Forest Lake Area Schools Truth in Taxation Hearing for Taxes Payable in 2010 December 3, 2009 Presented by: Larry Martini Director of Business Services

Forest Lake Area Schools Truth in Taxation Hearing for Taxes Payable in 2010

Dec 30, 2015

Forest Lake Area Schools Truth in Taxation Hearing for Taxes Payable in 2010. December 3, 2009 Presented by: Larry Martini Director of Business Services. Truth in Taxation Law. State law initially approved in 1988 and modified for 2009 Two major requirements - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Forest Lake Area SchoolsTruth in Taxation Hearing forTaxes Payable in 2010

December 3, 2009Presented by:Larry Martini

Director of Business Services

Truth in Taxation Law State law initially approved in 1988

and modified for 2009 Two major requirements

Counties must send out “proposed property tax statements” in November, based on preliminary tax levies set by all taxing jurisdictions

Taxing jurisdictions must hold a hearing

You are here for the school district’s annual required hearing

Truth in Taxation Hearings School district is required by law to

present information on: The budget for the current school year,

including sources of revenue and expenditures by program area

The proposed property tax levy, including:

The percentage increase over the prior year Specific purposes and reasons for which taxes

are being increased District must allow for public

comments

Agenda for Hearing A. Information on District Budget B. General Background Information on School District Property Taxes C. Information on the District’s Levy for 2010 Property Taxes D. Public Comments

A. 2009-10 Budget All school districts’ budgets are

divided into separate funds, as required by law

For our district, 5 funds: General Fund Food Service Fund Community Education Fund Debt Service Fund Trust Fund

A. Overview of Funds General Fund

Accounts for most daily operating expenses of district - everything not included in other funds; 84% of revenues for 2009-10

Salaries, benefits, supplies, other costs for instruction, administration, transportation, custodial services, etc.

Insurance, utilities, other purchased services

Also includes annual capital expenditures

A. Overview of Funds Food Service Fund

Accounts for all expenses of the National School Lunch and Breakfast Programs

Community Education Fund Accounts for expenses of educational and

recreational programs that are not part of the “regular” K-12 and special education programs

Early childhood family education Programs for adults Classes & Recreational programs

A. Overview of Funds Debt Service Fund

Accounts for principal and interest payments on the district’s voter-approved building bonds as well as the district’s OPEB bonds

