14 May 2014 Interim Report Q1 2014 1 Presentation of Interim Report Q1 2014

FLSmidth 1st Quarter Report 2014 Presentation

Jun 27, 2015

FLSmidth first quarter report for 2014 was released on 14 May 2014. Best viewed on a full screen mode, this Interim report for Q1 2014 informs the reader about the latest business and financial update from FLSmidth. It also gives a glimpse of the key highlights in the 1st Quarter as well as FLSmidth's growth strategies and new financial targets projected for the next quarter.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

14 May 2014 Interim Report Q1 2014 1

Presentation of Interim Report Q1 2014

Presentation of FLSmidth’s Interim Report 1st quarter 2014

Copenhagen, 14 May 2014 @ 11am CET

Business update – Thomas Schulz, Group CEO

Financial update – Lars Vestergaard, Group CFO

Agenda

Agenda

14 May 2014 Interim Report Q1 2014 2

Key highlights in Q1’14

Positive order intake growth (adjusted for currency)

Revenue as expected Significant improvement in earnings Unsatisfactory increase in net working capital

Focus on managing the cyclical downturn... ...and preparing for the upturn

14 May 2014 Interim Report Q1 2014 3

Mining capex

Downturn to continue throughout 2014 Flattish or slight decline in 2015 Slow growth in 2016

Cement capex

At a low level since 2009 Slightly higher level of activity in 2014 Recovery to commence in 2015

Customer Services resilient and growing

Overall market trends unchanged

Guidance

14 May 2014 Interim Report Q1 2014 4

Market reality in Mineral Processing

Reverse negative trend in net working capital

Increased sales activities & customer contact

Launch of new products

Leadership development

Current management focus areas

Management focus areas

14 May 2014 Interim Report Q1 2014 5

FLSmidth Salt Lake City, Ore characterization and process mineralogy laboratories

New FLSmidth office established in Colombia

Mobilisation of O&M contract in Nigeria well under way

License agreement with Kobe Steel, Japan for construction of iron ore pellet process in India

FLSmidth recognised as a leading supplier to the Chilean Mining Industry

FLSmidth BulkExpert™ winner of the 2013 Mining Magazine Bulk Handling award

Operational highlights in Q1 2014

Operation highlights

14 May 2014 Interim Report Q1 2014 6

Succesful commercialisation of MAAG CEM drive (gearbox with integrated motor)

FLSmidth’s Reflux™ Classifier technology accepted as the preferred fines gravity separator by the major producers of metallurgical coal

Sustainable technology highlights Q1 2014

Sustainable technology

14 May 2014 Interim Report Q1 2014 7

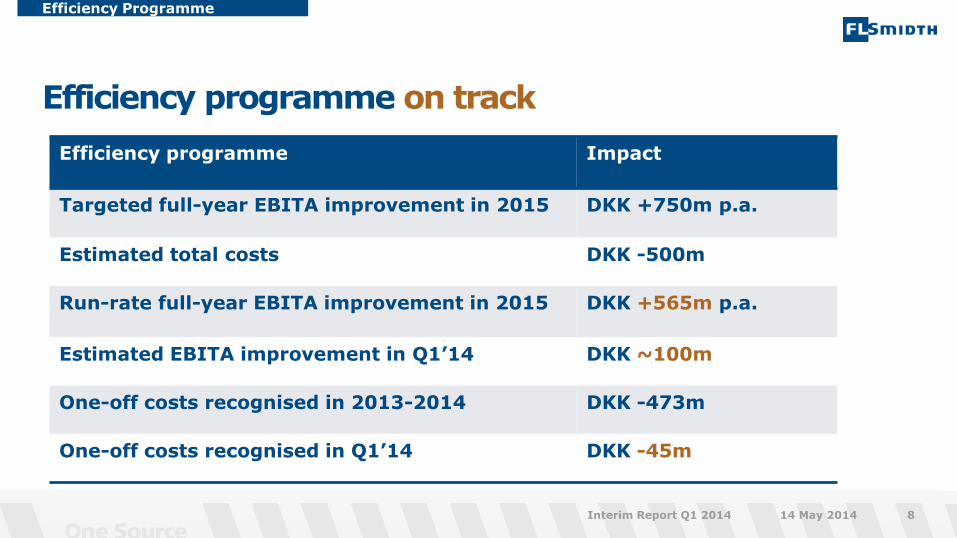

Efficiency programme on track

Efficiency Programme

14 May 2014 Interim Report Q1 2014 8

Efficiency programme Impact

Targeted full-year EBITA improvement in 2015 DKK +750m p.a.

Estimated total costs DKK -500m

Run-rate full-year EBITA improvement in 2015 DKK +565m p.a.

Estimated EBITA improvement in Q1’14 DKK ~100m

One-off costs recognised in 2013-2014 DKK -473m

One-off costs recognised in Q1’14 DKK -45m

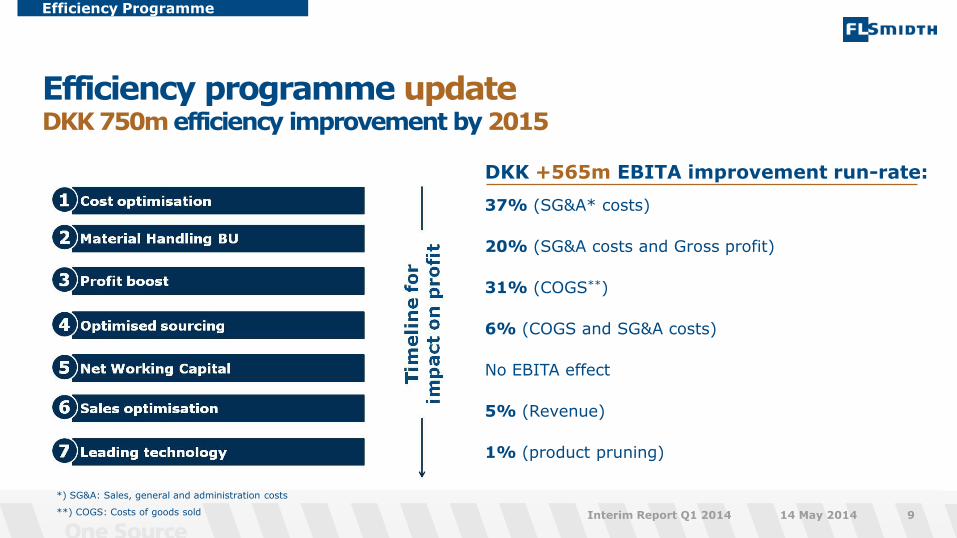

Efficiency programme update DKK 750m efficiency improvement by 2015

Efficiency Programme

14 May 2014 Interim Report Q1 2014 9

DKK +565m EBITA improvement run-rate:

37% (SG&A* costs)

20% (SG&A costs and Gross profit)

31% (COGS**)

6% (COGS and SG&A costs)

No EBITA effect

5% (Revenue)

1% (product pruning)

