FORECASTING EXCHANGE RATES USING EXTENDED MARKOV SWITCHING MODELS t by Hok-hoi Fung A thesis submitted in partial fulfillment of the requirements for the degree of Master of Philosophy in the Department of Economics The Chinese University of Hong Kong June 1995 I.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FORECASTING EXCHANGE RATES USING EXTENDED

MARKOV SWITCHING MODELS

t

by

Hok-hoi Fung

A thesis

submitted in partial fulfillment

of the requirements for the degree of

Master of Philosophy in the Department of Economics

The Chinese University of Hong Kong

June 1995 I.

I

- -It.

.

- -I

I: •

1

- - im.l- ;

-•

- I ; .

u

IJ

•

.

‘.

I

、-

-

••jl

---

•

- -

- II

••

- ••

- -

i-l-

I

! I

m-—

{I

.

IK

-I I

ll-t

二-

I

•-

•

-

-,

cn f'!./{/

t

7> (

“

•

ABSTRACT

FORECASTING EXCHANGE RATES USING EXTENDED

MARKOV SWITCHING MODELS

by

Hok-hoi Fung

It is documented in the literature that the 2-state Markov model with time-

vaiying transition probabilities (TVTP) and the 3-state Markov model are more

suitable for delineating movement of the exchange rates. The exchange rates seem

to be more stable since the Lourve accord of March 1987, and it implies the

occurrence of a new state characterized by low variances and less drift. Therefore,

the Markov model with more than 2 states is necessary to incorporate these

characteristics. The assumption on constant transition probabilities of the simple

Markov model may be unrealistic so that a more flexible structure should be

developed. For the TVTP model, it has extra flexibility to allow transition

probabilities to adjust before a rise or decline in the exchange rate, and hence

helps to identify the current state or regime and forecast when the exchange rate

switches regimes. Three major currencies: the German mark, the Japanese yen

and the British pound over the period from September 1973 to June 1992 are

examined in the paper and the results indicate that these extensions seem to offer

better description in sample and generate more satisfactory forecasts for some

currencies when compared to the simple 2-state Markov model. For instance, the

German mark is more likely to follow a stochastic process generated by the TVTP

model while the 3-state Markov model delineates Japanese yen much better.

However, the Markov models do not out-peiform the random walk in out-of-

sample forecasting over short horizons.

I

” ,

!

TABLE OF CONTENTS

Page

LIST OF TABLES ii

LIST OF FIGURES iii

CHAPTER

1. INTRODUCTION 1

2. LITERATURE REVIEW 3

3. METHODOLOGY 6

Formulation of the TVTP Model 6

Filtered and Smoothed Probabilities 9

Maximization of the Expected Log-likelihood 13

4. EMPIRICAL RESULTS 15

The Simple 2-state Markov Switching Model 15

The TVTP Model 17

The 3-state Markov Switching Model 26

5. OUT-OF-SAMPLE FORECASTING 34

6. CONCLUSION 40

APPENDICES 42

BIBLIOGRAPHY 58

LIST OF TABLES

Page

Table

1. Parameter Estimates for the 2-state Markov and

the TVTP Model 16

2. Parameter Estimates for the 3-state Markov Model 28

3. Post-sample Root Mean Squared Forecast Errors 36

4. Post-sample Mean Absolute Forecast Errors 37

ii

LIST OF FIGURES

Page

Figure

1. The Smoothed Probabilities of the 2-state Markov and the TVTP Models for Each Currency 18

2. The Transition Probabilities of the TVTP Model for Each Currency 23

3. The Smoothed Probabilities of the 3-state Markov Model for Each Currency 29

iii

CHAPTER 1

INTRODUCTION

Markov-switching model, originally devised by Hamilton, is claimed to

well model a random process which experiences discrete shifts in values of its

underlying parameters. During the past decade, the Markov model is broadly

applied to some economic issues as the business cycles dynamics (Goodwin 1993

and Filardo 1994),the term structure of interest rates (Hamilton 1988), the stock

price volatility (Hamilton and Susmel 1994) and the exchange rate analysis (Engel

and Hamilton 1990; Kaminsky 1993 and Engel 1994). As regard to the topic on

exchange rates, strong evidence has been found that the first difference in the log

of exchange rates of many major currencies experience shifts in regime from low

or negative to high or positive expected values.

Nevertheless, recent literature indicates that only simple 2-state Markov

model or its variant with constant transition probabilities is employed to trace out

the exchange rate movement. Engel (1994) proposed for future development that

the Markov model with more than two states may be operative in the exchange rate

analysis. Filardo (1994) introduced the time-varying instead of constant transition

probabilities (TVTP) in his study of the business cycles dynamics and found a

much better result and forecasting performance. Therefore, a natural question

emerges: can these extensions yield superior exchange rate forecasts when

compared to the simple Markov model, and even the driftless random walk? Or do

these formulations rather weaken the prediction power because oveifitting occurs

or the market fundamentals "distort" the estimates? The argument is based on the

fact that many structural exchange rate models, which use market fundamentals as

explanatory variables, produce unsatisfactory forecasts (Meese and Rogoff 1983).

These questions and corresponding answers constitute the main theme of

the discussion. In this paper, the 3-state Markov and TVTP models are estimated

for the US dollar against the German mark, the Japanese yen and the British pound

exchange rates, and are compared to the simple Markov and random walk models

in terms of forecasting performance. It is believed that these two extensions

should win over the simple 2-state Markov model because they have supportive

underlying rationales. As refer to the 3-state Markov model, Engel (1994) pointed

out that the poorer forecasts offered by the simple 2-state Markov model (when

compared to the zero-drift random walk) can be attributed to the Lourve accord of

March 1987. This accord seems to have stabilized the exchange rates and implied

the occurrence of a new state characterized by low variances and less drift (it is

called narrow spread) during his post-sample forecast period. Therefore, he

argued that the Markov model would perform better if it allowed for a third state

to incorporate the narrow spread characteristics of the exchange rate process. For

the TVTP model, it has extra flexibility to allow the transition probabilities to

adjust before a rise or decline in the exchange rate, and hence helps to identify the

current state or regime and forecast when the exchange rate switches regimes. It is

expected that the structure of the TVTP model is endowed with a satisfactory

prediction power.

The paper is organized as follows. The literature review is presented in

Chapter Two. Chapter Three delineates the formulation of the TVTP model with

the 2-state Markov model as a nested alternative. Chapter Four reports the

estimates of the 2-state and the 3-state Markov, and the TVTP models. Chapter

Five compares their forecasting performance. Conclusions are offered in Chapter

Six.

2

CHAPTER 2

LITERATURE REVIEW

The Markov model was first applied to the exchange rate analysis by Engel

and Hamilton (1990). The motivation of their study was that they observed

apparent long swings in several exchange rates against the dollar over the period

from the third quarter of 1973 to the first quarter of 1988 and this phenomenon

violated predictions from the stiiictural exchange rate models. For instance, if the

US real interest rate was driven up by the fiscal or monetary policies, it would

only result in one-time upward jump in the value of the dollar according to the

Dombusch (1976) sticky price model, and then the dollar would depreciate

gradually to equate the expected return across countries. However, reality told us

the truth that the dollar was instead much stronger for the subsequent one or two

years after a rise in the real interest rate during that period. Therefore, they were

questioned whether the exchange rates were generated by such stochastic process

that incorporated long swings as its systematic part, or just followed a random

walk with the directionless drifts. They applied the Markov model and assumed

any quarter's change in the exchange rate as driving from one of two regimes or

states which corresponded to episodes of a rising or falling rate respectively. The

results were robust in-sample that two different regimes were identified for

corresponding exchange rates and a given regime was likely to persist for several

years to support the phenomenon of long swings. However, the post-sample

forecasting ability of the Markov model was poor when compared to the zero-drift

random walk on the basis of the mean squared forecast error. In order to have a

complete and thorough comparison on the forecasting performance, Engel (1994)

examined eighteen exchange rates and chose thirteen rates as objects for the

contest. The post-sample forecast period began in the second quarter of 1986 and

ended in the first quarter of 1991. It was found that although the Markov model

3

was superior in forecasting the direction of change in exchange rates, it was still

out-performed by the zero-drift random walk in minimizing the mean squared

forecast eiTor.

Kaminsky (1993) argued that the poor forecasting performance of the

Markov irw del could be explained by its implicit assumption that investors used

only past exchange rate observations to make their forecasts. This information set

might not be enough to forecast changes in the economic environment which

would affect the future path of the exchange rate. Therefore, in his framework, it

was assumed that investors also included the announcements made by Federal

Reserve officials in their information set, and the news provided by such

announcements might be wrong in some situations but helped investors to identify

the current exchange rate regime. The model using this "imperfect,’ information

was termed the Markov model with imperfect regime classification information

(IRCI). The monthly dollar per British pound rate over the period from March

1976 to De:ember 1987 was examined, and it was shown that although the IRCI

model h a d � i higher forecasting performance when compared to the simple Markov

model, its forecasts were not superior than those offered by the zero-drift random

walk.

Filardo (1994) proposed another scheme to improve the forecasting

performance of the Markov model in the business cycle analysis. The transition

probabilities of the Markov model were allowed to evolve as a logistic function of

economic indicators, and were called the time varying transition probabilities

(TVTP). Sach flexibility would provide valuable additional information about

whether a particular business cycle phase had occurred and whether a turning

point was imminent. The idea was similar to those of the IRCI model that the

4

indicators helped to identify the current regime (expansion or contraction) which

the economy was in. The US business cycles over the period from January 1948

to August 1992 were considered, and they were measured by the growth rate in the

national output. The logarithmic first difference of seasonally adjusted total

industrial output from Federal Reserve was chosen as a proxy for the growth rate.

Data on the Composite Index of Eleven Leading Indicators, the Stock and Watson

Experimental index of Seven Leading Indicators, the Standard and Poor's

Composite Stock Index and so on were used as the economic indicators. It was

discovered that the TVTP model offered more satisfactory forecasts when

compared to the Markov model and time series models such as the ARJMA and

VAR.

5

CHAPTER 3

METHODOLOGY

The formulation of the TVTP model is presented in this chapter, and the

Markov models can be constructed by following the same rationale. The details of

the Markov models are described in Hamilton (1990,1993 and 1994).

Formulation of the TVTP Model

Following Diebold, Lee and Weinbach (1994), let the regime or state that a

given process is in at time t be indexed by an unobserved random variable s^,

which takes on the value zero or one, and it is assumed that changes in an

exchange rate e, follow such process. When S[ = 0’ the observed change, e is

assumed to be drawn from the N{/uq,ag^ ) distribution, whereas if s^ = 1, e^ is

drawn from the N(/// , cr;- ) distribution. Under this specification, the density

function of e conditional on ^ = /.’ i = 0 or I at time I is given by

r W I J

(1)

where <9 is a vector of distribution parameters which consists of the means {juq ,

/u j ) and variances (cr^^ , a;-) associated with the two regimes.

St is assumed to follow a first-order, two states Markov process with

transition probability matrix shown as follows.

i.

6

^'t-l

“ 0 0 - e x p C v i ' … 11 Pt 一 7 — r r Pt — 1 Pt

l + exp(x,_i a )

Pt 二 卜 凡 Pt —i + expOc卜 1,") • J

(2)

where 厂产 is the conditional probability p{Sf = k | s^.j = i) at time t for /•’ 众 = 0

or 1 and is a nxl vector of market fundamentals. The probabilities listed

above are assumed to evolve as a logistic function of such fundamentals. It is

obvious, but worth noting, that when the last n-l terms of the nxl probability

parameter vectors a and P are set to zero, the transition probabilities are time

invariant so that p P � a n d p / i are simply constant and the model reduces to the

simple Markov model.

In connection with (1), let X = [0, a, A p] be a (2«+5)xl vector of

population parameters, where p is the unconditional probability of Sj = 0. This

vector characterizes the joint probability density or sample likelihood function

,(^T-J, , ’ e j I Xt,Xf.j, , X 2 , X j ; X ) of the observed data, and our

tasks are then to find the value of the parameter X that maximizes this

function. p ( c ’ , , I "^r,^T - j,……,, Xj ; X) is defined as

P(叶’ct-I, ..,c)2,q|xr,xr-i,…,巧,义)

= Z Z - Z j : p { E r , S T \ X r a )

(3)

7

and

T

= 义 ) f l • , 丑 卜 i,、Vi,而;义)

t=2

T

t=2 T

= h ;约 p(5,i) n pi^t k ; /=2

T

= I 巧;动 p i h ) n pi^t k ;动 pI" t=2

(4)

where E^,S^,Xi,are vectors or matrices containing respective past information

on e, s and x through date i .

In practice, however, the numerical maximization of (3) using ordinary

differentiation methods to evaluate the slope of the sample likelihood is

computationally difficult. Therefore, the EM algorithm is used to find the optimal

parameter .'alues. The EM algorithm is an iterative method and is used to

maximize the expected log likelihood conditional on observed data, instead of the

sample likelihood as (3). It is straight forward to show (see Appendix 1) that the

sequences of estimates which maximize the expected log likelihood at each

iteration converge to the maximum likelihood estimates of the sample likelihood.