Trust Fund Accounts for revenues and expenses of our

Employee Cafeteria Plan and vending machine program

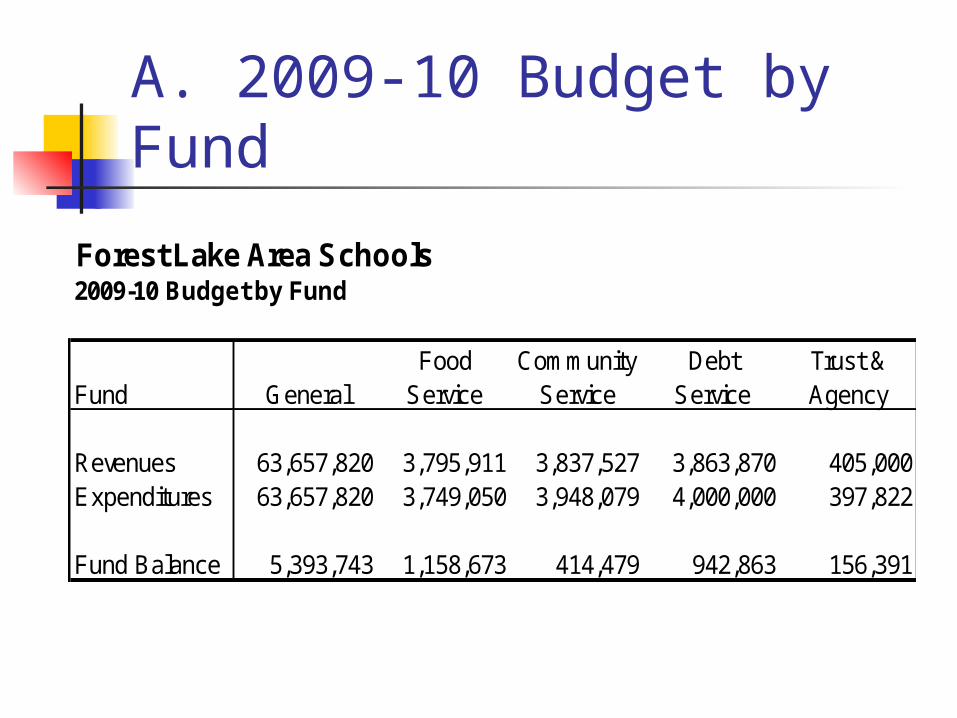

A. 2009-10 Budget by Fund

Forest Lake Area Schools2009-10 Budget by Fund

Food Community Debt Trust &Fund General Service Service Service Agency

Revenues 63,657,820 3,795,911 3,837,527 3,863,870 405,000Expenditures 63,657,820 3,749,050 3,948,079 4,000,000 397,822

Fund Balance 5,393,743 1,158,673 414,479 942,863 156,391

A. 2009-10 Revenues by Fund

2009-10 Revenue Budget by Fund

0.6%

5.0%

5.3%

5.2%

83.9%

General

Food Svc.

Comm. Svc.

Debt Svc.

Trust

A. General Fund Budget Highlights

2009-10 General Fund BudgetRevenues by Major Source

Property Taxes 10,426,700State Aid 49,139,314Federal Aid 2,604,406Other Local Revenue 1,487,400Total 63,657,820

4.1%

77.2%

16.4%

2.3%

PropertyTaxes

State Aid

Federal Aid

Other LocalRevenue

A. General Fund Budget Highlights

2009-10 General Fund BudgetExpenditures by Major Program Area

Administration 3,120,968District Support Svcs. 2,657,648Regular Instruction 28,526,505Vocational Instruction 935,884Exceptional Instruction 9,405,510Instr./Pupil Support Svcs. 10,613,992Sites & Buildings 7,356,373Other Operating Programs 1,040,940Total 63,657,820

4.2%

44.8%

1.5%14.8%

16.7%

11.6%1.6%4.9%

Administration

District Support Svcs.

Regular Instruction

Vocational Instruction

Exceptional Instruction

Instr./Pupil SupportSvcs.Sites & Buildings

Other OperatingPrograms

78 % of our funds are spend on direct services to students

A. General Fund Budget Highlights

2009-10 General Fund BudgetExpenditures by Object Category

Salaries and Wages 39,924,045Employee Benefits 12,448,317Purchased Services 6,756,030Supplies & Materials 3,083,852Capital Expenditures 1,281,261Other 164,315Total 63,657,820

19.6%

10.6%

4.8%2.0%

0.3%

62.7%

Salaries and Wages

Employee Benefits

Purchased Services

Supplies & Materials

Capital Expenditures

Other

B. Property Tax Background Every owner of taxable property pays

property taxes for the various “taxing jurisdictions” (county, city or township, school district, special districts) in which the property is located

Each taxing jurisdiction sets its own tax levy, often based on limits in state law

County sends out bills, collects taxes from property owners, and distributes funds back to other taxing jurisdictions

B. Property Tax Background

School District Property Taxes Each school district may levy taxes in

up to 30 different categories “Levy limits” (maximum levy amounts)

for all categories are set either by: State law, or Voter approval

Minnesota Department of Education (MDE) calculates detailed levy limits for each district

