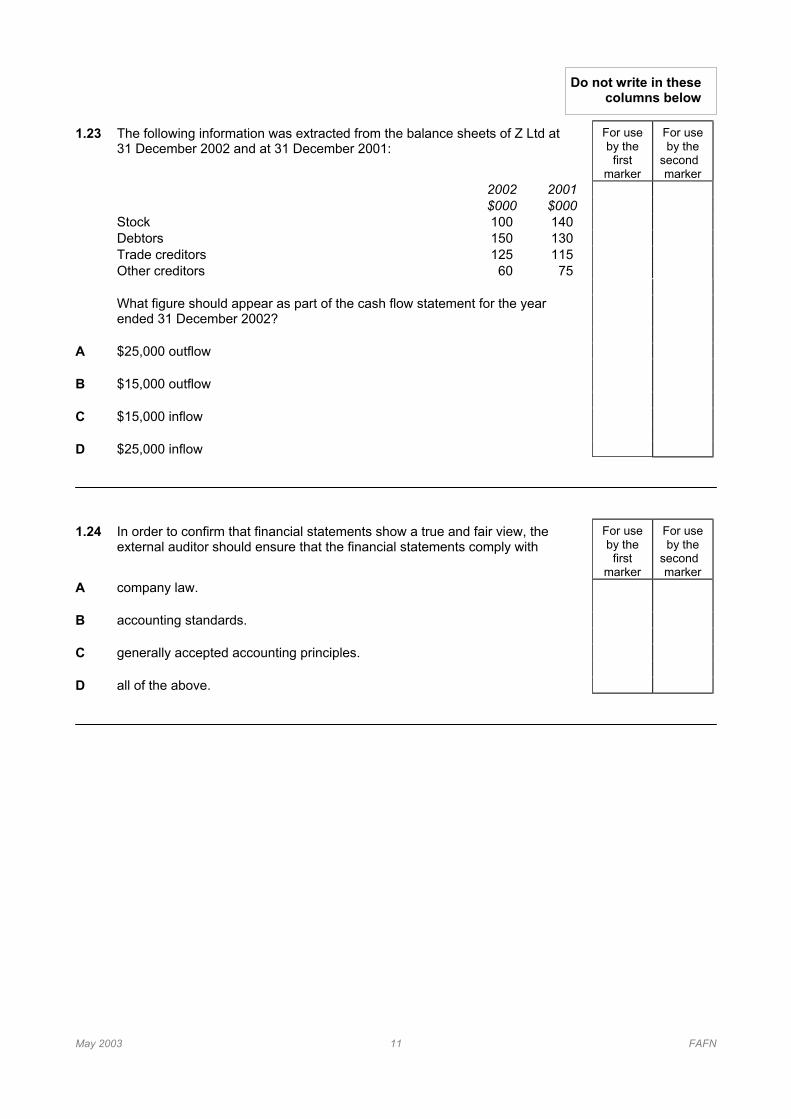

1.23 The following information was extracted from the balance sheets of Z Ltd at31 December 2002 and at 31 December 2001:

For useby thefirst

marker

For useby the

secondmarker

2002 2001$000 $000

Stock 100 140Debtors 150 130Trade creditors 125 115Other creditors 60 75

What figure should appear as part of the cash flow statement for the yearended 31 December 2002?

A $25,000 outflow

B $15,000 outflow

C $15,000 inflow

D $25,000 inflow

1.24 In order to confirm that financial statements show a true and fair view, theexternal auditor should ensure that the financial statements comply with

For useby thefirst

marker

For useby the

secondmarker

A company law.

B accounting standards.

C generally accepted accounting principles.

D all of the above.

