Disclaimer: This report does not purport to be all inclusive or to contain all the information that the recipient may require to form its decisions. No representation or warranty, express or implied, is or will be made in relation to the accuracy or completeness of this document. FOOD & BEVERAGE INDUSTRY IN TURKEY: SECTOR & MARKET ANALYSIS Sadık Baydere August, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Disclaimer: This report does not purport to be all inclusive or to contain all the information that the recipient may require to form its decisions. No representation or warranty, express or implied, is or will be made in relation to the accuracy or completeness of this document.

FOOD & BEVERAGE INDUSTRY

IN TURKEY:

SECTOR & MARKET ANALYSIS

Sadık Baydere

August, 2013

August, 2013

CONTENTS

1 EXECUTIVE SUMMARY .................................................................................................................... 3

2 GLOBAL OVERVIEW ......................................................................................................................... 5

3 DOMESTIC OVERVIEW..................................................................................................................... 8 3.1 Subsectors, Interacting Sectors and Trends........................................................................... 11 3.2 Regional Structures and Clusters ........................................................................................... 12 3.3 Investment and Employment................................................................................................... 13 3.4 Production, Sales and Capacity Utilisation ............................................................................. 15 3.5 Added Value, R&D and Competitiveness ............................................................................... 16 3.6 Cost Components ................................................................................................................... 18 3.7 Foreign Trade.......................................................................................................................... 19

3.7.1 Exports..................................................................................................................... 20 3.7.2 Imports ..................................................................................................................... 21

4 REGULATIONS ................................................................................................................................ 22 4.1 EU Food Safety Regulation..................................................................................................... 22 4.2 Turkish Food Codex................................................................................................................ 23 4.3 HACCP.................................................................................................................................... 25 4.4 CLP ......................................................................................................................................... 25 4.5 Waste Management ................................................................................................................ 26 4.6 Dangerous Goods Transportation........................................................................................... 26 4.7 ATP Convention ...................................................................................................................... 28

5 SUPPLY CHAIN & LOGISTICS........................................................................................................ 29 5.1 Logistics Service Providers to Food & Beverage Industry...................................................... 30

6 MAIN PLAYERS ............................................................................................................................... 33

7 SWOT ANALYSIS............................................................................................................................. 38 7.1 Strengths................................................................................................................................. 38 7.2 Weaknesses............................................................................................................................ 38 7.3 Opportunities........................................................................................................................... 39 7.4 Threats .................................................................................................................................... 40 7.5 Priority Problem Areas ............................................................................................................ 40

8 THE FUTURE PROJECTION AND CHALLENGES......................................................................... 41

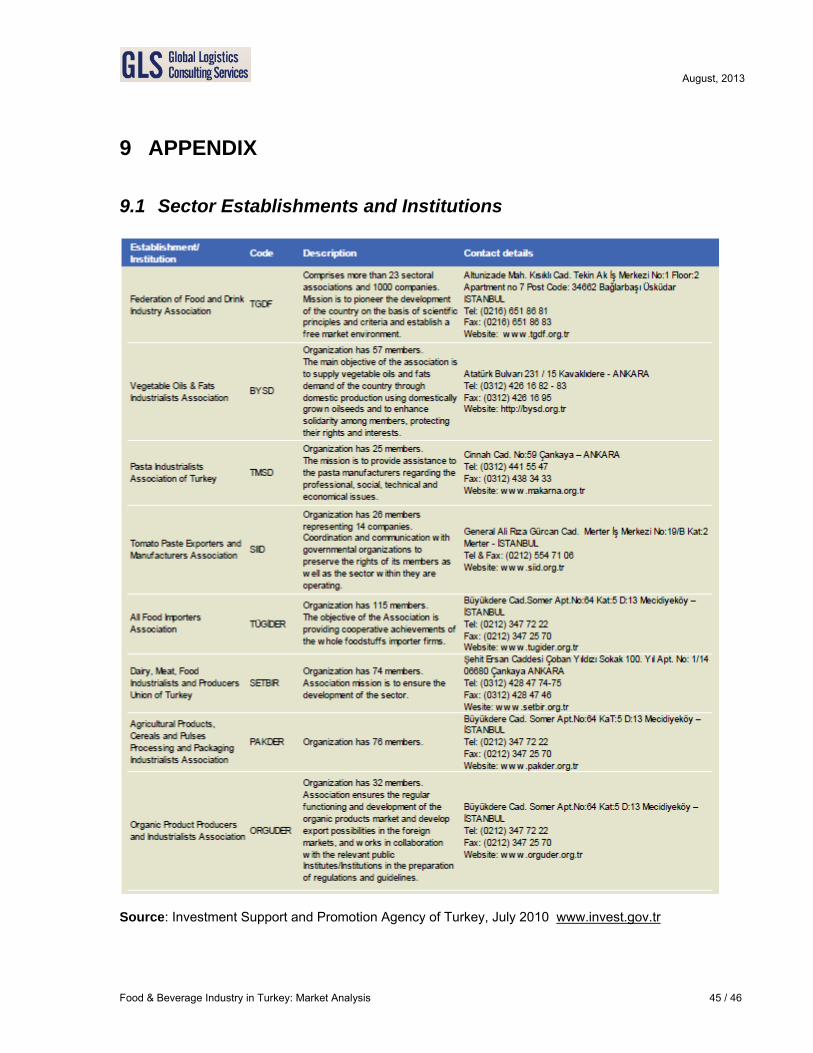

9 APPENDIX........................................................................................................................................ 45 9.1 Sector Establishments and Institutions ................................................................................... 45

Food & Beverage Industry in Turkey: Market Analysis 2 / 46

August, 2013

1 EXECUTIVE SUMMARY The objective of this report is to provide a brief outlook and market analysis of the Food and Beverage (F&B) Industry in Turkey. It has been prepared for information purposes relating to this sector based on publicly available information sources at the time this document was prepared. F&B industry is a global collective of diverse businesses with revenues of USD 7 trillion that together supply the processed food and drinks consumed by the world population. The industry comprises all companies involved in processing raw food materials, packaging, and distribution. This includes fresh, prepared foods as well as packaged foods, and alcoholic and non-alcoholic beverages. Any product meant for human consumption, aside from pharmaceuticals, passes through this industry. Requiring a labour-intensive system, F&B industry has a strategic importance for all countries socio-economically due to its critical role in the utilisation of agricultural products, supply of raw materials to industry, its contribution to employment and balanced nutrition of the public. The largest corporate producers worldwide, with plants in numerous countries include Cargill, Nestle, PepsiCo, Coca-Cola, Anheuser-Busch, Mondelez, Kraft, Mars, Unilever, SAB Miller, Danone, Heineken, Associated British Foods, Diageo, Kellogg, HJ Heinz and Pernod Richard with annual sales between USD 10 billion and 137 billion in 2012.

F&B industry is accepted as one of the strategic sectors in Turkish economy mainly due to its ability to create employment and its sizable share in exports of 6.2% generating a trade surplus with impressive exports to imports ratio of 186% in 2012.

In 2012, the food and beverage exports were USD 9.5 billion while imports amounted to USD 5.1 billion. The sector’s 2023 target of USD 40 billion in exports within Turkey’s 2023 target of USD 500 billion is achievable considering its average annual increase of 15.7% in the last 10 years. This is well above the other industrial products which average about 3%.

Turkey has become the 7th largest agricultural country in the world while ranking 1st in EU countries. In terms of food and beverage exports, it has become the 15th biggest exporter in the world with a share of 1.5% in global trade of over USD 600 billion.

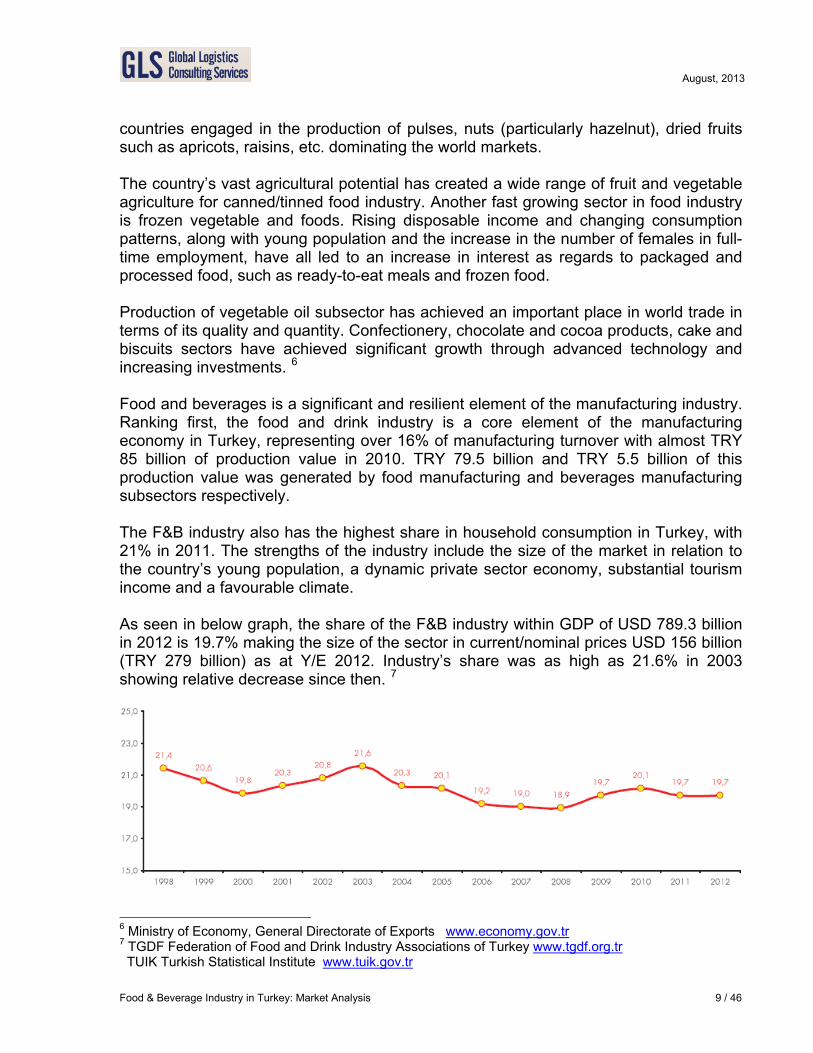

The share of the F&B industry within GDP of USD 789.3 billion in 2012 is 19.7% making the size of the sector in current/nominal prices USD 156 billion (TRY 279 billion) as at Y/E 2012.

Food & Beverage Industry in Turkey: Market Analysis 3 / 46

August, 2013

Within manufacturing industries, F&B industry has a 16% share in terms of production value, 11% of companies and 15% of employees. Having a total employment of about 420,000 it has a high labour intensity with a critical contribution to the employment of the country.

Turkish F&B industry has competitive advantages in global markets. However, this advantage is not because of the management factors such as branding, R&D, innovation and design but rather its strong position in national supply of agricultural raw materials, relatively low labour costs and geographical location.

The primary products exported by the Turkish F&B industry are covered by the subsectors of “Processed Vegetables and Fruits”, “Milled Grain Products”, “Vegetable and Animal Oils and Fats” and “Cocoa, Chocolate and Sugar Confectionery”.

Similar to EU, almost 99% of about 41,000 companies operating in the sector are small to medium-scale enterprises in SME category, spread throughout the country. Most of these companies are located in the cities of Istanbul, Izmir, Ankara, Manisa, Bursa, Gaziantep, Konya, Balıkesir, Mersin and Adana. Recognising the importance of the “Specialised Organised Industrial Zones” for the development and growth of the sector, infrastructure investments have been made lately.

There are total of 520 companies with foreign investment in the Turkish F&B industry as at year/end 2012. The sector attracted almost half of USD 2.1 billion foreign direct investments made in the manufacturing industries in 2012.

Production value of the sector reached to TRY 85 billion in 2010 while average annual increase of the production index has been around 4.7% between 2006 and 2012. The weighted capacity utilisation rate of the industry was around 70% in the last 5 years. Within the concept of “food safety”, F&B industry is a heavily regulated sector due to human health and safety and environmental concerns. Although not being a full member of EU, Turkey as a candidate has existing and upcoming obligations for regulations such as HACCP, CLP, Waste Management, Transport of Dangerous Goods, ATP Convention and EU Food Safety Regulation within the negotiation process started in October 2005. It is inevitable that these regulations impose high costs to the companies in the sector while improving the competitiveness of Turkish F&B industry in global markets. In line with Vision 2023, targets and relevant action points have been identified within the studies of Turkish F&B Industry Strategy and Action Plan where the major topics were “Competitiveness”, “Food Safety”, “Raw Material”, “R&D and Innovation”, “Human Resources” and “Legislation and Control”.

