Foodservice Industry Seminar 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Foodservice Industry Seminar 2018

Foodservice Solutions

• Since April 2016, Decision Lab is tracking the out of home eating and

drinking market in the key cities Hanoi, Ho Chi Minh City and Da Nang

• The Foodservice Monitor tracks all food & drink consumed out of home

on a daily basis with an annual sample size of 15,000 completed

interviews

• The respondents are Vietnamese consumers aged 15+ who also report

on the consumption by children (under 15 years) who were present at

the eating out occasion

How is Decision Lab tracking Foodservice Consumption?

Methodology

H O W W E T R A C K O U T - O F - H O M E

C O N S U M P T I O N

752,057ONLINE VIETNAMESE COMMUNITY MEMBERS

Annual Sample: 15,000

in HCMC, Hanoi, Danang are asked about what they ate

and drank out of home on the previous day

We cover three main cities HA NOI.

40%

HO CHI MINH

50%

DA NANG

10%

12,387,681

Total

adult population(Vietnamese aged 15 years old and above in

HCMC, Hanoi, Danang)

The data is extrapolated based on the GSO’s yearly population projection

HA NOI.

5,204,798

HO CHI MINH

6,432,322

DA NANG

750,561

FULL SERVICE

RESTAURANTS

(FSR)

FINE DINING

Average spend above

VND110K per person). Fine

Dining is segmented by

cuisine type (Vietnamese,

Japanese, Korean, Chinese,

French, Mexican etc..

FAST CASUAL

Average spend under

VND110K per person & pre-

coded chains). Fast Casual is

segmented by cuisine type

(Vietnamese, Japanese,

Korean, Chinese, French,

Mexican etc.), Fast Casual

example chains: Kichi Kichi,

Gogi House, Vietnammm,

Pizza Hut, Mon Hue, Thai

Express etc..

We monitor 7 Main Channels

QUICK SERVICE

RESTAURANTS

(QSR)

QS COFFEE/TEA

(Highlands Coffee,

Starbucks etc.)

QS BURGER

(McDonald’s, Burger King,

Lotteria etc.)

QS CHICKEN

(KFC, Jollibee etc.)

QS

SANDWICHES/WRAPS/

KEBAB/BAKERY

(Subway, Tous Les Jours

etc.)

QS BBQ

QS JAPANESE

QS VIETNAMESE

QS CHINESE

QS THAI

QS INDIAN

QS KOREAN

QS FRENCH

QS MEXICAN

QS PIZZA

(Domino’s, Pizza Inn etc.)

QS ICE CREAM

(Fanny, Baskin Robbins

etc.)

QS JUICE/SMOOTHIE

BAR

(Jamba Juice, Jungle Juice

etc.)

QS OTHER

We monitor 7 Main Channels

STREET FOOD

Food & Drink bought

from:

• Wet market

• Street vendor

• Mobile cart

ALCOHOL

PL ACES

Outlets that mainly

serve alcohol:

• Bar

• Club

• Karaoke

CONVENIENCE

STORES

Standard convenience

store such as

FamilyMart, 7-Eleven

that also offers meals

(some heated up) to

eat on- or off-premise

HOTELS

Establishments

providing

accommodation,

meals, and other

services for travelers

and tourists.

CANTEEN

• Workplace

• School

• University

We monitor 7 Main Channels

Track record in F&B industry

How has 2018 been for Vietnam’s Foodservice

industry?

L E T ’ S T A K E A L O O K !

Vietnam

Foodservice

Monitor

KEY INDICATORS FOR YEAR

ENDING Q3 2018

AVERAGE EATER SPENDING/ VISIT (IN VND)

31.4T33.7T

31.6T

26.0T28.0T

30.2T 29.7T

25.6T

31.6T27.6T

436M 443M 453M418M 435M

478M 474M452M

496M 492M

300M

350M

400M

450M

500M

550M

600M

650M

700M

750M

800M

T

5T

10T

15T

20T

25T

30T

35T

40T

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

Sales Visits

AVERAGE ANNUAL VISITS / CAPITA

HANOI

61,771 4%

HCMC

59,929 9%

DA NANG

49,236 15%

TOTAL

59,903 8%

HCMC

133 8%

HCMC

170 5%

DA NANG

166 4%

TOTAL

154 5%

The diverging development paths of FSR and QSR

• Market share of FSR & QSR across demographic groups - % visits

34%

24%22%

30%

39%

28%30%

25%28%

25%28%

25%

28%

25%

0%

10%

20%

30%

40%

50%

Male Female 15-24 25-34 35+ Ha Noi HCMC

Gender Age group Location

Full service Restaurants (n = 10,288) Quick service Restaurants (n = 7,293)

