State Laws Deprive Homeowners of Basic Protections John Rao and Geoff Walsh NATIONAL CONSUMER LAW CENTER INC ® —————————————— ▲ February 2009 FORECLOSING A DREAM

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

State Laws Deprive Homeowners of Basic Protections

John Rao and Geoff Walsh

NATIONALCONSUM ER LAW

CENTER INC®

——————————————▲

February 2009

FORECLOSINGA DREAM

ACKNOWLEDGMENTS

The authors would like to thank Carolyn Carter,Elizabeth Renuart, Margot Saunders, Eric Secoy,and Tara Twomey of NCLC for valuable guid-ance, feedback, and editorial assistance in the preparation of this report. Particular thanksto Rick Jurgens, Mary Kingsley, and ShirlronWilliams for research and to Julie Gallagher forgraphic design.

This report was funded in part by the FordFoundation. We thank them for their supportbut acknowledge that the findings and conclu-sions presented in this report are those of the au-thors alone, and do not necessarily reflect theopinions of the Foundation.

ABOUT THE NATIONAL CONSUMER LAW CENTER

The National Consumer Law Center®, a nonprofitcorporation founded in 1969, assists consumers,advocates, and public policy makers nationwideon consumer law issues. NCLC works toward thegoal of consumer justice and fair treatment, par-ticularly for those whose poverty renders thempowerless to demand accountability from theeconomic marketplace. NCLC has providedmodel language and testimony on numerousconsumer law issues before federal and state pol-icy makers. NCLC publishes an 18-volume seriesof treatises on consumer law, and a number ofpublications for consumers.

ABOUT THE AUTHORS

John Rao is an attorney with the National Con-sumer Law Center, Inc. who focuses on consumercredit and bankruptcy issues. He is a contribut-ing author and editor of NCLC’s Consumer Bank-ruptcy Law and Practice; co-author of NCLC’sForeclosures; Bankruptcy Basics; Guide to SurvivingDebt; and contributing author to NCLC’s StudentLoan Law. He is also a contributing author to Col-lier on Bankruptcy and the Collier Bankruptcy Prac-tice Guide. He serves as a member of the federalJudicial Conference Advisory Committee onBankruptcy Rules, appointed by Chief JusticeJohn Roberts in 2006. He is a Fellow of the Amer-ican College of Bankruptcy, secretary for the Na-tional Association of Consumer BankruptcyAttorneys, and former board member for theAmerican Bankruptcy Institute.

Geoff Walsh has been a legal services attorneyfor over twenty-five years and is presently a staffattorney with National Consumer Law Center inBoston. Before that, he worked with the housingand consumer units of Community Legal Serv-ices in Philadelphia and was a staff attorney withVermont Legal Aid in its Springfield, Vermont of-fice. His practice has focused upon housing andbankruptcy issues, particularly foreclosures ofmortgages in government-subsidized housingprograms. He is a contributing author to NCLC’sForeclosures.

I. Executive Summary

In recent months, a wave of foreclosures hasswept millions of American families from theirhomes. The magnitude of this crisis defies easycomprehension: more than 8 million Americanfamilies are expected to lose their homes to fore-closure in the next four years. Much has beenwritten about the financial and economic causesof this disaster. Much less notice has gone to an-other factor that has accelerated and multipliedthis grave loss of homes and savings: antiquatedstate laws that in some ways afford fewer protec-tions to homeowners than to renters.

State foreclosure laws tilted against homeownersThis report examines the laws that govern mort-gage foreclosures in the 50 states, and evaluateshow well the laws of a given state protect home-owners facing foreclosure. Regulation of mort-gage foreclosures has always been a fundamentalprovince of state laws. Now, as families, commu-nities and states face an onslaught of financialand social problems caused by the rising tide offoreclosures, states need to craft laws that canmaximize the number of their residents who willbe able to keep their homes.

Provisions in existing foreclosure laws thathurt homeowners include:

� In 30 states and the District of Columbia,mortgage holders who allege that homeownershave fallen behind in their payments can by-pass the courts and move directly to takeaway and auction off homes. This denies

homeowners due process protection com -parable to that given many tenants. It alsoplaces upon homeowners the heavy burden toget a judge to review the mortgage holder’sclaims and stop the foreclosure.

� In every state but California and Connecticut,mortgage holders can move directly to fore -closure without being required by state lawto consider or discuss ways to avoid loss ofthe home with homeowners, such as throughmodification of the terms of the loan.

� In every state but Massachusetts, New Jersey,and Pennsylvania, a mortgage holder whoclaims a homeowner has fallen behind in payments can immediately impose defaultfees and costs that reduce the chances thatthe homeowner can catch up by making thepayments owed.

� In 29 states, a mortgage holder has no obli-gation under state law to stop foreclosureeven if the homeowner, just before the househas been sold, comes up with the money tocatch up on the owed payments and all in-curred penalties and fees.

� In 33 states and the District of Columbia,there is no requirement that homeownersbe personally served with a foreclosure no-tice or legal documents that start a court fore-closure case.

� In 36 states and the District of Columbia,mortgage holders can pursue so-called “defi-ciency judgment” claims against homeown-ers even after the foreclosed home has beensold at auction. These claims, seeking to re-

FORECLOSING A DREAMState Laws Deprive Homeowners

of Basic Protections

cover the difference between the amount owedon the loan and the amount collected fromthe foreclosure auction, can be pursued with-out conditions in 15 states and the District ofColumbia, and only under certain conditionsin the other 21 states.

States can and must do more to allow familiesto avoid foreclosure and preserve their homesand the wealth and savings embodied in them.By adopting the recommendations set out in thisreport states can level a playing field now tilted infavor of mortgage holders.

RecommendationsAction is urgently needed in these key areas toprotect homeowners and restore basic fairness tothe foreclosure process.

� Mandate judicial supervision over fore-closures of all residential mortgages.Many states now allow mortgage holders tobypass the courts and use non-judicial proce-dures to take away homes from their owners.These procedures create enormous barriers forhomeowners who want to assert legal claimsand raise defenses against lenders, servicers,and mortgage holders. States should eithercompletely abandon the power of sale methodand require judicial foreclosure, or they shouldincorporate essential due process protectionsinto the existing non-judicial procedure.

� Require mortgage holders to considerloss mitigation, including loan modifica-tion and other workout alternatives, as acondition to allowing the foreclosure of a home. States have broad authority to setconditions upon a mortgage holder’s right toforeclose. For example, states have always hadthe authority to require mediation in certaincategories of disputes, and they can require mediation in home foreclosure cases. Several

states, local governments and courts have al-ready taken steps to implement these types ofmediation systems. States should require thatbefore a foreclosure may proceed, the mort-gage holder must prove that it or its servicerexplored all reasonable options to avoid foreclosure with the homeowner before theforeclosure was initiated. Mortgage holderswho do not comply in good faith with thesemediation procedures should not be permit-ted to use public officials, records, and servicesto enforce their claims.

� Require that homeowners be given aright to cure a default by catching up onmissed payments, without penalty, atleast 60 days before a mortgage holderdemands immediate full payment of theentire mortgage balance and before be-ginning any foreclosure proceeding.Homeowners should be sent a notice thatclearly informs them that before the end ofthe designated time period, they can stop theforeclosure by paying up the installments theyare behind without payment of any default-related costs or fees.

� Guarantee homeowners the right to re -instate the mortgage by paying the arrearage and costs up to the time of aforeclosure sale. Nearly half of the stateshave enacted statutes that provide for thisright to reinstate after the mortgage holder demands payment of the entire loan balance(acceleration). Such laws are cost neutral forthe mortgage holder because borrowers typi-cally pay all reasonable foreclosure costs in-curred up to the time of reinstatement. Statelaw should mandate a form of notice tohomeowners that provides detailed informa-tion about the foreclosure process and stepsthe homeowner can take to avoid foreclosure, including the right of reinstatement and loanmodification options.

4 FORECLOSING A DREAM

FORECLOSING A DREAM 5

� Require that homeowners be personallyserved with the notice of sale or foreclo-sure complaint. State laws should requirethat no matter which type of foreclosure proceeding is permitted, the mortgage holdermust provide proof of personal service of thelegal documents which both commence theforeclosure proceeding and schedule the sale,or the mortgage holder must document re-peated good faith attempts to make personalservice on the homeowners.

