-1 Chapter 15 Chapter 15 Required Required Returns and Returns and the Cost of the Cost of Capital Capital

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

15-1

Chapter 15Chapter 15Required Required

Returns and Returns and the Cost of the Cost of

CapitalCapital

15-2

Overall Cost of Overall Cost of Capital of the FirmCapital of the Firm

Cost of Capital is the required rate of return on the various types of financing. The overall cost of capital is a weighted average of the individual required rates of return (costs).

15-3

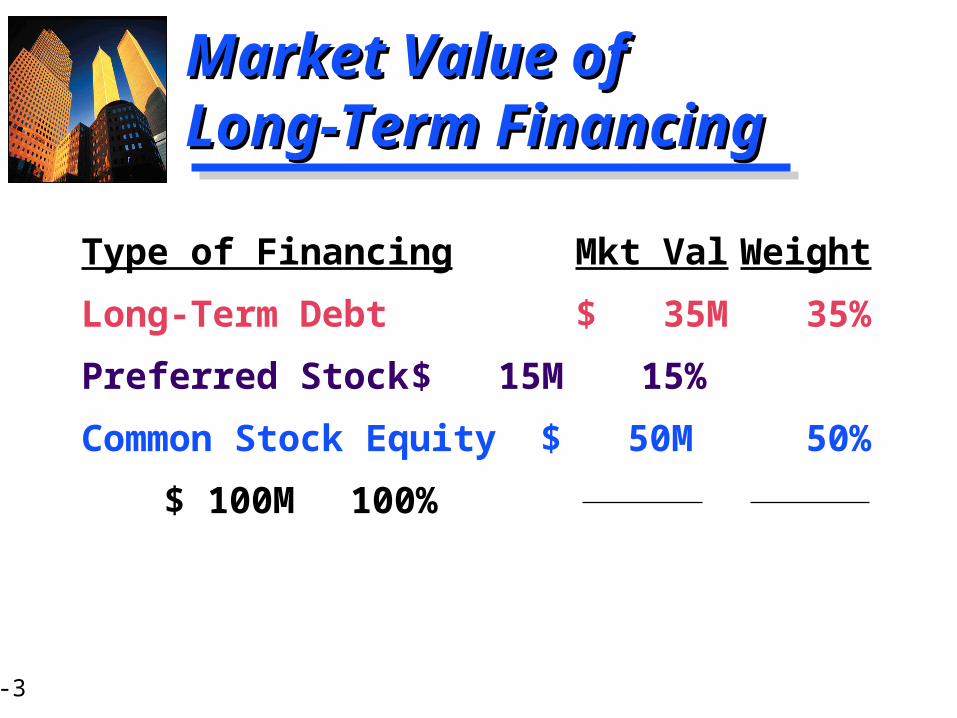

Type of Financing Mkt Val WeightLong-Term Debt $ 35M 35%Preferred Stock$ 15M 15%Common Stock Equity $ 50M 50%

