Appendix 1: Materials used by Mr. Kos January 27-28, 2004 195 of 238

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Appendix 1: Materials used by Mr. Kos

January 27-28, 2004 195 of 238

January 27-28, 2004 196 of 238

Appendix 2: Materials used by Mr. Reinhart

January 27-28, 2004 197 of 238

January 27-28, 2004 198 of 238

January 27-28, 2004 199 of 238

January 27-28, 2004 200 of 238

January 27-28, 2004 201 of 238

January 27-28, 2004 202 of 238

January 27-28, 2004 203 of 238

January 27-28, 2004 204 of 238

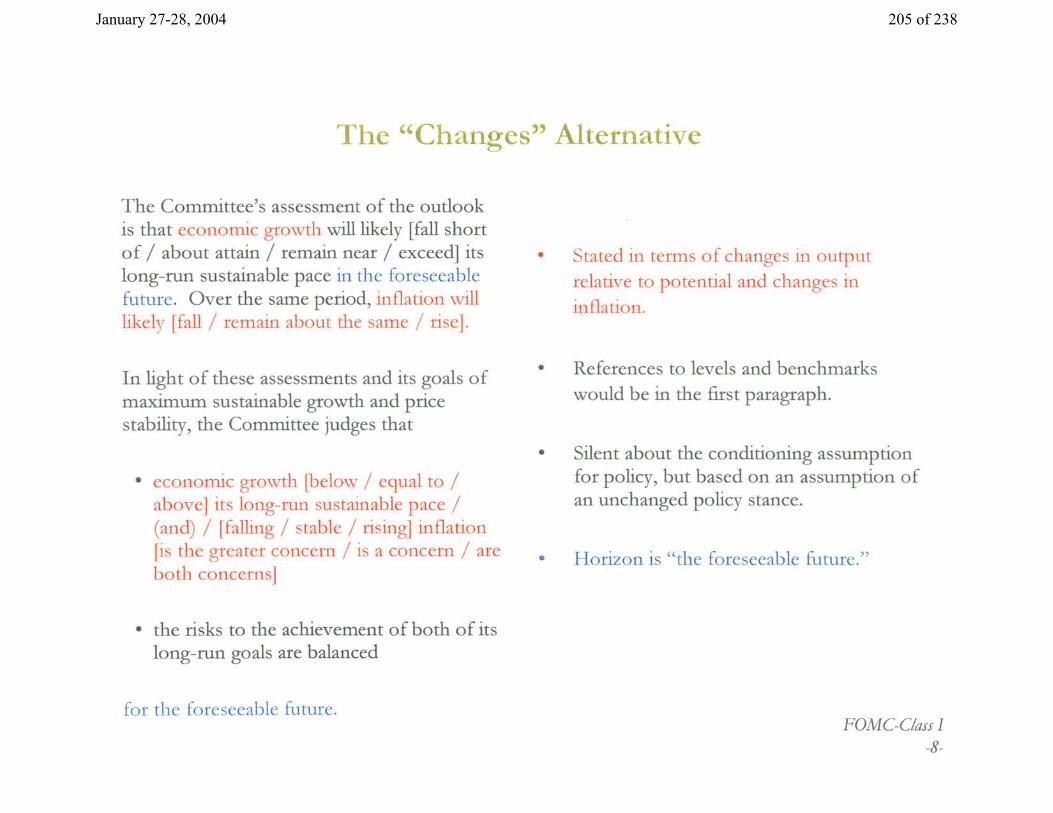

January 27-28, 2004 205 of 238

January 27-28, 2004 206 of 238

January 27-28, 2004 207 of 238

January 27-28, 2004 208 of 238

January 27-28, 2004 209 of 238

Appendix 3: Materials used by Mr. Kos

January 27-28, 2004 210 of 238

Current U.S. 3-Month Deposit Rates andRates Implied by Traded Forward Rate Agreements

October 1, 2003 - January 26, 2004 LIBOR Fixing 3M Forward 6M Forward 9M Forward

Page 1

0.51.01.52.02.53.03.54.04.55.0

1/1/2003 3/1/2003 5/1/2003 7/1/2003 9/1/2003 11/1/2003 1/1/20040.51.01.52.02.53.03.54.04.55.0

