RIGHT SOLUTIONS | RIGHT PARTNER 2013-14 Full Year Result Investor Presentation May 2014 Greg Kilmister – CEO Paul McPhee – Group General Manager Energy Division For personal use only

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RIGHT S O L U T I O N S | RIGHT PARTNER

2013-14 Full Year Result

Investor Presentation

May 2014

Greg Kilmister – CEO

Paul McPhee – Group General Manager Energy Division

For

per

sona

l use

onl

y

• This presentation has been prepared by ALS Limited, (ALS or the Company). It contains general information

about the Company’s activities as at the date of the presentation. It is information given in summary form and

does not purport to be complete. The distribution of this presentation in jurisdictions outside Australia may be

restricted by law, and you should observe any such restrictions.

• This presentation is not, and nothing in it should be construed as, an offer, invitation or recommendation in

respect of securities, or an offer, invitation or recommendation to sell, or a solicitation of an offer to buy,

securities in any jurisdiction. Neither this document nor anything in it shall form the basis of any contract or

commitment. This presentation is not intended to be relied upon as advice to investors or potential investors

and does not take into account the investment objectives, financial situation or needs of any investor. All

investors should consider such factors in consultation with a professional advisor of their choosing when

deciding if an investment is appropriate.

• The Company has prepared this presentation based on information available to it, including information

derived from public sources that have not been independently verified. No representation or warranty, express

or implied, is provided in relation to the fairness, accuracy, correctness, completeness or reliability of the

information, opinions or conclusions expressed herein.

• This presentation includes forward-looking statements within the meaning of securities laws. Any forward-

looking statements involve known and unknown risks and uncertainties, many of which are outside the control

of the Company and its representatives. Forward-looking statements may also be based on estimates and

assumptions with respect to future business decisions, which are subject to change. Any statements,

assumptions, opinions or conclusions as to future matters may prove to be incorrect, and actual results,

performance or achievement may vary materially from any projections and forward-looking statements.

• Due care and attention should be undertaken when considering and analysing the financial performance of the

Company.

• All references to dollars are to Australian currency unless otherwise stated.

IMPORTANT NOTICE AND DISCLAIMER

2RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Company Profile

ALS Limited (ASX:ALQ) is an ASX 100 company that provides professional technical services to

the global Metals & Mining, Life Sciences, Oil & Gas, and Industrial sectors throughout the

world. The Reward business is an Australian distributer of non-perishable hospitality supplies.

Energy Division

Industrial Division

Life Sciences Division

Minerals Division

Reward Distribution

Environmental

Food - Pharma

Electronics

Consumer Products

Geochemistry

Metallurgy

Inspection

Mine Site Services

Asset Care

Tribology

Coal

Oil & Gas

Market Capitalisation

$3.1 bn

People

12,000

Revenue

$1.5 bn

EPS

45 cents

Dividend

39 cents

3RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

OHS&E

4RIGHT SOLUTIONS | RIGHT PARTNER

Act ual

Score

PPI Tot al

Available

PPI

Achievement

4.98 6.25 6.25

1.78 6.25 6.25

10.24 6.25 0.00

842.00 6.25 6.25

3.00 12.50 12.50

2.00 12.50 12.50

0.97 12.50 12.50

0.98 12.50 12.26

0.98 12.50 12.24

1.02 12.50 12.50

93.25

Injury

Injury

Lost Time Injury Frequency Rate

(LTIFR) for chosen level

Average days lost per Lost Time

Injury (days)

2.00

10.00

Injury

Leadership

Leadership

Near Miss Report Submitted (2 per

year)

Number of Presentations of a safety

topic to staff (base employees and

management)

Manager participation in site safety

inspections (count)

2.00

Program

Program

Training

Close out of incident reports

reported on compliance portal (%)

Close out of Annual Compliance Sign-

off Corrective Actions (%)

New Employees completing

induction training including safety

components as outlined in ALS

minimum standard (%)

Total

Completion of Compliance Training

Sessions on PULSE (%)