Food & Beverage Industry in Turkey: Market Analysis 4 / 46

August, 2013

2 GLOBAL OVERVIEW With revenues of USD 7 trillion and a Compound Annual Growth Rate (CAGR) of 3.5%, F&B industry is one of the world’s key industries; a major contributor to growth in all economies. It is all companies involved in processing raw food materials, packaging, and distribution including fresh, prepared foods as well as packaged foods, and alcoholic and non-alcoholic beverages. Any product meant for human consumption, aside from pharmaceuticals, passes through this industry. 1 The F&B industry is highly fragmented and competitive. The production in this industry is divided among a few different companies where 4 largest players accounting for less than 5% of the total market value. However, no single firm has large enough share of the market to be able to influence the industry's direction or price levels. The industry is characterised not only by high levels of competition, but also sustainability and food safety concerns, a focus among consumers on health and wellbeing and a rise in merger and acquisition activity among food and beverage businesses. F&B industry is also one of the most unpredictable industries, significantly affected by regulations, legislation changes and adverse weather conditions. In recent years, the food and beverage industry has been the victim of rising commodity prices as a result of severe droughts, flooding and higher energy and transportation costs. Food and beverage manufacturers have witnessed tremendous growth and change in the last decade. Global players consolidated, the developing world emerged as a viable market, new technologies afforded greater product diversity, and stringent regulations challenged manufacturers to prioritise consumers and environmental health. In addition, manufacturers must manage high, volatile costs, a tough economic climate, and increasing competition from powerful retail brands. Demand for healthier food products is a mainstay of the industry landscape in developed markets and is gaining traction in emerging markets, presenting further expansion opportunities for food and beverage producers. Furthermore, the organic sector has proved largely resilient amid the recent economic downturn accounting for approximately $31 billion in sales each year. North America and Europe alone typically generate over 90% of global organic food and drink revenue on an annual basis. 2 In recent years, sustainability and environmental concerns has become a key purchase driver for consumers. Food and beverage companies are responding by exploring more environmentally friendly packaging, labelling and produce options in a bid to favourably position their brands with the ever increasing number of environmentally conscious consumers.

1 IMAP Food and Beverage Industry Global Report www.imap.com 2 Grant Thornton www.grantthornton.com

Food & Beverage Industry in Turkey: Market Analysis 5 / 46

August, 2013

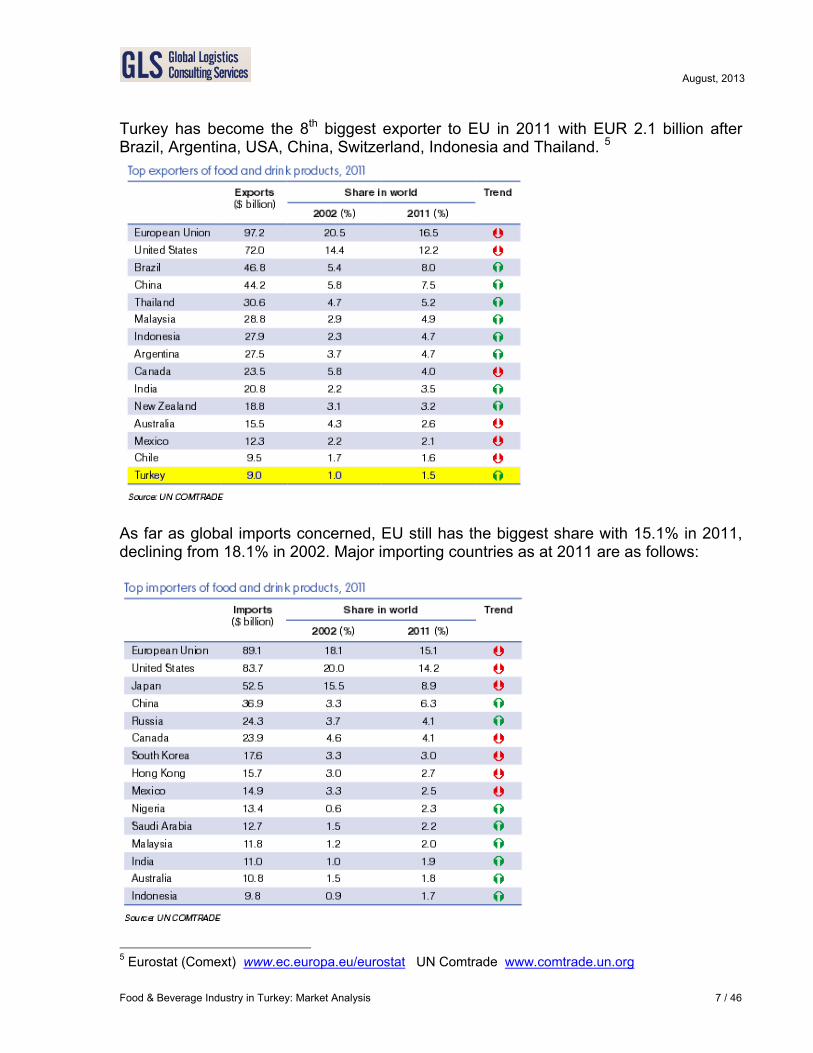

In light of some of the key challenges facing agriculture companies, such as climate change and rising commodity prices, numerous organisations in different parts of the industry value chain are looking to create synergies and focused efforts. Many of the larger players in the market are forcing consolidation amongst smaller players. Food processing and beverage production companies continue to engage in national and cross-border merger and acquisition activity in a bid to better position themselves in international markets. Transaction activity has been especially strong in emerging markets as companies look to expand into these markets, capitalising on demand generated by increasing population and rising wages. Global analysis shows that the food and drink industry plays an important role in the world economy. The leading food and beverage producers in the world are EU, USA, China, Japan, Brazil, Canada, Mexico, Australia, South Korea and New Zealand. While F&B industry constitutes 15% of total manufacturing sales in EU and USA, this rate is 5% in South Korea and 45% in New Zealand. 3 The major global players in F&B industry ranked by their sales are Cargill (USA), Archer Daniels Midland (USA), Nestle (CH), PepsiCo (US), Coca-Cola (USA), Anheuser-Busch (BE), Mondelez (USA), Mars (USA), Tyson Foods (USA), Unilever (NL/UK), SAB Miller (UK), Kirin (JP), Danone (FR), Heineken (NL), Suntory (JP), Luctalis (FR), Associated British Foods (UK), Asahi (JP), Diageo (UK), General Mills (USA), Fonterra (NZ), Kellogg (USA), ConAgra Foods (USA), Friesland Campina (NL), Vion (NL), Smithfield Foods (USA), Dean Foods (USA), HJ Heinz (USA) and Pernod Richard (FR) with annual sales ranging from USD 137 billion to USD 11 billion in descending order. In the EU, turnover of F&B industry in 2011 was EUR 1,017 billion making it the largest manufacturing sector with 14.9% share. Having 287,000 companies operating in the sector, it is a very fragmented industry where 99.1% are SMEs. In the EU, SMEs employ 4.3 million people making it the leading employer in manufacturing with 15% share. SME’s in the EU make 48% of food and beverage production and 50% of sales while providing 63% of employment in the F&B industry. 4 EU remains the global leader in F&B trade despite shrinking shares of the global F&B trade markets. EU has 16.5% share of the global exports with EUR 76.2 billion in 2011 shrinking from 20.5% in 2002, making the size of the global trade EUR 462 billion (~USD 600 billion) in terms of exports. EU imports were EUR 63.0 billion in 2011 in which Turkey has a 3.4% share as EU’s 8th biggest import partner. The following table lists the major exporters of food and beverage products worldwide based on 2011 data. As seen, with an increasing share, Turkey has become the 15th biggest exporter globally including the EU as a single entry with 1.5% share in global exports in the industry; 50% increase in 10 years between 2002 and 2011.

3 OECD STAN indicators database www.oecd.org 4 FoodDrinkEurope (CIAA) www.fooddrinkeurope.eu

Food & Beverage Industry in Turkey: Market Analysis 6 / 46

August, 2013

Turkey has become the 8th biggest exporter to EU in 2011 with EUR 2.1 billion after Brazil, Argentina, USA, China, Switzerland, Indonesia and Thailand. 5

As far as global imports concerned, EU still has the biggest share with 15.1% in 2011, declining from 18.1% in 2002. Major importing countries as at 2011 are as follows:

5 Eurostat (Comext) www.ec.europa.eu/eurostat UN Comtrade www.comtrade.un.org

Food & Beverage Industry in Turkey: Market Analysis 7 / 46

August, 2013

3 DOMESTIC OVERVIEW From the early years of Turkish Republic, F&B industry has been one of the fastest growing industries. The state did set up large-scale public enterprises, investing heavily. These businesses in the form of SOEs (State Owned Enterprises) operated mostly in sugar, tea, alcoholic drinks, meat, dairy and tobacco production. Despite the presence of large-scale SOEs, small-scale enterprises have been forming in an increasing scale in the sector while most of the SOEs have been privatised lately. After 1980, significant changes were implemented in the foreign trade regime including food and beverage products adopting an export-oriented strategy. Liberalisation of foreign trade and lowering taxes and duties in food and agricultural products considerably were the major changes in this period. Starting from 1980’s, the role of foreign capital in agricultural production and F&B industry increased significantly. Particularly between 1987 and 1998, the number of foreign companies and domestic companies with foreign participation increased. This trend continued after 2003 with more foreign capital flow to F&B industry. Turkey, having its production strength from its agricultural production, has registered a steady growth in food industry in recent years on its way to becoming a more active player in world markets. With its agricultural production of USD 62 billion, Turkey has become the 7th largest agricultural country in the world while ranking 1st in EU countries. In terms of exports, it has become the 15th biggest exporter in the world. In terms of utilised agricultural land, almost 39 million hectares of Turkey’s total area of 82 million hectares are used for agriculture making 47% of the country’s total area. Turkey ranks 6th in the world in terms of food self-sufficiency. Young and increasing population, preference to packaged products owing to rising consumer awareness for balanced and conscious nutrition, changing eating habits and personal dietary preferences are some of the factors positively affecting the fast growth of the F&B sector in recent years. Turkish consumers have been becoming increasingly demanding, driven by the multitude of choices offered by mass grocery retail outlets. As the sector is getting more sophisticated, Turkey is becoming one of the largest markets for baked goods with its bread - an important element of the Turkish diet - leading to some of the highest rates of per capita consumption in the world. On the other hand, dairy products subsector including milk, yoghurt, cheese, kefir and yoghurt drink ayran form an integral part of the traditional Turkish diet. Traditionally, unpackaged products have dominated the Turkish dairy market, holding back widespread growth but also posing a potential to the investors. Grains have a very important role in Turkish agriculture due to bread being the basic staple food of the country. In addition, Turkey has an important place among the

Food & Beverage Industry in Turkey: Market Analysis 8 / 46

August, 2013

countries engaged in the production of pulses, nuts (particularly hazelnut), dried fruits such as apricots, raisins, etc. dominating the world markets. The country’s vast agricultural potential has created a wide range of fruit and vegetable agriculture for canned/tinned food industry. Another fast growing sector in food industry is frozen vegetable and foods. Rising disposable income and changing consumption patterns, along with young population and the increase in the number of females in full-time employment, have all led to an increase in interest as regards to packaged and processed food, such as ready-to-eat meals and frozen food. Production of vegetable oil subsector has achieved an important place in world trade in terms of its quality and quantity. Confectionery, chocolate and cocoa products, cake and biscuits sectors have achieved significant growth through advanced technology and increasing investments. 6 Food and beverages is a significant and resilient element of the manufacturing industry. Ranking first, the food and drink industry is a core element of the manufacturing economy in Turkey, representing over 16% of manufacturing turnover with almost TRY 85 billion of production value in 2010. TRY 79.5 billion and TRY 5.5 billion of this production value was generated by food manufacturing and beverages manufacturing subsectors respectively. The F&B industry also has the highest share in household consumption in Turkey, with 21% in 2011. The strengths of the industry include the size of the market in relation to the country’s young population, a dynamic private sector economy, substantial tourism income and a favourable climate. As seen in below graph, the share of the F&B industry within GDP of USD 789.3 billion in 2012 is 19.7% making the size of the sector in current/nominal prices USD 156 billion (TRY 279 billion) as at Y/E 2012. Industry’s share was as high as 21.6% in 2003 showing relative decrease since then. 7

6 Ministry of Economy, General Directorate of Exports www.economy.gov.tr 7 TGDF Federation of Food and Drink Industry Associations of Turkey www.tgdf.org.tr TUIK Turkish Statistical Institute www.tuik.gov.tr

Food & Beverage Industry in Turkey: Market Analysis 9 / 46

August, 2013

The F&B industry contributes to Turkey’s exports as well, achieving USD 9.5 billion accounting over 6% of the total exports in 2012. The imports of the industry were USD 5.1 billion making the ratio of exports to imports an impressive 186%. The increase in income generated from agriculture, F&B sector has a significant potential for improving the welfare, wealth and quality of life of the country’s population. Turkey Industry Strategy Document (2001-2014) states that “The capability of F&B industry integration with the agricultural production regions brings the possibility of production in many different regions and high employment creation; hence increasing the importance of the F&B industry with its role to reduce regional disparities and unemployment”. 8 The size of the market due to young population, dynamic private sector economy, high tourism income and favourable climatic conditions are seen the strengths of the Turkish F&B sector. In this context, Federation of Food and Drink Industry Associations of Turkey has defined its 2023 export target for food and beverages as USD 40 billion.

