Financial Statement Analysis Hunter Ryffel [email protected] Micheal Sura [email protected] Garret Bruce [email protected] Joe Brewer [email protected] Jesse Ricones [email protected] Miles Arbuckle [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Statement Analysis

Hunter Ryffel [email protected]

Micheal Sura [email protected]

Garret Bruce [email protected]

Joe Brewer [email protected]

Jesse Ricones [email protected]

Miles Arbuckle [email protected]

2

Table of Contents

Executive Summary ................................................................................................... 8

Industry analysis .................................................................................................. 10

Accounting analysis .............................................................................................. 12

Financial analysis ................................................................................................. 13

Valuation Analysis ................................................................................................ 18

Company Overview ................................................................................................. 20

Industry Overview................................................................................................ 21

Five Forces Model ................................................................................................... 22

Rivalry among Competitors ...................................................................................... 22

Industry Growth Rate ........................................................................................... 23

Industry Concentration ......................................................................................... 24

Fixed-to-Variable Costs ......................................................................................... 24

Switching Costs ................................................................................................... 25

Exit Barriers ......................................................................................................... 26

Conclusion ........................................................................................................... 26

Threat of New Entrants ........................................................................................... 26

Barriers to Entry .................................................................................................. 27

Distribution Access and Relationships .................................................................... 27

Conclusion ........................................................................................................... 27

Threat of Substitutes ............................................................................................... 28

Relative Price and Performance ............................................................................. 28

Conclusion ........................................................................................................... 28

3

Bargaining Power of Suppliers ................................................................................. 29

Supplier Concentration ......................................................................................... 29

Conclusion ........................................................................................................... 30

Bargaining Power of Customers ............................................................................... 30

Competitor Concentration ..................................................................................... 30

Conclusion ........................................................................................................... 30

Porter’s Five Forces Conclusion ................................................................................ 31

Key Success Factors ................................................................................................ 32

Industry’s Competitive Advantages ....................................................................... 33

Low Input Costs ................................................................................................... 33

Low Distribution Costs .......................................................................................... 33

Efficient Production .............................................................................................. 34

Flexible Delivery ................................................................................................... 34

Conclusion ........................................................................................................... 34

AptarGroup’s Competitive Advantages ................................................................... 35

Production Process ............................................................................................... 35

Geographic Diversity ............................................................................................ 35

Local Production .................................................................................................. 36

Accounting Analysis................................................................................................. 36

Type One Accounting Policies ............................................................................... 37

Low Input Costs ................................................................................................... 37

Low Distribution Costs .......................................................................................... 38

Efficient Production .............................................................................................. 39

Type Two Accounting Policies ............................................................................... 39

4

Goodwill .............................................................................................................. 40

Research and Development .................................................................................. 40

Foreign conversion risk ......................................................................................... 41

Operating leases .................................................................................................. 42

Conclusion ........................................................................................................... 42

Accounting Flexibility Assessment ............................................................................ 43

Goodwill .............................................................................................................. 43

Research and Development .................................................................................. 44

Capital vs. Operating Leases ................................................................................. 44

Conclusion ........................................................................................................... 45

Evaluation of Actual Accounting Strategy .................................................................. 45

Goodwill .............................................................................................................. 46

Research & Development ..................................................................................... 46

Operating Leases ................................................................................................. 47

Quality of Disclosure - Type One .............................................................................. 48

Efficient Production .............................................................................................. 48

Low Input Costs ................................................................................................... 49

Distribution Costs ................................................................................................. 49

Quality of Disclosure – Type Two ............................................................................. 50

Goodwill .............................................................................................................. 50

Research and Development .................................................................................. 51

Foreign Conversion Risk ....................................................................................... 51

Operating Leases ................................................................................................. 52

Potential “Red Flags” ............................................................................................... 52

5

Goodwill .............................................................................................................. 53

Research & Development ..................................................................................... 53

Conclusion ........................................................................................................... 54

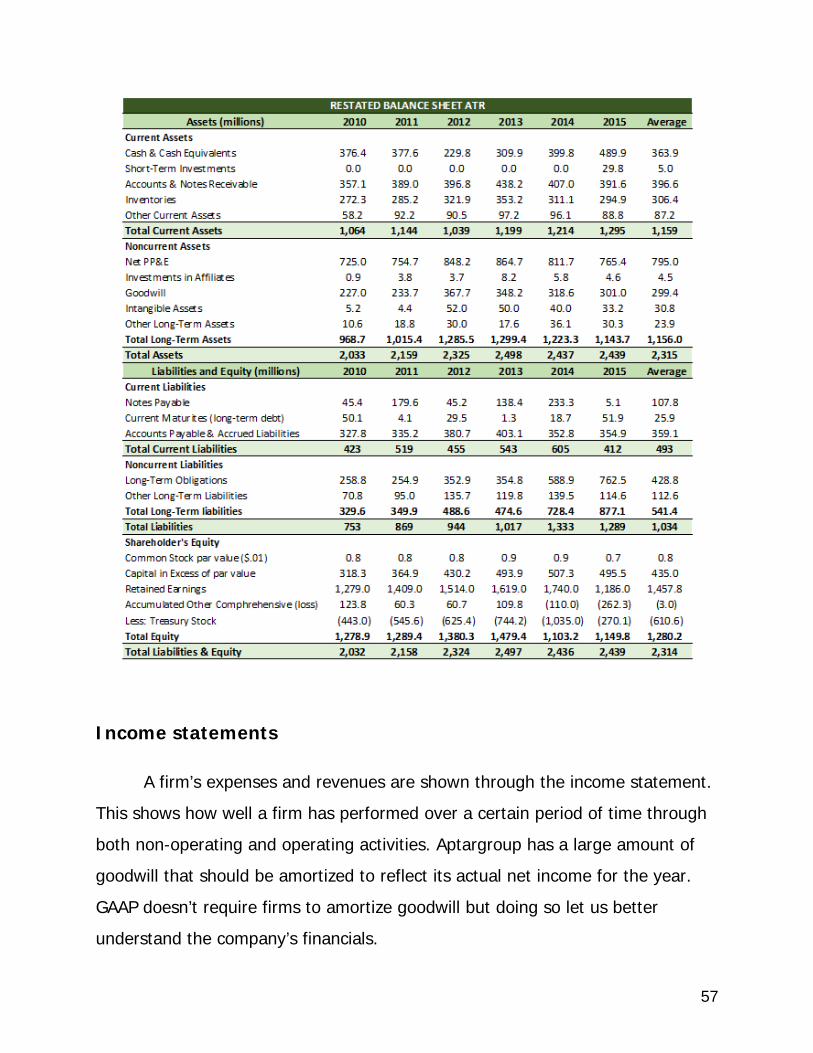

Financial Statements ............................................................................................... 54

Balance sheets ..................................................................................................... 54

Income statements .............................................................................................. 57

Conclusion ........................................................................................................... 59

Financial Analysis .................................................................................................... 59

Liquidity Ratios ....................................................................................................... 59

Current Ratio ....................................................................................................... 60

Quick Asset Ratio ................................................................................................. 62

Conclusion ........................................................................................................... 63

Operating Efficiency Ratios ...................................................................................... 63

Inventory Turnover .............................................................................................. 64

Accounts Receivable Turnover .............................................................................. 65

Working Capital Turnover ..................................................................................... 67

Days Supply of Inventory ..................................................................................... 68

Days Sales Outstanding ........................................................................................ 69

Cash to Cash Cycle .............................................................................................. 71

Conclusion ........................................................................................................... 72

Profitability Ratios ................................................................................................... 73

Annual Sales Growth ............................................................................................ 73

Gross Profit Margin .............................................................................................. 74

Operating Profit Margin ........................................................................................ 76

6

Net Profit Margin.................................................................................................. 78

