Financial Market Globalization, Asymmetric Tax and Endogenous Inequality of Nations LAM Wing Shing A Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of Master of Philosophy in Economics • The Chinese University of Hong Kong September 2006 The Chinese University of Hong Kong holds the copyright of this thesis. Any person(s) intending to use a part or whole of the materials in this thesis in a proposed publication must seek copyright release from the Dean of the Graduate School.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Market Globalization, Asymmetric Tax and Endogenous Inequality of Nations

LAM Wing Shing

A Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of

Master of Philosophy in

Economics

• The Chinese University of Hong Kong September 2006

The Chinese University of Hong Kong holds the copyright of this thesis. Any person(s) intending to use a part or whole of the

materials in this thesis in a proposed publication must seek copyright release from the Dean of the Graduate School.

學大 w ;^系仏書圖

:二 I,.. ^ 1 1 OCT m ] i

^ ^ ~ … 丁 Y “ 一 J _ l SYSTEM

ABSTRACT

In this thesis, I incorporate a capital income tax scheme into Matsuyama's (2004) basic framework to obtain a more comprehensive theory of financial market globalization and endogenous inequality of nations featuring credit market imperfection and asymmetric tax across nations. Allowing for asymmetric tax as a source of exogenous heterogeneities among nations, I identify three important factors that determine international capital flow - the level of tax rates across nations, the degree of dispersion of the tax rates, and the degree of credit market imperfection. I also demonstrate how these factors, thorough their effects on international capital flow, could affect the patterns of inequality of nations under integrated financial markets. The effect of financial market globalization is also discussed. In general, my study suggests that it is important to consider the international tax structure before and after globalization if one needs to more realistically assess its effects.

ii

摘要

本文在Matsuyama (2004)數理模式的基礎上弓丨入了資本收益稅制,並結合不完全

信用市場(imperfect credit market)和不對稱稅率(asymmetric tax)等元素’

以求推導出一套較全面的環球資本市場一體化和內生國際財富不均

(endogenous inequality of nations)的理論。在稅率不對稱時,不同國家的稅率

7jC平、不同國家稅率的差異程度及信用市場不完全的程度皆成爲影響國際資本

流動的重要因素,並會引致國際間不同形式的財富不均。槪言之,在探討全球

資本市場一體化如何對各國構成衝擊時,我們有必要同時考慮國際稅務結構所

帶來的影響。

iii

ACKNOWLEDGEMENTS

I would like to thank my thesis supervisor, Prof. Yip Chong Kee, for his guidance throughout the whole process of my thesis preparation. Prof. Yip has identified for me a topic of research that I eventually work out in this thesis. He has also given me several important reminders and suggestions during the different stages of my work, without which I could not have completed my thesis successfully. I would also like to thank Mr. Lai King Man for his timely and effective assistance in the preparation of the figures found in the appendices of this thesis and Mr. Horace H.Y. Lit for a refined Chinese version of the Abstract. All errors are mine.

i v

Table of Contents Abstract ii

摘要 出

Acknowledgements iv Table of Contents v 1 Introduction 1 2 Related Works in the Literature 4 3 The Model 8

3.1 The Basics 8 3.2 The Investment Decision 10 3.3 The Public Sector 11 3.4 The Constraints Combined 11

4 Autarky 13 5 The Small Open Economy 15 6 The World Economy 19

6.1 The World Economy under Symmetric Tax 19 6.1.1 Symmetric Steady States 19 6.1.2 Stable Asymmetric Steady States 21

6.2 The World Economy under Asymmetric Tax 23 6.2.1 Stable Steady States under Asymmetric Tax 23 6.2.2 Discussion 27

7 Conclusion 31 References 33 Appendices 34

Proof of Lemma 34

V

Proof of Proposition 2 36 Proof of Proposition 3 40 Proof of Proposition 4 43 Proof of Proposition 5 46 Figure 1 - Dynamics - autarky 58 Figure 2 - Asymmetric tax - autarky 58 Figure 3 - Dynamics - small open economy 59 Figure 4 - Asymmetric tax - small open economy 60 Figure 5 - Asymmetric tax - world economy 60 Figure 6 - Equality of nations in asymmetric tax 60 Figure A. 1 for Proof of Proposition 4 61 Figure A.2 for Proof of Proposition 5 61 Figures A.3-A.4(d) for Proof of Proposition 5 62 Figures A.4(e)-A.5 for Proof of Proposition 5 63

vi

1 Introduction

The effects of financial market globalization on the inequality of nations have long been considered by the academics. While the conventional view suggests that integration of financial markets is beneficial to poor countries, the structuralist's view maintains that it simply magnifies the existing income inequality of nations. The international capital market literature has recently made important progress in scrutinizing and rationalizing the last view. Studies in this literature suggest credit market imperfection plays an important role in determining the effects of financial market globalization. Matsuyama (2004), one of the most outstanding among these studies, lays out a formal theory of endogenous inequality of nations which advances the way financial market globalization could lead to endogenous heterogeneities across countries in the presence of credit market imperfection. It is, to my best knowledge, the first theoretical model which attempts to show that globalization does not always lead to inequality of nations and is tractable enough for complete characterizations over a full set of parameter values of all steady states and analytical derivations for their corresponding stability conditions without imposing any auxiliary assumption. On the other hand, there is also an extensive literature focusing on the international effects of taxation. For example, Bovenberg (1989) considers the effects of capital income taxation on international competitiveness and trade flows, and Gordon and Bovenberg (1996) examine international capital immobility and its explanations and implications for capital income taxation. More recent studies in the field investigate the welfare effects of tax policy in open economies (see, e.g., Mendoza and Tesar (1998)).

Given the widely-agreed significance of the international effects of taxation and

1

the still important problem of the effects of financial market globalization, it is natural for one to question about the link between tax policies and financial market globalization and their effects on the inequality of nations. In this thesis, I endeavor to incorporate a capital income tax scheme into Matsuyama's (2004) basic framework to obtain a broader theory of financial market globalization and endogenous inequality of nations featuring credit market imperfection and asymmetric tax across nations. Under symmetric tax, that is, when all countries adopt the same capital income tax rate, I replicate all the main results in Matsuyama (2004),

whose main concern is the application of symmetry-breaking in demonstrating how financial market globalization could inevitably lead to endogenous inequality of nations under imperfect credit markets. But under asymmetric tax, I no longer consider symmetry-breaking but offer a whole new set of novel results. Below I outline the major arguments I put forth in this thesis:

Under financial market globalization and asymmetric income tax, the level of tax rates across nations plays a dominant role in determining international capital flow when all countries are at a low (high) level of development: Countries adopting a higher tax accumulate less capital and become the 'poor' countries in any stable steady state. When countries adopting a lower tax rate are at a low level of development while the remaining countries are at a high level of development, the degree of dispersion of the tax rates and the degree of credit market imperfection interact to determine international capital flow. A lower relative tax and a higher degree of credit market imperfection put those countries at a low level of development at advantage and disadvantage respectively in competing for the world's savings. Accordingly, countries adopting a higher tax could be poorer than, richer than, or as richer as others in a stable steady state. In other words, countries trapped in a low level of development (possibly due to negative economic shocks)

2

are not necessarily worse off in a world stable steady state. After globalization, ‘poor,

countries could become ‘rich,’ 'rich countries could become 'poor', and there could even be endogenous equality of nations.

The rest of the thesis is organized as follows: Chapter 2 discusses related work in the literature. Chapter 3 develops the building blocks of the model. Chapter 4 and Chapter 5 analyze an individual country under the autarky and small open economy cases respectively. Chapter 6 considers the world economy under symmetric and asymmetric tax separately. Chapter 7 concludes.

3

2 Related Works in the Literature

Since my study is an extension of Matsuyama (2004),I will first give more details on it before surveying other related studies in the literature. In Matsuyama (2004), the world economy is composed of a continuum, with unit mass, of otherwise inherently identical countries that differ only in their initial levels of capital stock. A steady state of the world economy could be classified as being either symmetric or asymmetric: Either all the countries have the same level of capital stock (endogenous equality of nations), or a fraction of counties have the same level of capital stock higher than that of the remaining fraction (endogenous inequality of nations). Matsuyama (2004) demonstrates that the world economy has a unique and globally stable symmetric steady state in the absence of an international financial market (despite of credit market imperfection). But with a fully integrated international financial market, under some analytically expressed conditions which are both necessary and sufficient, symmetry-breaking materializes: The symmetric steady states become unstable and stable asymmetric steady states of the world economy emerge.

More formally, the world economy under autarky and financial market globalization are respectively modeled as a continuum of autarkic economies and small open economies. For any member of a world economy, multiple steady states (of different levels of capital stock) is only possible when it is an open economy (i.e., integrated to the international financial market). This feature of the framework, in consequence of dissimilar effect and interaction of two salient elements -diminishing returns technology and endogenous borrowing constraint — under autarky and financial market globalization, is the underlying requisite for the hallmark symmetry-breaking obtained under financial market globalization and

4

certain other conditions. Conceptually, symmetry-breaking, according to Matsuyama (2004, p.885), is a

mechanism by which minimal exogenous variation creates a variety of pronounced endogenous heterogeneities. It coincides with the structuralist's view that globalization assuredly magnifies inequality among nations. It is important to note that in Matsuyama's (2004) framework the rich countries achieve their affluence at the expense of others and the poor countries could not jointly escape from poverty by severing their links to the rich countries. Inequality of nations, in this particular symmetry-breaking approach, is no isolated problem at the individual country level -it has to be dealt with at the global level.

The literature on the symmetry-breaking approach to inequality of nations is scanty. As opposed to Matsuyama (2004), Krugman and Venables (1995) and Matsuyama (1996) investigate how goods market globalization and production agglomeration could lead to inequality of nations, and depict the case where globalization inevitably engenders symmetry-breaking. Krugman and Venables (1995) studies how inequality of nations evolves as the world economy progresses through different stages of globalization. By considering how globalization affects the location of manufacturing and gains from trade, they report that when transport costs are high, all countries have some manufacturing. But when the costs are considerably low, nations in the periphery suffer a decline in real income. At still lower costs real income converges - peripheral nations gain and core nations lose. On the other hand, Matsuyama (1996) and Matsuyama (2004) juxtapose the structure of the world economy pre- and post-globalization and endeavor to capture the idea that globalization inevitably divides nations into the rich and the poor. All these three hallmark studies of the field focus on formalizing, rationalizing and reconciling the conventional and heterodox perspectives on the impact of globalization on inequality

5

of nations. My study is related to those featuring capital market imperfection and/or

international capital flow. Boyd and Smith (1997), which is highly related to Matusuyama (2004), identifies the combination of international financial trade with a costly state verification problem in credit markets as a potential source of permanent international income inequality. They find that 'unrestricted international trade precludes otherwise identical economies from converging, and poor countries are necessarily net lenders to rich countries' (p.335). However, Boyd and Smith (1997) have invested highly in the exact mechanism that drives credit market imperfection. This renders their model rather elaborated and thus impossible for analytical derivations of stability conditions for the steady states. Sakuragawa and Hamada (2001) explore how the difference in the extent of informational frictions in the financial contract across regions could help to explain why capital flows from the South to the North. Having a superior information structure, the North might induce capital flight from the South, driving it into a poverty trap, thus liberalizing the capital market might not be beneficial to the South.