*) SG&A: Sales, general and administration costs

**) COGS: Costs of goods sold

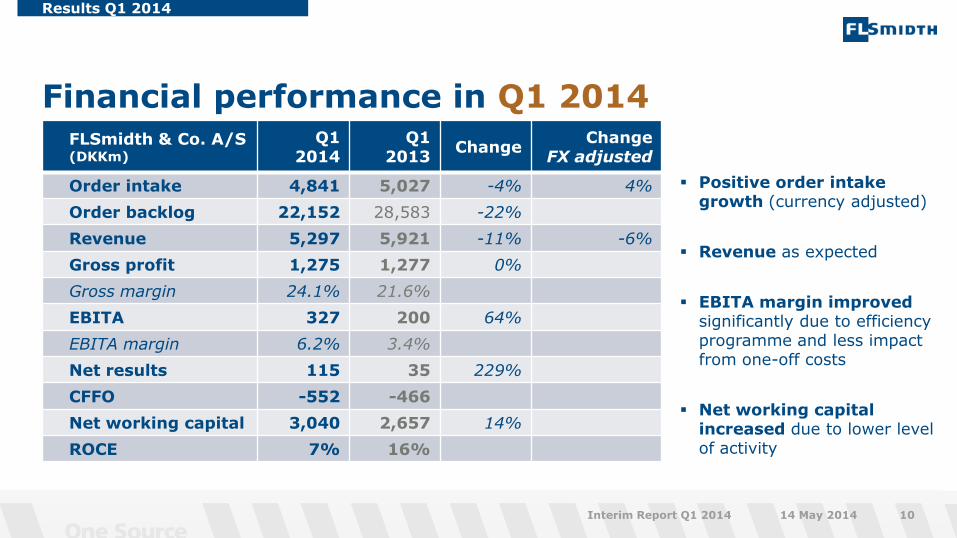

Positive order intake growth (currency adjusted)

Revenue as expected

EBITA margin improved significantly due to efficiency programme and less impact from one-off costs

Net working capital increased due to lower level of activity

Financial performance in Q1 2014

Results Q1 2014

14 May 2014 10 Interim Report Q1 2014

FLSmidth & Co. A/S (DKKm)

Q1 2014

Q1 2013

Change Change

FX adjusted

Order intake 4,841 5,027 -4% 4%

Order backlog 22,152 28,583 -22%

Revenue 5,297 5,921 -11% -6%

Gross profit 1,275 1,277 0%

Gross margin 24.1% 21.6%

EBITA 327 200 64%

EBITA margin 6.2% 3.4%

Net results 115 35 229%

CFFO -552 -466

Net working capital 3,040 2,657 14%

ROCE 7% 16%

41%

18%

6%

7%

2% 1%

25%

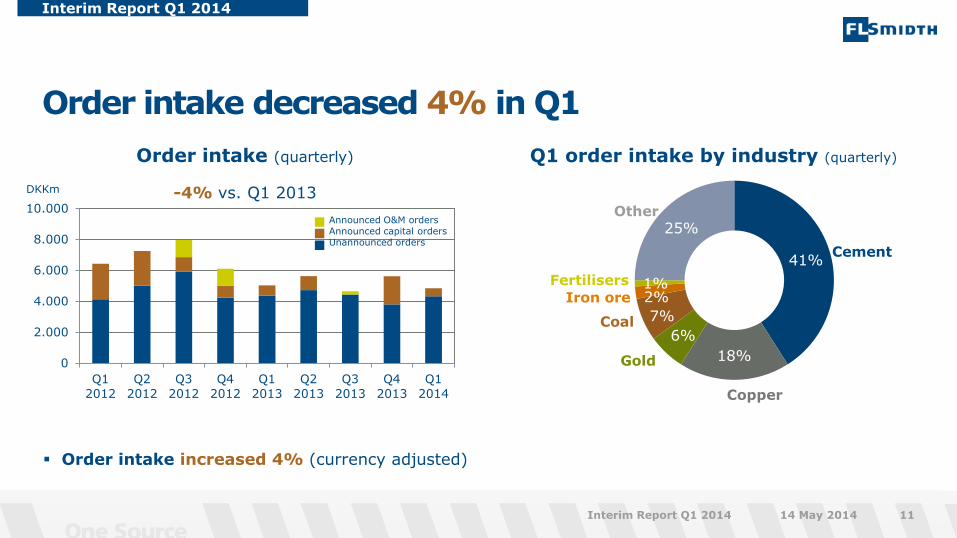

Order intake decreased 4% in Q1

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 11

Q1 order intake by industry (quarterly)

Cement

Coal

Iron ore

Other

Copper

Gold 0

2.000

4.000

6.000

8.000

10.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Order intake (quarterly)

-4% vs. Q1 2013 DKKm

Announced O&M orders Announced capital orders Unannounced orders

Order intake increased 4% (currency adjusted)

Fertilisers

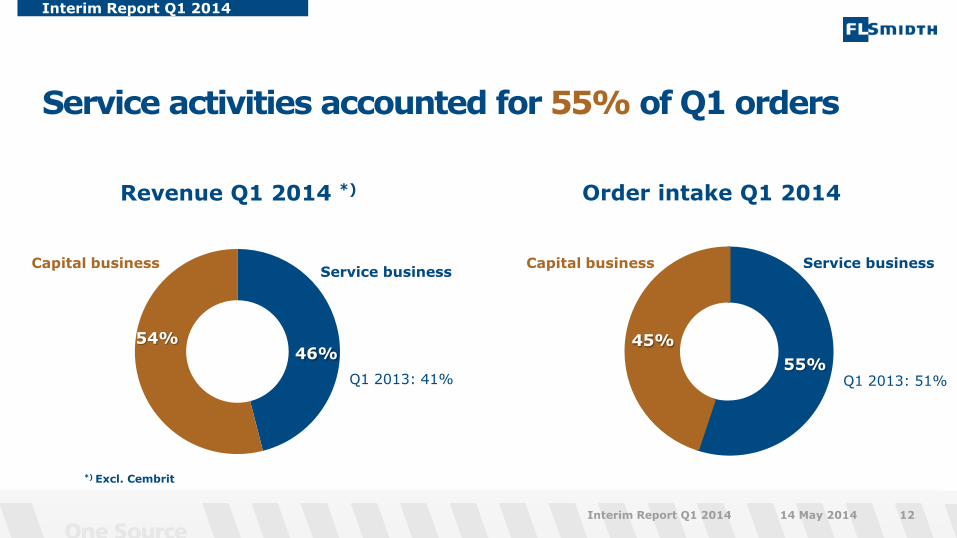

Service activities accounted for 55% of Q1 orders

Interim Report Q1 2014

Interim Report Q1 2014 12

Revenue Q1 2014 *)

14 May 2014

Order intake Q1 2014

46% 54%

Capital business

55%

45%

Service business Capital business Service business

Q1 2013: 41% Q1 2013: 51%

*) Excl. Cembrit

Gross margin improved

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 13

Gross margin

25,4% 21,6% 24,1%

0%

10%

20%

30%

40%

0

500

1.000

1.500

2.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Gross profit (quarterly)

Unchanged vs. Q1 2013 DKKm

Increase in gross margin due improved performance in Material Handling and Cembrit as well as positive impact from efficiency programme