Asset Turnover .................................................................................................... 79

Return on Assets.................................................................................................. 81

Return on Equity .................................................................................................. 82

Conclusion ........................................................................................................... 83

Capital Structure Ratios ........................................................................................... 84

Debt to Equity Ratio ............................................................................................. 84

Times Interest Earned .......................................................................................... 85

Debt Service Margin ............................................................................................. 87

Altman Z-Score .................................................................................................... 88

Internal Growth Rate ........................................................................................... 89

Sustainable Growth Rate ...................................................................................... 91

Conclusion ........................................................................................................... 92

Cost of Capital Estimation ........................................................................................ 92

Cost of Equity ...................................................................................................... 92

Backdoor Cost of Equity ....................................................................................... 94

Cost of Debt ........................................................................................................ 95

WACC (Weighted Average Cost of Capital) ............................................................ 96

Conclusion ........................................................................................................... 97

Forecasting Financial Statements ............................................................................. 97

Income Statement ............................................................................................... 98

Dividends Forecasting .......................................................................................... 99

Balance Sheet ...................................................................................................... 99

Cash Flow Statement ......................................................................................... 100

7

Method of Comparables ......................................................................................... 101

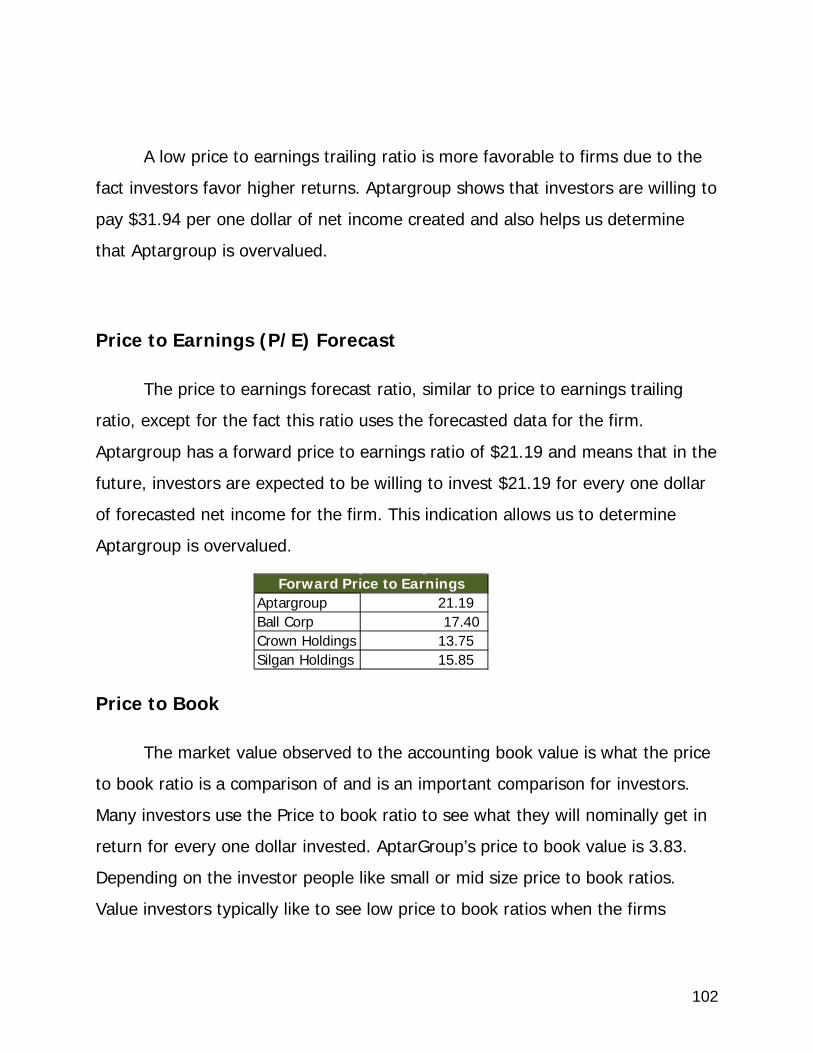

Price to Earnings (P/E) Trailing ........................................................................... 101

Price to Earnings (P/E) Forecast .......................................................................... 102

Price to Book ..................................................................................................... 102

Dividends to Price .............................................................................................. 103

Price to Earnings Growth (PEG) .......................................................................... 104

Price to EBITDA ................................................................................................. 104

Price to Free Cash Flow ...................................................................................... 104

Enterprise Value to EBITDA ................................................................................ 105

Price to Sales ..................................................................................................... 105

Conclusion ......................................................................................................... 106

Intrinsic Model Valuation ....................................................................................... 106

Discounted Dividends Model ............................................................................... 107

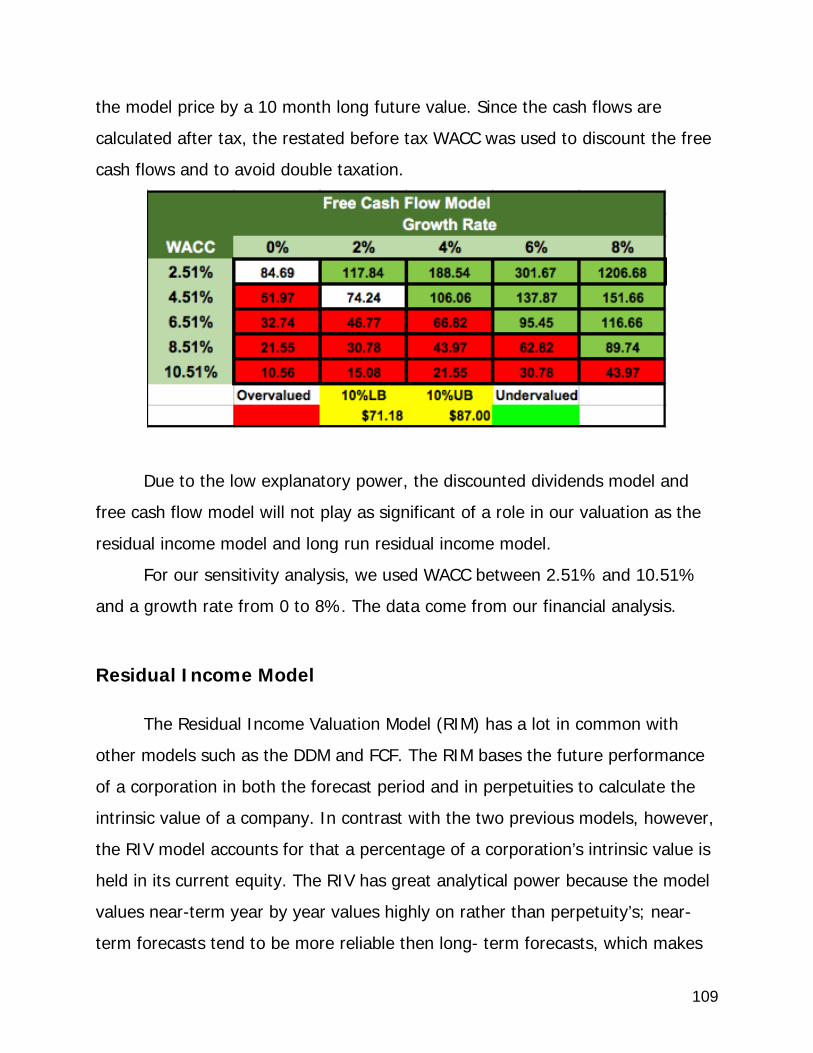

Discounted Free Cash Flow Model ....................................................................... 108

Residual Income Model ...................................................................................... 109

Long-Run Residual Income Model ....................................................................... 110

Intrinsic Valuation Model Conclusion ................................................................... 112

APPENDIX ............................................................................................................ 113

