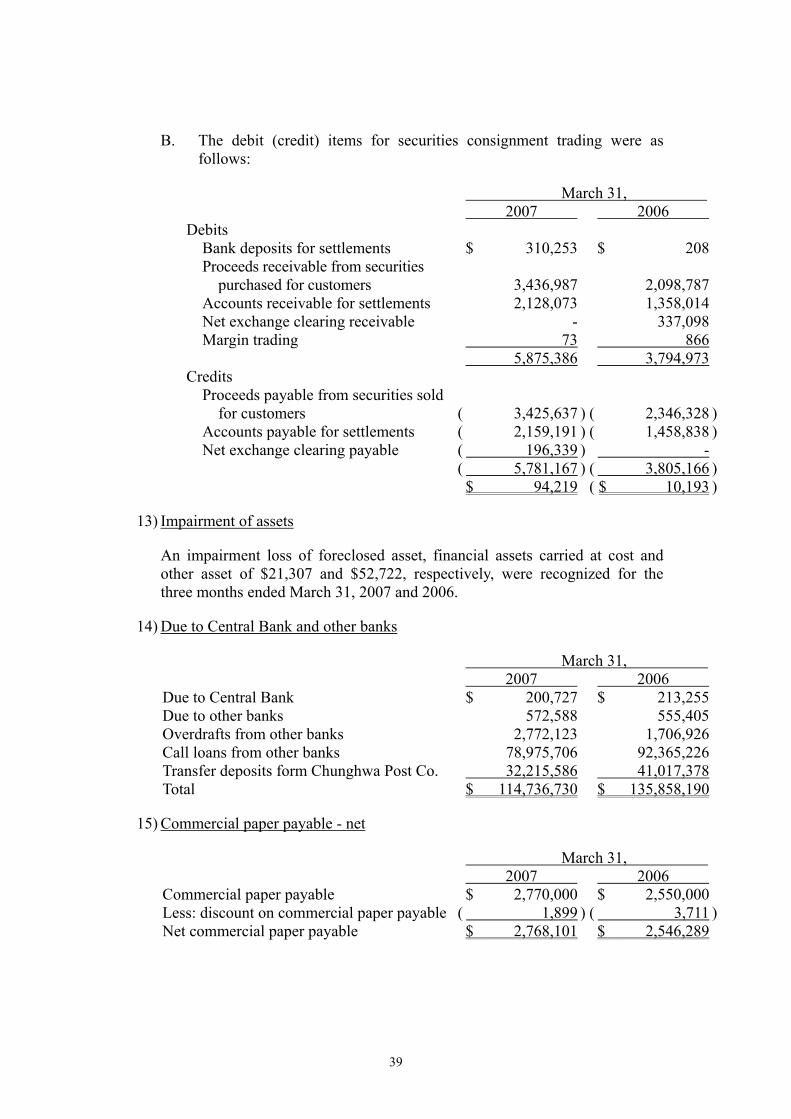

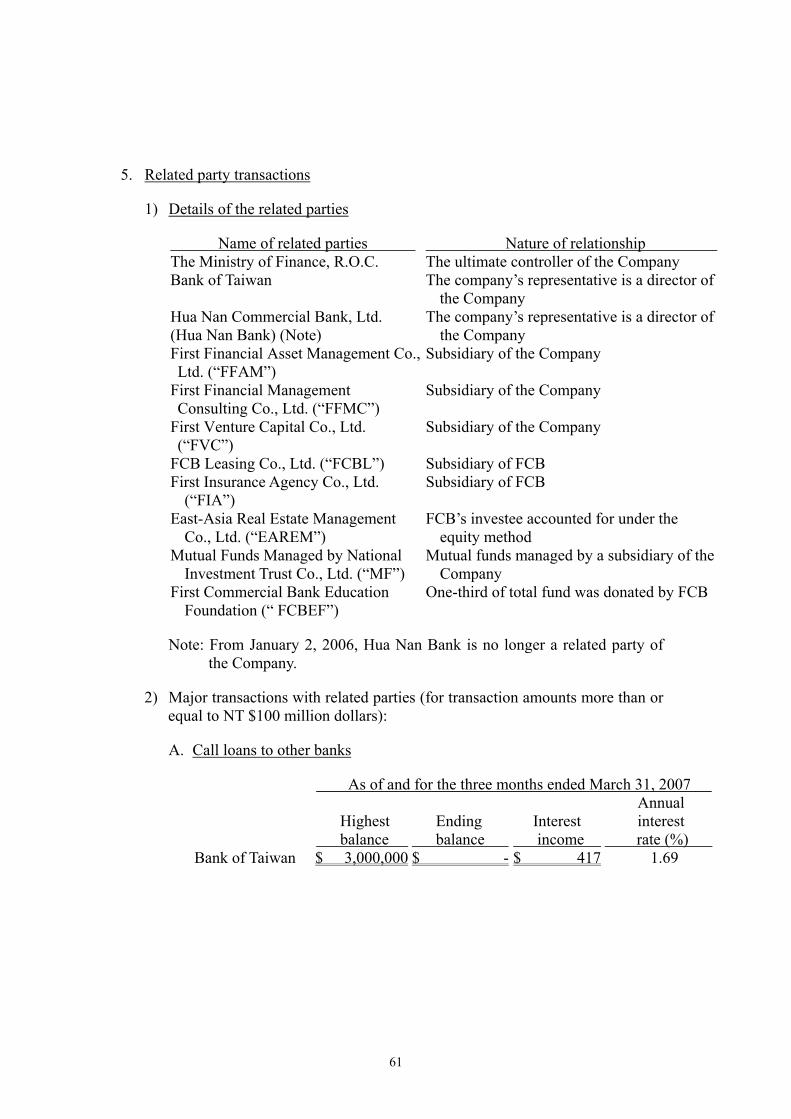

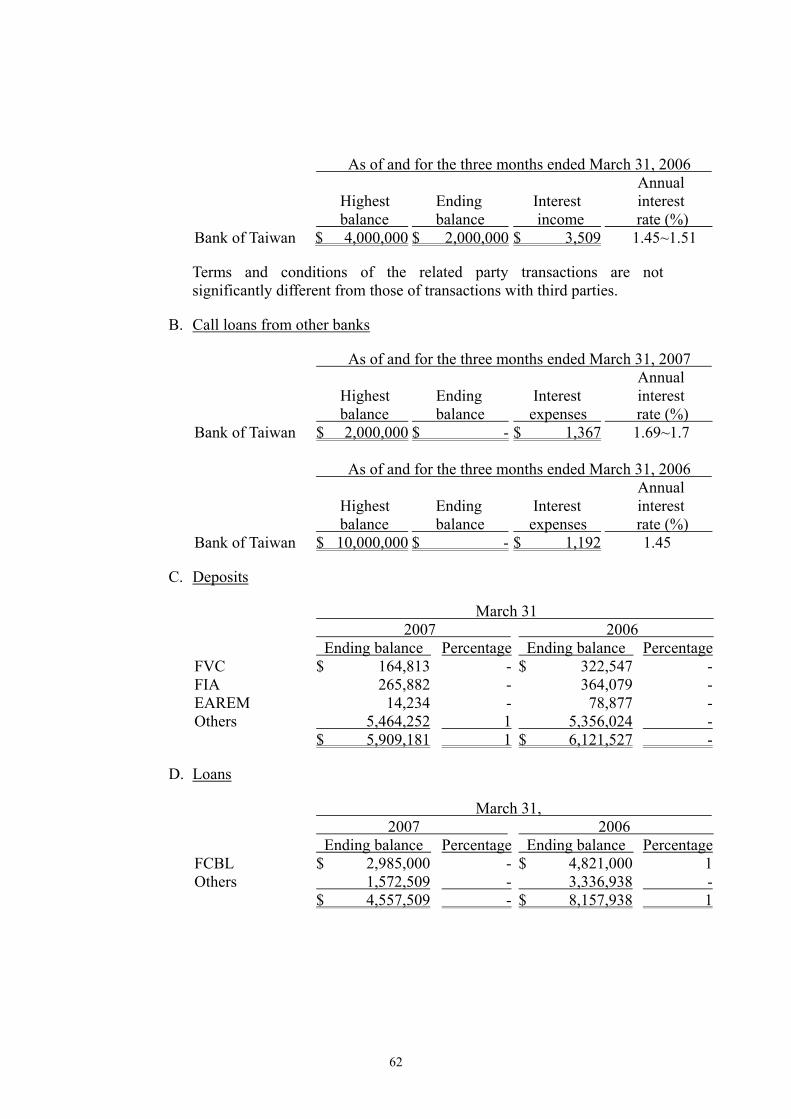

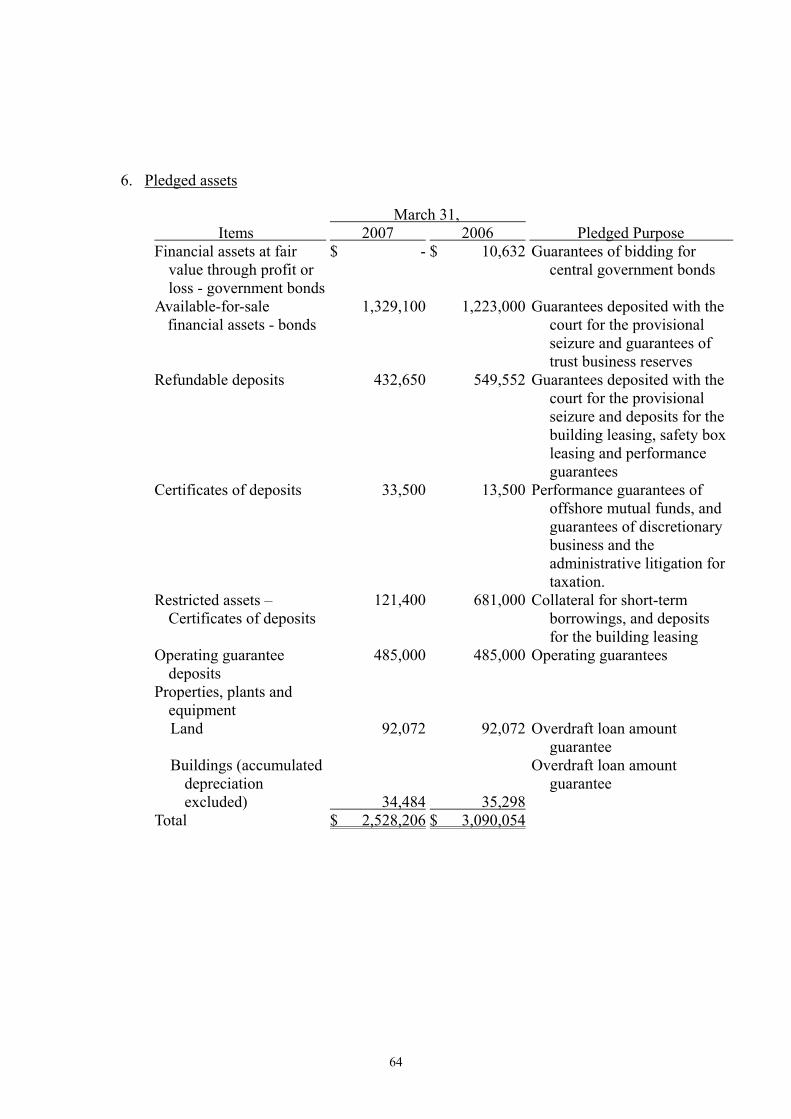

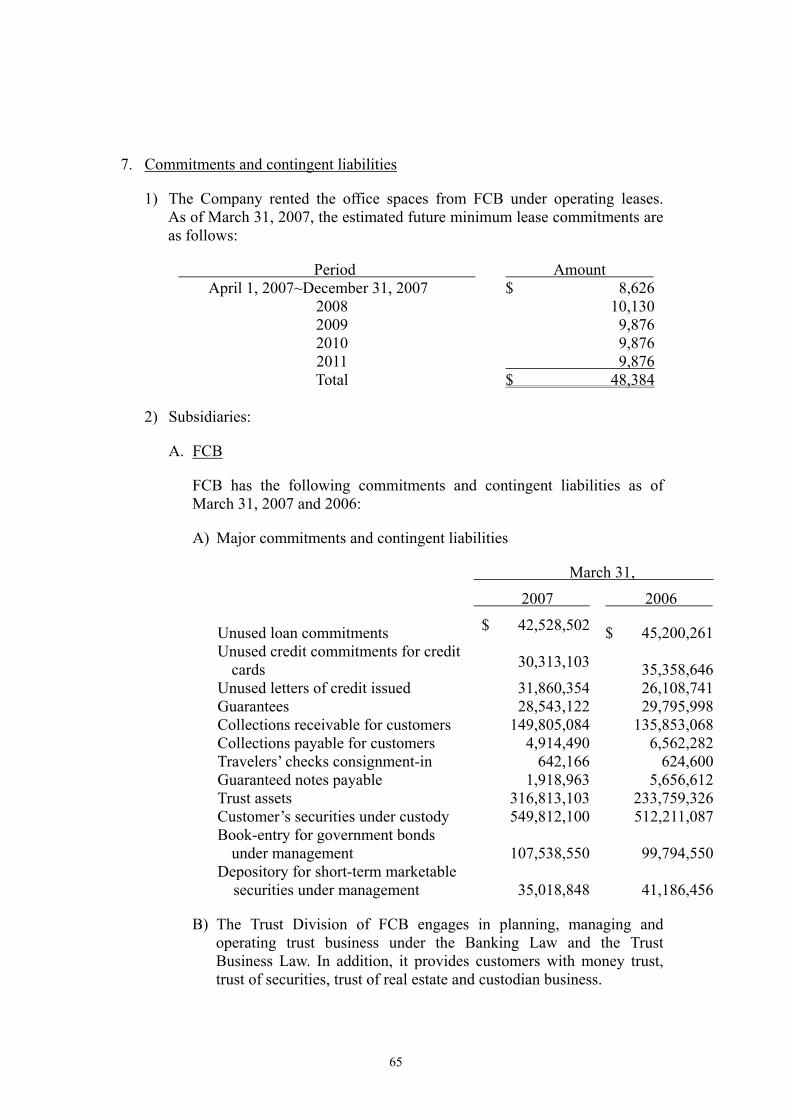

1 FIRST FINANCIAL HOLDING CO., LTD. AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT ACCOUNTANTS FOR THE THREE MONTHS ENDED MARCH 31, 2007 AND 2006