Gross margin Q1’14 vs. Q1’13 - by division

27,0%

11,8%

21,5% 19,8%

28,4%

18,0% 20,8% 19,9%

Customer Services

Material Handling

Mineral Processing

Cement

Q1’14 Q1’13 Q1’14 Q1’13 Q1’14 Q1’13 Q1’14 Q1’13

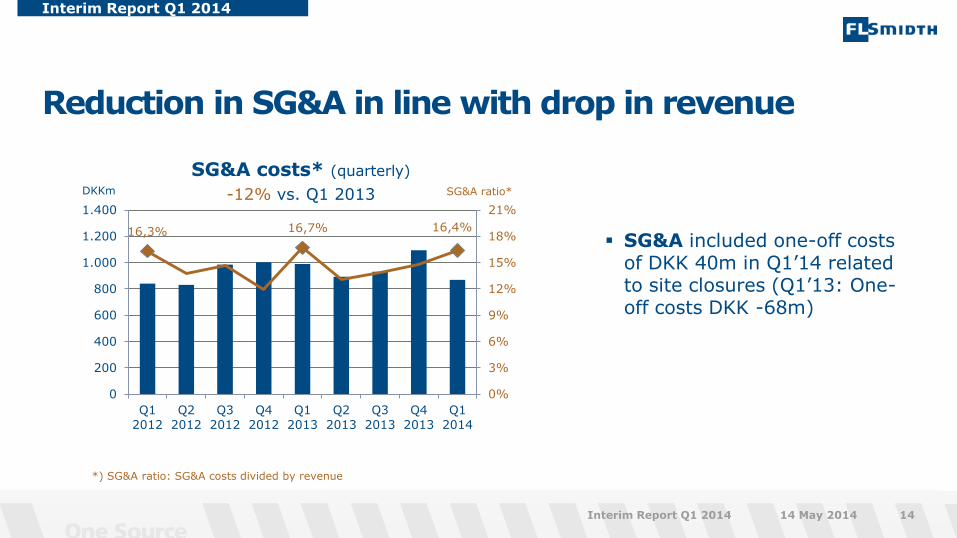

Reduction in SG&A in line with drop in revenue

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 14

SG&A included one-off costs of DKK 40m in Q1’14 related to site closures (Q1’13: One-off costs DKK -68m)

SG&A ratio*

16,3% 16,7% 16,4%

0%

3%

6%

9%

12%

15%

18%

21%

0

200

400

600

800

1.000

1.200

1.400

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

SG&A costs* (quarterly)

-12% vs. Q1 2013 DKKm

*) SG&A ratio: SG&A costs divided by revenue

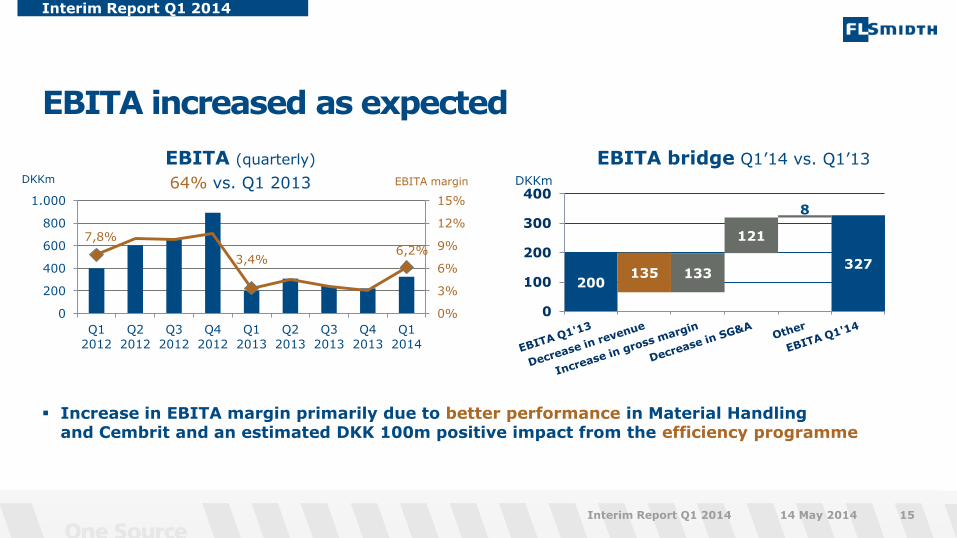

Increase in EBITA margin primarily due to better performance in Material Handling and Cembrit and an estimated DKK 100m positive impact from the efficiency programme

EBITA increased as expected

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 15

EBITA margin

7,8%

3,4% 6,2%

0%

3%

6%

9%

12%

15%

0

200

400

600

800

1.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

EBITA (quarterly)

64% vs. Q1 2013 DKKm DKKm

EBITA bridge Q1’14 vs. Q1’13

200

327 133

121

8

135

0

100

200

300

400

Increase in working capital expected to be reversed in 2014

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 16

Net working capital

DKKm End Q1 2014 vs. End Q4 2013

Change in net working capital

DKKm

0

500

1.000

1.500

2.000

2.500

3.000

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

2.382

3.040

606

536

171 154

47 112

-

1.000

2.000

3.000

4.000

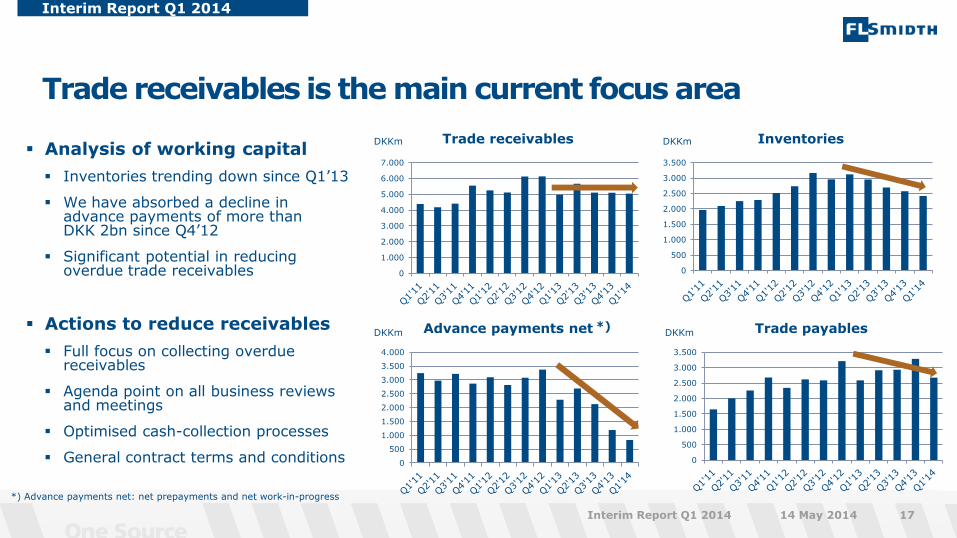

Trade receivables is the main current focus area

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 17

Analysis of working capital

Inventories trending down since Q1’13

We have absorbed a decline in advance payments of more than DKK 2bn since Q4’12

Significant potential in reducing overdue trade receivables

Actions to reduce receivables

Full focus on collecting overdue receivables

Agenda point on all business reviews and meetings

Optimised cash-collection processes

General contract terms and conditions

0

500

1.000

1.500

2.000

2.500

3.000

3.500

Inventories

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

Trade receivables

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

Advance payments net *)

*) Advance payments net: net prepayments and net work-in-progress

0

500

1.000

1.500

2.000

2.500

3.000

3.500

Trade payables

DKKm DKKm

DKKm DKKm

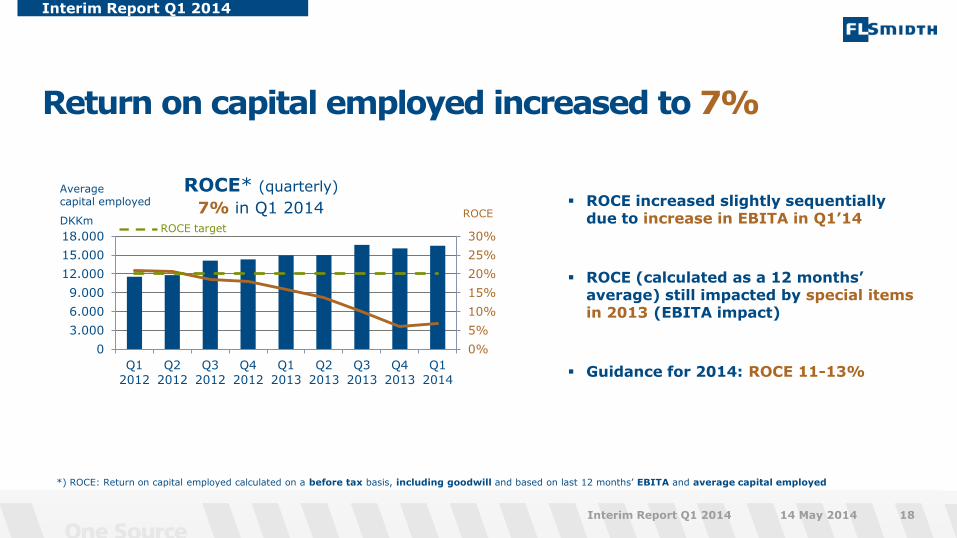

ROCE increased slightly sequentially due to increase in EBITA in Q1’14

ROCE (calculated as a 12 months’ average) still impacted by special items in 2013 (EBITA impact)

