Financing offshore wind Copenhagen 4 November Marie de Graaf m.degraaf@greengiraffe.eu +31646318495 greengiraffe.eu

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financing offshore wind Copenhagen 4 November Marie de Graaf m.degraaf@green-‐giraffe.eu +31646318495 green-‐giraffe.eu

Financing offshore wind

1. GGEB introduc7on

2. How projects are financed

3. The debt market

4. Risk analysis by the lenders

5. How to approach project finance

6. What GGEB can do for you

2

Table of contents

We have an unparalleled track record in successfully closing deals for our clients

1. GGEB introduc7on – the offshore wind finance specialists

Advisor to C-‐Power to raise project finance debt

325 MW

Belgium 2010

• 19 professionals in London (UK), Paris (FR), Utrecht (NL) and Hamburg (DE)

• Project & structured finance, full scope equity advisory and contrac\ng exper\se • Focus on renewables and specifically offshore wind

Advisor to Northwind to raise project finance debt

216 MW

Belgium 2012

(Sponsor)

Advisor to WindMW to raise project finance debt

288 MW

Germany 2011

The GroupBlackstone ®

Non-‐recourse financing of 25% stake in Walney offshore wind farm

367 MW

UK 2012

(Sponsor)

Advisor to Highland in the acquisi7on of the

Deutsche Bucht project

210 MW

Highland Group Holdings

Germany

2012

Financial advisory services French offshore

wind tender

1,428 MW

France 2012

3

Financing offshore wind

1. GGEB introduc\on

2. How projects are financed

3. The debt market

4. Risk analysis by the lenders

5. How to approach project finance

6. What GGEB can do for you

4

Table of contents

2. How projects are financed

“Balance sheet” vs “non recourse finance”

Direct contractors have a direct incen7ve to understand who will be funding the project

5

Large projects are typically developed through a stand alone project company • Owned by the project investors • With its own revenues & balance sheet and thus the

ability to raise debt on its own merits

There are only two discrete sources of funding • By the owners (directly via equity or shareholder loans,

or indirectly via guarantees) • By banks without recourse to the equity investors – this

is “project finance”

The way a project is funded will have a material impact on how it deals with contractors • In a project finance deal, you need to deal with the

banks’ requirements!

Project company

Lenders Sponsor(s)

Dividends Debt service

Equity Debt

No recourse

Recourse to investors is contractually limited • Lenders rely on project revenues only Capital intensive projects requiring long term financing • Lenders need LT opera\onal performance

Lenders need to make sure that the project works on a standalone basis, with no third party commitments than those made at financial close. Such commitments must be realis;c, credible and durable, both contractually and economically This typically entails very detailed contractual frameworks and extensive due diligence

No upside

Lenders receive a fixed remunera7on • Lenders do not benefit from beeer performance Low single digits margins vs high leverage • Risks to be commensurate to remunera\on

Lenders need risks to be measurable and to have probabili;es of occurring in the low single digits for investment to make sense. Risks which are (seen as) well understood are thus easier to bear

Project finance lenders will usually have priority access to cash-‐flows (aGer certain pre-‐agreed opera;on expenses necessary to keep the project running) and security on all assets, contracts and equity of the project

2. How projects are financed – non recourse debt

6

Revenue side constraint Capital expenditure constraint

Total capital expenditures

CONSTRUCTION

Turbines

Foundations

Electricals

Installation

Insurance

Construction engineering

Development costs

FINANCE

MLA and due diligence costs

Debt fees (arranging + commitment)

