FINANCING TRANSIT WITH LAND VALUES ANNUAL WORLD BANK CONFERENCE ON LAND AND POVERTY, 2014 Hiroaki Suzuki, Lecturer, National Graduate Institute for Policy Studies, Japan Ellen Hamilton, Lead Urban Specialist, World Bank

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FINANCING TRANSIT WITH LAND VALUES

ANNUAL WORLD BANK CONFERENCE ON LAND AND POVERTY, 2014

Hiroaki Suzuki, Lecturer, National Graduate Institute for Policy Studies, Japan

Ellen Hamilton, Lead Urban Specialist, World Bank

Outline

1. Rationale2. Land value capture instruments3. Advantages of DBLVC4. Case study: Hong Kong SAR5. Key findings6. Conclusion

2

3

Land Value Capture Links Planning and Financing Through TOD

Sustainable Urban

Development

LVC TOD

Coming Soon

4

Concept of Land Value Capture

Private land owners should profit from this portion of the increment.

Public service providers should capture this portion of the increment to cover the costs of public infrastructure and local service provision.

The government, on behalf of the general public, should keep this portion of the land value.

Increases in land value due to landowners’ investments.

Land buyers (or lessees) pay sellers (lessors) to obtain the property rights of land.

Intrinsic land value

Increases in land value due to public investment in infrastructure and changes in land use regulations.

Increases in land value due to population growth and economic development.

5

Features of Land Value Capture Instruments

Instrument Description

Tax- or Fee-Based

Property and Land Tax

Tax that is levied on estimated value of land or land and buildings combined. Revenues usually go into budgets for general purposes.

Betterment Levies and Special Assessments

Surtaxes imposed by governments on estimated benefits created by public investments, so as to require property owners who benefit directly from public investments to pay for their costs.

Tax Increment Financing (TIF)

A surtax on properties within an area that will be redeveloped by public investment to be financed by municipal bonds, against the expected increase in property tax, which is pledged. Instrument mainly used in US.

Exactions/Impact Fees

Fees (or in-kind contribution) collected from private developers to pay for the cost of providing additional public infrastructure and services, and to accommodate additional population generated by their new development projects.

Development-Based

Land Sale or Land Lease

Governments sell developers land for payment or the land use right, in return for either an upfront leasehold charge or payments of annual land rent through the term of the lease.

Air Right SaleGovernments sell development rights extended beyond the limits specified in land use regulations (e.g., FAR) or created by regulatory changes to raise funds to finance public infrastructure and services.

Land Readjustment

Landowners pool their land together for reconfiguration and contribute a portion of their land for sale to raise funds to partially defray public infrastructure development costs.

Urban Redevelopment Financing

Landowners together with a developer establish one cooperative entity to consolidate piecemeal land parcels into a single site that they then develop with new access roads and public open spaces. The local government then modifies zoning codes and increases maximum floor area ratios in the targeted redevelopment district (typically around rail transit stations). Instrument mainly used in Japan.