Guidance for 2014: ROCE 11-13%

Return on capital employed increased to 7%

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 18

ROCE* (quarterly) Average capital employed

DKKm

0%

5%

10%

15%

20%

25%

30%

0

3.000

6.000

9.000

12.000

15.000

18.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

ROCE

7% in Q1 2014

*) ROCE: Return on capital employed calculated on a before tax basis, including goodwill and based on last 12 months’ EBITA and average capital employed

ROCE target

Guidance

14 May 2014 Interim Report Q1 2014 19

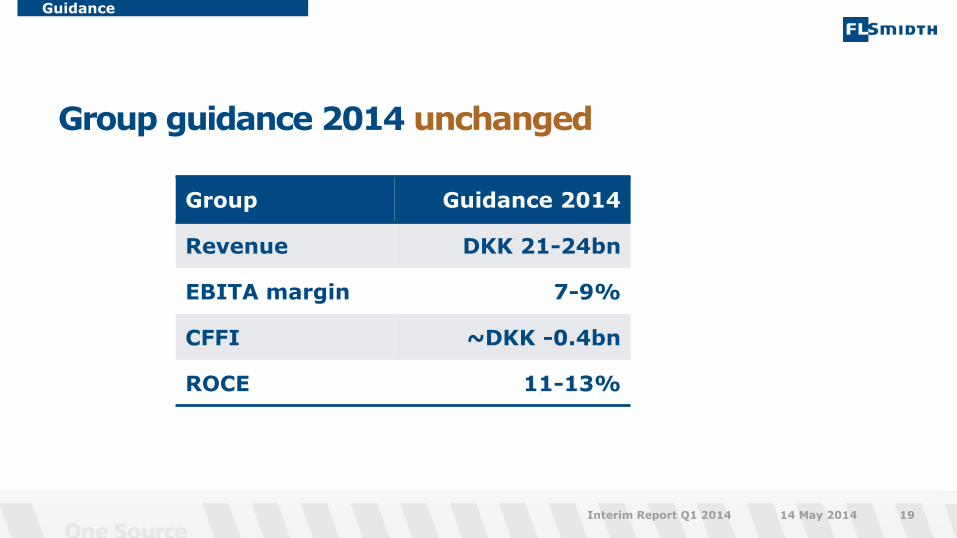

Group Guidance 2014

Revenue DKK 21-24bn

EBITA margin 7-9%

CFFI ~DKK -0.4bn

ROCE 11-13%

Group guidance 2014 unchanged

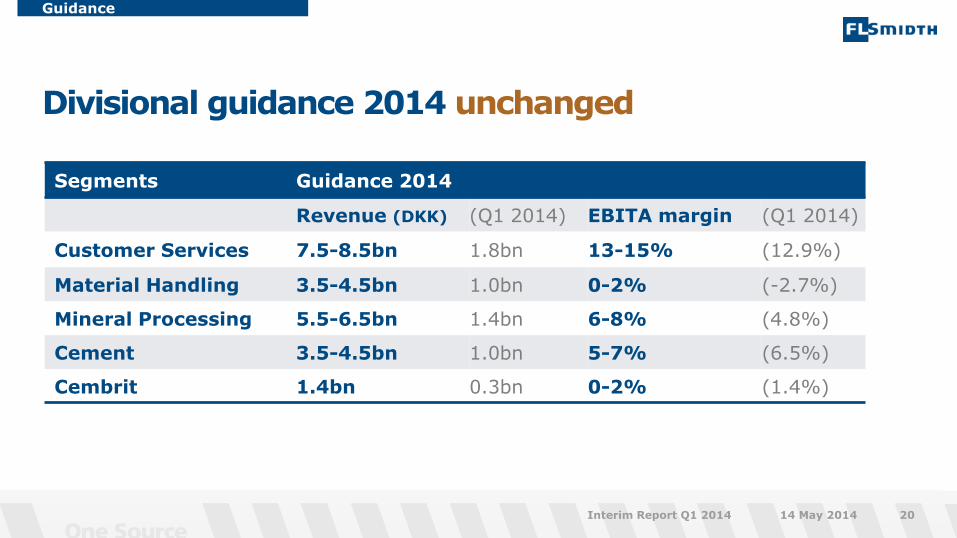

Divisional guidance 2014 unchanged

Guidance

14 May 2014 Interim Report Q1 2014 20

Segments Guidance 2014

Revenue (DKK) (Q1 2014) EBITA margin (Q1 2014)

Customer Services 7.5-8.5bn 1.8bn 13-15% (12.9%)

Material Handling 3.5-4.5bn 1.0bn 0-2% (-2.7%)

Mineral Processing 5.5-6.5bn 1.4bn 6-8% (4.8%)

Cement 3.5-4.5bn 1.0bn 5-7% (6.5%)

Cembrit 1.4bn 0.3bn 0-2% (1.4%)

Key highlights in Q1’14

Positive order intake growth (adjusted for currency)

Revenue as expected Significant improvement in earnings Unsatisfactory increase in net working capital

Focus on managing the cyclical downturn... ...and preparing for the upturn

14 May 2014 Interim Report Q1 2014 21

Forward-looking statements

Annual Report 2013

14 May 2014 Interim Report Q1 2014 22

FLSmidth & Co. A/S’ financial reports, whether in the form of annual reports or interim reports, filed with the Danish Business Authority and/or announced via the company’s website and/or NASDAQ OMX Copenhagen, as well as any presentations based on such financial reports, and any other written information released, or oral statements made, to the public based on this interim report or in the future on behalf of FLSmidth & Co. A/S, may contain forward-looking statements. Words such as ‘believe’, ‘expect’, ‘may’, ‘will’, ‘plan’, ‘strategy’, ‘prospect’, ‘foresee’, ‘estimate’, ‘project’, ‘anticipate’, ‘can’, ‘intend’, ‘target’ and other words and terms of similar meaning in connection with any discussion of future operating or financial performance identify forward-looking statements. Examples of such forward-looking statements include, but are not limited to: • statements of plans, objectives or goals for future operations, including those related to FLSmidth & Co. A/S markets, products, product research and product

development • statements containing projections of or targets for revenues, profit (or loss), capital expenditures, dividends, capital structure or other net financial items • statements regarding future economic performance, future actions and outcome of contingencies such as legal proceedings and statements regarding the underlying

assumptions or relating to such statements • statements regarding potential merger & acquisition activities. These forward-looking statements are based on current plans, estimates and projections. By their very

nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, which may be outside FLSmidth & Co. A/S’s influence, and which could materially affect such forward-looking statements.