Market share of FSR and QSR across demographic groups - % visits

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

14

These two channels currently account for the majority of OOH visits by consumers across all demographic groups in Vietnam

• Market share of FSR & QSR - % visits and servings

29%

21%

32%

17%

26%

20%

14%

33%

0%

5%

10%

15%

20%

25%

30%

35%

Total OOH visits Total Non-alcohol RTD

consumption

Total Alcohol

consumption

Total Dairy-based

product consumption

Full service restaurants (n = 10,288) Quick service restaurants (n = 7,293)

Market share of Full Service (FSR) & Quick Service (QSR) restaurants - % visits and servings

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

15

Full service and Quick service restaurants are the two most important channels for Manufacturers of various product categories

• Visits to Full service & Quick service restaurants by quarter (in million)

144M

131M

118M

129M

138M145M

135M

151M

142M

150M 151M

138M 140M

114M

102M98M

122M

109M

50M

70M

90M

110M

130M

150M

170M

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

Full service Restaurants (n = 10,288) Quick service Restaurants (n = 7,293)

Visits to Full Service (FSR) & Quick Service (FSR) restaurants by quarter (in million)

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

16

Meanwhile, Quick service

segment continued to slip away

from its past heyday.

Starting from Q3 2017, Full service restaurants officially took over as the largest Foodservice channel in Vietnam

-21%

+11%

17

The growth of Full service restaurants has been fueled mostly by women, and consumers above 35 years old

7%

20%

12% 12%

3%

12%

4%

20%

8%7%

18%

5%

0%

5%

10%

15%

20%

Male Female Ha Noi HCMC Da Nang 15-24 25-34 35+ Class A Class B Class C Class D

Gender Location Age group SEC

Year over Year Traffic Growth rate of key demographic groups in FSR

n = 10288Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

Channel’s growth

11%

• Visit and Average spending per head per visit to Full service Restaurants

131M

118M

129M

138M

145M135M

151M

142M

89K78K

95K83K 89K 85K 88K

77K

0K

50K

100K

150K

200K

250K

60M

80M

100M

120M

140M

160M

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

Visits Average spending per head per visit

n = 10288

Visit and Average spending per head per visit to Full service Restaurants (FSR)

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

18

Indeed, improving traffic has been the key to the revival of Full service restaurants