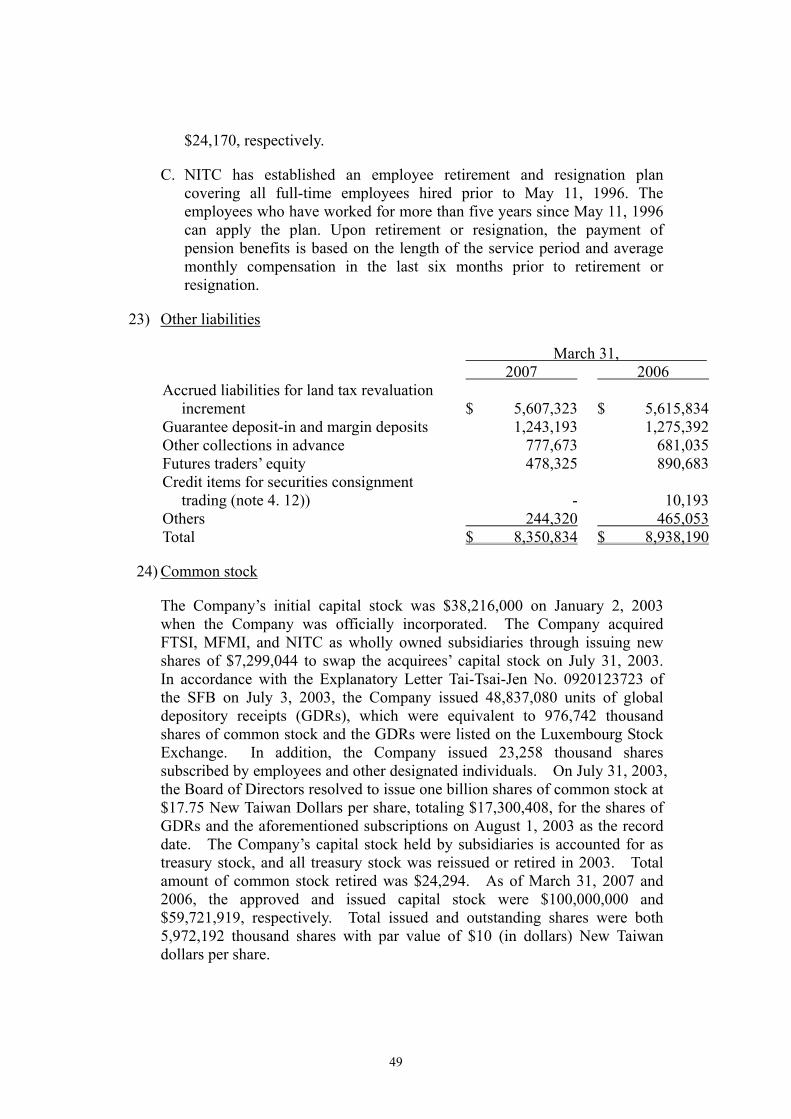

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

FIRST FINANCIAL HOLDING CO., LTD. AND ITS SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT ACCOUNTANTS

FOR THE THREE MONTHS ENDED

MARCH 31, 2007 AND 2006

2

(96) PWCR07000265

Review Report of Independent Accountants To: First Financial Holding Co., Ltd. We have reviewed the accompanying consolidated balance sheets of First Financial Holding Co., Ltd. (the “Company”) and its subsidiaries (collectively the “First Group”) as of March 31, 2007 and 2006, and the related consolidated statements of income and of cash flows for the three months then ended March 31, 2007. These consolidated financial statements are the responsibility of the First Group’s management. Our responsibility is to issue a review report on these consolidated financial statements based on our reviews.

Except as stated in the next paragraph, we conducted our reviews in accordance with the Statement of Auditing Standards No. 36 “Reviews of Financial Statements” in the Republic of China. A review consists primarily of inquiries of company personnel and analytical review procedures applied to financial data. It is substantially less in scope than an audit conducted in accordance with generally accepted auditing standards in the Republic of China, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

As described in Note 1. 3) to the consolidated financial statements as of and for the three months ended March 31, 2006, the financial statements of certain subsidiaries were not reviewed by independent accountants. Total assets of these subsidiaries as of March 31, 2006 were $1,404,186 thousand New Taiwan dollars, accounting for 0.09% of the total consolidated assets. As of March 31, 2006, total liabilities of these subsidiaries were $338,448 thousand New Taiwan dollars, accounting for 0.02% of the total consolidated liabilities. For the three months ended March 31, 2006, total net income of these subsidiaries was $140,541 thousand New Taiwan dollars, accounting for 1.73% of the consolidated net income.

Based on our reviews, except for the effects on the consolidated financial statements as of and for the three months ended March 31, 2006 of such adjustments, if any, as might have been determined to be necessary have the subsidiaries’ financial statements been reviewed as explained in the preceding paragraph, we are not aware of any material modifications that should be made to the consolidated financial statements referred to in the first paragraph in order for them to be in conformity with the “Guidelines Governing the Preparation of Financial Reports by Financial Holding

3

Companies”, “Guidelines Governing the Preparation of Financial Reports by Securities Issuers” ,“Guidelines Governing the Preparation of Financial Reports by Public Banks”, “Guidelines Governing the Preparation of Financial Reports by Securities Firms”, “Guidelines Governing the Preparation of Financial Reports by Futures Commission Merchants”, "Business Entity Accounting Act","Regulation on Business Entity Accounting Handling", and generally accepted accounting principles in the Republic of China.

As described in Note 3 to the consolidated financial statements, First Financial Holding Co., Ltd. and its subsidiaries have adopted Financial Accounting Standards No.34 “Financial Instruments: Recognition and Measurement” and No.36 “Financial Instruments: Disclosure and Presentation”, effective from January 1, 2006.

May 7, 2007 ------------------------------------------------------------------------------------------------------- The accompanying consolidated financial statements are not intended to present the consolidated financial position and consolidated results of operations and cash flows in accordance with accounting principles and practices generally accepted in countries and jurisdictions other than the Republic of China. The standards, procedures, and practices utilized in the Republic of China to audit such consolidated financial statements may differ from those generally accepted in countries and jurisdictions other than the Republic of China. Accordingly, the accompanying consolidated financial statements and review report of the independent accountants are not intended for uses by those who are not informed about the accounting principles or auditing standards generally accepted in the Republic of China and their applications in practice.

4

First Financial Holding Co., Ltd. And Its Subsidiaries Consolidated Balance Sheets

March 31, 2007 And 2006 (Expressed In Thousands of New Taiwan Dollars)

(Reviewed, Not Audited)

March 31, 2007 March 31, 2006 Change

Percentage March 31, 2007 March 31, 2006 Change

Percentage Amount Amount % Amount Amount % ASSETS LIABILITIES AND STOCKHOLDERS’ EQUITY Cash And Cash Equivalents (Note 4(1)) $ 38,474,530 $ 24,091,275 60 Due To Central Bank And Other Banks (Notes 4(14) and 5) $ 114,736,730 $ 135,858,190 ( 16) Due From Central Bank And Call Loans To Other Banks (Notes 4(2) and 5) 147,823,262 134,775,989 10 Funds Borrowed From Central Bank And Other Banks 169,731 231,559 ( 27) Financial Assets At Fair Value Through Profit Or Loss– Net(Notes 4(3) Commercial Paper Payable – Net (Note 4(15)) 2,768,101 2,546,289 9

5 and 6) 49,436,206 44,700,290 11 Financial Liabilities At Fair Value Through Profit Or Loss - Net Investments In Bills And Bonds Under Resale Agreements (Note 4(4)) 3,505,612 1,745,000 101 (Note 4(16)) 53,336,715 36,692,167 45 Receivables – Net (Note 4(5)) 31,792,940 25,813,755 23 Bills And Bonds Payable Under Repurchase Agreements Bills Discounted and Loans– Net (Notes 4(6) and 5) 983,913,161 874,046,566 13 (Note 4(17)) 14,464,437 16,956,125 ( 15) Available-for-sale Financial Assets – Net (Notes 4(7) and 6) 75,182,169 88,331,124 ( 15) Payables (Notes 4(18)) 49,310,202 36,358,177 36 Held-to-maturity Financial Assets – Net (Note 4(8)) 201,474,543 227,192,836 ( 11) Deposits And Remittances (Notes 4(19) and 5) 1,221,573,427 1,128,643,000 8 Equity Investments Accounted For Under The Equity Method (Note 4(9)) 3,455,919 3,291,510 5 Bonds Payable (Note 4(20)) 25,500,000 28,992,051 ( 12) Other Financial Assets – Net (Note 4(10) and (13)) 20,939,653 32,593,643 ( 36) Other Borrowings (Note 4(21)) 2,915,200 2,393,186 22 Properties , Plants And Equipment – Net (Notes 4(11) and 6) 24,079,034 24,684,513 ( 2) Accrued Pension Liabilities (Note 4(22)) 1,510,288 1,415,035 7 Intangible Assets 394,366 292,634 35 Other Financial Liabilities 518,985 6,557,019 ( 92) Other assets Reserves For Operation And Liabilities 833,116 796,445 5 Other Assets (Notes 4(12), and 6) 12,198,633 13,769,075 ( 11) Other Liabilities (Note 4(23)) 8,350,834 8,938,190 ( 7) Deferred Income Tax Assets (Note4(28)) 7,117,728 10,385,526 ( 31) TOTAL LIABILITIES 1,495,987,766 1,406,377,433 6 STOCKHOLDERS’ EQUITY Common Stock (Note 4(24)) 59,721,919 58,265,287 2

Additional Paid-in Capital (Note 4(25)) 15,704,668 15,718,385 - Retained Earnings Legal reserve (Notes 4(26)) 2,447,294 1,029,755 138 Special reserve (Notes 4(26)) 78,743 269,956 ( 71) Unappropriated earnings (Notes 4(27)) 19,639,422 18,974,074 4 Other Stockholders’ Equity Cumulative translation adjustments 112,353 ( 168,426 ) -

Unrealized gain or loss on available-for-sale financial assets

(Note 4(7)) 5,797,453 4,852,579 19 Unrealized gain or loss on cash flow hedges (Note 10(1)) 299,675 394,693 ( 24) Net loss not recognized as pension cost ( 1,537 ) - - TOTAL STOCKHOLDERS’ EQUITY 103,799,990 99,336,303 4 TOTAL ASSETS $ 1,599,787,756 $ 1,505,713,736 6 TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY $ 1,599,787,756 $ 1,505,713,736 6

The accompanying notes are an integral part of these consolidated financial statements.

See PricewaterhouseCoopers reviewed report date May 7, 2007.

5

First Financial Holding Co., Ltd. And Its Subsidiaries Consolidated Statements of Income

For The Three Months Ended March 31, 2007 And 2006 (Expressed In Thousands of New Taiwan Dollars, Except For Earnings Per Share)

(Reviewed, Not Audited)

For The Three Months Ended March 31,

2007 2006 Change

Percentage Amount Amount % Interest Income $ 11,557,599 $ 10,220,302 13 Less: Interest Expenses ( 6,275,506 ) ( 5,122,097 ) 23 Net Interest Income 5,282,093 5,098,205 4 Net Non-interest Income

Net service fee and commission income 1,958,430 1,479,099 32 Gains or losses on financial assets and

financial liabilities at fair value through profit or loss (Note4(3)(16)) 770,082 480,077 60

Realized gains or losses on available-for-sale financial assets 220,162 7,941 2,672

Realized gains or losses on held-to-maturity financial assets 1,845 1,864 ( 1)

Income from equity investments accounted for under the equity method – net(Note 4(9)) 70,023 108,961 ( 36)

Foreign exchange gains or losses 86,056 287,210 ( 70) Impairment losses (Note4(13)) ( 21,307 ) ( 52,722 ) ( 60) Other non-interest income

Bad debts and overdue accounts recovered 636,098 524,658 21 Other 15,703 171,453 ( 91)Net Revenues 9,019,185 8,106,746 11 Provision For Credit Losses ( 1,394,494 ) ( 1,362,421 ) 2 Operating Expenses

