Commercial Banks in Nepal Recent Trends Submitted by: Submitted to:

FMI - Commercial Banks in Nepal

Aug 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Commercial Banks in NepalRecent Trends

Submitted by: Submitted to:

Abhinav Das Shrestha Dr. K.B. Manandhar

Anisha Kharel FMI Faculty

Nikita Acharya Kathmandu College of Management

Nitish Saria

Shristi Ghale

Table of Contents

Acknowledgement

Abstract

Purpose of the study

Current Situation of Commercial Banking

Growth of Commercial Banks in Nepal

BFI’s Status of Assets, Deposits, and Loan Forwards

Consequence of the Mushroom Growth

Causes of the recent liquidity and banking crises

Moving forward: Merger and IPOs

Major Provisions of Merger By-Law

Process of Merger

Institutions that have merged already

Conclusion and Discussion

References

Acknowledgement

We would like to extend our heartfelt gratitude towards our Financial Markets and Institutions

teacher, Dr. K.B. Manandhar, for giving us an opportunity to conduct an in-depth research on the

topic of our term paper Commercial Banks in Nepal – Recent Trends. We are thankful for

providing us with insight on such an important topic that is useful not only for our study but also

for understanding the Nepalese banking sector from various perspectives.

We also thank our Teaching Assistant, Mr. Shiwir Karki, for his support and guidance

throughout the making of this report. Our sincere thanks also go to each member of the group, as

we could not have done it without the consistent support and understanding of each other.

Sincerely,

Abhinav Das Shrestha

Anisha Kharel

Nikita Acharya

Nitish Saria

Shristi Ghale

Abstract

This paper intends to track the recent developments of commercial banks in Nepal. This paper

explains the mushroom growth of Commercial Banks in Nepal. It also covers the mergers of

various Commercial Banks in Nepal. The developments for the BFIs in Nepal since 2006 is

worthy of a good look and analysis. The BFI situation of the nation has taken a complete turn in

these past seven to eight years, and this paper intends to identify the basic causes behind it,

which ultimately brings us to the currently prevailing situation of the sector.

Introduction

Commercial banks have been achieving several recent developments worthy of noting and in fact

worthy of studying. From the mushroom growth of these institutions beginning in the year 2006,

to the competition it faced, and finally the recent merger trends are all worthy of studying. This

paper as a whole brings together facts and data, and interprets them to give a wholesome picture

of the current situation of commercial banks in Nepal.

The correct chronological order of Banking System in Nepal is quite difficult to trace

considering the lack of proper historical records and data about it. However, Nepal bank Ltd. is

the first modern bank of Nepal. Nepal bank, which marks the beginning of the banking era in

Nepal was established in 1937 A.D. Nepal Bank was established as a semi government bank

with the authorized capital of Rs.10 million and the paid -up capital of Rs. 892 thousand. Until

mid-1940s, only metallic coins were used as medium of exchange. So the Nepal Government

(His Majesty Government on that time) felt the need of separate institution or body to issue

national currencies and promote financial organization in the country.

Nepal Bank Ltd. remained the only financial institution of the country until the foundation of

Nepal Rastra Bank is 1956 A.D. Due to the absence of the central bank, Nepal Bank has to play

the role of central bank and operate the function of central bank. Hence, the Nepal Rastra Bank

Act 1955 was formulated, which was approved by Nepal Government accordingly, the Nepal

Rastra Bank was established in 1956 A.D. as the central bank of Nepal. Nepal Rastra Bank

makes various guidelines for the banking sector of the country.

A sound banking system is important for smooth development of banking system. It can play a

key role in the economy. It gathers savings from all over the country and provides liquidity for

industry and trade. In 1957 A.D. Industrial Development Bank was established to promote the

industrialization in Nepal, which was later converted into Nepal Industrial Development

Corporation (NIDC) in 1959 A.D.

Rastriya Banijya Bank was established in 1965 A.D. as the second commercial bank of Nepal.

The financial shapes for these two commercial banks have a tremendous impact on the economy.

That is the reason why these banks still exist in spite of their bad position.

As the agriculture is the basic occupation of major Nepalese, the development of this sector plays

in the prime role in the economy. So, separate Agricultural Development Bank was established

in 1968 A.D. This is the first institution in agricultural financing. For more than two decades, no

more banks have been established in the country. After declaring free economy and privatization

policy, the government of Nepal encouraged the foreign banks for joint venture in Nepal.