According to Turkey Food and Drink Report Q3 2013 report prepared by Business Monitor International, strong continuing growth in the consumer sector is expected in Turkey. On a related note, Turkey’s increasing appeal to foreign investors – due to a number of factors such as market-friendly policies and enormous demand for infrastructure development, including power grids, transport infrastructure and housing – domestic demand will grow strongly over the next few years. As infrastructure develops, companies will be able to reach more consumers efficiently, speeding up the evolution of tastes and preferences across the country. Organised retail channels should develop quickly to support this development as more consumers trade up from informal independent stores. 9

BMI report highlights the following industry data with regards to growth in food and beverages in Turkey:

Food consumption growth in 2013 is expected as 7% while forecast compound annual growth to 2017 is 7.8%

Alcoholic drinks volume of sales in 2013 is expected to increase 3.6% while forecast compound annual growth to 2017 is 4.1%

Soft drinks volume of sales in 2013 is expected to increase 7.1% while forecast compound annual growth to 2017 is 7.7%

Mass grocery retail sales in 2013 is expected to increase 10.6% while forecast compound annual growth to 2017 is 12.0%

8 Ministry of Science, Industry and Technology, Directorate General of Industry www.sgm.sanayi.gov.tr 9 Business Monitor International, Food & Drink Q3 2013

Food & Beverage Industry in Turkey: Market Analysis 10 / 46

August, 2013

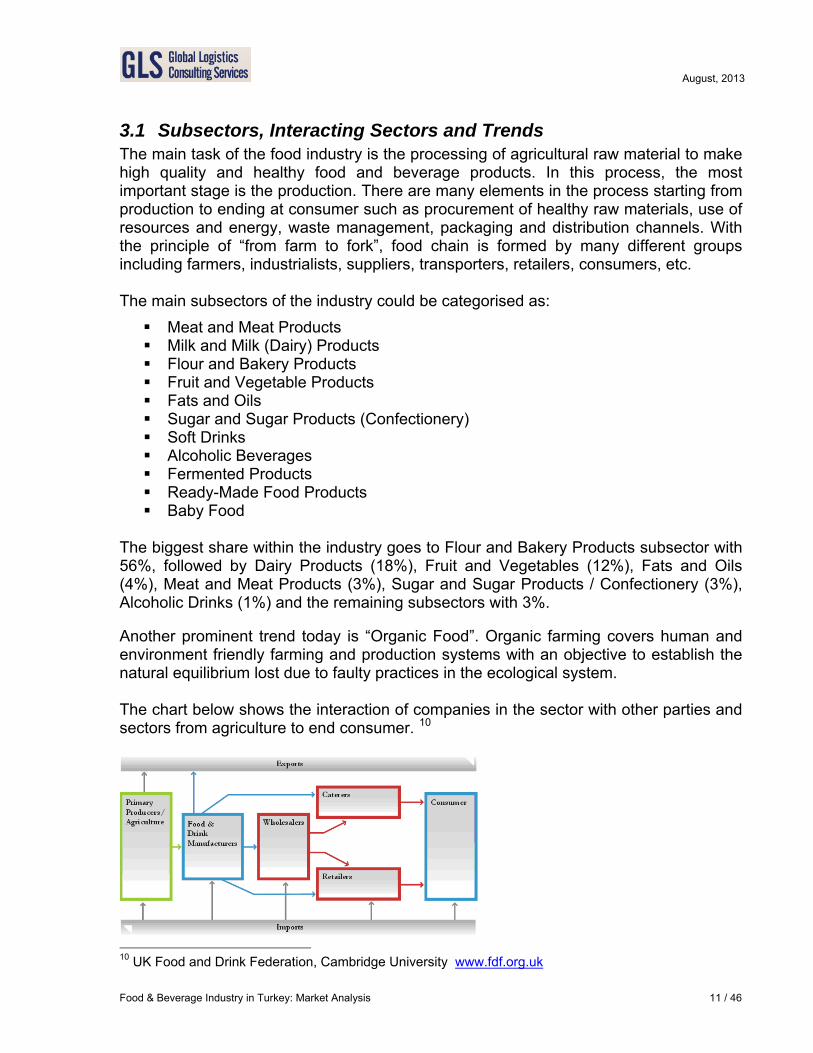

3.1 Subsectors, Interacting Sectors and Trends The main task of the food industry is the processing of agricultural raw material to make high quality and healthy food and beverage products. In this process, the most important stage is the production. There are many elements in the process starting from production to ending at consumer such as procurement of healthy raw materials, use of resources and energy, waste management, packaging and distribution channels. With the principle of “from farm to fork”, food chain is formed by many different groups including farmers, industrialists, suppliers, transporters, retailers, consumers, etc. The main subsectors of the industry could be categorised as:

Meat and Meat Products Milk and Milk (Dairy) Products Flour and Bakery Products Fruit and Vegetable Products Fats and Oils Sugar and Sugar Products (Confectionery) Soft Drinks Alcoholic Beverages Fermented Products Ready-Made Food Products Baby Food

The biggest share within the industry goes to Flour and Bakery Products subsector with 56%, followed by Dairy Products (18%), Fruit and Vegetables (12%), Fats and Oils (4%), Meat and Meat Products (3%), Sugar and Sugar Products / Confectionery (3%), Alcoholic Drinks (1%) and the remaining subsectors with 3%. Another prominent trend today is “Organic Food”. Organic farming covers human and environment friendly farming and production systems with an objective to establish the natural equilibrium lost due to faulty practices in the ecological system. The chart below shows the interaction of companies in the sector with other parties and sectors from agriculture to end consumer. 10

10 UK Food and Drink Federation, Cambridge University www.fdf.org.uk

Food & Beverage Industry in Turkey: Market Analysis 11 / 46

August, 2013

In terms of Hot Beverages, tea is the major hot drink consumed in Turkey. Turkey ranks 7th in tea cultivation area within the world, 5th in dry tea production, and 4th in annual per capita tea consumption.11 Among other hot drinks, Turkish coffee is widely consumed in Turkey although global coffee chains providing various alternative products have been entering the market widely. Bottled water ranks first with regards to the production capacities in the Turkish beverage industry, accounting almost half of the total beverage industry production capacity. Other soft drinks mainly including soda and fruit juice constituting approximately 40 percent of the total beverage industry production capacity. Top four alcoholic beverages produced in Turkey are beer, raki, wine and vodka. Beer is the main alcoholic drink, constituting about 90% of total alcoholic drinks production. However, wine production has been increasing fastest among the top four products.

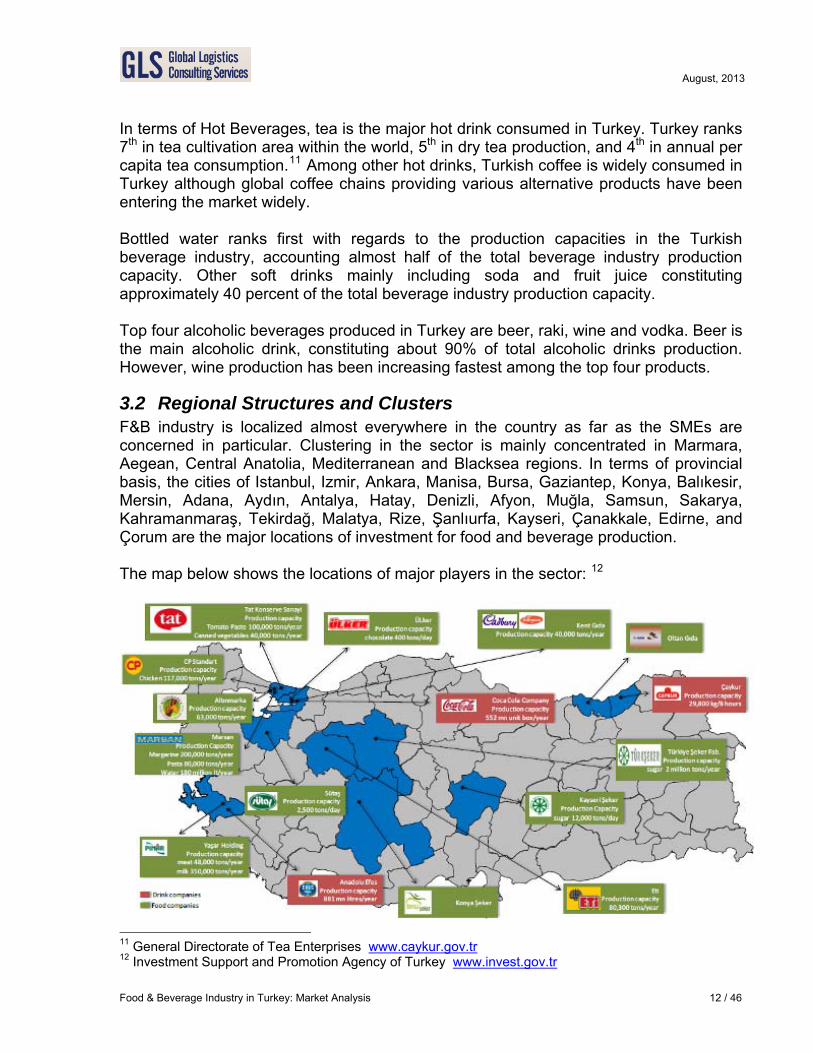

3.2 Regional Structures and Clusters F&B industry is localized almost everywhere in the country as far as the SMEs are concerned in particular. Clustering in the sector is mainly concentrated in Marmara, Aegean, Central Anatolia, Mediterranean and Blacksea regions. In terms of provincial basis, the cities of Istanbul, Izmir, Ankara, Manisa, Bursa, Gaziantep, Konya, Balıkesir, Mersin, Adana, Aydın, Antalya, Hatay, Denizli, Afyon, Muğla, Samsun, Sakarya, Kahramanmaraş, Tekirdağ, Malatya, Rize, Şanlıurfa, Kayseri, Çanakkale, Edirne, and Çorum are the major locations of investment for food and beverage production. The map below shows the locations of major players in the sector: 12

11 General Directorate of Tea Enterprises www.caykur.gov.tr 12 Investment Support and Promotion Agency of Turkey www.invest.gov.tr

Food & Beverage Industry in Turkey: Market Analysis 12 / 46

August, 2013

The cluster approach has been widely applied lately as a successful method of increasing productivity and competitiveness for various industries. “Specialised Organised Industrial Zones” (SOIZ) are very important for the development, competitiveness and growth of the sector. In this respect, investments were made to form Specialised Food and Beverage Organised Industrial Zones recently; Samsun in 2007, Kumluca - Antalya in 2008, and Kandıra – Kocaeli in 2010. Plans are in place for more SOIZs where in Geyve – Sakarya, 4th SOIZ for Food and Beverage industry to be established.

3.3 Investment and Employment In F&B industry, almost 420,000 people are employed by about 41,000 firms which compose approximately 15% of employees and 11% of the total number of companies in the manufacturing sector. Majority of the firms and employees were in food products subsector while only 1.5% of all companies and 3% of employees in the industry are in beverage/drink products subsector. According to official TUIK figures, 36,919 companies with 349,495 employees operated in 2009 showing increases of 11% and 20% respectively in 3 years between 2009 and 2012. Industrial employment index of 137.8 relating to F&B industry shows that employment provided by the industry is well over the overall manufacturing industry index of 111.3 as at year end 2012. Average annual increase of the employment index between 2007 and 2013 were 4.3% for food subsectors and 3.9% for beverage subsectors comparatively higher than 1.2% increase in the manufacturing industry. As highlighted before, the sector is highly fragmented. Similar to EU, 99% of the companies are in SME category which is mostly privately held. However, while SMEs in the EU has 48% share of F&B production, it is 61% in Turkey. Turkish Statistical Institute TUIK compares the revenues of each company to the highest 4 and 8 to find the degree of industry concentration for each subsector giving important clues about its monopolistic structure. Based on this study last conducted in 2013 providing the results for 2010; There is high concentration (high monopoly) in beverages subsector where the concentration in food subsectors is mostly medium and low except margarine, ready-to-eat and frozen foods including ice cream and homogenised foods production which have high monopolistic structure as the number of companies in beverages and the above mentioned food subsectors are relatively low. Taking the revenues of the companies in the sector, just over one half of the subsectors of the F&B industry is said to be dominated by a monopolistic structure but most of the

Food & Beverage Industry in Turkey: Market Analysis 13 / 46

August, 2013

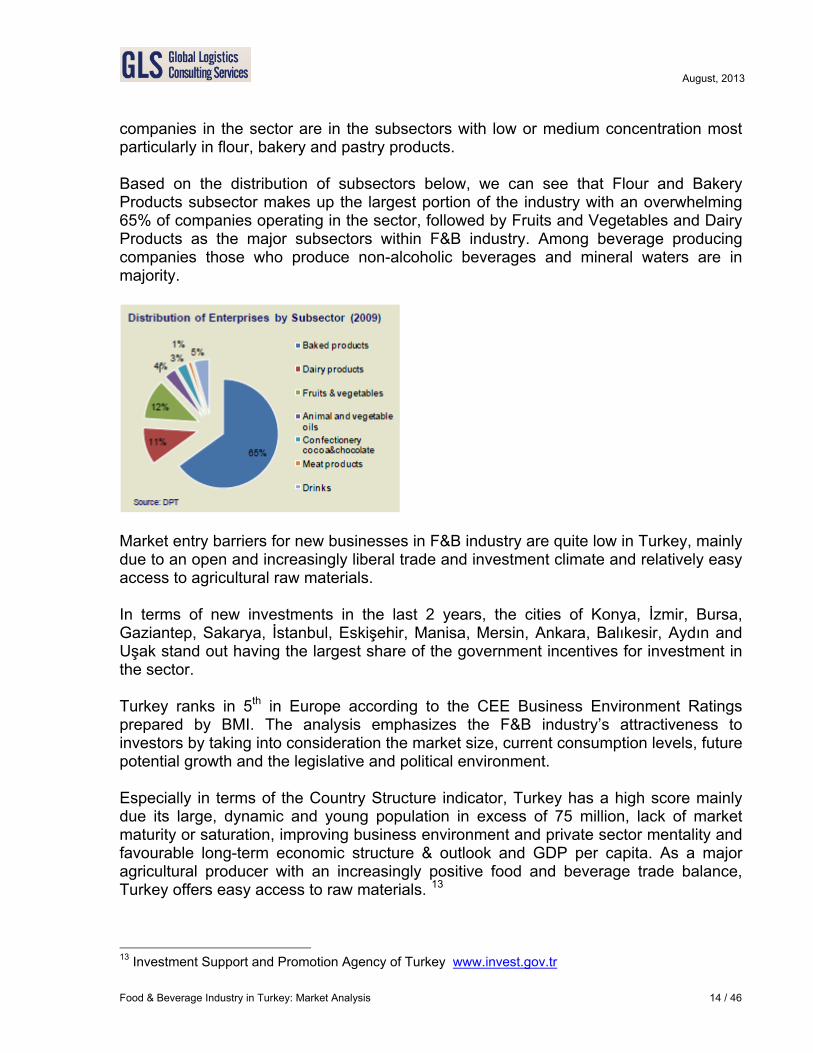

companies in the sector are in the subsectors with low or medium concentration most particularly in flour, bakery and pastry products. Based on the distribution of subsectors below, we can see that Flour and Bakery Products subsector makes up the largest portion of the industry with an overwhelming 65% of companies operating in the sector, followed by Fruits and Vegetables and Dairy Products as the major subsectors within F&B industry. Among beverage producing companies those who produce non-alcoholic beverages and mineral waters are in majority.