Interest during construction

DSRA

Senior Debt

Equity and quasi equity

2. How projects are financed – non recourse debt

Offshore DSCR constraint: 1.50 with p50 or 1.30 with p90

• No or very limited price risk on revenue side

• Net availability number in the 90-‐92% range

• Conserva\ve O&M cost assump\ons

Debt : Equity < 70:30

• Limited tolerance for junior debt mechanisms

• Limited tolerance for pre-‐comple\on revenues

• Strong requirement for equity to be paid upfront

7

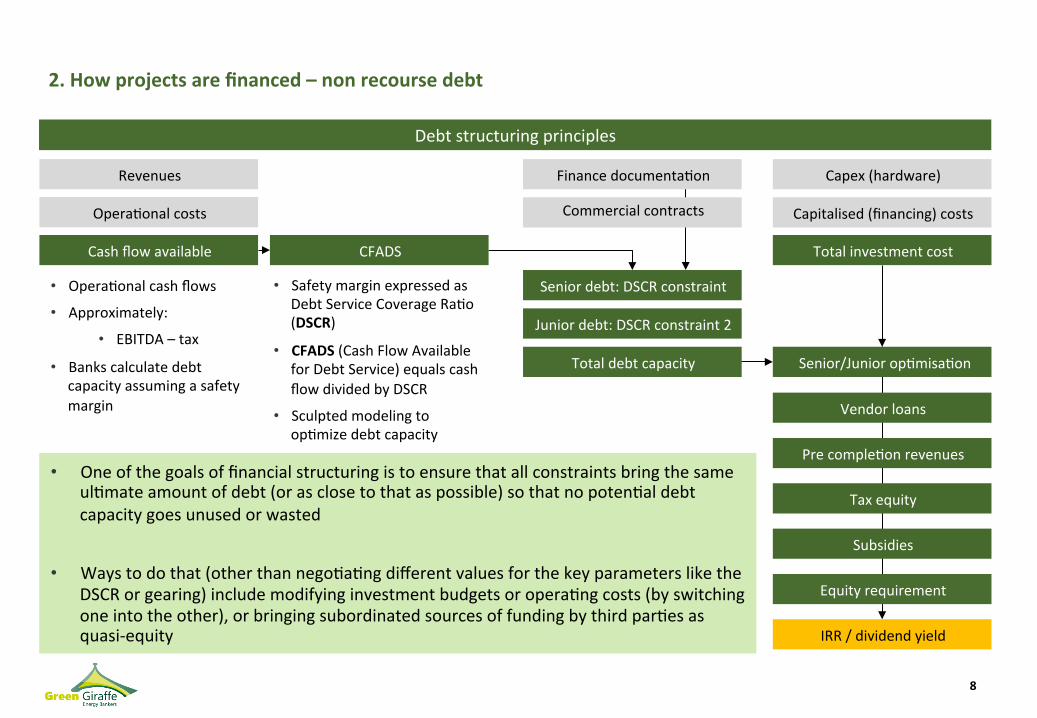

Debt structuring principles

Revenues

Opera\onal costs

Cash flow available

Senior debt: DSCR constraint

Junior debt: DSCR constraint 2

Total debt capacity

Total investment cost

• Opera\onal cash flows • Approximately:

• EBITDA – tax • Banks calculate debt

capacity assuming a safety margin

• Safety margin expressed as Debt Service Coverage Ra\o (DSCR)

• CFADS (Cash Flow Available for Debt Service) equals cash flow divided by DSCR

• Sculpted modeling to op\mize debt capacity

Capex (hardware)

Capitalised (financing) costs

IRR / dividend yield

Commercial contracts

Finance documenta\on

Pre comple\on revenues

Subsidies

Equity requirement

Senior/Junior op\misa\on

Vendor loans

Tax equity

• One of the goals of financial structuring is to ensure that all constraints bring the same ul\mate amount of debt (or as close to that as possible) so that no poten\al debt capacity goes unused or wasted

• Ways to do that (other than nego\a\ng different values for the key parameters like the DSCR or gearing) include modifying investment budgets or opera\ng costs (by switching one into the other), or bringing subordinated sources of funding by third par\es as quasi-‐equity