$ 100M 100%

Market Value of Market Value of Long-Term FinancingLong-Term Financing

15-4

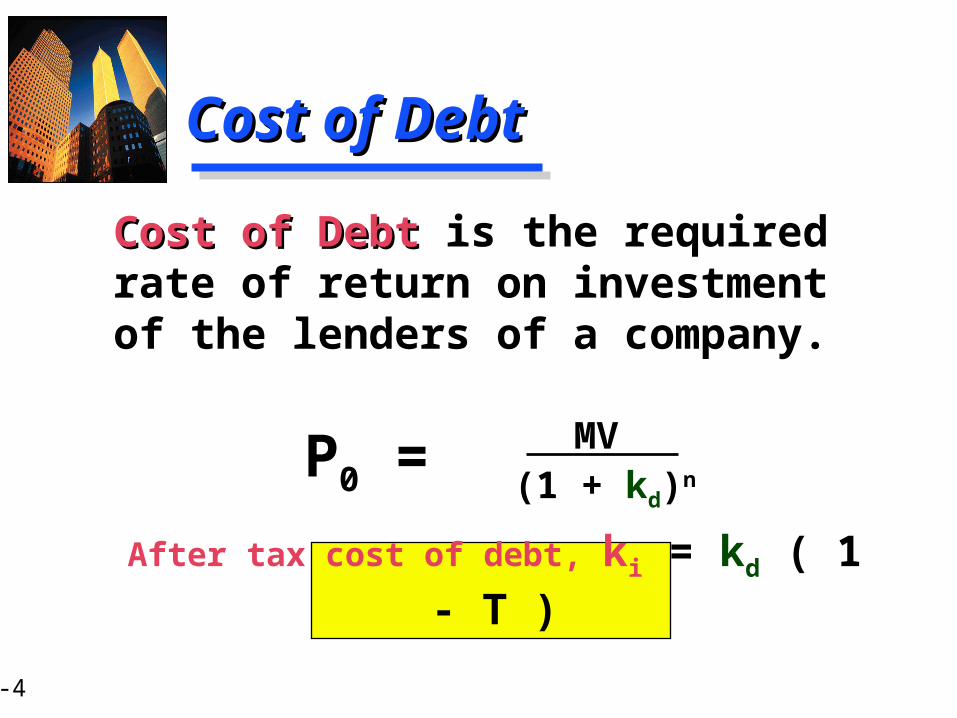

Cost of Debt Cost of Debt is the required rate of return on investment of the lenders of a company.

After tax cost of debt, ki = kd ( 1 - T )

Cost of DebtCost of Debt

P0 = MV(1 + kd)n

15-5

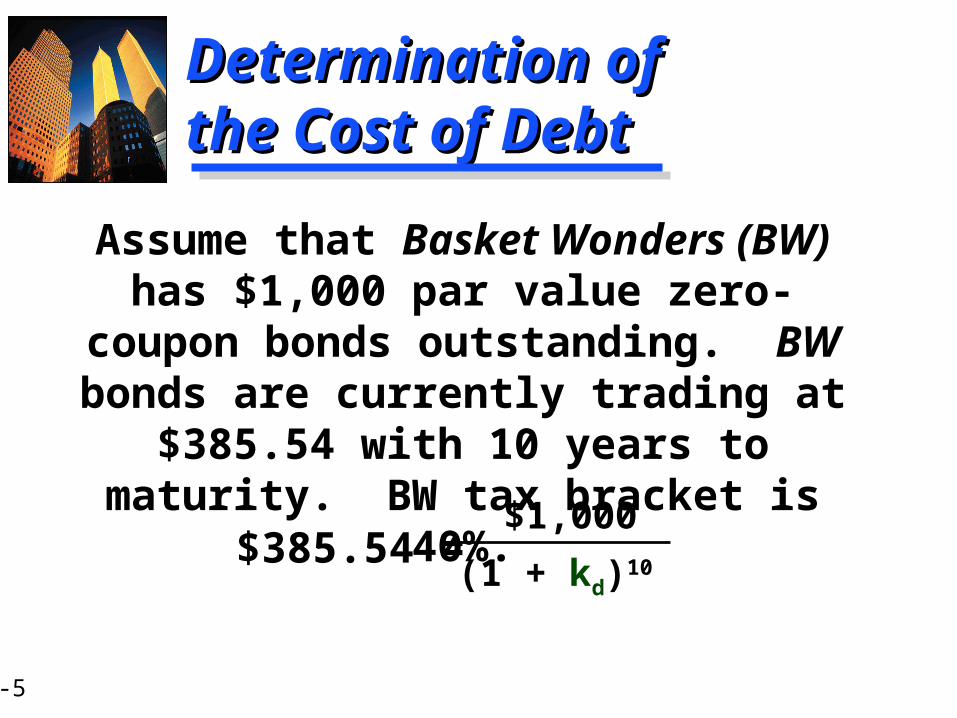

Assume that Basket Wonders (BW) has $1,000 par value zero-

coupon bonds outstanding. BW bonds are currently trading at

$385.54 with 10 years to maturity. BW tax bracket is

40%.