Market entry barriers for new businesses in F&B industry are quite low in Turkey, mainly due to an open and increasingly liberal trade and investment climate and relatively easy access to agricultural raw materials. In terms of new investments in the last 2 years, the cities of Konya, İzmir, Bursa, Gaziantep, Sakarya, İstanbul, Eskişehir, Manisa, Mersin, Ankara, Balıkesir, Aydın and Uşak stand out having the largest share of the government incentives for investment in the sector. Turkey ranks in 5th in Europe according to the CEE Business Environment Ratings prepared by BMI. The analysis emphasizes the F&B industry’s attractiveness to investors by taking into consideration the market size, current consumption levels, future potential growth and the legislative and political environment. Especially in terms of the Country Structure indicator, Turkey has a high score mainly due its large, dynamic and young population in excess of 75 million, lack of market maturity or saturation, improving business environment and private sector mentality and favourable long-term economic structure & outlook and GDP per capita. As a major agricultural producer with an increasingly positive food and beverage trade balance, Turkey offers easy access to raw materials. 13

13 Investment Support and Promotion Agency of Turkey www.invest.gov.tr

Food & Beverage Industry in Turkey: Market Analysis 14 / 46

August, 2013

The number of foreign companies operating in Turkey’s F&B sector increased from 280 in 2006 to 520 in 2012. Foreign direct investment (FDI) reached a peak of USD 2.1 billion in 2012 making up 49% of FDI made in manufacturing industries in total. Due to the effects of the global financial crisis, FDI in the manufacturing sector registered shrinkage of 58 percent in 2009 and of 83 percent in the F&B sector. Among 4,729 companies with foreign capital invested in Turkish manufacturing industry as at year/end 2011 making 16% of all foreign companies in Turkey, F&B industry comes second after chemical industry with 468 companies with foreign capital. This constitutes almost 10.4% of foreign companies invested in manufacturing industry. Germany takes the lead with 18.3% of foreign companies in food and manufacturing sector followed by Holland, USA, France and Italy. As the sector offers profitable investment opportunities to global investors, foreign direct investment in the last 10 years has been about USD 4 billion of which USD 2.1 billion was realised in 2012. Total number of companies with foreign capital investment was 14 in 2012.

3.4 Production, Sales and Capacity Utilisation The production value of the F&B industry in 2010 was almost TRY 85 billion making 16% of total manufacturing turnover of almost TRY 525 billion. While food manufacturing subsectors were making TRY 79.5 billion of the industry total, TRY 5.5 billion of this production value was generated by beverages manufacturing subsector respectively. The production value in 2003 was TRY 34.1 billion achieving an increase of 150% in 7 years. The weight of the sector within manufacturing industry in total is around 16% while it makes up 7.2% of production value in the overall Turkish economy. The production index of the food subsectors has increased from 85.1% in 2006 to 110.7% in 2012 while it was 82.8% and 110.0% in beverage/drinks subsector respectively. Between 2006 and 2012, the production index of food subsectors and beverage subsectors had average annual increases of 4.7% and 4.5% respectively while manufacturing industry in total achieved a lower rate of 3.7%. The sales/turnover achieved in 2010 was TRY 88.8 billion of which TRY 5.5 was of from beverages. This figure was TRY 34.4 billion in 2003 representing an increase of 155% in 7 years.

Food & Beverage Industry in Turkey: Market Analysis 15 / 46

August, 2013

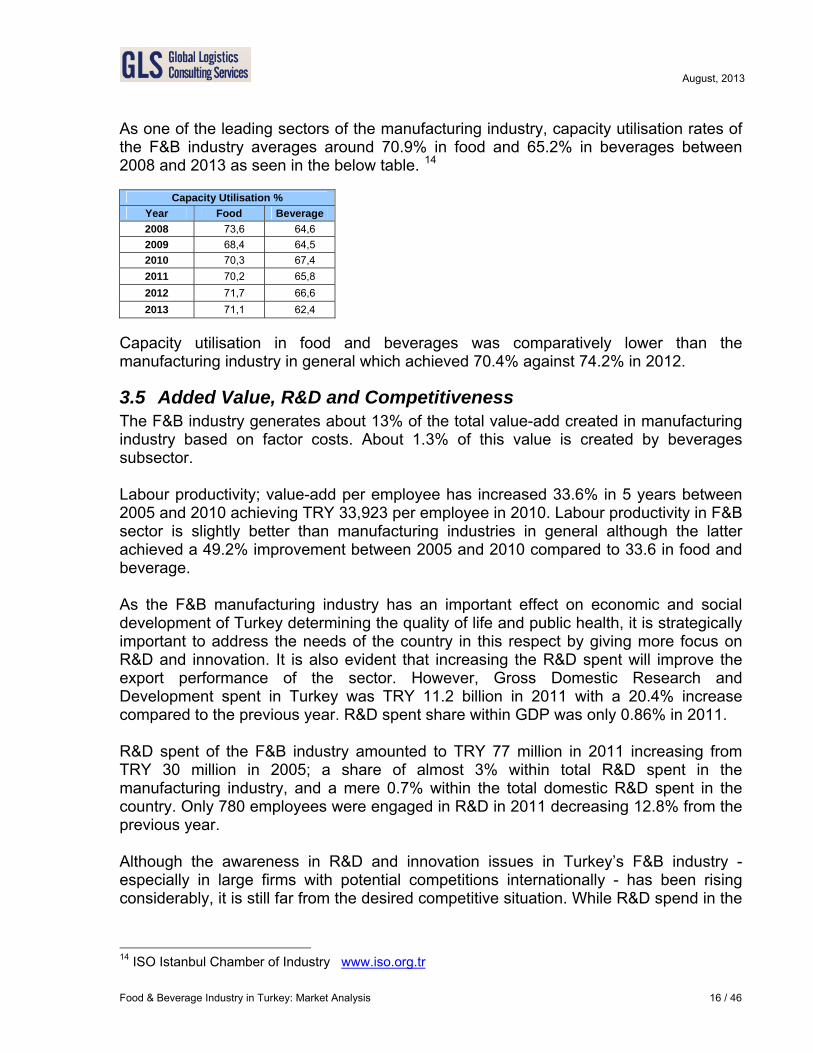

As one of the leading sectors of the manufacturing industry, capacity utilisation rates of the F&B industry averages around 70.9% in food and 65.2% in beverages between 2008 and 2013 as seen in the below table. 14

Capacity Utilisation % Year Food Beverage 2008 73,6 64,6 2009 68,4 64,5 2010 70,3 67,4 2011 70,2 65,8 2012 71,7 66,6 2013 71,1 62,4

Capacity utilisation in food and beverages was comparatively lower than the manufacturing industry in general which achieved 70.4% against 74.2% in 2012.

3.5 Added Value, R&D and Competitiveness The F&B industry generates about 13% of the total value-add created in manufacturing industry based on factor costs. About 1.3% of this value is created by beverages subsector. Labour productivity; value-add per employee has increased 33.6% in 5 years between 2005 and 2010 achieving TRY 33,923 per employee in 2010. Labour productivity in F&B sector is slightly better than manufacturing industries in general although the latter achieved a 49.2% improvement between 2005 and 2010 compared to 33.6 in food and beverage. As the F&B manufacturing industry has an important effect on economic and social development of Turkey determining the quality of life and public health, it is strategically important to address the needs of the country in this respect by giving more focus on R&D and innovation. It is also evident that increasing the R&D spent will improve the export performance of the sector. However, Gross Domestic Research and Development spent in Turkey was TRY 11.2 billion in 2011 with a 20.4% increase compared to the previous year. R&D spent share within GDP was only 0.86% in 2011. R&D spent of the F&B industry amounted to TRY 77 million in 2011 increasing from TRY 30 million in 2005; a share of almost 3% within total R&D spent in the manufacturing industry, and a mere 0.7% within the total domestic R&D spent in the country. Only 780 employees were engaged in R&D in 2011 decreasing 12.8% from the previous year. Although the awareness in R&D and innovation issues in Turkey’s F&B industry - especially in large firms with potential competitions internationally - has been rising considerably, it is still far from the desired competitive situation. While R&D spend in the

14 ISO Istanbul Chamber of Industry www.iso.org.tr

Food & Beverage Industry in Turkey: Market Analysis 16 / 46

August, 2013

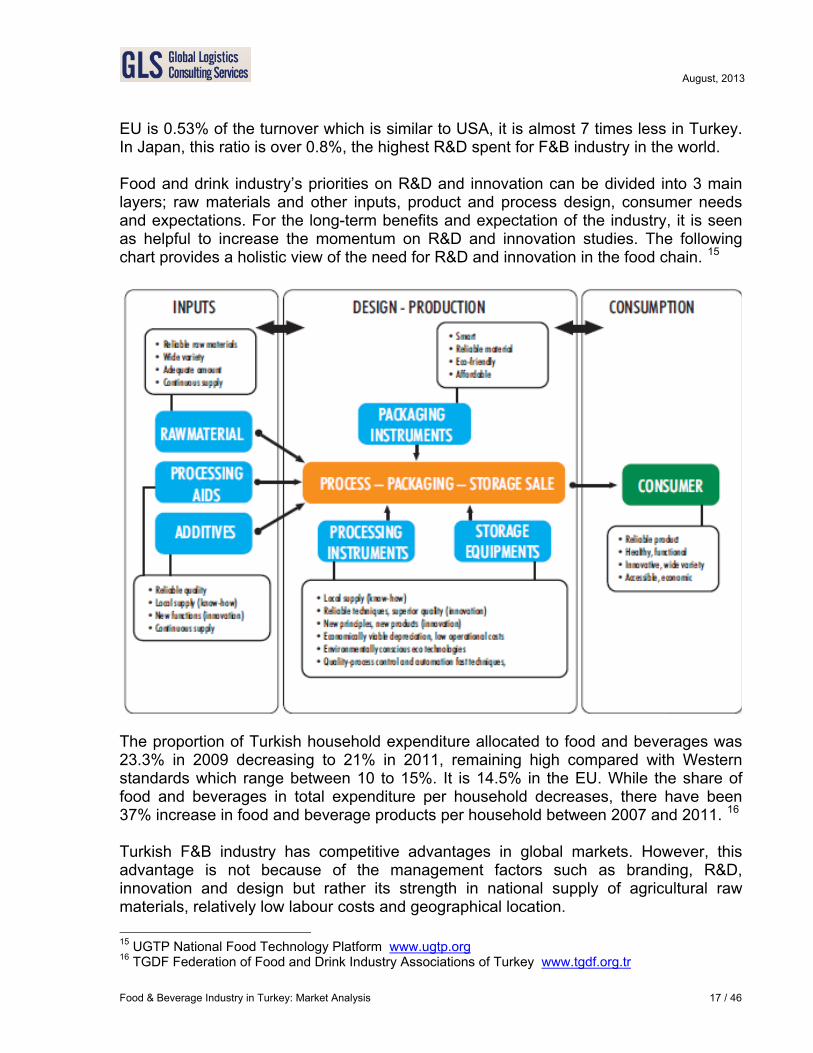

EU is 0.53% of the turnover which is similar to USA, it is almost 7 times less in Turkey. In Japan, this ratio is over 0.8%, the highest R&D spent for F&B industry in the world. Food and drink industry’s priorities on R&D and innovation can be divided into 3 main layers; raw materials and other inputs, product and process design, consumer needs and expectations. For the long-term benefits and expectation of the industry, it is seen as helpful to increase the momentum on R&D and innovation studies. The following chart provides a holistic view of the need for R&D and innovation in the food chain. 15

The proportion of Turkish household expenditure allocated to food and beverages was 23.3% in 2009 decreasing to 21% in 2011, remaining high compared with Western standards which range between 10 to 15%. It is 14.5% in the EU. While the share of food and beverages in total expenditure per household decreases, there have been 37% increase in food and beverage products per household between 2007 and 2011. 16 Turkish F&B industry has competitive advantages in global markets. However, this advantage is not because of the management factors such as branding, R&D, innovation and design but rather its strength in national supply of agricultural raw materials, relatively low labour costs and geographical location. 15 UGTP National Food Technology Platform www.ugtp.org 16 TGDF Federation of Food and Drink Industry Associations of Turkey www.tgdf.org.tr

Food & Beverage Industry in Turkey: Market Analysis 17 / 46

August, 2013

Food and drink industry has not reached its potential limits on high value-added products in internal markets yet. Pre-packaged foods, processed and ready-made frozen meat products, soft drinks and bottled waters are deemed to have potential for development. With the increasing demand for these sectors, it is estimated that more firms will join the fray and the competition will rise. In the approaching period, competition between firms is expected to be on high quality, healthy and hard to imitate products based on R&D activities. One of most important factors of threat for the industry in domestic markets is the unregistered/informal economy with unregistered employees without tax liability and non-compliant counterfeit products to some extent creating unfair competition. It is expected that almost half of the domestic market is affected by this. Lack of market surveillance and controls does not help to improve the situation where more involvement and support of state and local authorities are required.