Espinosa-Vega, Smith and Yip (2005) introduce barriers to international capital flows in the form of taxes to the model of Boyd and Smith (1997) and examine their short-run and long-run effects. Therefore, theirs is a model of international capital markets in the presence of domestic credit friction in terms of costly state verification. They show that under some conditions international financial integration in an otherwise symmetrical world can create permanent inequality between countries, lower world output and increase economic volatility. However, by appropriately selecting barriers to international capital movements, they demonstrate that the pernicious effects of international financial integration could be removed and even net capital flows and welfare in the steady state could be increased. My study is very

6

closely related to Espinosa-Vega, Smith and Yip (2005) in that both mine and theirs feature credit market imperfection, capital income taxation of nations and consider their effects on international capital movement. Yet, my thesis attempts to unify these features with the more-tractable framework of Matsuyama (2004) into a more comprehensive theory of financial market globalization and endogenous inequality of nations and provide other novel results.

7

3 The Model

In this chapter, I develop the framework upon which the analyses and discussions in the following chapters are based. In Section 3.1 I describe the basic elements of the model which is based on the Diamond overlapping generations model. In Sections 3.2 and 3.3 I describe the investment decision of the agents and the public sector respectively. In Section 3.4,I summarize the model by (4).

3.1. The Basics The basic framework is in essence the one in Matsuyama (2004), based on the

Diamond overlapping generations model with two-period lifetimes. Departures from Matsuyama (2004) would be clarified. A single final good is produced by two factors of production - labor, supplied by young agents, and physical capital, supplied by old agents. The final good produced in t could be, in that period, consumed, or invested in the production of physical capital, which becomes available in t+1 as final good. The final good can be traded inter-temporally between countries when the international financial markets are integrated; both factors of production are assumed to be non-tradable.

The technology for the production of final goods satisfies the standard, neoclassical properties. It is linearly homogeneous, given by K, 二 ) , where K, and L, are aggregate domestic supply of physical capital and labor in period t respectively. Expressed in the intensive form, we obtain:

兄三 ”//^, ,1)三/Ot,), where k丨三 YjL, . f{k) is C ' a n d satisfies

f \ k ) > 0 > /"(k), / ( 0 ) = 0 and /"(O) = oo. Factor markets are competitive.

‘ M a t s u y a m a (2004) assumes C ^ . 8

Factor payments, in terms of the final good, to physical capital and labor are respectively ) and )三 f(Jc,) - k j \ k , ) . Physical capital depreciates fully in one period.

Each generation consists of a continuum of homogenous agents with unit mass. Consider a young agent of any period, say t. He supplies one unit of labor invariably at t to produce the final good and consumes only in t+L Thus, L丨=1. At the end of t, he receives his wage income W(k,) plus a transfer a,W{k,), expressed as a fraction of his wage income, from the government. Thus, his stock of wealth at the end of t amounts to (1 + a, )W{k^) He could finance his consumption in t+J in either of two ways: Firstly, he could lend his entire wealth through the competitive credit market. His second-period consumption is then (1 + a, )W(k,), where r, , is the gross interest rate. Secondly, he might start one (and only one) investment project which transforms exactly one unit of final good from t into R > 0 units of physical capital in t+1.1 assume that

W{R) + TRf\R)<\\ (Al) It is explained below that (Al) is necessary to ensure (1 + a, )W{k,) is always less than 1 so that the agent needs to borrow +a,)W{k^) > 0 from the credit market to start the investment project. He is prohibited to start the project abroad. In t+1, that is, when he becomes old, he repays his debt plus interest

(1 — (1 + cir, )) and pays a tax )R 斗 that amounts to a portion of his

capital income.5 Thus, his second-period consumption is

(1 一 )R — (1 - (1 + a, )W{k,)).

2 Matsuyama (2004) does not model a public sector. In that case CJf, 二 0 for all admissible t. 3 Matsuyama (2004) only needs to impose W{R) < 1. 4 Matsuyama (2004) does not model a public sector. In that case T 二 0 • 5 Observe that the tax is not applicable to agents who did not choose to undertake the project when they are young.

9

3.2. The Investment Decision I continue to consider a young agent of any period, say t. He would consider

undertaking the investment project only if by doing so he could achieve a level of consumption in t+J no less than that if he lends his entire wealth. That is:

(1 — )R — r,+i (\-{\ + a, )Wik,)) > (1 + cc, )W{k,) ’

where r e [0,1) . Simplifying and rearranging: >0

R>——H—— (1) (1-r)氣)

I shall call (1) the profitability constraint. As noted earlier, the credit market is competitive in the sense that both lenders

and borrowers take the equilibrium rate r, , as given. However, it is not fully competitive because one cannot borrow any amount one wishes at the equilibrium rate. A borrower could pledge only up to /l(l — r)/'(众…)R, i.e., a fraction of their after-tax project revenues, for repayment, and thus will be lent at most this amount, discounted by the rate of interest. Therefore, the young agent could start the investment project only if 1 — (1 + or, )W{k, )<X{\- )尺斤…,or

尺〉 厂,+丨 H 1 + 仅譯 , )

where 0 < /I < 1.1 shall call (2) the (endogenous) borrowing constraint. It is assumed that agents could not pool their wealth together to overcome this constraint. The young agent starts the project only when they are willing to borrow and could borrow enough, that is, when both (1) and (2) are satisfied. The parameter A captures credit market friction parsimoniously. If it is zero, agents would never be able to borrow. If it is equal to one, the borrowing constraint would never be binding whenever the agents borrow because the right-hand-side of (1) is larger than that of

10

( 2 ) .

3.3. The Public Sector Recall that every agent of the same generation, regardless of whether he chooses

to borrow or lend, receives the same amount of transfer from the government in the end of his first period of life, and that the capital income tax is only applicable to borrowers in the second period of their lives. It follows that for any period, say t, the

k , government's total revenue and total expenditure are —Tf\k, )R and ) R

respectively, where kjR is the amount of old borrowers at t,Thus, an

intergenerational transfer is featured every period. I assume balanced government

budget, so for any t\

R Rearranging:

(3) Wik,) I shall call (3) the government budget constraint. Note that when T = 0, a, 二 a卜1 =0 .

3.4. The Constraints Combined With (3), I can rewrite the stock of wealth of an agent at the end of his first

period of life as f20t,t")三(1 + c i O V V(众)= 1 +辦� W(k) = W(k) + Tlrf\k). By V W{k) J

(Al),a(k,T)<\ for any k<R. Note that lim r) = lim {Wik) + Tl<f\k)) = 0 k -^0 k —>0

6 Recall that each agent could start only one investment project which transforms exactly one unit of final good into R units of physical capital. So if there are K! units of physical capital available in t, there must be k j R old borrowers at t.

11

and VimQ.{k,T) = \im(W(k) + Tl<f\k)) = +00 Moreover, Q.{k,T) is increasing in k k —>00 k -^00 over R++:

a,ik,T) = W\k) + T{fXk) + k f \ k ) ) = ~kf\k) + T f \ k ) + Tlrf\k) = {T-\W\k) + T f \ k ) >0

Therefore, for any r e [0 ,1 ) , is well-defined by !—以火(又:),:)=1,or A

\-A-Q.{KiA,T),T) = O.A\so, {k, T) = k f \ k ) > 0 . Note that and

= where R^{r) is given by 0),:r) = 1. Also,

KAX,T) = < 0 and

^ - < 0 .

—(欠 a T ) , T ) (T- i)Ka,T)f\Ka,r))+T八m,� Substituting (3) into (1) and (2),(l)-(3) could now be summarized as follows:

^ _ 1 - 琳 。 I f V 欠(又” 1 - r / U , , , ) /I ‘ R > R , ^ \ , (4)

^ if k, > K{A, T)

where R might be interpreted as the project productivity required for the project to be undertaken in t. Note that only if (4) is fulfilled, an agent starts the project. Now consider the case R> R, . If K{X, r),the borrowing constraint is satisfied and the profitability constraint is unbinding; if K, = K{A,T),both the borrowing and the profitability constraint are satisfied; if k, >K{X, r),the borrowing constraint is unbinding and the profitability constraint is satisfied. Finally, observe that when T = Q, (4) reduces to equation (3) in Matsuyama (2004). So, in some sense, my basic framework is a generalization of that in Matsuyama (2004).

7 When evaluating these two expressions I make use of the Inada conditions. 12

4 Autarky

In this chapter I focus on a particular autarkic member of the world economy. Without international lending and borrowing, domestic investment must be equal to domestic saving in equilibrium. From (4),domestic investment is equal to zero if R^ > R, and to one, if R, < R , and may take any value between zero and one if R^ = R . Domestic saving is equal to QXJC,, T),which is less than one if K, < R .

Thus, in equilibrium R = R, and the aggregate investment is equal to , r ) . It follows that the fraction of young agents who become borrowers at t is equal to QXJc,,r) and the rest becomes lenders. If k, >K{X, T) , the young agents are indifferent between borrowing and lending. If k, <K(又,T),they strictly prefer borrowing. Therefore, the equilibrium allocation necessarily involves credit rationing, where 1 - ,T) of the agents are denied credit. Since each borrower supplies R units of physical capital in period t-\-], we have

k 丨+\=RQik 丨,T), (5)

which is the counterpart to (4) in Matsuyama (2004). The dynamics of capital formation in autarky is described solely by (5). If k, < R ,hy (Al), K,^, = RQIK,,T)<RQ.{R,T)<R. Therefore, K^ e (O.R) implies K, < R and

, r ) < 1 for all r > 0 , as have been assumed. Substitute (5) into (4) and set R = R, to obtain the autarkic equilibrium interest

rate:

l{l-T)ARr(RQ(k^,T)) if K, <K(A,T) � = . (6)

(l-T)Rf\RQ(k,,T)) ifk,>Ka,T)

As in Matsuyama (2004), I impose the following assumptions: = w'(k)<0. (A2)

13

(A2) implies that ri, (0, r ) = (1 - T)W '(0) + rf '(0) - oo and

= (1 - r)W\k) + T f \ k ) < 0 . Thus, (Al) and (A2) ensure that (5)

constitutes a unique steady state K* = K*(R,T)E (O.R) implicitly defined by

k* = RQjX,f),and for k � e (O.R), k丨 converges monotonically to k* = K\R,T).

