FINANCING OPTIONS for Renewable Energy UNDP Regional Centre in Bangkok, Thailand Country Experiences

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FINANCING OPTIONS for Renewable Energy

UNDP Regional Centre in Bangkok, Thailand

Country Experiences

The analysis and policy recommendations of this Report do not necessarily refl ect the views of the United Nations Development Programme, its Executive Board or its Member States. The Report is an independent publication commissioned by UNDP. It is the fruit of a collaborative effort by a team of eminent experts, stakeholders and the Regional Energy Programme for Poverty Reduction (REP-PoR) team of the Regional Centre in Bangkok.

Copyright © 2008 UNDP

United Nations Development ProgrammeRegional Centre in BangkokRegional Energy Programme for Poverty Reduction (REP-PoR)UN Service BuildingRajdamnern Nok AvenueBangkok 10200 Thailandhttp://regionalcentrebangkok.undp.or.thhttp://regionalcentrebangkok.undp.or.th/practices/energy_env/rep-por

Design and layout of this revised version: Inís Communication (www.inis.ie)Cover illustration: Doungjun RoongruangOriginal design and layout: Imran Hussain

AcknowledgementsThis Report on Financing Options for Renewable Energy: Country Experiences is part of a set of three policy studies undertaken by Regional Energy Programme for Poverty Reduction (REP-PoR). This report builds extensively upon prior work undertaken for the Policy study on Regional Mapping of Options to Promote Private Investments in Alternative Energy Sources for the Poor. The other two policy studies consist of Overcoming Vulnerability to Rising Oil Prices: Options for Asia and the Pacific and Cross-Border Energy Trade and its Impacts on the Poor. The original study is the result of almost two years of evidence-based research and extensive consultations with experts to review the state of renewable energy options and to ensure that they can contribute to the sustainable economic growth, energy security, and poverty reduction goals of the Asia-Pacific countries. The research study was initiated in mid 2005 and completed by early 2007. The analysis and the discussions in this Report are based on the information that was available then (documented in volume I of the original study). Many people have contributed directly and indirectly to this collaborative effort.

The original research study, including the six national assessments and respective case-studies (documented in volumes II to VII of the original study), was undertaken by Winrock International under a study commissioned by UNDP/ REP-PoR. We appreciate the work of the Winrock International, ably led by the principal researcher, Bikash Pandey. We also acknowledge the contributions of the team that supported the lead researcher, including Jerome Weingart, Soma Dutta, Ellen Bomasang-Son and Chris Greacen. We appreciate the work of the country leads in Bangladesh (Lutfiyah Ahmed, Suman Basnet, Mohammed Khalequzzaman, Hasna Khan and Firoz Mallick), Cambodia (Sierra Fletcher and Curtis Hundley), Indonesia (Conrado Heruela, Bernard Castermans, PELANGI), Nepal (Suman Basnet, Yuba Raj Adhikari, Bharat Poudel, Karuna Sharma), Solomon Islands (Herbert A. Wade and Kenneth Bukehite) and Philippines (Conrado Heruela and Cristina Cayetano) for their data gathering and analysis. We acknowledge the first round of bibliography support by Fay Ellis, Anita Khuller and Mallika Aryl.

We express our appreciation to the individuals who participated in interviews, group discussions and questionnaires as part of the research undertaken for this work. These individuals are too numerous to mention by name, but include employees of government ministries, schools and clinics, energy companies, research organizations and, of course, members of the communities in which the case studies were conducted.

The analytical structure and conceptualization of the report was developed by the REP-PoR team in the UNDP Regional Centre in Bangkok, comprising Nandita Mongia (Team Leader),Thiyagarajan Velumail, Thomas Jensen, Bhava Dhungana and Sooksiri Chamsuk. The report and study underwent several reviews including sessions of technical committee feedback from experts and external partners [the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), the South Asian Network for Development and Environmental Economics (SANDEE) and the Asian Institute of Technology (AIT)], as well as several UNDP in-house consultations. Candid views and constructive suggestions helped to significantly improve the report. In particular, we would like to thank Kamal Rijal, Pranesh Chandra Saha and Ram Shrestha for their timely suggestions.

We acknowledge the advice provided by K. V. Ramani during the start up phase. An additional piece of analysis, a comparison of competitiveness of renewable energy systems and fossil fuels, included in chapter 3 of the Report, was completed by REP-PoR team in November 2007. Data and information of the final version of this abridged Report has been subsequently updated by Conrado Heruela and Sanna Salmela-Eckstein where data found available. Patient editorial support from Fareeda Hla helped us considerably to finalize the Report. The updating of data, compiling the references, editing and design of the Report owes much to the REP-PoR team members, including Imran Hussain, who contributed at different stages of the Report to bring it to fruition. All the above mentioned efforts have made the writing of this report possible.

Nandita Mongia, Ph.D. Chief, Regional Energy Programme

Asia and Pacific Region

IV

ContentsAbbreviations and Acronyms I

Glossary of Financing Terms V

Executive Summary 1

1. Introduction 9Background 9

The global energy-poverty discourse 9

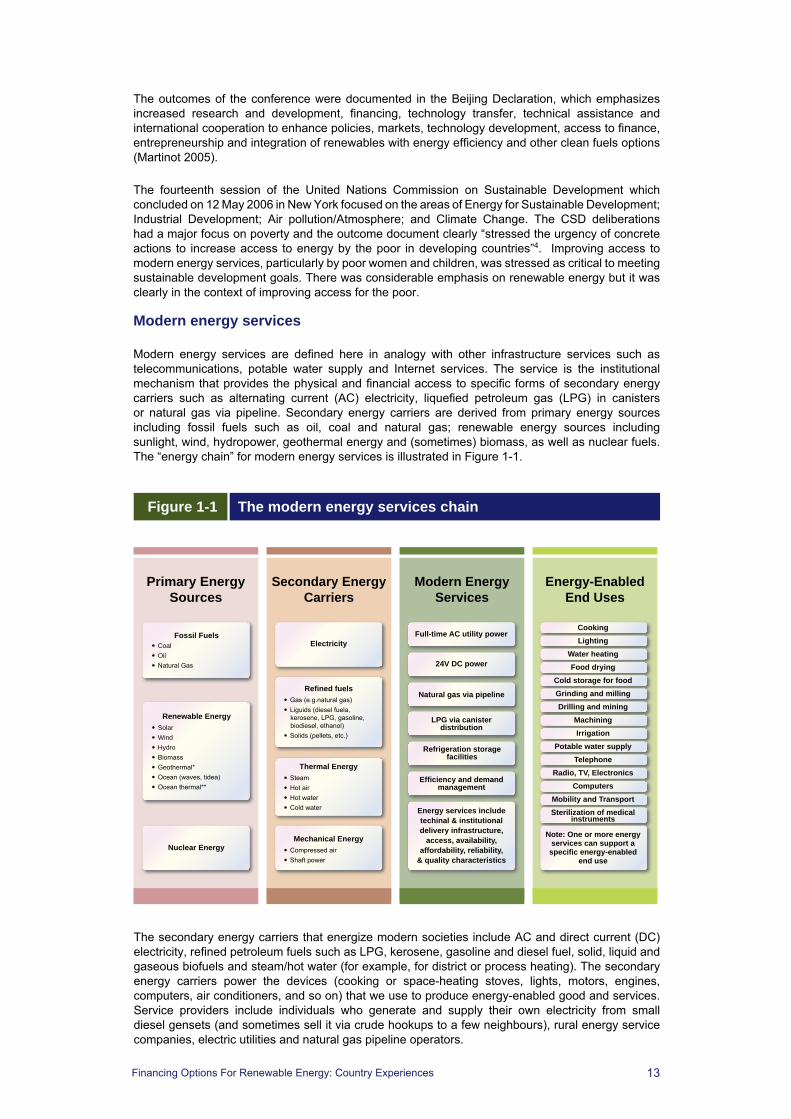

Modern energy services 13

The links among energy and development 16

Scaling up access to modern energy services 17

The UNDP-Winrock study 17

Structure of the document 18

2. Approach and Methodology 21Study approach 21

Global assessment 24

Regional assessment 26

National assessments 26

In-depth case studies 28

Scope and limitations of the study 28

3. Private Sector Investment in Renewable Energy 30Introduction 30

Decentralized renewable energy markets and applications 31

Growth in renewable energy markets 35

Trends in costs of energy produced by RETs 49

Growth trends in renewable energy markets in Asia and the Pacific 54

Emerging RET markets in Asia and the Pacific 57

Patterns of growth in RETs 58

Commercialization models for private investment in off-grid solar home sytems and household biogas 62

4. Barriers to Private Investment in Renewable Energy Technologies and Barriers to Access by the Poor 64Barriers to private investment in renewables 64

Barriers to RET access by the poor 68

V

5. Development drivers, policies and strategies in the markets for renewable energy technologies 76 Drivers and motivations 76

Mapping RET policies in Asia and the Pacific 87

Major renewable energy policy initiatives in the Asia and Pacific region 102

Regional programmes and initiatives to support private-sector investment in RETs 103

6. Experience With Models of RET Dissemination Led By The Private Sector 106Full commercialization models 106

Commercialization supported by civil society 107

Public-private involvement in community-based renewable energy systems 111

Teaming up with large IPPs – innovative public-private partnerships 114

The role of Government and national utilities in building markets for renewable energy through grid access laws and tariff setting 116