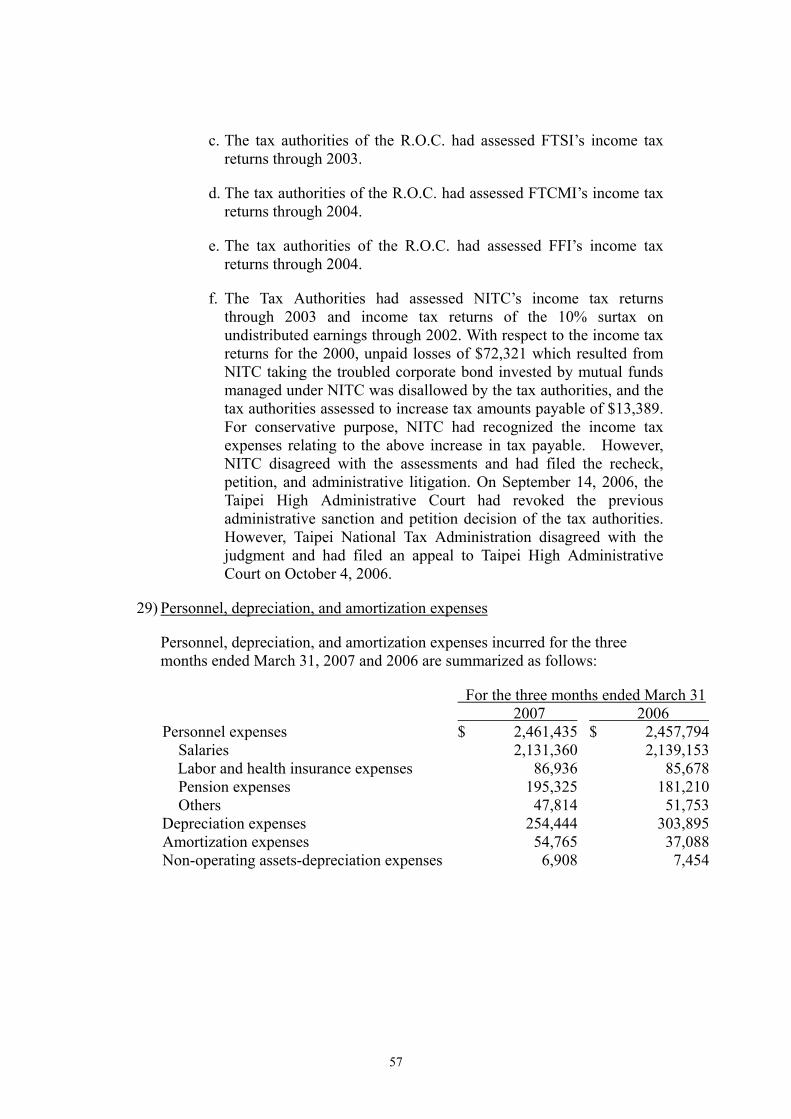

Personnel expenses (Note 4(29)) ( 2,461,435 ) ( 2,457,794 ) - Depreciation and amortization expenses

(Note 4(29)) ( 316,117 ) ( 348,437 ) ( 9) Business expenses and general and

administrative expenses ( 1,091,440 ) ( 1,040,006 ) 5 Consolidated Income From Continuing

Operations Before Income Taxes 3,755,699 2,898,088 30 Income Tax Expenses (Note 4(28)) ( 800,855 ) ( 694,895 ) 15 Consolidated Income From Continuing

Operations After Income Taxes 2,954,844 2,203,193 34 Cumulative Effect Of A Change In Accounting

Principle (Net Of Income Taxes Of $367 AND $0 ) - 647,608 ( 100)

Total Consolidated Net Income $ 2,954,844 $ 2,850,801 4 Total Consolidated Net Income Attributed to:

Stockholders of parent company $ 2,954,844 $ 2,850,801 Minority interests $ - $ -

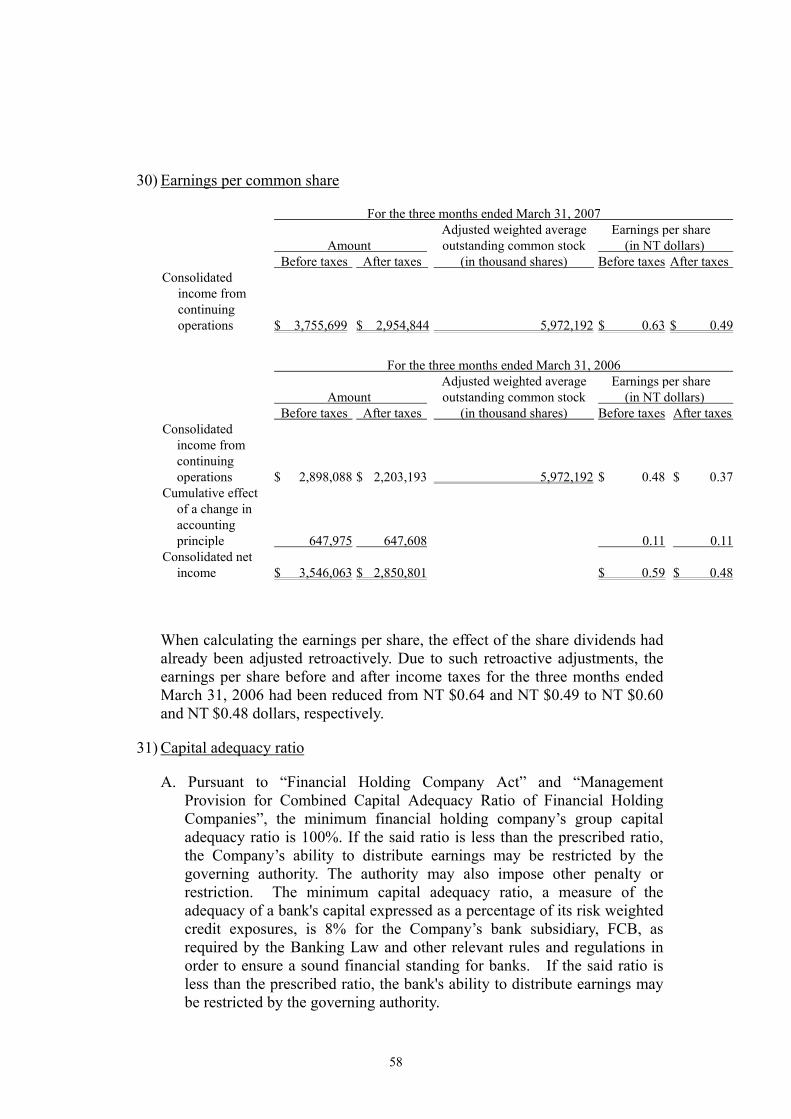

Earnings Per Common Share (Note 4(30)) Before Taxes After Taxes Before Taxes After Taxes Consolidated Income From Continuing

Operations $ 0.63 $ 0.49 $ 0.48 $ 0.37 Cumulative Effect Of A Change In Accounting

Principle (Note 3) - - 0.11 0.11 $ 0.63 $ 0.49 $ 0.59 $ 0.48

The accompanying notes are an integral part of these consolidated financial statements. See PricewaterhouseCoopers reviewed report date May 7, 2007.

6

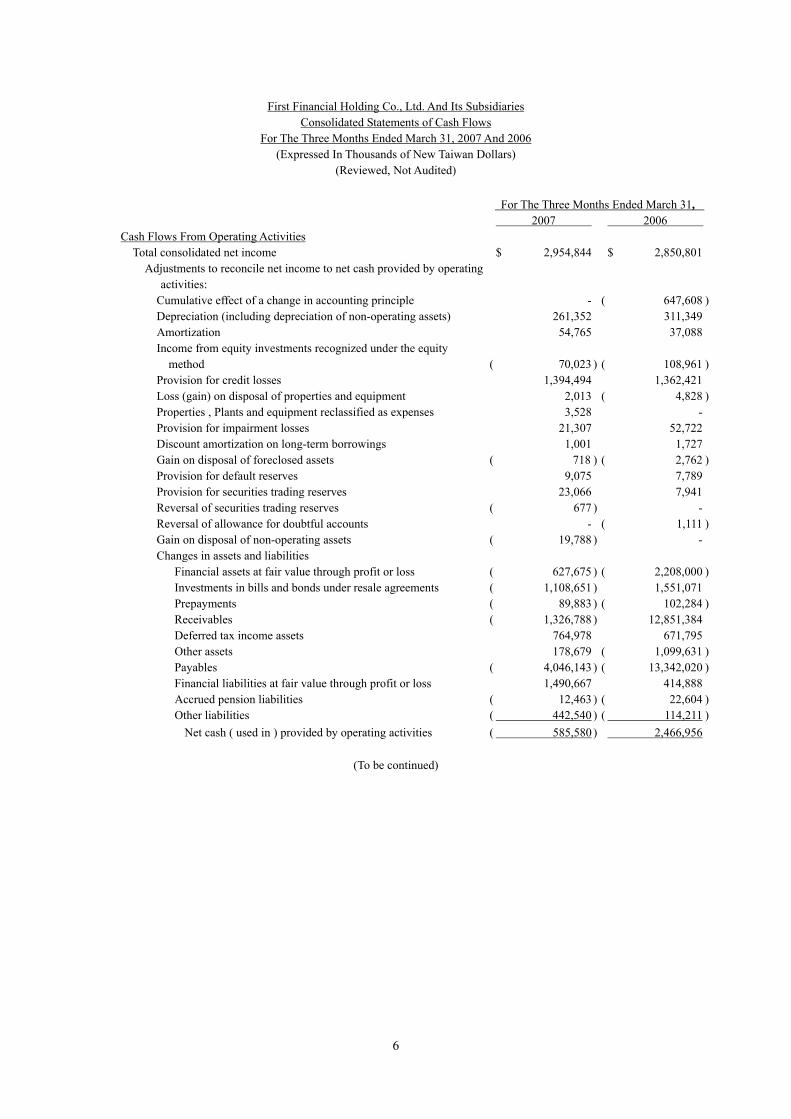

First Financial Holding Co., Ltd. And Its Subsidiaries Consolidated Statements of Cash Flows

For The Three Months Ended March 31, 2007 And 2006 (Expressed In Thousands of New Taiwan Dollars)

(Reviewed, Not Audited)

For The Three Months Ended March 31, 2007 2006 Cash Flows From Operating Activities Total consolidated net income $ 2,954,844 $ 2,850,801 Adjustments to reconcile net income to net cash provided by operating

activities: Cumulative effect of a change in accounting principle - ( 647,608 ) Depreciation (including depreciation of non-operating assets) 261,352 311,349 Amortization 54,765 37,088 Income from equity investments recognized under the equity

method ( 70,023 ) ( 108,961 ) Provision for credit losses 1,394,494 1,362,421 Loss (gain) on disposal of properties and equipment 2,013 ( 4,828 ) Properties , Plants and equipment reclassified as expenses 3,528 - Provision for impairment losses 21,307 52,722 Discount amortization on long-term borrowings 1,001 1,727 Gain on disposal of foreclosed assets ( 718 ) ( 2,762 ) Provision for default reserves 9,075 7,789 Provision for securities trading reserves 23,066 7,941 Reversal of securities trading reserves ( 677 ) - Reversal of allowance for doubtful accounts - ( 1,111 ) Gain on disposal of non-operating assets ( 19,788 ) - Changes in assets and liabilities Financial assets at fair value through profit or loss ( 627,675 ) ( 2,208,000 ) Investments in bills and bonds under resale agreements ( 1,108,651 ) 1,551,071 Prepayments ( 89,883 ) ( 102,284 ) Receivables ( 1,326,788 ) 12,851,384 Deferred tax income assets 764,978 671,795 Other assets 178,679 ( 1,099,631 ) Payables ( 4,046,143 ) ( 13,342,020 ) Financial liabilities at fair value through profit or loss 1,490,667 414,888 Accrued pension liabilities ( 12,463 ) ( 22,604 ) Other liabilities ( 442,540 ) ( 114,211 )

Net cash ( used in ) provided by operating activities ( 585,580 ) 2,466,956

(To be continued)

7

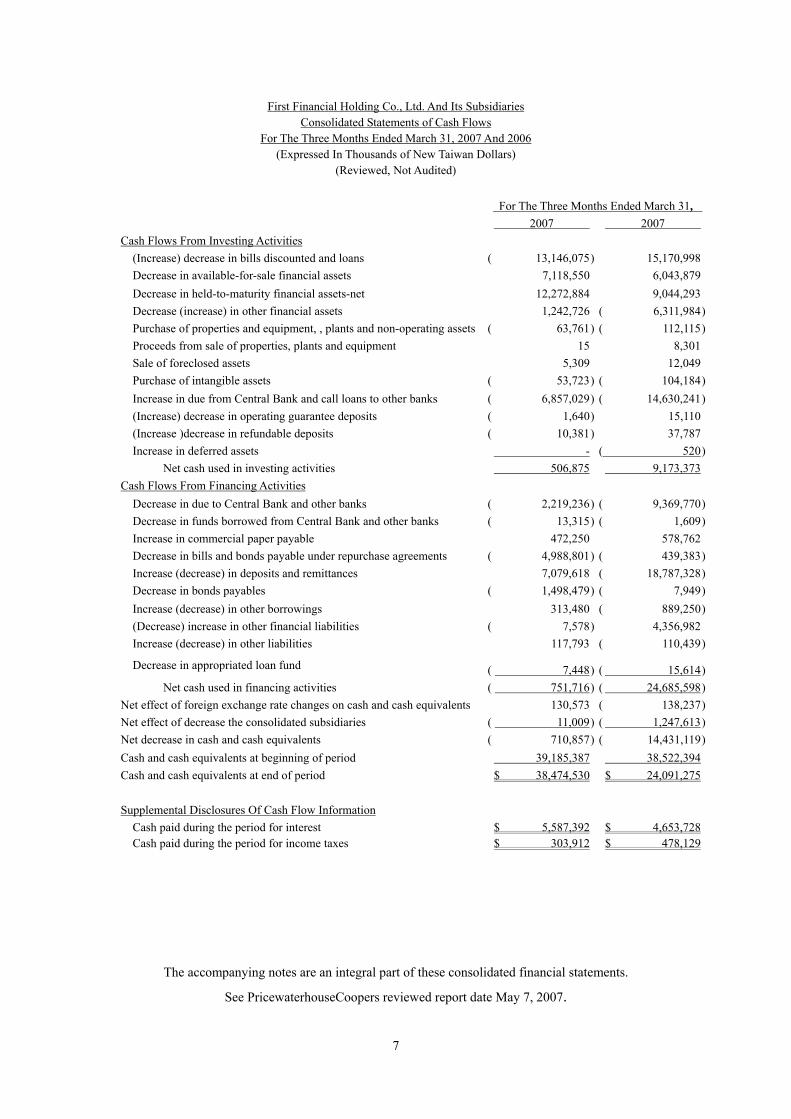

First Financial Holding Co., Ltd. And Its Subsidiaries Consolidated Statements of Cash Flows

For The Three Months Ended March 31, 2007 And 2006 (Expressed In Thousands of New Taiwan Dollars)

(Reviewed, Not Audited)