Today, the banking sector is more liberalized and modernized and systematic managed. There

are various types of bank working in modern banking system in Nepal. It includes central,

development, commercial, financial, co-operative and Micro Credit (Grameen) banks.

Technology is changing day by day. And changed technology affects the traditional method of

the service of bank. Banking software, ATM, E-banking, Mobile Banking, Debit Card, Credit

Card, Prepaid Card etc. services are available in banking system in Nepal. It helps both customer

and banks to operate and conduct activities more efficiently and effectively. For the development

of banking system in Nepal, NRB refresh and change in financial sector policies, regulations and

institutional developments in 1980 A.D. Government emphasized the role of the private sector

for the investment in the financial sector. These policies opened the doors for foreigners to enter

into banking sector in Nepal under joint venture.

Some foreign ventures are also established in Nepal such as Nepal Bangladesh Bank, Standard

Chartered Bank, Nepal Arab Bank, State Bank of India, ICICI Bank, Everest Bank, Himalayan

Bank, Bank of Kathmandu, Nepal Indo-Suez Bank and Nepal Sri Lanka Merchant Bank etc. The

NRB will classify the institutions into “A” “B” “C” “D” groups on the basis of the minimum

paid-up capital and provide the suitable license to the bank or financial institution. Group ‘A’ is

for commercial bank, ‘B’ for the development bank, ‘C’ for the financial institution and ‘D’ for

the Micro Finance Development Banks.

There are 32 commercial banks, 79 development banks, 79 financial companies, 18 micro credit

development banks and 16 saving and credit co-operation are established so far in Nepal. The

bank with the largest network in Nepal is The Nepal Bank Ltd. These commercial banks and

financial institutions have played significant roles in creating banking habit among the people,

widening area and business communities and the government in various ways.

Purpose of the study

A term paper is a research paper conducted by students on a particular subject matter for the

purpose of integrating what we have learned in the class. This term paper has been completed

with similar purpose of applying theoretical knowledge about the recent trends of commercial

bank. To fulfill our purpose we did detail study of establishment, growth, mergers, and

increasing competition of commercial bank. Also the various development that has increased in

this sector.

Current Situation of Commercial Banking

Nepal has been struggling to maintain macroeconomic balance for a couple of years now. Low

growth rate, high unemployment, balance of payments deficit, ballooning trade deficit, and high

and sticky inflation are some of the pressing existing macroeconomic challenges. Now, add to

that list banking and liquidity crises—engendered largely by the bank and financial institutions

(BFIs) themselves and to some extent by Nepal Rastra Bank (NRB), the central bank—and its

disastrous consequences in and beyond the banking system.

The NRB ignored the unhealthy competition, questionable lending to few sectors, and

governance in financial sector. In doing so it let new BFIs pop up without even evaluating if the

economy needs so many of them, and took damage control measures of late. Meanwhile, the

BFIs engaged in unhealthy and imprudent lending out of desperation to survive amidst cutthroat

competition, which is getting nasty by the day. The BFIs’ inability to effectively cope with the

pressure to increase deposit and lending, and to attain unsustainable profit targets is leading to a

situation where all profits are private but losses are social, i.e. taxpayers pay the cost of reckless

business practices of the BFIs in the form of expensive rescue packages.

The tendency to seek short term, quick returns against long term viability and sustainability is

leading the BFIs in a path of self-destruction. For a healthy banking industry, Nepal needs fewer

but stronger BFIs with sound corporate governance. Furthermore, there has to be an

enhancement of regulatory and supervisory capabilities of NRB. The playing field has gotten

unnecessarily congested amidst less than proportionate growth rate in the number of depositors.

When Vibor Bikas Bank (VBB) knocked on the doors of Nepal Rastra Bank (NRB) on June 9,

2011 to either inject money in the development bank or to take over management, it rattled the

banking industry and the already suspicious depositors. There were rumors and anticipation that

due to excessive loan exposure to real estate, housing and construction sectors bank and financial

institutions will land in a danger zone sooner or later.