The expected log likelihood at j th iteration is defined as

8

= [ \ o g p [ E r , S - f Xf

Sr

= = o | £ 7 , ’ A V ; A 厂 i)(logp(c’|«Sl =0;…+log/y.夕

+ ( 1 - • 二 拉 , ’ A V ; 1 ) ) [ " l o g • |、.i 二 1 ; … + 1 o g ( 1 V )

• \ 7

丁

⑶

where 厂 = i \ Ej , Xj ; ) and = k, s^., = i \ E-p , X^ • ) are the

smoothed state probabilities conditional on 丨 the best guess' of A at j-l iteration.

Hence, if we know the smoothed probabilities, we can maximize (5)

immediately with respect to the parameter vector M . However, a central question

is raised: how do we determine the smoothed probabilities?

Filtered and Smoothed Probabilities

The smoothed probabilities can be calculated after the filtered probabilities I

have been found. Let zW, | , = p{st = \ ?J'' ) be the filtered probability

of St = i for i = 0 or I and 於人 )十 / 1 , = 广 = k \ E" X^ 刃‘丨、be the filtered

probability of s^+j = k for k = Q or 1,and they are both estimated on time t

information set. Then ( j ) � i s called a posterior probability and interpreted as

9

/ \

, M c ' M • 广 - 1 , 义 " 义 广 \ = ] — ,

/ \ / \

_ 巧二。伊-1)厂(‘s) =/|E,-i,义/-i;义广\

/ \

一 M � k / •;没,-1)4-1

— • I五丨,义H ;义广 i )

(6)

where

(7)

and (j>^t+i\ t is called a prior probability and interpreted as

1 /=0

(8) j

where 丨力=/; ) is given by (1).

It is more convenient to express the derivation of the filtered probabilities in

matrix form. Let O , = [(f) \\t ’ ^t\t ]’ ^t+i\t =、伞 V / ] / ’ <t> ] and n广=

[p{e^ I 5广 0 ; 0 J - 1 � , I = 1 ; … " ) ] b e the matrices considered here. Then

10 .

(9)

and

�;+i | /=P/, i � ; k

(10)

Where P/+/ is the transition probability matrix as (2),and 1 is a column vector

whose elements are unity. The symbol * denotes element-by-element

multiplication.

Using (9) and (10), one can calculate the values of filtered probabilities �,丨,

and for each time t by iteration in the sample. Given the filtered

probabilities, the smoothed probabilities can be determined by following the

algorithm developed by Kim (1993). Let • = Pih = i \ Ej , Xj \ be the

smoothed probability of s^ = i on the time T information set and defined as

11

k=0

= Z / 4 + 1 二 众 |/ r,义 7,乂 二 小7+1 ="’五,’义。义叫 A: 二 0

f .-iV

= I : M-s’,+i = "五 r ,义 r ;义广 , .

/ \ ^

= 1 : / i ? , 卞 | 二 " | 五 r ’ 义 r ; 义 广 — — — — T ^

/ \

. 丨 、 乂 二 • + � , r ’ 义 r ; 广 1)

=p[S( = i ^ k=o = 五 / , 知 广 j

- / 4 + i = 0| 知 , 义 r;义广 1)

= • 卡 , ; 义 p i l l ]

(11)

provided that 厂 ( 〜 = i | V y 二 k , Et ’ 乂丁., ^!'') = = i | s …=k^E^.X^-, ?J'^) •

The algorithm can be made clear and compact in matrix form as

�The details of the proof can be found in Hamilton (1994).

12 .

(12)

where ^ ]• The symbol (+) denotes element-by-element division.

Therefore, the smoothed probabilities can be found by iterating on (12) backward

for t = T-1, T-2, 2, I. It is worth noting that the algorithm starts with Oj^j^

which is obtained from (9) for t = T.

Maximization of the Expected Log-likelihood

After the smoothed probabilities are obtained, the expected log likelihood

(5) is maximized directly with respect to the parameter M. The resulting 2n+5

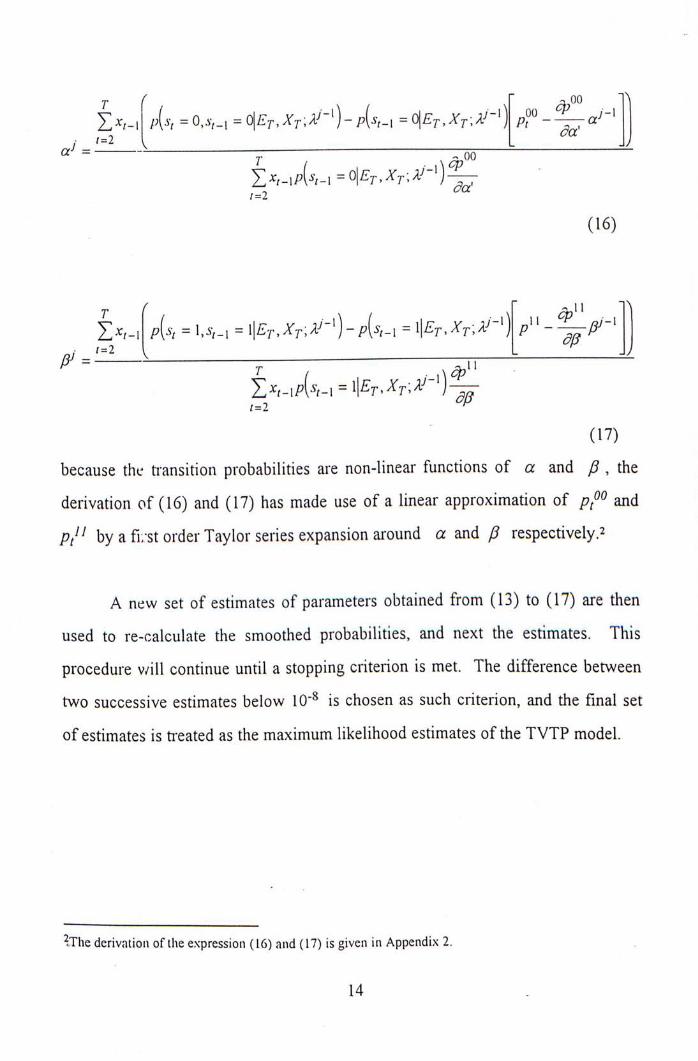

expressions for the likelihood estimates are listed as follows.

T _

J - l^i h 一 丁 . I、

(13)

T 2 / .一 1、

YM -Mi) M � = z | £ v,A > ;乂广

rP- - i ^ 《一 T .,、

(14)

for / = 0, 1

(15)

13 .

r { 「 ; ; I 00 1 �

^ >卜 | 厂 “ =0’‘y卜 1 二 0|£',,A V ;义广•卜 1 广 1) p ? ' - — / L Jz

“ 一丁

(16)

T { / , \ . , \ ,, dp^ 1 .,

n - — — - ^

T (

r=2 P

(17)

because the transition probabilities are non-linear functions of a and /? , the

derivation of (16) and (17) has made use of a linear approximation of 严 and

p/i by a fi:-st order Taylor series expansion around a and (5 respectively.2

A new set of estimates of parameters obtained from (13) to (17) are then

used to re-calculate the smoothed probabilities, and next the estimates. This

procedure will continue until a stopping criterion is met. The difference between

two successive estimates below 10"^ is chosen as such criterion, and the final set

of estimates is treated as the maximum likelihood estimates of the TVTP model.

2;rhe derivation of the expression (16) and (17) is given in Appendix 2.

14 ,

CHAPTER 4

EMPIRICAL RESULTS

The exchange rates examined in this paper are the US dollar against the

German mark, the Japanese yen and the British pound. Monetary theories state

that the exchange rate could be affected by such exogenous variables as the

difference in money supply changes, the difference in output changes, the

difference in interest rates and the difference in inflation rates between the

corresponding countries. Therefore, various combinations of the lagged values of

these variables have been attempted as the market fundamentals to influence the

transition probabilities, and it is observed that the interest rate differential ( R^, ,)

as proxied by the treasury bill rate differential or the call money rate differential

alone does the best in estimation and forecasting and its results are reported in this

thesis (the results produced by other combinations are also tried). In mathematical

term, this functional relation can be expressed as p!�=/( x^.j ) = / ( R^.j ) • The

data on exchange rates and market fundamentals are monthly series and obtained

from the International Financial Statistics (IFS). The sample period begins in

January 1976 for German mark and in September 1973 for Japanese yen and

British pound, and ends in January 1988. The starting point of the sample period

for each currency depends on the availability of data.

The Simple 2-state Markov Switching Model

The results are summarized in Table 1, and it can be seen that some

estimates on means are significant at the 5 or 10 percent level.^

^The estimates on the un-conditional probability p for each model are suppressed from Tables I and 2 because they are not the main concern of this paper.

15 .

Table I. Parameter estimates for the 2-state Markov and the T V T P model. Monthly , 1976:1-1988:1 for German mark, 1973:9-1988:1 for Japanese yen and British pound

Exch. rate German mark Japanese yen British pound

Parameter Markov T V T P Markov T V T P Markov T V T P (2-state) (2-state) (2-state)

jjo 0 . 8 2 9 8 2 0 . 4 5 4 1 7 0 . 6 9 5 4 8 0 . 6 5 3 7 6 0 . 8 4 3 4 5 0 . 8 4 9 3 4

( 0 . 6 9 5 5 5 ) ( 0 . 3 2 8 3 1 ) ( 0 . 3 7 9 1 9 ) ( 0 . 3 7 8 4 3 ) ( 0 . 4 9 3 2 0 ) ( 0 . 5 4 6 7 8 )

… - 0 . 2 9 6 1 9 0 . 2 6 4 1 8 - 0 . 1 9 2 8 6 - 0 . 0 8 1 7 3 - 1 . 8 5 6 5 4 - 2 . 0 7 3 3 3

( 0 . 4 4 5 7 0 ) ( 0 . 3 6 6 7 6 ) ( 0 . 2 3 3 4 6 ) ( 0 . 1 9 9 3 5 ) ( 0 . 2 7 7 9 5 ) ( 0 . 3 6 7 1 8 )

(jo 1 7 . 8 6 3 4 8 1 .86784 15 .54031 1 5 . 7 9 2 6 0 1 1 . 1 8 1 5 6 1 0 . 6 8 6 1 1

( 4 . 0 9 3 5 8 ) ( 0 . 5 2 4 4 1 ) ( 2 . 2 8 1 7 4 ) ( 2 . 3 6 0 5 4 ) ( 1 . 6 9 8 8 7 ) ( 1 . 6 7 6 7 1 )

o ) 3 . 7 7 3 9 8 14 .65241 0 . 9 9 0 9 0 0 . 9 0 3 1 1 4 . 0 7 0 9 4 3 . 7 6 5 0 1

( 1 . 6 2 3 7 3 ) ( 2 . 4 6 8 9 0 ) ( 0 . 3 4 5 0 3 ) ( 0 . 3 2 5 6 3 ) ( 1 . 2 8 0 0 6 ) ( 1 . 3 0 7 5 0 )

p。o 0.82016 …… 0.88614 —— 0.89471 ——

(0.12316) - ( 0 . 0 7 4 5 1 ) -…-- (0.07554) -…―

… … 12.44476 -…“ 1.26908 ------ 1.65792

-…-- (26.67309) -…― (0.56619) -…-- (0.70746)

cCi —— 5 . 9 5 9 6 4 0 . 1 4 2 4 5 —— 0 . 1 2 8 8 2

‘ -…― (12.47619) -…-- (0.13350) -…-- (0.16832)

p" 0 . 7 7 9 3 4 —— 0 . 7 2 3 2 9 —— 0 . 8 1 8 9 7 ——

(0.14373) -…— (0.13820) -“… (0.08898) -…—

Po —— 3 . 9 6 0 8 2 —— 0 . 6 2 0 8 6 —— 1 . 9 4 5 6 7 —— (2 .89519) —— ( 0 . 7 U 7 7 ) —— (0 . 7 3 2 6 6 )

—— 0 . 4 0 3 6 0 —— 0 . 4 1 8 9 8 0 . 3 3 2 9 4 -…― (0.50224) -…-- (0.24928) -…-- (0.26854)

L o g - - 3 7 8 . 2 8 5 9 - 3 7 1 . 6 5 7 5 - 4 3 9 . 9 1 8 7 - 4 3 5 . 0 7 3 4 - 4 4 0 . 3 5 9 9 - 4 3 8 . 5 3 7 5

l ikelihood

LR —— 13 .2568 —— 9 . 6 9 0 6 —— 3 . 6 4 4 8

Note: 1. Standard errors are in parentheses. Variables are measured in percentage.

2. T h e degrees o f freedom for the l ikelihood ratio test {LR) is equal to two.

16 .

For each exchange rate, two states can be distinguished since juq (appreciation)

and jjj (denreciation) differ in signs and values, and the variability is much greater

in the appreciation state. In this state, a 0.83 percent rise in the German mark, a

0.70 percent rise in the Japanese yen and a 0.84 percent rise in the British pound

are found on average, while these currencies decline by 0.30 percent, 0.19 percent

and 1.86 percent respectively in depreciation. The exchange rates experience long

swings during the sample period, as is demonstrated numerically by the point

estimates on 卯 and p " (p卯 ranges from 0.82 to 0.89 and p " goes from 0.72 to

0.82 ). These probabilities can cause the system to stay in either state for a long

time. Or it can also be seen from the smoothed probabilities in Figure 1 that

switches between states are somewhat infrequent."^

The TVTP Model

The results are shown in Table 1,and the TVTP model yields a similar

estimates on means and variances with the only exception on the German mark. In

the appreciation state, a 0.65 percent rise in the Japanese yen and a 0.85 percent

rise in the British pound are found on average, while these currencies fall by 0.08

percent and 2.07 percent respectively in depreciation. For the German mark,

however, /.Iq and juj are both positive in sign. It implies that on average the

German mark appreciates at different speeds. The exchange rates experience long

swings, as is shown in the smoothed probabilities of Figure 1 where the states do

not switch from one to another in a frequent fashion. It is not surprising that the

TVTP model obtains the smoothed probabilities similar to those of the simple

Markov model for the Japanese yen and the British pound because they have

analogies in formulation.

