FOREN 14-15 June 2012, Hotel Intercontinental Bucharest, The basic contractual structure of a non recourse project financed for renewable projects using an EPC contract. Robert Ghelasi Director of Energy Department Capital Partners [email protected]

FOREN 14-15 June 2012, Hotel Intercontinental Bucharest, The basic contractual structure of a non recourse project financed for renewable projects using.

Dec 11, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FOREN14-15 June 2012, Hotel Intercontinental Bucharest,

The basic contractual structure of a non recourse project financed for renewable

projects using an EPC contract.

Robert GhelasiDirector of Energy Department

Capital [email protected]

The following diagram illustrates the basic contractual structure of a non recourse

project financed wind farm project using an EPC contract.

Project Company

(SPV)Sponsors

Local Public Authorities

Financial Institutions

EPC

Contractor

O&M

Contractor

Network

Distributor

O&M Contracts Connection Agreement PPA + GCPA

Financing and Security

Agreements

Concession Agreement

Equity Support Agreement

EPC Contract

Power Offtaker

Green Certificates

Offtaker

Sub-contractor

Consultants/Advisers Superficies Agreement

Tripartite Agreements

Partner 1 Partner 2Other equity

investors Technical Advisor

Sponsor decision – wind farms needed to be located on sites that have with adjacent land uses

• Community acceptance and compatibility with adjacent land uses

• strong, steady winds throughout the year, including extreme wind conditions. Romania has one of the Europe’s best wind resources especially along the Black Sea Coast.

• good road access with adequate capacity to serve the wind plant (distance to publicly accessible areas) and spacing between turbines

• Seismic activity, noise constraints, altitude, corrosion, and extreme temperatures

• Environmental impact, including avian, bat and other biological considerations

• proximity to the electricity grid.

Operation services

•Control room operation (24h/7d)

•Remote monitoring

•Call centers

•Metering

•Energy management & automation

Maintenance services

•Field services

•Preventive & corrective maintenance

•Repairs

•Emergency response

•Inspection

•Spare part management

The recourse is limited both in terms of when it can occur and how much the sponsors are forced to

contribute. In practice, true non-recourse financing is rare. In most projects the sponsors are obliged to

contribute additional equity in certain defined situations.

Project financing is a generic term that refers to financing secured only by the assets of the project

itself. Therefore, the revenue generated by the project must be sufficient to support the financing. Project

financing can be “non-recourse” financing or “limited recourse” financing.

A construction contract for a wind farm includes various elements, from manufacture of the blades and towers and assembly of the nacelles and hubs and construction of the balance of the plant comprising civil and electrical works. There are a number of contractual approaches that can be taken to construct a wind farm. An EPC contract is one approach.

Another option is to have three separate contracts:• Wind Turbine Generator (WTC) supply contract;• Balance of Plant (BOP) contract;• Warranty Operating and Maintenance Agreement (WOM).

Balance of Plant (BOP) is the infrastructure of a wind farm project, in other words all elements of the wind farm, excluding the turbines. Includes civil works, SCADA and internal electrical system. It may also include elements of the grid connection.

Interestingly, on large project financed wind farm projects the contractor is increasingly becoming one of the sponsors, ie an equity participant in the project company. Contractors will ordinarily sell down their interest after financial close because, generally speaking, contractors will not wish to tie up their capital in operating projects.

The choice of contracting approach will depend on number of factors including:

• the time available• the lender requirements• the identity of the contractor(s).

The major advantage of the EPC contract over the other possible approaches is that it provides for a single point of responsibility.