CFADS

8

2. How projects are financed – non recourse debt

Financing offshore wind

1. GGEB introduc\on

2. How projects are financed

3. The debt market

4. Risk analysis by the lenders

5. How to approach project finance

6. What GGEB can do for you

9

Table of contents

3. The debt market – lessons learned from the early years

The banking market is there if the transac\ons are well structured

10

32% 5%

0% 41%

35%

37% 33%

0

500

1000

1500

2000

2500

2006 2007 2008 2009 2010 2011 2012

Offshore wind project financed volumes

Installed capacity (MW) - brought forward 2 years (est)

Project financed capacity (MW)

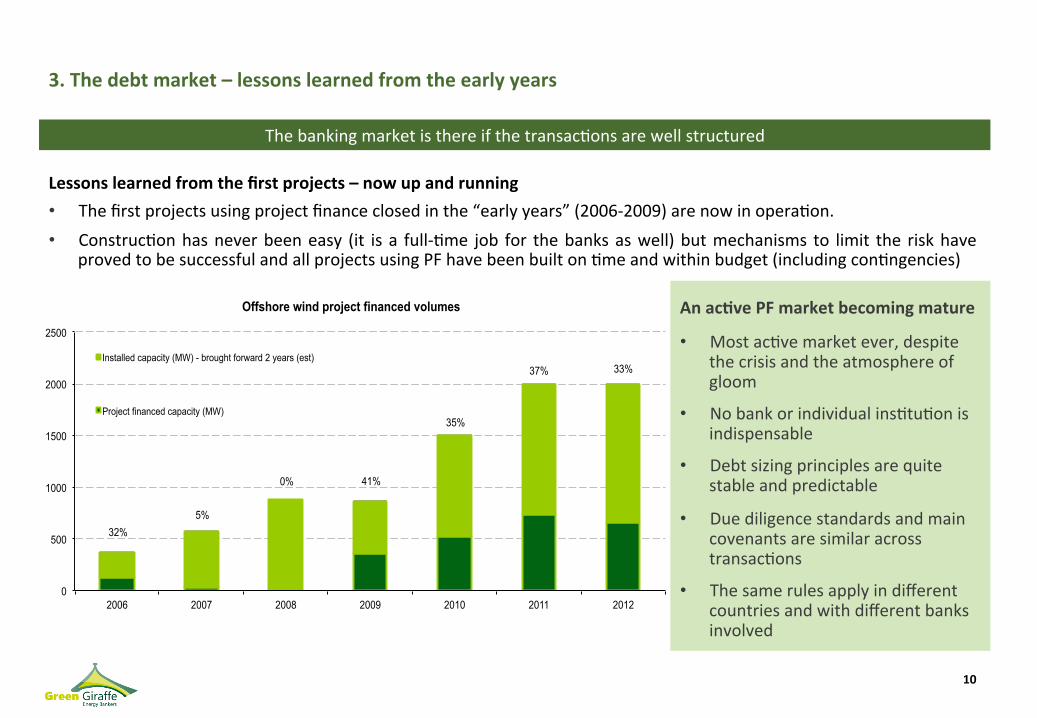

Lessons learned from the first projects – now up and running • The first projects using project finance closed in the “early years” (2006-‐2009) are now in opera\on. • Construc\on has never been easy (it is a full-‐\me job for the banks as well) but mechanisms to limit the risk have

proved to be successful and all projects using PF have been built on \me and within budget (including con\ngencies)

An ac7ve PF market becoming mature

• Most ac\ve market ever, despite the crisis and the atmosphere of gloom

• No bank or individual ins\tu\on is indispensable

• Debt sizing principles are quite stable and predictable

• Due diligence standards and main covenants are similar across transac\ons

• The same rules apply in different countries and with different banks involved

3. The debt market – some recent highlights

A number of large transac\ons have taken place

11

Notable transac7ons: • C-‐Power – Belgium – 2010:

billion-‐euro senior debt can be raised with construc\on risk for a project with new turbine