ALS Group Compliance Portal

PPI Chart

Profile: ALS LimitedFinancial Year: April 2013 – March 2014Total Score: 93.25%

PPI Met ric Descript ion

Total recordable injury frequency

rate (TRIFR) for chosen level

Target

Score

5.90

Met ric

Injury

2.00

2.00

0.90

1.00

1.00

1.00Training

1.8

0

2

4

6

8

10

12

14

FY

2006

FY

2007

FY

2008

FY

2009

FY

2010

FY

2011

FY

2012

FY

2013

FY

2014

Group LTIFR

ASX top 100 average = 3.6

16.0

11.49.5

0

5

10

15

20

FY 2012 FY 2013 FY 2014

Severity rate- Average days lost per LTI

LTIFR = Lost Time Injuries per million hours worked

For

per

sona

l use

onl

y

Financial Summary

AUD$mn

FY14

Statutory

Significant

Differences1

FY14

Underlying

FY13

Underlying2

Change in

Underlying

Revenue 1503.4 0 1503.4 1455.6 +3.3%

EBITDA 325.7 (13.3) 339.0 406.0 -16.5%

Depreciation &

Amortisation(83.2) (7.0) (76.2) (55.4) +37.5%

EBIT 242.5 (20.3) 262.8 350.6 -25.0%

Finance Costs (26.8) (26.8) (19.6) +36.7%

Tax Expense (59.1) 2.8 (61.9) (89.5) -30.8%

Net Profit After Tax 154.4 (17.5) 171.9 238.3 -27.9%

Basic EPS (cents) 40.7 45.3 69.7 -35.0%

1Acquisition costs, Restructuring and other one-off costs, Amortisation of Intangibles, Divestments and Impairments

2Excluding discontinued operations (Deltrex and Panamex)

5RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

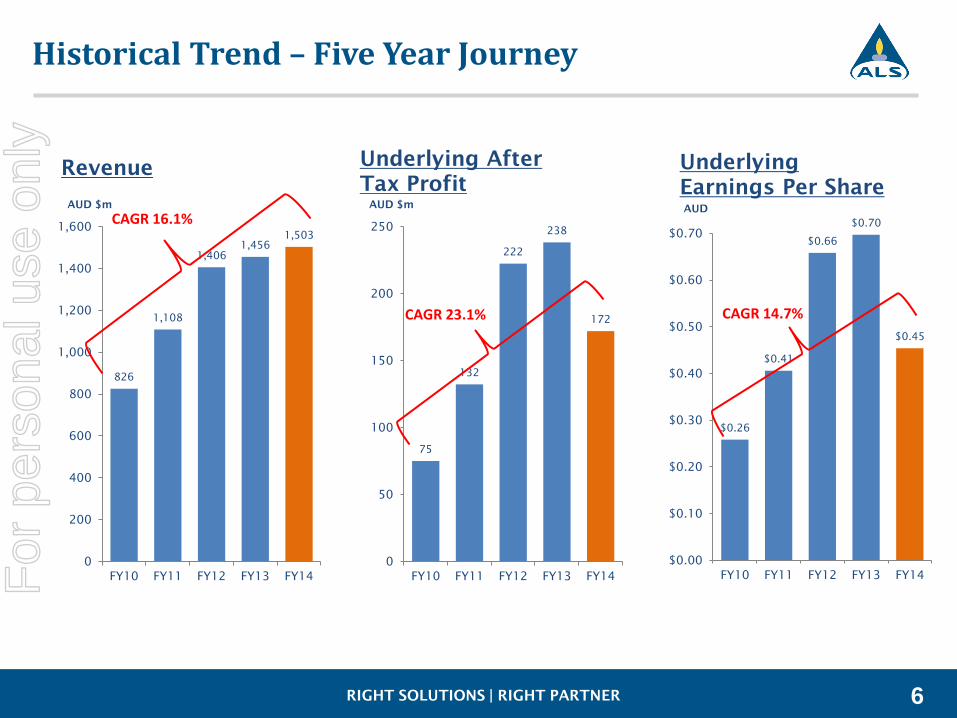

Historical Trend – Five Year Journey

826

1,108

1,406

1,456

1,503

0

200

400

600

800

1,000

1,200

1,400

1,600

FY10 FY11 FY12 FY13 FY14

AUD $m

Revenue

CAGR 16.1%

75

132

222

238

172

0

50

100

150

200

250

FY10 FY11 FY12 FY13 FY14

AUD $m

Underlying After

Tax Profit

CAGR 23.1%

$0.26

$0.41

$0.66

$0.70

$0.45

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

FY10 FY11 FY12 FY13 FY14

AUD

Underlying

Earnings Per Share

CAGR 14.7%

6RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

FY14 – Revenue by Region by Division

North America

South America

Europe

Africa

Middle East

Asia

Australia

Life Sciences Division

Minerals Division

Energy Division

Industrial Division

Reward Distribution

7RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Foreign Currency Revenues

47%

21%

15%

5%

3%

3%3%3%

AUD

42%

USD

22%

CAD

14%

EURO

6%

GBP

7%

Krona

3%

ZAR

2%

Asia

4%

FY2014 revenue

AUD $1.503 billion

Average Exchange Rate

FY2014 FY2013 Change

USD 0.9235 1.0323 -10.5%

CAD 0.9776 1.0354 -5.6%

EURO 0.6880 0.8016 -14.2%

GBP 0.5796 0.6536 -11.3%

SEK 6.0287 6.8819 -12.4%

ZAR 9.3955 8.8238 +6.5%

SGD 1.1639 1.2806 -9.1%

Note: Krona includes SEK, NOK, DKK & FMM

Asia includes HKD, SGD, THB, MYR, IDR, CYN & TWD

Outer annulus FY14, Inner annulus FY13

8RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

ALS (laboratories) Revenue Growth

• Organic Growth -18.0%

• Acquired Growth +17.5%

• Currency Impact +4.1%

Reported Growth 3.6%

0

250

500

750

1000

1250

Reven

ue (A

UD

$m

n)

Revenue Growth - laboratories

9

-40% -30% -20% -10% 0% 10% 20% 30% 40%

Minerals

Life Sciences

Energy

Industrial

Revenue Growth YoY

Organic Acquired FX Movement

+100%

RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

9

13

1921

19

11

15

26

27

20

0

10

20

30

40

50

FY10 FY11 FY12 FY13 FY14

AUD

cents

Dividend

Full Year Dividend per Share

18% CAGR

• Payout ratio 93%

• Franked to 50%

• Dividend Reinvestment Plan

retained at 5% discount

10RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

CAPEX (excluding land & building purchases) and Depreciation

11

$0

$5

$10

$15

$20Mill

ion

s

CAPEX Vs Depreciation & Amortisation1

Minerals Life Sciences Industrial Energy

CAPEX as a % of D&A

22% 91% 126% 70% 71% 58% 106% 64%

• Capacity CAPEX reduced substantially

in line with market conditions

• Replacement CAPEX being maintained

for inevitable market upswing

• Research and Development CAPEX

being maintained

• Higher near-future CAPEX required in

Oil & Gas and Food businesses during

the development phase

• Stronger business stream focus on

Return on Capital Employed

• Most major (hub) laboratory upgrades

now completed allowing footprint for

significant future capacity increases

1Amortisation does not include amortisation of goodwill

Reservoir Group acquired--

RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

0

50

100

150

200

250

300

350

400

450

EBITDA Cash

Flow

EBITDA Cash

Flow

. EBITDA Cash

Flow

AUD$m

Cash Flow

Underlying EBITDA $328mn -19%

Operating Cash Flow $346mn -6%

CAPEX (excl. land & buildings) $68mn -16%

FY12 FY13 FY14

Cash Flow and Funding

Mar-14 Mar-13

Statistics

Gearing Ratio Comfort 45% 33.9% 29.3%

Leverage (net debt / EBITDA) Max 3.00 2.2 1.0

EBITDA interest cover Min 3.75 12.2 20.7

Balance Sheet Measures ($ mn)