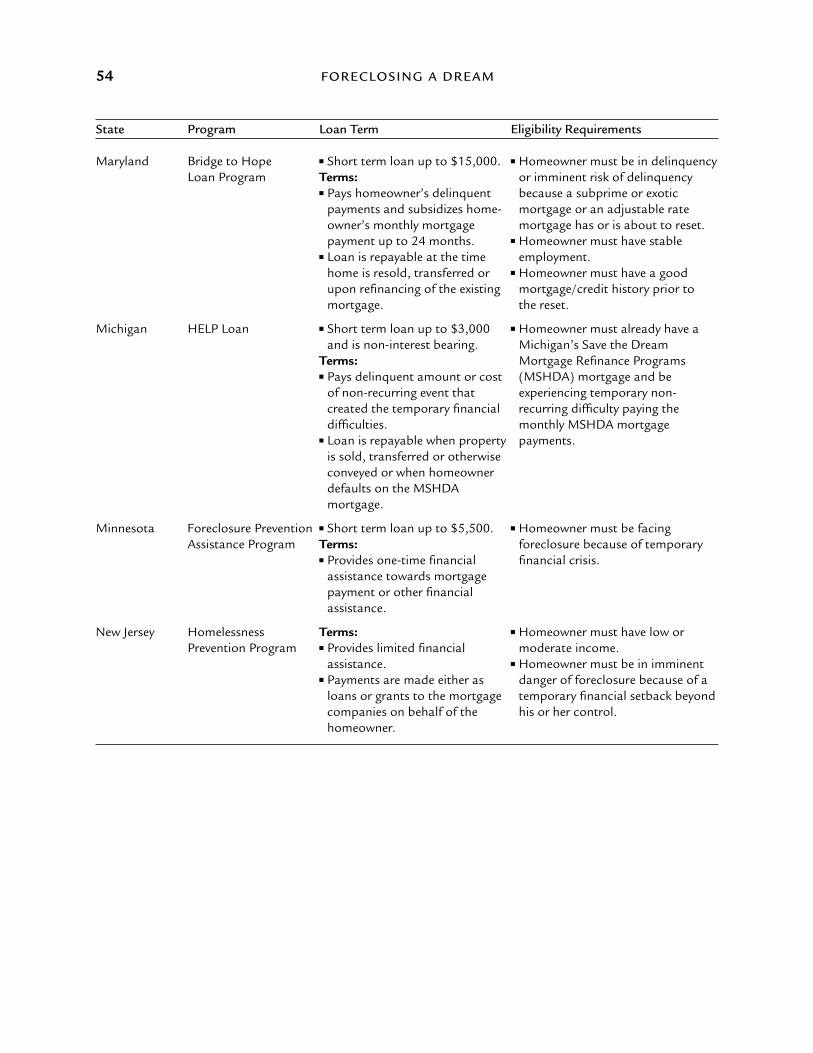

� Create and adequately fund programsthat provide emergency financial assis-tance to homeowners facing foreclosure.At least eight states already have statewideprograms offering such assistance to home-owners experiencing temporary financial diffi-culties such as loss of employment, illness,disability, death, divorce or legal separation.As the foreclosure crisis deepens and broadereconomic problems cause the unemploymentrate to increase, more states should considerdeveloping programs that 1) assist home-owners with monthly mortgage payments fora period of 12 to 24 months; 2) provide interest-free or below market rate loans to be repaidwhen the home is sold, transferred, or refi-nanced; and 3) are designed as revolvingfunds, with amounts replenished by loan repayment.

� Provide homeowners with a statutoryright to redeem and reacquire title totheir home, for a fixed period of timeafter a foreclosure sale. “Redemption”after a foreclosure sale allows a homeowner afixed period of time in which to set the fore-closure sale aside and regain title to the homeby paying the sale price, interest and costs ofthe sale. The payment compensates the mort-gage holder or other purchaser for their finan-cial outlay. Approximately half of the states

have a law on the books allowing such post-sale redemptions. However, in a number ofstates the right to redeem is limited to certaintypes of foreclosures and applies only for cer-tain outcomes of the sale. The right to redeemafter sale should uniformly apply to all resi-dential mortgage foreclosures.

� Prohibit mortgage holders from pursuinghomeowners for deficiency judgmentsafter foreclosures. Deficiency judgmentscan drive former homeowners into bank-ruptcy or burden them with an insurmount-able debt obligation. Deficiency judgmentscan also create an unfair windfall for mort-gage holders and reward them when their lackof marketing and publicity leads to a fore -closure sale at a winning bid far below marketvalue. Ten states bar deficiency judgmentsafter residential foreclosures and 21 otherstates substantially limit deficiencies by re-quiring lenders to calculate deficiencies withmeasures such as the property’s fair marketvalue rather than the artificially low foreclo-sure sale price. All states should simply enactoutright bars on deficiency judgments afterhome foreclosures.

� Require judicial supervision over the ac-counting of foreclosure sale proceeds anda prompt release of any surplus to theborrowers. In many states, the accountingof sale proceeds and the distribution of anysurplus left after payment of the mortgagedebt are handled almost entirely by the mort-gage holder or a private trustee, without anyexplicit procedures or formal court review.States should require that the proposed dis -tribution of sale proceeds be reviewed and approved by a neutral public official and thatany surplus funds be disbursed promptly tothe borrower.

