r ., ,. , I , i I J ITTO PROJECT PD 14/95 REV.2(F) MODEL FOREST MANAGEMENT AREA-SARAWAK-MFMA PHASE IT CONSULTANCY REPORT FOREST REGENERATION AND PLANTATION DEVELOPMENT A.J. LESLIE MAY 1999 FOREST DEPARTMENT KUCHING

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

r ., ,. ,

I ,

i I J

ITTO PROJECT PD 14/95 REV.2(F)

MODEL FOREST MANAGEMENT AREA-SARA WAK-MFMA PHASE IT

CONSULTANCY REPORT

FOREST REGENERATION AND

PLANTATION DEVELOPMENT

A.J. LESLIE

MAY 1999 FOREST DEPARTMENT

KUCHING

r I l' ___ '

>1 U

[l

:.j ':.! :1

ACKNOWLEDGEMENT

The consultancy report "For~st Regeneration and Plantation Development" is a result of Dr. AlfLeslie's engagement in early.1999 by the ITTO supp.orted Project "Model Forest Management Area, Sarawak" of the Forest Department.· The-policy review was based mainly on expected developments in the timber export markets and is considered timely as Sarawak forest industries are preparing plans for the establishment of tree plantations from 2000 onwards in a situation· of near-total dependence on the export markets.

Dr. Leslie has visited Sarawak frequently. Prior to his engagement by the Project, he participated in forestry reviews organized by World Bank, Washington, and consulted expert-studies on world wood supply levels and tree plantation establishment, carried-out at FAO Forest Department in Rome. His views are based on a long life-time of experience in following market developments and a compilation of existing data, considered the best available at this point of time.

The outlook presented by Dr. Leslie in this report is entirely his own personal view. Significantly, in this respect, he has ended his report with: "Because that is what all of this amounts to - a gamble ... And you will never know much earlier than before 2015 arrives". Nevertheless, it is a point of view based on thorough study of possible development outcomes and worth of serious consideration.

. I

[PENGU MANGGIL for Director <ffForest

Sarawak

--"-'-- -- -~'.-'

FOREST REGENERATION AND PLANTATION DEVELOPMENT

TABLE OF CONTENTS

Page EXECUTIVE SUMMARY • 1

• 1. INTRODUCTORY

1.1 The Terms of Reference 4 1.2 A House Built on Sand 4 1.3 "For Whom The Bell Toll" 5

2. THE POTENfIAL OF THE REGIONAL AND GLOBAL PLANTATION RESOURCE .~ "

7 2.1 Comparison of the various sources of resource information 8 2.2 Growth Rates 10 2.3 The sustainable plantation output 11 2.4 The South Pacific Outlook 12 2.5 The Global Plantation Supply Outlook 13

3. INFERENCES FROM THE FOREGOING EVALUATION 15 3.1 The implications for plantation policy in Sarawak 15 3.2 The decline in output from natural forests 16

4. THE OUTLOOK FOR FOREST PRODUCTS DEMAND 17 4.1 The resultant wood supply-demand balance 21 4.2 The South Pacific Plantation Resource 23 4.3 The 10g-pulpwood distribution of demand 24 4.4 Probability Considerations 25