Determination of Determination of the Cost of Debtthe Cost of Debt

$385.54 = $1,000(1 + kd)10

15-6

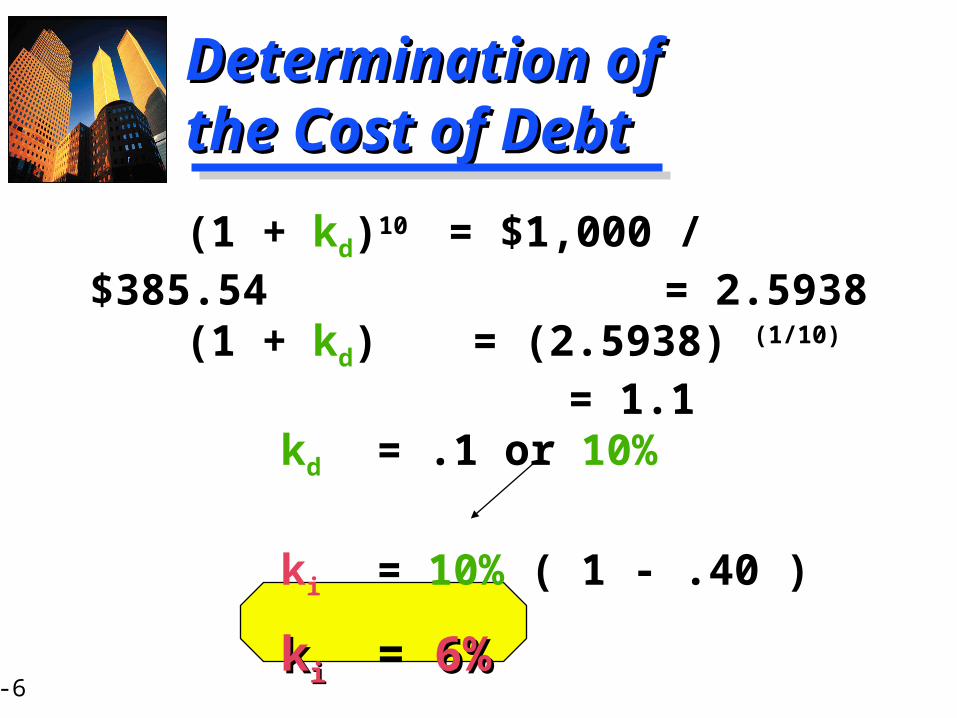

(1 + kd)10 = $1,000 / $385.54 = 2.5938

(1 + kd) = (2.5938) (1/10)

= 1.1 kd = .1 or 10%

ki = 10% ( 1 - .40 )

kkii = 6%6%

Determination of Determination of the Cost of Debtthe Cost of Debt

15-7

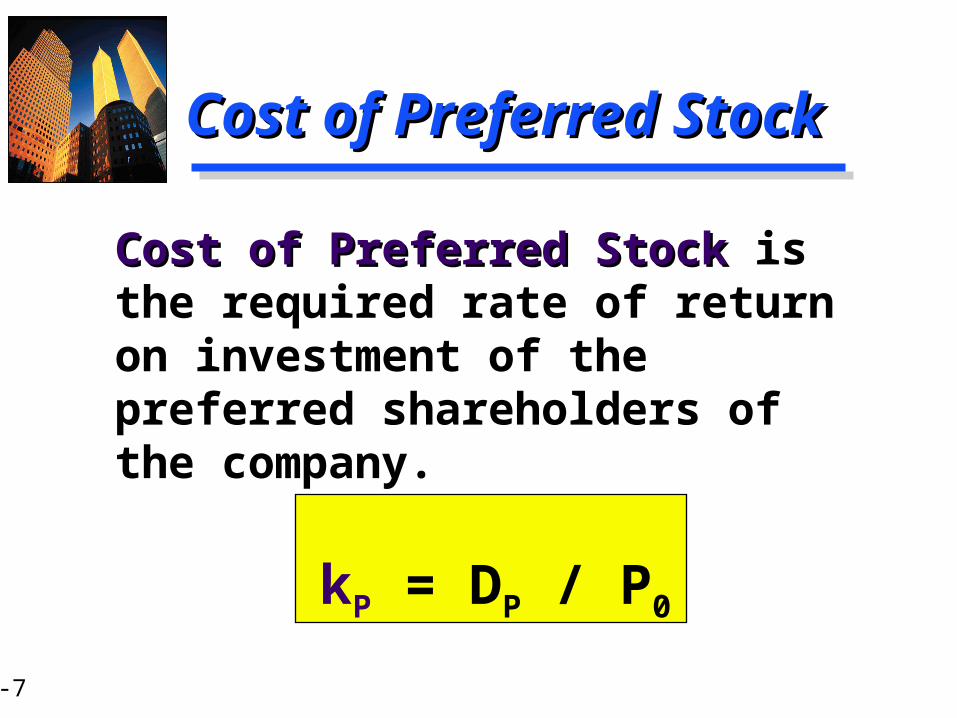

Cost of Preferred Stock Cost of Preferred Stock is the required rate of return on investment of the preferred shareholders of the company.