� T h e values of the smoothed probabilities of the 2-statc and 3-state Markov, and TVTP models are reported in Apoendix 3.

17 .

German mark

0.65

0.25 I" ‘ 1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01

Month

Panel A1 • The Movement in the Dollar Per German Mark

2-state Markov model for German mark ' [ I I ji rjFjr I I m I V I . V _ L r ^ j W W H f

f 0 ‘ ‘ ‘ “ ‘

1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01

Month

Pane: A2. The Smoothed Probabilities o f the 2-state Markov Model for German Mark

18 .

TVTP model for German mark

I r “ “

T n • t/i

^ 0.5 (U O O K

‘ J I m M I f i l i J I、aAI\ma • k

1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01 Month

Panel A3. The Smoothed Probabilities of the T V T P Model for German Mark

Japanese yen

I / 0.007 • / V

。 。 “ . A / X r ^ y 0.003 — , ‘

197:;.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel B l . The Movement in the Dollar Per Japanese Yen

19 ,

2-state Markov model for Japanese yen

。 I f f ! i _ i 哪 1/1 i i r t f 擎

1 I “ 『 I .

1 I V V F 0 —^^‘ ‘

1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel B2. The Smoothed Probabilities of the 2-state Markov Model for Japanese Yen

TVTP model for Japanese yen !

i ' l Q E W : I 0.5 - t f I P | H | 1

I IM f : o L _ _ ^ .

1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09 Month

Panel B3. The Smoothed Probabilities of the TVTP Model for Japanese Yen

20 .

British pound

T 〜 y \ .

c、,\\ \

I ‘ 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel C I . The Movement in the Dollar Per British Pound

2-state Markov model for British pound

【 n A A r ^ i N v r M n / | I A V h I / w 』/ [fj u

0 ‘ — 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month Panel C2. The Smoothed Probabilities of the 2-state Markov Model for British Pound

21 ,

TVTP model for British pound

1 p w i M n n 1 1 fflfvi

J l\lUW ^ \ V • 1 0 . 5 - j - i t H \ r r i M l — ^

1 i \r lUl 0 J ‘

1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09 Month

Panel C3. The Smoothed Probabilities of the T V T P Model for British Pound Figure I. The Smoothed Probabilities o f the 2-state Markov and the T V T P Models for

Each Currency

Two important points should be noted here: Although the transition probabilities |

of the TVTP model evolve over time as shown in Figure 2, almost all coefficients

on the market fundamentals are not statistically different from zero. With the null i

hypothesis that the simple Markov model is a true and correct model, the

likelihood ratio test (LR ) rejects this hypothesis at the 1 percent significant level

in favor of the TVTP model for the German mark and the Japanese yen. These

contradictory results may indicate that although the market fundamentals can, to a

large extern, help to find the true parameter values of /Uq, "/,cr^ and cr卜 they

cannot give any significant idea about the current and future regimes because of

high variability of estimated a and p.

22 ,

TVTP model for German mark

。 ' n r n n r i 0.5 1 " H H I I 1

o L u J J ~ 1 1 1 1 。 ~ l U Z _ _ U 1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01

Month

Panel A l . The Transition Probability o f the T V T P Model for German Mark

TVTP model for German mark

— 1 「 〜 、 ^ Y " ^ 八 〜 〜 〜

X) 2 CU c 0.5

.2

c 2 H

0 -L————‘ ‘ ‘ ^ 1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01

Month

Pane!八2. The Transition Probability p" o f the T V T P Model for German Mark

I.

23 -

TVTP model for Japanese yen

。 ‘ [ 广 〜 一 • . 、 , — _

1 V 〜 " ^ • a 0.5 o •Z75 c 2 H

0 ‘ 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel B l . The Transition Probability p � � o f the T V T P Model for Japanese Yen

i i

TVTP model for Japanese yen I

! ) 广 - \ n

u —~‘ ‘ ‘ ‘ ‘ — ^ 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Pane) B2. The Transition Probability p" o f the T V T P Model for Japanese Yen

I.

24 .

TVTP model for British pound

1 1

g 八 一 、 一 — - 、

u.

a 0.5 0 G 03 H

0 ‘ — — 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel C I . The Transition Probability / � o f the T V T P Model for British Pound

TVTP model for British pound

1 l i V H

0 J ‘ ‘ 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel C2. The Transition Probability p" o f the T V T P Model for British Pound

Figur-j 2. The Transition Probabilities o f the T V T P Model for Each Currency

25 .

The 3-state Markov Switching Model

The results are shown in Table 2, and it should be noted that in estimating

the 3-state Markov model, some are constrained to zero or one because their

unrestricted maximum likelihood estimates fall on the boiindaiy and this would

violate the regularity conditions to calculate the inverse of the information matrix

and hence the asymptotic standard errors. It can be seen that some estimates on

means are significant at the 5 or 10 percent l e v e l . ^ The appreciation, the

depreciation and the narrow spread states can be distinguished for each exchange

rate since / / … a n d differ in signs or values. The variability is higher in the

depreciation state for the German mark and the Japanese yen, while in the

appreciation state for the British pound. A 0.42 percent decline in the German

mark, a 0.03 percent rise in the Japanese yen and a 0.72 percent rise in the British

pound are found on average in the narrow spread state. These currencies rise by

5.25 percent, 5.20 percent and 2.01 percent in appreciation while decline in value

by 1.79 percent, 1.93 percent and 1.60 percent in depreciation respectively. Some

interesting features are observed: [1] when the German mark is in the depreciation

state, it will switch to the appreciation state next period (given p冗 is one), [2'

when the British pound is in the narrow spread state, it will never move to the

appreciation state next period (given p^^ is zero), [3] when the British pound is in

the depreciation state, it will never switch to the narrow spread state next period

(given is zero), [4] the German mark stays at the narrow spread state in a

frequent fashion, as is shown in the smoothed probabilities of Figure 3,and [5] the

Japanese yen and the British pound experience long swings during the sample

^For 3-state Markov model, the transition probability matrix is defined as

- 尸 0 0 ^ 1 0 尸 2 0 -

P = . 1 - / / ^ 0 _ , , 0 1

26 ,

period, as is justified by the point estimates of p" and p— ( p " ranges from 0.77

to 0.98 and p - goes from 0.71 to 0.88 ),or by the smoothed probabilities in Figure

o J .

27 .

Table 2. Parameter estimates for the 3-state Markov model.

Monthly , 1976:1 -1988:1 for German mark,1973:9-1988:1 for Japanese yen and British pound

Exch. rate German mark Japanese yen British pound

Parameter Markov (3-state)

^ 5 . 2 4 5 8 1 5 . 2 0 3 4 1 2 . 0 0 9 0 7

( 1 . 2 1 0 8 0 ) ( 0 . 4 9 8 6 9 ) ( 2 . 3 3 1 4 6 )

/Ui - 0 . 4 1 6 0 0 0 . 0 3 3 5 6 0 . 7 1 5 9 2

( 0 . 3 9 1 5 1 ) ( 0 . 1 8 2 3 7 ) ( 0 . 4 1 0 0 2 )

- 1 . 7 8 7 8 5 - 1 . 9 3 4 9 0 - 1 . 6 0 0 1 7

‘ ( 1 . 9 2 6 1 6 ) ( 0 . 5 5 8 3 1 ) ( 0 . 3 8 9 6 7 )

cTq 6 . 1 1 3 6 0 3 . 8 5 5 4 1 2 5 . 4 0 0 8 4

( 3 . 0 1 8 3 5 ) ( 1 . 3 2 9 3 3 ) ( 1 5 . 5 0 3 1 3 )

cry 5 . 4 0 2 4 3 1 . 1 5 3 6 2 9 . 2 7 4 1 6

( 1 . 1 7 0 2 9 ) ( 0 . 3 3 7 9 1 ) ( 1 . 6 8 4 1 6 )

cr, 2 0 . 3 8 6 6 1 6 . 3 0 3 9 3 4 . 4 6 4 5 1

“ ( 1 0 . 1 2 4 5 0 ) ( 1 . 7 6 0 1 2 ) ( 1 . 2 6 2 6 4 )

pOo 0 . 0 7 9 8 5 0 . 3 1 3 0 7 0 . 2 5 9 2 9

( 0 . 1 5 0 7 5 ) ( 0 . 0 9 5 0 3 ) ( 0 . 3 9 5 9 4 )

p0' 0 . 4 6 7 7 2 0 . 2 5 0 7 3 0 . 1 8 7 5 1

( 0 . 2 6 8 2 0 ) ( 0 . 1 3 3 5 1 ) ( 0 . 1 6 8 2 1 )

p'o 0 . 0 5 6 3 8 0 . 1 7 3 9 6 0 . 0 0 0 0 0

( 0 . 0 6 2 4 2 ) ( 0 . 0 7 0 5 6 ) -…—

p" 0 . 8 9 6 4 2 0 . 7 7 0 8 2 0 . 9 7 7 9 3

( 0 . 0 4 4 1 2 ) ( 0 . 0 8 2 3 4 ) ( 0 . 0 2 2 9 4 )

广 1.00000 0.23168 0.11767

—— (0.07801) (0.06780)

p2 丨 0 . 0 0 0 0 0 0 . 0 5 9 4 5 0 . 0 0 0 0 0 —— (0.05784) ——

Log- l ike l ihood - 3 7 3 . 9 9 4 9 - 4 3 3 . 8 3 1 5 - 4 3 5 . 7 9 4 8

Note: Standard errors are in parentheses. Variables are measured in percentage.

28

3-state Markov model for German mark

I 1 n

I.-4I1——[Mi I i i i i i n i n 。l i J i J i u i A AIu / I ajI j f i II l y

1976.01 1978.01 1980.01 1982.01 1984.(U 1986.01 1988.01

Month

Panel A l . The Smoothed Probabilities o f the 3-state Markov Model for German Mark

3 - s t a t e Markov model for German mark

I) 『\i 1 1 J\ I I M 」 _ _ J L 1 0.5 f t i — I t f t t I ^ J I S .

� 1 o i ^ J L i ^ — — -

1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01 Month

Panel A2 . The Smoothed Probabilities o f the 3-state Markov Model for German Mark

29 ,

3-state Markov model for German mark

, ' f ^ n p .

卜 l i l h r r t t l J . J i l t J Ik . n A A . I f i n i U I

1976.01 1978.01 1980.01 1982.01 1984.01 1986.01 1988.01 Month

Panel A3. The Smoothed Probabilities o f the 3-state Markov Model for German Mark

3-state Markov model for Japanese yen

! I [ T i l I I I I I I I 1 - ! " 一 h i i r r H 0 1 C/3 I

。丨 i “ j i J i l l 1111 lift A m i l l III 丨 II i L n i m . 11) I 111 III 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month Panel B l . The Smoothed Probabilities o f the 3-state Markov Model for Japanese Yen

30 .

3-slate Markov model for Japanese yen

一 A / ^ A H a II f| (1 . ( / )

X)

1 0 . 5 … 4 | m\ —

‘ J i l IllUfrJ III I I IL 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel B2. The Smoothed Probabilities of the 3-state Markov Model for Japanese Yen

3-slate Markov model for Japanese yen

i f T n i i i i / i i i n 11”TT 7 ) L i L V i . 1 I 0.5 H | - 1 - . 1/1 I | |

‘ j . i l l J l i I I Iw i l l 1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month Panel B3. The Smoothed Probabilities o f the 3-state Markov Model for Japanese Yen

31 .

3-state Markov model for British pound

I 1 —

o II .. 1/5

} ^^ 1

1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel C I . The Smoothed Probabilities o f the 3-state Markov Model for British Pound

3-state Markov model for British pound

1 ,飞 厂 、

JD 2 ; 0 . 5 <U

‘ J I 0 “—— —^ ^ ^ ^

1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09 Month

Panel C2. The Smoothed Probabilities o f the 3-state Markov Model for British Pound

32 ,

3-state Markov model for British pound

I n fiRnn ^ 0 5

1 丨 n n n

1973.09 1975.09 1977.09 1979.09 1981.09 1983.09 1985.09 1987.09

Month

Panel C3. The Smoothed Probabilities o f the 3-state Markov Model for British Pound

Figure 3. The Smoothed Probabilities o f the 3-state Markov Model for Each Currency

33 .

CHAPTER 5

OUT-OF-SAMPLE FORECASTING

A question of whether the TVTP and the 3-state Markov models offer better

forecasts than the simple 2-state Markov model out of sample is examined in this

chapter. The one period ahead forecast of the TVTP model are found by the

following expression.

