1 Activity-Based Costing in Danish Small and Medium- Sized Enterprises

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Activity-Based Costing in

Danish Small and Medium-

Sized Enterprises

2

Bachelor Thesis

Jeppe Green Krejberg ________________

Joachim Grøfte Ulfkjær ________________

Nikolay Ivanov Georgiev ________________

Supervisor: Ali Naef Mohammad

Aalborg University

Economics and Business Administration

6th Semester

26/05/2015

3

Thesis Abstract / Summary

This particular project was chosen to be on the topic of Management accounting. It was

learned through lectures that Time-Driven Activity Based Costing is not as widely used at it

should be despite the effectiveness. This inspired the group to look into what small to

medium sized enterprises can do to undertake this model. In order to reach a high level of

discussion, it was decided that a literature review would be done on the subject. On top of

that, it was also decided to make a survey to have independent results that could then be

compared and contrasted to the existing literature.

Literature was collected systematically based on keywords. These keywords were limited

down to find articles based on the adoption of Activity Based Costing. After looking through

the articles, the literature review presented the different contingency factors for the adoption

of Activity Based Costing. These contingencies inspired the questions for the survey which

was performed afterwards. The questions were presented to the subjects as relating to the

allocation of overhead costs. The survey was first focused on the adjusted criteria of Danish

small to medium sized enterprises (20-200 employees). These companies were found on an

online database and in the end the survey was sent out to over 1000 companies all over

Denmark.

The survey resulted in over 100 respondents, where nearly 14% responded that they used

Activity Based Costing or Time-Driven Activity Based Costing. A statistical analysis of the

survey results was then performed. Different tests were made to illustrate the reliability of the

results and to find different correlations associated with the use of Activity Based Costing.

Different connections were made between the questions relating to different contingencies

from the literature review and Activity Based Costing in the independent survey. Other

observations were also made that were not observed in the literature review or in the

statistical analysis. All these different findings were compared, contrasted, and discussed.

From that, a conclusion was able to be formed which presented, which factors were thought

to be the most influential in terms of adopting Activity-Based Costing in small to medium

sized enterprises in Denmark.

4

This research found a significant and strong correlation between the use of ABC and TDABC

and two factors: Complete cost overview within the company and leaders using

acknowledged principles. This shows that ABC and TDABC adoption is significantly

influenced by the companies currently having great cost overview and/or leaders using these

models are considered to be applying theory to practise, so this further contributes to the

discussion of the question of why the model is not applied to more cases. Additionally,

through the descriptive statistics available from the survey, Danish SME’s relevancy to ABC

is discussed, in regards to product variance, IT and others.

5

Table of Contents

1. Introduction ..................................................................................................................................... 7

1.1 Activity-Based Costing in Small and Medium-Sized Enterprises ................................................ 7

1.1.1 Diffusion of Activity-Based Costing ................................................................................... 10

1.2 Problem Formulation .................................................................................................................. 12

1.2.1 Research question ................................................................................................................ 13

1.3 Limitation .................................................................................................................................... 13

2. Methodology ................................................................................................................................. 15

2.1 Paradigms .................................................................................................................................... 15

2.2.1 Structuralism and ontology .................................................................................................. 17

2.2.2 Epistemology of structuralism ............................................................................................. 18

2.3 Method and puzzle solving techniques ....................................................................................... 18

2.3.1 Literature review .................................................................................................................. 18

2.3.2 Survey and techniques ......................................................................................................... 19

2.3.3 Non-response bias ................................................................................................................ 21

3. Theoretical background of Activity-Based Costing ...................................................................... 22

3.1 Time-Driven Activity-Based Costing ......................................................................................... 24

3.2 Development of ABC ................................................................................................................. 25

4. Literature review: Is ABC relevant for SMEs? ............................................................................. 26

4.1 TDABC’s application ................................................................................................................. 26

4.2 Activity-Based Costing’s application in SMEs .......................................................................... 27

4.3 Contingency based theory and ABC ........................................................................................... 29

4.3.1 Organizational size ............................................................................................................... 31

4.3.2 Organizational structure ....................................................................................................... 32

4.3.3 Organizational strategy ........................................................................................................ 33

4.3.4 Organizational culture .......................................................................................................... 34

4.3.5 External uncertainty ............................................................................................................. 34

4.3.6 Technology .......................................................................................................................... 35

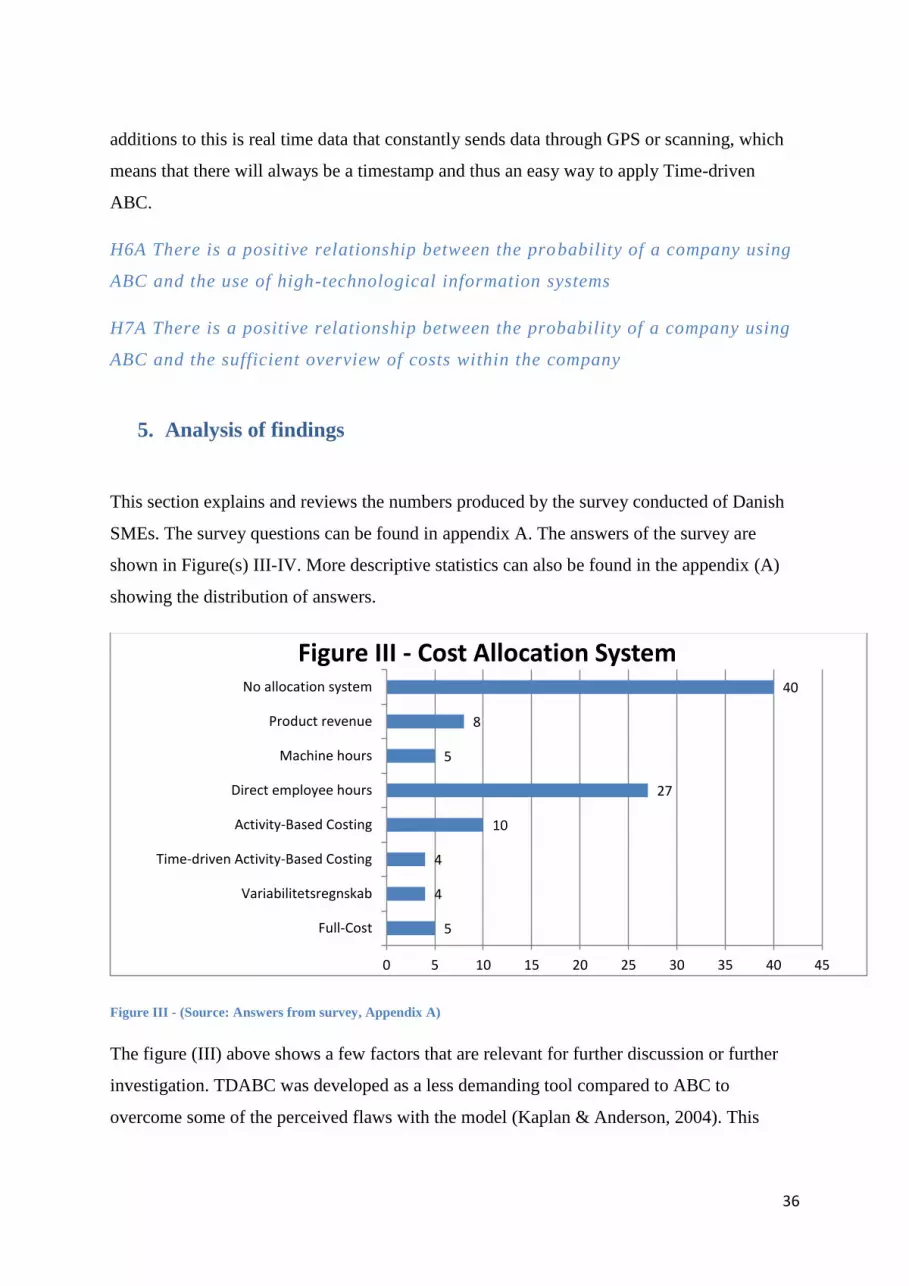

5. Analysis of findings ...................................................................................................................... 36

5.1 Hypothesis testing ....................................................................................................................... 39

