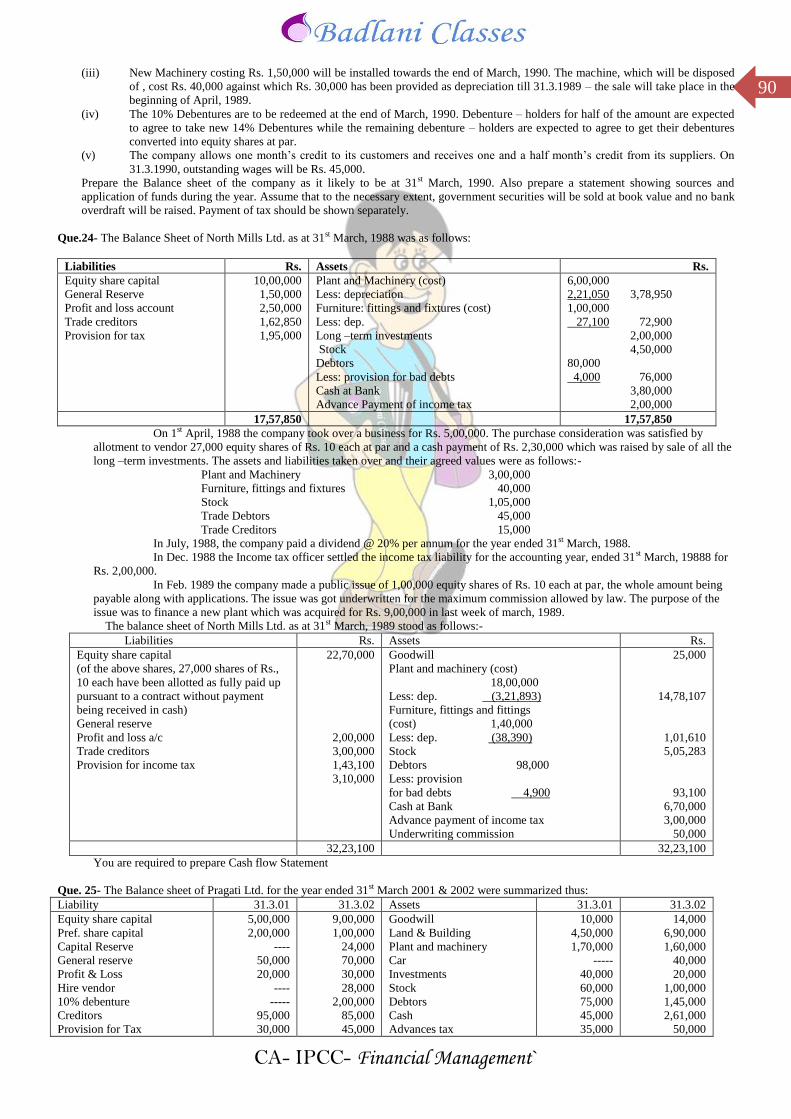

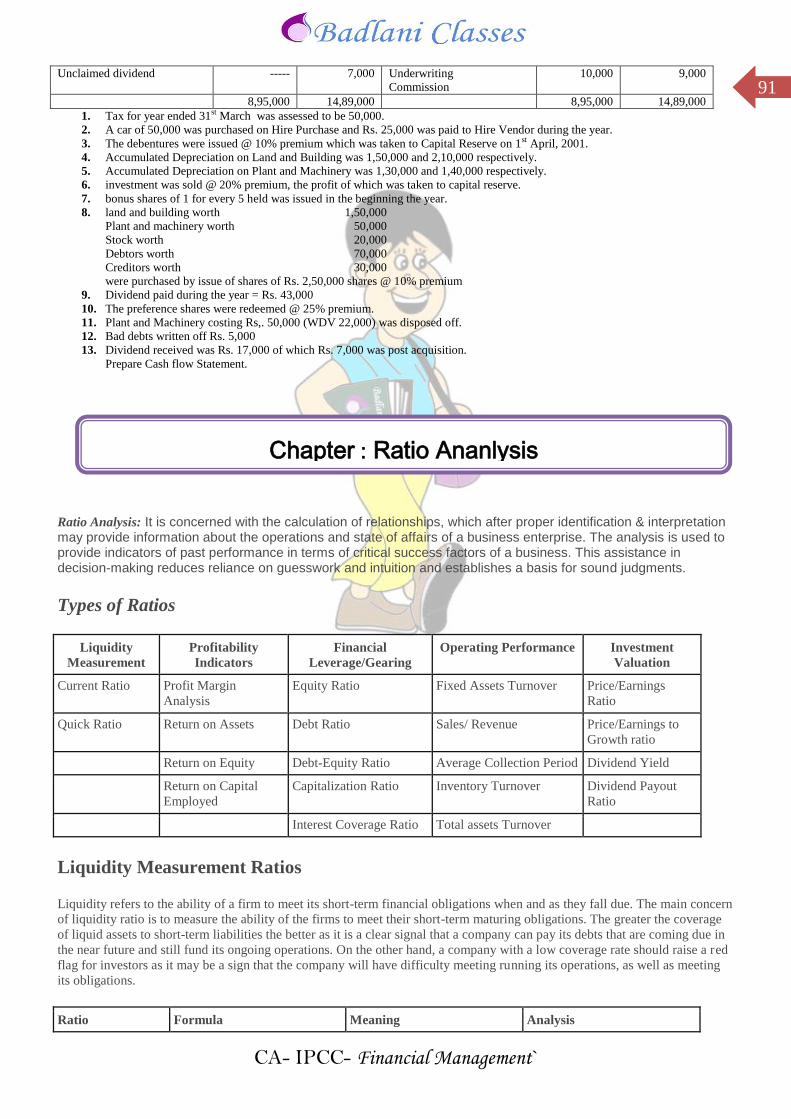

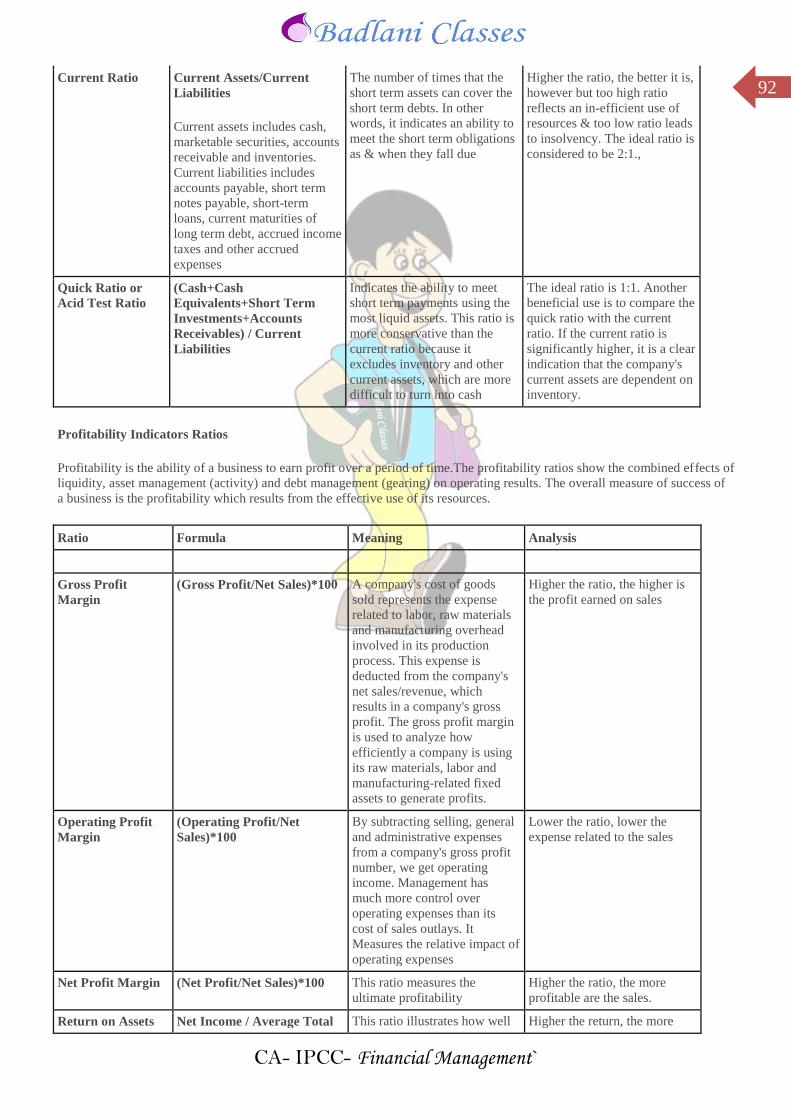

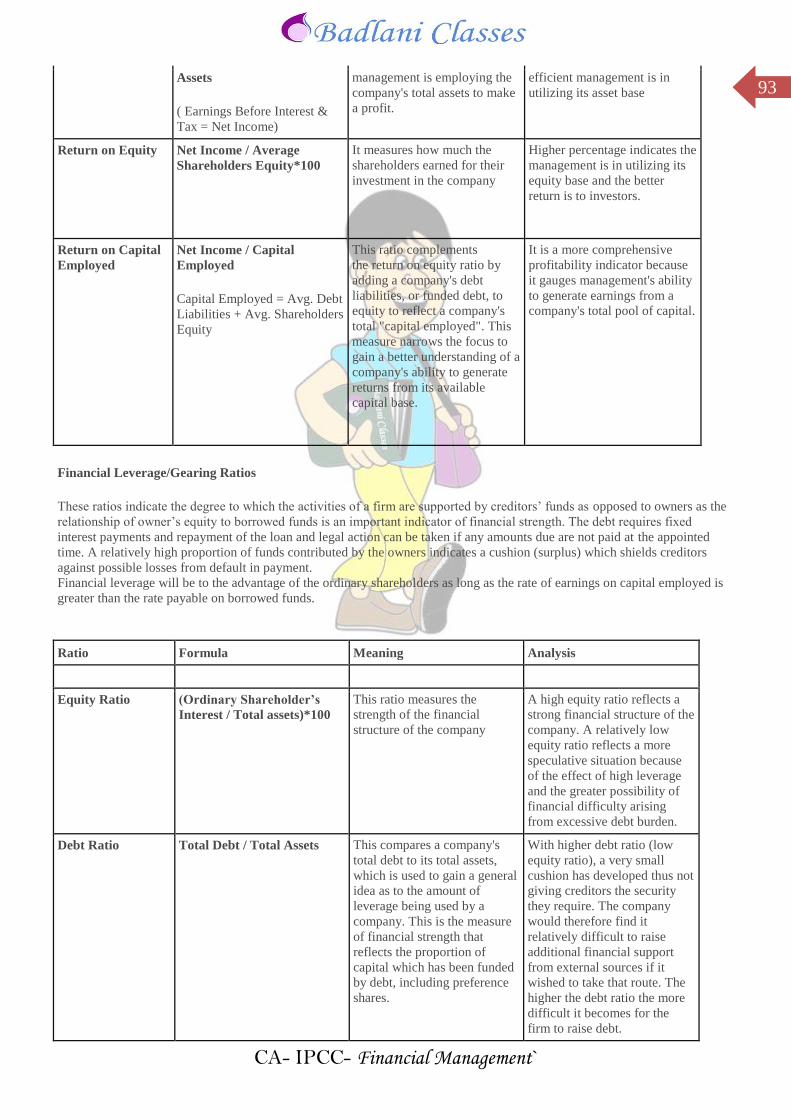

Financial Management` 1 Question : What do you mean by financial management ? Answer : Meaning of Financial Management : Financial management deals with procurement of funds and their effective utilisation in the business.. The primary task of a Chartered Accountant is to deal with funds, 'Management of Funds' is an important aspect of financial management in a business undertaking or any other institution like hospital, art society, and so on. The term 'Financial Management' has been defined differently by different authofrs. According to Solomon "Financial Management is concerned with the efficient use of an important economic resource, namely capital funds." Phillippatus has given a more elaborate definition of the term, as , "Financial Management, is concerned with the managerial decisions that results in the acquisition and financing of short and long term credits for the firm." Thus, it deals with the situations that require selection of specific problem of size and growth of an enterprise. The analysis of these decisions is based on the expected inflows and outflows of funds and their effect on managerial objectives. The most acceptable definition of financial management is that given by S.C.Kuchhal as, "Financial management deals with procurement of funds and their effective utilisation in the business." Thus, there are 2 basic aspects of financial management : 1) Procurement of funds : As funds can be obtained from different sources thus, their procurement is always considered as a complex problem by business concerns. These funds procured from different sources have different characteristics in terms of risk, cost and control that a manager must consider while procuring funds. The funds should be procured at minimum cost, at a balanced risk and control factors. Funds raised by issue of equity shares are the best from risk point of view for the company, as it has no repayment liability except on winding up of the company, but from cost point of view, it is most expensive, as dividend expectations of shareholders are higher than prevailing interest rates and dividends are appropriation of profits and not allowed as expense under the income tax act. The issue of new equity shares may dilute the control of the existing shareholders. Debentures are comparatively cheaper since the interest is paid out of profits before tax. But, they entail a high degree of risk since they have to be repaid as per the terms of agreement; also, the interest payment has to be made whether or not the