-7%

+11%

• YOY Traffic growth of key sub-segments in FSR

19

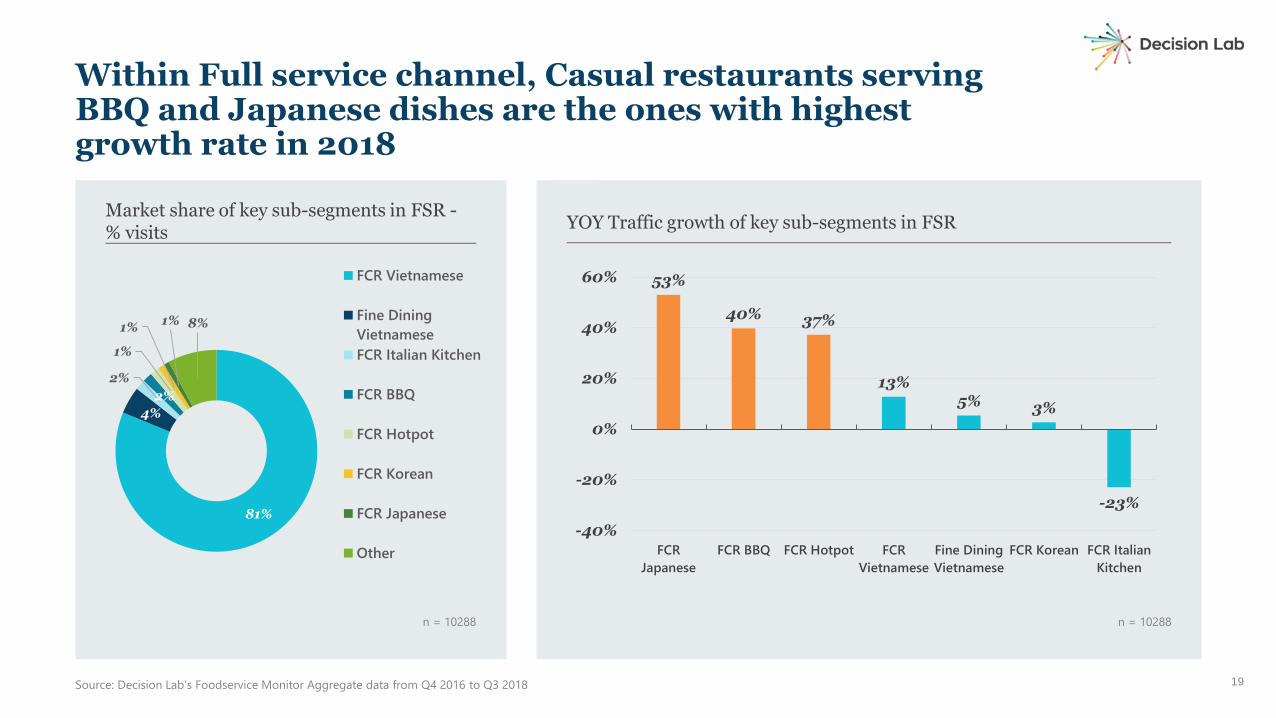

Within Full service channel, Casual restaurants serving BBQ and Japanese dishes are the ones with highest growth rate in 2018

YOY Traffic growth of key sub-segments in FSR

n = 10288

Market share of key sub-segments in FSR -% visits

n = 10288

81%

4%

2%

2%

1%

1%1% 8%

FCR Vietnamese

Fine Dining

Vietnamese

FCR Italian Kitchen

FCR BBQ

FCR Hotpot

FCR Korean

FCR Japanese

Other

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

53%

40% 37%

13%5% 3%

-23%

-40%

-20%

0%

20%

40%

60%

FCR

Japanese

FCR BBQ FCR Hotpot FCR

Vietnamese

Fine Dining

Vietnamese

FCR Korean FCR Italian

Kitchen

20

Meanwhile, Quick service outlets have been suffering from declining visits from all consumer groups, especially the lower middle class and people aged 25+ • Year over Year Traffic Growth rate of key demographic groups in Quick service restaurants

-22%-20% -20%

-18%

-45%

-16%

-23%-25%

-35%

-7%-5%

-32%

-50%

-40%

-30%

-20%

-10%

0%

Male Female Ha Noi HCMC Da Nang 15-24 25-34 35+ Class A Class B Class C Class D

Gender Location Age group SEC

Year over Year Traffic Growth rate of key demographic groups in Quick Service Restaurants (QSR)

n = 7293Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

Channel’s growth

-21%

151M

138M 140M

114M

102M98M

122M

109M

68K58K

51K 54K 50K 52K62K 57K

0K

50K

100K

150K

200K

250K

50M

70M

90M

110M

130M

150M

170M

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

Visits Average spending per head per visit

Visit and Average spending per head per visit to Quick service Restaurants (QSR)

21

It is plummeting footfall that has damaged Quick service restaurants over the past 2 years

Among various types of Quick service outlets, Cafes, Bakeries and Juice/Smoothie shops are those that witness the biggest drop in visits

YOY Traffic growth of key sub-segments in QSR

n = 7293

Market share of key sub-segments in QSR -% visits

n = 7293

32%

25%

22%

8%

5%8%

QS Vietnamese

Coffee/Tea

Bakery

Fast Food

Juice/ Smoothie

Other

-10%

-29%

-22%

-17%

-30%

-40%

-30%

-20%

-10%

0%

QS

Vietnamese Cafes Bakery

Fast Food

restaurants

Juice/

Smoothie

shops

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

258M

329M

0M

100M

200M

300M

400M

Q4 2016 to Q3

2017

Q4 2017 to Q3

2018

This does not mean Vietnamese are cutting down on these products. On the contrary, consumption of coffee, juice, and smoothies has increased in the past year

* Include non-RTD, freshly prepared

drinks only

Coffee beverage* servings

n=2237

* Include non-RTD, freshly prepared

drinks only

Juice & Smoothies* servings

n=2805

Baked goods* servings

n=5206

567M 543M

0M

200M

400M

600M

Q4 2016 to Q3

2017

Q4 2017 to Q3

2018

4%

254M271M

0M

100M

200M

300M

Q4 2016 to Q3

2017

Q4 2017 to Q3

2018

6%

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

*Baked goods include types of

bread, sandwich, cookies, cakes, etc.

27%

Vietnamese are switching to other channels to consume these daily food and drink items, leaving QSR to suffer

*Including Non-RTD, freshly

prepared coffee only

YOY Traffic growth with Coffee* consumption in channels - % visits

n=2237

*Including Non-RTD, freshly

prepared juice/smoothie only

YOY Traffic growth with Juice/Smoothie* consumption in channels - % visits

n=2805

YOY Traffic growth with Baked goods consumption in channels - % visits

n=5206

Source: Decision Lab’s Foodservice Monitor Aggregate data from Q4 2016 to Q3 2018

12%

-29%

39%43%

59%

99%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Total OOH QSR

FSR Street food

CVS Canteen

18%

-9%

20%14%

6%

117%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Total OOH QSR

FSR Street food

CVS Canteen

-3%

-29%

-4%

9%19%

87%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Total OOH QSR

FSR Street food

CVS Canteen

Vietnamese have started to come back to Full

service restaurants

It’s still a tough game for Quick service

restaurants, especially those selling Coffee/ Tea,

Juice/ Smoothie, and Bakeries.