Note that = 0 and = R^{t) . PAso,

KI{R,t)>0 s ince for all admiss ib le k Cl^(众,= k f \ k ) > 0 . The fo l lowing

proposition summarizes the dynamics of capital formation under autarky:

Proposition 1: Consider a particular r e [0 ,1) . In autarky, the dynamics ofk is given by = RQ.{k,,T), which is independent of A, but dependent of t , and converges monotonically to the unique steady state, K* (R,T),where K\R,T) is increasing in both R and T, /:*(0,r) = 0 and K*(iT(T),1:) = R+(j). If K*(R,T) < K{X, T), the borrowing constraint is binding in the steady state. If K* (R,T~) > K(A,T), the profitability constraint is binding in the steady state.

Fig. 1 in the Appendices illustrates Proposition 1. Fig. 2 depicts the dynamics of an autarkic economy under two different levels of tax ( f > r ) . A higher tax rate leads to a higher level of steady state physical capital because it generates a greater amount of intergenerational transfer that leads to a larger pool of savings. But note that the dynamics remains very similar. Essentially, the level of tax could be a source of exogenous heterogeneity that leads to inequality of nations in the long run under autarky.

14

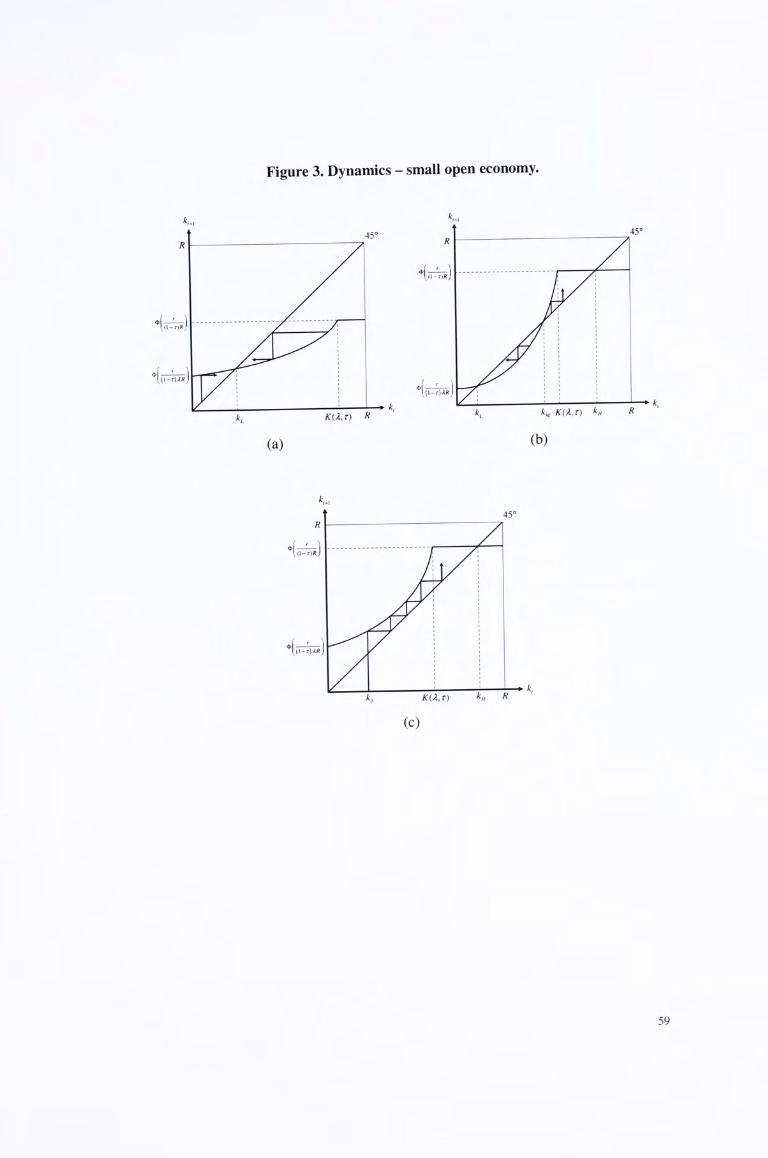

5 The Small Open Economy

In this chapter I examine a particular economy that is a member of and financially integrated to the world economy, i.e. a small open economy. This will serve as a preliminary step for the subsequent analysis of the world economy in the presence of an international financial market.

International lending and borrowing is now possible. Specifically, agents in the small open economy are allowed to trade inter-temporally the final good with the rest of the world at an invariant gross real interest rate = r,exogenously determined by the international financial market.

( r � For ease of exposition, in the sequel I focus exclusively on — —

or (1 - T)Rf\R) <r ^ Thus, the equilibrium condition is given by setting R, = R

in (4) as follows:

J r \-£L(k,,T)] F , � �

y J , (7)

� [ ( i - m ) where <I> is the inverse of /',as defined in Matsuyama (2004,p.864). (7) governs the dynamics of capital formation of the small open economy. Domestic investment is no longer required to be equal to domestic saving, so I could no longer impose (5).

When k, > K{X,T),the economy is said to be at a high level of development where only the profitability constraint is binding. When k, < K{A,T), the economy is said to be at a low level of development where only the borrowing constraint is

8 A counterpart of this restriction, R f \ R ) < r ’ could be found in Matsuyama (2004, p.864). These restrictions ensures that not all the young invests, so that 丨=中(/c, ,T) < R . This renders the notations more parsimonious.

15

binding. Also, at the low level of development, the after-tax return to investment is { — Q.{k ,T) higher than the world interest rate, with the gap represented by , A

reflecting a disadvantage in competing for the world's saving. For k,<K(A,T),

x p ( k , T ) = <!> ( . ) — — — ‘ ^ ——

‘ ‘ XR {\-Tf 小 , , 、 r -kJ\k,){\-T) + (\-Wik,)-TkJ\k,))

=<P ( • ) ";IR (L-T)'

=扑) r - 機 ) + l - / ( � , ) +槐) _ AR (l-rf

、)义R (1 —r)2 •

Therefore, with an increase in T ,中 decreases (increases) if F(K^) < 1 (> 1).

The steady states of the small open economy are given by the fixed points of the map (7) and fulfill k = . The following lemma summaries the possible sets and the essential properties of the fixed points:

Lemma: Define, from (21), k , a function of XR/r and r, by

(a) Equation (7) has at least one steady state. (b) Equation (7) has at most one steady state above K{X,T). If it exists, it is stable

f r ] and equal to <I> . U i - 浏 J

(c) Equation (7) has at most two steady states below K(A,T). If there is only one,

k^,either it satisfies 0<k^<k(A/?/r,t) and is stable, or k^ = k{AR/r,t),at

which 中 is tangent to the 45-degree line. If there are two, k^ and k^,they

satisfy 0<k^ <k{AR/r,T) < k^,where k^ is stable and k^ is unstable. 16

The proof can be found in the Appendices. The Lemma implies fixed points of (7) appear in three ways, depicted by Fig. 3(a)-(c). In Fig. 3(a), there is a unique fixed point K^ below K{A,T) . In Fig. 3(c), there is a unique fixed point above K{X,T) . In Fig. 3(b), there are three fixed points: /: and K^ are below K{X,T);

is above K{A, r). The following proposition gives the exact conditions for each of the three depicted cases.

Proposition 2: Consider a particular r e [0,1) and let / l^(r)e (0,1) be

defined by

f(K(A(T),T)) 4 = 1. Then: “ ^ nm^iTU)) (a) If (1 - z)Rf\K{X,r)) < r , there exists a unique steady state that is stable and satisfies k^ < K(义,t).

f {k{XRlr,T)) and A , there exists three steady states ki’ 似 and k^ . They satisfy

< K(A,t) < kf^ ; Jcl and k^ are stable while k^ is unstable, (c) If (1 - T)Rf\K{A,T)) > r and either

nUXRlr^z)) unique steady state that is stable and satisfies > K(A, r).

The proofs of Proposition 2 (and Propositions 3-5) are in the Appendices. Observe that the conditions given in Proposition 2 are solely expressed in terms of the parameters of the model. It should be possible to illustrate the conditions graphically, as in Matsuyama (2004). But I abstain from doing so because the algebraic conditions are, in this case, not tractable. Nonetheless, an appreciation of

17

the detail parameter configuration (for the steady states) of the small open economy is not required for an understanding of the main arguments of this thesis. A relevant implication of Proposition 2 is that, other things being equal, a different value of the tax rate T could allow for different steady states, thus modifying the dynamics of the economy. In Fig. 4 ,1 illustrate the small open economy under two different levels of tax ( f > r ) . In Fig. 4(a), I illustrate a generic case in which different levels of tax could lead to dissimilar dynamics. For a higher tax f,there are three steady states. For a lower tax r,the economy necessarily converge to a high level of development. In Fig. 4(b), I illustrate generically how different levels of tax could lead to fairly similar dynamics but different levels of steady state capital stock, given the same level of initial level k^. For a higher tax f , the economy converges to k � at a high

level of development. For a lower tax t,the economy converge to k^ at a low

level of development. Essentially, the level of tax could be a source of exogenous heterogeneity that lead to both heterogeneous dynamics and inequality of nations under an open economy.

18

6 The World Economy

Analyses of the world economy are based upon those in the last two chapters of an individual economy. The analyses in section 6.1 (for symmetric tax) largely resemble those found in Matsuyama (2004) for the world economy. However, an overview of the world economy under symmetric tax, especially the analysis of stable asymmetric steady states in Section 6.1.2, will facilitate my subsequent analyses and discussion under asymmetric tax. Indeed, the analyses under asymmetric tax are inspired by Section 6.1.2.

6.1. The World Economy under Symmetric Tax When the capital income tax x is the same for all countries, the world

economy is essentially composed of a continuum of inherently identical countries with unit mass. In the absence of international financial market, it is merely a collection of autarky economies analyzed in Chapter 4. Consequently, the world economy would converge to a unique, symmetric and stable steady state in which every country has K*{R,T) units of capital stocks.

For the remaining of section 6.1., I consider the case all countries are integrated to an international financial market. The world economy is then made up of inherently identical small open economies of the type analyzed in Chapter 5. Also note that the world economy as a whole is closed and the interest rate is endogenously determined to equate world saving and investment.