company makes profits. Funds can also be procured from banks and financial institutions, they provide funds subject to certain restrictive covenants. These covenants restrict freedom of the borrower to raise loans from other sources. The reform process is also moving in direction of a closer monitoring of 'end use' of resources mobilized through capital markets. Such restrictions are essential for the safety of funds provided by institutions and investors. There are other financial instruments used for raising finance e.g. commercial paper, deep discount bonds, etc. The finance manager has to balance the availability of funds and the restrictive provisions tied with such funds resulting in lack of flexibility. In the globalised competitive scenario, it is not enough to depend on available ways of finance but resource mobilization is to be undertaken through innovative ways or financial products that may meet the needs of investors. Multiple option convertible bonds can be sighted as an example, funds can be raised indigenously as also from abroad. Foreign Direct Investment (FDI) and Foreign Institutional Investors (FII) are two major sources of finance from abroad along with American Depository Receipts (ADR's) and Global Depository Receipts (GDR's). The mechanism of procuring funds is to be modified in the light of requirements of foreign investors. Procurement of funds inter alia includes : - Identification of sources of finance - Determination of finance mix - Raising of funds - Division of profits between dividends and retention of profits i.e. internal fund generation. 2) Effective use of such funds : The finance manager is also responsible for effective utilisation of funds. He must point out situations where funds are kept idle or are used improperly. All funds are procured at a certain cost Chapter : Introduction

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Management`

1

Quest ion : What do you mean by f inancia l management ?

Answer : Meaning of Financial Management :

Financial management deals with procurement of funds and their effective utilisation in the business..

The pr imary task of a Charte red Accountant i s to dea l wi th funds, 'Management o f Funds ' i s

an important aspect o f f inancia l management in a business under taking or any o ther ins t i tut ion l ike

hospi ta l , ar t soc iety, and so on. The term 'F inancia l Management ' has been def ined di fferently by

di fferent authofrs.

According to Solomon "Financial Management is concerned wi th the e ff icient use of an

important economic resource, namely cap ital funds." Phi l l ippa tus has given a more e laborate