Fully subsidized arrangements 116

Financing renewable energy technologies 116

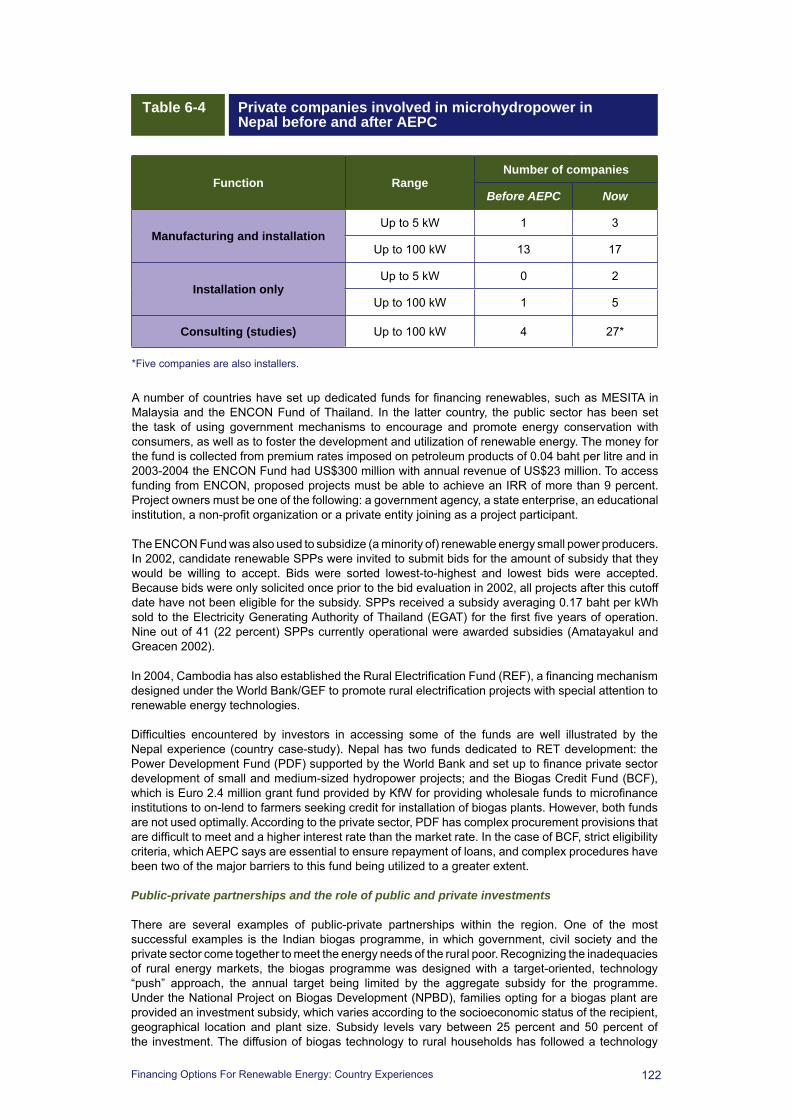

Conclusions on private and public involvement in RET dissemination 123

7. Renewable Energy & Poverty Reduction 126Poverty reduction impacts of RETs 126

Impacts on other MDGs 136

Energy access and energy security for the poor 139

Lessons learned 143

Facilitating the links among renewable energy, private investment and poverty reduction 148

8. Conclusions & Recommendations 156Summary of what is happening 156

Future directions 162

Future role of UNDP 174

Current status of private RET investment initiatives and next steps to increase investment and benefit the poor 176

References 180

VI

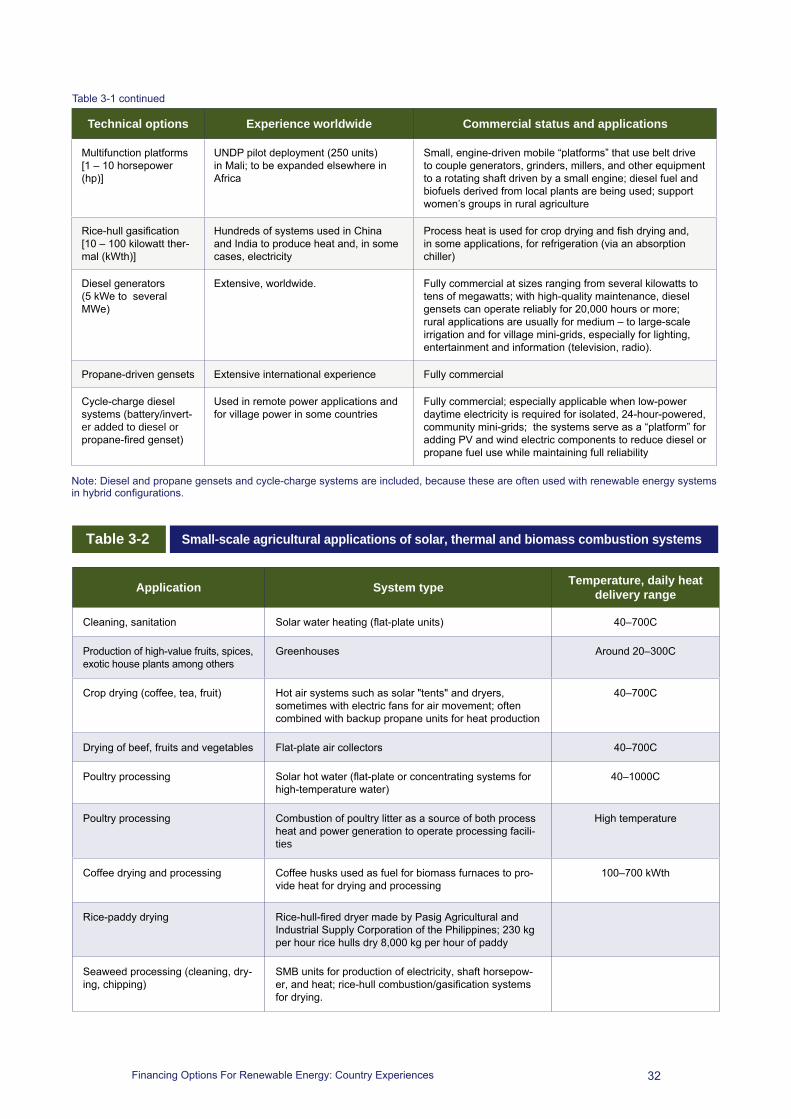

List of Tables, Figures and BoxesTablesTable 1-1 The Millennium Development Goals and modern energy services 15Table 2-1 Energy security 22Table 2-2 Questions addressed by case studies on the impact of RETs on MDGs 23Table 2-3 Meeting MDG targets 25Table 3-1 Renewable energy options for productive applications in off-grid areas 31

Table 3-2Small-scale agricultural applications of solar, thermal and biomass combustion systems 32

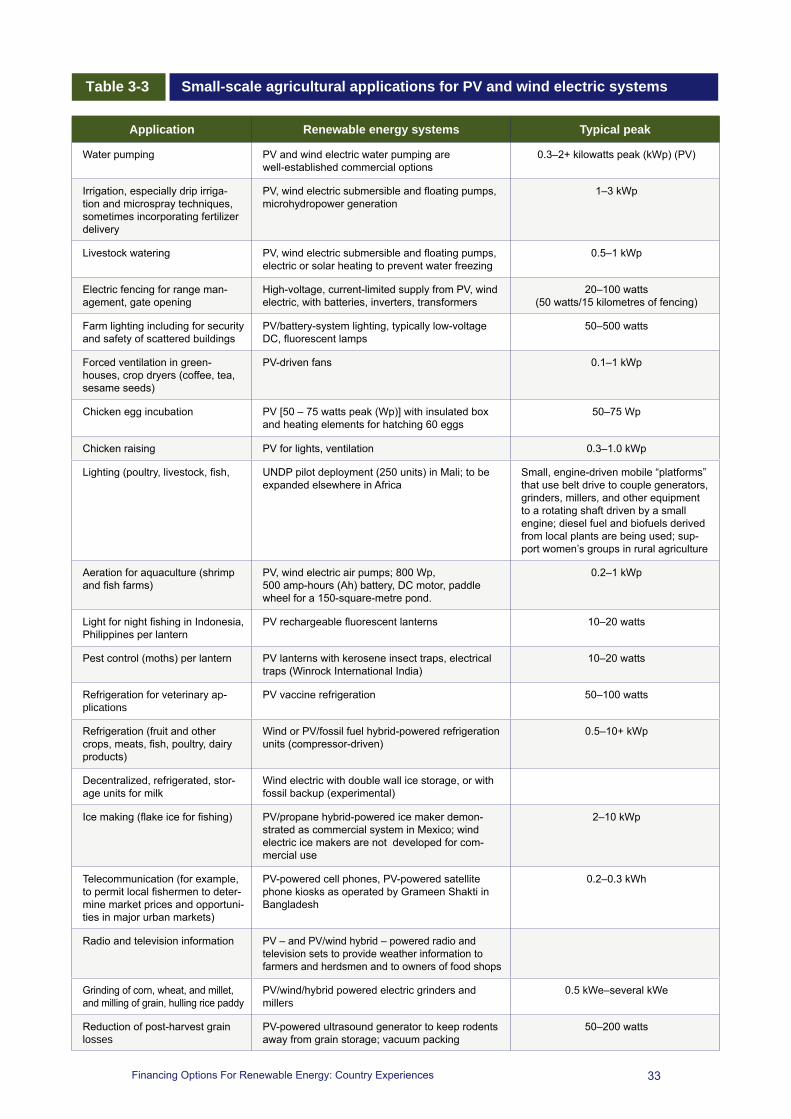

Table 3-3 Small-scale agricultural applications for PV and wind electric systems 33Table 3-4 Applications of renewable energy systems to community services 34Table 3-5 Electricity supply options for households and other free-standing facilities 34

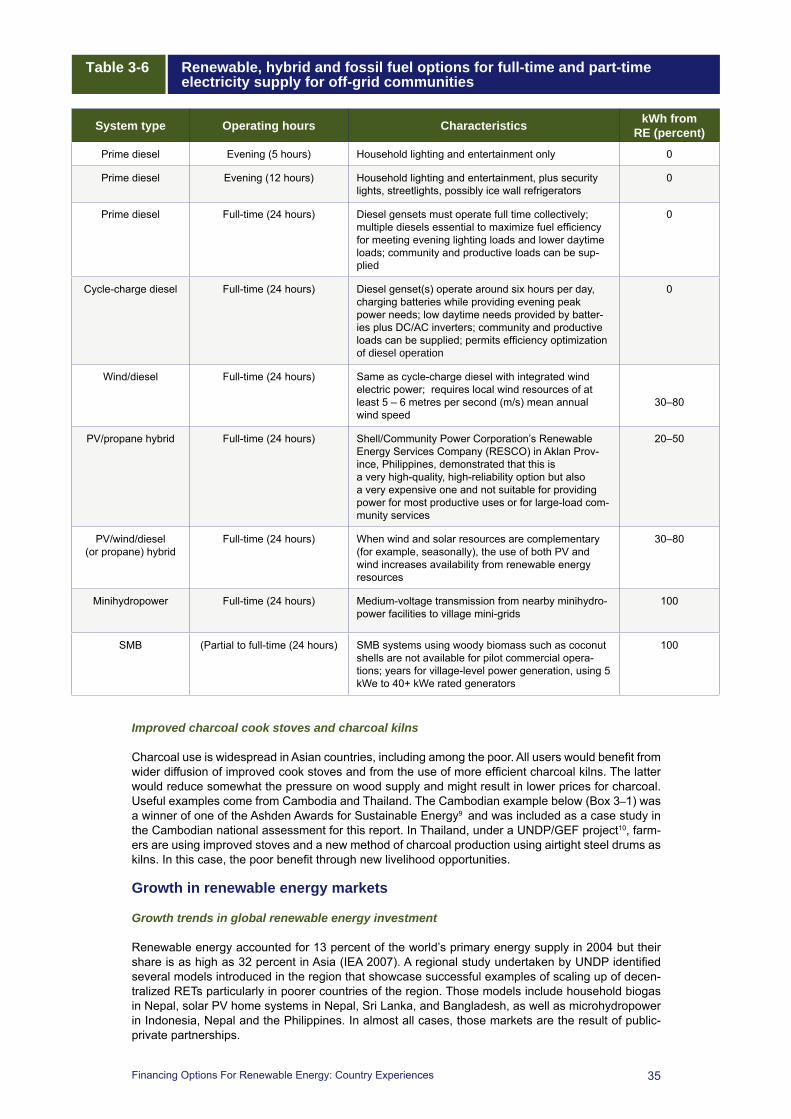

Table 3-6Renewable, hybrid and fossil fuel options for full-time and part-time electricity supply for off-grid communities 35

