© 2016 Ballentine Partners, LLC All Rights Reserved APRIL 2016 First Quarter 2016 Market Review Was the first quarter’s financial roller coaster foreshadowing what to expect for the rest of the year, or just much ado about nothing? Markets experienced renewed – and extreme – volatility for four major reasons: the initiation of higher interest rates from the US Federal Reserve, the perception of a looming global recession led by China, plunging crude oil prices, and a potentially contentious US Presidential primary outcome. There were many additional, less significant issues, but all weighed on market psyche. In the first six weeks of the year, global stocks sold off 11% only to then stage a 13% recovery to finish even for the quarter. Rattled by the markets’ steep decline, the Fed quickly stepped back from its public intention to raise interest rates four times in 2016. Rather than confirming the onset of economic doom, global indicators, including those for China, strengthened throughout the quarter. West Texas crude started and finished the quarter at $38 despite touching $26 in late January. Even the tone of the primary debates softened as the field consolidated. Looked at from a long term perspective, the quarter was mostly noise and little signal in our view. BA LLENTI N E P A R T N E R S Will Braman, Partner & Chief Investment Officer Global Equities and Headlines in the First Quarter

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2016 Ballentine Partners, LLC All Rights Reserved

APRIL 2016

First Quarter 2016 Market Review

Was the first quarter’s financial roller coaster foreshadowing what to expect for the rest of the year, or just much ado about nothing?

Markets experienced renewed – and extreme – volatility for four major reasons: the initiation of higher interest rates from the US

Federal Reserve, the perception of a looming global recession led by China, plunging crude oil prices, and a potentially contentious

US Presidential primary outcome. There were many additional, less significant issues, but all weighed on market psyche.

In the first six weeks of the year, global stocks sold off 11% only to then stage a 13% recovery to finish even for the quarter. Rattled

by the markets’ steep decline, the Fed quickly stepped back from its public intention to raise interest rates four times in 2016. Rather

than confirming the onset of economic doom, global indicators, including those for China, strengthened throughout the quarter.

West Texas crude started and finished the quarter at $38 despite touching $26 in late January. Even the tone of the primary debates

softened as the field consolidated. Looked at from a long term perspective, the quarter was mostly noise and little signal in our view.

B A L L E N T I N E

P A R T N E R S

Will Braman, Partner & Chief Investment Officer

Global Equities and Headlines in the First Quarter

© 2016 Ballentine Partners, LLC All Rights Reserved

While there are always many factors in play when market volatility surges, changing expectations about the Fed’s intentions account-

ed for much of it in the past quarter. Historically, mid-cycle monetary policy transitions have resulted in increased volatility and dis-

appointing returns for a period of digestion before continuing economic growth drives markets higher. Such has been the case over

the past year. Given that global fundamentals remain largely positive and are broadly improving, we would expect better returns for

risk assets in the year ahead.

Asset Class Performance

First quarter equity results were lackluster in aggregate but varied across geographies. Globally, stocks returned just 0.2% for the peri-

od led by emerging markets which rallied 5.7%. Conversely, developed international markets declined 3.0% mainly due to the 15%

swoon in the Japanese market. Counter to consensus expectations, foreign currencies aided returns as the US dollar weakened by 4%

in the quarter. Domestically, US equities returned 1.0% as measured by the broad Russell 3000 index.

Fixed income returns were positive across all segments for the quarter. Intermediate municipal bonds gained 1.1%; intermediate, in-

vestment-grade, taxable bonds gained 2.4%; and Treasury Inflation Protected bonds gained 4.5%. A more benign Fed caused yields

to decline across all bond categories.

Results from real asset strategies were mixed. Master Limited Partnerships (MLPs) lost 4.2% in the quarter. Infrastructure-oriented

MLPs continued to post positive fundamentals and during the quarter again increased distributions, bringing the current yield on the

Alerian MLP Infrastructure index to over 8%. In real estate, the domestic REITs returned 5.9% while international REITs gained

8.6%, benefiting in part from stronger foreign currencies.