References ........................................................................................................ 113

Forecasted Financial Statements ......................................................................... 113

8

Executive Summary

Analyst Recommendation: Don’t buy (Overvalued)

April 1st, 2016

Observed Price 2011 2012 2013 2014 201552 Week Range Scores 4.366 4.404 4.374 4.573 4.018RevenueMarket CapitalizationShares Outstanding

As Stated Restated ValuedTrailing P/E 31.94 32.65 Overvalued

Return on Equity Forward P/E 21.19 22.87 OvervaluedReturn on Assets Price to Book 3.83 4.05 Overvalued

Dividend to Price 0.02 0.01 UndervaluedRegression Beta P.E.G. Ratio 2.55 2.78 Overvalued24 months 0.93 Price to EBITDA 59.67 62.03 Overvalued36 months 0.96 Price to FCF 154.89 N/A N/A48 months 0.99 EV/EBITDA 71.87 69.56 Undervalued60 months 0.91 Price to Sales 89.45 91.23 Overvalued72 months 0.93

As Stated Valued$28.78 Overvalued

Actual Lower Upper Free Cash Flows $34.97 OvervaluedCost of Equity 9.75% 8.43% 11.07% Residual Income $24.35 UndervaluedWACCBT 6.70% 6.07% 7.32% $26.13 OvervaluedWACCAT 6.02% 5.40% 6.64%

Cost of Capital

AptarGroup NYSE (04/1/2016) Altman Z-Scores$67.90

$60.73 - $80.36$2317.15 Million

$4.82 Billion Financial Based Valuations63.16 Million

23%10.90%

Intrinsic Based Valuations

Discounted Dividends

Long Run Residual Income

R Squared51.39%56.30%54.90%53.74%58.60%

9

Figure 1.Error! No text of specified style in document..1 - Share price of AptarGroup in the last five years

Figure Error! No text of specified style in document..2 - Share price of AptarGroup and main competitors

10

Industry analysis

AptarGroup, Inc. (ATR) is a worldwide manufacturer of plastic containers

and lids predominantly for the beauty, healthcare, homecare and prescription

drug markets, and the food and beverage industry.

We have identified Ball Corporation (BLL), Crown Holdings (CCK), and

Silgan Holdings (SLGN) as AptarGroup’s main competitors.

The primary products that AptarGroup produces today are dispensing

pumps, aerosol valves and closures. Dispensing pumps are a convenient

dispensing device and are used for products such as soap and shampoo.

We used the Porter’s Five Forces Model in order to determine the

profitability a firm could expect in the P&C industry.

Five Forces Model

Rivalry Among Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products Medium

Bargaining Power of Customers High

Bargaining Power of Suppliers Low

11

Rivalry among existing firms is very high due to the fact that the P&C

industry is a highly competitive market with both public and private firms

competing locally and internationally to provide high quality low cost products

(ATR, CCK, SLGN 10-K).

The threat of new entrants is low since the industry has high barriers to

entry and requires efficient distribution access. The average firm in the industry

has a market capitalization of $5.39 billion. This is supported by billions in assets,

supporting the statement that new firms would have to be large to be able to

compete.

The threat of substitute products is mixed-high within the industry. In the

P&C industry, the manufacturers produce goods cost-efficiently. It is difficult for

a potential substitute to undercut the market participants. The suppliers can also

protect themselves by the imposing the contractual obligations on customers.

The bargaining power of customers is high. The P&C industry is highly

saturated with local and international competitors. The industry is highly

competitive, allowing customers to set prices. On the other hand, the bargaining

power of suppliers is low due to the large number of suppliers and low switching

costs.

The P&C industry is in the sector of basic materials. The costs in this

sector are low; this focus on low cost output is the result of price-taking behavior

12

of suppliers. We further assume that the industry is a price-taker in our

predictions of the factors that determine the success in the industry.

Accounting analysis

Accounting practices are reviewed and looked at to understand the nature

of the company and the packaging and container industry. It is very important

that we look at the accounting practices due to the flexibility that the Generally

Accepted Accounting Principles (GAAP) allows. The Flexibility of the GAAP on a

company’s financial statements can often hide information that needs to be

known when valuing a company. Many companies are hard to value due to the

lack of the financial statements disclosure. We have to look into the type 1

policies’ quality of disclosure in relation to the key success factors of the

company in comparison to the industry analysis. Then, we look at the type 2

policies which look at the distortion in the area of AptarGroup financial structure.

AptarGroup, Type 1 accounting policies, we evaluated the degree of

disclosure in terms of efficient production, low input costs, and distribution costs.

AptarGroup clearly represents risk in all of these three areas; therefore, type one

policies are not a major concern.

AptarGroup, Type 2 accounting policies, we evaluated operating leases to

find that the P&C industry is not heavily invested in operating leases. Operating

13

leases account for 20% or less of non-current liabilities in the P&C industry.

Since it is a small portion of non-current liabilities, it was not considered to be a

red flag. AptarGroup’s goodwill accounts for 40% of the net fixed assets and was

identified as a potential red flag. Also AptarGroup’s lack of expensing R&D when

the cost is incurred raised another potential red flag.

From the account analysis we find that AptarGroup is not very accurate in

terms of disclosure and lacks enough reliable information for an accurate

evaluation. The lack of disclosure for type 2 accounting policies leads us to the

need of restating the financial statements of AptarGroup to adjust for the

potential red flags in goodwill and the expense of R&D.

Financial analysis

For the purpose of the analysis, we calculated the liquidity, capital

structure, and profitability ratios. We formed liquidity ratio analysis is based on

the current and quick ratios, inventory turnover, days supply inventory, accounts

receivable turnover, accounts receivable days, cash to cash cycle, and working

capital turnover.

Determining the liquidity ratios are a vital step when valuing a firm

because the results can show if a firm has the ability to continue as a going

concern or enough cash to cover debts when a creditor is expecting payment.

14

Liquidity Ratio Analysis

Ratio Performance Trend

Current Ratio Outperforming Stable

Quick Ratio Outperforming Stable

Inventory Turnover Underperforming Stable

Days Supply Inventory Outperforming Stable

A/R Turnover Underperforming Stable

A/R Days Underperforming Stable

Cash to cash cycle Outperforming Stable

Working capital turnover Underperforming Increasing

AptarGroup is either completely outperforming all other competitors, or

underperforming showing the worst data comparing to their competitors and the

industry. The trends in liquidity ratio analysis are stable; the data has not been

fluctuating in the past five years.

To perform the profitability ratio analysis, we gathered and analyzed the

sales growth, gross profit margin, operating profit margin, net profit margin,

asset turnover, return on assets, and return on equity. The ratios show the

generated profit as a percent of the produced sales.

These ratios have a significant meaning for potential investors, since the

ratios measure the overall efficiency of a firm in generating returns for the

shareholders.

15

Profitability Ratio Analysis

Ratio Performance Trend

Sales Growth Average Unstable

Gross Profit Margin Outperforming Stable

Net Profit Margin Outperforming Stable

Asset Turnover Average Stable

Return on Assets Outperforming Stable

Return on Equity Average Stable

AptarGroup’s profitability ratios are appealing due to the fact that they are

either outperforming or at the industry’s average.

For the capital structure analysis, we evaluated the debt to equity ratio,

times interest earned, and the Altman’s Z-score. Altman’s Z-score shows whether

the company is heading towards bankruptcy. Since capital structure is the mix of

debt and equity, the debt to equity ratio provides with a better understanding of

the weight of debt and equity.

16

Capital Structure Ratio Analysis

Ratio Performance Trend

Debt to Equity Underperforming Stable

Times Interest Earned Outperforming Decreasing

Altman’s Z-score Average Unstable

After performing the ratio analysis, we forecasted the AptarGroup’ financial

statements. Although financial forecasts cannot be totally accurate, our trends

and ratio analysis help to be able to forecast with a reasonably high accuracy.