6.1.1. Symmetric Steady States The following proposition completely characterizes the symmetric steady states

19

under symmetric tax rates:

Proposition 3: Consider a particular T G [0 ,1) . Define R(�(r) e (0,R+ (T))

implicitly by f{K {R(T),T)) ; = 1.

f , ( r ( /?“r), r ) ) (a) If K*{R,T) < K{A,T) and R < R^(r), the state in which all countries have

K* = K* {R,T) units of physical capital is a stable steady state of the world economy.

(b) If K* (R,T) < K{A, T) and R> R^ (r),there exists no stable steady state in

which all the countries have the same level of capital stock. (c) If K^{R,T) > K{A, T) , the state in which all countries have k* = K* (R’T) units of physical capital is a stable steady state of the world economy.

When K* (R,R) < K(又,T),the borrowing constraint is binding and the steady

(l-T)ARf\K*(R,T)) state world interest rate is given by r = . Recall from part (c) L-N(K\R,T),T)

of the Lemma that a steady state below K (义,T) can either be stable or unstable. From the proof of Proposition 3, the stability of the steady state is determined by the

value of . ) ) - r f i K ^ R r n X K ^ K . ) ) ^ f \ K (R,T))

K* (R, T) < K* {R^ (r), r),the steady state is stable; if K* {R, T) > K* (R^ (R), R),it is

unstable. Thus, the conditions for stability are expressed succinctly in terms of

RC (r) and R. When IC (R, T) > K{X, T),the borrowing constraint is binding and the

steady state world interest rate is given by r = (1- T)Rf\K* {R, T)) . By part (b) of the Lemma, any steady state above T) is stable, leading to part (c) of the proposition.

2 0

6.1.2. Stable Asymmetric Steady States Suppose now that the world economy is in a stable steady state in which a

fraction X of the countries have capital stock amounts to K^ < K{X,T) and the

remaining fraction have capital stock amounts to k" > K(义,T). Since all countries

face the same world interest rate, K^ < K{A,T) and K" > K{X,T) must satisfy

( 1 -嘛 " ) … ( 1 二:y,。r

= (8)

in addition to k,<K{X,T)<k„. (9)

From part (b) of Lemma, /c, : k" is a stable steady state for a small open economy. T f � k ) f'ik )

By virtue of (24), the stability of k, 二� r e q u i r e s — ~ ' ' 口 < i ^ or f (众L) k,<K\R^{TU) = K{A iTU). (10)

Note that the current level of world capital stock (in the steady state) is equal to XICL . Since a young agent in a poor country saves ,r) and a young agent in a rich country saves D-ik^, z),world saving, which is equal to world investment, is given by X , T ) + ( 1 - X ,r). Consequently, the level of world capital stock for the next period is given by XRQ.(k^,r) + (1 — X)RQ.(KF^, T). But recall that the world economy is in a steady state. Hence, world capital stock must fulfill:

Xk^+(\-X)k„ = XR^IKI^, T) + (1 - X)RQ.{kf,, T) (11) A stable steady state with endogenous inequality exists if there are k^ and k^ that solve (8)-(l 1). The following proposition gives the conditions for the existence of such steady states:

21

Proposition 4: Consider a particular z e [0 ,1 ) . Define R^ (r) e (0,R+ (r))

and A^iT)e (0,1) by

The world economy has a continuum of stable steady states in which a fraction

X e c (0,1) of the countries have capital stock k�< K{X, T) and the

remaining fraction 1 - X have capital stock > K(A,T) if and only i f , for

R<R, A<A(T) and f\K{^.,T))> 儿(欠(尺,”)hold, and for R>R, C " 一 \-N(K {R,T),T) C

A<A(T) and A<-f\K\R,T)){{T-\)KU(T\T) + T ^ h o l d .

When R > R ^ , A<A^(T ) ,

/ l < - / ' ( r ( 7 ? , ” ) [ V —1)拟州,”+ 二 “ / ) � ’ � � ] a n d K � R , T ) < K(;i,T)

hold, by part (b) of Proposition 3 and Proposition 4, there exists no stable symmetric steady states but only stable asymmetric steady states. In other words, symmetry-breaking occurs under such circumstances.

I am to go straightly into the analyses under asymmetric tax, abstaining from illustrating the conditions given in Propositions 3 and 4 graphically, as in Matsuyama (2004), due to reason discussed earlier in Chapter 5. But do note, from the two propositions, that the level of tax commonly adopted by all nations plays an important role in determining the endogenous inequality/equality of nations under financial market globalization. This is because, as explained at the end of Chapter 5, a different level of tax could lead to very dissimilar dynamics of capital formation

2 2

when an economy is open.

6.2. The World Economy under Asymmetric Tax I now introduce asymmetric tax as a source of exogenous heterogeneity among

different countries. Consider the case in which a fraction X丁 e (0,1) of the countries set the capital income tax rate to r e [0,1) and the remaining fraction have it set to r e (0,1) > r . In the absence of international financial market, the world economy is merely a collection of autarky economies analyzed in Chapter 4. Consequently, the world economy would converge to a unique, asymmetric and

stable steady state in which a fraction XJ e (0,1) of the countries have K*(R,T)

units of capital stocks while the remaining countries have K* (/?, f ) units of capital stocks.

In the next sub-section I consider the case all countries are integrated to an international financial market. The world economy is then made up of small open economies of the type analyzed in Chapter 5.

6.2.1. Stable Steady States under Asymmetric Tax Rates Suppose now that the world economy is in a stable steady state in which a

fraction X j e (0,1) of the countries set the capital income tax rate to r e [0,1) with capital stock equal to k and the remaining fraction have it set to r e (0,1) > r

with capital stock equal to k . Note that the current level of world capital stock (in the steady state) is equal to

Xjk + {\- Xj)k . World saving, which is equal to world investment, is given by

Xj.Q.ik,T) + (1 - Xj)Q.{k,f). Consequently, the level of world capital stock for the

2 3

next period is given by XjRQ(k,T) + {\ — Xj)RQ.(k,f). But recall that the world

economy is in a steady state. Hence, world capital stock in the steady state must fulfill:

X^k + {\-X^)k= XjRaik, T) + (\- X 丁 )RQ(k,f). (12)

In the proof of Proposition 5,I claim that it is only when k=k^> K(A,T) and

k =k„ >K(A,f), k = K{X,T) and k <K(Ji,f),or k = ^ < K{X,T)

and k = ICH > K(A,f) that such a steady state might exist. In Fig. 5,1 illustrate the

three cases collectively in a generic situation where countries adopting different levels of tax have similar dynamics (presence of two stable steady states).

When k = k^ > K{A,T) and k > K{Z,f) holds, the profitability

constraint is binding in all countries regardless of the tax rate they adopt. Countries

all over the world face the same interest rate (1 - ;0Rf\k^ ) = r = (\- f ) R f \ k ^ ) .

Thus, the steady state should satisfy

= (13)

in addition to

k = > K { X , t ) and k >K{X,f). (14)

From part (b) of the Lemma, and k = k„ are stable steady states for a

small open economy. A stable steady state under asymmetric tax rates exists if there

are ^ and k„ that solve (12)-(14).

When k = k^< K{A,T) and k = k^ < K{X,f) holds, the borrowing

constraint is binding in all countries regardless of the tax rate they adopt. Countries

2 4

all over the world face the same interest rate — = r - ~-~ _ ~~.

Thus, the steady state should satisfy

_ { \ - f ) n K ) (15)

in addition to

<K{X,z) and k <K{A,f). (16)

By virtue of (24), the stability of k = ^ and 厂二厂 requires

^ < K\R^iT),T) = Ka^(T),T) and k, < = . (17)

A stable steady state under asymmetric tax rates exists if there are ^ and & that

solve (12) and (15)-(17).

When k=l^< K{A,T) and k =k„ > K(A,f) holds, the borrowing

constraint is binding in countries adopting a lower tax rate while the profitability constraint is binding in the remaining countries. Countries all over the world face the

. (\-T)ARf\L) _ same interest rate -——— —=厂=(1 — f)Rf ). Thus, the steady state 1 — {kj , should satisfy

( 1 - 姚 ( 1 8 )

in addition to

K = k<K(X[�and k=k„ >K{A,f). (19)

From part (b) of the Lemma, k = is a stable steady state for a small open

economy. By virtue of (24),the stability of 左 = & requires I^<K*{R^.iT),T) = K{A^.{T\T). (20)

2 5

A stable steady state under asymmetric tax rates exists if there are ^ and k" that

solve (12) and (18)-(20). The following proposition summarizes all the possible types of stable steady states under asymmetric tax rates:

Proposition 5: (a) If > K(A,T) and k = k" > K(A,f), stable steady

states could exist and such steady states must be asymmetric, fulfilling k <k.

(b) If k = kj^ < K(A,T) and k = k^ < K{X,f), stable steady states could exist and

such steady states must be asymmetric, fulfilling k <k.

(c) Define from (18) the function = and assume k fulfills k = ^(k).

Under k = k^< K{A,T) and k = k^ > K(A,f), three types of stable steady states,

satisfying k <k, k > k and k = k respectively are possible.

If A{\-T) > 1 - f , stable steady states, if exist, must fulfill k <k.

If / l(l - r ) <\-f and < 0 , stable steady states, if exist, must fulfill k >k.

If < \ - f , 0 < < 1 and k < K{X,f), stable steady states, if exist,

must fulfill k <k.

If ^{1-t) < l - f , 0 < < 1 and k > K(A,f), stable steady states, if exist,

could fulfill k < k, k > k or k =k.

If / l ( l - ; r ) < l - f , = 1 and k > K{A, f ) , stable steady states, if exist, could

fulfill k <k or k = k.

(d) There is no stable steady state with asymmetric tax rate that satisfies

竺二 L�A:(又I) and k =k^< K(A,f).

2 6

For clarity and facilitation of my subsequent discussion, I refrain from presenting the detailed necessary and sufficient conditions for the existence of the various types of stable steady states. Such conditions are derived in the proof of Proposition 5.

6.2.2. Discussion As argued above, in the absence of international financial linkage, countries

adopting a higher capital income tax converge to a steady state of greater amount of physical capital. In other words, countries providing greater incentives for young agents to become lenders (rather than borrowers) are richer in the steady state. This asymmetry is a direct result of asymmetric tax rates (tax and subsidy schemes) and happens because a higher tax rate features a greater amount of intergenerational transfer that leads to a larger pool of savings. But under financial market globalization, from Proposition 5, countries that penalize investment project undertaking more heavily are not necessarily the 'rich' countries in a steady state.