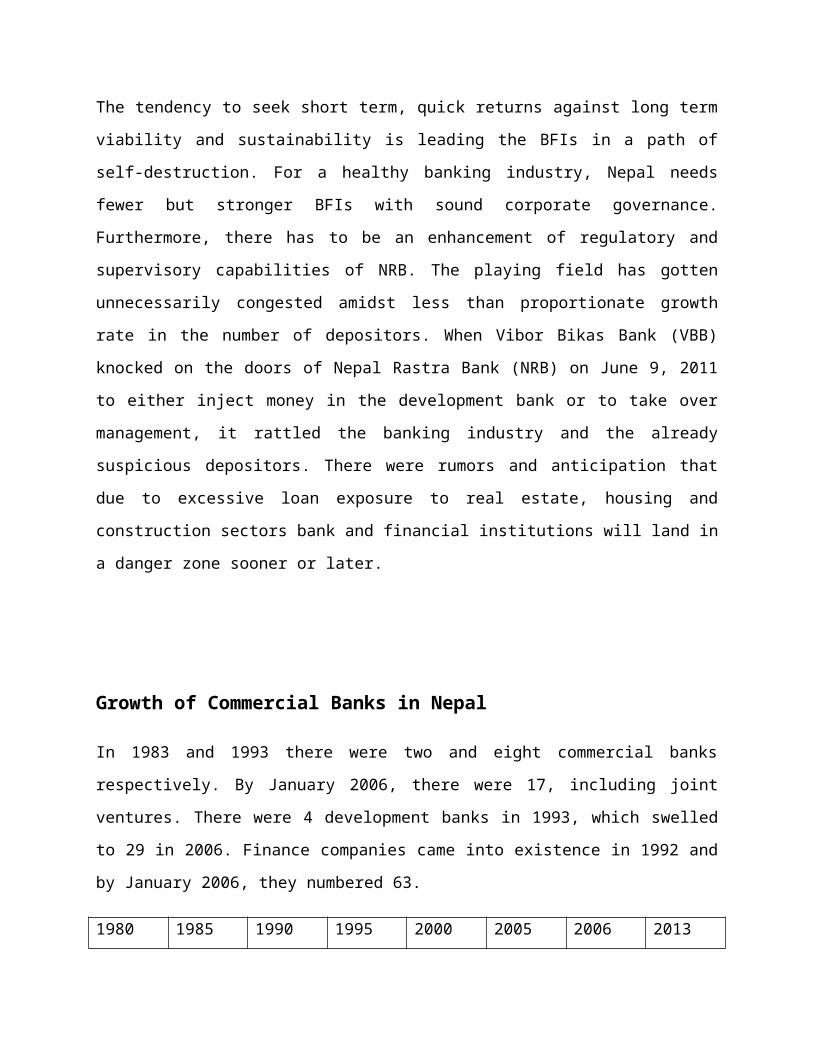

Growth of Commercial Banks in Nepal

In 1983 and 1993 there were two and eight commercial banks respectively. By January 2006,

there were 17, including joint ventures. There were 4 development banks in 1993, which swelled

to 29 in 2006. Finance companies came into existence in 1992 and by January 2006, they

numbered 63.