FAFN 12 May 2003

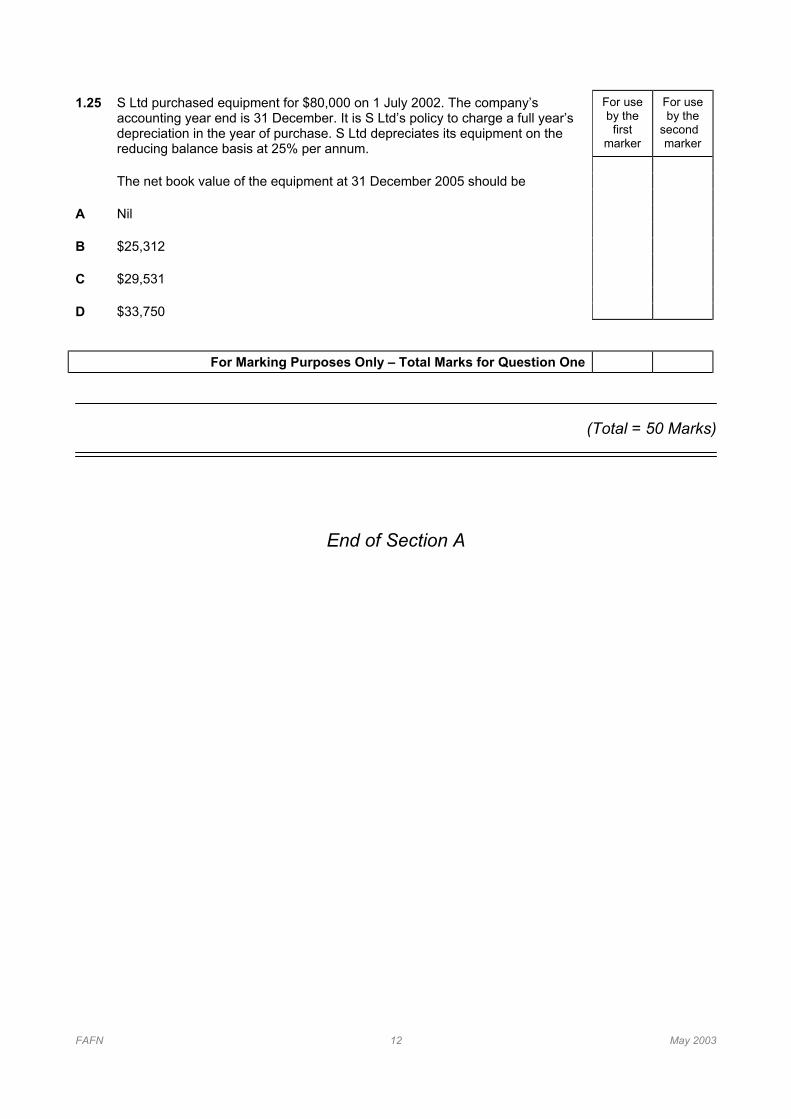

1.25 S Ltd purchased equipment for $80,000 on 1 July 2002. The company’saccounting year end is 31 December. It is S Ltd’s policy to charge a full year’sdepreciation in the year of purchase. S Ltd depreciates its equipment on thereducing balance basis at 25% per annum.

For useby thefirst

marker

For useby the

secondmarker

The net book value of the equipment at 31 December 2005 should be

A Nil

B $25,312

C $29,531

D $33,750

For Marking Purposes Only – Total Marks for Question One

(Total = 50 Marks)

End of Section A

May 2003 13 FAFN

SECTION B – 50 MARKS

ANSWER ALL THREE QUESTIONS

IMPORTANTMARKS ARE AWARDED FOR COMPLETING THE SHADED BOXES WITH THE CORRECTANSWER WHERE A MARK IS INDICATED IN THE RIGHT-HAND COLUMN.

DO NOT WRITE IN THE MARGINS NOR IN THE COLUMNS FOR USE BY MARKERS.