Table 3-7 Global capacities for renewable energy in power generation, GW 38Table 3-8 Global use of renewable energy for heating 41Table 3-9 Range of investment and generating costs, 2002 and 2010 48Table 3-10 Estimated decreases in capital costs for various technologies, 2004─2015 48Table 4-1 Key indicators of income and human poverty 70Table 4-2 Share of energy expenditures in household income (Percent) 72Table 4-3 People relying on biomass for cooking and heating in developing countries, 2000 73Table 5-1 Summary of likely scenarios for RET investment in case-study countries 81

Table 5-2Commitments made by case-study countries to RETs in their Initial National Communications to the UNFCCC 86

Table 5-3 Asian countries with renewable energy targets 90

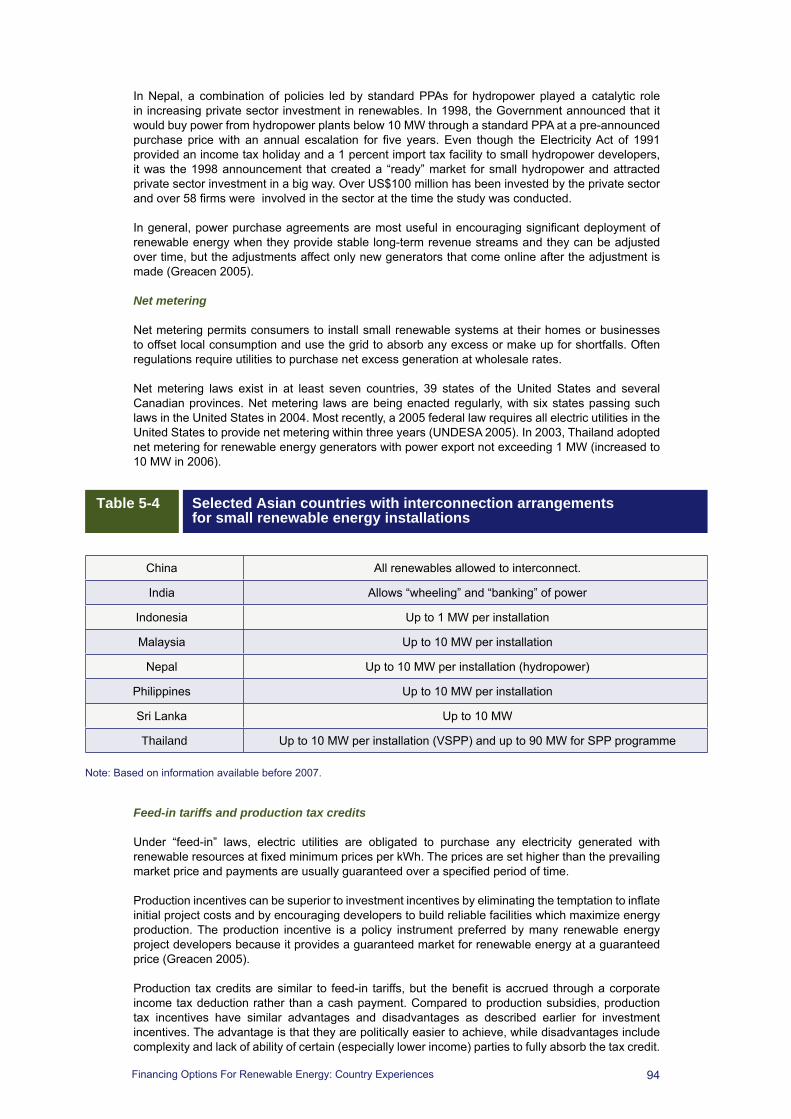

Table 5-4Selected Asian countries with interconnection arrangements for small renewable energy installations 95

Table 5-5Selected Asian countries with interconnection arrangements for small renewable energy installations 96

Table 5-6 Major renewable energy policy initiatives in selected Asian and Pacific countries 98Table 5-7 Summary matrix of energy policies in selected Asian countries 100Table 6-1 Private companies involved in solar PV in Sri Lanka before and after RERED 109

Table 6-2Increase in number of private companies involved in solar electricity in Bangladesh 110

Table 6-3 Elements of the TERI-NTPC model 115Table 6-4 Private companies involved in microhydropower in Nepal before and after AEPC 122Table 7-1 Monetary savings accruing to households from the use of RETs (Dollars per year) 127Table 7-2 Evidence from case studies on RETs and productive uses of energy 129Table 7-3 Summary of electrification benefits for rural Philippine households, 1998 131Table 7-4 Summary of poverty reduction impacts of RETs 136Table 7-5 Energy and rural household applications in India 139Table 7-6 Ownership patterns of RETs 140Table 7-7 Sustainability of RET delivery models 144Table 7-8 Addressing the MDGs with renewables 145Table 8-1 Policy recommendations for case study countries 163Table 8-2 Asian and Pacific countries by energy typology 164

Table 8-3Policy recommendations for Asian and Pacific countries to increase investment in RETs and energy access for the poor 166

Table 8-4Current status of private RET investment initiatives in Asia and the Pacific, future steps and the role of UNDP 177

VII

FiguresFigure 1-1 The modern energy services chain 13Figure 3-1 Global renewable energy installations, end-2006(GW) 37Figure 3-2 RET-based power generation capacity in developing countries, end-2006 37Figure 3-3 Renewable energy power capacity (GW) in developing countries, 2004-2006 38Figure 3-4 Leading countries using renewable energy for power generation in 2007 39Figure 3-5 Solar PV, existing world capacity, 1995-2007 39Figure 3-6 Wind power, existing world capacity, 1995-2007 39Figure 3-7 Biomass heating in developing countries of Asia 41Figure 3-8 Global solar water-heating installations, excluding pool systems, 1998–2004 42Figure 3-9 World ethanol and biodiesel production, 2000-2007 44Figure 3-10 Global fuel ethanol production, 2000 and 2005 44Figure 3-11 Comparison of diesel and biodiesel prices, 2007-2020 44Figure 3-12 Weekly prices for vegetable oils at Rotterdam, January 2006 to May 2007 45Figure 3-13 Projected growth of clean energy, 2006-2016 (billions of dollars) 47Figure 3-14 Cost comparison of off-grid renewable systems versus gasoline gensets,

lower cost trends, 2004-201550

Figure 3-15 Cost comparison of off-grid renewable systems versus gasoline gensets, most probable cost trends, 2004-2015

50

Figure 3-16 Cost comparison of off-grid renewable systems versus gasoline gensets, higher cost trends, 2004-2015

51

Figure 3-17 Cost comparison of off-grid renewable systems versus diesel gensets, lower cost trends, 2004-2025

51

Figure 3-18 Cost comparison of off-grid renewable systems versus diesel gensets, most probable cost trends, 2004-2015

51

Figure 3-19 Cost comparison of off-grid renewable systems versus diesel gensets, higher cost trends, 2004-2015

52

Figure 3-20 Cost comparison of mini-grid renewable systems versus diesel gensets, lower cost trends, 2004-2015

52

Figure 3-21 Cost comparison of mini-grid renewable systems versus diesel gensets, most probable cost trends, 2004-2015

53

Figure 3-22 Cost comparison of mini-grid renewable systems versus diesel gensets, higher cost trends, 2004-2015

53

Figure 3-23 Producer gas compared with other fuels for heating, India, 2004 56Figure 4-1 Linkages between energy and poverty reduction 69Figure 4-2 Global energy poverty 69Figure 4-3 Share of rural and urban population with access to electricity, by region 72Figure 4-4 Fuel for cooking in Phnom Penh 73Figure 4-5 Cooking fuels used in rural areas 74Figure 5-1 Carbon market share by renewable energy technology in Asia, April 2008 83Figure 5-2 CDM market share by country, April 2008 83Figure 7-1 Household income level and annual expenditure on energy 127

BoxesBox 3-1 The Cambodian Fuelwood Saving Project* 36Box 3-2 Future oil price scenarios 50Box 5-1 Rural electrification – a right of citizenship? 91Box 5-2 The electricity feed-in law of Germany* 96Box 6-1 Debt finance for renewable energy projects* 117Box 7-1 Poverty impacts of the Nepal Rural Energy Development 133Box 7-2 Benefits of a microhydropower scheme 133Box 7-3 Himalayan Light Foundation 134Box 7-4 Electricity empowers schools and clinics in the war on major diseases 136Box 7-5 Empowering rural women – lessons from REDP 139Box 7-6 Measures to extend RETs to the poor led by the private sector 141Box 7-7 A flawed renewable energy initiative in the Solomon Islands 145Box 7-8 The private sector and poverty reduction 147

I

AC alternating current ADB Asian Development Bank AEPC Alternative Energy Promotion Center, Nepal AfDB African Development Bank ah amp-hour AIT Asian Institute of Technology AKRSP Aga Khan Rural Support Programme APEC Asia-Pacific Economic Cooperation ARECOP Asia Regional Cookstove Program ARTI Appropriate Rural Technology Institute, India ASEAN Association of Southeast Asian Nations BCSE Business Council for Sustainable Energy, Australia BOS balance of system BRAC Bangladesh Rural Advancement Committee BSP Biogas Support Programme, Nepal BTU British thermal units CDM Clean Development Mechanism CER Certified Emission Reduction CFSP Cambodian Fuelwood Saving Project COGEN EC-ASEAN Programme on Technology Transfer for Energy Cogeneration from

Biomass in ASEAN countries CORE Council of Renewable Energy for the MekongCRT Centre for Rural Technology, Nepal CSD United Nations Commission on Sustainable Development DANIDA Danish International Development Agency DC direct current DEDE Department of Alternative Energy Development and Efficiency, Thailand DFID Department for International Development, United Kingdom EBRD European Bank for Reconstruction and Development EC European Commission EJ exajoule ENCON Energy Conservation Promotion Fund, Thailand EPPO Energy Policy and Planning Office, Thailand ESD Energy Service Delivery programmeESMAP Energy Sector Management Assistance Program EU European Union FAO Food and Agriculture Organization of the United Nations G8 Group of Eight GDP gross domestic product GEF Global Environment Facility GERES Groupe Energies Renouvelables, Environnement et Solidarités GHGs greenhouse gases GNESD Global Network on Energy for Sustainable Development GTG Global Transition Group GVEP Global Village Energy Partnership