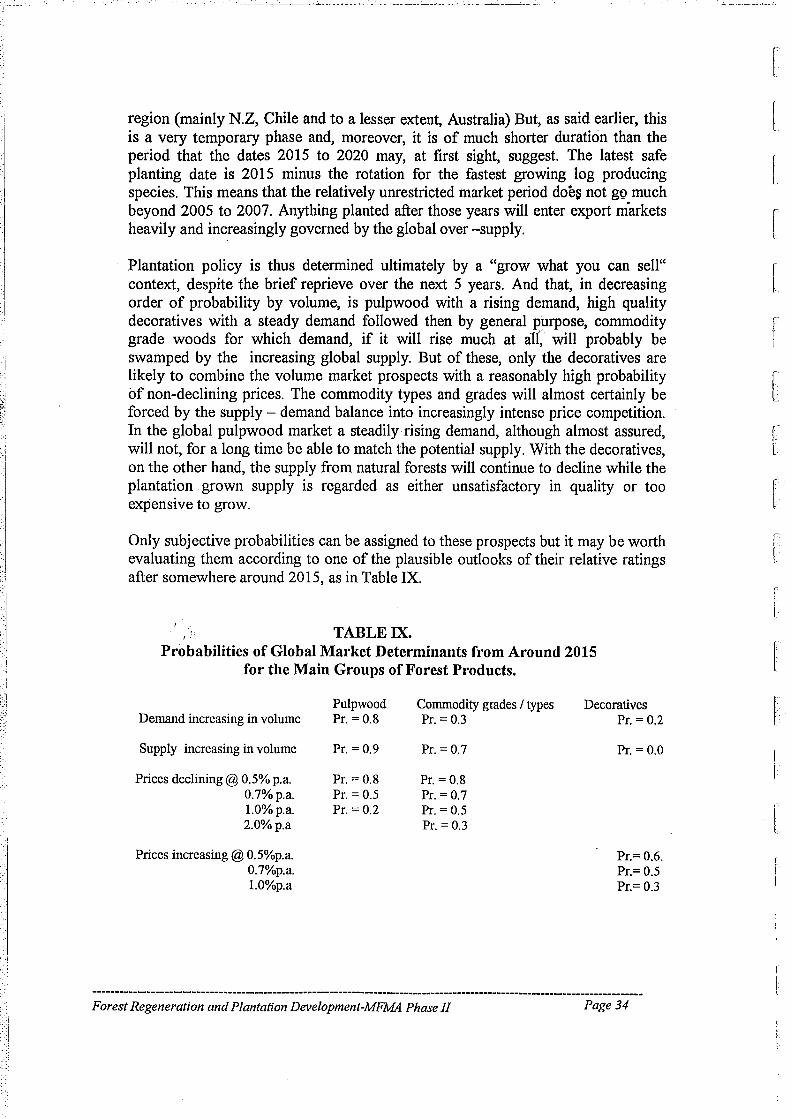

5. THE OUTLOOK 27 ;.~ 5.1 Factors influencing species selection 33 ,"-',

~~~ 5.2 Whose Job is it, Anyhow? 35 5.3 Plantations in the Market for Decorative 36 5.4 Plantation Policy for Pulp and Paper 37 5.5 Plantations for Log Production 39 5.6. Risk and Plantation Programme 42 5.7 The Dilemma in Plantation Strategy 43

6. A STRATEGY FOR PLANTATION DEVELOPMENT WITIDN MARKET AND SIL VICULTURAL LIMITS 48 6.1 The Role of the MFMA in Plantation Strategy 49 6.2 Implications for the MFMA Work Programme 2000 to 2003 51 6.3 A Caveat 54 6.4 Priority Ranking of the Recommendations 57

APPENDIX 1 - For Whom The Bell Tolls 61 APPENDIX II - The Decoratives 65

Forest Regeneration and Plantation Development-MFMA Phase II

r-.· -.

r

r (

I t

L f I ~:"'.

[,

I l

I I I

i i

!

-- ~~ ~~ -~~ ~- -~---- ----~ .

FOREST REGENERATION AND PLANTATION DEVELOPMENT

EXECUTIVE SUMMARY.

1. This report presents an analysis of:- . a) the way that regional and global wood supply - demand balances are likely to

evolve from around 2005 onwards and b) the implications of that for forest and plantation policy in Sarawak.

2. The analysis, the argument and the main findings are summarised below.

3. A combination of four factors is forcing Sarawak into a programme of forest plantation development. These factors are:-

a) the heavy dependence of the State economy on the forests sector and the already. established forest industry,

b) the almost total dependence on export markets for its outputs, c) the rising cost of log production from the natural forests aggravated by the

requirements of Sustainable Forest Management (SFM) and d) the very high probability that, with the coming on stream, initially of the Asia

Pacific region plantations followed soon afterwards by the global plantation resource, the export markets will, from 2003 to 2007 onwards, be increasingly over-supplied with the commodity type timbers that the natural forests largely produce.

4. Of these the dominant driving force is the prospect of oversupply in the export markets.

5. The first substantial surge in the supply from plantations will come in the Pacific rim marketS'~as the south Pacific plantations of New Zealand, Chile and Australia especially, add by'no later than 2007, at least 10 to 15 % to the annual supply of industrial roundwood in the region.

6. A surge of this magnitude is unlikely to be matched by an equivalent increase in regional demand, even allowing generously for growth in the Chinese market. Some downward pressure on price ceilings must, therefore, be expected. This review, however, does not indicate that the subsequent price competition will be more intense than the Sarawak industry can handle.

7. This is, however, no more than a very short-lived reprieve. When the second surge hits, less than ten years later, the global plantation resource will have the potential to meet almost all or even more than the world's total demand for industrial roundwood. Then, with supply greatly in excess of demand, price competition in commodity type timber markets will become increasingly intense. The Sarawak industry, as presently structured, is not well placed to cope with competition of the severity that is likely to prevail.

8. The development of a plantation resource might offer a way for Sarawak to ease, though not overcome the competitive situation, but the maximum leeway of 15 years available before that situation develops to its full extent, affords just enough time to bring the resource into being.

Forest Regeneration and Plantation Development -MFMA Phase11 Page J

-I

9. Two markets, however, are less vulnerable than the commodity timber market. One-the market for decorative timber - is almost totally so, but the other - that for pulpwood - is only so in a relative sense.

10. These cannot, however, maintain or substitute for the present industry. The sustainable yield of the decoratives is far too small and it cannot be expanded by plantatiOl). rapidly or certainly enough. Pulpwood is too low - valued a commodity for it to be an adequate revenue replacement.

11. Hence plantation development in Sarawak has to be part of an integrated, three pronged strategy linking and using the inter-dependence of-the natural forests and the plantations. The three prongs are:-

i) Supplementary plantations to provide a low cost roundwood output of probably-cnot less than say 75% of the present log intake capacity of the existing industry. This objective implies a total plantation resource of around 500,000 ha for commodity timber production,

ii) SFM in the natural forests concentrated on the decorative species which, on present indication, seem to have a sustained yield potential around 1. 5 to 2 million m3 and which might have the market capacity to carry the commodity type plantation timbers into the export markets through composite wood products and

iii) Pulpwood plantations for which the potential area is mainly limited by the availability of suitable sites within close range of export ports.

12. Each of these involves a different allocation of responsibility between the public and private sectors.

i) SFM of the natural forests is unavoidably a public sector responsibility. SFM is the key to continued access to overseas markets and as non-wood services

1 ~-, are the essence of SFM they must be safeguarded, which makes timber

ii)

i'production a conditional use. SFM and the maintenance of the timber industry around its present level are both, therefore, sine qua non for Sarawak. Thus the management and utilisation of the natural forests are concerned with the supply of public goods. This is a responsibility that the State is best equipped to meet.

Supplementary plantation could, in principle, be left to the private sector if it were not for one thing - the public goods nature of the continuity of the timber industry. There is no unavoidable compulsion for individual companies or the industry as a whole, to establish, maintain and manage a resource on the scale required. They can, at any time, stop, withdraw or liquidate their investment should financial considerations make it expedient to do so. This option is neither one for the State nor something which Sarawak can afford to happen or allow to happen. The necessity to safeguard the State's vital public interest in the plantation programme, therefore, means that the State must be involved in some form of joint ventures at least, to guarantee that this prong of the plantation programme is not abandoned or curtailed.

iii) Pulpwood plantations have virtually no public goods content. The responsibility for them can, therefore, be left entirely to the private sector.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 2

I

l

r-

[-

r l

r i (

[ r \

L

r f l:

j

l

l

f \ .

1

. li

i I

'.,

I· i

13. The maximum interval of 15 years 'before the full impact of the global surplus in commodity timber swamps the export markets is just enough time for Sarawak to establish and have a producing resource adequate to take on the competition and maintain its industry at its present level. The commencement, on a large scale, of the supplementary plantation programme cannot be safely delayed fo.r much longer than another year. •

14. It is fortunate, therefore, that the range of commodity timber species likely to succeed in Sarawak is already known and wide .enough for long term species trials not to be a necessary pre-condition. From a technical point of view, the programme could start today.

15. The MFMA has no essential role in the supplementary plantation programme. It does, however, have a vital role in developing the prescriptjpns for and the practice of SFM and the plantation technology for gap filling with decoratives in the natural forests. Without this the supplementary plantation programme is almost pointless.

16. The role of further processing is not, strictly speaking, a component of plantation strategy. It does, however, have a place in helping to ease the competitive pressure which will confront the Sarawak timber within the next few years. A few companies have developed niche markets especially in Europe and the USA, for specialty knocked down furniture and furniture components, working to customer specified designs. This type of market could certainly be extended geographically and possibly in product range. But. forest poliCY, in general, will have to develop measures to overcome problems experienced with the reliability, continuity and quality of log supply to the smaller companies who have pioneered many of these market developments. The future availability of some of the rare feature timber species which have been brought into these markets does have some relevance to plantation strategy. While this is probably more associated with the SFM issue, it does bring the MFMA into play as part of its experimental work involving gap -filling decoratives.

Forest Regeneration and Plantation Development -MFMA Phase JI Page 3

:.1

1. INTRODUCTORY

1.1 The Terms of Reference

The T.O.R. for this consultancy are to:-1. Review current state policy of plantation development and long-term wood

production prospects for Sarawak. ~ 2. Review natural forest regeneration and regrowth compared to plantation

growth prospects, including aspects of environmental impacts. 3. Advise on development strategy to be initiated as well as planning and

monitoring capabilities required from Forest Department/Corporation and compames.

4. Advise on a strategy for resource development in :MFMA with particular view to a work plan for the period 2000 to 2003 including tree plantation, natural·f~rest management and silvicultural treatments.

5. Prepare a review and recommendation report.

These T.O.R. largely amount to looking at the basis of the formulation and implementation of forest plantation policy in Sarawak, recommending any changes or modifications needed in it and how the policy should then be incorporated in the MFMA.

To that end, two analytical and interpretative processes are involved. Most obvious is the one concerning the choice of species for the plantation programme. This means assessing the suitability and likely performance of a number of possible candidate species under the range of ecological environments in Sarawak.