Treasury Note YieldsJanuary 1, 2003 - January 26, 2004 PercentPercent

2-Year Note

10-Year Note

1.00

1.50

2.00

2.50

10/1 10/15 10/29 11/12 11/26 12/10 12/24 1/7 1/211.00

1.50

2.00

2.50

90

95

100

105

110

115

120

9/1 9/20 10/9 10/28 11/16 12/5 12/24 1/1290

95

100

105

110

115

120

375400425450475500525550

9/1 9/20 10/9 10/28 11/16 12/5 12/24 1/12375400425450475500525550

Investment Grade Corporate Debt SpreadSeptember 1, 2003 - January 26, 2004

High Yield and EMBI+ SpreadsSeptember 1, 2003 - January 26, 2004

Basis Points Basis PointsBasis PointsBasis Points

Source: Merrill Lynch, JP MorganSource: Lehman Brothers

10/28FOMC

11/7 Oct.NFP:+126K

12/5 Nov.NFP:+57K

12/9FOMC

1/9 Dec.NFP: +1K

Merrill Lynch HighYield Bond Index OAS

EMBI+

Investment Grade CorporateIndex OAS

9/16FOMC

10/28 FOMC12/9FOMC

9/16 FOMC10/28FOMC

12/9 FOMC

6/25 FOMC:-25 BP

Percent Percent

12/9 FOMC

January 27-28, 2004 211 of 238

Page 2

Select Foreign Currencies Versus U.S. DollarAugust 1, 2003 - January 26, 2004 Index: 100 = 8/1/03Index: 100 = 8/1/03

80

85

90

95

100

105

8/03 9/03 10/03 11/03 12/03 1/0480

85

90

95

100

105

0

10

20

30

40

50

60

70

S&P 500 Nasdaq DJ Euro Stoxx Nikkei0

10

20

30

40

50

60

70

Global Equity ReturnsJanuary 1, 2003 - January 26, 2004

PercentPercent

-50

0

50

100

150

200

1/03 3/03 5/03 7/03 9/03 11/03 1/04-50

0

50

100

150

200

Interest Rate Differentials: Select 3-MonthGovernment Spreads to U.S. Treasuries

January 1, 2003 - January 26, 2004

Interest Rate Differentials: Select 10-YearGovernment Yields less U.S. Treasury Yields

January 1, 2003 - January 26, 2004Basis PointsBasis PointsBasis Points Basis Points

British Pound

Japanese Yen Australian Dollar

Canadian DollarEuro

Index Returns Returns in Euro Returns in Yen Returns in Dollars

50

100

150

200

250

300

350

400

1/03 3/03 5/03 7/03 9/03 11/03 1/0450

100

150

200

250

300

350

400

Australia

Great Britain

Canada

Germany

Australia

Canada

Germany

Great Britain

12/9FOMC

1/4 BernankeAEA Speech

1/12 Trichetcomments oneuro

U.S. DollarDepreciation

January 27-28, 2004 212 of 238

Page 3

105

110

115

120

125

8/03 9/03 10/03 11/03 12/03 1/04105

110

115

120

125

Japanese Yen Versus U.S. DollarAugust 1, 2003 - January 26, 2004

Yen per Dollar

-30

0

30

60

90

120

150

180

210

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004-30

0

30

60

90

120

150

180

210

Japanese Net Yearly Intervention in Dollar-Yen1989 - 2004 USD BillionsUSD Billions

600

650

700

750

800

850

900

1/1 3/1 5/1 7/1 9/1 11/1 1/1150

175

200

225

-30-101030507090

110130150

1/1 3/1 5/1 7/1 9/1 11/1-30-101030507090110130150

FRBNY Custody Holdings of Treasury andAgency Securities

January 2003 - January 2004

TIC Data: Cumulative Foreign Treasury Note andBill Purchases

January 2003 - January 2004USD BillionsUSD Billions

PrivatePurchases

Official Purchases

Yen per Dollar

Japanese Interventionin the IntermeetingPeriod: $80.5 bn

YTD

USD Billions

Treasuries (LHS)