Abbreviations and Acronyms

II

GW gigawatts GWEC Global Wind Energy Council GWth gigawatt thermalHDI human development index HIV/AIDS Human immunodeficiency virus/Acquired immunodeficiency syndrome HLF Himalayan Light Foundation hp horsepower HPI human poverty index ICSs improved cook stoves ICTs information and communications technologies IDB Inter-American Development Bank IDCOL Infrastructure Development Company Limited, Bangladesh IDEA Integrated Development Association, Sri Lanka IDS Institute of Development Studies IEA International Energy Agency IFC International Finance Corporation ILO International Labour Organization IREDA India Renewable Energy Development Agency IRR internal rate of return ITDG Intermediate Technology Development Group, Sri Lanka JICA Japan International Cooperation Agency JPOI Johannesburg Plan of Implementation KfW German Development Finance Group (Kreditanstalt für Wiederaufbau) kgoe kilogram of oil equivalentkWe kilowatt electric kWh kilowatt hours kWp kilowatts peak LED light-emitting diode LPG liquefied petroleum gas MDGs Millennium Development Goals MESITA Malaysia Electricity Supply Industry Trust Account MFI microfinance institutionMJ megajoule MRC Mekong River Commission MW megawatts MWe megawatts electric MWp megawatt peak NGOs non-governmental organizations NREL National Renewable Energy Laboratory, United States of America NTPC National Thermal Power Corporation, India OAS Organization of American States ODA Official Development Assistance OECD Organization for Economic Cooperation and Development PPA power purchase agreement PREGA Promotion of Renewable Energy, Energy Efficiency and Greenhouse Gas

AbatementPRSP Poverty Reduction Strategy PaperPV photovoltaic PVPS Photovoltaic Power Systems programme R&D research and development RD&D research, development and demonstrationRE renewable energy

III

REBF Renewable Energy Business Fund, Malaysia RECs Renewable Energy Credits REDP Renewable Energy Development Programme REE Rural Electricity Enterprises, Cambodia REED Rural Energy Enterprise Development REEEP Renewable Energy and Energy Efficiency Partnership REN21 Renewable Energy Policy Network for the 21st Century RERED Renewable Energy for Rural Economic Development REREDP Rural Electrification and Renewable Energy Development Project RESCO Shell/Community Power Corporation Renewable Energy Services Company RETs renewable energy technologies RPS renewable portfolio standards RWEDP Regional Wood Energy Development Programme in AsiaSAARC South Asian Association for Regional Cooperation SAREC South Asia Regional Energy Coalition SARI/Energy South Asia Regional Initiative for Energy SEEDS Sarvodaya Economic Enterprises Development Services, Sri Lanka SEFI Sustainable Energy Finance Initiative SEI Stockholm Environment Institute SELCO Solar Energy Light Company, India SHSs solar home systems SIDA Swedish International Development Cooperation Agency SMB small modular biopower SME small and medium-sized enterprise SMMEs small, medium-sized and microenterprises SNV Netherlands Development Organization SPP small power producer SWERA Solar and Wind Energy Resource Assessment TERI The Energy and Resources Institute, India UNCED United Nations Conference on Environment and Development UNDESA United Nations Department of Economic and Social Affaris UNDP United Nations Development Programme UNEP United Nations Environment Programme UNESCAP United Nations Economic and Social Commission for Asia and

the Pacific UNESCO United Nations Educational, Scientific and Cultural Organization UNFCCC United Nations Framework Convention on Climate Change UNICEF United Nations Children’s Fund UNIDO United Nations Industrial Development Organization USAID United States Agency for International Development VAT Value added taxVSPP very small power producer WEG wind electric generator WHO World Health Organization Wp watts peak WSSD World Summit on Sustainable Development SEI Stockholm Environment Institute SELCO Solar Energy Light Company, India SHSs solar home systems SIDA Swedish International Development Cooperation Agency SMB small modular biopower

IV

SME small and medium-sized enterprise SMMEs small, medium-sized and microenterprises SNV Netherlands Development Organization SPP small power producer SWERA Solar and Wind Energy Resource Assessment TERI The Energy and Resources Institute, India UNCED United Nations Conference on Environment and Development UNDESA United Nations Department of Economic and Social Affaris UNDP United Nations Development Programme UNEP United Nations Environment Programme UNESCAP United Nations Economic and Social Commission for Asia and

the Pacific UNESCO United Nations Educational, Scientific and Cultural Organization UNFCCC United Nations Framework Convention on Climate Change UNICEF United Nations Children’s Fund UNIDO United Nations Industrial Development Organization USAID United States Agency for International Development VAT Value added taxVSPP very small power producer WEG wind electric generator WHO World Health Organization Wp watts peak WSSD World Summit on Sustainable Development

V

Glossary of Financing TermsBondBonds are issued by governments, companies, other entities and individuals in return for cash from lenders andinvestors. The borrower pays interest to the lender or investor throughout the life of the bond. Borrowers seeking funds from the public through bond issues and spell out the details in a prospectus available from stock markets, banks etc. Bonds are generally medium to long-term fixed-interest securities.

Bond marketBond market is the market for trading bonds. Bond trading is carried out by phone and computer by organizations such as professional bond brokers and dealers, banks, investment banks and life assurance companies.

Corporate financingCorporate financing refers to financing a company where lenders would have full recourse to all assets and revenues of that company rather than only the project account. It is also term as balance sheet financing. Lenders in a corporate financing arrangement look to the cash flow and assets of the entire company to service the debt and to provide security.

Consumer financingConsumer financing is a loan made available to individuals, generally through hire purchase, personal loans, credit cards and other similar arrangements. It is also called consumer credit.

DebenturesDebentures are a type of fixed-interest security issued by borrowing companies in return for medium and longterm finance. Debenture-holders’ funds are invested with the borrowing company as secured loans, with the security usually in the form of a fixed or floating charge over the assets of the borrowing company. Debentures are issued for fixed periods but can be sold before maturity at a discount.

Debt financingDebt financing refers to funds loaned to the project company by financiers such as commercial banks, insurance and pension funds and multinational institutions. Financiers receive payments for principal and interest on the loans whether the company makes or loses money.

Equity financingEquity financing refers to funds put into the project company by shareholders of the company. Equity holders are owners of the company and they receive a return on their equity investment based on net profit as dividends as well as capital gains.

VI

Mezzanine financeMezzanine finance is a borrowing that falls between straight debt and equity, such as subordinated debt or equitylinked bond issues. Mezzanine debt generally has a higher risk and potential return than senior debt but a lower risk and potential return than equity. It is often provided by specialist investors in mezzanine finance such as venture capital funds or leveraged buy-out funds.

MicrofinanceThe definition of microfinance covers all mechanisms to provide financial services to the poor that includes microcredit, microsavings, micro-insurance and money transfer.

Preferred sharesShares which rank ahead of ordinary shares for the purposes of claiming dividend payments or any assets of the company should it be liquidated. Preferred shares rank behind debentures.

Project financingProject financing refers to financing for any particular type of project viewed as assets of the project company. In such arrangements, the project’s assets and its cash flow secure the debt and lenders do not have recourse to other assets of the company.

RefinancingRefinancing refers to applying for a secured loan intended to replace an existing loan secured by the same assets. Refinancing may be undertaken to reduce interest costs (by refinancing at a lower rate), to pay off other debts, to reduce one’s periodic payment obligations (sometimes by taking a longer-term loan), to reduce risk (such as by refinancing from a variable-rate to a fixed-rate loan) and/or to liquidate some or all of the equity that has accumulated in real property during the tenure of ownership.

Senior debtDebt ranked ahead of other debt. It has priority if debt has to be redeemed in cases of liquidation.

Subordinate debtA type of debt which ranks behind other debts should a company be liquidated. Typical providers of subordinated debt are major shareholders or a parent company. Subordinated debt offers advantages similar to increased capital but with greater flexibility in that the subordinated debt can be repaid fairly easily.

Venture capitalVenture capital is capital provided by outside investors for financing of new, growing or struggling businesses. Venture capital investments generally are high risk investments but offer the potential for above average returns.

1Financing Options For Renewable Energy: Country Experiences

Executive Summary

Energy is the invisible element in the Millennium Development Goals (MDGs). Although not explicitly discussed in the original formulation of the goals, without access to modern energy services they cannot be achieved. A world in which over a third of the human population lives in poverty is neither equitable nor just, nor is it likely to be sustainable.

Access to reliable, affordable, high-quality energy services makes it possible for the poor to increase incomes and obtain better education and health services. It also provides the energy underpinning of the small and medium-sized enterprise (SME) sector which is the engine of economic development in both developing and developed countries. While the source of the energy service may be unimportant to the poor, renewables are a subset of the options for producing modern forms of the energy that is needed as an input to increased and diversified incomes.

Poverty is a complex human condition, defined in many ways. The human development index (HDI) and the human poverty index (HPI) developed by the United Nations Development Programme (UNDP) provide consistent statistical measures of overall human development. However, some of the central components of poverty are missing from or inadequately captured in the indices. Among these is the lack of or difficulty in gaining access to infrastructure including energy services.

Trying to evaluate the impact on poverty of access to services derived from renewable energy (RE) and to renewable energy technologies (RETs) is very difficult because poverty reduction is the consequence of many factors and many inputs to communities and families and individuals. We show through examples that there are several ways in which availability of RETs and RE-derived energy services results in increased income, better health, improved education and knowledge, and so forth. What is more difficult to demonstrate is a clear causal link between expanded availability and use of renewables and improved conditions among the poor. We know that the relatively better off among the poor have resources that permit some access to modern energy services in many cases, while people living in extreme poverty typically do not, unless they happen to be in communities that help to provide access to vital services to their poorest members. For this reason, scaling up access and scaling up the use of renewables, within the context of expanded access, are considered as separate but related goals by, for example, the World Bank. As noted in a recent study, “...if the primary objective is to meet the energy needs of the unserved and underserved populations, neither the optimal solution nor the most equitable solutions will be found if their energy options are restricted to renewable sources ...” (Ramani and Heijndermans 2003).

This study reviewed the role of private sector investment and financing for renewable energy technologies in meeting the needs of the poor. It was organized along two tracks: (a) the role of renewable energy in enhancing the security of modern energy services for the poor; and (b) the contribution of renewable energy technologies to progress towards achieving the MDGs.

Trends in renewable energy investment were identified both globally and regionally. Policies, programmes and initiatives in the region were examined to assess their effectiveness in increasing investment in renewable energy. Specific studies were carried out in six countries to understand if that investment was able to increase access to modern energy services for the poor and to assess its contribution to reducing income and human poverty, as well as to the environment.

The major findings of this study are that substantial investment is taking place in both production capacity for renewable energy equipment and in renewable energy projects worldwide but mainly in the rich countries of the North and a few large, developing countries such as China and India. The investment is principally focused on grid-based renewables and biofuels and is driven by concerns about energy security, the rising price of oil and, increasingly, climate change. In most developing countries in the Asia and Pacific region, other than in China and India, total investment in renewables

“Poverty is the absence of all human rights. The frustrations, hostility and anger generated by abject poverty cannot sustain peace in any society. For building stable peace we must find ways to provide opportunities for people to live decent lives.”