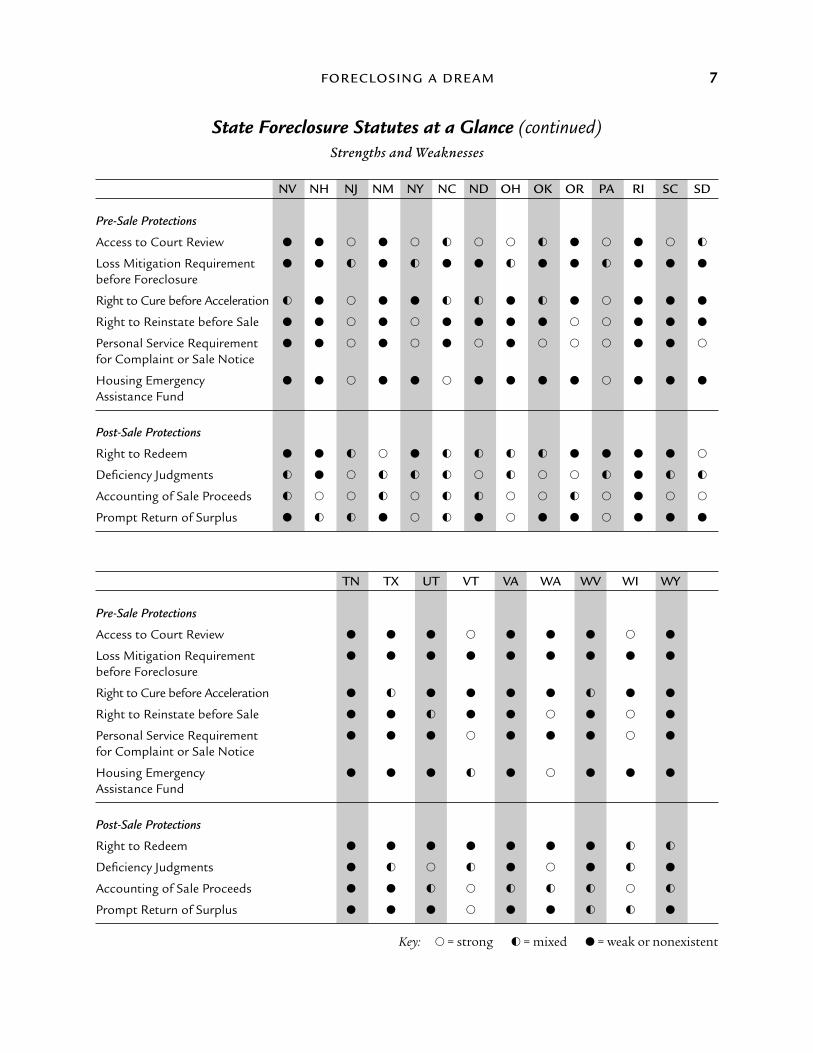

State Foreclosure Statutes at a GlanceStrengths and Weaknesses

AL AK AZ AR CA CO CT DE DC FL GA HI ID IL

Pre-Sale Protections

Access to Court Review � � � � � � � � � � � � � �

Loss Mitigation Requirement � � � � � � � � � � � � � �

before Foreclosure

Right to Cure before Acceleration � � � � � � � � � � � � � �

Right to Reinstate before Sale � � � � � � � � � � � � � �

Personal Service Requirement � � � � � � � � � � � � � �

for Complaint or Sale Notice

Housing Emergency � � � � � � � � � � � � � �

Assistance Fund

Post-Sale Protections

Right to Redeem � � � � � � � � � � � � � �

Deficiency Judgments � � � � � � � � � � � � � �

Accounting of Sale Proceeds � � � � � � � � � � � � � �

Prompt Return of Surplus � � � � � � � � � � � � � �

IN IA KS KY LA ME MD MA MI MN MS MO MT NE

Pre-Sale Protections

Access to Court Review � � � � � � � � � � � � � �

Loss Mitigation Requirement � � � � � � � � � � � � � �

before Foreclosure

Right to Cure before Acceleration � � � � � � � � � � � � � �

Right to Reinstate before Sale � � � � � � � � � � � � � �

Personal Service Requirement � � � � � � � � � � � � � �

for Complaint or Sale Notice

Housing Emergency � � � � � � � � � � � � � �

Assistance Fund

Post-Sale Protections

Right to Redeem � � � � � � � � � � � � � �

Deficiency Judgments � � � � � � � � � � � � � �

Accounting of Sale Proceeds � � � � � � � � � � � � � �

Prompt Return of Surplus � � � � � � � � � � � � � �

Key: � = strong � = mixed � = weak or nonexistent

6 FORECLOSING A DREAM

FORECLOSING A DREAM 7

State Foreclosure Statutes at a Glance (continued)Strengths and Weaknesses

NV NH NJ NM NY NC ND OH OK OR PA RI SC SD

Pre-Sale Protections

Access to Court Review � � � � � � � � � � � � � �

Loss Mitigation Requirement � � � � � � � � � � � � � �

before Foreclosure

Right to Cure before Acceleration � � � � � � � � � � � � � �

Right to Reinstate before Sale � � � � � � � � � � � � � �

Personal Service Requirement � � � � � � � � � � � � � �

for Complaint or Sale Notice

Housing Emergency � � � � � � � � � � � � � �

Assistance Fund

Post-Sale Protections

Right to Redeem � � � � � � � � � � � � � �

Deficiency Judgments � � � � � � � � � � � � � �

Accounting of Sale Proceeds � � � � � � � � � � � � � �

Prompt Return of Surplus � � � � � � � � � � � � � �

TN TX UT VT VA WA WV WI WY

Pre-Sale Protections

Access to Court Review � � � � � � � � �

Loss Mitigation Requirement � � � � � � � � �

before Foreclosure

Right to Cure before Acceleration � � � � � � � � �

Right to Reinstate before Sale � � � � � � � � �

Personal Service Requirement � � � � � � � � �

for Complaint or Sale Notice

Housing Emergency � � � � � � � � �

Assistance Fund

Post-Sale Protections

Right to Redeem � � � � � � � � �

Deficiency Judgments � � � � � � � � �

Accounting of Sale Proceeds � � � � � � � � �

Prompt Return of Surplus � � � � � � � � �

Key: � = strong � = mixed � = weak or nonexistent

8 FORECLOSING A DREAM

II. Scope of the Foreclosure Crisis

We are facing the greatest foreclosure crisis sincethe Great Depression. The statistics are grim. For2008, foreclosure filings nationwide were up 81%over 2007 filings.1 Completed foreclosures in2008 will likely exceed the one million mark.2

That annual figure translates into more than3,700 foreclosures every business day. As of July2008, bank-owned property (REO) representedmore than 16 percent of the inventory of existinghomes for sale.3 In some communities, bank-owned properties make up nearly 40 percent ofexisting inventory.4

In both the prime and subprime markets, seri-ously delinquent5 loans have continued to rise atan alarming rate, increasing three-fold since early2006.6 The figures for adjustable rate mortgages(ARMs) are more shocking. Seriously delinquentARMs have more than quadrupled in the pasttwo and a half years.7 By the third quarter 2008,nearly 3 out of 10 of subprime ARMs were morethan 90 days late or in foreclosure.8

As of November, 2008 the FDIC had reportedthat 1.6 million loans were over 60 days delin-quent.9 The FDIC estimates that through theend of 2009, there will be an additional 3.8 mil-lion new loans over 60 days past due.10 Nation-wide it is estimated that 8.1 million mortgageswill be in foreclosure over the next four years,through the end of 2012.11

The consequences of this foreclosure crisis areenormous, ripping through both Wall Street andMain Street. Abuses in the subprime market haveundermined the efforts of hardworking familiesto acquire and maintain the dream of homeown-ership. Instead of building wealth, families arelosing equity.12 Worse yet, some foreclosed fami-lies are unable to find replacement shelter andbecome homeless.13 Renters suffer too, as lendersquickly evict tenants from foreclosed homes.14

More and more Americans are being driven intobankruptcy.15 Neighborhoods are deteriorating

as foreclosed homes are boarded up and left va-cant.16 Crime in high-foreclosure neighborhoodsis on the rise.17 Overgrown lawns and trash-strewn yards symbolize growing communityabandonment and disinvestment.18

III. The Role of the ForeclosureProcess in the DeepeningCrisis

State Foreclosure Laws Escape ReformMost Americans not well-versed in property lawwould assume that homeowners have greaterrights than renters, or at least equal rights. Thestark reality is that while most states updatedtheir landlord/tenant laws decades ago to giverenters basic due process protections in the evic-tion process, no similar reform effort has beenmade to assist homeowners in the foreclosureprocess.

Many state foreclosure laws were enacted inthe 19th and 20th centuries and have gonelargely unchanged since that time. These lawscame into effect at a time when the residentialmortgage industry, to the extent it existed at all,bore no relation to what exists today. Signifi-cantly, these laws pre-date the enormous changesin the mortgage market that began in the 1980s.The typical American pursuing the homeowner-ship dream before the 1980s would have ob-tained a mortgage made by a bank using acceptedunderwriting guidelines which considered thehomeowner’s ability to repay the loan. Risks tothe lender and the homeowner were kept incheck by ensuring that the loan amount did notexceed an appropriate loan-to-value ratio, basedon a sound property appraisal. Mortgage loansmade before the 1980s were typically kept in thebank’s own portfolio of loans and not assignedto another entity, and would have been servicedby that same bank.

FORECLOSING A DREAM 9

The 1990s saw the increasing use of asset-based securities to fund an ever increasing supplyof mortgage credit.19 Creating capital flow in thisway, subprime mortgage lending took off duringthis period.20 Homeowners were encouraged,often through aggressive marketing campaignsthat deceptively touted lower payments and taxbenefits, to use their home equity to consolidatenon-mortgage debts. Practices such as charginghigh points and fees and flipping loans throughmultiple refinancings often stripped homeown-ers of their most valuable asset, the equity intheir homes, bringing many to the brink of fore-closure. The advent of today’s more dangerous“exotic” subprime mortgages sealed the fate ofmany homeowners, spiraling the mortgage mar-ket downward into the current full-blown fore-closure crisis.

The securitization process also brought aboutsignificant changes in the way homeowners dealwith their mortgage company. Servicing rights areoften assigned independently of the mortgage.Homeowners have no choice about servicing com-panies when taking out the mortgage and haveno ability to switch when problems arise.21 Someservicers have been too aggressive in pursuing fore -closure without offering workout options. Theymay also be the cause of the homeowner’s fore-closure problem due to negligent servicing or theimposition of excessive and unauthorized fees.22

MORTGAGE SERVICING ABUSES

Abusive servicing occurs when a servicer seeks tocollect unwarranted fees or other costs from bor-rowers, engages in unfair collection practices orthrough its own improper behavior precipitatesborrower default or foreclosure.23 Some well docu-mented examples include:

� misapplying payments;

� force-placing insurance for borrowers who havealready provided evidence of insurance;

� failing to pay property taxes when due, triggeringgovernmentally imposed late fees and penalties,or sometimes the forced sale of the home;

� charging late fees when borrowers are current ontheir payments

� engaging in coercive collection practices andfalsely claiming amounts due;

� failing to offer and respond to requests for lossmitigation alternatives.

Despite the enormous changes in the mort-gage market, our state foreclosure laws have re-mained frozen in the past. They have eludedmodernization that would ensure homeownerstheir basic constitutional rights before they aredeprived of their property and shelter.

States Should Act NowThe foreclosure crisis continues to spin out ofcontrol. Modernization and improvement of stateforeclosure laws can significantly help blunt theimpact of the crisis on individual homeownersand communities. The method by which homes areforeclosed in this country is almost exclusivelycontrolled by state law. States have historicallydecided under what circumstances a homeownercan lose a home to foreclosure and what proce-dure a mortgage holder must follow. This tradi-tional role for states presents a tremendousopportunity for state policymakers to take afresh look at their foreclosure laws. While reformof state foreclosure laws will not end the currentforeclosure crisis, it can significantly reduce thenumber of foreclosures. For example, researchhas shown that securitized mortgages in stateswith creditor-friendly foreclosure laws that per-mit quick foreclosure are less likely to be modi-fied and are foreclosed at a higher rate than instates that afford protections to homeowners.24

Too often foreclosures occur because home-owners are not aware of the process itself and ofthe options to avoid foreclosure. Rather thanadopt a triage approach in which homeownerswith an interest and ability to retain their homesare given a serious opportunity to explore loanmodification and other sustainable foreclosure

10 FORECLOSING A DREAM

avoidance options, state foreclosure laws oftenshunt borrowers into complicated legal proceed-ings that in many states lack oversight by a judi-cial officer or other basic due process protections.Rather than promote reconciliation and settle-ment, the arcane procedures in many states fur-ther isolate homeowners and create a sense ofhopelessness. Importantly, states can take stepsthat will make it possible for large numbers ofneedless foreclosures to be avoided. This reportpoints out the strengths and deficiencies in statelaws and recommends ways they may be improved.

IV. Data and Methodology

For many years, the National Consumer LawCenter has compiled and reported informationabout state foreclosure laws. One of our publica-tions, Foreclosures (2d ed. 2007 and 2008 Supp.)contains an extensive discussion of foreclosurecourt decisions and a summary of each state’sforeclosure laws. In preparing this report, we re-lied upon this data and supplemented it with re-search on recent state initiatives involving loanmodification and foreclosure diversion programs.