Total Equity 1,419 997

Net debt 729 413

0

50

100

150

200

250

300

2014 2015 2016 2017 2018 2019 2020 2021 2022

AUD$m

Debt Maturity

21%

6%

3%

23%

26%

21%

12RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Q1FY12

Q2FY12

Q3FY12

Q4FY12

Q1FY13

Q2FY13

Q3FY13

Q4FY13

Q1FY14

Q2FY14

Q3FY14

Q4FY14

Environmental Food/Pharma Consumer Products Geochemistry

Metallurgy Inspection Engineering Coal Oil & Gas

Asset Care Tribology Reward Distribution

Employee Numbers - total head count

• Mineral Division head count down by 46%

from peak in June 2012…but expertise and

management structure retained

• Life Sciences Division head count growing as

we enter new geographies (South America,

United Kingdom) and develop Food/Pharma

footprint

• Coal business stream head count down by

38% from peak in September 2012…but

underlying capabilities and service coverage

maintained

• +1000 staff added due to move into the Oil

& Gas sector

Africa

Asia

Australia

Europe

Middle East

North America

South America

13RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Margin – peer comparison

18.8%

16.8% 16.7%

15.7%

13.2%

5.8%

31.1%

24.3%

21.9%

20.5%

19.0%

15.4%

12.9%

33.4%

0%

5%

10%

15%

20%

25%

30%

35%

ALS SGS B.V. Intertek Eurofins Mistras Core Labs

EBIT EBITDA

Note: FY Dec 13 for all companies excluding ALS (FY Mar 14) and MISTRAS (FY Jun 13)

EBIT and EBITDA underlying margins

Data from company reports

14RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

0

200

400

600

800

1,000

1,200

1,400

1,600

0

200

400

600

800

1,000

1,200

1,400

1,600

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Cum

ulative N

et M

&A

Spend $

million

PealStreet Ltd.

Dec-09

Ecowise

Environmental

Pty Ltd..

Nov-09

Campbell

Brothers Ltd.,

Major Laundry

& Detergent

Brands

Oct-04

QCC

Hospitality

Aug-04

Ecochem

Jan-06

ETL Group

Jan-06

Caterworld

Jan-06

QCC

Hospitality

Jun-05

McCarthys

Feb-07

Campbell

Brothers Ltd.,

Pest Control &

Washroom

Services

Jan-07

Consulchem

Nov-06

Abilab

Nov-06

Pandee

Services

Sep-06

Analytica AB

Jul-06

Witlab

Nov-07

ACIRL Pty Ltd

Oct-07

eLab

Analytical Inc.

Aug-07

JK Tech

Mineralogy

Aug-07

DataChem

Oct-08

IQA

May-08

Stavely

Services

May-08

Microtech

Technical

Services Ltd.

Apr-08

Analytical

Laboratory

Services Inc.

Dec-10

Ammtec Ltd.

Nov-10

Campbell

Brothers

Limited

Cleantec

Business

Nov-10

LabMark

Environmental

Laboratories

May-10

Columbia

Analytical

Services

Nov-11

Austpower

Engineering.

Oct-11

PearlStreet

Energy

Services

Jul-11

Stewart Group

Jul-11

PMS Micro

Jun-11

Severn Trent

Laboratories

Feb-13

Corplab

Laboratories.

Dec-12

Panamex

Pacific

Oct-12

Deltrex

Chemicals

Sep-12

Artek

Laboratories

Aug-12

Milana A.S.

Jul-12

Eclipse

Scientific

Group

Apr-12

BMP

Enterprises

Feb-14

ALS Taiwan

Jan-14

OilCheck Pty

Ltd.

Oct-13

AIT

Oct-13

Reservoir

Group Ltd.

Aug-13

PSI Inc.

Aug-13

EarthData Pty

Ltd.

Jul-13

Reliance

May-13

Environmental Food/Pharma Consumer Products Geochemistry Metallurgy Inspection Engineering Oil & Gas

Coal Asset Care Tribology Reward Distribution Chemical Campbell Brothers Services

FY2005

revenue

$448m

FY2009

revenue

$951m

FY2014

revenue

$1,503m

Revenue $

million

Acquisition

Divestment

ALS journey over the last decade

15RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

-

200

400

600

800

1,000

1,200

1,400

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

AU

D$

m

illio

ns

-

50

100

150

200

250

300

350

400

450

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

AU

D$

m

illio

ns

Growth of non-Minerals Divisions

Life Sciences Energy Industrial Minerals

Lab Services Revenue Lab Services EBITDA

The non-Minerals revenue of ALS lab services is now more than ALS’ entire lab services revenue just three