When the profitability (borrowing) constraint is binding in all countries (refer to part (a) and (b) of Proposition 5), the level of tax rates across the countries plays a dominant role in determining the international capital flow. Intuitively, countries that adopt a higher capital income tax are at a disadvantage in competing for the world's pool of savings because a high relative tax exerts a downward pressure on their interest rate relative to others. Thus, there is a tendency for capital outflow from countries with a higher tax rate where young agents have a greater incentive to lend to foreigners. In a steady state, interest rate equalization occurs when countries with a lower tax rate accumulate more capital than the others and becomes the 'rich' countries.

When the borrowing constraint is binding in countries with a lower tax rate 2 7

while the profitability constraint is binding in the remaining countries (refer to part (c) of Proposition 5), the degree of dispersion (instead of the levels) of the tax rates across the countries is a crucial factor in determining international capital flows, although it is not the only important factor. The degree of credit market imperfection in this case also plays an important role. Note that whenever the borrowing constraint is binding, credit market imperfection drives a wedge between the interest rate and

return to investment. Such a wedge, represented by ,is present for \-Qik,T) countries that adopt a higher capital income tax but not for the others, as can be identified from the no arbitrage condition (18).^ While countries adopting a capital income tax rate considerably low relative to others are at advantage when competing for the world's savings, a higher degree of credit market imperfection puts these countries at disadvantage because a lower A exerts a downward pressure on their interest rate relative to others. This notion of the interaction between the two factors

manifests itself in the necessary condition, - r ) < 1 - f , for the existence of

stable steady states satisfying k > k or k = k stated in part (c) of Proposition 5.

Note that / i ( l - r ) < 1 - f translates to a relatively small dispersion of the tax rates

and/or a relatively large degree of credit market imperfection, which tends to curb capital flows out of the countries with a higher tax. Accordingly, countries that adopt a higher capital income tax rate could be poorer than, richer than or as rich as the remaining countries in the world economy in a stable steady state. Also note that if

/l = l , / l ( l - r ) > 1 - f and every stable steady state must satisfy 厂〈左,as in the

other cases (in parts (a) and (b) of Proposition 5) where international financial

9 Comparing (18) to (13) and (15) respectively, it is easy to see that the role of credit market imperfection plays a distinguished role in world interest rate equalization for the case

< K(A,T) and k =k„ > K(A,f). 2 8

markets integrated. Thus, credit market imperfection is no redundant construct in the extended analyses.

It is important to point out that whether the world economy is under part (a), (b), or (c) of Proposition 5 (assuming the economy is in a steady state) depends on the full parameterization of the model, including the productivity of the investment project (R), and the initial amount of physical capital stock each country has. Moreover, the asymmetric tax structure does not only affect the level of wealth of the different nations through its effect on international capital flows - an asymmetric tax structure, as discussed in Chapter 5, reflects heterogeneous dynamics among different nations, which unquestionably has a bearing on the level of wealth of different nations.

A substantial portion of the analyses above serves to depict the mechanism through which an asymmetric tax structure across members of the world economy channels international capital flows in the presence of imperfect credit markets under financial market globalization. It is also obvious through its effect on international capital flows that an asymmetric tax structure has a bearing on the international distribution of income. Thus, treated in a standalone manner. Section 6.2.1 is a theory of endogenous inequality of nations which offers a supplementary perspective to Matsuyama (2004) or Section 6.1 where members of the world economy are inherently identical. It is also worth mentioning that whenever the world economy is in a state of endogenous inequality where some countries are trapped in a lower level of economic development where the borrowing constraint is binding while others are at a higher level of development where the profitability constraint is binding, those countries which are trapped are not necessarily worse off in a world steady state under asymmetric tax. But when there is no asymmetric tax (refer to Section 6.1.2 or Matsuyama (2004) Section 6.2), those countries trapped in a low level of

2 9

development are necessarily worse off in a world stable steady state. The case

k = ki^< K{A,T) and k > K { X , f ) in Section 6.2.1 is in fact a

straight-forward generalization of the situation considered in Section 6.1.2. Under asymmetric taxes, financial market globalization could no longer feature

symmetry-breaking since there could be no symmetry before globalization. ‘Poor’ countries could become 'rich' countries and 'rich' countries could become 'poor' countries after globalization. It is also possible to achieve endogenous equality after globalization (refer to part (c) of Proposition 5). In Fig. 6,I depict a generic case where equality of nations is possible after globalization. In general, the analyses demonstrate that the tax structure adopted by different countries is a prominent factor in determining the effect of financial market globalization on inequality of nations.

3 0

7 Conclusion

In this thesis, I incorporate a capital income tax scheme into Matsuyama's (2004) basic framework to obtain a more comprehensive theory of financial market globalization and endogenous inequality of nations featuring credit market imperfection and asymmetric tax across nations. Allowing for asymmetric tax as a source of exogenous heterogeneities among nations, I identify three important factors that determine international capital flow - the level of tax rates across nations, the degree of dispersion of the tax rates, and the degree of credit market imperfection. I also demonstrate how these factors, thorough their effects on international capital flow, could affect the patterns of inequality of nations under integrated financial markets. The effect of financial market globalization is also discussed. In general, my study suggests that it is important to consider the international tax structure before and after globalization if one needs to more realistically assess its effect.

I will now discuss some limitation of the analyses of all the chapters. Firstly, the model assumes that globalization has no effect on the degree of credit market imperfection and results are conditional upon this assumption. Secondly, the model does not allow for sustainable growth. Thirdly, the taxation scheme has rendered the model less tractable. Thus, I have refrained from working out similar types of parameter configuration maps which can be found in Matsuyama (2004) and could probably offer refined intuitions. The increased complexity of the model stems from the transfer of tax proceeds to the young agents. I choose to retain the transfer in this thesis for the purpose of completeness. But if one would like to extend the analyses further, assuming no transfer will assuredly simplify the derivations and possibly produce sharper results. Fourthly, a stable world economy steady state does not

3 1

always exist under asymmetric tax. Lastly, tax rates are assumed to be exogenously determined in the present study. It might be illuminating to endogenize taxation in the present framework in future studies to consider the relations among optimal taxation, taxation cooperation and financial market globalizations, and their effects on the inequality of nations.

3 2

References Bovenberg, A. L. (1989). The Effects of Capital Income Taxation on International

Competitiveness and Trade Flows. The American Economic Review, 79, 1045-1064.

Boyd, J. H., & Smith, B. D. (1997). Capital Market Imperfections, International Credit Markets, and Nonconvergence. Journal of Economic Theory, 73, 335-364.

Espinosa-Vega, M. A., Smith, B. D., & Yip, C. K. (2005). Barriers to International Capital Flows: When, Why, How Big, and for Whom?. [Manuscript]

Gordon, R. H., & Bovenberg, A. L. (1996). Why is Capital So Immobile Internationally? Possible Explanations and Implications for Capital Income Taxation. The American Economic Review, 86, 1057-1075.

Krugman, P. R.,& Venables,A. K. (1995). Globalization and the Inequality of Nations. Quaterly Journal of Economics, 110, 857-880.

Matsuyama, K. (1996). Why Are There Rich and Poor Counties?: Symmetry-breaking in the World Economy. Journal of the Japanese and International Economies, 10,419-439.

Matsuyama, K. (2004). Financial Market Globalization, Symmetry-breaking and Endogenous Inequality of Nations. Econometrica, 72, 853-884.

Mendoza, E. G., & Tesar, L. L. (1998). The International Ramifications of Tax Reforms: Supply-side Economics in a Global Economy. The American Economic Review, 88, 226-245.

Sakuragawa, M., & Hamada, K. (2001). Capital Flight, North-South Lending, and Stages of Economic Development. International Economic Review, 42,1-24.

3 3

Appendices Proof of Lemma

The proof follows that of the lemma of Matsuyama (2004) closely. Part (a) of the Lemma follows from Brouwer's fixed point theorem and because ^ is a continuous map on [0,/?] into itself. Part (b) follows from the fact that the map 中

f r ) is constant above K(A,r) and equal to <I> — . [(I-T)RJ

To prove part (c), first obtain for k丨 <KiA,T) from (4)

;1(1 — r ) / '(於 ) R - r ( \ - n i k , , T ) ) = 0,from which then I can obtain: +

= - , — • > 0 .

By setting k = ,I obtain for a steady state k<K{X,T):

、(,

_ r((T-W\k) + T f \ k ) ) _ A{L-T)R(K)R

- - - : ^ 卜 + 徴 ’ (21)

f { k ) f \ k ) ) = — ( r - l ) H r f l ,⑷ r叫 ]

I , ⑷ 作 ) 刀 •

S / 1 \ ^ / 1 \ I assume so that for any 0<k<K{X,T) fulfilling

k = P 二 〃 � 1 is satisfied, for example, by f {k) = Ak\ v^hQxt

.Also note that ^CO r � > D

At the smallest steady state, 0 < k ^ < K a , T ) , if there is one, either

少 1 (、,r) = 1 (or U R / r ’ r ) ),in which case it is the only intersection below

3 4

K{X,T), or < 1 (or K^^ < k{AR/R,T)), in which case it is stable. At the

second smallest steady state k^,if it exists, {k^ > 1 (or k^ >k {XR/ r,T))

and hence it is unstable, which also implies that 中 cannot cut the 45 line from above between /: and T),ruling out the existence of a third steady state below K{A,T).

3 5

Proof of Proposition 2 The proof follows that of Proposition 2 of Matsuyama (2004) closely. Consider the non-generic case (1 — T)Rf\K(A,T)) = r,which is equivalent to f \

f K(A,T) = <I> . Then K{X,T) is a fixed point on the map ^ . From (21),

� ( 1 - r ) / ? obtain an expression for the left derivative of the map at K(义,t):

l i m = - , ‘ � 1 ) 火 ( 义 , ⑶ ) “ K M - 1 � f {K(A,T)) J

= " : ( y,� 1 . (\-T)f\Ka,T)))

The stability of the left derivative could be determined by the following expression:

^ i K g r ) - " : ( , ⑶ 1 - 1

: ) 卿 , 4 糾, r ) - h J - ^ 1 [ ( 1 - r ) / iK{A,T))) J

= j f (m,T)) [-i+w(KaT))+TKa,T)r(Ka,T)) ,

4 nK(A,T)) J Differentiate the expression inside the large parentheses in the last line with respect to A:

3 6

~2f\Ka,T))f\KiA,T))K,(A,T)f\Ka,T)y , 1 , -f\K{X, T))f\K{A, T))K, (A, T)

F(K(A, T))K. (A, T)-FL " � � ‘ r(K(A,T))riK{A,T))

=,(咖《,("{1 斗 二 :; 二 I, � / {KU,T))f iKi;i,T))JJ

= r ( m r M i ( A 4 i 十 小 - 〈 ( 拟 广 ) ) 广 严 t 叫 ) < 0 . t I r(K{A,T))r(KaT))))

Also note that 广(欠(1 TriK{\,T))f\K(\,T)) ^ TK(lT)f\K{lT))f\K{\,T))

f^KiU)) -八 K{\,T)r{K{\,T)) =0

< 1 = W{R^(T)) + TR'{T)f\R^{T)) = / ( / ? + ⑴)-(1 - ⑴/'(/?+ ⑴)

<F{KiO,T)) < / (火 ( ( U ) ) - (火 ( o , r , ) ) / ' (欠欠 ( 0’⑶ . f (K(0,t))

Therefore, (0,1) is well-defined by

/ ⑷ 从 ) , ⑶ - ( 产 ( 〜 ) ) = 1 (22) ^ n m ^ x T ) ) Note that A>(<)A(T)<^ lim <(>) 1. Also, for A<A(T) W has

k-^KUaT another fixed point 0 < ki^<K{X,T), but not for A > .