First quarter equity results were lackluster in aggregate but varied

across geographies. Globally, stocks returned just 0.2% for the

period led by emerging markets which rallied 5.7%.

Source: Bloomberg, Barclays

Asset Class Performance—1st Quarter 2016 and 2015

Page 2

© 2016 Ballentine Partners, LLC All Rights Reserved

Page 3 Macro Outlook

Despite seemingly widespread concerns to the contrary, growth continues to move forward and is doing so in all but two major econ-

omies, Brazil and Russia, which account for 6% of the global economy. The three fastest growing economies, India, China, and In-

donesia, are expanding at 6% and account for 17%. The next six economies, consisting of the US, Australia, and four emerging

countries, are growing at 2.5-3% and account for 31% of the world economy. Finally, Europe, Japan, and Canada are posting growth

of 1.5-2% and account for another 34%. Global growth of 3% is not the bleak picture that many appear to fear.

Indicators of future growth, specifically Purchasing

Managers Indices (PMIs) for manufacturing and

services, indicate expansion ahead for nearly every

major economy bar Russia and Brazil, but even

theirs have stopped deteriorating. PMIs improved

for many countries throughout the quarter. The US

had a 100% clean sweep for March, the first occur-

rence since April 2009 with both manufacturing

and services surprising to the upside. This bodes

well for our forecast of a recovery in corporate

earnings later this year.

Emerging and emerging market-dependent econo-

mies experienced a welcome uptick in PMIs due to

increases in orders from expanding trade. Such was the case for China whose manufacturing PMI moved back into expansion territo-

ry for the first time in over a year. Its services PMI has been and remains comfortably in expansion mode reflecting the transition to a

greater share of growth stemming from services and domestic consumption and less from government financed infrastructure.

Europe continues to defy growth skeptics. The Eu-

rozone composite PMI remains well into the expan-

sion zone. The recent strengthening of the €uro is

probably not enough to impact export competitive-

ness which is key to continued corporate earnings

growth. However, it would be surprising if ongoing

refugee immigration issues and the terror attacks in

Paris and Brussels do not have an impact on sum-

mer tourism.

Despite positive PMIs, Japan is

struggling to grow faster than 1-

1.5% due to its demographics

and lack of structural reforms.

The 12% rise in the ¥en in the

past year will be a headwind to

its competiveness and earnings

growth, but lower year over year

prices for energy and materials

should be a partial offset.

Source: Cornerstone Macro

Source: Cornerstone Macro

© 2016 Ballentine Partners, LLC All Rights Reserved

Oil & Central Banks

Better economic growth and higher corporate earnings should support higher stock prices. However, oil prices and central banks can

still wreak havoc with market sentiment and valuations.

Regarding crude oil, we believe production and

consumption should reach equilibrium this year.

Crude inventories are beginning to decline as re-

fineries are increasing production of gasoline in

advance of the summer driving season in the

northern hemisphere. We believe crude oil hit its

cycle low at $26 in January. While prices will

remain volatile, West Texas crude could reach

$50 this year which would be highly supportive of

risk asset prices.

Central banks are playing a game of tug-of-war

with one another in attempting to influence their

own economies without impacting their global

competitiveness. The European Central Bank (ECB) and the Bank of Japan (BOJ) are aggressively lowering rates to stimulate their

economies but have seen their currencies appreciate. The Federal Reserve is cautiously raising rates, restrained – it avers – by condi-

tions outside the US. Market reaction to its actions and statements earlier this year is likely a significant reason as well. The Fed

should be raising rates given domestic economic conditions. The disconnect is evident in comparing Cornerstone Macro’s leading

economic indicator (CSMLEI) and the US ten year Treasury yield below. This disconnect is further exacerbated by the Bank of Ja-

pan and European Central Bank pursuing negative interest rates and aggressive quantitative easing.