We forecasted growth rate, income statement, balance sheet, and the

statement of cash flows. To forecast the growth rate, we started by forecasting

the sales. Since sales growth rate is what drives the income forecast, the

forecast shows the data in accordance with the sales. Our forecasting of the

balance sheet is done through using the forecasting of the asset turnover ratio.

The forecast of the statement of cash flows usually has the lowest accuracy, due

to the fact that the statement of cash flows is the most volatile financial

statement.

Finally, we calculated AptarGroup’s cost of equity and cost of debt that

allowed us to estimate the weighted average cost of capital (WACC). The cost of

17

debt takes into account all interest rates in proportion with the weight that is

allocated to each rate. To estimate cost of equity, we used both the backdoor

cost of equity and the CAPM formula. We further picked the CAPM method as our

main method in finding the cost equity.

We gathered necessary inputs for the CAPM formula from the St. Louis

Federal reserve website and the regression models.

20 year regressions

Months Beta

Beta

LB

Beta

UB R^2 SP MRP Rf Ke Ke LB Ke UB

24 0.932 0.530 1.33 51.39% 1.00% 7.00% 2.25% 9.78% 6.96% 12.59%

36 0.958 0.665 1.25 56.30% 1.00% 7.00% 2.25% 9.96% 7.90% 12.02%

48 0.994 0.726 1.26 54.90% 1.00% 7.00% 2.25% 10.21% 8.33% 12.09%

60 0.905 0.684 1.13 53.74% 1.00% 7.00% 2.25% 9.58% 8.04% 11.13%

72 0.928 0.740 1.12 58.58% 1.00% 7.00% 2.25% 9.75% 8.43% 11.07%

We also provided with the WACC before and after tax. The following table

tells us that AptarGroup pays an average of 6.02 cents for every dollar in their

extra funding.

18

Market

Value

Amount (in

millions) Rate Weight W*R

Liabilities 1,289 3.97% 0.528538626 2.10%

Equity 1149.8 9.75% 0.471461374 4.60%

Firm Value 2,439 WACC 6.70%

WACC after

tax 6.02%

Valuation Analysis

After performing an industry analysis of AptarGroup, calculating the

correct cost of capital, discovering AptarGroup’s key accounting policies, and

forecasting AptarGroup’s financials, we are now able to value the company. The

evaluation will be based on AptarGroup’s April 1st share price of $79.09. We used

a 10% analysis to help us to decide whether the company was correctly valued,

overvalued, or undervalued.

The two methods that we used to determine our valuation of the company

were the intrinsic valuation models and the methods of comparables. The

intrinsic valuation models help us to evaluate the company using internal

information rather than using industry information. The models that we used

were the discount dividend model, discounted free cash flow model, residual

income model, and the long run residual income model. Each valuation model

takes advantage of using a sensitivity analysis model and includes our forecasted

financials to determine value under a variety of conditions. Intrinsic valuation has

a considerably higher weight when determining the valuation of the company.

We will also value residual income model and long run residual income model

19

more than the other two models because as they have the highest level of

illustrative power.

The method of comparables approach is the second approach we used to

determine company valuation. This approach used ratio analysis to compare

AptarGroup to its industry competitors and forecast share price. This method

relies on only one year of date so the results can be unreliable or inaccurate.

This method will not be as heavily weighted when determining the valuation of

the company. After using the 10% analyst position, we have determined that

AptarGroup is an overvalued company in both the stated and restated basis. We

take more consideration by looking at the restated basis which leaves us to a

clear cut decision that the company is overvalued.

End of Executive Summary

20

Company Overview

AptarGroup, Inc. (ATR) is a worldwide manufacturer of plastic containers

and lids predominantly for the beauty, healthcare, homecare and prescription

drug markets, and the food and beverage industry. AptarGroup was created in

the late 1940s when it first started producing aerosol valves. As of 2015

AptarGroup has 5000 customers around the world and none of those individual

customers accounted for more than 5% of its total sales (ATR 10-K). The

customers are both public and private firms from many countries from around

the world.

The primary products that AptarGroup produces today are dispensing

pumps, aerosol valves and closures. Dispensing pumps are a convenient

dispensing device and are used for products such as soap and shampoo. Its

products are used worldwide, and are gaining popularity for many different

products. Dispensing closures, which is another type of closure, is the

predominate type of closure produced which allows a product to be dispensed

from a container without removing the actual closure. AptarGroup also produces

medical vials and multiple medical products for the injectable industry (ATR 10-

K).

AptarGroup organizes its company into three segments: beauty, home and

pharma, food and Beverage. The beauty segment is the biggest segment and it

accounts for 58% of net sales. Pharms is the next largest section and it accounts

for 29% of net sales. Lastly food and beverage is the smallest segment

accounting for 13% of net sale. AptarGroup currently has 13,000 full time

employees. 2,100 are in the United States, 3,500 are in Asia, and 7,400 are in

Europe. AptarGroup is in the Packaging and Container (P&C) industry (ATR 10-

K).

21

Industry Overview

We have identified Ball Corporation (BLL), Crown Holdings (CCK), and

Silgan Holdings (SLGN) as AptarGroup’s main competitors. We compared firms

on market cap, revenue, and operating segments to determine which firms were

the most similar to AptarGroup. Throughout the rest of our analysis we will

assume these four firms are representative of the industry at large.

The table above shows the similarity of the factors we compared for our

industry sample based on 2015 data (Yahoo).

Company Ticker Industry Market Cap RevenueAptarGroup ATR P&C - personal 4,750 2,317Ball Corporation BLL P&C - industry 10,190 7,997Crown Holdings CCK P&C - personal 7,450 8,762Silgan Holdings SLGN P&C - personal 3,100 3,764Industry Sample Industry P&C 6,373 5,710

Packaging and Container Industry

22

Five Forces Model

We used the Porter’s Five Forces Model in order to determine the

profitability a firm could expect in the P&C industry. By determining where firms

have high or low competition, we can determine what the corporate strategies

firms should focus on to maximize profitability.

The Porter’s Five Forces Model evaluates the rivalry among existing firms,

the threat of substitutes, the threat of new entrants, the bargaining power of

suppliers, and the bargaining power of customers. As shown above, the P&C

industry has high overall competition.

Rivalry among Competitors

We began our Five Forces Analysis by examining the rivalry among

competitors. The sub-forces relevant to our industry are: the industry growth

rate, industry concentration, fixed-to-variable cost ratios, excess production

capacity, and the exit barriers (Palepu).

We believe that rivalry among competitors is the most telling of the five

forces because it has a broad influence on all other factors. If rivalry were high,

then firms would have less bargaining power due to greater threat of substitutes,

so they would be price-takers. If rivalry were low, then the firms would be price-

setters because of greater bargaining power. Therefore, we should be able to

determine the industry’s key success factors and AptarGroup’s competitive

advantages by deciding if the industry is a price-setter or price-taker.

The P&C industry is a highly competitive market with both public and

private firms competing locally and internationally to provide high quality low

23

cost products (ATR, CCK, SLGN 10-K). Many firms buy supplies and manufacture

containers in Asian countries to minimize cost, which makes outside competition

difficult. We will show in the following sections why we believe that the firms in

the P&C industry are price-takers because of high competition and a lack of

bargaining power.

Industry Growth Rate

Companies will compete more aggressively during times of limited growth.

During times of slow growth, firms will focus on the industry’s key success

factors, (discussed after Five Forces) which make it more difficult to generate

revenue. Times of rapid economic expansion allows firms to focus on expansion

and repayment to shareholders (dividends and shares repurchases).

We used revenue growth as our metric for economic expansion. Since we

will use revenue as the basis of financial statement forecasting later, it is

consistent with our measure of historical and future growth.