6

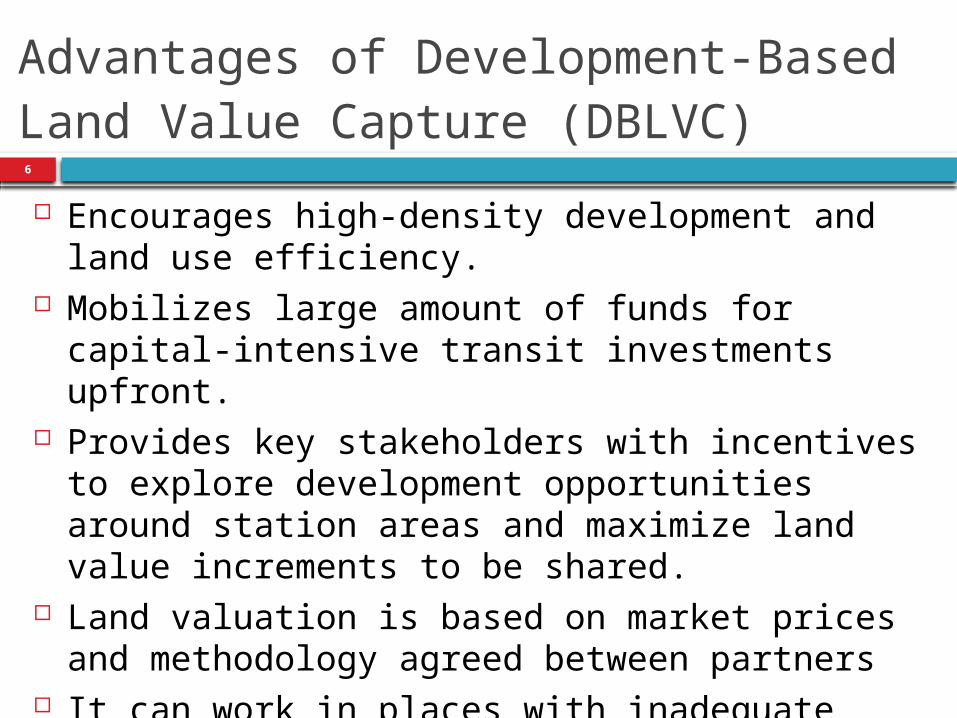

Advantages of Development-Based Land Value Capture (DBLVC)

Encourages high-density development and land use efficiency.

Mobilizes large amount of funds for capital-intensive transit investments upfront.

Provides key stakeholders with incentives to explore development opportunities around station areas and maximize land value increments to be shared.

Land valuation is based on market prices and methodology agreed between partners

It can work in places with inadequate property taxations systems

Strategic instrument for urban finance and planning.

7

Book’s Case studies Hong Kong, China Tokyo, Japan Nanchang, China Delhi and Hyderabad, India Sao Paulo and Rio de Janeiro, Brazil

8

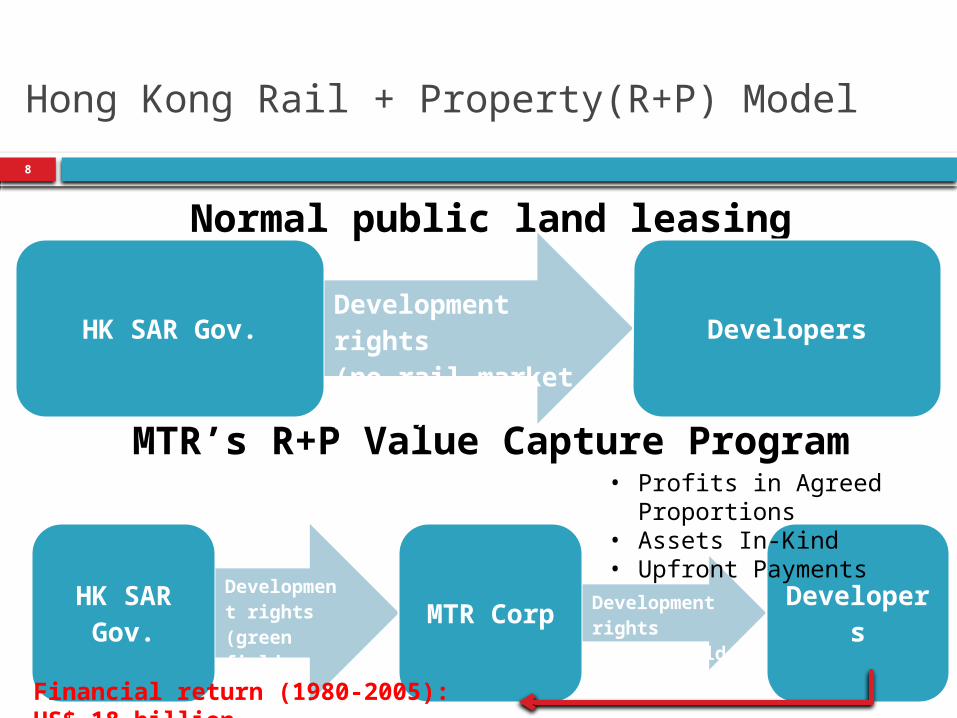

Hong Kong Rail + Property(R+P) Model

Normal public land leasing

MTR’s R+P Value Capture Program

HK SAR Gov.Development rights (no rail market price)

Developers

HK SAR Gov.

