Volume IV 2012–2013 Latin America High Yield Comprehensive Analysis of ‘B+’ Issuers and Below

Fitch Latin America High Yield 2012-2013

Oct 30, 2014

Comprehensive analysis of ‘B+’ Issuers and below by Fitch

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Volume IV 2012–2013

Latin America High Yield Comprehensive Analysis of ‘B+’ Issuers and Below

Latin America High Yield

November 8, 2012

Corporates

Table of Contents

Executive Summary .................................................. 1

Latin America Non-Financial Institutions Corporate

Financial Statistics ................................................ 11

AES Andres Dominicana, Ltd. .................................. 14

Alto Palermo S.A. (APSA) ........................................ 19

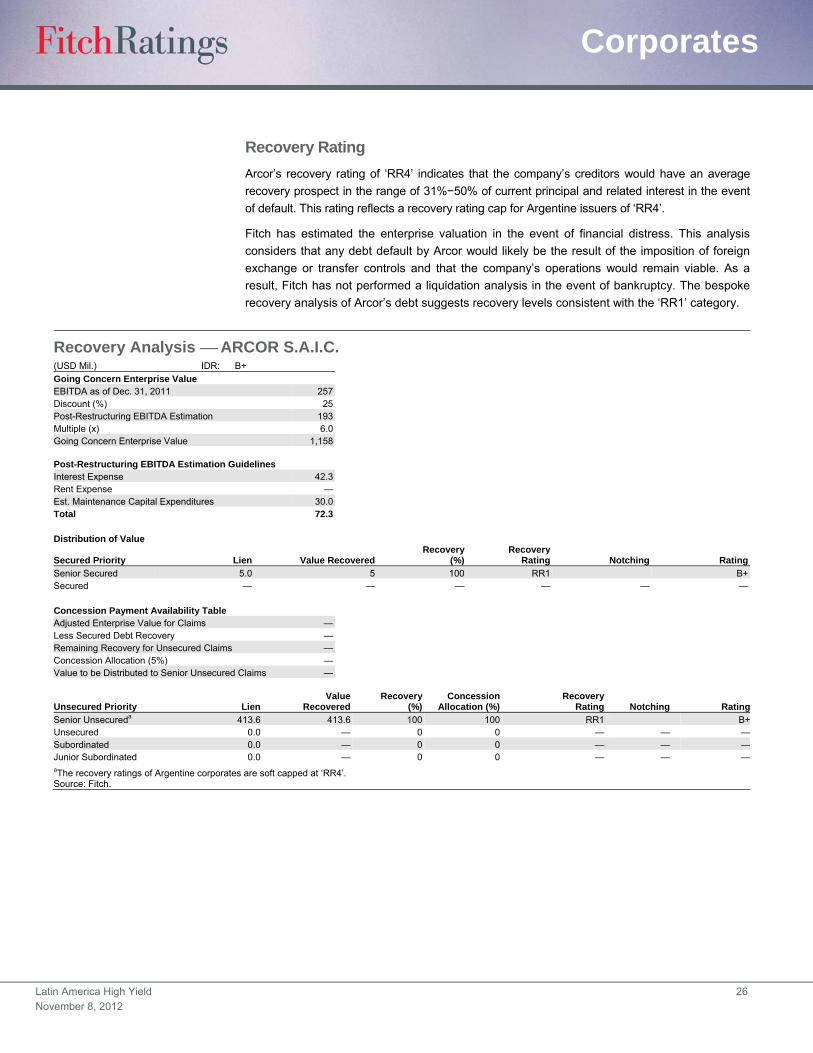

Arcor S.A.I.C. ............................................................ 25

Arendal, S. de R.L. de C.V. ...................................... 31

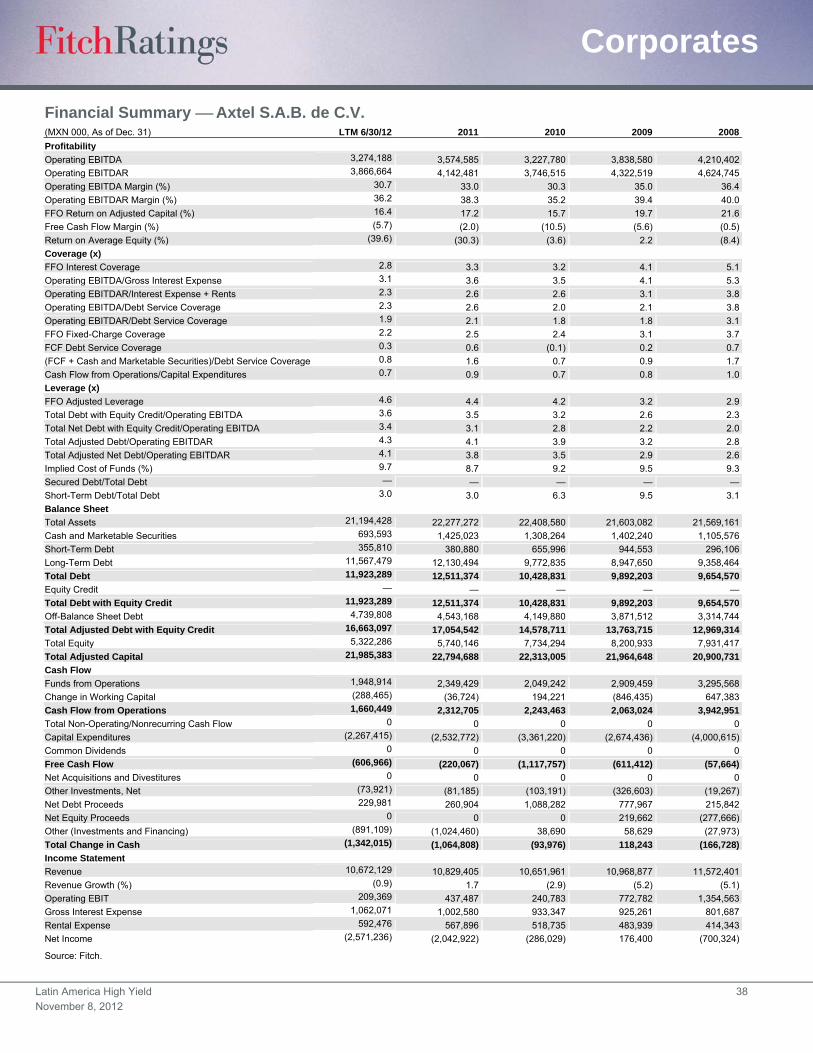

Axtel, S.A.B. de C.V. ................................................. 33

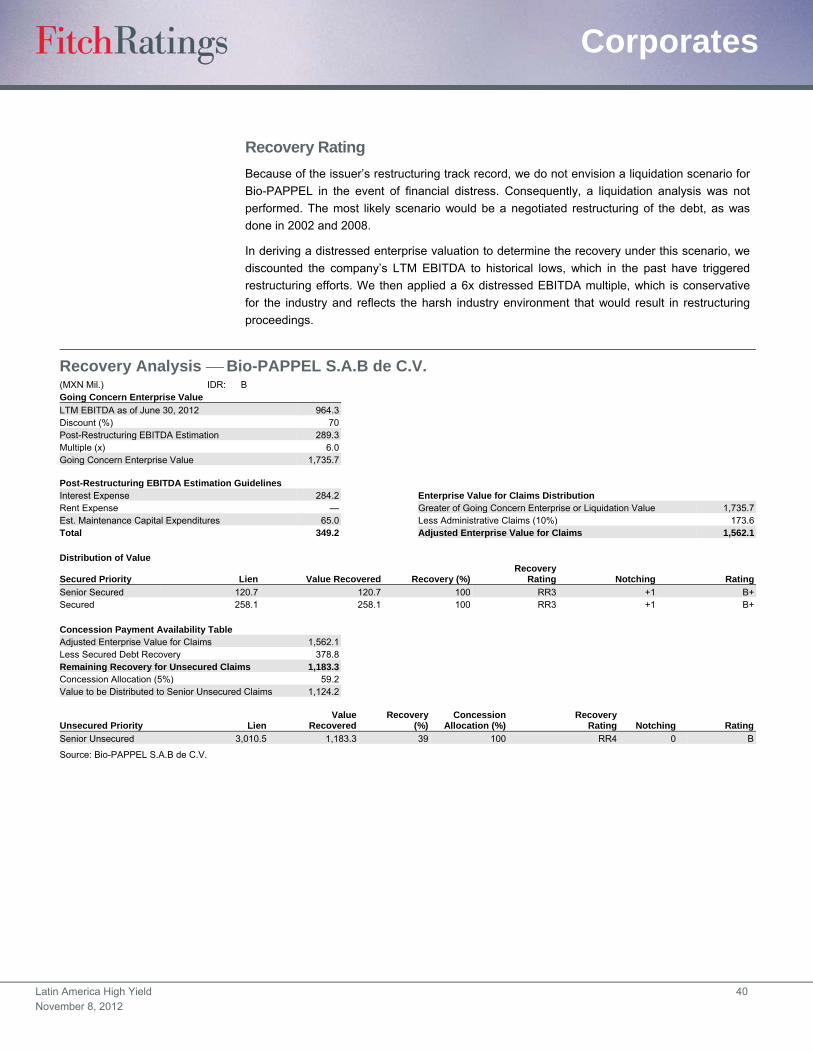

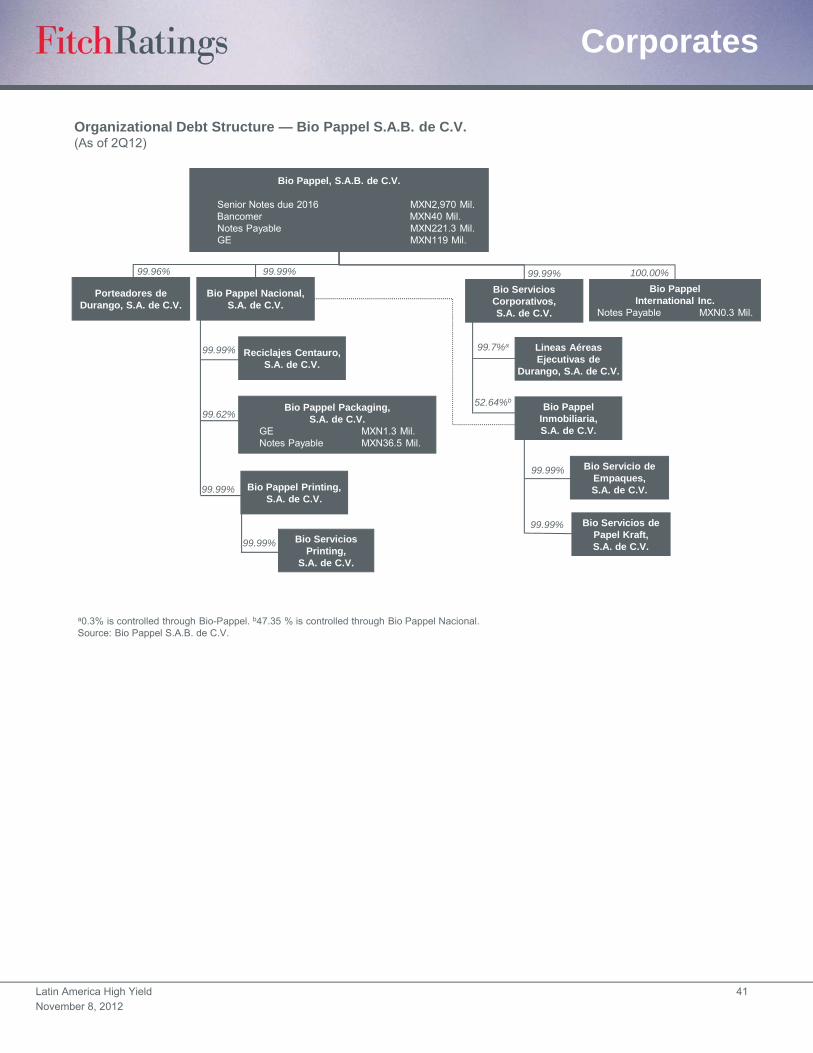

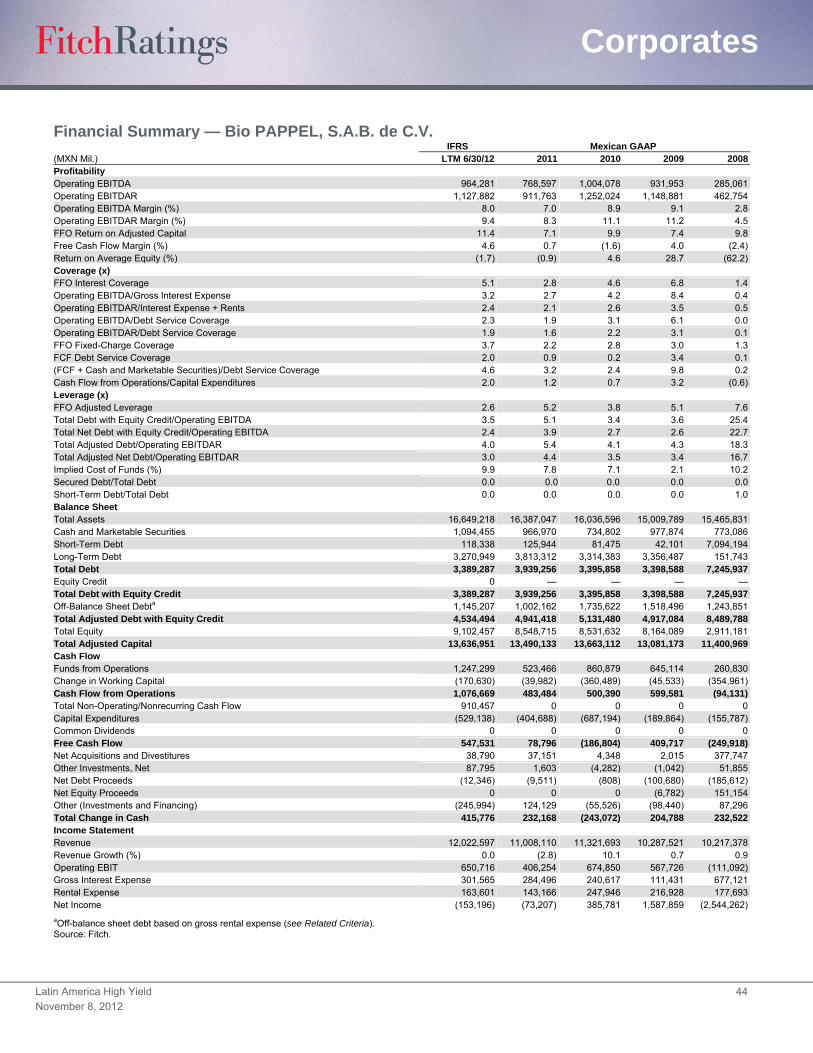

Bio-PAPPEL, S.A.B. de C.V. .................................... 39

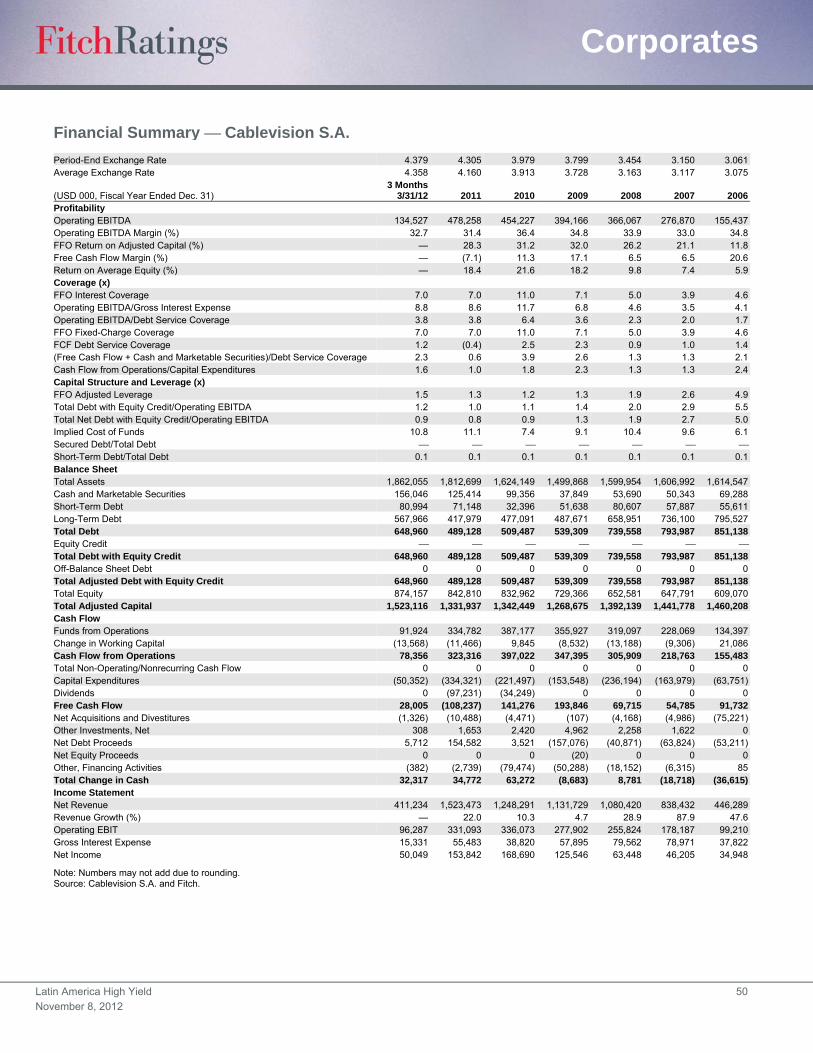

Cablevision S.A. ....................................................... 45

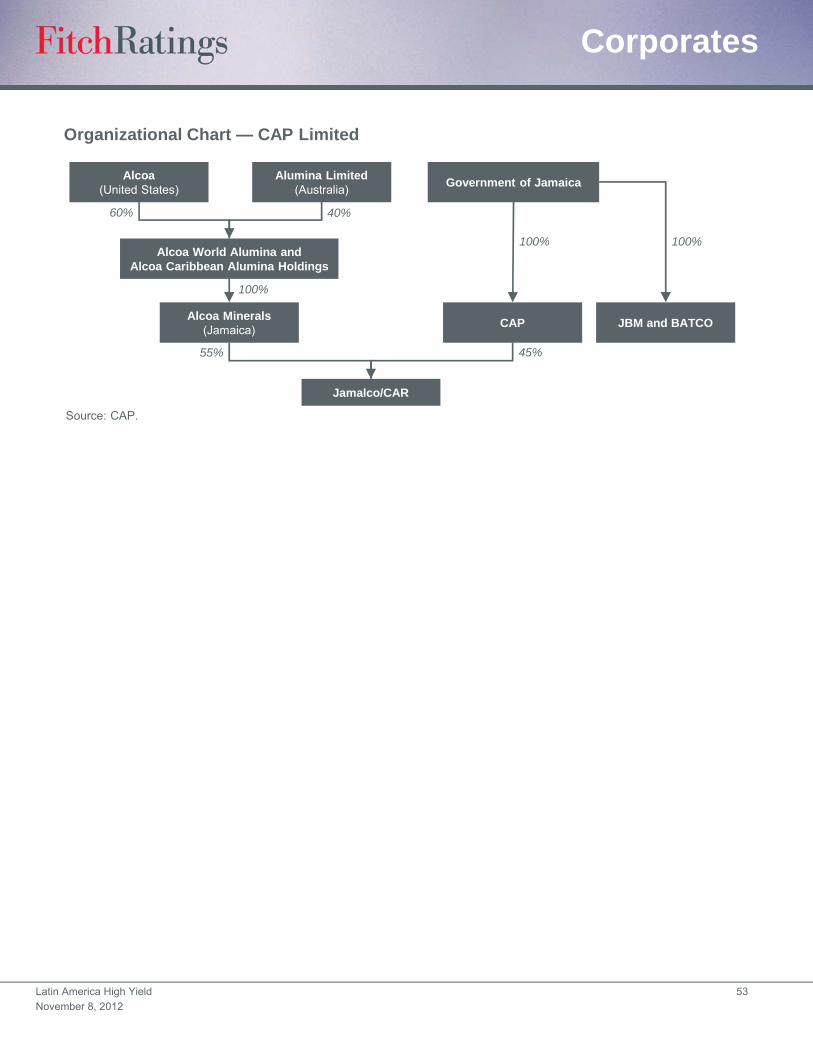

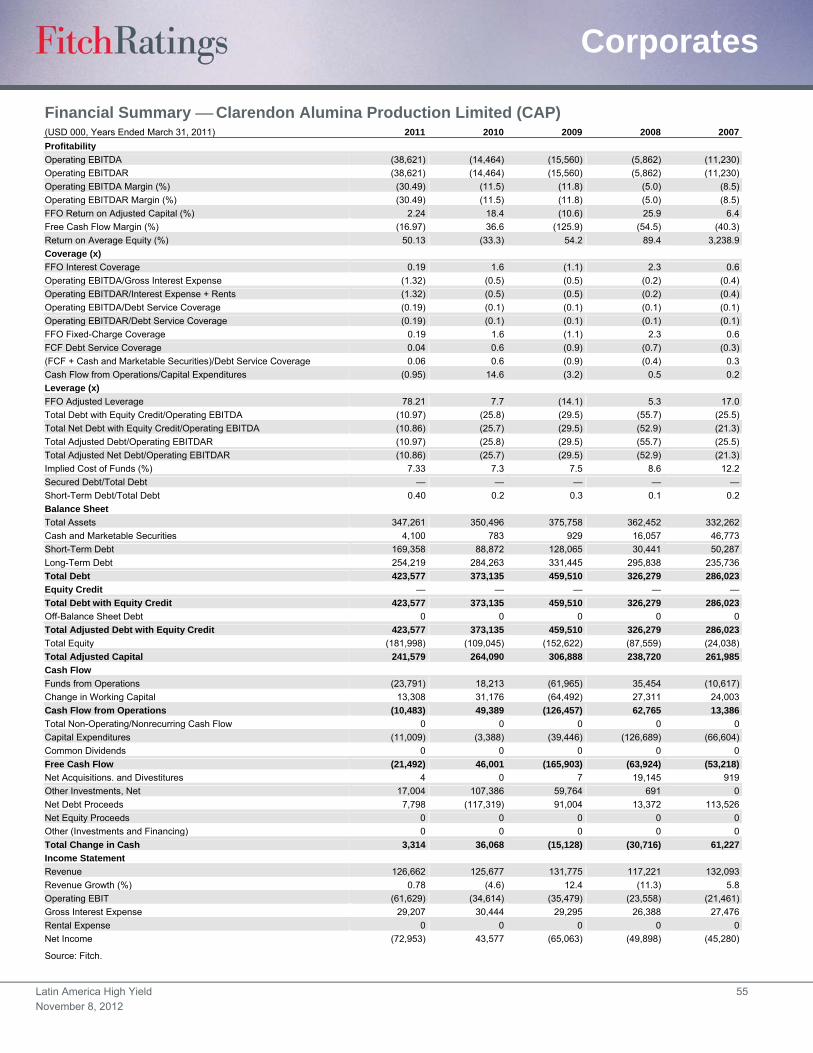

CAP Limited .............................................................. 51

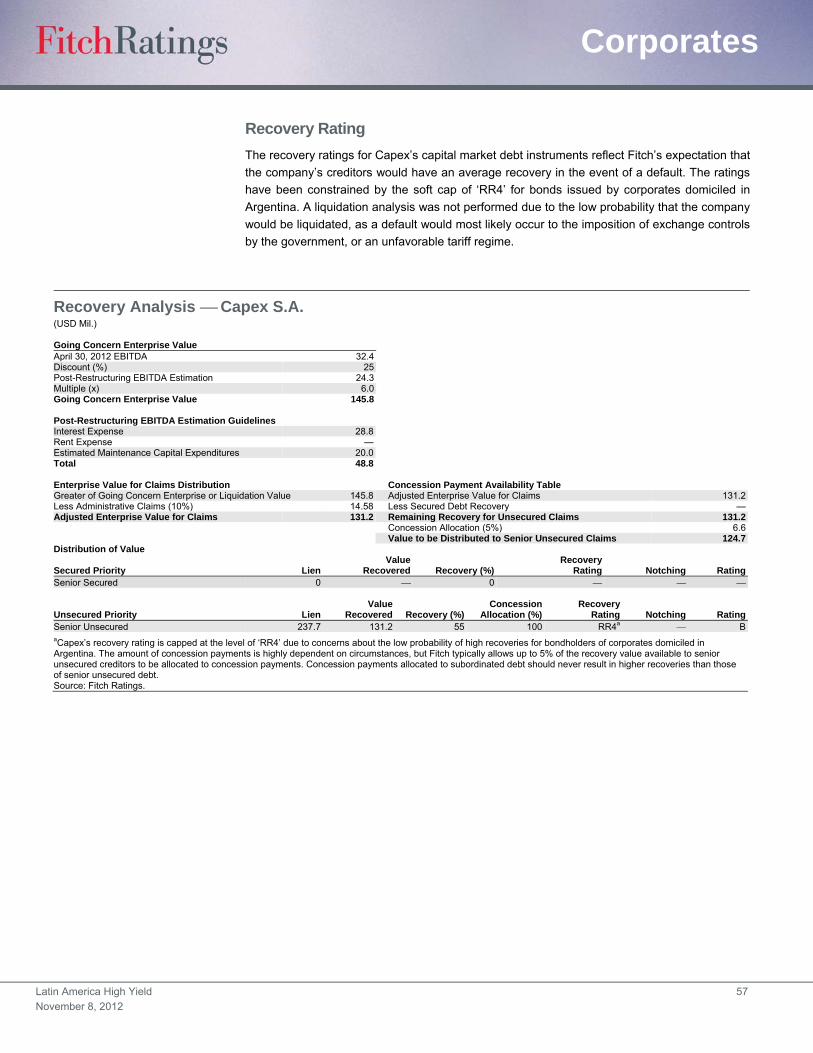

Capex S.A. ............................................................... 56

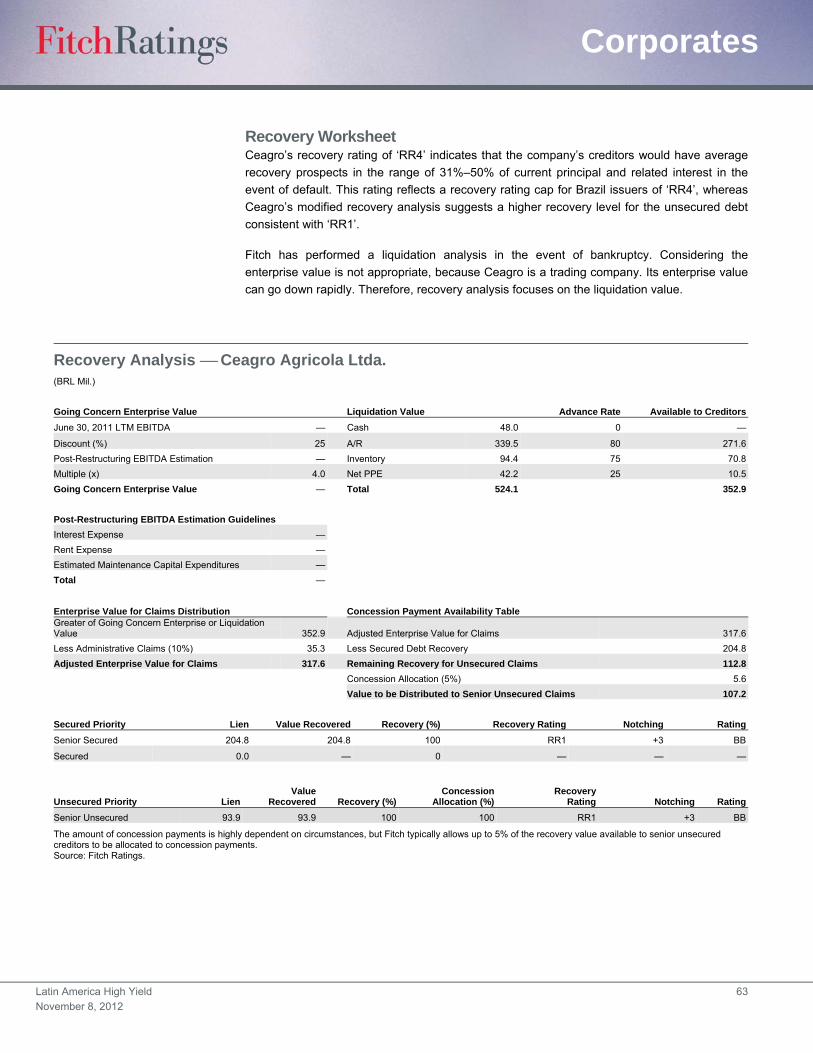

Ceagro Agricola S.A. ................................................ 62

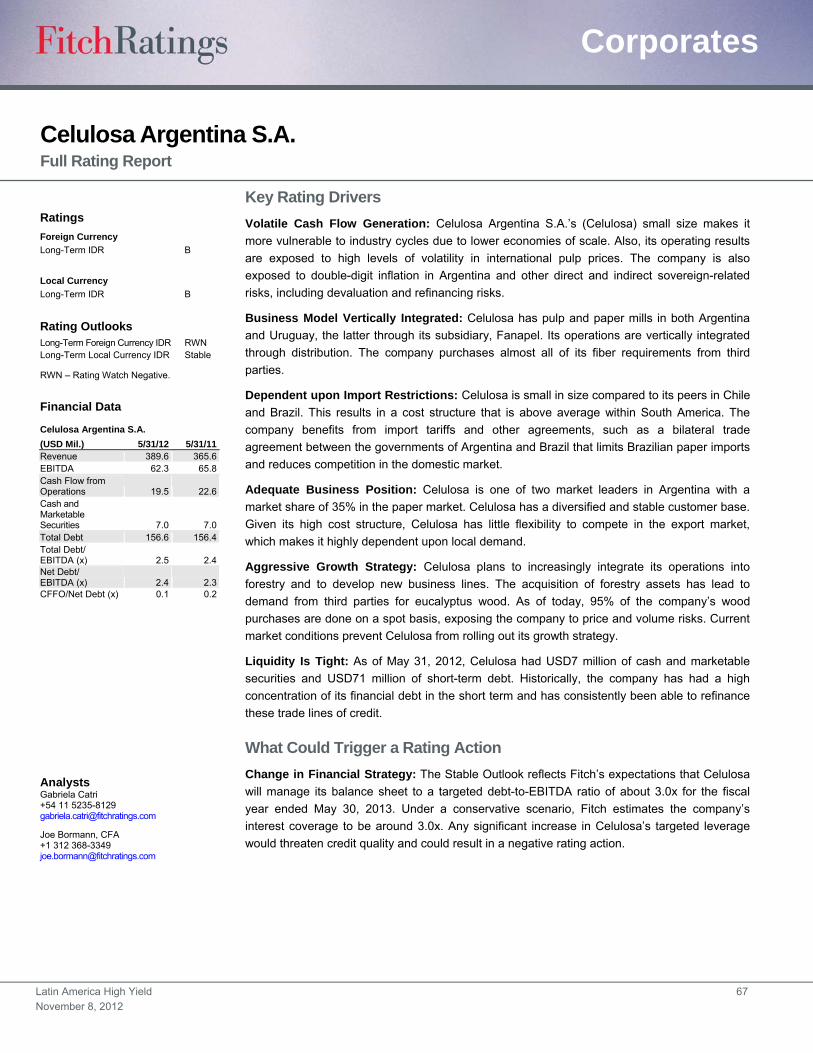

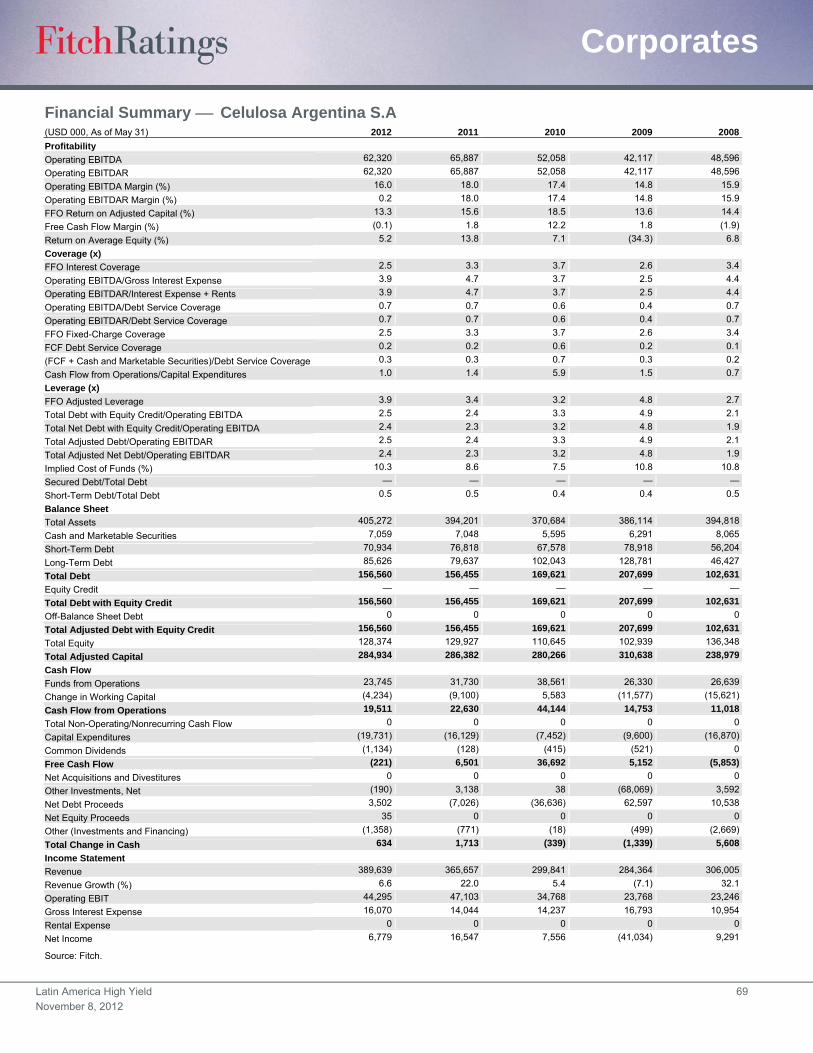

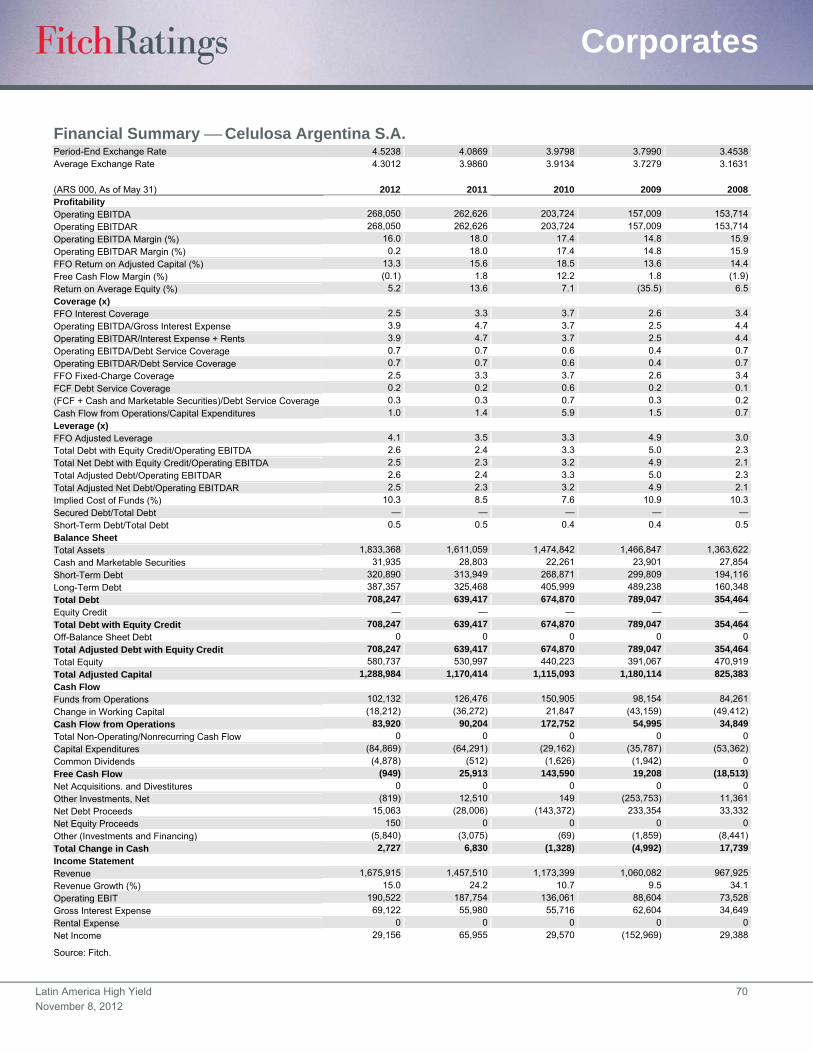

Celulosa Argentina Ltda. .......................................... 67

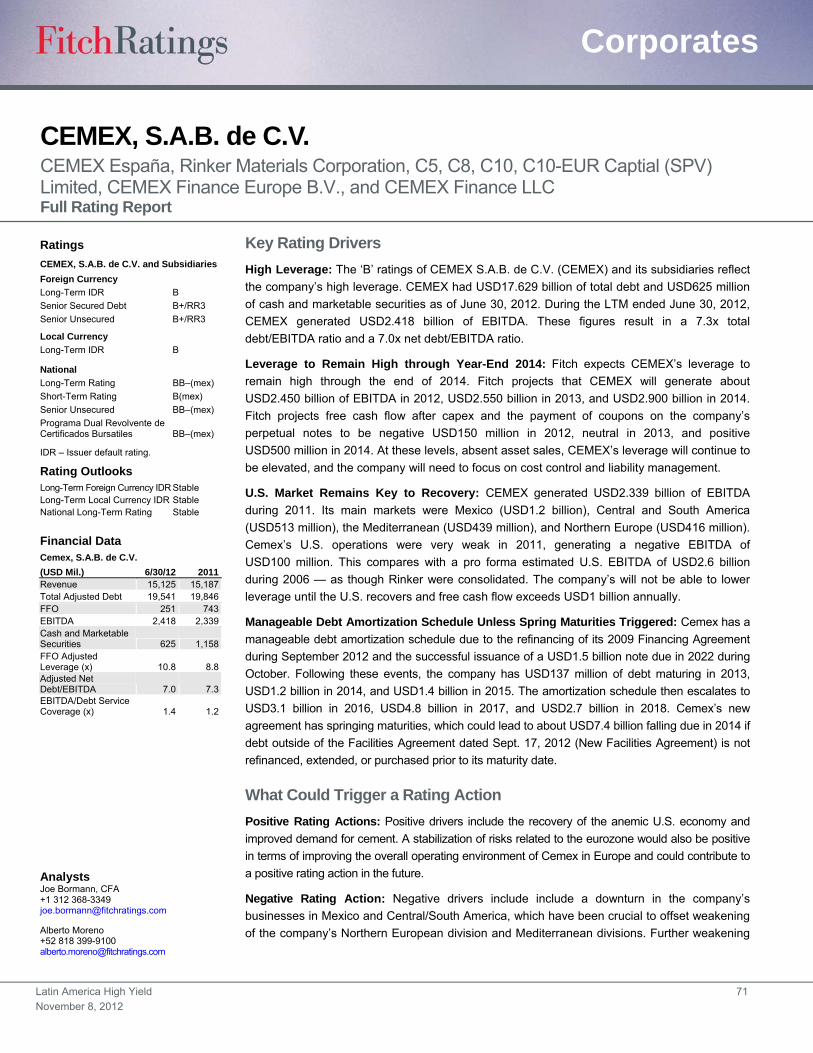

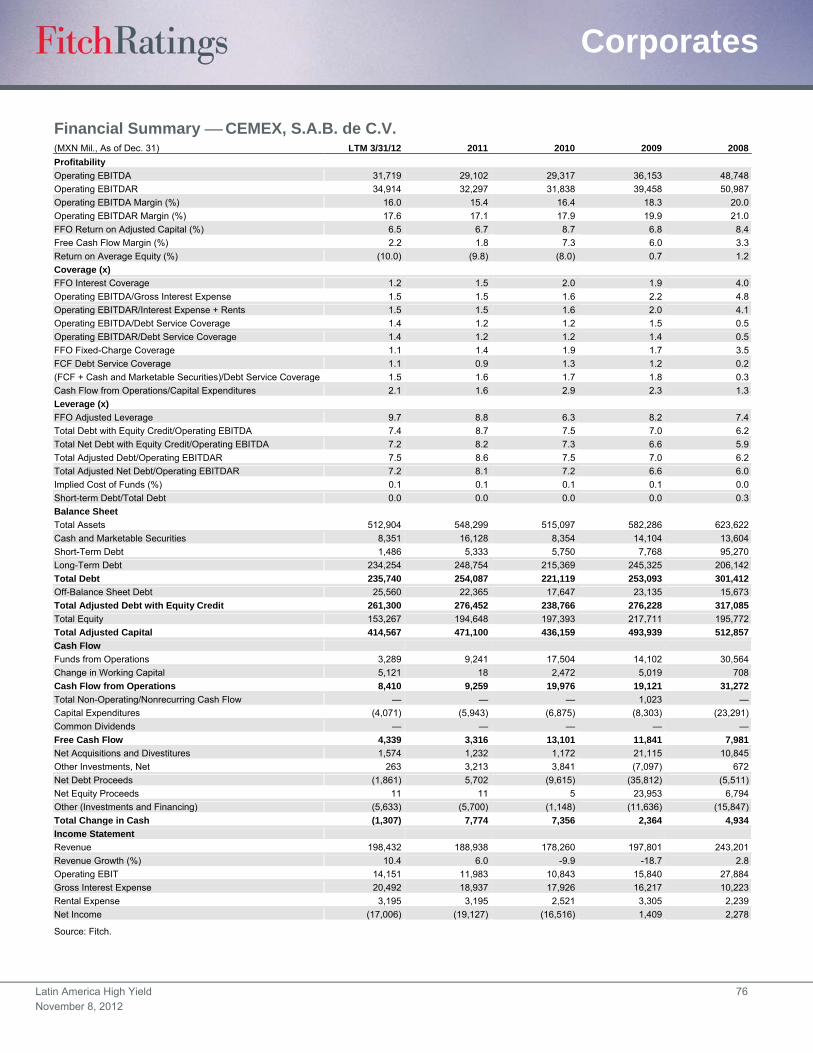

CEMEX, S.A.B. de C.V. ............................................ 71

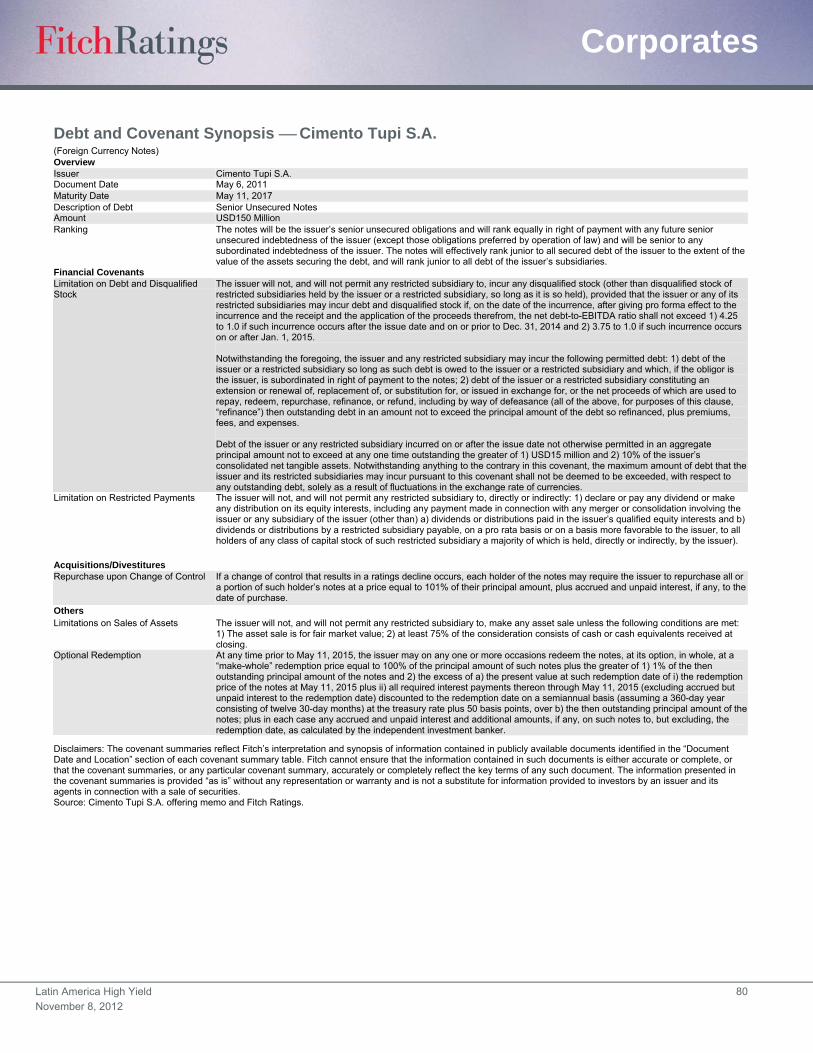

Cimento Tupi S.A. ..................................................... 77

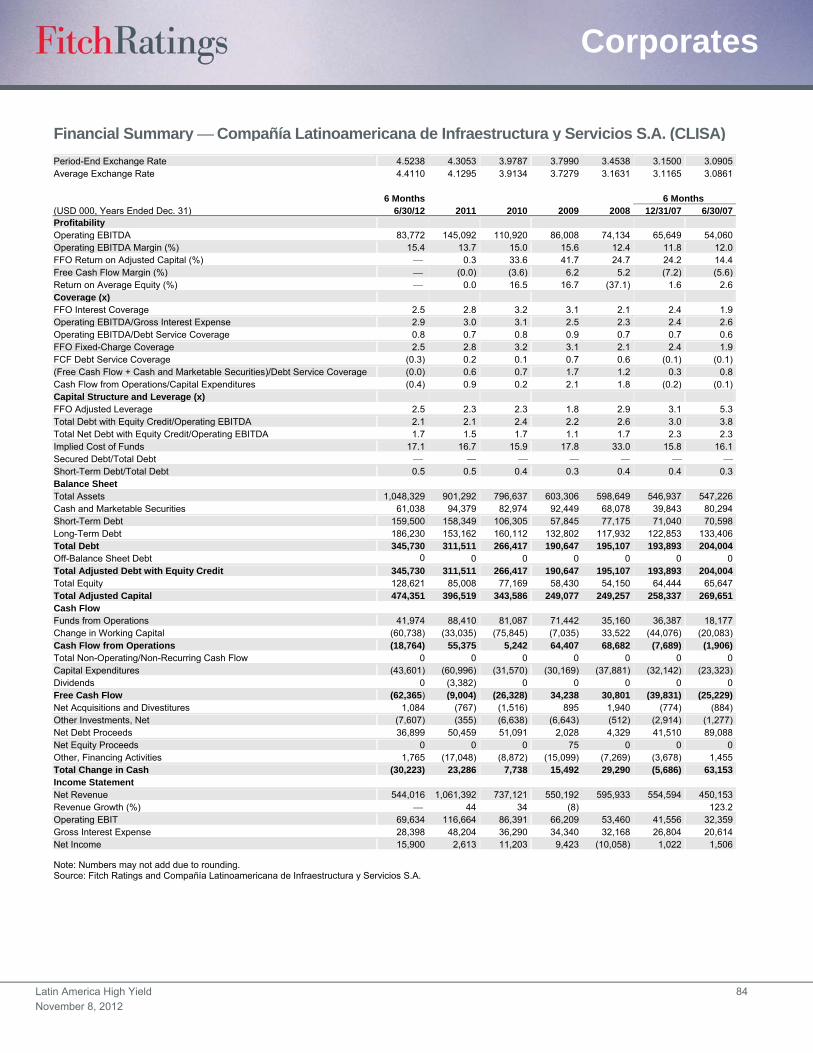

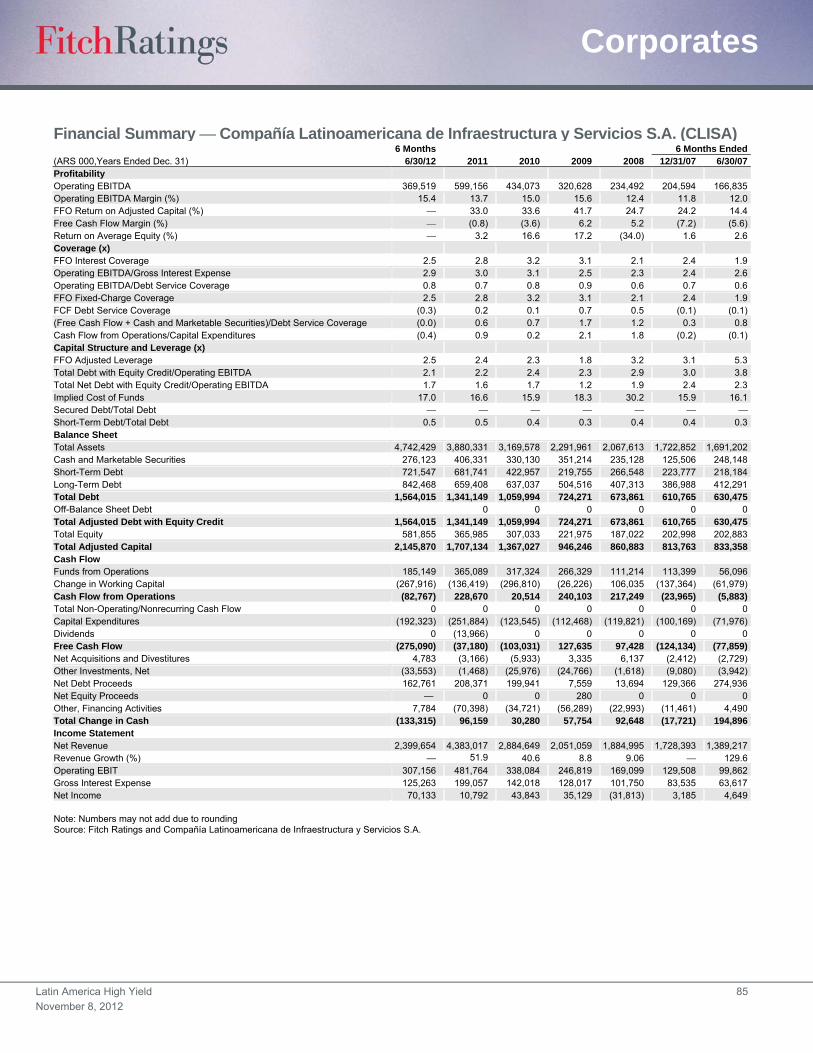

CLISA Compania Latinoamericana de

Infraestructura y Servicios ..................................... 82

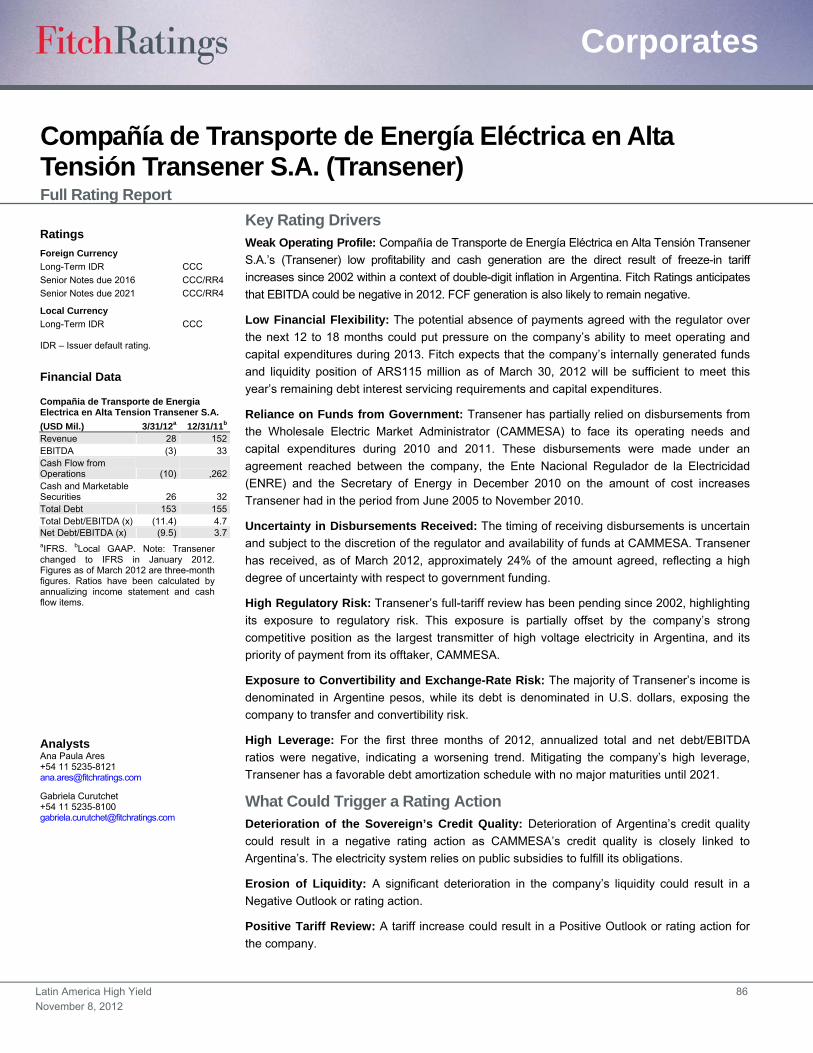

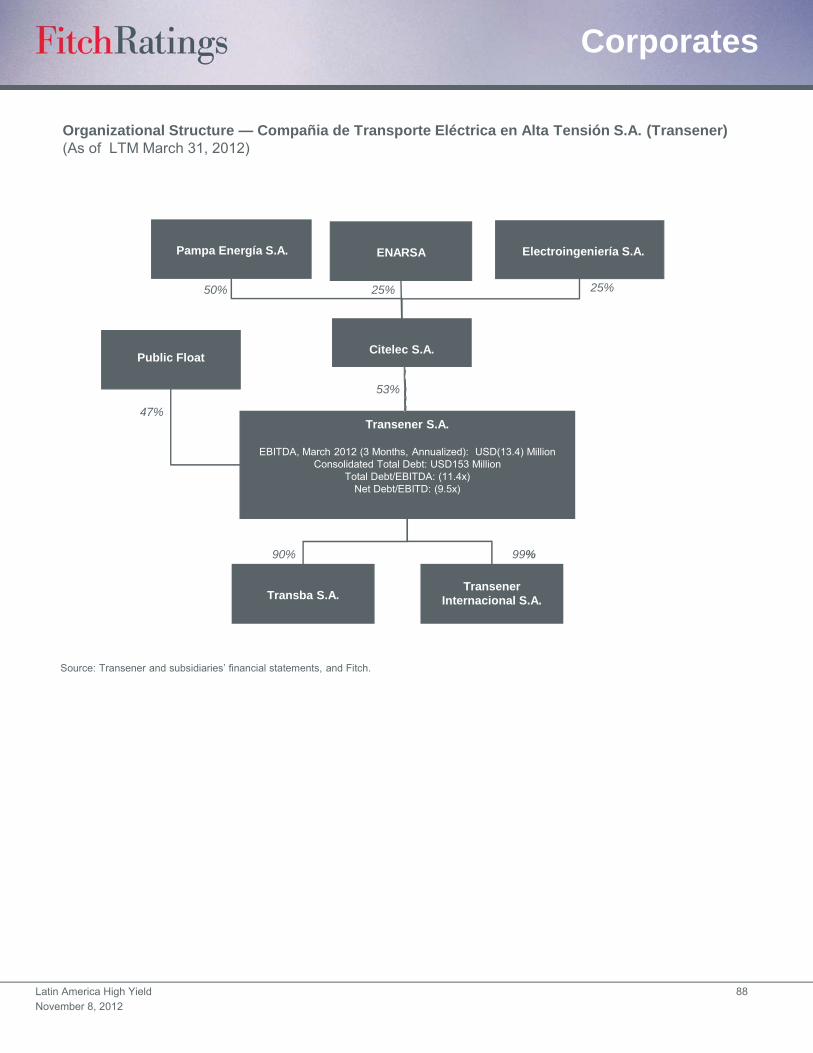

Compañía de Transporte de Energía Eléctrica en Alta

Tensión Transener S.A. (Transener) ..................... 86

Corporacion Electrica Nacional S.A.