3.6 Cost Components The main activity of the F&B industry is the procurement of agricultural raw materials and processing and transforming them into high quality food and beverage products. In this process, the main cost elements appear to be raw materials, labour and energy costs together with the costs associated to supply chain management and logistics. The main issues in production which is the focal point of the overall process are energy use, greenhouse gas emissions, resource and waste management, water and waste-water management and packaging in an efficiently planned manner. Although an important investment item, use of technology in the production process will undoubtedly optimise the overall costs. On the other hand, lack of industrial type production, quality issue in agricultural raw materials and higher domestic raw material prices than world markets increase the costs. Supply chain and logistics costs are particularly higher for the storage and distribution of perishable fast moving goods such as fresh products, frozen food, meat, dairy products etc. than the other categories. Appropriate infrastructure and expertise complying with hygiene, health, safety and environmental regulations are required for handling the SCM and logistics requirements of the F&B industry. If the priority is given to develop good agricultural and farming practices for minimising the effects of F&B industry on climate change by means of efficient energy use and waste management (particularly packaging waste), the costs of the industry will be optimised and significant contribution will be made to Turkish economy.

Food & Beverage Industry in Turkey: Market Analysis 18 / 46

August, 2013

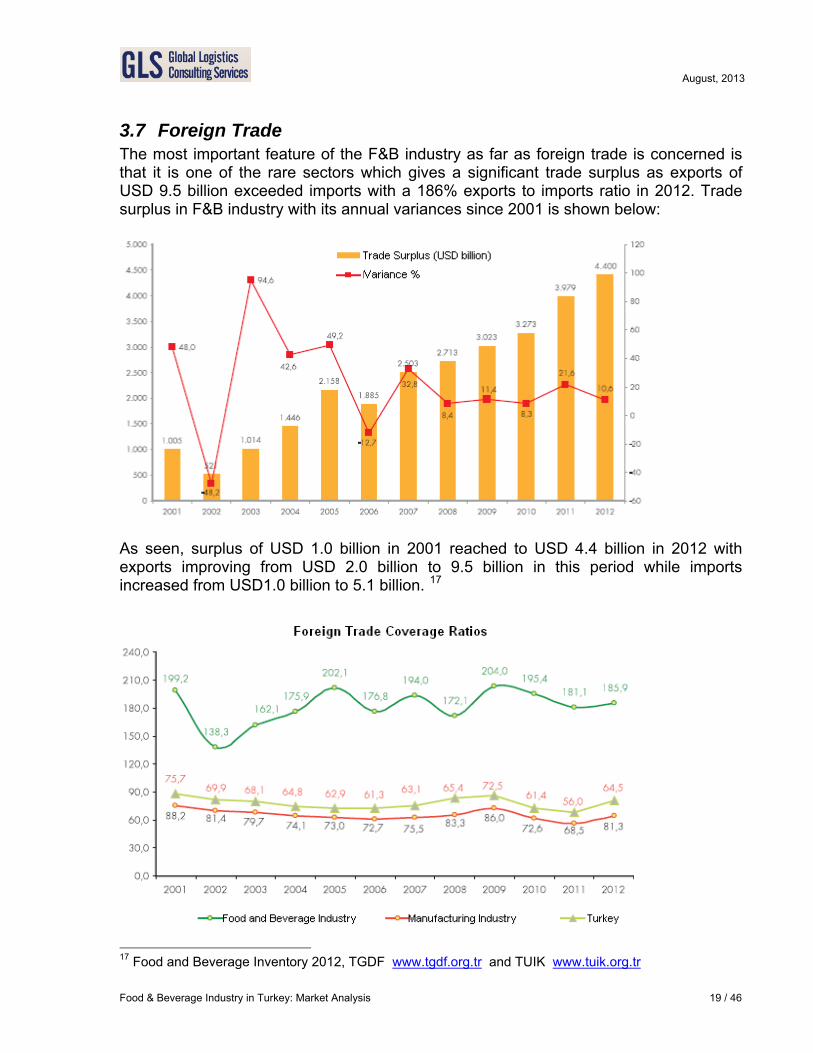

3.7 Foreign Trade The most important feature of the F&B industry as far as foreign trade is concerned is that it is one of the rare sectors which gives a significant trade surplus as exports of USD 9.5 billion exceeded imports with a 186% exports to imports ratio in 2012. Trade surplus in F&B industry with its annual variances since 2001 is shown below:

As seen, surplus of USD 1.0 billion in 2001 reached to USD 4.4 billion in 2012 with exports improving from USD 2.0 billion to 9.5 billion in this period while imports increased from USD1.0 billion to 5.1 billion. 17

17 Food and Beverage Inventory 2012, TGDF www.tgdf.org.tr and TUIK www.tuik.org.tr

Food & Beverage Industry in Turkey: Market Analysis 19 / 46

August, 2013

The above chart confirms that foreign trade coverage of the F&B industry has been performing impressively better compared to manufacturing industry and foreign trade of Turkey in total. Turkey is a major exporter of dried fruit (raisin, apricot), tobacco (from Aegean region) and hazelnuts (from the Blacksea coast). Turkey is the world's largest supplier of hazelnuts. Main agricultural imports include cotton, soya beans, vegetable oils, maize and rice. The following foreign trade figures are classified with NACE Rev.2 and ISIC Rev.4 codes of 10 and 11 for the subsectors of food production and beverage production respectively. 18

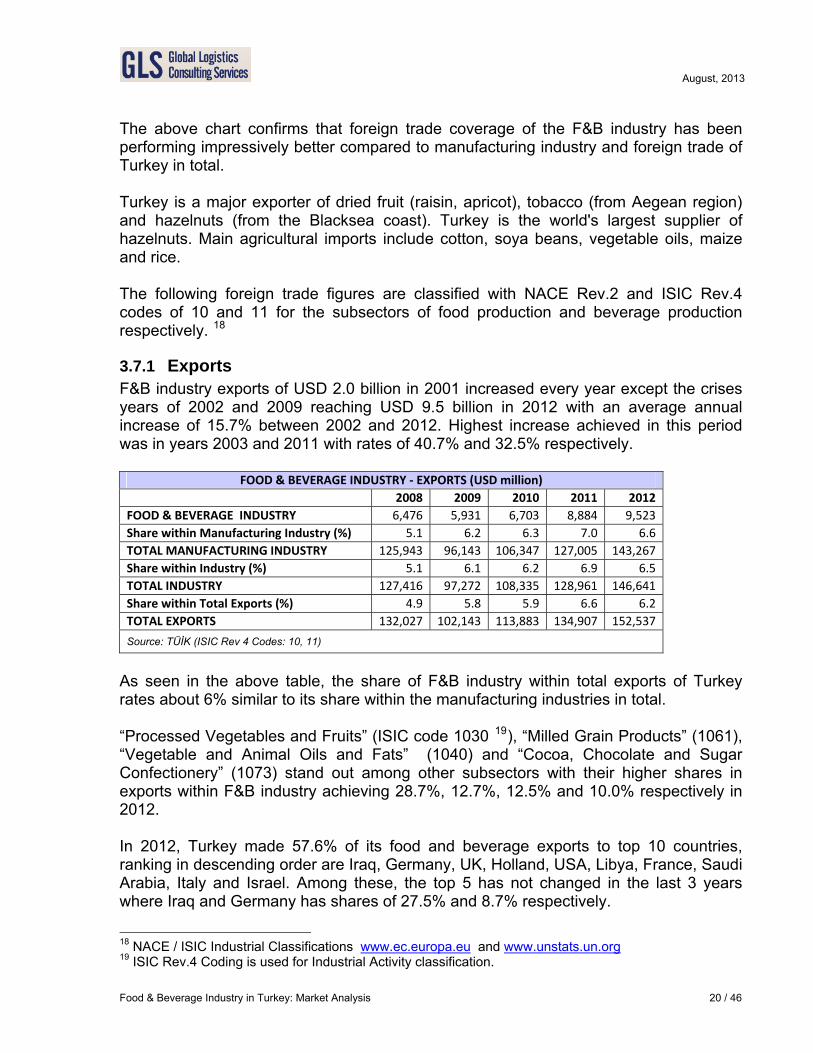

3.7.1 Exports F&B industry exports of USD 2.0 billion in 2001 increased every year except the crises years of 2002 and 2009 reaching USD 9.5 billion in 2012 with an average annual increase of 15.7% between 2002 and 2012. Highest increase achieved in this period was in years 2003 and 2011 with rates of 40.7% and 32.5% respectively.

FOOD & BEVERAGE INDUSTRY ‐ EXPORTS (USD million) 2008 2009 2010 2011 2012 FOOD & BEVERAGE INDUSTRY 6,476 5,931 6,703 8,884 9,523 Share within Manufacturing Industry (%) 5.1 6.2 6.3 7.0 6.6 TOTAL MANUFACTURING INDUSTRY 125,943 96,143 106,347 127,005 143,267 Share within Industry (%) 5.1 6.1 6.2 6.9 6.5 TOTAL INDUSTRY 127,416 97,272 108,335 128,961 146,641 Share within Total Exports (%) 4.9 5.8 5.9 6.6 6.2 TOTAL EXPORTS 132,027 102,143 113,883 134,907 152,537

Source: TÜİK (ISIC Rev 4 Codes: 10, 11)

As seen in the above table, the share of F&B industry within total exports of Turkey rates about 6% similar to its share within the manufacturing industries in total. “Processed Vegetables and Fruits” (ISIC code 1030 19), “Milled Grain Products” (1061), “Vegetable and Animal Oils and Fats” (1040) and “Cocoa, Chocolate and Sugar Confectionery” (1073) stand out among other subsectors with their higher shares in exports within F&B industry achieving 28.7%, 12.7%, 12.5% and 10.0% respectively in 2012. In 2012, Turkey made 57.6% of its food and beverage exports to top 10 countries, ranking in descending order are Iraq, Germany, UK, Holland, USA, Libya, France, Saudi Arabia, Italy and Israel. Among these, the top 5 has not changed in the last 3 years where Iraq and Germany has shares of 27.5% and 8.7% respectively.

18 NACE / ISIC Industrial Classifications www.ec.europa.eu and www.unstats.un.org 19 ISIC Rev.4 Coding is used for Industrial Activity classification.

Food & Beverage Industry in Turkey: Market Analysis 20 / 46

August, 2013

As one of the recent developments, the “Memorandum of Understanding for Food Safety” signed with China is expected to increase Turkey’s exports of agricultural and food products to China especially in vegetable and fruit, poultry and milk/dairy products. On the other hand, Turkey’s share of Russia’s agricultural products imports has been rising in recent years with more improvement forecasted in food products export figures with Russia.

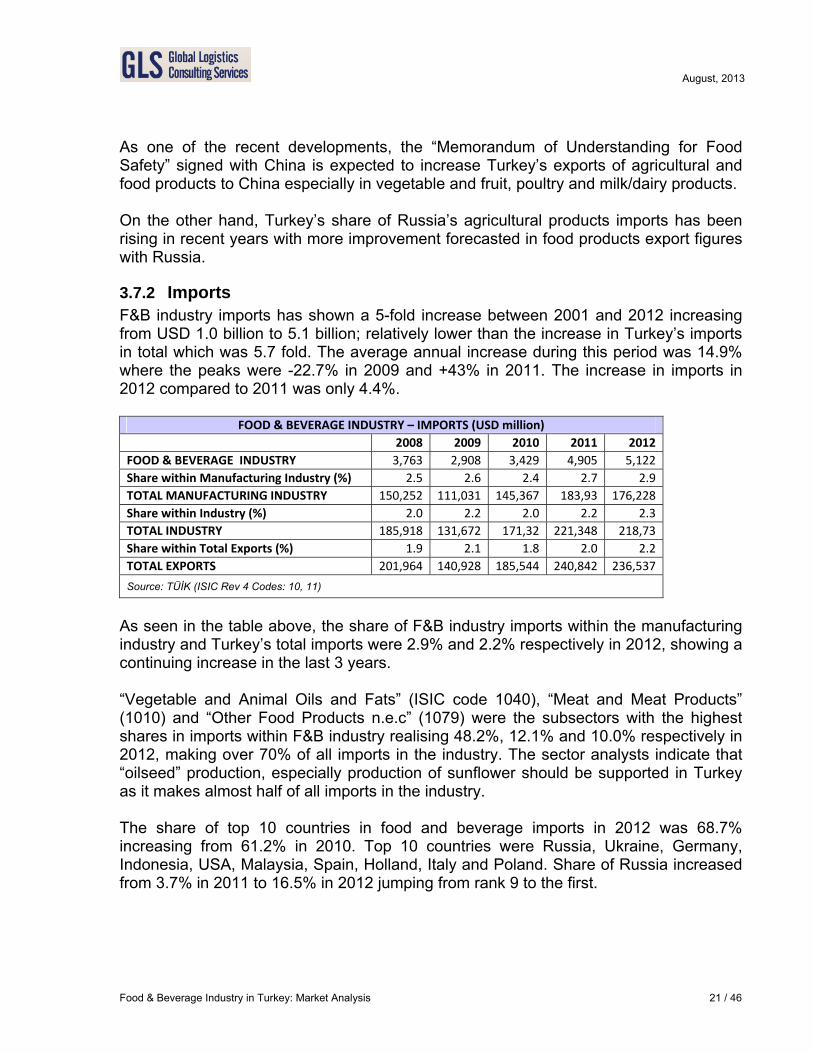

3.7.2 Imports F&B industry imports has shown a 5-fold increase between 2001 and 2012 increasing from USD 1.0 billion to 5.1 billion; relatively lower than the increase in Turkey’s imports in total which was 5.7 fold. The average annual increase during this period was 14.9% where the peaks were -22.7% in 2009 and +43% in 2011. The increase in imports in 2012 compared to 2011 was only 4.4%.