def ini t ion of the term, as , "Financial Mana gement, i s concerned wi th the manageria l decis ions that

result s in the acquis i t ion and financing of short and long term credi t s fo r the firm." Thus, i t deals

wi th the si tua tions tha t require select ion of speci fic prob lem of size and gro wth of an enterpr ise. The

analys is o f these decisions i s based on the expected inf lows and out flo ws of funds and the ir e ffect on

manager ia l object ives.

The most accep tab le def ini t ion of f inancia l management i s that given by S.C.Kuchhal

as, "Financial management deals w i th procurement o f funds and the i r effect ive ut i l isat ion in the

business." Thus, there a re 2 basic aspects o f f inancia l management :

1) Procurement of funds : As funds can be obtained from di fferent sources thus, the ir procurement i s a lways c onsidered

as a complex problem by business concerns. These funds procured from d i fferent sources have

di fferent charac ter is t ics in terms of r i sk, cos t and control that a manager must consider whi le

procuring funds. The funds should be procured at minimum cost , a t a balanced r i sk and cont rol

factors.

Funds ra ised by issue of equity shares a re the best fro m r isk po int o f view for the company,

as i t has no repayment l iabi l i ty except on winding up of the company, but from cost point o f view, i t

is most expensive, as dividend expectat ions o f shareholders are higher than prevai l ing interest rates

and dividends are appropriat ion of prof i t s and not al lo wed as expense under the income tax ac t . The

issue of new equity shares may di lute the contro l o f the exis t ing shareholders.

Debentures are compara tively cheaper s ince the interes t i s pa id out o f p rofi ts before tax. But,

they entai l a high degree of r isk s ince they have to be repa id as per the terms of agreement; a lso, the

interes t payment has to be made whether or not the company makes prof i t s .

Funds can a lso be procured from banks and financial inst i tut ions, they provide funds subject

to cer ta in res tr ict ive covenants. These covenants res tr ict f reedom of the borrower to raise loans fro m

other sources. The reform process i s also moving in direct ion of a c loser monitor ing of 'end use ' o f

resources mobil ized through cap ita l markets . Such restr ic t ions are essential for the safety o f funds

provided by ins t i tut ions and investors. There are other f inancia l instruments used for rais ing f inance

e .g . commercial paper , deep discount bonds, etc . The finance manager has to balance the ava ilabil i ty

of funds and the rest r ic t ive provis ions t ied wi th such funds result ing in lack of f lexib il i ty.

