Financial Services Compensation Scheme Claims Management: Reimbursement for Insured Depositors Kate Bartlett Director of Operations

Financial Services Compensation Scheme Claims Management: Reimbursement for Insured Depositors Kate Bartlett Director of Operations.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Services Compensation Scheme

Claims Management: Reimbursement for Insured Depositors

Kate BartlettDirector of Operations

• About the FSCS

• Faster Payout reforms • The Single Customer View

• The Change Process

• FSCS experience of Faster Payout using SCV

• Questions

Content of the Presentation

2

3

About the FSCS

About the FSCS

• Who we are: The FSCS is the UK's compensation fund of last resort for customers of authorised financial services firms. We may pay compensation if a firm is unable, or likely to be unable, to pay claims against it. This is usually because it has stopped trading or has been declared in default.

• How we operate: We are independent of the government and the financial industry, and were set up under the Financial Services and Markets Act 2000, becoming operational on 1 December 2001 (although we still cover claims from before this date). We do not charge individual consumers for using our service.

We have come to the aid of more than 4.5 million people since 2001 while paying out over £26bn in compensation.

• What we protect: Deposits Insurance policies Insurance broking Investment business Home Finance

• How we’re funded: The FSCS is funded by the financial services industry. Every firm authorised by the UK regulators is obliged to pay an annual levy, which goes towards our running costs and the compensation payments we make. 4

5

Faster Payout reforms

Background to Deposit Protection Reform - Key Events • September 2007 The ‘Run on the Rock’ – Northern Rock

The Tripartite (HM Treasury, Bank of England and the FSA) published:•October 2007‘Banking reform – protecting depositors: a discussion paper’• January 2008‘Financial stability and depositor protection: strengthening the

framework’ • July 2008‘Financial stability and depositor protection: further

consultation’ • Autumn 2008 - Spring 2009Banking failures in the UK - autumn 2008 and spring 2009

• February 2009Banking Act 2009 set up the Special Resolution Regime 6

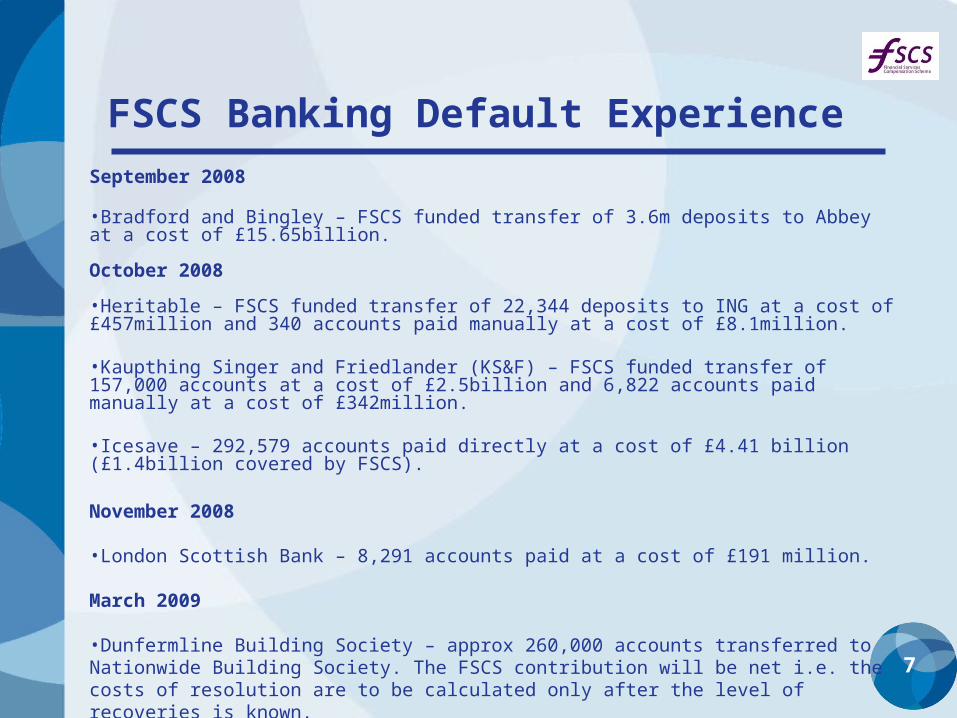

FSCS Banking Default ExperienceSeptember 2008

•Bradford and Bingley – FSCS funded transfer of 3.6m deposits to Abbey at a cost of £15.65billion.

October 2008

•Heritable – FSCS funded transfer of 22,344 deposits to ING at a cost of £457million and 340 accounts paid manually at a cost of £8.1million.