FOOD & BEVERAGE INDUSTRY – IMPORTS (USD million) 2008 2009 2010 2011 2012 FOOD & BEVERAGE INDUSTRY 3,763 2,908 3,429 4,905 5,122 Share within Manufacturing Industry (%) 2.5 2.6 2.4 2.7 2.9 TOTAL MANUFACTURING INDUSTRY 150,252 111,031 145,367 183,93 176,228 Share within Industry (%) 2.0 2.2 2.0 2.2 2.3 TOTAL INDUSTRY 185,918 131,672 171,32 221,348 218,73 Share within Total Exports (%) 1.9 2.1 1.8 2.0 2.2 TOTAL EXPORTS 201,964 140,928 185,544 240,842 236,537

Source: TÜİK (ISIC Rev 4 Codes: 10, 11)

As seen in the table above, the share of F&B industry imports within the manufacturing industry and Turkey’s total imports were 2.9% and 2.2% respectively in 2012, showing a continuing increase in the last 3 years. “Vegetable and Animal Oils and Fats” (ISIC code 1040), “Meat and Meat Products” (1010) and “Other Food Products n.e.c” (1079) were the subsectors with the highest shares in imports within F&B industry realising 48.2%, 12.1% and 10.0% respectively in 2012, making over 70% of all imports in the industry. The sector analysts indicate that “oilseed” production, especially production of sunflower should be supported in Turkey as it makes almost half of all imports in the industry. The share of top 10 countries in food and beverage imports in 2012 was 68.7% increasing from 61.2% in 2010. Top 10 countries were Russia, Ukraine, Germany, Indonesia, USA, Malaysia, Spain, Holland, Italy and Poland. Share of Russia increased from 3.7% in 2011 to 16.5% in 2012 jumping from rank 9 to the first.

Food & Beverage Industry in Turkey: Market Analysis 21 / 46

August, 2013

4 REGULATIONS The F&B industry is a heavily regulated sector mainly due to hygiene, human health and safety and environmental concerns. Although not being a full member of EU, Turkey as a candidate has existing and upcoming obligations for regulations such as Food Codex, CLP, Waste Management, Transport of Dangerous Goods, ATP Convention legislations as well as other law and regulations relating to food safety within the negotiation process started in October 2005 before becoming a full member. It is inevitable that adaptation to these regulations imposes high costs for the companies in the sector. The regulations relating to F&B sector is not collected under a single title within ”acquis communitaire” (EU Law and Policies) rather spread over to 35 different acquis chapters such as Company Environment, Transport Policy, Free Movement of Goods, Social Policy and Employment, Law, Enterprise and Industrial Policy, Taxation, Science and Research, Intellectual Property Law, etc.

Since food products are perishable items, it is very important to adopt and implement food safety and hygiene practices meticulously from raw material to sales stage (including farming, production, storage, transportation and distribution, etc.) with strict monitoring and control systems as well as the implementation of globally recognised production and logistics standards and regulations; such as GAP (Good Agricultural Practise), HACCP (Hazard Analysis Critical Control Points), GMP (Good Manufacturing Practices), GHP (Good Hygiene Practices), GLP (Good Laboratory Practices), RA (Risk Analysis: risk evaluation, management, and communication), BRC (British Retail Consortium) and IFS (International Food Standard) and ATP (International Carriage of Perishable Foodstuffs).

In this section, some of these regulations including EU Food Safety Regulation, Turkish Food Codex, HACCP, CLP, Waste Management, Transport of Dangerous Goods and ATP Convention will be examined briefly relating mainly to the supply chain and logistics requirements of the industry.

Specific technical regulations for food processing and production relating to hygiene, labelling, etc. are not included as it is not seen to be related with the main objective of this report.

4.1 EU Food Safety Regulation As far as the exports to EU are concerned, F&B industry has to comply with the EU requirements of General Food Law, i.e. Food Safety Regulation (EC) No 178/2002 passed in January 2002. Concentrating on food safety, the law ensures that unsafe food harmful and unfit to human consumption can not be placed on the market.

Food & Beverage Industry in Turkey: Market Analysis 22 / 46

August, 2013

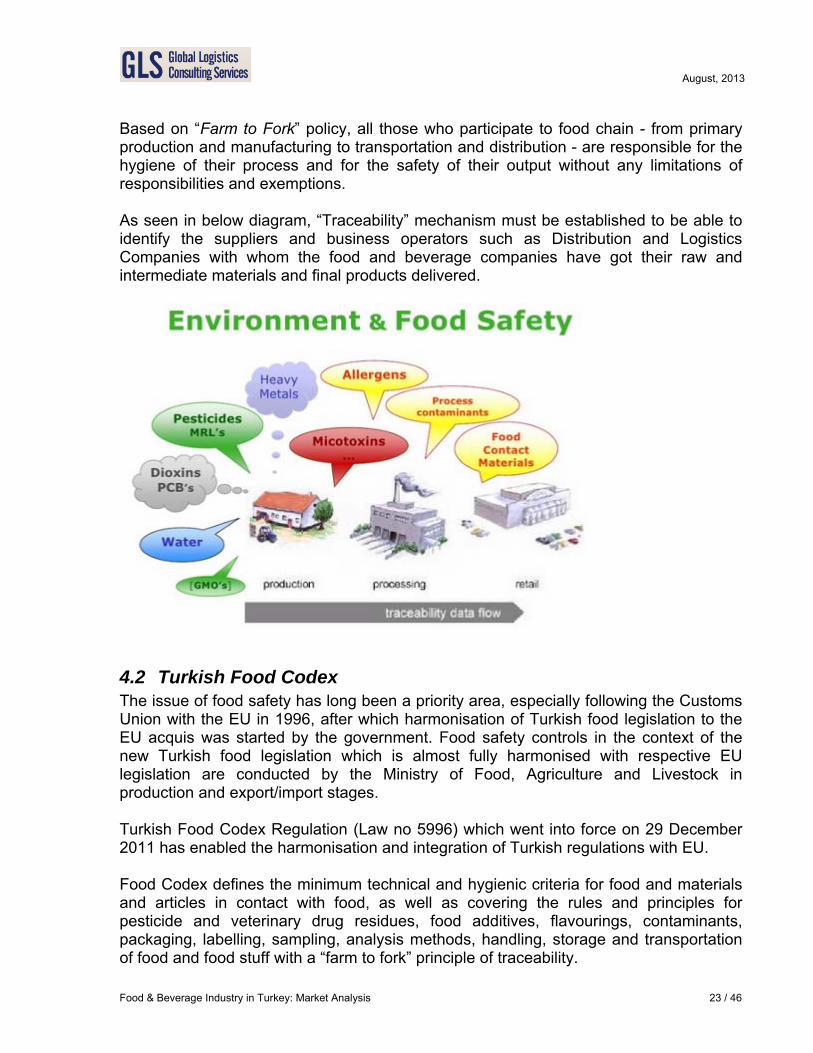

Based on “Farm to Fork” policy, all those who participate to food chain - from primary production and manufacturing to transportation and distribution - are responsible for the hygiene of their process and for the safety of their output without any limitations of responsibilities and exemptions. As seen in below diagram, “Traceability” mechanism must be established to be able to identify the suppliers and business operators such as Distribution and Logistics Companies with whom the food and beverage companies have got their raw and intermediate materials and final products delivered.

4.2 Turkish Food Codex The issue of food safety has long been a priority area, especially following the Customs Union with the EU in 1996, after which harmonisation of Turkish food legislation to the EU acquis was started by the government. Food safety controls in the context of the new Turkish food legislation which is almost fully harmonised with respective EU legislation are conducted by the Ministry of Food, Agriculture and Livestock in production and export/import stages. Turkish Food Codex Regulation (Law no 5996) which went into force on 29 December 2011 has enabled the harmonisation and integration of Turkish regulations with EU. Food Codex defines the minimum technical and hygienic criteria for food and materials and articles in contact with food, as well as covering the rules and principles for pesticide and veterinary drug residues, food additives, flavourings, contaminants, packaging, labelling, sampling, analysis methods, handling, storage and transportation of food and food stuff with a “farm to fork” principle of traceability.

Food & Beverage Industry in Turkey: Market Analysis 23 / 46

August, 2013

All new establishments after effective date of December 2011 have to comply with the Food Codex regulation while existing establishments before this date were allowed a transition time until 01 January 2013 to fully comply with its contents.

The Ministry of Food, Agriculture and Livestock in Turkey has passed many laws, regulations and procedures relating to the industry such as: 20

• Law on Veterinary Services, Plant Health, Food and Feed • Organic Farming Law • Regulation on Veterinary Medicinal Products • Regulations related to the Registry and Confirmation of the Food Businesses • Regulation Concerning the Subjection of Wooden Package Materials to Heat Treatment Process

and Their Marking • Regulation of Special Hygiene Rules for Animal Food • Regulation on Bovine Tuberculosis • Regulation on Feed Hygiene • Regulation on Food Hygiene • Regulation on Official Control of Plant Origin Food and Feed Import • Regulation on Placing Feeds on Market and Their Usage • Regulation on the Working Procedures and Principles of Risk Assessment Committees and

Commissions • Regulation on Turkish Food Codex Microbiological Criteria • Regulation Regarding Official Control of Food and Feed • Regulation on Struggle with Brucellosis • Regulation Determining the Special Rules About the Official Controls on Food of Animal Origin • Issue of Health Certificate for Food of Plant Origin and Feed Export and Implementing Regulation

for Products that Return from Export • Procedure for the Certification of Farms Producing Milk in accordance with the EU Standards • Control Procedure for Milk Facilities to be Approved for Exportation into European Countries

With these law and regulations, 102 in total, Turkey now monitors food safety issues more intensely bringing Turkey up to European standards in terms of food and animal safety with an effective monitoring and tracing mechanism for the agriculture industry all the way from the farm to the dinner table. Tracing mechanism covers all business operators and intermediaries such as primary producers, manufacturers, wholesalers, distributors, retailers, storage and transport service providers, etc. sharing the responsibility if there is a possible problem with the product. The regulations also enhance the process and procedures for carrying out periodic inspections relating to public health, hygiene and food safety.

Food Safety System which the new legislation established in food production is based upon the GAP (Good Agricultural Practise) in the farms; HACCP (Hazard Analysis Critical Control Points), GMP (Good Manufacturing Practices), GHP (Good Hygiene Practices), RA (Risk Analysis: risk evaluation, management, and communication) in the agro-industry, in parallel with the “Farm to Fork” food safety approach of EU. 20 Ministry of Food, Agriculture and Livestock www.tarim.gov.tr

Food & Beverage Industry in Turkey: Market Analysis 24 / 46

August, 2013

Food safety standards are gaining importance as trade regulations. These regulations affect exports in three main ways depending on the capacities of exporting countries; trade-impeding effects, neutral effects, and catalyst effects. Harmonization of standards as a requirement of economic integration also leads to improvement in export performance. The harmonization of EU food safety regulation in 2002 positively influenced the exports of primary food products. The rise in export unit values indicates that Turkish primary food products responded to the EU food safety regulation with quality improvements accompanied by higher unit prices.

4.3 HACCP HACCP is a quality system with a priority in food safety; determining specific hazards, critical points, control methods and corrective measures, and avoiding the hazards before they occur which might affect human health and product quality. First studies on HACCP were carried out by NASA in 1959 for error-free food production for astronauts. World Health Organisation published HACCP principles in its Codex Alimentarius in 1963. In Turkey, establishing HACCP system by food manufacturers was made compulsory and included within the regulation relating to production, consumption and inspection of food in 1998, later enhanced by law no 5179 in June 2004 and by law no 5996 (Law on Veterinary Services, Plant Health, Food and Feed) in December 2011 to make food production compliant with EU regulations. HACCP certification is granted by TSE Turkish Standards Institute and by authorised inspection and certification companies. With the increasing importance of HACCP, companies in F&B industry increase the potential product reliability by reducing the complaints about the product. Enabling the industry to reduce its costs, it enhances the product and company image hence improving its competitiveness especially in global markets.

4.4 CLP The classification, labelling, packaging and notification of food and feed substances and mixtures including food colourings, preservatives and food additives are regulated by CLP European Regulation. CLP Regulation (no. 1272/2008/EU) which came into force on 20 January 2009 aims to apply United Nation’s Globally Harmonized System GHS criteria. The Regulation is about the hazards of substances and mixtures and how to inform others about them. It is the task of industry to establish what are the hazards of substances and mixtures before these are placed on the EU market, and to classify them in line with the identified hazards. The companies that produce or import the substances and mixtures in EU will have to classify, label and package their products under CLP rules after a transition period.

Food & Beverage Industry in Turkey: Market Analysis 25 / 46

August, 2013

Two target dates were defined that affect the classification, hazard communication and packaging of hazardous substances and mixtures; 1st December 2010 for substances and 1st June 2015 for mixtures. Since the fines for not complying with CLP regulation is quite high, companies exporting to EU do give great emphasis for the implementation procedures.