In the globali sed co mpet i t ive scenario , i t is no t enough to depend on ava ilable ways of

f inance but resource mobil iza t ion i s to be under taken through innovat ive ways or financial p roducts

that may meet the needs o f investors. Mult iple op tion conver t ib le bonds can be sighted as an

example, funds can be raised indigenously as also fro m abroad. Foreign Direc t Investment (FDI) and

Fore ign Inst i tut iona l Investors (FI I) are two major sources o f f inance from abroad along wi th

Amer ican Depository Receip ts (A DR's) and Global Deposi tory Receipts (GDR's) . The mechanism of

procuring funds i s to be modified in the l ight of requirements o f fore ign investors. Procurement o f

funds inter al ia inc ludes :

- Ident i ficat ion of sources o f finance

- Determinat ion of f inanc e mix

- Raising of funds

- Division of p rofi ts between d ividends and retent ion of p rofi ts i .e . in terna l fund genera tion.

2) Effect ive use of such funds : The f inance manager i s also responsible for e ffect ive ut i l i sa t ion of funds . He must po int out

si tua tions where funds are kep t idle or are used improperly. All funds are p rocured at a cer ta in cost

Chapter : Introduction

CA- IPCC- Financial Management`

2

2

and after entai l ing a cer tain amount o f r i sk. I f the funds are no t ut i l ised in the manner so tha t they

genera te an income higher than cost o f procurement , there i s no meaning in running the business. I t is

an important considerat ion in dividend dec isions also, thus, i t i s cruc ia l to employ funds properly and

prof i tab ly. The funds a re to be employed in the manner so tha t the company can produce a t i t s

optimum level wi thout endangering i t s financia l solvency. Thus, f inancia l implicat ions o f each

decision to invest in fixed asse ts are to be properly ana lysed. For this, the f inance manager must

possess sound knowledge of techniques o f capita l budgeting and mus t keep in view the need of

adequate working capi ta l and ensure that whi le f irms enjoy an op timum leve l o f working cap ita l they

do no t keep too much funds blocked in inventor ies, book debts, cash, etc .

F ixed assets a re to f inanced fro m medium or lon g term funds, and not short term funds, as f ixed

asse ts cannot be so ld in shor t term i .e . wi thin a year , a l so a large amount o f funds would be blocked

in s tock in hand as the company cannot immedia tely sel l i ts finished goods.

Quest ion : Explain the scop e of f inancia l management ?

Answer : Scope of f inancial management : A sound f inancial management is essent ia l in a l l type of f inancia l organisat ions - whether

prof i t or iented or no t , where funds are invo lved and a lso in a central ly p lanned e conomy as also in a

capi tal i st set -up . Firms, as per the commercia l his tory, have not l iquidated because thei r technology

was obso lete or their products had no or lo w demand or due to any o ther factor , but due to lack of

f inancia l management. Even in boom per iod, when a co mpany makes high profi t s , there i s danger o f

l iquidat ion, due to bad f inancia l management. The main cause of l iquidat ion of such companies i s

over - trad ing or over -expanding without an adequate f inancia l base .

Financial management op timises the output f rom the given input o f funds and at tempts to use

the funds in a most productive manner . In a country l ike India, where resources are scarce and

demand on funds are many, the need for proper f inancia l management i s enormous. I f proper

techniques a re used most o f the enterpr ises can reduce the ir capi ta l employed and improve return on

investment. Thus , as men and machine are properly managed, f inances are also to be well managed.

In newly sta r ted companies, i t i s impor tant to hav e sound financial management, as i t ensures

their survival , o ften such companies ignores financia l management a t their own peri l . Even a s imple

act , l ike deposit ing the cheques on the day of the ir receip t i s not per formed. Such organisa t ions pay

heavy inte res t charges on borro wed funds, but a re tardy in real is ing the ir own deb tors. This i s due to

the fac t they lack real isat ion of the concept o f t ime value of money, i t is not appreciated tha t each

va lue of rupee has to be made use o f and that i t has a direct cost o f ut i l i sa t ion. I t must be real i sed

that keeping rupee idle even for a day, resul ts into losses . A non -profi t organisat ion may not be keen

to make profi t , t rad it ionally, but i t does need to cut down i t s cos t and use the funds at i t s disposa l to

their opt imum capaci ty . A sound sense of f inancia l management has to be cul t iva ted among our

bureaucra ts, administrators, engineers, educat ionis ts and public a t large . Unless this i s done, co lossa l

wastage of the capi ta l resources cannot be arrested.

Quest ion : What are the object ives of f inancia l management ?

Answer : Object ives of f inancial management : Eff ic ient f inancia l management requires exis tence of some objectives or goals because

judgment as to whether or not a financial decision i s e f f ic ient i s to be made in l ight o f some

objective . The two main objectives o f financial management are :

1) Profit Maximisat ion : I t is t rad it ional ly being argued, tha t the objec tive o f a company is to earn prof i t , hence the object ive

of f inancia l management i s prof i t maximisat ion. Thus, each a l ternat ive , i s to be seen by the f inance

manager from the view point o f prof i t maximisat ion. But , i t cannot be the only objec tive of a

company, i t i s a t best a l imi ted object ive else a number o f prob lems would ar ise. Some of them are :

a) The term profi t i s vague and does no t c lar i fy what exact ly i t means. I t conveys d i fferent meaning

to di fferent people.

b) Profi t maximisat ion has to be at tempted wi th a real isat ion of r i sks involved . There i s direc t

rela t ion bet ween r isk and profi t ; h igher the r isk, higher i s the prof i t . For maximising profi t , r i sk is

al together ignored, implying tha t f inance manager accep ts highly r isky proposals a lso. Pract ical ly,

r isk i s a very important factor to be balanced wi th profi t objec tive .

c) Profi t maximisat ion is an objec tive not taking into account the t ime pattern o f returns.

E.g. Proposa l X gives re turns higher than that by proposa l Y but , the t ime per iod i s say, 10 years and

7 years respect ively. Thus, the overal l prof i t is onl y considered no t the t ime per iod, nor the f low of

prof i t .

d) Prof i t maximisat ion as an object ive i s too narrow, i t fai l s to take into account the soc ial

considera t ions and obl iga tions to var ious interes ts o f workers , consumers, socie ty, as well as ethica l

CA- IPCC- Financial Management`

3

3

t rade prac tices. Ignor ing these fac tors, a company cannot survive for long. Prof i t maximisa tion at the

cost o f soc ial and moral obliga tions i s a shor t sighted pol icy.