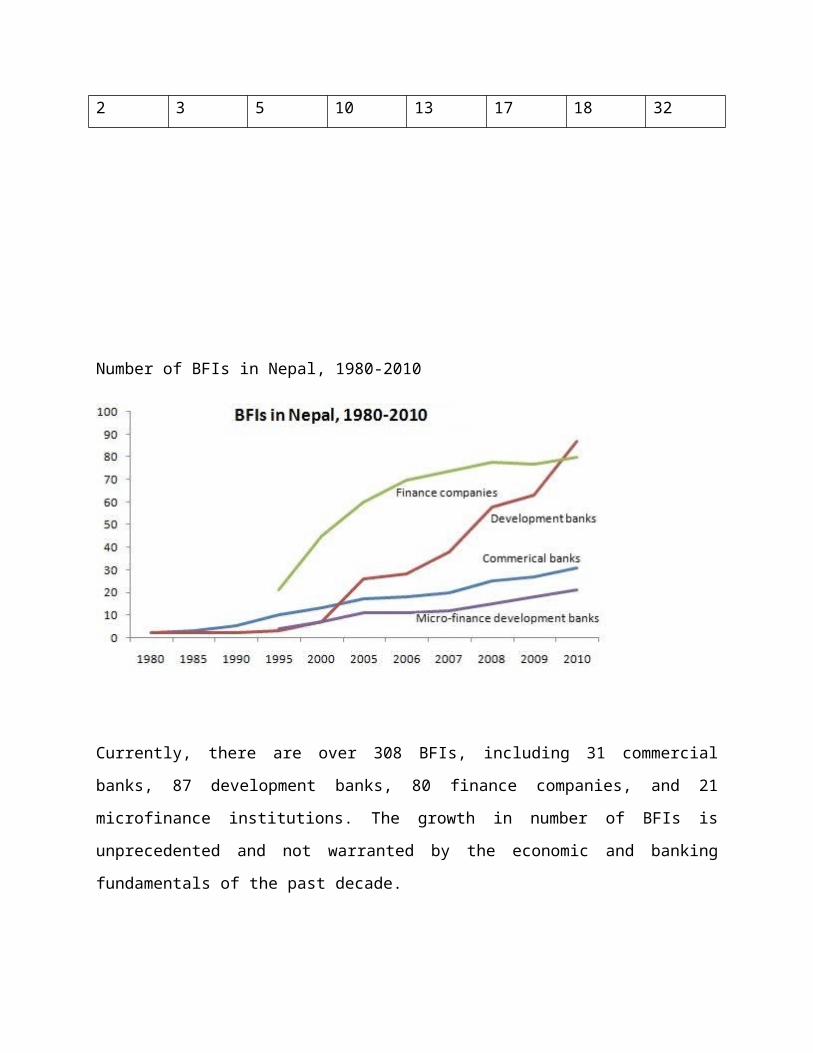

1980 1985 1990 1995 2000 2005 2006 2013

2 3 5 10 13 17 18 32

Number of BFIs in Nepal, 1980-2010

Currently, there are over 308 BFIs, including 31 commercial banks, 87 development banks, 80

finance companies, and 21 microfinance institutions. The growth in number of BFIs is

unprecedented and not warranted by the economic and banking fundamentals of the past decade.

BFI’s Status of Assets, Deposits, and Loan Forwards

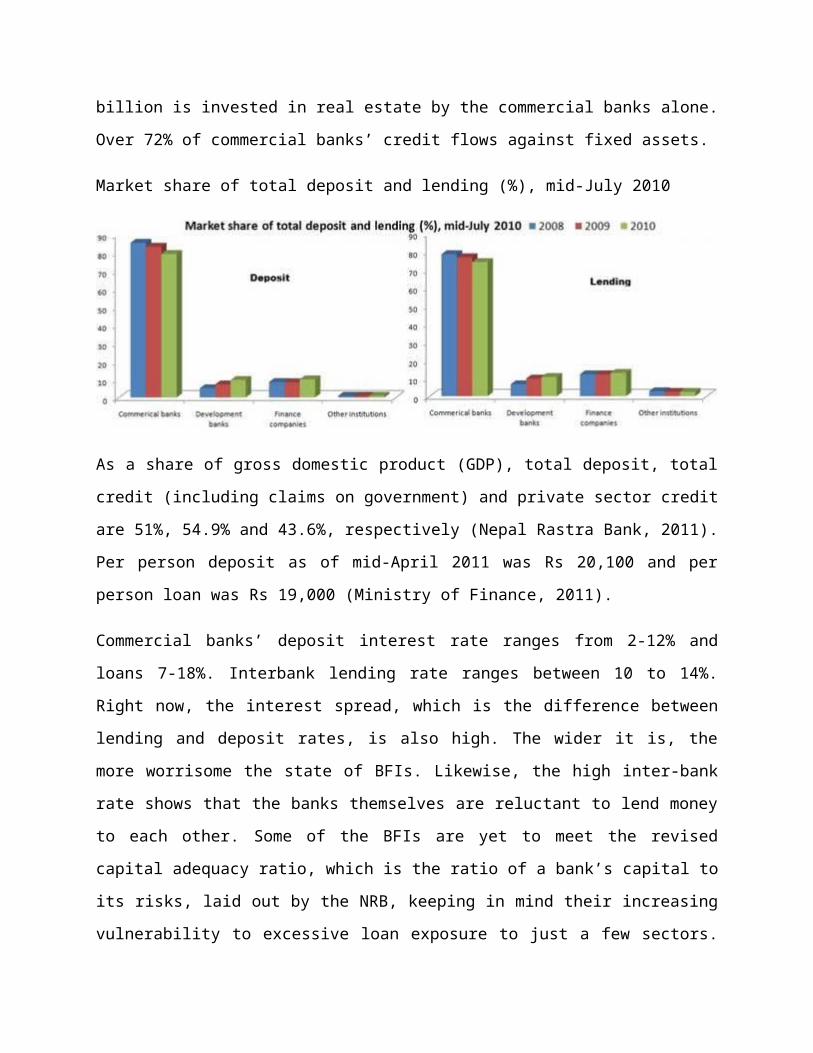

As of mid-July 2010, total assets and total deposits in banking sector amounted Rs 996.1 billion

and Rs 795.3 billion respectively. The total loans amounted to Rs 622.6 billion. The market share

of total deposits of commercial banks has declined from 85.6% in mid-July 2008 to 79.4% in

mid-July 2010, when the share of development banks, finance companies, and other BFIs was