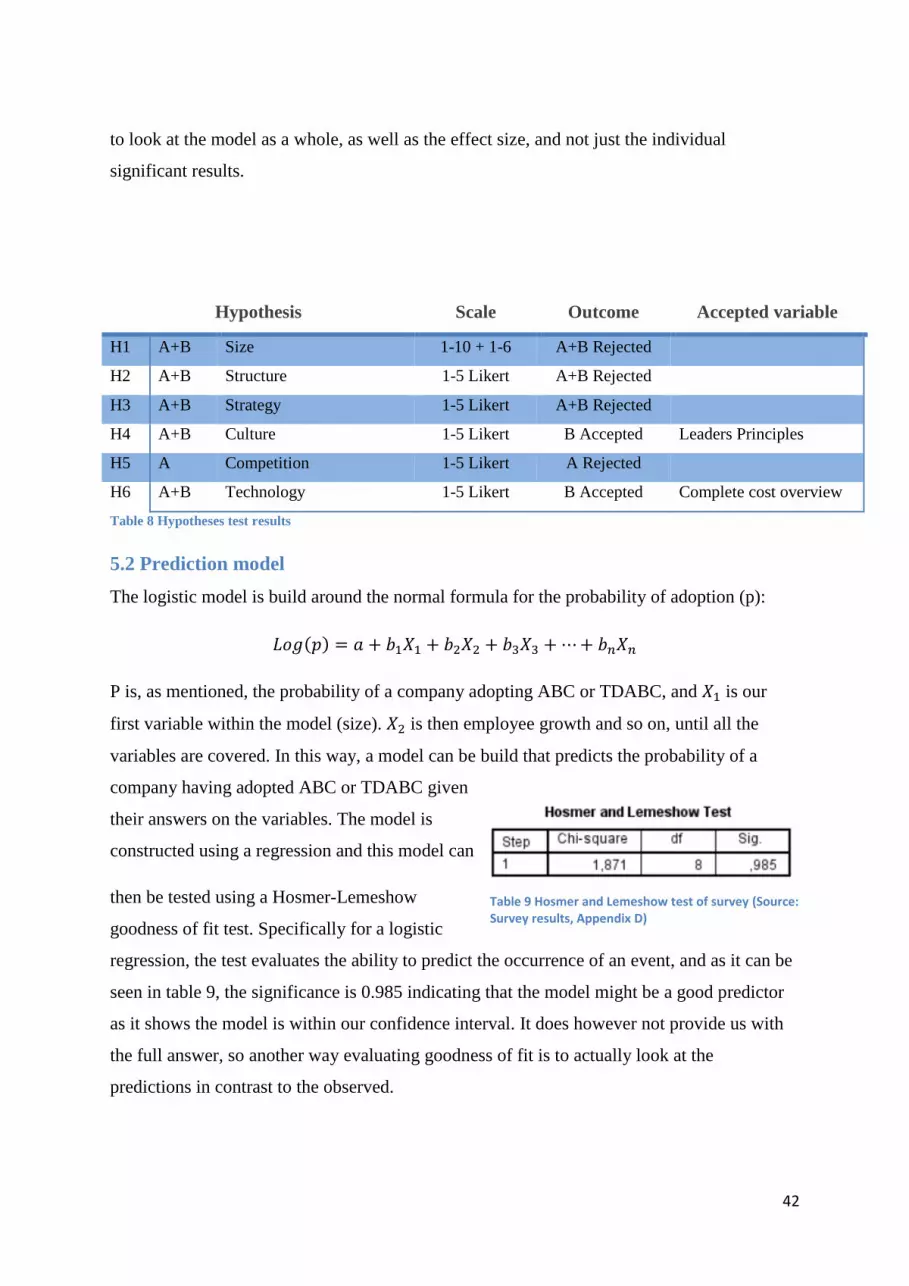

5.2 Prediction model ......................................................................................................................... 42

6. Discussion ......................................................................................................................................... 43

6.1 Model Flaws vs. Diffusion .......................................................................................................... 44

6

6.2 Most Significant Findings ........................................................................................................... 45

6.3 Contingency factors .................................................................................................................... 47

6.4 Other Relevant Findings ............................................................................................................. 49

6.4.1 Product Variation ................................................................................................................. 50

6.4.2 Product Variation / Cost Overview Correlation ................................................................... 50

6.4.3 IT systems /Cost Overview Correlation ............................................................................... 52

6.4.4 Non-Significant Predictors ................................................................................................... 53

7. Conclusion .................................................................................................................................... 53

8. Future research .............................................................................................................................. 54

8.1 Quantitative ................................................................................................................................. 55

8.2 Qualitative ................................................................................................................................... 56

Bibliography ......................................................................................................................................... 57

7

1. Introduction

With the current level of competitiveness in today’s world, where firms strive to maximize

profits and market share (Karl E. Chase, 2012), managers need methods of improving their

success. One significant part of the firm is the accounting and management of the firm’s

costs. Cost systems are different ways of accounting which a firm can adopt. These systems

differ from company to company, depending on a number of different factors. With proper

implementation of the systems and keeping them up-to-date, previous inconsistencies can be

fixed and possibly lead to a higher marginal profit.

Cost systems have existed for centuries and have been innovated in different ways since then.

Anthony (1989) explains that back in the day, it was often assumed that a company would

only make one product. With little variety, management accounting texts 60 years ago often

didn’t recognize differentiating products. However, the topic has been on the rise in the US,

with the rest of the world catching up. During the mid-1980’s Miller & Vollmann (1985)

emphasized the cost structures of manufacturing firms and their cost allocations. It was

shown how, because of the new more modern environment with diversified support activities

and diversified product portfolios, costs were incorrectly allocated. One of the main factors

for this improper allocation was the use of output volume as a driver for overhead cost.

Now that today’s firms have been growing to the point where their products are becoming

increasingly complex and the range of activities continue to broaden, their overhead costs

also start to increase (Gunasekarn & Sarhadi, 1998).This called for a more advanced costing

methodology. Robert Kaplan and Robin Cooper (1988) popularized a system that would help

companies take all the overhead costs into account, as well as all the activities associated with

them. They named it Activity-Based Costing (ABC).

1.1 Activity-Based Costing in Small and Medium-Sized Enterprises

ABC was originally found to be very complex and expensive for companies; this implies that

not all companies in the world can so easily adopt the system. However, as ABC evolved into

a simpler and more sustainable model, it naturally became more applicable to a wider range

of enterprises. Research has showed that ABC isn’t only relevant for large corporations, but

8

can be beneficial for smaller companies (Hicks, 1999). However, based on the amount of

literature collected for this project, very little has been written on ABC with a focus on

smaller companies.

This paper will concentrate on Small and Medium Sized Enterprises (SMEs) and their

relation to the ABC system. SMEs are defined by the Danish parliament (2005) in two

categories: the Håndværksråd definition (translated: Crafts Council) and the European Union

(EU) criteria. The criteria can be categorized in terms of total revenue and also the number of

employees in the company.

EU Criteria

Criteria Micro Small Medium

Number of

employees

<10 <50 <250

Revenue < 2 million Euros

(around 15 million

DKK)

< 10 million Euros

(around 75 million

DKK)

< 50 million Euros

(around 375 million

DKK)

Table 1 EU - SME criteria (Source: Danish Parliament, 2005)

Håndværksrådet Criteria

Criteria Small Medium

Number of employees <10 <100

Table 2 Håndværksrådets SME criteria (Source: Danish Parliament, 2005)

As seen on the tables above, the criteria for the number of employees differ quite

significantly. Denmarks Statistics (2012) reported that in 2010, that 93% of all Danish

companies in the private sector fell under the category of micro companies, while companies

with over 250 employees accounted for only 0.2%. These numbers arise from the EU criteria

which puts the majority of Danish companies within the definition of micro. Seeing that the

data of Danish companies is skewed in the eyes of the EU, the Håndværksråd came up with

their own definitions that better suit the Danish standards of an SME.

Håndværksrådet is an organization that works with the business community to help SMEs

thrive and secure them the best working conditions, in an environment where larger

9

companies have a lot of influence. Today it is an umbrella organization that represents around

20,000 SMEs within different industries in Denmark (Håndværksrådet, 2015). When taking

into account the EU criteria, it does not adequately reflect the Danish SME standards, but

when taking the criteria of Håndværksrådet into account, it won’t fully coincide with the

papers being analysed in the literature review. Therefore a customized criterion has been

established in order to best suit both situations.