As shown above there is overall low industry growth, especially between

2015 and 2014, which had a 6.2% decline in revenue. The 5 year revenue

growth average is 2.5%, which is below the 30 year T-Bond of 2.63% on 5/4/16

(CNBC). This indicates that the market is highly competitive, and we should

expect low prices in the industry.

Firm 2011 2012 2013 2014 2015 AverageATR 12.5% -0.3% 8.1% 3.1% -10.8% 2.5%BLL 13.1% 1.2% -3.1% 1.2% -6.7% 1.2%CCK 8.9% -2.0% 2.2% 5.1% -3.7% 2.1%

SLGN 14.2% 2.2% 3.4% 5.5% -3.8% 4.3%Industry 12.2% 0.3% 2.6% 3.7% -6.2% 2.5%

P&C Industry Revenue Growth

24

Industry Concentration

We found that many companies compete internationally in the P&C

industry. Furthermore, most of these firms had greater market share (all in our

industry sample). In addition to these large competitors, the market is saturated

with local competitors that operate within specific geographic areas common to

the industry (All 10-K).

We compared the percent of overall sales each firm accounts for to

determine the concentration of our industry sample. AptarGroup averaged the

lowest revenue at only 10.4%; this is in contrast to BLL and CCK, which account

for over 70% of the market (35% each). This tells us that the P&C industry is

highly concentrated, with two firms accounting for over 70% of the market.

Beyond this, the table above shows us how the relative revenue is almost fixed

across the five years. The unchanging relative revenue reveals that the firms

have been competing effectively to maintain their market shares.

Fixed-to-Variable Costs

The P&C industry requires that firms have relatively high fixed costs (ATR,

BLL, CCK, SLGN 10-K). Since firms focus on efficient production, it is necessary

that firms have the necessary facilities and equipment to produce packages and

containers both cheaply and quickly (ATR, SLGN 10-K).

Firm 2011 2012 2013 2014 2015 AverageATR 10.1% 10.1% 10.8% 10.7% 10.1% 10.4%BLL 37.3% 37.8% 36.3% 35.4% 35.0% 36.4%CCK 37.4% 36.6% 37.1% 37.6% 38.4% 37.4%

SLGN 15.2% 15.5% 15.9% 16.2% 16.5% 15.8%

P&C Industry Revenue Concentration

25

Firms will typically produce in high volumes, which means that the variable

costs will rise quickly compared to fixed costs. Yet, since the variable costs

primarily consist of raw materials, companies will have comparatively high fixed-

to-variable costs (ATR, BLL, CCK 10-K).

The P&C industry is currently experiencing mixed, but an overall positive

trend in its variable costs. We believe that the variable costs are favorable

because of the continued low oil prices. We valued low oil prices more than a

rise in other raw materials because of its wide-reaching effects. When oil prices

drop, shipping becomes cheaper for both the P&C industry and its suppliers,

which should decrease the majority of input goods pricing. This positive trend is

important because it indicates that rivalry is slightly lower since firms are more

easily able to get healthy margins.

Switching Costs

We looked at switching costs to determine how likely customers are to

switch competitors. If there are high switching costs: new infrastructure,

employee training, or contractual obligations, then the customer will only switch

when there is a significant advantage. Whereas, when switching costs are low

then customers will often choose based on price or quality.

The switching costs in the P&C industry are low because there is usually

non-restrictive contracts, and there is no significant difference between one

package or container compared to another (ATR, BLL, CCK, SLGN 10-K).

Furthermore, since the P&C supplier does not materially affect what customers

can retail their products for, there is no additional value added (BLL 10-K). We

consider this to be a key factor of price-taking behavior, and expect it to greatly

increase rivalry among existing firms.

26

Exit Barriers

Exit barriers can play a large role in the decision-making process of firms

looking to leave the industry. Since firms in the P&C industry invest heavily in

fixed assets, we looked at the growth of PP&E and the relative size of PP&E in

the table below.

Since P&C firms use specialized equipment, there is poor liquidity if a firm

needed to exit quickly. This could result in significant losses if a firm was forced

to exit because it was failing. Therefore, we believe firms will compete

aggressively with existing firms.

Conclusion

Overall, we believe the P&C industry has high rivalry among existing firms.

We based this on the fact that the industry has been experiencing low growth

(2.5%), is heavily concentrated (two firms = 70% revenue), there is high

overhead, customers have low switching costs, and there are high exit barriers.

Since all of these factors contribute to either lower margins or more aggressive

competition, this should increase the rivalry among existing firms.

Threat of New Entrants

We believe that there is a low threat of new entrants, which is beneficial to

firms already competing in the industry. We have identified the low threat

because the industry has high barriers to entry and requires efficient distribution

access.

27

Barriers to Entry

Within the industry, the average firm has $5.39 billion in market cap (CSI

Market). This is supported by billions in assets, which makes it difficult for new

competitors to raise the capital investment required. Furthermore, the average

plant can take years to construct, which increases the financial commitment

(BLL, SLGN 10-Ks). The high capital barriers protect existing firms from new

entrants looking to enter the market.

Distribution Access and Relationships

Distribution access is the ability to move your product from your facility to

the customer. Because firms sell to customers across six continents, while

focusing on minimizing costs, it becomes important to have good relationships

with distributors. The ability to move goods quickly and cheaply is what

empowers firms to retain and attract new firms (ATR, CCK, SLGN 10-K).

Conclusion

The high capital requirements will prevent new firms from seeking to enter

the market. The long payback period and the current rivalry in the market should

prevent new international competitors from entering the industry. This is

advantageous to existing P&C firms because it limits their competition to existing

companies.

28

Threat of Substitutes

The threat of substitute products is the risk of customers replacing

products currently sold by the industry with alternatives. The main two

determining factors to switching products are price and performance of the

substitute, and the customers’ willingness to switch products. Across the basic

materials sector replacing any product, including containers is simple. Therefore,

the risk of outside substitutes is low, but the risk of substitution within the

industry is mixed-high.

Relative Price and Performance

We found that switching costs are the main determinant of a customer’s

willingness to substitute products. Since there are no training costs associated

with switching suppliers, customers will only be affected by price and production

lead-times. Beyond the relative price of the goods, the expense of getting out of

a contract will determine a customer’s decision.

In the P&C industry goods are produced both cost-effectively and sold

cheaply. Therefore, it is difficult for a potential substitute to undercut the market

participants. Beyond this, firms could protect themselves by imposing contractual

obligations on customers. However, the competitive environment causes firms to

mainly impose short-term contracts, if any (BLL, CCK 10-K).

Conclusion

The threat of substitute products for this industry is mixed-high. Through

the use of short-term contracts, companies in the P&C industry create some

29

barriers to substitution. However, the limited duration and lack of indirect

expenses minimizes their production. Therefore, customers can be expected to

substitute packaging and containers if a better price/quality product is offered.

This should increase the degree of price-taking behavior in the industry.

Bargaining Power of Suppliers

The bargaining power of suppliers is determined by the price sensitivity

and relative bargaining power. These factors are primarily affected by the

number of available suppliers and the availability of raw materials needed for

production.

Supplier Concentration

In the P&C industry, most of the input goods are plastics, resins, and types

of metal, which are sold by a large number of different suppliers (ATR, CCK,

SLGN 10-K). Since these goods are similar to a commodity in terms of price, the

supplier will have very-low bargaining power.

However, the P&C industry also uses specialized products, such as the

aerosol valve, which are sold by a limited number of “specialized” suppliers. We

believe the points of emphasis are that there are few suppliers, which are all

specialized. This should give these suppliers high bargaining power unless the

input is easily substituted. Yet, firms cannot easily substitute aerosol valves and

other specialized products, which maintains the high bargaining power.