To evaluate state foreclosure laws, we devel-oped a set of questions designed to determinewhether certain basic protections are providedfor residential homeowners. Each state was re-viewed based on the following questions:

1. Before losing their home to foreclosure, dohomeowners have access to a court proceed-ing in which they can present objections andpursue options to avoid foreclosure?

2. Are mortgage holders required to engage inmeaningful loss mitigation efforts before ahome mortgage may be foreclosed?

3. Are homeowners given a right to cure a mort-gage default for at least 60 days before theloan is accelerated and before any legal fees orforeclosure costs are incurred?

4. Are homeowners provided notice of the rightto reinstate after acceleration but before sale,by bringing the loan current including fore-closure fees and costs?

5. Are homeowners provided personal service ofthe notice of sale or foreclosure complaint?

6. Does the state have a housing emergency as-sistance fund or similar program to assisthomeowners in default due to temporary fi-nancial difficulties?

7. Are homeowners provided protections afterthe foreclosure sale, such as redemptionrights, limitations on deficiency judgments,and procedures for accounting and return ofsurplus sale proceeds?

The answers to these questions for each stateare compiled in Appendix A, Survey of StateForeclosure Laws. The results are based on lawsin effect as of December 2008. While many stateshave rarely made changes to their foreclosurelaws, as discussed earlier, we are pleased to reportthat a number of states have very recently en-acted new laws in response to the foreclosure cri-sis. We are hopeful that many more states willfollow this lead, perhaps after considering howthey appear in this report. Thus, we hope to con-tinue reporting on state law changes by regularlyupdating the Survey of State Foreclosure Lawsand making it available on the Center’s websiteat www.consumerlaw.org.

In Part V of this report we provide a detaileddiscussion of the homeowner protections ad-dressed in the survey questions. Results of thesurvey are provided for each question. Finally, weconclude the discussion of each topic with a setof recommendations state policymakers mightconsider in reforming state foreclosure laws.

FORECLOSING A DREAM 11

V. Findings andRecommendations

1. Provide access to a court pro -ceeding in which the homeownerhas an opportunity to presentobjections and to pursue options to avoid foreclosure.

Access to justiceA fundamental due process protection is the “op-portunity to present objections” to an impartialdecision-maker before an individual’s propertycan be taken away.25 Recognition and wide ac-ceptance of this essential right led to reform ofstate eviction laws beginning in the 1960s andthe elimination of “self-help” evictions in whichlandlords could physically remove a tenant’s be-longings and padlock the door without any courtproceeding. In virtually every state, tenants arenow given the right to a hearing before a judge ina proceeding initiated by the landlord before theymay lose the right to possession of their resi-dence and be evicted. Although firmly acceptedin the rental context, our state laws have not em-braced this fundamental right for all homeowners.

In thirty states and the District of Colum -bia, homeowners can lose their homes to fore -closure with no court oversight over the processand without an opportunity to be heard. In thesestates, foreclosures are accomplished by the mort -gage holder’s exercise of the “power of sale” con-tained in the mortgage or deed of trust. Themortgage holder does not need to initiate a courtproceeding to foreclose and the homeowner hasno clear access to a court hearing. The holdertypically only needs to send a notice of sale to thehomeowner, place a legal advertisement in a localnewspaper, and hire an auctioneer to sell theproperty on the scheduled sale date.

If the homeowner disputes that there has beena default in a non-judicial foreclosure state, thereis often no one that a homeowner can turn to inthe foreclosure process to resolve the dispute. Tocontest a foreclosure by power of sale, the home-

owner must file an affirmative court action andrequest an injunction to stop the sale. If this stepis not taken, there will be no judicial involvementat all in the foreclosure. The homeowner willneed to satisfy the demanding pleading and proofrequirements which courts impose before issuinginjunctions, making it virtually impossible to ob-tain this relief without the assistance of an attor-ney. Most courts also require that a bond beposted prior to the issuance of any injunctive re-lief. In many cases, these bonds are set at anamount in excess of the amount that may be indispute and effectively shut the courthouse doorsto most homeowners.

Without some judicial oversight over the fore-closure process, mortgage servicer errors go un-challenged and homeowner defenses that couldprevent foreclosure are not addressed. For example,a homeowner in Massachusetts spent several yearstrying to get a straight answer from her mortgageservicer while it continued to foreclose on herhome.26 Shortly after she received notice that theservicer had taken over servicing of her mort-gage, she and a housing counselor assisting hermade numerous attempts to get informationabout the account and an itemized payoff figure.The servicer first sent a letter stating that thetotal payoff amount was $264,603.13, but thenone week later claimed it was owed $363,603.38.During the next two-year period, the servicer andits foreclosure attorneys quoted six different pay-off figures on the mortgage ranging from a lowof $121,948.38 to a high of $430,707.28. With nojudge overseeing the power of sale foreclosure,the homeowner eventually had to file bankruptcyto stop the sale and try to sort things out. It wasrevealed in the bankruptcy court that the servicerhad never obtained a payment history on the ac-count from the old servicer and did not even havea copy of the original loan documents. The bank-ruptcy judge found that the servicer had “in ashocking display of corporate irresponsibility, re-peatedly fabricated the amount of the Debtor’sobligation to it out of thin air.” None of thiswould have come to light if there had not been a

12 FORECLOSING A DREAM

court proceeding to compel disclosure by the ser-vicer. And if there had been a judicial foreclosureproceeding, the homeowner could possibly haveavoided filing bankruptcy.

HOW JUDICIAL FORECLOSURE WORKS

In less than half of the states, mortgages are alwaysforeclosed by judicial action, either because of statelaw requirements or local custom. In these statesthe mortgage holder must file an action in court,usually in the county where the property is located,to obtain a judicial decree authorizing a foreclosuresale. Generally, to obtain a judgment, the partyseeking to foreclose must prove that there is a validmortgage between the parties, that it is the holderof the mortgage or proper party with authority toforeclose, that the borrower is in default, and thatthe proper procedure has been followed. Thehomeowner then has an opportunity to raise de-fenses to the foreclosure, such as the alleged de-fault did not exist, the mortgage is invalid based onviolations of state and federal consumer protectionlaws, or the servicer accepted but failed to processan application for a loan workout. The homeownercan also bring affirmative claims against the mort-gage holder which may offset amounts claimed tobe in arrears.

If the homeowner and mortgage holder are un-able to resolve the dispute, the court may acceptthe defenses, dismiss the foreclosure action, andaward other relief based on the homeowner’s affir-mative claims. If the court concludes, after consid-ering any defenses, that there has in fact been adefault and that the mortgage holder has the legalright to foreclose, the court will determine the totalamount owed. In some states the homeowner hasthe right to pay this amount to avoid foreclosure. Ifthis amount is not paid by a deadline set by thecourt, the foreclosure will proceed, usually accord-ing to local rules or statutes governing foreclosuresales. Typically the sale is conducted by the sheriffor other public officer appointed by the court. Inmany states after the sale the court must review thesale procedures and confirm that the sale was con-ducted in accordance with the law. (Additionalpost-sale protections are discussed in Section 7,infra.).

Survey Results As mentioned, in thirty states and the Districtof Columbia, the most common form of residen-tial home foreclosure is by non-judicial power ofsale.27 In these states, homeowners generally donot have a meaningful opportunity for court re-view before their home is lost to foreclosure.After the auctioneer’s hammer falls in most states,the sale itself is final and cannot be undone, re-gardless of any claims and defenses the home-owner might have been able to assert before theforeclosure.28 Only after the foreclosure sale isthere a court proceeding in these states to removea homeowner who does not voluntarily vacate,but by then it is usually too late to contest the sale.

States Which Do Not Require CourtInvolvement in Foreclosures

Alabama MontanaAlaska NebraskaArkansas NevadaArizona New HampshireCalifornia New MexicoDistrict of Columbia OklahomaGeorgia OregonHawaii Rhode IslandIdaho South DakotaMaryland TennesseeMassachusetts TexasMichigan UtahMinnesota VirginiaMississippi WashingtonMissouri West Virginia

Wyoming

FORECLOSING A DREAM 13

In all of these states foreclosure occurs withoutjudicial involvement. Homeowners have no oppor-tunity to present any claims or defenses to a judgeunless they file an affirmative lawsuit in court.

Oklahoma is an exception as a power of salestate, offering a hybrid-type procedure. If anOklahoma mortgage includes a power of sale,which most do, the mortgage document itselfmust contain a warning that the mortgage holdercan “take the mortgaged property and sell itwithout going to court” upon default.29 The mort-gage document must also include a disclosurethat if the homeowner sends a written notice bycertified mail to the mortgage holder that a “ju-dicial foreclosure is elected” at least ten days be-fore the home is to be sold under the power of sale,the mortgage holder must stop the power of saleforeclosure and renew the foreclosure in a judi-cial proceeding.30 This right to elect a judicialproceeding must also be prominently disclosedin the notice of sale which is personally served onthe homeowner.31

Similar to Oklahoma, South Dakota also per-mits a homeowner to request that a power of saleforeclosure be converted to a judicial action.32

However, this conversion is not automatic uponnotification to the mortgage holder as the home-owner in South Dakota must first submit an ap-plication making the request to a court whichhandles foreclosures.