2) Wealth maximisat ion : The companies having profi t maximisa tion as i t s object ive, may adopt po lic ies yielding

exorb itant profi ts in the shor t run which are unheal thy for the growth, survival and overal l interests

of the business. A company may not under take planned and prescr ibed shut -downs of the p lant for

maintenance, and so on for maximis ing profi ts in the shor t run. Thus , the objec tive of a f irm should

be to maximise i t s va lue or weal th.

Accord ing to Van Horne, "Value of a firm is represented by the market pr ice of the

company's common stock. . . . . . . the marke t pr ice of a firm's stock represents the foca l judgment of al l

market par t icipants as to what the value of the par t icular f irm is. I t takes into account present as a lso

prospective future earnings per share, the t iming and r i sk o f these earning, the d ivide nd pol icy of the

f irm and many other fac tors having a bear ing on the market pr ice o f s tock. The market pr ice serves as

a per formance index or report card of the firm's progress . I t ind ica tes how wel l management i s doing

on behal f o f stockholders." Share pr ices in the share market , a t a given point o f t ime, are the resul t o f

a mixture o f many fac tors, as genera l economic outlook, par t icular outlook of the co mpanies under

considera t ion, technica l fac tors and even mass psychology, but , taken on a long term bas is, they

ref lect the value , which var ious par t ies, put on the company.

Normally this va lue i s a funct ion, o f :

- the l ikely rate o f earnings per share o f the company; and

- the capi ta l i sa t ion rate .

The l ikely ra te of earnings per share (EPS) depends upon the assessment as to the profi tably

a company is go ing to operate in the future or what i t i s l ikely to earn aga inst each of i t s ordinary

shares.

The cap ital isat ion ra te re f lec ts the l iking of the investors o f a company. I f a comp any earns a

high rate o f earnings per share through i ts r i sky operat ions or r isky f inancing pa ttern, the investors

wi l l not look upon i t s share wi th favour . To tha t extent , the market va lue of the shares o f such a

company wi l l be lo w. An easy way to de term ine the cap ital i sat ion ra te is to s tar t wi th fixed deposit

in teres t rate o f banks , investor would want a higher re turn i f he invests in shares, as the r i sk

increases . How much higher return is expected, depends on the r i sks involved in the par t icular share

which in turn depends on company po licies, pas t records, type of business and confidence commanded

by the management. Thus, cap ita l i sa t ion ra te i s the cumula tive result o f the assessment o f the var ious

shareholders regard ing the r i sk and o ther quali tat ive fac tors o f a company. I f a co mpany invests i t s

funds in r i sky ventures, the investors wi l l put in thei r money i f they ge t higher re turn as compared to

that f rom a low r i sk share.

The market va lue of a share i s thus, a function of earnings per share and capital i sat ion rate .

Since the profi t maximisat ion cr i ter ia cannot be applied in real wor ld si tua tions because of i ts

technica l l imi tat ion the f inance manager o f a company has to ensure tha t his dec is ions a re such tha t

the market va lue of the shares o f the company is maximum in the long run. This impl ies tha t the

f inancia l policy has to be such tha t i t opt imises the EPS, keeping in view the r i sk and other factors.

Thus, wealth maximisa t ion i s a be tter object ive for a commercial under taking as com pared to return

and r i sk.

There i s a growing emphasis on socia l and other obl igat ions of an enterpr ise. I t cannot be

denied tha t in the case of under takings, especia l ly those in the publ ic sector , the question of weal th

maximisat ion i s to be se en in context o f soc ia l and o ther ob ligat ions o f the enterpr ise .

I t must be unders tood that financial dec is ion making i s re lated to the objec tives of the

business. The finance manager has to ensure tha t there i s a posit ive impact o f each f inanc ia l decision

on the fur therance of the business objec tives . One of the main object ive of an under taking may be to

"progress ive ly bui ld up the capabil i ty to under take the des ign and development o f a ircraft engines,

he licopters, e tc ." A finance manager in su ch cases wi l l a l loca te funds in a way that this object ive i s

achieved a l though such an al loca tion may no t necessar i ly maximise weal th .

Quest ion : What are the funct ions of a Finance Manager ?

Answer : Functions of a Finance Manager : The twin aspects, procurement and effect ive ut i l i sat ion of funds are cruc ial tasks faced by a

f inance manager . The f inancial manager is requi red to look into the f inancial implicat ions o f any

decision in the f irm. Thus al l decisions involve management o f funds under the purview of the

f inance manager . A large number o f dec is ions involve substantial or mater ia l changes in value of

funds procured or employed . The finance manager , has to manage funds in such a way so as to make

their opt imum ut i l isat ion and to ensu re the ir procurement in a way tha t the r isk , cos t and cont rol are

properly balanced under a given s i tuat ion. He may not , be concerned wi th the decis ions , that do no t

affec t the basic financia l management and s truc ture .

CA- IPCC- Financial Management`

4

4

The nature o f job of a n accountant and finance manager i s di ffe rent , an accountant 's job is

pr imar i ly to record the business transactions, prepare financial sta tements sho wing resul t s of the

organisat ion for a given per iod and i t s financia l condi t ion a t a given point o f t ime. H e i s to record

var ious happenings in monetary terms to ensure tha t assets, l iabi l i t ies, incomes and expenses are

properly grouped, c lass i fied and d isclosed in the f inancia l s tatements . Accountant i s not concerned

wi th management o f funds that is a spec ial i sed task and in modern t imes a complex one. The finance

manager or control ler has a task entirely d i fferent from that o f an accountant , he i s to manage funds .