• Meerwind – Germany – 2011: private equity enters into the market and uses PF

• Walney – UK – 2012: first commercial financing of a minority stake

3. The debt market – current market – volumes available

12

The bank market is broader and broader • More than 30 banks have taken offshore wind risk today • More than 20 banks have construc\on exposure • Experienced banks – an ac\ve pool of banks able to structure and lead transac\ons:

• Rabobank, KfW-‐IPEX, Unicredit, BoTM, SocGen, BNPP, Santander, Commerzbank, (Dexia) • HSH, NordLB (German focus)

• Many banks were involved in recent deals in the last 2 years:

• Lloyds, ING, KBC, Siemens Bank, Deutsche Bank, NIBC, ASN • Calyon, BayLB, NAB, Helaba, SEB, Deka, DnB Nor, Na\xis, NIBC, Sabadell, Nordea, BBVA, LBBW, Mizuho, SMBC • RBS, HSBC (UK focus)

• More have expressed their appe\te

An average EUR 100 M available per bank per year

• EUR 30-‐150 M exposure per bank per year, in 1-‐3 deals

Commercial banks

At least EUR 2.5 billion available per year

3. The debt market – current market – volumes available

13

Public Financial Ins\tu\ons

Several ac7ve public financial ins7tu7ons • EIB – historic key player with cheaper funds (support to European offshore projects), but generally conserva\ve • EKF – offshore wind’s “best kept secret”: par\cipa\on linked to Danish exports, up to EUR 250 M per transac\on • Euler-‐Hermes – par\cipa\on linked to German exports, can do large \ckets • KfW – poten\ally large amounts available (in Germany): able to provide cheaper funding in significant volumes • GIB – UK Green Investment Bank, first involved in Walney

Their role has been instrumental to get deals done

• Will typically bear approximately half of the risk and/or funding of a transac\on • Will normally take the same risks as the commercial banks, but they usually run their own internal assessment • Some geographical / na\onal restric\ons • Small deal teams, so availability is a constraint

Can contribute as much as the commercial banks

3. The debt market – current market – financial condi7ons

Market trends

14

Typical project finance condi\ons offshore Leverage Maturity

post-‐comple\on Margins Maximum underwri\ng

2006-‐2007 60:40 10-‐15 years 150-‐200 bp 50-‐100 M

2009 70:30 15 years 300 bp 30-‐50 M

2010-‐2011 65:35 12-‐15 years 250-‐300 bp 50-‐75 M

Current market 70:30 10-‐15 years 275-‐375 bp 30-‐50 M

Structures have been quite stable since 2007

• Long-‐term debt is s\ll available

• Consensus on 70% leverage

• DSCR reflects price risk in the UK

Banks have refocused on known clients, core countries and strategic sectors of ac7vity

• The good news is that offshore wind is unambiguously “strategic” for many banks today

• Countries where offshore wind is developing are seen as “safe” (Germany – un\l now) and core for most banks

Debt is not that expensive

• Margins rise reflects higher bank cost of funding rather than higher cost of risk, but the overall cost of debt is stable

• Recent deals have seen overall cost of >15-‐year debt at 6.0% or less

Financing offshore wind

1. GGEB introduc\on

2. How projects are financed

3. The debt market

4. Risk analysis by the lenders

5. How to approach project finance

6. What GGEB can do for you

15

Table of contents

Development phase Construc7on phase Opera7onal phase

No project!