For The Three Months Ended March 31, 2007 2007 Cash Flows From Investing Activities (Increase) decrease in bills discounted and loans ( 13,146,075 ) 15,170,998 Decrease in available-for-sale financial assets 7,118,550 6,043,879 Decrease in held-to-maturity financial assets-net 12,272,884 9,044,293 Decrease (increase) in other financial assets 1,242,726 ( 6,311,984 ) Purchase of properties and equipment, , plants and non-operating assets ( 63,761 ) ( 112,115 ) Proceeds from sale of properties, plants and equipment 15 8,301 Sale of foreclosed assets 5,309 12,049 Purchase of intangible assets ( 53,723 ) ( 104,184 ) Increase in due from Central Bank and call loans to other banks ( 6,857,029 ) ( 14,630,241 ) (Increase) decrease in operating guarantee deposits ( 1,640 ) 15,110 (Increase )decrease in refundable deposits ( 10,381 ) 37,787 Increase in deferred assets - ( 520 )

Net cash used in investing activities 506,875 9,173,373 Cash Flows From Financing Activities Decrease in due to Central Bank and other banks ( 2,219,236 ) ( 9,369,770 ) Decrease in funds borrowed from Central Bank and other banks ( 13,315 ) ( 1,609 ) Increase in commercial paper payable 472,250 578,762 Decrease in bills and bonds payable under repurchase agreements ( 4,988,801 ) ( 439,383 ) Increase (decrease) in deposits and remittances 7,079,618 ( 18,787,328 ) Decrease in bonds payables ( 1,498,479 ) ( 7,949 ) Increase (decrease) in other borrowings 313,480 ( 889,250 ) (Decrease) increase in other financial liabilities ( 7,578 ) 4,356,982 Increase (decrease) in other liabilities 117,793 ( 110,439 )

Decrease in appropriated loan fund ( 7,448 ) ( 15,614 )Net cash used in financing activities ( 751,716 ) ( 24,685,598 )

Net effect of foreign exchange rate changes on cash and cash equivalents 130,573 ( 138,237 )Net effect of decrease the consolidated subsidiaries ( 11,009 ) ( 1,247,613 )Net decrease in cash and cash equivalents ( 710,857 ) ( 14,431,119 )Cash and cash equivalents at beginning of period 39,185,387 38,522,394 Cash and cash equivalents at end of period $ 38,474,530 $ 24,091,275 Supplemental Disclosures Of Cash Flow Information Cash paid during the period for interest $ 5,587,392 $ 4,653,728 Cash paid during the period for income taxes $ 303,912 $ 478,129

The accompanying notes are an integral part of these consolidated financial statements.

See PricewaterhouseCoopers reviewed report date May 7, 2007.

8

First Financial Holding Co., Ltd. And Its Subsidiaries Notes To The Consolidated Financial Statements

For the Three Months Ended March 31, 2007 and 2006 (Expressed in Thousands of New Taiwan Dollars, Unless Otherwise Indicated)

(Reviewed, Not Audited)

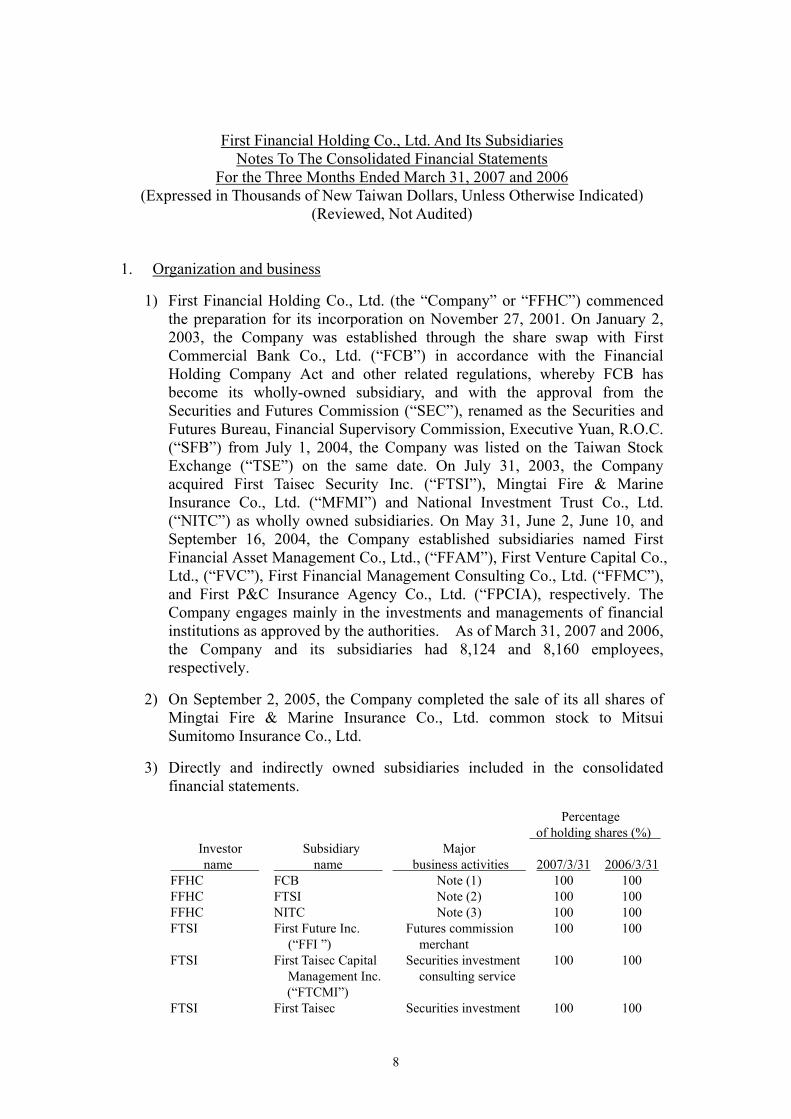

1. Organization and business

1) First Financial Holding Co., Ltd. (the “Company” or “FFHC”) commenced the preparation for its incorporation on November 27, 2001. On January 2, 2003, the Company was established through the share swap with First Commercial Bank Co., Ltd. (“FCB”) in accordance with the Financial Holding Company Act and other related regulations, whereby FCB has become its wholly-owned subsidiary, and with the approval from the Securities and Futures Commission (“SEC”), renamed as the Securities and Futures Bureau, Financial Supervisory Commission, Executive Yuan, R.O.C. (“SFB”) from July 1, 2004, the Company was listed on the Taiwan Stock Exchange (“TSE”) on the same date. On July 31, 2003, the Company acquired First Taisec Security Inc. (“FTSI”), Mingtai Fire & Marine Insurance Co., Ltd. (“MFMI”) and National Investment Trust Co., Ltd. (“NITC”) as wholly owned subsidiaries. On May 31, June 2, June 10, and September 16, 2004, the Company established subsidiaries named First Financial Asset Management Co., Ltd., (“FFAM”), First Venture Capital Co., Ltd., (“FVC”), First Financial Management Consulting Co., Ltd. (“FFMC”), and First P&C Insurance Agency Co., Ltd. (“FPCIA), respectively. The Company engages mainly in the investments and managements of financial institutions as approved by the authorities. As of March 31, 2007 and 2006, the Company and its subsidiaries had 8,124 and 8,160 employees, respectively.

2) On September 2, 2005, the Company completed the sale of its all shares of Mingtai Fire & Marine Insurance Co., Ltd. common stock to Mitsui Sumitomo Insurance Co., Ltd.

3) Directly and indirectly owned subsidiaries included in the consolidated financial statements.

Percentage of holding shares (%)

Investor Subsidiary Major name name business activities 2007/3/31 2006/3/31FFHC FCB Note (1) 100 100 FFHC FTSI Note (2) 100 100 FFHC NITC Note (3) 100 100 FTSI First Future Inc.

(“FFI ”) Futures commission

merchant 100 100

FTSI First Taisec Capital Management Inc.

(“FTCMI”)

Securities investment consulting service

100 100

FTSI First Taisec Securities investment 100 100

9

Percentage of holding shares (%)

Investor Subsidiary Major name name business activities 2007/3/31 2006/3/31

Securities (Asia) Limited (“FTSL”) (Note 4)

consulting service

FTSL

First Worldsec Securities Limited (‘FWSL”) (Note4)

Securities investment consulting service

100 100

Note (1) FCB was established in 1899 and it had been a listed company since February 9, 1962. It was privatized on January 22, 1998. On January 2, 2003, FCB became the subsidiary of First Financial Holding Co., Ltd. through the share swap and was de-listed from the TSE to become a public company in accordance with the related regulations set forth by the SFB. As of March 31, 2007, FCB comprises various Divisions, including Operation Division, Trust Division, International Business Division, Offshore Banking Unit, domestic and overseas branches, and representative offices. FCB engages mainly in the following business activities:

1) Business activities provided by the Banking Law;

2) Trust business as authorized by the authorities;

3) Establishing overseas branches to engage in those business activities as approved by the respective local governments;

4) Other business activities approved by the authorities.

Note (2) FTSI (formerly known as Taisec Securities Inc.) was established in August 1988 and it became the subsidiary of the Company on July 31, 2003. FTSI is authorized to engage in the following business activities:

1) Brokerages and proprietary trading of marketable securities at the securities exchange markets;

2) Underwriting of marketable securities;

3) Registration and transfer agency service for securities;

4) Margin loans and stock loans of marketable securities trading;

5) Futures introducing broker business;

6) Brokerages of futures business; and

7) Other securities-related businesses as approved by the competent authorities.

10

FTSI transferred its futures brokerage business to First Futures Inc. (the wholly owned subsidiary of FTSI) to promote its business in November 2003. FTSI founded futures dealing department to perform future business in September 2005.

As FCB and FTSI are both wholly owned subsidiaries of the Company, the Board of Directors of FTSI resolved to acquire securities brokerage business of FCB at book value to leverage the synergies of the First Group, effective on December 1, 2003.

Note (3) NITC became the wholly owned subsidiary of the Company through the share swap on July 31, 2003. NITC engages mainly in the management of securities investment trust funds.

Note (4)The financial statements of such investees which are consolidated in the First Group’s first quarter consolidated financial statements were not reviewed by the independent accountants as of and for the three month ended March 31, 2007 and 2006. The Company believed that the impact, if any, would be insignificant had the investees’ financial statements been reviewed.

4) Movement of consolidated entities.

A. Increase in consolidated entities: None

B. Decrease in consolidated entities

Percentage of the Company’s direct/ indirect holding ownership (%)

Name RelationshipMajor Business

Activities March 31, 2007 March 31,2006 Note

NITC (Cayman Islands) Ltd.

(“NITC (Cayman)”)

Indirect Subsidiary

1. Issuing beneficiary certificates and raising securities investment trust funds;

2. Managing securities investment trust funds to invest in securities;

3. Engaging in trading and investments approved by the British Cayman Islands government

100 100 Note 1

Note 1: Effective from January 1, 2006, NITC prepares its consolidated financial statements pursuant to the amended Statement of Financial Accounting Standards No.7, “Consolidated Financial Statements”. As the NITC Cayman’s total assets accounts for less than 1% of the NITC’s total assets and its net revenue account for less than 0.2% of NITC’s net revenue, the NITC Cayman is immaterial to NITC. Therefore, excluding the NITC Cayman financial statements from the consolidated financial statements will

11

not significantly affect the First Group’s overall consolidated financial statement presentation.

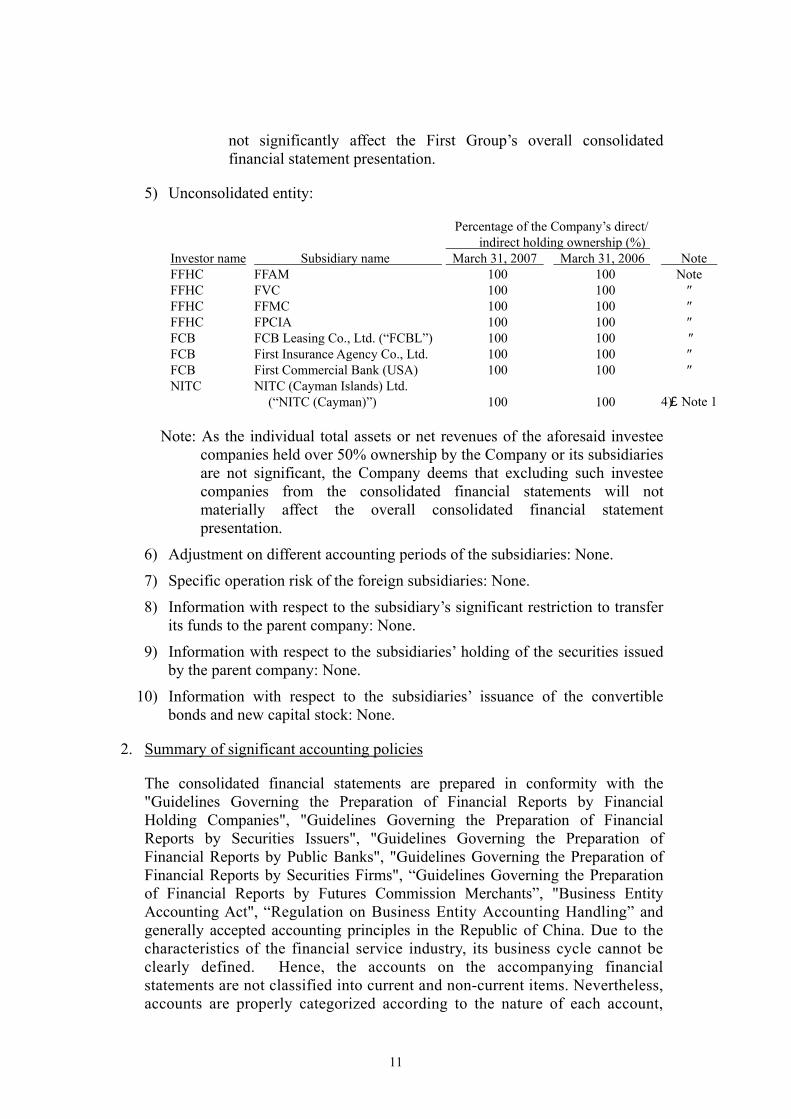

5) Unconsolidated entity:

Percentage of the Company’s direct/ indirect holding ownership (%)

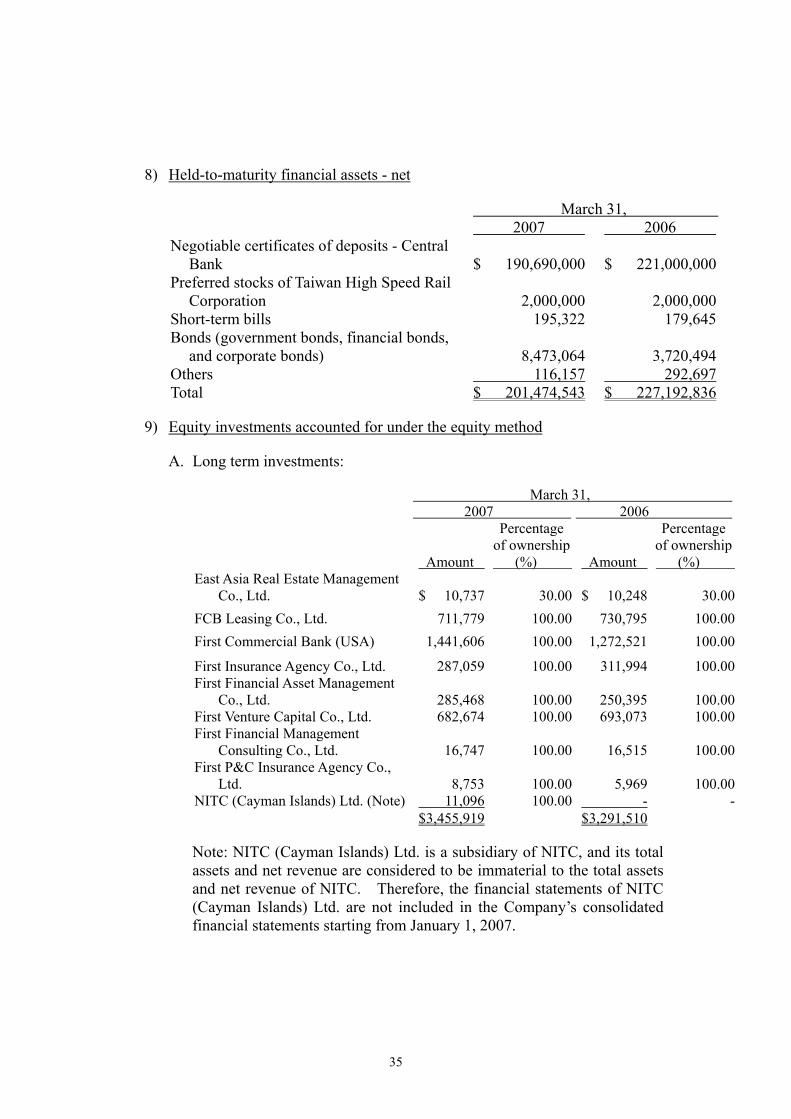

Investor name Subsidiary name March 31, 2007 March 31, 2006 Note FFHC FFAM 100 100 Note FFHC FVC 100 100 ″ FFHC FFMC 100 100 ″ FFHC FPCIA 100 100 ″ FCB FCB Leasing Co., Ltd. (“FCBL”) 100 100 ″ FCB First Insurance Agency Co., Ltd. 100 100 ″ FCB First Commercial Bank (USA) 100 100 ″ NITC NITC (Cayman Islands) Ltd.

(“NITC (Cayman)”)

100

100

4)、Note 1

Note: As the individual total assets or net revenues of the aforesaid investee companies held over 50% ownership by the Company or its subsidiaries are not significant, the Company deems that excluding such investee companies from the consolidated financial statements will not materially affect the overall consolidated financial statement presentation.

6) Adjustment on different accounting periods of the subsidiaries: None.

7) Specific operation risk of the foreign subsidiaries: None.

8) Information with respect to the subsidiary’s significant restriction to transfer its funds to the parent company: None.

9) Information with respect to the subsidiaries’ holding of the securities issued by the parent company: None.

10) Information with respect to the subsidiaries’ issuance of the convertible bonds and new capital stock: None.

2. Summary of significant accounting policies

The consolidated financial statements are prepared in conformity with the "Guidelines Governing the Preparation of Financial Reports by Financial Holding Companies", "Guidelines Governing the Preparation of Financial Reports by Securities Issuers", "Guidelines Governing the Preparation of Financial Reports by Public Banks", "Guidelines Governing the Preparation of Financial Reports by Securities Firms", “Guidelines Governing the Preparation of Financial Reports by Futures Commission Merchants”, "Business Entity Accounting Act", “Regulation on Business Entity Accounting Handling” and generally accepted accounting principles in the Republic of China. Due to the characteristics of the financial service industry, its business cycle cannot be clearly defined. Hence, the accounts on the accompanying financial statements are not classified into current and non-current items. Nevertheless, accounts are properly categorized according to the nature of each account,

12

and sequenced by their liquidity. Significant accounting policies of the Company are summarized below:

1) Principles for preparation of the consolidated financial statements

A. Since the first quarter of 2006, in compliance with the amended “Guidelines Governing the Preparation of Financial Reports by Financial Holding Companies”, the Company has only prepared the consolidated financial statements. In addition to the bank subsidiary, insurance subsidiary, and securities subsidiary, which have been included in the consolidated financial statements, in accordance with the amended Statement of Financial Accounting Standards (SFAS) No. 7 “Consolidated Financial Statements” in the Republic of China, the investees whose voting stock interests are more than 50% directly or indirectly held by the Company are included in the consolidated financial statements except for those whose total assets and operating revenues are considered to be immaterial to the Company. Under the newly amended SFAS No 7, the prior year consolidated financial statements are not required to be restated to consolidate the previously unconsolidated subsidiaries.

B. Accounting treatment for obtaining or losing control over subsidiaries during the year is in accordance with the Financial Accounting Standards No. 7 “Consolidated Financial Statements”, the Company shall include the subsidiaries’ revenues and expenses in the consolidated financial statements from the date of obtaining the control or shall exclude the subsidiaries’ revenues and expense in the consolidated financial statements from the date of losing the control.

C. The Company prepares the consolidated financial statements by aggregating the Company’s and subsidiaries’ assets, liabilities, revenues, and expenses. Inter-company transactions and balances, as well as investment in subsidiaries versus subsidiaries’ stockholders’ equity, have been eliminated during the consolidation. The contents of the consolidated financial statements conformed to the “Guidelines Governing the Preparation of Financial Reports by Financial Holding Companies” and the guidelines governing the preparation of financial reports for each business line.

D. Under Article 4 of the Financial Holding Company Act, a controlling interest is that a financial holding company holds more than twenty-five percent of voting interests or capital stock of a bank, insurance company or securities firm, or has directly or indirectly designated more than half of the directors of a bank, insurance company or securities firm.

E. The financial statements of FCB include head office accounts, branch office accounts, and offshore banking branch accounts. All significant inter-office accounts and transactions have been eliminated in the consolidated financial statements.

13

2) Cash and cash equivalents

Cash includes cash on hand, demand deposits, checking deposits, and cancelable time deposits. Cash equivalents are short-term investments that are readily convertible to known amounts of cash and are so near the maturity date that such investments present insignificant risk of value arising from changes in interest rates. Such investments include treasury bills, commercial paper, bankers’ acceptance, and so forth whose maturity dates are less than three months from the investment dates.

3) Financial assets and financial liabilities at fair value through profit or loss

A. Equity securities and beneficiary certificates are accounted for using trade date accounting; debt securities, and derivative financial instruments are accounted for using settlement date accounting. Financial instruments are initially recognized at their fair values.

B. Financial assets and liabilities at fair value through profit or loss shall be measured at fair value with changes in fair value recognized as gains or losses in the current period. For stocks listed on TSE or OTC and closed-end funds, fair value is determined based on the closing price at the balance sheet date. For open-end funds, fair value is determined based on the net asset value of the given fund at the balance sheet date. For beneficiary securities, fair value is determined based on the discounted value of expected future cash flows at the balance sheet date. For bonds listed on TSE or OTC, fair value is determined based on the latest transaction price of Automatic Order Matching and Execution System in OTC. For those bonds not listed on the TSE or OTC, fair value is determined based on the discounted value of expected future cash flows at the balance sheet date or the market price provided by Bloomberg or Reuters. For derivative financial instruments for trading purpose, fair value is determined based on a quoted market price in an active market at the balance sheet date if there is a quoted market price in an active market, or is determined based on applying other valuation techniques, such as discounted cash flow analyses or option pricing models, to estimate the fair value at the balance sheet date if there is no quoted market price in an active market.

C. Criteria to designate financial assets and financial liabilities as at fair value through profit or loss are as follows:

A) Hybrid (combined) instruments;

B) The designation can eliminate or significantly reduce a measurement or recognition inconsistency; or

C) The designation is in compliance with a documented risk management or investment strategy of the Company and its subsidiaries to evaluate the performance of assets or liabilities based on a fair value basis.

14

4) Bills and bonds under repurchase or resale agreements

Bills and bonds under resale or repurchase agreements are accounted for under the financing method. Bills and bonds sold under repurchase agreements are recorded as “Bills and bonds payable under repurchase agreements” at the sale date. Bills and bonds invested under resale agreements are recorded as “Investments in bills and bonds under resale agreements” at the purchase date. The difference between the cost and the repurchase price is recorded as interest expenses between the sale date and the repurchase date. The difference between the cost and the resale price is recorded as interest income between the purchase date and the resale date.

5) Margin loans, stock loans and refinancing

A. FTSI conducts margin loan business to provide funds for its customers to purchase securities. The margin loans given to customers are recorded as “margin loans receivable” and are collateralized by the securities that the customers purchase. The collateral securities are recorded through memorandum accounts and are returned to customers when the loans are repaid.

B. FTSI conducts stock loan business to lend securities to its customers to sell short. The deposits received from customers on FTSI’s securities lending are recorded as “deposits received on securities lending”. Proceeds from sales of securities lent to customers less any securities exchange taxes, dealer’s commissions, and financing charges are as the collateral for securities lent and are recorded under “collateralized proceeds payable from securities lending”, the securities lent to customers to sell short are recorded through memorandum accounts. When the customers return the securities, FTSI gives the deposits received and the proceeds from securities sold back to customers.

C. The “refinancing of margin loans” refers to refinancing to borrow funds from securities finance companies when there are insufficient funds to conduct margin loan business. The refinancing of margin loans is recorded as “refinancing borrowing” and is collateralized by the securities purchased by customers on margin loans.

D. The “refinancing of stock loans” refers to refinancing to borrow securities from securities finance companies when there are insufficient securities to conduct securities lending business. The deposits or collateral given to securities finance companies by FTSI are recorded as “refinancing margin deposits”. The proceeds from securities lent to customer to sell short are given to the securities finance companies as the collateral and are recorded as “collateralized proceeds payable from securities lending” and “refinancing deposits receivable”, respectively.

15

6) Customer margin deposit account

FFI conducts futures brokerage business and requires customers to open margin accounts to receive margin deposits and premiums, and to adjust the mark-to-market differences.

7) Futures trader’s equity / Futures margin deposits receivable

The futures trader’s equity includes margin deposits and premiums received from futures customers and the mark-to-market adjustment, and the futures trader’s equity is recorded as liabilities on the balance sheet. The customers’ margin accounts cannot be offset reciprocally except for the same type of account under the same customer. When the futures trader’s equity results in a debit balance, it should be recorded as futures margin deposits receivable.

8) Bills discounted and loans

A. Bills discounted and loans (including non-performing loans) are recorded at the amounts of principal outstanding. Interest income is recognized on an accrual basis except for interest on non–performing loans.

B. All non-performing loans under which there is no principal payment after the lapse of six full months, lawsuit has been filed against borrower and guarantor(s) or the collaterals are executed shall be transferred to non-accrual loans account item. Interest shall cease to be accrued for non-performing loans that are transferred to non-accrual loans account item. Any unpaid interest due on a non-performing loan prior to its transfer to a non-accrual loan shall be transferred to the non-accrual loans item together with principal.

C. When there is postponement or modification of the credit terms for the debtors, the Bank agrees to receive partial interests and the rest of interests will cease accrual and will be recognized after cash is received.

9) Available-for-sale financial assets

A. Equity securities are accounted for using trade date accounting; Debt securities are accounted for using settlement date accounting. Such financial instruments are initially recognized at fair value plus the acquisition or issuance cost.

B. Available-for-sale financial assets are measured at fair value with changes in fair value recognized in an adjustment account in the stockholders’ equity. When the financial asset is derecognized, the cumulative gain or loss that was previous recognized in equity is recognized in profit or loss in income statement. For stocks listed on the TSE or OTC and closed-end funds, fair value is determined based on the closing price at the balance sheet date. For open-end funds, fair value is determined based on the net asset value of the given fund at the

16

balance sheet date. For beneficiary securities, fair value is determined based on the discounted value of expected future cash flows at the balance sheet date. For bonds listed on TSE or OTC, fair value is determined based on the latest transaction price of Automatic Order Matching and Execution System in OTC. For those bonds not listed on the TSE or OTC, fair value is determined based on discounted value of expected future cash flows at the balance sheet date or the market price provided by Bloomberg or Reuters.

C. An impairment loss is recognized when there is objective evidence of impairment. In the subsequent period, if the amount of the impairment loss decreases due to an event occurring after the impairment was originally recognized, for equity instruments, the decrease shall be recognized as an adjustment account in the stockholders’ equity; and for debt instruments, the previously recognized impairment loss is reversed through profit and loss.

10) Held-to-maturity financial assets

A. Held-to-maturity financial assets are accounted for using settlement date accounting and are initially recognized at fair value plus the acquisition or issuance cost. Gains or losses are recognized in the income statement when the investments are derecognized.