B. Property Tax Background

School District Property Taxes Key steps in the process are

summarized on the next slide Any of these steps may affect the taxes

on a parcel of property, but the district has control over only 1 of the 7 steps

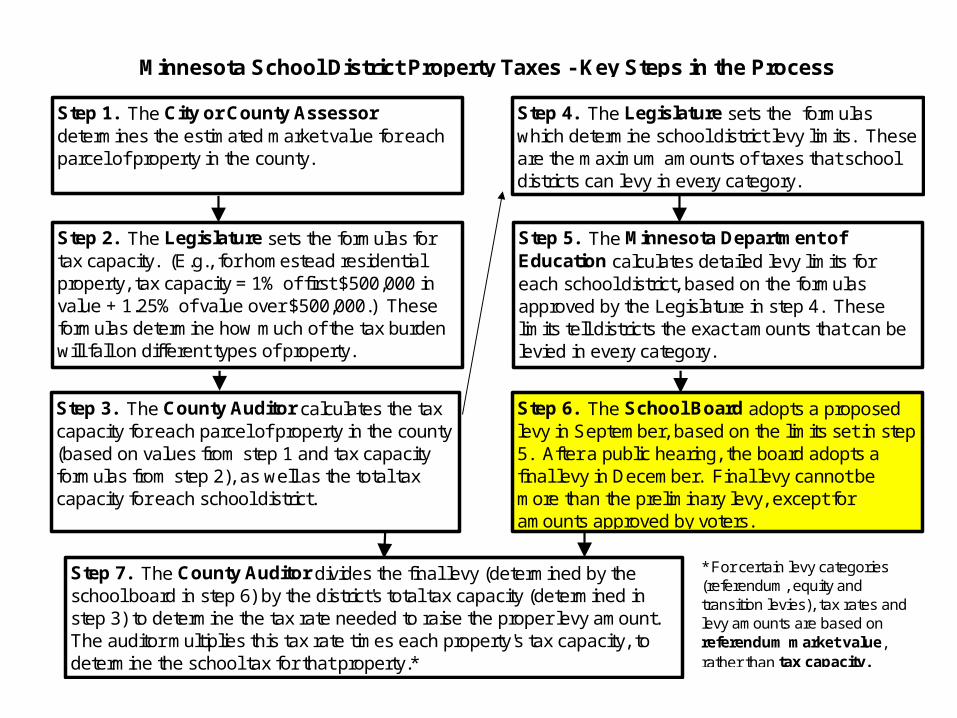

Minnesota School District Property Taxes - Key Steps in the Process

Step 1. The City or County Assessor determines the estimated market value for each parcel of property in the county.

Step 4. The Legislature sets the formulas which determine school district levy limits. These are the maximum amounts of taxes that school districts can levy in every category.

Step 2. The Legislature sets the formulas for tax capacity. (E.g., for homestead residential property, tax capacity = 1% of first $500,000 in value + 1.25% of value over $500,000.) These formulas determine how much of the tax burden will fall on different types of property.

Step 5. The Minnesota Department of Education calculates detailed levy limits for each school district, based on the formulas approved by the Legislature in step 4. These limits tell districts the exact amounts that can be levied in every category.

Step 6. The School Board adopts a proposed levy in September, based on the limits set in step 5. After a public hearing, the board adopts a final levy in December. Final levy cannot be more than the preliminary levy, except for amounts approved by voters.

Step 3. The County Auditor calculates the tax capacity for each parcel of property in the county (based on values from step 1 and tax capacity formulas from step 2), as well as the total tax capacity for each school district.

Step 7. The County Auditor divides the final levy (determined by the school board in step 6) by the district's total tax capacity (determined in step 3) to determine the tax rate needed to raise the proper levy amount. The auditor multiplies this tax rate times each property's tax capacity, to determine the school tax for that property.*

* For certain levy categories (referendum, equity and transition levies), tax rates and levy amounts are based on referendum market value, rather than tax capacity.

QUOTE: Senator Randy Peterson When Senator Peterson was chair of the

Senate’s Education Committee he stated:

“as a practical matter, school districts really don’t have very much authority, any meaningful authority anyway, over their local taxing decisions. With the exception of decisions to build school buildings and the excess-levy referendums…school district taxing decisions are pretty much a matter of state law…”

QUOTE: Dr. Tom Melcher Dr. Melcher is the leader of Program

Finance for the Minnesota Department of Education:

“For most levy categories, if a school district reduces the amount of the levy, there is a proportionate, corresponding reduction in state aid…”