Now consider the case (1 - T)Rf\K{X,T)) < r . This case can be studied by reducing R starting from the case (1 — T)Rf\K{X, r)) = r while fixing X,r and r. This change is captured by a downward shift of the map 中.With any downward shift,中 has a unique stable fixed point K^ < T) . This proves part (a) of the proposition.

Now consider the case (1 - r)Rf\K{X, r)) > r by increasing R from the original case (1 - T)Rf\K{X, r)) = r, fixing X, r and r. This results in an upward shift of the map 少.Suppose A>A(T) ( lim < 1). Then 中 has a

3 7

unique stable fixed point = <I>(r/(l - T)R) > K{X,T) after any upward shift.

Conversely, suppose X <A(T) ( lim 少,(K,T) > 1). Then there exists a critical k—K(A’rr

value of R, R',such that, if r/(l - T)f\K(A, T)) < R < there are three fixed points < K(Z, T)<k„ , and if R > R\ there is a unique fixed point

kf^ r /( l - T)R) > K(A,t) . In the generic case R = 中 is tangent to the

45-degree line below K{/1,T) . From part (c) of the Lemma, the value of k at the

tangency is given by k{AR'/r,r), and hence r,r),r) = k{AR'/r,r),

which can be rewritten, from (7), as

n i 叫 , 你 � � ( l - r ) / ? X

Substitute for 厂 (by = 1) and j r i n A\\ — TJR

(23):

A W / r / m f (1 - 咖 从 ‘ / ⑶ -

I fJkUR/r,T))) =1 r)) - TkUR'/r, T) f \k{AR'/r, T))

I f\kaR'lr,T))) =1 - fikURyr, D) + k{AR'/r, T ) f \ k m ' / r , r))

/(似zr/⑷•作(収 浙 ' (似⑶二 1.

f\k{XR'lr,T)) Since k{AR/r ,T) is increasing in R and

3 8

3 (r.J. T f \ k ) f \ k ) \ _ 二 2 f \ k ) f \ k ) r { k ) - f \ k ) f \ k ) r { k ) f i k ) J " r(k)r{k)

I , � , � J

I I / � m J J I I f ik)rik)))

f ih圳 r 圳 r:T)) f'ijcaRl r < ^ —(【己,three fixed points and f\k{AR/r,T))

fCk(AR/r,T)) - �丨• , unique steady state f\kaR/r,T))

K^ = <I>(r/(l - T)R) > K{X,T) . This proves part (b) and (c) of the proposition.

3 9

Proof of Proposition 3 The proof follows the analyses in Matsuyama (p.869, Section 6.1, 2004) closely. Suppose that all countries have the same level of capital stock, in a steady state. Then, world saving is equal to Q.{k* ,T) . Since the world economy as a whole is closed, the measures of young agents that invest in this steady state must be equal to Q{k* ,T) . Since every one of them produces R units of capital, the steady state capital must satisfy k* = RQ(k\T), or equivalently, k* = K\R,T).

Consider k* = K* (R,R) > K(A,T) . Then the borrowing constraint is not binding, and hence the world interest rate in this steady state is, from (6),

r = ( l - T ) R f \ R Q ( K * (R, T), T)) = ( 1 - T ) R f \ K * (R, r ) ) .

By construction, k* = and = 0. Thus, I have demonstrated the

existence of a stable symmetric steady state k* 二 K* {R,T) under the condition K\R,T)> K{X,T).

Now consider K � - K* (R,T) < K{A,T) . Then the borrowing constraint is binding, and hence the steady state world interest rate is, from (6),

,二 (\-T)ARf\R^iK\R,T),T)) 二 (\-T)ZRf\K'iR,T)) 厂- \-niK*{R,T),T) \-Q.iK\R,T),T)

By construction, if =少(r,r). Utilizing (21) and , , \ 二 (火(尺,『))

—r)尺 \~a(K\R,TU)

4 0

中丨(众*,”-1

1-n( / r (7?, r), r ) l^ f\K\R,T)))

� ^ f - / { R , T ) ) [ { T - X)K'(/?,r) + I ^ ^ ^ ^ l M l l - 1 \-Q.{K {R,z\z){ ( r(K {R,T))))

1 {-f (/?, D) f (r - {R, T) + I ^ l ^ ^ l ) I f iK\R,T)) J

… [ —(1 —(尺, r), r ) ) )

1 f — f (R, T)) f (r - l ) r (R, T) + ” ( 尺 ’ � T I f iK {R,T)) J

I -\ + W(K* (R, T)) + TK* (R, T)f\K* (R, T))少

…t -\ + f{K\R, T)) - K* (R, T)f\K* (R, T)) , […八 f\K\R,z)) )

The stability of the steady state is thus determined by the value of / ( / T (凡 r ) ) - r 广 (《 * ( f ,⑶广 ( f (艮⑶ - 1 . (24)

r{K\R,T)) Differentiate (24) with respective to R to obtain

'2f\K\R,T))f\K\R.T))Kl{R,T)f\K\R,T)) / ' ( r ( / ^ , 邮 ; ( 糾 ) 作 * (如 i n n 咖�c",:;」

- f � K ( 尺 , 佩 ( 凡 r ) 卜 - 告 * 二 恤 J

r(K (R,T))r(K (R,T))JJ = ( R r ) ) r ( / ^ r ) l - r - r f l - > 0 .

Using the fact that R+ � = K * (R+ ⑴,t),we have:

4 1

導 ( 0 , ⑶ ^

= 0 < 1

= / ( / ? + � ) - ( 1 - � / ' ( / r ⑴) <F{K\R\T\T))

⑴ , I 的 f (尺制 )广 (《 * (作 ) ,: ))•

riK*(R'iT),T))

Therefore, R^ (R) E (0, R+ (r)) is well-defined by

/ ( r ( 尺 拟 r ) ) - … 尺 制 ) 广 ( 欠 * ( 尺 拟 ⑶ = 1 . Note that R c � satisfies N K (RC(T),T))

K*(R^(T),T) = KU^(T),T) b y (22 ) .

4 2

Proof of Proposition 4 The proof follows that of Proposition 4 of Matsuyama (2004) closely. First, note that (8) defines k„ as a function of /c乙,denoted by k„ Differentiating (8)

shows that (j) is increasing if and only if < i ^ or

equivalently, K, < K*[R(人_ = K { ? :

疋 二 7 ^ ) “

7 " ( � ) ( 1 - /(於 J + K f \ K ) - r K f \ K ) ) \

二 n M ( i -

_ - /(M)+

二—A ^

Furthermore, 0(0) 二 0 and = K(A,T) . Suppose Then, KU,T) < KU^i rXT) . Hence for any

= ( ] ) � k j < (I>{K{X,t)) 二 , and thus (9) is violated. On the other hand, suppose 2 < A,( r ) . Then K{X,R) > , which in turn implies 0 二 外0) < K{X,T:) 二 ((){K{X,T)) < (T){K{X^{T\T)). Recall 中 is continuous and is increasing up to k,^ 二 K{A^iT),T). Therefore, there exist k , < K a ^ i T \ T ) < K { A , T ) such that 火(又〈外、T h e s e t o f i k „ k „ )

4 3

that satisfies (8)-(10) is non-empty and is illustrated by the 'thick solid portion' of •

in Fig. A.l.iG From (11), obtain an expression for X\

Xk, +{\-X)k„ = XRQ.{k,,r) + (l- X)Ra{k„,t)

Xk^ +{\-X)k„ = XRQik, ,r) + ( l - X )Rn{k„, r) X(k,- RQXJCL ,T)) + (l-X){k^ - ,T)) = 0

X 二 Ra{k„,T)-k„ = RQ{k„,T)-k„ - � - R Q i k , R以 , T ) - k ^ - { R Q ( k „ T ) - k , ) '

With (A2) and (9): K„ = K\R,T) and ^^ =K*{R,T) imply X = 0 and X =1

respectively, k^ < K*{R,T) implies either X > 1 or X < 0. And K^ > K*{R,T)

implies X > 1. But for � < K* {R, T)<K„, XE (0,1). Therefore, (A2) and (9)

imply that (11) has a solution X e c (0,1) if and only if

KI < K*{R,T) < ICH . This condition is illustrated by the ‘shaded area' in Fig. A.l .