B. Held-to-maturity financial assets are measured at amortized cost using the interest method at the balance sheet date.

C. An impairment loss is recognized when there is objective evidence of impairment. In the subsequent period, if the amount of the impairment loss decreases due to an event occurring after the impairment was originally recognized, the previously recognized impairment loss is reversed through profit and loss to the extent that the carrying amounts shall not exceed the amortized cost that would have been determined had no impairment loss been recognized in prior years.

11) Equity investments accounted for under the equity method

A. The Company was formed by FCB pursuant to the Explanatory Note (90) No. 182 of the Accounting Research and Development Foundation of the R.O.C. dated October 29, 2001. Capital expenditure incurred by the Company to acquire equity interest in a financial institution through share swap is stated at the book value of the respective financial institution’s assets less the book value of liabilities. The par value of the new shares issued is recorded as common stock, and the amount in excess of the par value is recorded as capital surplus.

B. Long-term equity investments that the First Group owns at least 20% of the investees’ voting stock interests or exercises significant influence over the investees are accounted for under the equity method. The

17

carrying amount of such equity investments are evaluated pursuant to the investment costs plus or minus the net income or loss and changes in stockholders’ equity of the investee recognized proportionally according to the percentage of the investee’s ownership held by the First Group. The cash dividends received from investees are recorded as deduction of the investment cost. For the stock dividends received from investees, the investment amount will not be increased and the investment income will not be recognized. A memorandum entry will be made to record the additional shares received. When there is sufficient evidence to indicate that the fair value of the investment is impaired and the probability of the recovery is remote, the loss on investments is recognized in the current period. If such equity investments are disposed of, the cost is calculated under the weighted average method.

C. Effective from January 1, 2006, for an investee company accounted for under the equity method, if the First Group does not have control interests but can exercise significant influence over the investee, investment losses are recognized to the extent that the balance of the investment plus advances to the investee is reduced to zero, unless the First Group guarantee the debts of investee company or has a commitment or intention to provide financial support to the investee company and then recognizes the investment loss proportionally according to the percentage of the investee’s ownership held by the Company continuously. However, if the First Group has control interests over the investee company, the investment losses in excess of the investee’s stockholders equity’s balance shall be fully recognized, unless other stockholders of the investee company have the obligation and ability to provide additional capital to take the losses. When the investee company begins to make a profit in the subsequent periods, the earnings are attributed to the First Group until the originally recognized excess losses are fully recovered.

D. For unrealized gain or loss from the downstream transactions between the Company and an investee accounted for under the equity method, if the Company has control interests over the investee, unrealized gain or loss shall be fully eliminated while if the Company does not have control interests over the investee, unrealized gain or loss shall be eliminated according to the percentage of the investee’s ownership held by the Company in the year end. For the unrealized gain or loss on transactions between investees accounted for under the equity method, if the Company has control interest over both the investees, unrealized gain or loss is eliminated according to the percentage of the ownership held by the Company in the investee generating the unrealized gain or loss, otherwise, it shall be eliminated according to the product of the percentage of each investee’s ownership held by the Company. Unrealized gain or loss is not recognized until it is realized.

E. The cumulative translation adjustment resulted from translation of the financial statements of foreign equity investments accounted for under

18

the equity method is recognized proportionally in the stockholders’ equity account based on the percentage of the investees’ ownership held by the First Group.

12) Other financial assets and financial liabilities

A. Financial assets measured at cost

A) Long-term investments in equity securities, which are not listed on the TSE or OTC, are accounted for using trade date accounting. Such financial instruments are initially recognized at fair value plus the acquisition or issuance cost and are subsequently carried at cost at the balance sheet date.

B) For financial assets measured at cost, an impairment loss shall be recognized if there is objective evidence of impairment. The impairment loss shall not be reversed.

B. Bond investments with no active market

A) Bond investments with no active market are accounted for using settlement date accounting. Such financial instruments are initially recognized at fair value plus acquisition or issuance cost. Gains or losses are recognized in the income statement when the investments are derecognized.

B) Bond investments with no active market shall be subsequently measured at amortized cost using the interest method.

C) An impairment loss is recognized when there is objective evidence of impairment. In the subsequent period, if the amount of the impairment loss decreases due to an event occurring after the impairment was originally recognized, the previously recognized impairment loss is reversed through profit and loss to the extent that the carrying amounts shall not exceed the amortized cost that would have been determined had no impairment loss been recognized in prior years.

C. Derivative financial assets and financial liabilities held for hedging

Derivative financial assets and financial liabilities held for hedging are those derivative financial assets and financial liabilities that are designated as effective hedging instruments under the hedge accounting and are measured at fair value.

19

13) Hedge accounting

A. Fair value hedge

When all the criteria of fair value hedge accounting are met, it recognizes the offsetting effects on gains or losses of changes in the fair values of the hedging instrument and the hedged item. The accounting treatment for hedging instruments is that the gain or loss from remeasuring the hedging instrument at fair value or the foreign currency component of its carrying amount shall be recognized immediately in the statement of income. The accounting treatment for hedged items is that the gain or loss attributable to the hedged risk shall adjust the carrying amount of the hedged item and be recognized immediately in the statement of income.

B. Cash flow hedge

A) When all the criteria of cash flow hedge accounting are met, the effective hedge portion of the gain or loss on the hedging instrument shall be recognized directly in the stockholders’ equity, and the ineffective hedge portion of the gain or loss on the hedging instrument shall be recognized in the statement of income.

B) The accounting treatment for a forecast transaction is as follows:

a. If a hedge of a forecast transaction subsequently results in the recognition of a financial asset or a financial liability, the related gains or losses that were originally recognized directly in the stockholders’ equity shall be reclassified into the statement of income in the same period or periods during which the asset acquired or liability assumed affects profit or loss. However, if it is expected that all or a portion of a loss recognized directly in stockholders’ equity will not be recovered in one or more future periods, the amount that is not expected to be recovered shall be reclassified into the statement of income immediately.

b. If a hedge of a forecast transaction subsequently results in the recognition of a non-financial asset or a non-financial liability, or if a forecast transaction for a non-financial asset or non-financial liability becomes a firm commitment for which fair value hedge accounting is applied, then the associated gains and losses that were recognized originally and directly in stockholders’ equity shall be reclassified into the statement of income in the same period or in the periods during which the asset acquired or liability assumed affects profit or loss or shall be adjusted to the initial cost or other carrying amount of the asset or liability, and this accounting treatment shall be adopted consistently.

20

14) Allowance for doubtful accounts and credit losses

A. The Bank shall classify on and off balance sheet credit assets and determines the allowance for credit losses by evaluating the recoverability of the outstanding balances of various loans at the balance sheet date according to “Guidance for Credit Assets Risk Assessment” and “Standard for Risk Classification of Credit Assets”. As to non-credit assets, the Bank evaluates the possible risks by the characteristics of assets in accordance with “Guidance for Non-Credit Assets Risk Assessment” and generally accepted accounting principles.

According to the amended “Regulations Governing the Procedures for Banking Institutions to Evaluate Assets and Deal with Non-performing / Non-accrual Loans” of the MOF, loans are classified into five categories: (1) normal (2) special attention (3) substandard (4) doubtful and (5) unrecoverable. Except that the normal loans are classified under categories 1, the abnormal loans shall be evaluated based on the status of the loan collateral and the length of time overdue. The allowance for credit losses for abnormal loans is provided at 2%, 10%, 50%, and 100% on loans classified under categories 2, 3, 4, and 5, respectively. Furthermore, the additional reserve is provided for specific loans as needed if the aforementioned allowance is insufficient according to the recoverability.

Upon the approval of the Board of Directors and the notice to the supervisors of FCB, the overdue loans are written off in accordance with the guideline of the “Regulations Governing the Procedures for Banking Institutions to Evaluate Assets and Deal with Non-performing / Non-accrual Loans”.

B. Allowance for doubtful accounts of FTSI and its subsidiaries are provided by assessing the collectibility of the notes and accounts receivable at the period-end. Securities dealing department’s allowance for bad debts evaluation is provided based on the Explanatory Letter Tai-Tsai-Jen (2) No. 82416 dated September 29, 1999 of the Securities and Futures Commission.

(1) Margin trading:

(a) When the Margin Ratio of a margin loan receivable is lower than the regulated minimum ratio and the balance of the margin loan receivable has not been partially collected to the extent that the margin ratio reaches the minimum ratio by the scheduled time, the related receivable should be transferred to and recorded as “overdue receivables”. The allowance for doubtful debts should be at least 50% and action should be taken to collect the receivable within 6 months. Additional allowance for bad debts within 6 months may need to be provided based on facts and circumstances if the receivable can not be collected.

21

(b) If the marketable securities in customers’ margin trading account are not disposable, the balance of the related margin loan receivable should be transferred to and recorded as “other receivables” immediately and 100% allowance for doubtful debts should be provided. Action should be taken to collect the receivable and review the appropriateness of its classification. Receivable not collected after further action is taken should be transferred to and recorded as “overdue receivables”.

(c) For these margin loan receivable that agreement has been reached with customers and the customers has fulfilled the obligation according to the agreement, no allowance for doubtful debts need to be provided. However, if there is any default on the subsequent payments, additional allowance for doubtful debts should be provided according to the above A or B.

(2) Normal trading part:

The receivables generated from customers breaching contracts should be transferred to and recorded as “other receivables” and 100% allowance for doubtful debts should be provided. Actions should be taken to collect the receivable and review the appropriateness of its classifications. Receivables not collected after further actions are taken should be transferred to “overdue receivables”

In accordance with the Value-added and Non-value-added Business Tax Law (the “Business Tax Law”), the business tax rate was adjusted from 5% to 2%, effective from July 1, 1999. The 3% tax reduction shall be set aside as additional allowance for doubtful accounts or be used to write off overdue accounts within four years, starting from July 1, 1999. If a company does not follow the above regulations, the tax authorities will impose 3% business taxes on the sales violating the “Business Tax Law”.

According to the Explanatory Letter Tai-Tsai-Jen Ruling (2) No.0920002964 of the MOF dated July 17, 2003, effective from July 1, 2003, the aforementioned regulation is no longer applicable to securities firms. However, if there is an outstanding balance of the aforesaid allowance for doubtful accounts on June 30, 2003, securities firms should comply with the Explanatory Letter Tai-Tsai-Jen (2) No.82416 dated September 29, 1999 to retain such a balance to write off overdue accounts in the future.

15) Properties, plants and equipments / non-operating assets

A. Properties, plants and equipments / non-operating assets are stated at cost except for appraisal increment as permitted under the relevant regulations. At the balance sheet date, the non-operating assets are evaluated at the

22

lower of carrying amount or recoverable amount. Depreciation is provided on a straight-line basis over the estimated service lives of the assets plus an additional year as salvage value, except for leasehold improvements, which are depreciated over the shorter of the leasing periods of the lease agreement or 5 years. The service lives of major properties and equipment range from 3 to 60 years.

B. Major renewals and improvements, which are incurred to increase the future economic benefits of the assets, are capitalized and depreciated. Routine maintenance and repairs are charged to expenses as incurred.

C. When properties, plants and equipment, and non-operating assets are sold or abandoned, the cost and accumulated depreciation are removed from the respective accounts and the related gain or loss on the disposal of property, plants and equipment is recorded as ”other non-interest income or loss ”.

16) Other Assets

Other assets are mainly comprised of non-operating assets, foreclosed assets, refundable deposits, operating guarantee deposits and settlement clearing funds, restricted assets, prepayments, temporary payment and suspense accounts, other assets to be adjusted, and so on.

Foreclosed assets are recorded at acquisition costs and are revalued at the lower of carrying amounts or recoverable amounts as of the balance sheet date. If the foreclosed assets are impaired, an impairment loss is recognized in the current period. In the subsequent period, if the recoverable amount increases, the previously recognized impairment loss is reversed to the extent that the carrying amounts, after the reversal, shall not exceed the carrying amounts that would have been determined had no impairment loss been recognized for the assets in the prior years.

17) Intangible assets

Intangible assets, mainly comprising of computer software costs, are initially recorded at cost and are amortized over 3 to 5 years under the straight-line method.

18) Reserve for guarantees

Reserves for guarantees of FCB are determined based on the estimated losses arising from default possibility of the ending balances of guarantees receivable, bills accepted receivable, and letters of credit receivable, net of the margin deposits received from customers.

23

19) Reserve for default

As required by Article 12 of the “Rules Governing Securities Firms”, a securities firm should allocate 0.0028% of the amounts of monthly securities consignment trading as the reserves for losses from default, and such reserves are recorded as other liabilities. The reserves should only be used for recovering the losses caused by default on such consignment trading or for other purposes as approved by the SFB. When the accumulated reserve balances reach $200,000, no further reserve provision is required.

20) Reserve for securities trading losses

As required by the “Rules Governing Securities Firms”, a securities firm should set aside 10% of the excess of monthly gains over losses from “trading securities – proprietary trading” and “ issuance of call (put) warrants” as the reserves for securities trading losses while engaging in proprietary trading business. Such reserves can only be used to offset losses over gains arising from the aforesaid securities trading. The reserves must be provided until the accumulated reserve balances reach $200,000.

Futures commission merchants should set aside 10% of monthly net realized gains from trading securities as the reserves for securities trading losses while engaging in proprietary trading business. The reserves must be provided until the accumulated reserve reaches the portion of the regulated minimum issued capital stock, working capital or operating capital. Such reserves can only be used to offset losses over gains arising from the aforesaid securities trading.

21) Retirement plan and pension cost

A. In compliance with the Statement of Financial Accounting Standards No.18, “Accounting for Pensions”, if the retirement plan is a defined benefit pension plan, the First Group recognizes the difference as the minimum pension liability when the accumulated benefit obligation exceeds the fair value of plan assets. For interim financial statements, minimum pension liability is adjusted for the difference between net periodic pension costs and appropriated funds. The net periodic pension costs, which include the service cost, interest cost, expected return on plan assets, amortization of unrecognized net transition asset or obligation, amortization of pension gains or losses, and amortization of prior period service cost, are recognized based on the actuarial report.