In the Sarawak context, however, it is the second process which is, initially, more,critical. This takes, as the starting point, the markets for the plantation grown iwood rather than species suitability. If Sarawak is to realise anything more than a tiny fraction of its forest resource potential it will for many years, have to export close to all of its output of forest products. The reality is that it is the export markets of several decades into the future, not the growing conditions in Sarawak, which govern the choice of species, and, in fact, whether there should be a plantation policy at all.

That, of course, is just a restatement of the old aged dilemna in forestry expressed in the adage "To sell what you can grow or to grow what you can sell." With the natural forests there is little choice - to sell what has grown naturally and what can be grown in them. For Sarawak that is a matter of the export markets, but with plantations there is a choice, but more in principle than in actuality. Again it is a matter of the export markets. So the export markets hold the key not just to plantation policy but to forest policy in general and forest industry policy.

It may be worth noting here that this market dependence applies only to plantations for industrial wood supply. Afforestation for other purposes such as land rehabilitation, erosion control, watershed protection, fuelwood, carbon sequestration is best done with species that are known to grow on the sites in

Forest Regeneration and Plantation Development -MFMA Phase II Page 4

r:

t

r [

r I

r f l

f

L

I

f L

n U

I I

,

<1,>

mind. These are relatively minor objectives in Sarawak so that plantations for wood supply are plantations for export markets. Grow what you can sell ought to be the compelling motive and that becomes what will sell in the export markets, one rotation at least into the future.

And that requires, like it or not, forecasts of regional and even glob.al markets 15 years hence at least and more probably 20 to 30 years and more int<> the fuj:ure. But the future of production in the natural forests also depends on future markets in the short term as well as the longer. The market outlook on a continuous basis in the immediate, middle and long term distance is an unavoidable necessity for an export dependent sector.

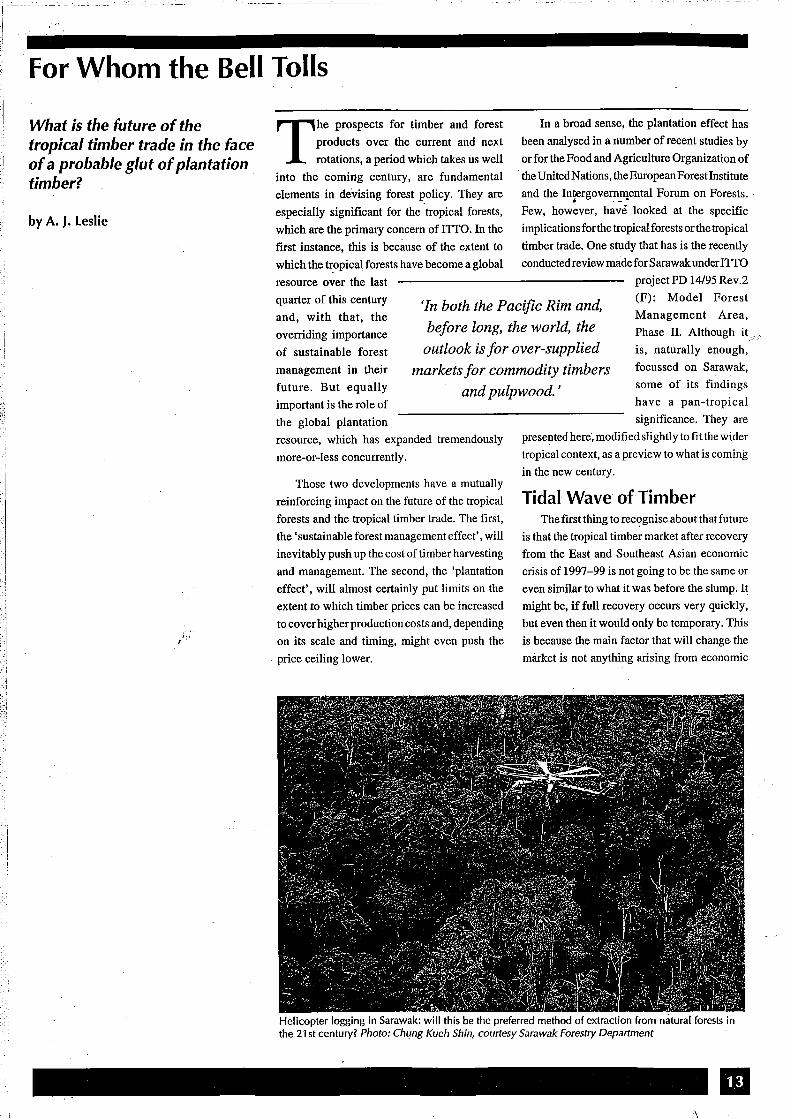

An introductory note on this theme - "For Whom The Bell Tolls" - was drafted in mid-1998 and has had some limited circulation (included in this review as Appendix I). The argument in it was that the future markets for most of the Sarawak production would be over-supplied and hence subject to tight and lowering price ceilings. The outlook follows from the likelihood that by the second' decade of the 21st Century the global plantation resource already established by 1998 would have a sustainable output capacity close to the world demand for industrial roundwood. Together with the supply, even if it is declining, from natural forests and additional planting after 1998, the total supply available could well greatly exceed demand within the next 30 years or so." The only thing that could change this outlook is a growth in demand for industrial roundwood considerably greater than the historical record suggests is possible.

The note was prepared hurriedly, at short notice and largely without access to documentary sources. The implications of the outlook outlined in the note are strongly contrary to much of current thinking and opinion. Even if they are only rougb.ly. right, present plantation policy and forest industry strategies would have to be almost completely over-turned.

1.2 A House Built on Sand The elements of a plantation policy all derive from the answers to a single question - why? This is because the purpose or purposes of a programme for plantation development govern what to grow, how much to grow, how to grow it, when to grow it and by whom it should be done, entirely in some cases but largely in all. Fundamental though that question is, discussion of and about plantation policy is almost invariably about the derived elements rather than the one from which they all originate - the question "why plantations?"

Plantation policy is a classic illustration of this approach. In the publication "Planted Forests in Sarawak" of February 1998, one of the definitive public statements on plantation policy, the reasons for the proposed development of plantations in Sarawak are barely mentioned. In the 160 pages of papers the number of places in which the purpose of the plantations is mentioned add up to no more than half a page. The most definitive of those occasional references are:-• "The State had reached its peak in producing timber from natural forests and

needed to find better ways to sustain timber resources"

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 5

.' : i

• "Reforestation with fast growing species to supplement timber production" • "A good demand for wood for pulp ... .in view of the large pulp and paper

plant to be implemented in the State".

Clearly plantation policy in Sarawak is motivated by timber production but with a twofold purpose. The first is to maintain the existing industry (~nd, .although not specifically mentioned, possibly to provide the raw material basis' for. its expansion). The second is to build up the raw material base for a "large" pulp and paper industry.

On the whole this makes sense, at least in respect of the first objective. The capacity of the existing industry is already greater than the sustainable capacity of the PFE and with much of that capacity in "state of the art" manufacturing plants the industry is well worth sustaining. And in that line of reasoni~g. Sarawak is far from unique. This fact has been and still is the standard thinking behind most of the large scale plantation programmes in the rest of the world.

What is not often made clear is the crucial assumption on which that line of reasoning depends. Underlying it all is the belief that the market for the unprocessed, semi-processed and more fully processed products which can be made from the plantation wood will continue to absorb the present volumes (and probably more) at the same (or higher) prices. The present slump in which the contrary is happening is generally assumed to be a temporary abberation; when it is over the future will resume its pre-slump course.

Nowhere in the proceedings of the conference is this assumption mentioned, let alone questioned. More significantly it is rarely questioned anywhere else either. In effect, the assumption is taken as a fact rather than an assumption. But it is a pseudo-fact.

J ..

Until ll(1)W there has been nothing much wrong with using it. Since the end of World War II, the demand for all industrial wood products has been rising steadily while on the supply side, the area of the world's forest has been declining just as quickly. Putting those two trends together, readily allows the assumption to be translated into fact. But that situation no longer holds. The demand side of the equation has been changing in recent years while the supply side is about to change dramatically. Put bluntly, the global wood supplydemand balance for industrial wood is moving towards over-supply in commodity types and grades of wood. With that, any post-recovery resumption of the pre-slump course and conditions can only be very short lived. The pseudo-fact is reverting to the assumption it really is and always has been. And that assumption is wrong.

1.3 "For Whom The Bell Tolls" This interpretation of the trend in the global (and regional) wood supply-demand balances and its implication for forest policy generally in Sarawak were outlined in the note "For Whom The Bell Tolls" of July 1998. The note was mainly directed at the sustainable management of natural forests. Plantation policy was mentioned but only in passing. Nevertheless the implications for plantation

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 6

[ i

l r

r '. [

r' f

["

l

f'

l r L·

""","" . -~----- -- ---- --------- -- -----'---------'-----------,--

J 'i ·:1

i

i.

I I. !

:1 I i . !

policy, if the analysis of the wood supply-demand balance is anywhere near valid, are equally devastating.

But the interdependencies and interactions between the supply from natural forests and any proposed plantations, between the utilization patterns, technologies and potentials of the two wood sources and the~ between the forests sector of Sarawak and the rest of the world are so strong 'andinmcate that it makes no sense to consider natural forest policy and plantation policy independently of each other. Much of the analysis and interpretation in "For Whom The Bell Tolls" applies in fact, with equal force to the plantations.

The implications in that note follow entirely from the anticipations in it of the impact on regional and global wood supply-demand relationships of the world's plantation resource built up over the past 20 to 30 years, as it comes into maturity early in the 21st Century. Especially significant for Sarawak is that part of the resource in the south Pacific area which is on the verge of a large scale entry into the Asia-Pacific' regional supply.

In short, the basis of the "For whom .... " note is that regional over-supply of the general purpose, utility commodity timbers is imminent and the world will move into a similar position not long aftetwards.

The important point at this stage is therefore the validity of this prospect of over-supply. If it is even roughly true as a representation of the outlook for the forest and forest industries sector in the Pacific Rim region then the implications for natural forest management in the tropics are almost inevitable. They, in turn, make much of the current thinking about plantation policy questionable and perhaps, untenable and consequently, a drastic rethinking of plantation policy could well be needed. But if that over-supply prospect is not valid, then present policies .. may be on the right cqurse. May be, of course, does not necessarily mean that they are.

2. THE POTENTIAL OF THE REGIONAL AND GLOBAL PLANTATION RESOURCE

There are certainly plausible grounds for some scepticism about the reasoning and the implication in the note "For Whom The Bell Tolls". For a start, the estimates in it of the magnitude of the south Pacific and the world plantation resource are just that-estimates. There was certainly little authoritative about them. More authoritative figures are now available.

Shortly after the note was written, FAO published a summary and review of the global plantation resources as part of a survey of progress with its Global Fibre Supply Study (The GFSS). The New Zealand Ministry of Forestry also produced its latest "National Forest Description" in 1998, with revised forecasts of its plantation output for well into the 21 st century. Australia also launched the "Plan" announced in 1997 for trebling the area of its plantations by the year 2020. FAO's "Outlook Study for the Asia-Pacific Forestry Sector" has just been approved (November 1998) for publication. Drafts of the final report of the GFSS (now renamed as a "Model" rather than a "Study") and a

