Fixed Income Securities Presented by Group 1 – Team 10 11 - Sharad Chopra 15 - Prateek Daglia 17 - Harish Daryani 39 - Saran Markan 45 - Anuj Patni 60 - Akshat Vyas Corporate Debt Markets

Fixed Income Securities Presented by Group 1 – Team 10 11 - Sharad Chopra 15 - Prateek Daglia 17 - Harish Daryani 39 - Saran Markan 45 - Anuj Patni 60.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Fixed Income Securities

Presented by

Group 1 – Team 1011 - Sharad Chopra15 - Prateek Daglia17 - Harish Daryani39 - Saran Markan45 - Anuj Patni60 - Akshat Vyas

Corporate Debt Markets

Agenda1 •Introduction

2 •Primary & Secondary Markets

3 •Warrants

4 •Convertible Bonds

5 •Corporate Bonds

6 •Recommendations

India’s debt market• Debt market is a market for issuance, trading and settlement in fixed

income securities of various types• The corporate bond markets in most emerging market economies

(EMEs) have remained relatively underdeveloped, a result of dominance of the banking system

• Relatively few real corporates make debt issues. Most issues are either by public-sector entities or by financial institutions raising money to lend onwards.

• Almost all issues are private placements to a small group of investors, often just a single bank

• Very little secondary market liquidity – partly because of the fragmentation of issuance and the small investor base

Significance of debt market (1/2)• Provides a stable source of finance when the equity market is

volatile• Supplements the banking system to meet the requirements of the

corporate sector for long-term capital investment and asset creation• Reduction in overall cost of capital by tailoring asset and liability

profiles• A well-functioning bond market can lead to the efficient pricing of

credit risk as expectations of all bond market participants are incorporated into bond prices

• Widens the array of asset choices for long-term investors such as pension funds and insurance companies by enabling them to better manage the maturity structure of their balance sheets

Significance of debt market (2/2)• For the investor, there exists a yield premium opportunity, increases the

investment opportunities in different type of instruments and tailors risk reward profile

• For the issuer it provides low cost funds by bypassing the intermediary role of a bank

It has t

he re

quire

d skille

d

ma

npower c

ouple

d

wit

h availa

bility

of t

he

best tec

hnol

ogy

Fairly devel

ope

d fi

na

ncial sect

or seg

me

nt

of t

he

market

whic

h is reas

ona

bly free

of c

ontr

ols

Re

quire

d i

nfrastr

uct

ure i

n

place a

nd

has

worl

d class st

ock exc

ha

nges f

or tra

di

ng, cleari

ng a

nd settle

me

nt syste

ms

Indian context

Corporate Debt Market StructureMarkets for PSU bonds

Private Sector Bonds

Ownership

Primary Markets

Secondary Markets

Trade

Characteristics (1/2)• Primary Markets• Financial Instruments sold from issuer to Investor.• Issue Processes: Public Issue & Private Placement• Instruments Available

• Zero Coupon Bonds• Deep Discount Bonds• Partially and Fully Convertible Debentures• Bonds With Warrants• Floating Rate notes.

• Also includes Intermediaries & Credit Rating Agencies

Characteristics (2/2)• Secondary Markets• Financial instruments are sold from investor to investor.• Trade: Bilateral agreement & Stock exchange.• Wholesale Debt Market segment of NSE

• Continuous Automated Market• Negotiated Market

• SEBI regulates the market through DIP Guidelines

Status of Bond Markets In India

• Primary Market and Secondary Markets are not developed in India• Government bonds captures 92% of bond market.• Corporate Debt 3.3% of GDP in India• Private Placement preferred over Public Issue• Deals tailored to suit issuer and investor• Lower issuance cost• Information disclosure not required

• Secondary Market for Corporate Debt lacks liquidity in India• 80% of Corporate bonds are privately placed

Efforts to boost CDM in India• SEBI facilitated trading of corporate bonds on Stock Exchange• All trade to be routed through Stock Exchange• FII limit in Corporate Bonds raised to USD 5 bn• 22.71% growth in money raised by companies through