North Carolina is also unique in that severalprotections have been added to its power of saleprocedure. The mortgage holder in North Carolinamust first serve a “notice of hearing” on thehomeowner and file it with the clerk of court.33 Ahearing is then held before a clerk who deter-mines whether 1) there is a valid debt, 2) therehas been a default, 3) the mortgage holder legallyhas the right to foreclose, and 4) proper noticehas been given.34 If the clerk finds that all ofthese conditions have been met, the clerk can au-thorize the issuance of a notice of sale and themortgage holder can proceed under the power ofsale. The clerk’s decision can be appealed to ajudge. North Carolina’s procedure was enacted inresponse to a 1975 court decision which struck

down the existing procedures on constitutionalgrounds because they did not provide minimumdue process.35

Of the states which require judicial foreclosure,several have recently implemented mediation ordiversion programs as part of their foreclosureprocess. In each of these states, Connecticut,Florida, New York, New Jersey, Ohio, andPennsylvania, procedures implementing theprograms have been developed by the court sys-tem. These programs are discussed more fully inthe next section and summarized in Appendix B.

Recommendations for Homeowner ProtectionsThe current foreclosure crisis, with its devastat-ing impact on affected families, local communi-ties, and property values, presents a call to actionfor state policy makers. Now more than everstates should consider bringing their foreclosurelaws into the 21st century by ensuring that basicdue process protections and foreclosure avoid-ance procedures are afforded to all homeowners.At a minimum, residential homeowners must beafforded a meaningful opportunity to presentwhatever grievances they may have to an impar-tial and disinterested court official. States shouldeither completely abandon the power of salemethod and require judicial foreclosure, or theyshould look to ways in which essential protec-tions are incorporated into the existing non-judi-cial procedure. States which currently havejudicial foreclosure procedures should considerinnovations to facilitate foreclosure avoidancesettlements, such as court-mandated mediationprograms or settlement conferences. Specific rec-ommendations include:

1. Require Judicial ForeclosureThe most obvious way to give homeowners ac-cess to justice is to require judicial foreclosure, astwenty-one states currently do. In most statesthat permit power of sale foreclosures, a mort-gage holder currently has the option to bring aforeclosure action in court, so there already exists

14 FORECLOSING A DREAM

a structure and legal framework for judicial fore-closures in those states. Thus, this change wouldnot require a substantial rewriting of a state’sforeclosure laws.

2. Create a Hybrid SystemStates wishing to retain the power of sale struc-ture can improve access to justice by enactinglaws which create a hybrid procedure in whichthe process would begin as non-judicial butwould convert to a court procedure if a home-owner seeks review of an unfavorable workoutdecision or responds by asserting foreclosure de-fenses. This process would require the mortgageholder to initiate a court action after some trig-gering event, such as receipt of a formal responsefrom the homeowner to a notice invoking thepower of sale. While many foreclosures wouldprobably still proceed without court involvementunder this regime, homeowners having legiti-mate foreclosure defenses and claims would notbe deprived of an opportunity for court review.

3. Establish Streamlined Procedure forHomeowner to Invoke Court Review

Another approach to reform in non-judicial fore-closure states would be to establish a simple andlow-cost alternative procedure for homeownersto seek judicial review of a mortgage holder’s rightto foreclose by power of sale. Borrowing fromlandlord/tenant procedures in many states, thelaw would create plain language legal forms thatcould be used easily by homeowners who are un-represented by counsel. It is essential that home-owners have an opportunity for court reviewwithout having to post a bond, and that no otherfinancial barriers to court access be imposed. More-over, homeowners under this procedure shouldnot be required to obtain a court injunction tostop the sale. The filing of the court action by thehomeowner should come with an automatic stayof the sale issued by the court, similar to the au-tomatic stay entered upon the filing of a bank-ruptcy case,36 at least until some preliminarycourt hearing can he held. Similar to bankruptcylaw, the procedure could include provisions to

prevent abuse if the homeowner invokes the pro-cedure more than once during a certain period oftime such as one year.37 While most homeownerswould not avail themselves of the procedure, itwould help eliminate wrongful foreclosures byproviding a meaningful check on a mortgageholder or servicer’s decision to foreclose.

4. Require Participation in Mediation Programs

Both judicial and non-judicial foreclosure statescan improve their procedures by requiring thatthe parties confer and consider all options to avoidforeclosure. The hearing procedure in judicialforeclosure states should recognize and treat sep-arately homeowners facing payment default whoare seeking to negotiate a loan modification orworkout agreement with the mortgage holder, orwho wish to access other loss mitigation options. Ifa resolution is not reached by the parties on theirown, they should be referred to a court media-tion program. A similar program can be set up innon-judicial foreclosure states. This recommen-dation is discussed more fully in the next section.

2. Provide that mortgage holdersmust engage in meaningful lossmitigation efforts before a homemortgage may be foreclosed.

Loss mitigation reduces investors’ lossesLoss mitigation was first developed by the Fed-eral Housing Administration (FHA) as a way ofbalancing its purpose of facilitating homeowner-ship with the need to be fiscally responsible withthe federal government’s funds.38 In the context ofpre-foreclosure practice, loss mitigation is essen-tially a mechanism that requires an evaluation ofwhether there is an alternative to foreclosure thatwill reduce the losses to the investor from thehomeowner’s default. The losses that are mea -sured in this context are the investor’s, ratherthan the homeowner’s. Nevertheless, homeownershave traditionally benefitted from loss miti -gation programs because they avoid the loss ofthe home.

FORECLOSING A DREAM 15

Fannie Mae and Freddie Mac are both govern-ment sponsored enterprises (“GSEs”) created byfederal charter as private, for-profit entities withthe mission of facilitating and supporting home-ownership.39 In recognition of their public pur-pose, as well as the reality that loss mitigationefforts provide more income for the investor,Fannie Mae and Freddie Mac have followed thelead of the FHA in this regard. Both agencies haveloss mitigation regulations which servicers are re-quired to follow before initiating a foreclosure.

Investors and servicers of securitized, pri-vately-held mortgages have also come to recog-nize the benefits of loss mitigation strategies,though such efforts are generally encouragedrather than mandated. The servicing contractsfor loans held by private investors often include aloss mitigation plan and contain a standardclause allowing the servicer to modify seriouslydelinquent or defaulted mortgages, or mortgageswhere default is “reasonably foreseeable.”40

Despite widespread acceptance in the mort-gage industry that loss mitigation efforts can re-duce foreclosure rates, reduce investor losses, andsave homes, most state foreclosure laws fail to in-corporate any notice or opportunity for home-owners to access such options before or duringthe foreclosure process, and do not require thatthey be pursued by the mortgage holder as an al-ternative to foreclosure.

Loss mitigation optionsLoss mitigation covers a range of measures toavoid foreclosure. For homeowners who wish toretain their homes, the common options include:

� Repayment Plan—which allows the home-owner to get current by making regular mort-gage payments plus an amount on the arrearsspread out usually over a period of less thansix months;

� Forbearance Plan—which is also a paymentplan that may reduce or suspend the home-owner’s payments for a period generally nomore than twelve months;

� Loan Modification—which involves modify-ing the mortgage, such as by changing the interest rate or term of the mortgage, capital-izing arrears by adding them to the mortgage,and reducing the principal balance of themortgage.

For homeowners who no longer wish to keeptheir homes, the options include:

� Short Sale—which allows the homeowner tosell the home before the foreclosure at anamount less than the mortgage balance;

� Deed in Lieu—which involves the mortgageholder or servicer accepting a deed for thehome from the borrower in exchange fordropping the foreclosure process.

Voluntary efforts lacking Among the loss mitigation options, loan modifi-cation has been identified as one of the preferredstrategies for addressing the current foreclosurecrisis.41 In fact, because many of the loans in orsoon to be in foreclosure were made without con-sidering the homeowner’s ability to pay or wereunderwritten using inflated property appraisals,any plan to ameliorate the current crisis thatdoes not include some form of loan modificationas an essential component will fail. While the po-tential benefits of loan modifications are clear,42

the response from the financial services industryhas been lacking and is dwarfed by the magni-tude of the foreclosure problem.

Since the start of the current foreclosure crisis,there have been several efforts to encourage loanmodifications through voluntary measures. InSeptember 2007, the federal and state bankingregulators issued a joint statement on loss miti-gation strategies, referencing earlier guidanceand encouraging use of loss mitigation authorityavailable under pooling and servicing agree-ments.45 In October 2007, as part of the HOPENOW program, Treasury Secretary Paulson soughtvoluntary commitments from servicers to con-tact borrowers and explore new loan modification

16 FORECLOSING A DREAM

approaches.46 Then in December 2007, SecretaryPaulson announced a plan for “fast track” loanmodifications.47

WHAT IS A LOAN MODIFICATION?

