Financial Statement Analysis: Presented by: Ng Wen Ying Wang Si Jie (Jessie) Wu Shan Cao Ya Jie

Financial statement analysis of sing post (part 2)

Jul 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Statement Analysis:

Presented by: Ng Wen YingWang Si Jie (Jessie)Wu ShanCao Ya Jie

Singapore Post Limited

About SingPost• Commonly abbreviated as SingPost• Subsidiary of Singapore Telecommunications

Limited• Singapore’s designated Public Postal Licensee• 3 main businesses

Overview of Company and Industry

Mail Digital Services

• Domestic & International Mail

• Philately & Stamps

• Hybrid Mail

• Digital Services

Logistics

• Courier: ‘Speedpost’

• E-Fulfilment

• Warehousing, Fulfilment & Distribution Freight

• Self-Storage

Retail & Financial Services e-Commerce

• Agency Services

• Financial Services

• E-Commerce

Industry Characteristics• Letter business in decline; Parcel (e-commerce) business growing• Porter’s five analysis shows relatively low rivalry within industry

AdjustmentsOperating lease

Assumptions:• the discount rate is cost of debt (1.64%).

𝑅 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡 =interest expense

(𝑇𝑜𝑡𝑎𝑙 debt2013+𝑇𝑜𝑡𝑎𝑙 𝑑𝑒𝑏𝑡2014)/2

• the payment after 2019 make the full payment at 2020.

Adjust for operating leasePV of Operating Leases at Singpost In 2014

Commitments Discounted factor PV of Operating lease2015 19.3 0.98 18.932016 9.4 0.96 9.052017 9.4 0.94 8.882018 9.4 0.93 8.712019 9.4 0.91 8.54

Thereafter 31.3 0.89 27.91Total 88.20 82.02

AdjustmentsOperating lease

capitalize the operating Leases of Singpost In 2014

beginning net book value

depreciationexpense

accumulateddepreciation

ending net book value

2014 82.017 16.403 16.403 65.614

2015 65.614 16.403 32.807 49.210

2016 49.210 16.403 49.210 32.807

2017 32.807 16.403 65.614 16.403

2018 16.403 16.403 82.017 0.000

Assumptions:• Straight-line method • Salvage value = 0• Estimated useful life = 5yrs

AdjustmentsOperating lease

Assumptions:operating lease = imputed interest expense + depreciation,

FS Adjustment done Final Effect

IncomeStatement

• Plus operating lease expense(+18.858)• Minus interest expense(-16.403 )• Minus depreciation(-2.455)

None

BalanceSheet

Assets• Add capitalized Leases(+82.017)• Minus depreciation(-16.403)

• Increase assets (+65.614)

• Increase liabilities(+65.614)Liabilities • Add ending book value(+65.614)

Equity • No change

Statement of Cash Flow

• Move principal payments from operating CF tofinancial CF (17.3 )

Principal Payment= Lease payments - Begin Lease Liability * Interest Rate

• Changes in capital Expenditure offsets changes in net debt

• OCF decrease(-65.614)

• FCF increase(-65.614)

• FCFE: no change

AdjustmentsOther adjustments

• Intangible Assets

FS Adjustment done Final Effect

Balance Sheet

Assets • Minus goodwill(-167.202) • Minus other Intangibles(-16.423)

• Decrease assets (-183.625 )

• Decrease liabilities(-183.625 )

Liabilities • No change

Equity • Minus goodwill(-167.202)• Minus other Intangibles(-16.423)

• InventoryAverage cost method

• PP&EUseful life is close to industry average

Income Statement AnalysisRevenue and Operating Profit Breakdown

Revenue from Mail increasesover years, but operatingprofit from Mail shows nosignificant change.

Revenue from Logisticsincreased a huge amount, butthe operating profit didn’tshow a responding increase.

Income Statement AnalysisSegment Operating Profit Margin

Mail is much profitablethan other two segment.

