Forwards and Swaps: Interest Rates

Forwards and swaps interest rates

Dec 05, 2014

This slide set is a work in progress and is embedded in my Principles of Finance course, which is also a work in progress, that I teach to computer scientists and engineers

http://awesomefinance.weebly.com/

This slide set is under serious development!

http://awesomefinance.weebly.com/

This slide set is under serious development!

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Forwards and Swaps: Interest Rates

2

Learning Objec-ves

¨ Understand and manage interest rate risk via forward and swap agreements

¨ Understand the rela-onship between discount rates, swap rates, zero coupon rates, forward rates, and bond yields

Interest Rate Risk 3

t0=0 tS=0.5 tL=1.0 yrs yrs yrs

q

f

• A firm requires a $10,000,000 loan over a period from 6 to 12 months from present • Over the period 0.5 ≤ t ≤ 1.0

• The firm’s treasurer believes that the interest rate offered will rise over the next 6 months i.e., interest expense will be greater in the near future • Assume that the company can borrow and deposit funds at LIBOR. • Current 6 month LIBOR is 4.28363%, q (simple annual rate) • Current 12 month LIBOR is 4.51863%, r (simple annual rate)

r • The firm might borrow for 12 months, but loan the funds for the first 6 months leaving an effec-ve ‘forward’ rate, f

)tr1())tt(f1()tq1( LSLS ⋅+=−⋅+⋅⋅+

⎥⎦

⎤⎢⎣

⎡−

⋅+⋅+

−= 1

)tq(1)tr(1

)t(t1f

S

L

SL4.65395%

10.5).0428363(11.0).0451863(1

0.5)(1.01f

=

⎥⎦

⎤⎢⎣

⎡−

⋅+

⋅+

−=

Forward Rate Agreement 4

t0 tS tL qB-qO

fB-fO

rB-rO

FRA term loan term

Similar to foreign exchange risk and ‘money market’ hedges, banks have a product called a ‘FRA’ forward rate agreement which packages the interest rate hedge

The actual loan interest rate will be set at tS while the actual interest will be paid at tL The FRA will be executed at t0 and settled at tS The effective loan or forward rate is set at t0, but the relative benefit of the FRA and cost of the loan are not known The FRA includes a ‘notational principal’, and is cash settled

Forward Rate Agreement 5

FRA buyer • is the loan borrower and takes the long position in the FRA • believes that interest rates may rise so seeks to hedge its interest rate risk exposure • becomes a fixed rate payer instead of a floating rate payer as it is initially • Equivalently makes the following transactions

• Borrows at the long offer rate rO over term t0 to tL • Lends at short bid rate qB over term t0 to tS • Locks in the forward offer rate fO over term tS to tL

FRA seller • is often a financial intermediary such as bank and takes the short position, but most likely will ‘lay off’ its risk • takes the short position in the FRA and becomes a floating rate payer • Equivalently makes the following transactions

• Lends at the long bid rate rB over term t0 to tL • Borrows at short offer rate qO over term t0 to tS • Locks in the forward bid rate fB over the term tS to tL

⎥⎦

⎤⎢⎣

⎡−

⋅+⋅+

−= 1

)tq1()tr1(

)tt(1f

SO

LB

SLB⎥

⎦

⎤⎢⎣

⎡−

⋅+⋅+

−= 1

)tq1()tr1(

)tt(1f

SB

LO

SLO

6

t0 = 0 tS = .5 tL = 1.0

4.4092%

1.5).0428363(11.0).0439363(1

0.51fB

=

⎥⎦

⎤⎢⎣

⎡−

⋅+

⋅+=

%4.7793

10.5).0415863(11.0).0451863(1

0.51fO

=

⎥⎦

⎤⎢⎣

⎡−

⋅+

⋅+=

• If the treasurer buys a FRA with notational principal of $10M and forward offer (borrowing) rate of 4.7793% • Treasurer effectively locks in the forward offer rate for a six month loan (tS < t ≤ tL) with principal $10M commencing in 6 mo. at tS. • The FRA is actually settled in cash at FRA expiry which we assume here is also the time of loan commencement. • Note that the FRA and loan are two completely separate agreements and transactions and that a party can buy or sell a FRA for speculation and not only to hedge a natural interest rate risk.