Forest Regeneration and Plantation Development -MFMA Phase II Page 7

complementary "Thematic Study on Plantations" as part of the FAO Global Forest Products Outlook Study are now under review.

All of this work could affect the "For Whom .... " figures and conclusions. Hence, with a lot more and apparently better information available than that which went into the note, a re-assessment of its validity is clearly warranted. Whether it would greatly modify the implications for Sarawak" i:;;' how~ver, problematical. After all neither of the two FAO _ reports on the plantation resource claim any great accuracy for their figures. For example, the Thematic Study is "at best a ball park analysis. . .. aimed at an order of magnitude in the results rather than any definitive prediction". And the FAO paper "The Role of Industrial Plantations in Future Global Fibre Supplies" makes the point that "The present lack of reliable information on almost every aspect of forest plantations, in developed and developing countries and regions alike, makes predictions about future supplies hazardous and liable to gross errors".

In effect, these more authoritative sources of information may not be all that much better than the estimates that went into the note "For Whom The Bell Tolls". In any case, with such a large in-built "error term" the differences would have to be enormously large for them to invalidate its analysis and implications. Nevertheless it is worth seeing whether there are such differences.

Two steps are involved. The first is to assess the nature and magnitude of the differences between the sources and the estimates underlying the "For Whom .... " note. The second then is to work out whether those differences warrant any significant change to the implications and findings of that note.

2.1 Comparison of the various sources of resource information The most recent and more official sources which can be used for comparative purposes are referred to earlier in this analysis (page 7). The three FAO papers and dr~fts superceded its earlier assessments of 1990 and 1992. The two national statements (Australia and New Zealand) are their latest, official accounts. Being as FAO points out, virtually the only fully reliable and clear cut statements of national plantation resources, they can be safely inserted into the FAO global figures whenever a correction seems to be needed.

Even a cursory comparison of the various sources is enough to show some considerable differences. On closer examination four classes of differences show up. These are:-

a) between the estimates underlying the "For Whom ... " note and some of the other sources

b) between the various other sources c) between estimates originating in the same agency, and d) within some of the individual reports and papers

Only the first two sets of differences really matter. The other two sets actually represent the preliminary status of the reports. The inconsistencies will no doubt, be reconciled as the reports go through the review and revision processes before they are released. Take, as an example, the differences within the FAO paper

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 8

[ l

r l

r I

r-' I

I

-,.-. ...:.-.-~

"The Role of Industrial Plantations ... " (Unasylva, 193: 37-43 of 1998) between a total area for industrial plantations in South America in the summary total and 7 x 106 ha. for Brazil in the text and between that paper and the 4.2 x 106 ha for Brazil in the thematic study. It is unlikely that such wide differences will show up in the finalised reports.

• The first two sets of differences are another matter. A most obviouS'differeoce is in the global area of the industrial plantation resource. The "For Whom ... " note is based on the estimate of the area in 1998 of 150 x 106 ha. The Unasylva paper has the area at 119 x 106 ha in 1995, the thematic study at 98 x 106 ha in one place and 113 x 106 ha in another. Allowing for the area added between 1995 and 1998, then, depending on the rate at which the annual new planting is estimated would give four figures for the 1998 area, as follows:-

"For Whom .... " note Unasylva Thematic Study Thematic Study

150 X 106 ha 137 x 106 ha (119 x 106 ha + 3 x 5 X 106 ha) 113 x 106 ha (98 x 106 ha + 3 x 5 X 106 ha) 131 x 106 ha (113 x 106 ha + 3 x 6 X 106 ha)

But the 1998 areas depend on the planting rates over the three years 1995 to 1998 and there is no definitive statement of what that global figure was or now is. In the note, a global rate of additional industrial plantation establishment of 5 to·8 x 106 ha was assumed. It is difficult to find a more definitive rate in the FAO reports. The thematic study puts the current annual rate of additional plantation establishment at "slightly more than 4 million ha per annum" in " tropical and sub-tropical countries. If it is assumed, as some of the internal evidence in the reports suggests, that the rate in boreal and temperate countries is roughly the same, then the global rate would be a little over 8 x 106 ha a year i.e. the upper bound assumed in the note. There is a chance then that there is no diffefjence in this aspect between the note and the other sources. Certainly it is safe t6'say that the rates assumed (5 and 6 x 106 ha a year) in deriving a 1998 area from the FAO information for 1995 are unlikely to be exaggerations.

The area estimates underlying "For Whom The Bell Tolls" are not, therefore, so far out of line with the more authoritative estimates as to negate or undermine its implications. A possible exception is the lower figure in the thematic study where the discrepancy between it and, that for sub-regional supply in the note is around 25%. But, given the extent of .approximation, guesswork and unreliability in the data base, a 25% extent difference is probably within the confidence limits of the FAO estimates.

The area of the plantation resource is, however, only one component in assessing the impact of plantations on wood supply outlooks. Equally important are the growth rates and, for the timing of the impact on and flow into the markets, the age class distributions and rotations.

The pivotal feature in the "For Whom ... "note was the age class distribution of the south Pacific Plantations, heavily biased by the great acceleration of the rate of planting in the 1970's and 80's. As a result a sharp and massive increase in the availability of mature plantation timber (mainly radiata pine) was predicated

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 9

1-----~---- -

! I

i

from about the years 2003 to 2005 on rotations between 25 and 35 years and growth rate of 15 to 25m3/ha/a.

In much the same vein, a roughly parallel development of the global plantation supply was predicated in the note although on a much larger scale and now the initial surge occurring 10 or 50 years later. The known rotation information (10 to 50 years and even more in some northern hemisphere cases) Rl'ld the-more limited growth rate, information (4 to 30m3/ha/a mai) could not be used in the absence of age class distribution information. So the global surge was taken as occurring around 2010 to 2015 with an overall average mai of 12m3/ha/a.

Now that a much bigger and more detailed set of more up to date information is available it is possible to get some idea on how the approximations us·ed in the note stand up:.

Four elements of the plantation outlook are critical. They are:

• The rate at which the area of the plantation resource is expected to be likely to increase in the future.

• For how long the area will continue to increase at that rate or at a higher (whatever that is) rate or a lower (whatever that is) rate.

• The growth rates to be expected and then

• From these the potential sustainable output of plantation timber.

2.2 Growth Rates Although it is virtually impossible to judge the validity of the 12m3/ha/a. used in the not~ as an estimate of the global plantation M.A.I. it is actually the easiest component to deal with. The FAD thematic study lists growth rates for tropical and sub-tropical hardwood plantations ranging from 1.5 to 25· m3/ha/a, according to species and country and similarly for temperate and boreal plantations ranging from 1 to 24 m3/ha/a . The lists are fairly complete for the main species and cover most of the relevant countries. However, without matching area information, only a simple unweighted mean can be derived from the lists. This, at around 13m3/ha/a. supports the estimate underlying the note.

The Unasylva paper has a much shorter list of sample growth rates both by species and countries but with corresponding area data. The weighted mean of the minimum growth rates quoted is 9.4 m3/ha/a. and of the maxima, 10.2. That is the average MAl could be 15 to 25% lower than in the note.

Neither set - the one questionable because it is unweighted and the other because it is so incomplete - provides much evidence to suggest that the average growth rate of 12 m3/ha/a underlying the note is seriously incorrect.

Forest Regeneration and Plantation Development -MFMA Phase II Page 10

[

r , I

f t

r

r

l

r l

f I l

i (-

\.

I I

l

il

2.4 The sustainable plantation output The other two elements which feed into the plantation supply outlook are matters entirely of conjecture. Certainly some countries have set announced targets for additional planting. Some have ideas of how much they anticipate planting or will plant and many hardly have a clue. Not that any of them mean much. Targets can be increased, decreased or abandoned virtually. overnight as the circumstances seem to suit. Expectations similarly may be reali~ed, . may go unrealised, may be upset by new entrants or by unforeseen withdrawals. Future planting rates and changes in them are mere guesses.

Perhaps therefore, it is on this account that many of the attempts to forecast future supply from plantations start with a "basic case" scenario of no additional planting. This is realistic enough in that only plantations which are already established can be confidently counted on for future supply. But it is also often unrealistic in that some additional plantations will be planted, at least over the next few years. Other scenarios are then simulated with different rates of additional planting continuing indefinitely or for various periods into the future or increasing or decreasing at various rates over future time.