(CORPOELEC) .............................................. 92

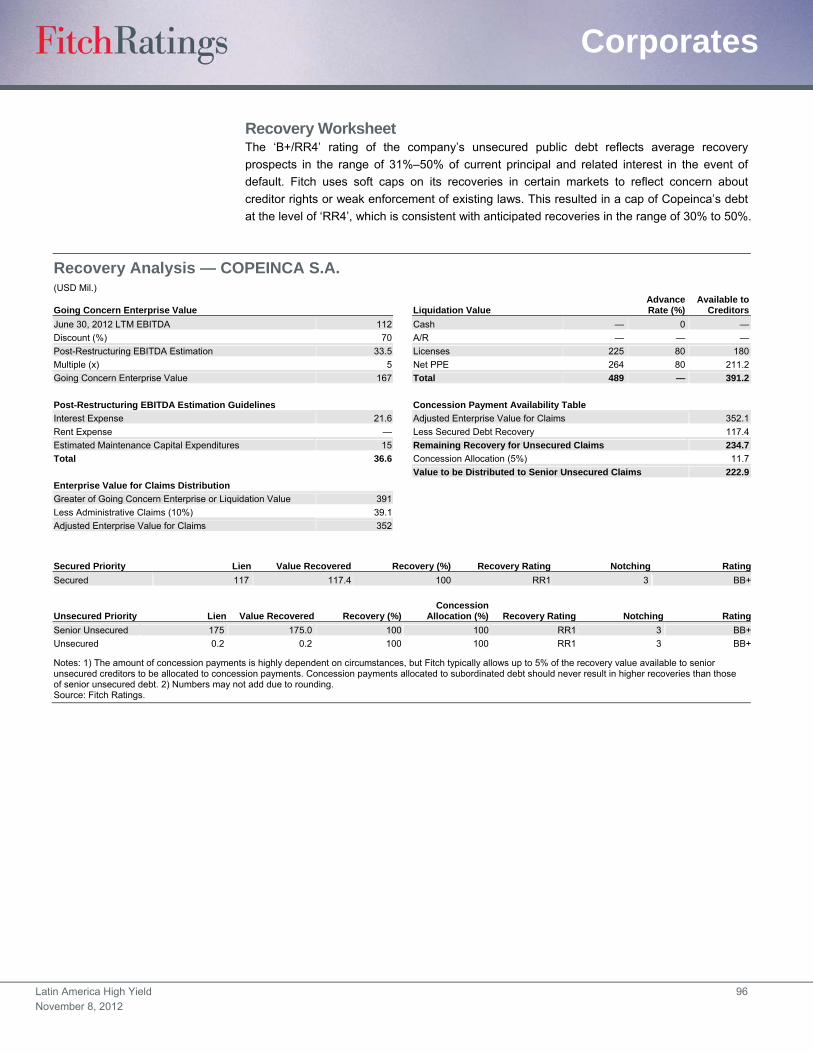

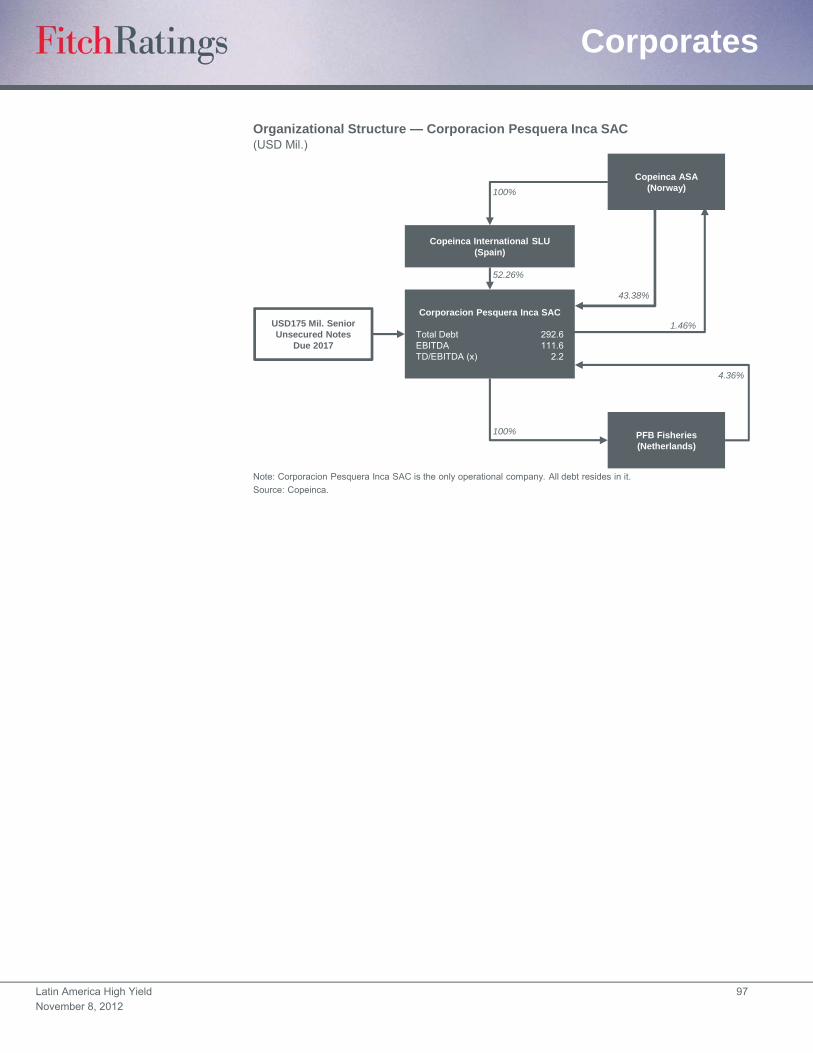

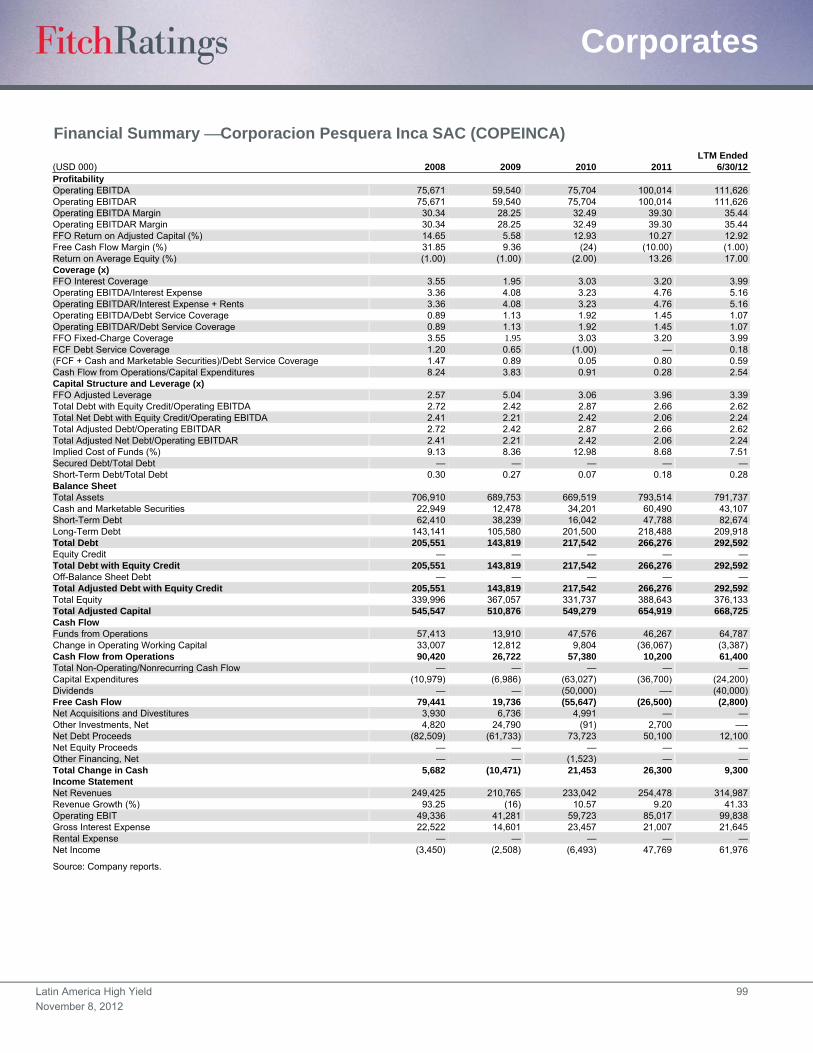

Corporacion Pesquera Inca SAC .............................. 95

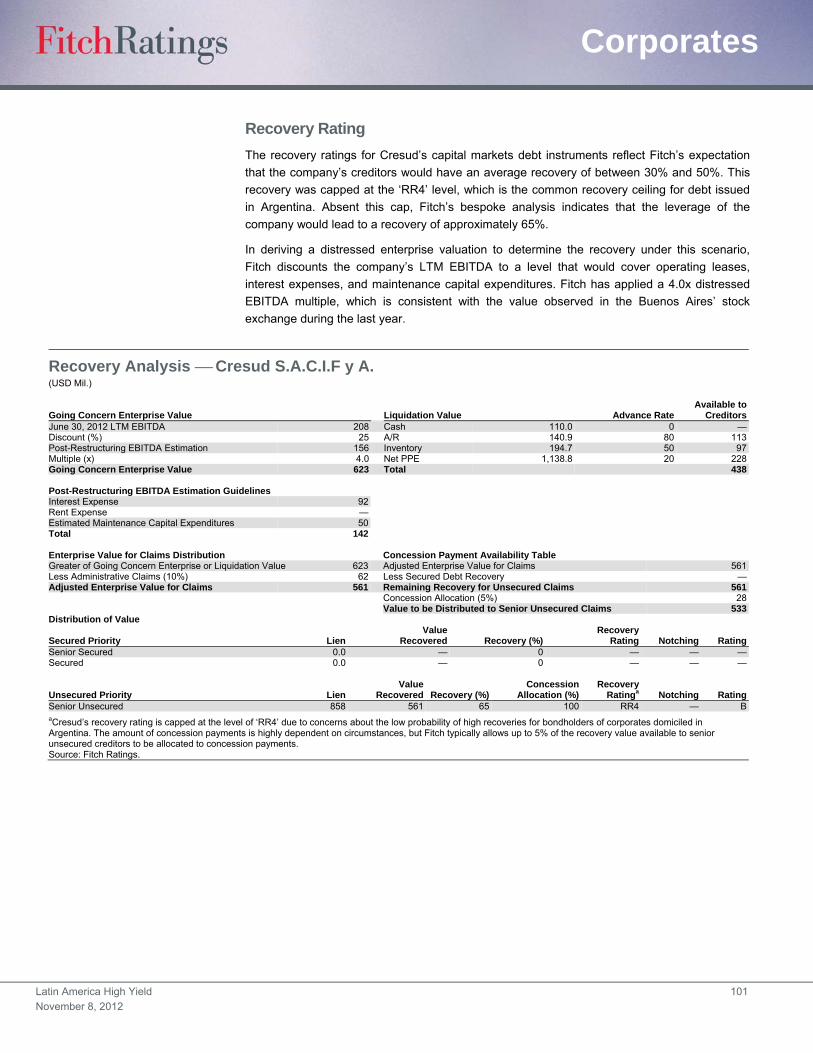

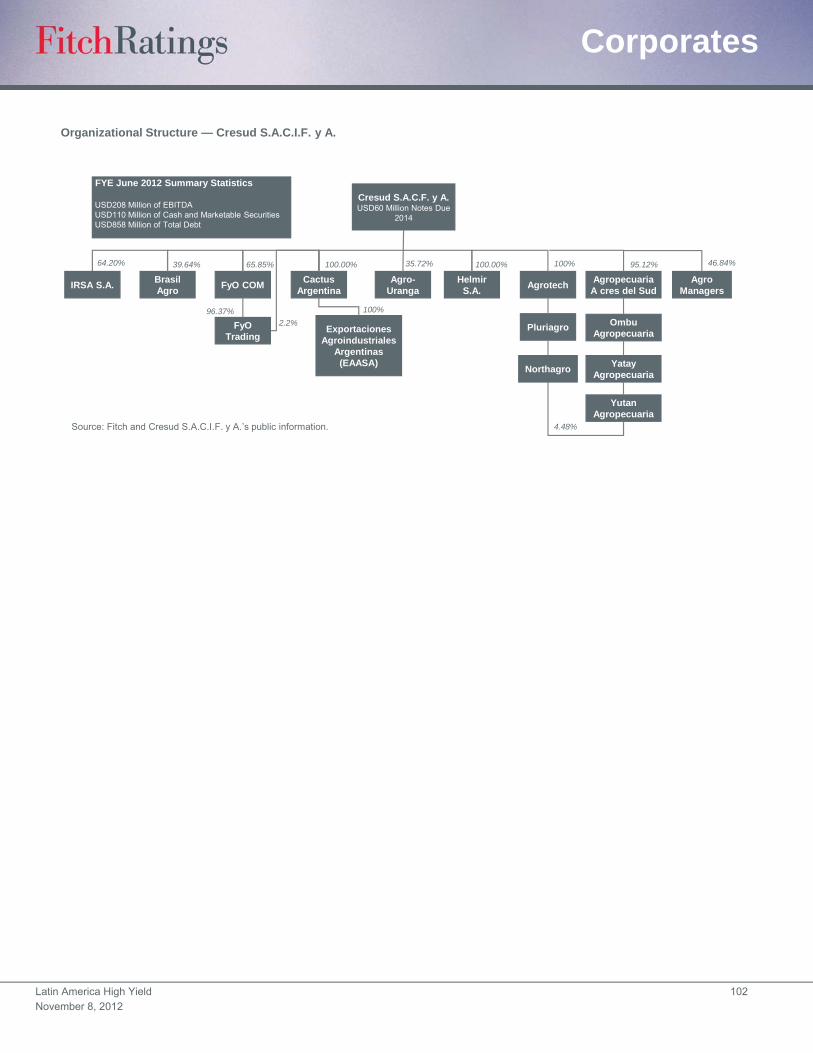

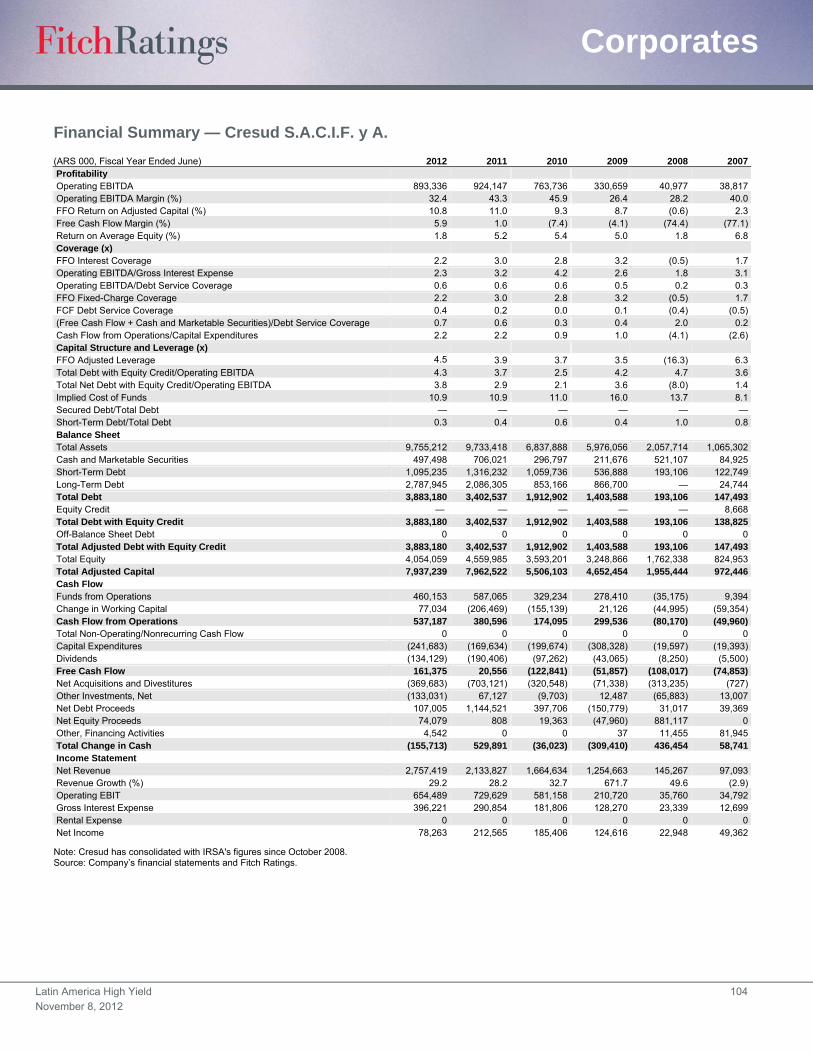

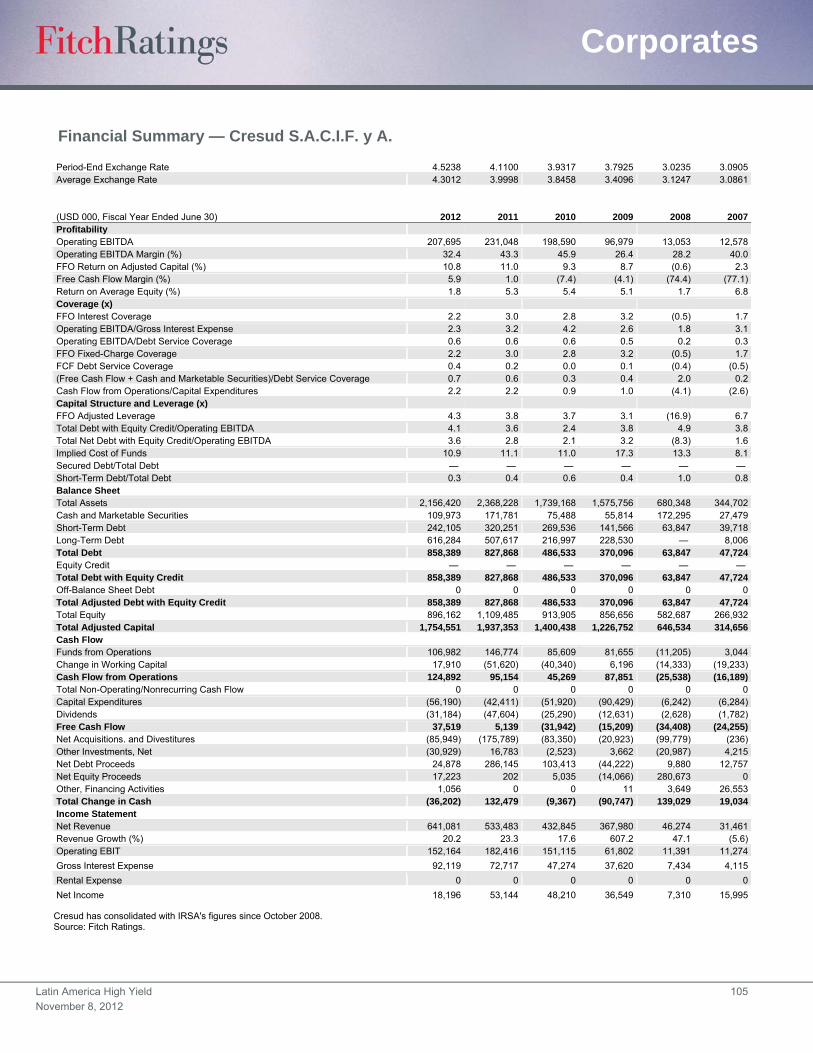

Cresud S.A.C.I.F. y A. .............................................. 100

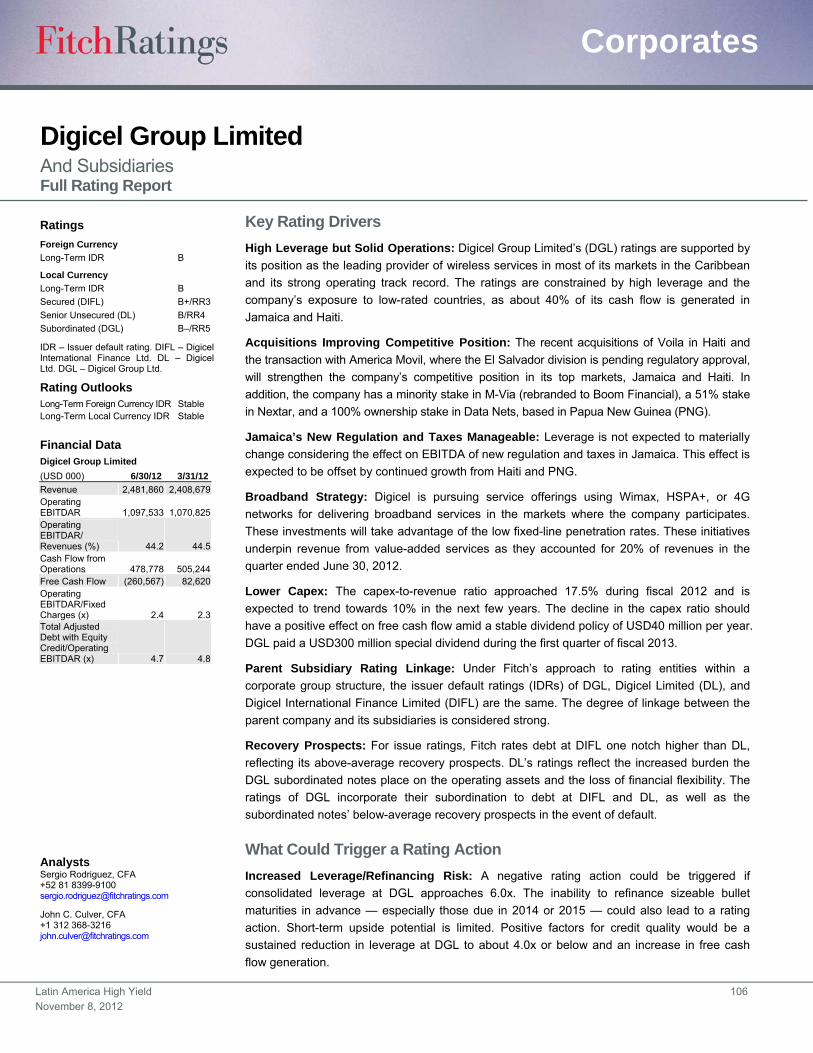

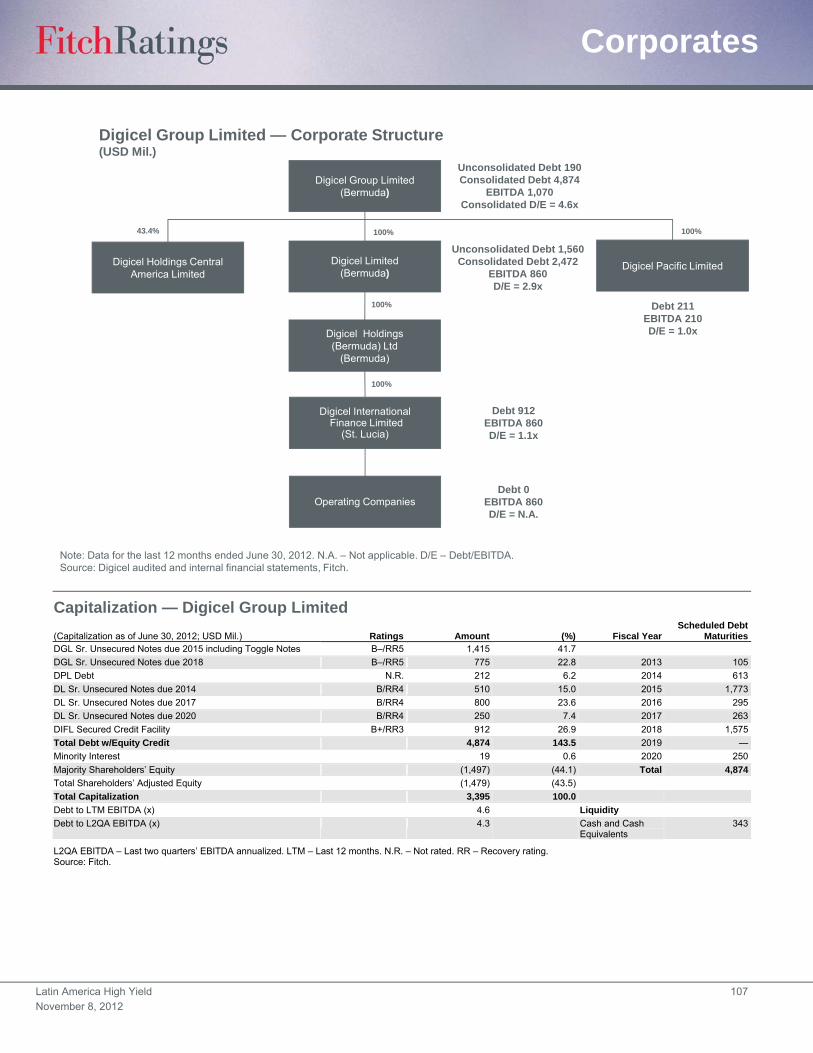

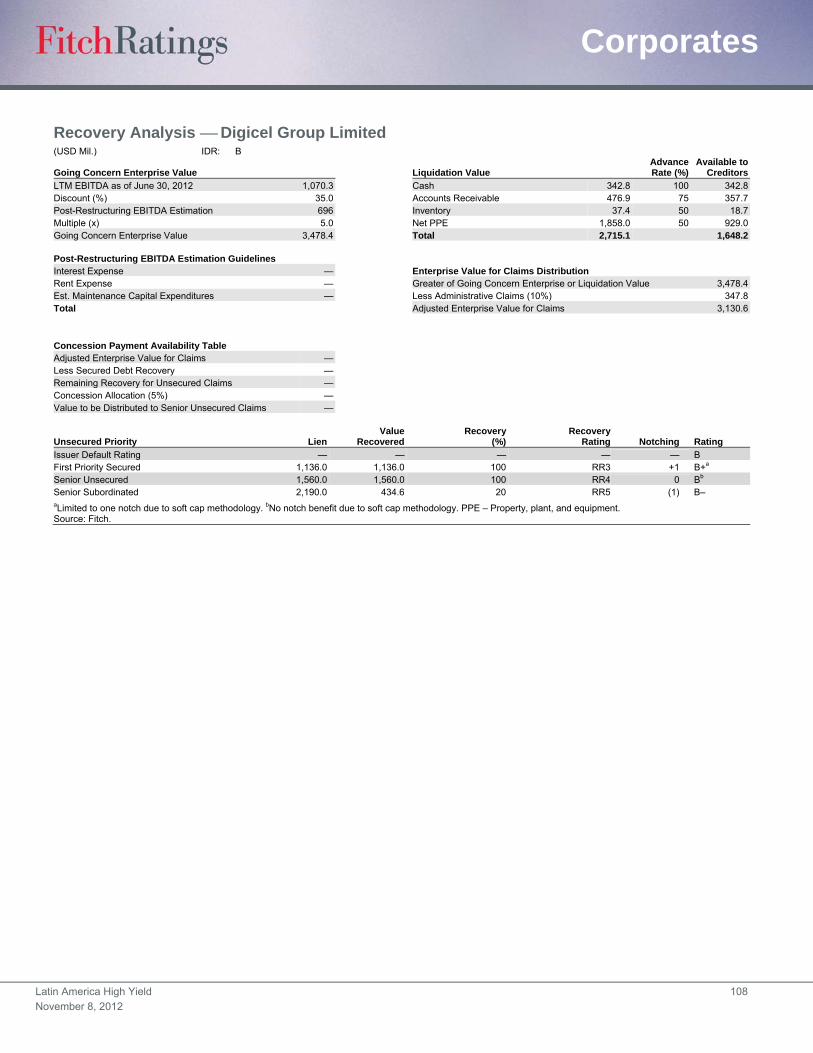

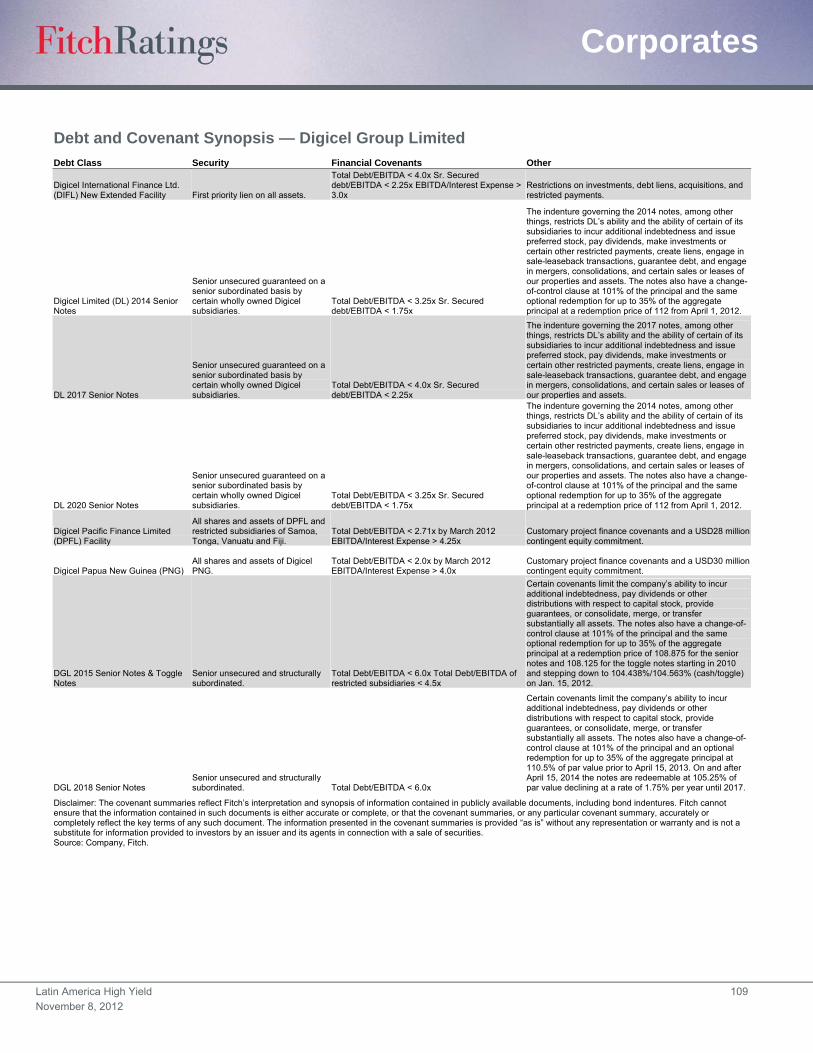

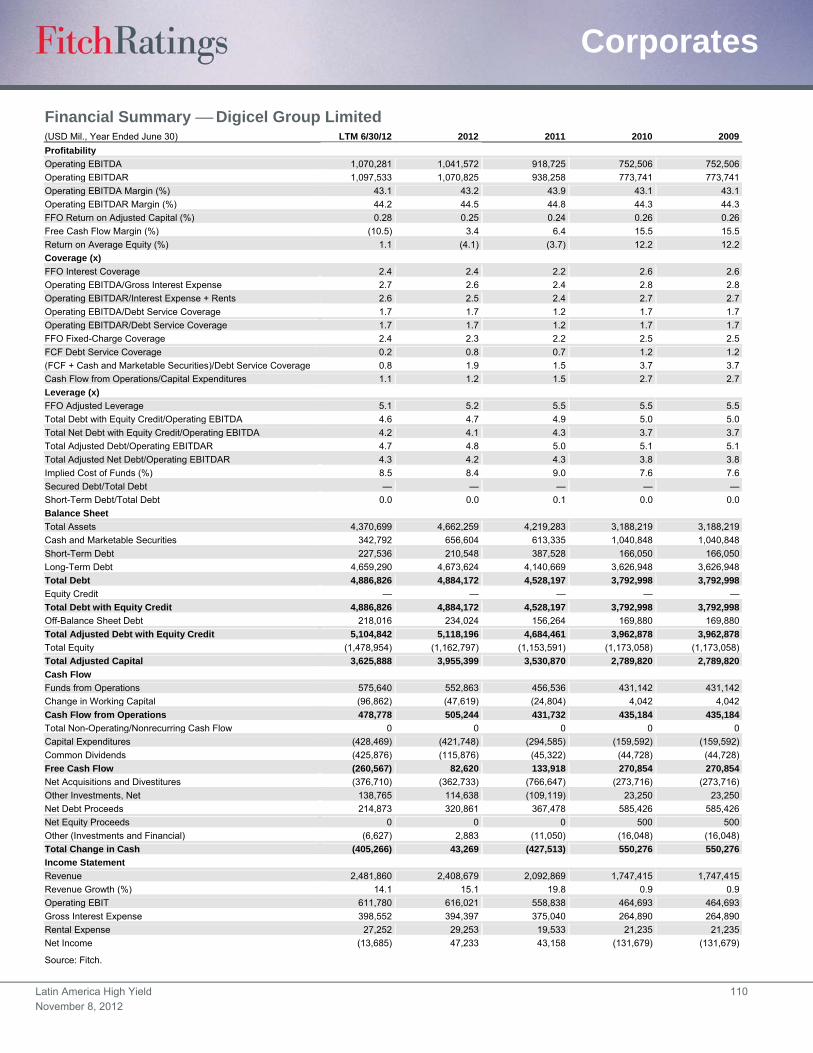

Digicel Group Limited ............................................... 106

Empresa Generadora de Electricidad Haina, S.A. .... 111

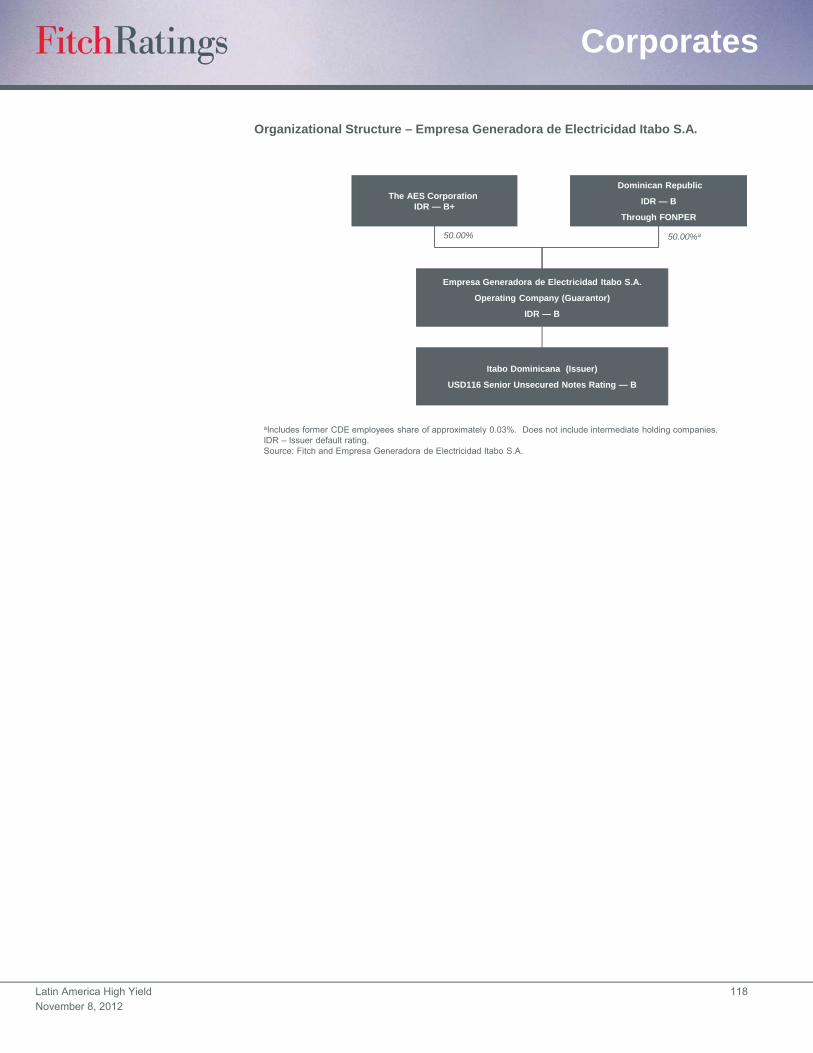

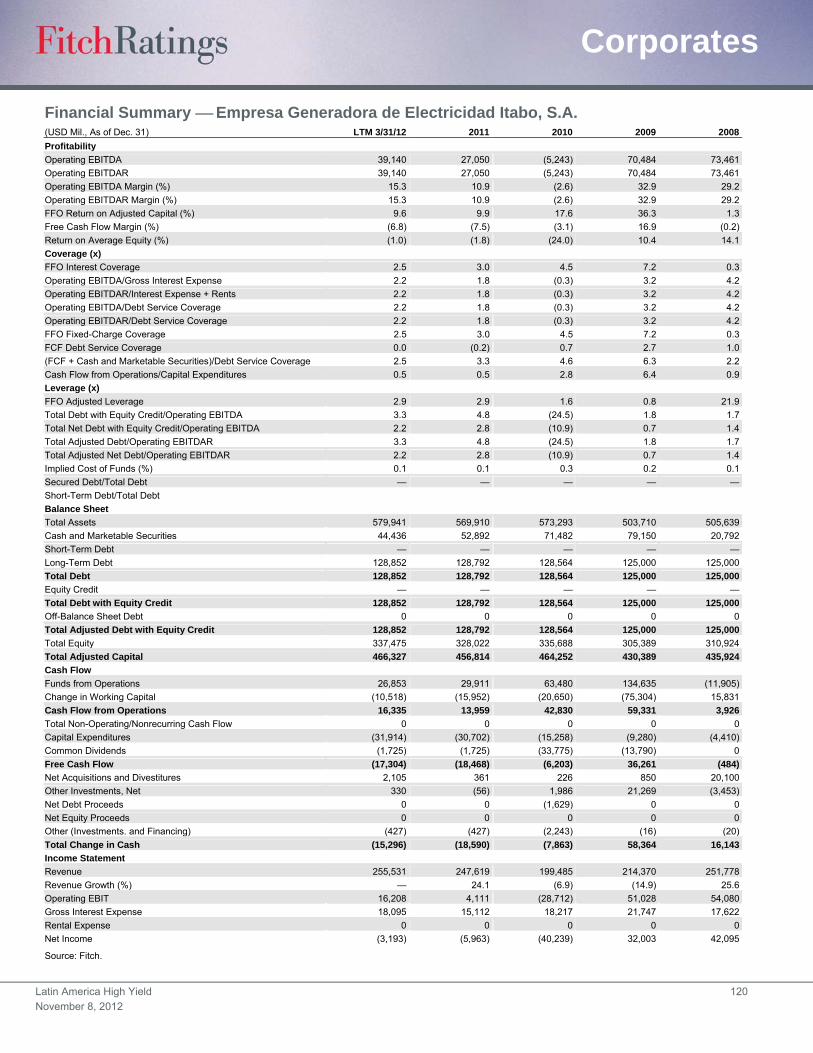

Empresa Generadora de Electricidad Itabo, S.A. ..... 116

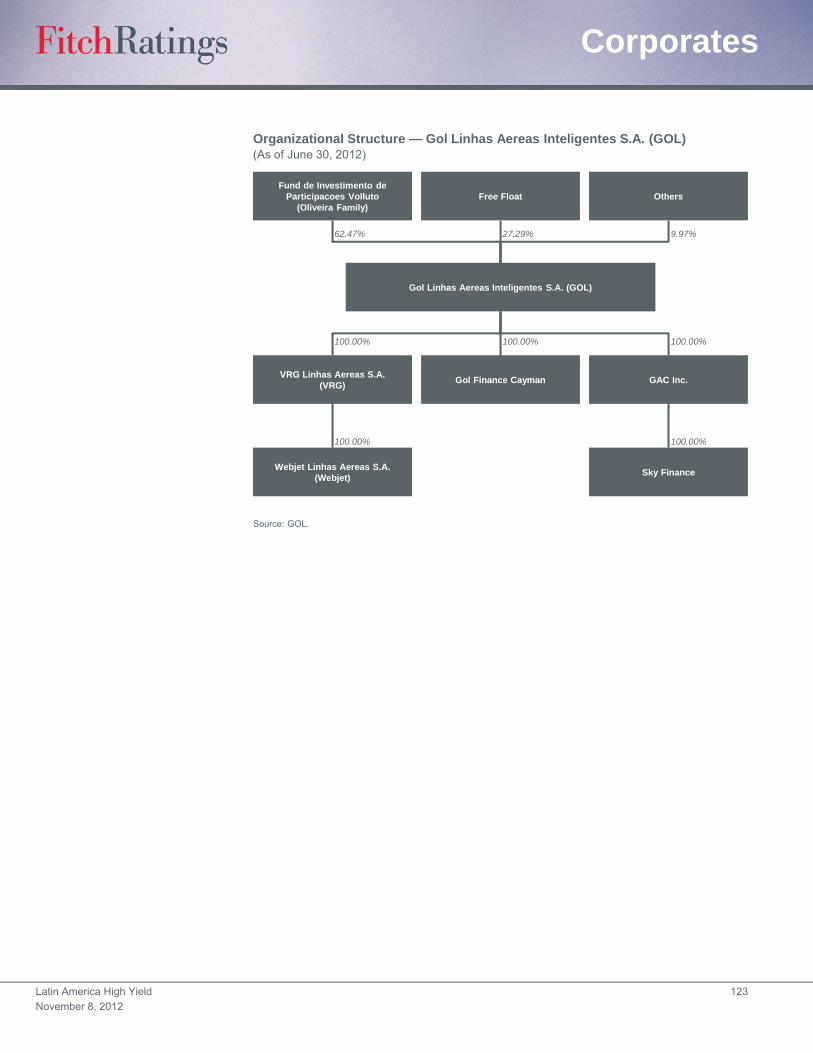

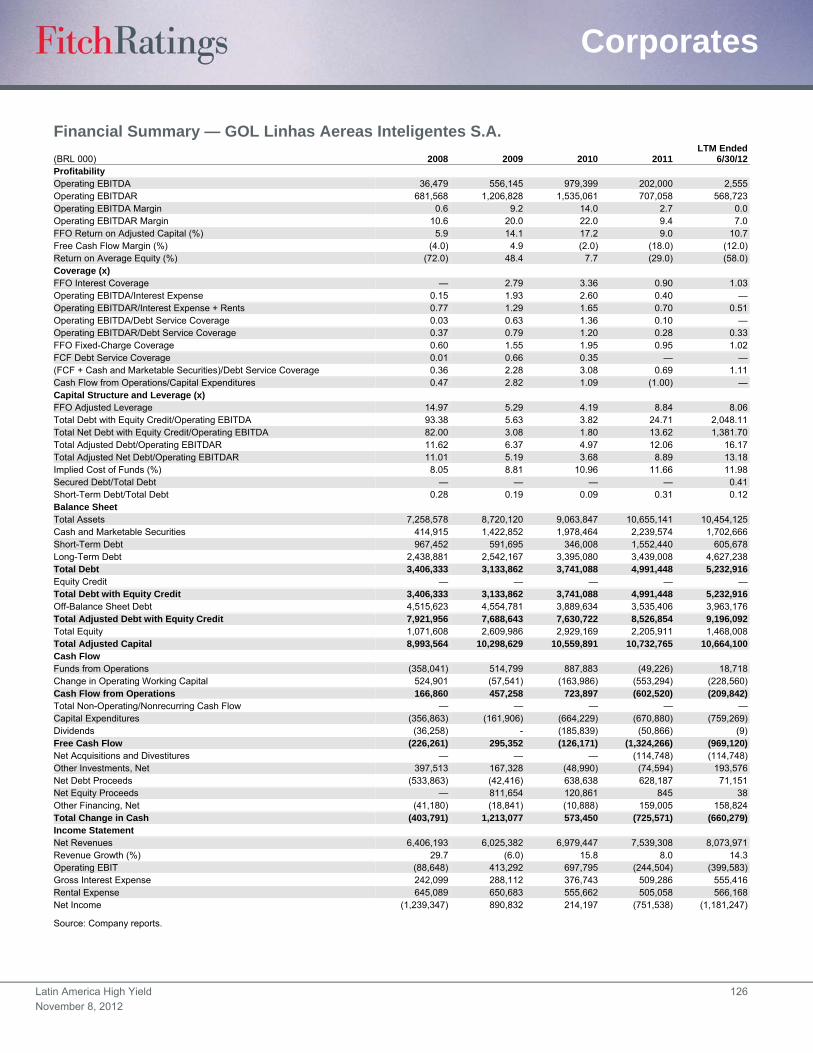

Gol Linhas Aereas Inteligentes S.A. ......................... 121

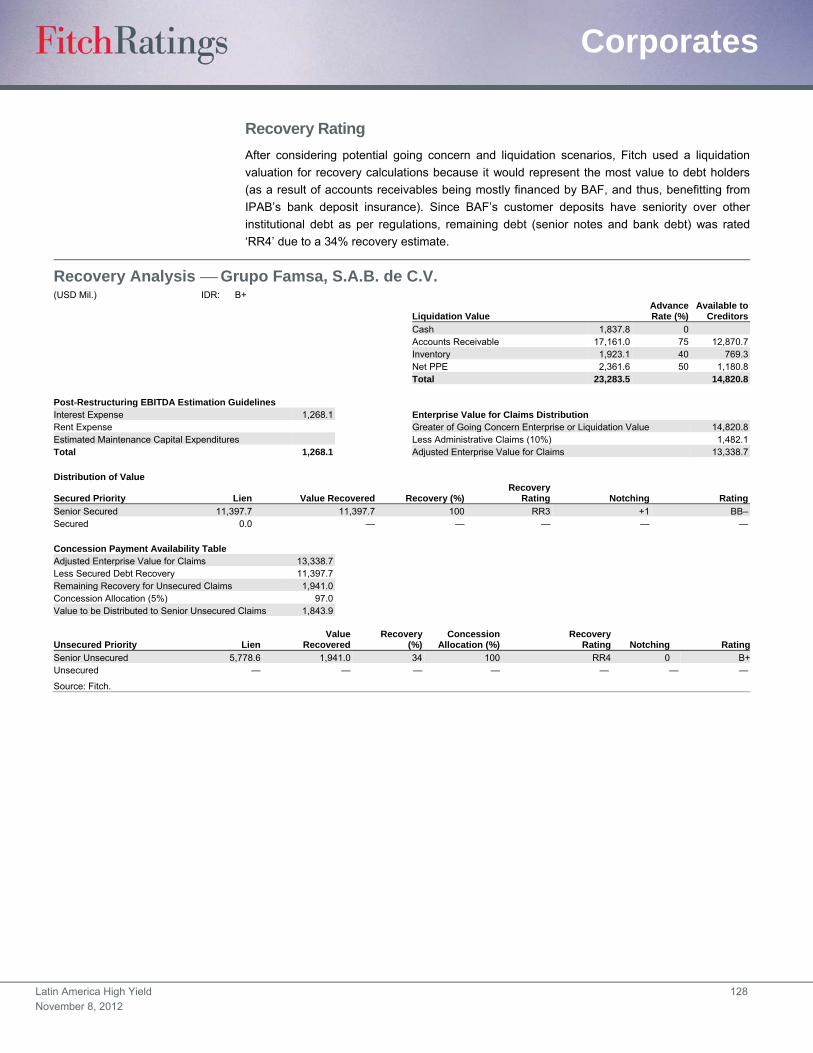

Grupo Famsa, S.A.B. de C.V. ................................... 127

Grupo Posadas, S.A. de C.V. ................................... 132

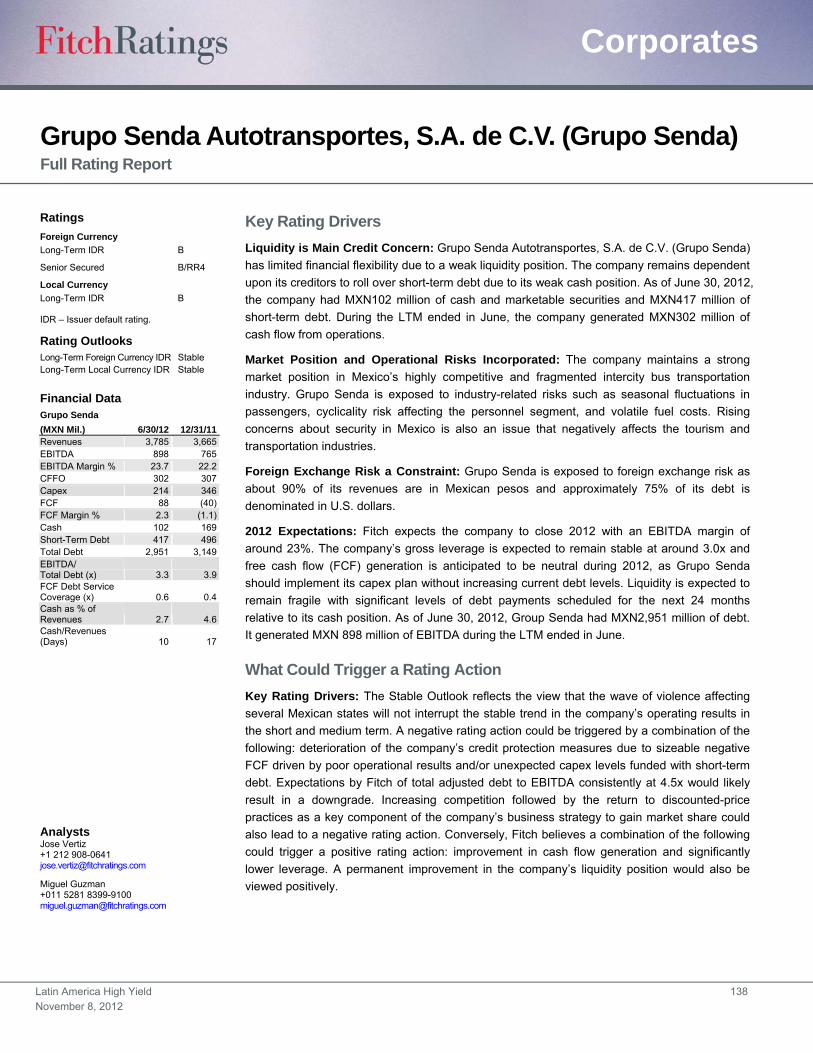

Grupo Senda Autotransporte, S.A. de C.V.