A stable steady state {k^,k„,X) exists if and only if the 'thick solid portion' overlaps with the 'shaded area'. This condition is equivalent to, for R < R^,

KU,T) < (/>{K*IR,T)), a n d f o r R>R^,

= (I>{K\R^{T\T)) > r (i?,r). Or,for R c R �

f \ K a , T ) ) > 义 (尺’”)and for 1-Q(K*(R,T),T)

AF\KU^(T),T)) = AR(K\R(T),T)) < * ^

Note that the last inequality could be rewritten to >^<—/'(/r(/?,r))|V — l)/a/Mr),r) + r " f / 5 ( ’ ( r ) ’ ” ) ] because

f (KOic�,T)) J

Fig. A. 1 is very similar to Fig. A.3 of Matsuyama (2004). 4 4

= /1/'(拟“制)

- 1 — f(K{A^{TU)) + (1 — T)K(A^{T), T)f\K(A^.{T),T)) = —Tf\K(A^XTU))f\KU^iT),T)) , ,, Mr, j , 一 T � 尸 , r , � , � �

f {K{A^{T),T))

4 5

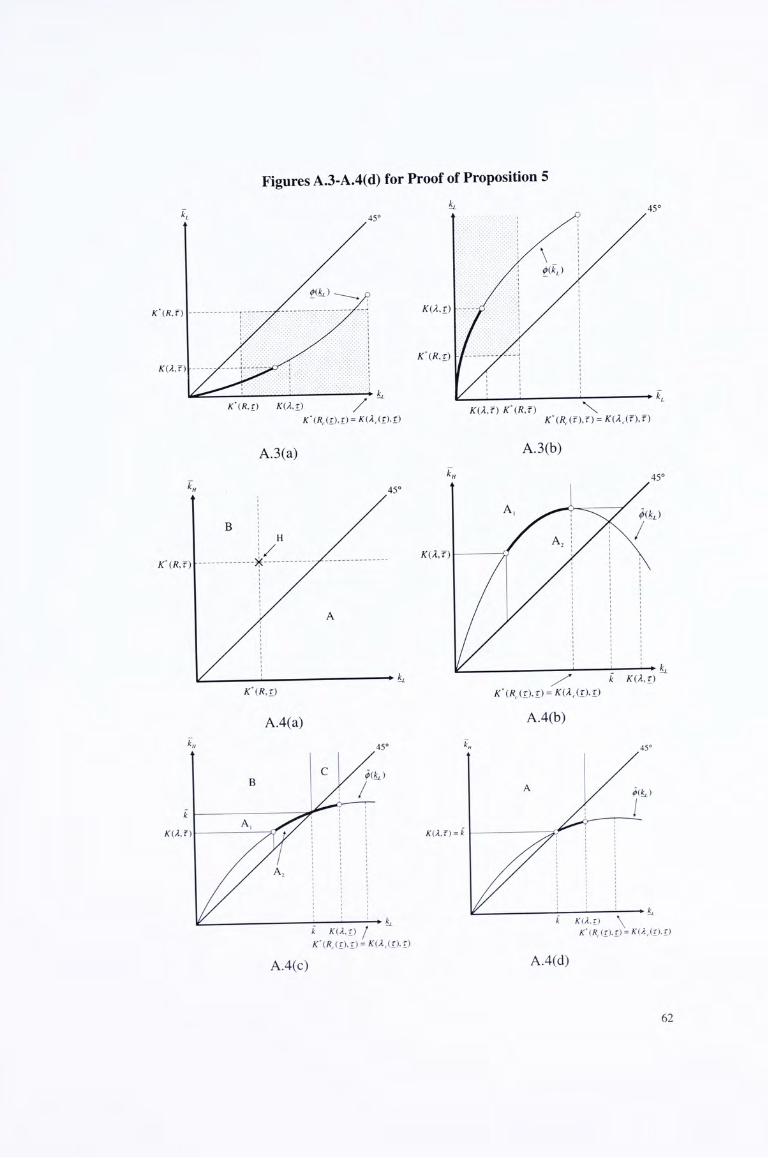

Proof of Proposition 5 From (12), obtain an expression for 乂丁:

X j ( k - RQ.{k, T)) + (\-X-,)(ki^-RQik, f ) ) = 0 X 八 l£- RQ{k, T)-(k- RQ{k, f ) ) ) + {k- RQ{k, f ) ) = 0

X ^ Ra{k,f)-k = Ra{k,f)-k (25) ^ k-RQ.{k,T)-[k-Ra(kJ)) RQ.{kJ)-k-[Ra{k,T)-k)

With (A2) and (25): k = K* (R,f) and k = K\R,T) imply = 0 and =1

respectively, k <K*(R,f) implies RQ{k , f ) - k > 0, and Xj e (0,1) if and only

if RQ.{k,z)-k<(d or, equivalently, k>K\R,z)\ k>K\R,T) implies

Xy-e (0,1) if and only if k <K\R,f). k > K\R,f) implies X ^ e (0,1) if and

only if k<K\R,T)\ k<K*(R,T) implies G (0,1) if and only if

k>K\R,f).

Therefore, (A2) and (25) imply (12) has a solution 6 c (0,1) in

general when k < K* ( R , f ) and k > K*(R,T), or k > K*(R,f) and k < K\R,Z). If k <k is required: the condition k > K*(R,f) and k < K\R,T),

which implies k<K* (R, T) < K* {R, f ) <k , have to be discarded. If k > k is required, both conditions would be retained. If k = k is required, the condition k>K*{R,f) and 左 < A:*(尺,:),which implies k < K*(R,T) < K \ R , f ) < have to be discarded.

In the following I characterize all the stable steady states with asymmetric tax rates:

Case 1: k = > K(A,T) and k =k„ >

4 6

Consider the case k = > K{X,T) and k =k„ > K{Jl,f) .From (13), in the

steady state it is necessary that < k^ . Also, (13) defines ^ as a function of k„,

denoted by k^ Differentiating (13) shows that ; is increasing:

� - - ( l - f ) m ) ^ ^

3 厂" ( l - D A ^ ) •

Furthermore, ^(0) = 0 and ^(oo) = cx>. (A2), (25) and k„ < imply (12) has a

solution Xy-e c (0,1) if and only if k„ < K*{R,f) and k^ > K*{R,T).

In Fig. A.2(a) and A.2(b), the 'thick solid portion' of (f> represents the set of

(厂",D satisfying (13), ^ = ^ > and 厂=厂“〉A:(/l’f). The ‘shaded

area' illustrates the condition 厂"< K*{R,f) and = > K*(R,[). A stable

steady state exists if and only if the 'thick solid portion' overlaps with

the 'shaded area'. For the case K*{R,f) < K{A,T) , as depicted in Fig. A.2(a), the overlapping occurs if and only if ^(K*(R,f)) > K{A,T) ; for the case K* (R,F) > K{A,T),as depicted in Fig. A.2(b), the overlapping always occurs.

Case 2: k = K{X,T) and k < K U , f )

Now consider the case k=J^< K{A, T) and k =k^< K{A, f ) . Define from { \ - T ) f \ k ) (15) H{k,T) = -——-——.Note that: //(0,r) = oo;

\-Q.{k,T)

47

H,ik,T) = (\-T) ( 1 - 肌 r ) )

- ( 1 T)广柳—他 + 料、-r 炒'(众))+ / U ) ( ( r - \)kf\k) + T f \ k ) )

. f \ k ) ( [ - f { k ) ) + T f \ k ) f \ k ) = ( l - r )

( \ - m , T ) f V 广⑷ J ’

H,ik,T)<0 if and on ly if k < K* (R^XT),T) = K(A^{T),T);

�_-f\k)(\-W{k)-TirfXk)) + (\-T) f j k W X k ) — f j k ) ( f ( k ) -1) "2(欠,r) — : 一 一, T—;

(i—i (众,r)) ( l - a ( / : , r ) f

H^{k,T)<0 if k < K*{R^{T),T) = K(A^(T),T) ; given r , H attains a minimum at

k = K\R^ ⑴,T) e (0,IT ⑴)over [0, iT � ] .

Sub-case J: H(K*(R^(t),t),t) > H ( K \ R ^ ( f ) , f ) , f )

Suppose H(K\R^.(T),T),T) > H { K \ R ^ { f \ f \ f ) . Then, given r and f ,

for any ^ E [0, K* {R^ (r) , r ) ) , there is a unique 厂乙 e [0,/:* (尺“f ),f)) satisfying

(15). Thus, I could legitimately define a continuous function

^ : [0, K*�Rc(r), T)) — [0, K*�Rc ( f ) , f ) ) , which satisfies, for ^ g [0’ K* {R^ (r) , r)),

厂L = (piki) <=> = H(k^,f). Note that over the entire domain of (J),

kj^<K* (尺c (幻’ I ) and ) = ki^<K* {R^ ( f ) , f),thus satisfying the necessary

conditions for stability when the borrowing constraints are binding. Moreover,

^(0) 二 0,and 中 is increasing because

4 8

f T f\k ) f\k ) �

( 1 - ^ ( ^ , 1 ) ) FM_,))—— 1

V — J Now, recall that / / , ( ) t , r ) < 0 and H ^ { k , T ) < 0 under any stable steady state k.

Therefore, given any permissible if there are ( and f that fulfill (15),

it is necessary that 厂乙�& since f > T. Consequently, the portion of ^ over

(0,K*(RJt),t)) is under the 45-degree line. (A2), (25) and imply (12)

has a solution E CZ (0,1) if and only if ^^ < K*{R,f) and

k^ > K�R,幻.

In Fig. A.3(a),the 'thick solid portion' of ^ represents the set of 厂乙)

satisfying (15), k = K(A,t) and 厂二& < Ki/i,f). The ‘shaded area'

illustrates the condition ) = k^< K*(R,f) and k^ > K*(R,T) . A stable steady

state exists if and only if the 'thick solid portion' overlaps with the

'shaded area,. This happens if and only if ^{K*{R,T)) < K(A,F).

Sub-case 2: H{K*(R^(T),T),T) < H(K*(R^(f),f\f)

Now suppose H{K*{R^(T\T\T) < H (K* ( R ^ ( f ) , f ) , f ) . Then, given T and

f, for any k^ e [0, K* (R^ ( f ) , f ) ) , there is a unique ^ 6

satisfying (15). Thus, I could legitimately define a continuous function

t : [0,K* (Rc ( f ) , f ) ) -> [0,K* (R^ (T), T)),which satisfies, for k^ e [0, K* (R^. ( f ) , f)),

49

一 一 一 一 一 一 一 一 一 一 一 一 一 一 ———————————————————— 一 一 一 一 一 一

^ = )<=> H{ki^,T) = H{k^,f). Note that over the entire domain of (f),

厂乙 < K \ R ^ { f ) , f ) and ^ = K*(R^(T),T),thus satisfying the necessary

conditions for stability when the borrowing constraints are binding. Moreover,

^(0) = 0 , and (j) is increasing because

(1 — i X 辦厂J,幻)2(1 — ( 厂 J — (厂)二 V J yki^) 一 7 .

- L r^n 、产/厂��f ��工广(列&))/'(辦厂乙))

[\-m„r)) (\-T)f i^ik,)) f m , ) ) - - - 上 1 I ~ f (帆)) )

Now, recall that / / , {k,r) < 0 and H^ {k,z) < 0 under any stable steady state k.

Therefore, given any permissible , if there are ^ and r that fulfill (15),

it is necessary that ^ > ^^ since r < T . Consequently, the portion of 伞 over

is above the 45-degree line. (A2), (25) and imply (12)

has a solution X j e c: (0,1) if and only if 厂乙 < K* (尺,f) and ^ >K\R,T).

In Fig. A.3(b), the 'thick solid portion' of 中 represents the set of (A: , ^ )

satisfying (15), k = kj^< K(Ji,T) and f =厂乙 < K(A, f ) . The 'shaded area'

illustrates the condition 厂乙 < fT ( R , � � a n d 々 ( 厂 二 ^ > K*(R,T) . A stable steady

state exists if and only if the 'thick solid portion' overlaps with the

'shaded area,. This happens if and only if K*{R,T) > .