Muhammad Yunus, founder of the Grameen Bank and Nobel Peace Prize laureate, Nobel Lecture, Oslo, 10 December 2006

2Financing Options For Renewable Energy: Country Experiences

has been modest and has not been able to make a significant impact on poverty reduction. However, in recent years there has been substantial new investment in large-scale production of photovoltaic (PV) modules of 50-100 megawatts (MW) per year new capacity in Asia, including in China, India, Malaysia, Philippines and Thailand. None of this investment is explicitly linked with poverty reduction initiatives but the potential for lower costs for PV systems available locally can facilitate production of small, affordable lighting units for relatively poor small entrepreneurs and households.

UNDP has several financial and technical assistance instruments available that can support pathbreaking initiatives which in turn can lead to larger-scale renewable energy production and project investment and lending by the multilateral development banks, host countries, and industry. They include two Thematic Trust Funds, namely Energy and Environment for Sustainable Development, earmarked for US$100 million over four years starting in 2007, and Poverty Reduction which are now available to support the expanded application of renewable energy for poverty alleviation and development.

Several low income countries have been able to increase the number of off-grid renewables, such as solar home systems (SHSs) and household biogas units, quite significantly through public-private partnerships. For the first time outside China, coverage of those technologies has begun to reach tens of thousands of households; in a few cases coverage has reached 5 percent of a country’s rural households. Private-sector companies have developed the modalities for supply and maintenance support to those systems. However, the technologies have not been able to reach the poor or significantly increase the incomes of users. Community-based energy systems, often using microhydropower, have been able to provide energy services more equitably and also provide sufficient power for productive end-uses. Scaling up the community-based model and others that have demonstrated the use of energy for specific livelihood enhancement applications remains a challenge.

In the evolution of off-grid renewables, a range of technological solutions is now sufficiently developed such that reliable and competitively priced energy systems, including packages for specific applications, are widely available. This is the outcome of a development process that started seriously in the 1970s and continues to this day. The commercialization models developed in the last decade have demonstrated how to get systems to large numbers of purchasers through a public-private investment model. The challenge now for development organizations is to integrate the technologies into income-generation and livelihood programmes to reduce poverty and to meet other MDGs. The report suggests how an appropriate agenda might be set for this in the coming years.

Investment trends

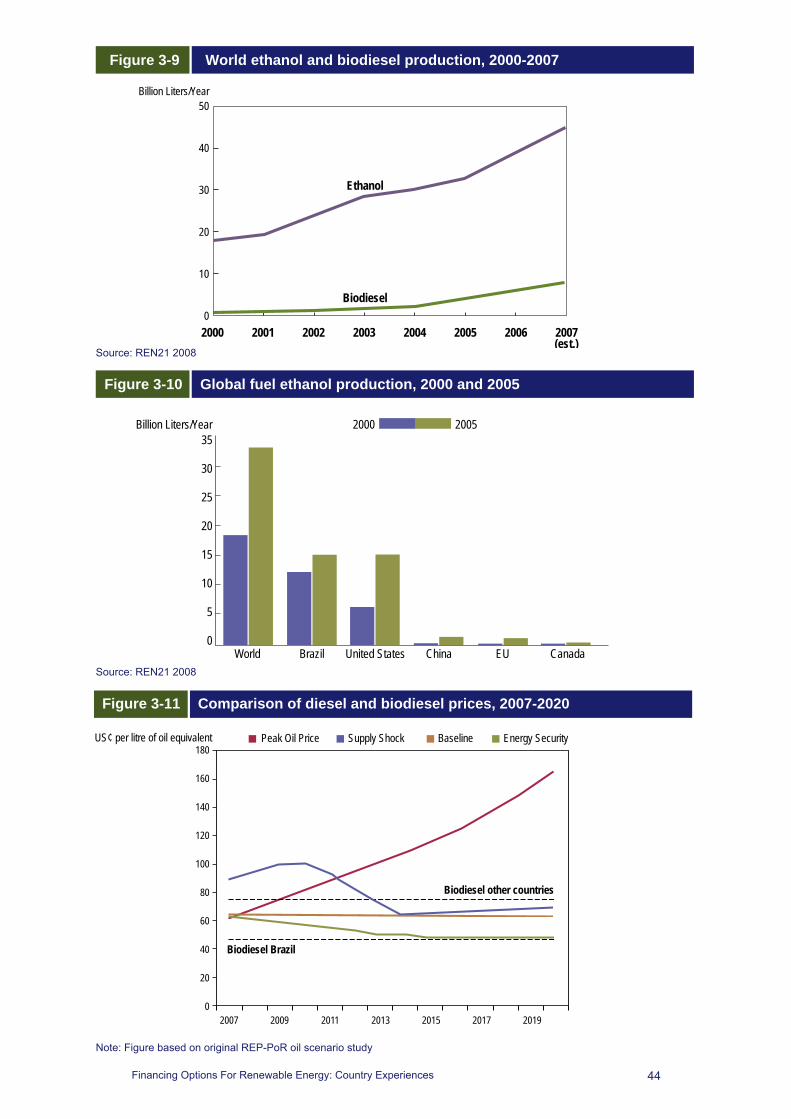

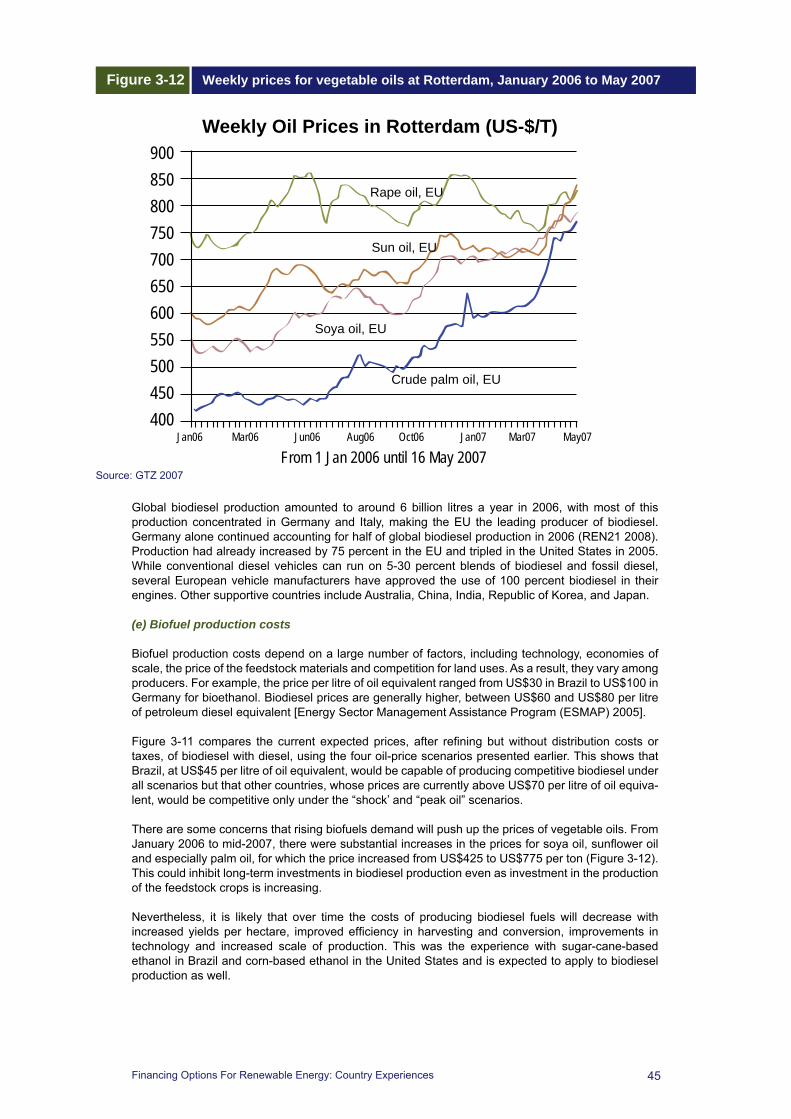

At the global level, private investment in RETs is the fastest growing among all energy sectors. Investment in RETs increased by close to 27 percent in 2004-2005, compared with 2-3 percent for fossil-fuel-based power generation and large hydropower projects. In absolute terms as well, investments are large with around US$38 billion invested in RETs in 2005 (REN21 2005). Roughly one dollar in four invested in the power sector in 2005 was invested in a RET. In 2006 and 2007 investments in RETs were around US$55 billion and US$71 billion (REN21 2008). Biofuels represent another area that has seen rapid growth in recent years. Ethanol production from sugar increased 8 percent worldwide in 2005, while biodiesel production grew 66 percent, albeit from a much smaller base. There were around US$16 billion of sales of ethanol and another US$1 billion of biodiesel in the same year.

Much of the increased investment in RETs and biofuels has been concentrated in countries that are member of the Organization for Economic Cooperation and Development (OECD) and in the larger developing countries, mainly China, India, and Brazil. Investments in RETs and bioenergy in OECD countries are driven by concerns about climate change and the need to meet Kyoto targets, as well as a desire to diversify energy supply sources away from overdependence on petroleum fuels. More recently, the high price of petroleum has become an important driver for increased investment in the production and use of RETs and biofuels.

Although the growth in RET investment in developing countries has been at half the global rate, it is at historically high levels. The growth rate could accelerate and catch up with global rates as larger developing countries, particularly China and India, have started investing heavily in the two fastest-growing RETs, wind power and solar PV, in the last few years. So far, investment in developing countries has been dominated by small hydropower and biomass generation projects. Although grid-connected renewables account for much of the investment volume, in China there is large-scale investment in solar-powered water heating and the country is now the largest producer and user of solar water-heaters in the world by far.

3Financing Options For Renewable Energy: Country Experiences

The success of the larger developing countries in increasing the percentage of renewable power on their grids is being replicated in a small number of other developing countries in the Asian and Pacific region that have established enabling regulatory and investment environments, such as standard power purchase agreements (PPAs), feed-in tariffs, net metering and the availability of bank financing for both producers and users of RE equipment. However, investment in RETs is very uneven in the region, with many of the smaller and less able countries lagging far behind the leaders in attracting such investment. The same is true for investment in biofuels.

Several renewable energy implementation models introduced in relatively poor South Asian countries have provided successful examples of the scaling up of off-grid RETs such as SHSs, household biogas units and community based microhydropower. In almost all cases, the existing markets are the result of public-private partnerships. Public investments are used to provide a partial subsidy, to enforce standards and to leverage quality control. The private sector provides the technology under warranty, as well as repair and maintenance services. Users typically pay 50-80 percent of the cost of the systems and also bear the cost of repair and maintenance. The models began with household biogas in Nepal and SHSs in Nepal and Sri Lanka, and now Bangladesh, and have been shown to be sufficiently robust to be effective in other countries as well. The challenge is to build on robust technologies and supply mechanisms and to make use of those technologies to reduce poverty.