Development rights (green field price)

MTR CorpDevelopment rights (green field price)

Developers

• Profits in Agreed Proportions

• Assets In-Kind • Upfront Payments

Financial return (1980-2005): US$ 18 billion

9

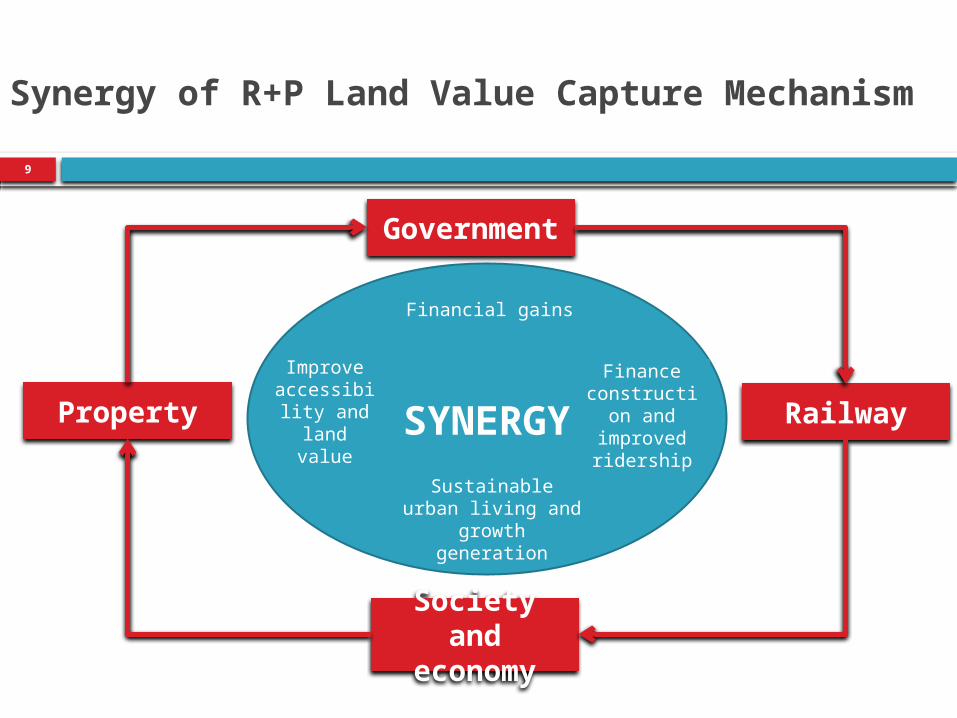

SYNERGY

Government

Property Railway

Society and

economy

Synergy of R+P Land Value Capture Mechanism

Financial gains

Sustainable urban living and growth

generation

Finance construction

and improved ridership

Improve accessibility and land

value

10

Factors contributing to success

Macro conditions: economic competitiveness and population growth

Government’s capability: Clear territorial development strategy Planning capacity Land management (high density) Low use of private transportation (62 cars per 1,000

persons) MTR’s Institutional Framework.

Technical expertise (design, real state)