Income Statement AnalysisExpenses Breakdown

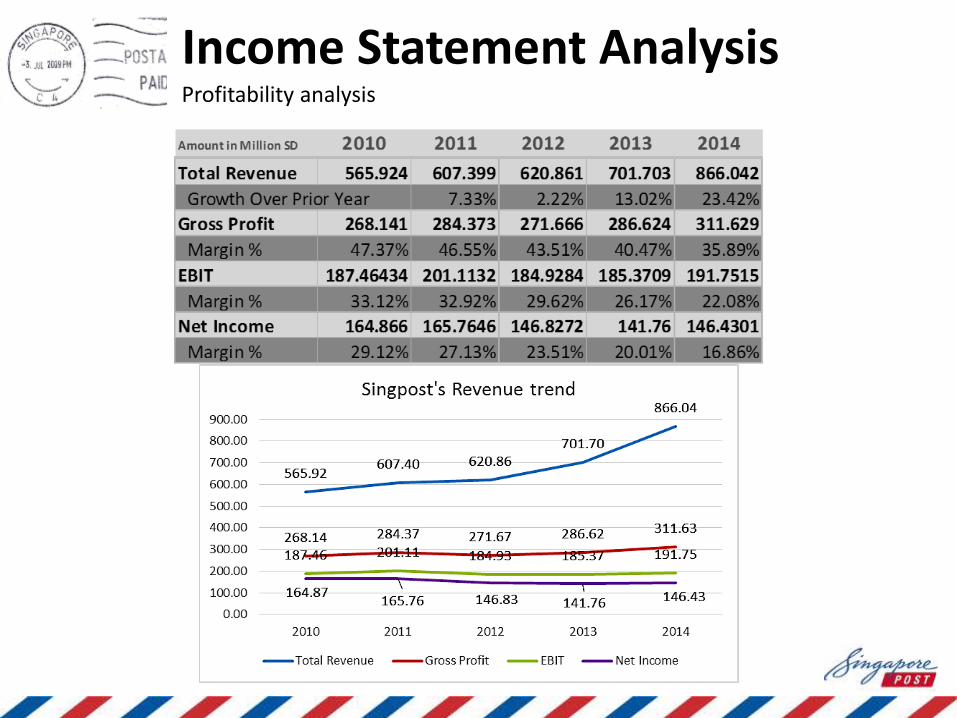

Income Statement AnalysisProfitability analysis

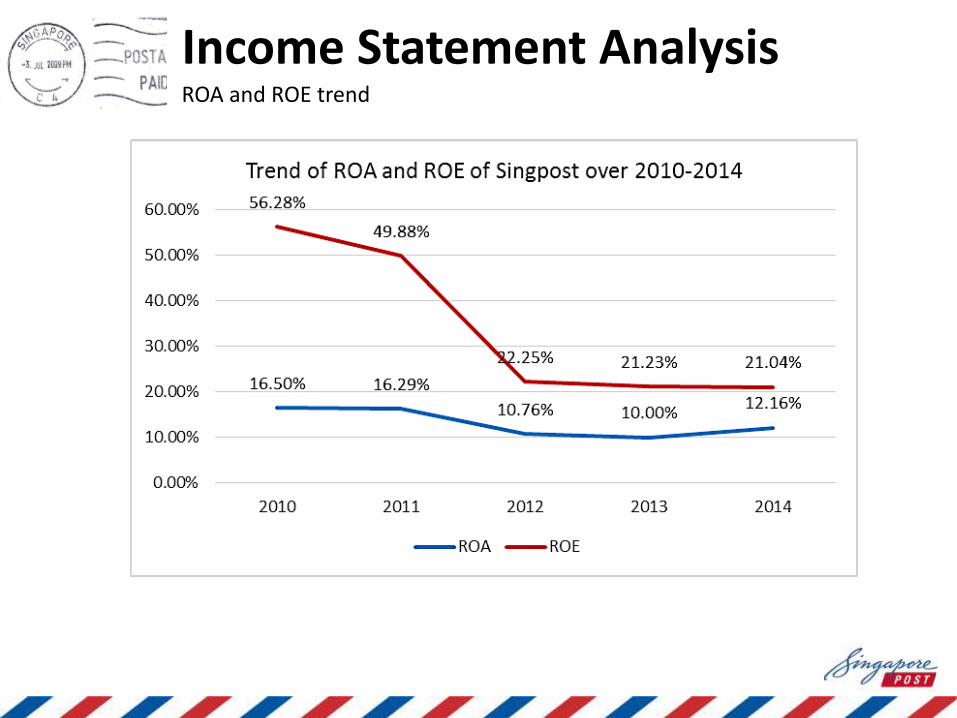

Income Statement AnalysisROA and ROE trend

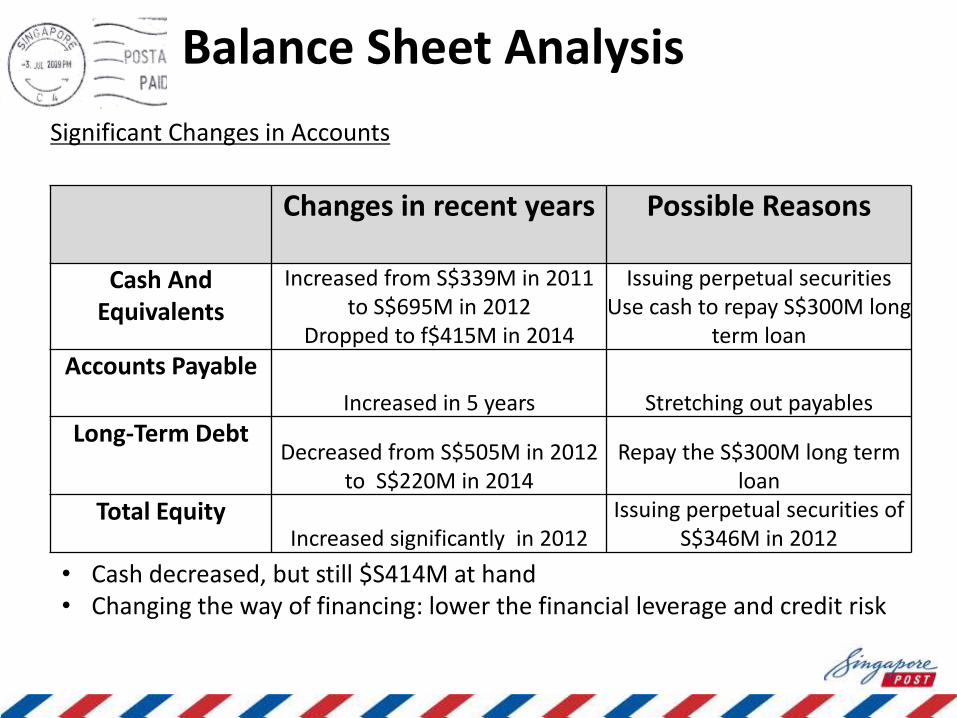

Significant Changes in Accounts

Changes in recent years Possible Reasons

Cash And Equivalents

Increased from S$339M in 2011to S$695M in 2012

Dropped to f$415M in 2014

Issuing perpetual securities Use cash to repay S$300M long

term loan

Accounts Payable

Increased in 5 years Stretching out payables

Long-Term DebtDecreased from S$505M in 2012

to S$220M in 2014Repay the S$300M long term

loan

Total EquityIncreased significantly in 2012

Issuing perpetual securities of S$346M in 2012

• Cash decreased, but still $S414M at hand• Changing the way of financing: lower the financial leverage and credit risk

Balance Sheet Analysis

(500.0)

(400.0)

(300.0)

(200.0)

(100.0)

0

100.0

200.0

300.0

400.0

Mar-31-2009Mar-31-2010 Mar-31-2011 Mar-31-2012 Mar-31-2013 Mar-31-2014

Cas

hA

mo

un

t Cash from Operation

Cash from Investing

Cash from Financing

Net Change in Cash

• Net changes in cash and changes in financing cash flow were more significant and fluctuant than that of operating cash flow and investing cash flow. Trend of net changes in cash was mainly decided by the changes from financing activities