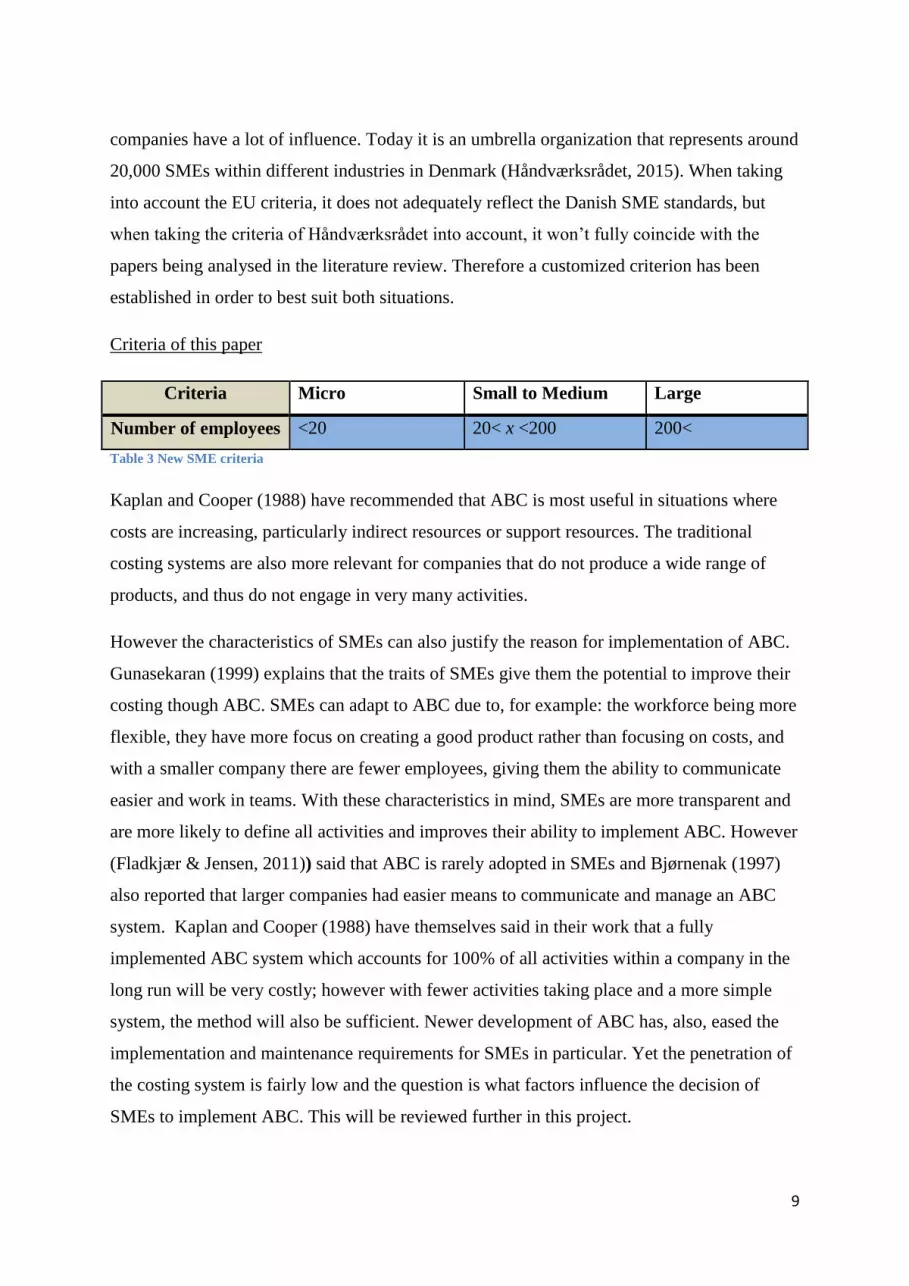

Criteria of this paper

Criteria Micro Small to Medium Large

Number of employees <20 20< x <200 200<

Table 3 New SME criteria

Kaplan and Cooper (1988) have recommended that ABC is most useful in situations where

costs are increasing, particularly indirect resources or support resources. The traditional

costing systems are also more relevant for companies that do not produce a wide range of

products, and thus do not engage in very many activities.

However the characteristics of SMEs can also justify the reason for implementation of ABC.

Gunasekaran (1999) explains that the traits of SMEs give them the potential to improve their

costing though ABC. SMEs can adapt to ABC due to, for example: the workforce being more

flexible, they have more focus on creating a good product rather than focusing on costs, and

with a smaller company there are fewer employees, giving them the ability to communicate

easier and work in teams. With these characteristics in mind, SMEs are more transparent and

are more likely to define all activities and improves their ability to implement ABC. However

(Fladkjær & Jensen, 2011)) said that ABC is rarely adopted in SMEs and Bjørnenak (1997)

also reported that larger companies had easier means to communicate and manage an ABC

system. Kaplan and Cooper (1988) have themselves said in their work that a fully

implemented ABC system which accounts for 100% of all activities within a company in the

long run will be very costly; however with fewer activities taking place and a more simple

system, the method will also be sufficient. Newer development of ABC has, also, eased the

implementation and maintenance requirements for SMEs in particular. Yet the penetration of

the costing system is fairly low and the question is what factors influence the decision of

SMEs to implement ABC. This will be reviewed further in this project.

10

1.1.1 Diffusion of Activity-Based Costing

From the birth of the costing system until recent times, as it will be shown further below,

ABC has had a very turbulent life. Its first idea of being only a costing system has been

rethought and different applications of it have emerged. During its existence, the model has

been through highs and lows, marked by different innovations in the usage of it (Gosselin,

2007). It has been praised and criticized heavily, yet it has been concluded that it is a more

accurate costing method than the traditional costing systems used (Cooper & Kaplan, 1988).

Additionally, its diffusion process (the spread of the costing system) has been very

ambiguous (Gosselin, 1997), which will be shown throughout the paper.

A definition Bjørnenak (1997) uses to define diffusion is given by Webster (1971): “The

social process by which an innovation spreads through a social system over time.” It can be

divided into two sub-categories, which will be examined below.

Relocation diffusion is a sub-category of diffusion, related to how ideas spread through areas,

without necessarily increasing number of adopters. Bjørnenak (1997) elaborates on this

concept through his study which showed a significant number of companies did not have any

knowledge of the ABC system and thus pointed out that there are still issues when it comes to

the supply-side of ABC. One thing that can’t be argued with, though, is that Activity-based

costing is one of the most popular innovations in management accounting in the past 30 years

(Gosselin, 2007). Following its introduction and development in various papers during the

late 80’s by Kaplan and Cooper, ABC started becoming popular among academics. This led

to the innovation spreading rapidly to Europe (Gosselin, 2007). Gosselin (2007) conducted a

study on the number of papers that were written on ABC during the period from 1988 to 2004

and concluded a total of 1477 articles written on the subject for those 17 years. The costing

system has therefore been part of numerous articles; it has been incorporated in most, if not

all, accounting programs and books (Gosselin, 2007) and has been part of the most popular

text books in the UK and USA (Atkinson, et al., 2004) (Hilton, 2005) (Horngren, et al.,

2002).

Therefore, whether or not Bjørnenak’s results are relevant at present time could be taken

under consideration. Even though, the scope of this paper does not cover relocation diffusion

(knowledge) of ABC, it can be assumed from the all of the above that its level is high, though

having in mind the less widened communication channels of SMEs.

11

The table below shows a summary of surveys of several companies in different countries and

the implementation rates of ABC could be examined in relation to the above discussed high

popularity. This is related to the second type of diffusion – Expansion diffusion, which is

related to growth of adopters of a specific innovation, in this case - the rise of adoption

among firms (Bjørnenak, 1997).

Authors Country Adoption rate of ABC

Innes et al. (2000) United Kingdom 17,5%

Bescos et al. (2002) Canada and France 23.1%

Cotton et al. (2003) New Zealand 20,3%

Kianni & Sangeladji (2003) USA 11,8%

Pierce & Brown (2004) Ireland 27,9%

Cohen et al. (2005) Greece 40,9%

Askrarany (2007) Australia 13,7%

Al-Omiri (2007) United Kingdom 29%

Breiley (2008) United Kingdom 5%

Kallunki (2008) Finland 28%

Baird (2008) Australia 42%

Jankala (2012) Finland 12%

(Sandalgaard, et al., 2012) Denmark 10%

Table 4 Developed from Gosselin (2007)1

As it can be seen on the numbers, considering the cost system’s popularity, the low rate of

adoption is clearly illustrated. This creates a paradox that will be addressed in more detail

further down.

1 Gosselin (1997) and Baird (2004) showed that there might be some confusion in the understanding of what

exactly is ABC. Furthermore, Gosselin (2007) also discussed the tendency of ABC non-adopters to be less inclined to answer surveys. All of this would therefore lead to the over-estimation of the rates of implementation.

12

1.2 Problem Formulation

As it can be seen from the surveys conducted, the diffusion process of ABC is not as strong

as one might expect. When the extensive amount of literature on the subject is contrasted to

the implementation rates of ABC it is very easy to see the point of issue. There are two main

suggestions made about why this is so. One of them is that the model is just not appropriate

for most companies, due to its high maintenance and accounting education requirements

(Brown, et al., 2004) . This notion is backed up by the surveys showing companies adopting/

implementing ABC and then abandoning it (Kaplan & Anderson, 2004). The other suggested

explanation is that people don’t know about the costing system (Bjørnenak, 1997). These

reasons could both be particularly true for SMEs, as smaller companies tend to have less

educationally specialized managers and fewer resources (Gunasekaran & Singh, 1999).

Additionally, the past failure of large companies to deal with the costing system has created

the impression that SMEs should not undertake ABC (Hicks, 1999). All this has possibly

contributed to a very low penetration rate in SMEs.

However, as argued about above, ABC is one of the most popular systems out there.

Furthermore, its recent development and the introduction of TDABC have made it more

simplified and reduced its complexity and necessities greatly (Kaplan & Anderson, 2004)

Even so, the diffusion of ABC continues to stay low, especially amongst SMEs (Jänkälä &

Silvola, 2012).This creates, as Gosselin (1997), Kennedy & Affleck-Graves (2001) and

others referred to, an ABC-Paradox.