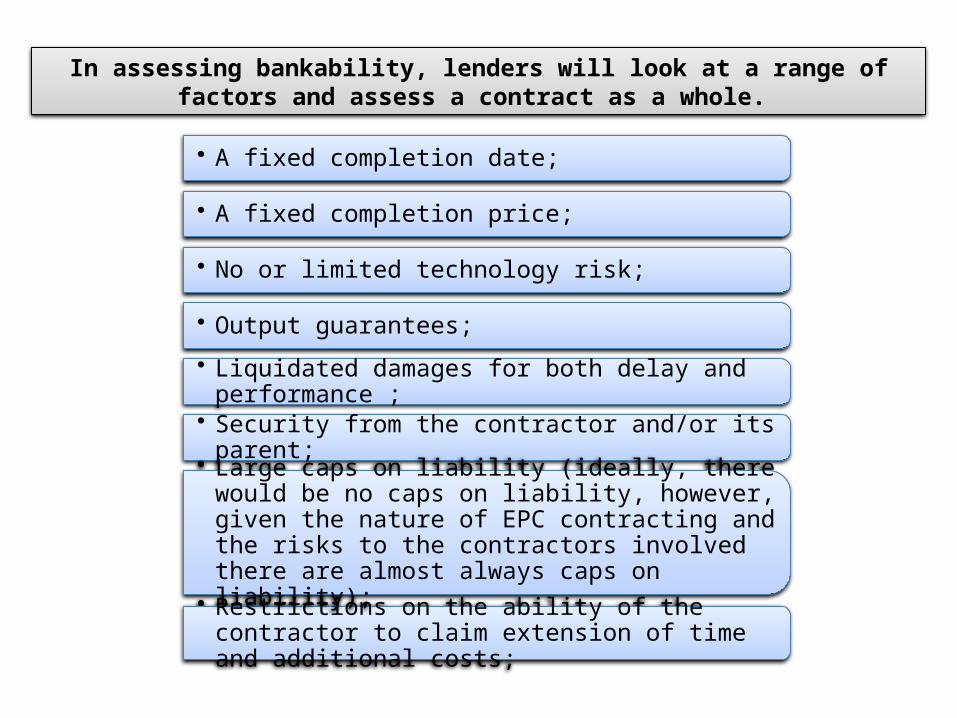

In assessing bankability, lenders will look at a range of factors and assess a contract as a whole.

• Restrictions on the ability of the contractor to claim extension of time and additional costs;

• A fixed completion date;

• A fixed completion price;

• No or limited technology risk;

• Output guarantees;

• Liquidated damages for both delay and performance ;

• Security from the contractor and/or its parent;

• Large caps on liability (ideally, there would be no caps on liability, however, given the nature of EPC contracting and the risks to the contractors involved there are almost always caps on liability);

This is one of the major reasons why they are the predominant form of construction contract used on

large-scale project financed power and infrastructure projects.

An EPC contract delivers all of the requirements listed above in one integrated package, being designed to satisfy the lenders‟ requirements for bankability.

E CCPEngineering

Applying acquired

knowledge and

experience to efficiently

DesignThe wind

farm according to requirements

ProcurementSupplying of equipment at

the best possible cost to meet the needs of the

project in terms of quality,

quantity time and location

ConstructionBuilding and assemblying

the ifrastructure

and the equipment. Requires

competive costs, carefull planning of works and materials,

QHSE awareness, etc

Contract

EPC Contracting - Abbreviation

Supplier

EPC

Technical Advisor

EPC Contracting – Scenarios

• The sponsor and lenders sign separate contracts with the EPC contractor (BoP) and the Equipment supplier;

• An Interface Table regulates the responsibilities between the involved parties;

• The supplier warranties the equipment and optionally, maintains theequipment under a long term contract;

• The EPC Contractor warranties the infrastructure;

Scenario 1

Project Company

Financing

• The Sponsor and the Lenders sign one contract with the EPC Contractor ;

• The Supplier sign also a contract with the EPC Contractor ;

• The Interface Table regulates the responsibilities between the involved parties.

• The EPC Contractor warranties the project;

• Optionally the Supplier maintains the equipment under a long term contract;

Scenario 2

Supplier

EPC

Technical Advisor

Project Company

Financing

• Professional liability insurance (PLI), also commonly known as errors & omissions (E&O) in the US, is a form of liability insurance that helps protect the professional advice and service by EPC contractor from bearing the full cost of remedying works because of fault design.