30

Conclusion

We find that the bargaining power of suppliers is mixed-low. Although

some suppliers for specialized inputs have high bargaining power, this accounts

for a small percentage of the overall input costs. Therefore, we gave it mixed-

low since the rest of these suppliers have low bargaining power.

Bargaining Power of Customers

The bargaining power of customers is determined similar to that of

suppliers. Customer’s mainly get their bargaining power from the number of

suppliers and the diversity among suppliers.

Competitor Concentration

As stated earlier, the P&C industry is highly saturated with local and

international competitors. Furthermore, the market is highly competitive with

relatively homogenous goods. This means that customers can easily choose a

different P&C company if they are unhappy with the price or quality of another.

This effect is magnified since there are low substitution costs for doing so (as we

showed earlier).

Conclusion

Customers of the P&C industry have high bargaining power. We believe

this because the industry has thousands of competitors that all provide similar

31

products. The high bargaining power of customers should further contribute to

the P&C industry’s price-taking behavior.

Porter’s Five Forces Conclusion

The P&C industry is a part of the basic materials sector. This sector is

known for its low cost, high output behavior like the P&C industry. This focus on

low cost output is a result of price-taking behavior. As shown above, the P&C

industry has high rivalry among existing firms, mixed-high threat of substitutes,

and high customer bargaining power. These three factors all contribute greatly to

the price-taking behavior, especially rivalry among existing firms. Although there

is a low threat of new entrants, this does not offset the high rivalry among

existing firms. Lastly, although the industry’s suppliers have mix-low bargaining

power, it is often transferred to the more influential customer’s bargaining

power. We will use our determination that the industry is a price-taker to predict

what factors determine success in the industry, and what strategies firms will use

to gain these competitive advantages.

32

Key Success Factors

We used our industry analysis to determine what strategies will be most

effective for a P&C company to use. Since the P&C industry is price-takers, firms

should focus on cost-leadership and differentiation. Firms should prioritize

competitive advantages that help them achieve the relevant key success factors.

We discovered that all firms discussed cost-leadership and differentiation

in their business strategy. Each firm described how they had multiple suppliers

for the majority of their raw materials, but relied on a few suppliers for some

inputs. Firms also mentioned in the 10-K how they were focusing on local

markets for faster delivery.

By prioritizing cost leadership companies are able to manage costs through

tight cost controls. In order to have tight cost controls, firms will focus on

minimizing input costs, distribution costs, and efficient manufacturing. Firms

should actively manage input costs by finding low cost suppliers and partnering

with their supplier when appropriate. Maintaining low distribution costs depends

on appropriate facility placement and forecasting demand. Finally, by having as

efficient of a manufacturing process as possible, firms can convert their inputs to

finished goods without unnecessary expenses, delays, or defects.

Firms should differentiate themselves from their competitors because it

should help with customer retention. Firms do not compete on quality because

customers demand high quality products without defects (BLL, CCK 10-K).

Therefore, we believe firms can differentiate themselves by having flexible

delivery. This would allow the firm to package or produce a container, and

deliver it to its destination in less time than its competitors (at a similar price-

point).

33

Industry’s Competitive Advantages

Low Input Costs

The P&C industry has a sufficient supply of the raw materials (plastic

resins, rubber and certain metal products) used in the production of packages

and containers from existing and alternate suppliers (ATR, BLL, CCK, SLGN 10-

K). Across the industry raw materials accounts for nearly 40% of total

inventories, which is why it is important for firms closely manage their input

costs (ATR, CLL, SLGN 10-K). The lower input costs will either transfer into lower

prices, which should increase volume, or higher margins which would increase

overall profitability.

Low Distribution Costs

It’s important for companies in the P&C industry to keep distribution costs

as low as possible to avoid unnecessary overheads. This becomes even more

important when a firm operates internationally, like all of the firms in our sample.

Most firms in the industry use one of two strategies for production, which will

have a significant impact on distribution costs. For firms that mainly produce in

Asian countries for the lower input costs, (especially labor) they can expect to

have higher distribution costs when shipping elsewhere. However, firms that

manufacture in many different geographic areas can expect lower distribution

costs since the finished goods will originate significantly closer to the destination.

34

Efficient Production

Through efficient production firms can maintain control of the material and

time waste in manufacturing. In the P&C industry the main initiatives to maintain

efficiency is to close unnecessary facilities (ATR, CCK, SLGN 10-K). Although it

could include anything that decreases waste or increases output such as: the

purchase of new equipment, changing the layout of the facilities, or outsourcing

parts of the production process; facility closure is one of the most significant

policies firms use for efficient production.

Flexible Delivery

Flexible delivery is one of the only relevant differentiators in the P&C

industry. Since the industry’s customers demand high quality, defect-free

products, firms cannot differentiate themselves through quality. However, the

customers of packages and containers can sometimes demand rapid production

and delivery, which is why having an efficient production chain with short lead

time and fast shipping can help a firm gain a competitive advantage.

Conclusion

We believe that a company’s success will depend on which competitive

strategy they use and how well they implement it. For the P&C industry we

believe that cost leadership is significantly more important than differentiation.

Although a firm can try to set itself apart, that advantage is eroded rapidly by a

competitor with lower prices. Despite the importance of cost controls,

maintaining high quality products with flexible delivery cannot be forgone.

35

AptarGroup’s Competitive Advantages

The packaging and container industry is highly competitive with large firms

operating internationally and thousands of competitors operating in limited

geographic areas. Therefore, it is necessary for AptarGroup to focus on the key

success factors that drive this industry. If AptarGroup’s competitive advantages

align with the industry’s competitive advantages, then we would feel comfortable

with AptarGroup’s strategic goals.

Production Process

AptarGroup focuses on its ability to manufacture high-quality silicone and

elastomer products quickly. AptarGroup has recently closed two of its facilities,

affecting over 200 employees in order to remove overhead (ATR 10-K).

Furthermore, AptarGroup uses a logistics model, which keeps the production

facilities near the suppliers, and then stores the finished inventory near the

customers’ location. This helps AptarGroup realize the key success factors of low-

input costs and efficient production.

Geographic Diversity

As stated earlier, firms can focus on minimizing production costs by

focusing on Asian countries, or firms can prioritize low distribution costs and

short lead-times. To this end, AptarGroup prioritizes its distribution channels. By

operating factories and warehouses across the globe, AptarGroup can minimize

the distribution costs of receiving inputs and shipping finished goods. This helps

AptarGroup focus on the key success factors of low-distribution costs and flexible

delivery.

36

Local Production

As stated, AptarGroup not only stores its inventory globally, but it

produces it locally. This local production has been reported to result in higher

quality products and better customer service. Although neither of these are

supported by facts nor are they key success factors, it has the potential to

provide an advantage. However, local production does give AptarGroup the

ability to produce finished goods closer to their destination, which reduces lead-

times and reduces shipping costs. This helps AptarGroup meet the key success

factors of efficient production, low-distribution costs, and flexible delivery.

Accounting Analysis

The accounting policies utilized by a firm can have the ability to alter the

actual value of the firm. Firms in different industries each have a broad degree of

flexibility when choosing their accounting policies and can possibly distort the

investor’s idea of the firm when examining the financial statements. Due to this

fact, we will be carefully examining the accounting policies used by Aptargroup

and its competitors in the packaging and containers industry.

The accounting policies used by firms can be broken into two parts: Type

One and Type Two accounting policies. We will first describe and examine the

Type One accounting policies in the following section. Type Two accounting

policies for the firms when then follow after.

37

Type One Accounting Policies

Type one accounting policies are directly related to the firm’s key success

factors and how they implement these to compete in the industry. For the

Packaging & Containers industry these include: low input costs, low distribution

costs, and efficient production. These are factors of cost leadership to create a

competitive advantage.