A loan modification is a written change to the agree-ment between the mortgage holder (or its servicer)and the homeowner that alters one or more of theoriginal terms of the note so that the loan will nolonger be considered in default. The goal of a loanmodification is to prevent foreclosure and facilitatethe homeowner’s ability to keep up with regularpayments on the loan.43 Loan modifications may befor short or long terms, or for the life of the loan.Modifications may do any or all of the following:

� capitalize the overdue amounts of interest, escrow items and fees in the mortgage amount(adding these amounts to the principal and mak-ing the payments higher than before);

� waive interest, late fees and other default relatedfees;

� reduce the interest rate and/or make it fixed (forthe life of the loan or for a set period of time);

� reduce the principal of the loan;

� defer payment of loan principal for a period oftime (resulting in a “balloon” payment at the endof the loan);

� extend the term of the loan, generally by re-amortizing the remaining amount due over a new 30-year term, or in some cases extending itto 40 years.44

Despite these efforts, the financial services in-dustry has failed to implement a loan modifica-tion strategy to stop the foreclosure crisis. TheHOPE NOW program issued its first data in early2008, demonstrating that little progress had beenmade.48 The Mortgage Bankers Association’s re-port on loan modifications issued in January2008 revealed similar results. The major findingwas that, in the third-quarter of 2007, mortgageservicers worked out 183,000 repayment plansand 54,000 loan modifications, while starting384,000 new foreclosures.49 Both reports con-firmed that servicers relied heavily during this pe-

riod on repayment plans rather than loan modifi-cations. Repayment plans require homeownersto make increased monthly payments to cure ar-rears. They do not address payment affordabilityproblems caused by high interest rates and rateresets on adjustable rate mortgages.

A recent study illustrates that problems persistand that the industry has not yet engaged inmeaningful loan modifications.50 When loanlevel information from service remittance reportsfrom July 2007 through June 2008 was analyzed,the conclusion was inescapable that:

[W]hile the number of modifications rose rapidlyduring the crisis, mortgage modifications in the aggre-gate are not reducing subprime mortgage debt. Mort-gage modifications rarely if ever reduced principaldebt, and in many cases increased the debt. Nor aremodification agreements uniformly reducing pay-ment burdens on households. About half of all loanmodifications resulted in a reduced monthly pay-ment, while many modifications actually increasedthe monthly payment.

A report by Credit Suisse reaches similar re-sults in finding that loan modification progressis slow and that plans with higher payments aremore common than modifications with lowerpayments.50 As of August 2008, Credit Suisse re-ported that modifications accounted for just 3.5percent of the loans that are delinquent for sixtydays or more. Moreover, after modifications thatfreeze the interest rate at the pre-reset amount,the most common form of modification was onein which the payment increased.

Mortgage modifications which do not reduceprincipal balances or interest rates generally alsofail to reduce the monthly payments. This meansthat while there may be some delay, ultimately,these mortgage loans will still fail. Loan modifi-cations with higher payments re-default almosthalf of the time.52 Not surprisingly, modifica-tions involving principal reduction are much lesslikely to default again.53

FORECLOSING A DREAM 17

AFFORDABLE PAYMENTS NEEDED

A Massachusetts homeowner’s failed attempt toget an affordable modification as reported in theBoston Globe helps illustrate that affordable pay-ments are needed:

Ask LaWanda Fils. This single mother was behind onpayments on her Dorchester two-family home whenshe asked for help from her lender, Option One Mortgage Corp. The solution Option One offered didn’t seem to make sense—she would pay $800 a month more, after rolling in past-due principal,taxes, and insurance. Desperate to save her home, Fils agreed to the deal anyway in February.

Two months later, she defaulted and now is againfacing foreclosure.

“I think it is more for them to pat themselves on theback to say at least they tried,” said Fils. “It’s not feasible and it doesn’t work and they end up havingpeople falling behind.”

* * *

“I don’t know why a lender would enter into that kindof agreement knowing what the outcome would be,”said Kevin Cuff, executive director of the Massachu-setts Mortgage Bankers Association. “Why would itnot go into foreclosure? Why would it not fail?”

Reworked Mortgages Not Working, Boston Globe, December9, 2008.

Unless mandated, homeowners can’t findthe decision-makerFrom the homeowner’s perspective one of thebiggest obstacles to loan modification is findinga live person who can provide reliable informa-tion about the loan account and who has author-ity to make loan modification decisions. Storiesabound of exasperated homeowners attemptingto navigate vast voice-mail systems, being bouncedaround from one department to another, and re-ceiving contradictory information from differentservicer representatives.54 For example, a Neigh-borhood Housing Services of Chicago surveyfound that “countless counselors shared storiesof having a client in the office ready to begindealing with long-deferred financial problems,

but then having to wait 30 minutes or more inorder to talk to an appropriate loss mitigationstaff person.”55 Unfortunately, things have onlygotten worse as servicers struggle to keep up withthe increased workload caused by the foreclosurecrisis.56 When asked to comment on the problems,one housing counseling agency stated the follow-ing about some mortgage servicers: “1. They donot return calls; 2. Take 30–60 days to give us awritten answer; 3. Require their own authoriza-tion to release information forms; 4. Take toolong to assign cases; 5. Keep changing officerswhen cases are assigned; 6. They give wrong in-formation regarding the loan; 7. Always have torefax and explain the situation to different peo-ple; 8. Customer Service sends us to the wrongdepartment; 9. They hang up; and 10. Never will-ing to work any details—they always have newpersonnel.”57

Court-ordered mortgage modificationsWhile federal bankruptcy law generally permitsclaims of secured creditors to be modified inbankruptcy cases, it currently singles out homemortgage claims and shields them from modifi-cation, other than through a plan which cures amortgage default. This provision in the Bank-ruptcy Code prevents homeowners from chang-ing the interest rate, amortization, or term ofmortgage loans in a chapter 13 case, the type ofbankruptcy consumers often file to save a homefrom foreclosure. Several bills pending in Con-gress would repeal this provision and allow mod-ification of home-secured loans in chapter 13cases.58 This change in the law would greatly as-sist homeowners and would complement statelaws that encourage loan modifications outsideof bankruptcy.

Survey ResultsWhile loss mitigation in general—and loan modi-fications specifically—have gained acceptance asstrategies for assisting all parties after mortgage

18 FORECLOSING A DREAM

defaults, clear requirements have not been incor-porated into state foreclosure laws. No stateshave amended their foreclosure laws to requirethat mortgage holders engage in loss mitigationefforts before a home mortgage may be fore-closed. Although limited in scope, several stateshave taken steps in the right direction. Califor-nia and Connecticut have enacted laws requir-ing notice of an opportunity for a meeting beforea foreclosure. New York now has a law that man-dates mediation in many home foreclosures. Inaddition, several judicial foreclosure states haveimplemented court-annexed mediation programs.

Mandated Contact. In a law which went intoeffect in September 2008, California now re-quires that before sending a notice of default, themortgage holder or its servicer must contact theborrower in person or by telephone in order to“assess the borrower’s financial situation and ex-plore options for the borrower to avoid foreclo-sure.”59 During this initial contact, the holder orservicer must advise the borrower that he or shehas the right to request a subsequent meeting.The law does not specify what should occur atthe meeting or provide any clear enforcementmechanism if the holder or servicer does notoffer any meaningful workout options or negoti-ate in good faith. Also, California is a non-judi-cial foreclosure state, and the law fails to add anyprocess for court or some third-party review ifthe borrower is dissatisfied with the outcome.These significant limitations may cause the lawto have a limited impact.

During the initial contact under this new Cali-fornia law, the holder or servicer must also advisethe borrower that a subsequent meeting, if re-quested, shall be scheduled to occur within 14days and may be held telephonically. The noticemust also give the borrower the Department ofHousing and Urban Development (HUD) toll-free telephone number to find a HUD-certifiedhousing counseling agency. The borrower maydesignate a housing counselor or attorney to dis-cuss workout options with the holder or servicer.Assessment of the borrower’s financial situation

and discussion of options may occur during thefirst contact or at the subsequent meeting. Anynotice of default may not be sent until 30 daysafter contact is made with the borrower and thenotice must include a declaration that the holderor servicer contacted the borrower or diligentlytried to make contact.

The California law applies only to loans onowner-occupied residences made between Janu-ary 1, 2003 and December 31, 2007, and the lawwill remain in effect only until January 1, 2013unless extended.

Court Sponsored Mediation Programs. Anumber of states and cities have adopted media-tion programs in response to the current foreclo-sure crisis. Appendix B, infra. provides a summaryof the known programs.

Philadelphia’s program is the most ambi-tious and—by many informal accounts—quitesuccessful. It is mandatory for all mortgage fore-closure cases in which the property is residential,owner-occupied and located in PhiladelphiaCounty. Allegheny County, Pennsylvania courtsand those in several Florida judicial districtsalso have mandatory mediation programs.

The supreme courts of New Jersey, New York,and Ohio have established voluntary mediationprograms for local courts to modify and use aseach court determines is appropriate. Unfortu-nately, local courts are not required to use theprograms in all instances. New York has added anotice to the foreclosure complaint which ad-vises borrowers of the right to request a settle-ment conference.