•Kaupthing Singer and Friedlander (KS&F) – FSCS funded transfer of 157,000 accounts at a cost of £2.5billion and 6,822 accounts paid manually at a cost of £342million.

•Icesave – 292,579 accounts paid directly at a cost of £4.41 billion (£1.4billion covered by FSCS).

November 2008

•London Scottish Bank – 8,291 accounts paid at a cost of £191 million.

March 2009

•Dunfermline Building Society – approx 260,000 accounts transferred to Nationwide Building Society. The FSCS contribution will be net i.e. the costs of resolution are to be calculated only after the level of recoveries is known. 7

• All deposit firms must have a “Single Customer View” for eligible depositors holding protected deposits:

— FSCS is entitled to rely on the data provided by deposit takers— Information required for SCV file is detailed in the regulator’s handbook – COMP 17— Firms with more than 5,000 accounts must hold the SCV in an electronic format— SCV must be capable of being produced within 72 hours of a request

• Responsibility for determining eligibility of each product and account held lies with the deposit taker. Eligibility of accounts should be checked on a routine (annually) basis.

• Eligibility of depositors criteria is simplified – but there are still some exclusions.

• Depositors to be reimbursed within 20 days in line with DGSD requirement but additional UK aspiration to pay within 7 days.

• Payout is gross – no off-setting against credit balances, no negative balances are included.

• Balances of all types of account are calculated at date of default.

• Customers do not need to submit an application for compensation.

• Assignment of customers’ rights to FSCS is automatic after payment.

• Insolvency Practitioners must assist FSCS in the execution of its duty

• Raise awareness of FSCS – reinforce consumer protection.

Reform: changes to make Faster Payout possible

8

9

Single Customer View

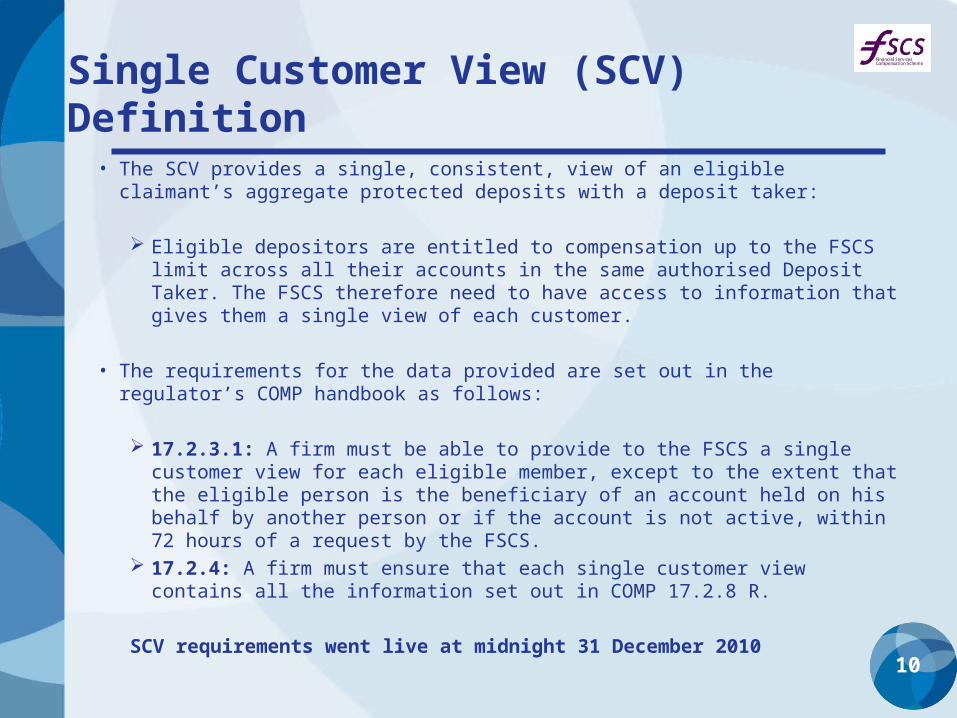

Single Customer View (SCV) Definition

• The SCV provides a single, consistent, view of an eligible claimant’s aggregate protected deposits with a deposit taker:

Eligible depositors are entitled to compensation up to the FSCS limit across all their accounts in the same authorised Deposit Taker. The FSCS therefore need to have access to information that gives them a single view of each customer.

• The requirements for the data provided are set out in the regulator’s COMP handbook as follows:

17.2.3.1: A firm must be able to provide to the FSCS a single customer view for each eligible member, except to the extent that the eligible person is the beneficiary of an account held on his behalf by another person or if the account is not active, within 72 hours of a request by the FSCS.

17.2.4: A firm must ensure that each single customer view contains all the information set out in COMP 17.2.8 R.