4.5 Waste Management EU waste legislation is formed with the principles of encouraging environmentally friendly production technology and processes producing minimum level of waste, re-usage as much as possible, enabling recycling or making it usable as a source of energy, and improving waste disposal through effective means of environmental legislation. Turkey has achieved substantial compliance to the Regulation on General Principles of Waste Management published in 2008, Waste Framework Directive of EU 2006/12/EC and to IPPC Directive on Integrated Pollution Prevention and Control. Regulations prepared based on EU Waste Catalogue and Decision 2000/532/EC for establishing a Waste List, lists all hazardous and non-hazardous waste in a way consistent with EU. In addition, National Waste Management Plan (2009-2013) has been accepted within the framework of “Methodological Guide to the Preparation of Waste Management Plan”. It is envisaged that Regional/Local Waste Management Plans are prepared in addition to the so called plan aiming to build a Waste Management System which is more organised, integrated and institutionally structured. Released in 2010, the Regulations on Landfill and Incineration of Waste have harmonised the Turkish legislation with the relevant regulations of EU. Turkey has achieved substantial compliance to EU legislation regulating management of packaging waste (Packaging and Packaging Waste Directive 94/62/EC with amendments 2004/12/EC and 2005/20/EC) by means of “Packaging Waste Control Regulation” which came into force in 2007 and updated in 2011. The regulation does not contain recovery and recycling targets for packaging materials while it is compatible with EU rules in many respects particularly including essential requirements for releasing and using the packaging products on the market, the maximum limit for concentrations of heavy metals, marking the packaging products during production, and the management of packaging waste According to TUIK, 12.5 million tons of waste was produced by the manufacturing industry in total in 2008. Almost 20% of this was generated by F&B industry.

4.6 Dangerous Goods Transportation EU regulation on the transport of dangerous goods covers the transport of these goods within and among EU countries by means of road, rail and inland waterways. The relevant Directive contains provisions on the implementation of international agreements that sets the rules and regulations governing the transport of dangerous goods both

Food & Beverage Industry in Turkey: Market Analysis 26 / 46

August, 2013

internationally and nationally. These international agreements are European Agreement on the International Carriage of Dangerous Goods by Road (ADR), Regulations Concerning the International Carriage of Dangerous Goods by Rail (RID), and the European Agreement on the International Carriage of Dangerous Goods by Inland Waterways (ADN). Classification, packaging, labelling, loading and unloading of the goods in question, technical standards which should be complied by transport vehicles, appointment and training of security advisers in addition to the rules concerning the transport of dangerous goods and common audit procedures are some of the criteria which have been transferred and adapted to EU legislation in line with international regulations and agreements. In order to transfer and implement the relevant EU legislation, Turkey has approved and published the ADR Regulation for the transport of dangerous goods by road in March 2007 including the amendments to this regulation later in June 1008, July 2009 and December 2010. However, only certain items of the ADR Regulation have been in force due to a defined gradual implementation schedule. Accordingly, the items relating to the objective, scope and underlying provisions and definitions went into effect as of January 2011 while the application about packaging, labelling and marking officially started in January 2012. The provisions concerning transport vehicles and units which is the most crucial part of the regulation was going to go into force in January 2013 but postponed to January 2014. The remaining provisions of the ADR Regulation will come into force in January 2014 if not postponed again. RID Regulation concerning the international transport of dangerous goods by rail was applied as an enclosure/appendix to the existing COTIF Convention for International Carriage by Rail of which Turkey is a party since 1999. ADN Agreement for international carriage of goods by inland waterways has not been transferred into Turkish law yet. Transport of Dangerous Goods by Sea has been applied in line with the provisions of IMDG code as in the EU. Regulation for the training and authorisation under international code relating to dangerous cargo by sea was published in February 2012. This regulation relating to dangerous cargo transported by sea defines the rules and procedures for classification, packaging, marking, labelling, name-plating, loading-unloading, load handling, stacking, preparation of shipping documents and evacuation plans, storage, transportation as well as the training of persons involved in preparation, control and audit processes, etc. Regulation for the Transport of Dangerous Goods by Air published by the Ministry of Transport Directorate General of Civil Aviation sets the rules and procedures in accordance with the ICAO Technical Instructions, as in the EU.

Food & Beverage Industry in Turkey: Market Analysis 27 / 46

August, 2013

4.7 ATP Convention “The Agreement on the International Carriage of Perishable Foodstuffs and on the Special Equipment to be Used for such Carriage” (ATP) was approved in September 1970 and entered into force on 21 November 1976. The main objective of the ATP Convention is to ensure the safe transportation of perishable food to protect human health. ATP is an Agreement between countries and there is no overall enforcing authority. In practice, highway checks are carried out by contracting parties, and non-compliance may then result in legal action by national authorities against offenders in accordance with their domestic legislation. ATP itself does not prescribe any penalties. Currently, there are 52 countries party to the convention. 21 Turkey was not a party to the Convention for years until it was approved by the Parliament and published in the Official Gazette on 10 May 2012 as Law no 6298 relating to become a party to ATP Convention. Although the approval of becoming party to ATP convention has been achieved, the relevant legislation and regulations will need to go into force with the establishment of relevant infrastructure including the testing and FRC certification facilities for the refrigerated transportation units used in cold chain transportation both international and domestic. The full application of the convention will go into force one year after the acceptance of Turkey’s application to UN by the Ministry of Transport, Maritime Affairs and Communications. The convention which has been expected by F&B industry for a long time will contribute to Turkey’s export targets and eliminate economic losses due to waste of perishable products during their transportation under inappropriate conditions. It is calculated that in 2011, approximately 25% of 46 million tons of fresh produce (fruits and vegetables) with a value of almost TRY 19 billion is wasted due to inappropriate packaging, storage, transportation and shelving not confirming to international good practices and regulations. This figure does not include other categories of perishable food such as milk-dairy, meat, fish, poultry, etc. products where the waste in these categories is estimated to total up to 500,000 tons a year. 22 The wish of the industry is now to see the full application of the convention as soon as possible avoiding the lengthy process experienced in ADR Regulation which is still not in full force.

21 UNECE United Nations Economic Commission for Europe www.unece.org 22 Ministry of Customs and Trade www.gtb.gov.tr

Food & Beverage Industry in Turkey: Market Analysis 28 / 46

August, 2013

5 SUPPLY CHAIN & LOGISTICS The optimisation of the supply chain and logistics processes is particularly important for the sustainable development, growth and competitiveness of not only the F&B industry itself but for the economic growth and competitiveness of Turkey as a whole. Having the largest fleet of trucks in Europe, most of the domestic transportation within Turkey, as well as to/from near geographies such as Europe, Near and Middle East is done by road. However, further investment is required in cold chain storage and transportation since the supply chain infrastructure for cold chain products needs improvement. As well as the manufacturer, users and customers, Supply Chain Management (SCM) covers the agricultural and processed mixtures and substances suppliers of the F&B industry, warehouse, terminal and port operators, domestic and international transportation companies as carriers and forwarders (road, rail, sea, inland waterways and intermodal), customs brokers, and many other intermediary business lines and people. In order to ensure the integrity and continuity of the integration between order and delivery, coordination of all these parties in the supply chain in line with environment, hygiene, health and safety regulations is inevitably very critical which should be handled in a specialised manner by the experts. SCM requires the understanding and compliance with laws and regulations to ensure the fulfilment of all the conditions relating to documentation and tracing of products and shipments as well as storage, handling, packaging, labelling, transportation, etc. These conditions may vary depending on the countries, different regions of a country and the level of the international trade. The complex structure of the operating environment involving many parties requires a comprehensive exchange of information. The systems and data used may not be technically compatible with each other, most of the time. SCM is becoming more and more dependent on rapidly evolving Information Technology in terms of its effectiveness. Increasing use of RFID technology in supply chain traceability is an example for the importance of IT in SCM. “Traceability” in the supply chain especially for perishable food products such as fresh vegetable and fruits, meat and dairy products and frozen food is very critical for food safety, hygiene and human health; supported by a proper storage and transportation infrastructure. Geographical traceability, also called Geographical Indication (GI) is also becoming important for the traceability of agricultural raw materials and substances used during the manufacturing of food products to their original location of production.

Food & Beverage Industry in Turkey: Market Analysis 29 / 46

August, 2013

Logistics service providers to F&B industry should focus improving the hygienic conditions and traceability in their facilities and transportation vehicles and units which is a must for the sector in terms of food safety. Providing logistics services to F&B industry requires expertise and higher investment than the other industrial sectors such as durable goods and FMCG. Therefore, as will be seen in the following section, the number of major logistics service providers to F&B industry is limited in Turkey not comparable to other industrial sectors. Most companies in F&B industry still prefers to handle their own supply chain and logistics requirements with their own resources because of the limited number of logistics service providers meeting the necessary criteria and regulations of the F&B industry. While not compulsory, some system standards such as ISO-9001 Quality Management System, ISO-14001 Environmental Management System and OHSAS-18001 Occupational Health and Safety Management System are becoming increasingly common in F&B industry mostly implemented depending on the supplier-customer relationships. Additionally, GMP (Good Manufacturing Practices), GHP (Good Hygiene Practices), GLP (Good Laboratory Practices), RA (Risk Analysis: risk evaluation, management, and communication), BRC and IFS systems are adopted and applied particularly by major players in Turkey IN F&B industry, where effective storage and distribution has upmost importance for food safety, one of the main elements for global competitiveness has undoubtedly been the successful management of the supply chain especially for perishable fresh produces and cold chain products. Therefore, focusing on “SCM effectiveness” is vital firstly for establishing then preserving the sustainable competitiveness of the Turkish F&B industry. With this in mind, the parties in the F&B industry should cooperate with each other and invest for the optimisation of their SCM processes including the handling of logistics activities by global expert service providers to F&B industry.

5.1 Logistics Service Providers to Food & Beverage Industry It is an accepted fact that outsourcing the logistics processes to expert service providers enables significant benefits to manufacturers by creating economies of scale and reducing the unit costs where logistics costs have a significant share. Outsourcing also enables the companies to concentrate their own core processes such as R&D, production, marketing and sales increasing the effectiveness of their supply chain including inventory efficiency and most importantly their customer satisfaction and competitiveness. This is even more valid for the companies in F&B industry since the handling, storage and transportation of foodstuff and beverages require upmost expert attention complying with national and international regulations relating to human health in terms

Food & Beverage Industry in Turkey: Market Analysis 30 / 46

August, 2013

of hygiene and safety, and the environment in the strictest way. This is very critical for the sector as highlighted. As far as the logistics service providers providing specialised expert services required by the F&B industry in Turkey is concerned, one can only spell out the names of a limited number of logistics companies. Most of these service providers concentrate only to the storage and transportation (particularly domestic) of the inputs and outputs of the industry in liquid, powder and/or gas form by appropriate transportation units such as IBCs, flexi-tanks, tank cars/wagons, trucks and containers; in refrigerated form for cold chain foodstuff and products. The full enactment of the international regulations mentioned, particularly ADR regulation for dangerous goods and ATP Convention for perishable food, will complete the transformation on the transportation of dangerous and perishable goods which is very critical to F&B industry. These regulations will benefit expert logistics service providers which have understood the seriousness of this transformation hence made the necessary investments accordingly. Currently, road freight has the biggest share followed by sea in transportation of the F&B industry products and materials. Having the largest fleet of trucks in Europe reaching almost 50,000, it is estimated that 12,000 of these have refrigerated units appropriate for perishable food and cold chain transportation. Rail freight is expected to gain momentum when the existing projects for rail transportation infrastructure are completed. This is strategically important for foreign trade to/from Europe, Middle and Near East regions. In terms of storage requirements is concerned, a small portion of sector requirement is outsourced to logistics service providers in Turkey. In this respect, there is a considerable market for specialised storage and value-added warehousing services for the logistics sector to meet this requirement of the F&B industry. This potential is also valid for on-site value-added services to support pre and post-production processes of the industry within its manufacturing facilities. The volume of imports and exports in terms of tonnage in F&B industry has been recorded as almost 10 million tons in 2012 while the share of logistics spent in the industry reaches as high as 15% within its total costs. There is a considerable potential for logistics service providers in Turkey which could meet the strict regulations and the requirements of the F&B industry by means of establishing the right infrastructure and the procedures for hygiene and food safety. As well as the growing market for domestic distribution, logistics sector has a vital importance for Turkish economy in order to be able to reach the export targets of the F&B industry and other sectors, particularly to the markets in close proximity to Turkey.