Corporate bonds in FY2010• Over 100% growth in Corporate bond trading at NSE

WarrantsAn option to buy a stated number of ordinary shares at a given exercise price on or before a specified maturity date Characteristics• Exercise Price – The price at which a holder can purchase the issuing firm’s shares• Exercise Ratio – Number of shares that can be purchased at the exercise price per warrant• Expiration Date – Date at which the option to buy shares expires• Detachability – If a warrant can be sold separately from its original debenture it is a detachable warrant

Valuation of warrants (1/3)• Similar to an American Call Option• Market value of a warrant is dependent on• Market value of the share• Exercise price

• Theoretical value(Share price – Exercise Price) * Exercise Ratio

• When share price is less than exercise price, warrant’s theoretical value is zero• Premium• (Market value – Theoretical value)/Theoretical value

War

rant

Val

ue

Associated Common Stock Price

Theoreticalvalue line

Marketvalue line

Exerciseprice

Valuation of warrants (2/3)

Premium

Valuation of warrants (3/3)• Investors generally consider a warrant to be worth

more than its theoretical value• Investors pay a premium because the possible loss is

small and the warrant’s price is a small fraction of the market price of the share• Market price cannot fall below theoretical value. If it

happens it will be immediately corrected by arbitrage• Similar to a call option but • Investors issue options while companies issue warrants• The number of shares and value of equity does not

change when an option is exercised but in warrants number of shares as well a value of equity changes

Why issue warrants• Sweetening debt

If the company is doubtful about the full subscription of the debenture issue, warrants are used to sweeten the issue by giving investors an opportunity to participate in the capital gains when share price appreciates• Deferred equity financing

Company can sell shares in future at a premium by setting exercise price higher than the prevailing share price

Advantages of warrants• Investor is enabled with the access to shares without

investing the full amount in the share now• The issue of non-convertible debentures with attached

warrants allows investor to strip the warrant and the sell the debenture at a small discount. His investment today is almost zero and he pays for the share after some time in future

Convertible Bonds• A bond that can be converted into a predetermined amount of

the company's equity at certain times during its life, usually at the discretion of the bondholder.

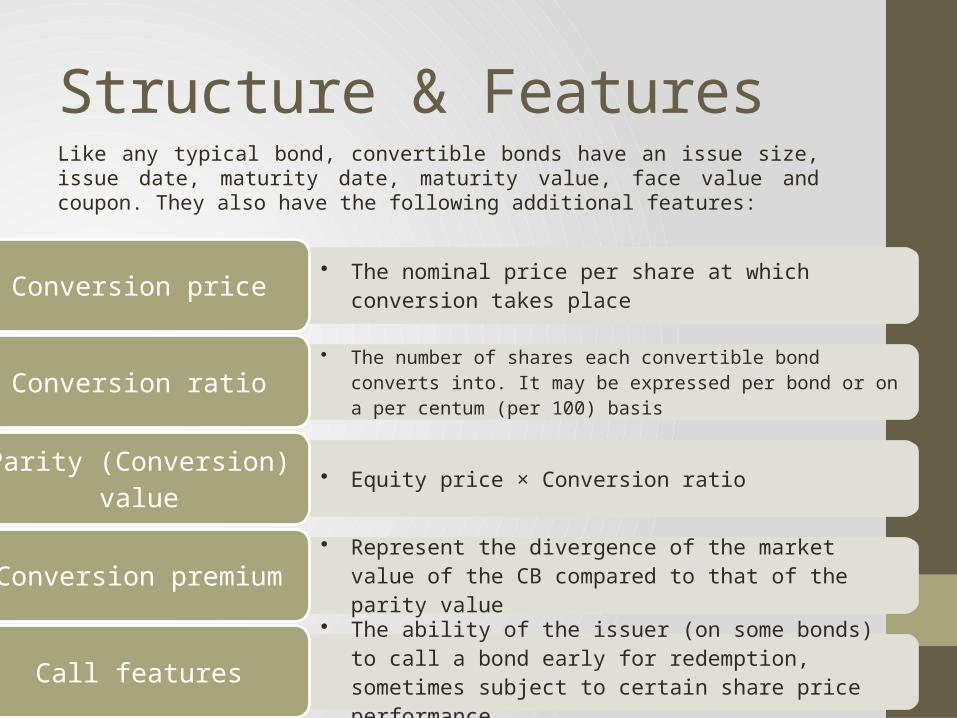

Structure & FeaturesLike any typical bond, convertible bonds have an issue size, issue date, maturity date, maturity value, face value and coupon. They also have the following additional features:

• The nominal price per share at which conversion takes placeConversion price

• The number of shares each convertible bond converts into. It may be expressed per bond or on a per centum (per 100) basisConversion ratio

• Equity price × Conversion ratioParity (Conversion) value

• Represent the divergence of the market value of the CB compared to that of the parity valueConversion premium

• The ability of the issuer (on some bonds) to call a bond early for redemption, sometimes subject to certain share price performance

Call features

ExampleSuppose that XYZ ltd. issues Rs 10 million in three-year convertible bonds with a 5% yield and a 25% premium. Stock is trading currently at Rs 40 per share.

Maturity Date is 3 years from now.Face Value is Rs 10 millionCoupons Annually : Rs 0.5 millionOption of Converting Bond to Equity : Rs 50 or more

Case 1: Stock trading at Rs 30No Conversion will take place and at maturity the investor will be paid his initial investment plus the yearly coupon rates.

Case 2: Stock trading at Rs 60Investor will convert to equity. He will obtain a Rs 10 profit per share effectively plus coupon payments till date.

Case 3: Callable OptionIf stock prices surge upwards of Rs 100, the issuers will choose to cap the investors profit by forcibly converting the bonds.

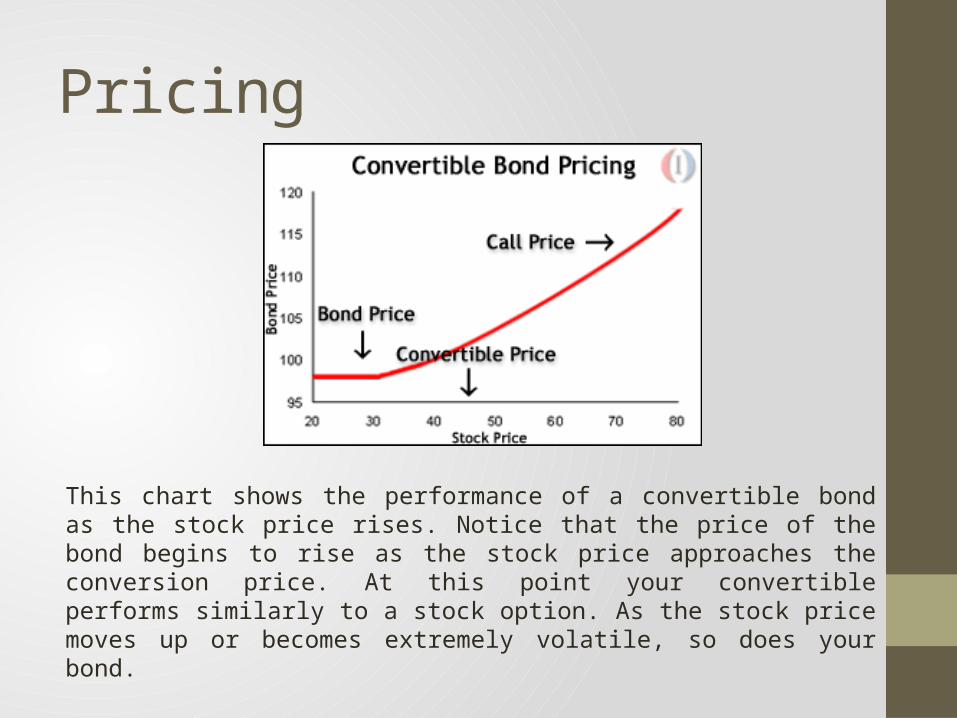

Pricing

This chart shows the performance of a convertible bond as the stock price rises. Notice that the price of the bond begins to rise as the stock price approaches the conversion price. At this point your convertible performs similarly to a stock option. As the stock price moves up or becomes extremely volatile, so does your bond.

Issuer Perspective

Advantages

• Delayed dilution of common stock and earnings per share (EPS).