E ( c y + i | � + I , & 义 r;义)

= J " c Y + i P ( c Y + i k r + i ’ 五r,义r;义)"cY+i

l/=o

l/=o ‘

= H 行 + 1 , 五 ' 厂 , 和 ; 义 ) J 印 二 五 r , 和 ; 义 印 + 1 /=0

= = 和 r+i,"^r,义 r ; 义 ) = ,,"^7>1,丑 r ’ 义 r;义)

/=0

= S P ( 叶 + 1 = Et,XT.’X)E(cy+1 I T +i 二 /•,知,;义)

/=o 1

i=0

(18)

provided that 厂(叶+/1 � + / ’五r,义r ; 义 ) 丨 五 r , 义 r ;义).

Hence, it is equal to the weighted average of the conditional forecasts. The

weights are given by the forecasts for a Markov Chain which are the same as the

34 ,

filtered probabilities, (jj了+ 丨\丁 . These probabilities are determined by (8) or (10).

The m-period ahead forecast can be made by following the same rationale.

The forecasting period goes from February 1988 to June 1992. The choice

of when to start forecasting is arbitrary. The rolling regression technique is

applied to l e-estimate the parameters of three models for each forecast period in

order to fully utilize the most up-to-date information. Forecasts are generated at

the one, thi se, six, twelve and twenty-four month horizons and in the ex-post sense

for the TVTP model. It is assumed that the future values of the market

fundamentals are known with certainty. Minimization of the root mean squared

error (RMSE) and the mean absolute error (MAE) are chosen as measures to judge

the out-of-sample accuracy. The RMSE and the MAE are shown in Tables 3 and

4, and first consider the comparison between the 2-state and the 3-state Markov

model. The 3-state Markov model has the lower RMSE at the six, twelve and

twenty-four-month horizons for the German mark, at the one, six, twelve and

twenty-four-month horizons for the Japanese yen, and at the six and twenty-four-

month horizons for the British pound. Based on the MAE criterion, it out-

peifoiTns the 2-state Markov model at the six and twelve-month horizons for the

German mark, at all horizons for the Japanese yen, and at the twenty-four month

horizon for the British pound. These results indicate that the 3-state Markov

model performs much better for the Japanese yen. They are consistent with the

higher in-sample log-likelihood value in contrast with the simple 2-state Markov

model as shown in Table 2.

35 .

Table 3. Post - sample root mean squared forecast errors. . Forecast period, monthly, 1 9 8 8 : 2 - 1 9 9 2 : 6

Model Markov Markov T V T P Random (2-state) (3-state) walk

Exch. rate Horizon

German mark 1 month 3 . 6 1 4 9 8 6 3 . 7 7 9 5 0 4 3 . 5 8 1 6 0 3 3 . 5 6 0 0 3 2 3 months 3 . 6 8 8 1 3 9 3 . 6 9 9 6 7 1 3 . 5 9 7 8 2 1 3 . 6 1 9 4 9 6

6 months 3 . 6 1 8 7 4 2 3 . 6 0 6 1 4 0 3 . 5 7 4 0 3 3 3 . 6 1 6 1 5 3

12 months 3 . 6 7 7 4 9 7 3 . 6 7 5 0 5 1 3 . 6 9 6 0 4 9 3 . 6 8 2 7 3 5 24 months 3 . 6 0 5 4 9 9 3 . 5 9 9 5 2 4 ‘ 3 . 6 4 6 3 8 2 3 . 6 2 0 4 5 2

Japanese yen 1 month 3 . 1 6 3 0 2 8 3 . 1 5 7 7 6 9 3 . 1 7 1 5 5 4 3 . 1 2 8 3 4 5 3 months 3 . 2 0 8 4 5 5 3 . 2 1 2 2 8 8 3 . 2 2 2 8 6 3 3 . 1 7 5 0 7 2 6 months 3 . 1 8 9 9 2 4 3 . 1 8 2 9 9 9 3 . 2 0 2 9 4 4 3 . 1 7 2 2 4 3 12 months 3 . 1 6 5 2 8 0 3 . 1 6 3 2 6 3 3 . 1 8 7 7 8 1 3 . 1 3 3 1 4 0 2 4 months 3 . 0 2 6 2 9 2 3 . 0 2 4 0 4 3 3 . 0 3 3 4 4 0 3 . 0 5 1 9 2 2

British pound 1 month 3 . 6 5 5 1 2 2 3 . 7 2 4 3 0 2 3 . 7 0 3 5 4 0 3 . 6 4 1 1 0 7 3 months 3 . 6 6 0 2 1 3 3 . 7 2 5 3 7 5 3 . 6 7 3 0 5 0 3 . 6 1 4 8 7 1 6 months 3 . 5 5 9 9 8 0 3 . 5 3 4 9 8 4 3 . 5 6 0 0 9 2 3 . 5 4 6 2 4 0 12 months 3 . 6 4 2 0 9 8 3 . 7 0 2 6 1 8 3 . 5 7 9 8 1 1 3 . 6 3 0 6 2 0 24 months 3 . 5 4 3 4 4 0 3 . 5 0 9 7 3 4 3 . 4 8 2 8 2 6 3 . 5 1 8 2 3 5

Note: T h e underline denotes the smaller R M S E when compared to the random walk.

36 .

Table 4. Post -sample mean absolute forecast errors. Forecast period, monthly, 1988 :2 -1992:6 •

Model Markov Markov T V T P Random (2-state) (3-state) walk

Exch. rate Horizon

German mark 1 month 2 . 6 7 0 6 6 5 2 . 8 8 9 5 5 8 2 . 6 6 0 4 1 2 2 . 6 5 6 9 2 6 3 months 2 . 7 4 3 1 5 3 2 . 7 6 5 7 7 7 2 . 6 5 4 3 3 8 . 2 . 7 1 2 4 6 2 6 months 2 . 6 5 5 5 8 1 2 . 6 4 5 9 8 8 2 . 6 3 4 4 7 7 2 . 6 8 8 1 4 8

12 months 2 . 6 9 0 6 4 0 2 . 6 8 6 4 5 8 2 . 6 7 7 9 3 9 2 . 7 2 9 7 8 5 2 4 months 2 . 3 9 6 0 0 8 2 . 3 9 7 7 7 7 2 . 4 6 2 8 1 1 2 . 4 2 9 0 1 0

Japanese yen 1 month 2 . 4 9 2 0 0 3 2 . 4 2 7 1 6 5 2 . 4 9 9 9 1 9 2 . 4 1 2 3 2 9 3 months 2 . 5 2 9 9 5 0 2 . 5 1 2 9 3 8 2 . 5 4 3 5 0 5 2 . 4 5 4 6 7 7 6 months 2 . 5 4 2 7 9 4 2 . 5 2 9 5 2 1 2 . 5 5 5 6 7 4 2 . 4 7 6 3 2 3

12 months 2 . 5 3 3 9 7 9 2 . 5 2 9 9 9 2 2 . 5 4 9 0 8 9 2 . 4 5 8 4 0 5 2 4 months 2 . 4 1 4 2 6 9 2 . 4 1 1 1 2 2 2 . 4 1 3 4 6 6 2 . 3 8 7 1 4 9

British pound 1 month 2 . 8 5 5 9 7 8 2 . 9 5 9 9 7 0 2 . 9 0 8 8 2 5 2 . 8 0 1 1 0 8 3 months 2 . 8 4 3 6 4 9 2 . 9 4 0 9 1 2 2 . 8 8 3 1 2 1 2 . 7 9 2 3 9 0 6 months 2 . 7 5 2 4 2 2 2 . 7 6 8 9 5 9 2 . 7 7 8 1 5 6 2 . 7 5 8 4 2 4 12 months 2 . 8 4 2 9 9 4 2 . 9 1 5 4 1 9 2 . 8 1 5 6 6 7 2 . 8 4 0 8 3 2 2 4 months 2 . 7 3 7 7 8 7 2 . 7 3 2 9 6 3 2 . 7 4 2 0 4 3 2 . 7 1 1 8 6 1

Note: T h e underline denotes the smaller M A E when compared to the random walk.

The performance of the TVTP against the 2-state Markov model is

different. The TVTP model has the lower RMSE at the one, three and six-month

horizons for the German mark, and at the twelve and twenty-four-month horizons

for the British pound. Using the MAE criterion, it out-performs the 2-state

Markov model at the one, three, six and twelve-month horizons for the German

mark, at the twenty-four-month horizon for the Japanese yen, and at the twelve-

month horizon for the British pound. It seems that the TVTP model has a superior

37 .

forecasting power for the German mark, which is consistent with the large LR in

Table 1. The comparison in terms of the RMSE among the 2-state and the 3-state

Markov, the TVTP and the random walk models are also considered, and at the

one-month horizon the random walk does the best for all three currencies. At the

three-month horizon the TVTP and the random walk models do the best for one

and the remaining two currencies respectively. At the six and twelve-month

horizons the 3-state Markov, the TVTP and the random walk models perform

better for one currency individually. At the twenty-four-month horizon, the 3-state

Markov model yields more satisfactory forecasts for two currencies while the

TVTP model perfonns better for the remaining currency. Similar results are

drawn using the criterion of the MAE. At the one-month horizon the random walk

does the best for all three currencies. At the three-month horizon the TVTP and

the random walk models do the best for one and the remaining two currencies

respectively. At the six-month horizon the 2-state Markov, the TVTP and the

random walk models perform better for one currency individually. At the twelve-

month horizon the TVTP model produces more satisfactory forecasts for two

currencies while the random walk performs better for the remaining currency. At

the twenty-four-month horizon the 2-state Markov model out-performs the others

for one currency while the random walk offers more attractive prediction for the

remaining two currencies. These results show that the Markov models do not out-

perform the random walk in terms of forecasting over short horizons. To put the

picture differently, when the 2-state and the 3-state Markov and the TVTP models

are grouped together as a single entity and is compared to the random walk, it can

be observed that this entity has lower RMSE at the three, six, twelve and twenty-

four-month horizons for the German mark, at the twenty-four-month horizon for

the Japanese yen, and at the six, twelve and twenty-four-month horizons for the

British pound. Using the MAE criterion, it out-peiforms the random walk at the

38 .

three, six, twelve and twenty-four-month horizons for the German mark, at the six

and twelve-month horizons for the British pound. These results indicate that

although the Markov models as an entity offers more satisfactory forecasts for the

German mark, it is still defeated by the random walk in the contest of prediction

for the Japanese yen and the British pound.

I.

39 .

CHAPTER 6

CONCLUSION

This thesis demonstrates that the extended Markov switching models offer

better description of movement of some exchange rates in the sample than the

simple Markov switching model. For instance, the German mark is more likely to

follow a stochastic process generated by the TVTP model, while the TVTP and the

3-state Markov models delineate the Japanese yen much better. Moreover, the

TVTP model has higher out-of-sample prediction power for the German mark

while more satisfactory forecasts are given by the 3-state Markov model for the

German mark and the Japanese yen in contrast with the simple 2-state Markov

model. Nevertheless, one point should be noted that although the TVTP model is

suitable for modeling the Japanese yen in sample, it generates the poorest

forecasts. The reason may be that high variability of the estimates on the

coefficients of the transition probabilities causes the influence of the market

fundamentals ambiguous, or the coefficients may change over time as random

variables or also experience discrete shifts in regime in and out of sample. When

the contest with the random walk is considered, the results of the thesis indicate

that although the Markov models as a group have better forecasting ability for the

German mark, it is still defeated by the random walk in the contest for the

Japanese yen and the British pound, and as a whole the Markov models do not out-

perform the random walk in offering good forecasts over short horizons.

Exchange markets sometimes appear quite calm and at other times highly

volatile. Therefore, one can consider the changes in volatility over time in the

Markov-switching framework. The approach suggested by Hamilton and Susmel

(1994) is to modify the Markov model to incorporate the autoregressive

conditional heteroskedasticity (ARCH) effect. Nevertheless, some difficulties will

40 ,

be encountered that on the one hand, one must determine the lag order of the

conditional variance and the criteria for the order determination proposed by Engle

(1982) cannot be directly applied in this situation. On the other hand, the

algorithm developed by Kim (1993) cannot be adopted because this algorithm is

limited in use to the conditional density function which only depends on the

current state s , like (1),but the density function with the ARCH effect will

depend on St ’ .s^.y,....••, s . where z is the number of the lag of the conditional

variance. Therefore, these two restrictions cause estimation of the Markov model

with the ARCH effect more complicated.

One can also consider building a 3-state Markov model with time-varying

transition probabilities although the formulation is more complex since one cannot

again make use of the advantage on mathematical simplicity provided by the

logistic function for the 2-state TVTP model.

41 .

APPENDIX 1

The derivative of the expected log likelihood of the TVTP model evaluated

at the estimated parameter A at j th iteration can be rewritten as

±E[\ogp[Er.Sr\XT-xj)}

dX

二 J { 妄知 I 义一 )似‘?—丑‘厂’〜义厂 i )

二 妄 厂 ( 帖 丨 义 — — - — —

= 0

If a fixed point M = ?J'! is found, the above expression can be reduced to

二 ^ ( ^ i i y 去 知 , 知 丨 义 )

= -^\ogp[Ej\Xj\X)

aX = 0

(A. I)

Since the maximization of the sample log likelihood implies the likelihood

is maximized, it proves the result.

42 ,

APPENDIX 2

Maximization of the expected log likelihood of the TVTP model with

respect to a and p results in the following first-order conditions.