Agencies(RHS)

USD Billions

12/9 FOMC

January 27-28, 2004 213 of 238

Percent Percent

Page 4

70

90

110

130

150

170

1/03 2/03 3/03 4/03 5/03 6/03 7/03 8/03 9/03 10/03 11/03 12/03 1/0470

90

110

130

150

170Index 100 = 1/6/2003Index 100 = 1/6/2003

2.00

2.25

2.50

2.75

3.00

10/1 10/15 10/29 11/12 11/26 12/10 12/24 1/7 1/212.00

2.25

2.50

2.75

3.00

Current Euro Area 3-Month Deposit Rates andRates Implied by Traded Forward Rate Agreements

October 1, 2003 - January 26, 2004

0.0

0.5

1.0

1.5

0.0

0.5

1.0

1.5

Japanese Yield Curve PercentPercent

3M 6M 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y

LIBOR Fixing 3M Forward 6M Forward 9M Forward

January 26, 2004

January 24, 2003

June 13, 2003

Bank Sub-Index

Electronics Sub-Index

Topix

12/9FOMC

Japanese Topix Index and Select Sub-IndicesJanuary 1, 2003 - January 26, 2004

January 27-28, 2004 214 of 238

Appendix 4: Materials used by Mr. Slifman

January 27-28, 2004 215 of 238

Orders and Shipments of Durable Goods(Percent change from comparable previous period,

seasonally adjusted)

2003 2003

Category Q2 Q3 Q4 Oct. Nov.r Dec.a

Annual rate Monthly rate

Nondefense capital goodsOrders 12.9 17.9 5.0 2.4 -6.0 0.2Aircraft 2140.8 36.1 1.1 31.1 -14.5 13.7Excluding aircraft 3.2 17.1 5.1 1.4 -5.6 -.4

Computers and peripherals 65.1 26.6 0.9 -.8 0.1 2.0Communications equipment -31.2 80.8 -56.2 16.3 -48.5 -21.3All other 1.0 7.6 21.0 -.8 2.4 1.4

Shipments 5.7 16.4 7.4 0.3 0.4 -.2Aircraft 8.6 32.6 -8.5 -9.6 18.8 -13.2Excluding aircraft 5.6 15.6 8.3 0.8 -.4 0.5

Computers and peripherals 35.8 43.5 3.4 4.6 -2.4 -1.3Communications equipment -6.5 35.2 7.9 2.8 -1.3 -1.0All other 2.7 8.4 9.3 -.3 0.2 1.0

Supplementary orders seriesDurable goods -.8 17.1 15.9 3.9 -2.3 -.0

Real adjusted durable goods -1.6 17.8 3.1 -2.4

Capital goods 10.8 14.9 9.7 4.7 -5.3 0.2Nondefense 12.9 17.9 5.0 2.4 -6.0 0.2Defense -2.1 -3.8 47.2 23.2 -1.3 0.1

r Revised.a Advance.* Contains industry detail not shown separately.

January 27-28, 2004 216 of 238

Appendix 5: Materials used by Messrs. Slifman, Struckmeyer and Kamin

January 27-28, 2004 217 of 238

STRICTLY CONFIDENTIAL (FR) CLASS I-FOMC*

Material for

Staff Presentation on the Economic Outlook

January 28, 2004

*Downgraded to Class II upon release of the February 2004 Monetary Policy Report.

January 27-28, 2004 218 of 238

January 27-28, 2004 219 of 238

January 27-28, 2004 220 of 238

January 27-28, 2004 221 of 238

January 27-28, 2004 222 of 238

Chart 5

Financial Developments

2002 200375

85

95

105

115

*Trade-weighted average of exchange rates against major currenciesand currencies of other important trading partners.

Broad*

Major currencies

Other important trading partners

June FOMCWeekly

Nominal Dollar IndexesIndex, Jan. 4, 2002=100

2002 200360

70

80

90

100

110

120

130

*Foreign currency/dollar.