Trying to understand the sluggish diffusion process, contingency theory began to be

considered appropriate. The limits outlined by Noreen (1991) and the other implications

connected to ABC showed that ABC was not designed for all companies. Therefore,

researchers started examining contingency factors related to adoption of the management

accounting system. These factors are comprised of external and internal criteria that included

size, structure, strategy, culture, technology and perceived external uncertainty that influence

the organization (Chenhall, 2007). Between the start of the contingency criteria research

(around 1995) and present time, many articles have been published on what factors influence

the decision to adopt and implement ABC/TDABC (Gosselin, 2007), which include both

survey and case study analysis. However, very little focus has been given to contingency

factors of influencing the smaller sized enterprises, despite the fact that their contribution to

13

the Global and Danish economies is especially high and increasing and that ABC was argued

to be relevant to smaller enterprises (Hicks, 1999) (Gunasekaran, et al., 1999).

Based on the different issues that ABC is faced with, including diffusion, model flaws, and

relevance to SMEs, this paper will look into contingency theory and examine the linkage

between contingency factors that influence ABC adoption and characteristics of smaller

enterprises. In order to do so, a number of hypotheses will be developed through the literature

review, which will be answered through the analysis of the survey. Additionally, an attempt

to create a framework that would progress the understanding of management accounting

innovations’ diffusion in SMEs will be made.

Based on the problem formulation, this paper’s research question is written below.

1.2.1 Research question

What factors influence the adoption of ABC and TDABC in Danish SMEs?

In relation to this research question, these sub-questions would also need to be answered:

What factors influence the adoption of ABC excluding size variables (non-SME specific)?

Is ABC relevant for SMEs?

1.3 Limitation

A number of limitations have been encountered during the process of writing this project.

These limitations arose both through the collection of literature as well as the independent

study. Due to this research being very general as well, there are a number of things that were

not always taken into account.

To start, this study did not differentiate between the adoption or non-adoption of ABC and

TDABC, where TDABC was proven to be simpler and more applicable to companies who

may not previously have been able to adopt ABC (Kaplan & Anderson, 2004). Also, since

TDABC is a newer concept, the diffusion process was not differentiated between it and that

of ABC, but looked at both collectively, so there is still potential for the widespread success

of TDABC. Management accounting innovations have been discussed to require 4 or 6 stages

of implementation and the same goes for ABC (Hage, 1980) (Kwon & Zmud, 1987) The

14

contingency theory used in this paper is generally related to a specific stage of

implementation; however, this is left outside of the scope of the project and it was not

differentiated between the implementation of the system into individual departments or the

full organization.

In terms of literature collection, a limit was set for the sources not being older than 20 years

old, due to the fact that the information would be more valid to today’s business environment,

despite the development of the system going back further in time. ABC has also developed

and the ABC of 2015 is not the same as when it was created. The chosen papers were also

found to be written about cases of ABC/TDABC in already developed countries, distorting

the potential for the system to be used worldwide. With studies having primarily been carried

out in the US and EU, culture was not an aspect that was looked into very much in terms of

national traits. The culture within different countries could have an effect on the use, but this

would increase the scope too much. Likewise could the culture of employees and the

implementation process be of use, but this is kept as a future research.

Aside from the contingencies that have been researched, the idea of the life-cycle presented

by (Kallunki & Silvola, 2008), which illustrated an alternative way of looking at the

contingencies.

There were two ways of looking at ABC implementation: if companies were fit to adopt the

system, or if the company had experienced success with implementing ABC. The research

question asks what factors influence adoption, so the contingencies presented an idea of what

the companies require to be able to implement, but it does not guarantee the success in the

end.

When it came to the independent study, it was noticed that some of the answers may have

favoured the performance of the leaders. This may have been due to us asking the CEO or

CFO to fill out the survey. However, the answers were still acknowledged as truthful. Some

respondents also wrote to us that the questions were too theory based and expressed their

frustration with that fact, whereas some companies also wrote that since they were not a

production company, they deemed the survey inappropriate for them.

This paper also only focuses on expansion, hierarchical diffusion. It only differentiates

between adopters and non-adopters of ABC. Details of whether a certain unit has considered

15

ABC and abandoned it; or implemented ABC before and abandoned it, etc.; will not be

included in the analysis. Had that question been asked, a better understanding of the diffusion

process of ABC might have been reached. Further on, in the ABC case that has been selected,

the hierarchical category is the natural choice as the diffusion of the costing system has been

observed to be size-sensitive (Innes & Mitchell, 1995). This research also only looked into

the demand side of diffusion, since only the company’s point of view is taken into account,

instead of looking into the suppliers of ABC.

2. Methodology

The methodology of this research consist of three parts; all contributing to the discussions of

the others. For the sake of clarity we differ between the ontological and epistemological

choices and considerations, and the two methods used for solving the research question. The

methods described are natural puzzle solving tools that belong to a certain paradigm, which

we will elaborate further on.

When a researcher tackles a problem, he must first develop a discussion of his philosophy of

science (Kuada, 2012), where the reasoning behind his action is shown and discussed. This

discussion has different purposes: it relates to the type of problem and how the researcher

thinks this can be tackled in the best way possible or “Best practice”. This project handles a

quantitative subject, where the role of the researcher is to test specific hypotheses and the

data collection will often be vast so, as to reach statistical significance. The method of using

quantitative data is also often very specified, as there are certain customs and traditions that

must be held, in order to handle the issue of validity and reliability (Kuada, 2012).This

particular case used data collected from a survey which is considered one of the two main

ways of quantitative data collection, and will then seek to analyze the data statistically in

order to test some hypotheses.

2.1 Paradigms

The usage of paradigm in modern science is largely attributed to Thomas Kuhn with the

development of “The structure of Scientific revolutions” from 1962. In this book Kuhn

defines paradigms as:

16

“Men whose research is based on shared paradigms are committed to the same rules and

standards for scientific practice. That commitment and the apparent consensus it produces

are prerequisites for normal science i.e., for the genesis and continuation of a particular

research tradition.” (Kuhn, 1962)

This definition is still today adopted by many and will also be applied to this research as the

definition of paradigms. What this means is that paradigms are something shared within the

scientific community and it can be ways of doing quantitative research, and other puzzle

solving activities. The paradigms chosen set the standards for the research and it is within

those standards that you find the epistemology and ontology of the research.

Paradigms have since been discussed by many scholars in many different ways, especially the

debate on objectivism and subjectivism, which has created controversy. This has caused a

variety of paradigms to appear, and with them, different ways of classifying them.

Previously, classification was done using the FISI (Functionalism, interpretivism,

structuralism, interactionalism) model, which classified them on a two-dimensional graph.

The same was used for the RRIF (Radical Humanist, Radical Structuralist, Interpretive, and

Functionalist) model of Burell and Morgan (1979). These classification systems were

however criticised for choosing the research from the paradigm, and not letting the scope of

the research justify the choice (Deetz, 1996)

One of the more recent models is that of Arbnor and Bjerke (2009). This framework for

paradigms identifies three approaches: The analytical, the systems and the actors, which

subcategorize all of their nine paradigms. The framework also promoted and discussed the

correlation between paradigms and epistemology and ontology, which will be reviewed in

regard to the specific research question of this research. The analytical approach is the first

and most objective approach. In many ways it is similar to the functionalist’s paradigm,

where there is an objective truth, that the researcher can accurately depict by decomposing a

certain object and putting it back together to create the full picture (Arbnor & Bjerke, 2009).

This approach has met a lot of critique in the field of social science as the tools for gathering

information often requires communicative skill and thus renders the notion of objectivity

invalid. (Deetz, 1996)

17

The actors approach is more like the social constructivists paradigm and it is a subjective

approach that works from the notion that truth is a construction of human interaction, and

thus a subjective truth. This also means that this approach is more inclined to look at how the

interaction that the researcher contributed in was affected, and the idea is then, that a

discussion of this will create the notion of reliability (Arbnor & Bjerke, 2009).

The systems approach is somewhere in between but leaning towards the objective notion that

there is a truth, but the context and content of this truth is constantly changing. This also

means that the systems approach cannot make the assumption that the subject of investigation

is stable. Like the other two approaches there are 3 paradigms within that vary from leaning

towards objectivity to an objective-subjective mixture. The ontology of the paradigms also

differ highly, but This is the paradigm chosen for this research as it includes a level of self-

reflection as imposed by Deetz (1996), which creates the basics for the rest of this

methodological discussion.

2.2.1 Structuralism and ontology

The paradigm could be called structuralism as it has many of the traits that we know from

that paradigm. Structuralism also views the world in systems, and tries to find and explain

possible structures. It has deep roots the philosophy and has some parallels to determinism.

The paradigm as described by Abnor and Bjerke does however take on a more modernized

form of structuralism as it is also mentioned as an inspiration for the systems approach

(Arbnor & Bjerke, 2009). Kuada (2012) defines ontology as describing “… the nature of

what the researcher seeks to know (i.e., the “Knowable” or “Reality”).” The ontology of the

systems approach and the paradigm within is divided as a discussion of ontology is often a

definition of a subjective or objective worldview, and it does not provide a final answer. This

is due to the objective-subjective nature of the systems approach placement on the

continuum, and the fact that even though there is a reality, it is a dynamic one. Instead the

ontology of structuralism is “Reality as mutually dependent fields of information” (Kuada,

2012). What this means is that when trying to comprehend reality, we are looking at

interdependencies and structure in the fields of information. In the specific case it would be to

find the correlations between the ABC-system and the criteria that have been established by

other research.