Local advocates attribute the success of thePhiladelphia mediation program in substantiallyreducing foreclosures to a number of critical factors:

� There are several parties at every conference:1) the representative of the mortgage holderwho is required to have authority to modify themortgage; 2) an independent person (usually alocal attorney unaffiliated with the mortgageindustry) who acts as the mediator in the con-ference; 3) the homeowner, and 4) generally a

FORECLOSING A DREAM 19

trained housing counselor who is familiarwith the dynamics of both the foreclosureprocess in the city and the different types of,and arguments in support of, the variety ofloan modifications which will make the loansustainable and affordable.

� The community group ACORN has beenhired by the City to go door-to-door to per-sonally explain the mediation process, its ben-efits and procedures to homeowners facingfore closure.

� Housing counselors—with the permission ofthe homeowner—prepare and submit a writtenproposal to the holder’s attorney before theconference outlining ways to mitigate theforeclosure.

� The program builds on the availability of thestate Homeowners’ Emergency Mortgage As-sistance Program (HEMAP)60 which has fundsavailable to make modified loans more afford-able to homeowners and acceptable to mort-gage holders.

Recommendations for Homeowner ProtectionsThe most effective way to ensure that mortgageholders and their servicers attempt in good faithto negotiate meaningful loan workouts withhomeowners is to incorporate the requirementinto the state’s foreclosure laws and make it acondition precedent to foreclosure. The lawshould require that before a foreclosure may pro-ceed, the mortgage holder must prove that it orits servicer explored all reasonable options toavoid foreclosure with the homeowner before theforeclosure was initiated.

States can employ a number of strategies tobridge the huge communication gap betweenmortgage holders and homeowners. These strate-gies include:

� Notice regarding the availability and benefitsof loan modification and other loss mitiga-

tion programs should be provided to home-owners very early in the foreclosure process,and other outreach efforts required. Careshould be taken to make the notice stand outfrom other notices, letters or solicitations(often from foreclosure rescue scammers) thehomeowner might receive.

� Loan modifications and workouts must beconsidered before a foreclosure can proceed.The failure to satisfy this requirement shouldbe treated in the foreclosure proceeding as adefense to foreclosure.60

� Diversion programs should be establishedand funded. If a resolution is not reached bythe parties after considering options to avoidforeclosure, they should be referred to a medi-ation program under the supervision of theforeclosure court or an appropriate stateagency. The procedure should ensure that theforeclosure process is stayed until a decision ismade on any pending workout applicationand any further mediation efforts are con-cluded. To be effective the program must re-quire that a representative of the mortgageholder with authority to approve a loan modi-fication or other workout be present or readilyavailable at the mediation sessions.

3. Provide notice of default and rightto cure, with a cure period of atleast 60 days, before accelerationand before any legal fees orforeclosure costs are incurred.

Pre-acceleration right to cure and noticeWhen a homeowner receives a letter from a mort-gage holder declaring that a home mortgage hasbeen accelerated, the impact can be devastating.A typical acceleration letter announces that theentire loan balance, along with an assortment ofcosts and fees, must be paid immediately. If thehomeowner does not pay the full loan balanceright away, the letter states that the mortgageholder will go ahead with the foreclosure and sale

20 FORECLOSING A DREAM

of the home. Essentially, an acceleration noticeinforms homeowners that they have lost theright to pay off the loan in monthly installments.Just making up the missed payments will notstop the foreclosure.

Upon receipt of such a notice, which is oftensent by a lawyer who represents the mortgageholder, it is not surprising that many homeown-ers view their situation as hopeless. They do notknow where to turn, do not seek out alternativesto foreclosure, and simply await the inevitablesale and eviction.

Neither mortgage holders nor borrowers haveanything to gain from creating this prematuresense of hopelessness, particularly when a fore-closure can be prevented by some relatively sim-ple steps. State law requiring that the mortgageholder give the homeowner a notice of default be-fore accelerating the loan and charging defaultfees provides an effective antidote to an unin-formed borrower’s impulse to lose hope and walkaway from the mortgage obligation prematurely.Contrary to the unilateral fiat conveyed by manyacceleration notices, there are often optionsshort of full payment of the loan that can pre-vent foreclosure after a default in payments. Amandatory pre-acceleration notice informing thehomeowner of these options ensures that home-owners receive accurate information about themeans to avoid foreclosure.

Opportunity to cure when it can make a differenceIt is critically important that homeowners begiven an opportunity to cure early in the pro cessbefore default fees accrue and the costly formalforeclosure proceedings begin. If the homeowneris not given this right, the amount needed to cureimmediately before and after acceleration candramatically increase, often adding several thou-sand dollars in legal fees, property appraisal fees,legal advertising costs, and auctioneer fees. Whilemortgage holders in all states typically send bor-rowers pre-acceleration notices of default as required by the Fannie Mae and FreddieMac uni-

form mortgage documents, default-related feesare assessed during the cure period. The uniformmortgage documents do not prohibit assessmentof fees during the cure period.

ESCALATING FEES PREVENT CURE

Some temporary financial setbacks in the autumnof 2005 caused Jennie Richards of Columbus,Ohio, to fall behind on her monthly mortgage pay-ments of $780. Anxious to save the modest, 1,200-square-foot house she had bought a decade earlier,Richards scrambled to get caught up. On Hallow -een she went in person to drop off an overdue pay-ment to her lender, a subsidiary of Cleveland-basedNational City Corp., and left believing she hadbrought her account current.

But when Richards received her December state-ment from National City—whose website proclaims“We care about doing what’s right”—she received ashock: a demand that she pay $3,300. A few dayslater she got another shock: a foreclosure notice.

Richards, a 47-year-old insurance claims exam-iner, managed to come up with the full $3,300 andpaid National City a few days before its Jan. 16deadline. But that wasn’t enough. Instead, in earlyFebruary the bank sent her another demand—thistime for $6,800. And on Valentine’s Day, the bank’slawyer asked a judge to order that Richards’ housebe sold in a foreclosure auction.

Facing the imminent loss of her house and un-able to halt the inexplicably growing mountain offees, Richards sought help from Rachel Robinson, alawyer for the Equal Justice Foundation, a non-profit organization that provides legal representa-tion to low-income people in the Columbus area.

“I worked hard to own a home and I do notwant to lose my home,” Richards wrote in an affi-davit submitted to support Robinson’s motion tooverturn the foreclosure order. “I can afford mymortgage payments but I do not have the money topay everything that National City has demanded inforeclosure fees and costs and the extra interestthat National City has demanded.”

As of November 2008, Richards remained in herhome pending an appeals court’s ruling on her bidto overturn the foreclosure. She also remained inlimbo. “I can’t move forward because my life is onhold, not knowing if I’m going to have a home ornot with my kids,” she said in an interview. “Thishas been a physical torment on me.”

FORECLOSING A DREAM 21

Particularly for low and moderate incomehomeowners, the inclusion of collection chargesover and above the overdue installments can cre-ate insurmountable barriers to a cure.

Requiring a pre-acceleration notice before de-fault fees may be imposed can provide positiveincentives for both servicers and homeowners.Rather than allowing the mortgage holder toincur unnecessary fees and costs and then shiftthem to the borrower, a clear pre-accelerationcure right will encourage the holder or servicer towork with the homeowner. The pre-accelerationnotice may also inform the borrower that if thecure is not made by the deadline date and fore-closure goes ahead, then fees and costs could beassessed against the homeowner in the future.This information gives an incentive to the home-owner to cure during the period when no feesand costs can be assessed.

Time period for cureHomeowners should be given a period of at least60 days to cure an alleged default before themortgage can be accelerated and before defaultfees may be charged. In some cases, the mortgageservicer may be wrongly claiming that the ac-count is in default due to its misapplication ofpayments or some other account error. If this oc-curs it can often take weeks if not months for thehomeowner just to get an answer from the ser-vicer after attempting to resolve the dispute. Inaddition to not prohibiting assessment of fore-closure fees during the cure period, the 30-daycure period provided under the FannieMae andFreddieMac uniform mortgage documents is notlong enough.

The timing of the cure period should coincidewith the important dispute resolution procedurefor mortgages available under federal law. If thehomeowner exercises legal rights under the federalReal Estate Settlement Procedures Act (RESPA) todispute a mortgage account error or to seek ac-count information, by sending a written “qualifiedwritten request,” the servicer is given 60 businessdays (almost three months) to provide a re-

sponse.62 It makes no sense to give homeowners apre-acceleration cure period which is signifi-cantly less than the time period servicers have torespond to a RESPA qualified written request.

Example from Spencer Savings Bank, SLA v. Shaw,2007 WL 1964676 (N.J. Super. Ct. Chancery Div.July 6, 2007), aff ’d 401 N.J. Super. 218, 949 A.2d218 (N.J. Super. Ct. App. Div. 2008):

The Shaws were three months behind in theirmortgage payments when they received a “Noticeof Intention to Foreclose” from their lender. TheNotice had been sent to them in accordance withthe New Jersey statute which grants homeownersthe right to cure a mortgage default for at leastthirty days from the date of the Notice without lia-bility for any fees and costs. (N.J.S.A. 2A:50-56). Arelated provision of New Jersey law allowed a lenderto require a homeowner to pay fees and costs if thehomeowner cured after a foreclosure lawsuit wasstarted. However the statute was silent on the ques-tion of whether the lender could add fees and coststo the cure amount if the homeowner paid duringthe period between the end of the thirty-day noticeperiod and the time the lender actually filed a fore-closure case in court.