Source: IEA, TPH

Source: Cornerstone Macro

Regarding crude oil, we believe production and consumption should reach equilibrium this year. Crude inventories are beginning to decline as refineries are increasing production

of gasoline in advance of the summer driving season in the northern hemisphere.

Page 4

© 2016 Ballentine Partners, LLC All Rights Reserved

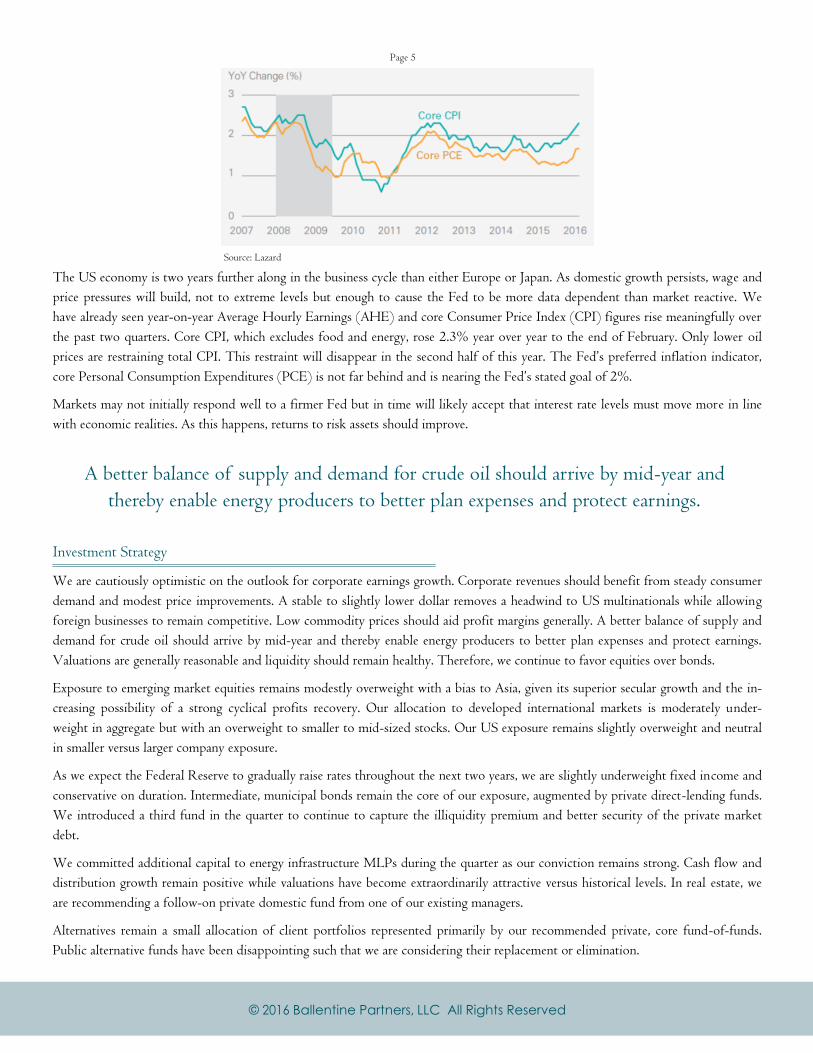

The US economy is two years further along in the business cycle than either Europe or Japan. As domestic growth persists, wage and

price pressures will build, not to extreme levels but enough to cause the Fed to be more data dependent than market reactive. We

have already seen year-on-year Average Hourly Earnings (AHE) and core Consumer Price Index (CPI) figures rise meaningfully over

the past two quarters. Core CPI, which excludes food and energy, rose 2.3% year over year to the end of February. Only lower oil

prices are restraining total CPI. This restraint will disappear in the second half of this year. The Fed’s preferred inflation indicator,

core Personal Consumption Expenditures (PCE) is not far behind and is nearing the Fed’s stated goal of 2%.

Markets may not initially respond well to a firmer Fed but in time will likely accept that interest rate levels must move more in line

with economic realities. As this happens, returns to risk assets should improve.