kP = DP / P0

Cost of Preferred StockCost of Preferred Stock

15-8

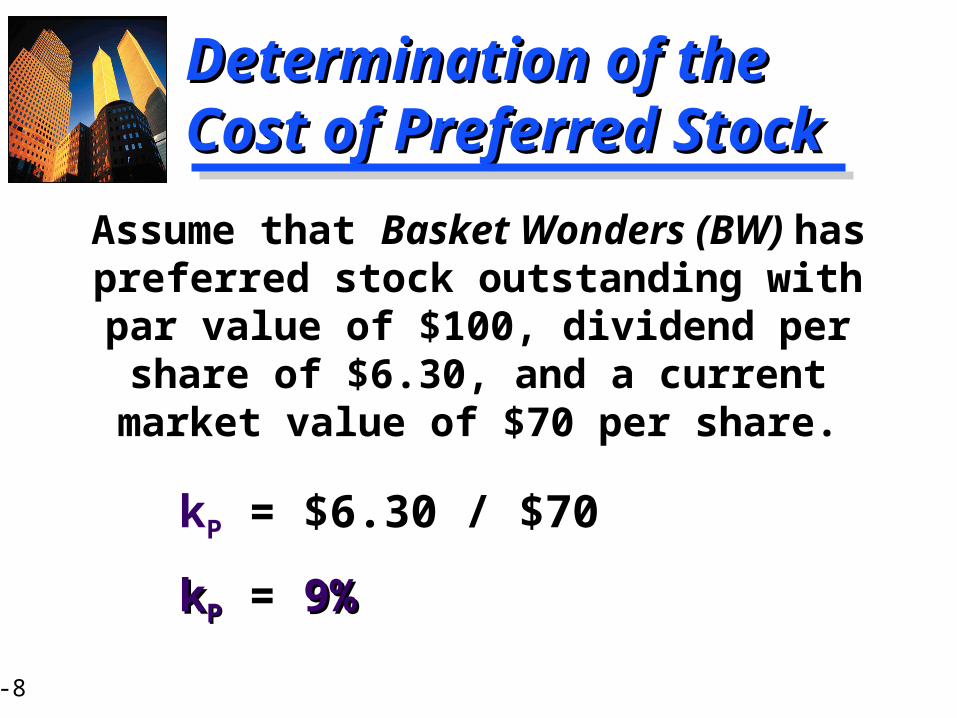

Assume that Basket Wonders (BW) has preferred stock outstanding with par value of $100, dividend per share of $6.30, and a current market value of $70 per share.

kP = $6.30 / $70kkPP = 9%9%

Determination of the Determination of the Cost of Preferred StockCost of Preferred Stock

15-9

Constant Growth ModelConstant Growth Model Capital-Asset Pricing Capital-Asset Pricing

ModelModel Before-Tax Cost of Before-Tax Cost of Debt plus Risk PremiumDebt plus Risk Premium