No permits No tariff / PPA No contracts

Not enough money

Delay and cost overruns

Scope gaps Contractor delays Adverse weather

Accidents

Lost revenue

Lower availability Higher O&M cost Lower prices Less wind

Mi7ga7on cascade

Project management Detailed planning

Commieed sponsors

Project coordina\on Solid contracts (LDs) Con\ngency budget

Insurance

Project management LT O&M contract

Turbine manufacturer commitment Insurance

Risks are different in each project phase

4. Risk analysis by the lenders

16

Stuff happens, offshore

4. Risk analysis by the lenders

A crane collapsed in the marshaling harbour

A monopile sank and was damaged

17

4. Risk analysis by the lenders

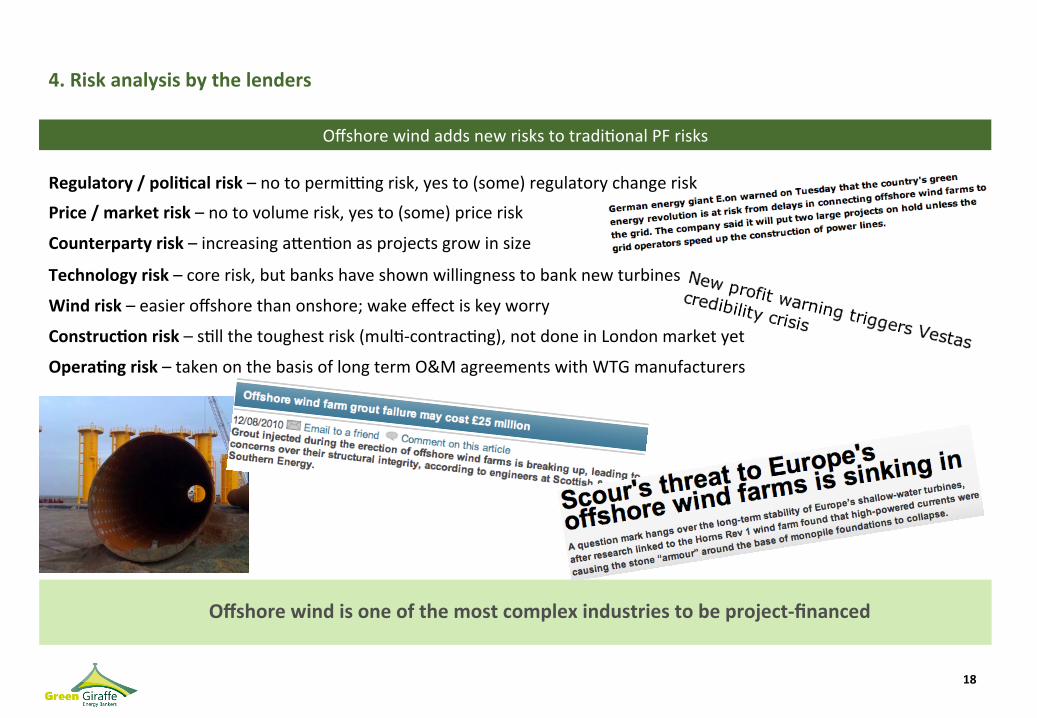

Regulatory / poli7cal risk – no to permisng risk, yes to (some) regulatory change risk

Price / market risk – no to volume risk, yes to (some) price risk

Counterparty risk – increasing aeen\on as projects grow in size

Technology risk – core risk, but banks have shown willingness to bank new turbines

Wind risk – easier offshore than onshore; wake effect is key worry

Construc7on risk – s\ll the toughest risk (mul\-‐contrac\ng), not done in London market yet

Opera7ng risk – taken on the basis of long term O&M agreements with WTG manufacturers

18

Offshore wind adds new risks to tradi\onal PF risks

Offshore wind is one of the most complex industries to be project-‐financed

4. Risk analysis by the lenders

Banks do take construc7on risk • Really non-‐recourse • Commercial terms of contracts not substan\ally different from contracts with non-‐banked clients

Focus on project management capacity and project 7metable • Overall risk dealt with through conserva\ve project schedule and con\ngency mechanism (both \me and money) • iden\fica\on of cri\cal path / long lead items / knock on risks • Specific aeen\on to availability of vessels, including for extended periods, and availability of “plan Bs”

They actually prefer mul7-‐contrac7ng (2 to 8 contracts) • Easier to make interfaces visible and deal with them explicitly in the contracts and project \metable • Makes due diligence more transparent