Euro area

Japan

Mexico

Korea

UK

June FOMCWeekly

Dollar Exchange Rates*Index, Jan. 4, 2002=100

2002 20030

2

4

6

United States Germany

Japan

UK

June FOMCWeekly

Ten-Year Government Bond YieldsPercent

2002 200340

60

80

100

120

140

*Source: MSCI.

Industrial countries

Emerging markets

June FOMCWeekly

Stock Price Indexes*Index, Jan. 4, 2002=100

2002 2003300

600

900

1200

50

100

150

200

250

300

350

*Corporate over government debt.

US BBB*

Euro-area BBB*

EMBI+

June FOMCWeekly

Bond Spreads Basis points Basis points

15

25

35

45

55

65

75

300

400

500

600

700

800

900Industrial countries

Emerging markets

*Source: Dealogic(Bondware, Loanware).

Quarterly

Cross-border Debt Issuance* Billions of dollars Billions of dollars

1997 1999 2001 2003

January 27-28, 2004 223 of 238

Chart 6

Foreign Outlook

2001 2002 200395

96

97

98

99

100

101

102

280

300

320

340

360

380

400

*United States and 32 trading partners. IP weighted by 2002 GDPin dollars. Hong Kong and Indonesia IP through September.

Exports

IP

OctMonthly

Global Trade and IP* Index, Jan. 2001=100 Billions of dollars

2001 2002 2003 2004 200580

90

100

110

120

130

16

20

24

28

32

36

40

*IMF component indexes weighted by U.S. import shares.

WTI spot

Non-fuel commodities*

Monthly

Oil and Non-fuel Commodity Prices Index, Jan. 2001=100 Dollars per barrel

2001 2002 2003 2004 2005-1

0

1

2

3

4

5

6

7

8

*Aggregates weighted by shares in U.S. non-oil imports.

Industrial

Latin America

Asia

Quarterly

Consumer Price Inflation*Four-quarter percent change

2001 2002 200396

97

98

99

100

101

85

88

91

94

97

100

103

*3-month moving average.

Euro area IP*

German Ifo

Jan

Nov

Monthly

Euro Area - Industrial Sector Indicators Index, Jan. 2001=100 Index, Jan. 2001=100

2001 2002 20034.6

4.8

5.0

5.2

5.4

5.6

75

80

85

90

95

100

105

Core machinery orders

Unemployment rate Nov

Monthly

Japan Percent Index, Jan. 2001=100

Real GDP Growth: Industrial CountriesPercent, SAAR*

*Years are Q4/Q4; half years are Q2/Q4 or Q4/Q2.**Aggregates weighted by shares of U.S. exports.

2003 H1 H2

1. Total foreign** 0.6 3.9 3.8 3.5

2. Indust. countries 0.7 2.4 2.9 2.8

of which:

3. Euro Area -0.2 1.8 2.4 2.2

4. Japan 2.0 2.4 2.0 1.8

5. Canada 0.6 2.4 3.4 3.3

6. United Kingdom 1.5 3.4 3.0 2.5

2004 2005

January 27-28, 2004 224 of 238

Chart 7

Emerging Market Countries

1999 2000 2001 2002 20030

10

20

30

40

100

110

120

130

140

*Weighted by U.S. exports; includes Malaysia, Philippines, Singapore, South Korea, Taiwan, and Thailand.

Total semiconductor shipments

Asian IP*

Oct

Nov

Monthly

Worldwide Semiconductor Shipments and Asian IP Billions of chips Index, June 1996=100

1999 2000 2001 2002 2003-12

-6

0

6

12

18

24

30

36

-3.0

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

9.0

CPI inflation

Trade balance

China Billions of dollars Four-quarter percent change

1999 2000 2001 2002 200370

90

110

130

150

170

190

210

*Includes Hong Kong, Korea, Malaysia, Philippines, Singapore,Taiwan, and Thailand. **2003:Q4 data through November forChina and US and through October for EU.

to China

to U.S.

to EU

Quarterly**

Exports by Developing Asia ex. China*Billions of dollars, AR

2000 2001 2002 20030

50

100

150

200

250

300

350

400

450

500

550

*2003:Q4 data through October and November.**Includes Hong Kong, Indonesia, Korea, Malaysia, Philippines,Singapore, Taiwan, and Thailand.

