Foreign Direct Investment Mode Choice: Entry and Establishment Modes in Transition Economies Author(s): Desislava Dikova and Arjen van Witteloostuijn Source: Journal of International Business Studies, Vol. 38, No. 6 (Nov., 2007), pp. 1013-1033 Published by: Palgrave Macmillan Journals Stable URL: http://www.jstor.org/stable/4540472 . Accessed: 27/09/2013 05:22 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . Palgrave Macmillan Journals is collaborating with JSTOR to digitize, preserve and extend access to Journal of International Business Studies. http://www.jstor.org This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AM All use subject to JSTOR Terms and Conditions

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Foreign Direct Investment Mode Choice: Entry and Establishment Modes in TransitionEconomiesAuthor(s): Desislava Dikova and Arjen van WitteloostuijnSource: Journal of International Business Studies, Vol. 38, No. 6 (Nov., 2007), pp. 1013-1033Published by: Palgrave Macmillan JournalsStable URL: http://www.jstor.org/stable/4540472 .

Accessed: 27/09/2013 05:22

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Palgrave Macmillan Journals is collaborating with JSTOR to digitize, preserve and extend access to Journal ofInternational Business Studies.

http://www.jstor.org

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1014

Anderson (1988), Kim and Hwang (1992), Brouthers et al. (1998), Delios and Beamish (1999), Pan and Tse (2000), Luo (2001), Meyer (2001), Brouthers (2002) and Yiu and Makino (2002) investigated the choice between wholly owned subsidiaries and joint ventures. Our aim is to provide four contributions to these two streams of literature.

First, both streams of research are valuable but limited in one important way, as these studies tend to investigate how certain factors affect either the establishment or the entry mode choice in isolation. The argument is that these two choices are conceptually different, covering diverse aspects of FDI. The establishment mode decision is argued to depend mainly on the effective combination of the MNE's and local assets, while the choice of ownership structure is said to hinge largely on the need for control over the subsidiary's assets (Gatignon and Anderson, 1988). However, most scholars agree that both types of foreign investment choice are influenced by similar firm-, industry- and country-level covariates. In this study, there- fore, our first contribution is to bridge both streams of literature by focusing exclusively on shared elements with prevalent logic to arrive at a conceptual synthesis that provides the frame for an examination of the effects of the same set of covariates on the dual entry-establishment mode choice made in the context of a single foreign investment. This gives our first research question: In a foreign direct investment decision, what set of factors determine the choice between acquisition and greenfield, as well as the establishment of a wholly owned outlet or a subsidiary with shared ownership?

Second, firm-level factors have received much attention in earlier work on the establishment mode choice. By contrast, research on the influence of country-level factors is limited, to date, to testing the effect of cultural distance on the establishment mode choice (Kogut and Singh, 1988; Brouthers and Brouthers, 2000; Larimo, 2003). Although the influence of institutional variables has been exam- ined in entry mode studies, to the best of our knowledge the impact of the institutional environ- ment has not yet been investigated in the context of research on establishment modes. Here lies our second contribution: we introduce a long- neglected, country-level predictor of establishment mode choice - the host country's institutional environment. This produces our second research question: To what extent does the host country's

institutional environment affect the establishment and entry mode choices?

Third, in relation to this, we offer a third contribution. Past studies testing for institutional effects on entry modes cover issues related to political hazards (Delios and Henisz, 2000), legal restrictions on foreign ownership (Delios and Beamish, 1999; Yiu and Makino, 2002) and country risks (Brouthers et al., 2004). We contribute to both streams of FDI literature by using a different and more encompassing measure of features of a host country's institutional environment, namely the World Bank's governance indicators, which offer a comprehensive measure of a country's political stability, government effectiveness, regulatory qual- ity, rule of law, voice and accountability, and corruption control. We coin this new measure institutional advancement. Institutional advance- ment is defined as the degree to which a host country's institutional environment matches the standards well established in developed market economies.

Fourth, and finally, previous research on estab- lishment modes (and most of the literature on entry modes) studied the effect of firm-level and country-level factors in isolation, and hence failed to demonstrate how a particular investment loca- tion may moderate the effect of firm specificities on the choice between an acquisition and a greenfield (or a wholly owned vs a partially owned subsidiary). We therefore test the moderating effect of the host country's institutional environment on the impact of the parent firm's features on establishment and entry mode choices. This provides our final research question: Does the institutional environ- ment moderate the effects of firm-level character- istics on establishment and entry mode choices? Throughout the paper, we focus on a specific aspect of the institutional environment - its level of advancement - in a specific context - transition economies. As we will argue below in greater detail, we believe that institutional advancement is the key to understand the main and moderating effects of the institutional environment on an MNE's FDI mode choices, particularly in the context of transi- tion economies.

So, this study consists of two conceptual parts: the first part discusses the main and moderating effects of institutional advancement on the choice between an acquisition and a greenfield entry mode, and the second part analyses the main and moderating effects of institutional advancement on the choice between wholly owned subsidiaries and

journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1015

subsidiaries with shared ownership. Our hypoth- eses are tested with survey-collected data of 160 western European MNEs that recently invested in transition economies in central and eastern Europe (CEE), offering appropriate institutional variety. In the next section we introduce the theoretical foundations, and develop hypotheses that predict how MNE features may determine the establish- ment and entry mode choices in a particular institutional setting. Subsequently, in the metho- dology section, we describe the data collection procedures, the measures of our variables, and the analytical tools used to test the hypotheses. Next, we present the results of our study. Finally, we conclude with a discussion and appraisal, including suggestions for future research.

Theory The decision as to whether to establish an acquisi- tion or a greenfield subsidiary or to opt for full or partial ownership in a foreign investment carries significant strategic importance owing to the inherent benefits and risks of each foreign estab- lishment and entry mode. For instance, although acquisitions offer a speedy establishment of local presence, they may be associated with post-acquisi- tion integration failures, which are often rooted in cross-cultural differences and technological mis- matches. Reversely, although greenfields offer an opportunity to preserve and replicate valuable corporate cultures abroad, they require a longer establishment period and more time to build business networks locally. In addition, ventures with shared ownership enable MNEs to tap into valuable resources of a local partner and minimise investment risks, but they also are at times challenging to administer owing to the partners' diverging capabilities, interests and goals. In con- trast, wholly owned subsidiaries offer the benefits of managerial autonomy and full control over local operations, yet the process of overcoming the liability of foreignness may be difficult without the legitimacy of a local partner.

Traditionally, transaction cost economics (TCE; Williamson, 1975) is broadly applied to such establishment and entry mode choice issues (Zhao et al., 2004). Among the influential studies that develop the TCE approach are those by Kogut and Singh (1988), Hennart and Park (1993), Andersson and Svensson (1994), Brouthers and Brouthers (2000) and Larimo (2003), who investigated the choice between greenfields and acquisitions, and by Gatignon and Anderson (1988), Kim and Hwang

(1992), Delios and Beamish (1999), Meyer (2001) and Brouthers (2002), who examined the choice between wholly owned subsidiaries and subsidiaries with shared ownership. According to Yiu and Makino (2002), the TCE tradition tends to under- state the significance of contextual factors in the choice of a foreign investment mode. Therefore, in this paper, we follow Williamson's (2000) new institutional economics (NIE) approach, as it best incorporates North's (1990) ideas about the central role of the larger environment in constraining the optimality of a firm's actions. As we aim at shedding more light on the importance of institu- tions to MNEs' foreign direct activities, we make a clear contribution to the literature by applying insights from NIE for the first time in a study on establishment modes.

Although the social dimension of institutions, as related to nations' norms, customs and traditions, is typically critical, we decided to ignore this dimension here, as social aspects of the institu- tional environment change very slowly over time 'in the order of centuries or millennia' (Williamson, 2000: 596). Our focus is limited to the institutional environment of a host country that comprises a country's 'formal rules' (such as constitutions, laws, and property rights) (North, 1991: 97). According to Williamson (2000), major changes in the rules of the game occur in the order of decades or centuries, as 'cumulative change of a progressive kind is very difficult to orchestrate' unless 'rare windows of opportunity' that induce a broad reform are opened (Williamson, 2000: 598). Such a window of oppor- tunity is the collapse of communist CEE and the former Soviet Union, and their subsequent transi- tion to a market economy, as this produced volatile institutional environments that offer ideal settings to demonstrate the crucial role of institutions in facilitating or constraining business (Meyer, 2001). We refer to the extent to which market-economy- consistent rules of the game are operational as the degree of institutional advancement.