years ago

Non-Mineral EBITDA margin

21% 21% 24% 20% 24% 23% 25% 25% 24%

16RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Overview

• Geochemistry EBIT margin 26.0% for full year

• Rationalization of Hub and Spoke laboratories to protect

margin

• Inspection EBIT margin improved from 9.5% to 20.3% YoY

• New metallurgical facility in Santiago (Chile) fully

operational

• Joint Venture Inspection business established in Tianjin

(China) now fully operational

• Mine Site strategy working

Outlook

• Improved margin performance in Metallurgy and

Inspection in FY15

• Geochemical sample flow to be down in H1FY15 pcp

before recovering in H2 to be flat pcp for full year

• Increase in market share due to new services and cyclical

recovery in H2

• Pricing to remain flat

• Focus on better data management/presentation for

clients

• Pipeline of Mine Site opportunities remains strong

2014 2013 Change

Revenue $426mn $608mn -30%

EBITDA $126mn $234mn -46%

EBIT $102mn $212mn -52%

EBIT Margin 24.0% 34.9%

Minerals Division

0

100

200

300

400

500

600

FY09 FY10 FY11 FY12 FY13 FY14

Revenue (A

UD

$m

n)

Geochemistry Metallurgy Inspection Other

17

geochemistry

metallurgy

inspection

mine site services

RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Overview

• Pricing pressure in Australia and Canada

• 6% organic growth in environmental revenue in Europe

• Operational issues in South America fixed

• Centre of Excellence (GLP laboratory) in Edmonton closed

• Exited Taiwan market

• New laboratory in Beijing - China

• New global Food LIMS and client portal developed

• Food/Pharma revenue grew 10% to $57mn

Outlook

• US market to continue improving

• New hub food chemistry lab to open in England in June

2014

• Focus on growing business in Latin America

• Acquisitions in the food sector

• Geographic expansion of environmental business

2014 2013 Change

Revenue $527mn $454mn +16%

EBITDA $124mn $114mn +9%

EBIT $94mn $90mn +5%

EBIT Margin 17.9% 19.9% -200bps

Life Sciences Division

0

100

200

300

400

500

600

FY10 FY11 FY12 FY13 FY14

Revenue (A

UD

$m

n)

Asia Australia Europe North America South America

CAGR 20.3%

18

environmental

food/pharma

electronics

consumer products

RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Overview

• Successful acquisition and integration of the Reservoir

Group and EarthData

• Operations in 60 countries with 1,650 staff

• Coring – soft in North America in Q4FY14

• Oil & Gas EBITDA 25.3% - weaker than expected

Outlook

• Australian coal market to remain challenging

• Oil & Gas operations to balance exploration Vs

production

• Margin improvement in Oil & Gas as integration benefits

flow

• Australian coal production and exports expected to grow

• Integration of Oil & Gas service offerings and geographic

leverage

2014 2013 Change

Revenue $248mn $105mn +136%

EBITDA $69.2mn $36.1mn +92%

EBIT $53.5mn $32.6mn +64%

EBIT Margin 21.6% 31.1% -950bps

Energy Division

0

50

100

150

200

250

FY10 FY11 FY12 FY13 FY14

Revenue (A

UD

$m

n)

Asia Australia Europe

North America South America Africa

Middle East

19

coal

oil & gas

RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Overview

• Revenue mix shifted from “outage” to construction

• Australian market price sensitivity impacted margins

• Declining power and welding & fabrication markets -

higher margin work

• Significant mobilization costs for LNG projects

• strong recovery in H2

• third LNG project secured in Feb-14

• Demand for in-service plant inspection continued to

grow

• Epicor (Asset Care LIMS) rolled out to 90% of sites

• OilCheck and AIT integrations completed

Outlook

• Restructured Asset Care business along market segment

lines cf. geographies - creating better focus and client

alignment

• Australian market to remain challenging

• Mining sector very cost focused

• Leveraging capabilities of AIT into Australian

construction projects

• Tribology to continue growing in line with previous years

2014 2013 Change

Revenue $183mn $169mn +8%

EBITDA $31.6mn $35.4mn -11%

EBIT $26.4mn $30.7mn -14%

EBIT Margin 14.4% 18.2% -380bps

Industrial Division

0

40

80

120

160

200

FY10 FY11 FY12 FY13 FY14

Revenue (A

UD

$m

n)

Australia South America North America

20

asset care

tribology

RIGHT SOLUTIONS | RIGHT PARTNER

For

per

sona

l use

onl

y

Related Documents