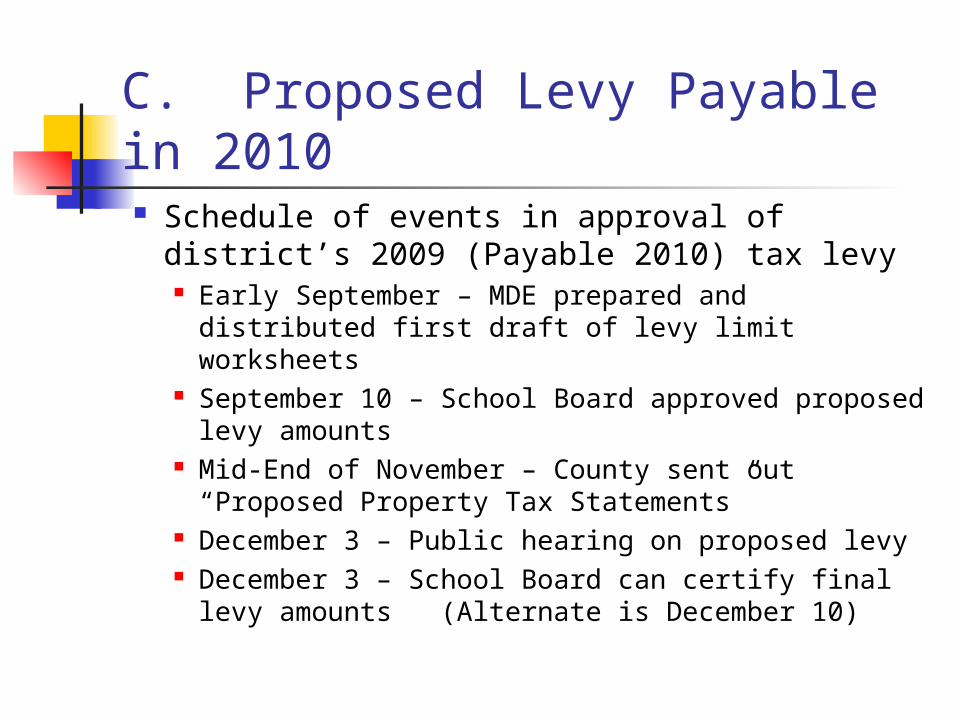

C. Proposed Levy Payable in 2010 Schedule of events in approval of

district’s 2009 (Payable 2010) tax levy Early September – MDE prepared and

distributed first draft of levy limit worksheets September 10 – School Board approved

proposed levy amounts Mid-End of November – County sent out

“Proposed Property Tax Statements” December 3 – Public hearing on proposed

levy December 3 – School Board can certify final

levy amounts (Alternate is December 10)

Forest Lake Area SchoolsComparison of Levy Payable in 2010 to Actual Levy Payable in 2009

X = Has Corresponding State Aid Actual Levy Proposed Levy Percent

Fund Levy Category Payable in 2009 Payable in 2010 Change Change

General Fund X Voter Approved Referendum 6,399,445 6,313,307 -86,138 X Equity 911,677 940,183 28,506 X Transition 158,506 155,529 -2,977 X Alternative Compensation 644,442 0 -644,442 X Operating Capital 1,216,597 1,184,117 -32,480 X Health and Safety 801,941 528,208 -273,733

Crime/Safe Schools 249,092 244,415 -4,677Building Lease 289,850 286,426 -3,424

X Deferred Maintenance 424,026 443,997 19,971Career & Technical 106,874 106,874 0Re-Employment 50,000 80,000 30,000Adjustments for Prior Years -244,222 -636,136 -391,914Total, General Fund 11,008,228 9,646,921 -1,361,307 -12.4%

Community Service Fund X Basic Community Education 348,460 349,288 828 X Early Childhood Family Education 216,357 208,854 -7,503 X School-Age Care 150,000 150,000 0

Home Visiting 5,128 5,160 32Adults with Disabilities 8,500 8,500 0Adjustments for Prior Years 83,342 67,015 -16,327Total, Community Service Fund 811,787 788,817 -22,970 -2.8%

Debt Service Fund X Voter Approved Debt Service 4,194,489 4,304,213 109,724

OPEB based Debt Service 0 535,623 535,623Adjustments for Prior Years 10,691 6,352 -4,339Reduction for Excess Fund Balance -341,302 -295,803 45,499Total, Debt Service Fund 3,863,878 4,550,384 686,506 17.8%