(Grupo Senda) ...................................................... 138

Industrias Metalurgicas Pescarmona S.A. (IMPSA) ... 144

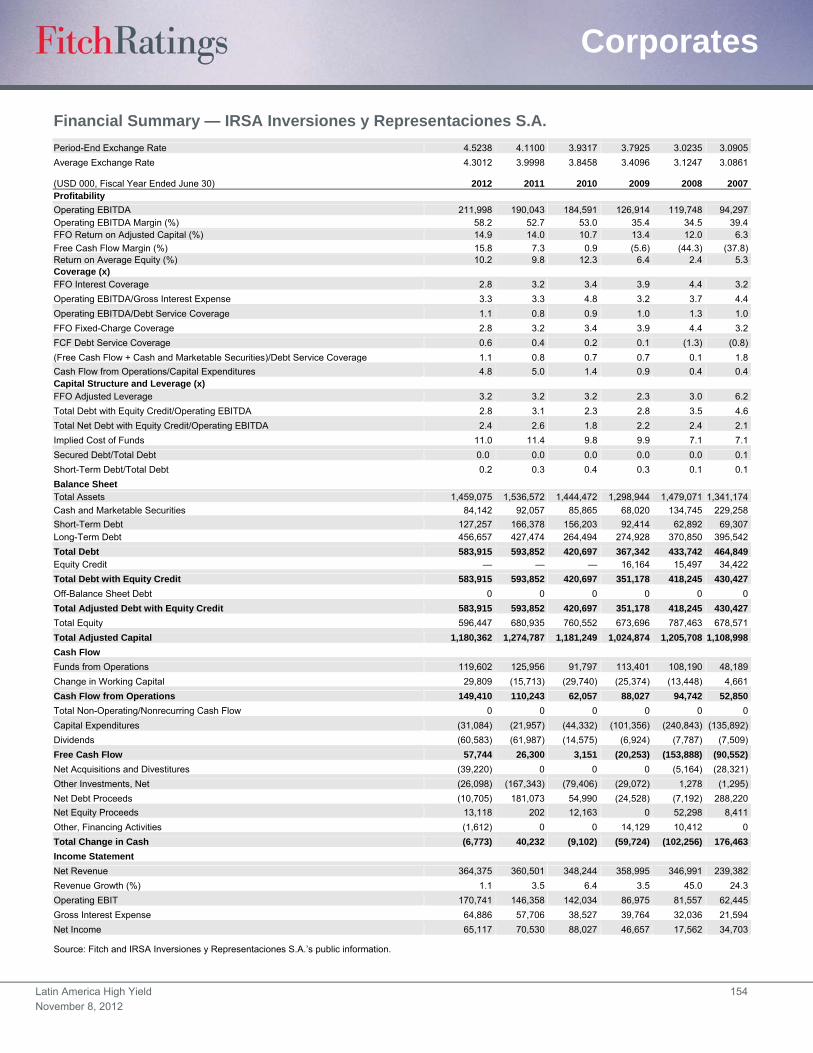

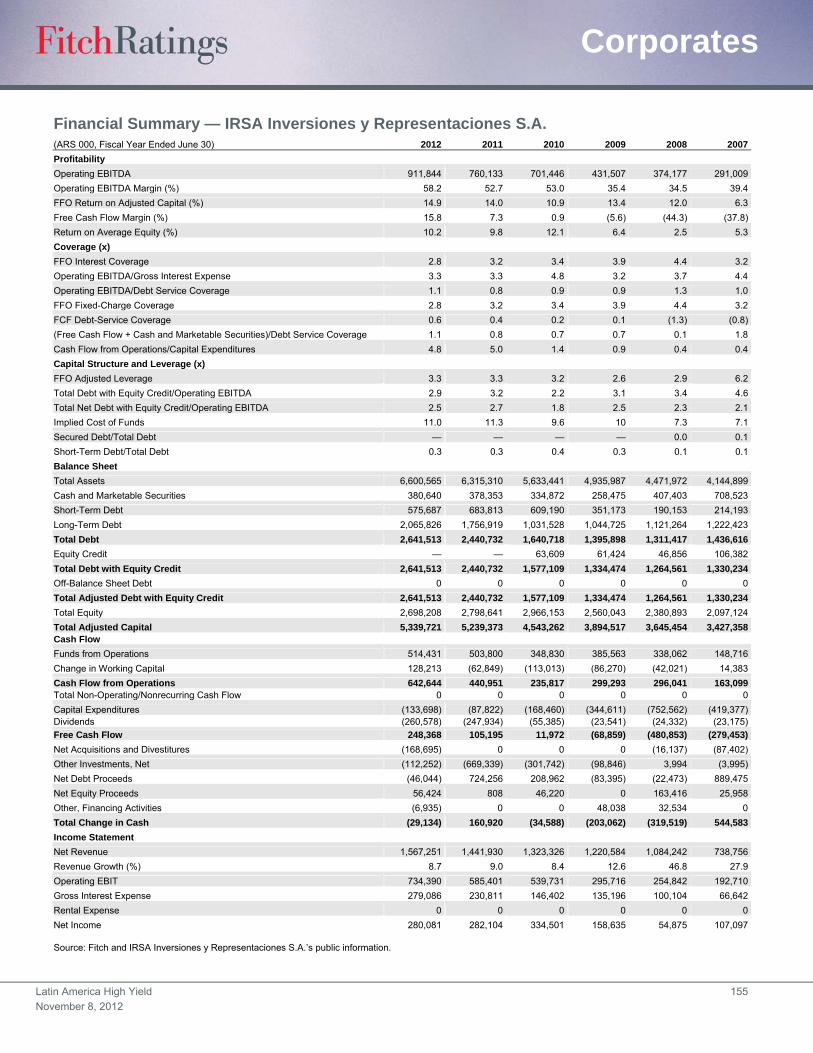

Inversiones y Representaciones S.A. ....................... 150

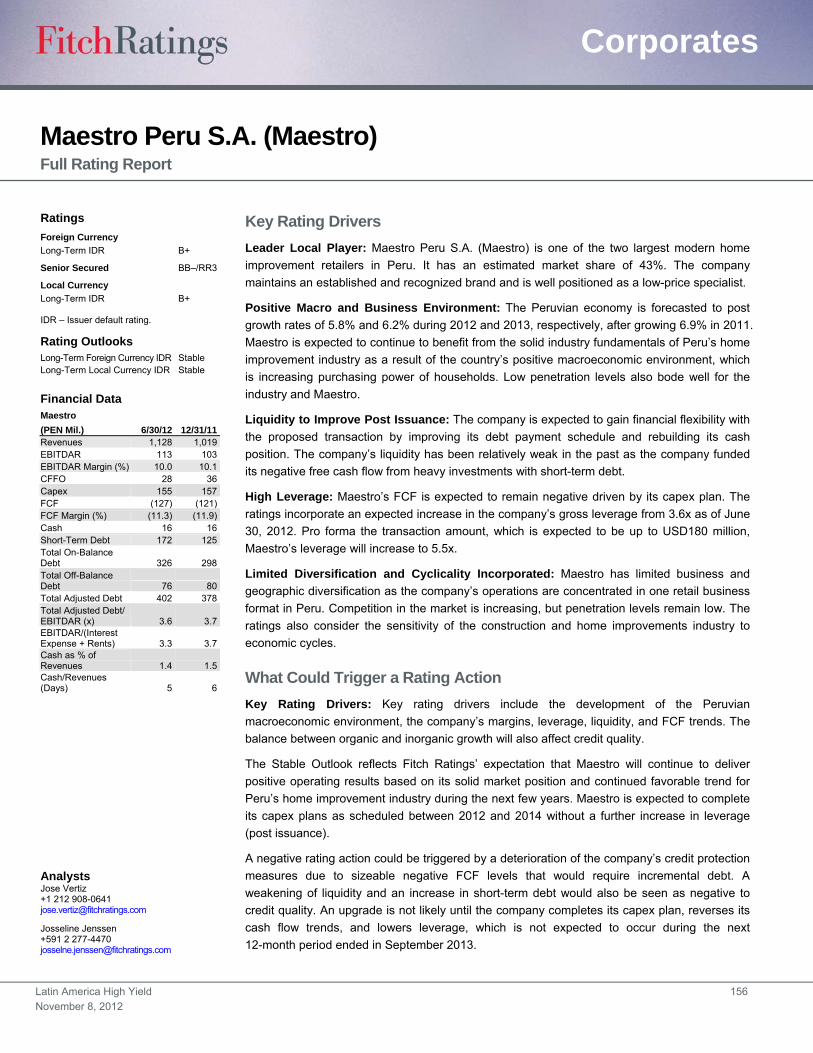

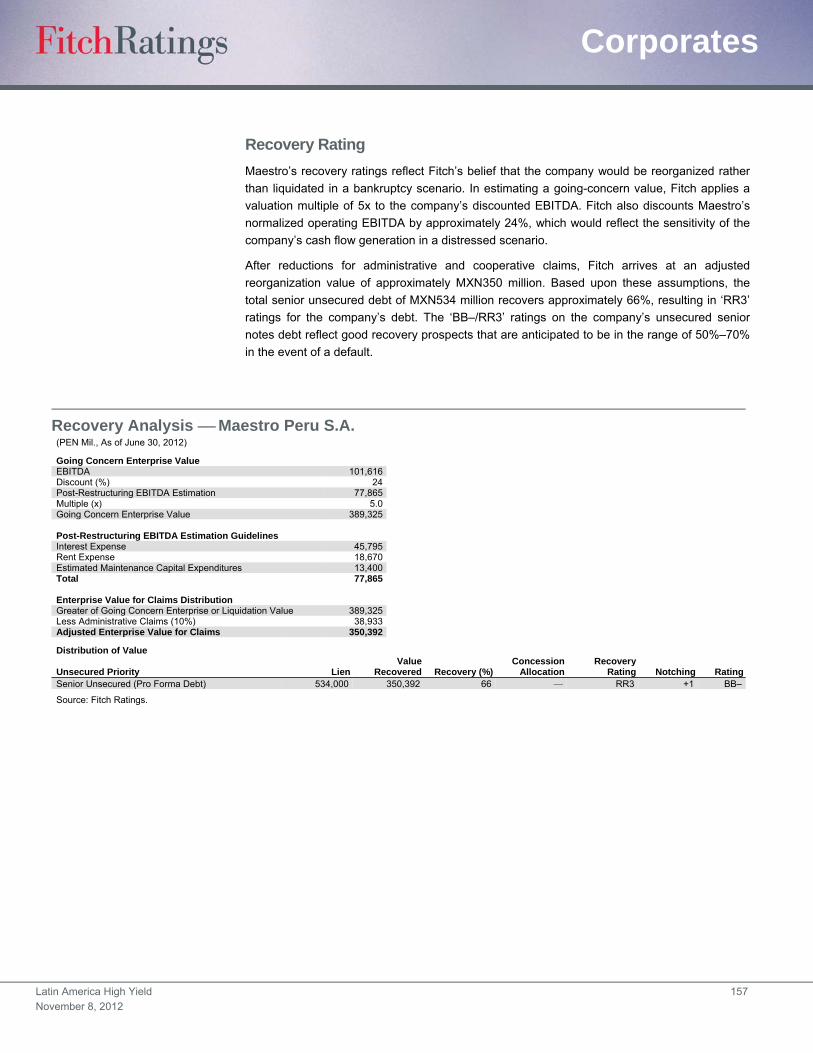

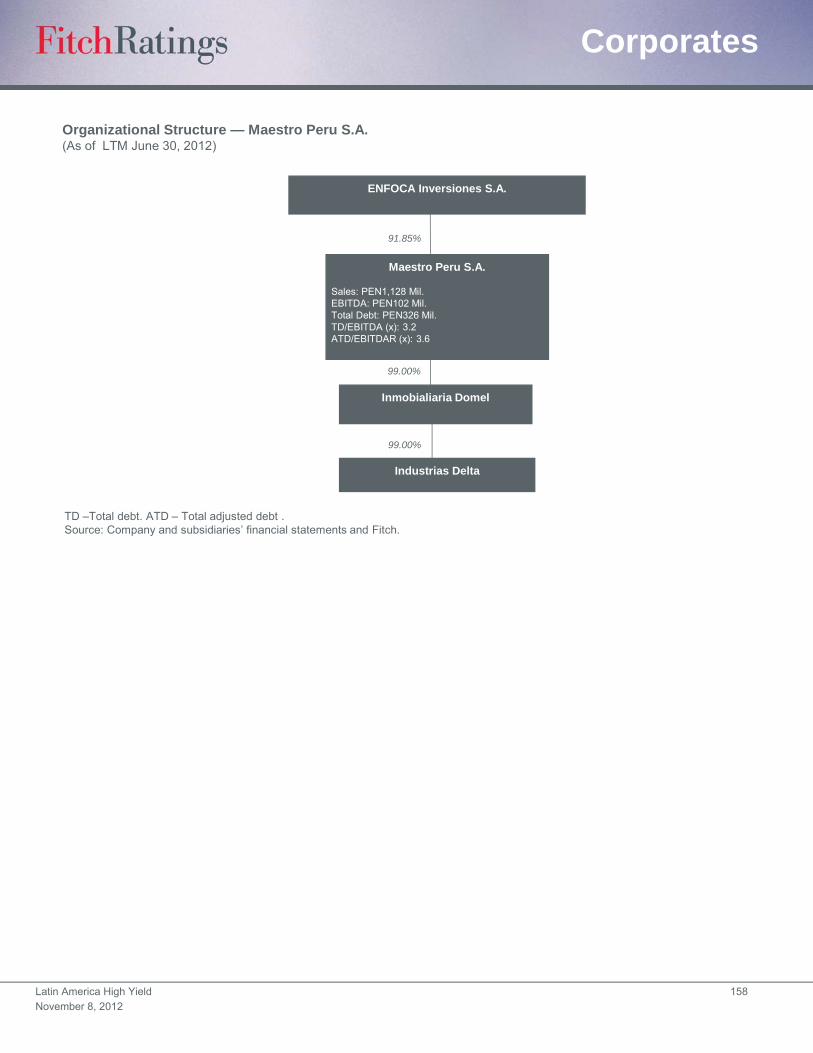

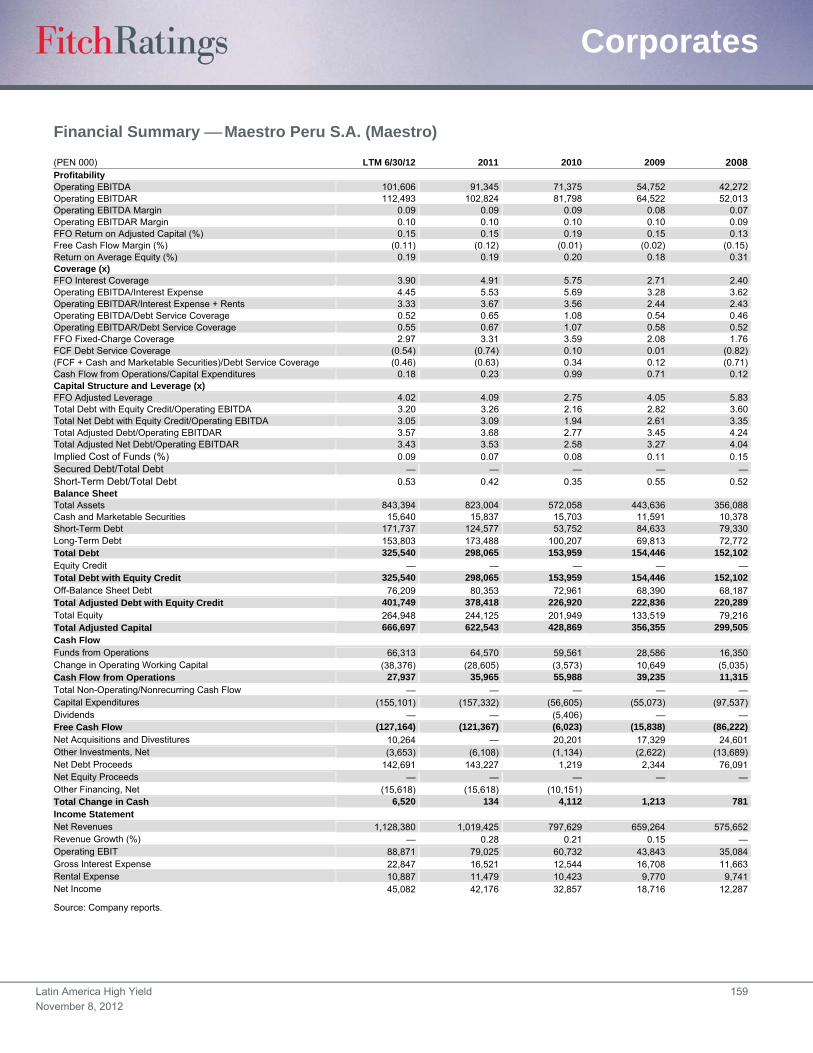

Maestro Peru S.A. (Maestro) .................................... 156

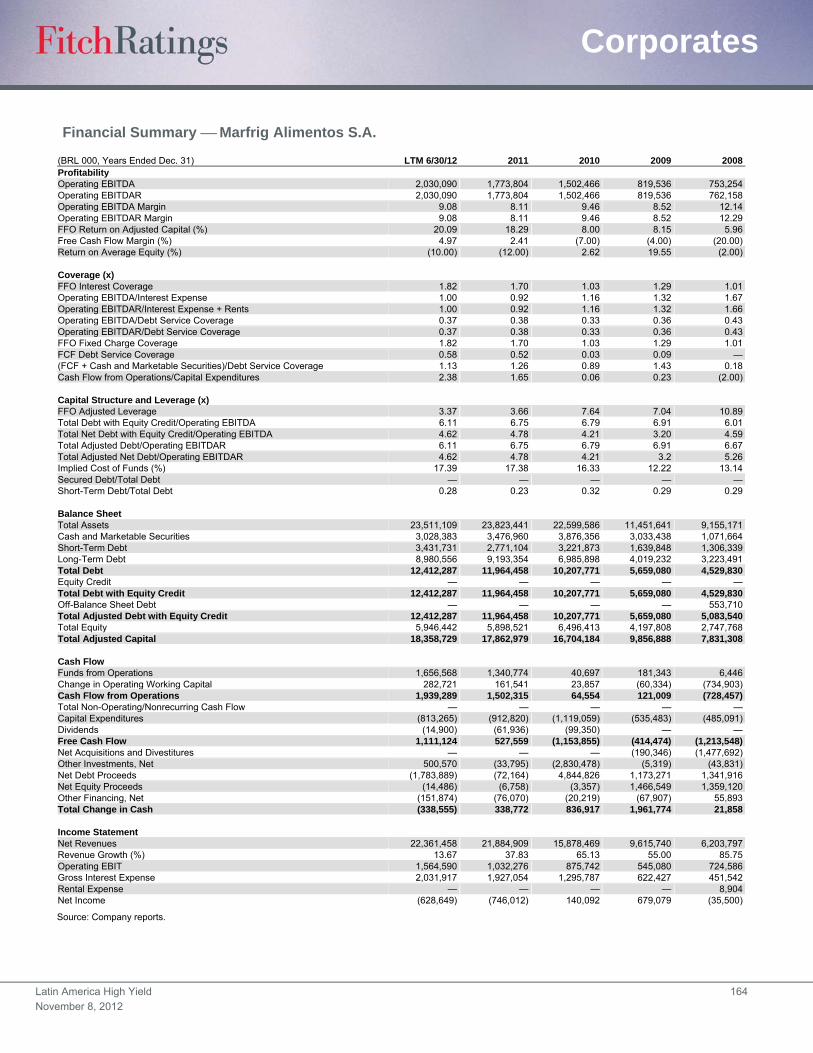

Marfrig Alimentos S.A. .............................................. 160

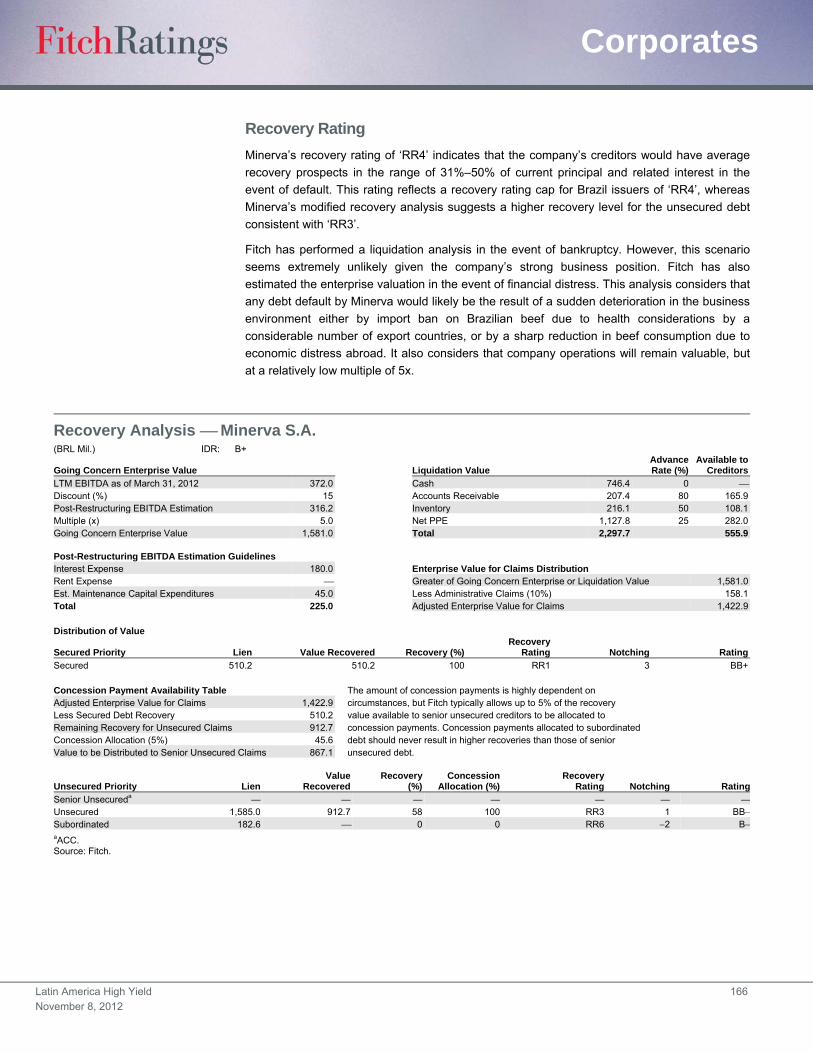

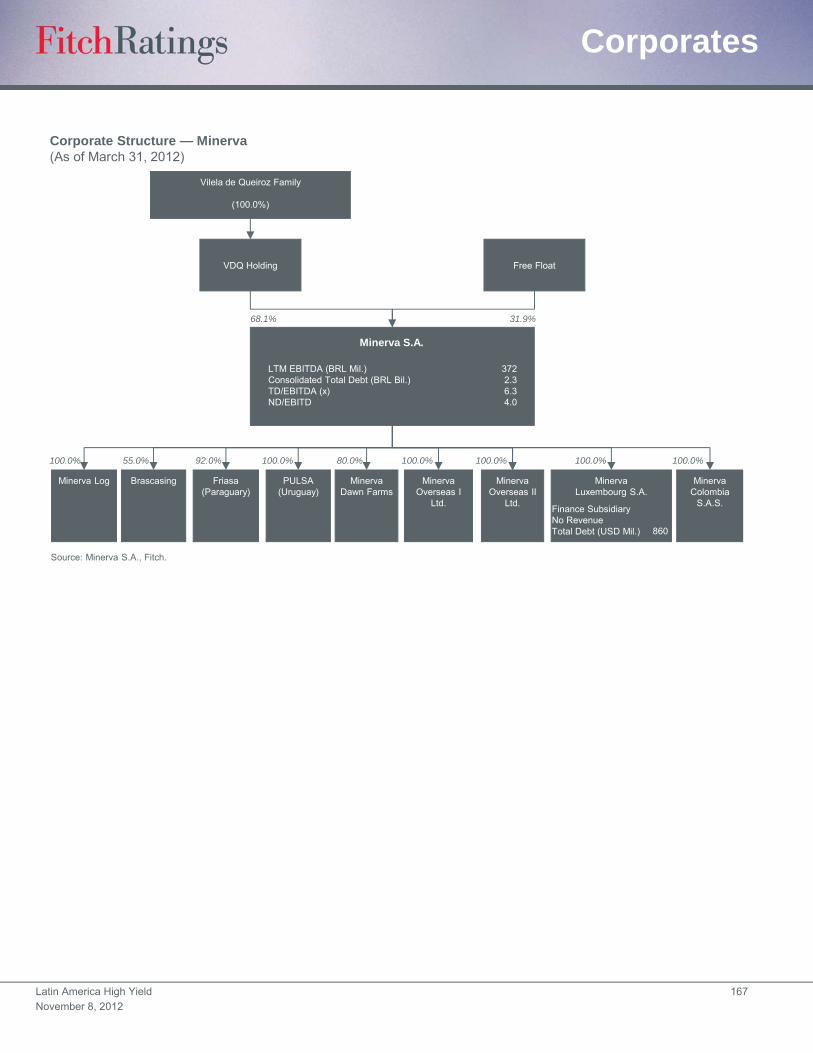

Minerva S.A. ............................................................. 165

OAS S.A. .................................................................. 170

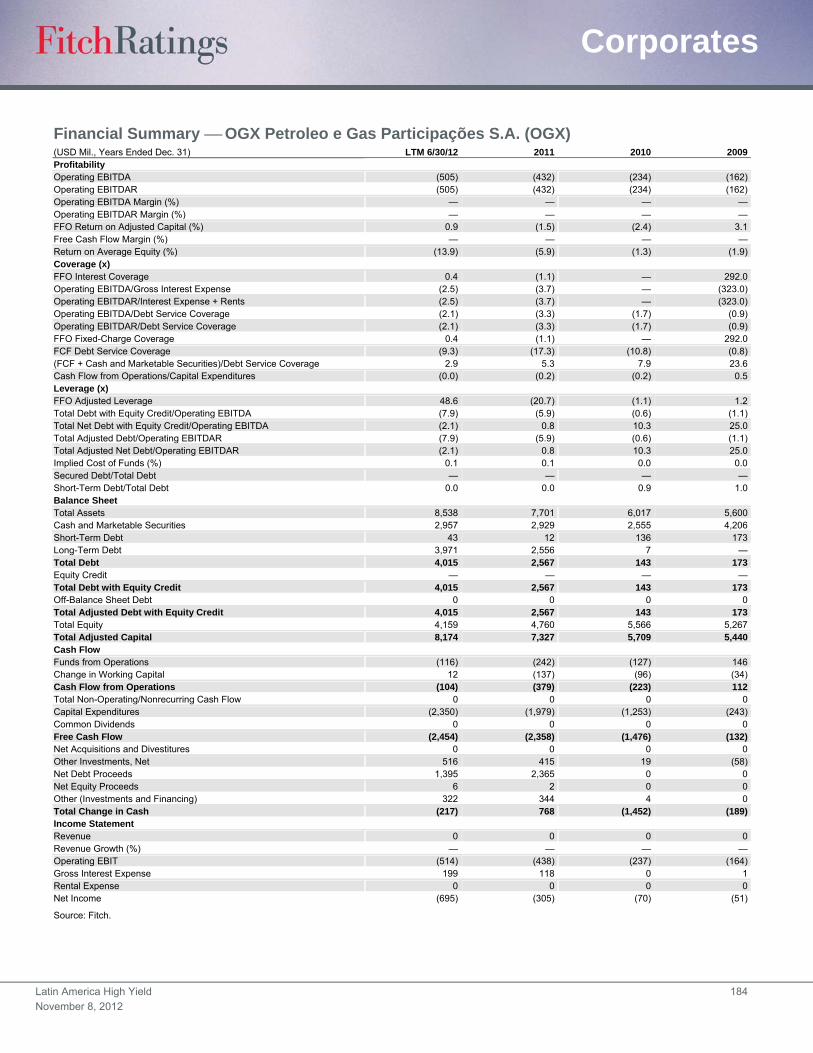

OGX Petroleo e Gas Participações S.A. ................... 180

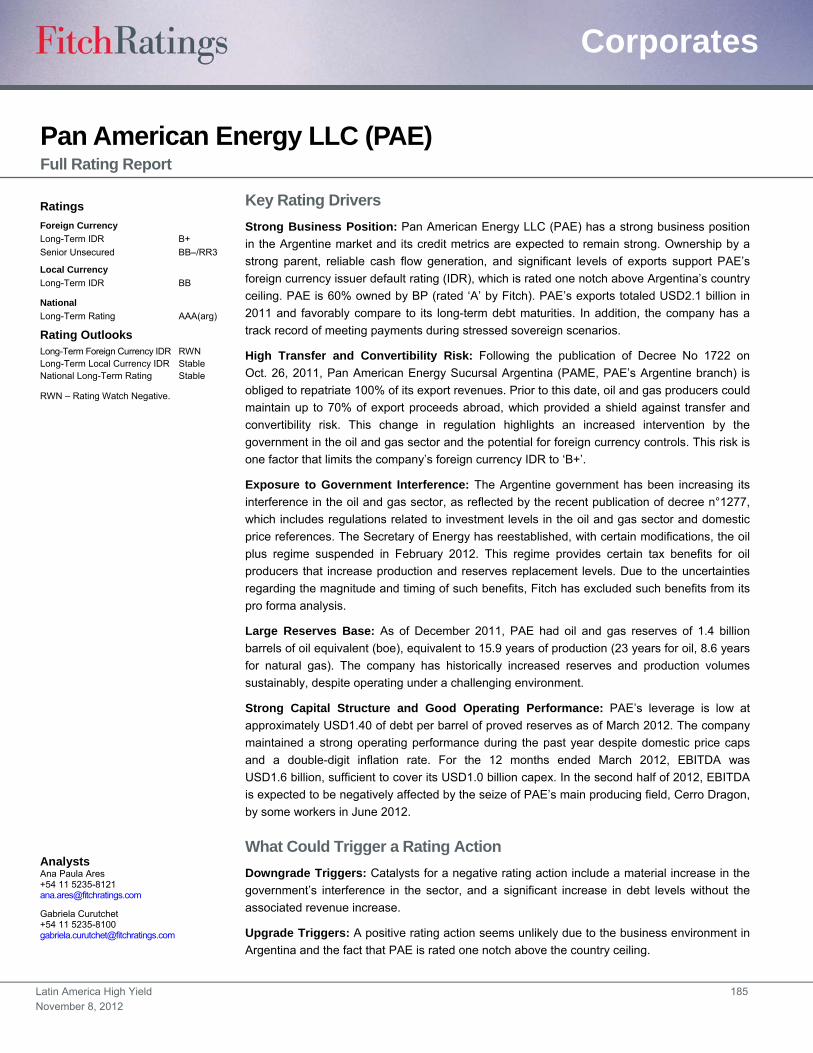