Food & Beverage Industry in Turkey: Market Analysis 31 / 46

August, 2013

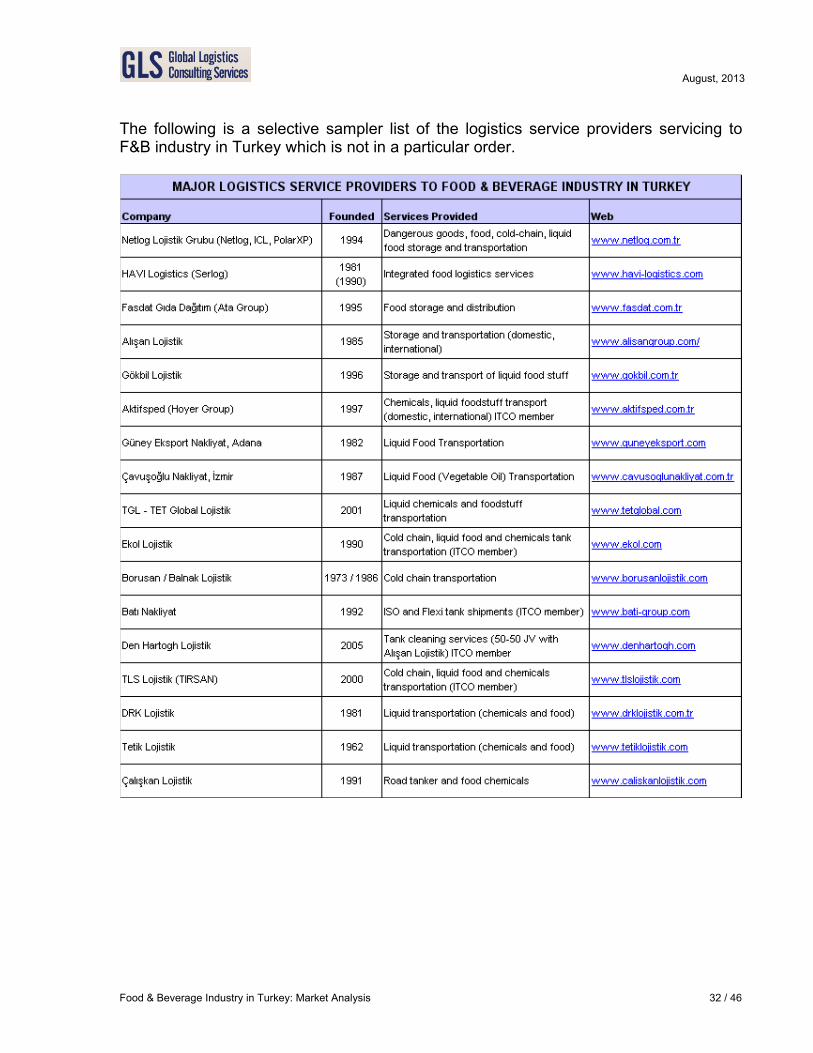

The following is a selective sampler list of the logistics service providers servicing to F&B industry in Turkey which is not in a particular order.

Food & Beverage Industry in Turkey: Market Analysis 32 / 46

August, 2013

6 MAIN PLAYERS

Food & Beverage Industry in Turkey: Market Analysis 33 / 46

August, 2013

Food & Beverage Industry in Turkey: Market Analysis 34 / 46

August, 2013

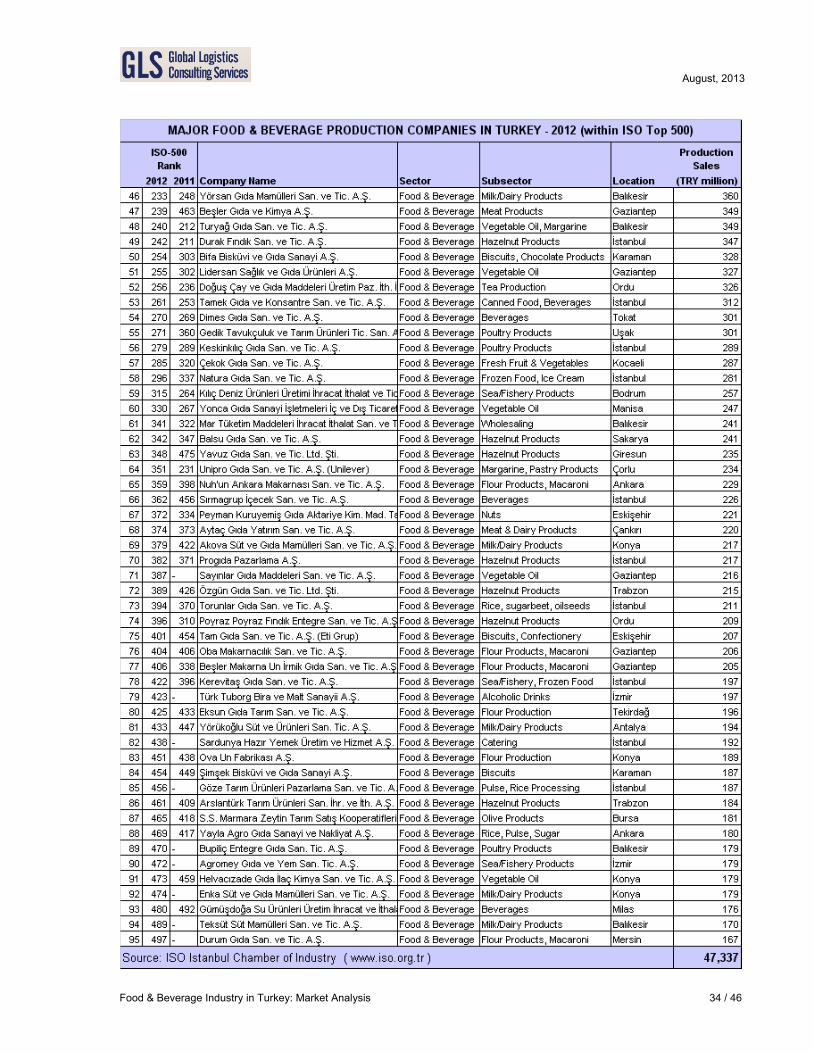

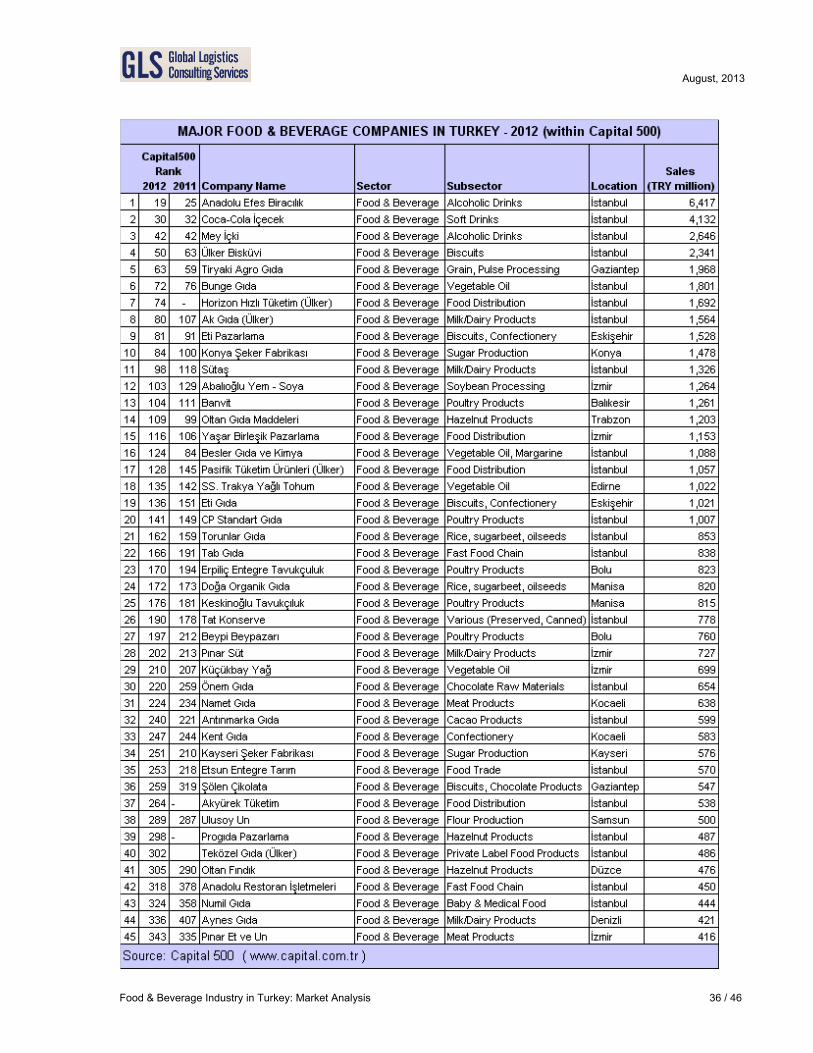

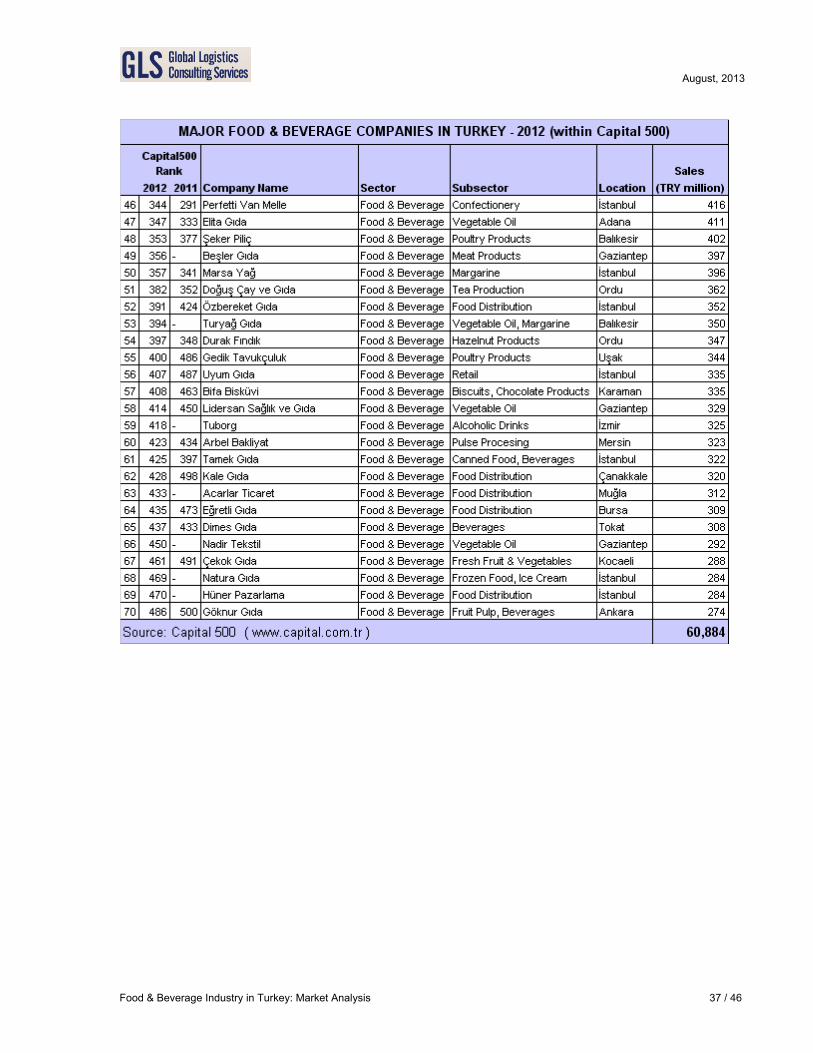

The above list of 95 companies operating within the F&B industry has been derived from the “Top 500 Industrial Companies of Turkey” as at year ending 2012 published by ISO Istanbul Chamber of Industry. 23 As could be identified with our own interpretation, companies in the F&B industry make a total of TRY 47.3 billion of production based net sales corresponding to 13.6% of Top-500 in 2012 out of TRY 348 billion. (Note: Share of 13.6% could be misleading since the details of 17 new entry companies including their sales turnover are not listed in top 500 list) Out of 95 food and beverage production companies listed in ISO-500, Vegetable Oil Production subsector ranks first with 12 companies, followed by Poultry Products (10), Dairy/Milk Products (9), Biscuits & Confectionery (9), Hazelnut Products (9), Beverages (6), Flour Production (6) and Meat Products (5). In terms of location, city of İstanbul ranks first with 27 companies, followed by Gaziantep (8), Balıkesir (7), İzmir (5) and Konya (5) as major locations. While ISO 500 List above ranks the industrial companies in the manufacturing industry based on their production-based net sales only, recently published “Capital 500” list of Capital business magazine listed 70 companies in F&B industry within Turkey’s top 500 private companies (including manufacturing, services and trade, but excluding banking and finance) in its August 2013 issue based on their 2012 total sales turnover. 24 In Capital 500 list included on the following pages, total sales of all 70 food and beverage companies listed amounts to TRY 61 billion within a total of TRY 662 billion. Having a 9.2% share within top 500, these 70 companies involved in the manufacturing, trade, distribution of food and beverages and fast food chains. Based on Capital 500 list of top 500 private companies in Turkey, with a total of 70 companies, F&B sector takes the lead far ahead of automotive sector with 42 companies followed by energy-petrol and chemical sector with 37 companies each.

23 ISO Istanbul Chamber of Industry, Top 500 Industrial Companies of Turkey http://www.iso.org.tr/tr/web/BesYuzBuyuk/turkiye-nin-500-buyuk-sanayi-kurulusu--iso-500-raporunun-sonuclari.html 24 Capital 500, Capital Magazine August 2013 www.capital.com.tr

Food & Beverage Industry in Turkey: Market Analysis 35 / 46

August, 2013

Food & Beverage Industry in Turkey: Market Analysis 36 / 46

August, 2013

Food & Beverage Industry in Turkey: Market Analysis 37 / 46

August, 2013

7 SWOT ANALYSIS The following SWOT analysis aims to show the strong (strengths and opportunities) and weak (weaknesses and threats) points of the F&B industry in Turkey analysing its ability for global competitiveness. It is a compilation derived from the information available in various resources such as TGDF Federation of Food and Drink Industry Associations of Turkey, UGTP National Food Technology Platform, Investment Support and Promotion Agency of Turkey, and Ministry of Science, Industry and Technology. 25