9.7%, 10% and 0.9% respectively (Ministry of Finance, 2011). In the last three years, there has

been a slight decrease in deposits in commercial bank but increase in development banks and

finance companies (see Figure 2).

Meanwhile, of the total loans, commercial bank’s market share has declined from 78.6% in mid-

July 2008 to 74.2% in mid-July 2010. During the same period, the share of total loans of

development banks, finance companies and other BFIs was 10.6%, 12.8% and 2.4% respectively.

As of April 2011, NRB data shows that the total deposits at commercial banks stand at around Rs

642 billion. Of the total commercial banks’ deposits, demand deposits, savings deposits, and

fixed deposits stand at 12%, 36%, and 52% respectively. They have liquid funds of Rs 114

billion (cash in hand Rs 16.2 billion, and deposits with NRB Rs 39.3 billion). More than Rs 110

billion is invested in real estate by the commercial banks alone. Over 72% of commercial banks’

credit flows against fixed assets.

Market share of total deposit and lending (%), mid-July 2010

As a share of gross domestic product (GDP), total deposit, total credit (including claims on

government) and private sector credit are 51%, 54.9% and 43.6%, respectively (Nepal Rastra

Bank, 2011). Per person deposit as of mid-April 2011 was Rs 20,100 and per person loan was Rs

19,000 (Ministry of Finance, 2011).

Commercial banks’ deposit interest rate ranges from 2-12% and loans 7-18%. Interbank lending

rate ranges between 10 to 14%. Right now, the interest spread, which is the difference between

lending and deposit rates, is also high. The wider it is, the more worrisome the state of BFIs.

Likewise, the high inter-bank rate shows that the banks themselves are reluctant to lend money to

each other. Some of the BFIs are yet to meet the revised capital adequacy ratio, which is the ratio

of a bank’s capital to its risks, laid out by the NRB, keeping in mind their increasing

vulnerability to excessive loan exposure to just a few sectors. (Nepal Rastra Bank).

Consequence of the Mushroom Growth

By overlooking the need for having a limited number of BFIs, the evolving depositor base, and

financial penetration over the years, the NRB let too many BFIs to pop up. It created a BFI

bubble. This was followed by intense competition of not only between banks in the same

category but also between BFIs in different categories, leading to an informal war in offering

high deposit rates and lending without differentiating markets, products, and borrowers’

creditworthiness. It reflected bad corporate governance, and a lack of innovation and R&D in the

sector. The resulting lending surge in real estate and housing markets unnaturally swelled their

prices, leading to a real estate and housing bubble.

Causes of the recent liquidity and banking crises

Below we list out the points worthy enough of being labeled as a cause for the recent banking

and liquidity crisis. There have been misleading and incongruous arguments floating around

about the causes of the ongoing liquidity and banking crisis. They are made by stakeholders who

fail to see how their vested interest and incompetence is jeopardizing the future of the banking

industry, and is potentially derailing an already unstable economy.

First, bankers and businessmen are arguing that delayed budget and disbursement of

development expenditures are causing liquidity crisis. This argument does not hold much

water. It is true that budgets have been coming out late for two years now, and there has

not been normal flow of money from the Ministry of Finance and other Ministries to the

respective corners of the country via BFIs. This has definitely limited liquidity in the

banking system. But it in itself is not the main cause. Instead, it is a minor stimulant to

the liquidity crisis. If delay in development expenditure is the cause, then why did Nepal

not have liquidity crisis when similar episodes occurred in the past?

Second, the withdrawal of large amount of money by institutional depositors, especially

NRB and Nepal Army, has drastically reduced reserves in BFIs’, especially category B

and C, vaults and squeezed available liquidity. This again is a stimulant to the liquidity

problem, not its main cause. If just by pulling out a few millions of mature deposits by

institutional depositors puts the BFIs in trouble, then there is something wrong with the

way they are doing business. It points to bankers’ incompetence and inability to run BFIs.