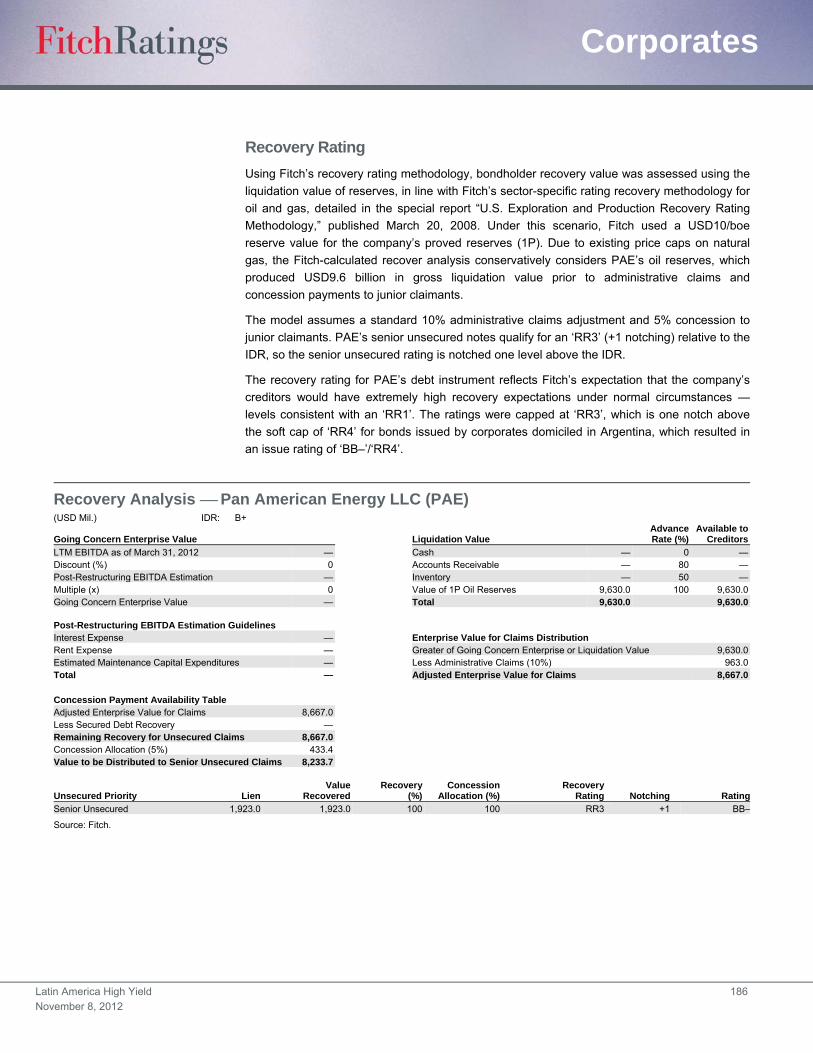

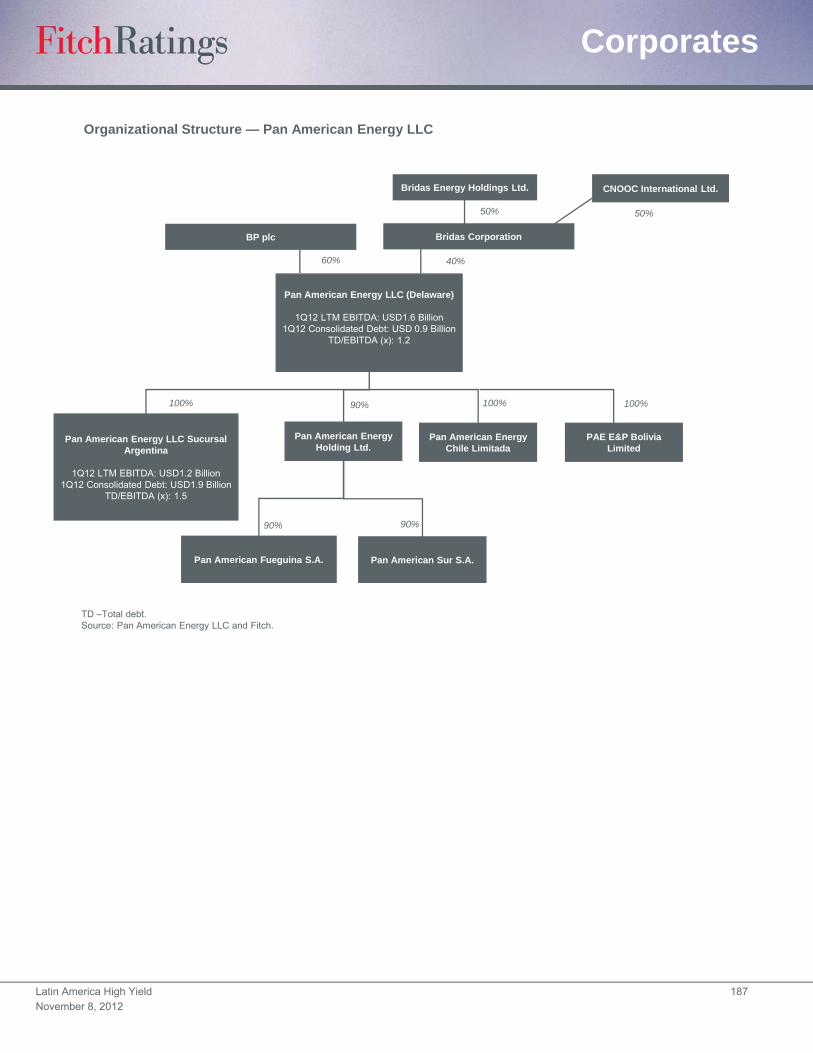

Pan American Energy LLC ....................................... 185

Petroleos de Venezuela S.A. (PDVSA) .................... 189

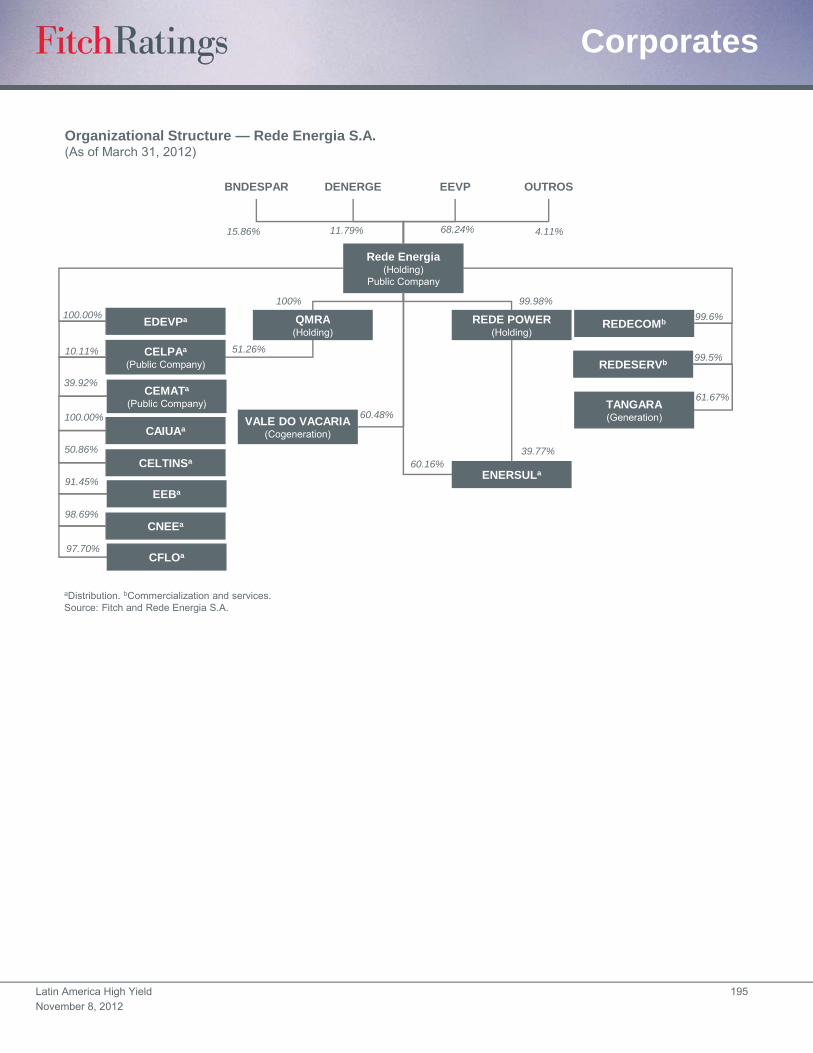

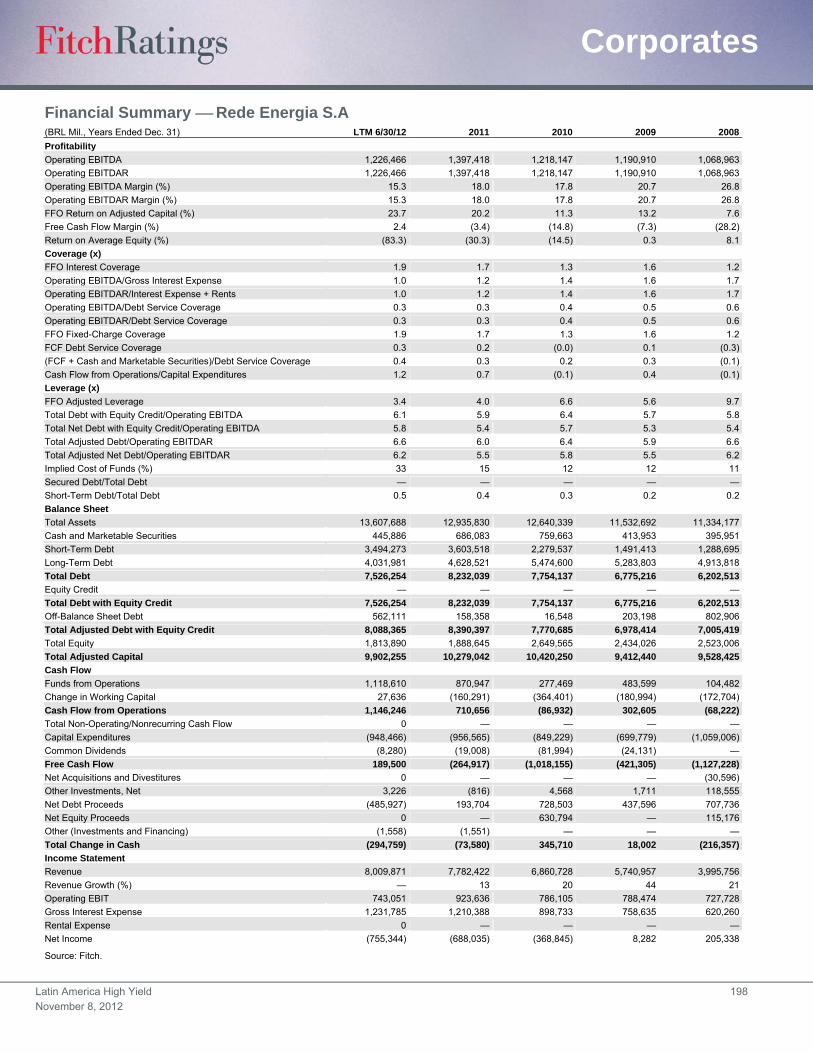

Rede Energia S.A. .................................................... 193

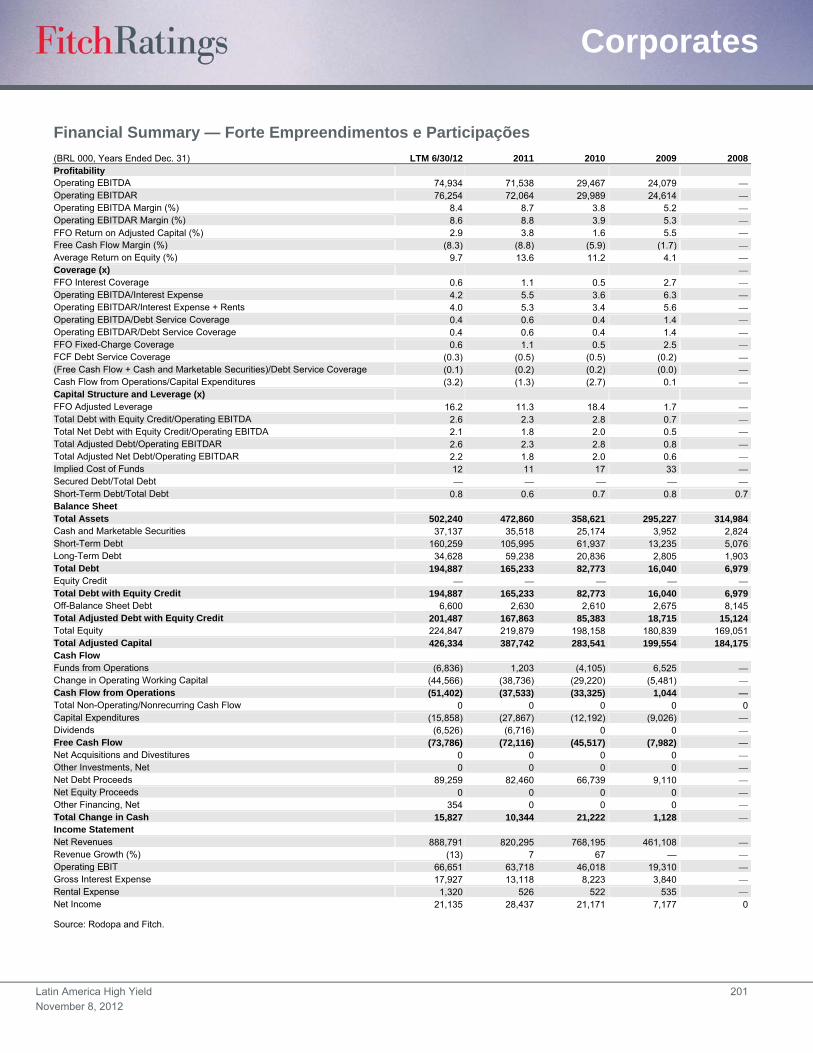

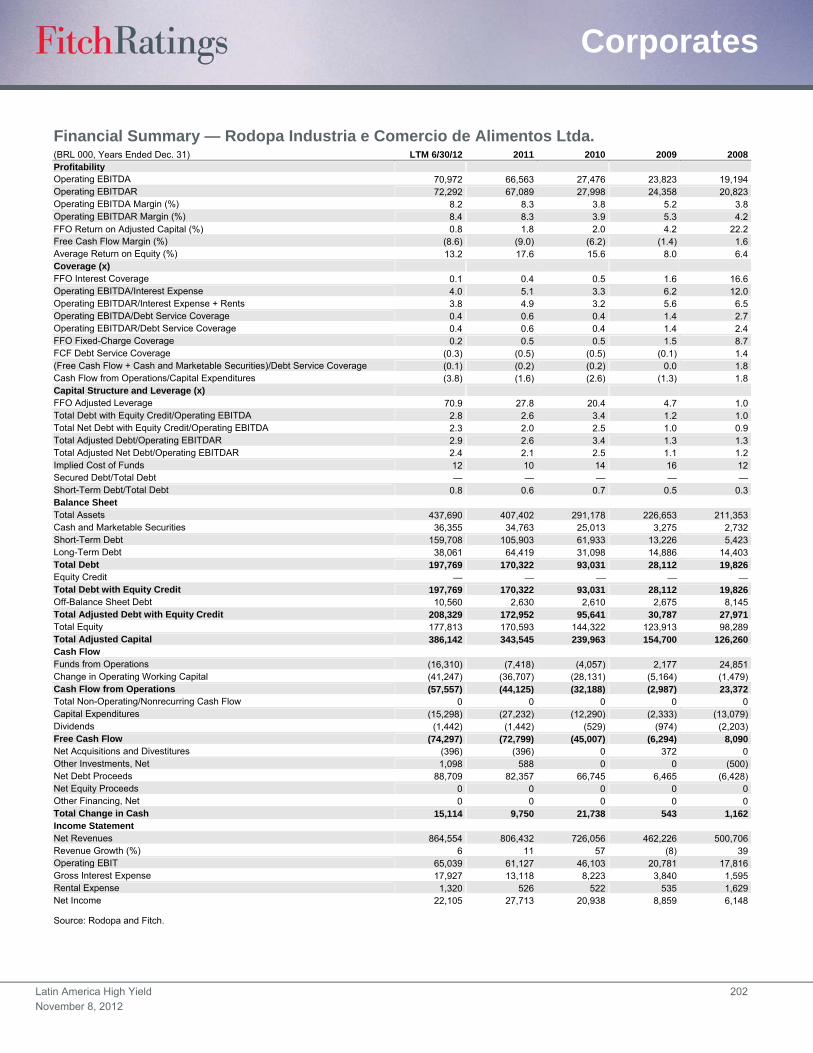

Rodopa Industria e Comercio de Alimentos Ltda. .... 199

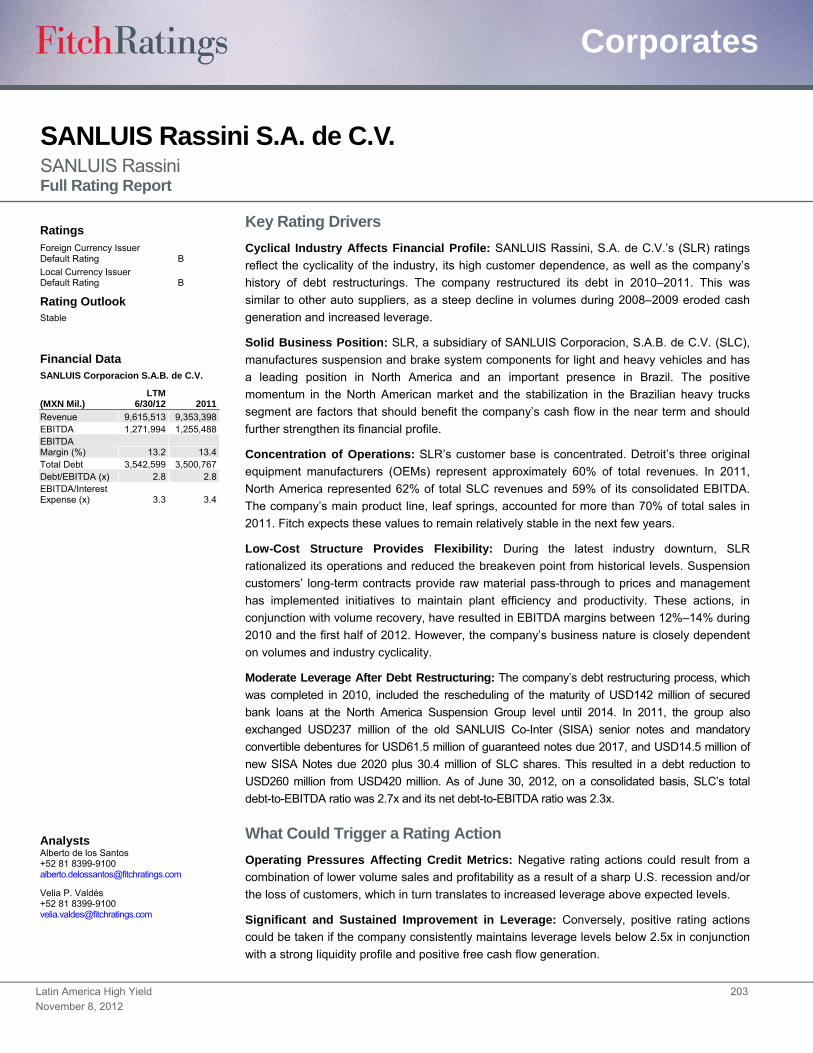

SANLUIS Rassini S.A. de C.V.. ................................ 203

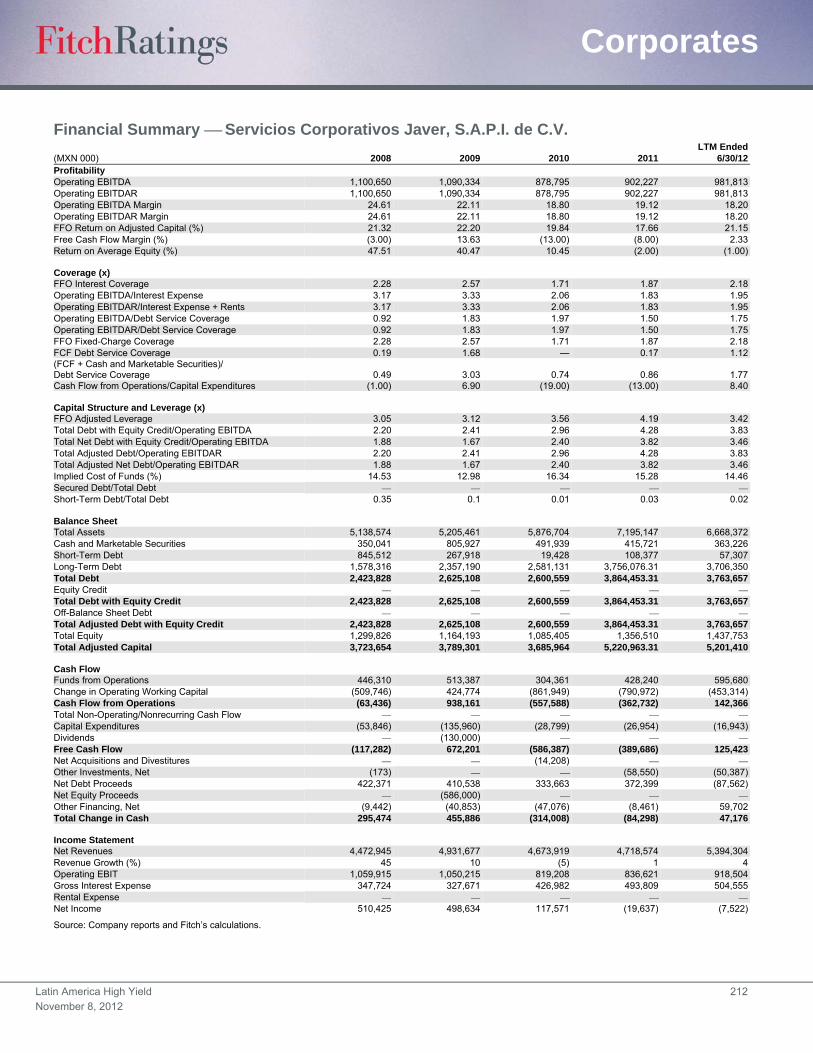

Servicios Corporativos Javer, S.A.P.I. de C.V. ......... 207

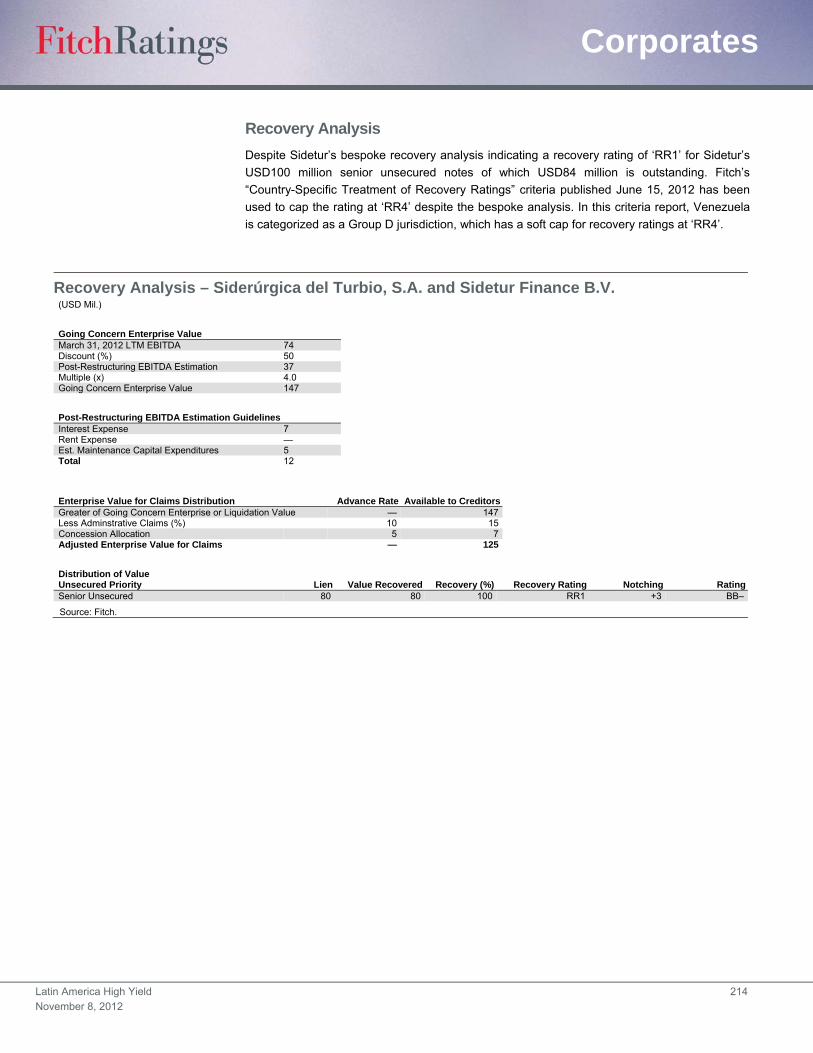

Sidetur (Siderurgica del Turbio, S.A.) ....................... 213

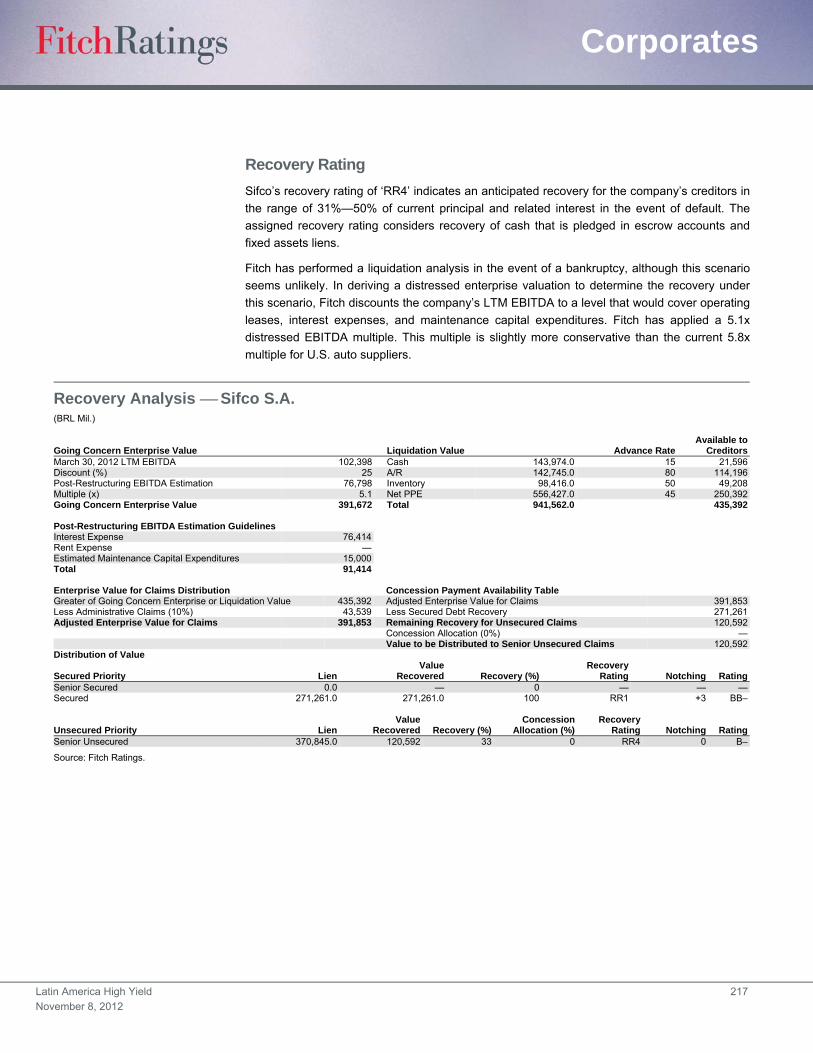

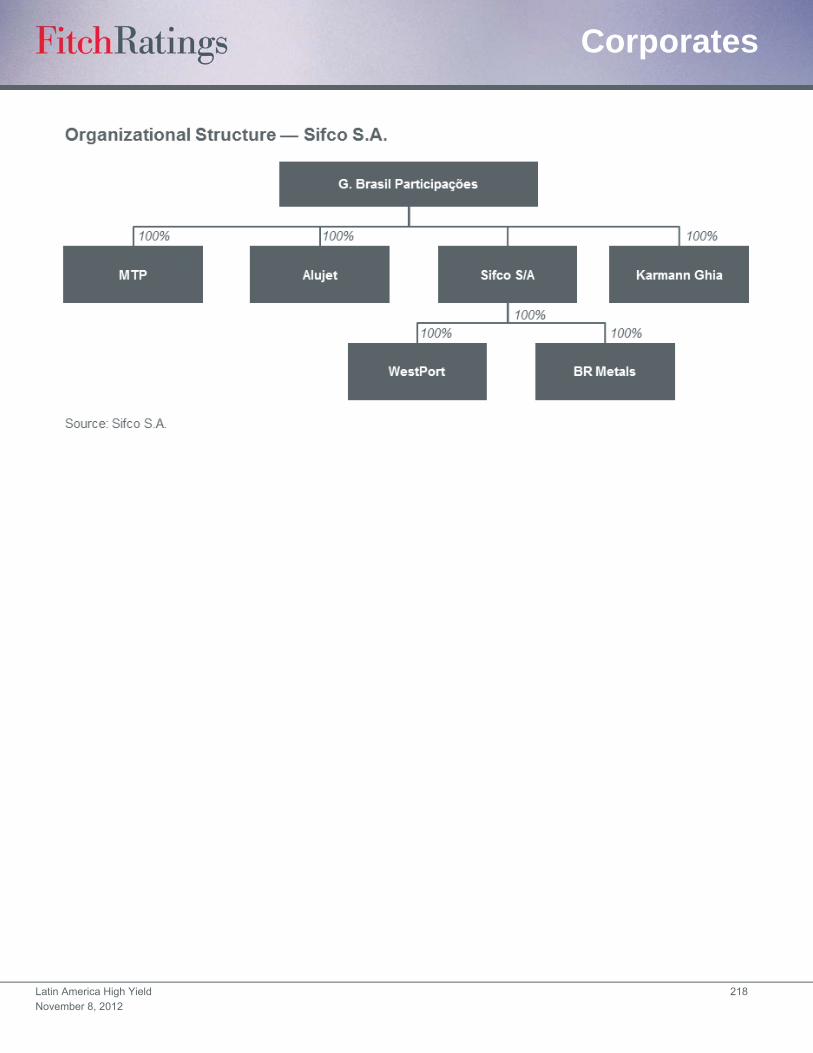

Sifco S.A. .................................................................. 216