qB = 4.15863% rB =4.39363%

qO = 4.28363% rO =4.51863%

7

d1

z1·∆t f2·∆t f3·∆t f4·∆t f5·∆t f6·∆t

k 0 1 2 3 4 5 6

tk 0.0 0.5 1.0 1.5 2.0 2.5 3.0 d2 d3

d4 d5 d6

2t2

22

)z1(

tz

+

=⋅

6t6 )z1( +5t

5)z1( +4t4)z1( +3t

3)z1( +2t2)z1( +

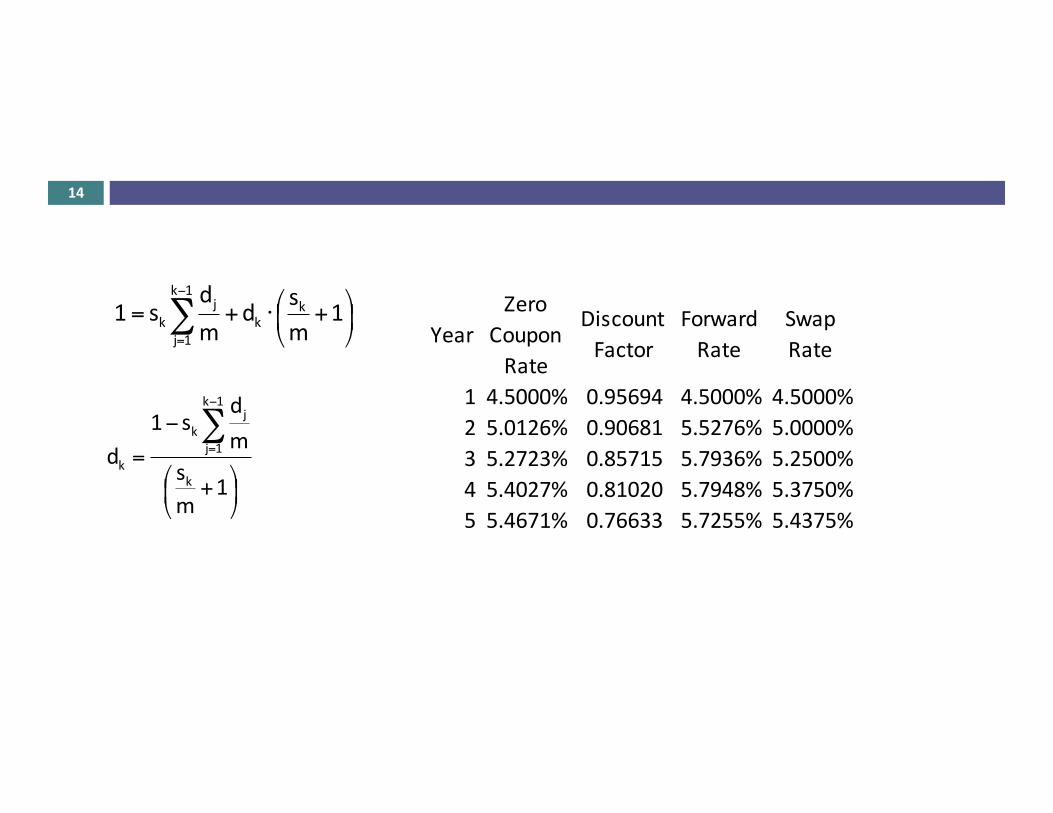

Now consider a sequence of future lending requirements – semi-annual for 3 years Zero coupon rates, zk 1 ≤ k ≤ 6 Forward rates, fk Δt = .5 Discount rates, dk

8

Δt)z(1CC1

10 ⋅+=

ktk

k0 )z(1

CC+

=

⎟⎠⎞

⎜⎝⎛ +

=Δ⋅+

=

mz1

1t)z(1

1d11

1

ktk

k )z(11

d+

=

1)-‐(d1m

1)-‐(d1

t1z

111 =

Δ=

1d1

z kt

kk −=

9

Δt)z(11d1

1 ⋅+=

Δt)f(1d

d2

12 ⋅+=

Δt)f(1d

dk

1kk ⋅+= −

⎟⎟⎠

⎞⎜⎜⎝

⎛−=⎟⎟

⎠

⎞⎜⎜⎝

⎛−= −− 1

ddm1

dd

Δt1f

k

1k

k

1kk

YearZero

Coupon Rate

Discount Factor

Forward Rate

1 4.5000% 0.95694 4.5000%2 5.0126% 0.90681 5.5276%3 5.2723% 0.85715 5.7936%4 5.4027% 0.81020 5.7948%5 5.4671% 0.76633 5.7255%