A) The Company has a defined benefit plans in accordance with the Labor Standards Law of the R.O.C. From September 2005, monthly contributions made to the pension fund that is deposited in the designated pension account at the Central Trust of China have been reduced from 10% to 6% of the total monthly salaries and wages.

24

B) NITC contributes to the pension fund based on 2% of monthly salaries in accordance with the approval of Bei Shih Lao (2) NO. 09432136500 of the Department Of Labor, Taipei City Government (8% prior to May 2001 and 6% from May 2001 to April 2005). Such pension funds are administered by the Supervisory Committee of the Labor Retirement Fund of NITC and are deposited in the designated pension account at the Central Trust of China under the name of the Supervisory Committee.

B. If the retirement plan is a defined contribution pension plan, the contributions are based on an accrual basis and are recognized as pension costs in the current period. Effective from July 1, 2005, the contributions made pursuant to the Labor Pension Act are under the defined contribution pension plan. Such contributions are made monthly based on not less than 6% of the employee's salaries and are deposited in the labors’ individual pension fund accounts at the Bureau of Labor Insurance.

22) Foreign currency transactions and translations of foreign currency financial statements

The First Group’s foreign currency transactions are recorded in New Taiwan dollars at the spot rates of the transaction dates. Differences between actual payments or receipts and recorded transaction amounts are recognized as foreign exchange gains or losses in the current period. The revaluation of the foreign currency assets and liabilities at the balance sheet date is as follow:

A. Except that a cash flow hedge or a hedge of a net investment in a foreign operation is accounted for under the hedge accounting, monetary assets and liabilities denominated in foreign currencies are revalued using the spot foreign exchange rates at the balance sheet date, and the resulting foreign exchange gain or loss on the revaluation should be included in current income.

B. Non-monetary assets and non-monetary liabilities denominated in foreign currencies that are financial assets or financial liabilities at fair value through profit or loss are revalued using the spot foreign exchange rates at the balance sheet date, and the related foreign exchange gains or losses are recorded as gains or losses in the current period. Those that are available-for-sale financial assets are revalued using the spot foreign exchange rates at the balance sheet date, and the related foreign exchange gains or losses are recorded in the stockholders’ equity. Those that are financial assets or financial liabilities carried at cost are stated using the historical foreign exchange rates of the transaction dates.

C. For equity investments accounted for under the equity method whose functional currency is foreign currency, the translation differences arising from the foreign currency financial statements translated into domestic currency financial statements are recognized proportionally as the

25

cumulative translation adjustment in the stockholders’ equity based on the percentage of the investees’ ownership held by the First Group.

D. When the financial statements of a foreign operation are translated into domestic currency financial statements, all asset and liability accounts are translated using the spot foreign exchange rate at the balance sheet date, and the shareholders’ equity accounts are translated at the historical foreign exchange rate except that the beginning retained earnings are stated at the translated carrying amount of the ending retained earnings in the prior year and except that the profit and loss accounts are translated at the average foreign exchange rate in the reporting period. The final translation differences are recorded as the cumulative translation adjustment in the stockholders’ equity.

23) Revenue and expense recognition

A. Revenues are recognized in accordance with the provisions of Statement of Financial Accounting Standards No. 32 “Accounting for Revenue Recognition” and the following statements.

B. Interest income on loans of FCB is recognized on an accrual basis. However, interest income arising from loans which meet any of the following criteria is recognized on cash basis when the proceeds are received:

A) Reclassified as non- accrual loans.

B) Interest from restructured loans that are agreed to extend their maturities are not recognized as interest income but recorded on the memo accounts.

Handling fee is recognized when cash is received, or the earning process is substantially completed.

C. Under respective securities investment trust contracts, NITC earns annual management fees ranging from 0.20% to 2.00% of the average daily net asset value of each of the managed mutual funds. It also earns sale service fees according to various percentages of the transaction value of the beneficiary certificates issued and reissued by the managed mutual funds.

D. Revenue and expense recognition principles of FTSI, FTSL, FWSL, and FFI are as follows:

A) Brokerage commissions, gains (losses) on sale of securities, and related handling fee expenses are recognized on the transaction date.

B) Interest income and interest expenses resulting from margin loan business, stock loan business, and bills and bonds under repurchase or resale agreements are recognized on an accrual basis during the transaction periods.

26

C) Underwriting commission income or expenses: subscription handling fees are recognized when the amounts are received; underwriting commission income and related commission expenses are recognized at the completion of such underwriting contracts.

D) Service fee income from providing registration and transfer agency service for securities are recognized monthly according to the contracts.

E) Futures commission income: futures commission income resulted from engaging in futures introducing broker business and received from the futures commission merchants is recognized on the accrual basis during the transaction periods.

F) Futures contract income: futures margin deposits are recorded at cost originally. The gains or losses of futures contracts resulting from the daily market-to-market adjustment and the opposite transactions to close out or the settlement at maturity are recognized as gains or losses in the current period. Handling fees are recognized as expenses on futures transaction dates.

E. Service revenue of FTCMI is recognized when the earnings process is substantially completed and when the income is realized or realizable. Related expenses are recognized as current expenses when incurred.

24) Income taxes

A. According to the Statement of Financial Accounting Standards No. 22 “Accounting for Income Taxes” of the R.O.C., the Company is required to apply the inter-period and intra-period income tax allocations. Under the inter-period income tax allocation, the income tax effects of deductible temporary differences, loss carry forwards, and income tax credits are recognized as deferred income tax assets, and the income tax effects of taxable temporary differences are recorded as deferred income tax liabilities. Valuation allowance is provided against deferred income tax assets if it is more likely than not that the deferred income tax assets will not be realized. Deferred income tax assets or liabilities are classified as current items or non-current items according to the related asset and liability classifications or the expected realization period of temporary differences. The adjustment for over-provision or under-provision of previous years’ income taxes is included in the current year’s income taxes. Under the intra-period income tax allocation, the income tax expenses (benefits) should be allocated to continuing operations, discontinued operations, extraordinary gains or losses, cumulative effect of a change in accounting principle, and prior period adjustments of retained earnings.

27

B. In accordance with the Statements of Financial Accounting Standards No. 12, “Accounting for Income Tax Credits”, income tax credits resulting from purchases of equipment, research and development expenditures, employee trainings, and investments in equity stocks are recognized as incurred.

C. Pursuant to the Explanatory Letter Tai-Tsai-Shui No.0910458039 of the MOF dated February 12, 2003 to promulgate the “Criteria for Profit-seeking Enterprises in Filing Consolidated Profit-seeking Enterprise Income Tax Returns According to Article 49 of the Financial Holding Company Act and Article 40 of the Business Mergers and Acquisitions Law”, if a financial holding company holds at least 90% of the issued capital stock of its domestic subsidiaries for twelve months in a fiscal taxable year, starting from such a fiscal taxable year, the financial holding company may elect to have itself as the taxpayer to file the consolidated profit-seeking enterprise income tax returns and to file the profit-seeking enterprise income tax returns of the 10% surtax on undistributed earnings, whereas other tax affairs should be handled separately by the financial holding company and its domestic subsidiaries. The 10% surtax on undistributed current earnings calculated pursuant to the Income Tax Law of the R.O.C is recorded as income tax expenses in the resolution year when the earnings distribution is approved by the Shareholders’ Meeting.

D. Effective on January 1, 2006, in accordance with the Alternative Minimum Tax Act, the Company should calculate the alternative minimum tax in addition to the regular income tax. If the regular income tax is lower than the alternative minimum tax, the differences should be accrued as an income tax adjustment.

E. The accounting treatment for the Company and its subsidiaries to adopt the consolidated income tax return system to file the consolidated income tax returns is in compliance with the Explanatory Note (92) No. 240 of the Accounting Research and Development Foundation of the R.O.C. dated October 3, 2003. The Company and its subsidiaries should separately apply the Statement of Financial Accounting Standards No. 22, “Accounting for Income Taxes” to cope with the income taxes according to their respective income tax returns. However, settlements received or paid within the affiliated group arising from filing consolidated income tax returns have to adjust the deferred income tax assets / liabilities or income taxes payable / refundable in the current period based on a reasonable, consistent, and systematic method. Besides, while estimating the provision for income taxes in the financial statements, the Company should record such settlements receivable from subsidiaries or settlements payable to subsidiaries as “other receivable from / other payable to subsidiaries for consolidated income tax return system”.

28

25) Financial asset securitization transaction

According to the “Financial Asset Securitization Act” and the “Trust Law”, FCB entrusted the rights of personal residential mortgage loans and related rights and obligations to Deutsche Bank AG, Taipei Branch (the Trustee) under special purpose trust. The Trustee raised funds for FCB by issuing beneficiary securities. Because FCB lost control of transferred assets under the framework of securitization transaction, FCB derecognized the assets from loans and recognized servicing assets, recourse liabilities, and the gain on securitization. The portion of subordinated beneficiary securities held by FCB for credit enhancement was recorded as held-to-maturity financial assets.

There is no market price for the retained interests of the subordinated beneficiary securities, so FCB estimates the fair value based on the expected prepayment rate, expected weighted average useful lives, expected credit loss rate, and discount rate of residual cash flows.

Interest income is recognized with respect to the subordinated beneficiary securities when the Trustee pays the interest.

Servicing assets are recorded as other assets and are amortized under straight-line method over the period of service lives.

26) Impairment of assets

An impairment loss shall be recognized when circumstances that have changed or events that have occurred indicate that an asset’s recoverable amount is less than its carrying amount. The recoverable amount of an asset is the higher of its fair value less costs to sell and its value in use. The fair value less costs to sell is the amount obtainable from the sale of an asset in an arm’s length transaction between knowledgeable, willing parties, less the costs of disposal. The value in use is the present value of the future cash flows expected to be derived from an asset.

If there is an indication that an impairment loss recognized in the prior periods for an asset other than goodwill may no longer exist or may have decreased, the impairment loss recognized could be reversed, and such a reversal shall not exceed the impairment loss recognized in the prior periods. Besides, the impairment loss recognized for goodwill in a previous period shall not be reversed in the subsequent periods.

27) Use of estimates

In preparing the consolidated financial statements in conformity with generally accepted accounting principles in the R.O.C., the management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities as of the date of the consolidated financial statements, and the reported amounts of

29

revenues, costs of revenues, and expenses during the reporting period. Therefore, actual results could differ from those estimates.

28) Contingency loss

If the development of events is probably confirmed that assets have been impaired or liabilities have been incurred as of the balance sheet date and the loss amount could be reasonably estimated, the amount shall be recognized as loss for the current year. If the development of events is probably confirmed that assets have been impaired or liabilities have been incurred as of the balance sheet date but the loss amount could not be reasonably estimated, it shall be disclosed in the consolidated financial statements.

3. Changes in accounting principles

1) Financial instruments

A. As of January 1, 2006, the Company and its subsidiaries adopted the Statements of Financial Accounting Standards No.34 and No.36 to account for the financial instruments.

B. The change in the accounting principle for such financial instruments credited other adjustments to stockholders’ equity for $4,852,579, and the effects on the consolidated net income for the three months then ended March 31, 2006 were as follows:

Amount

Earnings per share (NTD)

Income before income tax ( $ 31,712 ) ( $ 0.005 )Cumulative effect of a change in

accounting principle (Net of income tax expense of $367) 647,608 0.108

Net income $ 615,896 $ 0.103

4. Summary of significant accounts

1) Cash and cash equivalents

March 31, 2007 2006 Cash on hand $ 9,901,756 $ 9,118,677 Checks for clearance 24,027,722 9,819,220 Short-term bills 414,097 475,529 Due from other banks 4,130,955 4,677,849 Total $ 38,474,530 $ 24,091,275

30

2) Due from Central Bank and call loans to other banks

March 31, 2007 2007 Reserve for deposits - account A $ 12,998,187 $ 4,387,702 Reserve for deposits - account B 31,448,439 29,267,713 Central Bank deposits 2,100,000 - Inter-bank clearing fund 1,820,771 1,819,143 Reserve for deposits - foreign currency 122,014 72,683 Deposits of overseas branches with

foreign Central Banks 819,303 606,356 Deposits of national treasury account 869,274 859,116 Call loans and overdrafts to other banks 97,645,274 97,763,276 Total $ 147,823,262 $ 134,775,989

The FCB’s reserve for deposits is required by the Banking Law to maintain the reserve requirements based on the monthly average balance of each kind of deposits and the reserve ratio set by the Central Bank of China and to deposit in the reserve deposit account at the Central Bank of China. According to the regulations, such reserve requirements for reserve for deposits - account B can not be withdrawn except for monthly adjustments of the reserve for deposits.