FLSmidth & Co. A/S cautions that a number of important factors, including those described in this presentation, could cause actual results to differ materially from those contemplated in any forward-looking statements. Factors that may affect future results include, but are not limited to, global as well as local political and economic conditions, including interest rate and exchange rate fluctuations, delays or faults in project execution, fluctuations in raw material prices, delays in research and/or development of new products or service concepts, interruptions of supplies and production, unexpected breach or termination of contracts, market-driven price reductions for FLSmidth & Co. A/S’ products and/or services, introduction of competing products, reliance on information technology, FLSmidth & Co. A/S’ ability to successfully market current and new products, exposure to product liability and legal proceedings and investigations, changes in legislation or regulation and interpretation thereof, intellectual property protection, perceived or actual failure to adhere to ethical marketing practices, investments in and divestitures of domestic and foreign enterprises, unexpected growth in costs and expenses, failure to recruit and retain the right employees and failure to maintain a culture of compliance. Unless required by law FLSmidth & Co. A/S is under no duty and undertakes no obligation to update or revise any forward-looking statement after the distribution of this presentation.

Questions & Answers Next update: Interim Report on 13 August 2014 Follow us on Twitter and LinkedIn

14 May 2014 Interim Report Q1 2014 23

Appendices - backup slides

14 May 2014 Interim Report Q1 2014 24

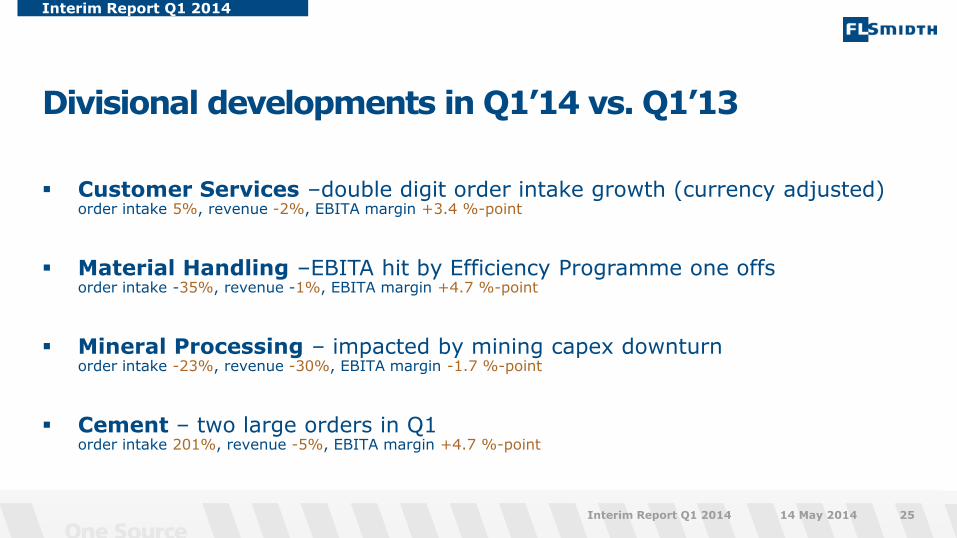

Customer Services –double digit order intake growth (currency adjusted) order intake 5%, revenue -2%, EBITA margin +3.4 %-point

Material Handling –EBITA hit by Efficiency Programme one offs order intake -35%, revenue -1%, EBITA margin +4.7 %-point

Mineral Processing – impacted by mining capex downturn order intake -23%, revenue -30%, EBITA margin -1.7 %-point

Cement – two large orders in Q1 order intake 201%, revenue -5%, EBITA margin +4.7 %-point

Divisional developments in Q1’14 vs. Q1’13

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 25

Customer Services

14 May 2014 Interim Report Q1 2014 26

Revenue increased 4% (currency adjusted)

Order intake increased 13% adjusted for currency

Customer Services

14 May 2014 Interim Report Q1 2014 27

0

1.000

2.000

3.000

4.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Order intake (quarterly)

5% vs. Q1 2013 DKKm

Announced O&M orders Announced capital orders Unannounced orders

Revenue (quarterly)

DKKm EBITA margin -2% vs. Q1 2013

0%

4%

8%

12%

16%

20%

0

500

1.000

1.500

2.000

2.500

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

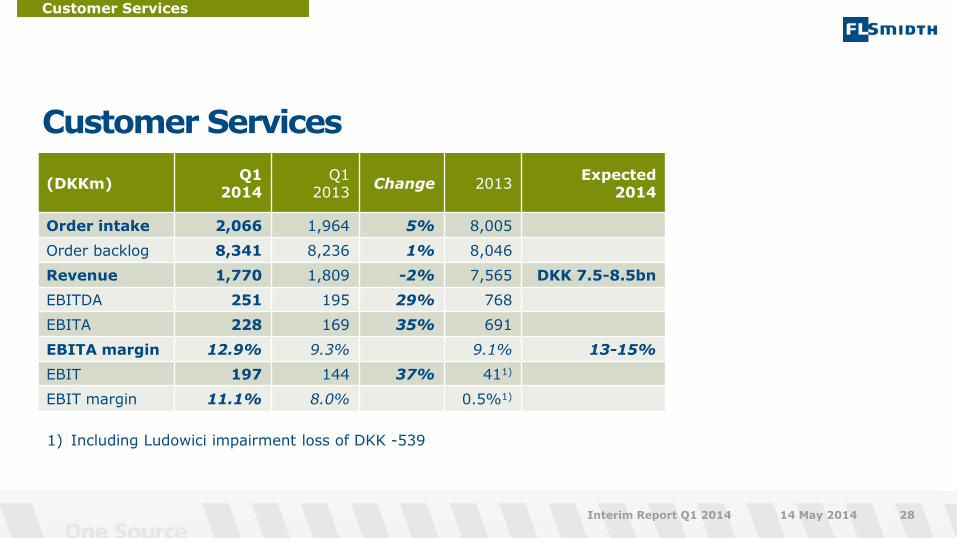

Customer Services

Customer Services

14 May 2014 Interim Report Q1 2014 28

(DKKm) Q1

2014 Q1

2013 Change

2013

Expected 2014

Order intake 2,066 1,964 5% 8,005

Order backlog 8,341 8,236 1% 8,046

Revenue 1,770 1,809 -2% 7,565 DKK 7.5-8.5bn

EBITDA 251 195 29% 768

EBITA 228 169 35% 691

EBITA margin 12.9% 9.3% 9.1% 13-15%

EBIT 197 144 37% 411)

EBIT margin 11.1% 8.0% 0.5%1)

1) Including Ludowici impairment loss of DKK -539

Material Handling

14 May 2014 Interim Report Q1 2014 29

No large orders in Q1

EBITA margin of -2.7% included one-off administrative cost of DKK -40m related to the Efficiency Programme

Strong order intake in challenging market

Material Handling

14 May 2014 Interim Report Q1 2014 30

0

500

1.000

1.500

2.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Order intake (quarterly)

-35% vs. Q4 2012 DKKm

111111

Announced orders Unannounced orders

Revenue (quarterly)