EPC Contracting – Project Insurance

Coverage

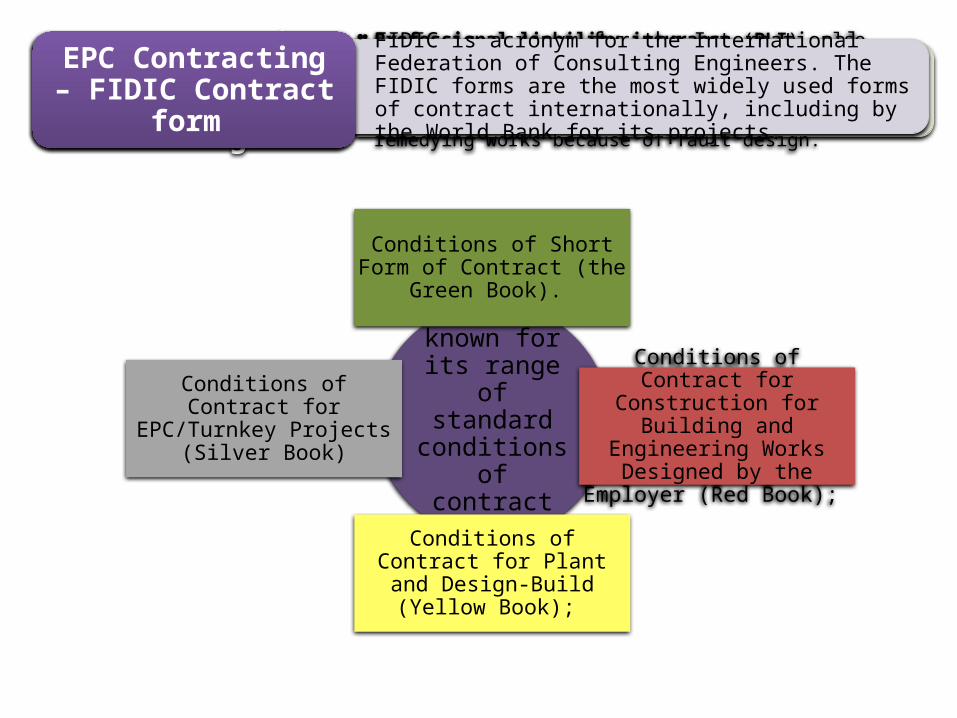

• FIDIC is acronym for the International Federation of Consulting Engineers. The FIDIC forms are the most widely used forms of contract internationally, including by the World Bank for its projects.

EPC Contracting – FIDIC Contract form

It is best known for its range of

standard conditions of contract for:

Conditions of Short Form of Contract (the Green Book).

Conditions of Contract for Construction for Building and Engineering Works Designed by the Employer (Red Book);

Conditions of Contract for Plant and Design-Build (Yellow

Book);

Conditions of Contract for EPC/Turnkey Projects (Silver

Book)

EPC contracts provide for: • The contractor is responsible for all design, engineering,

procurement, construction, commissioning and testing activities. Therefore, if any problems occur the project company need only look to one party – the contractor – to both fix the problem and provide compensation. As a result, if the contractor is a consortium comprising several entities, the EPC contract must state that those entities are jointly and severally liable to the project company.

A single point of responsibility.

• Risk of cost overruns and the benefit of any cost savings are to the contractor‟s account. The contractor usually has a limited ability to claim additional money, which is limited to circumstances

A fixed contract price

• EPC contracts include a guaranteed completion date that is either a fixed date or a fixed period after the commencement of the EPC contract. If this date is not met the contractor is liable for Delay Liquidated Damages (DLDs). DLDs are designed to compensate the project company for loss and damage suffered as a result of late completion of the wind farm.

A fixed completion

date

• The project company’s revenue will be earned by operating the wind farm. Therefore, it is vital that the wind farm performs as required in terms of output and reliability. Therefore, EPC contracts contain performance guarantees , payable by the contractor if it fails to meet the performance guarantees. These performance guarantees usually comprise a guaranteed power curve and an availability guarantee guaranteeing the level of generation of electricity

Performance guarantees

• Most EPC contractors will not, as a matter of company policy, enter into contracts with unlimited liability. Therefore, EPC contracts for power projects cap the contractor’s liability at a percentage of the contract price. This varies from project to project.

Caps on liability.

• It is standard for the contractor to provide performance security to protect the project company if the contractor does not comply with its obligations under the EPC contract. The security takes a number of forms including:

Security

A bank performance guarantee for a percentage, normally in the range of 5–15%, of the contract price. The actual percentage will depend on a number of factors including:

Retention Money Guarantee, ie withholding a percentage (usually 5%–10%) of each payment.

Advance payment guarantee, if an advance payment is made

A parent company guarantee - this is a guarantee from the ultimate parent (or other suitable related entity) of the contractor, which provides that it will perform the

contractor‟s obligations if, for whatever reason, the contractor does not perform

• the other security available to the project company;

• the payment schedule (because the greater the percentage of the contract price unpaid by the project company, the smaller the bank guarantee can be);

• the identity of the contractor and the risk of it not properly performing its obligations;

• the price of the bank guarantee and the extent of the technology risk;

Vă mulţumesc,

Robert GhelasiDirector Energy Department

Capital PartnersEmail: [email protected]

Mobil: 0724377661

Related Documents