We focus on institutional advancement in the context of a host country's formal rules of the game, which in the process of transition undergo important changes to secure market economy rule. Institutional advancement in this study is a dynamic concept as it pertains to changes in (formal) institutions over time. Our approach is similar to that applied by Meyer (2001), who studies the effects of progress in institution build- ing on entry modes in several transition economies. Valuable as they are, Meyer's findings are limited by

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

*Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1016

a methodological restriction - the EBRD institu- tional data used in his study are derived from a single year of observation (1997), thus eliminating the possibility of capturing variations in institution building over time and their effect on foreign investment modes. However, as we will explain in detail below, estimates of the World Bank's indica- tors demonstrate substantial change for some countries in some periods: for example, between 1996 and 2004 the Slovak Republic registered large changes in 'voice and accountability', Latvia and Lithuania in government effectiveness, Estonia and Lithuania in rule of law, and Bulgaria, Estonia and Latvia in corruption control (Kaufmann et al., 2005). Therefore we advance Meyer's approach by accounting for changes over time in the transfor- mation of institutions to a form appropriate for a market economy: that is, we introduce a time- variant measure of institution building.

In addition to institutional effects, we look at three firm-level factors that turned out to be influential in earlier establishment and entry mode choice studies. For one, the main contribution of TCE to the study of FDI has been the concept of asset specificity (Delios and Beamish, 1999). The basic premise of TCE in the context of FDI activities is that a greater degree of asset specificity induces a greater need for full ownership. Another element of TCE, the efficiency aspect, is the predominant logic in studies of establishment mode choice: firms with a high degree of asset specificity would typically set up a greenfield subsidiary as the most efficient way of transferring those specificities abroad (Hennart and Park, 1993). Thus the first firm-level factor to be examined here within the framework of NIE and FDI modes is parent firm's asset specificity.

The second firm-level factor we take on board is international strategy. Harzing (2000, 2002) found that global companies tend to establish greenfield subsidiaries to ease the transfer of the parent firm's core competences and preserve valuable corporate cultures. Reversely, multidomestic companies tend to prefer acquisitions, as they are the most efficient way of achieving the goal of local knowledge absorption and conforming to diverse local demands as multidomestic MNEs' activities are

usually 'tied to the buyer's location' (Harzing, 1999: 39). In addition, Hill et al. (1990) conceptua- lise that the entry mode decision is determined by environmental, transaction and strategic variables, as one of the main strategic decisions an MNE has to make is whether to adopt a global or a multi- domestic strategy. In similar vein, Luo (2001)

argues that the entry mode choice is associated with firm-specific factors such as knowledge protection, global integration and host-country experience.

Finally, according to TCE, firms with more international experience develop organisational capabilities that enable them to make greater commitments to a foreign investment (Johanson and Vahlne, 1977). As firms with greater interna- tional experience face fewer local knowledge dis- advantages, the need for local partner to ease up liabilities of foreignness decreases and the desire for full ownership increases. Similar logic is behind the organisation capabilities argument that firms applying the same establishment mode abroad develop specific skills to either create replicas of the parent firm (in the case of a predominance of greenfield investments) or efficiently integrate foreign firms (in the case of a predominance of acquisition establishments). The development of such firm-specific skills increases the likelihood that these skills will be further exploited in the context of the same establishment mode applied subsequently in a different location (Chang and Rosenzweig, 2001). Because of the supra-national character of international experience in all its forms (including host-country and establishment mode experience), we do not predict a moderating effect of the institutional environment on the influence that such MNEs' experience has on subsequent establishment and entry mode choices. However, in our empirical analyses, we control for the effects of international, regional and establishment experi- ence. Hence we focus on the expected moderating effects of institutional advancement on the impact of a parent firm's asset specificity and international strategy on the establishment and entry mode choice.

Hypotheses

Institutional advancement In this study we concentrate exclusively on the effect of formal or regulative institutions on the MNE's establishment and entry mode choice, because such regulative forces are often targeted directly at economic behaviour, and are therefore most commonly studied in international business research (e.g., Delios and Beamish, 1999; Brouthers, 2002). Moreover, the regulatory processes in transi- tion economies are very likely to be an influential force in MNE decision-making as to (the mode of) foreign entry and establishment. Regulative forces

journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1017

include laws and regulations, as well as political and other societal configurations. In this sense, regulatory institutions provide the 'rules of the game' in the host country, and the structure in which firms have to interact (North, 1990).

The replacement of the old central planning regimes with market economy mechanisms requires the initiation of a wide array of far- reaching institutional reforms. The most urgent yet most problematic and time-consuming of such reforms are the legal and judicial transformations aiming at establishing and safeguarding the rule of law. The critical importance of legal and judicial reforms in the CEE transition economies is best illustrated by the EU decision to postpone Bulgaria's and Romania's accession until 2007, conditional on the continuous reforms in the so- called 'red flag' sectors. Some of the red flag sectors for Romania include judicial reform and the fight against corruption, and for Bulgaria intellectual property rights (Global Insight, 2006). Clearly, market-based institutions have been established in the CEE countries, all designed to comply with relevant EU regulations, but as they underwent numerous changes, this generated inconsistency between the requirements of different institutions, leading to uncertainty over future institutional changes (Meyer, 2001). Thus, over more than a decade of transition, the transformation of the institutional environment of CEE countries, often described as emerging rather than established market economies, created a certain extent of environmental volatility that left a mark on the outlook of foreign direct investment activity.

TCE explains how the institutional environment might impact upon FDI. Studies rooted in TCE consider greenfield entries as more risky than entries through acquisitions. This is because launching an acquisition means buying an existing enterprise with a team of managers who are familiar with industry and local market conditions, which reduces the uncertainty about the subsidiary's future. Thus launching an acquisition generally implies going for a lower but more certain expected rate of return (Caves, 1996). By contrast, a green- field establishment has to be built from scratch. Hence it represents a combination of inputs (assets) that has not yet proved to be successful in the particular foreign market. Not surprisingly, per- haps, studies on acquisitions in transition econo- mies arrive at conclusions that are in conflict with this popular logic. Uhlenbruck and De Castro (2000: 385) note that country risk is of 'paramount

importance' to firms involved in acquisitions in the CEE region as it can 'change the basis upon which an investment decision was made'. The transition from a centrally planned to a market economy may create risks not anticipated by foreign acquirers (Murtha and Lenway, 1994). Furthermore, Uhlenbruck and De Castro (2000) report that, owing to high country risk in CEE, long-term returns in acquired local firms are more uncertain. They conclude that acquisitions in high-risk coun- tries may improve performance of the acquired firm only in the short run, or only in those countries where environmental conditions continue to improve. Based on these regional observations, we argue that an improved institutional environment positively affects the likelihood of acquisition establishments. Therefore, conditional on the extent to which smoothly functioning and sustain- able market economy institutions are established, we suggest:

Hypothesis la: Greater institutional advance- ment is positively associated with the likelihood of acquisition establishments.

In developed market economies, effective property rights protection ensures that the owner of an asset 'has the discretion over the uses to which the asset is put and is able to appropriate returns from the asset' (Delios and Beamish, 1999: 919). Conversely, according to Rawski (1994), property rights are perceived as weak in emerging markets in terms of enactment and enforcement. Furthermore, past research rooted in TCE reports that investors in transition economies typically face high transac- tion costs for any of the enlisted reasons: foreign firms lack information about local partners; they must 'negotiate with agents inexperienced in business negotiations; and they face unclear reg- ulatory frameworks, inexperienced bureaucracies, underdeveloped court systems and corruption' (Meyer, 2001: 358). However, firm-specific compe- tences and tacit knowledge are the prominent determinants of MNE's sustainable competitive advantage in emerging markets (Luo, 1997). There- fore MNE's competitive advantage is better pro- tected against infringement and piracy by setting up a wholly owned subsidiary, as this entry mode provides a vehicle for maximum control to safe- guard proprietary knowledge (Luo, 2001).