It’s a mixed bag of opportunity and challenges

However, their spending per visits has not really

improved over the past year

➢ Operators do need to re-evaluate the effectiveness

of their promotional campaign and make some

changes that aim at higher consumer spending.

➢ Manufacturers should also look into how to present

and serve your products in a better way that can

bring up the check size.

The problem is not consumers’ declining

consumption of these products. It is the

competition from other low-end channels

➢ It’s highly time to differentiate and communicate to

your core consumer base.

So, what are the key takeaways?

The March of the Women

26

27

“Women are the CEO of the household. They often act as the chief purchasing officer. They purchase on behalf of themselves, but also their husbands and kids.”

Mary Van Note, partner of Ginger Consulting LLC, a Minneapolis-based branding firm

that’s served names in the industry such as Starbucks, McDonald’s, Taco Bell, and

Sonic Drive-In.

The myths about female diners

28

MYTH 1:

Women are more likely to be concerned about health when eating out

Compared to men, a significantly lower proportion of women state “health” as a driver to select a foodservice outlet

16%CHOSE HEALTHY FOOD AND

DRINKS AS THE REASON TO V IS IT

A CERTAIN OOH OUTLET

MEN

12%CHOSE HEALTHY FOOD AND

DRINKS AS THE REASON TO

CHOOSE A CERTAIN OOH OUTLET

WOMEN

Women are also less health-conscious about their food selections than their counterparts

19%CHOSE HEALTH AS THE REASON

OF CERTAIN FOOD CHOICE

MEN

15%CHOSE HEALTH AS THE REASON

OF CERTAIN FOOD CHOICE

WOMEN

Women only show more deliberate health concern when it comes to the drinks they consume

21%CHOSE HEALTH AS THE REASON

OF CERTAIN DRINK CHOICE

MEN

26%CHOSE HEALTH AS THE REASON

OF CERTAIN DRINK CHOICE

WOMEN

MYTH 2:

Women prefer to sit down and enjoy their meal on premises

Women consume on-premises much less than men. They instead show a higher preference for off-premises consumption

60%OF MALE OOH VIS ITS WERE ON

PREMISE

MEN

47%OF FEMALE OOH VIS ITS WERE ON

PREMISE

WOMEN

MYTH 3:

Women love a good discount and would use vouchers much more than men

Women and men are not so different when it comes to using vouchers/promotions for eating out

6%OF MALE OOH VIS ITS UT IL IZED

VOUCHERS

MEN

7%OF FEMALE OOH VIS ITS UT IL IZED

VOUCHERS

WOMEN

The 15-34 year-olds account for 82%

of the female visits, and more than

half of the visits come from white-

collar workers. Students are also

proven to be the driving force of

female visits at 25%.

814 mil.FEMALE OOH VISITS IN THE PAST

YEAR*

• 15 - 34

• White collar and students

• Classes C or D (SEC)

Who are the typical female consumers in the Out of Home market?

* Source: Decision Lab Foodservice Monitor Aggregate data from Q4 2017 to Q3 2018

To be fair, the traffic growth in the past year came from both genders, with men bringing in the bigger increase