18

2.2.2 Epistemology of structuralism

Epistemology is defined as how the researcher perceives truth as well as how knowledge is

created. For structuralism where truth is in structures, it means that the researcher is trying to

find answer to a truth. This is important as the structuralism views the duality of truth from

both sides, but tries to establish some rules in the continuously shifting world. And

knowledge is created in doing so.

In this case specifically it is, as mentioned, done by finding correlations, but not only in

through the survey and analysis. The literature review is also created in order to establish and

categorize a system, in which knowledge is created. These structures created can be made up

of almost anything, from cultural structures to organizational leadership structures.

When looking for these structures, and with the duality of structuralism, it is important to

note that almost all research oriented at the epistemology can be used. Structuralism is thus

not limited to quantitative measure, but as it has roots in linguistics, it can also undertake

qualitative research like interviews and bind them together. This research does however not

branch out as our limitation also makes clear. This issue of finding the criteria could however

be done in different ways through the structural paradigm, but the statistical analysis and the

structural equation modelling is, from an economics perspective, a large part of creating the

framework and the structure in the use of ABC.

2.3 Method and puzzle solving techniques

This segment will attempt to portray the methods used in the two main parts of the research;

The literature review that laid the basis for the development of new hypotheses, and the

survey and the techniques used to create validity and reliability.

2.3.1 Literature review

A systematic literature review is a comprehensive framework that takes into account all

relevant literature within certain search parameters, and then attempts to categorize and create

a system in the vast amounts of literature on a certain topic. Denyer & Tranfield (2008)

defines the need as: “For academic evidence to be used by managers it needs to be rendered

accessible, palatable, relevant and useful.” For this Denyer & Tranfield (2008) developed a

framework and a 5 step way of creating this framework. This method will be applied in

creating a systematic literature review (Denyer & Tranfield, 2008).

19

First step in the process was searching peer-review journals from the last 20 years relating to

Activity-Based Costing and Time-drive Activity-Based Costing in English. This provided us

with an initial pool of 3,521, so next we focused on a few key-words in order to diminish the

number of articles. The key-words used were: Implementation (implement/adoption

/application of), SME (small and medium sized enterprises) and criteria (factor). We then

focused on empirical studies and skimmed through the titles and abstracts of 264 articles.

In order to ensure that all relevant theory was recorded we applied the ancestry approach to

multiple articles that provided a detailed relatively new literature review such as: (Baird, et

al., 2007), (Jänkälä & Silvola, 2012) and (Gosselin, 2007). At the end we had 73 articles that

lived up to our criteria. The peer-reviewed part would also require that the journal of

publication was on the list of Bibliometric research indicator (Bibliometrisk

forskningsindikator – Autoritetsliste, 2015) released by Danish university as a way of

classifying journals.

Of those 73 articles, 20 are SME specific and the rest are related to the criteria in general or

the contingencies of adoption of the ABC-model. From that we find that a great number of

these can be subcategorized into a contingency framework developed by Chenhall (2007).

This is a way of systemizing the relevant literature as well as providing supported hypotheses

for further research.

2.3.2 Survey and techniques

In order to answer the hypotheses it was necessary to develop a survey and analyses the

result. The data is gathered using a simple survey method inspired by that of Jänkälä &

Silvola (2012) as well as the survey questions from Sandalgaard, et al. (2012). Lastly to

produce the best result we applied the theories of Van der Stede, et al. (2005) which provides

an overview of studies done on surveying in management accounting research and with that,

a framework for ensuring greater quality in the surveys done.

(1) purpose and design of the survey, (2) population definition and sampling,

(3) survey questions and other research method issues, (4) accuracy of data

entry, and (5) disclosure and reporting.

(Van der Stede, et al., 2005)

20

The purpose has been outlined in the development of the research question, so we will start

with point number 2. The population of consists of Danish SME’s with 20-200 employees.

The actual sampling was done based on 1005 companies with a Danish CVR and between

20-200 employees. However through the survey we found out that the government database

used, might not be 100 % up-to-date as some companies reported having over 200

employees. Further investigation did however show that only 1 of the companies that

answered ‘200+ employees’, did in fact have more than 250. Furthermore we initially used

SME’s in Northern Jutland, as these would be more likely to have a higher response rate, due

to the fact that a lot of the companies are working with Aalborg University. In order to ensure

that this survey would represent Danish companies and not just companies in Northern

Jutland, we randomly selected an additional number of companies from the rest of Denmark,

this will be further discussed in the Non-response bias. We did not differentiate between

public and private companies, but there seems to be possibilities for further investigations as

many publically own companies are applying ABC or TDABC, as part of the public policy.

The questions can be read in appendix A, and constitutes a combination of earlier research

with surveys for contingencies. As mentioned, these were based on (Jänkälä & Silvola, 2012)

and (Sandalgaard, et al., 2012), but as these questions did vary from those two, we followed

the format in order to create new contingency based categories. Furthermore the answers are

on a Likert scale (1-5) except for size (groupings of 20; 20-200) and growth (groupings of 5;

-10-10). When reviewing the answers in the appendix there is a tendency of a skewed normal

distribution, meaning that 1-7 might have given a different more normalized answer as people

would refrain from the extremes (Wakita, et al., 2012).

Point 4 is mainly based on validity and reliability of the results, and for that we will need to

test the actual data for biases, as well as discuss other available data, and if there are

significant differences.

During the statistical analysis the data was attempted to be analyzed from a neutral stance.

This means not committing any “Statistical sins” That are described cleverly by perspectives

to Dante Alighieri’s Inferno in a humorous way (Neurosceptic, 2012). Each “Sin” of

statistical fraud will have a fitting punishment in the nine circles of Scientific Hell. Cumming

(2014) suggests that when testing the hypotheses, p values should not be the only thing

evaluated, and he raises the point that at a significance level of 0.1, 1 in every 10 factors

21

might actually be wrongly assesed. Determining this value is also considered a random task

with huge implications for the study. Therefor the statistical tests of hypotheses should not

only be limited to significant values, but also apply effect size as a tool2. This is further

explained by the need for 10 Events Per predictor Variable (EPV), as this has been a rule of

thumb in order to reduce type I and type II errors (Hosmer, et al., 2013). Events in this case,

are responding companies, but this rule has, however been discussed since, and it has been

established that 6-9 EPV shows that there are possibilities of minor issues (Vittinghoff &

McCulloch, 2006). This study finds an EPV of 6.05 leading to say that there is a possibility of

these errors, that could be solved by collecting more answers.

2.3.3 Non-response bias

In order to discuss the validity and reliability of a survey and the results, it is very important

to look at the biases that might be present. Non-response bias is a huge problem with

surveying, as a lot of people cannot be bothered to answer, and these people might represent a

certain group. That ultimately means that the survey is not representative of the population as

there might be a group with specific answers missing. (Whitehead, et al., 1993)

There are a few ways to calculate a non-response bias; first there can be made a follow-up

survey, where the people who did not answer, are given a shorter version, and then

comparing the answers. This method still relies on people wanting to answer something, but

provides some insight. Another way is to look at the disparity between the people who

answered on second and third mailing round and the people who answered instantaneously.

This way is used by different studies and assumes that the people who were last to answer are

more similar to those who did not answer (Sandalgaard, et al., 2012). Lastly the bias can be

viewed by looking at people who answered the whole survey and people who only answered

part of it. The issue here would be that there might be other reasons for people not wanting to

answer or fill out the whole thing.

This study applies the “last answer” method, and compares the 19 answers received from the

second/third round with the early answers. When testing for the mean, it produces a number

that should be within the confidence interval (α=0,1), and with a value of 0.38 there is not a

reason to think that there is a high non-response bias, however it is still possible given that

the test is based on assumptions. Given the low number of respondents, there is however still