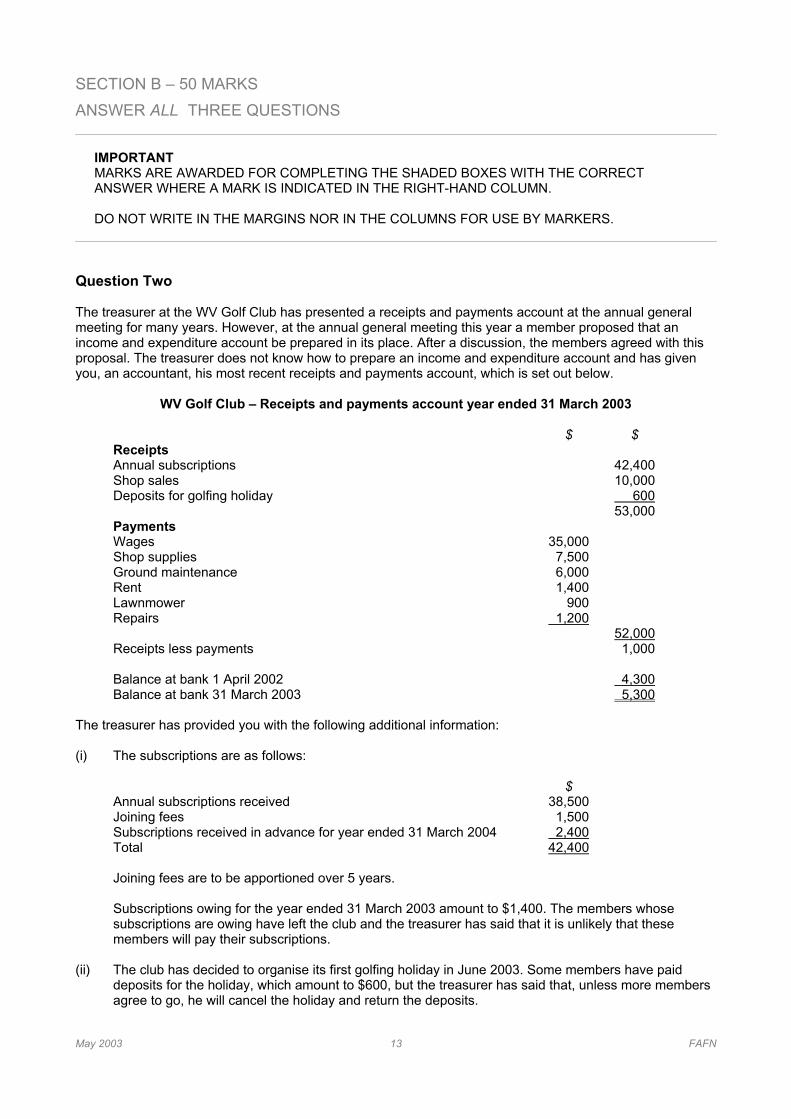

Question Two

The treasurer at the WV Golf Club has presented a receipts and payments account at the annual generalmeeting for many years. However, at the annual general meeting this year a member proposed that anincome and expenditure account be prepared in its place. After a discussion, the members agreed with thisproposal. The treasurer does not know how to prepare an income and expenditure account and has givenyou, an accountant, his most recent receipts and payments account, which is set out below.

WV Golf Club – Receipts and payments account year ended 31 March 2003

$ $ReceiptsAnnual subscriptions 42,400Shop sales 10,000Deposits for golfing holiday 600

53,000PaymentsWages 35,000Shop supplies 7,500Ground maintenance 6,000Rent 1,400Lawnmower 900Repairs 1,200

52,000Receipts less payments 1,000

Balance at bank 1 April 2002 4,300Balance at bank 31 March 2003 5,300

The treasurer has provided you with the following additional information:

(i) The subscriptions are as follows:

$Annual subscriptions received 38,500Joining fees 1,500Subscriptions received in advance for year ended 31 March 2004 2,400Total 42,400

Joining fees are to be apportioned over 5 years.

Subscriptions owing for the year ended 31 March 2003 amount to $1,400. The members whosesubscriptions are owing have left the club and the treasurer has said that it is unlikely that thesemembers will pay their subscriptions.

(ii) The club has decided to organise its first golfing holiday in June 2003. Some members have paiddeposits for the holiday, which amount to $600, but the treasurer has said that, unless more membersagree to go, he will cancel the holiday and return the deposits.