11

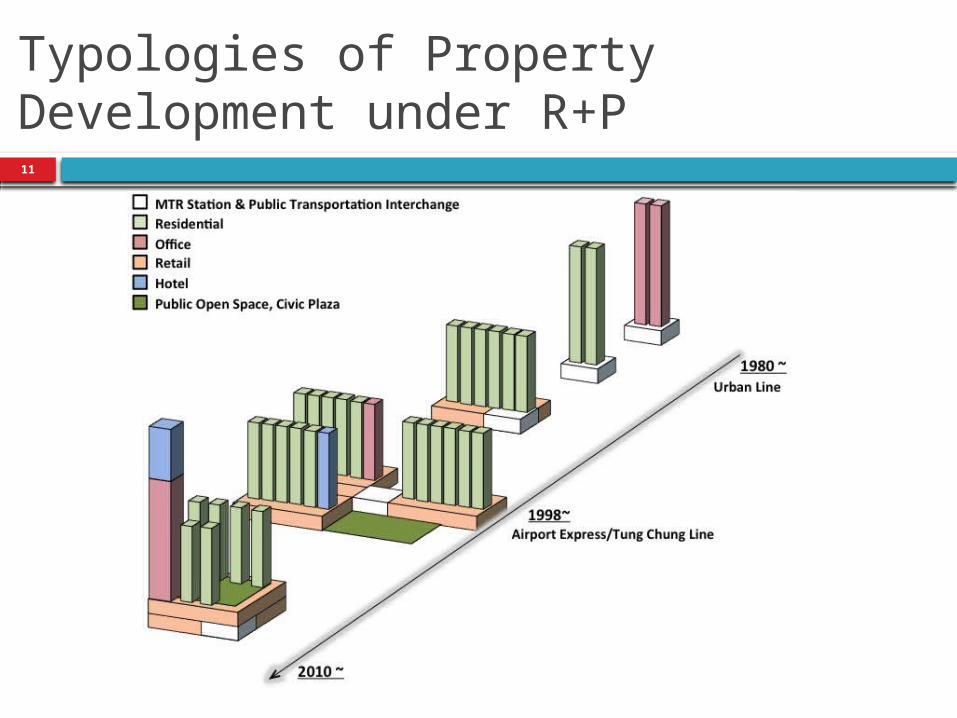

Typologies of Property Development under R+P

12

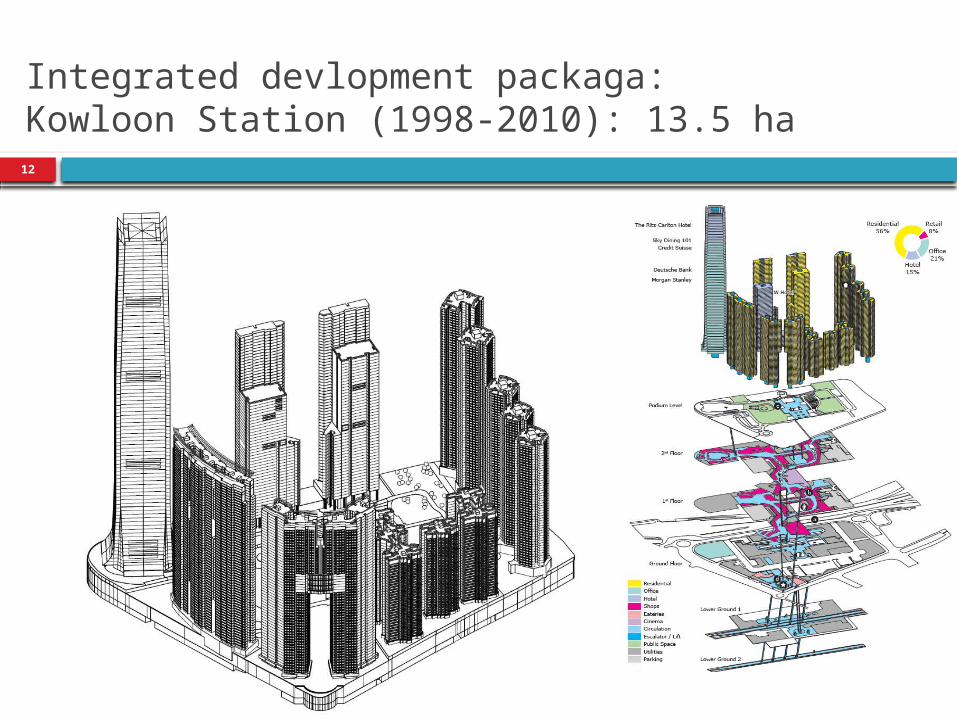

Integrated devlopment packaga:Kowloon Station (1998-2010): 13.5 ha

13

Key findings

DBLVC as Inclusive Value Creation Exercise. Public Land Ownership Not A Necessary Condition of

DBLVC DBLVC based on Sound Planning Principle. Enabling factors

Macro fundamentals Visionary master plan Flexible zoning Multiple finding sources Intergovernmental collaboration Entrepreneurship Clear, fair and transparent rules Key instruments

14

Challenges and risks

Overreliance on DBLVC Corruption related to land transactions Displacement of Low Income Households

as a Result of Gentrification in TOD Area

Related Documents