In short, in underdeveloped institutional envir- onments characterised by weak property rights regimes, full ownership modes are more efficient

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1018

because they reduce the transaction costs of unwanted dissemination. Conversely, in transition economies with institutional safeguards offering greater property rights protection, lower ownership modes are more efficient as the risk of asset expropriation is less and 'costly governance struc- tures do not need to be constructed to protect assets' (Delios and Beamish, 1999: 919). Building on the above arguments, indicating that progress in institution building reduces the transaction costs of operating an outlet with a local partner, and diminishes the necessity of setting up a costly governance structure, we have:

Hypothesis ib: Greater institutional advance- ment is positively associated with the establish- ment of subsidiaries with shared ownership.

Technological intensity and institutional advancement There are numerous reasons for firms to enter into international markets, but the level of technologi- cal development is certainly considered to be one of the critical determinants of FDI (Kobrin, 1991; Dunning, 1993). Firms from high-technology- intensive industries frequently enter into foreign markets to cover their costly R&D investments, prevent product obsolescence, and gain market share (Harris and Ravenscraft, 1991). Through a foreign entry, MNEs transfer and share their proprietary technologies, skills and knowledge with local organisations in the hope of gaining addi- tional profits or amortising the costs of R&D over a larger quantity of products sold at home and abroad (Tihanyi and Roath, 2002). In the context of the establishment mode literature, past studies unanimously consider greenfields as the most appropriate establishment mode for technologi- cally intensive firms. As the competitive advantages of technologically intensive firms are deeply embedded in their organisational practices and labour force skills, the most efficient way of transferring them abroad is by establishing a subsidiary from scratch, hiring and training a local labour force accordingly (Hennart, 2000). In the context of the entry mode literature, a number of studies observe a positive relationship between asset specificity and higher level of ownership (Kim and Hwang, 1992; Erramilli and Rao, 1993). Owing to the abundance of past studies with similar findings, we first posit these two types of relationship as the main effect of technological intensity on the likelihood of greenfield establish-

ment and full-ownership entry, and we present our arguments on how institutional advancement moderates these established relationships next.

A greenfield project entails building a subsidiary from scratch to enable foreign production and/or sale: real estate is purchased locally, and domestic employees are hired and trained by applying the investing firm's technology, know-how, manage- ment and capital (Meyer and Estrin, 2001). Markets for complementary resources, such as land and real estate, are relatively efficient in market economies, but not necessarily so in transition economies. Estrin et al. (1997) report that inefficiencies in markets for complementary resources lead to sub- stantial extra costs and delays of greenfield invest- ments. For example, inefficient bureaucracies in the local land registries hinder real estate markets in CEE, and the resulting transaction costs inhibit greenfield projects (Meyer and Estrin, 2001). Clearly, the level of institutional advancement of a host country plays an important role in the success of greenfield projects in transition econo- mies, as market-economy regulations and law- enforcement mechanisms can facilitate the process of establishing fairly well-developed local markets for complementary resources. In addition, techno- logically intensive firms are likely to benefit from well-developed and well-administered labour mar- kets that not only provide easy access to local technical labour with mathematical and engineer- ing skills, but also serve as an indirect mechanism for keeping under control expenses for retraining MNEs' local employees.

Moreover, we build on past findings that techno- logically intensive firms prefer greenfield invest- ments because these reduce the chances of dissemination of firm-specific advantages (Hennart and Park, 1993). As these findings are derived primarily from observations on foreign investments in developed economies, we argue that such an establishment strategy can be applied effectively only in institutionally safeguarded environments. That is, the advancement in the progress of institutional reforms in transition economies and the successful approximation of a wide range of laws and norms to those established in market economies is likely to positively affect greenfield establishments by technologically intensive MNEs. As stated earlier, transition countries undergo numerous institutional transformations that in some instances significantly reform their business environments to match a market economy rule system. This implies lengthy lists of reforms, the

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1019

most compelling of which relate to the enforce- ment of property rights, specific anti-inflation measures, promotion of economic growth, and establishing local competition (Tihanyi and Roath, 2002). We argue that institutional reforms advance institution building, lessen the differences between institutions in developed and transition economies, and are likely to exert a positive moderating effect on the relationship between an MNE's technologi- cal intensity and its preference for greenfield establishments. Thus we formulate:

Hypothesis 2a: Greater institutional advance- ment has a positive moderating effect on the tendency of technologically intensive MNEs to establish greenfield subsidiaries.

The other stream of FDI mode research examines the choice of foreign entry to invest in a wholly owned outlet or a subsidiary with shared owner- ship. A significant number of empirical studies have applied TCE to predict the circumstances under which MNEs would choose to establish either one of the alternative types of subsidiary (Gomes-Casseres, 1990; Hennart, 1991). These studies have generally confirmed the hypothesis that parent firms with advanced proprietary tech- nologies, most likely transferring technology to foreign ventures to gain competitive advantage over indigenous firms, are inclined to opt for entry via wholly owned affiliates rather than subsidiaries with shared ownership. Maximally controlled ven- tures are preferred because of the risk of opportu- nism on the side of the foreign partner and the potential loss of proprietary technology after its transfer to a jointly owned venture. In the case of the underdeveloped institutional framework in transition economies, the transfer of knowledge may be of particular concern because of the insufficient abilities of institutions to provide protection of intellectual property rights. Further- more, enforcement of intellectual property rights relies on the general enforcement powers of the courts: where the judicial system is corrupt, or where property rights are not respected, the ability of firms to transfer valuable intellectual property will be compromised (Oxley, 1999). Hence technology-intensive firms would have stronger reasons to seek full control over their assets in transition economies. Such knowledge- intensive assets, as put by Meyer, include 'transfer of production know-how, assessment of market opportunities for innovative products, as well as

training of sales and service personnel' (Meyer, 2001: 360).

In contrast, sharing the control over a foreign operation locally is needed if the collaboration with the local partner provides complementary resources, which may consist of specific technolo- gies or local market knowledge (Belderbos, 2003). In addition to cultural barriers, most transition countries have a longer history of sheltered econo- mies than the newly written history of openness to trade and investment, which results in relatively short local investment experience for most MNEs. This suggests that many MNEs would lack specific knowledge related to an assessment of local market opportunities or possession of local technologies, and hence would seek access to such resources. An involvement of a local partner is clearly beneficial to the MNE as it provides the most efficient access to local knowledge, yet is likely only in an institutionally advanced environment. We propose that, as the level of advancement in institutional environments decreases the transaction costs asso- ciated with international knowledge transfer by providing better safeguard mechanisms against infringement and piracy, this exerts a positive moderating effect on the likelihood of investors opting for an alternative to the full ownership entry mode. So, we suggest:

Hypothesis 2b: Greater institutional advance- ment has a positive moderating effect on the tendency of technologically intensive MNEs to establish subsidiaries with shared ownership.

International strategy and institutional advancement MNEs following a multidomestic strategy typically aim at establishing a sustainable local market presence. Their primary concern is a proper response to local consumer preferences. In general, acquisitions can be an attractive establishment mode as they provide local brands, market knowl- edge, distribution channels and network relation- ships with both the host country's business and governmental authorities. Past literature provides empirical support that the best way to attain control over marketing assets such as local brands is through the acquisition of a local firm, even if these are the only valuable assets that the firm controls (Meyer and Estrin, 2001). We first posit this established relationship between an MNE's multidomestic strategy and the likelihood of acqui- sition establishment as the main effect, and subse-

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1020

quently present our arguments on how institu- tional advancement moderates this relationship.

In many instances, multidomestic MNEs face the challenge of a profound restructuring of the acquired local firm, because firms in (former) socialist and capitalist societies have a very differ- ent 'dominant logic' (Newman, 2000). The incen- tives created by central planning produced severe distortions, such as production of large volumes of low-quality products, lack of concern for consumer preferences, and a disregard for environmental protection. Furthermore, one of the leading objec- tives of socialist societies was securing full employ- ment: firms employed 'far more people than necessary to achieve output targets as labour costs were not a constraining variable' (Meyer, 2002: 271). Labour relationships were based on lifetime employment, and in most cases local enterprises provided for the social needs of both current and retired employees. To accomplish a successful transformation of organisational rules and perfor- mance criteria from those based on the central planning system to their counterparts that fit with a market economy, MNEs need not only a transfer and re-configuration of resources, but also radical changes of organisational cultures, processes and structures (Meyer, 2002).