Male

Decision Lab Foodservice Monitor Data from Q4 2016 to Q3 2018 n = 27591

AVG. ANNUAL VIS ITS PER CAPITA

172 183 7%

Female 121 128 5%

Q4-16 | Q3-17 Q4-17 | Q3-18

42

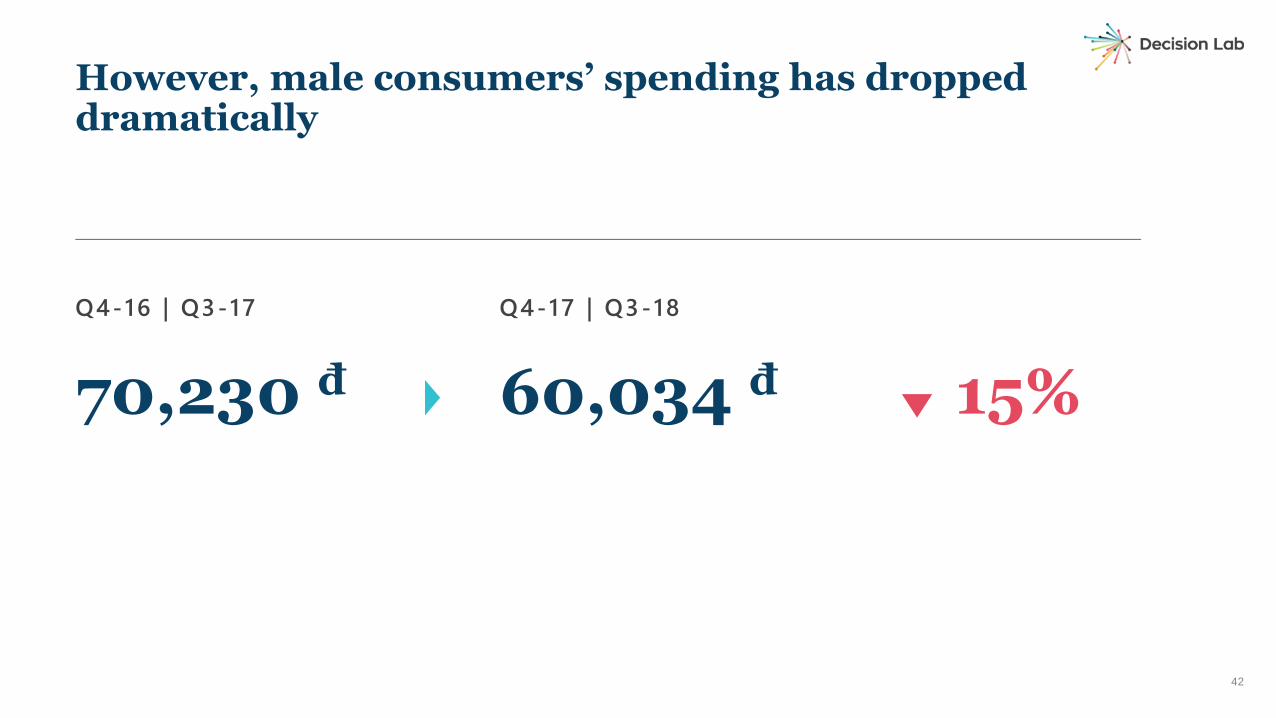

However, male consumers’ spending has dropped dramatically

70,230 đ 15%

Q4-16 | Q3-17

60,034 đ

Q4-17 | Q3-18

43

While female consumers have started to spend visibly more

57,829 đ 3%

Q4-16 | Q3-17

59,732 đ

Q4-17 | Q3-18

n = 27591

YOY Average spending growth by Gender

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

Indeed, women have spent more for Out of Home consumption across all the channels in the past year

-4%

-12%-10%

-22%

-9%

2%2%

5%

1%

5%

16%

12%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

FSR QSR Street food CVS Canteen Alcohol

places

Male

Female

45

The boost in women’s spending partly comes from their increased preference to consume both food and drink when going out

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

YOY Traffic growth by consumption type – in %

2%

0%

16%

-2%

-12%

23%

-20%

-10%

0%

10%

20%

30%

Eat only Drink only Eat & Drink

Male Female

n = 27591

Average spending by consumption type – in VND

EAT ONLY

42,907 VND

EAT & DRINK

81,224 VND

FEMALE AVERAGE SPENDING IN TOTAL OOH

n = 13339

FROM Q4 2016 – Q3 2017

TO Q4 2017 – Q3 2018

-8%MALE SALES CONTRIBUTION TO THE TOTAL OOH

FROM Q4 2016 – Q3 2017

TO Q4 2017 – Q3 2018

+10%FEMALE SALES CONTRIBUTION TO THE TOTAL OOH

As a result, women’s contribution to the market revenue has increased by a whopping 10%

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

n = 14252 n = 13339

32%

11%

30%

9%

12%

6%

31%

14% 24%18%

9%

3%Breakfast Morning snack Lunch Afternoon snack Dinner Late night snack

Male Female

Women consume Out of Home much more than men during daytime snacking occasions

3.7 billions VISITS TO OOH OUTLETS IN

YEAR ENDING Q3 2018

Male visits are concentrated on

Breakfast and Lunch, while

female visits are more spread out

across occasions.

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

65%

52%

12%

11%

8%

14%

8%

12%

1%4%

5% 7%

0%

20%

40%

60%

80%

100%

Male Female

VN Cuisine Coffee/Tea Bakery Non-VN Cuisine Juice/Smoothie Other

n = 17578

Preference in Full Service & Quick Service Restaurants by Gender - % visits

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

When it comes to cuisine selection, women are more keen to try foreign cuisine and visit outlets that offer non-Vietnamese dishes

Among the foreign cuisines, women are showing more and more appetite for Hotpot, BBQ and Japanese food

-21% -27%

27%19%

30%

-15%

47%

-71%

-13%

-52%

68%62%

68%

2%

-2%

-33%

-100%

-50%

0%

50%

100%

Fast Food Italian Kitchen BBQ Hotpot Japanese Korean Other Asian Western

Male

Female

YOY Traffic growth of cuisines in Foreign cuisines

n = 2962Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

*Low sample size (<30). Use with caution

FOR MANUFACTURERS

• For Food manufacturers, convenient

solutions for take-away and deliveries

to ease the off-premise consumption

will definitely get the interest of the

female population

• For Drink manufacturers, “health” is

important in your key product

message. In addition, make sure you

have products that capture women

during daytime snacking occasions.