Total Levy, All Funds 15,683,893 14,986,122 -697,771 -4.4%

Business Services / December 3, 2009

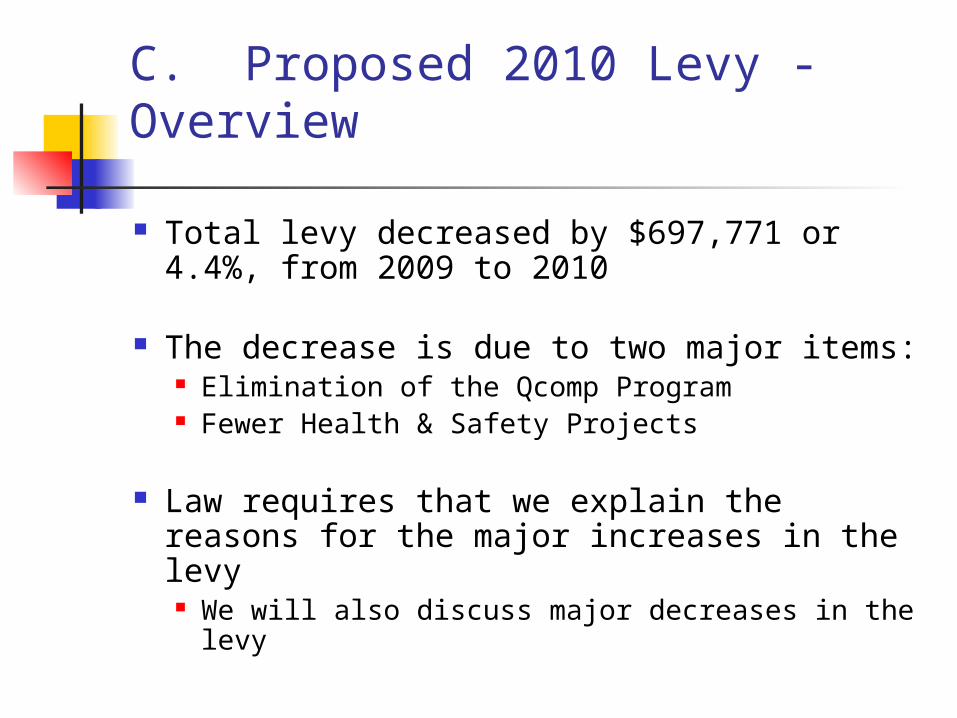

C. Proposed 2010 Levy - Overview

Total levy decreased by $697,771 or 4.4%, from 2009 to 2010

The decrease is due to two major items: Elimination of the Qcomp Program Fewer Health & Safety Projects

Law requires that we explain the reasons for the major increases in the levy We will also discuss major decreases in the

levy

C. Explanation of Levy Changes (Items +or- $75,000)

Category: Voter Approved Referendum

Change: -86,138 Use of funds: general operating

expenses Reason for Decrease:

Decrease in pupils

C. Explanation of Levy Changes

Category: Alternative Compensation

Change: -$644,442 Use of funds: restricted to Qcomp

plan approved by MDE Reason for Decrease:

Teachers voted against Qcomp Program

C. Explanation of Levy Changes

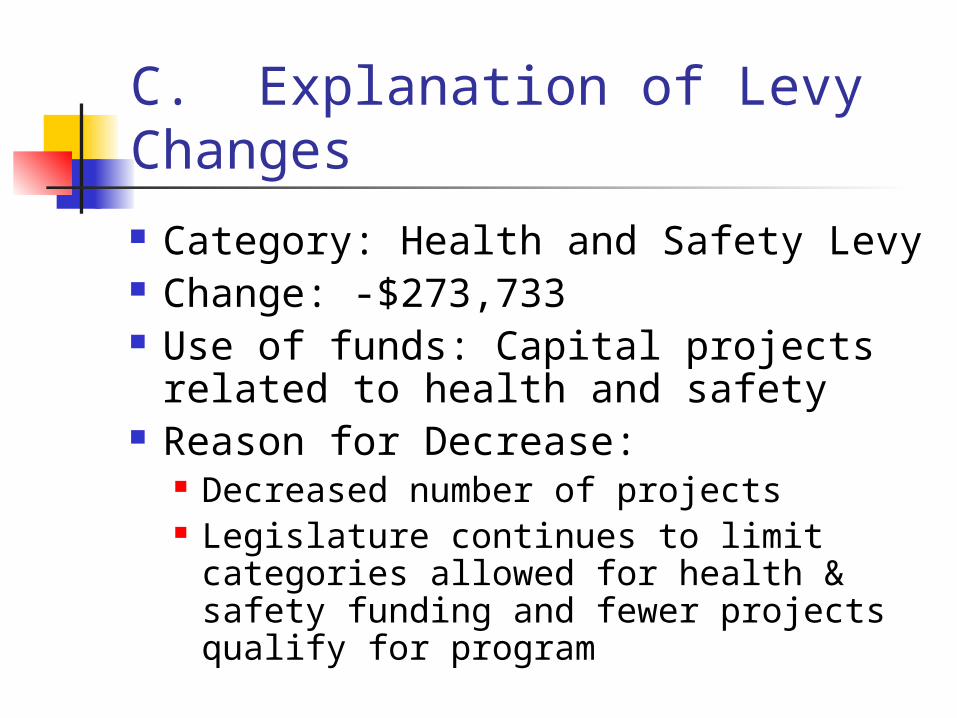

Category: Health and Safety Levy Change: -$273,733 Use of funds: Capital projects

related to health and safety Reason for Decrease:

Decreased number of projects Legislature continues to limit

categories allowed for health & safety funding and fewer projects qualify for program

C. Explanation of Levy Changes

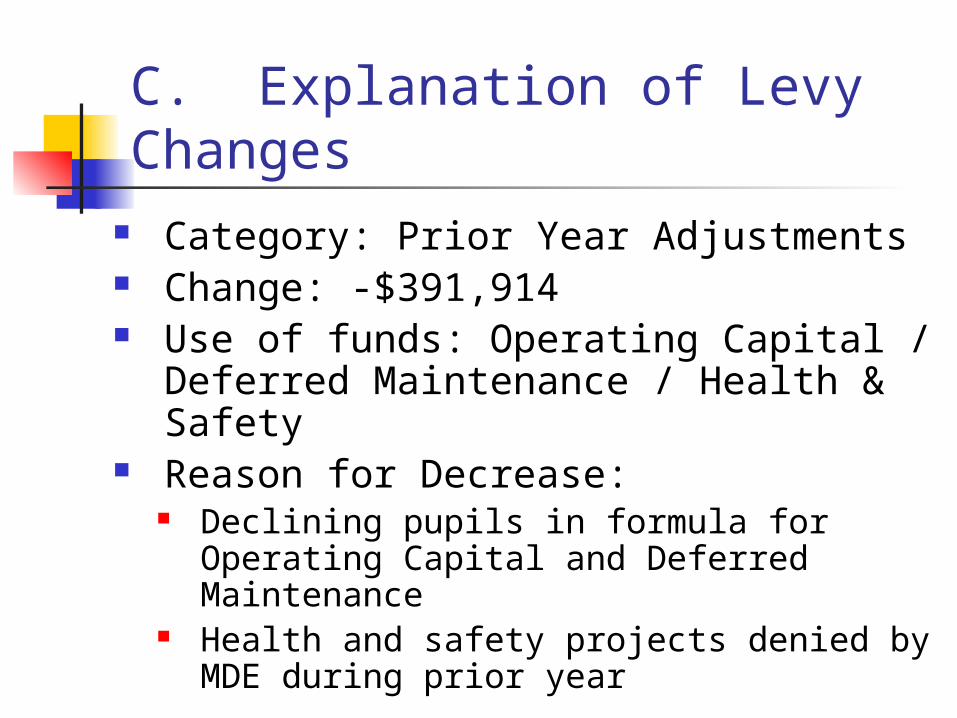

Category: Prior Year Adjustments Change: -$391,914 Use of funds: Operating Capital /