0%

1%

2%

3%

4%

5%

6%

7%

0 1 2 3 4 5

Rat

est years

10

Discount factors

dk

Zero coupon rates

zk

Forward rates

fk

Yields for coupon bonds

yj

‘Boot-‐strapping’

1d1

z kt

kk −=

ktk

k )z(11

d+

=

Δt)f(1d

dk

1kk ⋅+= −

⎟⎟⎠

⎞⎜⎜⎝

⎛−= − 1

dd

Δt1f

k

1kk

Interest Rate Swaps 11

Firm

Swap Dealer

Bank LIBOR

+2%

SWAP Rate

LIBOR

Net interest rate = LIBOR – (LIBOR +2%) – swap rate

= - (swap rate +2%)

12

YearZero

Coupon Rate

Discount Factor

Forward Rate

Swap Rate

Floating Cash Flow

Fixed Cash Flow

Net Flow to Swap Buyer

1 4.5000% 0.95694 4.5000% 4.5000% 450,000$ 543,750$ (93,750)$ 2 5.0126% 0.90681 5.5276% 5.0000% 552,764$ 543,750$ 9,014$ 3 5.2723% 0.85715 5.7936% 5.2500% 579,359$ 543,750$ 35,609$ 4 5.4027% 0.81020 5.7948% 5.3750% 579,479$ 543,750$ 35,729$ 5 5.4671% 0.76633 5.7255% 5.4375% 572,549$ 543,750$ 28,799$

Present Value 2,336,729$ 2,336,729$

13

kkk

2k

1k dFd

mcF...d

mcFd

mcFP ⋅+⋅⋅++⋅⋅+⋅⋅=

kkk

2k

1k dFd

msF...d

msFd

msFF ⋅+⋅⋅++⋅⋅+⋅⋅=

kkk

2k

1k dd

ms...d

msd

ms1 +⋅++⋅+⋅=

∑=

=k

1j

jkk m

dsd-‐1

∑=

= k

1j

j

kk

mdd-‐1

s

⎟⎠⎞

⎜⎝⎛ +⋅++⋅+⋅= 1msd...d

msd

ms1 k

k2k

1k

14

⎟⎠⎞

⎜⎝⎛ +⋅+= ∑

−

=

1msd

md

s1 kk

1k

1j

jk

⎟⎠⎞

⎜⎝⎛ +

−

=∑−

=

1ms

md

s1d

k

1k

1j

jk

k

YearZero

Coupon Rate

Discount Factor

Forward Rate

Swap Rate

1 4.5000% 0.95694 4.5000% 4.5000%2 5.0126% 0.90681 5.5276% 5.0000%3 5.2723% 0.85715 5.7936% 5.2500%4 5.4027% 0.81020 5.7948% 5.3750%5 5.4671% 0.76633 5.7255% 5.4375%

15

Discount factors

dk

Zero coupon rates

zk

Forward rates

fk

Yields for coupon bonds

yj

‘Boot-‐strapping’

1d1

z kt

kk −=

ktk

k )z(11

d+

=

Δt)f(1d

dk

1kk ⋅+= −

⎟⎟⎠

⎞⎜⎜⎝

⎛−= − 1

dd

Δt1f

k

1kk

Swap rates

sk

∑=

= k

1j

j

kk

mdd-‐1

s

⎟⎠⎞

⎜⎝⎛ +

−

=∑−

=

1ms

md

s1d

k

1k

1j

jk

k

16

CME begins clearing interest rate swaps CHICAGO/NEW YORK Mon Oct 18, 2010 (Reuters) - CME Group Inc said on Monday that it had begun providing clearing to the $400 trillion interest-rate swaps market, the largest of the opaque markets that lawmakers are forcing onto more transparent venues.

CME Information

Essen-al Concepts 17

Related Documents