Cash Flow AnalysisChanges in Cash Flows

(200.00)

(100.00)

-

100.00

200.00

300.00

400.00

500.00

600.00

2009 2010 2011 2012 2013 2014

FCFF

FCFE

• Significant increase of FCFE in 2010:SingPost issued $S200M loan.

• Steep fall of FCFE in 2014: company repaid the debt of S$315M.

• Although repayment of debt lowered default risk, negative FCFE indicated the company might havetrouble paying shareholderdividend.

• FCFF in 2014 is positive, indicating that the firm has the ability to generated enough profit to cover its costs and investment activities.

Changes in FCFF & FCFEReasons behind the changes

BenchmarksChoice of Comparable Companies

Businesses: Mail, Parcel & LogisticsCoverage: One of the Largest in UKClientele: Businesses, e-commerce users Market Cap: £218.8 million

Businesses: Mail, Parcel & e-CommerceCoverage: Germany’s only universal provider of postal services Clientele: Individuals, BusinessesMarket Cap: €30.12 billion

Ratio AnalysisProfitability

FY 2014 Singapore Post Limited UK Mail Group Deutsche Post AGPerformance RatioGross Margin 35.89% 13.40% 11.40%EBIT Margin 22.08% 4.50% 4.00%Net Income Margin 16.86% 3.40% 3.80%Basic EPS $0.08 ₤0.32 € 1.73

Profitability RatiosReturn on Assets % 12.163% 10.288% 5.894%Return on Equity % 28.588% 24.205% 20.810%Return on Common Equity % 42.219% 24.205% 21.213%