Case 3: K = I£L < and k =k„ > K{X,f)

Consider the case k = J^< K{/i,T) and k > K{X,f). The stability of

5 0

k = L^<KU,T) requires < K\R^T),T) = K{A^{T),T) . (18) defines k„ as

a function of ^ , denoted by = ) . Differentiating (18) shows that ^ is

increasing if and only if ^ < K* = :

9 {K) = 二 •

(1-^) 驰 ,幻)

Note t h a t � ( 0 ) 二 0 . Now, suppose 厂 " = & = � > 0. Then (18) reduces to

1 = ——^, implying k<K{X,T). k is well-defined if and only if ^ V • —

>1

- ^ <—, in which case d intersects the 45-degree line. Moreover, whenever k (1 - f ) A is well-defined, it is unique.

To facilitate subsequent discussions, in Fig. A.4(a) I illustrate the condition k <K*iR,f) and k>K*{R,T) by 'Quadrant A', and the condition k > K*{R,f) and k < K*(R,T) by ‘Quadrant B' . The position of the point H = (K* {R,T),K\R,f)), which must be above the 45-degree line given the way I draw the graph, is, as evident below, pivotal for the existence of various types of stable steady states.

Sub-case 1": A(l~T)<l-f, < 0 and K{Xj) < ^{K* {R^{T\T))

In Fig. A.4(b), observe that the decreasing portion of ^ intersects the

45-degree line under this sub-case. The 'thick solid portion' of 夺,which is

1 ‘ I only present the conditions for the existence of the various types of stable steady states graphically in all the sub-cases under Case 3. But note that the exact conditions in algebraic form could easily be translated from the graphs.

5 1

non-empty if and only if K(A,F) < ^(K* (R^.(T\T)) , represents the set of (&,/:")

satisfying (18), k=k^< K*{R^{t),t) <k< K{X,t) and k > N o t e

that along the 'thick solid p o r t i o n '厂 " = ) > ^ . Consequently, (A2), (25) and

> kj^ imply (12) has a solution X j e {X" cz (0,1) if and only if

< K*{R,f) and ^ > K*(R,T), or k„ > K \ R , f ) and ^ <K*{R,T).

Therefore, stable steady states with > k^ exist if and only if

H = {K*{R,f),K\R,f)) is within area A, or K^ AiH is in area A,, the 'thick

solid portion' overlaps with 'Quadrant A', and if H is in area Aj,the 'thick solid

portion' overlaps with 'Quadrant B,.

Sub-case 2: A ( l - r ) < 1 - f , 0 < < 1 and

K{X,f) <k< i f / l > <

K U , f ) < k < i f / l <

In Fig. A.4(c)i2,observe that the increasing portion of ^ intersects the

45-degree line under this sub-case. The 'thick solid portion' of 夺,which is

non-empty if and only if < for X > and

K{X,F) < for A < , represents the set of (&,厂") s a t i s f y i n g

(18), k = <k<mm{KiA,T), K*(R(TXT)] and k =k„ > . Note that

the 'thick solid portion' intersects the 45-degree line. Consequently I have three In this sub-case and the following 3, I only illustrate the case A > for conciseness. In

each of these sub-cases the possible types of stable steady states are the same and very similar graphical characterization could be obtained under either A > or A < •

5 2

possible types of steady states, namely,厂"〉&,厂"�& and 厂 “ = & . Recalling

the conditions for a solution X j e c= (0,1) to (12), I illustrates the

conditions for the existence of the steady states in Fig. A.4(c). Whenever

H = {K* {R,T),K* {R,f)) lies in region A, or A,,there exist only stable steady

states ,XJ) with 厂"〉&. Whenever H lies in region B, stable steady states

with 厂 " 〉 L , < KJ^ or =1^=K coexist. Lastly, whenever H

lies in region C, there exist only stable steady states , ^^, ) with 厂"< & .

Sub-case 3: / l ( l - r ) < 1 - f , 0 < < 1 and

< K{A,f) < ifA> A^(T) k < K{A,f) < ifA<

This sub-case is the same as Sub-case 2 except that here I consider k < K ( A , f ) .

As depicted in Fig. A.4(d), although the increasing portion of ^ still intersects the

45-degree line under this sub-case, the 'thick solid portion' of 夺 is now strictly

below it, implying /: < ^ for any potential stable steady state. Whenever

H = (K* (R, T), K* {R, F)) lies in region A, there exist stable steady states

with kf < kj^.

Sub-case 4: / l ( l - r ) < \ - f , = 1 and

<k< i f / l > 又 K{XJ) <k< if 义 < ?

5 3

In Fig. A.4(e), observe that the increasing portion of 夺 is tangential to and

below the 45-degree line under this sub-case. The 'thick solid portion' of 添,which

is non-empty if and only if K{X,F) < ^{K{X,T)) for X > and

K { X , f ) < ^{K* {R^{T),T)) for A represents the set of (&,【")satisfying

(18), k = ^ <min{A:(/ l , r) , K*(RJt),t)} and k =k„ > . Since the 'thick

solid portion' is tangential to the 45-degree line, there are three possible types of

steady states, namely,厂"〉&, < kj and 厂 " = . Recalling the conditions for

a solution X j e e (0,1) to (12), I illustrates the conditions for the

existence of the steady states in Fig. A.4(e). Whenever H = (K* (R,T),K* {R,f))

lies in region A or C, there exist only stable steady states with

< k . Whenever H lies in region B, stable steady states , ^^ , Xy) with

kf < kj or = Kl-^ coexist.

Sub-case 5: ^ ( l - r ) < \ - f , = 1 and

k < K { X , f ) < ifA> J k < K{A,f) < ifA<

This sub-case is the same as Sub-case 4 except that here I consider ic < K{A,f).

As depicted in Fig. A.4(f), although the increasing portion of 添 is still tangential to

and below the 45-degree line under this sub-case, the 'thick solid portion' is now

strictly below it, implying /: < ^ for any potential stable steady state. Whenever

H =(lC (R, t), K* {R, f ) ) lies in region A, there exist stable steady states

5 4

with 厂

Sub-case 6: / l ( l - r ) > l - f , A>Jl^(r) and K{X,f) <

In Fig. A.4(g), observe that 夺 is below the 45-degree line under this sub-case.

The 'thick solid portion' of ^,which is non-empty if and only if

K ( A , f ) < ^(K(yl,T)), represents the set of (&,厂")satisfying (18),

k = kj^< K(Z,T) and k = k„ > K{A,f). In this sub-case (12) has a solution

Xy. 6 if and only if k^ < K \ R , f ) and ^ > K\R,T).

Therefore, stable steady states with 厂"< & exist if and only if

H = (K* (尺,I), K* (R, f ) ) is within area A.

Sub-case 7: A { l - T ) > l - f , A<A^(T) and K{Ji,f)<^(K*(R^{T),T)

In Fig. A.4(h), observe that ^ is again below the 45-degree line under this

sub-case. The 'thick solid portion' of ^,which is non-empty if and only if

KIA,F) < ^{K* {R^(T),T) , represents the set of satisfying (18),

k=kj^< K*(R^(T),T) and k =k„ > K{A,f). In this sub-case (12) has a solution

E if and only if < K\R,f) and ^ >K\R,r).

Therefore, stable steady states with 厂 " � & exist if and only if

H = iK*iR,T),K\R,f)) is within area A.

5 5

From the above sub-cases, I find that: If / l ( l - r ) > l - f , stable steady states, if

exist, must fulfill 厂〈左;if / l ( l - r ) < l - f and < 0 , stable steady states, if

exist, must fulfill 厂〉左;If / l ( l - r ) < l - f , 0 < < 1 and k<K{A,f),

stable steady states, if exist, must fulfill 厂〈左;if A ( l - r ) < 1 - r , 0 < < 1

and k > K{X,f), stable steady states, if exist, could fulfill k <k, k > k or

k =k.

Case 4: k = k^ > K(A,T) and k =ki^< K{X,f)

Consider the case k = k^ > K(A,T) and k =kj^< K{X,f). Countries all over

the world face the same interest rate ——=r = (1 - T)Rf ( ^ ) , or

,(…iizll 卿 (26) ( i - i )

The stability of K{XJ) requires 厂,< K \ R ^ { f \ f ) = K(A^{f),f). (26)

defines ^ as a function of k^ ’ denoted by ^ = ).Differentiating (26) shows

that ( f ) is increasing if and only if 厂[< A:* (尺(.(J),f) 二 A^(义“f ),f):

办 — i i z i M _ _ I ^ — I ~ (1 —幻

Note that ^(0) = 0 • Now, suppose [ = ^ = � > 0. Then (26) reduces to (1 _ f ) ; _ _ 1 = ^ i z ’ implying k = k,> K(A,f),which is a contradiction. (1-r) l-Q(k,f)

‘ V ‘ <1

56

一 一 一 ———— 一

Therefore,中 does not intersect the 45-degree line for positive k i . In Fig. A.5,1

depict the function (j). For any admissible K{A,f), any k^ smaller than K(A,f)

fulfills K^ = (L>{KI^)< K{X,F) < K{X,T) . Thus, there does not exist any

satisfying k=k„> K(A,T) and 厂=厂乙 < K{A,f). I could now conclude that

there is no stable steady state with asymmetric tax rates under this sub-case.

5 7

Figure 1. Dynamics 一 autarky.

r+I “ 45°

R 7

Figure 2. Asymmetric tax - autarky.

众丨 ‘‘ 4 5 �

匪. K'{R,f)

5 8

Figure 3. Dynamics - small open economy.

t 45° \ ^45°

- f e ) 1

A \ 奸 I n ;

(a) (b) . 4 5 ° R

•fe)

jf\ .(I 丨 i ;

/ ! ! • K K r) K丨 R

(C)

5 9

Figure 4. Asymmetric tax 一 small open economy.

I �+1 •

45。 ‘

亡 R 、 k, K k〒 R

(a) (b)

Figure 5. Figure 6. Asymmetric tax - world economy. Equality of nations in asymmetric tax.

45° 尺 R :; R /

匪• k^ ^ KU,f)KiA,T) k„ k,, R R

(a) (b)

6 0

Figure A.l for Proof of Proposition 4.

k„ 45。

欠(义’ r) — — �

乙 ~ ‘ ~ i “L Z K ' { R , t ) K { X , T )

Figure A.2 for Proof of Proposition 5

^ 4 5 ° ’ 4 5 °

— ( / I 乙 K ^ i • ‘

K\R,f) K'(R,f) A.2(a) A.2(b)

6 1