Poverty impacts of RETs

Renewable energy technologies that are being widely disseminated through market mechanisms as described above have had a positive impact on education and health status, gender issues and on the environment. Yet they are seldom able to increase the incomes of users. This limits their take-up to the more wealthy rural elite for whom their benefits are related to consumption rather than production. For the poor to make use of those technologies, they would have to become affordable by contributing to higher incomes. As some examples below show, access to a small amount of reliable modern energy has allowed some people living in poverty to lease or own small RE systems.

Investment in grid-connected renewables in most Asian and Pacific countries contributes to poverty reduction by supplying power to often overloaded grids. Employment in the region is largely generated by agriculture and by SMEs that require reliable and affordable power from the grid to operate efficiently and profitably. This is one of the most important links between renewable energy technology and increased incomes for the poor.

Adding lower-cost power on the grid from RETs at prices isolated from petroleum prices lowers the risks of higher energy prices and improves availability of power as petroleum prices increase. Most developing countries are perpetually short of investment for grid power. This results in regular brownouts with high costs to SMEs, hurting their profitability and limiting their ability to expand and create employment. Farmers’ incomes suffer when there is insufficient power on the grid to operate pumps for groundwater irrigation during planting and other periods of high irrigation demand. Sufficient power availability on the grid is also a precondition to expansion of rural electrification. A number of studies have shown the positive impacts of access to grid power in terms of poverty reduction and meeting of MDGs.

The poor can often benefit significantly from the manufacture of some of the renewable energy equipment and devices, even if opportunities available to increase incomes from their use are limited. Off-grid renewables tend to be labour-intensive in their production, as well as in their sale and repair. Moreover, many of the skills required for manufacturing, installing, and repairing some of the equipment can be easily mastered by poor people with little training and education. Improved cook stoves (ICSs) are largely manufactured by artisans as a small enterprise, while biogas units are built by masons from within user communities.

Some of the grid-intertied renewables also provide opportunities to increase the income of the poor on the generation side. This is particularly true of rice husk and other biomass-based electricity generation projects where the raw material is often grown by poor farmers. However, despite this potential, farmers have not always been able to take advantage of those opportunities. Examples in Thailand suggest that farmers are receiving no benefits from the newly-found use of rice husks to generate power that is sold to the grid. The high global demand for biofuels in light of higher petroleum prices points to opportunities to increase employment for the rural poor in countries that can grow sugar cane and oil seeds. Here, too, the risk is that the high demand will give rise to corporate plantation farms where farmers will be reduced to selling their labour. Moreover, the need for high efficiency in production, harvesting and processing of sugar cane and oil-seed crops reduces employment opportunities for the poor, as has already happened in the most efficient sugar cane industries in, for example, Brazil and Australia.

4Financing Options For Renewable Energy: Country Experiences

Despite the successful models of commercialization leading the way to sales of large numbers of off-grid RETs, few of the purchasers of SHSs and biogas are among the poor. Moreover, only a small number of purchasers have been able to use the systems to increase income and generate employment. Again, were the technologies able to generate higher incomes, they would become affordable for the poor and there have been some examples of successful initiatives where access to RETs has increased the incomes of users. However, adopting those examples on a larger scale has proved to be difficult since some of the other elements in the production value chain differ among communities and are often absent.

It is proposed that UNDP and the development community at large make a concerted effort to link income generation into a broad range of enterprises that span agriculture, SMEs, crafts supported by non-governmental organizations (NGOs) and so on. Renewable energy technologies are now of much higher quality and private sector modalities for supplying systems to large numbers of people are in place so that such a movement can be launched.

Promising avenues for promoting the use of RETs to increase the incomes of the poor could include: (a) promotion of microfinance institutions as on-the-ground integrators of energy inputs into income-generation activities, especially if those institutions are already financing both income-generating enterprises and energy systems; (b) linking up with NGOs, Governments and bilateral and multilateral institutions engaged in initiatives focused on increasing the incomes of the poor to introduce energy services into poverty reduction programmes where they can add value; (c) linking up with SME-promotion programmes to identify where renewable energy might make a contribution; (d) strengthening private sector vendors of RETs to be able to respond to demands for applying RETs to income-generating activities; and (e) extending community-based microhydropower systems as multifunction platforms to many countries in Asia and the Pacific for productive end uses of energy.

Investment drivers

The main drivers for investment in RETs and biofuels in developing countries of the Asia and Pacific region are concerns about national energy security and the recent very high prices of petroleum. The countries that are most linked to global fuel markets have taken the biggest steps on the energy security front by investing in RETs. The supportive regulatory environment they have put in place follows from commitments many of those countries have made for meeting a certain percentage of their energy needs from renewable energy sources. Asian countries with renewable energy targets are Bangladesh, China, India, Indonesia, Japan, Lao People’s Democratic Republic, Malaysia, Pakistan, Philippines, Republic of Korea, Singapore, Thailand and Viet Nam. In addition to energy security, it is likely that concerns about local environmental pollution are also partially responsible for increased investment in renewable energy technologies, particularly in China. Although it cannot yet be considered a major driver, the Clean Development Mechanism (CDM) is increasingly being used to improve somewhat the cost competitiveness of RET investments in developing countries. Through refinements in the programmatic CDM, many small renewable energy initiatives can be combined to reduce overhead costs and to leverage higher emission credit prices than if the projects had to be considered individually. This is an area that is under rapid development but is not yet mature, with methodologies still to be fully agreed upon.

The commitment to achievement of the MDGs has not so far had a major impact on investment in renewable energy in most Asian and Pacific countries. Several countries have targets for universal electrification, which they intend to meet partially with renewables. Other countries have promoted renewables to meet local environmental challenges such as deforestation and pollution. However, the links between renewables and MDGs, while clearly demonstrated in many individual cases, has not been strongly supported in national programmes.

A recent study on the impact of rising oil prices on the poor (UNDP 2007) presents four scenarios for oil prices through the year 20151. Countries that are most linked to the global petroleum economy have already set targets for RETs and biofuels and are encouraging investment in those sectors under the baseline scenario. They are likely to continue to accelerate investment in RETs in all scenarios except if oil prices were to come down drastically and stay at those levels. Among those countries that have been slow to stimulate investment in renewables, some will be prompted into action with the shock in oil prices outlined in the supply shock scenario. However, for other countries where governance problems are significant, such as Cambodia and Solomon Islands, the peak oil scenario will have to occur before countries overcome their paralysis and put in the necessary policies and regulations and take the steps needed to attract investment.

Countries that depend on imported diesel to a large extent to produce electricity, such as many Pacific island economies which are virtually 100 percent dependent on diesel generation and Sri Lanka (56 percent), suffer increases in power tariffs when petroleum prices rise. They should have

5Financing Options For Renewable Energy: Country Experiences

the strongest incentives to invest in RETs. The first reaction of countries that have access to other fossil fuels is to invest in exploration of those fuels. Bangladesh and Pakistan will invest in new natural gas fields and they may also move to coal, as Indonesia appears to be doing. Except for Malaysia, countries with fossil fuel reserves have generally been slow in attracting investment into RETs and biofuels. Countries with a large kerosene subsidy burden for rural lighting are likely to invest in scaling up of RET access. They will also look to investment from donor countries for much of the production and use of off-grid RETs.

Barriers to investment in RETs and access for the poor

There continue to be two distinct sets of barriers to the growth of renewable energy in developing countries of the Asian and Pacific region, as elsewhere. The first set prevents sufficient private investment being attracted to RETs. The fundamental barriers in this regard include: (a) lack of awareness of the technologies and their applications among users and policy makers; and (b) lack of understanding of the sustainability aspects of installed systems. An obstacle to private sector investment in pro-poor, renewable-energy-based systems is that earning an adequate profit on that investment is difficult if not impossible. Sustainability requires technical capability to operate, maintain and repair systems but it also requires profitability. This is both an issue of technical knowledge and of having mechanisms for collecting adequate resources from users, as well as from governments and donor partners, to meet operational and maintenance costs.

In most countries there is some understanding of what can be termed “first-generation barriers” and how to overcome them, at least for some of the RETs. Those countries have had successful government-sponsored or donor-funded programmes, which have resulted in sustainable applications of RETs through a number of rounds of trial and error. Most Asian and Pacific countries today have active, private sector RET suppliers of good quality systems that are able to maintain them. However, this is not universally the case, especially among the smaller Pacific island countries, as well as countries such as Cambodia and Afghanistan that are emerging from conflict. In such countries, sustainable energy systems of high quality are hard to find and internal markets remain too small to support a technology base for RETs.

A few Asian and Pacific countries have also been able to overcome “second-generation barriers” that stand in the way of scaling up investment in RETs to supply large numbers of rural users with both equipment and modern energy services. The successful countries have been able to establish private sector suppliers that can respond to a significant increase in demand from users. They have also been able to stimulate substantial demand for RET systems from users. The principal obstacles to scaling up RETs include lack of confidence in the market on the part of suppliers and lack of confidence in product quality and long-term product support on the part of consumers. A shortage of suitable supplier, dealer and end-user financing to support meaningful scale-up is also a handicap. Countries that have been successful in bringing about a substantial scaling up in RET investment have developed modalities for a public-private partnership that typically provides for quality standards, subsidies and financing for off-grid systems.

For grid-connected renewable energy systems, the main barriers to scale-up are the absence of clear government or utility policies on feed-in tariffs and net metering, and standard power purchase agreements which have faced some resistance. Another common barrier is the inability to obtain loans from banks for financing systems. Countries that have been able to attract private investment into grid-connected renewable energy systems, such as wind, small hydropower, biomass-based and geothermal have put in place clear policies and related tariff structures and have also developed mechanisms to provide credit to investors and developers.

Insufficient financing often stands in the way of the poor gaining access to renewables, even in those countries where the first and second generation barriers mentioned earlier have been addressed. The high cost of good-quality renewable energy systems as well as lack of financing stands in the way of the poor gaining access to renewable energy equipment and RE-derived energy services. Furthermore, opportunities for the poor to increase their incomes directly through the use of energy services are limited as they often lack the necessary knowledge and resources to do so. Such obstacles can collectively be thought of as “third-generation barriers” to adoption of renewable energy technologies. There are a number of pilot programmes in countries in Asia and the Pacific that illustrate how to this set of barriers may be overcome. But addressing those issues on a country-wide scale requires focused attention and commitment on the part of both Governments and civil society, aided by development partners.