Some of the impor tant decisions as regards f inance are as fo l lo ws :

1) Estimating the requireme nts of funds : A business requires funds for long term purposes i .e .

investment in fixed assets and so on. A careful est imate o f such funds i s required to be made. An

assessment has to be made regard ing requirements o f working cap ita l involving, es t imat io n of amount

of funds blocked in cur rent assets and tha t l ikely to be genera ted for short per iods through current

l iab il i t ies. Forecast ing the requirements o f funds is done by use o f techniques o f budgetary cont rol

and long range planning. Estimates o f requ irements o f funds can be made only i f a l l the physical

act ivi t ies o f the organisat ion are fo recas ted. They can be trans la ted into monetary terms.

2) Decis ion regarding capital structure : Once the requirements o f funds i s es t imated , a decision

regarding var ious sources from where the funds would be ra ised i s to be taken. A proper mix of the

var ious sources i s to be worked out , each source of funds involves di ffe rent i ssues for considerat ion.

The finance manager has to carefully look into the exis t ing c api ta l s tructure and see how the var ious

proposa ls o f ra ising funds wi l l a ffec t i t . He i s to mainta in a proper ba lance between long and shor t

term funds and to ensure that suff ic ient long -te rm funds are raised in order to finance fixed assets

and o ther long-term investments and to provide for permanent needs o f working cap ita l . In the

overal l volume of long -term funds, he i s to ma inta in a proper ba lance between own and loan funds

and to see tha t the overal l cap ita l i sa t ion of the company is such, that the co mpany is ab le to p rocure

funds at minimum cost and is ab le to tolera te shocks of lean per iods . All these decisions are kno wn

as ' f inancing dec is ions ' .

3) Investment dec ision : Funds procured from d i fferent sources have to be invested in var ious kinds

of asse ts. Long term funds are used in a projec t for f ixed and a lso current assets. The investment o f

funds in a project is to be made af ter careful assessment o f var ious projects through capital

budgeting. A par t o f long term funds i s a lso to be kept for f in ancing working capi tal requirements.

Asse t management pol ic ies are to be laid do wn regarding var ious i tems of current asse ts, inventory

policy i s to be de termined by the production and finance manager , while keeping in mind the

requirement o f production an d future pr ice es t imates o f raw mater ials and avai lab il i ty o f funds .

4) Dividend decision : The finance manager is concerned wi th the decis ion to pay or declare

dividend. He i s to assis t the top management in decid ing as to what amount o f dividend should be

paid to the shareholders and what amount be retained by the company, i t involves a large number of

considera t ions. Economica lly speaking, the amount to be retained or be paid to the shareholders

should depend on whether the company or shareholders can make a more profi tab le use o f resources,

a l so considerat ions l ike trend of earnings, the t rend of share market pr ices , requi rement o f funds for

future gro wth, cash f low si tua tion, tax posit ion of share holders, and so on to be kept in mind.

The pr incipal funct ion of a finance manager re lates to decisions regard ing procurement,

investment and dividends.

5) Supply of funds to a l l parts of the organisation or cash management : The finance manager has

to ensure that al l sec t ions i .e . branches , factor ies, unit s or depar tments o f the organisat ion are

suppl ied wi th adequate funds. Sec tions having excess funds contr ibute to the centra l pool for use in

other sect ions that needs funds. An adequate supply of cash at a l l points o f t ime is absolute ly

essentia l for the smooth flo w of business operat ions. Even i f one of the many branches is short of

funds, the whole business may be in danger , thus, cash management and cash d isbursement polic ies

are impor tant wi th a view to supplying adequate funds at a l l t imes and points in an organisa t ion. I t

should ensure that there is no excess ive cash.

6) Evaluating f inancia l performance : Management contro l sys tems are usual ly based on financia l

analys is, e .g. ROI (return on investment) sys tem of d ivisional contro l . A finance manager has to

constant ly review the f inancial per formance of var ious unit s o f the organisat ion. Analys is of the

f inancia l per formance he lps the management for assess ing ho w the funds are ut i l i sed in var ious

divisions and what can be done to imp rove i t .

7) Financial negot iat ions : Finance manager 's major t ime is ut i l i sed in carrying out negotiat ions

wi th financial inst i tut ions, banks and publ ic depositors. He has to furnish a lot o f informat ion to

CA- IPCC- Financial Management`

5

5

these ins t i tut ions and persons in order to ensu re tha t ra ising of funds is wi thin the statutes .

Negot ia t ions for outside f inancing of ten requires spec ia l i sed skil ls .

8) Keeping in touch with stock exchange quotations and behavior of share prices : I t involves

analys is o f major t rends in the s tock mar ket and judging the ir impact on share pr ices o f the

company's shares .

Quest ion : What are the various methods and tools used for f inancia l management ?

Answer : Finance manager uses var ious too ls to discharge his functions as regards financia l

management. In the area o f f inancing there are var ious methods to procure funds from long as also

short term sources. The f inance manager has to decide an op timum cap ital structure tha t can

contr ibute to the maximisat ion of shareholder 's wealth. Financial leverage or t rading on equity is an

important method by which a f inance manager may increase the return to common shareholders.

For eva luat ion of cap ita l proposals, the f inance manager uses capital budgeting techniques

as payback, internal ra te of re turn, ne t present va lue, prof i tab il i ty index, average rate o f return. In

the a rea o f current assets management, he uses methods to check eff icient ut i l isat ion of current

resources a t the enterpr ise 's disposal . An enterpr ise can increase i t s prof i tab il i t y wi thout a ffec t ing i t s

l iquid ity by an efficient management of working cap ital . For ins tance, in the area o f working capital

management, cash management may be central ised or de -central ised; cent ral i sed method i s considered

a bet ter too l o f managing the e nterpr ise 's l iquid resources. In the area o f dividend decis ions , a fi rm is

faced wi th the prob lem of dec larat ion or postponing dec larat ion of d ividend, a problem of interna l

f inancing.

For evaluat ion of an enterpr ise 's per formance, there ar e var ious methods, as rat io ana lys is.