SCV requirements went live at midnight 31 December 2010 10

Verifying the SCV

11

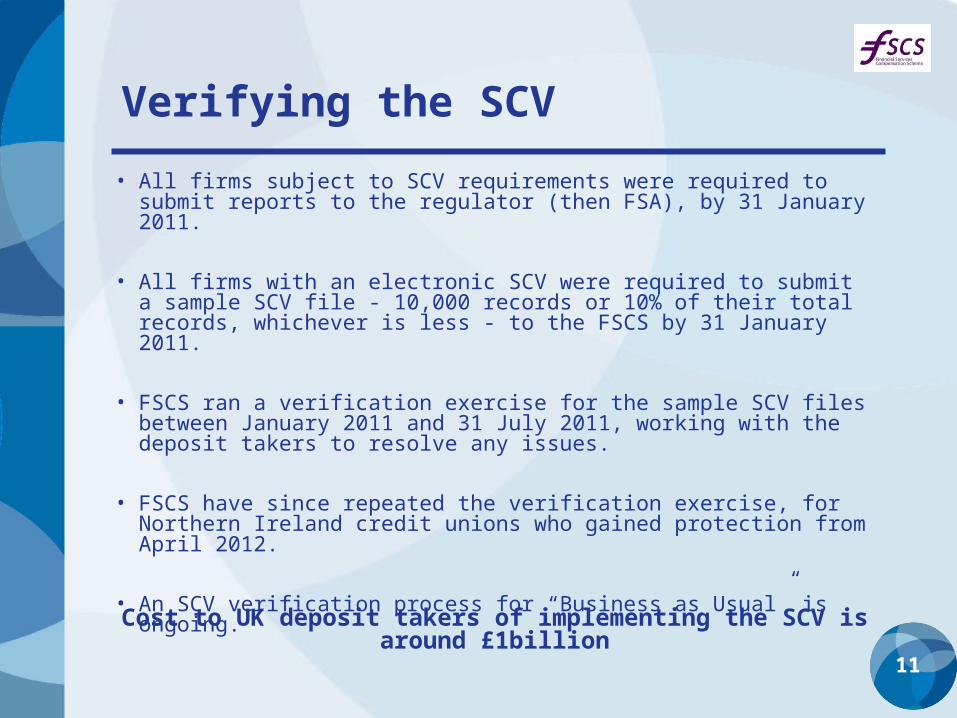

• All firms subject to SCV requirements were required to submit reports to the regulator (then FSA), by 31 January 2011.

• All firms with an electronic SCV were required to submit a sample SCV file - 10,000 records or 10% of their total records, whichever is less - to the FSCS by 31 January 2011.

• FSCS ran a verification exercise for the sample SCV files between January 2011 and 31 July 2011, working with the deposit takers to resolve any issues.

• FSCS have since repeated the verification exercise, for Northern Ireland credit unions who gained protection from April 2012.

• An SCV verification process for “Business as Usual” is ongoing.

Cost to UK deposit takers of implementing the SCV is around £1billion

12

The Change Process

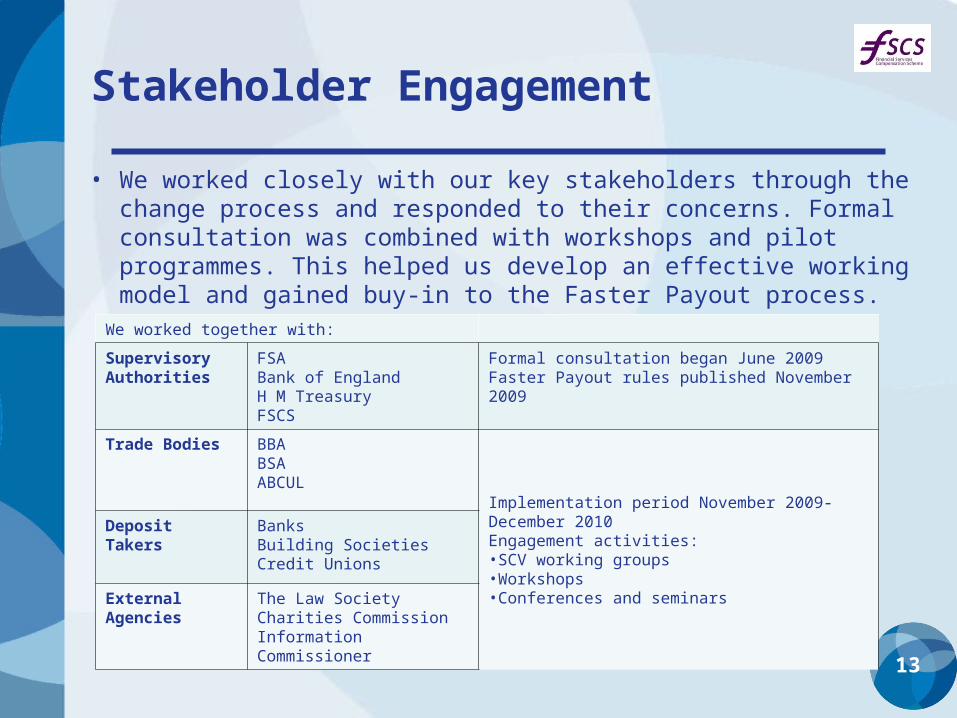

We worked together with:

Supervisory Authorities

FSA Bank of EnglandH M TreasuryFSCS

Formal consultation began June 2009Faster Payout rules published November 2009

Trade Bodies BBA BSA ABCUL

Implementation period November 2009-December 2010Engagement activities:•SCV working groups•Workshops•Conferences and seminars

Deposit Takers

BanksBuilding SocietiesCredit Unions

External Agencies

The Law SocietyCharities CommissionInformation Commissioner

Stakeholder Engagement

13

• We worked closely with our key stakeholders through the change process and responded to their concerns. Formal consultation was combined with workshops and pilot programmes. This helped us develop an effective working model and gained buy-in to the Faster Payout process.

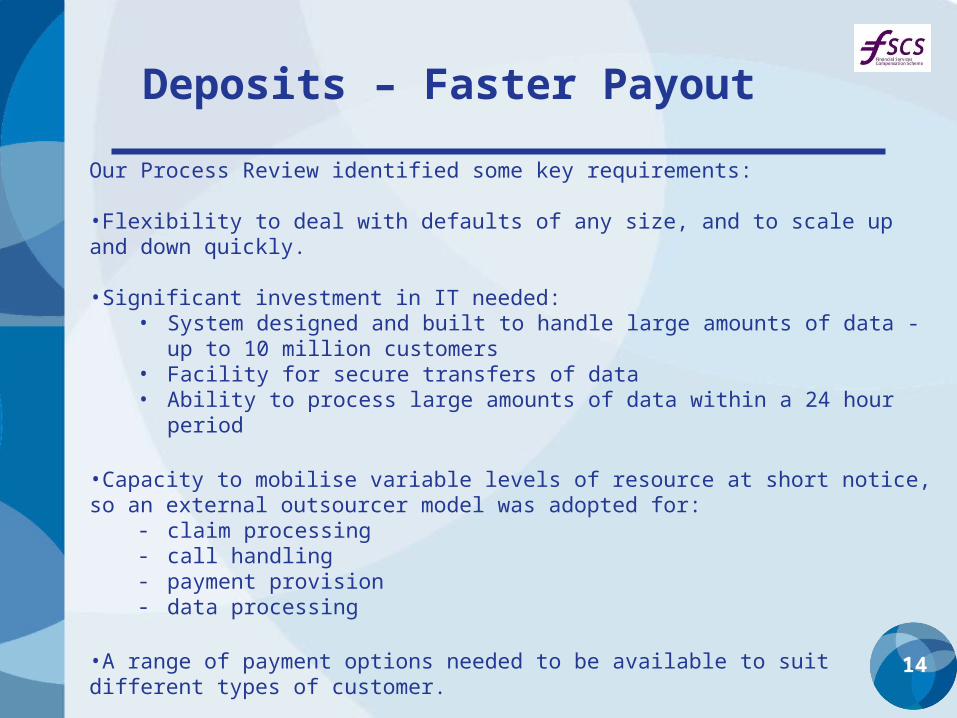

Our Process Review identified some key requirements:

•Flexibility to deal with defaults of any size, and to scale up and down quickly. •Significant investment in IT needed:

• System designed and built to handle large amounts of data - up to 10 million customers

• Facility for secure transfers of data• Ability to process large amounts of data within a 24 hour period

•Capacity to mobilise variable levels of resource at short notice, so an external outsourcer model was adopted for:

- claim processing- call handling- payment provision- data processing

•A range of payment options needed to be available to suit different types of customer.

•Sufficient liquid funds needed to be in place to allow a large payout in days.