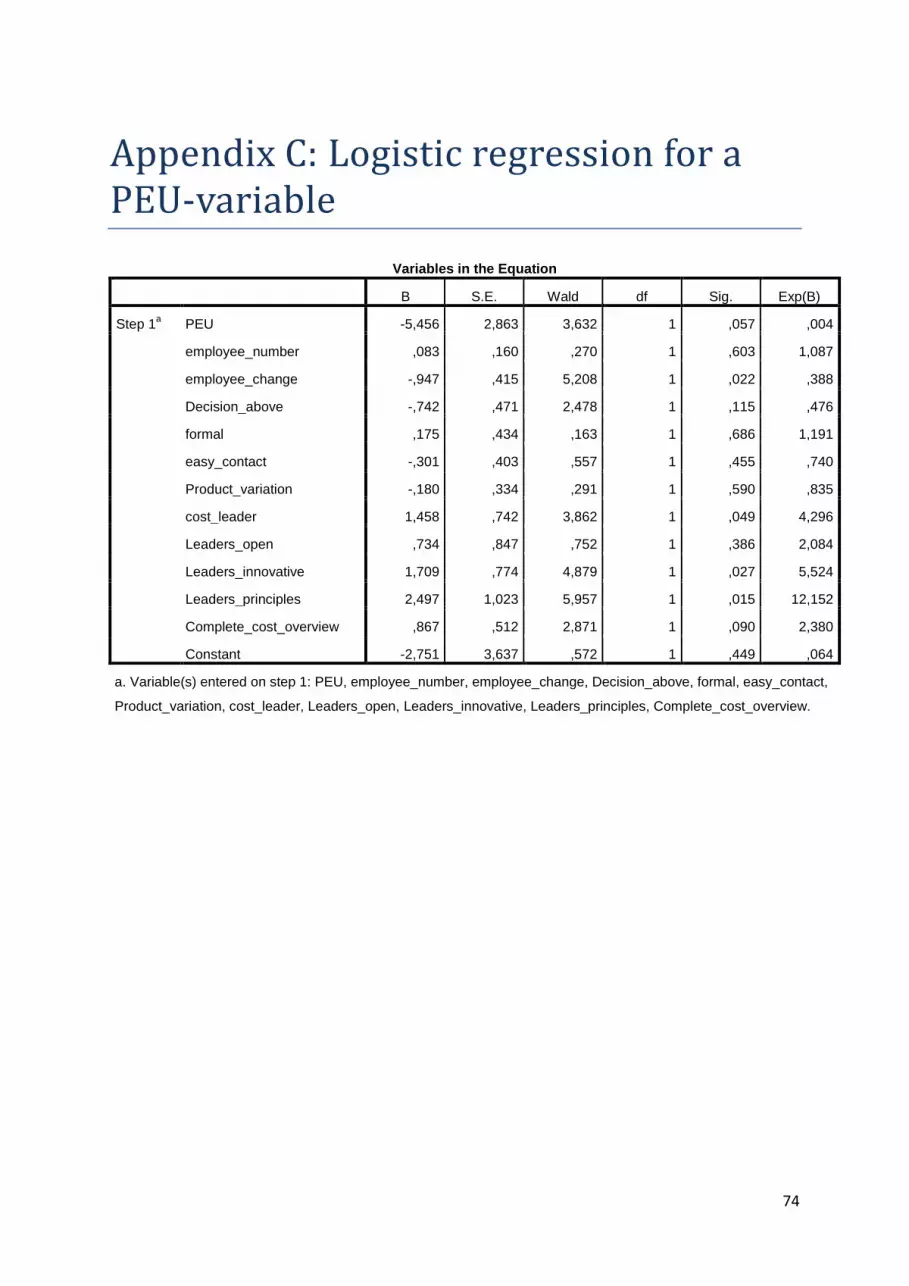

2 In logistic regression the Exp(B) value is assessed as it provides information of how strong the correlation is.

22

a chance that there might be a response bias. One concrete issue could be geographic. As

mentioned earlier, the survey is conducted from Aalborg University; this could mean that

companies in Northern Jutland are more inclined to answer, as many of these companies are

used to working with AAU.

3. Theoretical background of Activity-Based Costing

ABC can be divided up into stages as part of a four-stage model in order to develop a fully

implemented ABC system. Stage I is described as not being able to account for routine tasks.

These systems can be found in newly formed companies who haven’t yet had the chance to

develop further, or even companies who previously had a costing system that was

satisfactory, but due to internal reasons have lost control of their accounting. Some of the

older costing systems are described are described as Stage II standard costing systems, or

traditional costing systems, which were used commonly throughout the world, and are

traceable back to the industrial revolution. These systems are considered by Kaplan and

Cooper (1998) to answer the question of

“How can the organization allocate costs for financial reporting and for department cost

control?” (Kaplan & Cooper, 1988). While this is a necessary question to ask, this way of

allocating costs did not fully describe all the costs that were attributed to the good or service

being sold. These costs can be marketing, delivery or the process of selling the good. Still,

these methods proved to be effective enough, however not fully accurate (Kaplan and

Cooper, 1998).

The ABC system goes beyond the question which Stage II costing systems answers. ABC can

answer: what activities are being undertaken by the company, what each of these activities

and other processes cost, why these activities and processes are necessary for the firm, and

how much each activity needs to be exercised in order to fully satisfy all the stakeholders.

When taking more things into account and approaching the costs and activities in a different

way, the company is able to account for more expenses and is able to map out the entire

organization (Kaplan and Cooper, 1998). ABC became a solution to the widespread problem

of distortion of costs. As ABC was presented, it became one of the most popular innovations

in management accounting in the last decade and has contributed to the development of new

23

specific terminology like cost drivers, activity drivers, activity cost pools, cost objects and

others (Dierks & Cokins, 2000) (Gosselin, 2007).

The two examples of cost system structures below are seemingly identical, but they are

different from each other in fundamental ways. It is the ABC mentality of identifying

processes and all activities associated with those processes, rather than directly allocating

costs, that distinguishes itself from the traditional costing systems.

While Traditional costing systems on Figure I rely on direct labour hours and machine hours

in order to allocate costs, the ABC structure on Figure II identifies every activity in the firm.

The number of activities taking place can up be towards the 100’s or even 1000’s, depending

on the size and/or production volume of the company and can vary from different material

costs to scheduling employee’s shifts (Kaplan & Cooper, 1988).Originally, in order to

determine which activities were taking place, project teams would conduct surveys within the

company and question every employee about what percentage of their time they would spend

on each activity (Atkinson, et al., 2011). These activities are translated into cost drivers,

which quantify the different activities so they can be accounted for, for example ‘supervision’

is converted to ‘labour hours’, or ‘assembly of parts’ is ‘number of parts’. In the end as seen

on Figure II, the different cost drivers are assigned to different cost objects, for example a

particular product or a particular service.

This is an example used by Kaplan and Cooper’s Cost and Effect (1998.).

Figure I Traditional Cost Systems Allocate Overhead Costs to Production Cost (Kaplan & Cooper, 1998)

Figure II ABC Systems Trace Resource Expenses to Activities and Use Activity Cost Drivers for Tracing Activity Costs to Objects (Kaplan & Cooper, 1998.)

24

Simple Factory produces one million pens in one colour. Complex factory also produces one

million pens, however they make 2000 different varieties and each have varying production

volumes; some being part of large scale production (eg. 100,000 units), or specialty pens (eg

100 units). Since Complex Factory requires many more resources to manage all the different

types of pens, they will have much higher overhead costs and thus need to maintain a much

larger set of information. When it comes to applying the situation of Complex Factory to

Stage II costing systems, the costs would be reported in terms of production volume, where

for example 1000 pens out of the total of one million would be 0.1% of the total production

volume, and would therefore have 0.1% of the overhead costs allocated to them. This would

give every different pen produced roughly the same cost per unit as they don’t account for the

many different indirect costs of all the different pens. With the same cost being allocated to

all 2000 different pens, regardless of the volume of production, the true value is distorted and

instead gives a false number.

3.1 Time-Driven Activity-Based Costing

Kaplan & Anderson proposed that many companies were deciding to abandon ABC model

because the costs were too high and employees were irritated by its implementation and

complexity. They also acknowledged difficulty in implementing the model. As an answer to

the issues around ABC, Kaplan & Anderson (2004) introduced “Time-Driven Activity-Based

Costing” (TDABC).

The model was a transition from a “rate-based” approach to a “time-driven” one. In ABC,

cost driver rates were established to assign activity costs to cost objects, whereas under

TDABC these rates were already set on a time basis Kaplan & Anderson (2004) However,

the new model does not solve all the problems with the old model: unused capacity, fixed

costs being considered variable, and others. Nevertheless, the model was perceived as easier

to implement, cheaper and overall less demanding.

In the new system, only two estimates are required – cost per time unit of capacity and unit

times of activity. The first parameter could be obtained when dividing the cost of the

supplying resource by “practical capacity”, which is the time employees have excluding idle

time (suggested 80-85%).The second one could be acquired from interviews or direct

observation. The managers are not required to review how spend their time, but use the

25

practical capacity of the resources (which is a percentage of its theoretical capacity). (Kaplan

& Anderson, 2004)

The ABC system identifies a very broad range of activities compared to the more traditional

systems and leads to more accurate costs. However, with more work going into this method,

it ends up being more expensive and complicated to implement and also requires upkeep.

These factors can also influence which kind of companies choose to adopt this costing system

(Gosselin, 1997).

3.2 Development of ABC

In this section the development of ABC in to a more widely applicable costing system will be

reviewed. A focus will be put on Time-Driven ABC as it (as talked about above) is an

improvement to the original costing system. Additionally, after a brief review of the recently

published existing literature, it is clear to see that not much research has been done on ABC

in relation to TDABC.

Even though it started off as only a costing system, activity costing has undergone significant

changes in its purpose and execution. Researchers and practitioners started looking into the

information of financial and non-financial data that the system provided and recognized that

it could be used for management decisions and evaluations (Gosselin, 2007). Turney (1989)

argued that ABC shouldn’t be only for costing purposes, but should also identify relevant

strategies, improve designs, and making operating activities more efficient should be key

outcomes of the whole ABC package.