The answer to this question made a significantdifference for the Shaws. After the initial thirty-daycure period, but before the lender filed a foreclo-sure case in court, the Shaws offered the lender thethree monthly payments due. The lender refused toallow the cure, demanding instead an additional$1,174.50 in fees and costs. These fees and costsincluded charges for an appraisal and legal fees in-curred in anticipation of filing a foreclosure case incourt.

The New Jersey trial and appellate courts ruledthat the Shaws had effectively cured their mortgagedefault and the lender had no right to proceed witha foreclosure in court. The courts found that thestate legislature intended that no costs and fees ofany kind could be charged to homeowners if theypaid up their missed payments before the lenderfiled a foreclosure action in court.

In some states the entire foreclosure processtakes only three to four months. Allowing a 60-dayperiod before acceleration and commencementof foreclosure gives homeowners the time to findthe funds for repayment. The time can also be

22 FORECLOSING A DREAM

used to negoti ate, gather required financial in-formation, and finalize a workout agreement,loan modification, or some alternative to foreclo-sure that is mutually beneficial to all parties.

TIME TO FIND SOLUTION

Texas has some of the quickest foreclosures in thecountry. Homeowners are initially given only a 20-day cure period before the process begins. Thenthey are given a 21-day advance notice of the intentto sell the property. If the homeowner is unable tocure the default within the 21 days, the property issold at the county courthouse at a public auctionheld on the first Tuesday of the month. While theTexas non-judicial foreclosure process from defaultto foreclosure sale generally takes about threemonths to complete, it can be as short as 41days.63 This brief time period gives little opportunityfor some homeowners to find a solution, as de-scribed in this Dallas Morning News story:

Mr. Brannon, a 78-year-old veteran, is running out oftime to save his home after he got behind on his monthlypayments, which almost doubled in recent months,from $379 to $700.

Mr. Brannon said his finances were imperiled whenhe and his wife had to spend more money on healthcare, including a $3,000 bill for dental work. He gotbehind on his mortgage, then received a notice hishome would be sold about a month ago.

First Franklin Loan Services, his servicer, has agreedto work with him, Mr. Brannon said. But he has lessthan a month to find a solution, he said.

“I can’t hardly write, and now I’ve got to send bankstatements and fax forms,” said Mr. Brannon, a for-mer postal worker who lives off disability from an in-jury he sustained on the job. “I feel I should havemore time to get these mortgage payments together.The thing about it is, I could pay a little extra and getcaught up.”

Texas’ swift foreclosure process puts struggling homeowners in abind, Dallas Morning News, December 10, 2008.

Content of noticeAn effective notice of default should inform thehomeowner of the serious nature of the situa-tion. It should go beyond a routine dunning letterand accurately describe the foreclosure proceed-

ings that lie ahead if the homeowner does notpay the arrears within a time limit set by the statute.The notice should state the basis for the mortgageholder’s claim of default, itemizing the paymentsand other charges allegedly due. The homeownershould be directed to appropriate individualsemployed by the mortgage holder or servicer whocan help to resolve any disputes over charges. Thenotice should inform the borrower of rightsunder the federal Real Estate Settlement Proce-dures Act and similar state laws to invoke formaldispute and information gathering procedures.

As discussed in the previous section, the noticeshould also provide information about the ser-vicer’s loss mitigation programs, again providingcontact information that will direct the home-owner to someone who can effectively respond toa workout request. Information about state orlocal mortgage assistance programs, mediationprograms and other resources should be in-cluded. The notice should also direct the home-owner to appropriate agencies for legal and hous-ing counseling. A well-designed notice shouldstress the benefits of resolution of the default atan early stage, before an unmanageable arrearagein installments, costs and fees makes a cure ofthe default impossible.

WHERE TO TURN?

In 2005, Freddie Mac conducted a survey of home-owners to learn more about how they interact withtheir mortgage lenders and servicers.64 The surveywas updated again in 2007 after the foreclosure cri-sis had begun. Not surprisingly, most homeownersare not aware of options to avoid foreclosure:

� The majority of homeowners (57% of borrowersin default and 65% in good standing) were notaware of loss mitigation options

� One-quarter (25%) of homeowners in defaulthad not contacted their mortgage servicers todiscuss their difficulties and nine in ten (92%)said they would be more likely to contact theirservicers if they knew alternatives could be offered

� More than half (57%) said they did not knowabout forbearance agreements

FORECLOSING A DREAM 23

� Only 52% said they knew their mortgage holdercould extend the mortgage term

� More than half (56%) said they were unaware offoreclosure counseling, while 74% indicated will-ingness to use such services once they becameaware they existed

Survey Results The vast majority of states do not have any lawsmandating a pre-acceleration notice and a rightto cure. Although servicers do send borrowerspre-acceleration default notices based on the uni-form mortgage documents, these notices typicallydo not include the important protections de-scribed above. Most notably, without a state lawrequiring that the cure amount be limited to themonthly installments that the homeowner is be-hind, mortgage holders and their servicers typi-cally demand costly property inspection fees,broker price opinion fees, legal fees and otherfees related to the alleged default.

Massachusetts, New Jersey, and Pennsylva-nia are the only states that give all residentialhomeowners the right to cure a default before ac-celeration and before default fees may be charged.The Massachusetts statute prohibits the mort-gage holder from accelerating the mortgage untilthe borrower is given a 90-day period to cure thedefault without being required to pay any charge,legal fees or penalty related to the default, exceptlate fees. New Jersey and Pennsylvania law givethe homeowner the right to cure without pay-ment of default fees for thirty days before com-mencement of a judicial action to foreclose. ThePuerto Rico statute also expressly prohibitsmortgage holders from charging fees and costs asa condition to a cure before acceleration.

Although they do not place effective limits oncosts and fees, the statutes of Hawaii, Iowa,Maine, Maryland, Nevada, North Carolina,North Dakota, Oklahoma, Texas, and WestVirginia provide for a type of pre-accelerationnotice of default that includes many of the pro-tections described above. The required informa-

tion typically includes an itemization of theamounts due and the identity of contact personsfor dispute resolution and consideration of work-out agreements. These statutes prohibit the lenderfrom proceeding with acceleration and foreclo-sure until the notice period has passed without acure. The Maryland and New Jersey statutes di-rect that proof of compliance with the notice requirement be included in later judicial foreclo-sure filings. Massachusetts requires that the notice be filed with the state division of banks.

States Which Mandate a Notice to Homeowners of

Pre-Acceleration Right to Cure

Hawaii New JerseyIowa North CarolinaMaine North DakotaMaryland OklahomaMassachusetts PennsylvaniaNevada Puerto Rico

Texas

Several states including Florida, Illinois, In-diana, Kentucky, New Mexico, Tennessee, andVirginia, have enacted laws extending a pre-acceleration right to cure to homeowners whohave high-cost mortgages.65 These cure and feelimitation provisions are generally included aspart of more comprehensive legislation dealingwith predatory lending. However, due to the lim-ited definition of high-cost loans in many ofthese states, the protections are applicable onlyto a small percentage of home mortgages. Thesestates should consider amending their foreclo-sure laws to include these rights for all home-owners, not just those with high-cost mortgages.

During 2008 a number of states enacted legis-lation requiring mortgage holders to give home-owners new pre-foreclosure notices. The noticegives homeowners contact information regard-ing the mortgage holder’s loss mitigation officeand refer the homeowner to housing counsel-ing programs. Recent enactments in Georgia,

24 FORECLOSING A DREAM

Minne sota, and North Carolina require thatthis type of notice specifically identify employeesof the mortgage holder or servicer who have au-thority to negotiate workouts and loan modifica-tions. A California law discussed earlier imposesnew requirements for notice and a meeting withan authorized representative of the mortgageholder to “explore options for the borrower toavoid foreclosure” before the statutory notice ofdefault leading to a sale may be sent. Recent Col-orado and New York enactments require thatmortgage holders give homeowners pre-foreclo-sure notices containing contact information tofind out about housing counseling services.While this information can certainly be helpfulto homeowners, the recent enactments do not es-tablish a right to cure for a specific time withoutassessment of costs and fees.

States with Laws Mandating LimitedNotice of Loss Mitigation And

Counseling Options

California MinnesotaColorado New YorkGeorgia North Carolina

Recommendations for Homeowner ProtectionsWhile no single law in effect in any state providesa truly comprehensive set of protections forhomeowners before foreclosure, a combinationof elements found in several of them can maxi-mize these protections. The following items arerequired content in notices mandated by one ormore of the laws in effect in Hawaii, Maryland,Massachusetts, New Jersey, and North Caro -lina. These items should be required content inthe pre-acceleration notices mandated by eachstate’s statute

1. A specific description of what the homeownermust do to cure, including an itemization ofall cure amounts and directions on how to obtain updated statements of any additionalsums coming due during the cure period (HI,MD, MA, NJ, NC);