Deposits – Faster Payout

14

15

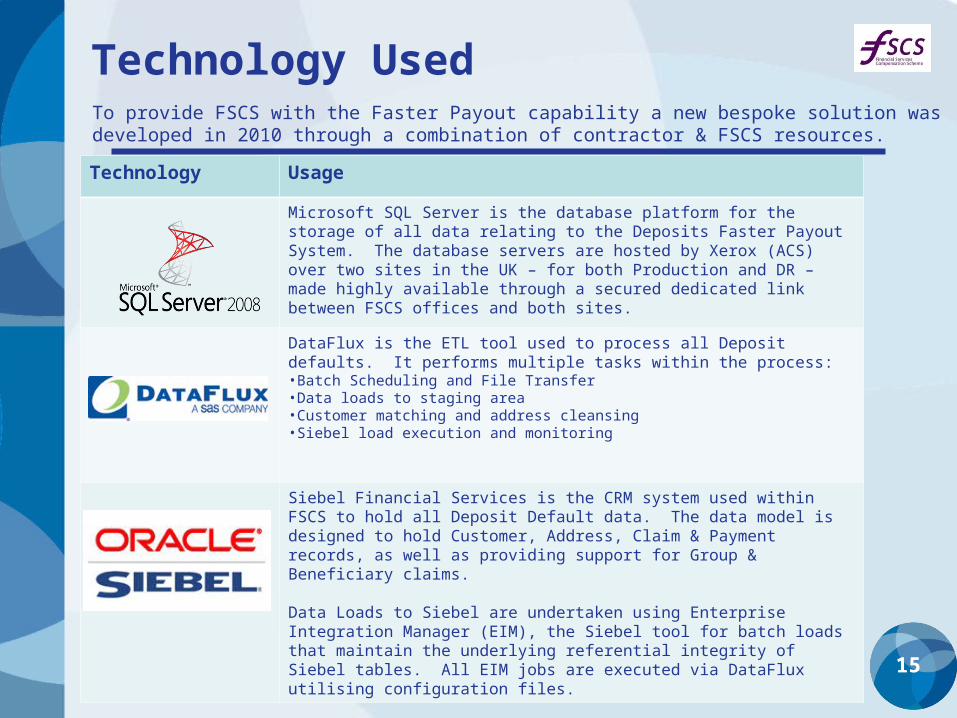

Technology Usage

Microsoft SQL Server is the database platform for the storage of all data relating to the Deposits Faster Payout System. The database servers are hosted by Xerox (ACS) over two sites in the UK – for both Production and DR – made highly available through a secured dedicated link between FSCS offices and both sites.

DataFlux is the ETL tool used to process all Deposit defaults. It performs multiple tasks within the process:•Batch Scheduling and File Transfer•Data loads to staging area•Customer matching and address cleansing•Siebel load execution and monitoring

Siebel Financial Services is the CRM system used within FSCS to hold all Deposit Default data. The data model is designed to hold Customer, Address, Claim & Payment records, as well as providing support for Group & Beneficiary claims.

Data Loads to Siebel are undertaken using Enterprise Integration Manager (EIM), the Siebel tool for batch loads that maintain the underlying referential integrity of Siebel tables. All EIM jobs are executed via DataFlux utilising configuration files.

To provide FSCS with the Faster Payout capability a new bespoke solution was developed in 2010 through a combination of contractor & FSCS resources.