FAFN 14 May 2003

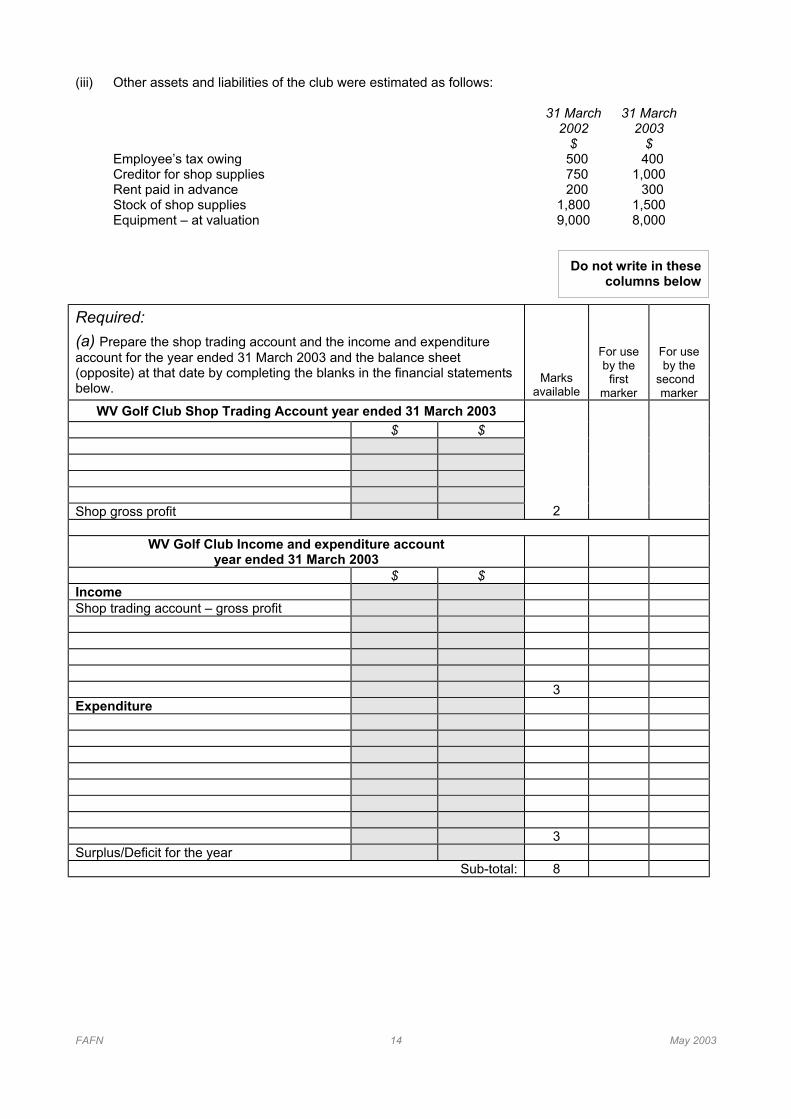

(iii) Other assets and liabilities of the club were estimated as follows:

31 March2002

31 March2003

$ $Employee’s tax owing 500 400Creditor for shop supplies 750 1,000Rent paid in advance 200 300Stock of shop supplies 1,800 1,500Equipment – at valuation 9,000 8,000

Do not write in thesecolumns below

Required:

(a) Prepare the shop trading account and the income and expenditureaccount for the year ended 31 March 2003 and the balance sheet(opposite) at that date by completing the blanks in the financial statementsbelow.

Marksavailable

For useby thefirst

marker

For useby the

secondmarker

WV Golf Club Shop Trading Account year ended 31 March 2003

$ $

Shop gross profit 2

WV Golf Club Income and expenditure accountyear ended 31 March 2003

$ $IncomeShop trading account – gross profit

3Expenditure

3Surplus/Deficit for the year

Sub-total: 8

May 2003 15 FAFN

Question Two continued

Do not write in thesecolumns below

WV Golf Club Balance Sheet year at 31 March 2003

Marksavailable

For useby thefirst

marker

For useby the

secondmarker

$ $Fixed assetsEquipment

Current assets

Current liabilities

Net current assets

Accumulated funds

1/2

11/2

2

4

Sub-total: 8

(i) State TWO advantages (in the shaded area below) of a receiptsand payments account.

(Maximum of 30 words)

(ii) Explain ONE advantage (in the shaded area below) of anincome and expenditure account compared to a receipts andpayments account.

(b)

(Maximum of 30 words)