An enterprise restructuring typically starts with laying off excess workers, shedding redundant assets and/or shifting the product mix to survive under hard-budget constraints (Brada, 1996; Carlin, 2000). Divestment of local firms' social assets, such as kindergartens and health care facilities, is socially acceptable only if there are other providers of these services (at municipal or state level) (Meyer, 2002). Studies on privatisation argue that the future development of privatised firms is highly dependent on institutional change and public policy (Uhlenbruck and De Castro, 1998; Meyer, 2002). In general, profound organisational trans- formations are possible only when changes are safeguarded by market economy institutions, parti- cularly the necessary regulatory framework.

Finally, the establishment mode choice implies costs and time spent on integration and adaptation. In acquisitions, typically preferred by multidomes- tic MNEs, bringing together assets previously held by different businesses incurs transaction costs in the market for corporate control. Transaction costs of foreign acquisitions in transition economies may be significant as markets for corporate control are highly imperfect: 'costs are incurred for searching suitable targets, analysing their economic viability,

and negotiating with management, owners and government authorities' (Meyer and Estrin, 2001: 579). It could be that an acquisition under such circumstances is not the most viable establishment strategy for multidomestic MNEs in transition economies. Therefore we argue that, in the context of a successful realisation of a multidomestic strategy by acquiring a local entity for its valuable assets, only advanced institution building can facilitate the complex process of locating and purchasing the appropriate acquisition target, initi- ating a profound organisational restructuring and integrating the newly established subsidiary within the MNE's structure and organisational culture. Hence we provide:

Hypothesis 3a: Greater institutional advance- ment has a positive moderating effect on the tendency of multidomestic MNEs to establish acquisitions.

Hill et al. (1990) suggest that a lower degree of control is required for firms pursuing a multi- domestic strategy. The attributes of products vary between nations according to the tastes and preferences of different consumers. Hence each subsidiary will have its own marketing function and its own manufacturing facilities. Hence Hill et al. (1990) argue that firms pursuing a multi- domestic strategy will favour low-control (owner- ship) entry modes. This relationship implies the main effect of international strategy on entry mode that is likely to be moderated by the level of institutional advancement. As locally customised products demand considerable local knowledge, the process of customisation requires the investing firm to work actively with the local partner (entity) to accomplish the product customisation that will meet the specific requirements of the local custo- mer. Accordingly, working relationships between the personnel of the parent firm (the investor) and the local partner need to be developed, thus creating firm-specific knowledge about what to expect from individuals and how to communicate information between headquarters and subsidiaries (Anderson and Gatignon, 1986). This firm-specific knowledge constitutes an asset that locks in the investing firm, as the asset is a product of the joint effort of the investor and the local partner, and its positive effect exists only within the boundaries of the newly established entity (Anderson and Gatignon, 1986). In line with TCE, unless there is an external safeguarding mechanism in place to

journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn * 1021

protect such asset from free-riding by local firms, a higher degree of control (ownership) may be needed to preserve it. We argue that in the context of an underdeveloped institutional environment, which fails to create external safeguarding mechan- isms against the threat of free-riding by local firms, striving for maximum control may be the only option for protection of locally created, firm- specific knowledge. Hence, if institutional mechan- isms of intellectual property protection are not in place, to eliminate the danger of free-riding and piracy a multidomestic firm may trade some of the subsidiary's freedom in directing local marketing and production operations for a less effective mechanism of maximum control (full ownership). Conversely, in the case of advanced institution building, the multidomestic MNE faces less neces- sity for full control of the subsidiary. From this, we expect that:

Hypothesis 3b: Greater institutional advance- ment has a positive moderating effect on the tendency of multidomestic MNEs to establish subsidiaries with shared ownership.

Methodology

Data collection To test the above hypotheses, we conducted an international mail survey among international companies from the EU that have invested in 10 transition economies in the CEE region. We initially selected from the Amadeus data set all registered companies based in the then 15 members states of the EU that had at least a 10% ownership stake' in a branch/subsidiary located in any of the following countries: Bulgaria, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Roma- nia, Slovakia and Slovenia. These countries were chosen for this study because they were, and still are, in various stages of transformation from centrally planned to market economies. Therefore this set of countries offer a unique opportunity to test the extent to which our theoretical arguments and hypotheses hold true.

An English-language questionnaire was created that contained 33 open- and closed-ended ques- tions (available upon request). The questionnaire was pilot-tested with managers in four Dutch companies who were competent in the English language and knowledgeable of their firm's inter- national expansions into CEE countries. The pilot tests revealed full understanding of the posited

questions, and supported our expectations of managers' ability to answer them accurately and comprehensively. Additionally, five well-known international academic researchers reviewed the questionnaire, and their comments and suggestions were integrated into a revised version. The final English-language questionnaire was translated into German, French and Italian by a team of profes- sional interpreters.2 The translated versions of the questionnaire were back-translated into English by native-speaking academics at our university. In total, initially 2798 questionnaires were mailed: 35 were returned as non-deliverable, which com- pressed the sample size to 2763 questionnaires. We received 208 usable questionnaires, representing an overall response rate of 7.5%.3 The greenfield establishments represent 59.8% of the sample (hence the share of acquisitions is 40.2%), and the wholly owned subsidiaries include 60% of the total sample. As a result of missing data, we could use 160 questionnaires in the current study.

To test the representativeness of our sample, we conducted a t-test comparing the firm size variable (number of employees worldwide) of our sample with a random selection of the firm population, which revealed no statistically significant differ- ences in the two means. Furthermore, from the Amadeus database we downloaded available infor- mation on the number of employees worldwide for 125 of the firms in our sample, as well as available information about total sales for 142 of the MNEs in our sample. We performed statistical tests to compare our primary data with these pieces of secondary-source information. Paired-sample t-tests showed that the differences in means between the survey-collected information and the Amadeus data were insignificant for the employees variable (t=0.96, d.f.-89 and P=0.33). The tests on sales volumes revealed less encouraging results (t=0.39, d.f.=141 and P=0.69), most likely because the archival data had a wide range in terms of the last year of recording (from 1998 to 2002). As our survey was conducted in mid-2003, we selected only those firms for which Amadeus reported 2002 as the last year of record. The paired t-tests revealed that t=1.22, d.f.=51 and P=0.22 for the number of worldwide employees, and t=1.05, d.f.=59 and P=0.29 for worldwide sales. In addition, following Uhlenbruck and De Castro (2000), we determined a reliability coefficient of 0.97 for 53 of the firms in our sample that had data in Amadeus recorded for the year 2002 as to both variables. To obtain this coefficient, we used the general form of the

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

SForeign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1022

Spearman-Brown prophecy formula and incorpo- rated the correlations of 0.93 (employees) and 0.91 (sales) between the archival data and our survey information. So, all tests conducted confirm that our survey sample is representative for the larger population.

Finally, although not all our measures are based on our single-respondent questionnaire (see below), we also checked the primary data for potential common-method variance. Podsakoff and Organ (1986) argue that if the single-respon- dent variables in a study all load on one factor, or if there is one factor that explains the majority of the variance, then common-method variance may be a problem. We performed a factor analysis for the questionnaire-based dependent and independent variables used in this study, which resulted in a four-factor solution, with the largest factor explain- ing only 19% of the variance. Therefore it appears that our data set does not suffer from common- method variance.

Measures The dependent variables are the MNEs' latest Estab- lishment mode choice (greenfield vs acquisition) and Entry mode choice (full vs shared ownership) into a CEE country. They were obtained through the questionnaire enquiring about whether the MNE, in the process of its most recent foreign entry event into a CEE country, had acquired an existing local company or whether it had built an operation from scratch, and how much its ownership share was in this foreign operation. So Establishment mode is captured by a dummy variable, which takes the value of 1 in the case of a greenfield establishment and 0 in the case of an acquisition establishment. Entry mode is also captured by a dummy variable, which takes the value of 1 if the subsidiary had shared ownership and 0 in the case of full owner- ship. Since 60% of our sample represented invest- ments with 100% ownership, to obtain satisfactory level of variation we consider subsidiaries with shared ownership to be all occasions of investments representing between 13 and 90% ownership (47 observations in total).

