Fixed Match Tilting Against FDs Dipak Mondal Delhi Edition: September 2011 With interest rates on bank fixed deposits (FDs) touching 9-9.5 per cent, are you in a fix hether to allocate a part of your in!estible surplus to the inco"e fund your financial planner has ad!ised or are you instead te"pted to park your "oney "eant for fixed inco"e in!est"ent in bank FDs# $n the current scenario, "ost risk-a!erse in!estors ould opt for FDs. %he lure of near double-digit annual returns ith al"ost no risk is too hard to resist gi!en that the a!erage return gi!en by the top 5& inco"e funds in the past one year has been 'ust per cent. $nco"e funds are debt funds offered by mutual funds that seek current inco"e rather than groth of capital. %hey in!est in stocks and bonds that pay high di!idend and interest. $f you ha!e based your in!est"ent decision on the abo!e pre"ise, you "ay ha!e erred not on one but to counts. First, you are co"paring present FD rates ith the past one years perfor"ance of debt funds. $deally, you should co"pare debt fund returns ith FD rates a year a go. *econd, the returns co"pared abo!e are pre-tax, hich "ay gi!e you a co"pletely rong picture. *rikanth +eenakshi, director, Wealth $ndia Financial *er!ices, says often in!estors co""it the "istake of co"paring current FD rates ith the past perfor"ance of debt funds. $deally, debt fund returns should be co"pared to FD rates pre!ailing at the start of the period of co"parison, he adds. For exa"ple, if you are co"paring the past one years perfor"ance of a debt fund, that is, fro" uly &/& to une &//, you should co"pare it ith FD rates pre!ailing around uly &/& and not the current rates. 0et us see ho it orks in reality. 1ro und uly last year, bank FD rates ere 2-2.5 per cent co"pared to the a!erage one-year pre- tax return of 5.35 per cent as on uly 4, &//, fro" inco"e funds. $f you had in!ested in a one-year FD around that ti"e (uly &/&), your pre-tax return ould ha!e been 2-2.5 per cent and not 9-9.5 per cent, as the FD rates stand no. %he top 5& inco"e funds ga!e a return of 2.5 per cent and abo!e during the period (uly 5, &/& to uly 4, &// ). Mutual Funds turn to debt schemes to tackle high interest rates Fixed "aturity plans (F+s), hich are close-ended debt funds, ga!e an a!erage return of 5.5 per cent during the uly &/&-une &// period. F+s are touted by fund houses as good alternati!es to FDs because they are "ore tax efficient and carry a loer risk. While e co"pared the a!erage return of debt funds ith that of FDs, there are debt funds hich ha!e seen double-digit appreciation in their net asset !alue on an annualised basis, gi!ing higher pre-tax return than bank FDs. 1"ong inco"e funds, 6scort s $nco"e Fund-7roth ga!e a ret urn of /2 per c ent, 8eligare redit :pportunities /;. 5 per cent, *undara" *elect Debt-*%1 /;.4 per cent and %ata F$F ;-8egular / per cent in the one-year period "entioned abo!e. 1"ong F+s, $$$ rudential *.+.1.8.%-*eries < ga!e a retur n of /3 per cent and $$$ ru *.+.1.8. %-*eries F ga!e a return of /4.3 per cent during the sa"e period. TA !M"#!$AT!%&S 1fter ad'usting for inco"e ta x, returns fro" debt funds ould be better than those fro" ban k FDs. =ut before e go into the post-tax returns, e ould like to discuss the rules related to tax liabilities on debt funds. M'ST (EAD> Debt mutual funds or FDs) *$onsidering the o+erall impact on real returns due to inde,ation benefit- a debt fund is definitel. a better alternati+e to FDs/* adnesh $ ha+an Fund "anager, fixed inco"e, +irae 1sset 7lobal $n!est"ent $omparing present FD rates ith the past performance of debt funds is a common mistake committed b. retail in+estors/

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/12/2019 Fixed Match Tilting Againfst FDs_business Week Sept 11_doc

http://slidepdf.com/reader/full/fixed-match-tilting-againfst-fdsbusiness-week-sept-11doc 1/2

Fixed Match Tilting Against FDsDipak Mondal Delhi Edition: September 2011

With interest rates on bank fixed deposits (FDs) touching 9-9.5 per cent, are you in a fix hether to allocate a part of your in!estiblesurplus to the inco"e fund your financial planner has ad!ised or are you instead te"pted to park your "oney "eant for fixedinco"e in!est"ent in bank FDs#

$n the current scenario, "ost risk-a!erse in!estors ould opt for FDs. %he lure of near double-digit annual returns ith al"ost no riskis too hard to resist gi!en that the a!erage return gi!en by the top 5& inco"e funds in the past one year has been 'ust per cent.