Third, while some argue that people are either stashing money at home or are investing in

commodities like gold and silver, others assert that the compulsion to divulge source of

income on transactions above Rs 1 million is restricting deposi87YUts. Again, both are

not the real causes, but stimulant to the liquidity crisis. These arguments are trumpeted by

certain businessmen who are afraid of divulging their sources of income and dutifully pay

taxes to the government.

Fourth, some argue that a decline in reserves, precisely monetary base (which is equal to

currency in circulation and reserves of banks held in central bank), due to a slowdown in

growth of remittances, led to a situation where credit growth was higher than deposit

growth. They assert that it is resulting in a liquidity crisis, and to return to normal, the

NRB should purchase bonds and treasury bills and lower cash reserve ratio and the

already high capital requirements (all of which will help increase liquidity). Of all the

arguments, this holds some truth. But increasing liquidity without correcting the distorted

market would only postpone the inevitable.

The main cause is that Nepal has too many BFIs catering to too few customers (note that

a 2006 study on financial penetration shows that only 26 percent of households in Nepal

have bank accounts, meaning that in order to survive and meet ever-increasing profit

targets, the BFIs have to have constant flow of money from all sources, that also in higher

proportion than previous flows. The competition to attract deposits and give out loans

intensified with the increase in the number of BFIs, who competed without much product

and market differentiation. Without considering total deposits and their ability to fulfill

demand for withdrawals, the BFIs lent unsustainable amount of loans to earn quick

returns to meet profit target before the annual general meeting of shareholders and

directors. This translated into real estate and housing sectors bubble, which sucked in as

much as Rs 110 billion of commercial bank’s deposit.

Driven by easy finance and loans, real estate transactions and housing complexes rose rapidly.

Sometimes artificial demand was created just to jack up prices. This is evident from the fact that

our shaky economic fundamentals do not justify multifold increase in land prices in a matter of

days. Moreover, money is pumped into this sector without properly assessing risks and the

ability of borrowers to repay loans. The BFIs are hardly distinguishing between normal and

subnormal loans. There is little product and market differentiation. This was assuaged by NRB’s

easy monetary policy, lax supervision (by near-retiring officials who had expectations of moving

into private sector banking) and inflow of remittances, which is approximately one-fourth of

GDP right now.

This created market disequilibrium, i.e. the supply of real estate and housing complexes

outstripped demand, leading to decline in prices by as much as 30 percent. As prices dipped,

borrowers are and will be unable to honor principal and interest payments on time, forcing the

BFIs to restructure loans and variably increase lending rates. This in turn led to and is leading to

buyers canceling bookings even after paying the minimum required down payment. Soon the

major urban centers will see ‘ghost’ apartments, i.e. empty apartments waiting for customers to

either buy or rent them. This will ultimately hit the BFIs even harder unless it goes fundamental

restructuring and consolidation.

Moving forward: Merger and IPOs

Many financial and economic analysts failed to perceive the rapid changes happening in the

banking sector. Similarly, business journalists utterly failed to even read clues of troubles

starting more than a decade ago when the now liquidated Nepal Development Bank (NDB) was

put under management review, and when the number of BFIs increased multifold in a matter of

just five years.

Financial institutions have mushroomed in the country, thanks to the liberal policies adopted by

Nepal Rastra Bank in the past. Given the size of our financial system, the number of BFIs looks

more than normal. Many of these institutions had invested in the real estate sector without any

long-term benefits. NRB was forced to fix a ceiling on real estate investment by banks after a

surge in the volume of nonperforming loans.Investment by financial institutions in unproductive

sectors caused a liquidity crisis in the market. These institutions also failed to maintain corporate

governance. Financial institutions should be able to return money to depositors as required.

NRB had introduced Merger Bylaws 2011 to improve the condition of financial institutions.

The introduction of merger policy has created opportunities for banks to increase their capital

base. At the same time, the BFIs are also going ahead with Initial Public Offerings (IPOs) to

increase their capital base. The trend of announcing merger plans by the banks and financial

institutions (BFIs) has gathered pace in recent months. According to Nepal Rastra Bank, a total

of 28 banks and financial institutions (BFIs) have already merged with each other reducing the

total number of BFIs by 15. Similarly, some 24 BFIs have already received Letter of Intent (LoI)

to be merged with one other, and upon completion of this process, the total number of BFIs will

reduce by another 14. And, other 12 BFIs have applied for the LoI. Once these too complete the

process, the number of BFIs will be reduced by additional 5.