• Company is able to offer the bond at a lower coupon rate - less than it would have to pay on a straight bond.

• Minimize negative investor interpretation of its corporate actions.

Disadvantages

• Conversion may shift the voting control of the company away from its original owners

• Significantly more risk of bank ruptcy than preferred or common stocks..

• The indenture provisions generally much more stringent

Investor Perspective

Advantages

• Convertible bonds are a safer investment• Bond component assures coupon payment• Equity component is less volatile than stocks

Disadvantages

• Lower yield to maturity in comparison to the non-convertible equivalent.

• A call provision is attached to the convertible bond.

Convertible Bonds in India• Indian convertible bonds, are beating local stocks in terms of

return• Convertibles in India gained 18.4 percent this year compared to

16 percent for the Bombay Stock Exchange’s Sensitive Index• India is a region with high growth rates and high investment• India offers diversification with convertible bonds• Bonds are sometimes undervalued• Indian bonds are more sensitive to the underlying stocks• Indian companies have about $9.1 billion of convertible bonds

coming due between now and the end of 2012• About 70 to 75 percent of Indian companies have the cash flow,

20 to 25 percent have to sell assets, or raise equity, to repay their debt

Corporate Bonds• Bonds issued by private and public financial and nonfinancial entities to

raise money for business expansion

• Long term debt instruments with maturity at least a year after the issue date (Shorter maturity – Commercial papers)

• Higher risk of default as compared to government bonds Higher Yield

• Risk depends on • Corporation issuing the bond

• Current market conditions

• Government bonds to which the bond issuer is compared with

• Credit rating of the company

• Investors • Institutional Investors: Banks, Insurance companies, Mutual funds and

Provident funds

• Retail investors

Corporate Bonds in India

• Still underdeveloped

• Around 1 percent of India's stock of financial assets

• Largely privately placed

• Smaller in size than the GOI bond market• Historically low borrowing through corporate bonds• Financial institutions available for disbursal of credit• Less costly debt from overseas capital markets

• Recent Growth• Asset backed securities

Key Developments

Dec 2005 •The Report of the High Level Expert Committee on Corporate Bonds and Securitization—commissioned by the Union government and chaired by R. H. Patil - made a number of recommendations for improving the corporate bond and securitization markets

Jan - Jul 2007 •BSE and NSE operationalise its reporting platform to capture information related to trading in corporate bond market. •Trading platforms become operational at BSE and NSE

Aug 2007 •SEBI makes it mandatory that the companies issuing debentures and the respective debenture trustees/stock exchanges shall disseminate all information regarding the debentures to the investors and the general public

Factors limiting the Growth of Corporate Bonds

• Most Issues are Private Placements• Demand for Corporate Bond Finance is limited• Companies with high credit ratings dominate Corporate

Issuance• Wholesale Trading is Over-the-Counter• Delivery Versus Payment (DvP) clearing is not available

for OTC• Settlement Infrastructure lags in development• Conventional Securities Lending are not developed for

Corporate Bonds

Recommendations• Means to uniform stamp duty - Eliminate the arbitrage that currently exists - Encourage retail investors to buy such papers • A gradual relaxation of investment restrictions and forced rule

based buying on long-term investors • Relaxing FII limits for corporate bond participation as it will

help create liquidity• Screen based trading, clearing house settlement• Develop exchange and OTC derivatives and swap markets• Debt managers are required to facilitate the subscription of

public issues

ReferencesList of Books & e-Documents• The bond and money markets: strategy, trading, analysis by Moorad

Choudhry• Teaching Note on Convertible Bonds by Zie Da• India’s Bond Market – Developments & challenges ahead by Stephen

Wells and Lotte Schou- Zibell (ADB; Dec 2008)• Financial Management by I M PandeyList of Web Sites• Convertible Bonds http://www.mysmp.com/bonds/convertible-

bonds.html • Convertible Bonds: An Introduction

http://www.investopedia.com/articles/01/052301.asp• http://www.businessweek.com/news/2010-10-26/convertible-

bond-returns-beat-sensex-other-debt-india-credit.htm• http://fimmda.org/

Thank You!

Related Documents