Reviewing these factors will allow us to evaluate how firms in this industry

gain and keep a competitive advantage. This will also allow firms to retain and

increase their customer base, instead of losing them to the competition.

Low Input Costs

The packaging and containers industry contains competitors that are

always attempting to beat out each other with a low input cost strategy. This

strategy involves firms buying their raw materials to make their products at a

very low cost and generating a high gross profit from it. Firms favor a high gross

profit because this means the cost of goods sold is a lot less than the net sales

generated from the product sold. We will be using the gross profit margin to

examine which firms have the lowest input costs. The gross profit margin is

calculated by dividing gross profit by net sales for the year. Below is a table

showing our results.

As shown above, Aptargroup dominates each of the other competitors for

this industry with the highest gross profit margin. Aptargroup was able to

38

generate a high enough sales with a very low cost of goods sold resulting in

higher gross profits for each of the years examined. Aptargroup’s 10-K reveals its

input costs include resin, metal, anodization costs, transportation and energy

costs, but does not go any further disclosing the costs of each. The other

competitors do not reveal their actual raw material costs for the years in their

10-Ks.

Low Distribution Costs

The packaging and containers industry is a competitive industry and any

competitive advantage that can be acquired by a firm is very critical to exploit

like low distribution costs. Aptargroup has a very low distribution costs and

allows the firm to gain a competitive advantage over the firm's competitors. “The

majority of the Company’s products shipped from the U.S. transfers title and risk

of loss when the goods leave the Company’s shipping location. The majority of

the Company’s products shipped from non-U.S. operations transfer title and risk

of loss when the goods reach their destination” (ATR 10-k). With this method of

shipping products, Aptargroup is able to acquire a low distribution cost because

they aren’t responsible and won't suffer a loss if the products don't reach their

destination in the United States. The other competitors still retain the title and

risk of loss until the products reach their destination in the United States. This

allows Aptargroup to stand out from the competition by not tying up cash to

distribute its products over the United States.

39

Efficient Production

Another important factor for firms to obtain is efficient production so they

can improve their competitive advantage. Efficient production is a crucial factor

for this because the more products that can be made in a quicker amount of

time will greatly affect annual sales. Aptargroup has technical expertise in

injection molding, robotics, clean-room facilities and high speed assembly. The

firm uses high speed equipment to create the pumps and aerosol valves used in

its products. This allows for a small amount of time to be used to finish the final

products and prepare them for sale. The production requirements set by the firm

have always been met on time by its manufacturing facilities resulting in no back

orders for products and satisfied customers in a timely manner. Aptargroup’s

plan to optimize production was completely met in 2014 with incremental cost

savings.

Type Two Accounting Policies

Type two accounting policies reflect the accounts managers have flexibility

over. The degree of flexibility when creating these financial statements varies

greatly across the different industries firms compete in. These accounts include

goodwill, research and development, foreign risk, and operating leases. We will

examine these policies because they can be used to hide material information

about the company that investors need to know about in order to make

beneficial decisions. If any accounts is above the certain benchmarks set by the

GAAP, we will later restate those accounts in order to make them reflect their

actual true value.

40

Goodwill

Goodwill is an intangible long-term asset that arises when one firm buys

another entire firm. The amount of goodwill is determined by the total cost of

acquiring another firm subtracted by the sum of the fair market value of the

tangible assets and the liabilities acquired during the purchase. This value of

goodwill is then reported under the intangible assets on the firm’s balance sheet.

Goodwill needs to be impaired if the carrying value of goodwill exceeds the

original fair value of goodwill at the time of the acquisition. If goodwill is not

checked each year for impairment, this will possibly distort the firm’s financial

statements. If not correctly impaired, the goodwill account may be overstated

and the firm’s expenses will be understated, resulting in an overstatement of the

firm’s net income.

Aptargroup evaluates the amount of its goodwill on a unit level annually or

if there is evidence of potential impairments. Aptargroup did not report any

impairments of its goodwill for the years except in 2014-2015 and the amounts

can be seen in the table below.

Research and Development

Research and Development is the account with the total cost a firm incurs

when they create or innovate their products in order to boost annual sales. The

GAAP requires all research and development costs to be expensed each year.

Firms rather favor the capitalization of research and development because this

will reduce their operating expenses. The downside of high research and

development costs is that the new or innovated product can fail resulting in a big

41

loss for the firm. Research and development is a vital factor in the packaging and

containers industry to boost sales. Below is a table showing the research and

development costs incurred by the firms being analyzed.

As shown above, Aptargroup invests the most money in its research and

development compared to the competitors. Even though Aptargroup invests the

most, it still has the lowest annual sales each year, which may be an indication

of Aptargroup investing too much into this department without receiving the

benefits of it. Silgan Holdings didn’t disclose its research and development costs

for the years analyzed because they reported the costs as not material

information. This can be misleading to investors because Silgan Holdings may

have over or understated its net income. Ball Corporation generates the highest

sales each year even though they invest the least amount of money into the

research and development department.

Foreign conversion risk

For companies whose sales are largely driven by foreign business, there is

risk when converting the revenue back into their domestic currency. In some

instances, it can significantly reduce income. Within the P&C industry this has not

historically been the case, despite the majority of sales being generated outside

the U.S. We discovered that the industry reports their foreign conversion hedging

strategies, which explains the low losses from forex. The degree of reporting was

nearly identical across the industry for foreign conversion exposure (ATR, BLL,

CCK, SLGN 10-Ks).

42

Operating leases

When negotiating the use of fixed assets, a firm often chooses between

operating and capital leases. Unlike a capital lease, the operating lease does not

grant ownership rights (and liabilities), so it does not show up on the balance

sheet as an asset or a liability. When operating leases are a significant part of

short-term contractual obligations, it can indicate that management is trying to

avoid the impact expected on the balance sheet. In these instances it could be

necessary to account for this effect.

As shown above, operating leases average around 5% for the industry.

Aptar is slightly higher than the industry with an average around 8% (ATR, BLL,

CCK, SLGN 10-Ks). Regardless, all these values are insignificant enough that we

believe it will have little-to-no effect on our valuation.

Conclusion

We have analyzed the Type Two Accounting Disclosures to discover which

accounts need to be restated for our valuation. Of the Type Two disclosures:

goodwill, R&D, foreign conversion risk, and operating leases, only goodwill needs

to be restated.

43

Accounting Flexibility Assessment

Depending on industry policies, companies can have very different degrees

of flexibility. In industries with a high degree of flexibility, companies can exploit

the flaws in GAAP and report their financials in a way that is most favorable to

them . The GAAP sets the accounting standards for firms to follow and the

Financial Accounting Standards Board regulates them. We will analyze the

degree of flexibility of Aptargroup and its’ competitors on how they report their

financial accounts including: goodwill, research & development, and operating

and capital leases.

Goodwill

Goodwill is generated when a firm mergers with another firm and is

reported as the intangible asset account categorized as a long term asset. This

can be used to measure the competitive advantage acquired by the firm that is

taking over the other. Goodwill impairment arises when the goodwill fair value is

smaller than the goodwill carrying value and should be accounted as an expense

on the income statement and decrease the goodwill asset value on the balance

sheet. GAAP’s standard for impairment testing is at the reporting unit - either an

operating segment or one level below.

Firms have a high degree of flexibility with the goodwill account. It falls on

the management to determine if and how often to check for goodwill

impairment. They also determine the amount of years to amortize goodwill and

the amount of years can affect the financial statements’ values. A firm’s earnings

can be overstated if the impairment test wasn’t correctly conducted and can

distort an investor’s idea of a firm.

44

Research and Development

Research and development are critical factors for a firm to maintain and

add to their competitive advantage over the competition like new products,

innovated products, or facilities. The GAAP general rule for the research and

development costs should be charged to the operating expense section on the

income statement due to the fact of unpredictable future benefits.