FOR OPERATORS

• The growing influence of women on the foodservice market is

real: they are going out more and they are willing to spend

more

• They are not as health conscious when eating out as perceived

so no need to stress out on healthy food options for now.

• Make sure most of your offerings include both food and drink

items to capture women’s habit.

• Look into your menu to see if you can tailor particular items to

meet women’s snacking needs.

51

Implications

Vietnamese’ quest to explore foreign cuisine

TOTAL CUISINE

Quick service restaurants and Full service restaurants

that serve cuisines as below:

• Vietnamese

• Fast Food

• Italian Kitchen

• Western

• BBQ

• Hotpot

• Japanese

• Korean

• Other Asian (e.g. Chinese, Thai, Indian)

*Quick Service outlets such as Coffee/Tea, Bakery,

Juice/Smoothie and Ice Cream are excluded

Definitions

53

VIETNAMESE CUISINE

Quick service restaurants and Full service restaurants

specialized in Vietnamese cuisine. Pre-coded chains

include:

• Mon Hue

• Pho 24

• 37th Street

• Wrap & Roll

• Hoang Yen

• Com Tam Cali

• Net Hue

• Pho 10 Ly Quoc Su

and etc.

FAST FOOD

Quick service restaurants

specialized in fast food. Pre-coded

chains include:

• KFC

• Lotteria

• Jollibee

• Domino’s Pizza

• Burger King

• McDonald’s

• Five Star Chicken

and etc.

Definitions

54

ITALIAN KITCHEN

Full service restaurants specialized

in Italian cuisine and pizza. Pre-

coded chains include:

• Pizza Hut

• Pizza Company

• Pizza 4P’s

• Capricciosa

• Pendolasco

• Namo Artisanal Pizzeria

and etc.

WESTERN

Quick service restaurants and Full

service restaurants specialized in

higher-end burgers, French and

Mexican cuisines. Pre-coded

chains include:

• Al Fresco’s

• Relish & Sons

• Jaspas

• District Federal

• Bonjour Resto

and etc.

BBQ

Quick service restaurants and Full

service restaurants specialized in

BBQ, regardless of the grill style

(e.g. Western, Japanese, Korean…).

Pre-coded chains include:

• Quan Ut Ut

• SumoBBQ

• Gogi House

• King BBQ

• Tasaki BBQ

• Mr. Park

• Pepper Lunch

• Hotto

and etc.

Definitions

55

HOTPOT

Full service restaurants specialized

in Hotpot. Pre-coded chains

include:

• Kichi Kichi

• Hutong – Hot Pot Paradise

• Ashima

• Hotpot Story

• ThaiExpress

• MK Restaurants

and etc.

JAPANESE

Quick service restaurants and Full

service restaurants specialized in

Japanese cuisine, including sushi,

ramen and udon outlets. Pre-

coded chains include:

• Sushi Hokkaido Sachi

• Tokyo Deli

• Marukame Udon

• Daruma

• Sushi Kei

• YEN Sushi & Sake Pub

• Sukiya

• NamBento

and etc.

KOREAN

Quick service restaurants and Full service restaurants

specialized in Korean cuisine, including Korean fried

chicken outlets. Pre-coded chains include:

• K-Food

• Poki Poki

• Mi Han Quoc

• Hanuri

• GAXEO Chicken

• Don Chicken

• Papa’s Chicken

and etc.

Definitions

56

OTHER ASIAN

Quick service restaurants and Full service restaurants

specialized in Chinese, Thai and Indian cuisine. Pre-

coded chains include:

• Crystal Jade Kitchen

• San Fu Lou

• Baozi

• Bamboo Dimsum

• Lac Thai

• Tuk Tuk Thai Bistro

• Tandoor

• Spices

and etc.

n = 13730

Preference of cuisines in Full Service and Quick Service Restaurants - % visits

*Full Service and Quick Service Restaurants, excluding Coffee/Tea, Bakery, Juice/Smoothie and Ice Cream

outlets

The dominance of Vietnamese cuisine in the Out of Home market is undisputable

80% 5% 2%1%1%1%1%%1%

0% 20% 40% 60% 80% 100%

Vietnamese Fast Food Italian Kitchen BBQ Hotpot

Japanese Korean Western Other Asian

58

Besides the obvious advantage of convenience, Vietnamese cuisine claims its dominance thanks to the innate ability to replace home cooked meals