Despite the general tendency of praising ABC at the time, there were some that questioned

the effectives of the costing system. (Johnson, 1990) (Johnson, 1992) (Piper, 1990) (Piper,

1991). Noreen (1991) provided some research on when ABC delivers accurate costs. He

provided conditions, which in some cases aren’t met and could explain why managers had

issues using ABC model for decision makings. Issues with the model were outlined further

by Kaplan & Anderson (2004) that focused the maintenance, complexity problems and model

flaws.

As discussed, unlike the traditional ABC, where reported employee time-capacity very

frequently added up to 100%, whereas TDABC allowed for a more accurately estimated

unused capacity. Additionally, the model’s updating became easier and less time consuming.

26

In order to add new activities, management was required to estimate the unit time that it

required (Kaplan & Anderson, 2004). The majority of differences in the model were based on

the previous weaknesses of ABC (Kaplan & Anderson, 2004). As previously mentioned, the

model was presented as a more simplified version of ABC. Kaplan and Anderson (2007b)

presented a case study where 1200 activities were condensed down into 200 processes, which

additionally provides proof of the system’s simplification. Everaert et al. (2008b) argued that

the high cost and time spent on updating the model was reduced due to the time equation,

which is part of the TDABC. Additionally, Kaplan and Anderson (2007a)discussed the

difficulty in gathering data from ERP systems in the old model and promoted TDABC as

more easily compatible with different information systems.

4. Literature review

After the terminology has been explained and the scope of the project has been identified, a

review of existing literature will be made in an attempt to show and explain the application of

ABC in SMEs. Before the main research question is addressed, it is important to answer the

question of whether or not Time-Driven ABC and ABC are relevant to SMEs.

4.1 TDABC’s application

Even though ABC is still relevant and creates value for its users (Stratton, et al., 2009), the

focus of research is falling on TDABC. In recent years a number of researches have been

made on costing system, examining its usefulness in different contextual backgrounds.

Kaplan and Anderson (2007b) discussed the successful implementation of TDABC in

logistics and service companies, which was later acknowledged by Everaert et al. (2008b). It

has been confirmed by research that TDABC is capable of capturing the complexity of

logistic company activities (Bruggeman, et al., 2005). Everaert et al. (2007)

(2008a)conducted a case study on a logistics company and researched whether the company

should continue with ABC implementation or switch to TDABC. The results indicated that

ABC failed to capture all the factors associated with the activities, whereas TDABC could.

Everaert et al. (2008b) examined a Belgian wholesaler and concluded that TDABC was able

to trace logistics operations very accurately, despite their complexity. Furthermore, as

suggested by Kaplan & Anderson (2004), it managed to give information on unnecessary

27

costs. The system was able to provide managers with adequate information on strategic

decisions (Korpunen, et al., 2010) (Öker & Adigüzel, 2010) as well as accurately estimate

product costs (Fladkjær & Jensen, 2011).

However, even after the significant reduction of complexity and time-consumption,

researchers have outlined that companies still have issues with those factors (Ratnatunga, et

al., 2012). Gervais et al. (2010) talked about how data gathering and complexity of

implementation was burdensome. This was backed up (Fladkjær & Jensen, 2011).

The conclusion that could be made from examining the recent literature, however, points

towards the fact that TDABC, compared to ABC, is an improvement in regards to two

different factors. Simplicity - Kaplan and Anderson (2007b) discussed it as being one of the

major features of TDABC, which was later confirmed by Somapa et al. (2012). Its resource

requirements enable people without extensive economical or business education, such as

some SMEs, to be able to handle TDABC. As previously mentioned by Kaplan and

Anderson (2007a), adaptability is when managers don’t need to put as much effort updating

the system. Stout and Propri (2011) confirmed this notion. Furthermore, as the system is very

versatile, it allowed easier linkage to existing information systems (e.g ERP systems) (Kaplan

& Anderson, 2004); (Varila, et al., 2007), which Reddy et al. (2011) also debated as a major

benefit. This clearly also reduced the resources and time required for implementing / adopting

TDABC. What’s more is that it enabled small and medium sized enterprises with not-so-

complex activities at hand to use simple spreadsheets for support as software. (Somapa, et al.,

2012) (Kaplan & Anderson, 2004)

As ABC’s evolution lead to its simplification and maintenance improvements, the general

idea that ABC is only useful for large corporations started to get tested. Even though research

on the implementation of activity-costing in SMEs is not particularly popular, there are a

number of studies that find the relevance and compatibility of the two (Hicks, 1999)

(Gunasekaran, et al., 1999).

4.2 Activity-Based Costing’s application in SMEs

Further down the existing literature on Activity-Based costing in SMEs will be examined.

After analysing several case studies above, it could be argued that Kaplan & Anderson’s

(2004) claims are justified and the improvements to the system are being realized.

28

ABC is found more frequently in large companies than in smaller ones (Bjørnenak, 1997)

(Krumwiede, 1998) (Gosselin, 2007). Due to the difficulties with understanding and

sustaining the system, it was unsurprisingly assumed that ABC is not appropriate for SMEs

(Hicks, 1999). There have also been several arguments against the adoption. SMEs often

face a lack of resources. Inadequate financial, human and technical resources could restrict

companies in engaging in higher complexity models (Roztocki, et al., 2004). Furthermore,

Baxendale (2001) argued that smaller enterprises often gather information only for lenders

and tax purposes, which makes the necessary information to support ABC hard to compile.

Needy et. al. (2000) mentions the additional costs of hiring consultants and the reduced

productivity during the implementation stages (also confirmed by Roztocki, et al., (2004)).

Resistance to change in the employees was also found to be an issue (Bharara & Lee, 1996).

Despite these, even before the popularization of TDABC, there has been evidence that ABC

is appropriate for companies with lesser size and provides benefits for them (Hicks, 1999)

(Bharara & Lee, 1996). As shown in the previous section, the introduction of TDABC only

strengthened that argument. Additionally, implementation procedures have been developed

in aiding the companies with using the system (Gunasekaran, 1999, Bharar & Lee, 1996,

Roztocki, 2004). Moreover, because of the less simple structures and less diversified

activities, smaller companies are able to use spreadsheets, allowing them to capture the

benefits of ABC without complex systems or huge costs (Hicks, 1999, Bharar & Lee, 1996,

Needy, et al., 2000). More recently, Somapa, et al. (2012) conducted a case study towards

TDABC’s usefulness in SMEs, but pointed out the need for IT improvements. Also, Jänkälä

& Silvola, (2012) concluded that SMEs seem to benefit from TDABC, if they are suffering

from decline of growth or have been previously profitable.

Summing up, although SMEs lack the knowledge and resources of bigger companies, they do

make up for more flexibility and simplified requirements. As it can be seen from above, even

though ABC isn’t perfect, some of the major issues of the original model have been

addressed in the new time-driven one. In doing so, it has become more applicable to smaller

enterprises than previously. However, as the problem formulation states, the diffusion of

ABC amongst those units is low. In the next section, a review of the contingency factors that

influence the adoption of management accounting practices will be made, from which a

29

framework will be derived. This will lead into an attempt to find significance between factors

in the framework and the characteristics of SMEs (gathered from the survey conducted).

4.3 Contingency based theory and ABC

Contingency based theory is a large emerging concept within studies of management

accounting, that combines the models like ABC and traditional budgets with contextual

information (Chenhall, 2007). A contingency in management accounting is addressing the

vast possibilities and randomness that characterize every company, and it is in contrast to a

unified theory where there is one answer and one model that applies for every situation. The

concept of contingencies has been applied for over 25 years, during which time the

framework has been developed and applied by different studies, especially relating to

Activity-Based Costing (Gosselin, 1997). The framework’s main contributor has been

Chenhall (1998, 2003, 2004 and 2007) all of which have added to the management control

systems contingencies in different ways.