Technology Used

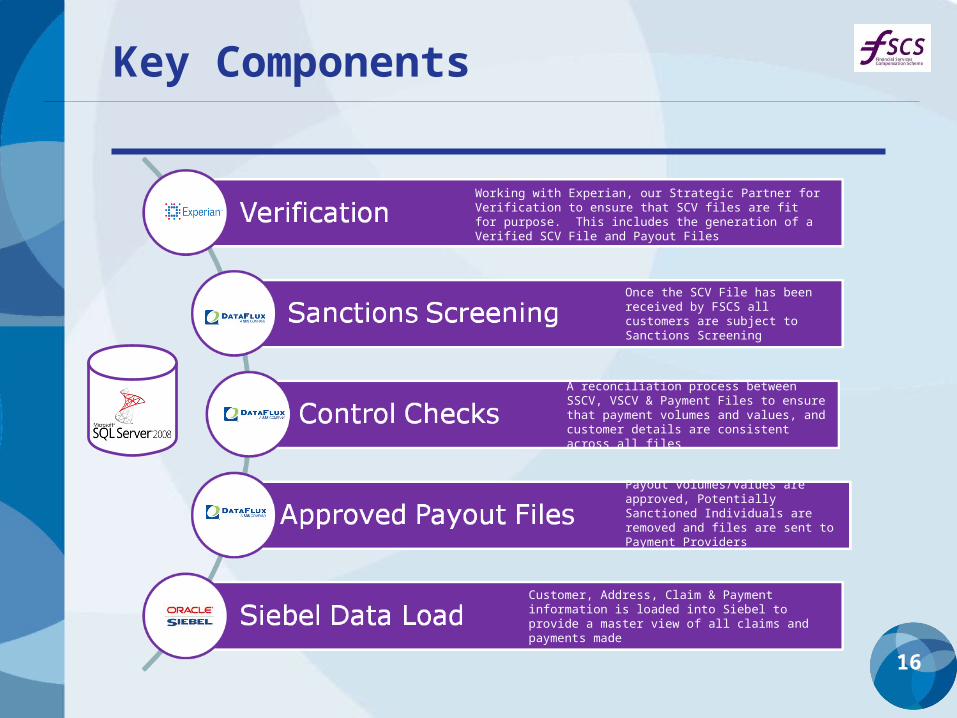

Key Components

16

Working with Experian, our Strategic Partner for Verification to ensure that SCV files are fit for purpose. This includes the generation of a Verified SCV File and Payout Files

Once the SCV File has been received by FSCS all customers are subject to Sanctions Screening

A reconciliation process between SSCV, VSCV & Payment Files to ensure that payment volumes and values, and customer details are consistent across all files

Payout volumes/values are approved, Potentially Sanctioned Individuals are removed and files are sent to Payment Providers

Customer, Address, Claim & Payment information is loaded into Siebel to provide a master view of all claims and payments made

Payout Mechanisms

• There are currently two payment methods available for the payout of claims – Cheque and Cash Over The Counter

Post Office

Cash Over the Counter

• Payments are automatically assigned a particular payment channel, depending upon factors such as value of the claim. The assignment of payments to a particular channel is undertaken by Experian, in the form of payout files, at the same time as the Verified SCV file is produced

• The Cash Over the Counter option has been used on most defaults since it was introduced in January 2011. The cash limit has been set at £1,000 per payment and is the quickest way of reimbursing customers with low value claims

• Work continues on possible alternative payout options

17

18

Our experience of Faster Payout

19

• We have introduced speed and accuracy to payouts and increased customer confidence.

• Although there is an increased element of risk inherent in the new faster process, so far there has been no evidence of inaccuracy by deposit takers.

• Faster Payout process has now been used successfully for the 23 failed deposit firms in the UK since 1 January 2011.

• For each default most of the customers have been paid within 7 days of the failure and all within 20 days.

• Over 80% of those customers have been paid by the “straight-through” route.

• Only 4 of those failed firms had opted-in to the electronic SCV process, so: - additional work was needed on the data of most firms before payout

- most firms were not familiar with the secure data transmission process.

• We are continuously improving the process by:- Reviewing our results and identifying potential opportunities- Ongoing projects in combination with the Regulator - Working with the Tripartite to plan for major and combined failure scenarios

• Each default payout has used a combination of cheque and cash over the counter letter payments.