DKKm EBITA margin -1% vs. Q1 2013

-40% -30% -20% -10% 0% 10% 20% 30% 40%

-2.400 -1.800 -1.200

-600 0

600 1.200 1.800 2.400

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Material Handling

Material Handling

14 May 2014 Interim Report Q1 2014 31

(DKKm) Q1

2014 Q1

2013 Change

2013

Expected 2014

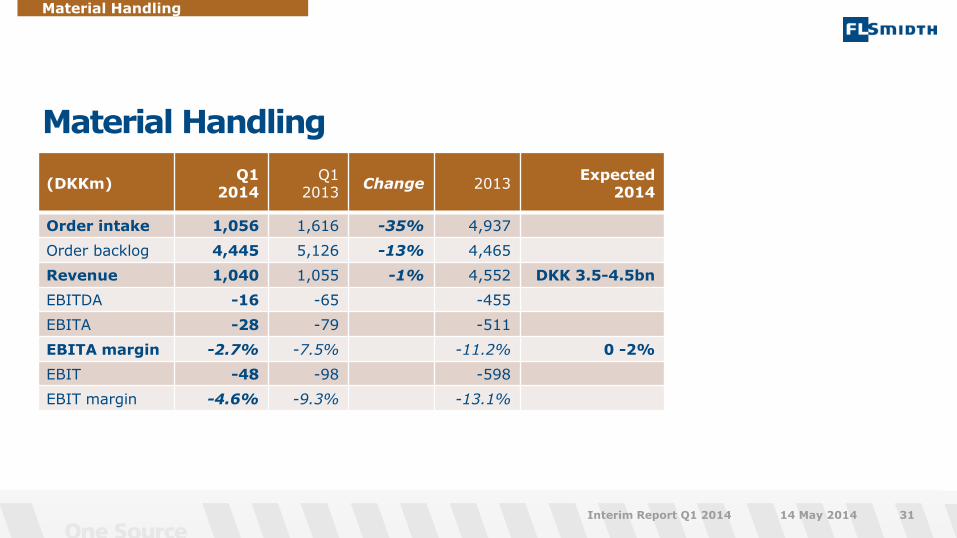

Order intake 1,056 1,616 -35% 4,937

Order backlog 4,445 5,126 -13% 4,465

Revenue 1,040 1,055 -1% 4,552 DKK 3.5-4.5bn

EBITDA -16 -65 -455

EBITA -28 -79 -511

EBITA margin -2.7% -7.5% -11.2% 0 -2%

EBIT -48 -98 -598

EBIT margin -4.6% -9.3% -13.1%

No new problematic projects identified

14 projects out of a total portfolio of 190 projects

in the Material Handling Business Unit are

currently regarded as risky (end of Q4 2013: 14 projects)

These projects accounted for DKK 356m or 8%

of the backlog at the end of Q4 (end of Q4 2013: DKK

481m or 11%)

The one-off costs of DKK 323m realised in Q2 2013 still expected to cover future losses related to the legacy projects

Status on legacy projects in Material Handling

Material Handling

14 May 2014 Interim Report Q1 2014 32

Mineral Processing

14 May 2014 Interim Report Q1 2014 33

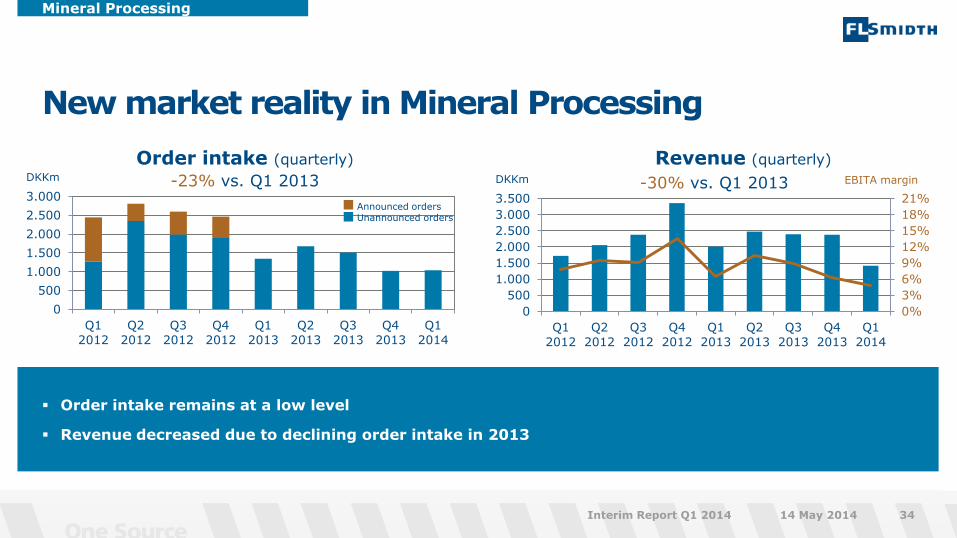

Order intake remains at a low level

Revenue decreased due to declining order intake in 2013

New market reality in Mineral Processing

Mineral Processing

14 May 2014 Interim Report Q1 2014 34

Revenue (quarterly)

DKKm EBITA margin -30% vs. Q1 2013

0%

3%

6%

9%

12%

15%

18%

21%

0

500

1.000

1.500

2.000

2.500

3.000

3.500

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

0

500

1.000

1.500

2.000

2.500

3.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Order intake (quarterly)

-23% vs. Q1 2013 DKKm

Announced orders Unannounced orders

Mineral Processing

Mineral Processing

14 May 2014 Interim Report Q1 2014 35

(DKKm) Q1

2014 Q1

2013 Change

2013

Expected 2014

Order intake 1,041 1,345 -23% 5,559

Order backlog 4,635 9,057 -49% 4,993

Revenue 1,416 2,010 -30% 9,256 DKK 5.5-6.5bn

EBITDA 89 151 -41% 850

EBITA 68 130 -48% 757

EBITA margin 4.8% 6.5% 8.2% 6-8%

EBIT 38 88 -57% 2111)

EBIT margin 2.7% 4.4% 2.3%1)

1) Including Ludowici impairment loss of DKK -362

Cement

14 May 2014 Interim Report Q1 2014 36

0

500

1.000

1.500

2.000

2.500

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

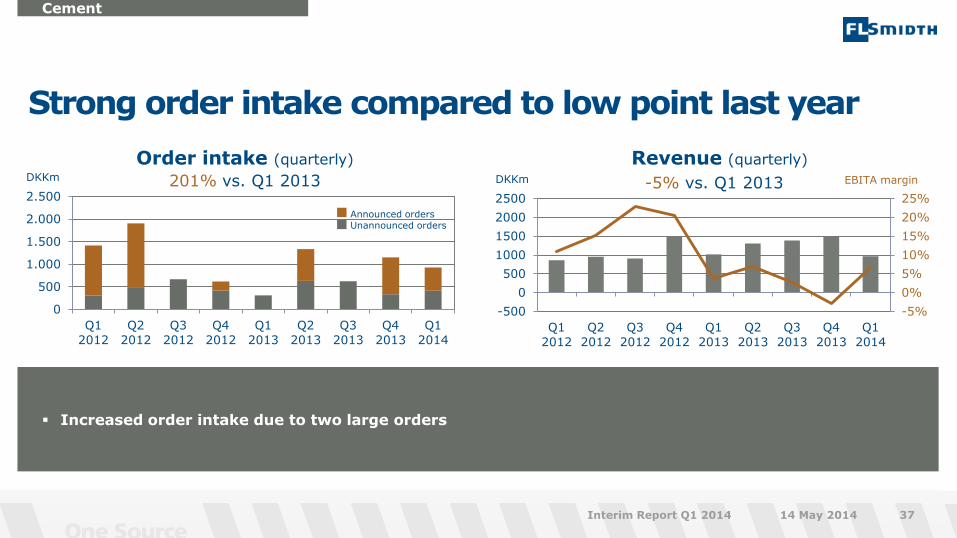

Increased order intake due to two large orders

Strong order intake compared to low point last year

Cement

14 May 2014 Interim Report Q1 2014 37

Revenue (quarterly)

DKKm EBITA margin -5% vs. Q1 2013

-5%

0%

5%

10%

15%

20%

25%

-500

0

500

1000

1500

2000

2500

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Order intake (quarterly)