Our hypotheses relate to three independent vari- ables. First, Institutional advancement is a composite measure obtained from the World Bank's Govern- ance Indicators (Kaufmann et al., 2005), which provide a score on items such as voice and account- ability (measuring political, civil and human rights), political stability (measuring the likelihood of violent threats to or changes in government),

government effectiveness (measuring the competence of the bureaucracy and the quality of public service delivery), regulatory quality (measuring the inci- dence of market-unfriendly policies), rule of law (measuring the quality of contract enforcement, the police, and the courts, as well as the likelihood of crime and violence) and corruption control (measuring the exercise of public power for private gain). The composite measure ranges from -2.5 to 2.5, with higher scores corresponding to higher institutional advancement. We use these indicators for particular reasons. For one, to date, these indicators encompass the broadest range of institu- tional issues and years of measurement. The governance indicators measure six institutional dimensions, cover the 1996-2004 period of obser- vation, and are updated every 2 years. Moreover, the indicators are 'based on several hundred individual variables measuring perceptions of governance drawn from 37 separate data sources constructed by 31 different organizations' (Kaufmann et al., 2005: 6). This implies that these aggregate estimates are informative about changes over time in the relative institutional positions of individual countries. The dynamics of our measure are covered by matching the biennial data of the World Bank to the stated year of investment in our observations. As our observations cover all years in the period 1992-2002, whereas the governance indicators reflect the institutional environment in years 1996, 1998, 2000 and 2002, we added the odd-year observations to the even years to match the institutional estimates (e.g., for investments performed in years 1997 and 1998, we included the host country's institutional advancement as of 1998). Finally, all investments prior to 1996 represent only 8% of our total sample and were imperfectly linked to the institutional indicators for 1996.

Second, Technological intensity is obtained from our primary data. In past studies, technological intensity has often being proxied by the ratio of R&D expenditures to total sales, at either the industry or the firm level (Caves and Mehra, 1986; Hennart and Park, 1993; Cho and Padmanabhan, 1995). As most of our data were collected through a survey, it was believed that respondents would be unlikely to answer ade- quately or at all to questions regarding an estima- tion of the annual sales spent on research and development (R&D). Therefore we asked the respondents to estimate on a Likert scale (1 denoting little amounts, and 5 great amounts)

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1023

how much money as a percentage of annual sales was spent on R&D activities.

Third, International strategy was obtained by asking two sets of multi-scale questions describing multidomestic and global strategies. The questions were adapted from Harzing (2000, 2002), who constructed four statements that measure whether international competition in the industry of invest- ment is predominantly global and focused on achieving economies of scale, or multidomestic and aiming at local differentiation. We performed a cluster analysis, which resulted in a two-cluster grouping of the four constructs as multidomestic and global, and performed an independent-samples t-test to check for significant difference in the mean scores of the two groups. The results are reported in Table 1.

Clearly, the profiles of the multidomestic and global strategies are significantly different, along the lines expected by the theory. The type of international strategy is captured in the regressions by a dummy variable taking the value of 1 if the strategy is predominantly multidomestic, and 0 if it is predominantly global.

Finally, consistent with previous research, we included 11 control variables. Following the method used by Padmanabhan and Cho (1999), we separate international experience into three groups: estab- lishment mode experience, general international experience, and general regional experience. Unlike Padmanabhan and Cho, we replaced their country- specific experience with its region-specific counter- part; the rationale behind this decision was the observation that 50% of all surveyed firms answered negatively to the question whether they had prior investments in any of the CEE countries. Establishment mode experience is captured with

two composite measures (used in the establishment mode analysis), Acquisition experience and Greenfield experience, obtained by asking the respondents to indicate (a) the number of countries worldwide in which their company previously undertook acqui- sition and/or greenfield investments and (b) the number of times acquisitions and/or greenfields were established. For each pair of questions, we performed a factor analysis to ensure that the pair of items obtained for acquisition and greenfield experience converged on one factor (the principal component in the first factor analysis explained 96.85% of the variance and the component in the second 86% of the variance). A similar approach was applied to the other two measures of experi- ence. International experience is a composite measure obtained by asking the respondents to indicate at the time of investment (a) for how many years and (b) in how many countries worldwide (and outside home country) the parent firm made investments. Regional experience is a composite measure con- structed by asking the respondents to indicate the number of countries and the number of years they have been doing business in CEE, not limited to FDI operations. Establishment mode experience is used in the models testing the choice of a greenfield or an acquisition foreign establishment, while inter- national and regional experience are included in the models testing the choice of wholly owned vs shared ownership foreign entry.

The arguments leading to the introduction of both Host-market concentration and Host-market growth as controls are derived from TCE logic. A greenfield establishment increases local supply, which often reduces prices and may provoke a competitive response from the incumbents if the industry in question is growing slowly (Hennart

Table 1 Cluster analysis of strategy variables (scaled from 1 to 5)

Cluster names Economies of scale Global competition Domestic competition Differentiation (product adaptation)

Global 3.08 3.78 2.01 2.67 Multidomestic 2.63 2.05 4.12 3.92 t-value 2.497 10.525 -1 6.231 -7.809

(0.013) (0.000) (0.000) (0.000)

Items (Scale: Strongly disagree 1 2 3 4 5 Strongly agree). (a) Our company's worldwide strategy was focused on achieving economies of scale by concentrating its important activities at a limited number of locations. (b) Our company's competitive position was defined in worldwide terms. Different national product markets were closely linked and interconnected. Competition took place on a global basis. (c) Our company's worldwide competitive strategy was to let each subsidiary compete on a domestic level as national product markets were judged too different to make competition on a global level possible. (d) Our company not only recognised national differences in taste and values, but also actually tried to respond to these national differences by consciously adapting products and policies to the local market.

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1024

and Park, 1993). If an industry is growing rapidly, the supply increasing features of greenfields impose less threat of curbing incumbents' profits. In addition, a large number of entry mode studies found that if the host market has a high potential for growth, a firm benefits more if it has full ownership of its subsidiary in that country (e.g., Caves and Mehra, 1986; Davidson and McFetridge, 1985). Furthermore, higher market concentration will positively affect the likelihood of acquisition establishments, while rapid market growth is likely to attract more greenfields. In the context of entry- mode literature, high levels of industry concentra- tion lead to the establishment of jointly owned subsidiaries (Hennart and Larimo, 1998). Therefore we asked the respondents to evaluate, on a five- point Likert-type scale, the intensity of local competition (market concentration) and expected host market's growth at the time of their invest- ment in CEE. Previous studies provide evidence that MNEs expanding into new industries prefer to establish acquisitions, as this allows them to obtain the tacit product-specific knowledge they need to operate successfully in the new industry (Hennart and Park, 1993; Caves, 1996). Furthermore, to mitigate the need for new knowledge and assets, an entry into an unrelated industry is expected to utilise the option of shared ownership to a greater extent than a non-diversifying entry (Gomes- Casseres, 1989; Hennart, 1991). We therefore measure Investment relatedness by asking respon- dents to answer two five-point Likert-type ques- tions on how related the investment was in terms of both the product line and the line of business respectively. We created a dummy variable to control for an investment in a Production subsidiary because we believe that the decision to invest in a production rather than a sales outlet is more costly, which might influence the choice of an acquisition vs a greenfield mode, and full vs shared ownership mode.

We control for the presence of Investment incen- tives by creating a dummy variable with a value of 1 if at the time of investment there were any incentives by the host-country government that might have influenced the type of investment in any way, and 0 if that was not the case. The variable Relative size of the investment represents the relative size of the foreign operation, which was measured by dividing the initial number of employ- ees of the subsidiary by the number of employees worldwide. Previous studies found a positive effect of this variable on the likelihood of an acquisition

(Caves and Mehra, 1986; Kogut and Singh, 1988; Cho and Padmanabhan, 1995). Firms attempting to create a large greenfield venture (relative to firm size) may experience a shortage of financial and/or managerial resources (Hennart and Park, 1993), implying that a relatively large investment is more likely to be utilised as an acquisition (Brouthers and Brouthers, 2000). Literature on entry mode choice considers relative size of great importance as well: 'if investment is large relative to the parent firm, the parent is less likely to possess all the assets required to entry' (Delios and Beamish, 1999: 923). Consequently, the larger the relative size of the investment, the greater the need for a partner with complementary assets (Hennart, 1991). Advertising intensity is another control variable, as Meyer (2001) found that management skills in the central planning system were fundamentally different, implying that the transfer of knowledge in areas such as marketing, accounting, finance and mod- ern leadership skills is of primary importance. In addition, Kim and Hwang (1992) and Erramilli and Rao (1993) observed a positive relationship between advertising intensity and the level of ownership. We asked the respondents to estimate on a Likert scale (1 denoting little amounts, and 5 great amounts) how much money as a percentage of annual sales is spent on marketing activities. In addition, we asked the respondents to specify the industry of investment. By using the Amadeus database we subsequently determined the MNE's ISIC codes (the European version of the US SIC codes). Subsequently, by implementing the OECD Manufacturing Industry Classification, which ranks manufacturing industries according to industry- level expenditures on R&D (available upon request), we created three dummy variables - High-technology, Low-technology (both manufactur- ing) and Non-manufacturing industry - as a robust- ness check of our primary technological intensity variable.4