Japan

Developing Asia ex. China**

China

TOTAL

Quarterly*

U.S. Imports from AsiaBillions of dollars, AR

2000 2001 2002 200312.0

12.5

13.0

13.5

14.0

14.5

15.0

95

97

99

101

103

105

U.S. IPMexican IP

Mexican exports

Dec

Nov

Nov

Monthly

Mexico Billions of dollars Index, Jan. 2000=100

Real GDP GrowthPercent, SAAR*

*Years are Q4/Q4; half years are Q2/Q4 or Q4/Q2.**Aggregates weighted by U.S. exports.

2003 H1 H2

1. Total developing** 0.5 6.1 5.1 4.62. Developing Asia -0.6 11.0 5.7 5.4 of which:3. China 6.3 13.6 8.3 7.74. Korea -2.2 4.8 5.2 5.2

5. Latin America 0.9 2.0 4.8 4.0 of which:6. Mexico 1.6 1.0 5.2 4.27. Brazil -4.0 2.8 3.5 3.5

2004 2005

January 27-28, 2004 225 of 238

Chart 8

U.S. External Outlook

2002 2003 2004 2005-5

0

5

10

15

*Years are Q4/Q4; half years are Q2/Q4 or Q4/Q2.

ExportsImports

Real Exports and ImportsPercent change, SAAR*

2002 2003 2004 20050

1

2

3

4

5

6

7

*Years are Q4/Q4; half years are Q2/Q4 or Q4/Q2.**U.S. export weights.

U.S.Total foreign**

Real GDPPercent change, SAAR*

2002 2003 2004 200585

90

95

100

105

Jan. 2004 Greenbook

June 2003 Greenbook

Broad index

Real Exchange Rate OutlookIndex, 2001:Q1 = 100

1996 1998 2000 2002 2004-7

-5

-3

-1

1

-700

-500

-300

-100

100Quarterly

Level

Percent of GDP

Current Account Percent Billions of dollars

*October and November.

2002 2003:H1 2003:Q3 2003:Q4*

1. Current account -481 -556 -540 NA

2. Official capital, net 88 194 170 247

3. Private capital, net 440 387 323 NA Of which: 4. Foreign purchases of U.S. securities 408 418 246 309 5. U.S. purchases of foreign securities 16 -37 -116 -62 6. Foreign DI in U.S. 40 114 33 NA 7. U.S. DI abroad -138 -129 -150 NA