201% vs. Q1 2013 DKKm

Announced orders Unannounced orders

Cement

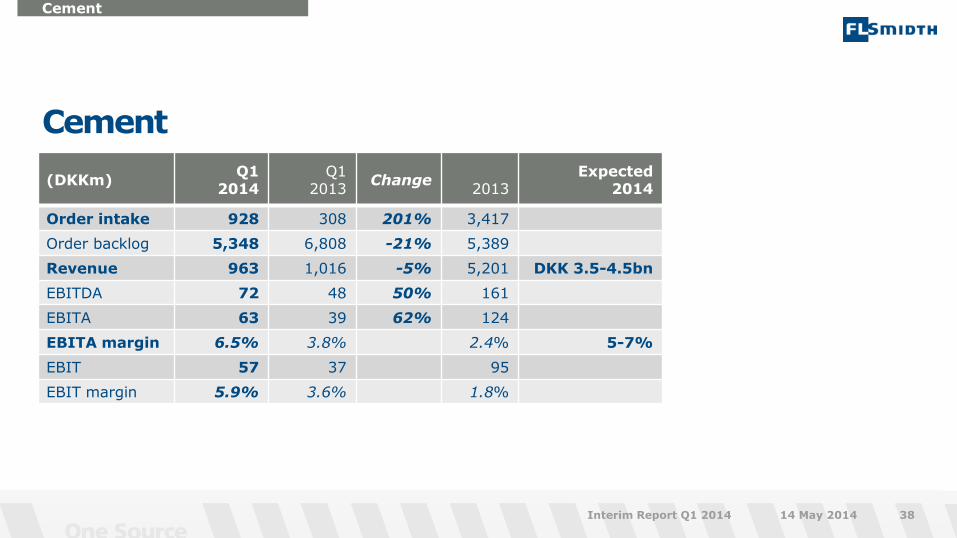

Cement

14 May 2014 Interim Report Q1 2014 38

(DKKm) Q1

2014 Q1

2013 Change

2013

Expected 2014

Order intake 928 308 201% 3,417

Order backlog 5,348 6,808 -21% 5,389

Revenue 963 1,016 -5% 5,201 DKK 3.5-4.5bn

EBITDA 72 48 50% 161

EBITA 63 39 62% 124

EBITA margin 6.5% 3.8% 2.4% 5-7%

EBIT 57 37 95

EBIT margin 5.9% 3.6% 1.8%

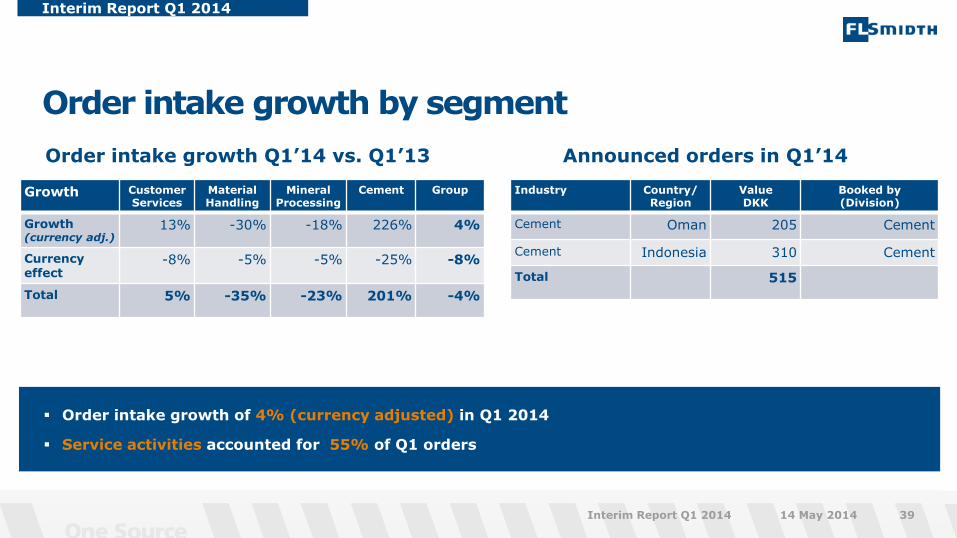

Order intake growth of 4% (currency adjusted) in Q1 2014

Service activities accounted for 55% of Q1 orders

Order intake growth by segment

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 39

Growth Customer Services

Material Handling

Mineral Processing

Cement Group

Growth (currency adj.)

13% -30% -18% 226% 4%

Currency effect

-8% -5% -5% -25% -8%

Total 5% -35% -23% 201% -4%

Order intake growth Q1’14 vs. Q1’13

Industry Country/ Region

Value DKK

Booked by (Division)

Cement Oman 205 Cement

Cement Indonesia 310 Cement

Total 515

Announced orders in Q1’14

Revenue growth of -6% (currency adjusted) in Q1 2014

Service activities accounted for 46% of Q1 revenue

Expected backlog conversion to revenue: 52% in 2014, 31% in 2015 and 17% in 2016 and beyond. O&M* contracts accounted for DKK 5.2bn (23%) of the order backlog at the end of Q1

Revenue growth by segment

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 40

Growth Customer Services

Material Handling

Mineral Processing

Cement Group

Growth (currency adj.)

4% 6% -24% -2% -6%

Currency effect

-6% -7% -6% -3% -5%

Total -2% -1% -30% -5% -11%

Revenue growth Q1’14 vs. Q1’13

*) Order backlog divided by last-twelve-months revenue

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Revenue (quarterly)

-12% vs. Q4 2012 DKKm

Order backlog

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 41

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Order backlog (quarterly)