Cost of Equity Cost of Equity ApproachesApproaches

15-10

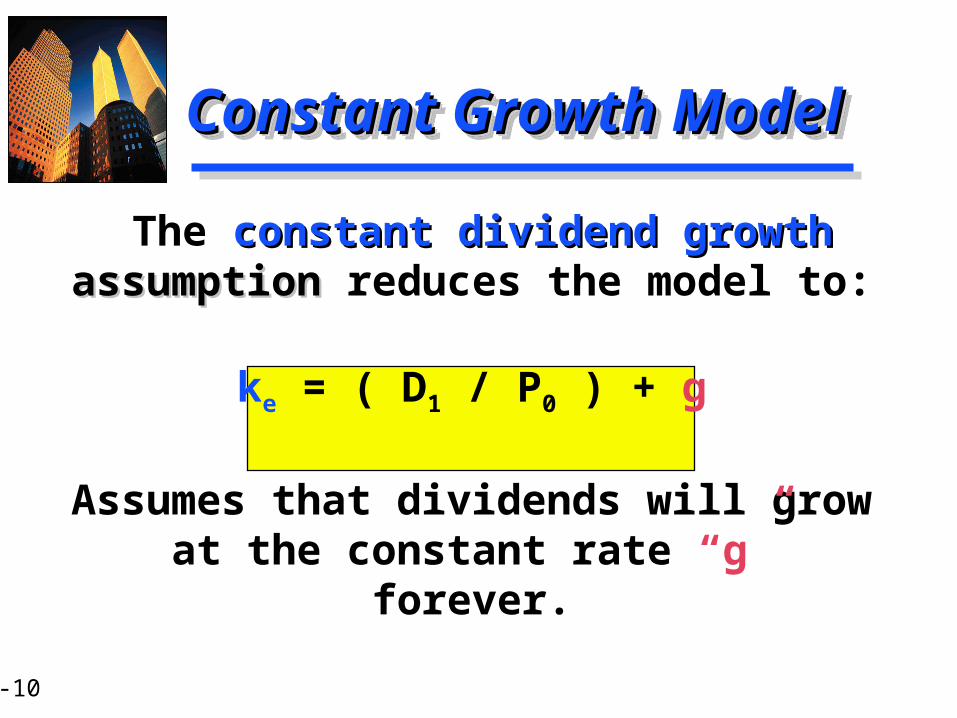

Constant Growth ModelConstant Growth Model

The constant dividend growth constant dividend growth assumptionassumption reduces the model to:

ke = ( D1 / P0 ) + g

Assumes that dividends will grow at the constant rate “g”

forever.

15-11

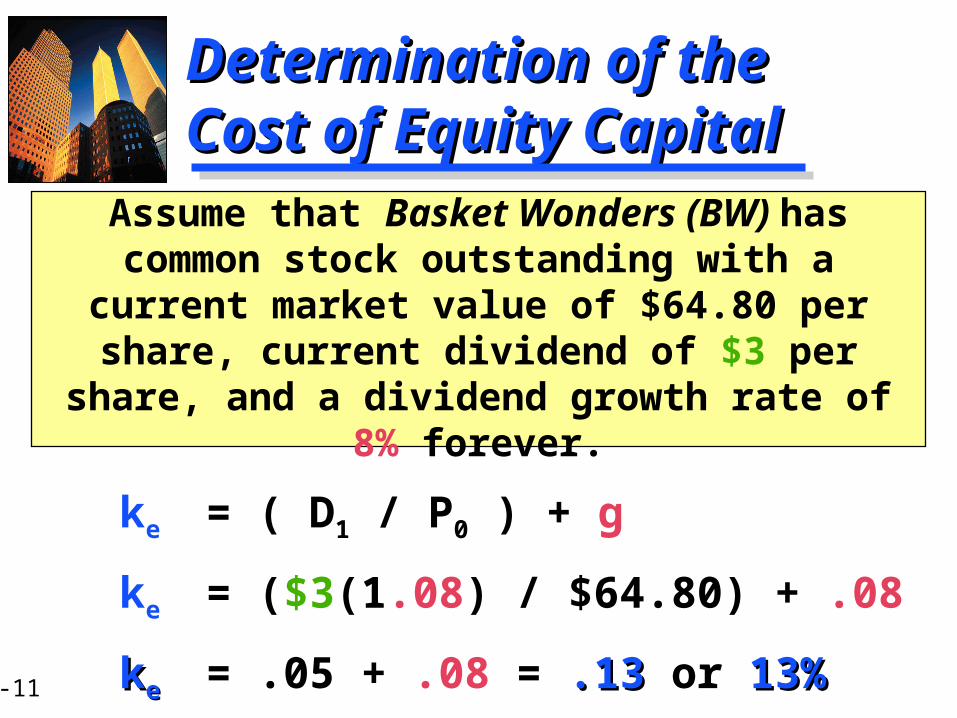

Assume that Basket Wonders (BW) has common stock outstanding with a

current market value of $64.80 per share, current dividend of $3 per

share, and a dividend growth rate of 8% forever.

ke = ( D1 / P0 ) + gke = ($3(1.08) / $64.80) + .08kkee = .05 + .08 = .13.13 or 13%13%

Determination of the Determination of the Cost of Equity CapitalCost of Equity Capital