2

2

Sub-total: 4

Question Two Total Marks = 20

FAFN 16 May 2003

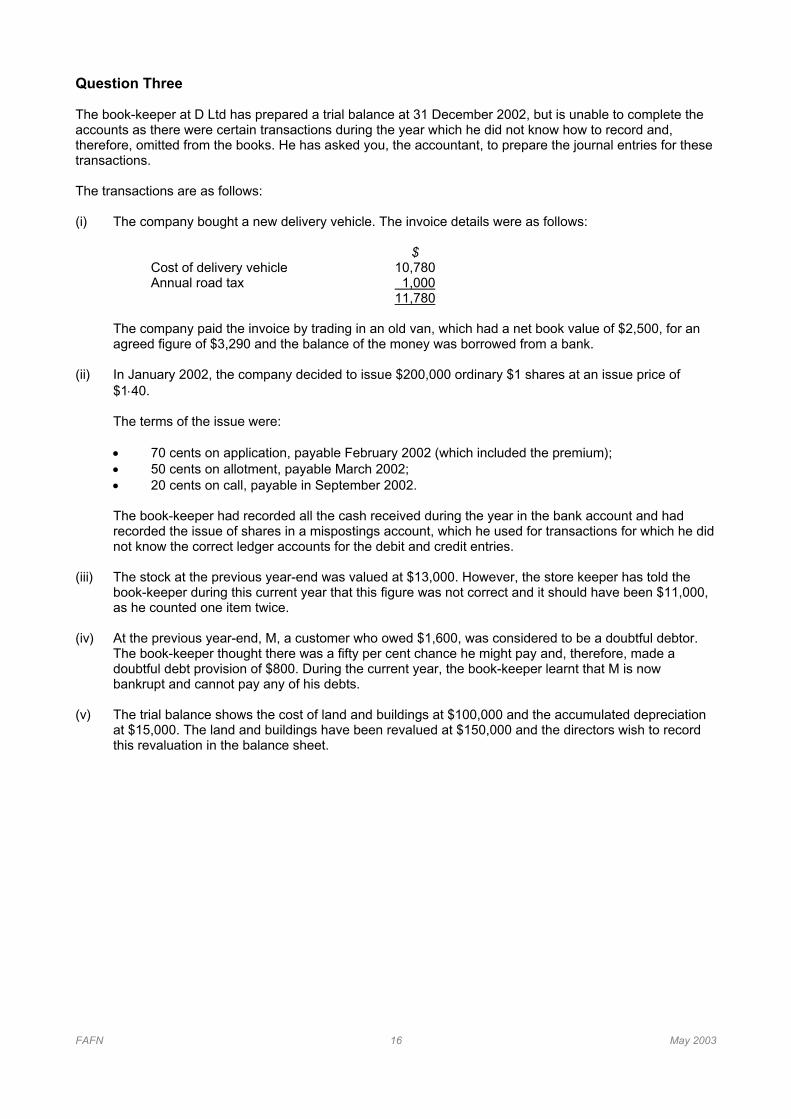

Question Three

The book-keeper at D Ltd has prepared a trial balance at 31 December 2002, but is unable to complete theaccounts as there were certain transactions during the year which he did not know how to record and,therefore, omitted from the books. He has asked you, the accountant, to prepare the journal entries for thesetransactions.

The transactions are as follows:

(i) The company bought a new delivery vehicle. The invoice details were as follows:

$Cost of delivery vehicle 10,780Annual road tax 1,000

11,780

The company paid the invoice by trading in an old van, which had a net book value of $2,500, for anagreed figure of $3,290 and the balance of the money was borrowed from a bank.

(ii) In January 2002, the company decided to issue $200,000 ordinary $1 shares at an issue price of$1⋅40.

The terms of the issue were:

• 70 cents on application, payable February 2002 (which included the premium);• 50 cents on allotment, payable March 2002;• 20 cents on call, payable in September 2002.

The book-keeper had recorded all the cash received during the year in the bank account and hadrecorded the issue of shares in a mispostings account, which he used for transactions for which he didnot know the correct ledger accounts for the debit and credit entries.

(iii) The stock at the previous year-end was valued at $13,000. However, the store keeper has told thebook-keeper during this current year that this figure was not correct and it should have been $11,000,as he counted one item twice.

(iv) At the previous year-end, M, a customer who owed $1,600, was considered to be a doubtful debtor.The book-keeper thought there was a fifty per cent chance he might pay and, therefore, made adoubtful debt provision of $800. During the current year, the book-keeper learnt that M is nowbankrupt and cannot pay any of his debts.

(v) The trial balance shows the cost of land and buildings at $100,000 and the accumulated depreciationat $15,000. The land and buildings have been revalued at $150,000 and the directors wish to recordthis revaluation in the balance sheet.

May 2003 17 FAFN

Required:

Prepare the journal entries for the transactions opposite by completing theshaded areas of the schedule below.

You are NOT required to write a narrative for each journal.

Do not write in these

columns below

Dr

$

Cr

$Marks

available

For useby thefirst

marker

For useby the

secondmarker

Journal (i)

Journal (ii)

Journal (iii)

Journal (iv)

Journal (v)

2

2

2

2

2Total: 10

Question Three Total = 10 Marks

FAFN 18 May 2003

Question Four

You are the senior accountant in a company and in charge of the accounts department.

One of your junior staff is very good at book-keeping and you have identified her as a person with potentialfor promotion. You have therefore agreed to pay for her tuition on a financial accounting course. She hasasked you what she will learn apart from book-keeping.

Required:

Marksavailable

For useby thefirst

marker

For useby the

secondmarker

State briefly (in the shaded area below) the purpose and contents ofEITHER the International Accounting Standards Board’s “Framework forthe Preparation and Presentation of Financial Statements”

OR the Accounting Standards Board’s “Statement of Principles forFinancial Reporting”.

(a)

Explain (in the shaded area below) the objective of financialstatements.

(b)

Describe (in the shaded area below) the characteristics of usefulinformation.

(c)

3

3

3

Sub-total: 9

May 2003 19 FAFN

Question Four continued

Required:

Marksavailable

For useby thefirst

marker

For useby the

secondmarker

(d) Explain (in the shaded areas below) the following accountingconcepts:

business entity(i)

money measurement(ii)

cost(iii)

realisation(iv)

3

3

3

2

sub-total: 11

Total: 20

Question Four Total = 20 Marks

End of Question Paper

Related Documents