This technique i s used by a l l concerned persons. Different rat ios serving di fferent object ives. An

investor uses var ious rat ios to eva lua te the prof i tabi l i ty o f investment in a par t icular company. They

enable the inve stor , to judge the prof i tab il i ty, solvency, l iquid ity and growth aspec ts o f the firm. A

short - term credi tor i s more inte rested in the l iquid ity aspect o f the firm, and i t i s poss ible by a study

of l iquid ity rat ios - current rat io , quick ra t ios , e tc . The ma in concern of a f inance manager is to

provide adequate funds from best poss ible source, at the r ight t ime and a t minimum cost and to

ensure tha t the funds so acquired are put to best possib le use . Funds f low and cash f low s ta tements

and projected financia l statements help a lo t in this regard.

Quest ion : Discuss the role of a f inance manager ?

Answer : In the modern enterpr ise , a finance manager occupies a key posit ion, he be ing one of the

dynamic member o f corporate manager ial team. His role , i s becom ing more and more pervasive and

signi ficant in so lving complex managerial problems. Tradi t ional ly, the role o f a f inance manager was

confined to rais ing funds from a number o f sources, but due to recent develop ments in the socio -

economic and po li t ical scenario throughout the wor ld, he i s placed in a cent ral posi t ion in the

organisat ion. He i s responsib le fo r shaping the for tunes o f the enterpr ise and i s invo lved in the most

vi ta l decision of a l loca tion of cap ital l ike mergers, acquisi t ions, e tc . A finance m anager , as other

members o f the corpora te team cannot be averse to the fas t developments, around him and has to take

note o f the changes in o rder to take re levant steps in view of the dynamic changes in c ircumstances .

E.g. in troduction of Euro - as a single currency of Europe is an interna tional leve l change, having

impact on the corporate f inancia l plans and pol icies world -wide.

Domest ic developments as emergence of f inancia l services sec tors and SEBI as a watch dog

for investor pro tection an d regula t ing body of capita l markets i s contr ibuting to the importance of the

f inance manager 's job. Banks and f inancia l ins t i tut ions were the major sources o f f inance, monopoly

was the s tate o f a ffa ir s of Indian business, shareholders sat is fact ion was no t the pro moter 's concern

as most o f the co mpanies, were close ly held . Due to the opening of economy, compet i t ion increased ,

se l ler 's market i s being conver ted into buyer 's market . Development of interne t has brought new

chal lenges before the managers. India n concerns no longer have to compete only nat ional ly, i t i s

facing internat ional competi t ion. Thus a new era i s ushered during the recent years, in financia l

management, special ly, wi th the develop ment o f f inancia l too ls, techniques, ins truments and

produc ts. Also due to increasing emphasis on public sec tor under takings to be sel f -suppor t ing and

their dependence on capital market for fund requirements and the increas ing signi f icance of

l iberal isat ion, global i sat ion and deregulat ion.

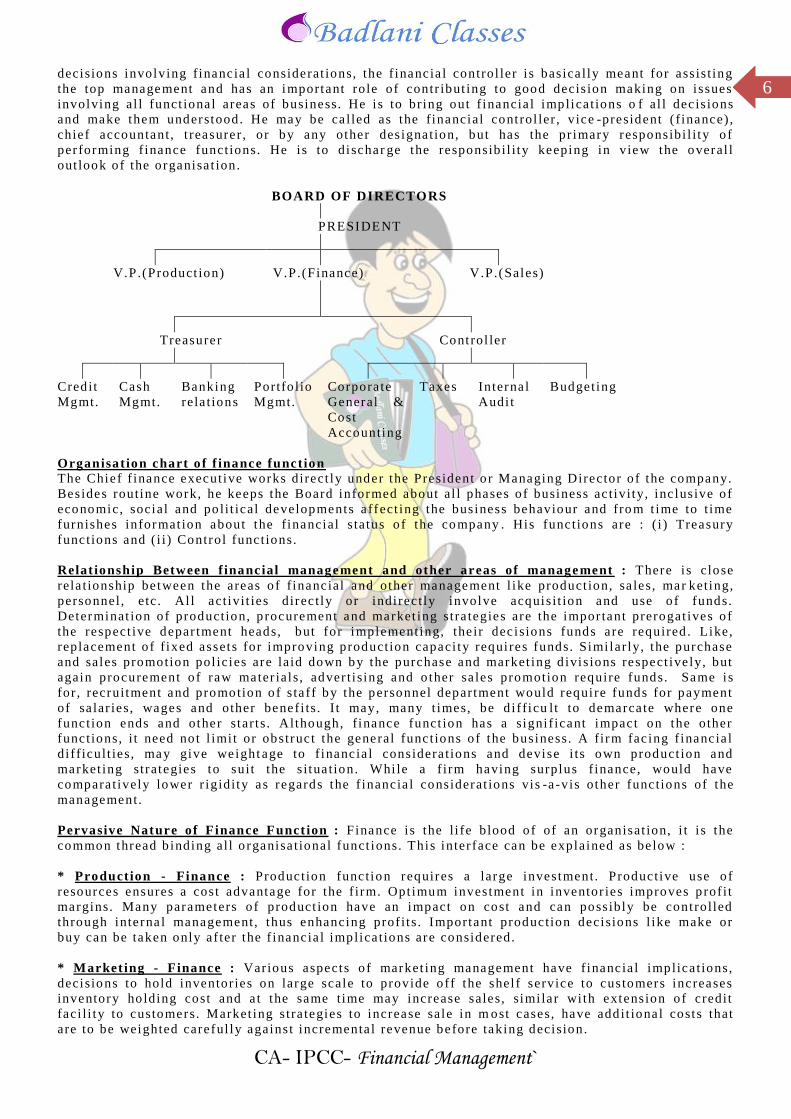

Quest ion : Draw a typi cal organisat ion chart highl ighting the f inance funct ion of a co mpany ?