Deferred Maintenance / Health & Safety

Reason for Decrease: Declining pupils in formula for Operating

Capital and Deferred Maintenance Health and safety projects denied by

MDE during prior year

C. Explanation of Levy Changes

Category: Voter Approved Debt Service

Change: +$109,724 Use of funds: Retirement of

Principal and Interest on Bonds Reason for increase:

MDE determines this category by formula ( +2.6% change)

C. Explanation of Levy Changes

Category: OPEB Debt Service Change: +$535,623 Use of funds: Retirement of

Principal and Interest on OPEB Bonds

Reason for increase: New Legislation allowed OPEB bonds

to be issued

C. Property Taxes - Going Down Again

$16,366,468.57

$15,683,893.40

$14,986,122.12

Pay 2008 Pay 2009 Pay 2010

C. State Property Tax Refunds State of Minnesota has two tax refund

programs available for owners of homestead property

Both programs may reduce the net tax burden for local taxpayers, but only if you take time to complete and send in the forms

For help with the forms and instructions: Consult your tax professional, or Visit the Department of Revenue web site at

www.taxes.state.mn.us

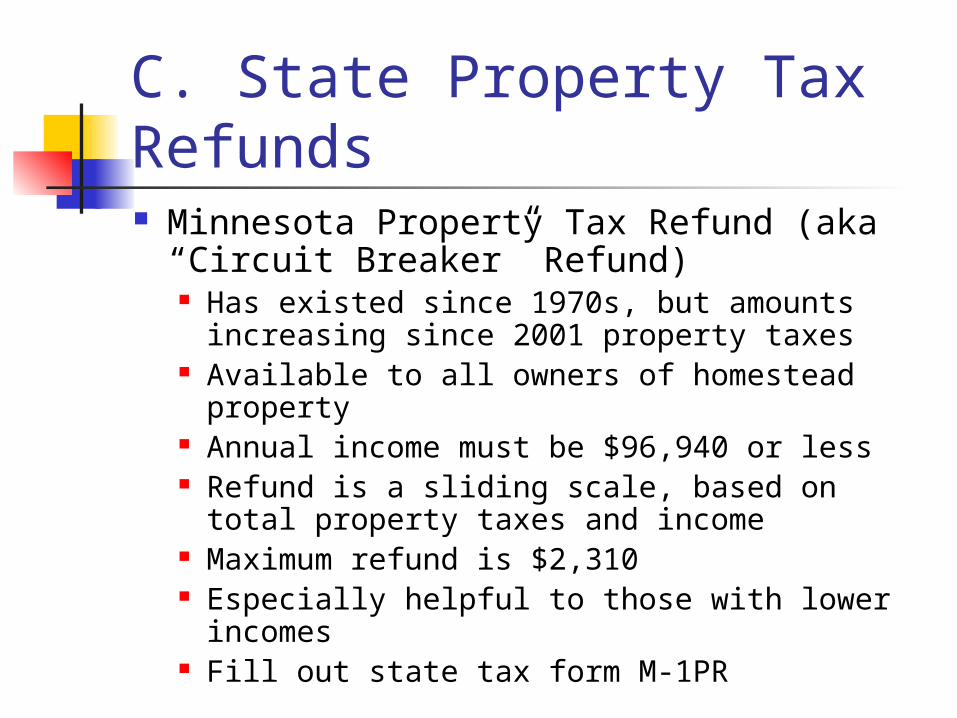

C. State Property Tax Refunds Minnesota Property Tax Refund (aka

“Circuit Breaker” Refund) Has existed since 1970s, but amounts

increasing since 2001 property taxes Available to all owners of homestead

property Annual income must be $96,940 or less Refund is a sliding scale, based on total

property taxes and income Maximum refund is $2,310 Especially helpful to those with lower

incomes Fill out state tax form M-1PR

C. State Property Tax Refunds Targeted Homeowners Property Tax

Refund Available for all homestead properties with

a gross tax increase of at least 12% and $100 over the prior year

Refund is 60% of the amount by which the tax increase exceeds 12%, up to a $1,000 maximum

No income limits Fill out state tax form M-1PR

D. Public Comments

Related Documents