Firms have little flexibility over the research and development costs

because GAAP clearly define and lines out the criteria for this account. Firms

would rather capitalize these costs due to the unpredictable future benefits, but

cannot due to the general rules set by GAAP.

Capital vs. Operating Leases

The degree of flexibility for operating and capital leases is high for how the

leases are reported on the financial statements of a firm. A small level of risk is

transferred for ownership to the firm when the firm uses capital leases and is

reported as an asset and liability on firm’s balance sheet. The asset is

depreciated and the interest expense is reported as a liability for the lease

payments each year on the balance sheet.

An operating lease transfers only the right to use property to the firm for a

time period that was agreed upon, but the risk of ownership is not taken over by

the firm. The lease expense is included in the operating expenses on the income

statement and doesn’t change the balance sheet values.

Firms favor using operating leases over capital leases because the lease

payments aren’t reported as a liability, but instead reported as an operating

expense. Also, the operating lease does not appear on balance sheet, therefore,

not increasing the liabilities or assets.

45

Conclusion

Firms have a high degree of flexibility when it comes to goodwill and

capital vs. operating leases. They have a low degree of flexibility with the

research and development costs because the GAAP clearly sets the rules for this.

Since firms have a high degree of flexibility with the two accounts stated earlier,

it is very important to see how they report those accounts and may have to

possibly restate the financial statements.

Evaluation of Actual Accounting Strategy

GAAP’s full disclosure principle requires firms to report all information that

will affect the understanding of their financial statements must be noted with

them. The GAAP clearly defines the minimum amount of information required to

be disclosed by firms. Disclosures of firms are classified as either high or low,

and depending on the classification of disclosure of a firm will greatly impact the

idea an investor has about the firm. The management decides on what

information is material and can sometimes be abused to not show some of the

information that may be vital for investors.

Aggressive and conservative accounting strategies is another vital factor

firms choose between in a way for firms to report their financials that is

favorable to them. Companies are able to report either low yearly earnings using

a conservative strategy or high yearly earnings using an aggressive strategy

depending on the recognition of expenses and revenues at different times.

Revenues are recognized later than expenses during the year under a

46

conservative strategy, conversely; revenues are recognized earlier than expenses

during the year under an aggressive strategy.

Goodwill

Goodwill is one type of the intangible assets owned by a firm and is a

categorized as a long term asset in that section on the balance sheet. Firms have

an incentive to maximize goodwill to improve leverage ratios and asset value.

However, this incentive can compromise the firm’s quality. Aptargroup examines

the goodwill account values annually or if there is evidence of impairment

potentially. Its’ impairment test requires critical judgment on factors like changes

in market conditions or unit cash flows that could materially affect the operating

results.

Within the packaging and containers industry, the representativeness

threats we observed were irregular amortizations and short justifications in the

notes disclosed. Aptargroup had average reporting policies towards both of these

issues (ATR 10-k). Aptargroup did not perform the annual two-step impairment

test for goodwill for the years analyzed. Although firms like Crown Holdings had

not amortized goodwill in the past five years; they spent the most time justifying

the accumulation of goodwill (CCK 10-K). This is in contrast to Ball Corporation

who has amortized goodwill more regularly than any of other competitors

analyzed, but only barely discussed the advantage created by their goodwill (BLL

10-K).

Research & Development

Research and Development costs are able to provide competitive

advantages over a firm's competition by providing new or innovated products to

the market. These costs are incurred as an expense with a firm’s hopes of the

47

cost returning future economic benefits. Aptargroup has the most money

invested in research & development and raises cause to look how it is

amortized. We found that we needed to restate Aptargroup research &

development expenses because not enough was be amortized each year to

reflect the true value. Below is a table showing our results for the restated R&D

expenses for the years analyzed.

After the restatement of this expense, Aptargroup’s income statement

better reflects the firm’s true value and will be very helpful in this valuation

analysis.

Operating Leases

Operating leases can provide significant advantages over capital leases.

Since operating leases only show on the income statement, they can be closed

so they won’t affect valuation ratios. Normally this isn’t an issue unless the

operating leases are significant portion of contractual obligations. When

operating leases are a large percentage, it can be an indicator that management

is trying to hide its obligations from the balance sheet.

48

Within the P&C industry, operating leases account for 6% of contractual

obligations on average. We do not consider this abnormal, and with ATR just

above the average we feel no need to restate their statements for this account

(ATR, BLL, CCK, SLGN 10-K).

Quality of Disclosure - Type One

Type One Accounting Policies can be defined as accounting policies based

on key success factors. These reporting practices are used throughout the

industry in regard to the key success factors. In order to ensure that

AptarGroup’s disclosure of type one accounting policies provide enough

information for readers of their 10-K to make well informed decisions, we will

compare its quality of disclosure to that of it’s competitors. These competitors

will include Ball Corporation (BLL), Crown Holdings, Inc. (CCK), and Silgan

Holdings, Inc. (SLGN)

Efficient Production

The industry relies on efficient production to drive all costs down. If a

company is unable to produce their products efficiently, then the firm inturn will

not be competitive and be forced to leave the industry. The packaging and

containers industry requires a lot of cost cutting and PP&E to create efficient

production. The 10-Ks of AptarGroup and its competitors clearly state how they

are able to produce efficiently and the contingencies that allow them to have a

competitive advantage. These contingencies are stated clearly in the financials

along with which costs they are able to cut due to great efficient production.

49

Low Input Costs

Input costs control is an essential factor for companies in the packaging

and containers industry, which will always compete on cutting costs. However,

Aptargroup gives very few details on its input costs which make it hard to

interpret. The industry has several ways of receiving timber, and in Aptargroup’s

financials it does not state how and if they bought the timber with the lowest

price. It would be necessary to know whether they were purchasing products in

less developed countries or how much it could have saved buying from another

source to be able to tell if Aptargroup is doing everything they can to keep their

input costs minimized. Aptargroup also does not disclose that the price of timber

which has been volatile recently.

Distribution Costs

AptarGroup and its competitors clearly present the risk associated with

distribution cost. Spikes in the cost of gasoline are a potential threat to its

distribution costs. 10k’s in the Industry are not very detailed about the actual

value of each individual shipping expense. It would be easier to compute the

actual risk of increasing fuel costs if these notes were disclosed. The quality

disclosures of hedging fuel costs would be a great advantage to help in creating

an genuine valuation. We decided that the quality of disclosure on distribution

costs is low.

50

Quality of Disclosure – Type Two

Type Two Accounting Disclosures are accounts that give management

discretion over reporting. GAAP allows accounts such as goodwill, operating

leases, R&D, and foreign currency to be reported in favorable ways for the

company. Although not misrepresentative, when these accounts are reported

aggressively it can significantly alter our valuation of the company.

The risk of distortions is significant enough that we will test each of these

for representativeness. If any account tests too aggressively then we will restate

the financial statements for an accurate analysis.

Goodwill

Goodwill can be defined as the excess price paid for a company from the

company’s market value. AptarGroup’s goodwill accounts for 39% of net fixed

assets on average. This goodwill balance is the result of multiple mergers and

acquisitions Aptargroup undertook. Aptargroup acquired Mega Airless, which

significantly increased the value of goodwill. Since Aptargroup has not been

amortizing the goodwill balance from the acquisitions, it has grown to a sufficient

level to distort the financials.

51

The table above shows the significance of goodwill on net fixed assets

before and after restatement. When we restate goodwill, the account loses

around 10% of its value, while accounting for 3% less of net fixed assets (ATR

10-K). We believe this section makes Aptargroup look slightly overvalued.

Research and Development

No company in the P&C industry shows sufficient detail for research and

development. All firms in the industry combine SG&A with R&D, which keeps us