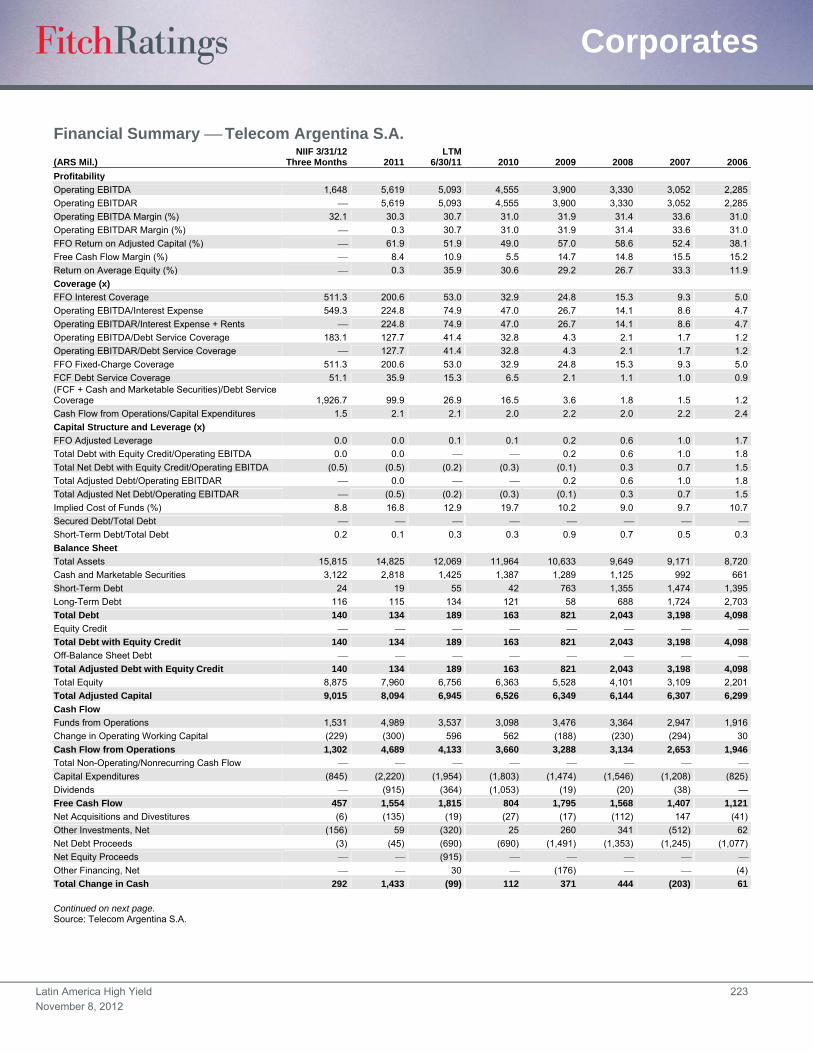

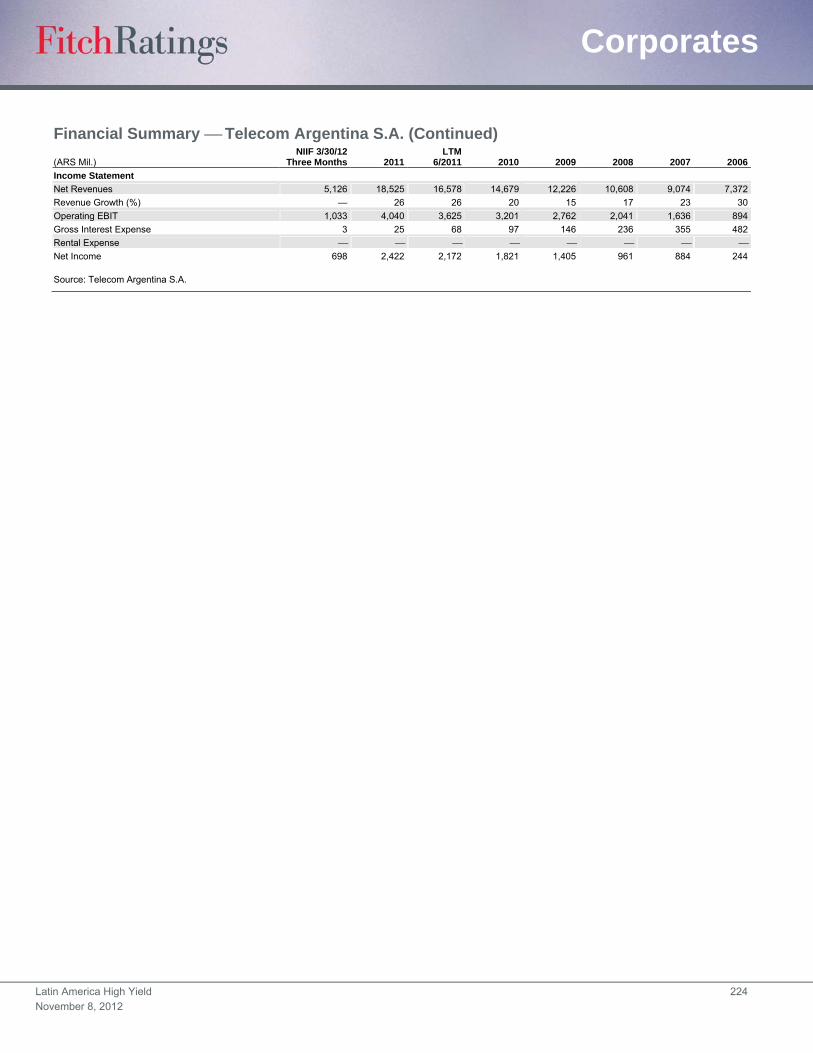

Telecom Argentina S.A. ............................................ 221

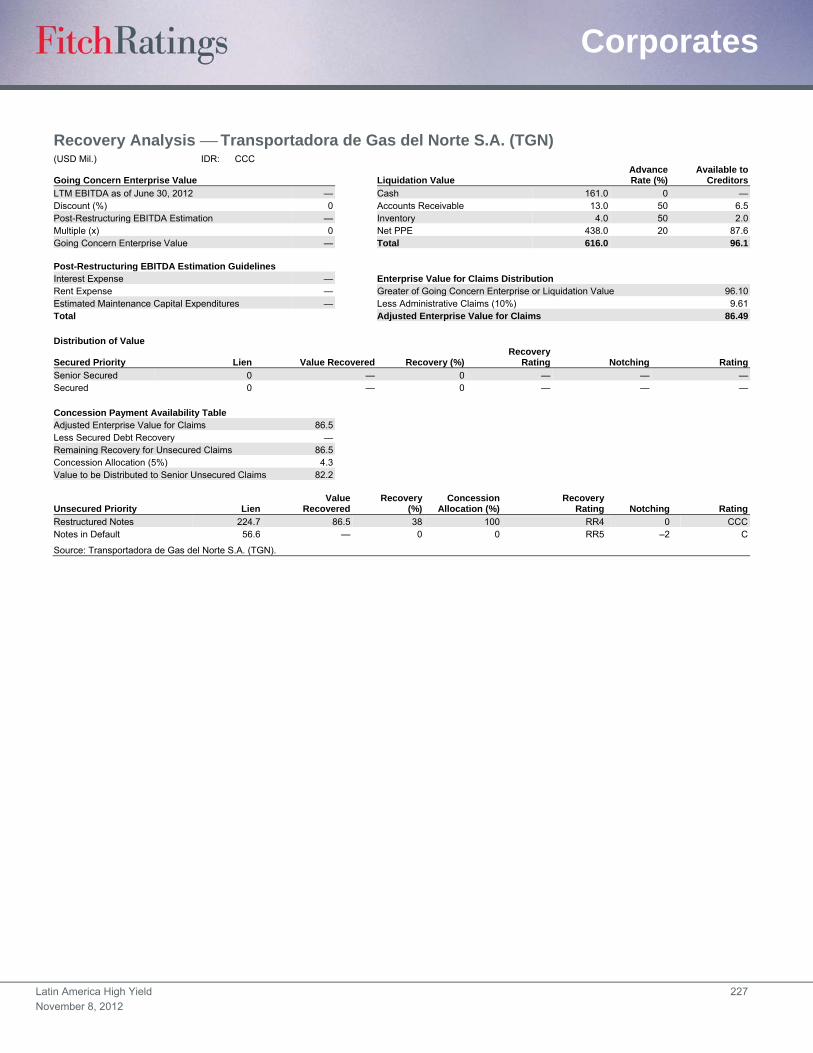

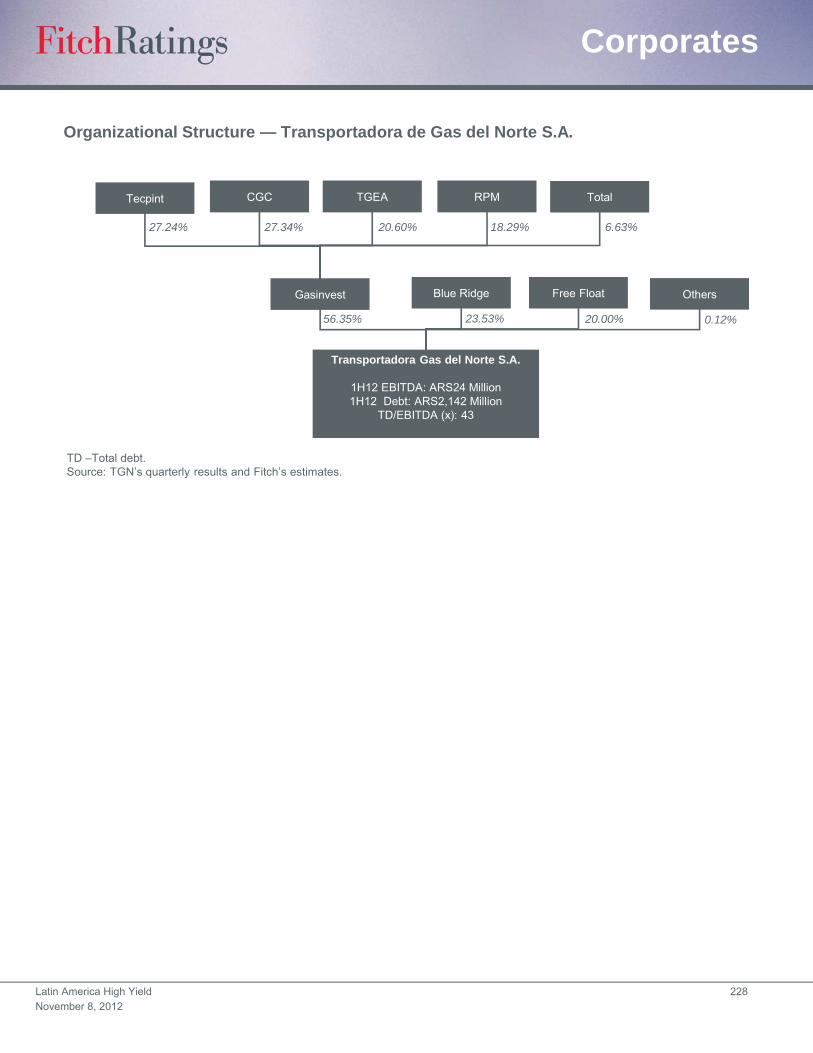

Transportadora de Gas del Norte S.A. (TGN) .......... 225

Transportadora de Gas del Sur S.A. (TGS) .............. 233

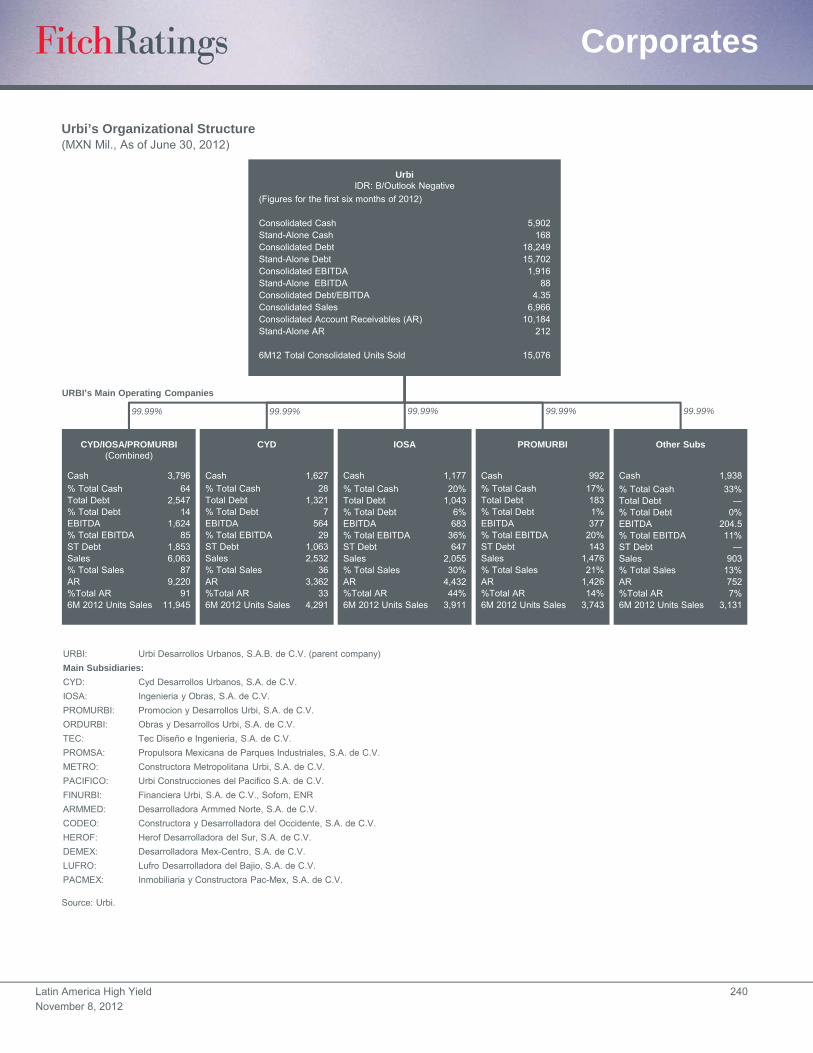

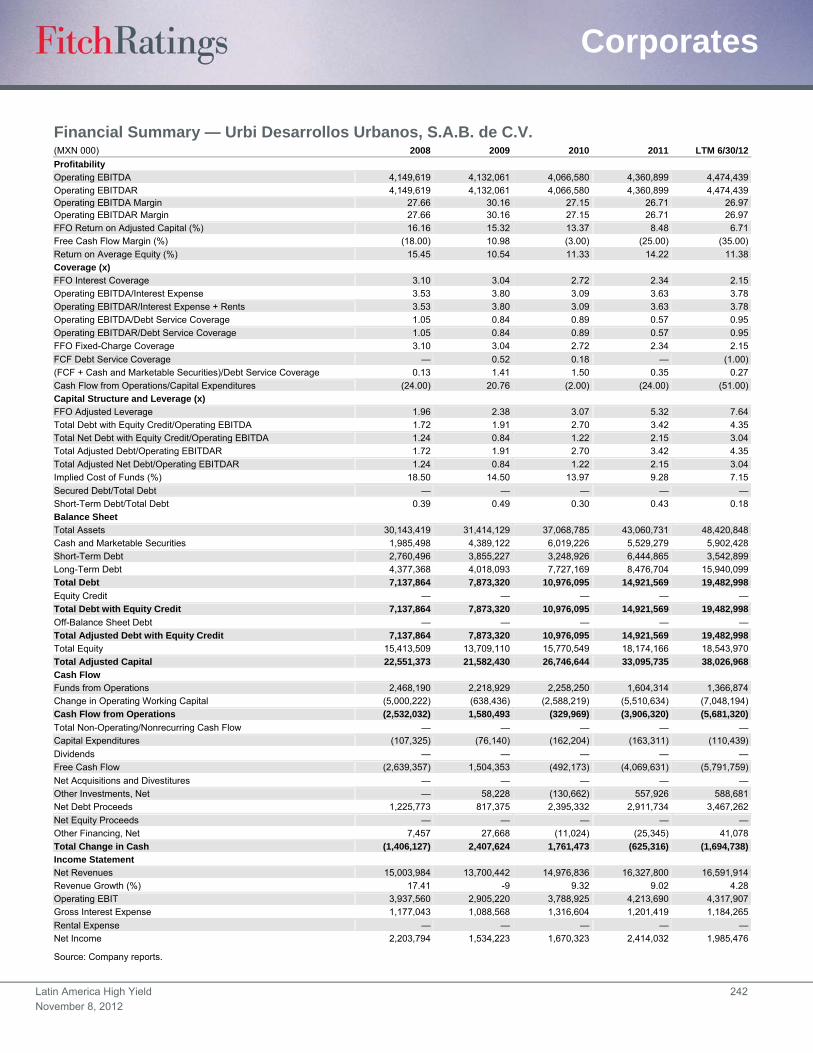

Urbi Desarrollos Urbanos, S.A. B. de C.V. ............... 238

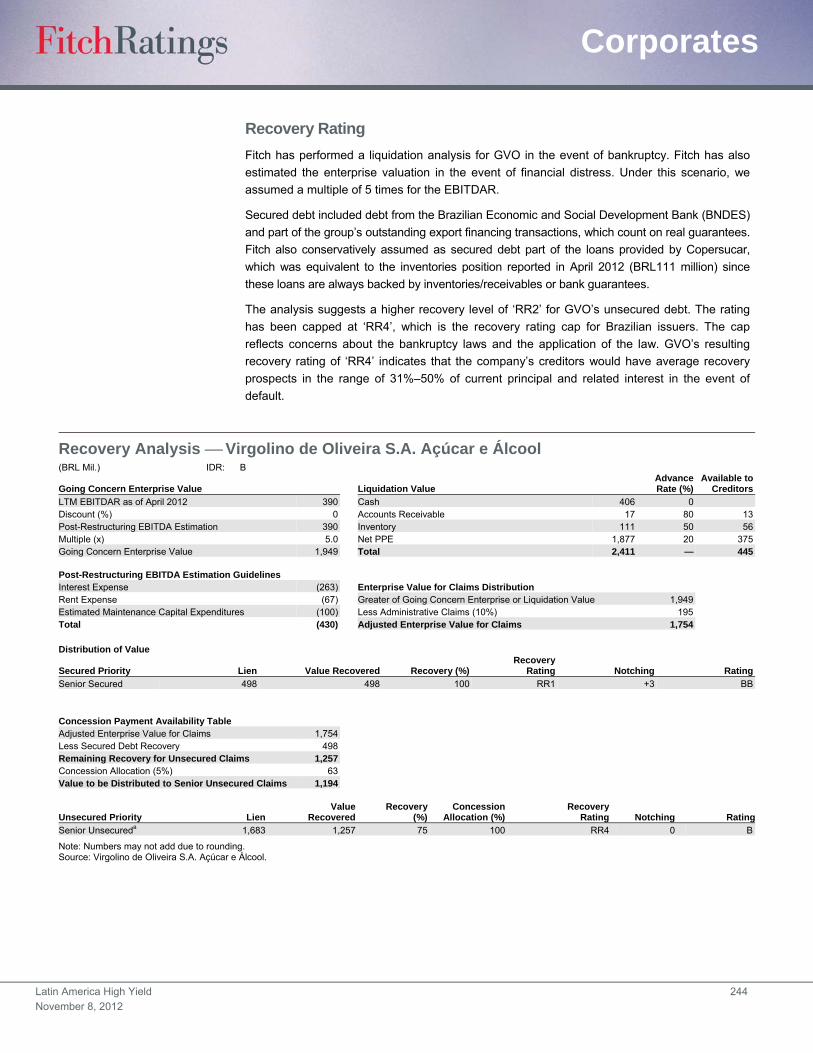

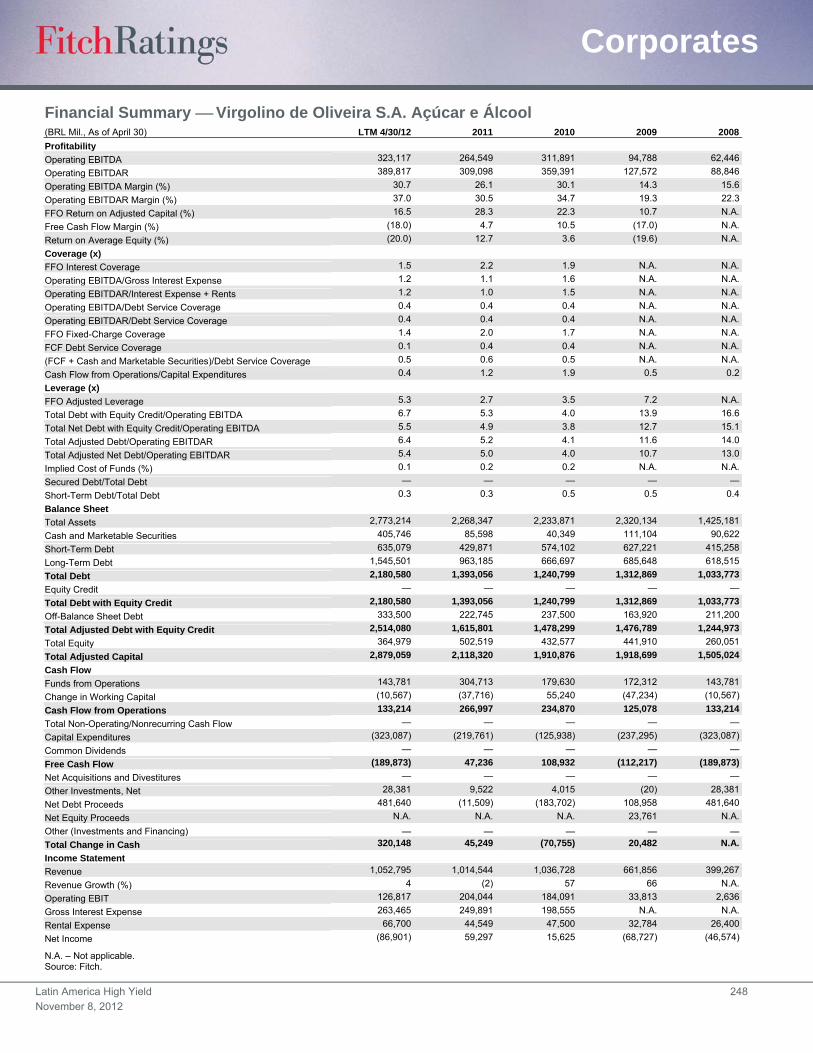

Virgolino de Oliveira S.A. Açúcar e Álcool ................ 243

WPE International Cooperatief (WPEI) ..................... 249

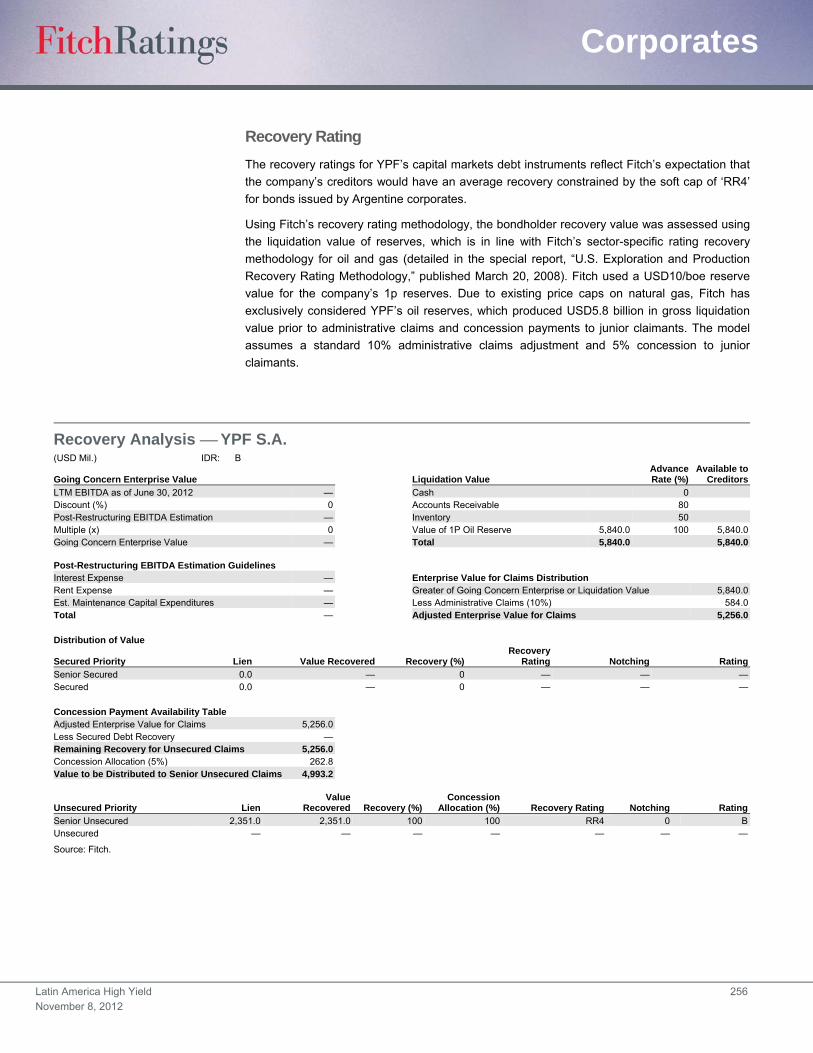

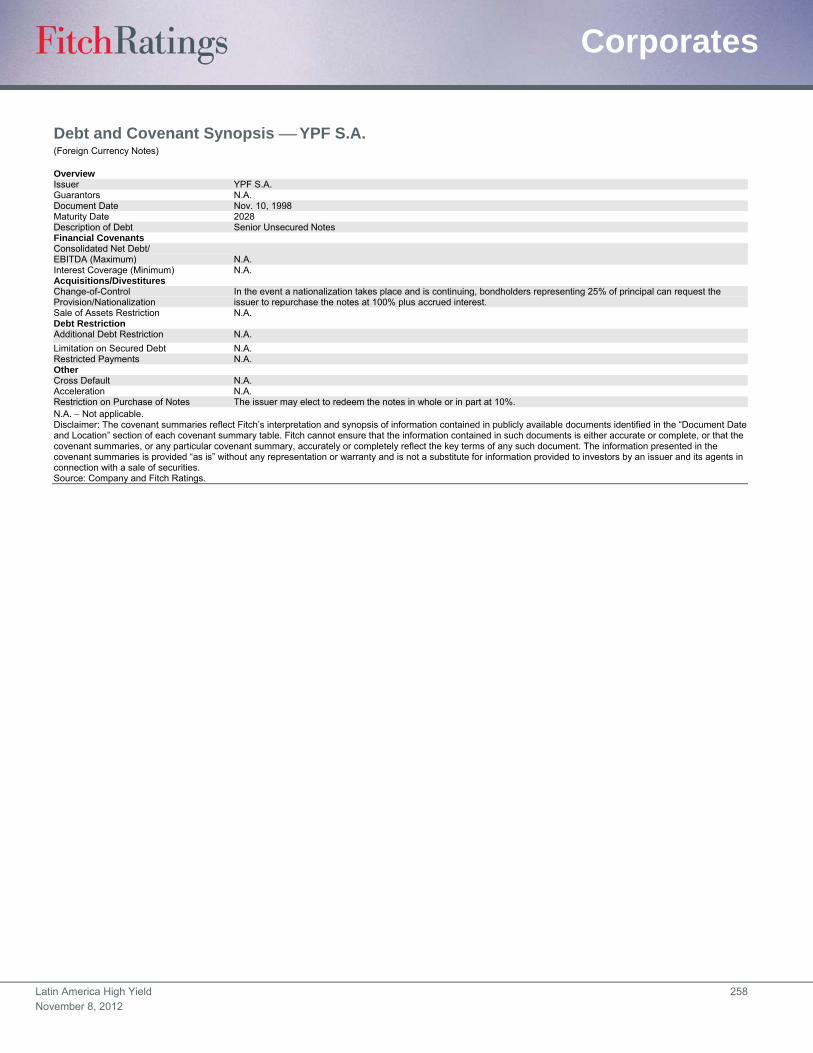

YPF S.A. ................................................................... 255

Fitch Analyst Directory ............................................. 260

www.fitchratings.com November 8, 2012

Corporates

Latin America High Yield Comprehensive Analysis of ‘B+’ Issuers and Below

Credit Outlook Turns Mildly Positive for Speculative Credits

Improving Macroeconomic Backdrop: Fitch forecasts GDP growth to be 3.9% in 2013 in

Latin America, an improvement from 3.0% in 2012. Consumer demand is strong due to low

unemployment levels, rising wages, modest inflation, improving consumer confidence, and

wider access to credit. The key growth engine for 2013 is Brazil, which also has the highest

number of leveraged corporates in the ‘B’ rating category. Fitch expects growth to reach 4.2%

in Brazil during 2013, a sharp improvement from forecasted growth of 1.5% in 2012.

Record Capital Market Activity Lowers Refinancing Risk: Latin America corporates issued

USD48 billion of debt in the international capital markets during the first nine months of 2012.

This figure compares favorably with USD51 billion of issuance activity during the 12 months of

2011. Speculative credits such as Cemex, Digicel, Maestro, Minerva, PDVSA, Virgolino,

Cimento Tupi, OAS, OGX, and VRG Linhas Aereas were very active during 2012, issuing

about USD9 billion of debt.

Eurozone Financial Crisis Should Not Hurt Access to Credit: Concern over the potential for

a disorderly default in the eurozone has diminished. As a result, Fitch’s base case scenario

expects credit market access for Latin America corporates during 2013 to grow versus 2012

due to low interest rates in developed markets and high demand for emerging market debt. The

risk of bank credits being withdrawn from ‘B’ credits in Latin America due to the Euro crisis is

small and manageable.

Downgrades to Upgrade Ratio Should Revert to Normal Levels: The credit quality of highly

speculative corporate ratings in Latin America weakened sharply during the first nine months of

2012. Fitch downgraded nine corporates rated ‘B+’ and lower and upgraded only four similarly

rated companies. This compares with 23 upgrades and 21 downgrades for its broader Latin

America corporate portfolio. The 2.2x ratio of downgrades to upgrades during 2012 should

revert to around 1.0x during 2013.

Negative Leverage Trends: Leverage ratios have been weakening since 2009 for the 48

companies rated ‘B+’ and lower due to USD16 billion of additional debt, which was offset by

only USD1.4 billion of additional EBITDA. Lower levels of capex in 2013 and an improving

operating environment should reverse the trend. During the LTM, the aggregate total

debt/EBITDA ratio for these companies was 4.2x, while their collective net debt/EBTIDA ratio

was 3.4x. In comparison, during 2009 these leverage ratios were 3.4x and 2.5x, respectively.

Modest Direct Exposure to China and Commodities: Direct exposure to China and

commodity prices is low among the weakest credits in Latin America. Only seven of the 48

speculative corporates are in the metals and mining, pulp and paper, or oil and gas sectors.

All of their businesses are focused on their respective domestic markets.

Above-Average Recovery Prospects in the Event of a Default: Fitch’s bespoke analysis for

36 companies that have issued USD20 billion of bonds in the international capital markets

indicates above-average aggregate recovery levels of 70% in the event of a default. Concerns

about the bankruptcy framework in many markets, as well as the application and enforcement

of existing laws, can limit the uplift on issuance ratings.

Analysts Joe Bormann, CFA +1 312 368-3349 [email protected]

Jay Djemal +1 312 263-1032 [email protected]

Yolanda Torres +1 312 606-2301 [email protected]

Juan Pablo Arias +1 312 606-2329 [email protected]

Ingo Araujo +55 11 4504-2205 [email protected]

Ana P. Ares +54 11 5235-8121 [email protected]

Lucas Aristizabal +1 312 368-3260 [email protected]

Miguel Guzman Betancourt +52 81 8399-9100 [email protected]

Gabriela A. Catri +54 11 5235-8129 [email protected]

John C. Culver, CFA +1 312 368-3216 [email protected]

Gabriela Curutchet +54 11 5235-8122 [email protected]

Rogelio Gonzalez +52 81 8399-9100 [email protected]

Debora Jalles +55 21 4503-2629 [email protected]

Josseline Jenssen +591 2 277-4470 [email protected]

Viktoria Krane +1 212 908-0367, x1367 [email protected]

Managing Director of Latin America Corporates Daniel R. Kastholm, CFA +1 312 368-2070 [email protected]

Editorial Advisor Traci Dixon, Editor

Latin America High Yield 2

November 8, 2012

Corporates

Strong Balance Sheets but High Government Meddling in Argentina: Argentine corporates

have strong capital structures to mitigate issues such as high inflation, government intervention,

economic uncertainty, and limited access to debt markets. Access to local and international

debt markets is restricted due to concerns about the sovereign.

Brazilian Corporates Should Benefit from Government Actions: Brazilian corporates in the

‘B’ category are the most leveraged in Latin America. A rebound in the Brazilian economy

would be an important step in reversing the negative credit trends that have developed since

2009. Small companies such as Cimento Tupi, Rodopa, Sifco, and Virgolino would benefit

most from improving cash flow trends, as they do not have the business profile to attract

lending under a distressed scenario.

Corporate Governance Remains a Key Concern in Mexico: Many of the weakest credits in

Mexico are controlled by families. Concern about corporate governance is extremely high

among investors due to a bankruptcy regime that allows intra-company loans to be treated pari

pasu with external debt. From a macro perspective, the near-term outlook for Mexican

corporates is positive due to a rebound in its manufacturing sector.

2012 Portfolio Overview and Performance Review

Fitch’s portfolio of corporates rated ‘B+’ and lower grew to 48 issuers in 2012 from 43 during

2011. The growth of the this speculative group of issuers was due to the addition of five new

ratings in the ‘B’ category — Corporacion Electrica Nacional (Corpoelec), Maestro Peru,

Rodopa Industria e Comercio de Alimentos Ltda., SANLUIS Rassini, Virgolino de Oliveira S.A.,

and Acucar e Alcool — and the downgrade of four credits into the ‘B’ category from the ‘BB’

category — Corporacion Pesquera Inca SAC (COPEINCA), GOL Linhas Aereas Inteligentes

S.A., Pan American Energy LLC, and Urbi Desarrollos Urbanos, S.A.B. de C.V.

During 2012, Fitch withdrew the ‘B–’ rating of Agro Industrial Vista Alegre Ltda., the ‘B’ rating of

ODS S.A. and the ‘B’ rating of Galvao Participações. The only company to get upgraded out of

the ‘B’ category was TAM S.A., which was upgraded to ‘BB’ from ‘B+’ following its merger with

LATAM Airlines Group.

The credit performance of these 48 corporates was weaker than Fitch’s broader Latin America

portfolio. During the first nine months of 2012, Fitch upgraded the ratings of 23 corporates in

Latin America and downgraded the ratings of 21 companies. In contrast, among the highly

speculative ratings, downgrades outpaced upgrades by a ratio of 2.2x, as Fitch downgraded

nine corporates and only upgraded the ratings of four companies rated ‘B+’ or lower.

Upgrades included Arendal to ‘B’ from ‘B–’; TGN to ‘CCC’ from ‘D’; Grupo Senda to ‘B’ from

‘B–’; and TAM to ‘BB’ from ‘B+’. Notable downgrades include Urbi to ‘B’ from ‘BB–’; OGX to ‘B’

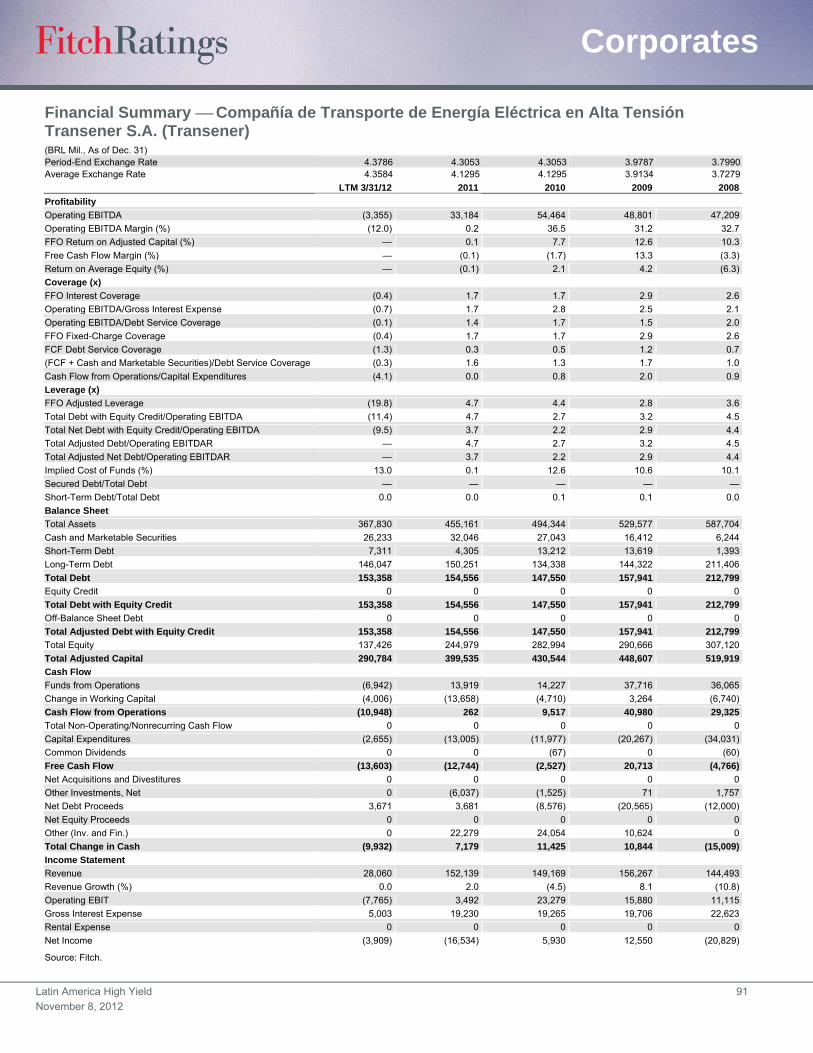

from ‘B+’; Axtel to ‘B–’, Rating Watch Negative, from ‘B’; and Transener to ‘CCC’ from ‘B–’.

The only defaults among Latin America corporates during 2012 were those of Rede Energia

and its subsidiaries, Centrais Eletricas do Para (Celpa) and Centrais Eletricas Matogrossenses

S.A. (Cemat). Rede Energia had been rated ‘B–’ since 2009 and was downgraded to ‘CCC’ in

2011, while Celpa and Cemat had been rated ‘B–’ since 2011. These defaults were due to the

lethal combination of weak liquidity, high leverage, poor cash flow generation, and large

investments.

Analysts (Continued) Francisco Mercadal +5 62 499-3340 [email protected]

Cecilia Minguillón +54 11 5235-8123 [email protected]

Alberto Moreno +52 81 8399-9100 [email protected]

Natalia O’Byrne +57 1 326-9999 [email protected]

Gisele Paolino +55 21 4503-2624 [email protected]

Renata Pinho +55 11 4504-2207 [email protected]

Sergio.Rodriguez, CFA +5281 8399-9100 [email protected]

Indalecio Riojas +52 81 8399-9100 [email protected]

Jose R. Romero +55 11 4504-2601 [email protected]

Alberto de los Santos +52 81 8399-9100 [email protected]

Mauro Storino +55 11 4503-2625 [email protected]

Fernando Torres +55 11 5235-8124 [email protected]

Julio Ugueto +58 212 286-3232 [email protected]

Jose Vertiz +1 212 908-0641 [email protected]

Liliana Yabiku +55 11 4504-2208 [email protected]

Latin America High Yield 3

November 8, 2012

Corporates

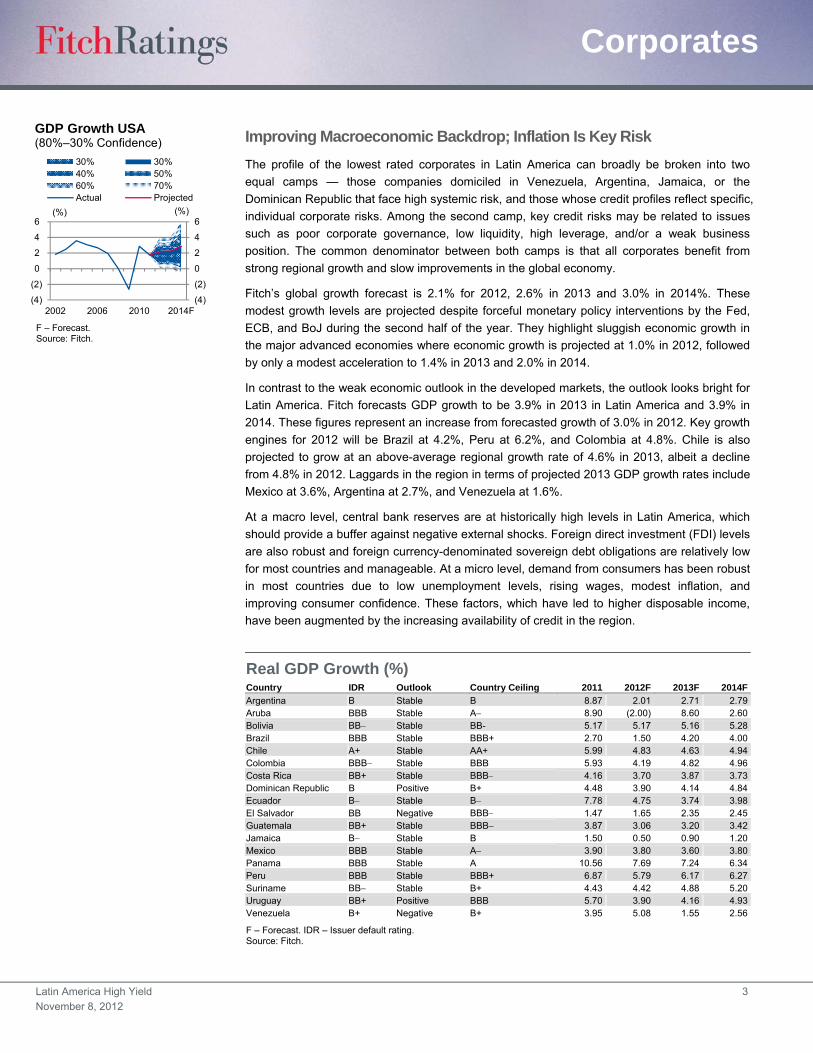

Improving Macroeconomic Backdrop; Inflation Is Key Risk

The profile of the lowest rated corporates in Latin America can broadly be broken into two

equal camps — those companies domiciled in Venezuela, Argentina, Jamaica, or the

Dominican Republic that face high systemic risk, and those whose credit profiles reflect specific,

individual corporate risks. Among the second camp, key credit risks may be related to issues

such as poor corporate governance, low liquidity, high leverage, and/or a weak business

position. The common denominator between both camps is that all corporates benefit from

strong regional growth and slow improvements in the global economy.

Fitch’s global growth forecast is 2.1% for 2012, 2.6% in 2013 and 3.0% in 2014%. These

modest growth levels are projected despite forceful monetary policy interventions by the Fed,

ECB, and BoJ during the second half of the year. They highlight sluggish economic growth in

the major advanced economies where economic growth is projected at 1.0% in 2012, followed

by only a modest acceleration to 1.4% in 2013 and 2.0% in 2014.

In contrast to the weak economic outlook in the developed markets, the outlook looks bright for

Latin America. Fitch forecasts GDP growth to be 3.9% in 2013 in Latin America and 3.9% in

2014. These figures represent an increase from forecasted growth of 3.0% in 2012. Key growth

engines for 2012 will be Brazil at 4.2%, Peru at 6.2%, and Colombia at 4.8%. Chile is also

projected to grow at an above-average regional growth rate of 4.6% in 2013, albeit a decline

from 4.8% in 2012. Laggards in the region in terms of projected 2013 GDP growth rates include

Mexico at 3.6%, Argentina at 2.7%, and Venezuela at 1.6%.

At a macro level, central bank reserves are at historically high levels in Latin America, which

should provide a buffer against negative external shocks. Foreign direct investment (FDI) levels

are also robust and foreign currency-denominated sovereign debt obligations are relatively low

for most countries and manageable. At a micro level, demand from consumers has been robust

in most countries due to low unemployment levels, rising wages, modest inflation, and

improving consumer confidence. These factors, which have led to higher disposable income,

have been augmented by the increasing availability of credit in the region.

(4)

(2)

0

2

4

6

2002 2006 2010 2014F(4)

(2)

0

2

4

6

30% 30%40% 50%60% 70%Actual Projected

F – Forecast.Source: Fitch.

GDP Growth USA(80%–30% Confidence)

(%) (%)

Real GDP Growth (%) Country IDR Outlook Country Ceiling 2011 2012F 2013F 2014F

Argentina B Stable B 8.87 2.01 2.71 2.79Aruba BBB Stable A 8.90 (2.00) 8.60 2.60Bolivia BB Stable BB- 5.17 5.17 5.16 5.28Brazil BBB Stable BBB+ 2.70 1.50 4.20 4.00Chile A+ Stable AA+ 5.99 4.83 4.63 4.94Colombia BBB Stable BBB 5.93 4.19 4.82 4.96Costa Rica BB+ Stable BBB 4.16 3.70 3.87 3.73Dominican Republic B Positive B+ 4.48 3.90 4.14 4.84Ecuador B Stable B 7.78 4.75 3.74 3.98El Salvador BB Negative BBB 1.47 1.65 2.35 2.45Guatemala BB+ Stable BBB 3.87 3.06 3.20 3.42Jamaica B Stable B 1.50 0.50 0.90 1.20Mexico BBB Stable A 3.90 3.80 3.60 3.80Panama BBB Stable A 10.56 7.69 7.24 6.34Peru BBB Stable BBB+ 6.87 5.79 6.17 6.27Suriname BB Stable B+ 4.43 4.42 4.88 5.20Uruguay BB+ Positive BBB 5.70 3.90 4.16 4.93Venezuela B+ Negative B+ 3.95 5.08 1.55 2.56

F – Forecast. IDR – Issuer default rating. Source: Fitch.

Latin America High Yield 4

November 8, 2012

Corporates

Inflation remains a key risk for the region as loose monetary and fiscal policies in developed

markets have increased the money supply. Several central banks in Latin America have taken

actions to weaken their currencies in response to the measure taken by the Fed, ECB, and BoJ.

In Latin America, food and energy are a disproportionally high percentage of the consumer

basket. Food, as a percentage of the CPI basket, is more than 35% in Peru and ranges

between 20% and 30% in Brazil, Colombia, and Mexico. Any sharp increase in the prices for

these items could weaken disposable income in the region and could lower demand.

Weakening Leverage Trend Should Abate

Leverage ratios have been trending down since 2009 due to a USD16 billion increase in

aggregate debt levels and only a USD1.4 billion increase in EBITDA. During the last 12 months

(LTM), the aggregate total debt/EBITDA ratio for the companies rated ‘B+’ and lower was 4.2x,