T

2 >卜 1 ( / 7 ( 1 � = 0 ,‘ y 卜 1 二0| 五 义 广 = 0 | i r r ’ X , , ; 义 " - 1 ) ) 二 0

1=2

(A.2)

1=2

(A.3)

The conditions are nonlinear in a and p. The linear expressions are,

however, found by approximating and P t " using a first-order Taylor series

expansion around a�'丨 and p j ] respectively. The approximations are given by

„00 ”00 , Cp, j-\\ Pt h 丨 I仅一仅

(A.4)

o 1 1

Pt - A p=/}'AP-P

(A.5)

and the (Ixa?) vectors of partial derivatives are derived as

o 00 - . > / \ 1

^O.r-1 Pt [^-Pt . ^n-U-lPt V Pt I dd I- J

(A.6)

43 ,

ap L J

(A.7)

where x,, is the /山 element of x .y.

Substitute (A.4) and (A.5) into (A.2) and (A.3) respectively, we get the

following linear first-order conditions.

T ( 厂 一 00 1、 厂(、.,=0,、,,_1二0|£,厂’1厂;2广1)_/7(�1=0|£厂’^>;义广1) p,oo + l ( “ _ a 广 I ) = 0

'=2 V L V

(A.8)

= U - i = 1 | 五 r , 义 丨 ) - P “ - i = 1 |五 r ’义 r ;义叫 P” + 誓 ( / ^ - 广 丨 ) 1 = 0

/=2 V L " 」)

(A.9)

Re-arrangement of (A.8) and (A.9) results in the expression (16) and (17).

44

APPENDIX 3

Smoothed Probabilities of the 2-state Markov, 3-state Markov and TVTP Models.

Germany

Date 2-state TVTP 3-state Markov Markov

S = 0 S = 0 S = 0 S = 1 S=2 1976.01 0.0000 1.0000 0.0000 1.0000 0.0000 1976.02 0.0749 1.0000 0.0102 0.9856 0.0042 1976.03 0.1047 1.0000 0.0130 0.9848 0.0021 1976.04 0.1118 1.0000 0.0061 0.9936 0.0003 1976.05 0.1402 1.0000 0.0007 0.9939 0.0054 1976.06 0.1626 1.0000 0.0128 0.9785 0.0086 1976.07 0.2110 1.0000 0.0275 0.9680 0.0046 1976.08 0.2790 1.0000 0.0125 0.9297 0.0578 1976.09 0.4534 1.0000 0.1594 0.8273 0.0133 1976.10 0.3067 1.0000 0.0292 0.9647 0.0061 1976.11 0.2173 1.0000 0.0097 0.9777 0.0126 1976.12 0.2198 1.0000 0.0324 0.9673 0.0002 1977.01 0.1886 1.0000 0.0006 0.9888 0.0106 1977.02 0.1611 1.0000 0.0208 0.9771 0.0021 1977.03 0.1366 1.0000 0.0066 0.9866 0.0068 1977.04 0.1456 1.0000 0.0182 0.9794 0.0024 1977.05 0.1386 1.0000 0.0070 0.9888 0.0042 1977.06 0.1710 1.0000 0.0114 0.9748 0.0138 1977.07 0.2355 1.0000 0.0415 0.9573 0.0012 1977.08 0.2232 0.9996 0.0030 0.9901 0.0068 1977.09 0.2945 0.9966 0.0145 0.9242 0.0614 1977.10 0.4810 0.9013 0.1952 0.7953 0.0095 1977.11 0.6116 0.4302 0.0234 0.6302 0.3464 1977.12 0.9306 0.0027 0.7586 0.2379 0.0035 1978.01 0.6719 0.0993 0.0076 0.6280 0.3644 1978.02 0.6748 0.0132 0.4320 0.5637 0.0043 1978.03 0.3999 0.1404 0.0147 0.9831 0.0022 1978.04 0.2953 0.0270 0.0028 0.9964 0.0008 1978.05 0.2649 0.0523 0.0017 0.9813 0.0170 1978.06 0.3328 0.1176 0.0471 0.9404 0.0125 1978.07 0.4722 0.1083 0.0382 0.8209 0.1409 1978.08 0.6811 0.0559 0.3602 0.6066 0.0332 1978.09 0.8228 0.0825 0.0724 0.3729 0.5547

45

1978.10 1.0000 0.0000 0.9999 0.0001 0.0000 1978.11 1.0000 0.0000 0.0000 0.0003 0.9997 1978.12 0.9629 0.0027 0.9998 0.0002 0.0000 1979.01 0.4940 0.0914 0.0016 0.9430 0.0553 1979.02 0.2849 0.2631 0.0606 0.9387 0.0007 1979.03 0.1984 0.1612 0.0024 0.9967 0.0010 • 1979.04 0.2007 0.0827 0.0020 0.9960 0.0020 1979.05 0.2578 0.2258 0.0053 0.9601 0.0345 1979.06 0.4557 0.0418 0.1091 0.8695 0.0214 1979.07 0.4245 0.1551 0.0509 0.9388 0.0103 1979.08 0.5432 0.1759 0.0187 0.7378 0.2435 1979.09 0.8982 0.0027 0.7028 0.2971 0.0001 1979.10 0.8507 0.0066 0.0002 0.3843 0.6155 1979.11 0.8621 0.0129 0.6890 0.3094 0.0016 1979.12 0.5407 0.2405 0.0086 0.9789 0.0125 1980.01 0.4744 0.1436 0.0147 0.9798 0.0055 1980.02 0.6121 0.0705 0.0164 0.9836 0.0000 1980.03 0.9995 0.0000 0.0000 0.0077 0.9923 1980.04 0.9990 0.0000 0.9990 0.0009 0.0001 1980.05 0.5767 0.7659 0.0183 0.8703 0.1114 1980.06 0.3927 0.8048 0.1250 0.8745 0.0005 1980.07 0.2653 0.8125 0.0015 0.9947 0.0038 1980.08 0.2460 0.8246 0.0061 0.9933 0.0006 1980.09 0.3415 0.7333 0.0020 0.9980 0.0000 1980.10 0.6329 0.0000 0.0001 0.9951 0.0048 1980.11 0.5218 0.1486 0.0063 0.9931 0.0006 1980.12 0.6241 0.2266 0.0019 0.9981 0.0000 1981.01 0.9790 0.0000 0.0000 0.9467 0.0533 1981.02 0.7165 0.2822 0.0551 0.9400 0.0050 1981.03 0.7228 0.2571 0.0173 0.9827 0.0000 1981.04 0.8874 0.0001 0.0001 0.9998 0.0002 1981.05 0.8706 0.0003 0.0002 0.9987 0.0011 1981.06 0.6963 0.0512 0.0015 0.9980 0.0005 1981.07 0.6576 0.0102 0.0011 0.9738 0.0250 1981.08 0.6991 0.1575 0.0533 0.8324 0.1144 1981.09 0.8828 0.0045 0.3507 0.5706 0.0787 1981.10 0.7804 0.0402 0.1488 0.7462 0.1049 1981.11 0.6034 0.0205 0.1373 0.8619 0.0008 1981.12 0.4251 0.0260 0.0013 0.9978 0.0009 1982.01 0.3628 0.0389 0.0013 0.9985 0.0002 1982.02 0.3803 0.0051 0.0005 0.9982 0.0013 1982.03 0.3678 0.1368 0.0025 0.9563 0.0412

46

1985.10 0.8717 0.0993 0.0826 0.3601 0.5574 1985.11 0.9295 0.0079 0.6517 0.2459 0.1024 1985.12 0.8733 0.0812 0.2808 0.4716 0.2476 1986.01 0.9239 0.0358 0.2933 0.2602 0.4465 1986.02 0.9995 0.0000 0.9949 0.0051 0.0000 1986.03 0.9694 0.0007 0.0001 0.0347 0.9653 1986.04 0.9970 0.0002 0.9974 0.0026 0.0000 1986.05 0.9891 0.0000 0.0000 0.0373 0.9627 1986.06 0.9927 0.0010 0.9759 0.0121 0.0121 1986.07 0.9752 0.0008 0.5060 0.2541 0.2399 1986.08 0.7870 0.0114 0.2648 0.5004 0.2348 1986.09 0.6882 0.0056 0.3242 0.6742 0.0016 1986.10 0.7129 0.0025 0.0022 0.5168 0.4810 1986.11 0.9201 0.0012 0.8007 0.1889 0.0104 1986.12 0.8932 0.0041 0.0274 0.2094 0.7633 1987.01 0.9937 0.0000 0.9589 0.0397 0.0013 1987.02 0.5034 0.1066 0.0048 0.9141 0.0812 1987.03 0.3292 0.2061 0.0907 0.9049 0.0044 1987.04 0.2335 0.2074 0.0149 0.9844 0.0007 1987.05 0.1841 0.0327 0.0013 0.9954 0.0033 1987.06 0.1735 0.1142 0.0078 0.9917 0.0005 1987.07 0.2364 0.0610 0.0016 0.9312 0.0672 1987.08 0.4111 0.0732 0.1885 0.8094 0.0021 1987.09 0.5498 0.0742 0.0058 0.6197 0.3745 1987.10 0.9797 0.0004 0.8081 0.0717 0.1201 1987.11 0.9977 0.0001 0.2948 0.0366 0.6686 1987.12 0.9629 0.0216 0.8321 0.1678 0.0001 1988.01 0.9603 0.0000 0.0001 0.2735 0.7264

Japan

Date 2-state TVTP 3-state Markov Markov

S=0 S=0 S=0 S=1 S=2 1973.09 0.0000 0,0000 0.0000 1.0000 0.0000 1973.10 0.2338 0.3507 0.0127 0.7261 0.2611 1973.11 0.9995 1.0000 0.0000 0.0005 0.9995 1973.12 0.8630 0.7116 0.0100 0.0203 0.9696 1974.01 1.0000 1.0000 0.0000 0.0000 1.0000 1974.02 1.0000 0.9999 0.8599 0.0004 0.1397 J974.03 0.9998 0.9997 0.9068 0.0009 0.0922

48 .

1974.04 0.5903 0.3805 0.0020 0.2415 0.7565 1974.05 0.4330 0.2028 0.0030 0.2386 0.7583 1974.06 0.5221 0.3269 0.0042 0.1722 0.8236 1974.07 0.9989 0.9998 0.0000 0.0024 0.9976 1974.08 0.6393 0.6240 0.0018 0.2982 0.6999 1974.09 0.4234 0.3391 0.0989 0.6660 0.2351 1974.10 0.1707 0.1070 0.0028 0.8859 0.1113 1974.11 0.1217 0.0683 0.0026 0.9366 0.0608 1974.12 0.1866 0.1291 0.0021 0.9420 0.0559 1975.01 0.4917 0.3600 0.0371 0.8863 0.0766 1975.02 0.9974 0.9919 0.9422 0.0217 0.0361 1975.03 0.8237 0.7417 0.0007 0.4288 0.5705 1975.04 0.3132 0.1079 0.0112 0.7879 0.2009 1975.05 0.1803 0.0315 0.0115 0.8907 0.0979 1975.06 0.1414 0.0298 0.0005 0.9151 0.0844 1975.07 0.0640 0.0116 0.0016 0.9624 0.0360 1975.08 0.0494 0.0115 0.0015 0.9767 0.0217 1975.09 0.0703 0.0282 0.0004 0.9750 0.0246 1975.10 0.0448 0.0187 0.0024 0.9878 0.0098 1975.11 0.0347 0.0199 0.0009 0.9920 0.0071 1975.12 0.0362 0.0278 0.0006 0.9928 0.0065 1976.01 0.0431 0.0267 0.0028 0.9931 0.0041 1976.02 0.0483 0.0312 0.0028 0.9936 0.0037 1976.03 0.0582 0.0411 0.0050 0.9913 0.0036 1976.04 0.0470 0.0305 0.0015 0.9945 0.0040 1976.05 0.0614 0.0378 0.0011 0.9943 0.0046 1976.06 0.1351 0.0920 0.0056 0.9891 0.0053 1976.07 0.2527 0.1902 0.0168 0.9750 0.0082 1976.08 0.3129 0.2295 0.0292 0.9582 0.0127 1976.09 0.2421 0.1463 0.0048 0.9711 0.0241 1976.10 0.3170 0.2777 0.0003 0.9438 0.0559 1976.11 0.2446 0.1372 0.0009 0.9676 0.0314 1976.12 0.3525 0.1855 0.0099 0.9707 0.0194 1977.01 0.5542 0.3128 0.0204 0.9558 0.0238 1977.02 0.8237 0.6164 0.1561 0.8174 0.0265 1977.03 0.7551 0.4880 0.0768 0.8826 0.0406 1977.04 0.4958 0.1722 0.0026 0.9479 0.0494 1977.05 0.5488 0.2266 0.0080 0.9251 0.0670 1977.06 0.9835 0.9892 0.8609 0.1209 0.0183 1977.07 0.5446 0.3575 0.0175 0.8796 0.1029 1977.08 0.4179 0.2012 0.0018 0.9125 0.0858 1977.09 0.5608 0.3346 0.0215 0.8854 0.0931

49 ,

1 9 7 7 . 1 0 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 6 7 0 . 0 0 0 0 0 . 0 0 3 3

1 9 7 7 . 1 1 0 . 9 7 4 2 0 . 9 3 3 0 0 . 2 9 0 9 0 . 4 5 1 2 0 . 2 5 7 9

1 9 7 7 . 1 2 0 . 9 5 1 7 0 . 9 3 5 2 0 . 3 0 9 5 0 . 5 1 5 2 0 . 1 7 5 3

1 9 7 8 . 0 1 0 . 7 1 2 2 0 . 4 9 7 4 0 . 0 0 3 0 0 . 7 7 6 8 0 . 2 2 0 2

1 9 7 8 . 0 2 0 . 7 8 7 0 0 . 6 3 1 5 0 . 0 5 2 4 0 . 7 5 6 0 0 . 1 9 1 6

1 9 7 8 . 0 3 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 9 0 0 . 0 0 0 0 0 . 0 0 1 0 .