6Financing Options For Renewable Energy: Country Experiences

The way forward

Developing countries in the Asia and Pacific region need support to increase investment in renewable energy for greater energy security and reduced vulnerability to oil price increases, as well as to meet MDG targets. Global trends indicate that much of this investment will come from the private sector, often as the result of public-private partnerships. In light of global experience, including the experience of the larger countries of the region, the way forward for those developing countries might be as follows:

a) Create the environment for increased investment in grid-connected RETs. Most countries in the Asia and Pacific region have largely untapped renewable energy resources. Countries that have achieved the largest investment volumes also have transparent and well-advertised mechanisms, such as feed-in tariffs and standard power purchase agreements, for connecting small generators to the grid. They also have financial organizations that provide credit on a project finance basis. Those are essential elements of an enabling environment for attracting private investment and public-private partnerships.

b) Increase investment in biofuels but with caution. Domestic biofuels production can improve energy security for countries with large agricultural sectors or for landlocked or island states where the supply of petroleum fuels is irregular and expensive. Bioenergy crops can also generate rural employment but developing countries in the Asian and Pacific region need to understand the trade-off between energy farming and food security better. They also need support in developing models for farming bioenergy crops that are beneficial to communities particularly to ensure that local farmers obtain a fair and equitable share of the benefits. The social and environmental impacts of truly large-scale biofuels production are inadequately understood and they can be quite serious.

c) Expand models for the commercialization of RETs for households and make them more accessible to the poor. Government officials and prospective private sector investors need to take lessons from the market-based expansion of RETs such as SHSs, biogas and ICSs in countries such as Bangladesh, Nepal and Sri Lanka that have seen rapid expansion of those markets. While the World Bank has already undertaken significant initiatives in this area, it should consider investing in those models even more widely across the region as could the Asian Development Bank (ADB).

d) Replicate scale-up of community-based energy systems. Although community-based RETs such as microhydropower have been shown to provide reliable and low-cost energy in an equitable manner in a number of countries in Asia and the Pacific, the models have not been scaled up to their full potential. Approaches such as the Renewable Energy Development Programme (REDP) in Nepal and the Aga Khan Rural Support Programme (AKRSP) in Pakistan are slowly being replicated in other countries in the region. This replication needs to be accelerated, ultimately on a vast scale, so that hundreds of thousands of communities that could benefit from those systems can do so.

e) Develop a global alliance to integrate renewable energy for productive end uses. RETs must be used for generating income for the poor, if they are to become affordable. The RET community needs to form a global alliance with the larger development community to integrate energy into non-energy development projects and entry points need to be found to integrate energy into wider poverty reduction programmes. The pioneering efforts of Grameen Shakti and other organizations that have promoted productive end uses alongside sales of RETs need to be replicated widely.

f) Increase the use of renewable energy for high-value public services. There is much room for expanding the use of RETs in powering high-value public services (vaccine refrigeration, telecommunications, distance learning and Internet connectivity). An example is the rural health posts and clinics in the developing world, which are almost all without electricity and therefore limited in the services that can be provided. The participation of the private sector in providing some of those services can be increased in the interests of sustainability. The best examples are telephony and Internet connectivity services provided by the private sector for a fee.

g) Increase availability of RET finance. Banks and microfinance institutions throughout the Asian and Pacific region need to be encouraged and trained to provide financing for RETs. Finance must be made available not just to suppliers of modern energy services but also to the enterprises that will use the energy to generate income and provide employment. Financing institutions need to be encouraged to play a coordinating role to foster integration of energy inputs and income-generating activities at the enterprise and household levels.

7Financing Options For Renewable Energy: Country Experiences

h) Strengthen the role of carbon financing for RETs. The CDM executive board needs to be encouraged to provide preferential treatment for RET projects with a high MDG impact by simplifying the baseline and monitoring methodologies. This will reduce transaction costs and make it attractive for many developers to pursue RET projects under the CDM. In order to give priority to projects with high impacts on MDGs, indicators need to be developed to assess this and a methodology for monitoring such projects needs to be developed as well. The use of programmatic CDM initiatives to facilitate establishment of evolving portfolios of small renewable energy projects and programmes should be encouraged by the CDM executive board, the secretariat of the United Nations Framework Convention on Climate Change (UNFCCC) and associated agencies. This will lower the transaction costs for such projects and should result in enhanced prices for carbon emission reduction credits.

i) Changes in project monitoring procedures. In most RET programmes monitoring systems are not designed to capture poverty and gender-specific impacts. Project planning and monitoring protocols that are sensitive to those impacts need to be developed further and their widespread use encouraged. Such protocols could also be used by socially conscious buyers of carbon credits to pay higher prices for Certified Emission Reduction (CER) units from projects that also score high in terms of the MDGs.

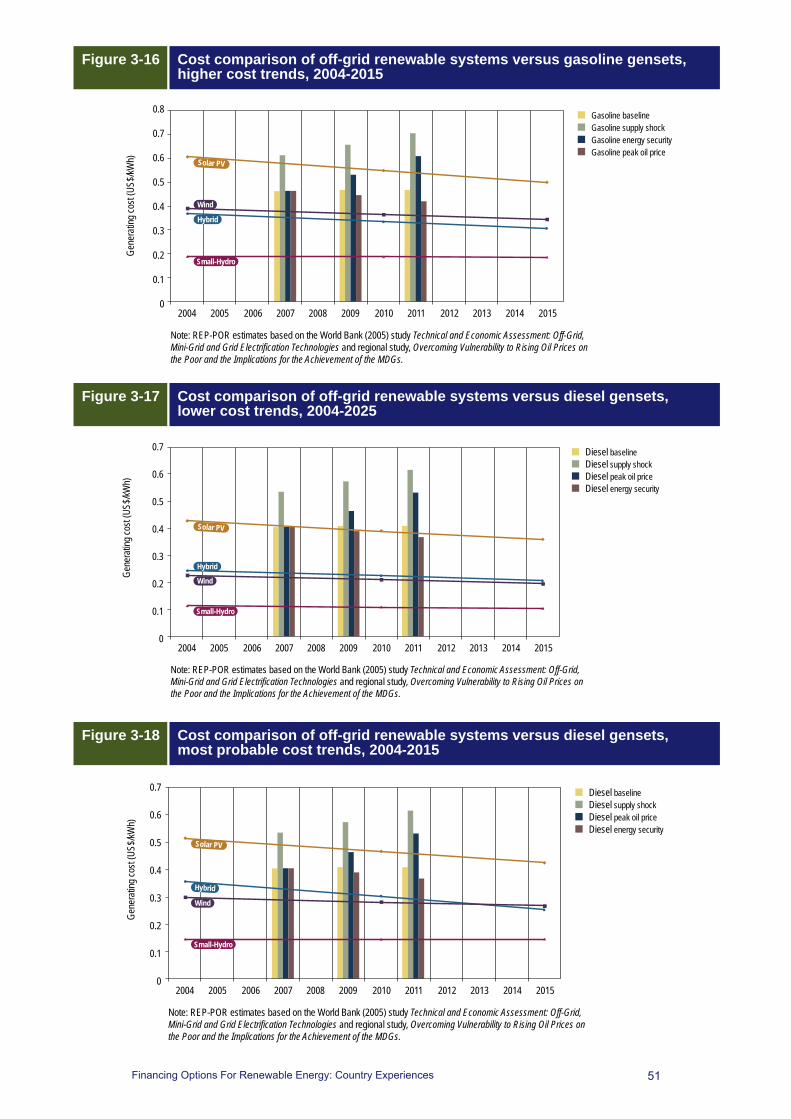

Endnotes1The “baseline’ scenario assumes prices remaining at an average of around US$70. A second “supply shock” scenario has oil prices rising to $100 and beyond in the short to medium term and declining to the baseline US$70 in the long term. A third “peak oil” scenario shows oil prices rising gradually to US$100 per barrel as supply peaks and then increasing expo-nentially thereafter. The last scenario, “energy security”, assumes reduced oil demand as a result of energy and environmental concerns with oil prices falling from the baseline value to US$50 per barrel in the medium term, remaining constant thereafter. The scenarios were defined during the study period 2006─2008.

8

1. Introduction

9Financing Options For Renewable Energy: Country Experiences

United Nations Millennium Project, available at www.unmillenniumproject.org

Background

On 8 September 2000, the United Nations General Assembly adopted the United Nations Millennium Declaration (A/RES/55/2) and established the Millennium Development Goals.

As a recent report on progress towards achievement of the MDGs in Asia and the Pacific noted, the absolute size of social and economic deprivation remains enormous. Two thirds of Asians or a total of 1.5 billion people are still without access to basic sanitation and the region has nearly three times as many underweight children and people living on less than one dollar a day as sub-Saharan Africa and Latin America combined [United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP) 2007].

Even though access to modern energy services was not included as a separate goal, it is widely acknowledged that addressing the energy and poverty linkage is essential if the MDGs are to be attained. Access to reliable, affordable, high-quality energy services helps make it possible for the poor to increase their incomes and benefit from better education and health services. Electricity or wind energy for water pumping, biogas and ICSs, as well as water milling can lessen the drudgery of women in carrying out subsistence chores – carrying water and firewood and milling grain – freeing them to take on more empowering responsibilities.

Moreover, reliable, affordable electricity and high-quality fuels provide the energy underpinning of the SME sector, which is the engine of economic development both in the developing world and in the OECD countries. Most jobs are created by SMEs and to the extent that quality energy services can facilitate expansion of profitability of those enterprises, employment can be extended to many people unable to establish ventures on their own. Consequently the links between modern energy services and reduction of poverty are often indirect. Both direct and indirect links are discussed in this report.

The global energy-poverty discourse

The interest in renewables in the 1970s was driven by the oil price shocks of 1973 and 1979, fears of depletion of fossil fuels reserves and other price-related pressures. Many national Governments launched research and development programmes and projected optimistic scenarios about what renewables could or should contribute in the years to come. There was resurgence in interest in the 1990s, the main drivers being environmental pressures, particularly climate change, and the loss of faith in nuclear energy as a desirable alternative to fossil fuels.

Since publication of the Brundtland Report in 1989, sustainable development2 represents an impor-tant element in the political debate on future environmental, economic and societal development. The work of the Brundtland Commission led directly to the United Nations Conference on Environ-ment and Development (UNCED) held at Rio de Janeiro in 1992. Energy was viewed primarily as an environmental issue, particularly in the context of climate change. It was discussed in the Agen-da 21, one of the principal non-binding intergovernmental outcomes of UNCED, which highlighted the fact that current levels of energy consumption and production are not sustainable, especially if demand continues to increase. Agenda 21 stressed the importance of using energy resources in a way that is consistent with protection of human health, the atmosphere and the natural environment.

1. IntroductionThe MDGs are the world’s time-bound and quantified targets for addressing extreme poverty in its many dimensions – income poverty, hunger, disease, lack of adequate shelter and exclusion – while promoting gender equality, education and environmental sustainability. They are also basic human rights the rights of each person on the planet to health, education, shelter and security.