Analysis: - Efficient management of cost of operation.- Ability to withstand downturn is higher versus the comparable.- Drastic difference could be attributed to higher cost of labour in UK

and Germany - Leveraged on technology, less capital-intensive structure and better

returns Higher ROA

Ratio AnalysisLeverage

FY 2014 Singapore Post Limited UK Mail Group Deutsche Post AGSolvency RatiosTotal liabilities% of Total Assets 57.45% 57.50% 71.68%Total Debt/Equity Ratio 1.350 1.353 2.531 Long Term Debt/Equity Ratio 0.558 0.158 0.482 Short Term Debt/Equity Ratio 0.686 1.195 1.207

Coverage RatiosEBIT/Interest Exp. 17.6 227 12.5Debt coverage 0.41 0.29 0.12Interest coverage 49.85 331.00 42.32

Analysis:- Debt ratio similar to peers, less reliance on short-term funding More stable- Interest coverage ratio within industry standards, bearing in mind its lower reliance

on cheaper but less stable short-term funding.

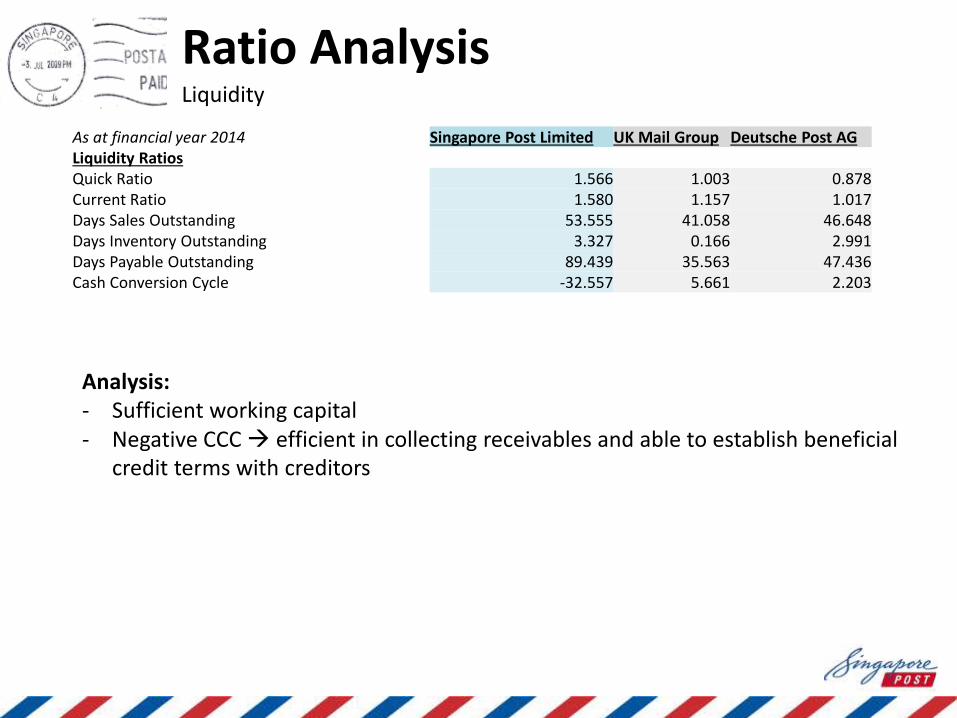

Ratio AnalysisLiquidity

As at financial year 2014 Singapore Post Limited UK Mail Group Deutsche Post AGLiquidity RatiosQuick Ratio 1.566 1.003 0.878 Current Ratio 1.580 1.157 1.017 Days Sales Outstanding 53.555 41.058 46.648 Days Inventory Outstanding 3.327 0.166 2.991 Days Payable Outstanding 89.439 35.563 47.436 Cash Conversion Cycle -32.557 5.661 2.203

Analysis:- Sufficient working capital- Negative CCC efficient in collecting receivables and able to establish beneficial

credit terms with creditors

Ratio AnalysisCash Flow Statement Analysis

As at financial year 2014 Singapore Post Limited UK Mail Group Deutsche Post AGPerformance RatioCash flow to revenue 1.81 1.60 1.37Cash return on assets 0.20 0.16 0.09Cash return on equity 0.37 0.39 0.33Cash to income 1.41 1.22 1.24

Analysis: - Cash flow ratios all slightly better than industry- Cash flow position is healthy and liquidity will not be an issue

Conclusion:- Healthy financials- Coupled with strategic alliance with strong industry players like Alibaba and

a clear direction towards sectors with more potentials (e-commerce, logistics)

- Dividend of $0.025/year Stable investment in the long term ($1.7 $1.92) ✓✓✓

The End

Presented by: Ng Wen YingWang Si Jie (Jessie)Wu ShanCao Ya Jie

Related Documents