53%

44%41%

35% 33% 33%27%

47%

32%

40%36% 37%

30% 31%

0%

20%

40%

60%

Convenient

location

Did not want to

cook

Quality of food Clean

environment

Taste of food Good value for

money

Friendly service

Vietnamese Cuisine Non-Vietnamese Cuisine

Reason for outlet choice - % visits

n = 13730Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

59

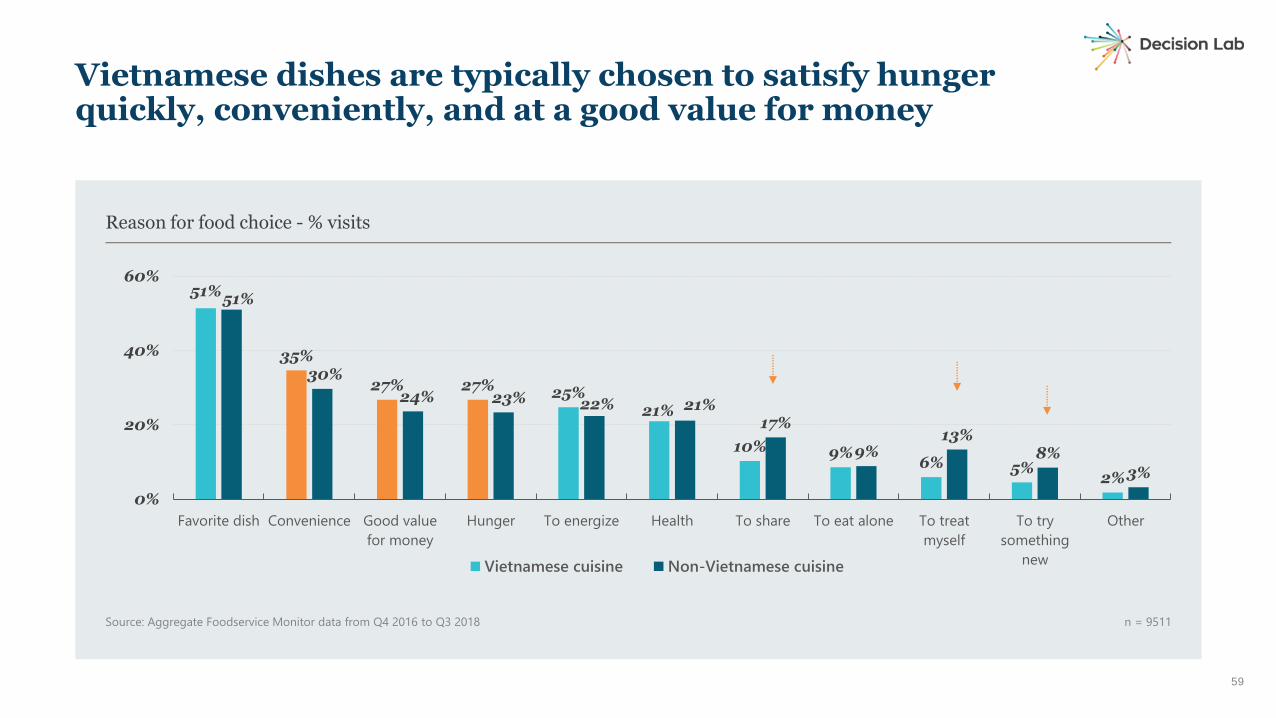

Vietnamese dishes are typically chosen to satisfy hunger quickly, conveniently, and at a good value for money

51%

35%

27% 27% 25%21%

10% 9%6% 5%

2%

51%

30%

24% 23% 22% 21%17%

9%13%

8%

3%

0%

20%

40%

60%

Favorite dish Convenience Good value

for money

Hunger To energize Health To share To eat alone To treat

myself

To try

something

new

Other

Vietnamese cuisine Non-Vietnamese cuisine

Reason for food choice - % visits

n = 9511Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

Fast food, the biggest type of non-Vietnamese cuisine consumed, has been suffering from a significant lost of traffic year over year…

Market share of non-VN cuisines in FSR and QSR in year ending Q3 2018 - % visits

n = 2962

Fast food outlet visits

-17%YOY TRAFFIC GROWTH

39%

13%10%

10%

9%

9%

8%

1%

Fast Food

BBQ

Other Asian

Hotpot

Italian Kitchen

Japanese

Korean

Western

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

-17%

46%

23%

37%

-40%

49%

-6%

-61%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

Fast Food BBQ Other

Asian

Hotpot Italian

Kitchen

Japanese Korean Western

n = 2962

YOY Traffic growth of non-VN cuisines

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

61

…leaving the market to the giant hands of players specialized in BBQ, Hotpot and Japanese cuisine