1 9 7 8 . 0 4 0 . 6 2 2 6 0 . 4 5 5 9 0 . 0 0 6 8 0 . 7 6 4 2 0 . 2 2 9 0

1 9 7 8 . 0 5 0 . 6 2 2 6 0 . 4 5 8 6 0 . 0 0 6 8 0 . 7 7 4 2 0 . 2 1 9 0

1 9 7 8 . 0 6 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 9 7 0 . 0 0 0 0 0 . 0 0 0 3

1 9 7 8 . 0 7 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 8 7 0 . 0 0 0 0 0 . 0 0 1 3

1 9 7 8 . 0 8 0 . 6 9 3 4 0 . 5 4 5 6 0 . 0 1 3 1 0 . 8 0 2 5 0 . 1 8 4 4

1 9 7 8 . 0 9 0 . 7 0 7 8 0 . 5 7 4 1 0 . 0 2 0 3 0 . 8 0 7 4 0 . 1 7 2 3 .

1 9 7 8 . 1 0 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 7 7 0 . 0 0 0 0 0 . 0 0 2 3

1 9 7 8 . 1 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 0 1 . 0 0 0 0

1 9 7 8 . 1 2 0 . 9 5 8 5 0 . 8 8 7 4 0 . 0 9 7 1 0 . 0 1 4 7 0 . 8 8 8 2

1 9 7 9 . 0 1 0 . 9 8 9 9 0 . 9 9 7 6 0 . 0 0 0 0 0 . 0 0 1 6 0 . 9 9 8 3

1 9 7 9 . 0 2 0 . 8 5 2 3 0 . 6 7 5 8 0 . 0 0 4 8 0 . 0 1 7 6 0 . 9 7 7 6

1 9 7 9 . 0 3 0 . 9 9 5 1 0 . 9 9 8 3 0 . 0 0 0 0 0 . 0 0 0 4 0 . 9 9 9 6

1 9 7 9 . 0 4 0 . 9 9 9 1 0 . 9 9 9 9 0 . 0 0 0 0 0 . 0 0 0 4 0 . 9 9 9 6

1979.05 0.4606 0.6503 0.0054 0.2869 0.7077 i 1 9 7 9 . 0 6 0 . 3 5 1 5 0 . 7 7 3 3 0 . 0 6 6 5 0 . 3 8 2 6 0 . 5 5 0 9 •;

1 9 7 9 . 0 7 0 . 2 3 8 9 0 . 5 7 9 9 0 . 0 0 8 9 0 . 4 0 3 0 0 . 5 8 8 2 ‘

1 9 7 9 . 0 8 0 . 3 2 2 8 0 . 7 0 6 1 0 . 0 0 2 0 0 . 2 9 2 4 0 . 7 0 5 6

1 9 7 9 . 0 9 0 . 5 5 7 3 0 . 7 7 7 9 0 . 0 0 1 7 0 . 1 4 6 0 0 . 8 5 2 3

1 9 7 9 . 1 0 1 . 0 0 0 0 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 0 1 . 0 0 0 0

1 9 7 9 . 1 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 0 1 . 0 0 0 0

1 9 7 9 . 1 2 0 . 9 9 9 7 0 . 9 9 9 8 0 . 7 4 0 8 0 . 0 0 0 6 0 . 2 5 8 6

1 9 8 0 . 0 1 0 . 8 8 0 8 0 . 6 9 2 0 0 . 0 3 1 1 0 . 1 0 1 5 0 . 8 6 7 3

1 9 8 0 . 0 2 0 . 9 9 9 6 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 1 6 0 . 9 9 8 4

1 9 8 0 . 0 3 0 . 8 6 4 6 0 . 6 4 9 1 0 . 0 1 9 5 0 . 1 5 6 1 0 . 8 2 4 4

1 9 8 0 . 0 4 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 3 4 4 0 . 0 0 0 3 0 . 0 6 5 3

1 9 8 0 . 0 5 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 3 9 0 . 0 0 0 0 0 . 0 0 6 1

1 9 8 0 . 0 6 0 . 9 9 9 1 0 . 9 9 8 6 0 . 6 8 5 0 0 . 0 0 4 5 0 . 3 1 0 5

1 9 8 0 . 0 7 0 . 9 9 9 9 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 4 0 . 9 9 9 6

1 9 8 0 . 0 8 0 . 9 9 9 8 0 . 9 9 9 6 0 . 7 8 4 6 0 . 0 0 1 1 0 . 2 1 4 3

1 9 8 0 . 0 9 0 . 9 9 7 4 0 . 9 9 0 5 0 . 7 2 7 1 0 . 0 2 2 4 0 . 2 5 0 4

1 9 8 0 . 1 0 0 . 8 4 0 6 0 . 5 2 7 8 0 . 0 2 4 9 0 . 2 4 4 0 0 . 7 3 1 1

1980.11 0.9429 0.8796 0.0005 0.1669 0.8326 1 9 8 0 . 1 2 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 8 8 0 0 . 0 0 0 0 0 . 0 1 2 0

1 9 8 1 . 0 1 0 . 6 4 4 1 0 . 8 0 4 1 0 . 0 0 4 7 0 . 1 6 8 1 0 . 8 2 7 2

1 9 8 1 . 0 2 0 . 6 2 1 0 0 . 9 6 1 4 0 . 0 0 0 5 0 . 1 0 8 3 0 . 8 9 1 2

1 9 8 1 . 0 3 0 . 5 7 3 4 0 . 7 8 8 2 0 . 0 0 2 1 0 . 0 9 0 0 0 . 9 0 8 0

50 ,

1 9 8 1 . 0 4 0 . 7 6 4 1 0 . 9 1 0 9 0 . 0 0 0 6 0 . 0 3 3 9 0 . 9 6 5 5

1 9 8 1 . 0 5 0 . 9 9 7 6 0 . 9 9 9 9 0.0000 0.0002 0 . 9 9 9 8

1 9 8 1 . 0 6 0 . 8 7 1 2 0 . 8 3 3 9 0 . 0 0 2 9 0 . 0 1 3 1 0 . 9 8 4 0

1 9 8 1 . 0 7 1 . 0 0 0 0 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 0 1 . 0 0 0 0

1 9 8 1 . 0 8 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 3 1 2 0 . 0 0 0 0 0 . 0 6 8 8

1 9 8 1 . 0 9 0 . 8 8 4 8 0 . 9 6 5 5 0 . 0 0 0 8 0 . 2 5 5 4 0 . 7 4 3 8

1 9 8 1 . 1 0 0 . 7 9 0 0 0 . 7 5 0 1 0 . 0 0 7 5 0 . 3 4 5 2 0 . 6 4 7 3

1 9 8 1 . 1 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 8 4 0 . 0 0 0 0 0 . 0 0 1 6

1 9 8 1 . 1 2 0 . 9 8 7 0 0 . 9 7 9 9 0 . 0 0 0 2 0 . 0 0 5 8 0 . 9 9 4 0

1 9 8 2 . 0 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 0 1 . 0 0 0 0 ‘

1 9 8 2 . 0 2 0 . 9 9 2 0 0 . 9 8 8 1 0 . 0 0 0 1 0 . 0 0 0 5 0 . 9 9 9 4

1 9 8 2 . 0 3 0 . 9 9 9 7 0 . 9 9 9 8 0 . 0 0 0 0 0 . 0 0 0 2 0 . 9 9 9 8

1 9 8 2 . 0 4 1 . 0 0 0 0 1 . 0 0 0 0 0 . 8 9 5 7 0 . 0 0 0 0 0 . 1 0 4 3

1 9 8 2 . 0 5 0 . 9 9 8 9 0 . 9 9 9 0 0 . 0 0 0 0 0 . 0 0 0 5 0 . 9 9 9 5

1 9 8 2 . 0 6 0 . 9 9 9 6 0 . 9 9 9 9 0 . 0 0 0 0 0 . 0 0 0 0 1 . 0 0 0 0

1 9 8 2 . 0 7 0 . 8 2 4 1 0 . 8 3 6 3 0 . 0 0 1 0 0 . 0 1 2 2 0 . 9 8 6 9

1 9 8 2 . 0 8 0 . 8 3 3 9 0 . 8 7 0 9 0 . 0 0 0 7 0 . 0 1 0 9 0 . 9 8 8 5

1 9 8 2 . 0 9 0 . 9 7 5 7 0 . 9 8 6 6 0 . 0 0 0 1 0 . 0 0 1 7 0 . 9 9 8 3

1 9 8 2 . 1 0 0 . 9 9 1 0 0 . 9 8 8 8 0 . 0 0 0 1 0 . 0 0 4 7 0 . 9 9 5 1

1982.11 1.0000 1.0000 0.9992 0.0000 0.0008 i 1 9 8 2 . 1 2 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 9 0 0 . 0 0 0 0 0 . 0 0 1 0 ‘;

1 9 8 3 . 0 1 0 . 5 2 7 4 0 . 6 1 4 5 0 . 0 0 2 0 0 . 7 9 3 8 0 . 2 0 4 2

1 9 8 3 . 0 2 0 . 3 5 3 3 0 . 5 3 1 3 0 . 0 2 1 4 0 . 8 6 8 7 0 . 1 0 9 9

1 9 8 3 . 0 3 0 . 2 5 5 5 0 . 5 6 8 4 0 . 0 0 0 5 0 . 8 9 4 6 0 . 1 0 4 9

1 9 8 3 . 0 4 0 . 1 6 6 2 0 . 4 3 8 8 0 . 0 1 4 3 0 . 9 2 7 6 0 . 0 5 8 2

1 9 8 3 . 0 5 0 . 0 9 5 6 0 . 3 1 5 0 0 . 0 0 1 5 0 . 9 3 5 9 0 . 0 6 2 6

1 9 8 3 . 0 6 0 . 1 1 1 9 0 . 3 2 1 7 0 . 0 0 2 1 0 . 9 0 7 7 0 . 0 9 0 2

1 9 8 3 . 0 7 0 . 2 4 2 3 0 . 4 5 7 4 0 . 0 0 2 5 0 . 8 2 6 4 0 . 1 7 1 1

1 9 8 3 . 0 8 0 . 6 5 7 9 0 . 8 3 9 4 0 . 0 0 1 2 0 . 6 6 3 0 0 . 3 3 5 8

1 9 8 3 . 0 9 0 . 9 9 9 4 1 . 0 0 0 0 0 . 9 7 8 7 0 . 0 0 5 3 0 . 0 1 6 0

1 9 8 3 . 1 0 0 . 5 3 1 7 0 . 6 3 6 1 0 . 0 3 7 9 0 . 8 8 7 2 0 . 0 7 4 9

1 9 8 3 . 1 1 0 . 2 4 2 3 0 . 4 0 8 5 0 . 0 0 2 2 0 . 9 5 7 2 0 . 0 4 0 6

1 9 8 3 . 1 2 0 . 2 0 6 7 0 . 4 7 0 7 0 . 0 0 7 8 0 . 9 6 0 3 0 . 0 3 1 9

1 9 8 4 . 0 1 0 . 2 4 6 6 0 . 4 9 7 5 0 . 0 0 0 8 0 . 9 4 5 2 0 . 0 5 4 0

1 9 8 4 . 0 2 0 . 4 3 6 0 0 . 5 6 6 7 0 . 0 1 6 7 0 . 9 0 6 6 0 . 0 7 6 7

1 9 8 4 . 0 3 0 . 9 9 6 6 0 . 9 9 9 6 0 . 9 4 1 9 0 . 0 0 8 4 0 . 0 4 9 8

1 9 8 4 . 0 4 0 . 8 1 4 3 0 . 6 1 9 1 0 . 0 0 7 9 0 . 1 1 5 4 0 . 8 7 6 7

1 9 8 4 . 0 5 0 . 9 2 2 9 0 . 9 5 1 7 0 . 0 0 0 3 0 . 0 2 3 4 0 . 9 7 6 3

1 9 8 4 . 0 6 0 . 9 6 7 4 0 . 9 7 2 8 0 . 0 0 0 1 0 . 0 0 6 3 0 . 9 9 3 6

1 9 8 4 . 0 7 0 . 9 8 7 0 0 . 9 9 7 3 0 . 0 0 0 1 0 . 0 0 7 5 0 . 9 9 2 4

1984.08 0.8054 0.9123 0.1796 0.2096 0.6107 1 9 8 4 . 0 9 0 . 4 8 6 5 0 . 8 5 0 8 0 . 0 0 1 0 0 . 3 9 3 7 0 . 6 0 5 3

f.

51 .