This shows that in spite of several weaknesses to implement monetary policy, Nepal Rastra Bank

(NRB) has become quite successful in implementing its merger policy. Earlier, the central bank

had announced packages of rebates, discounts, waivers and facilities to the BFIs opting for

mergers. But now, the bankers themselves believe that merger has become compulsory for many

banks which are suffering from the problem of low capital base and limited geographical

coverage. Similarly, a wave of Initial Public Offerings (IPOs) has started among the new BFIs.

In the last Nepali calendar year that ended on mid-April, 20 BFIs issued IPOs, issuing shares

worth Rs 5.6 billion. More offering such IPOs are in the pipeline. Though BFIs can increase their

capital base also through Further Public Offering (FPO) of their shares, very few of them have

opted for this route.

Merger: Why is it needed?

Apparently, the universal objectives of the merger or acquisition are to consolidate the capital,

reduce operational expenses, expand business and maximize profits. However, in our case,

mergers of three distinct natures now seem to be in the offing.

Firstly, relatively large institutions are planning to create a larger capital base so they could

compete with global players who could potentially begin their operations here owing to WTO

arrangements. The second type of merger would be compulsive of sorts as the NRB has asked

the BFIs belonging to the same business house to integrate without any “ifs and buts’’. The third

types are those who fear the complete meltdown if they fail to merge soon to consolidate

resources, introduce corporate best practices and reduce expenses.

As there is no environment for increasing capital by issuing rights shares and bonus shares as

that will not be enough to raise capital to the required level, finance companies have no

other option than to go for a merger. Many finance companies have thought that’s it’s better to

opt for a merger than to face action from the central bank for failing to increase the capital to the

required level next year. Also the shaken public confidence on towards banking institutions due

to recent problems in the banking sector and their inability to give proper returns to their

shareholders, has forced the BFIs to increasingly lean towards consolidation.

Consolidation is necessary also to increase the paid-up capital since the possibility to increase of

paid up capital by issuing rights shares is very slim. Moreover, the size of loans being demanded

by single borrowers has been increasing in recent years. So, BFIs having low paid-up capital

cannot fulfill such demand.

Major Provisions of Merger By-Law

‘A’, ‘B’ and ‘C’ class financial institutions can merge into each other. ‘D’ class FI

can merge with another ‘D’ class FI only.

FIs that want to merge should form a separate merger committee and sign

Memorandum of Understanding (MoU).

The due process including MoU should be completed before applying to the Nepal

Rastra Bank (NRB)for Letter of Intent (LoI). NRB should hold a meeting within 15

days of receiving LoI application.

NRB decides whether to issue LoI or not after conducting discussions and detailed

study of concerned institutions.

Due Diligence Audit should complete within six months of receiving LoI from the

central bank.

The detailed factual report comprising assets and liabilities of concerned institutions

should be submitted to the NRB.

Copy of the decision regarding name, address and share ratio of concerned financial

institutions should be submitted to NRB.

Action plan of concerned financial institution including date of operation after merger

process is completed should be submitted to NRB.

Other documents as prescribed by the NRB should be submitted to NRB.

NRB can ask for merger if the following situation prevails

In case representatives of a family, business group, firm or company are found

assuming posts in the boards of directors of two or more BFIs and/or their financial

conditions remain unhealthy.

If the non-performing loans (NPL) exceeded 5 percent of the total loan portfolio for 3

consecutive years.

Increase in systematic risk (i.e. in a situation when a BFI seems likely to fail to meet

liabilities).

If independent operation of a BFI is causing negative impact on the banking system.

If a BFI faces prompt corrective action (PCA) for three times or more.

If NRB finds that merger of systemically important BFIs will strengthen the entire

banking system.

Process of Merger

Merger is a need of the entire financial system of Nepal. The share swap ratio is obviously an

issue of tension in the pre-merger phase. NRB provides counseling services to all institutions

which want to go for merger. The process is very simple. At first, the BFIs should take the

special decision of merger thorough the General Meeting of shareholders. Then they should sign

a Memorandum of Understanding (MoU) for merger. Then, after forming a merger committee,

they should apply to the central bank for the Letter of Intent. NRB conducts interaction with

concerned stakeholders and provides insights including strengths and weaknesses of the merging

BFIs. If BFIs want to continue the merger process even after the interaction, NRB approves the

LoI. Concerned financial institutions should approve new structure which will come into effect

after the completion of the merger process.