None ofthese devices nor any amount of econometric analysis can convincively hide the fact that, in the end, forecasts of wood supply from plantations are largely guesswork. Actually, it cannot be otherwise. Many of the "facts" regarding the area of already established plantation are no more than suspect approximations, while estimates of what might be added in the future are just anybody's guesses.

The FAO thematic study presents three scenarios. The base case scenario is zero increase in plantation areas, the second allows for a 1% increase in the plantation annually over the whole forecast period and the third has the area of additi,Onal planting declining from the current rate in 25% steps for each 10 years and coming down to zero by 2050. The illustrative test of the FAO global fibre supply model is based on reducing the annual rate of planting by 7% per annum until it reaches zero in 2010. Being principally concerned with the development of the model, this scenario is apparently not meant to be taken as a prediction.

None of these fits at all well with projections or outlooks available from some national authorities. The New Zealand scenarios set out three ievels of additional planting at 40,000, 60,000 and 90,000 ha annually, continuing at least until 2040. The Australian vision sets a target of 90,000 ha a year until the total area of plantations is trebled. Chile is reported as continuing with additional planting at around 120,000 ha annually.

The rate of additional planting will no doubt decline, if only because the implications of potential over-supply could become too obvious to ignore. But any prediction based on an early phasing out of additional supply will certainly under-estimate the plantation supply from 2020 onwards.

Hence, despite the greater detail, and presumably the greater precision of the more authoritative information now available, it is still no easy matter to

Forest Regeneration and Plantation Development -MFMA Phase II Page 11

, I

I

evaluate it against the simple basis underlying the note. Nor when that is done is there likely to be much certainty that the comparison would be any more conclusive. All the same it is worth a try; especially for the south Pacific from where any significant impact will first come and for which the information is the least speculative.

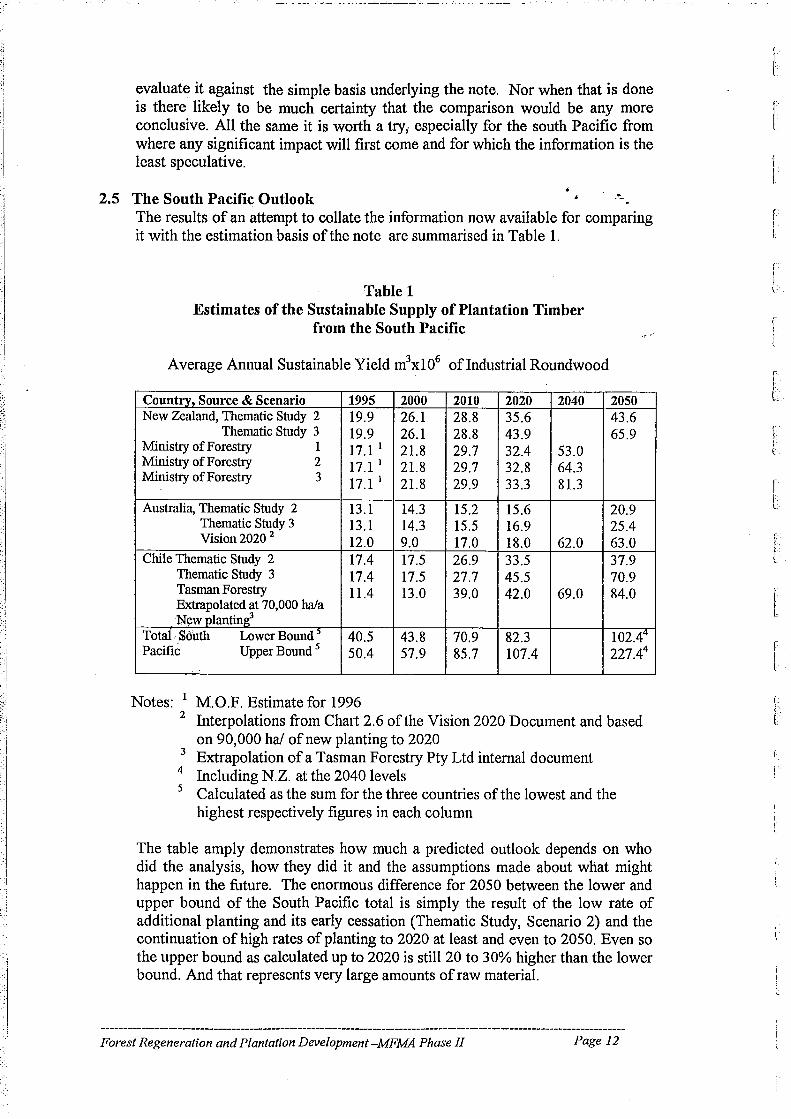

2.5 The South Pacific Outlook --The results of an attempt to collate the information now available for comparing it with the estimation basis of the note are summarised in Table 1.

Table 1 Estimates of the Sustainable Supply of Plantation Timber

from the South Pacific

Average Annual Sustainable Yield m3x106 ofIndustrial Roundwood

Country, Source & Scenario 1995 2000 2010 2020 2040 New Zealand, Thematic Study 2 19.9 26.1 28.8 35.6

Thematic Study 3 19.9 26.1 28.8 43.9 Ministry of Forestry 1 17.11 21.8 29.7 32.4 53.0 Ministry of Forestry 2 17.11 21.8 29.7 32.8 64.3 Ministry of Forestry 3 17.11 21.8 29.9 33.3 81.3

Australia, Thematic Study 2 13.1 14.3 15.2 15.6 Thematic Study 3 13.1 14.3 15.5 16.9 Vision 2020 2 12.0 9.0 17.0 18.0 62.0

Chile Thematic Study 2 17.4 17.5 26.9 33.5 Thematic Study 3 17.4 17.5 27.7 45.5 Tasman Forestry 11.4 13.0 39.0 42.0 69.0 Extrapolated at 70,000 hala N~w plantint

Total South Lower Bound 5 40.5 43.8 70.9 82.3 Pacific Upper Bound 5 50.4 57.9 85.7 107.4

Notes: 1 M.O.F. Estimate for 1996

2050 43.6 65.9

20.9 25.4 63.0 37.9 70.9 84.0

102.44

227.44

2 Interpolations from Chart 2.6 ofthe Vision 2020 Document and based on 90,000 ha! of new planting to 2020

3 Extrapolation ofa Tasman Forestry Pty Ltd internal document 4 Including N.z. at the 2040 levels 5 Calculated as the sum for the three countries of the lowest and the

highest respectively figures in each column

The table amply demonstrates how much a predicted outlook depends on who did the analysis, how they did it and the assumptions made about what might happen in the future. The enormous difference for 2050 between the lower and upper bound of the South Pacific total is simply the result of the low rate of additional planting and its early cessation (Thematic Study, Scenario 2) and the continuation of high rates of planting to 2020 at least and even to 2050. Even so the upper bound as calculated up to 2020 is still 20 to 30% higher than the lower bound. And that represents very large amounts of raw material.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 12

r I I

r i I ,

r L

r i l

·i

I ; I. ~

:.:-....::.:.----'-:~-:. _ ... _.- -~., - -- -.~- _._--- -- - -- ----- - -- -'---'--- '-~

There are also some surprising differences between sources which have nothing to do with assumptions. Even at the starting date - 1995 - when actual data should have been equally available and hence, identical, appreciable differences show up. It would seem that different statistical series are in use in different places. If what should be firmly established fact has a fairly wide error range, differences in conjectural information are hardly a cause for woqder. But it is certainly a cause for treating them with caution if not scepticism: As the:FAO thematic study says they are "ball park" figures at best.

It should be noted also that the levels quoted for 1995 are estimates of the potential sustainable yield from the plantations established by that year. Some may be the actual recorded output for 1995 but others do seem to estimate the potentiaL This could account for the "surprising" inconsistency for 1995. But with the actual cut in 1995 for Australia being well below the corresponding sustainable yield of the existing plantations, the increase in possible output in subsequent years is somewhat greater than would appear from Table 1.

The concern in Table 1 is not, however, with the inconsistencies and the variations in the information now available, striking as they are. The main purpose is to help assess the validity of the estimate of 60 x 106 m3 annually being added to the Asia Pacific regional supply from around 2005 onward and which is the basis of the implications considered in the note "For Whom The Bell Tolls".

Nevertheless, "ball park" figures or not, the contents of Table 1 strongly suggest that 60 x 106 m3 by early in the 21st Century is too high. A more credible figure to plan on would be an increase in roundwood supply in the region of around 40 x 106 m3 annually by 2010 and probably, judging by the N.z. annual predictions, from around 2005. The 60 x 106 m3 level could, however, be reached before 2020··

1 :. - I

2.6 The Global Plantation Supply Outlook For a number of reasons including, especially, data quality, completeness and reliability the outlook on the magnitude and timing of the global plantation resource in global wood supply is even more problematic and even less predicable. The detailed analysis on the FAO thematic study, which omits Europe and the former USSR, shows an age class distribution of the rest of the world's plantation resource heavily skewed towards the younger age classes. "Overall, 67% of the five-region plantation total is less than 15 years of age, with 30% [of the total area] planted between 1990 and 1995". Only 13% of that total area is in plantations of 30 years and older.

On that basis, the total potential sustainable yields as calculated in the study are summarised in Table n.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 13

!"

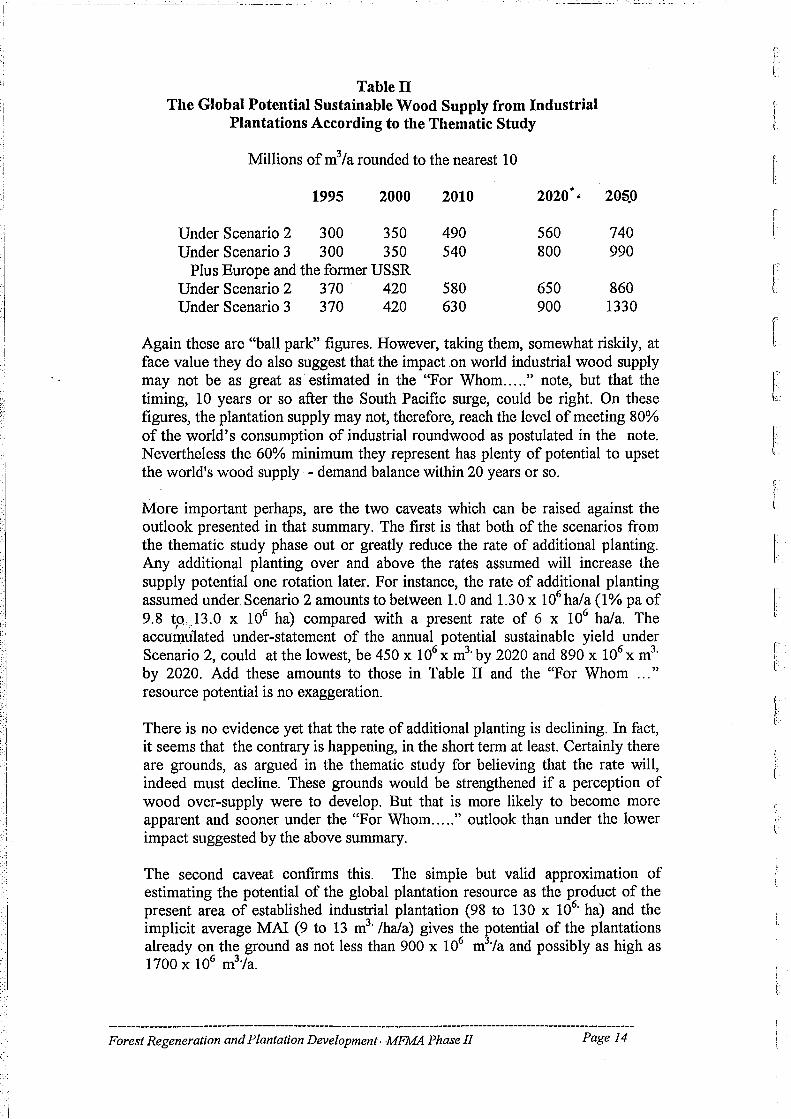

Table 11 The Global Potential Sustainable Wood Supply from Industrial

Plantations According to the Thematic Study

Millions of m3 la rounded to the nearest 10

1995 2000 2010 2020· •

Under Scenario 2 300 350 490 560 Under Scenario 3 300 350 540 800

Plus Europe and the former USSR Under Scenario 2 370 420 580 650 Under Scenario 3 370 420 630 900

205.0

740 990

860 1330

Again these are "ball park" figures. However, taking them, somewhat riskily, at face value they do also suggest that the impact on world industrial wood supply may not be as great as estimated in the "For Whom ..... " note, but that the timing, 10 years or so after the South Pacific surge, could be right. On these figures, the plantation supply may not, therefore, reach the level of meeting 80% of the world's consumption of industrial roundwood as postulated in the note. Nevertheless the 60% minimum they represent has plenty of potential to upset the world1s wood supply - demand balance within 20 years or so.

More important perhaps, are the two caveats which can be raised against the outlook presented in that summary. The first is that both of the scenarios from the thematic study phase out or greatly reduce the rate of additional planting. Any additional planting over and above the rates assumed will increase the supply potential one rotation later. For instance, the rate of additional planting assumed under Scenario 2 amounts to between 1.0 and 1.30 x 106 ha/a (1 % pa of 9.8 t,o,)3.0 x 106 ha) compared with a present rate of 6 x 106 ha/a. The accumu1ated under-statement of the annual potential sustainable yield under Scenario 2, could at the lowest, be 450 x 106

X m3. by 2020 and 890 x 106

X m3.

by 2020. Add these amounts to those in Table IT and the "For Whom " resource potential is no exaggeration.

There is no evidence yet that the rate of additional planting is declining. In fact, it seems that the contrary is happening, in the short term at least. Certainly there are grounds, as argued in the thematic study for believing that the rate will, indeed must decline. These grounds would be strengthened if a perception of wood over-supply were to develop. But that is more likely to become more apparent and sooner under the "For Whom ..... " outlook than under the lower impact suggested by the above summary.

The second caveat confirms this. The simple but valid approximation of estimating the potential of the global plantation resource as the product of the present area of established industrial plantation (98 to 130 x 106

. ha) and the implicit average MAl (9 to 13 m3·/ha/a) gives the rotential of the plantations already on the ground as not less than 900 x 106 m ·/a and possibly as high as 1700 x 106 m3/a.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 14

r l

r f

! t (

f

f: .. " L

i j

;,1

"I

The risk, referred to earlier in taking the figures in Table 11 at their face value is therefore quite real. Actually, the grounds for accepting the estimates in the "For Whom .... " note are probably stronger than those for discarding them on the basis of the most authoritative information now available.