Data analysis To explore the influence of the independent and control variables on the likelihood of either a (fully or partially owned) acquisition or greenfield invest- ment, we conducted a binomial logistic regression analysis. This statistical method was applied because of the ability of logistic regression techni- ques to incorporate a wide range of diagnostics, the dichotomous characteristic of the dependent, and the mix of continuous and categorical independent variables we use (Hair et al., 1995). Since our data

journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1025

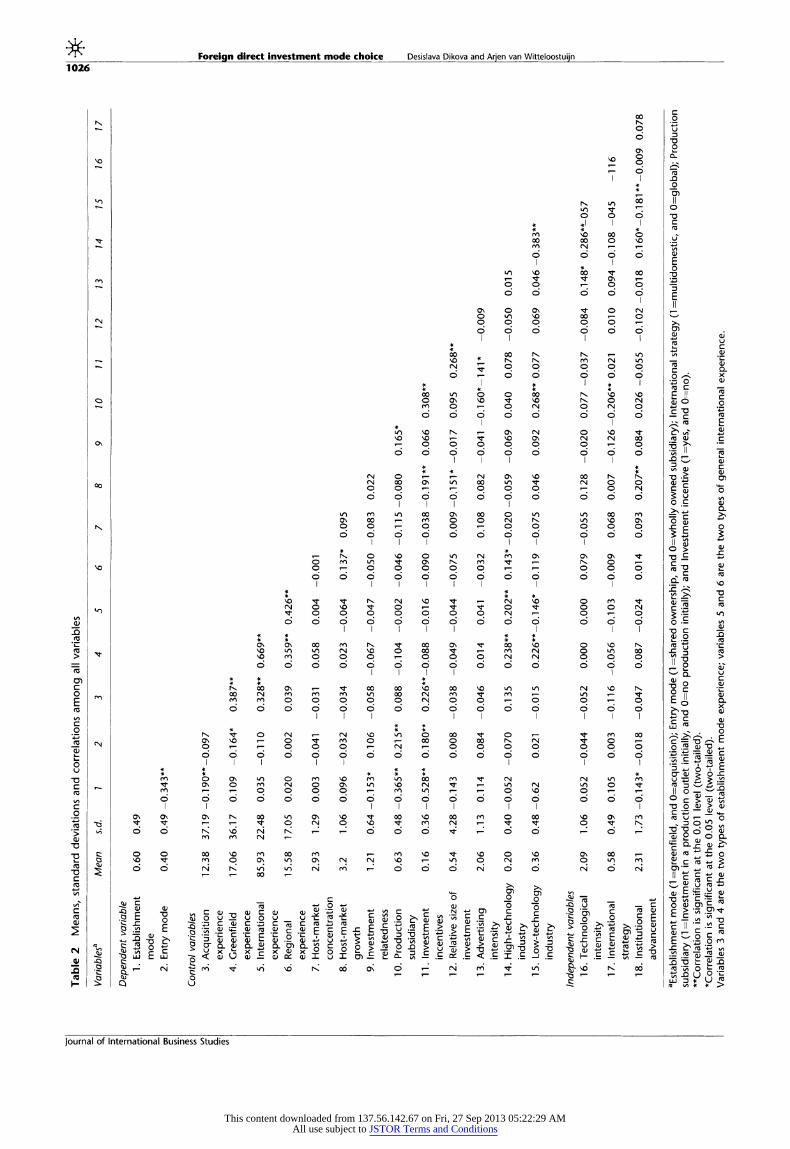

set is composed of continuous, categorical, single- scale and multiple-scale constructs, all variables were converted to standardised z-scores, prior to the analysis. Before performing the moderations of the institutional variable with a number of independent variables, all predictors were centred to avoid potential multicollinearity problems. Table 2 shows the means, standard deviations and correlation coefficients for all variables under study.

In the binomial logistic regression specification that we employed, the regression coefficients estimate the impact of the independent (or control) variable on the probability that the establishment mode is of the acquisition type (which carries the value of 1). The model can expressed as

1 P(Y) -P (1) 1 + e-

where Y is the dependent variable, and Z is the linear combination of the independent and control variables. That is,

Z = fo + PflXl + #2X2 + '-' - nXn (2)

where f is the intercept, fp ... fn, are the regression coefficients, and X1 ... Xn denote the independent and control variables.

We conducted the analysis by creating six models. Model 1 estimates the main effects of our predictor variables on the likelihood of a greenfield type of entry, and Models 2 and 3 add the moderating effects of institutional advancement on the effect of the MNEs' technological intensity and international strategy. Model 4 estimates the main effects of our predictor variables on the likelihood of an entry mode via subsidiary with shared ownership, and Model 5 and 6 add the moderating effects of institutional advancement on the impact of the MNE's technological intensity and international strategy. The models are esti- mated with SPSS 12.0.1, using the maximum-like- lihood method. Before presenting the evidence, two further methodological remarks are worth making.

First, we did some tests with regard to our two interaction terms. For one, we split the sample into two groups - a subsample for MNEs with a global strategy and a subsample for MNEs with a multi- domestic strategy. We then performed logistic regression analysis for both subsamples (without interactions) and compared the results of the Wald chi-square statistics to test for differences between

covariates' coefficients for global and multidomes- tic strategy. Following the approach of Allison (1999), we use the formula

(bg - bm)2

[s.e.(bg)]2 + [s.e.(bm)]2

where bg is the coefficient for global strategy, bm is the coefficient for multidomestic strategy, and s.e. is the estimated standard error. Each statistic has one degree of freedom. Despite the fact that this is a very conservative test, owing to a low number of observations in each subsample (less than 100), the coefficients of both independent variables, Techno- logical intensity and Institutional advancement, are significantly different at the 0.1 level.5 The differ- ence suggests that Institutional advancement and Technological intensity influence the establishment of greenfields differently for global and multi- domestic firms. Hence the subsamples should not be pooled. The test concerning the entry mode model produced weaker results - both Technological intensity and Institutional advancement are borderline significantly different at the 0.1 level.6 In addition, we performed a test to determine the probability of greenfield establishment and shared ownership entry, when all covariates except international strategy are at the average. This test reveals that when all independent and control variables are at their respective averages, and the international strategy is global, the probability of a greenfield establishment is 81%. The probability of a green- field investment is 50% when all independent and control variables are at their respective averages and the international strategy is multi- domestic. The difference in probability is quite substantial, so we conclude that eliminating the International Strategy variable is not desirable. The test for entry mode is less conclusive: the prob- ability of shared ownership entry is 80% when all independent and control variables are at their respective averages and international strategy is global, and the probability of shared ownership is 70% when international strategy is multidomestic. In all, we may conclude that including our two interaction terms in our regression analyses is methodologically sound.

Second, the null hypothesis that all coefficients

(fs) except 13o are zero was tested with the model chi-square statistical test. We were able to reject the null hypothesis, and could conclude that our set of independent variables improved the prediction of the probability of acquisition occurrence, because

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1027

in every tested model the (overall) model chi- square significance was high (P=0.0001) and all models demonstrated high predictability (reported as model's sensitivity, specificity and overall per- centage of predictability).

Results The results are reported in Tables 3 and 4.