NRB should always deal the entire merger process carefully because merger should not promote

monopolistic business.

Institutions that have merged already

Himchuli Development Bank & Birgunj Finance forming H&B Development Bank Ltd

Narayani Finance & National Finance forming Narayani National Finance

Nepal Bangladesh Bank & Nepal-Sri Lanka Merchant Bank forming Nepal Bangladesh Bank

Ltd

Kasthamandap Development Bank & Shikhar Finance forming Kasthamandap Development

Bank Ltd

Business Development Bank & Universal Finance forming Business Universal Development

Bank Ltd

Machhapuchchhre Bank & Standard Finance forming Machhapuchchhre Bank Ltd

Global Bank & IME Financial Institution & Lord Buddha Finance forming Global IME Bank

Ltd

Infrastructure Development Bank & Swastik Merchant Finance forming Infrastructure

Development Bank Ltd

Annapurna Development Bank & Suryadarshan Finance forming Supreme Development Bank

Ltd

Vibor Bikas Bank & Bhajuratna Finance forming Vibor Bikas Bank Ltd

Alpic Everest Finance & Butwal Finance & CMB Finance forming Synergy Finance Co Ltd

Shine Development Bank & Resunga Development Bank forming Shine Resunga

Development Bank

Pashupati Development Bank & Udyam Development Bank forming Axis Development Bank

Ltd

Prudential Finance & Gorkha Finance forming Prudential Finance Company Ltd

NIC Bank & Bank of Asia forming NIC Asia Bank Ltd (Process ongoing)

Letter of Intent (LoI) Received

Premier Finance & Imperial Finance to form Premier Imperial Finance

Royal Merchant Banking and Finance, Rara Bikas Bank & Api Finance

Araniko Development Bank & Surya Development Bank

Central Finance Ltd & Patan Finance Ltd

Diyalo Bikas Bank Ltd & Professional Bikas Bank Ltd

NDEP Development Bank & Hama Finance Ltd

Siddhatha Development Bank & Public Development Bank Ltd

Five Regional Development Bank to form One National Level Gramin Bikas Bank

Shangrila Development Bank Ltd & Bagheshwor Development Bank

Conclusion and Discussion

Having overlooked at the need or requirement of BFIs in the economy, the increasing depositing

trend and financial penetration that followed has now after several years led to a situation which

should have been predicted by the nations eceonomists and most importantly, it should have

been realized by Nepal Rastra Bank. This was followed by intense competition of not only

between banks in the same category but also between BFIs in different categories, leading to an

informal war in offering high deposit rates and lending without differentiating markets, products,

and borrowers’ creditworthiness. The increased competition and the informal war had led to a

situation of bad corporate governance, lack of Research and Development and innovation. The

result further created a surge in real estate market and created a bubble. The bubble was a result

of banks not considering the long term attractiveness of the real estate market. The current

situation is that of a liquidity crisis, where banks are having a difficult time keeping up in the

intense competition.

The introduction of merger policy has created opportunities for banks to increase their capital

base. At the same time, the BFIs are also going ahead with Initial Public Offerings (IPOs) to

increase their capital base. As there is no environment for increasing capital by issuing rights

shares and bonus shares as that will not be enough to raise capital to the required level, finance

companies have no other option than to go for a merger. Many finance companies have

thought that’s it’s better to opt for a merger than to face action from the central bank for failing

to increase the capital to the required level next year. Also the shaken public confidence on

towards banking institutions due to recent problems in the banking sector and their inability to

give proper returns to their shareholders, has forced the BFIs to increasingly lean towards

consolidation.

References

Siromani Dhungana, Yagya Banjade and Rashesh Vaidya, Nepali Banking in Transition, New

Business Age (2013)

Ministry of Finance. (2011). Economic Survey 2010/11. Kathmandu: Ministry of Finance,

Government of Nepal.

Sharma, M. M. (2011, June 9). Sinking Vibor Bank Seeks Mgmt by NRB. Republica Daily

Website

Monetary Policy 2010-2011. Kathmandu: Nepal Rastra Bank.

Nepal Rastra Bank released journals

Chandan Sapkota, Nepalese Banking Crisis, (Swatee.org)

Related Documents