3) Financial assets at fair value through profit or loss-net

March 31, 2007 2006 Financial assets for trading purpose Stocks $ 3,576,263 $ 1,989,232 Bonds (government bonds, financial

bonds, and corporate bonds) 11,720,719 1,767,341 Beneficiary certificates 275,013 940,000 Other marketable securities 1,175,609 468,584

Derivative financial instruments 3,118,978 1,901,925Valuation adjustment for financial

assets for trading purpose - non-derivative instruments 582,428 65,031

Subtotal 20,449,010 7,132,113Financial assets designated as at fair

value through profit or loss 28,079,790 36,514,731Valuation adjustment for designated

financial assets as at fair value through profit or loss 907,406 1,053,446

Subtotal 28,987,196 37,568,177Total $ 49,436,206 $ 44,700,290

31

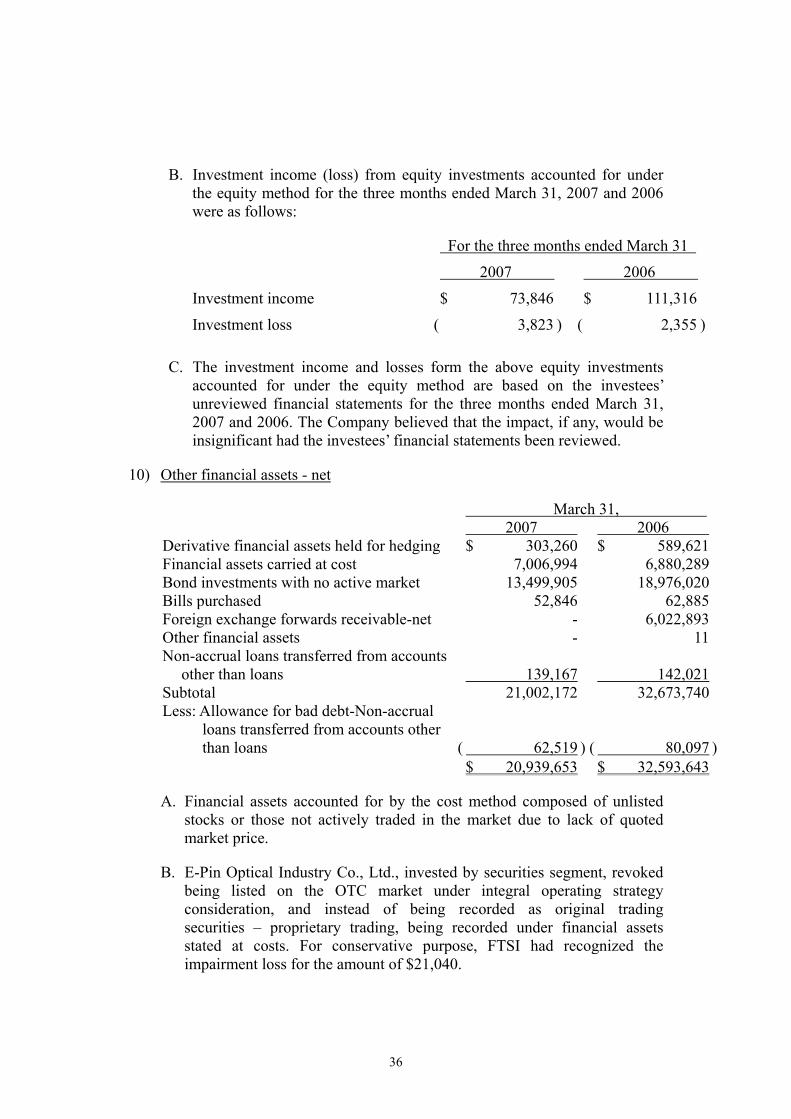

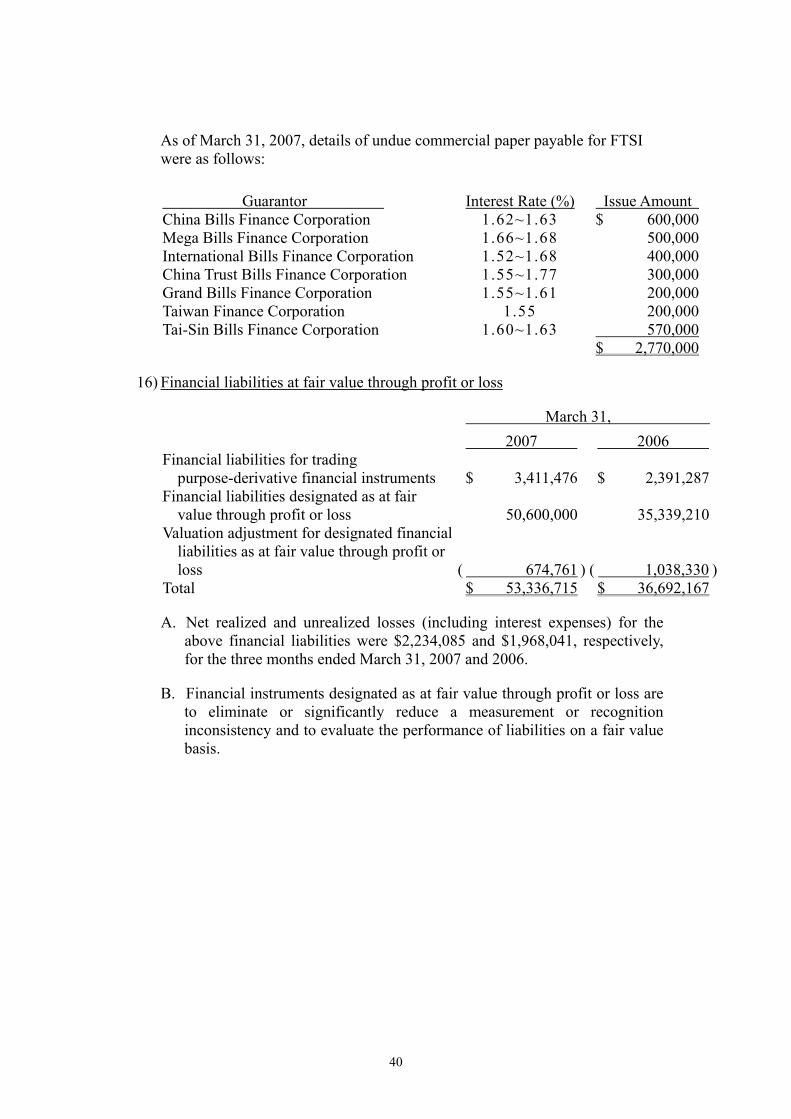

A. For the three months ended March 31, 2007 and 2006, the net gains on financial assets for trading purpose and the net realized and unrealized gains (including interest income) on designated financial assets as at fair value through profit or loss amounted to $3,004,167 and $2,448,118, respectively.

B. Financial instruments designated at fair value through profit or loss are to eliminate or significantly reduce a measurement or recognition inconsistency and to evaluate the performance of assets on a fair value basis.

C. As of March 31, 2007 and 2006, the above financial assets for trading purposes undertaken for repurchase agreements were $2,996,770 and $950,596, respectively.

D. Please refer to Note 6 for details of the above financial assets at fair value through profit or loss pledged as collateral as of March 31, 2007 and 2006.

E. Types of derivative financial instruments held for trading purpose and related contract information were as follows:

March 31, 2007 March 31, 2006

Financial Instruments Contract amount

(Notional principal) Credit Risk Contract amount

(Notional principal) Credit Risk Trading Purpose:

Foreign exchange contracts

(FX swaps and forwards) $ 84,619,833 $ 568,486 $ 75,268,088 $ 57,972 FX margin trading 4,949,969 247,255 3,580,241 265,947 Non-delivery FX forwards 10,675,384 95,710 630,781 7,929 FX Options written 10,061,186 - 283,087 - Interest rate options written 16,330,750 - 200,000 - Bond options written 3,344,809 - 746,,626 - Interest rate options held 12,550,977 97,278 1,267,055 9,326 Interest rate swaptions held 2,000,000 12,306 1,200,000 200 Bond options held 165,375 79 5,846,316 4,163 Cross currency swap contracts 18,048,963 260,253 9,126,327 162,353 Interest rate swap contracts 263,496,770 1,766,032 140,526,399 1,021,222 Futures margin deposits (Note) - 60,073 - 329,618

Options purchased - futures 4,212 4,354 2,827 1,898 Bond options 300,000 71 2,400,000 2,087 Asset swap options 49,635 7,081 714,120 39,210

32

Note: The credit exposure amounts stated on March 31, 2007 are the excess margin deposits of future trading of the bank business segment. The balance stated on March 31, 2006 is the margin deposits that securities segment engaged in TAIFEX Taiwan stock index futures trading and this margin deposits include the excess margin deposits of the amount of $228,839.

4) Investments in bills and bonds under resale agreements

March 31, 2007 2006 Central government construction bonds $ 3,065,612 $ 1,305,000Financial bonds 440,000 440,000 $ 3,505,612 $ 1,745,000

As of March 31, 2007 and 2006, the Company and its subsidiaries are obliged to subsequently sell the above bonds at purchase price plus a mark-up based on the resale agreements, and such resale amount are $3,518,159 and $1,751,292, respectively. As of March 31, 2007 and 2006, bonds dealing department is obliged to investment in bills and bonds to fulfill resale agreements with the price $1,015,612 and 305,000, respectively.

5) Receivables - net

March 31, 2007 2006 Interest receivable $ 6,101,346 $ 5,288,892Acceptances receivable 7,642,220 5,716,607Margin loans receivable 8,152,414 6,166,175Accounts and notes receivable 2,188,924 1,484,198Accrued income 384,577 144,250Credit card account receivable 3,725,117 4,619,397Income tax refundable 2,740,167 2,004,715Other receivables 1,091,351 680,983 32,026,116 26,105,217Less: allowance for doubtful accounts ( 233,176 ) ( 291,462 )Net amount $ 31,792,940 $ 25,813,755

As of March 31, 2007 and 2006, FCB’s reserves for guarantees, including acceptances receivable and guarantees receivable, were both $450,518, and such reserves were recorded under ” reserves for operation and liabilities.”

33

6) Bills discounted and loans – net

March 31, 2007 2006 Bills discounted $ 5,132,332 $ 5,039,570Overdrafts 856,795 1,343,390Short-term loans 307,998,163 244,476,540Medium-term loans 280,929,320 273,414,825Long-term loans 376,841,712 339,495,331Import-export negotiations 3,556,592 2,762,059Non-accrual loans 16,772,671 15,460,810Sub-total 992,087,585 881,992,525Less: allowance for credit losses ( 8,174,424 ) ( 7,945,959 )Net amount $ 983,913,161 $ 874,046,566

A. Gain from hedge evaluation was $181,432, which was included in the balances of loans as of March 31, 2007. The fair values of fixed-rate loans held by overseas branches may fluctuate with changes in interest rates. FCB assessed that the risk might be significant, so hedged such risk by engaging in interest rate swap contracts.

B. As of March 31, 2007 and 2006, non-accrual loans and other credit extensions where interest accruals had been ceased were $16,643,629 and $15,467,312, respectively. For the three months ended March 31, 2007 and 2006, interests that were not accrued were $133,529 and $157,189, respectively.

C. Proper prosecutions of claims against debtors have been made before any credit extensions and loans were written off for the three months ended March 31, 2007 and 2006.

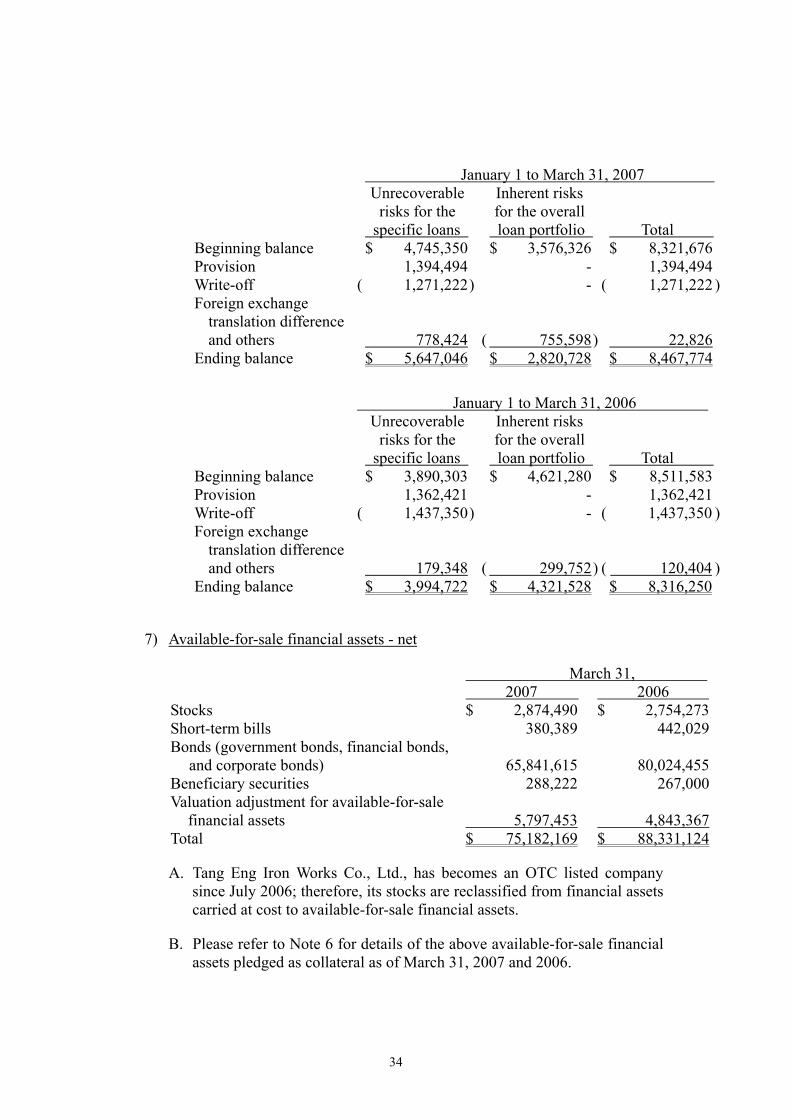

D. The bank business segment had revalued the allowance for doubtful receivables, loans, bills discounted, and non-accrual loans by considering unrecoverable risks for the specific loans and inherent risks for the overall loan portfolio. Movements in allowance for credit losses of doubtful receivables, loans, bills discounted, and non-accrual loans for the three months ended March 31, 2007 and 2006 were as follows:

34

January 1 to March 31, 2007 Unrecoverable

risks for the specific loans

Inherent risks for the overall

loan portfolio Total Beginning balance $ 4,745,350 $ 3,576,326 $ 8,321,676Provision 1,394,494 - 1,394,494Write-off ( 1,271,222 ) - ( 1,271,222 )Foreign exchange

translation difference and others 778,424 ( 755,598 ) 22,826

Ending balance $ 5,647,046 $ 2,820,728 $ 8,467,774

January 1 to March 31, 2006 Unrecoverable