10Financing Options For Renewable Energy: Country Experiences

An important milestone in the development debate took place in 2000 when leaders from across the world adopted the Millennium Development Goals. It initially appeared to be a setback for the energy sector that energy did not feature in the MDGs as a separate goal. The omission has however started a fresh debate on the energy-poverty linkage and it is increasingly being recognized that addressing that linkage is going to be a critical factor in the attainment of the Millennium Development Goals [see Table 1-1 below and Department for International Development (DFID) 2002]. Specifically:

The goal of halving poverty by 2015 cannot be reached without energy inputs to increase production, income and education; to create jobs; and to reduce the daily grind involved in survival;

• Halving hunger will not come about without energy for more productive growing, harvesting, processing and marketing of food;

• Improving health and reducing death rates will not happen without energy for the refrigeration needed for clinics, hospitals and vaccination campaigns;

• Acute respiratory infection, the major cause of infant mortality, cannot be checked until the smoke from cooking fires in rural homes is reduced;

• Universal primary education will remain a distant dream unless children have light in their homes to study in the evenings;

• Clean water will not be pumped or treated without energy;

• Rural women cannot be empowered until such time that they are freed from the onerous tasks of fuelwood and water collection; and

• Poor communities will remain most vulnerable to global warming because they lack the resources to cope with crises resulting from climate change.

Energy, which is a derived demand, provides a wide range of services that can have a positive impact on enhancing the livelihoods of people and reducing poverty. UNDP has been at the forefront of this discussion, and has been advocating the adoption of a new global target for energy as a prerequisite to fulfilling other international development targets of the MDGs. The proposed target is to halve the proportion of people without access to clean and affordable fuels and electricity by 2015 (Ramani 2003).

Increasing interest in the expanded use of renewable energy was also demonstrated in the Group of Eight (G8) Renewable Energy Task Force Report issued in 2001, which stressed the need to give priority to efforts to develop renewable energy markets, particularly in the industrialized countries. The underlying expectation was that this would lead to a decrease in costs and thus open the way for use of renewable energy in developing countries.

The ninth session of the Commission on Sustainable Development (CSD) in 2001 was an important landmark in the energy-poverty debate. With energy as one of the major themes, countries at CSD-9 agreed that stronger emphasis should be placed on the development, implementation and transfer of cleaner, more efficient energy technologies and that urgent action is required to further develop and expand the role of alternative energy sources. The Governments of the world concluded: “To implement the goal accepted by the international community to halve the proportion of people living on less than US$1 per day by 2015, access to affordable energy services is a prerequisite”3.

The follow-up international event, the World Summit on Sustainable Development (WSSD), held in 2002, brought discussions on energy to the centre of the global development debate. The WSSD gave new impetus to global action to fight poverty and protect the environment. The agenda for sustainable development was broadened, emphasizing particularly the linkages among poverty, the environment and the use of natural resources. The following important commitments related to energy and the environment were made at the summit (World Bank 2004):

Access to energy – Improve access to reliable, affordable, economically viable, socially acceptable and environmentally sound energy services and resources, sufficient to achieve the Millennium Development Goals, including the goal of halving the proportion of people in poverty by 2015

Renewable energy – Diversify energy supply and substantially increase the global share of renewable energy sources in order to increase its contribution to total energy supply.

11Financing Options For Renewable Energy: Country Experiences

Energy efficiency – Establish domestic programmes for energy efficiency with the support of the international community. Accelerate the development and dissemination of energy efficiency and energy conservation technologies, including the promotion of research and development.

Energy markets – Remove market distortions, including through the restructuring of taxes and the phasing out of harmful subsidies. Support efforts to improve the functioning, transparency, and information about energy markets with respect to both supply and demand, with the aim of achieving greater stability and ensuring consumer access to energy services.

An outcome of the WSSD was the adoption of the Johannesburg Plan of Implementation (JPOI) in which energy was addressed in the context of sustainable development. The JPOI stressed that access to reliable and affordable energy services facilitates the eradication of poverty and made specific recommendations on energy access to facilitate the achievement of the MDGs and established a clear link between energy and the eradication of poverty. The importance of producing, distributing and consuming energy services in ways that support sustainable development is also emphasized in relation to changing patterns of production and consumption as well as protecting and managing the natural resource base. The JPOI aims to promote the integration of the three components of sustainable development – economic development, social development and environmental protection – as interdependent and mutually reinforcing pillars. Among other things, the JPOI calls for action to:

• Improve access to reliable, affordable, economically viable, socially acceptable and environmentally sound energy services;

• Recognize that energy services have positive impacts on poverty eradication and the improvement of standards of living;

• Develop and disseminate alternative energy technologies with the aim of giving a greater share of the energy mix to renewable energy and, with a sense of urgency, substantially increase the global share of renewable energy sources;

• Diversify energy supply by developing advanced, cleaner, more efficient and cost-effective energy technologies;

• Combine a range of energy technologies, including advanced and cleaner fossil fuel technologies, to meet the growing need for energy services;

• Accelerate the development, dissemination and deployment of affordable and cleaner energy efficiency and energy conservation technologies, as well as the transfer of such technologies to developing countries; and

• Take action, where appropriate, to phase out subsidies in this area that inhibit sustainable development.

The WSSD also saw the launch of many partnerships between industrialized and developing countries to promote sustainable development with a focus on energy. In relation to energy, a total of 39 partnerships to promote sustainable energy programmes in developing countries were presented to the United Nations Secretariat for WSSD, 23 with energy as a central focus and 16 with a considerable impact on energy (Goldemberg and Johansson 2004). Some of the key partnerships that have emerged in the energy sector include the Global Village Energy Partnership, the Renewable Energy and Energy Efficiency Partnership (REEEP), the Global Network on Energy for Sustainable Development (GNESD), the United Nations Environment Programme (UNEP) Sustainable Energy Finance Initiative (SEFI) and the Renewable Energy Policy Network for the 21st Century (REN21). REEEP and REN21 have a clear mandate to promote renewables.

At the WSSD, there was a strong effort to reach agreement on a global target on renewable energy, with some proposing that 10 percent of total energy supply should come from renewable sources by 2010, but this ran into stiff opposition and deliberations were complicated by the fact that no clear definition of renewable energy was put forward, especially concerning the role of large hydropower and biomass as sources of energy. However, it was agreed that the contribution of renewables to world energy use should be substantially and urgently increased. Increased use of renewables should be achieved by joint actions and improved efforts to work together at all levels, by public-private partnerships and by deeper regional and international cooperation in support of national efforts.

12Financing Options For Renewable Energy: Country Experiences

In the period 1998-2003, there were increased concerns about energy security (both physical security and security of supply), further emphasized by the 11 September 2001 events in New York and Washington, as well as the war in Iraq (Goldemberg and Johansson 2004). A number of countries – including Brazil, Germany and Spain and some states in the United States – adopted successful laws and regulations designed to increase the use of renewable energy sources.

The International Conference for Renewable Energies, held at Bonn on 1-4 June 2004, was attended by over 3,000 participants from 150 countries and hundreds of non-governmental and intergovernmental organizations. The conference led to formal commitments by countries and organizations to renewable energy targets, programmes and initiatives. They are encapsulated in the main outcome of the conference, the International Action Programme, which was adopted by 170 countries, with 200 actions and commitments by Governments, international organizations and non-governmental organizations to accelerate the use of renewable energies. Other outcomes adopted by the conference reconfirmed the commitment to renewables and included a Political Declaration, outlining shared goals for increasing the role of renewable energies and a joint vision of a sustainable energy future; and Policy Recommendations for Renewable Energies, to support the development of new approaches, strategies and partnerships in scaling up those technologies. The financial sector’s position statement after the Bonn conference emphasized that financial institutions, both regional and international, should play an enhanced role in financing and attracting private capital to renewable energy in emerging markets.

Perhaps the most defining development for renewables came with the ratification of the Kyoto Protocol by Russia, and its entry into force on 16 February 2005. The Protocol sets binding targets for developed countries to reduce greenhouse gas emissions by an average 5.2 percent below 1990 levels. With its entry into force, Kyoto’s emission targets become binding legal commitments for those industrialized countries that have ratified it.

Some of the more recent perspectives on renewables include the following [United Nations Department of Economic and Social Affaris (UNDESA) 2005]:

In July 2005, at the Gleneagles Summit, the G8 countries pledged to introduce innovative measures to achieve substantial reductions in greenhouse gas emissions and promote low-emitting energy systems. This pledge was supported by five major non-G8 countries, namely Brazil, China, India, Mexico and South Africa.

Also in July 2005, Australia, China, India, Japan, Republic of Korea and the United States announced the Asia-Pacific Partnership on Clean Development and Climate to promote the development and deployment of existing cleaner, more efficient technologies and practices. The partnership, which has since been joined by Canada, will be consistent with and contribute to the efforts under the UNFCCC and will complement, but not replace, the Kyoto Protocol.

The World Bank, after a five-year retrenchment, pledged to achieve 20 percent average annual growth in renewable energy and energy efficiency in the next five years, starting 2004.

Other organizations such as the Inter-American Development Bank (IDB), ADB, the African Development Bank (AfDB), the European Bank for Reconstruction and Development (EBRD), the Organization of American States (OAS) and Asia-Pacific Economic Cooperation (APEC) showed similar support for renewable energy, including for poverty reduction.

The renewable energy sector saw an emergence of new players including Fortune 500 firms, large international banks, investment houses, venture capital firms, public banking institutions, development banks and foundations investing in renewable energy projects and programmes.

The Beijing International Renewable Energy Conference took place on 7-8 November 2005 as a follow up to the Bonn Conference of 2004. The conference brought together policy makers, NGOs, companies and many others to discuss the current status of renewable energy worldwide, prospects for international cooperation (especially South-South cooperation), and efforts to monitor progress with existing international commitments and programmes. During the conference, host country China announced a target of 15 percent of total primary energy from renewables by 2020. This target includes large hydropower and represents a significant increase from today’s existing 7 percent.

13Financing Options For Renewable Energy: Country Experiences

The outcomes of the conference were documented in the Beijing Declaration, which emphasizes increased research and development, financing, technology transfer, technical assistance and international cooperation to enhance policies, markets, technology development, access to finance, entrepreneurship and integration of renewables with energy efficiency and other clean fuels options (Martinot 2005).

The fourteenth session of the United Nations Commission on Sustainable Development which concluded on 12 May 2006 in New York focused on the areas of Energy for Sustainable Development; Industrial Development; Air pollution/Atmosphere; and Climate Change. The CSD deliberations had a major focus on poverty and the outcome document clearly “stressed the urgency of concrete actions to increase access to energy by the poor in developing countries”4. Improving access to modern energy services, particularly by poor women and children, was stressed as critical to meeting sustainable development goals. There was considerable emphasis on renewable energy but it was clearly in the context of improving access for the poor.

Modern energy services