Progress to Date

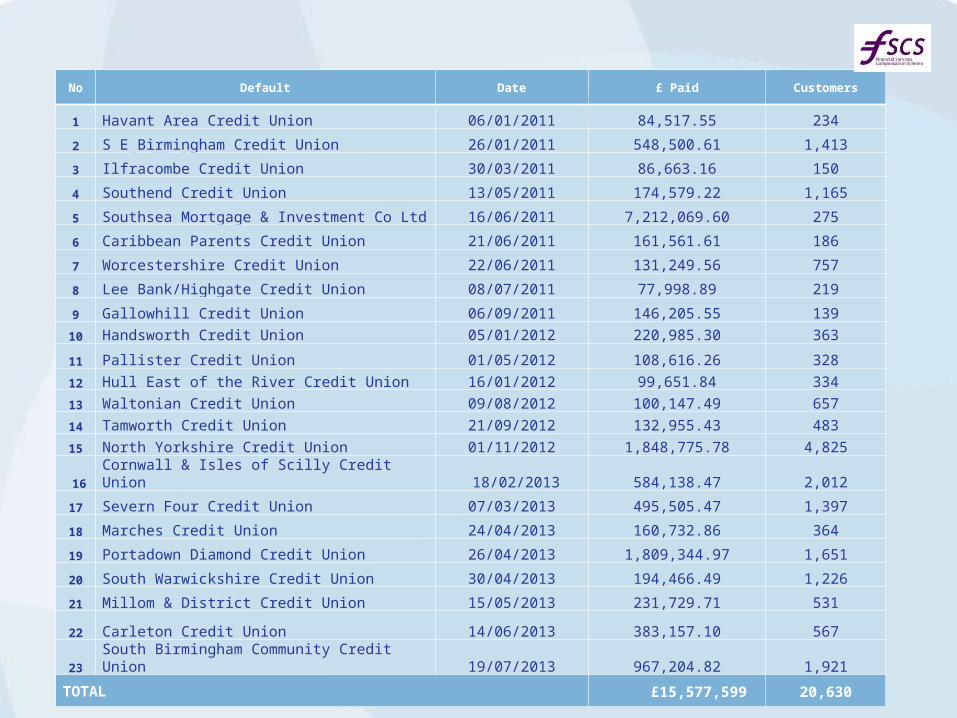

Our SCV Pay-out experience so far

No Default Date £ Paid Customers

1 Havant Area Credit Union 06/01/2011 84,517.55 234

2 S E Birmingham Credit Union 26/01/2011 548,500.61 1,413

3 Ilfracombe Credit Union 30/03/2011 86,663.16 150

4 Southend Credit Union 13/05/2011 174,579.22 1,165

5 Southsea Mortgage & Investment Co Ltd 16/06/2011 7,212,069.60 275

6 Caribbean Parents Credit Union 21/06/2011 161,561.61 186

7 Worcestershire Credit Union 22/06/2011 131,249.56 757

8 Lee Bank/Highgate Credit Union 08/07/2011 77,998.89 219

9 Gallowhill Credit Union 06/09/2011 146,205.55 139

10 Handsworth Credit Union 05/01/2012 220,985.30 363

11 Pallister Credit Union 01/05/2012 108,616.26 328

12 Hull East of the River Credit Union 16/01/2012 99,651.84 334

13 Waltonian Credit Union 09/08/2012 100,147.49 657

14 Tamworth Credit Union 21/09/2012 132,955.43 483

15 North Yorkshire Credit Union 01/11/2012 1,848,775.78 4,825

16 Cornwall & Isles of Scilly Credit Union 18/02/2013 584,138.47 2,012

17 Severn Four Credit Union 07/03/2013 495,505.47 1,397

18 Marches Credit Union 24/04/2013 160,732.86 364

19 Portadown Diamond Credit Union 26/04/2013 1,809,344.97 1,651

20 South Warwickshire Credit Union 30/04/2013 194,466.49 1,226

21 Millom & District Credit Union 15/05/2013 231,729.71 531

22 Carleton Credit Union 14/06/2013 383,157.10 567

23 South Birmingham Community Credit Union 19/07/2013 967,204.82 1,921

TOTAL £15,577,599 20,630

Key Success Factors Engage with regulators, industry trade bodies and solution providers early on

through workshops and seminars to clarify requirements and technical implementation

Be as prescriptive as you can in your SCV requirements of deposit takers – and avoid allowing opt-outs

Offer opportunities for early SCV submissions and testing— FSCS ran a Pilot programme with deposit takers

Establish capacity and scalability requirements at the start of the project, before solution design and build commences

— Specify and mandate all technical requirements, such as file type & format— Think about the ongoing application and hardware support model

Ensure sufficient technical expertise – new systems are not just about policy

Don’t under-estimate testing – it needs to be integrated across solutions

Be prepared for deposit takers’ transmission and security concerns— Beware of local legislative restrictions

Ensure primary ownership of Intellectual Property (IP), even if the solution is outsourced

The need for continued oversight and testing

21

22

Questions

Appendices

Single Customer View definition

Faster Payout Process overview

23

24

Faster Payout Rules and Single Customer View Tables

Customer detailsSingle customer view record number Unique customer identifier

Title Title

Customer 1st Forename 1st Forename

Customer 2nd Forename 2nd Forename

Customer 3rd Forename 3rd Forename

Customer Surname/Company Name Surname or Company Name or Name of Claimant

Previous Name Any former name of account holder

National Insurance number National Insurance number

Contact details (one of two formats)

Single customer view record number

Unique customer identifier

House number House number/Premise name

Street Street

Locality Locality

County County

Postcode Postcode

Country Country

Details of account (s)

Single customer view record number

Unique customer identifier

Account title Surname or company name, first name, any other account initials or middle name identifier

Account number Unique number for this account

Product type Type of product or service – instant access/term

Account holder indicator This field applies to joint or multiple accounts - it must identify whether the customer is the primary account holder or secondary account holder (or other such status)

Account status code Active accounts only to be included

Account balance At end of business on date of request from FSCS. The amount(s) inserted into each single customer view as the account balance(s) and aggregate balances across all accounts should be the total of principal plus any interest or premium attributable up to the quantification date

Aggregate Balance

Single customer view record number

Unique customer identifier

Aggregate balance

across all accounts

At end of business on date of request from FSCS

Compensatable

amount

At end of business on date of request from FSCS which shows the amount to be compensated subject to the limit check that must be performed by the firm pursuant to COMP 17.2.5R (this could be lower than the aggregate balance across all accounts if this exceeds the maximum payment for a protected deposit set out in COMP 10.2.3R).