With the high focus on Activity-Based Costing in current literature proven by this literature

review, it is shown that even though many articles tackle the individual contingencies

(Bruggeman & Slagmulder, 1995) (Kennedy & Affleck-Graves, 2001) and others multiple

contingencies (Baird, et al., 2007) (Jänkälä & Silvola, 2012), no framework, to the

knowledge of the authors, investigates all contingency factors within the same study. These

contingencies have been challenged by the emerging research on Organisational Life Cycle

(OLC) that assesses the adoption of ABC on the stage of the company rather than the actual

contingency factors (Kallunki & Silvola, 2008). This is especially relevant for the size of the

company, as previous studies has concluded that company size has a positive correlation with

adopters of ABC. Kallunki & Silvola (2008) did however conclude that the OLC has a

correlation independent of size, meaning that a smaller company in the same stage of the life

cycle would be as likely to adopt ABC as a larger sized company. These findings do not

however affect the contingencies, but merely add to the question of company sizes

Through the litterature review for this study, it was found that a large part of the studies

contributes in a way to the contingency framework. This has then been used to create a

framework, catagorizing the different areas of which the articles contributes to:

30

Contingency Factors Literature

Organizational Size (Brierley, 2008) (Krumwiede, 1998), (Bjørnenak,

1997) (Brown, et al., 2004) (Chenhall, 2004)

(Kallunki & Silvola, 2008)(Baird et al., 2004) (Innes

& Mitchell, 1995) (Major & Hopper, 2005) (Al-Omiri

& Drury, 2007)

Organizational Structure (Gosselin, 1997) (Kallunki & Silvola, 2008)

(Anderson, 1995)

Organizational Strategy (Cooper & Kaplan, 1998) (Bjørnenak, 1997)

(Brown et al., 2004) (Brierley, 2008) (Krumwiede,

1998) (Gosselin, 1997) (Innes & Mitchell, 1995)

(Kennedy & Affleck-Graves, 2001) (Chenhall &

Langfield-Smith, 1998)(Baird, et al., 2007) (Kallunki

& Silvola, 2008) (Schoute, 2011)

(Shields, 1995) (Al-Omiri & Drury, 2007)

Organizational Culture (Malmi, 1997) (Baird, et al., 2007) (Baird, et al.,

2004)(McGowan, 1998) (Anderson & Young, 1999)

(Arnaboldi & Lapsley, 2005) (Major & Hopper,

2005)(Brown, et al., 2004) (Brewer, 1998) (Shields,

1995) (Vieira & Hoskin, 2002)

External Uncertainty (Mia & Clarket, 1999) (Cooper & Kaplan, 1998)

(Anderson, 1995) (Anderson, et al., 2002) (Arnaboldi

& Lapsley, 2005) (Kallunki & Silvola, 2008) (Al-

Omiri & Drury, 2007) (Jänkälä & Silvola, 2012)

(Cardinaels, et al., 2004)

Technology (Ittner, et al., 2002) (Askarany, et al., 2007)

(Bruggeman & Slagmulder, 1995) (Krumwiede, 1998)

(Anderson, 1995)(Arnaboldi & Lapsley, 2005)

(Shields, 1995) (Somapa, et al., 2012)

Table 5 Framework for literature in contingency factors

31

This framework will be used as a basis for developing the hypothesees under each segment as

well as an explanation of how the relevant contributions have been made.

4.3.1 Organizational size

Organizational size is one of the most researched and developed areas in ABC litterature.

This could be due to the straightforwardness of the research, as it requires only a few

questions that can easily be answered with only limited knowledge of the company. The

relationship between size and sophisticated control systems was first touched upon by

Khandwalla (1977), where the research stated that a large organisation undertakes complex

activities and that formalisation of procedures are more beurocatric. In relation to more recent

ABC related litterature Innes & Mitchell (1995) found that bigger companies had a higher

ABC adoption rate. This research was however focused on companies with either above or

below a turnover of 223$ million, so the proportions were high.

Later studies showed the relationsship in smaller companies as well, but addressed the need

for a certain size. This was done by Bjørnenak (1997) as an example, in a study of diffusion

of the ABC model that has since been used as a base for a lot of the recent research.

Bjørnenak (1997) addresed the fact that the system demands resources to be applied, and thus

needs a certain size. This is furthermore the reason for selecting companies with at least 20

employees in the following survey.

Studies of organizational size vary in their approach as some look mostly at the turnover or

other financial measures such as sales (Al-Omiri & Drury, 2007) (Innes & Mitchell, 1995)

(Krumwiede, 1998) (Baird, et al., 2004) while others use number of employees (Brown, et

al., 2004) (Kallunki & Silvola, 2008) as well or the Organisational Life Cycle as mentioned

earlier. This is one of the most debated factors, as Kallunki and Silvola (2008) found that size

is only part of OLC and thus the life cycle should be focused over size. This also creates the

relevance for further research into SME’s like that of Jänkälä & Silvola (2012). With the

question of size, the question of growth also emerges, and this has been implemented in many

of the forementioned studies of organisational size, but there does seem to be some

discrepancies.Kallunki and Silvola (2008) uses the financial aspects of growth to show what

stage of the life cycle the company is in, however employee growth showcases some of the

same tendencies.

32

Given the above mentioned research, a few hypotheses can be developed in order to further

examine organizational size. The same will be done for the following contingencies.

H1A There is a positive relationship between the probability of a company using

ABC and the organizational size.

H1B There is a positive relationship between the probability of a company using

ABC and the company growth in employees.

4.3.2 Organizational structure

Gosselin (1997) wrote in regards to Activity-Based costing that: “Organizational structure

influences the capability of an organization to implement innovations.” This means that there

should be correlation between the organizational structure and the use of ABC, and

furthermore it seems that mechanistic structures are more likely to be successful in the

implementation of ABC (Gosselin, 1997). This mechanistic structure meant that the company

would or should at least be more likely to implement ABC when it is centralized and

formalized. Gosselin (1997) also found a direct correlation between vertical differentiation

and the use of ABC.

This research also builds on earlier studies, which showed that innovative businesses were

more open to undertake new management accounting systems. This has also been shown by

Chenhall (2007), but this was for management accounting tools in general.

Kallunki & Silvola (2008) further explored the strategy associated with the organizational life

cycle, and their findings also pointed towards that companies in a mature state were more

likely to apply more sophisticated cost systems, and these companies also showed a more

formal and bureaucratic organizational structure than that of companies in growth. There is,

however, some level of ambiguity in some of the research done in the area. Anderson (1995)

showed that there was both a positive and negative effect of centralizing. The negative effect

was that the centralized decisions limited new ideas and new costing systems from entering

the organization. This was a case study of General Motors and it showed some of the

considerations of the managers in regards to applying a new costing system. Even with

anecdotal evidence there seems to be some things that are still not clear in regards to

organizational structure. This leads to the hypotheses:

33

H2A: There is a positive relationship between the probability of a company using

ABC and the structure being formal

H2B: There is a positive relationship between the probability of a company using

ABC and the structure being centralized

4.3.3 Organizational strategy

When looking into the purpose of ABC we see a great deal of strategic decisions benefitting

from the model. ABC provides a lot of information and based on that information the strategy

can be made (Cooper & Kaplan, 1998). This means that if a company provides customized

production, ABC has a high value to see what product provides the highest profits and thus

where to focus (Schoute, 2011). This was also a conclusion made by Krumwiede (1998) in a

study of complexity on manufacturing and costing systems, as well as a few others (Chenhall

& Langfield-Smith, 1998) (Gosselin, 1997).

The second major part of organizational strategy in ABC literature is based on the ability of

ABC to find problems in product costs (Cooper & Kaplan, 1998), and this has created a

ground for the research of strategies. Many of the studies that investigate the company

strategy find that cost leaders are more prone to using ABC (Kallunki & Silvola, 2008) (Al-

Omiri & Drury, 2007) (Shields, 1995). These conclusions were made by looking at the use of

Just-In-Time production (JIT) and the use of LEAN that both seemed to be correlated with

the use of ABC. There is, however, another strategy than just cost-leadership. The prospector

strategy was associated with the ABC by Gosselin (1997). This part is highly controversial as

both sides have findings and arguments that support a certain hypothesis. Gosselin (1997)

suggest that rising companies driven by innovation and aggressive strategies are more likely

to undertake new costing systems as well in order to gain an edge. Kallunki & Silvola (2008)

argues that companies are more likely to pursue ABC when reach maturity and focus on cost

leadership, as that is one of the main functions of the ABC. The question can also be related

to that of Bjørnenak (1997) as he shows that the diffusion process has influence on the ABC,

but other studies have shown that some companies apply ABC only to revert back after some

time (Kaplan & Anderson, 2004). There seems to be two main ideas about why companies

aren’t using ABC; first that the diffusion process is at a lower stage and second that the

framework has issues that means that not all companies can apply it. This will be further

reviewed in the discussion.

34

H3A: There is a positive relationship between the probability of a company using

ABC and the use of product differentiation

H3B: There is a positive relationship between the probability of a company using

ABC and companies ability to be cost leaders

4.3.4 Organizational culture

Organizational culture is a broad term and thus the research in the area is very diverse. Malmi

(1997) established that many of the problems that affected the ABC implementation were a

product of resistance from within the company. This resistance was both amongst leaders, as

well as employees and it was the finding that culture has huge influence on the adoption of

ABC (Baird, et al., 2004) (Baird, et al., 2007). The first step to change the culture is the

leadership change (Gosselin, 1997), but some studies have undertaken the task of evaluating

employee perception and the correlation with ABC (McGowan & Klammer, 1997) (Baird, et

al., 2007) (Vieira & Hoskin, 2002) (Major & Hopper, 2005). However, as the employee

perception is harder to evaluate given the scope of this study, the leadership is to be evaluated

first.

In order to look at the resistance within the organization it is important for the management to

appear open and innovative, so that new ideas like ABC can be accepted by management in

the first step. ABC is as mentioned one of the most supplied costing systems (Gosselin,

2007), and at the same time it is recommended by many books for higher education as

previously mentioned. This would mean that leaders who use recommended principles would

be more likely to adopt ABC.

H4A There is a positive relationship between the probability of a company using

ABC and the management wanting to appear innovative.

H4B There is a positive relationship between the probability of a company using

ABC and the management applying recomended management accounting

principles.

4.3.5 External uncertainty