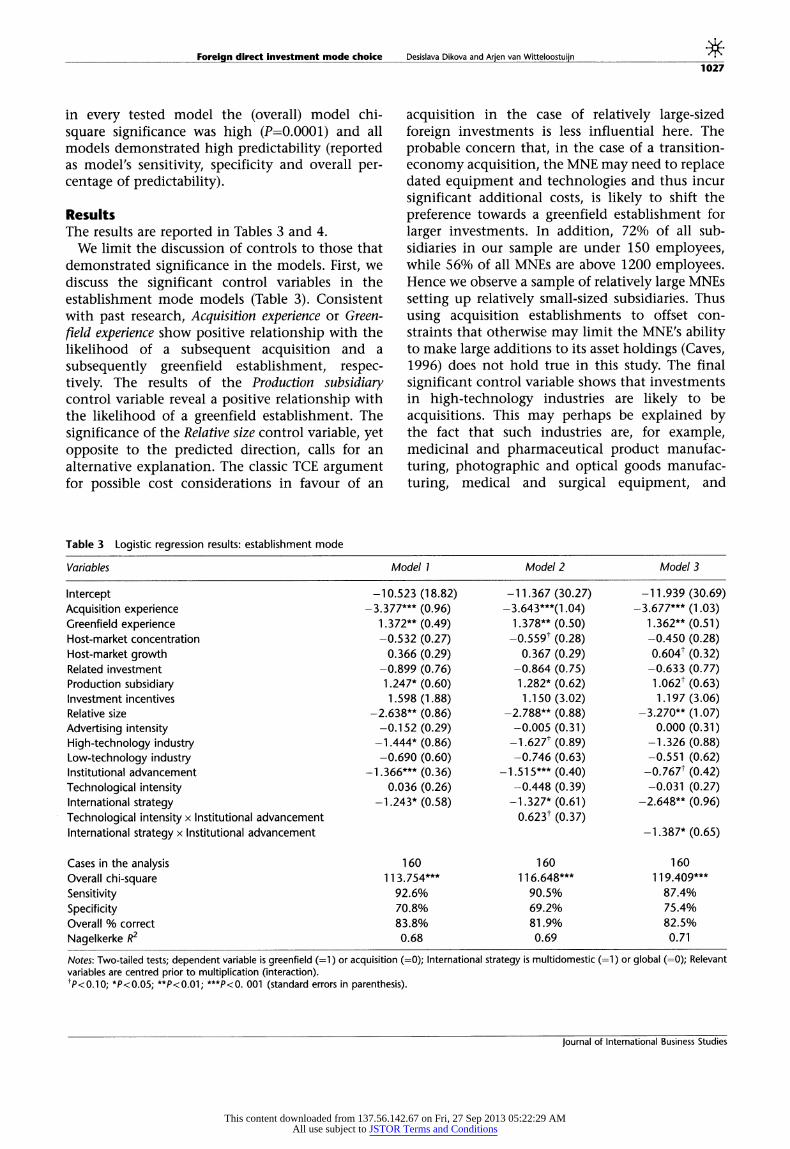

We limit the discussion of controls to those that demonstrated significance in the models. First, we discuss the significant control variables in the establishment mode models (Table 3). Consistent with past research, Acquisition experience or Green- field experience show positive relationship with the likelihood of a subsequent acquisition and a subsequently greenfield establishment, respec- tively. The results of the Production subsidiary control variable reveal a positive relationship with the likelihood of a greenfield establishment. The significance of the Relative size control variable, yet opposite to the predicted direction, calls for an alternative explanation. The classic TCE argument for possible cost considerations in favour of an

acquisition in the case of relatively large-sized foreign investments is less influential here. The probable concern that, in the case of a transition- economy acquisition, the MNE may need to replace dated equipment and technologies and thus incur significant additional costs, is likely to shift the preference towards a greenfield establishment for larger investments. In addition, 72% of all sub- sidiaries in our sample are under 150 employees, while 56% of all MNEs are above 1200 employees. Hence we observe a sample of relatively large MNEs setting up relatively small-sized subsidiaries. Thus using acquisition establishments to offset con- straints that otherwise may limit the MNE's ability to make large additions to its asset holdings (Caves, 1996) does not hold true in this study. The final significant control variable shows that investments in high-technology industries are likely to be acquisitions. This may perhaps be explained by the fact that such industries are, for example, medicinal and pharmaceutical product manufac- turing, photographic and optical goods manufac- turing, medical and surgical equipment, and

Table 3 Logistic regression results: establishment mode

Variables Model 1 Model 2 Model 3

Intercept -10.523 (18.82) -11.367 (30.27) -11.939 (30.69) Acquisition experience -3.377*** (0.96) -3.643***(1.04) -3.677*** (1.03) Greenfield experience 1.372** (0.49) 1.378** (0.50) 1.362** (0.51) Host-market concentration -0.532 (0.27) -0.559t (0.28) -0.450 (0.28) Host-market growth 0.366 (0.29) 0.367 (0.29) 0.6041 (0.32) Related investment -0.899 (0.76) -0.864 (0.75) -0.633 (0.77) Production subsidiary 1.247* (0.60) 1.282* (0.62) 1.062t (0.63) Investment incentives 1.598 (1.88) 1.150 (3.02) 1.197 (3.06) Relative size -2.638** (0.86) -2.788** (0.88) -3.270** (1.07) Advertising intensity -0.152 (0.29) -0.005 (0.31) 0.000 (0.31) High-technology industry -1.444* (0.86) -1.627t (0.89) -1.326 (0.88) Low-technology industry -0.690 (0.60) -0.746 (0.63) -0.551 (0.62) Institutional advancement -1.366*** (0.36) -1.515*** (0.40) -0.767t (0.42) Technological intensity 0.036 (0.26) -0.448 (0.39) -0.031 (0.27) International strategy -1.243* (0.58) -1.327* (0.61) -2.648** (0.96) Technological intensity x Institutional advancement 0.623t (0.37) International strategy x Institutional advancement -1.387* (0.65)

Cases in the analysis 160 160 160 Overall chi-square 113.754*** 116.648*** 119.409***

Sensitivity 92.6% 90.5% 87.4%

Specificity 70.8% 69.2% 75.4% Overall % correct 83.8% 81.9% 82.5%

Nagelkerke R2 0.68 0.69 0.71

Notes: Two-tailed tests; dependent variable is greenfield (=1) or acquisition (=0); International strategy is multidomestic (=1) or global (=0); Relevant variables are centred prior to multiplication (interaction). tP<0.10; *P<0.05; **P<0.01; ***P<0. 001 (standard errors in parenthesis).