Single Customer View A firm must be able to provide a SCV to the FSCS for each eligible claimant within 72 hours of a request. A firm must ensure that

each SCV contains all information included in the SCV data tables set out below, and that the additonal Faster Payout rules have been applied. If a claimant holds more than one account the ‘Details of account(s)’ table must be replicated for each acount held. Each table must be linked by a unique customer identifier.

Compensation amount The SCV file must contain aggregrated balances for eligible customers, up to the limit of £85,000 (equivalent to €100,000).

Eligibility flags A firm must be able to identify which accounts are held by eligible claimants and which accounts are held on behalf of

beneficiaries who are, or who may be, eligible claimants. Firms must check if customers are still eligible for compensation at least annually.

Calculating aggregrate balance, including term accounts at default If a protected deposit is not due and payable on or before the default date, the compensation amount must include the principle

sum on the basis that it is due and payable on that date; interest accrued to that date; and unaccrued interest in respect of the period to that date.

Unique customer identifier (UCI) Every customer must be allocated a UCI number.

24

25

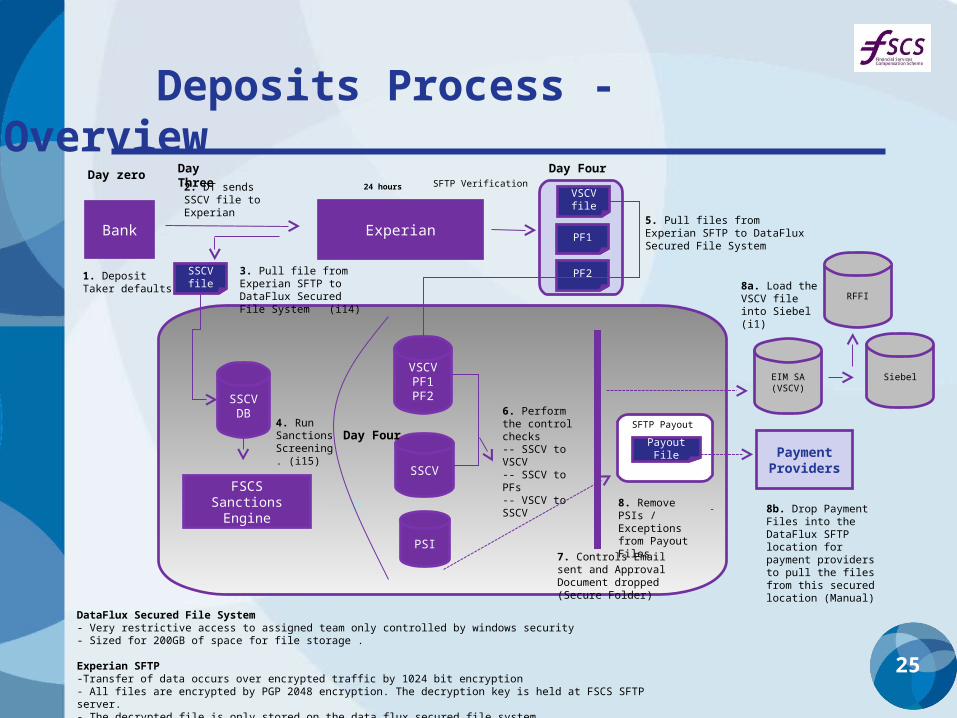

Deposits Process - Overview

Bank

SSCV file

Experian

VSCV file

PF1

PF2

SFTP Verification

FSCS SanctionsEngine

SSCV

SSCV DB

VSCVPF1PF2

Payout File

SFTP Payout

EIM SA(VSCV)

Payment Providers

1. Deposit Taker defaults

4. Run Sanctions Screening. (i15)

5. Pull files from Experian SFTP to DataFlux Secured File System

Day zero Day Three

Day Four

24 hours

Day Four

3. Pull file from Experian SFTP to DataFlux Secured File System (i14)

-

6. Perform the control checks-- SSCV to VSCV-- SSCV to PFs-- VSCV to SSCV

8b. Drop Payment Files into the DataFlux SFTP location for payment providers to pull the files from this secured location (Manual)

8a. Load the VSCV file into Siebel (i1)

Siebel

DataFlux Secured File System- Very restrictive access to assigned team only controlled by windows security- Sized for 200GB of space for file storage .

Experian SFTP -Transfer of data occurs over encrypted traffic by 1024 bit encryption- All files are encrypted by PGP 2048 encryption. The decryption key is held at FSCS SFTP server.- The decrypted file is only stored on the data flux secured file system

2. DT sends SSCV file to Experian

8. Remove PSIs / Exceptions from Payout Files

PSI7. Controls Email sent and Approval Document dropped (Secure Folder)

RFFI

Related Documents