while the net debt/EBTIDA ratio was 3.4x. The former ratio compares unfavorably with ratios of

4.0x in 2011, 3.5x in 2010, and 3.4x in 2009, while the net leverage ratio shows weakness

versus 3.1x in 2011, 2.6x in 2010, and 2.5x in 2009.

Combined, the group of credits rated ‘B+’ and lower have USD12 billion of cash, USD13 billion

of short-term debt obligations and USD63 billion of total debt obligations. These figures

compare with USD15.1 billion of EBITDA generation during the LTM. They exclude PDVSA,

which is owned by the Venezuelan government and is disproportionally large relative to the

other 47 corporates.

Leverage is significantly higher for the group if you eliminate the 24 companies domiciled in

countries rated ‘B+’ or lower, whose ratings are capped by the sovereign ceilings of Argentina,

Venezuela, the Dominican Republic, and Jamaica. The trends are also negative for this group

of corporates.

During the LTM, the 24 companies domiciled in the investment-grade countries — Brazil,

Mexico, and Peru — generated USD5.4 billion of EBITDA. This compares with USD5.5 billion

in 2011, USD6.2 billion in 2010, and USD5.6 billion in 2009. Total debt for these 24 companies

increased to USD45 billion from USD34 billion during this time period, while cash and

marketable securities declined to USD9 billion from USD10 billion.

As a group, the total leverage ratio of the companies in investment-grade markets climbed to

8.4x from 6.1x, while net leverage rose to 6.8x from 4.4x. These ratios are heavily affected,

however, by the increasing leverage of large companies such as Marfrig, Minerva, OGX, and

CEMEX. Median ratios show far less leverage but similar trends. The median net leverage ratio

of the Brazilian, Mexican, and Peruvian corporates was 3.8x in the LTM, similar to 2011 levels,

but up from 3.2x in 2009.

Robust Debt Capital Market Activity to Continue; History Suggests Caution

Issuance totals were at elevated levels during 2012, as investors aggressively sought emerging

market corporate debt due to slow economic growth rates and low interest rates in developed

markets. Many Latin America corporates improved their capital structures by accessing

financing with lower rates and longer tenors.

Growth in the BRICs (%) 2011 2012F 2013F 2014F

Brazil 2.7 1.5 4.2 4 Russia 4.3 3.5 3.5 4 Indiaᵃ 6.5 6 7 7.5 China 9.2 7.8 8.2 7.5 aIndia forecasts represent fiscal years: 2011 = FY12, 2012 = FY13. F – Forecast. Source: Fitch.

(5)

0

5

10

15

Net ExportsInvestmentGovernment ConsumptionPrivate ConsumptionGDP

Source: IBGE, Fitch.

(Year over Year %)

BRIC Contributions to Quarterly Real GDP Growth

(10)(5)05

10152025

Source: FGV.

(%)

BRIC Industrial Production(Year-over-Year Growth)

Latin America High Yield 5

November 8, 2012

Corporates

During the first nine months of 2012, Latin America corporates issued USD48 billion of debt in

the international capital markets. This compares favorably with the yearly totals for 2011, 2010,

and 2009 of USD 51 billion, USD 44 billion, and USD 40 billion, respectively.

Market activity was widespread and constant throughout the year. Through the first nine

months, 70 different issuances occurred. This total is equal to that for all of 2011 and only

slightly lower than the level achieved in 2010, when 72 different transactions occurred. The

strong volumes heading into the last quarter suggest that new levels of market activity will be

reached. In contrast to 2011, where market activity ground to a halt during the second half of

the year following the acceleration of the euro crisis, cross border debt activity was relatively

constant throughout 2012.

High risk credits benefited from the strong market. Cemex, Digicel, Maestro, Minerva, PDVSA,

Virgolino, Cimento Tupi, OAS, OGX, and VRG Linhas Aereas issued about USD9 billion of

debt in the international capital markets, or about 20% of the cross border market activity.

Local markets have also been a healthy source of funding for Latin America corporates. During

the first nine months of 2012, Latin America corporates raised USD20 billion of debt through

141 issuances in the local debt capital markets. The most robust market in the region was

Brazil, which accounted for USD14 billion of the total activity through 57 separate issuances.

History suggests that Latin America corporates cannot count on market windows being open at

all moments. The market was essentially closed to Latin America corporates during the third

and fourth quarter of 2008 and during the month of August during 2011. Some of the largest

debt amortizations occurring before the end of 2014 are those of Grupo Posadas

(MXN2.250 billion, April 2013), and Digicel (USD510 million, April 2014).

Eurozone Financial Crisis Should Not Hurt Access to Credit in 2013

Risks related to the Euro financial crisis remain the most crucial global risk monitored by Fitch

in terms of urgency and the potential negative impact upon credits globally. As of Sept. 30,

2012, 45% of Western European sovereign ratings had a Negative Outlook, as did 37% of the

financial institutions in the region and 21% of corporates. Weak business and household

sentiment in the region, high unemployment levels, tight financing conditions and the impact of

fiscal consolidation on domestic economic activity will curb growth in the eurozone. For 2012,

Fitch projects that GDP in the eurozone will contract by 0.5%. During 2013 and 2014, Fitch

projects continued weak growth rates of 0.3% and 1.4%, respectively.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

International Domestic Total

Source: Fitch Ratings.

(USD Bil.)

Non-FI Latin America Corporate Debt Issuance (First-Quarter 2006–Thrid-Quarter 2012)

(4)

(2)

0

2

4

6

2002 2006 2010 2014F(4)

(2)

0

2

4

6

30% 30%40% 50%60% 70%Actual Projected

F – Forecast.Source: Fitch.

GDP Growth Euro Zone(80%–30% Confidence)

(%) (%)

Latin America High Yield 6

November 8, 2012

Corporates

Key euro-related risks for speculative Latin America corporates are whether capital market

access would disappear for a prolonged period of time and if bank lines would be withdrawn.

Secondary risks would be whether economic growth rates in the region would drop sharply if

broad-based support for the euro dissolved, which is not Fitch’s base case, and whether export

opportunities would diminish.

Positively for all corporates, including the ‘B’ rated companies in Latin America, concern over

the potential for a shock to the eurozone from a disorderly default has been lessened as

ongoing negotiations among politicians in Europe represent a willingness to maintain the

European Union. The willingness to make concessions, as well as the aggressive position

taken by the ECB, should result in a gradual normalization of financial market conditions.

Fitch’s base case scenario is that credit market access for Latin America corporates during

2013 will grow vis-à-vis 2012 given low interest rates and strong demand for emerging market

debt. This type of environment suggests that most corporates will have the opportunity to

refinance upcoming debt obligations, including the most speculative credits. It is doubtful,

however, that the pace of market activity will remain as steady as 2012.

The risk of bank credits being withdrawn from ‘B’ credits in Latin America due to the Euro crisis

is small and should be manageable. The largest foreign banking presence in the region is in

Chile, where foreign loans as a percentage of GDP is estimated to be close to 30%. Fitch has

no corporates rated in the ‘B’ range in that country. In contrast, the presence of foreign banks is

low in the countries where 60% of the ‘B’ rated corporates are domiciled — Argentina and

Brazil. In Brazil, foreign bank loans are less than 10% of GDP and in Argentina they are less

than 4% of GDP. If a credit line is withdrawn by a foreign bank in Brazil, most companies with

reasonable business prospects should be able to obtain financing either from a government or

private sector bank. The foreign banking presence in Mexico and Peru ranges between 12%

and 15% of GDP. These two countries combined account for 23% of the lowest rated credits.

Modest Direct Exposure to China and Commodities

The slowdown in China’s economy to 7.6% in second-quarter 2012 from 9.3% in 2011 has

refocused attention on the possibility of slower future growth rates. Fitch has trimmed its

expectations for China’s 2012 growth to 7.8% and expects growth to rebound slightly to 8.2%

in 2013 due to some modest quasi-fiscal stimulus.

Direct exposure to China and commodity prices is low among the weakest credits. Only seven

of the 48 speculative corporates are in the metals and mining, pulp and paper, or oil and gas

sectors. All of their businesses are focused on their respective domestic markets. None of them

export to China. Two Brazilian protein producers, Marfrig and Minerva, have a very small

percentage of their revenues linked to China — Minerva through exports and Marfrig via a joint

venture.

Despite modest direct links to China among these credits, the indirect impact upon companies

cannot be underestimated due to China’s size and contribution to global growth. Since 2006,

the level of exports from Latin America to China has increased to USD76 billion in 2010 from

USD25 billion. Nearly 77% of the region’s commodity sales and 70% of its total exports to

China were comprised by only eight primary products: copper, feedstuff, gas, meat, metal ores

and scrap, oil, pulp, and soy.

Trade Balance with China Five-Year Average (20062010) Country X/GDP M/GDP TB/GDP

Chile 6.2 3.5 2.7 Costa Rica 3.6 2.5 1.1 Peru 3.0 2.6 0.4 Venezuela 1.5 1.2 0.3 Brazil 1.1 1.0 0.0 Argentina 1.7 1.8 (0.2) Bolivia 0.8 1.2 (0.5) Aruba 0.0 0.9 (0.9) Dom. Rep. 0.3 1.4 (1.1) Jamaica 0.7 1.9 (1.2) Colombia 0.4 1.7 (1.3) Uruguay 1.0 2.4 (1.4) El Salvador 0.0 2.0 (2.0) Guatemala 0.1 2.2 (2.1) Ecuador 0.4 3.0 (2.6) Suriname 0.3 3.2 (2.8) Mexico 0.2 3.4 (3.1) Panama 0.0 5.6 (5.6) LatAm 1.1 2.0 (0.8)

X – Exports. M – Imports. TB – Trade balance. Source: UNCTAD, Fitch.

Latin America High Yield 7

November 8, 2012

Corporates

Five Latin American economies — Brazil, Chile, Costa Rica, Peru, and Venezuela —

accounted for 81% of the total regional sales to the Asian giant in 2010. Among them, Brazil,

Chile, and Peru have achieved the greatest ratings momentum by turning a cyclical upturn into

credit strength, as they strengthened their external liquidity and solvency positions. Colombia

has also benefited. On the other side of the equation, Jamaica and the Dominican Republic

have suffered from rising energy and food costs, as it imports these products. These countries

faced balance of payments imbalances and confidence shocks, making them reliant upon the

IMF.

Higher Government Meddling in Argentina; Strong Balance Sheets

Argentine corporates represent 16 of the 48 companies rated in the ‘B’ category or lower by

Fitch. These companies have strong capital structures to mitigate issues such as high inflation,

government intervention, economic uncertainty, and limited access to debt markets. The

median liquidity ratio (measured by cash plus EBITDA/short-term debt) of these corporates is

2.0x, while the median leverage ratio is 1.6x. These key credit protection measures are much

stronger than that of their ‘B’ rated peer group, which are not constrained by systemic

government risk.

All but two of the corporate ratings in Argentina are capped by the ‘B’ country ceiling of the

Argentine government due to their exposure to the imposition of transfer and convertibility

restrictions on foreign currency. The trend has not been positive for capital controls as the

government has tightened exchange restrictions in response to declining reserve levels.

Several of the ratings were placed on Rating Watch Negative on Oct 31, 2012, following Fitch's

decision to place the ‘B’ foreign currency issuer default rting (IDR) of the Republic of Argentina

(Argentina) on Rating Watch Negative, as a result of increased uncertainty about the

government’s ability to service its international securities issued under New York Law due to a

ruling in a U.S. court about on a timely basis using the U.S. financial system. In and of itself,

this ruling should not directly affect the ability of the Argentine corporates to make payments on

their foreign currency obligations using the U.S. financial system. Indirectly, this ruling may

further affect the willingness of the Argentine government to provide corporates with foreign

exchange to make payments to their cross currency debt obligations.

Debt capital market activity has been limited for Argentine corporates due to concerns about

government interference in the private sector. During 2012, no Argentine corporate issued

bonds in the international markets. International issuances have ground to a halt following the

government’s actions after the 2011 elections — particularly the nationalization of YPF, the

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Oil Soy Copper Gold

Source: Bloomberg, Fitch.

(Index)

A Decade-Long Commodity Price Boom(Jan. 2000 = 100)

Fitch’s Ratings Actions During the Commodity Boom (2003–2011)

Country LT FC IDR

Net Notching

Brazil BBB 6 Argentinaª B 5 Peru BBB 4 Uruguayª BB+ 4 Bolivia B+ 2 Chile A+ 2 Colombia BBB 2 Panama BBB 2 Costa Rica BB+ 1 Ecuadorª B 1 Mexico BBB 1 Suriname B+ 1 Venezuela B+ 1 Aruba BBB 0 Guatemala BB+ 0 Dom. Rep.ª B -1 El Salvador BB -1 Jamaicaª B -2

ªTotals are influenced by multi-notch upgrades/downgrades during sovereign defaults or restructuring exercises. Note: Countries in bold have deeper trade and financial linkages with China. LT – Long-term. FC – Foreign currency. IDR – Issuer default ratings. Source: Fitch.

Latin America High Yield 8

November 8, 2012

Corporates

imposition of additional capital controls on select industries, and the change in the central

bank’s charter. Among companies with international ratings, only IRSA, IMPSA, Cresud, and

YPF placed bonds in the domestic market during 2012. Many companies are reluctant to tap

the local debt market following the nationalization of the pension funds, as they seek to limit the

government’s ownership of their stock and bonds.