Ac7ve due diligence and involvement in contract nego7a7ons • Sub-‐contractors, supply chains, quality control procedures, creditworthiness & infrastructure of suppliers • More detail on turbine supply and long term O&M than to other contracts

Construc\on risk and mul\-‐contrac\ng

19

4. Risk analysis by the lenders

Offshore wind transac7ons require a tradi7onal PF security package • Pledge of all accounts, assets and rights of the project • Pledge on the shares of the project company

Equity reten7on clauses are more stringent than usual • Lenders are very sensi\ve to both who owns and who manages the project • Share reten\on and ownership clauses are stronger than in other sectors • This is linked to payment commitments during construc\on, but also to the perceived need for strong owners in the

early years of opera\ons when problems are perceived as more frequent • This has been a topic of difficult nego\a\ons between lenders and project sponsors

Requirement for direct agreements and oversight of commercial contracts • Tradi\onal in PF but more systema\c (and with more counterpar\es) in offshore wind • Lenders also want stronger involvement in commercial contracts (right to allow or veto changes) • Confiden\ality issues with contractors are quite sensi\ve • More intrusive due diligence in contracts & subcontractors and more informa\on provisions

Security package

20

Financing offshore wind

1. GGEB introduc\on

2. How projects are financed

3. The debt market

4. Risk analysis by the lenders

5. How to approach project finance

6. What GGEB can do for you

21

Table of contents

5. How to approach project finance

It needs to be an early decision by investors • A lot of the value from project finance discipline comes at an early stage, when choosing the contractual structure and

nego\a\ng the relevant contracts • The good news is that a lot of that work can be done without involving large banking groups, by using a small number

of specialised advisors

It requires experienced advisors • Bring in at your side en\\es which have credibility as lenders’ advisors and ask them to look at the project from the

perspec\ve of lenders • Technical advisors (Moe, Sgurr) are indispensable • We believe we can also bring value in pre-‐packaging a deal that banks will accept

Investors and contractors need to be commiged to it • Counterpar\es will accept to incorporate banks’ requirements in their commercial offers only if they really believe that

the project will not happen without external financing

• Do take into account the feedback from specialised advisors, otherwise it won’t work

You cannot improvise a project finance deal

22

5. How to approach project finance

It helps improve risk discipline for the project • More external eyes on contracts, interfaces and detailed project structure • Specific focus by banks and their advisors on poten\al downside scenarios • Project can “work” on a stand-‐alone basis (which makes it easier to sell)

It can help investors – and contractors! – obtain more favorable contractual terms • Using banks as a “bad cop” can be useful in contractual nego\a\ons (true for both investors and contractors!) • 3-‐way nego\a\ons can allow you to get away from zero-‐sum nego\a\ons

It’s really non-‐recourse • Banks take construc\on risk on the basis of the contracts and commieed con\ngency mechanisms • While sponsor involvement is valued, banks evaluate deals with no expecta\on of addi\onal cash in

It’s no longer so expensive • Recent deals have seen overall cost of >15-‐year debt at 6%

Project finance for offshore wind is not just about leverage

23

5. How to approach project finance – Conclusion: PF is available for well-‐structured projects

Structuring a deal is 7me-‐intensive • Non-‐recourse finance requires a specific discipline

and approach to project risks • Mul\ple complex tasks to run in parallel, with

numerous third par\es (with owen contradictory requirements)

• Several cri\cal paths to manage • ongoing development work • external advisors • contract nego\a\ons • internal approvals

How to make a deal bankable

24

The quality of the contracts can help bridge the difference

• The more « bankable » the contracts are, and the more flexible banks will be on equity issues

• The stronger the contractual commitments, the less important the owner will be

• No zero-‐sum game: enhancing some terms can lead to win-‐win-‐win solu\ons

Offshore wind projects have access to a very diverse project finance universe, as long as some rules are respected • the contractual package has to include banks requirements as early as possible • experienced advisors consulted upstream • \ming adapted to the banking process