15-12

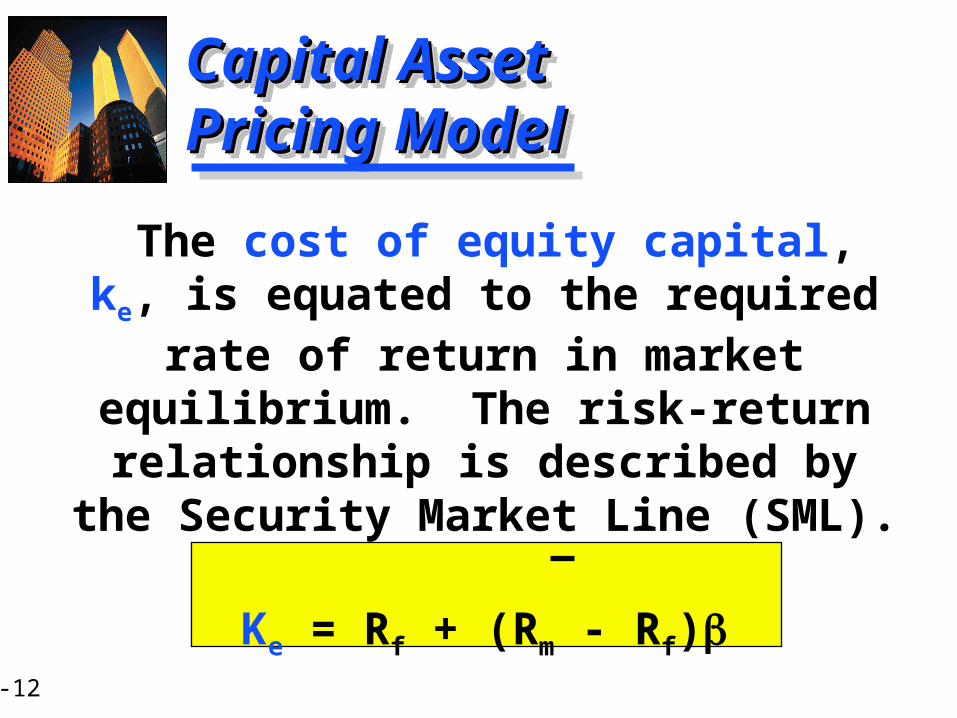

Capital Asset Capital Asset Pricing ModelPricing Model

The cost of equity capital, ke, is equated to the required

rate of return in market equilibrium. The risk-return relationship is described by

the Security Market Line (SML).

Ke = Rf + (Rm - Rf)