Argentina’s economy is intertwined with Brazil’s through exports, as it ships about 20% of its

exports to Brazil — or close to 40% of its total Latin America exports. These corporates could

benefit from a cyclical rebound in the Brazilian economy that should lead to growth in excess of

4% in Brazil during 2013. Approximately 67% of Argentine exports to Brazil are in the

manufacturing sector. Vehicles and auto parts make up the bulk of this number. This sector

should perform well in 2013. Argentina is also highly reliant upon the export of soybeans, which

should enjoy a good year due to the record drought in the U.S. that has led to elevated soy

prices globally.

Brazil Corporates Should Benefit from Government Actions; Trends Have Been Negative

Brazilian corporates in the ‘B’ category are the most leveraged in Latin America and the credit

protection measures have been weakening both in relative and aggregate terms. The dozen

speculative credits in Brazil can be roughly divided into two groups: small companies with low

leverage and large companies such as Marfrig, OAS, and GOX that have weak capital

structures.

A rebound in the Brazilian economy would be an important step in reversing the negative

trends that have developed since 2009. Small companies such as Cimento Tupi, Rodopa, Sifco,

and Virgolino would benefit most from improving cash flow trends, as they do not have the

business profile to attract lending under a distressed scenario.

Fitch expects growth to reach 4.2% in Brazil during 2013, a sharp improvement from

forecasted growth of 1.5% in 2012. The poor 2012 performance is a result of the weak

industrial sector, which contracted by 2.4% in the second quarter. This sector’s performance

was hurt by soft external market conditions and rising costs.

Monetary stimulus as well as temporary tax breaks and continued quasi-fiscal stimulus through

the development bank BNDES will be key components of the recovery. Key sales tax breaks

include those on autos and white goods. Cement, steel, and construction companies should

benefit from the government’s USD66 billion plan to improve the country’s infrastructure.

In terms of competitiveness, manufacturing companies should be better able to compete with

their global peers due to measures the government recently took to reduce electricity tariffs.

Exporters should benefit from a Brazilian real that is managed by the government to be in the

range of BRL2.0/USD. This exchange level should also slow the tide of imports, as will import

tariffs on approximately 100 different goods.

The aggregate total leverage ratio for the dozen Brazilian credits rated in the highly speculative

category was 12.6x during the LTM, while the net leverage ratio was 8.5x. These are increases

from 9.5x and 5.8x in 2011. Some of the largest companies — Rede, OGX, OAS, GOL, and

Virgolino — have driven the weakening of aggregate protection measures.

Median ratios, which eliminate the impact of the large and highly leveraged companies, show

lower leverage levels, but also highlight negative trends. For the LTM, the median net leverage

0

10

20

30

40

50

60

China E.U.

LatAm U.S.

Source: UNCTAD, Fitch.

(%)

LatAm's Main Trading Partners(% of Total Exports and Imports )

Latin America High Yield 9

November 8, 2012

Corporates

ratio of the Brazilian credits was 5.2x. This ratio compares unfavorably with those of 4.5x in

2011 and 4.0x in 2010 and is about 60% higher than during 2009 when it was 3.2x.

Corporate Governance Remains a Key Concern in Mexico

The 10 credits in Mexico rated in the range of ‘B+’ or lower are in industries such as cement,

home building, auto parts, oil services, food and beverage, packaging, retailing, lodging, and

transportation. This disparate group of credits have few things in common other than high

leverage. Some corporates, such as Arendal and Axtel, are small relative to their competitors.

Others, such as Urbi and Javer, are relatively big companies within fragmented industries that

exhibit high operating risk. Several companies are in the ‘B’ category because their

management teams have made poor strategic or financial decisions. This group includes

companies such as Posadas, Cemex, Bio-Pappel, Senda, and SANLUIS.

Unlike its peers in Brazil, the Mexican credits have been deleveraging during the past few

years. The median net leverage ratio of the Mexican credits during the LTM was 3.3x. This

ratio compares with 3.8x in 2011 and 3.7x in 2010 and 4.3x in 2009.

From a macro perspective, the near-term outlook for Mexican corporates is positive. Mexico’s

exposure to the U.S. is high due to trade and remittances. For 2013 and 2014, Fitch projects

U.S. growth rates of 2.25% and 2.8%, respectively. These growth rates should support growth

levels in Mexico of about 3.6% in 2013 and 3.8% during 2014. Continuing challenges that need

to be addressed to increase Mexico’s low growth rate relative to other emerging economies are

the country’s moderate saving and investment rates, monopolies in important industries, state

ownership of the energy sector, high labor informality, and limited flexibility.

A bright spot for the Mexican economy has been a revival of its manufacturing sector due to

the country’s close proximity to the U.S. market and rising costs in China. The auto sector has

probably been the sector that has benefited to the greatest degree. Unlike several countries in

Latin America that have a high degree of exposure to China and commodity prices, Mexico’s

risks as they relate to those issues are more modest. Exports to China have averaged about

0.2% of GDP during the past five years, while imports have averaged 3.4% of GDP.

While corporate governance is a global credit concern, unease is extremely high among

investors in the weakest credits in Mexico. The bankruptcy regime in Mexico is relatively new

and untested. There is a lack of precedent on many issues and rulings can be unpredictable.

Many of the lowest rated Mexican corporates are controlled by families, despite being publicly

traded companies. The participation of key family members as executives in business

operations is high and there is often a lack of independent members in the board of directors.

Related party transactions are numerous.

The actions of Mexican glassmaker Vitro have elevated concerns about corporate governance

and Mexico’s bankruptcy regime. Vitro defaulted on its debt during 2009 due to declining

demand for glass from construction and auto manufacturers, losses on derivative instruments,

and a weak capital structure. After the default, the company created a very large intracompany

loan. In late 2010, the company filed for bankruptcy and these intracompany loans were

recognized by the judge in the case, which allowed them to vote on the restructuring plan. This

essentially gave the company’s shareholders the ability to impose large losses on external

creditors and retain control.

Vitro’s actions could have repercussions for companies that want to issue bonds in the future.

CEMEX’s new facilities agreement, which was completed in September 2012, had restrictions

and conditions imposed on intercompany loans. Among them, any amount payable under any

Latin America High Yield 10

November 8, 2012

Corporates

intercompany claim of any obligor would be subordinated to claims under the new facilities

agreement and all other senior debt of such obligors in the event of insolvency or similar

proceedings in relation to Cemex. The Intercreditor Agreement established a Mexican-law

regulated voting trust mechanism whereby intercompany claims of Cemex entities incorporate

in Mexico at any time would be voted in a Concurso Mercantil proceeding in accordance with a

trustee that is under instruction from the third-party lenders under the new facilities agreement.

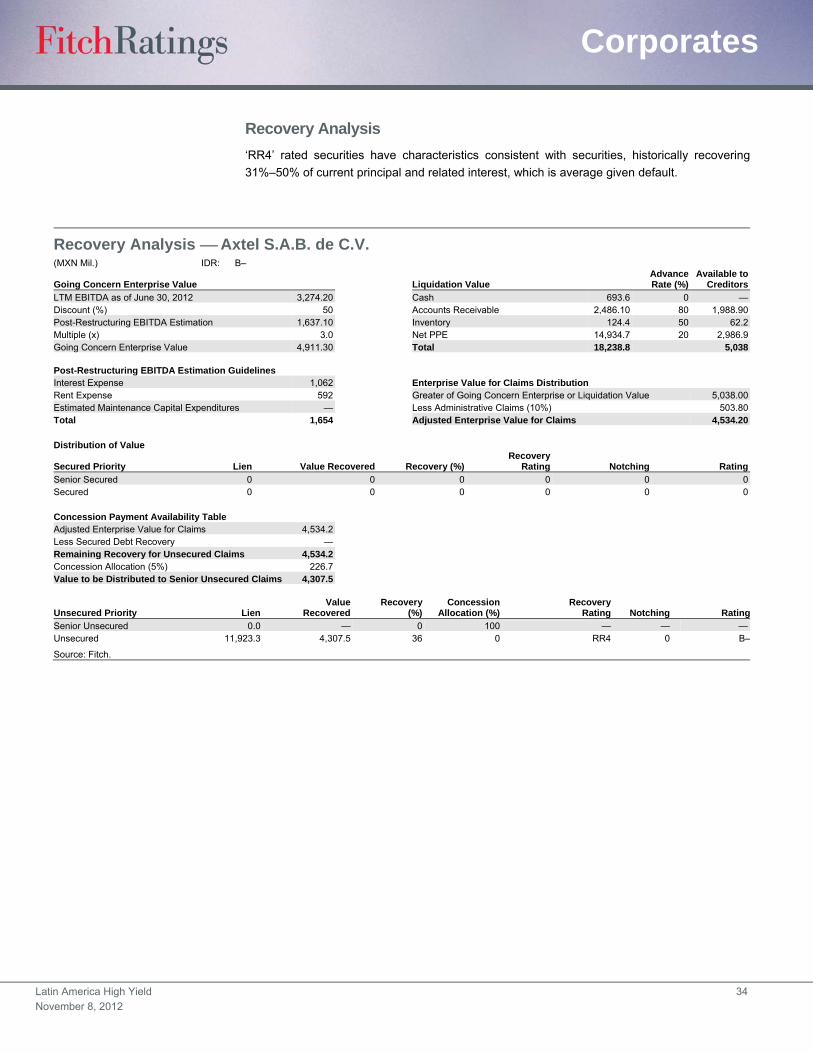

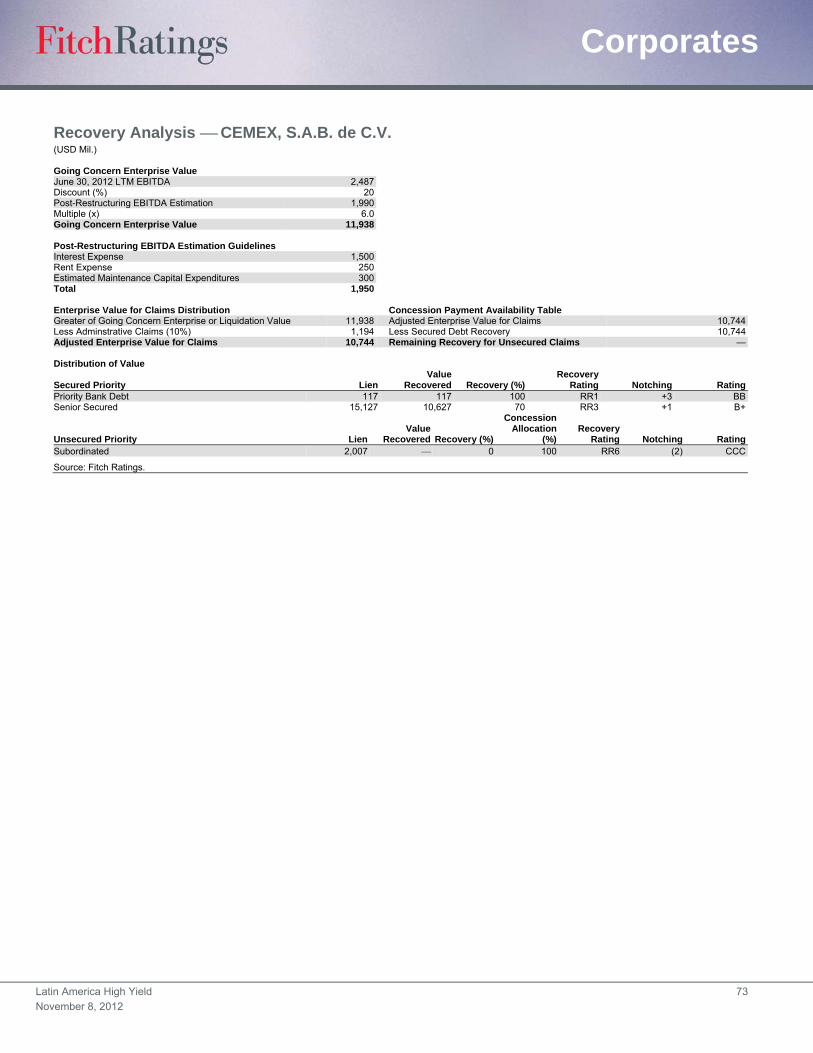

Recovery Prospects Are Above Average in the Event of a Default

Fitch’s bespoke analysis for 36 companies that have USD20 billion of bonds in the international

capital markets (excluding PDVSA) and have USD56 billion of combined debt indicates an

aggregate recovery of 70%. This recovery level is consistent with above-average recovery

expectations in the event of default, or an ‘RR3’ rating.

Despite high anticipated levels of recoveries, many of the rated bonds have been assigned

recovery ratings of ‘RR4’, which is consistent with recoveries in the range of 30%–50%. The

recovery ratings of many of these bonds were constrained due to concerns about the

bankruptcy framework in many markets, as well as the application and enforcement of existing

laws.

Fitch Default Rates by Major Sector: Jan. 1, 2012–June 30, 2012 (%) Global Corporates Latin America Corporates

AAA 0.00 0.00AA 0.00 0.00A 0.00 0.00BBB 0.00 0.00BB 0.00 0.00B 0.79 2.44CCCᵃ 15.38 33.33

Investment Grade 0.00 0.00Speculative Grade 1.07 1.78All 0.33 0.96

ᵃIncludes ‘CCC’ to ‘C’ for corporates, sovereigns, and public finance. Source: Fitch Ratings.

Latin America High Yield 11

November 8, 2012

Corporates

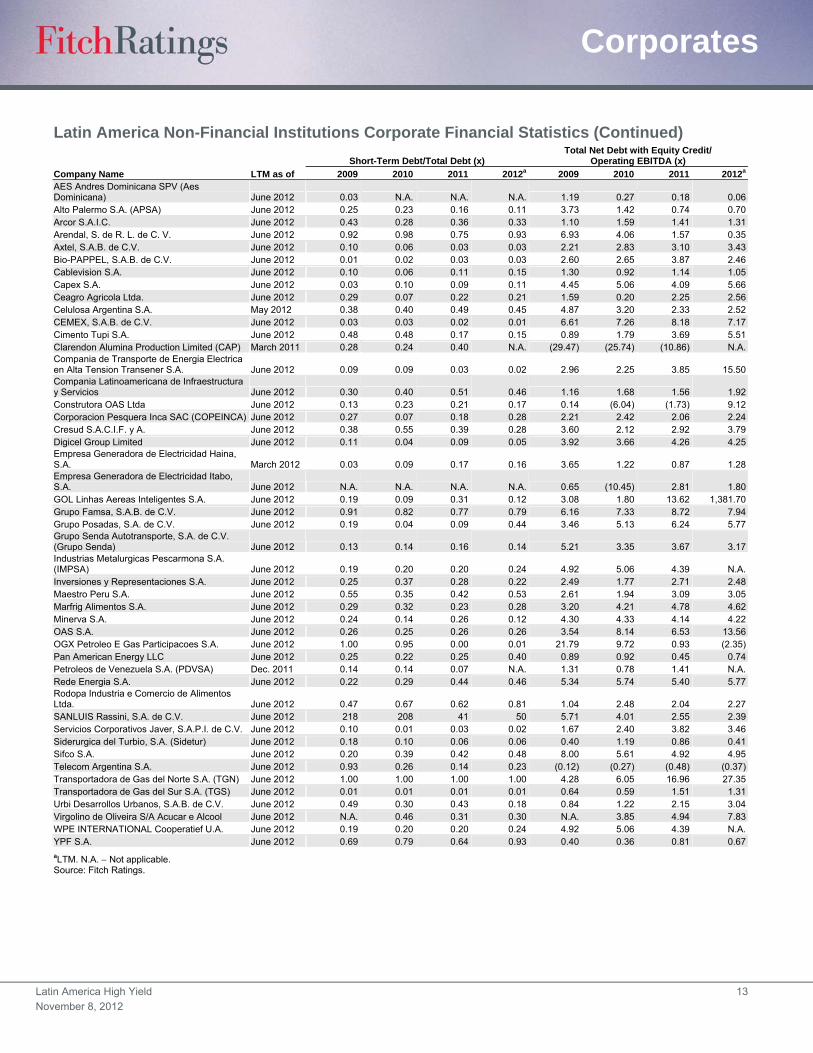

Latin America Non-Financial Institutions Corporate Financial Statistics (USD Mil.) Cash Total Short-Term Debt Total Debt

Company Name LTM as of 2009 2010 2011 2012a 2009 2010 2011 2012a 2009 2010 2011 2012a

AES Andres Dominicana SPV (Aes Dominicana) June 2012 63 120 131 155 5 N.A. N.A. N.A. 161 164 164 164Alto Palermo S.A. (APSA) June 2012 17 18 42 31 62 52 30 18 246 226 180 172Arcor S.A.I.C. June 2012 186 190 99 126 178 140 161 154 417 497 449 472Arendal, S. de R. L. de C. V. June 2012 5 5 6 24 29 31 27 35 31 32 35 37Axtel, S.A.B. de C.V. June 2012 107 106 102 51 72 53 27 26 758 844 894 873Bio-PAPPEL, S.A.B. de C.V. June 2012 75 59 69 80 3 7 9 9 260 275 282 248Cablevision S.A. June 2012 38 100 126 143 52 33 72 101 542 512 655 652Capex S.A. June 2012 24 26 45 6 8 20 20 27 261 199 230 238Ceagro Agricola Ltda. June 2012 4 120 43 24 10 9 34 31 34 131 156 149Celulosa Argentina S.A. May 2012 6 6 7 7 80 69 77 72 212 173 157 159CEMEX, S.A.B. de C.V. June 2012 1,080 676 1,153 611 595 465 381 109 19,381 17,894 18,162 17,251Cimento Tupi S.A. June 2012 9 5 28 35 20 30 26 33 42 63 155 215Clarendon Alumina Production Limited (CAP) March 2011 1 1 4 N.A. 128 89 169 N.A. 460 373 424 N.A.Compania de Transporte de Energia Electrica en Alta Tension Transener S.A. June 2012 16 27 32 28 14 13 4 4 159 148 155 154Compania Latinoamericana de Infraestructura y Servicios June 2012 93 83 95 61 58 107 159 159 192 268 313 346Construtora OAS Ltda June 2012 138 312 608 384 19 46 87 98 146 199 414 571Corporacion Pesquera Inca SAC (COPEINCA) June 2012 12 34 60 43 38 16 48 83 144 218 266 293Cresud S.A.C.I.F. y A. June 2012 56 76 173 110 142 272 322 242 372 490 832 858Digicel Group Limited June 2012 492 1,041 613 343 350 166 388 228 3,140 3,793 4,528 4,887Empresa Generadora de Electricidad Haina, S.A. March 2012 40 111 184 149 6 20 48 48 202 207 281 301Empresa Generadora de Electricidad Itabo, S.A. June 2012 79 72 53 51 N.A. N.A. N.A. N.A. 125 131 129 129GOL Linhas Aereas Inteligentes S.A. June 2012 818 1,174 1,205 843 340 205 835 300 1,801 2,219 2,685 2,590Grupo Famsa, S.A.B. de C.V. June 2012 131 90 104 134 786 898 890 987 864 1,100 1,162 1,257Grupo Posadas, S.A. de C.V. June 2012 50 47 30 35 72 17 40 194 380 471 452 443Grupo Senda Autotransporte, S.A. de C.V. (Grupo Senda) June 2012 11 11 12 7 29 30 35 30 222 218 225 216Industrias Metalurgicas Pescarmona S.A. (IMPSA) June 2012 93 62 53 61 111 117 169 324 578 579 845 1,343Inversiones y Representaciones S.A. June 2012 68 86 93 84 93 156 167 127 370 421 597 584Maestro Peru S.A. June 2012 4 6 6 6 29 19 46 64 53 55 111 122Marfrig Alimentos S.A. June 2012 1,743 2,299 1,871 1,499 942 1,911 1,491 1,698 3,252 6,055 6,437 6,143Minerva S.A. June 2012 244 342 402 405 167 141 291 139 703 972 1,131 1,204OAS S.A. June 2012 392 690 788 925 185 393 521 635 719 1,554 2,019 2,410OGX Petroleo E Gas Participacoes S.A. June 2012 4,216 2,516 2,936 2,942 173 134 12 43 173 141 2,574 3,994Pan American Energy LLC June 2012 232 434 958 753 384 381 447 747 1,554 1,759 1,756 1,874Petroleos de Venezuela S.A. (PDVSA) Dec. 2011 6,981 6,017 8,610 N.A. 2,956 3,604 2,396 N.A. 21,445 24,950 34,892 N.A.Rede Energia S.A. June 2012 238 451 369 221 857 1,352 1,939 1,729 3,893 4,600 4,429 3,725Rodopa Industria e Comercio de Alimentos Ltda. June 2012 2 15 19 18 8 37 57 79 16 55 92 98SANLUIS Rassini, S.A. de C.V. June 2012 13 21 21 37 218 208 41 50 233 364 250 259Servicios Corporativos Javer, S.A.P.I. de C.V. June 2012 62 40 30 27 21 2 8 4 201 210 276 275Siderurgica del Turbio, S.A. (Sidetur) June 2012 58 51 29 45 19 9 5 5 106 90 83 79Sifco S.A. June 2012 49 72 90 99 43 141 155 176 220 360 367 368Telecom Argentina S.A. June 2012 341 351 658 521 202 11 4 7 217 41 31 29Transportadora de Gas del Norte S.A. (TGN) June 2012 81 124 153 175 381 414 453 473 381 414 453 473Transportadora de Gas del Sur S.A. (TGS) June 2012 271 275 107 150 4 4 4 4 401 380 379 378Urbi Desarrollos Urbanos, S.A.B. de C.V. June 2012 336 487 395 432 295 263 461 259 603 888 1,067 1,426Virgolino de Oliveira S/A Acucar e Alcool June 2012 N.A. 23 54 91 N.A. 332 271 324 N.A. 717 879 1,092WPE INTERNATIONAL Cooperatief U.A. June 2012 93 62 53 61 111 117 169 324 578 579 845 1,343YPF S.A. June 2012 567 639 341 102 1,238 1,561 1,894 2,186 1,804 1,969 2,980 2,350

aLTM. N.A. Not applicable. Continued on next page. Source: Fitch Ratings.

Latin America High Yield 12

November 8, 2012

Corporates

Latin America Non-Financial Institutions Corporate Financial Statistics (Continued)

Operating EBITDA (USD Mil.) Cash/Short-Term Debt (x) Cash+EBITDA/

Short-Term Debt (x)

Company Name LTM as of 2009 2010 2011 2012a 2009 2010 2011 2012a 2009 2010 2011 2012a

AES Andres Dominicana SPV (Aes Dominicana) June 2012 82 164 183 150 12.60 N.A. N.A. N.A. 29.00 N.A. N.A. N.A.Alto Palermo S.A. (APSA) June 2012 49 113 144 157 0.27 0.34 1.41 1.71 1.05 2.49 6.27 10.37 Arcor S.A.I.C. June 2012 210 193 248 265 1.04 1.36 0.62 0.82 2.22 2.74 2.16 2.54 Arendal, S. de R. L. de C. V. June 2012 4 7 18 36 0.17 0.17 0.24 0.70 0.30 0.38 0.93 1.75 Axtel, S.A.B. de C.V. June 2012 294 261 256 240 1.48 1.99 3.74 1.95 5.55 6.91 13.13 11.15 Bio-PAPPEL, S.A.B. de C.V. June 2012 71 81 55 68 23.23 9.02 7.68 9.25 45.36 21.34 13.78 17.13 Cablevision S.A. June 2012 389 449 464 483 0.73 3.07 1.76 1.42 8.22 16.86 8.26 6.22 Capex S.A. June 2012 53 34 45 41 3.18 1.25 2.22 0.22 10.21 2.93 4.44 1.75 Ceagro Agricola Ltda. June 2012 19 58 50 49 0.36 12.98 1.27 0.78 2.31 19.31 2.77 2.37 Celulosa Argentina S.A. May 2012 42 52 65 60 0.08 0.08 0.09 0.10 0.60 0.84 0.93 0.93 CEMEX, S.A.B. de C.V. June 2012 2,768 2,372 2,080 2,321 1.82 1.45 3.02 5.62 6.47 6.55 8.48 26.97 Cimento Tupi S.A. June 2012 37 32 34 33 0.46 0.15 1.06 1.05 2.26 1.23 2.37 2.04 Clarendon Alumina Production Limited (CAP) March 2011 (16) (14) (39) N.A. 0.01 0.01 0.02 N.A. (0.11) (0.15) (0.20) N.A.Compania de Transporte de Energia Electrica en Alta Tension Transener S.A. June 2012 48 54 32 8 1.21 2.05 7.44 7.36 4.72 6.10 14.84 9.48 Compania Latinoamericana de Infraestructura y Servicios June 2012 85 110 140 148 1.60 0.78 0.60 0.38 3.06 1.81 1.47 1.31 Construtora OAS Ltda June 2012 63 19 112 21 7.24 6.74 6.98 3.90 10.58 7.14 8.27 4.11 Corporacion Pesquera Inca SAC (COPEINCA) June 2012 60 76 100 112 0.33 2.13 1.27 0.52 1.88 6.85 3.36 1.87 Cresud S.A.C.I.F. y A. June 2012 88 195 226 197 0.39 0.28 0.54 0.45 1.01 1.00 1.24 1.27 Digicel Group Limited June 2012 676 753 919 1,070 1.41 6.27 1.58 1.51 3.34 10.80 3.95 6.21 Empresa Generadora de Electricidad Haina, S.A. March 2012 45 79 112 119 6.59 5.66 3.86 3.13 14.02 9.67 6.21 5.62 Empresa Generadora de Electricidad Itabo, S.A. June 2012 70 (6) 27 43 N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A.GOL Linhas Aereas Inteligentes S.A. June 2012 320 581 109 1 2.40 5.72 1.44 2.81 3.34 8.55 1.57 2.82 Grupo Famsa, S.A.B. de C.V. June 2012 119 138 121 141 0.17 0.10 0.12 0.14 0.32 0.25 0.25 0.28 Grupo Posadas, S.A. de C.V. June 2012 95 83 68 71 0.70 2.73 0.76 0.18 2.02 7.57 2.47 0.54 Grupo Senda Autotransporte, S.A. de C.V. (Grupo Senda) June 2012 40 62 58 66 0.39 0.36 0.34 0.24 1.80 2.43 1.98 2.40 Industrias Metalurgicas Pescarmona S.A. (IMPSA) June 2012 99 102 180 N.A. 0.84 0.53 0.31 0.19 1.72 1.41 1.38 0.19 Inversiones y Representaciones S.A. June 2012 114 180 186 202 0.74 0.55 0.55 0.66 1.96 1.70 1.66 2.25 Maestro Peru S.A. June 2012 19 25 34 38 0.14 0.29 0.13 0.09 0.78 1.62 0.86 0.68 Marfrig Alimentos S.A. June 2012 471 891 954 1,005 1.85 1.20 1.25 0.88 2.35 1.67 1.89 1.47 Minerva S.A. June 2012 107 146 176 190 1.46 2.43 1.38 2.92 2.09 3.47 1.98 4.29 OAS S.A. June 2012 92 106 188 110 2.12 1.76 1.51 1.46 2.62 2.03 1.88 1.63 OGX Petroleo E Gas Participacoes S.A. June 2012 (186) (244) (389) (448) 24.38 18.77 248.09 68.32 23.31 16.94 215.18 57.92 Pan American Energy LLC June 2012 1,487 1,435 1,779 1,521 0.60 1.14 2.14 1.01 4.47 4.90 6.12 3.04 Petroleos de Venezuela S.A. (PDVSA) Dec. 2011 11,065 24,171 18,684 N.A. 2.36 1.67 3.59 N.A. 6.10 8.38 11.39 N.A.Rede Energia S.A. June 2012 684 723 752 607 0.28 0.33 0.19 0.13 1.08 0.87 0.58 0.48 Rodopa Industria e Comercio de Alimentos Ltda. June 2012 14 16 36 35 0.25 0.40 0.33 0.23 2.05 0.85 0.96 0.67 SANLUIS Rassini, S.A. de C.V. June 2012 39 86 90 93 0.06 0.10 0.51 0.74 0.24 0.51 2.69 2.60 Servicios Corporativos Javer, S.A.P.I. de C.V. June 2012 83 71 64 72 3.01 25.32 3.84 6.34 7.08 70.55 12.16 23.47 Siderurgica del Turbio, S.A. (Sidetur) June 2012 119 33 62 84 2.98 5.81 5.83 8.94 9.15 9.54 18.17 25.66 Sifco S.A. June 2012 21 51 56 54 1.15 0.51 0.58 0.56 1.65 0.88 0.94 0.87 Telecom Argentina S.A. June 2012 1,032 1,151 1,312 1,339 1.69 33.02 148.32 76.00 6.80 141.48 444.05 271.39 Transportadora de Gas del Norte S.A. (TGN) June 2012 70 48 18 11 0.21 0.30 0.34 0.37 0.40 0.42 0.38 0.39 Transportadora de Gas del Sur S.A. (TGS) June 2012 204 175 181 173 68.42 74.31 28.98 40.84 119.88 121.64 77.83 87.89 Urbi Desarrollos Urbanos, S.A.B. de C.V. June 2012 316 329 312 327 1.14 1.85 0.86 1.67 2.21 3.10 1.53 2.93 Virgolino de Oliveira S/A Acucar e Alcool June 2012 N.A. 180 167 128 N.A. 0.07 0.20 0.28 N.A. 0.61 0.81 0.67 WPE INTERNATIONAL Cooperatief U.A. June 2012 99 102 180 N.A. 0.84 0.53 0.31 0.19 1.72 1.41 1.38 0.19 YPF S.A. June 2012 3,130 3,728 3,275 3,358 0.46 0.41 0.18 0.05 2.99 2.80 1.91 1.58

aLTM. N.A. Not applicable. Continued on next page. Source: Fitch Ratings.

Latin America High Yield 13

November 8, 2012

Corporates

Latin America Non-Financial Institutions Corporate Financial Statistics (Continued)

Short-Term Debt/Total Debt (x) Total Net Debt with Equity Credit/

Operating EBITDA (x)

Company Name LTM as of 2009 2010 2011 2012a 2009 2010 2011 2012a

AES Andres Dominicana SPV (Aes Dominicana) June 2012 0.03 N.A. N.A. N.A. 1.19 0.27 0.18 0.06Alto Palermo S.A. (APSA) June 2012 0.25 0.23 0.16 0.11 3.73 1.42 0.74 0.70Arcor S.A.I.C. June 2012 0.43 0.28 0.36 0.33 1.10 1.59 1.41 1.31Arendal, S. de R. L. de C. V. June 2012 0.92 0.98 0.75 0.93 6.93 4.06 1.57 0.35Axtel, S.A.B. de C.V. June 2012 0.10 0.06 0.03 0.03 2.21 2.83 3.10 3.43Bio-PAPPEL, S.A.B. de C.V. June 2012 0.01 0.02 0.03 0.03 2.60 2.65 3.87 2.46Cablevision S.A. June 2012 0.10 0.06 0.11 0.15 1.30 0.92 1.14 1.05Capex S.A. June 2012 0.03 0.10 0.09 0.11 4.45 5.06 4.09 5.66Ceagro Agricola Ltda. June 2012 0.29 0.07 0.22 0.21 1.59 0.20 2.25 2.56Celulosa Argentina S.A. May 2012 0.38 0.40 0.49 0.45 4.87 3.20 2.33 2.52CEMEX, S.A.B. de C.V. June 2012 0.03 0.03 0.02 0.01 6.61 7.26 8.18 7.17Cimento Tupi S.A. June 2012 0.48 0.48 0.17 0.15 0.89 1.79 3.69 5.51Clarendon Alumina Production Limited (CAP) March 2011 0.28 0.24 0.40 N.A. (29.47) (25.74) (10.86) N.A.Compania de Transporte de Energia Electrica en Alta Tension Transener S.A. June 2012 0.09 0.09 0.03 0.02 2.96 2.25 3.85 15.50Compania Latinoamericana de Infraestructura y Servicios June 2012 0.30 0.40 0.51 0.46 1.16 1.68 1.56 1.92Construtora OAS Ltda June 2012 0.13 0.23 0.21 0.17 0.14 (6.04) (1.73) 9.12Corporacion Pesquera Inca SAC (COPEINCA) June 2012 0.27 0.07 0.18 0.28 2.21 2.42 2.06 2.24Cresud S.A.C.I.F. y A. June 2012 0.38 0.55 0.39 0.28 3.60 2.12 2.92 3.79Digicel Group Limited June 2012 0.11 0.04 0.09 0.05 3.92 3.66 4.26 4.25Empresa Generadora de Electricidad Haina, S.A. March 2012 0.03 0.09 0.17 0.16 3.65 1.22 0.87 1.28Empresa Generadora de Electricidad Itabo, S.A. June 2012 N.A. N.A. N.A. N.A. 0.65 (10.45) 2.81 1.80GOL Linhas Aereas Inteligentes S.A. June 2012 0.19 0.09 0.31 0.12 3.08 1.80 13.62 1,381.70Grupo Famsa, S.A.B. de C.V. June 2012 0.91 0.82 0.77 0.79 6.16 7.33 8.72 7.94Grupo Posadas, S.A. de C.V. June 2012 0.19 0.04 0.09 0.44 3.46 5.13 6.24 5.77Grupo Senda Autotransporte, S.A. de C.V. (Grupo Senda) June 2012 0.13 0.14 0.16 0.14 5.21 3.35 3.67 3.17Industrias Metalurgicas Pescarmona S.A. (IMPSA) June 2012 0.19 0.20 0.20 0.24 4.92 5.06 4.39 N.A.Inversiones y Representaciones S.A. June 2012 0.25 0.37 0.28 0.22 2.49 1.77 2.71 2.48Maestro Peru S.A. June 2012 0.55 0.35 0.42 0.53 2.61 1.94 3.09 3.05Marfrig Alimentos S.A. June 2012 0.29 0.32 0.23 0.28 3.20 4.21 4.78 4.62Minerva S.A. June 2012 0.24 0.14 0.26 0.12 4.30 4.33 4.14 4.22OAS S.A. June 2012 0.26 0.25 0.26 0.26 3.54 8.14 6.53 13.56 OGX Petroleo E Gas Participacoes S.A. June 2012 1.00 0.95 0.00 0.01 21.79 9.72 0.93 (2.35)Pan American Energy LLC June 2012 0.25 0.22 0.25 0.40 0.89 0.92 0.45 0.74 Petroleos de Venezuela S.A. (PDVSA) Dec. 2011 0.14 0.14 0.07 N.A. 1.31 0.78 1.41 N.A.Rede Energia S.A. June 2012 0.22 0.29 0.44 0.46 5.34 5.74 5.40 5.77 Rodopa Industria e Comercio de Alimentos Ltda. June 2012 0.47 0.67 0.62 0.81 1.04 2.48 2.04 2.27 SANLUIS Rassini, S.A. de C.V. June 2012 218 208 41 50 5.71 4.01 2.55 2.39 Servicios Corporativos Javer, S.A.P.I. de C.V. June 2012 0.10 0.01 0.03 0.02 1.67 2.40 3.82 3.46 Siderurgica del Turbio, S.A. (Sidetur) June 2012 0.18 0.10 0.06 0.06 0.40 1.19 0.86 0.41 Sifco S.A. June 2012 0.20 0.39 0.42 0.48 8.00 5.61 4.92 4.95 Telecom Argentina S.A. June 2012 0.93 0.26 0.14 0.23 (0.12) (0.27) (0.48) (0.37)Transportadora de Gas del Norte S.A. (TGN) June 2012 1.00 1.00 1.00 1.00 4.28 6.05 16.96 27.35 Transportadora de Gas del Sur S.A. (TGS) June 2012 0.01 0.01 0.01 0.01 0.64 0.59 1.51 1.31 Urbi Desarrollos Urbanos, S.A.B. de C.V. June 2012 0.49 0.30 0.43 0.18 0.84 1.22 2.15 3.04 Virgolino de Oliveira S/A Acucar e Alcool June 2012 N.A. 0.46 0.31 0.30 N.A. 3.85 4.94 7.83 WPE INTERNATIONAL Cooperatief U.A. June 2012 0.19 0.20 0.20 0.24 4.92 5.06 4.39 N.A.YPF S.A. June 2012 0.69 0.79 0.64 0.93 0.40 0.36 0.81 0.67

aLTM. N.A. Not applicable. Source: Fitch Ratings.