3 INFERENCES FROM THE FOREGOING EVALUATION

3.1

In general then, the informational basis of the "For Whom ... " note is not seriously invalidated by the more authoritative' information now available. There is one major exception - the south Pacific surge in supply will probably be smaller and its timing later than stated in the note. Nevertheless the surge will still be considerable - 35 to 40 x 106 m3'/a - and it will still occur like a tidal wave, but a year or two later than 2005 rather than earlier. The short term impact on the industrial wood supply-demand balance of an addition of 7 to 10% to the annual supply instead of the 15 to 20% in the note could therefore be less dramatic. But it leaves the longer term outlook from 2020 onwards, much the same as developed in the note and, for the moment, the implications remain.

What needs to be investigated in the light of the revised short term figures is the effect of the smaller first wave from the South Pacific resource.

The implications for plantation policy in Sarawak Plantations established from 1995 onwards will mature into the wood supply -demand situation of 2010 to 2020 onwards. Hence it is the longer term outlook for wood supply-demand balances that counts in the formulation of plantation policy. That situation could, as argued in the "For Whom .... " note, be one of potential industrial wood supply considerably greater than demand for the general purpose, utility or commodity grades and species.

Only, tyJo things could upset that outlook and its implications for Sarawak espeCi'aily. One is a much greater decline in production from natural forests than that allowed for in the supply outlook. The second is a substantial increase in regional and global demand for industrial wood products. As a combination of the two would obviously require a lower rate of increase in each than either one operating alone, it is that possibility whose effects need to be examined. But in order to establish the bounds of possible or likely combinations, each factor has to be first considered separately.

Before turning to that however, something does need to be said about the effects of the downward revision in this short term outlook. It has no direct implications for plantation development policy but industrial strategy decisions taken in the light of the possibly lessened threat could have an indirect influence in several ways.

First the smaller size of the surge in supply in the Pacific rim region could be interpreted as assurance that the export markets are not going to be depressed by prices and competition as implied in the "For Whom .... note".

Forest Regeneration and Plantation Development -MFMA Phase II Page 15

3.2

Then secondly, the possibly delayed onset of the surge gives the sector that much longer to adjust and re-structure to the changed conditions before they amve.

But thirdly there is a danger that the extra time could lull the sector into thinking any recovery from the "economic crisis" would bring a permanent return to the • pre-slump market situation.-·

Only the second of those inferences is both positive and unquestionable. Even so, it is only an advantage if the sector uses the extra time to make its adjustments. But the other two, if they are taken as accurate, would indicate that neither adjustment nor the time to make it, are needed. That however would no more than be a temporary reprieve. Eventually and before long, the longer term global ov~r,..supply would take effect and the need for adjustment and restructuring re-emerge.

The point of that digression was to show how long ·ter:~ considerations can be constrained by how the temporary short term outlook is interpreted. With that out of the way, the deferred discussion of the two factors - declining output from natural forests and increasing demand for forest products - can be resumed, but with that point always in mind.

The decline in output from natural forests A decline in the production of industrial wood from natural forests is allowed for in the supply outlooks outlined above, especially in the GFSM. If the actual rate of decline in production from natural forests turns out to be greater than that allowed for in the supply outlooks, the total industrial wood supply potential would be correspondingly less and the chances of oversupply correspondingly reduced. The converse would hold if the rate of decline turned out to be less.

, A greater rate of decline seems more likely than a lesser. The pressure for the transfer of natural forests into fully or highly protected reserves is not likely to decrease. Silvicultural measures aimed at increasing timber productivity to counter-act the reduction in operable resources will become increasingly difficult to apply under strict definitions of S.F.M. In developing countries especially, conversion of forests to other forms of land use must continue unless economic and social development greatly reduce the social demand for agricultural expansion.

To some degree such trends are already allowed for in the various outlooks of wood supply. But they could accelerate and if they do, the vital question is "by how much?"

Withdrawals from timber production for environmental, watershed or heritage protection tend to occur sporadically and in biggish lumps.

The reported reduction of timber production in mountain region forests of China in response to the heavy flooding earlier in 1998 year is typical. Similar large "lump sum" withdrawals can be expected although neither when, where or extent can be predicted. Perhaps of equal cumulative importance, is the

------------------------------------------------------------------------------------------Forest Regeneration and Plantation Development -MFMA Phase Il Page 16

r I l

r !

r l

[ l

r l r [

! ~ . \.

'-'I

- --~-~' ---.:....---.~--~.-~.------~ '. __ L--':'_ ._- _~~_~~-----=-~ -_____ . _______ _

continuing withdrawal of small strips and patches as protecting margins and corridors are extended into and within blocks of natural forest designated for multiple use management.

The major cause of loss of forest area in tropical countries - conversion to agriculture - amounting to around 11 x 106 ha/a is already allO''Yed for in the future supply estimates. The problem is how much non-deforestation lQ~s of timber production forest to allow for.

In the GFSM the "area under protection" is reported as having increased by 140% between 1900 to 1990. Most of the increase has taken place over the last 20 to 30 years with the reservations increasing from around 50 x 106 ha in 1970 to just on 120 x 106 ha in 1990. Extrapolation at the annual rate of increase of around 5% p.a. which this represents would virtually eliminate natural forest as a source of industrial woo'dby the year 2050. This seems unlikely to happen but some continuation of the trend to further withdrawal is certain. How much has been allowed for in the GFSM is unclear as the draft report is incomplete. However, to meet the semi-official IUeN target of 10% of the world's forest eco-systems in totally protected areas would involve the transfer of roughly

- another 250 x 106 ha. That could be taken, perhaps, as the minimum of the nondeforestation loss ofthe timber production natural forest resource.

If that were to materialise over the next 30 years then, combined with the continuing encroachment of small scale protection patches into' timber management areas, an average annual reduction of around 10 million ha up to the year 2030 would have to be allowed for. In effect, the sustainable supply would be reduced by around 25 x 106 m3/a. That could, however, set the upper end of the reduction. Protection of reserved areas, even in developed countries, is not always 100% effective and is notoriously ineffective in some developing countries. Hence, allowing for such leakages, for variations in the scale and timing of the reservations target and for the overall lumpiness of the reservation process, could lower the rate of decline in the supply of industrial roundwood from natural forest as a result of non-deforestation losses, at least in the earlier years.

It might, therefore, be more realistic to express that rate of decline as a range of say 15 to 20 x 106 m3 annually on average instead of the 25 x 106 m3'estimated above.

4 THE OUTLOOK FOR FOREST PRODUCTS DEMAND

The informational basis for forecasting the future of the markets for forest products is even weaker on the demand side than it is for supply. For a start the basic data that are available are for consumption which, at best, is only an approximation to demand, being a resultant of demand inter-acting with supply forces. Then in very few countries do their statistics from which the consumption figures are derived, allow for movements into and out of stocks. That is, the consumption data are a step further from demand in approximation. And this is further aggravated by the estimation of production in many countries rather than its actual measurement.

Forest Regeneration and Plantation Development -MFMA Phase II Page 17

.-.-~-- --- :_------------'-

Then the data, naturally, refer only to the past. Unlike the future supply of wood, which, to a marked degree is limited ,by what has happened in the past, there is much less necessary dependence of future demand on past demand. There is some continuity from the past to the future but no necessary governing or limiting of the future by the past. Nevertheless with the only data available being unavoidably those from the past, most forecasts of future wood demand are direct or indirect extrapolations of or from past trends in consumptipn. Simple, direct projection of consumption ("demand" so called) from trends detected in data from the past have given way to indirect but more sophisticated econometric derivations of consumption from extrapolations of trends detected or assumed of the factors on which consumption is believed to depend.

For many years the lead in this field for the forestry and forest products sector has come from FAO, starting with its series or regional outlook studies i~, the early 1950's. After a lapse in the 1970's and the 1980's this type of activity has now been revived and some comprehensive outlook studies are now coming out. A provisional global outlook published by FAO in 1997 and a regional outlook for Asia-Pacific' which has just been cleared for publication are the latest and most relevant.

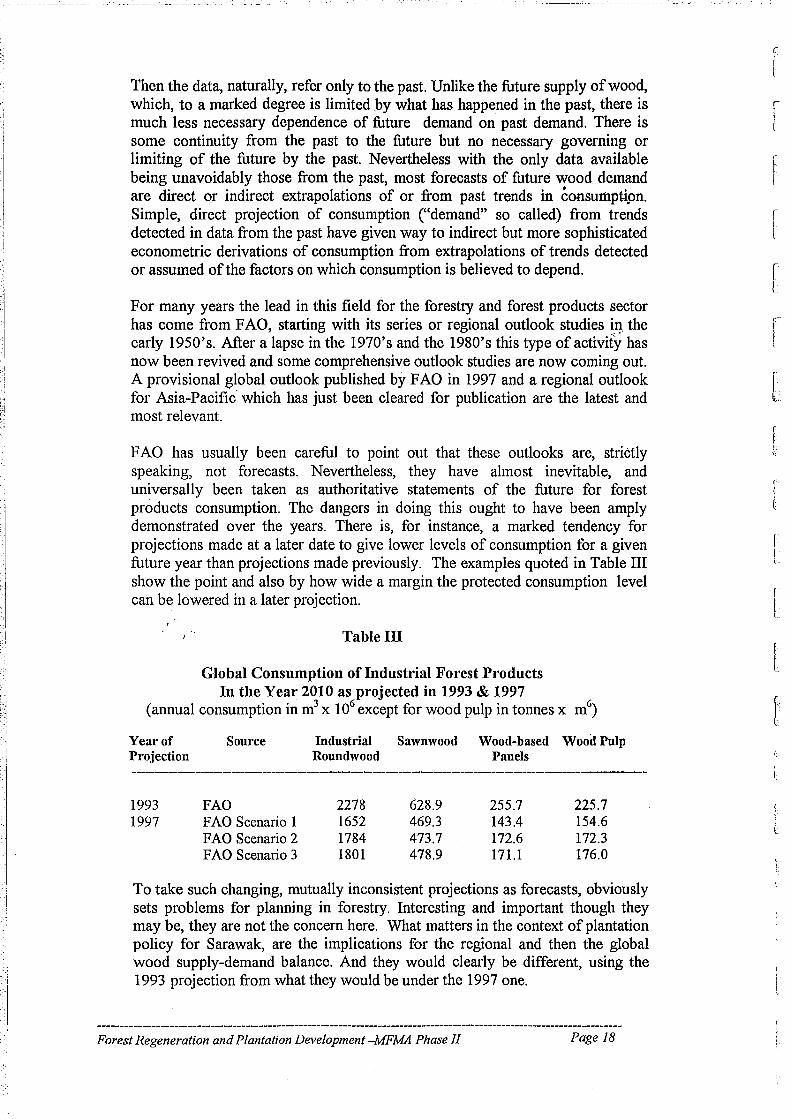