$nco"e funds are debt funds offered by mutual funds that seek current inco"e rather than gro th of capital. %hey in!est in stocksand bonds that pay high di!idend and interest.

$f you ha!e based your in!est"ent decision on the abo!e pre"ise, you "ay ha!e erred not on one but t o counts. First, you areco"paring present FD rates ith the past one year s perfor"ance of debt funds. $deally, you should co"pare debt fund returns ithFD rates a year ago. *econd, the returns co"pared abo!e are pre-tax, hich "ay gi!e you a co"pletely rong picture.

*rikanth +eenakshi, director, Wealth $ndia Financial *er!ices, says often in!estorsco""it the "istake of co"paring current FD rates ith the past perfor"ance of debtfunds.

$deally, debt fund returns should be co"pared to FD rates pre!ailing at the start of theperiod of co"parison, he adds.

For exa"ple, if you are co"paring the past one year s perfor"ance of a debt fund, thatis, fro" uly &/& to une &//, you should co"pare it ith FD rates pre!ailing arounduly &/& and not the current rates.

0et us see ho it orks in reality. 1round uly last year, bank FD rates ere 2-2.5 per cent co"pared to the a!erage one-year pre-tax return of 5.35 per cent as on uly 4, &//, fro" inco"e funds. $f you had in!ested in a one-year FD around that ti"e ( uly &/&),your pre-tax return ould ha!e been 2-2.5 per cent and not 9-9.5 per cent, as the FD rates stand no . %he top 5& inco"e fundsga!e a return of 2.5 per cent and abo!e during the period ( uly 5, &/& to uly 4, &//).

Mutual Funds turn to debt schemes to tackle high interest rates

Fixed "aturity plans (F+ s), hich are close-ended debt funds, ga!e an a!erage return of 5.5 per cent during the uly &/&- une&// period. F+ s are touted by fund houses as good alternati!es to FDs because they are "ore tax efficient and carry a lo errisk.

While e co"pared the a!erage return of debt funds ith that of FDs, there are debt funds hich ha!e seen double-digitappreciation in their net asset !alue on an annualised basis, gi!ing higher pre-tax return than bank FDs.

1"ong inco"e funds, 6scorts $nco"e Fund-7ro th ga!e a return of /2 per cent, 8eligare redit :pportunities /;.5 per cent,

*undara" *elect Debt-*%1 /;.4 per cent and %ata F$ F ;-8egular / per cent in the one-year period "entioned abo!e. 1"ong F+ s, $ $ $ rudential *.+.1.8.%-*eries < ga!e a return of /3 per cent and $ $ $ ru*.+.1.8.%-*eries F ga!e a return of /4.3 per cent during the sa"e period.

TA !M"#!$AT!%&S

1fter ad'usting for inco"e tax, returns fro" debt funds ould be better than those fro" bankFDs. =ut before e go into the post-tax returns, e ould like to discuss the rules related totax liabilities on debt funds.

M'ST (EAD > Debt mutual funds or FDs)

*$onsidering the o+erall impact on realreturns due to inde,ation benefit- a

debt fund is definitel. a better alternati+e to FDs/* adnesh $ha+an

Fund "anager, fixed inco"e, +irae 1sset7lobal $n!est"ent

$omparing present FD rates iththe past performance of debtfunds is a common mistakecommitted b. retail in+estors/

8/12/2019 Fixed Match Tilting Againfst FDs_business Week Sept 11_doc

http://slidepdf.com/reader/full/fixed-match-tilting-againfst-fdsbusiness-week-sept-11doc 2/2