Financing offshore wind

1. GGEB introduc\on

2. How projects are financed

3. The debt market

4. Risk analysis by the lenders

5. How to approach project finance

6. What GGEB can do for you

25

Table of contents

• Specialised competence & exper7se with regard to debt & equity raising and structuring, project development and contrac\ng for complex transac\ons

• Credibility in the equity markets through a strong and proven track record in buy/sell side advisory and brokerage in the wind and solar industry

• Access to an extensive and first class network with investors, EPC/technology suppliers, banks, advisors and intermediaries in the renewables market which we leverage to the benefit of your project

• The lessons we have already learned (some\mes the hard way) will enable you to op\mize the project development process and avoid costly mistakes and delays

• We are deeply commiged to the success of our clients and we offer you highly compe77ve fees structures including success oriented schemes

We have a proven track record in closing transac7ons and maximising value for our clients and their projects

6. What GGEB can do for you – our value added

What GGEB brings to the table The services we can offer

26

Strategic financial advisory • Renewable energy strategic development • Technology and project bankability assessment • Business plan analysis, financial modelling and valua\on • Assis\ng in bidding process

Debt and equity raising and structuring • Detailed financial analysis and valua\on • Prepara\on of all necessary support materials (informa\on

memo, financial models, management presenta\ons, etc.) • Draw tailor made commercial proposi\on to banks/investors • Ac\ve marke\ng of your project(s) to a selec\on of poten\al

debt and equity investors from our extensive network • Commercial nego\a\ons with investors or banks • Transac\on documenta\on Assistance in project contract nego7a7ons • Review of contrac\ng strategy to ensure bankability • Review of commercial terms (EPC warran\es, availability,...)

GGEB’s comprehensive approach

6. What GGEB can do for you – roadmap to financial close

Logis7cs

Technology

Equity Financing

Insurance

PPA

Contrac7ng

• Check robustness of business plan

• Verify input (on a no names basis) with shortlisted suppliers

• Assess (financial) impact of opera7ng decisions

• Request indica7ve term sheets

• Selec7on of EPC and other partners

• Nego7ate main commercial terms

• Process management

• Nego7ate commiged term sheets

• Develop effec7ve financing strategy

• Select most preferred bank consor7um and effec7ve process management

• Nego7ate commiged terms from banks

• Finalisa7on of financing documenta7on

Prepara7on Business plan Project contracts Financial Close

Project Financing

Inpu

t Business p

lan

Project Financing

Draw

dow

n of fu

nds

and Start con

struc7on

Added Value GGEB:

• Exper7se to perform detailed review incl. financial modeling

• Informal market sounding for quotes, etc.

• Sanity check on process and 7metables

Added Value GGEB:

• Experience with all key project contracts

• Many lessons learnt (some the hard way..)

• Ensure process discipline and contain (legal) costs

Added Value GGEB:

• Proven track record

• Extensive network with financing banks

• Independent posi7on

• Provide comprehensive process management

Permits

• Develop effec7ve equity raising strategy

• Valua7on

• Effec7ve process management

• Comparison of offers and final nego7a7ons

• Finalisa7on of transac7on documents

Equity raising

Added Value GGEB:

• Proven track record

• Extensive network with poten7al investors

• Independent posi7on

• Provide comprehensive process management

Financing Project organiza7on

27

8 rue d’Uzès, 75002 Paris

tel: + 331 4221 3663

email: fr@green-‐giraffe.eu

Maliebaan 83a, 3581 CG Utrecht

tel: + 31 30 820 0334

email: nl@green-‐giraffe.eu

30 Crown place, London EC2A 4EB

tel: + 4475 5400 0828

email: uk@green-‐giraffe.eu

tel: + 4917 6551 28283

email: de@green-‐giraffe.eu

Green Giraffe Energy Bankers

Paris

London

Utrecht

Hamburg

28

Related Documents