FAO has usually been careful to point out that these outlooks are, strictly speaking, not forecasts. Nevertheless, they have almost inevitable, and universally been taken as authoritative statements of the future for forest products consumption. The dangers in doing this ought to have been amply demonstrated over the years. There is, for instance, a marked tendency for projections made at a later date to give lower levels of consumption for a given future year than projections made previously. The examples quoted in Table III show the point and also by how wide a margin the protected consumption level can be lowered in a later projection.

, .

Table III

Global Consumption of Industrial Forest Products In the Year 2010 as projected in 1993 & 1997

(annual consumption in m3 x 106 except for wood pulp in tonnes x m6)

Year of Projection

Source Industrial Sawnwood Wood-based Wood Pulp Roundwood Panels

--------------------------------------------------------------------------------_._-_.

1993 1997

FAO FAO Scenario 1 FAO Scenario 2 FAO Scenario 3

2278 1652 1784 1801

628,9 469.3 473.7 478,9

255.7 143.4 172.6 17l.1

225.7 154,6 172.3 176.0

To take such changing, mutually inconsistent projections as forecasts, obviously sets problems for planning in forestry, Interesting and important though they may be, they are not the concern here. What matters in the context of plantation policy for Sarawak, are the implications for the regional and then the global wood supply-demand balance. And they would clearly be different, using the 1993 proj ection from what they would be under the 1997 one.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 18

;-

I

r t

r t

r I

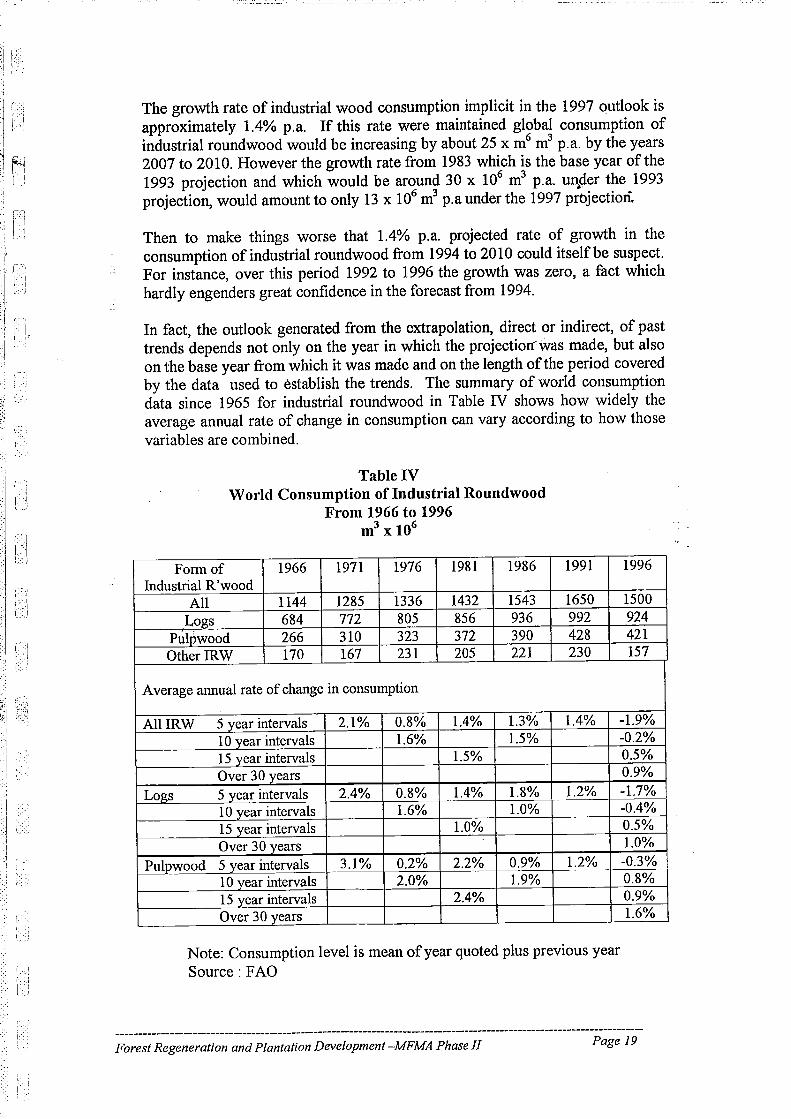

The growth rate of industrial wood consumption implicit in the 1997 outlook is approximately 1.4% p.a. If this rate were maintained global consumption of industrial roundwood would be increasing by about 25 x m6 m3 p.a. by the years 2007 to 2010. However the growth rate from 1983 which is the base year of the 1993 projection and which would be around 30 x 106 m3 p.a. un.der the 1993 projection, would amount to only l3 x 106 m3 p.a under the 1997 projection.

Then to make things worse that 1.4% p.a. projected rate of growth in the consumption of industrial roundwood from 1994 to 2010 could itself be suspect. For instance, over this period 1992 to 1996 the growth was zero, a fact which hardly engenders great confidence in the forecast from 1994.

In fact, the outlook generated from the extrapolation, direct or indirect, of past trends depends not only on the year in which the projection<was made, but also on the base year from which it was made and on the length of the period covered by the data used to establish the trends. The summary of world consumption data since 1965 for industrial roundwood in Table IV shows how widely the average annual rate of change in consumption can vary according to how those variables are combined.

Table IV World Consumption of Industrial Roundwood

From 1966 to 1996 m3 x 106

Fonn of 1966 1971 1976 1981 1986 Industrial R'wood

All 1144 1285 1336 1432 1543 Logs 684 772 805 856 936

Pulpwood 266 310 323 372 390 OtherIRW 170 167 231 205 221

Average annual rate of change in consumption

All IRW 5 year intervals 2.1% 0.8% 1.4% 1.3% 10 year intervals 1.6% 1.5% 15 year intervals 1.5% Over 30 years

Logs 5 year intervals 2.4% 0.8% 1.4% 1.8% 10 year intervals 1.6% 1.0% 15 year intervals 1.0% Over 30 years

Pulpwood 5 year intervals 3.1% 0.2% 2.2% 0.9% 10 year intervals 2.0% 1.9% 15 year intervals 2.4% Over 30 years

1991

1650 992 428 230

1.4%

1.2%

1.2%

Note: Consumption level is mean of year quoted plus previous year Source: FAO

1996

1500 924 421 157

-1.9% -0.2% 0.5% 0.9% -1.7% -0.4% 0.5% 1.0% -0.3% 0.8% 0.9% 1.6%

Forest Regeneration and Plantation Development -MFMA Phase II Page 19

i I

Several features of importance in the use or misuse of forecasts/projections are apparent from the figures in Table IV. Amongst them are:-

(1) A steady and fairly well sustained rise in the consumption of industrial roundwood in total and in its main components since 1965 .. This is

• probably why the users of forecasts, consciously or not, envisage the demand for industrial forest products continuing to rise well· into the future.

(2) A reversal of that upward trend over the last five years for which data are available. This does not appear to have changed the "bullish" view of the future, which suggests that the users of forecasts, if they have noticed this global fall, are treating it as a temporary deviation rather than as the start of a new trend. And that could well be right. The downturn coincides with the dismantling of the U.S.S.R. and the near collapse of its forest products sector in the subsequent economic turmoil. The halving that resulted in the Russian output represents a reduction of about 10% in the global level, which is enough to bring about the reversal indicated over 1992-1996.

(3) A noticeably but not consistently faster rate of growth in the consumption of pulpwood than of logs. This reflects the well documented tendencies for wood-based panels to displace sawnwood in its traditional markets, for reconstituted panel boards to displace plywood as well as sawnwood and the almost unbroken continuing rise in the use of paper. It may therefore suggest, although not strongly, that future markets for the pulpwood based products are more assured than those products depending on log quality raw material.

(4) Average annual rates of growth in the consumption of all or any form of industrial roundwood vary greatly over time but in no consistent, discernible pattern. Clearly they are neither definitive nor reliable

,predictors of the future development of demand. Hence the use of past . consumption data in forecasting future demand needs to be accompanied

by considerable qualification and scepticism.

In the light of all this, it would be difficult and, indeed, precarious, to pick out anyone rate which past consumption data show is the most likely predictor of the future. It would be much less hazardous to express the measured rates of changes in consumption in terms of a range rather than as anyone selected rate.

Growth in the consumption of industrial roundwood since 1965 could thus be condensed to within the following:-

Range of growth rate for all industrial roundwood Range of growth rate for logs Range of growth rate for pulpwood

0.5 to 2.1% p.a. 0.5 to 2.4% p.a. 0.8 to 3.1% p.a.

In the FAO 1997 projection the implicit rates of growth in the consumption of industrial roundwood up to 2010 are shown as to 0.88% under Scenario 1, l.12% p.a. under Scenario 2 and l.64% p.a. under Scenario 3. These rates fall neatly within the range of rates experienced over the last 30 years. But that is no reason for adopting anyone of them as the appropriate rate for forecasting future

Forest Regeneration and Plantation Development -MFMA Phase II Page 20

f I

r I

[

r

f

t

r-I \1

demand. Nor, however, does it provide any reason for not adopting anyone of them. But, in view of what has just been said about the hazards of selecting just one rate, it is probably better to stay with a range.

The trouble still is how to pick the range. On what can, with some exaggeration, be called "the evidence" the range seems likely to run from sOlllething above zero at the minimum to a maximum rate not greater than 2.0% p.a. • -.:

Selecting a range of positive rates as covering the possibilities has some dangers. It ignores the negative growth rates recorded during the last 5 years, treating them, in effect, as temporary interruptions to the more or less steady upward trend. If they actually represent early signals of a permanent reversal or change, then projections at any positive rate will greatly over-state future demand. But the case for that is, at thee )1loment, less persuasive than that for their being of a temporary nature.

4.1 The resultant wood supply-demand balance _ , The argument in "For Whom The Bell Tolls' led to the conclusion that global

over-supply of industrial roundwood from early in the next century was almost inevitable. Some implications for Sarawak forest policy in general were drawn from the increasingly, intensified competition that would bring in export ,markets, especially.

The more detailed information available for this review suggests that:-(a) The wood supply potential of the plantation resource may not be as great as

suspected in the note, especially in the earlier years; (b) The demand for industrial forest products will continue to grow at a positive

rate and (c) The supply, potential and actual, from natural forests could decline more

sh~rply than was (implicitly) allowed for in the note. - J

Intuitively, it might be expected that this different configuration of the supply and the demand forces would make quite a difference to the expectation of an over-supply of general purpose/community grade industrial roundwood. But that cannot, however, be taken for granted. The forces tend to pull or push in different directions and act at different times. Hence the effect of the global wood supply-demand balance will have to be calculated from quantified estimates of the magnitude of the supply and demand forces, in combinations built up from the range of values as derived or discussed above.

One important determinant does, however, warrant more consideration first. This is the wood supply potential from natural forests. At present, natural forests are the dominant source of industrial wood, providing around 90% of the world's production. That their supply potential will continue to decline is inevitable and an allowance for that has been assessed earlier. But in examining the possibility of over-supply resulting from the plantation impact, the initial size of the supply potential of the natural resource has to be the starting point.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 21

". ---~----'.------'

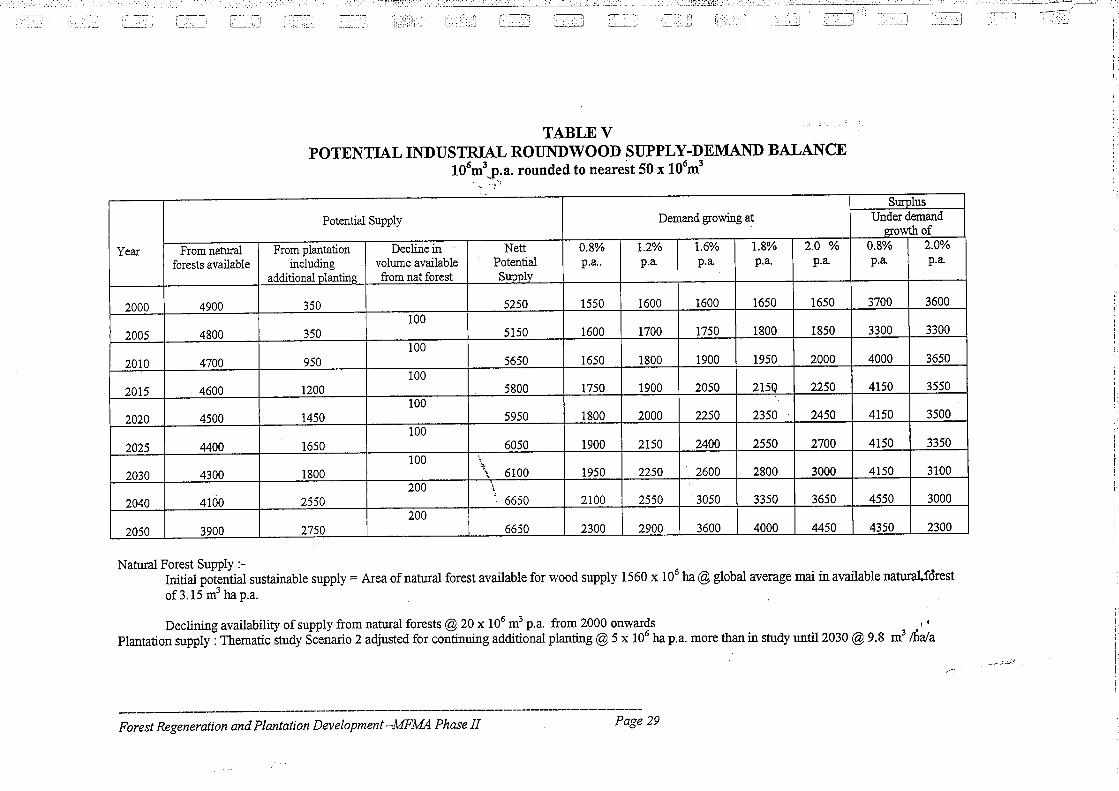

The GFSM shows the area of the world's forest resource as 3.22 x 109 ha, rather less than the 3.45 x 109 ha. given in the FAO "State of the World's Forests, 1997". Of this only 1.56 x 109 ha is considered in the GFSM as "available for supply". The remainder being excluded on the grounds of reservation for totally protected services, or economic inaccessibility or workability or the conversion to other land uses. On the basis of the increment estimates in the GfSM, the sustainable potential supply would amount to approximately 4900~~ 106 ~.p.a. The global increment of commercial species i.e. the available roundwood is given, however, at 2700 106 m3 p.a.