-22% vs. Q1 2013 DKKm Book-to-bill ratio*

*Order backlog divided by last 12 months revenue

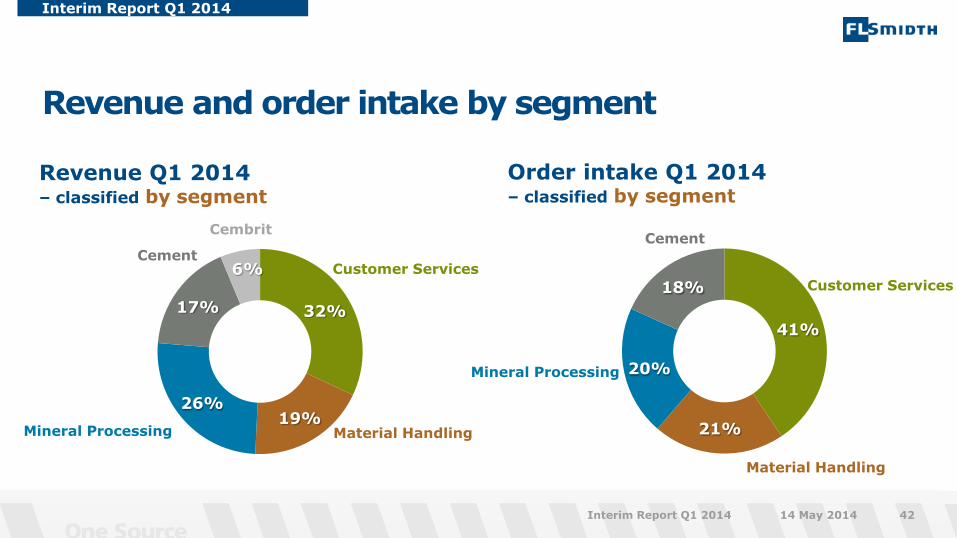

Revenue and order intake by segment

41%

21%

20%

18%

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 42

Order intake Q1 2014 – classified by segment

Customer Services

Material Handling

Cement

32%

19% 26%

17%

6%

Material Handling

Mineral Processing

Revenue Q1 2014 – classified by segment

Customer Services Cement

Mineral Processing

Cembrit

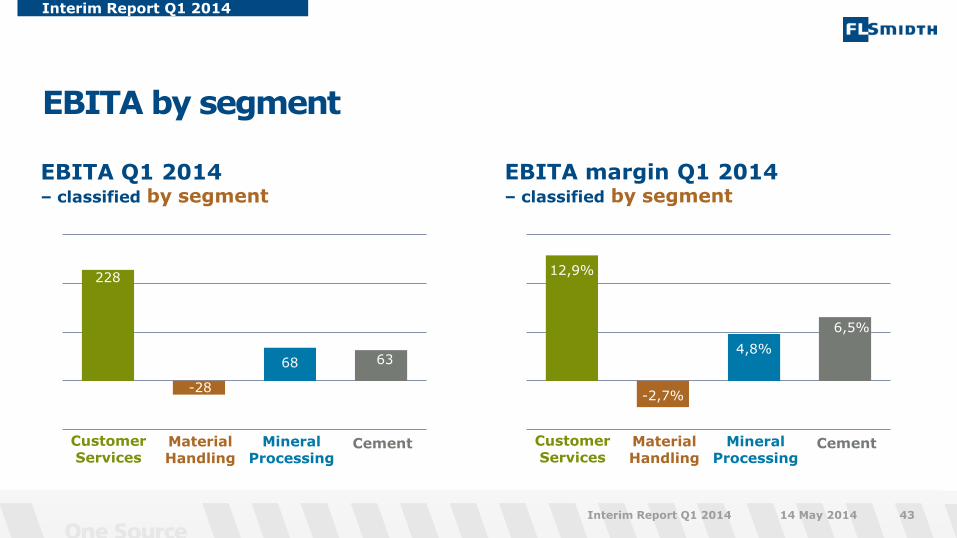

EBITA by segment

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 43

EBITA Q1 2014 – classified by segment

228

-28

68 63

Customer Services

Material Handling

Mineral Processing

Cement

EBITA margin Q1 2014 – classified by segment

12,9%

-2,7%

4,8%

6,5%

Customer Services

Material Handling

Mineral Processing

Cement

Cash flow from investments (CFFI) reflects that acquisitions are currently on hold and that other investments are managed closely

CFFO impacted by increase in working capital

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 44

CFFO (quarterly) DKKm

-800

-400

0

400

800

1.200

1.600

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

CFFI (quarterly)

DKK -72m in Q1 2014 DKKm

-3.000

-2.400

-1.800

-1.200

-600

0

600

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

DKK -552m in Q4 2013

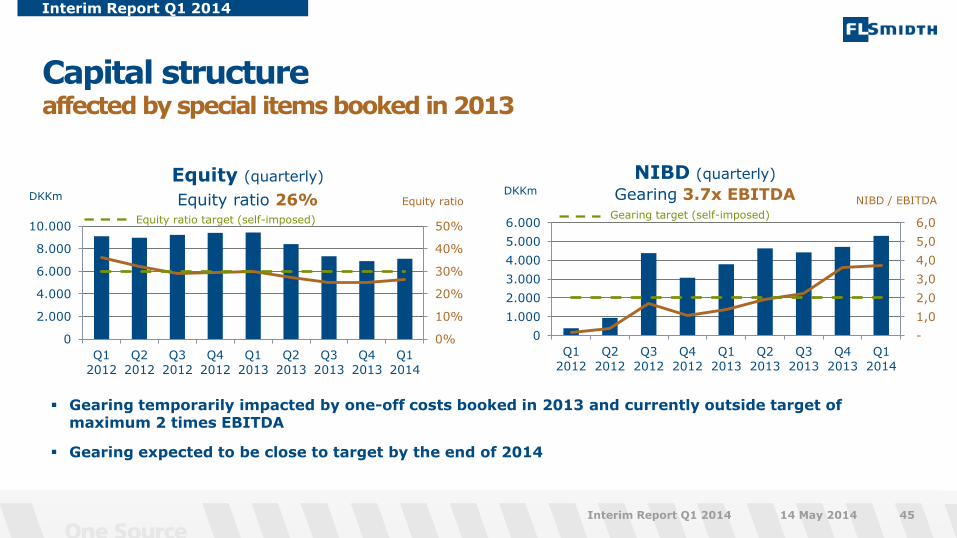

Capital structure affected by special items booked in 2013

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 45

NIBD (quarterly) DKKm

-

1,0

2,0

3,0

4,0

5,0

6,0

0

1.000

2.000

3.000

4.000

5.000

6.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Gearing 3.7x EBITDA Gearing target (self-imposed)

0%

10%

20%

30%

40%

50%

0

2.000

4.000

6.000

8.000

10.000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Equity (quarterly)

DKKm Equity ratio Equity ratio 26%

Equity ratio target (self-imposed)

Gearing temporarily impacted by one-off costs booked in 2013 and currently outside target of maximum 2 times EBITDA

Gearing expected to be close to target by the end of 2014

NIBD / EBITDA

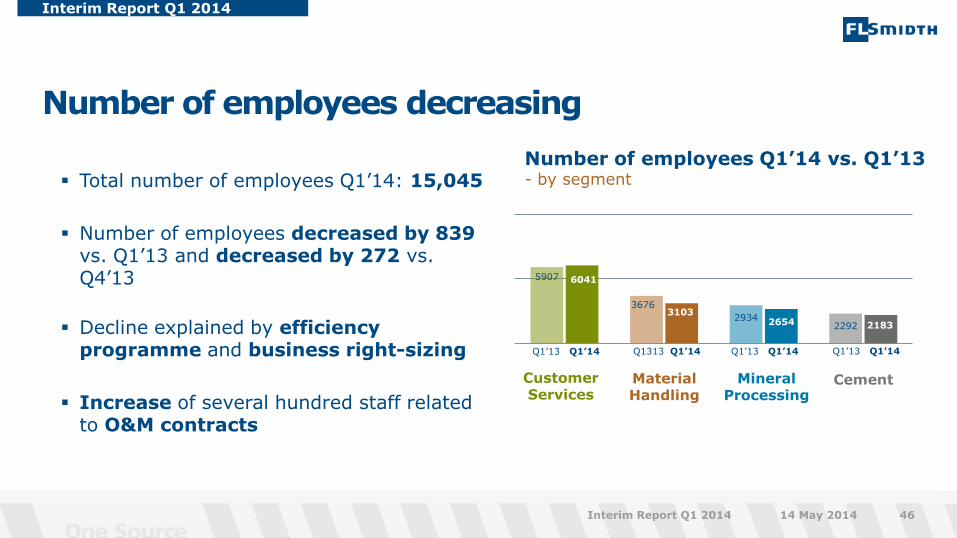

Number of employees decreasing

Interim Report Q1 2014

14 May 2014 Interim Report Q1 2014 46

Number of employees Q1’14 vs. Q1’13 - by segment

5907

3676

2934 2292

6041

3103 2654 2183

Customer Services

Material Handling

Mineral Processing

Cement

Q1’14 Q1’13

Total number of employees Q1’14: 15,045

Number of employees decreased by 839 vs. Q1’13 and decreased by 272 vs. Q4’13

Decline explained by efficiency programme and business right-sizing

Increase of several hundred staff related to O&M contracts

Q1’14 Q1313 Q1’14 Q1’13 Q1’14 Q1’13

Long term financial targets

Targets

14 May 2014 Interim Report Q1 2014 47

Financial targets

Annual revenue growth Above market average

EBITA margin 10-13%

ROCE* > 20%

Tax rate 32-34%

Equity ratio >30%

Financial gearing** <2

Pay-out ratio 30-50%

*) ROCE: Return on capital employed calculated on a before tax basis as EBITA divided by average Capital Employed including goodwill **) Financial gearing: NIBD / EBITDA

Related Documents