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

SForeign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1028

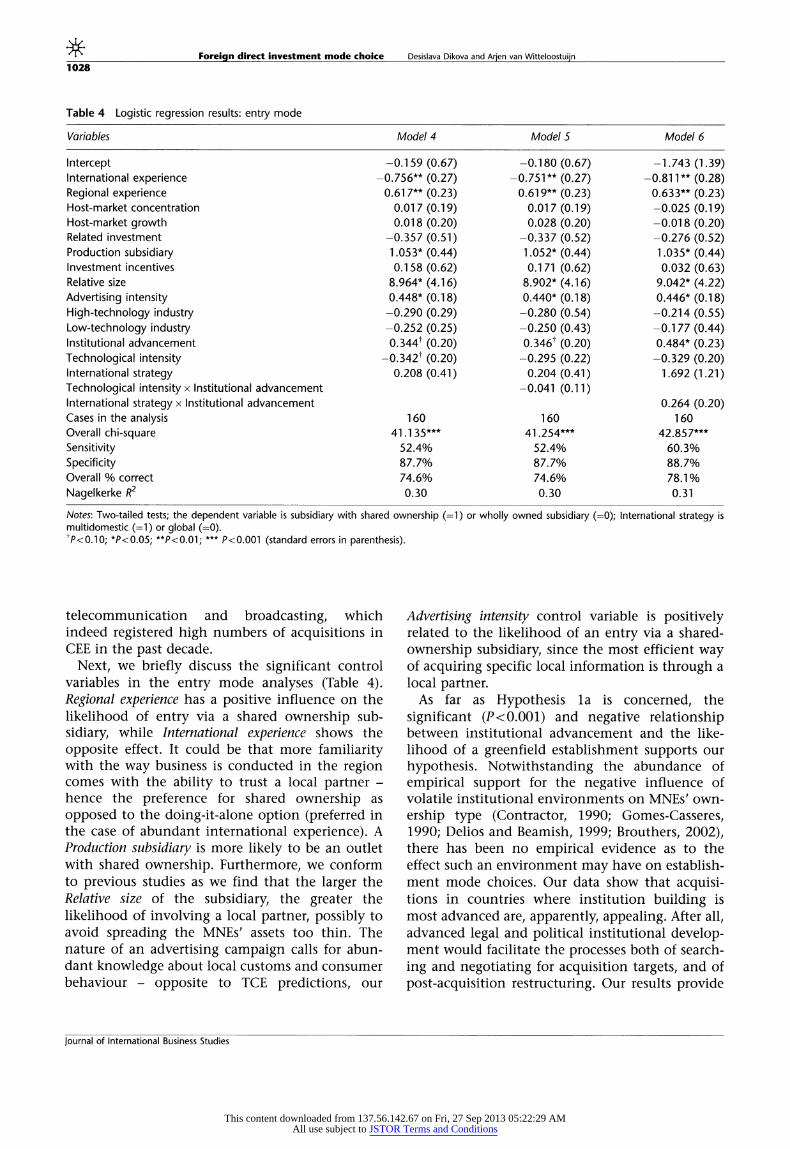

Table 4 Logistic regression results: entry mode

Variables Model 4 Model 5 Model 6

Intercept -0.159 (0.67) -0.180 (0.67) -1.743 (1.39) International experience -0.756** (0.27) -0.751** (0.27) -0.811** (0.28) Regional experience 0.617** (0.23) 0.619** (0.23) 0.633** (0.23) Host-market concentration 0.017 (0.19) 0.017 (0.19) -0.025 (0.19) Host-market growth 0.018 (0.20) 0.028 (0.20) -0.018 (0.20) Related investment -0.357 (0.51) -0.337 (0.52) -0.276 (0.52) Production subsidiary 1.053* (0.44) 1.052* (0.44) 1.035* (0.44) Investment incentives 0.158 (0.62) 0.171 (0.62) 0.032 (0.63) Relative size 8.964* (4.16) 8.902* (4.16) 9.042* (4.22) Advertising intensity 0.448* (0.18) 0.440* (0.18) 0.446* (0.18) High-technology industry -0.290 (0.29) -0.280 (0.54) -0.214 (0.55) Low-technology industry -0.252 (0.25) -0.250 (0.43) -0.177 (0.44) Institutional advancement 0.3441 (0.20) 0.346t (0.20) 0.484* (0.23) Technological intensity -0.342t (0.20) -0.295 (0.22) -0.329 (0.20) International strategy 0.208 (0.41) 0.204 (0.41) 1.692 (1.21) Technological intensity x Institutional advancement -0.041 (0.11) International strategy x Institutional advancement 0.264 (0.20) Cases in the analysis 160 160 160 Overall chi-square 41.135*** 41.254*** 42.857*** Sensitivity 52.4% 52.4% 60.3% Specificity 87.7% 87.7% 88.7% Overall % correct 74.6% 74.6% 78.1%

Nagelkerke R2 0.30 0.30 0.31

Notes: Two-tailed tests; the dependent variable is subsidiary with shared ownership (=1) or wholly owned subsidiary (=0); International strategy is multidomestic (=1) or global (=0). tp<0.10; *P<0.05; **P<0.01; *** P<0.001 (standard errors in parenthesis).

telecommunication and broadcasting, which indeed registered high numbers of acquisitions in CEE in the past decade.

Next, we briefly discuss the significant control variables in the entry mode analyses (Table 4). Regional experience has a positive influence on the likelihood of entry via a shared ownership sub- sidiary, while International experience shows the opposite effect. It could be that more familiarity with the way business is conducted in the region comes with the ability to trust a local partner - hence the preference for shared ownership as opposed to the doing-it-alone option (preferred in the case of abundant international experience). A Production subsidiary is more likely to be an outlet with shared ownership. Furthermore, we conform to previous studies as we find that the larger the Relative size of the subsidiary, the greater the likelihood of involving a local partner, possibly to avoid spreading the MNEs' assets too thin. The nature of an advertising campaign calls for abun- dant knowledge about local customs and consumer behaviour - opposite to TCE predictions, our

Advertising intensity control variable is positively related to the likelihood of an entry via a shared- ownership subsidiary, since the most efficient way of acquiring specific local information is through a local partner.

As far as Hypothesis la is concerned, the significant (P<0.001) and negative relationship between institutional advancement and the like- lihood of a greenfield establishment supports our hypothesis. Notwithstanding the abundance of empirical support for the negative influence of volatile institutional environments on MNEs' own- ership type (Contractor, 1990; Gomes-Casseres, 1990; Delios and Beamish, 1999; Brouthers, 2002), there has been no empirical evidence as to the effect such an environment may have on establish- ment mode choices. Our data show that acquisi- tions in countries where institution building is most advanced are, apparently, appealing. After all, advanced legal and political institutional develop- ment would facilitate the processes both of search- ing and negotiating for acquisition targets, and of post-acquisition restructuring. Our results provide

journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and Arjen van Witteloostuijn 1029

support for one of the propositions posited earlier that an acquisition establishment is less risky than the greenfield alternative, as it provides a lower but more certain expected rate of return, albeit only within an environment with established institutional safeguards. The significant (P<0.1) and positive relationship between institutional advancement and the second dependent variable, namely the likelihood of shared ownership, pro- vides moderate support for our Hypothesis lb. The results are in line with earlier arguments that, in institutional environments with sufficient institu- tional protection of investors' proprietary assets, the need for costly governance structures is lower, so that alternative (to full ownership) ownership modes are likely to be chosen by MNEs.

We find moderate support for Hypothesis 2a, as the moderating effect of institutional advancement on technological intensity is marginally significant (P<0.1) with the predicted sign - greater institu- tional advancement positively influences the ten- dency of technologically intensive MNEs to establish greenfield operations. The main effect of the Technological intensity variable is insignificant. We therefore fail to find any support in our CEE setting for the traditional TCE prediction that technologically intensive firms typically establish greenfields. However, our observations show that advanced institutional development in terms of intellectual property protection and improved market conditions for complementary resources has a positive influence on the likelihood of technologically intensive investors establishing greenfield subsidiaries. Our results provide no support for our Hypothesis 2b owing to the insignificant interaction effect of Technological intensity and Institutional advancement.

The regression results support Hypothesis 3a: the coefficient of the interaction effect of International strategy and Institutional advancement is significant (P<0.05) and has the hypothesised sign, demon- strating that greater institutional advancement positively affects the likelihood that multidomestic MNEs will launch acquisitions in CEE. The main effect of the International strategy variable is also in the expected direction. This suggests that MNEs following a predominantly multidomestic strategy prefer the acquisition establishment mode, whereas MNEs with a global strategy opt for a greenfield investments. However, an advanced institutional environment facilitates the process of acquiring and integrating local firms, and thus positively affects the established relationship between multi-

domestic firms and acquisition establishments. Unfortunately, our International strategy predictor is insignificant in the entry mode choice analysis, so we cannot conclude that MNEs adhering to a predominantly multidomestic strategy tend to opt for subsidiaries with shared ownership. The inter- action of International strategy and Institutional advancement is also insignificant. Hence no support is provided for Hypothesis 3b.

Conclusion We provided answers to three main research questions in this study. Regarding the first one, we found that within the domain of TCE there are certain firm-level factors that influence both the decision to establish a greenfield or an acquisition, and the choice between full or shared ownership. Our results reveal that MNEs' technological inten- sity and international strategy are influential in the complex foreign investment decision concerning establishment and entry modes. Within the realm of our second research question, we demonstrated that indeed NIE is an appropriate theoretical framework to examine foreign direct investment activities in transition economies, as this approach accounts for the influence of institutional develop- ment on investment decisions. We provide empiri- cal support for the argument that investment decisions, typically explained by TCE in the extant literature, are indeed influenced by institutions. A revealing example is the classic TCE argument that greenfield subsidiaries are riskier establishments than acquisitions. According to the empirical evidence provided in this study, acquisitions are desirable only if the institutional environment is fairly advanced. In addition, in the context of entry mode decisions, institutional advancement in transition economies prompts investors to trade costly governance structures of full subsidiary ownership for local partnerships. Therefore, to present a broader perspective on business activities, researchers need to extend leading theoretical perspectives, such as TCE, by integrating North's insights about the central role of the institutional environment in facilitating (or constraining) firms' behaviour. Furthermore, not accounting for earlier deficiencies in the legal and judicial system in transition economies or the subsequent develop- ments of the institutional environment would

clearly lead to a distorted view of reality, and an underestimation of the obstacles imposed on busi- ness activities in transition economies.

Journal of International Business Studies

This content downloaded from 137.56.142.67 on Fri, 27 Sep 2013 05:22:29 AMAll use subject to JSTOR Terms and Conditions

Foreign direct investment mode choice Desislava Dikova and n vand Aren van

Witteloostuijn 1030