1 9 8 4 . 1 0 0 . 2 2 8 8 0 . 5 5 8 3 0 . 0 0 9 6 0 . 5 4 6 2 0 . 4 4 4 2

1 9 8 4 . 1 1 0 . 1 9 5 0 0 . 5 1 5 6 0 . 0 0 4 2 0 . 5 6 3 5 0 . 4 3 2 3

1 9 8 4 . 1 2 0 . 3 3 7 8 0 . 7 8 9 4 0 . 0 0 0 6 0 . 4 9 4 3 0 . 5 0 5 1

1 9 8 5 . 0 1 0 . 4 1 1 8 0 . 6 7 2 4 0 . 0 0 1 1 0 . 4 9 0 2 0 . 5 0 8 7

1 9 8 5 . 0 2 0 . 6 2 7 9 0 . 8 1 5 6 0 . 0 0 0 8 0 . 4 8 0 1 0 . 5 1 9 2

1 9 8 5 . 0 3 0 . 8 5 6 4 0 . 9 6 9 5 0 . 4 9 3 7 0 . 3 7 0 5 0 . 1 3 5 8 •

1 9 8 5 . 0 4 0 . 4 6 2 5 0 . 4 2 5 9 0 . 0 0 7 1 0 . 8 7 7 2 0 . 1 1 5 7

1 9 8 5 . 0 5 0 . 4 2 0 0 0 . 3 6 9 8 0 . 0 0 4 6 0 . 9 0 8 9 0 . 0 8 6 5

1 9 8 5 . 0 6 0 . 6 4 6 0 0 . 6 3 2 1 0 . 0 4 8 5 0 . 8 5 5 1 0 . 0 9 6 4

1 9 8 5 . 0 7 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 1 3 0 . 0 0 0 2 0 . 0 0 8 5 ‘

1 9 8 5 . 0 8 0 . 8 5 9 6 0 . 6 2 5 8 0 . 0 1 4 3 0 . 5 3 6 9 0 . 4 4 8 8

1 9 8 5 . 0 9 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 9 4 0 . 0 0 0 0 0 . 0 0 0 6 ‘

1 9 8 5 . 1 0 0 . 9 9 6 2 0 . 9 8 7 0 0 . 6 5 3 3 0 . 0 7 8 3 0 . 2 6 8 4

1 9 8 5 . 1 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 6 0 8 0 . 0 0 0 4 0 . 0 3 8 8

1 9 8 5 . 1 2 0 . 9 0 9 0 0 . 7 4 7 9 0 . 0 6 5 7 0 . 5 1 9 6 0 . 4 1 4 7

1 9 8 6 . 0 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 6 3 3 0 . 0 0 0 6 0 . 0 3 6 1

1 9 8 6 . 0 2 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 6 0 0 . 0 0 0 0 0 . 0 0 4 0

1 9 8 6 . 0 3 0 . 8 6 4 9 0 . 6 3 2 0 0 . 0 2 2 4 0 . 5 6 2 1 0 . 4 1 5 6

1 9 8 6 . 0 4 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 2 7 0 . 0 0 0 0 0 . 0 0 7 3

1 9 8 6 . 0 5 0 . 9 6 6 1 0 . 9 1 6 5 0 . 0 0 1 1 0 . 1 1 9 9 0 . 8 7 9 0

1 9 8 6 . 0 6 1 . 0 0 0 0 0 . 9 9 9 9 0 . 8 9 9 9 0 . 0 0 0 8 0 . 0 9 9 3 ;

1 9 8 6 . 0 7 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 4 1 0 . 0 0 0 0 0 . 0 0 5 9 ‘

1 9 8 6 . 0 8 0 . 8 5 0 5 0 . 7 0 0 4 0 . 0 0 3 0 0 . 1 9 0 3 0 . 8 0 6 7

1986.09 0.9153 0.8286 0.1447 0.1072 0.7481 1 9 8 6 . 1 0 1 . 0 0 0 0 1 . 0 0 0 0 0 . 0 0 0 0 0 . 0 0 0 3 0 . 9 9 9 7

1 9 8 6 . 1 1 0 . 8 3 5 3 0 . 5 8 6 7 0 . 0 0 5 8 0 . 1 5 7 8 0 . 8 3 6 4

1 9 8 6 . 1 2 0 . 9 5 3 2 0 . 9 0 1 1 0 . 3 1 0 3 0 . 1 5 4 3 0 . 5 3 5 4

1 9 8 7 . 0 1 0 . 9 9 9 9 0 . 9 9 9 9 0 . 9 2 4 3 0 . 0 0 1 7 0 . 0 7 4 0

1 9 8 7 . 0 2 0 . 8 6 0 1 0 . 6 3 9 0 0 . 0 1 2 5 0 . 4 9 0 8 0 . 4 9 6 8

1 9 8 7 . 0 3 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 7 3 2 0 . 0 0 0 1 0 . 0 2 6 7

1 9 8 7 . 0 4 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 2 4 9 0 . 0 0 0 1 0 . 0 7 5 0

1 9 8 7 . 0 5 0 . 9 9 2 9 0 . 9 9 4 1 0 . 0 0 0 1 0 . 0 0 5 2 0 . 9 9 4 7

1 9 8 7 . 0 6 0 . 9 2 0 1 0 . 9 0 4 2 0 . 0 0 0 3 0 . 0 2 2 5 0 . 9 7 7 2

1987.07 0.8893 0.8168 0.0014 0.0621 0.9365 1 9 8 7 . 0 8 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 0 2 4 0 . 0 0 0 0 0 . 0 9 7 6

1 9 8 7 . 0 9 0 . 9 9 1 0 0 . 9 8 2 5 0 . 0 0 0 3 0 . 0 3 3 6 0 . 9 6 6 1

1 9 8 7 . 1 0 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 7 6 5 0 . 0 0 0 0 0 . 0 2 3 5

1 9 8 7 . 1 1 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 6 6 1 0 . 0 0 0 2 0 . 0 3 3 8

1 9 8 7 . 1 2 1 . 0 0 0 0 1 . 0 0 0 0 0 . 9 9 5 5 0 . 0 0 0 0 0 . 0 0 4 5

1 9 8 8 . 0 1 0 . 9 8 3 2 0 . 9 8 7 7 0 . 0 0 0 2 0 . 0 3 0 1 0 . 9 6 9 8

I.

52 .

UK

Date 2-state TVTP 3-state Markov Markov

S=0 S=0 S=0 S=1 S=2 ‘ 1973.09 0.0000 0.0000 0.0000 0.0000 1.0000 1973.10 0.1385 0.2266 0.0813 0.0000 0.9187 1 9 7 3 . 1 1 0 . 1 5 2 9 0 . 2 2 4 1 0 . 0 4 6 5 0 . 0 0 4 8 0 . 9 4 8 7 气

1973.12 0.2509 0.3520 0.0444 0.0106 0.9450 ‘ 1 9 7 4 . 0 1 0 . 4 0 2 0 0 . 5 5 2 5 0 . 0 5 0 1 0 . 0 1 8 1 0 . 9 3 1 8 :

1974.02 0.7764 0.8835 0.1856 0.0295 0.7849 1974.03 0.9540 0.9950 0.5444 0.0454 0.4102 1974.04 0.8609 0.9370 0.2076 0.0562 0.7362 1974.05 0.5968 0.6878 0.0468 0.0547 0.8985 1974.06 0.5068 0.6231 0.0505 0.0516 0.8979 1974.07 0.4323 0.5528 0.0422 0.0496 0.9081 1974.08 0.4054 0.5320 0.0344 0.0489 0.9167 1974.09 0.5172 0.6705 0.0682 0.0489 0.8829 1974.10 0.5686 0.7131 0.0559 0.0502 0.8939 i 1 9 7 4 . 1 1 0 . 6 2 5 8 0 . 7 8 0 9 0 . 0 4 9 8 0 . 0 5 0 9 0 . 8 9 9 3 :

1974.12 0.7402 0.8952 0.0970 0.0501 0.8530 1975.01 0.7770 0.9350 0.1241 0.0463 0.8296 1975.02 0.7370 0.9234 0.1816 0.0312 0.7872 1975.03 0.4143 0.6088 0.0574 0.0212 0.9214 1975.04 0.1992 0.3351 0.0362 0.0151 0.9487 1975.05 0.1169 0.2230 0.0345 0.0120 0.9535 1975.06 0.0824 0.1806 0.0571 0.0091 0.9338 1975.07 0.0724 0.1870 0.0318 0.0092 0.9591 1975.08 0.0909 0.2274 0.0322 0.0096 0.9581 1975.09 0.1377 0.3380 0.0411 0.0109 0.9480 1975.10 0.2838 0.6772 0.1245 0.0140 0.8615 1975.11 0.2288 0.6031 0.0408 0.0198 0.9394 1975.12 0.2756 0.7508 0.0630 0.0232 0.9137 1976.01 0.2745 0.7492 0.0627 0.0281 0.9091 1976.02 0.2302 0.6300 0.0571 0.0325 0.9104 1976.03 0.1686 0.4059 0.0918 0.0357 0.8725 1976.04 0.1423 0.2979 0.0572 0.0497 0.8931 1976.05 0.1879 0.3791 0.0894 0.0658 0.8448 1976.06 0.3371 0.7254 0.1269 0.1080 0.7652 1976.07 0.3663 0.7512 0.0876 0.1596 0.7528 1 9 7 6 . 0 8 0 . 3 7 0 4 0 . 6 8 1 2 0 . 0 8 0 7 0 . 1 9 5 1 0 . 7 2 4 2

t.

53 .

1 9 7 6 . 0 9 0 . 4 0 8 0 0 . 6 0 0 4 0 . 2 0 0 7 0 . 2 2 7 0 0 . 5 7 2 2

1 9 7 6 . 1 0 0 . 5 3 5 2 0 . 6 5 4 6 0 . 2 2 2 2 0 . 3 4 9 8 0 . 4 2 8 1

1 9 7 6 . 1 1 0 . 9 1 9 7 0 . 9 8 6 7 0 . 3 4 5 6 0 . 5 1 8 8 0 . 1 3 5 6

1 9 7 6 . 1 2 0 . 9 7 1 8 0 . 9 9 7 1 0 . 1 7 5 2 0 . 7 6 2 3 0 . 0 6 2 5

1 9 7 7 . 0 1 0 . 8 9 7 5 0 . 9 6 6 4 0 . 0 4 1 8 0 . 8 6 9 0 0 . 0 8 9 2

1 9 7 7 . 0 2 0 . 8 1 7 8 0 . 9 3 0 1 0 . 0 2 1 7 0 . 8 9 1 2 0 . 0 8 7 1

1 9 7 7 . 0 3 0 . 7 9 5 9 0 . 9 3 4 4 0 . 0 2 3 3 0 . 9 0 1 9 0 . 0 7 4 9

1 9 7 7 . 0 4 0 . 7 5 8 4 0 . 9 0 0 9 0 . 0 1 8 7 0 . 9 1 3 5 0 . 0 6 7 8

1 9 7 7 . 0 5 0 . 7 5 5 5 0 . 8 8 3 5 0 . 0 1 8 4 0 . 9 2 3 0 0 . 0 5 8 6

1 9 7 7 . 0 6 0 . 7 9 1 1 0 . 8 8 7 4 0 . 0 1 9 4 0 . 9 3 3 0 0 . 0 4 7 6 ‘

1 9 7 7 . 0 7 0 . 8 4 9 6 0 . 9 2 6 4 0 . 0 2 0 5 0 . 9 4 3 9 0 . 0 3 5 5

1 9 7 7 . 0 8 0 . 8 7 2 0 0 . 9 3 5 1 0 . 0 1 5 1 0 . 9 5 5 5 0 . 0 2 9 4 ‘

1 9 7 7 . 0 9 0 . 9 1 6 8 0 . 9 5 5 5 0 . 0 1 5 4 0 . 9 6 2 9 0 . 0 2 1 7

1 9 7 7 . 1 0 0 . 9 9 6 4 0 . 9 9 9 0 0 . 0 3 3 3 0 . 9 6 5 0 0 . 0 0 1 7

1 9 7 7 . 1 1 0 . 9 5 7 3 0 . 9 5 9 2 0 . 0 0 9 9 0 . 9 8 2 7 0 . 0 0 7 4

1 9 7 7 . 1 2 0 . 9 9 7 6 0 . 9 9 8 3 0 . 0 2 0 8 0 . 9 7 8 5 0 . 0 0 0 7

1 9 7 8 . 0 1 0 . 9 4 1 7 0 . 9 4 3 0 0 . 0 1 3 1 0 . 9 8 2 2 0 . 0 0 4 7

1 9 7 8 . 0 2 0 . 6 7 8 9 0 . 5 5 9 2 0 . 0 0 7 5 0 . 9 8 1 7 0 . 0 1 0 7 .