15-13

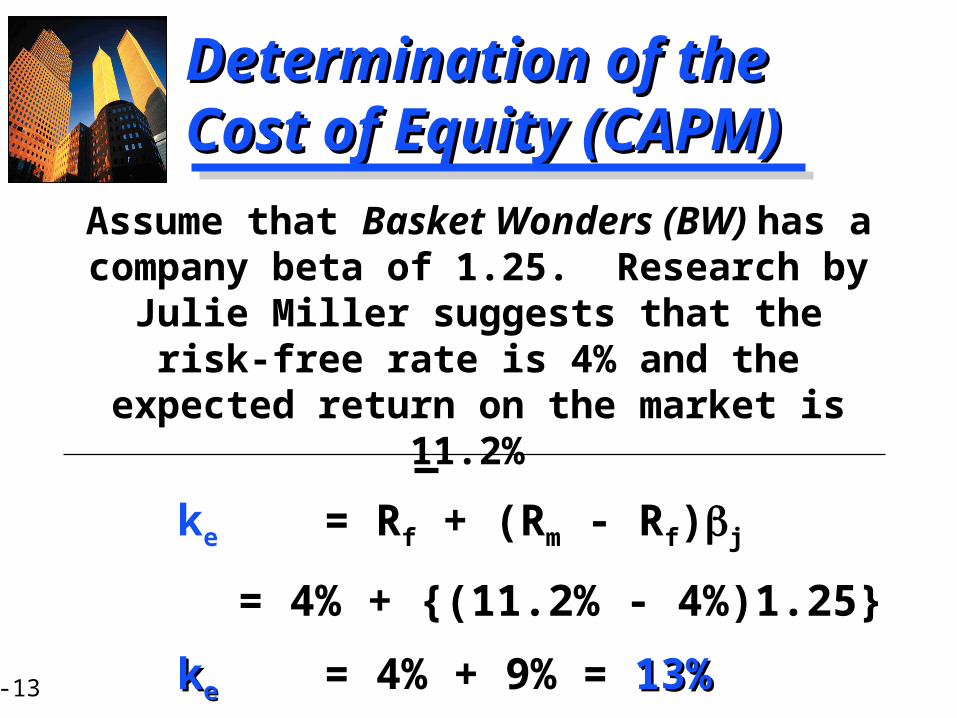

Assume that Basket Wonders (BW) has a company beta of 1.25. Research by

Julie Miller suggests that the risk-free rate is 4% and the

expected return on the market is 11.2%

ke = Rf + (Rm - Rf)j = 4% + {(11.2% - 4%)1.25}

kkee = 4% + 9% = 13%13%

Determination of the Determination of the Cost of Equity (CAPM)Cost of Equity (CAPM)

15-14

Before-Tax Cost of Debt Before-Tax Cost of Debt Plus Risk PremiumPlus Risk Premium