Financial Flows Billions of Dollars, SAAR

January 27-28, 2004 226 of 238

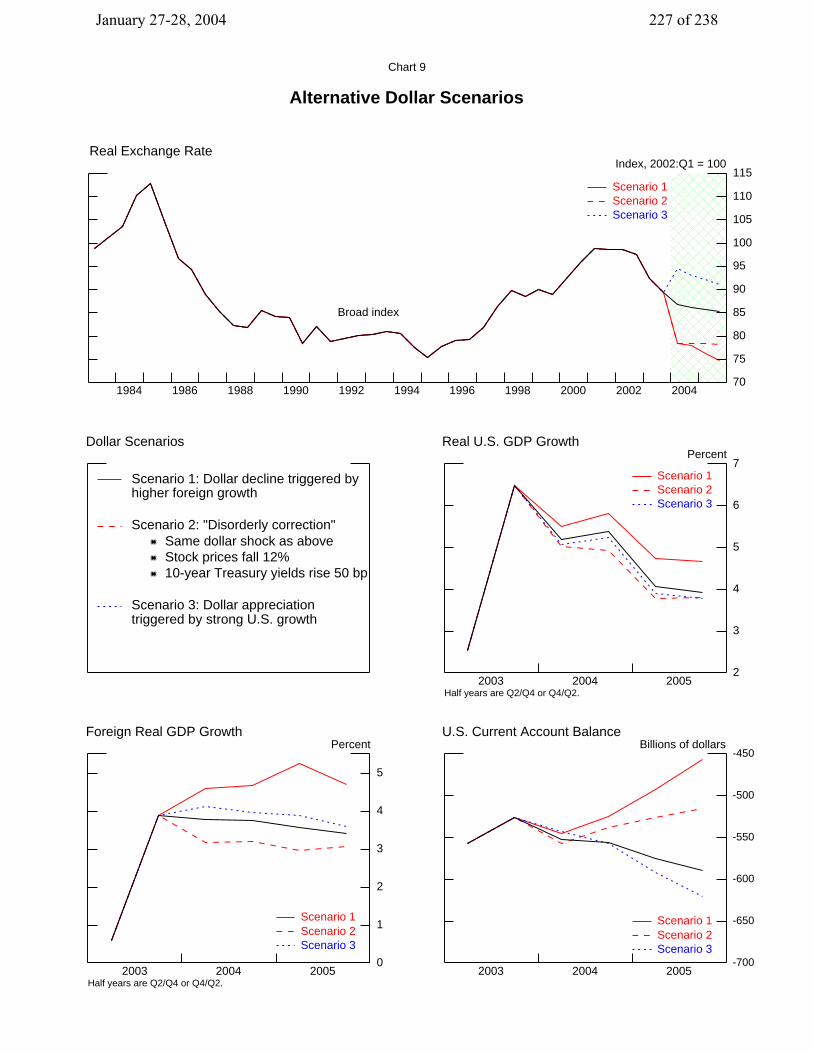

Chart 9

Alternative Dollar Scenarios

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 200470

75

80

85

90

95

100

105

110

115

Broad index

Scenario 1Scenario 2Scenario 3

Real Exchange RateIndex, 2002:Q1 = 100

Scenario 1: Dollar decline triggered by higher foreign growth

Scenario 2: "Disorderly correction"Same dollar shock as aboveStock prices fall 12%10-year Treasury yields rise 50 bp

Scenario 3: Dollar appreciation triggered by strong U.S. growth

Dollar Scenarios

2003 2004 20052

3

4

5

6

7

Half years are Q2/Q4 or Q4/Q2.

Scenario 1Scenario 2Scenario 3

Real U.S. GDP GrowthPercent

2003 2004 20050

1

2

3

4

5

Half years are Q2/Q4 or Q4/Q2.

Scenario 1Scenario 2Scenario 3

Foreign Real GDP GrowthPercent

2003 2004 2005-700

-650

-600

-550

-500

-450

Scenario 1Scenario 2Scenario 3

U.S. Current Account BalanceBillions of dollars

January 27-28, 2004 227 of 238

January 27-28, 2004 228 of 238

January 27-28, 2004 229 of 238

January 27-28, 2004 230 of 238

January 27-28, 2004 231 of 238

Chart 14

ECONOMIC PROJECTIONS FOR 2004

FOMC

Range CentralTendency

Staff

-------------Percentage change, Q4 to Q4------------

Nominal GDP (June 2003)

Real GDP (June 2003)

PCE Prices (June 2003)

5½ to 6½ (4¾ to 6½)

4 to 5½(3½ to 5¼)

1 to1½ (¾ to 2)

5½ to 6¼(5¼ to 6¼)

4½ to 5(3¾ to 4¾)

1 to 1¼(1 to 1½)

6.2

5.3

1.0

--------------Average level, Q4, percent---------------

Unemployment rate (June 2003)

5¼ to 5½(5½ to 6¼)

5¼ to 5½(5½ to 6)

5.3

Central tendencies calculated by dropping high and low three from ranges.

January 27-28, 2004 232 of 238

Appendix 6: Materials used by Mr. Reinhart

January 27-28, 2004 233 of 238

Material forBriefing on Monetary Policy AlternativesJanuary 28, 2004

STRICTLY CONFIDENTIAL (FR)CLASS I FOMC

January 27-28, 2004 234 of 238

Exhibit 1

Expected Federal Funds Rates*

--------- December 8, 2003January 27, 2004

Percent

11 I III1111 IIIIItII I I1111 11

Jan. May Sept. Jan. May Sept. Jan.2004 2005 2006

*Estimates from federal funds and eurodollar futures, with anallowance for term premia and other adjustments.