1 9 7 8 . 0 3 0 . 5 3 9 1 0 . 3 5 7 6 0 . 0 0 9 2 0 . 9 7 8 6 0 . 0 1 2 2

1 9 7 8 . 0 4 0 . 5 6 2 8 0 . 3 6 6 0 0 . 0 0 6 7 0 . 9 8 1 3 0 . 0 1 2 0 |

1 9 7 8 . 0 5 0 . 7 0 4 7 0 . 5 3 3 0 0 . 0 0 7 7 0 . 9 8 3 3 0 . 0 0 9 1 ;

1 9 7 8 . 0 6 0 . 9 3 2 9 0 . 9 2 0 2 0 . 0 1 1 1 0 . 9 8 5 4 0 . 0 0 3 5

1 9 7 8 . 0 7 0 . 9 9 2 3 0 . 9 9 6 1 0 . 0 1 1 3 0 . 9 8 7 9 0 . 0 0 0 8

1 9 7 8 . 0 8 0 . 9 7 0 4 0 . 9 7 5 2 0 . 0 0 5 7 0 . 9 9 2 3 0 . 0 0 2 1

1 9 7 8 . 0 9 0 . 9 8 2 1 0 . 9 9 8 4 0 . 0 0 7 7 0 . 9 9 0 6 0 . 0 0 1 8

1978.10 0.9997 0.9996 0.0234 0.9765 0.0001 1 9 7 8 . 1 1 0 . 9 7 3 7 0 . 9 4 6 2 0 . 0 2 9 4 0 . 9 6 8 8 0 . 0 0 1 8

1 9 7 8 . 1 2 0 . 9 9 4 8 0 . 9 9 6 3 0 . 0 1 7 2 0 . 9 8 2 2 0 . 0 0 0 6

1 9 7 9 . 0 1 0 . 9 1 1 4 0 . 8 7 9 7 0 . 0 0 6 3 0 . 9 8 9 9 0 . 0 0 3 9

1 9 7 9 . 0 2 0 . 9 4 7 2 0 . 9 4 5 6 0 . 0 0 6 3 0 . 9 9 1 0 0 . 0 0 2 7

1 9 7 9 . 0 3 0 . 9 6 2 0 0 . 9 7 7 0 0 . 0 0 6 9 0 . 9 9 1 0 0 . 0 0 2 1

1 9 7 9 . 0 4 0 . 9 1 7 0 0 . 9 1 3 4 0 . 0 0 4 9 0 . 9 9 1 8 0 . 0 0 3 2

1 9 7 9 . 0 5 0 . 9 4 2 9 0 . 9 4 0 9 0 . 0 0 6 2 0 . 9 9 0 9 0 . 0 0 2 9

1 9 7 9 . 0 6 0 . 9 9 8 9 0 . 9 9 9 2 0 . 0 1 7 6 0 . 9 8 2 2 0 . 0 0 0 2

1 9 7 9 . 0 7 0 . 9 9 7 7 0 . 9 9 9 0 0 . 0 2 9 0 0 . 9 7 0 6 0 . 0 0 0 4

1 9 7 9 . 0 8 0 . 7 7 4 3 0 . 7 5 2 5 0 . 0 0 9 7 0 . 9 7 3 1 0 . 0 1 7 2

1 9 7 9 . 0 9 0 . 7 0 1 2 0 . 6 6 7 4 0 . 0 0 9 0 0 . 9 7 1 1 0 . 0 2 0 0

1 9 7 9 . 1 0 0 . 7 8 2 3 0 . 7 6 9 8 0 . 0 2 2 5 0 . 9 6 3 9 0 . 0 1 3 6

1 9 7 9 . 1 1 0 . 9 9 8 1 0 . 9 9 9 1 0 . 0 3 1 9 0 . 9 6 7 8 0 . 0 0 0 3

1979.12 0.9784 0.9783 0.0096 0.9865 0.0039 1 9 8 0 . 0 1 0 . 9 6 9 4 0 . 9 7 9 4 0 . 0 0 8 5 0 . 9 8 7 4 0 . 0 0 4 1

1 9 8 0 . 0 2 0 . 9 2 3 2 0 . 9 3 6 5 0 . 0 0 7 3 0 . 9 8 6 6 0 . 0 0 6 1 ••

54 .

1 9 8 0 . 0 3 0 . 8 9 9 9 0 . 9 1 4 2 0 . 0 1 3 9 0 . 9 7 9 8 0 . 0 0 6 3

1 9 8 0 . 0 4 0 . 9 9 6 9 0 . 9 9 7 9 0 . 0 2 3 3 0 . 9 7 5 4 0 . 0 0 1 2

1 9 8 0 . 0 5 0 . 9 9 1 3 0 . 9 9 0 0 0 . 0 2 4 5 0 . 9 6 9 3 0 . 0 0 6 1

1 9 8 0 . 0 6 0 . 9 5 7 3 0 . 9 7 0 7 0 . 0 2 4 9 0 . 9 5 5 8 0 . 0 1 9 2

1 9 8 0 . 0 7 0 . 9 0 4 2 0 . 9 2 9 8 0 . 0 1 9 8 0 . 9 4 3 7 0 . 0 3 6 5

1 9 8 0 . 0 8 0 . 9 4 2 3 0 . 9 8 4 6 0 . 0 5 2 7 0 . 9 0 8 6 0 . 0 3 8 7 ‘

1 9 8 0 . 0 9 0 . 8 8 8 1 0 . 9 4 2 1 0 . 0 4 3 7 0 . 8 7 9 1 0 . 0 7 7 2

1 9 8 0 . 1 0 0 . 8 8 8 2 0 . 9 5 9 9 0 . 1 0 6 3 0 . 8 0 2 8 0 . 0 9 0 9

1 9 8 0 . 1 1 0 . 7 4 9 0 0 . 8 1 7 8 0 . 0 6 3 1 0 . 7 5 7 2 0 . 1 7 9 7

1 9 8 0 . 1 2 0 . 7 8 2 0 0 . 8 3 0 6 0 . 0 8 3 3 0 . 7 0 7 7 0 . 2 0 9 0 ‘

1 9 8 1 . 0 1 0 . 7 5 6 7 0 . 7 4 2 4 0 . 1 0 9 9 0 . 6 3 5 4 0 . 2 5 4 6

1 9 8 1 . 0 2 0 . 7 5 9 1 0 . 6 8 7 9 0 . 4 9 5 1 0 . 3 0 8 2 0 . 1 9 6 7 •

1 9 8 1 . 0 3 0 . 6 9 2 0 0 . 5 8 9 5 0 . 2 7 0 9 0 . 2 3 0 8 0 . 4 9 8 3

1 9 8 1 . 0 4 0 . 3 6 3 6 0 . 2 0 3 2 0 . 1 3 3 6 0 . 1 5 9 5 0 . 7 0 6 9

1 9 8 1 . 0 5 0 . 2 3 5 4 0 . 0 8 8 2 0 . 0 6 5 3 0 . 1 3 5 4 0 . 7 9 9 3

1 9 8 1 . 0 6 0 . 2 2 6 7 0 . 0 4 9 8 0 . 1 4 1 7 0 . 1 0 2 1 0 . 7 5 6 2

1 9 8 1 . 0 7 0 . 2 2 5 8 0 . 0 5 4 3 0 . 0 6 1 0 0 . 0 9 7 8 0 . 8 4 1 3

1 9 8 1 . 0 8 0 . 3 1 8 1 0 . 1 4 2 1 0 . 0 4 0 1 0 . 0 9 8 3 0 . 8 6 1 6

1 9 8 1 . 0 9 0 . 4 9 0 1 0 . 2 6 9 1 0 . 0 5 7 1 0 . 0 9 8 4 0 . 8 4 4 5

1 9 8 1 . 1 0 0 . 9 2 0 0 0 . 8 3 5 9 0 . 4 1 4 3 0 . 0 9 0 5 0 . 4 9 5 2 !

1 9 8 1 . 1 1 0 . 9 9 7 6 0 . 9 9 8 9 0 . 9 6 1 5 0 . 0 2 4 6 0 . 0 1 3 9

1 9 8 1 . 1 2 0 . 4 5 3 2 0 . 4 7 0 4 0 . 1 0 1 0 0 . 0 1 6 1 0 . 8 8 2 8

1 9 8 2 . 0 1 0 . 2 6 0 0 0 . 3 0 9 9 0 . 0 4 1 8 0 . 0 1 1 0 0 . 9 4 7 2

1 9 8 2 . 0 2 0 . 1 6 0 3 0 . 1 7 7 4 0 . 0 3 7 6 0 . 0 0 7 6 0 . 9 5 4 8

1 9 8 2 . 0 3 0 . 1 5 0 0 0 . 1 4 3 2 0 . 0 3 2 9 0 . 0 0 6 4 0 . 9 6 0 6

1 9 8 2 . 0 4 0 . 1 9 4 0 0 . 1 8 7 3 0 . 0 5 9 8 0 . 0 0 5 3 0 . 9 3 5 0

1 9 8 2 . 0 5 0 . 1 8 0 3 0 . 1 6 6 5 0 . 0 5 4 4 0 . 0 0 4 1 0 . 9 4 1 5

1 9 8 2 . 0 6 0 . 1 2 5 9 0 . 1 0 5 7 0 . 0 3 3 6 0 . 0 0 3 3 0 . 9 6 3 1

1 9 8 2 . 0 7 0 . 1 3 7 3 0 . 1 1 9 3 0 . 0 5 0 6 0 . 0 0 2 8 0 . 9 4 6 6

1 9 8 2 . 0 8 0 . 1 0 6 8 0 . 0 7 8 6 0 . 0 3 5 0 0 . 0 0 2 6 0 . 9 6 2 4

1 9 8 2 . 0 9 0 . 0 8 9 9 0 . 0 7 4 4 0 . 0 3 1 3 0 . 0 0 2 5 0 . 9 6 6 2

1 9 8 2 . 1 0 0 . 0 9 5 4 0 . 0 8 9 9 0 . 0 3 4 0 0 . 0 0 2 6 0 . 9 6 3 3

1 9 8 2 . 1 1 0 . 1 1 0 3 0 . 0 9 5 1 0 . 0 3 7 5 0 . 0 0 3 1 0 . 9 5 9 4

1 9 8 2 . 1 2 0 . 1 9 0 7 0 . 1 6 3 8 0 . 0 5 6 7 0 . 0 0 4 4 0 . 9 3 8 9

1 9 8 3 . 0 1 0 . 2 2 9 6 0 . 1 8 9 4 0 . 0 7 1 0 0 . 0 0 6 1 0 . 9 2 2 9

1 9 8 3 . 0 2 0 . 3 4 2 6 0 . 3 5 0 0 0 . 0 4 8 8 0 . 0 1 1 3 0 . 9 4 0 0

1 9 8 3 . 0 3 0 . 5 0 9 5 0 . 5 1 9 3 0 . 0 9 1 2 0 . 0 1 5 1 0 . 8 9 3 7

1 9 8 3 . 0 4 0 . 9 9 2 6 0 . 9 9 8 2 0 . 9 1 3 4 0 . 0 1 7 9 0 . 0 6 8 7

1 9 8 3 . 0 5 0 . 9 5 3 3 0 . 9 6 8 3 0 . 5 5 1 6 0 . 0 2 9 7 0 . 4 1 8 7

1 9 8 3 . 0 6 0 . 5 7 1 7 0 . 5 2 3 1 0 . 1 1 8 2 0 . 0 2 1 3 0 . 8 6 0 6

1 9 8 3 . 0 7 0 . 4 2 1 5 0 . 3 7 5 2 0 . 0 4 8 0 0 . 0 1 8 2 0 . 9 3 3 7

1983.08 0.3293 0.2758 0.0344 0.0161 0.9495 t.

55

1983.09 0.3396 0.2866 0.0547 0.0142 0.9311 1983.10 0.3229 0.2658 0.0509 0.0126 0.9365 1983.11 0.2936 0.2241 0.0324 0.0118 0.9558 1983.12 0.3655 0.2930 0.0401 0.0115 0.9484 1984.01 0.5134 0.4311 0.0929 0.0109 0.8962 1984.02 0.9692 0.9829 0.9406 0.0035 0.0559 ‘ 1984.03 0.4070 0.3306 0.0909 0.0032 0.9059 1984.04 0.2014 0.1261 0.0364 0.0020 0.9616 1984.05 0.1370 0.0746 0.0367 0.0013 0.9620 1984.06 0.0858 0.0386 0.0298 0.0009 0.9693 �

1984.07 0.0749 0.0319 0.0344 0,0007 0.9648 1984.08 0.1029 0.0842 0.0583 0.0006 0.9411 ‘ 1984.09 0.0707 0.0421 0.0536 0.0004 0.9460 1984.10 0.0599 0.0292 0.0304 0.0005 0.9691 1984.11 0.0721 0.0324 0.0313 0.0006 0.9682 1984.12 0.0958 0.0370 0.0340 0.0007 0.9652 1985.01 0.1808 0.0767 0.0340 0.0013 0.9647 1985.02 0.4015 0.2625 0.0967 0.0022 0.9012 1985.03 1.0000 1.0000 0.9981 0.0019 0.0000 1985.04 0.9694 0.9584 0.1615 0.6016 0.2369 | 1985.05 0.9872 0.9872 0.1351 0.6871 0.1778 \ 1985.06 0.9882 0.9848 0.1246 0.7217 0.1537 1985.07 1.0000 1.0000 0.3324 0.6676 0.0000 1 9 8 5 . 0 8 0 . 8 9 2 4 0 . 8 5 3 6 0 . 0 5 1 1 0 . 8 7 4 7 0 . 0 7 4 2

1985.09 0.9150 0.8989 0.0341 0.9102 0.0557 1985.10 0.9805 0.9899 0.0505 0.9307 0.0188 1985.11 0.9652 0.9761 0.0262 0.9580 0.0158 1985.12 0.8070 0.7168 0.0100 0.9671 0.0229 1986.01 0.8157 0.7171 0.0107 0.9699 0.0194 1986.02 0.9877 0.9939 0.0252 0.9718 0.0030 1986.03 0.9801 0.9800 0.0103 0.9850 0.0047 1986.04 0.9916 0.9965 0.0180 0.9800 0.0020 1 9 8 6 . 0 5 0 . 8 7 4 7 0 . 8 5 8 1 0 . 0 1 2 6 0 . 9 7 8 3 0 . 0 0 9 1