Latin America High Yield 14

November 8, 2012

Corporates

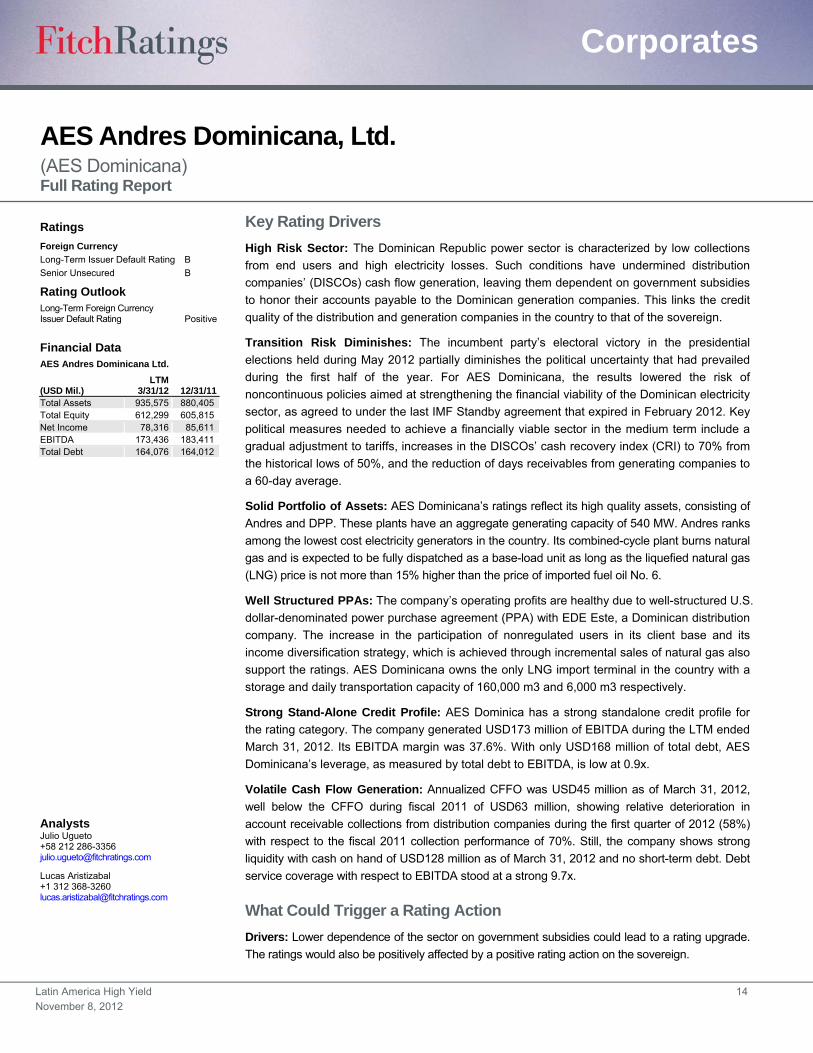

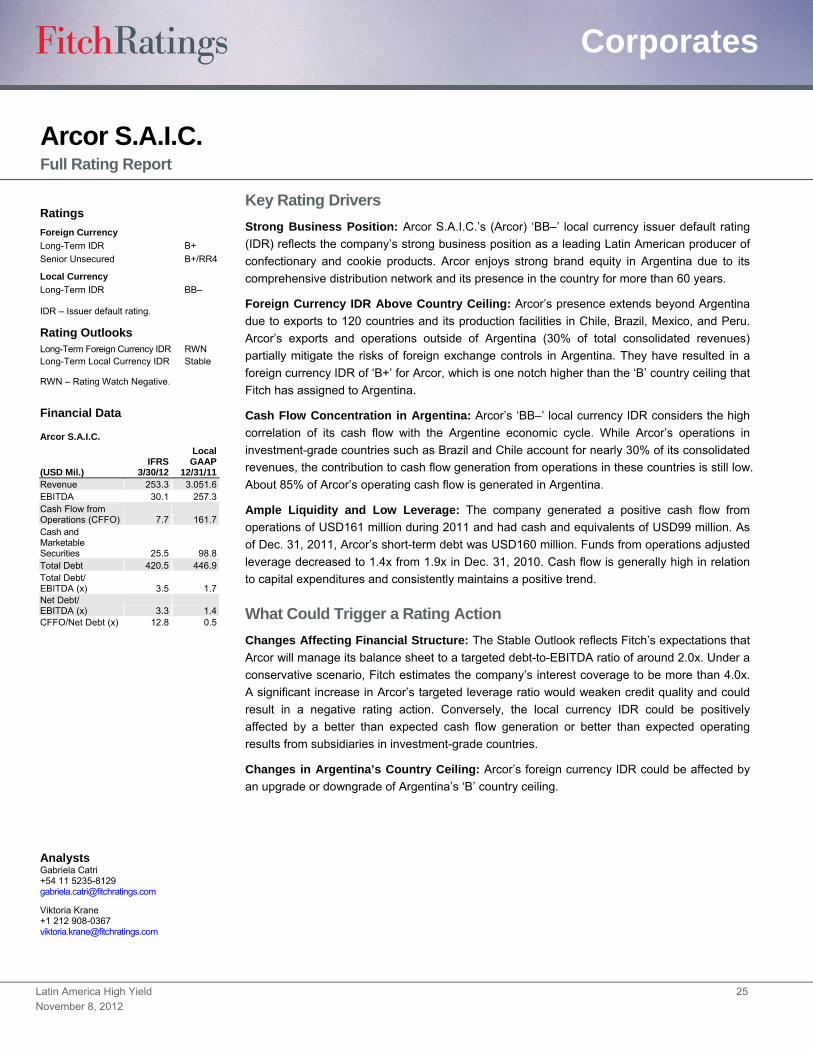

AES Andres Dominicana, Ltd. (AES Dominicana) Full Rating Report

Key Rating Drivers

High Risk Sector: The Dominican Republic power sector is characterized by low collections

from end users and high electricity losses. Such conditions have undermined distribution

companies’ (DISCOs) cash flow generation, leaving them dependent on government subsidies

to honor their accounts payable to the Dominican generation companies. This links the credit

quality of the distribution and generation companies in the country to that of the sovereign.

Transition Risk Diminishes: The incumbent party’s electoral victory in the presidential

elections held during May 2012 partially diminishes the political uncertainty that had prevailed

during the first half of the year. For AES Dominicana, the results lowered the risk of

noncontinuous policies aimed at strengthening the financial viability of the Dominican electricity

sector, as agreed to under the last IMF Standby agreement that expired in February 2012. Key

political measures needed to achieve a financially viable sector in the medium term include a

gradual adjustment to tariffs, increases in the DISCOs’ cash recovery index (CRI) to 70% from

the historical lows of 50%, and the reduction of days receivables from generating companies to

a 60-day average.

Solid Portfolio of Assets: AES Dominicana’s ratings reflect its high quality assets, consisting of

Andres and DPP. These plants have an aggregate generating capacity of 540 MW. Andres ranks

among the lowest cost electricity generators in the country. Its combined-cycle plant burns natural

gas and is expected to be fully dispatched as a base-load unit as long as the liquefied natural gas

(LNG) price is not more than 15% higher than the price of imported fuel oil No. 6.

Well Structured PPAs: The company’s operating profits are healthy due to well-structured U.S.

dollar-denominated power purchase agreement (PPA) with EDE Este, a Dominican distribution

company. The increase in the participation of nonregulated users in its client base and its

income diversification strategy, which is achieved through incremental sales of natural gas also

support the ratings. AES Dominicana owns the only LNG import terminal in the country with a

storage and daily transportation capacity of 160,000 m3 and 6,000 m3 respectively.

Strong Stand-Alone Credit Profile: AES Dominica has a strong standalone credit profile for

the rating category. The company generated USD173 million of EBITDA during the LTM ended

March 31, 2012. Its EBITDA margin was 37.6%. With only USD168 million of total debt, AES

Dominicana’s leverage, as measured by total debt to EBITDA, is low at 0.9x.

Volatile Cash Flow Generation: Annualized CFFO was USD45 million as of March 31, 2012,

well below the CFFO during fiscal 2011 of USD63 million, showing relative deterioration in

account receivable collections from distribution companies during the first quarter of 2012 (58%)

with respect to the fiscal 2011 collection performance of 70%. Still, the company shows strong

liquidity with cash on hand of USD128 million as of March 31, 2012 and no short-term debt. Debt

service coverage with respect to EBITDA stood at a strong 9.7x.

What Could Trigger a Rating Action

Drivers: Lower dependence of the sector on government subsidies could lead to a rating upgrade.

The ratings would also be positively affected by a positive rating action on the sovereign.

Ratings

Foreign Currency

Long-Term Issuer Default Rating B

Senior Unsecured B

Rating Outlook Long-Term Foreign Currency Issuer Default Rating Positive

Financial Data AES Andres Dominicana Ltd.

(USD Mil.) LTM

3/31/12 12/31/11 Total Assets 935,575 880,405 Total Equity 612,299 605,815 Net Income 78,316 85,611 EBITDA 173,436 183,411 Total Debt 164,076 164,012

Analysts Julio Ugueto +58 212 286-3356 [email protected]

Lucas Aristizabal +1 312 368-3260 [email protected]

Latin America High Yield 15

November 8, 2012

Corporates

Recovery Analysis

AES Dominicana’s senior notes issuance has been assigned a recovery rating of ‘RR4’. The

recovery was based upon the treatment of AES Dominicana as a going concern, as a

liquidation scenario is considered highly unlikely. The ratings have been capped at ‘RR4’ due

to concerns about the low probability of high recoveries for bondholders of corporates

domiciled in the Dominican Republic.

Fitch currently maintains a positive outlook for the sovereign, and, as such, we do not foresee a

bankruptcy scenario for AES Dominicana unless a low probability event, such as a severe

fiscal crisis that impacts the company’s cash flow to a point that its liquidity is constrained.

As a result we have opted for estimating a distressed enterprise valuation to arrive at the

recovery scenario attached below. The distressed EBITDA is calculated to cover the

company’s fixed charges and critical maintenance capex, which is then adjusted by a

conservative 5x multiple to arrive at a distressed company valuation. This distressed valuation

would be associated with a severe fiscal crisis that would lead to a sustained cash flow drain

for all generating companies in the country and contemplates the low probability event of a

nonfriendly renegotiation scenario of the company’s PPA’s with distribution companies to the

detriment of AES Dominicana. In this hypothetical scenario, it would be reasonable to expect a

low demand for the company’s assets under a competitive bidding process, further supporting

the distressed valuation commented above.

Recovery Analysis AES Dominicana (USD Mil.) IDR: B Going Concern Enterprise Value

LTM EBITDA as of March 31, 2012 173.4 Discount (%) 83.9 Distressed EBITDA 28.0 Multiple (x) 5.0 Going Concern Enterprise Value 140.0 Post-Restructuring EBITDA Estimation Guidelines Interest Expense 18 Distribution of Value by Priority Rent Expense — Greater of Going Concern Enterprise or Liquidation Value 140.0Est. Maintenance Capital Expenditures 10 Less Administrative Claims (10%) 14.0Total Adjusted Enterprise Value for Claims 126.0 Distribution of Value

Secured Priority Lien Value Recovered Recovery (%)Recovery

Rating Notching Rating

Senior Secured — — — — — —Secured — — — — — —

Unsecured Priority Amount

Outstanding Value

RecoveredRecovery

(%)Concession

Allocation (%) Recovery Rating Notching Rating

Issuer Default Rating — — — — — — BSenior Unsecured 164 126 77 — RR2 +2 BB–Subordinated — — — — — — —Junior Subordinated — — — — — — —

Source: Fitch.

Latin America High Yield 16

November 8, 2012

Corporates

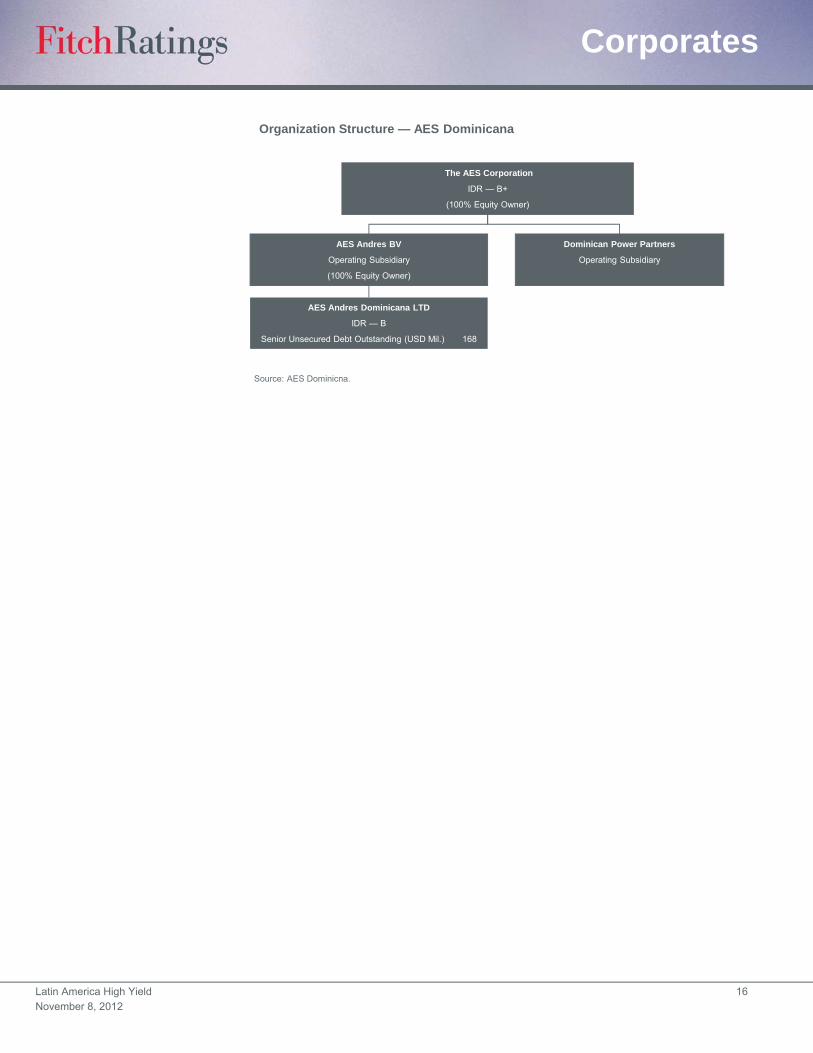

Source: AES Dominicna.

AES Andres BV

Operating Subsidiary

(100% Equity Owner)

Dominican Power Partners

Operating Subsidiary

Organization Structure — AES Dominicana

The AES Corporation

IDR — B+

(100% Equity Owner)

AES Andres Dominicana LTD

IDR — B

Senior Unsecured Debt Outstanding (USD Mil.) 168

Latin America High Yield 17

November 8, 2012

Corporates

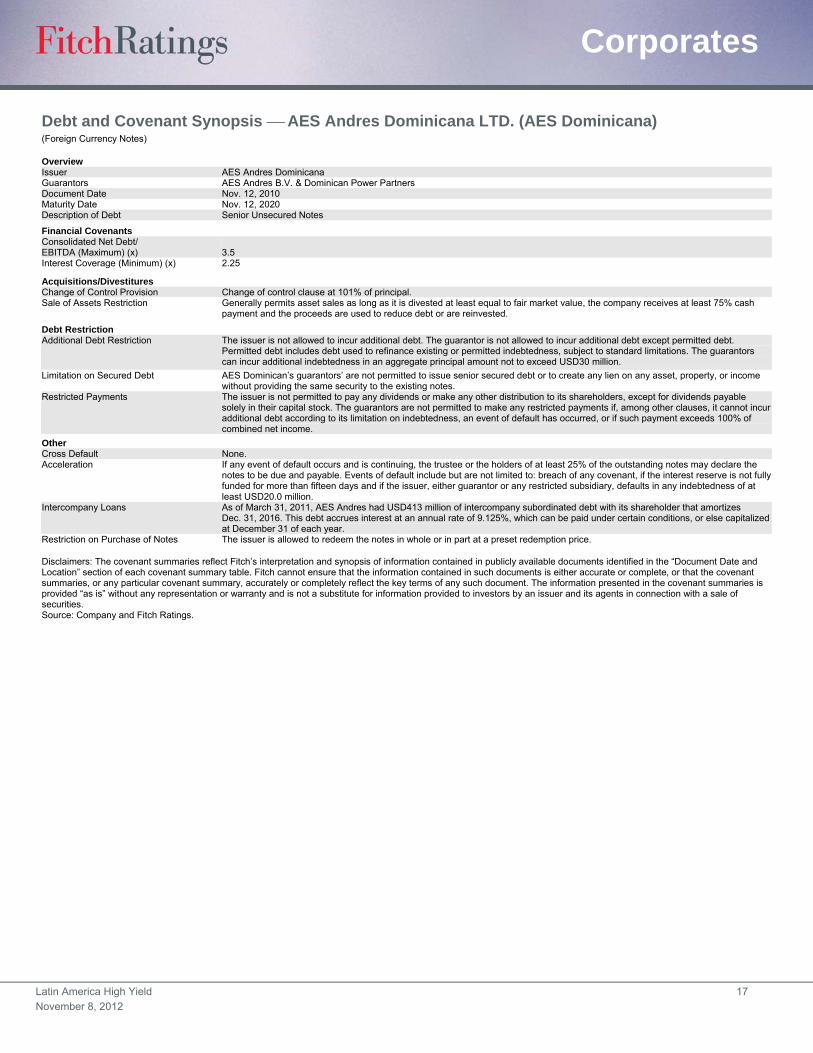

Debt and Covenant Synopsis AES Andres Dominicana LTD. (AES Dominicana) (Foreign Currency Notes)

Overview Issuer AES Andres Dominicana Guarantors AES Andres B.V. & Dominican Power Partners Document Date Nov. 12, 2010 Maturity Date Nov. 12, 2020 Description of Debt Senior Unsecured Notes

Financial Covenants Consolidated Net Debt/ EBITDA (Maximum) (x) 3.5 Interest Coverage (Minimum) (x) 2.25

Acquisitions/Divestitures Change of Control Provision Change of control clause at 101% of principal. Sale of Assets Restriction Generally permits asset sales as long as it is divested at least equal to fair market value, the company receives at least 75% cash

payment and the proceeds are used to reduce debt or are reinvested.

Debt Restriction Additional Debt Restriction The issuer is not allowed to incur additional debt. The guarantor is not allowed to incur additional debt except permitted debt.

Permitted debt includes debt used to refinance existing or permitted indebtedness, subject to standard limitations. The guarantors can incur additional indebtedness in an aggregate principal amount not to exceed USD30 million.

Limitation on Secured Debt AES Dominican’s guarantors’ are not permitted to issue senior secured debt or to create any lien on any asset, property, or income without providing the same security to the existing notes.

Restricted Payments The issuer is not permitted to pay any dividends or make any other distribution to its shareholders, except for dividends payable solely in their capital stock. The guarantors are not permitted to make any restricted payments if, among other clauses, it cannot incur additional debt according to its limitation on indebtedness, an event of default has occurred, or if such payment exceeds 100% of combined net income.

Other Cross Default None. Acceleration If any event of default occurs and is continuing, the trustee or the holders of at least 25% of the outstanding notes may declare the

notes to be due and payable. Events of default include but are not limited to: breach of any covenant, if the interest reserve is not fully funded for more than fifteen days and if the issuer, either guarantor or any restricted subsidiary, defaults in any indebtedness of at least USD20.0 million.

Intercompany Loans As of March 31, 2011, AES Andres had USD413 million of intercompany subordinated debt with its shareholder that amortizes Dec. 31, 2016. This debt accrues interest at an annual rate of 9.125%, which can be paid under certain conditions, or else capitalized at December 31 of each year.

Restriction on Purchase of Notes The issuer is allowed to redeem the notes in whole or in part at a preset redemption price. Disclaimers: The covenant summaries reflect Fitch’s interpretation and synopsis of information contained in publicly available documents identified in the “Document Date and Location” section of each covenant summary table. Fitch cannot ensure that the information contained in such documents is either accurate or complete, or that the covenant summaries, or any particular covenant summary, accurately or completely reflect the key terms of any such document. The information presented in the covenant summaries is provided “as is” without any representation or warranty and is not a substitute for information provided to investors by an issuer and its agents in connection with a sale of securities. Source: Company and Fitch Ratings.

Latin America High Yield 18

November 8, 2012

Corporates

Financial Summary AES Andres Dominicana Ltd. (USD Mil., As of Dec. 31) LTM 3/31/12 2011 2010 2009 2008

Profitability

Operating EBITDA 173,436 183,411 161,900 82,438 112,253

Operating EBITDAR 173,436 183,411 161,900 82,438 112,253

Operating EBITDA Margin (%) 38 41 43 35 31

Operating EBITDAR Margin (%) 38 41 43 35 31

FFO Return on Adjusted Capital (%) 9 14 13 7 9

Free Cash Flow Margin (%) (4) 0 21 (3) (5)

Return on Average Equity (%) 26 15 19 1 5

Coverage (x)

FFO Interest Coverage 3.9 6.4 4.4 1.9 2.9

Operating EBITDA/Gross Interest Expense 9.7 10.9 7.8 3.4 5.6

Operating EBITDAR/Interest Expense + Rents 9.7 10.9 7.8 3.4 5.6

Operating EBITDA/Debt Service Coverage 9.7 10.9 7.8 2.8 2.5

Operating EBITDAR/Debt Service Coverage 9.7 10.9 7.8 2.8 2.5

FFO Fixed-Charge Coverage 3.9 6.4 4.4 1.9 2.9

FCF Debt Service Coverage (0.1) 0.9 4.9 0.6 0.0

(FCF + Cash and Marketable Securities)/Debt Service Coverage 7.0 8.7 10.7 2.8 0.9

Cash Flow from Operations/Capital Expenditures 1.5 2.2 7.6 0.7 (1.7)

Leverage (x)

FFO Adjusted Leverage 2.4 1.5 1.8 3.5 3.1

Total Debt with Equity Credit/Operating EBITDA 0.9 0.9 1.0 2.0 1.6

Total Net Debt with Equity Credit/Operating EBITDA 0.2 0.2 0.3 1.2 1.3

Total Adjusted Debt/Operating EBITDAR 0.9 0.9 1.0 2.0 1.6

Total Adjusted Net Debt/Operating EBITDAR 0.2 0.2 0.3 1.2 1.3

Implied Cost of Funds (%) 0.2 0.1 0.3 0.1 0.1

Secured Debt/Total Debt — — — — —

Short-Term Debt/Total Debt — — — 0.0 0.1

Balance Sheet

Total Assets 935,575 880,405 853,356 713,062 718,418

Cash and Marketable Securities 127,703 131,130 119,652 63,040 40,450

Short-Term Debt — — — 5,000 25,000

Long-Term Debt 164,076 164,012 163,773 156,000 156,000

Total Debt 164,076 164,012 163,773 161,000 181,000

Equity Credit — — — — —

Total Debt with Equity Credit 164,076 164,012 163,773 161,000 181,000

Off-Balance Sheet Debt — — — — —

Total Adjusted Debt with Equity Credit 164,076 164,012 163,773 161,000 181,000

Total Equity 612,299 605,815 559,193 458,304 454,676

Total Adjusted Capital 776,375 769,827 722,966 619,304 635,676

Cash Flow

Funds from Operations 51,802 90,649 70,285 20,957 37,850

Change in Working Capital (6,460) (27,823) 22,857 (3,616) (49,343)

Cash Flow from Operations 45,342 62,826 93,142 17,341 (11,493)

Total Non-Operating/Nonrecurring Cash Flow — — — — —

Capital Expenditures (29,742) (28,617) (12,273) (23,479) (6,743)

Common Dividends (35,903) (35,903) — — —

Free Cash Flow (20,303) (1,694) 80,869 (6,138) (18,236)

Net Acquisitions and Divestitures — — — — —

Other Investments, Net 7,978 14,179 (16,277) 51,571 12,155

Net Debt Proceeds 2 7 (3,492) (20,000) 9,596

Net Equity Proceeds — — — — —

Other (Investments and Financing) (1,045) (1,014) (3,279) (1,286) (1,473)

Total Change in Cash (13,368) 11,478 57,821 24,147 2,042

Income Statement

Revenue 461,351 444,386 376,738 234,536 358,249

Revenue Growth (%) 4 18 0151 (35) 26

Operating EBIT 146,515 157,343 135,414 66,900 97,500

Gross Interest Expense 17,872 16,800 20,625 24,399 19,910

Rental Expense — — — — —

Net Income 78,316 85,611 53,823 3,493 21,378

Source: Fitch.

Latin America High Yield 19

November 8, 2012

Corporates

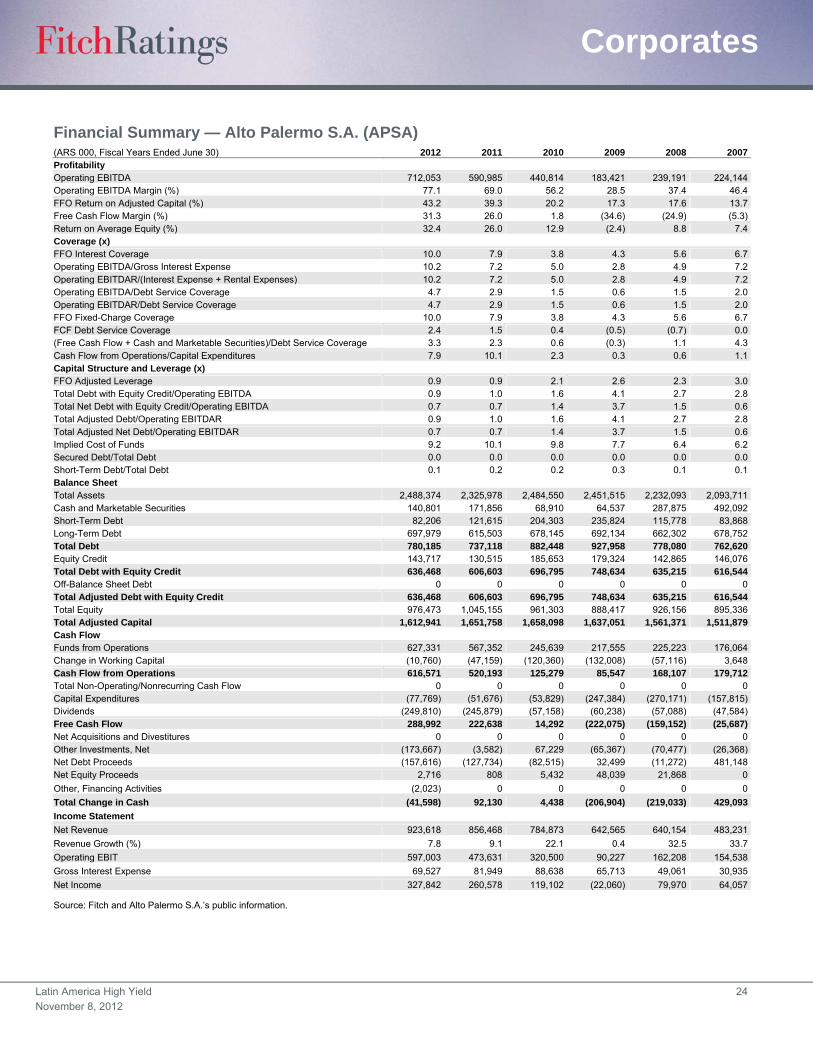

Alto Palermo S.A. (APSA) Full Rating Report

Key Rating Drivers

Linkage to IRSA and Argentina: While debt at Alto Palermo S.A. (APSA) is low in relation to

cash flow, Fitch Ratings has linked the credit quality of APSA with its more highly leveraged

parent company, IRSA Inversiones y Representaciones S.A. (IRSA). APSA’s foreign currency

IDR continues to be constrained at ‘B’ by the ‘B’ country ceiling assigned to Argentina by Fitch.

Its local currency (LC) issuer default rating (IDR) is constrained at ‘BB–’ due to the high degree

of risk associated with operating in Argentina’s real estate industry.

Devaluation Risk: Devaluation risk is also present for APSA as most of its cash flow is

denominated in Argentine pesos and a substantial part of its debt is in U.S. dollars. This risk is

partially mitigated by APSA’s dollar-denominated asset portfolio and its long-term debt profile.

Strong Business Position: APSA’s ‘BB–’ LC IDR is supported by the company’s strong

market position in the Argentine shopping center industry. APSA operates 13 shopping centers

with a gross leasable space of 309,021 square meters. The high quality of these malls and

their strategic locations result in sales per square meter that exceed the market average and

occupancy rates of more than 98%.

Hedge Against Consumer Inflation: APSA’s revenues are partially hedged against consumer

inflation, as the company receives a percentage of the sales made by tenants of its malls. The

company’s high operating margins are due to leases that result in the tenants paying direct

expenses and a percentage of the common expenses.

Cyclical Business: APSA’s results are closely correlated with the performance of the

economy, which has proven to be quite volatile. APSA shows some concentration in the near-

term for its lease agreements (33% of lease contracts expiring in 2013), as the contracts are

generally for 36 months. While this ratio is high for the industry, APSA’s strong market position

allows it to renew contracts updating leasing terms.

Diversified Asset Base: For the real estate industry, the emphasis of Fitch's methodology is

on portfolio quality and diversity, and size of the asset base. APSA’s portfolio of assets is

strong, with an undepreciated book capital as of June 30, 2012 of USD629 million. These

assets are mostly unencumbered, as secured debt represents less than 5% of total debt. The

company’s leverage, as measured by net debt as a percentage of undepreciated book capital,

was 17% as of June 30, 2012. This percentage would be even lower at market values. The

large pool of unencumbered assets at APSA provides financial flexibility and results in above-

average recovery prospects in the event of default.

What Could Trigger a Rating Action

Changes Affecting APSA’s Conservative Financial Structure: The Stable Outlook reflects

Fitch’s expectations that APSA will manage its balance sheet to a targeted ratio of debt-to-

EBITDA of about 1.5x and interest coverage to be above 5.0x. Fitch estimates that the

company’s EBITDA margin will remain above 70%. Any significant increase in APSA’s targeted

leverage ratio would threaten credit quality and could result in a negative rating action.

Changes in Argentina’s Country Ceiling: APSA’s foreign currency (FC) IDR would be

affected by an upgrade or downgrade of the Argentine country ceiling of ‘B’.

Ratings

Foreign Currency

Long-Term IDR B

Senior Unsecured B+/RR3

Local Currency

Long-Term IDR BB–

IDR – Issuer default rating.

Rating Outlooks Long-Term Foreign Currency IDR RWN Long-Term Local Currency IDR Stable

RWN – Rating Watch Negative.

Financial Data

Alto Palermo S.A.

(USD Mil.) 6/30/12 6/30/11 Revenue 214.7 214.1 EBITDA 165.5 147.7 Cash Flow from Operations (CFFO) 143.3 130.0 Cash and Marketable Securities 31.1 41.8 Total Debt 172.5 147.6 Total Debt/ EBITDA (x) 0.8 1.0 Net Debt/ EBITDA (x) 0.7 0.7 CFFO/Net Debt (x) 1.3 1.2

Analysts Gabriela Catri +54 11 5235-8129 [email protected]

Jose Vertiz +1 212 908-0641 [email protected]

Latin America High Yield 20

November 8, 2012

Corporates

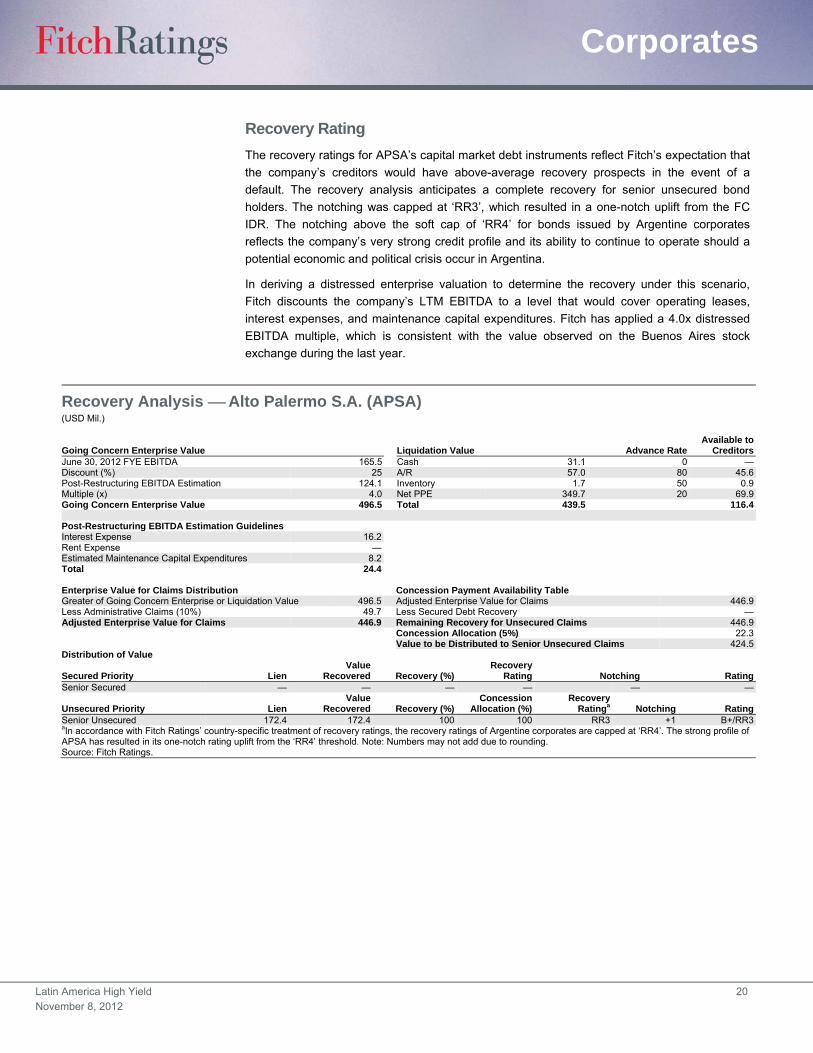

Recovery Rating

The recovery ratings for APSA’s capital market debt instruments reflect Fitch’s expectation that

the company’s creditors would have above-average recovery prospects in the event of a

default. The recovery analysis anticipates a complete recovery for senior unsecured bond

holders. The notching was capped at ‘RR3’, which resulted in a one-notch uplift from the FC

IDR. The notching above the soft cap of ‘RR4’ for bonds issued by Argentine corporates

reflects the company’s very strong credit profile and its ability to continue to operate should a

potential economic and political crisis occur in Argentina.

In deriving a distressed enterprise valuation to determine the recovery under this scenario,

Fitch discounts the company’s LTM EBITDA to a level that would cover operating leases,

interest expenses, and maintenance capital expenditures. Fitch has applied a 4.0x distressed

EBITDA multiple, which is consistent with the value observed on the Buenos Aires stock

exchange during the last year.

Recovery Analysis Alto Palermo S.A. (APSA) (USD Mil.)

Going Concern Enterprise Value Liquidation Value Advance RateAvailable to

CreditorsJune 30, 2012 FYE EBITDA 165.5 Cash 31.1 0 —Discount (%) 25 A/R 57.0 80 45.6Post-Restructuring EBITDA Estimation 124.1 Inventory 1.7 50 0.9Multiple (x) 4.0 Net PPE 349.7 20 69.9Going Concern Enterprise Value 496.5 Total 439.5 116.4 Post-Restructuring EBITDA Estimation Guidelines Interest Expense 16.2Rent Expense —Estimated Maintenance Capital Expenditures 8.2Total 24.4

Enterprise Value for Claims Distribution Concession Payment Availability Table Greater of Going Concern Enterprise or Liquidation Value 496.5 Adjusted Enterprise Value for Claims 446.9Less Administrative Claims (10%) 49.7 Less Secured Debt Recovery —Adjusted Enterprise Value for Claims 446.9 Remaining Recovery for Unsecured Claims 446.9 Concession Allocation (5%) 22.3 Value to be Distributed to Senior Unsecured Claims 424.5Distribution of Value

Secured Priority Lien Value

Recovered Recovery (%)Recovery

Rating Notching RatingSenior Secured — — — — — —

Unsecured Priority Lien Value

Recovered Recovery (%)Concession

Allocation (%)Recovery

Ratinga Notching RatingSenior Unsecured 172.4 172.4 100 100 RR3 +1 B+/RR3aIn accordance with Fitch Ratings’ country-specific treatment of recovery ratings, the recovery ratings of Argentine corporates are capped at ‘RR4’. The strong profile of APSA has resulted in its one-notch rating uplift from the ‘RR4’ threshold. Note: Numbers may not add due to rounding. Source: Fitch Ratings.

Latin America High Yield 21

November 8, 2012

Corporates

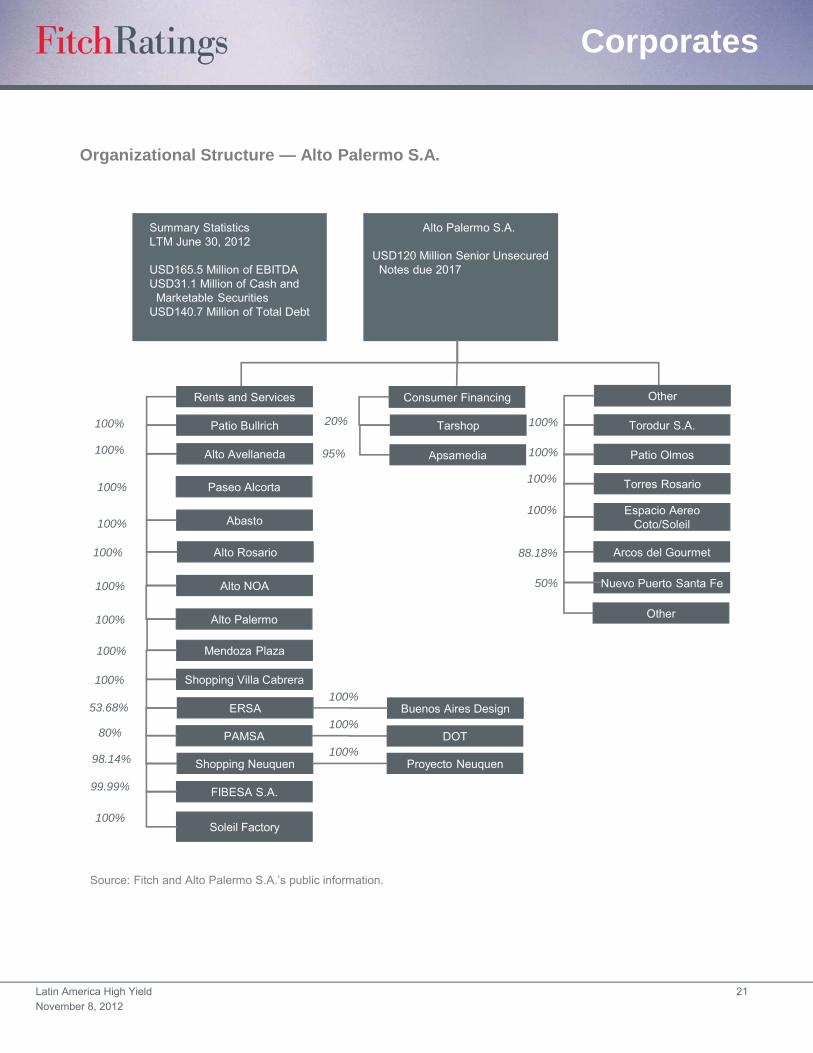

Organizational Structure — Alto Palermo S.A.

Alto Palermo S.A.

USD120 Million Senior UnsecuredNotes due 2017

Source: Fitch and Alto Palermo S.A.’s public information.

Summary StatisticsLTM June 30, 2012

USD165.5 Million of EBITDAUSD31.1 Million of Cash and

Marketable SecuritiesUSD140.7 Million of Total Debt

Rents and Services Consumer Financing Other

Patio Bullrich

Apsamedia

Arcos del Gourmet

Espacio Aereo Coto/Soleil

Torres Rosario

Tarshop

Patio Olmos

Torodur S.A.

Alto Avellaneda

Abasto

Alto Rosario

Alto NOA