Investment Strategy

We are cautiously optimistic on the outlook for corporate earnings growth. Corporate revenues should benefit from steady consumer

demand and modest price improvements. A stable to slightly lower dollar removes a headwind to US multinationals while allowing

foreign businesses to remain competitive. Low commodity prices should aid profit margins generally. A better balance of supply and

demand for crude oil should arrive by mid-year and thereby enable energy producers to better plan expenses and protect earnings.

Valuations are generally reasonable and liquidity should remain healthy. Therefore, we continue to favor equities over bonds.

Exposure to emerging market equities remains modestly overweight with a bias to Asia, given its superior secular growth and the in-

creasing possibility of a strong cyclical profits recovery. Our allocation to developed international markets is moderately under-

weight in aggregate but with an overweight to smaller to mid-sized stocks. Our US exposure remains slightly overweight and neutral

in smaller versus larger company exposure.

As we expect the Federal Reserve to gradually raise rates throughout the next two years, we are slightly underweight fixed income and

conservative on duration. Intermediate, municipal bonds remain the core of our exposure, augmented by private direct-lending funds.

We introduced a third fund in the quarter to continue to capture the illiquidity premium and better security of the private market

debt.

We committed additional capital to energy infrastructure MLPs during the quarter as our conviction remains strong. Cash flow and

distribution growth remain positive while valuations have become extraordinarily attractive versus historical levels. In real estate, we

are recommending a follow-on private domestic fund from one of our existing managers.

Alternatives remain a small allocation of client portfolios represented primarily by our recommended private, core fund-of-funds.

Public alternative funds have been disappointing such that we are considering their replacement or elimination.

Source: Lazard

A better balance of supply and demand for crude oil should arrive by mid-year and

thereby enable energy producers to better plan expenses and protect earnings.

Page 5

© 2016 Ballentine Partners, LLC All Rights Reserved

Page 6

Summary

This year started with a great number of uncertainties. The major ones are becoming clearer. Most importantly, global growth is

clearly picking up and is likely sustainable for another two to three years. The direction of US Federal Reserve-set interest rates is

still higher but the pace and magnitude more gradual. China’s transition from infrastructure to consumption is progressing but there

will be bumps along the way. Numerous geopolitical uncertainties remain: the UK exiting the European Union, ISIS terrorism here

and abroad, and refugee migration into Europe to name a few. Notwithstanding, looking at all factors in aggregate, the environment

is sufficiently positive to support improving returns on risk assets in the year ahead.

As always, if there are any questions, please call.

This report is the confidential work product of Ballentine Partners. Unauthorized distribution of this material is strictly prohibited.

The information in this report is deemed to be reliable but has not been independently verified. Some of the conclusions in this report are intended to be generali-

zations. The specific circumstances of an individual’s situation may require advice that is different from that reflected in this report. Furthermore, the advice

reflected in this report is based on our opinion, and our opinion may change as new information becomes available.

Nothing in this presentation should be construed as an offer to sell or a solicitation of an offer to buy any securities. You should read the prospectus or offering

memo before making any investment. You are solely responsible for any decision to invest in a private offering.

The investment recommendations contained in this document may not prove to be profitable, and the actual performance of any investment may not be as favora-

ble as the expectations that are expressed in this document. There is no guarantee that the past performance of any investment will continue in the future.

About Ballentine Partners

Ballentine Partners is an independent wealth management firm providing comprehensive investment and family office services to

wealthy families and entrepreneurs. The firm was one of the first to deliver independent, objective, and comprehensive financial ad-

vice for wealthy families 30 years ago, and continues to be a thought leader in the field. Ballentine’s clients require comprehensive,

integrated, and objective advice. The firm advises on more than $5.9b in assets under management (as of 12/31/2015). Ballentine

scales its services to meet the breadth of clients’ needs, whether it’s investment management and planning for an entrepreneur or a full

suite of family office services for a multigenerational family, including family meetings and education, philanthropic advising, and

family office administration.

Global growth is clearly picking up and is likely

sustainable for another two to three years.

Related Documents