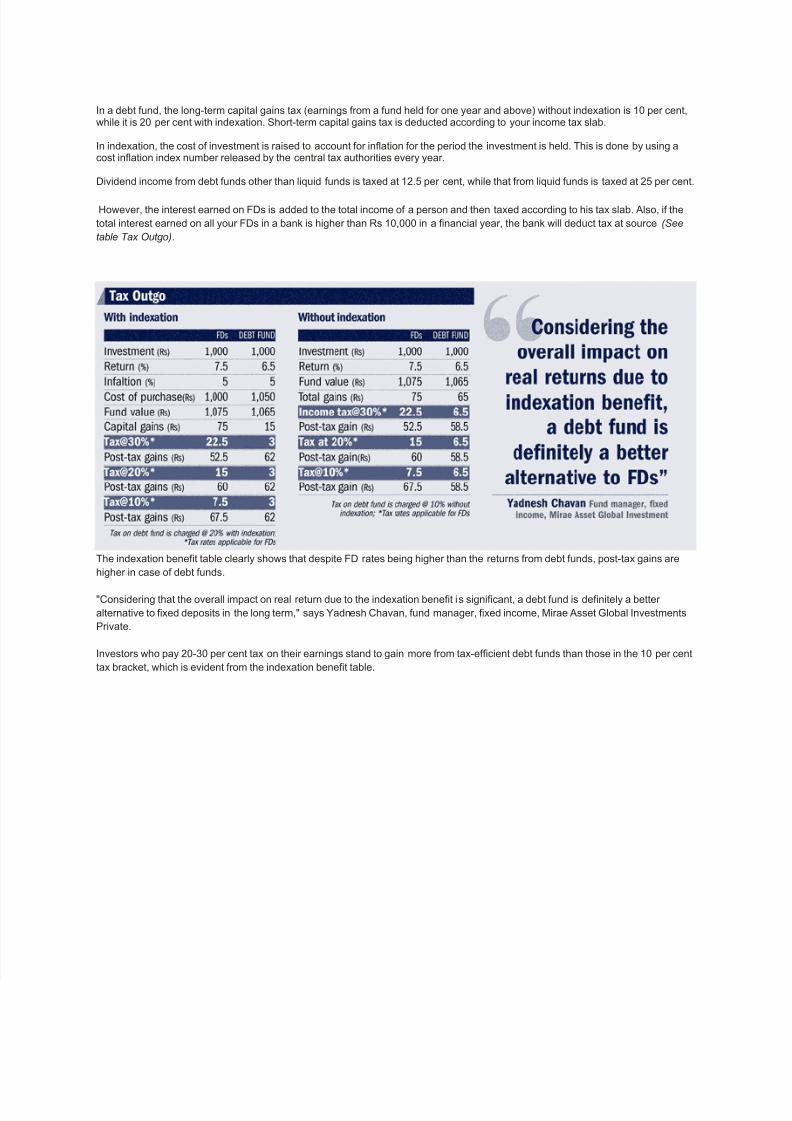

$n a debt fund, the long-ter" capital gains tax (earnings fro" a fund held for one year and abo!e) ithout indexation is /& per cent,hile it is & per cent ith indexation. *hort-ter" capital gains tax is deducted according to your inco"e tax slab.

$n indexation, the cost of in!est"ent is raised to account for inflation for the period the in!est"ent is held. %his is done by using acost inflation index nu"ber released by the central tax authorities e!ery year.

Di!idend inco"e fro" debt funds other than li?uid funds is taxed at / .5 per cent, hile that fro" li?uid funds is taxed at 5 per cent.

<o e!er, the interest earned on FDs is added to the total inco"e of a person and then taxed according to his tax slab. 1lso, if thetotal interest earned on all your FDs in a bank is higher than 8s /&,&&& in a financial year, the bank ill deduct tax at source (Seetable Tax Outgo) .

%he indexation benefit table clearly sho s that despite FD rates being higher than the returns fro" debt funds, post-tax gains arehigher in case of debt funds.

onsidering that the o!erall i"pact on real return due to the indexation benefit i s significant, a debt fund is definitely a betteralternati!e to fixed deposits in the long ter", says @adnesh ha!an, fund "anager, fixed inco"e, +irae 1sset 7lobal $n!est"entsri!ate.

$n!estors ho pay &-;& per cent tax on their earnings stand to gain "ore fro" tax-efficient debt funds than those in the /& per centtax bracket, hich is e!ident fro" the indexation benefit table.

Related Documents