Implied Distribution of Federal Funds RateAbout 6 Months Ahead* Percent

January 27, 2004

I -- )I

December 8, 2003

I l

IL-t0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.25

*Based on the distribution of the three-month eurodollar rate fivemonths ahead (adjusted for a risk premium), as implied by optionson eurodollar futures contracts.

Desk Dealer Survey - FOMC Statement

Probability Distribution of Time to the Beginning ofTightening Percent

--------- December 8, 2003January 27, 2004

5 10 15

Months Ahead

Desk Dealer Survey - Onset of TighteningNumber of Dealers

2004 H2 2005 H12004 Q1 2004 02

Private Sector Forecasts

Output Risk

Inflation Risk

Overall Risk

Considerable Period

21 Balanced1 Upside

18 Balanced4 Downside

20 Balanced or None2 Unwelcome Disinflation

17 Retained5 Removed

GDP Growth

Greenbook

Inflation (Core PCE)

Greenbook

Unemployment

Greenbook

2004

H1 H2

4.5 4.0

5.4 5.1

1.1 1.4

1.2 1.1

5.8 5.7

5.9 5.4

2005

3.7

3.8

1.7

1.1

5.4

5.1

January 27-28, 2004 235 of 238

Exhibit 2

TIIS Yield Curve Percent

1 3 5 7 10 20 30

Maturity in Years

Implied One-Year Real Forward Rate

1999 2000 2001 2002 2003

The Case for Easier Policy

* Business confidence may remainimpaired.

* Inflation is low and poised to golower.

The Case for Firmer Policy

* Considerable financial accomodationis in place.

* Inflation pressures may emerge morequickly than in the staff forecast.

Selected Money and Credit AggregatesChange in Selected Financial Market ConditionsSince Last FOMC

M2

Bank Credit

Business Loans

2003 2004

H1 Q3 Q4 Jan.

7.7 7.0 -1.8 -1.5

-9.7 4.6 -0.5 2.2

-6.4 -13.9 -9.7 -7.4

Ten-Year Treasury

A Corporate

Wilshire

Major Currency Index

Percent

Basis Points

-20

-22

Percent

7.2

January 27-28, 2004 236 of 238

Exhibit 3Alternative Strategies for Removing Policy Accomodation

Case for Keeping Policy on Hold

* Long-term inflation expectations seemwell-anchored.

* Simulations suggest that policy can remainon hold for an extended period withoutfueling strong inflation pressures.

Inflation Expectations

Percent

- Michigan Survey 10-year expected inflation -

TIS-based inflation compensationfrom 5 to 10 years ahead .

1999 2000 2001 2002 2003

Nominal Federal Funds Rate

Percent6

Long-run inflation:1% 51/2% ..... ...11/2% 4

-- * 2

- 0

2002 2003 2004 2005 2006 2007 2008 2009 2010 -2002 2003 2004 2005 2006 ~2007 200A 2009 2010

Real Federal Funds Rate'

PercentS5

I

-2002 2003 2004 2005 2006 200

2002 2003 2004 2005 2006 2007 2008 2009 2010

Civilian Unemployment Rate

Percent- 6.5

6

5

5------C---------

- 4

4

2002 2003 2004 2005 2006 2007 2008 2009 2010

PCE Inflation (ex. food and energy)(Four-quarter percent change)

2002 2003 2004 2005 2006 2007 2008 2009 2010

1. The real federal funds rate is calculated as the quarterly average nominal funds rate minus the four-quarter lagged core PCE inflationrate as a proxy for inflation expectations.

Percent

January 27-28, 2004 237 of 238

Exhibit 4The Considerable Period Sentence

December 2003 FOMC Statement

"With inflation quite low and resource use slack, the Committeebelieves that policy accomodation can be maintained for aconsiderable period."

Considerable Period Options

Retain

* Confident economy willevolve in a benignmanner.

* Or inflation on low sideof desired range.

Drop

* Tightening within nextfew meetings notruled out.

* Costs of having to delaytightening or renegedamaging.

Modify

* Outsized market reactionto dropping.

* "Patience" would implygradual firming.

Potential Alternative

"With inflation quite low and resourse use slack, the Committee believesthat it can be patient in removing its policy accomodation."

January 27-28, 2004 238 of 238

Related Documents