• YOY average spending growth of non-VN cuisines

-10%

-2%

12%16%

-3%

1%

42%

5%

105K

271K

184K

225K210K

280K

191K209K

-25%

0%

25%

50%

75%

Fast Food BBQ Other

Asian

Hotpot Italian

Kitchen

Japanese Korean Western

YOY average spending growth % Average spending in year ending 2018 (VND)

n = 2962

Average spending per head per visit and YOY growth among types of Non-Vietnamese cuisine

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

62

Among the 3 rising cuisines, Hotpot is the only one that enjoys the luxury of increasing consumer spending in the past year

63

Consequently, the market pie has shifted significantly: further away from Western foods and heavily toward Asian-centric cuisine

YOY sales contribution growth of non-VN cuisines

-25%

43%51%

59%

-42%

38% 34%

-59%-80%

-40%

0%

40%

80%

Fast

Food

BBQ Japanese Hotpot Italian

Kitchen

Other

Asian

Korean Western

n = 2962

Market share of non-VN cuisines in FSR and QSR in year ending 2018 - % sales

23%

20%

14%

12%

11%

10%

8%1%Fast Food

BBQ

Japanese

Hotpot

Italian Kitchen

Other Asian

Korean

Western

n = 2962

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

BBQ

YOY VISITS INCREASE

+4.0m

↓

73% FROM FEMALE 15-34

23% FROM MALE 25-34

HOTPOT

YOY VISITS INCREASE

+2.5m

↓

51% FROM FEMALE 25-34

33% FROM MALE 15-24

JAPANESE

YOY VISITS INCREASE

+2.8m

↓

51% FROM FEMALE 15-34

64

Young female consumers are the core growth engine for restaurants offering the 3 cuisines over the past year

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

The drivers of consumer choice for these cuisines may differ, but all hint at Vietnamese’ underlying expectations toward a dining destination

BBQ Restaurants:

CELEBRATION/ TREAT

QUALITY OF FOOD/DRINK

FRIENDLY SERVICE

Hotpot Restaurants:

GOOD FOR SOCIALIZING

SPECIAL OCCASION

CELEBRATION

CLEAN ENVIRONMENT

Japanese Restaurants:

QUALITY OF FOOD/DRINK

HEALTHY OFFERINGS

GOOD VALUE FOR MONEY

31% 48%

40% 42%

38% 50%

Lunch time Dinner time

30.7 million TOTAL VISITS IN YEAR ENDING

Q3 2018

BBQ and Japanese cuisine are

more preferred for dinner, while

Hotpot strikes a balance and is

equally chosen for both meals.

BBQ restaurants have become more attractive destinations for dinner, while Hotpot and Japanese outlets enjoy increasing footfall during lunch

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

• Party size - % visits

35%27%

55%

44%

39%

27%

21%

35%

19%

0%

20%

40%

60%

80%

100%

BBQ Restaurants Hotpot Restaurants Japanese Restaurants

<=2 people 3-4 people 5+ people

n=602

Party size by cuisine - % visits

Source: Aggregate Foodservice Monitor data from Q4 2016 to Q3 2018

Hotpot and BBQ restaurants show amazing capability to accommodate consumers’ needs across different party sizes

Vietnamese eat Vietnamese food, but they have

also shown more appetite for BBQ and Asian-

centric cuisine such as Hotpot and Japanese

foods.

Young female consumers are the growth

engine of restaurants offering these cuisines.

➢ To Operators currently in these winning

segment, stay focused, listen to your consumers

and be ready to adapt as competition from new

and current players is definitely getting more

fierce.

➢ To all Operators that specialize in foreign cuisine,

look into how you can adapt some of these

restaurants’ success drivers, e.g. facilitative

environment for special occasions, appeal to

women, great service, exciting interaction

between consumers and food, etc.

➢ To Drinks and Fresh food Manufacturers, focus

your effort in winning BBQ, Hotpot and Japanese

chains if you are looking for growth.

So, what are the key takeaways?

Reach out to us

4 4 F L O O R - B I T E X C O F I N A N C I A L T O W E R

2 H A I T R I E U , D I S T R I C T 1

H O C H I M I N H C I T Y , V I E T N A M

+ 8 4 2 8 3 9 1 5 1 9 1 9 | D E C I S I O N @ D E C I S I O N L A B . C O

W W W . D E C I S I O N L A B . C O

Related Documents