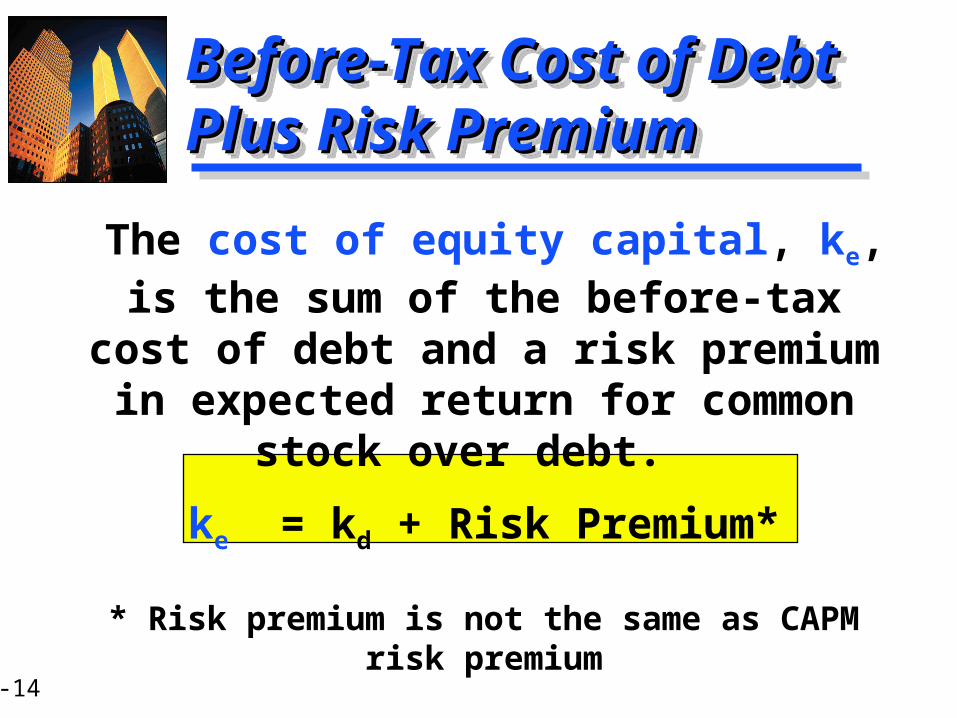

The cost of equity capital, ke, is the sum of the before-tax

cost of debt and a risk premium in expected return for common

stock over debt. ke = kd + Risk Premium*

* Risk premium is not the same as CAPM risk premium

15-15

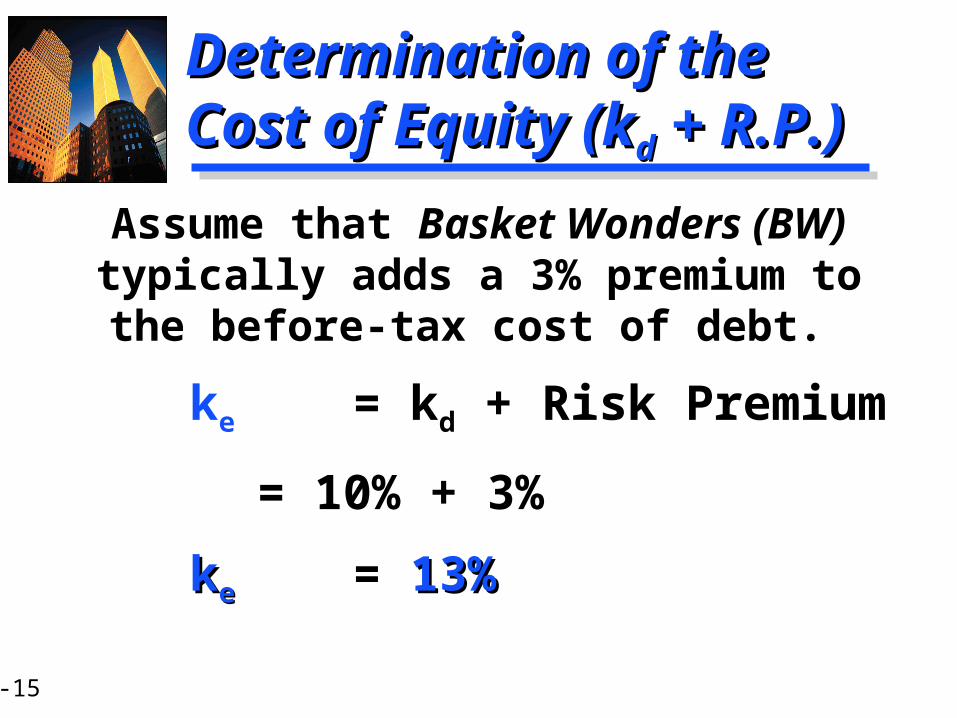

Assume that Basket Wonders (BW) typically adds a 3% premium to the before-tax cost of debt. ke = kd + Risk Premium

= 10% + 3% kkee = 13%13%

Determination of the Determination of the Cost of Equity (kCost of Equity (kdd + R.P.) + R.P.)

15-16

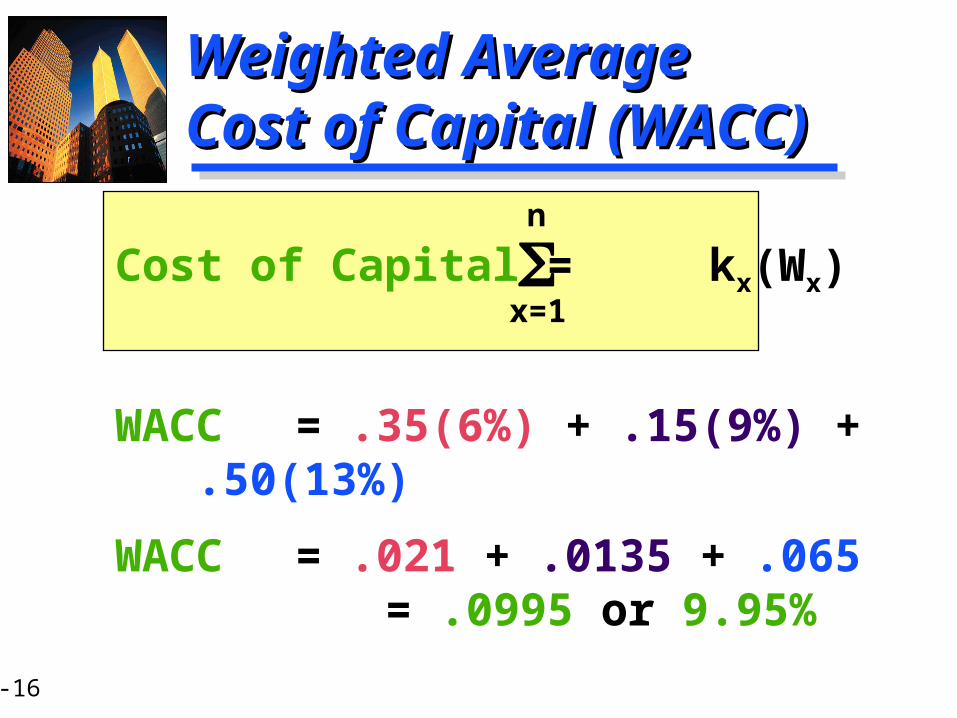

Cost of Capital = kx(Wx)

WACC = .35(6%) + .15(9%) + .50(13%)WACC = .021 + .0135 + .065 = .0995 or 9.95%

Weighted Average Weighted Average Cost of Capital (WACC)Cost of Capital (WACC)

n

x=1

Related Documents