The two levels can, for present purposes, be taken as setting the range of values for the initial potential of the natural forest resource.

Th~~ the limits for each of the determinants of the future wood supply-demand bal~mce adopted for the assessment are as follows:-

Ci) Natural Forest Supply Initial 2700 to 4900 x 106 m3 p.a. Declining by 15 to 20 x 106 m3 p.a. over and above reductions in availability already built into the estimates

Cii) Plantation Supply Area established 1997 113 x 106 to 131 X 106 ha with M.A.I. 9.8 to13.0m3 hala Additional planting from 1997 onwards over and above that in the FAO Thematic Study, Scenario 2 of 5 x 106 hala

Ciii) Demand Growing at 0.8% p.a. to 2.0% p.a.

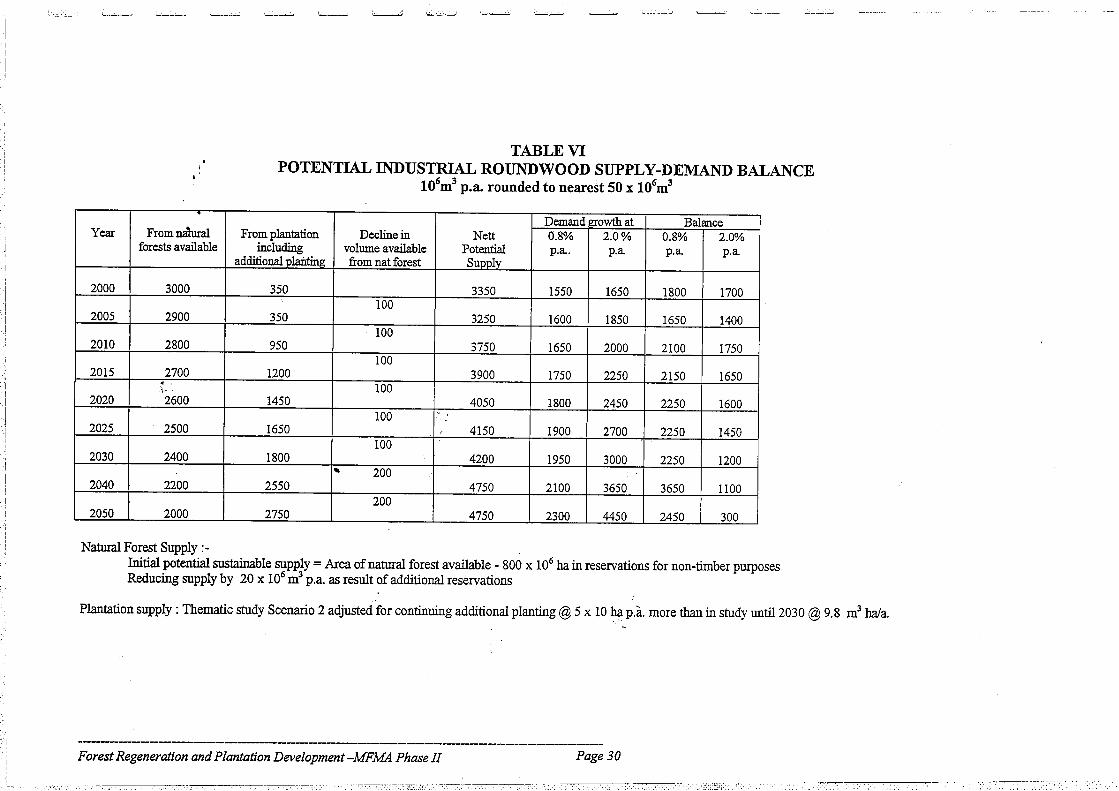

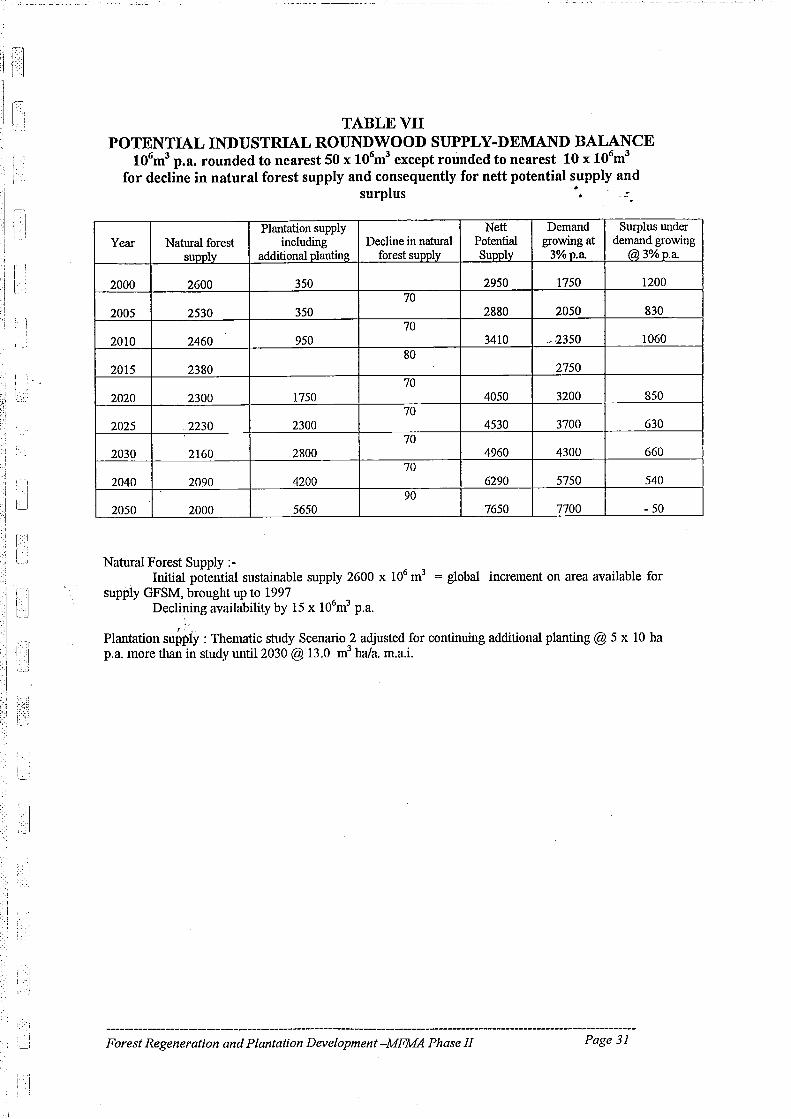

Thes~obviously do not cover the full range of possible levels for all or anyone of the' determinants. The ranges listed are, at best, only those for which the evidence seems to be the least tenuous. But, even within this selection out of the possible ranges, many combinations are feasible. The three combinations whose results are summarised in Tables V, VI and VII are presented, therefore, partly for illustrative purposes. They can, however, be taken as indicative in terms of some of the implications for plantation policy. The outlook summarised in Table V thus represents a future in which a wood supply surplus develops towards the maximum. That in Table VI represents a wood supply surplus more towards the middle of the possibles. On the other hand the future presented in Table VII is of an eventual development of a wood supply deficit under an exceptionally high rate of growth in demand.

From that sampling over the range of possibilities the conclusion is inevitable -a wood supply surplus dominating the industrial roundwood market over most of the first half of the 21st Century. Actually a wood supply surplus already exists. The sustainable capacity of the natural forest resource is rather more than twice the present demand and even at a low base level it remains above demand until after 2020. But that surplus is one of potential only. The sustainable capacity of the world's natural forest resource is under-utilized because there is neither the need nor the pressure, on a global scale, to force

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 22

[ [

[ I \

[ t

r l

r

L

I L

[

,

" . , ~_i.

timber harvesting into the large and largely unused forests of the Congo Basin, the Amazon or Siberia.

With the plantation resource, however, it is altogether different. For the most part the plantations have been and are being established, located and managed with a market, sometimes a specific market, in mind. Hence as t}1ey approach maturity, the pressure from the initial and accumulated investment will force the potential to be realised. Potential supply will become actual supply, but it will not dominate the wood supply balance much before 2015. From around 2010 the plantation supply into world markets will have begun to flow, sharply at first, then steadily until there is another sharp rise about 30 years later. By 2020 the actual supply from plantation sources could be meeting at least 70% of the demand and even, at its highest almost all of the demand.

Thus the plantation resource does much more than just add to the potential global supply of industrial roundwood. It creates, almost on its own, an eventual over-supply.

One of the main purposes behind the above analysis was to test the possibility of a potential global over supply of commodity types and grades of industrial roundwood development as the global plantation resource moves into maturity. That it is a distinct possibility is amply confirmed. Nevertheless the analysis is still incomplete. Three things at least, are missing. The first is the· question which triggered the analysis. That is, whether the wood supply-demand balance in Pacific Rim markets is going to tilt towards over supply now that the surge in supply from the south Pacific plantations will be smaller and possibly start a little later. The second concerns the distribution of the demand for industrial roundwood between the two main components, namely logs and pulpwood. And the third is the likelihood or probability of the outlook inferred from the analysis being~. credible guide to the future for the sector in Sarawak.

, J .'

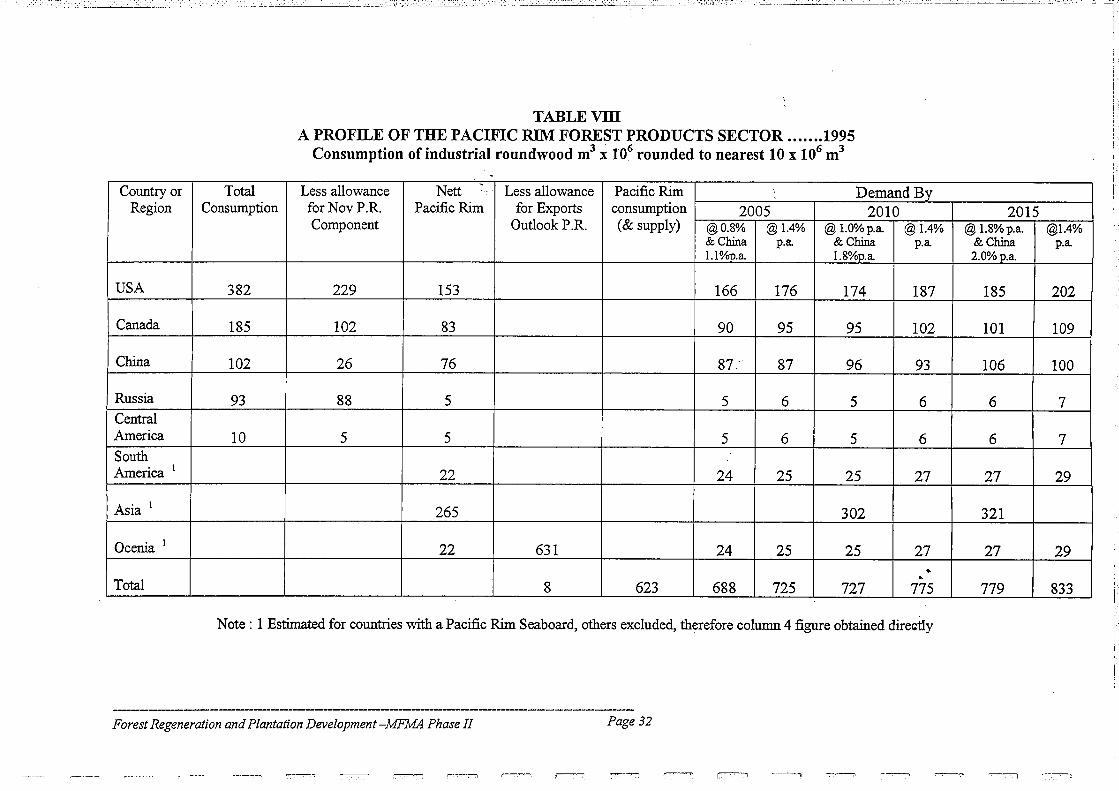

4.2 The South Pacific Plantation Resource The Pacific Rim Economies, especially those of East Asia, have been the driving force for the Sarawak forestry sector for almost three decades. They seem likely to continue to play that role well into the future, although other markets are becoming increasing significant. Hence what the South Pacific plantation resource could do to the wood supply-demand balance in the region is of vital concern to Sarawak. The sudden addition of30 to 40 x 106 m3 within the next few years must be expected to have some impact. What sort and how big depends, to a considerable extent, on the size of the industrial roundwood market now and how it is evolving. Neither, however, are easy to estimate, let alone ascertain, mainly because the Pacific Rim does not figure as a geographical or economic unit in the statistical collections generally available. Those collections are built up country by country but four of the biggest participants in the forest products sector of the Pacific Rim have economies which stretch well beyond the Pacific Rim. Some gigantic approximations are involved in trying to separate the Pacific Rim content out of the national data.

Forest Regeneration and Plantation Development -MFMA Phase 11 Page 23

I I

Nevertheless, an attempt must be made in order to gauge, even in the broadest terms, the South Pacific plantation effect. Table VIII presents the basic and results of such an attempt

From those estimates the increase in the demand for industrial wood in the Pacific Rim would rise, depending on the rate of growth in demand, as follows:-

•

Between 1995-2005 At a low rate 65 At a high rate 102

2005-2010 39 50

2010-2015 52 52

Too much should not, of course, be made of these very bold and rough approximations. Nevertheless they do give some indications which could be useful and valid enough for present purposes. One is that an incre~~e in the demand for industrial roundwood of65 x 106 m3 to100 x 106 m3 per year before 2005 could put pressure on supply if plantations were the only source of additional supply. Very little additional supply can come from the existing resource much before 2005. However natural forests within or adjoining the region have more than enough spare capacity to cope with any such increase in demand. However, from around 2005 the sudden and sharp rise in the availability of plantation wood changes the outlook markedly.

Over supply in the region is nowhere near as likely as it would have been had the surge in supply been the 60 x 106 m3 foreseen in the "For Whom .... " note. The respite, however, is rather fragile. It would not take much of a decline in the assumed rate of growth of demand and/or much of the increase in the magnitude, of the surge in plantation supply to tilt the balance towards oversupply. Even if neither of these possibilities does eventuate, the respite is short lived anyhow. By 2015 the global plantation resource is starting to come on strearpand in a big way. Over-supply is then a virtual certainty.

Thus the answer to the question that triggered this analysis in the light of the more detailed information now available is a little less alarming. The changes of over-supply following the almost certain surge in supply from the South Pacific plantation, while still there, seem low enough for the sector in Sarawak to continue on its present course. But cautiously; over supply is a near certainty once the global plantation resource starts to hit the world supply-demand balance by around 2015.

4.3 The log-pulpwood distribution of demand One very important aspect of plantation policy is the outlook for the two main categories of industrial roundwood i.e.logs and pulpwood. The importance lies in their asymmetry. Logs, if the circumstances call for it, can be used as pulpwood but the reverse, largely by definition, does not apply. Pulpwood, in general, is roundwood which does not come up to log specifications.

The extent to which the pulpwood/log mix in the demand for industrial roundwood is changing can be gauged from the following ratios calculated from the data summarised in Table IV.

Forest Regeneration and Plantation Development -MFMA Phase If Page 24

v [

r I

I I (

r I

r c"

i : I

I ·1

fl 1. 1

•• 1

","\

Ratio of pulpwood to logs in 1965 0.39 1975 0.40 1980 0.42 1995 0.43

However the 1997 FAO projections are in marked contrast to this historical •

trend. The Scenario 2 projection has the proportion of the pulpwood complment implicitly staying constant from 1994 to 2010 while the other two scenanos have the implied proportion declining.

It is a bit hard to see such a cessation, let alone reversal of the trend occurring so relatively quickly. After all the main driving force behind the trend seems to be associated with the steady and almost unbroken rise in the rate at which the consumption of paper is increasing averaging around 2% p.a. Combined with a relatively low rate of growth in sawn timber consumption of around 0.5% globally, the proportion of pulpwood must continue to rise for as long as such relativities hold. The trend may, however, be slackening as the proportion has increased only slightly over the last 5 years (1991 to 1996).

Nevertheless, if even this recent slower rate of increase in the proportion of the pulpwood component were to continue then by 2010 close to 35% of the demand for industrial roudwood would be as pulpwood from 37% by 2020. As mentioned on p.20 plantations established and managed for pulpwood would "." seem to have a more secure basis than those established primarily for logs.

One other aspect of the distribution is worth mention. While logs for sawmilling may not be as good a proposition as pulpwood in plantation policy in general,

c.. the GFS study indicates that a shortage of hardwood (non-coniferous) logs, .... could develop "within the very near future". This is likely if present logging

practtqes continue more or less unchanged. It is rather less likely if reduced impact logging and other S.F.M. measures are introduced. To some extent, S.F.M. in natural forests becomes an alternative to plantations.