Answer : The f inance function i s the same in al l enterpr ises , de ta i l s may di ffer , but major features

are universa l in na ture. The f inance funct ion occupies a s igni f icant posi t ion in a n organisat ion and i s

not the responsibi l i ty o f a sole execut ive. The impor tant aspects o f finance manager a re to carr ied on

by top management i .e . managing d irec tor , chairman, board of directors. The board of directors takes

CA- IPCC- Financial Management`

6

6

decisions involving financia l considerat ions, the f inancia l control ler i s bas ica l ly meant for ass is t ing

the top management and has an important role of contr ibut ing to good decis ion making on i ssues

involving al l funct ional areas of business. He i s to br ing out f inancia l implica t ions o f al l dec is ions

and make them understood. He may be ca lled as the financial cont rol ler , v ice -president ( finance) ,

chief accountant , t reasurer , or by any other des ignation, but has the pr imary responsibi l i ty o f

per forming f inance functions. He i s to dischar ge the responsib il i ty keeping in view the overal l

out look of the o rganisa t ion.

BOARD OF DIRECTORS

PRESIDENT

V.P.(Product ion) V.P.(Finance) V.P.(Sales)

Treasurer Control ler

Cred it

Mgmt.

Cash

Mgmt.

Banking

rela t ions

Portfo l io

Mgmt.

Corpora te

General &

Cost

Accounting

Taxes Interna l

Audi t

Budgeting

Organisation chart o f f inance function The Chief f inance executive works direct ly under the President o r Managing Director o f the company.

Besides routine work, he keeps the Board informed about al l phases o f business ac t ivi ty, inc lus ive of

economic, social and po li t ical developments a ffect ing the business behaviour and fro m t ime to t ime

furnishes informat ion about the financial s tatus o f the co mpany . His functions are : ( i ) Treasury

functions and ( i i) Control functions.

Relat ionship Between f inancial management and other areas of management : There i s close

rela t ionship be tween the areas o f financial and other management l ike product ion, sa les, mar keting,

personnel , e tc . Al l act ivi t ies direc t ly or indi rec tly involve acquis i t ion and use o f funds.

Determinat ion of production, p rocurement and market ing stra tegies are the impor tant prerogat ives o f

the respect ive depar tment heads, but for implement ing, the ir dec isions funds a re required . Like,

replacement o f fixed assets for improving production capaci ty requi res funds. Simi lar ly, the purchase

and sales promotion pol icies are laid down by the purchase and market ing d ivis ions respect ive ly, but

again procurement o f raw mater ials , adver t i sing and o ther sa les promotion require funds. Same is

for , recruitment and promotion of s ta ff by the personnel department would requi re funds for payment

of sa lar ies, wages and other benefi ts . I t may, many t imes, be d i fficu lt to demarca te where one

function ends and other star t s . Although, finance funct ion has a signi f icant impact on the other

functions, i t need no t l imi t or obstruc t the general functions o f the business. A firm fac ing f inancia l

di fficult ies, may give weight age to f inancia l considera t ions and devise i ts own product ion and

market ing strategies to suit the s i tua tion. Whi le a f irm having surplus f inance, would have

compara tively lower r igidity as regards the f inancia l considerat ions vis -a -vis other functions of the

management.

Pervasive Nature of Finance Funct ion : Finance i s the l i fe blood of of an organisat ion, i t i s the

common thread b inding al l o rganisa t ional funct ions. This inter face can be explained as be low :

* Production - Finance : Production function requires a large investment. Productive use o f

resources ensures a cos t advantage for the f irm. Opt imum investment in inventor ies improves p rof i t

margins. Many parameters o f product ion have an impact on cost and can poss ibly be cont rolled

through interna l management, thus enhancing prof i t s . Important production decisions l ike make or

buy can be taken only a f ter the f inancia l implica t ions are considered.

* Market ing - F inance : Various aspects o f market ing management have f inancia l implica t ions,

decisions to hold inventor ies on large scale to provide off the shel f service to customers increases

inventory ho lding cost and a t the same t ime may increase sales, simi lar wi th extension of credit

faci l i ty to customers. Market ing s tra tegies to increase sale in m ost cases, have add it iona l costs that

are to be weighted careful ly agains t incrementa l revenue before taking decision.

CA- IPCC- Financial Management`

7

7

* Personnel - Finance : In the globali sed competi t ive scenario , business organisa t ions are moving to

a f la t ter organisa t ional structure . Investments in human resource developments are also increasing.

Restructur ing of remunerat ion structure, vo luntary ret irement schemes, sweat equi ty, e tc . have

become major financial decisions in the human resource management.

Quest ion : What is the rele vance of t ime va lue of money in f inancia l dec ision making ?

Answer : A finance manager is required to make dec isions on investment, f inancing and d ividend in

view of the company's objectives. The dec is ions as purchase of asse ts or p rocurement o f funds i .e .

the investment/ f inancing decisions a ffect the cash f low in di fferent t ime per iods. Cash out f lows

would be at one point o f t ime and inf low a t some o ther point of t ime, hence, they are not comparable

due to the change in rupee va lue of money. They can b e made comparable by introducing the interest

factor . In the theory of f inance, the interest factor is one of the c rucial and exclus ive concept , kno wn

as the t ime va lue of money.

Time va lue of money means that worth of a rupee received today i s d i fferent from the same

rece ived in future. The preference for money now as compared to future i s known as t ime preference

of money. The concept i s app licable to both individuals and business houses.

Reasons of t ime preference of money :

1) Risk : There is uncer ta inty about the receip t o f money in future.

2) Preference for present consumption : Most o f the persons and companies have a preference for present consumption may be due to urgency

of need.

3) Investment opportunit ies : Most of the persons and companies have preference for present money because of avai lab il i t ies of

opportuni t ies o f investment for earning add it ional cash flo ws.

Importance of t ime va lue of money : The concept o f t ime va lue of money helps in ar r iving at the co mparab le valu e of the di fferent rupee

amount a r i sing at d i fferent points o f t ime into equivalent values o f a par t icular po int o f t ime, p resent

or future. The cash f lows ar i s ing at di fferent points o f t ime can be made comparab le by us ing any one

of the fo l lo wing :

- by compounding the present money to a future date i .e . by find ing out the value of present money.

- by discounting the future money to present da te i .e . by f inding out the present va lue(PV) of future

money.

Notes on:- Finance Function

The finance function is most important for all business enterprises. It remains a focus of all activities. It starts with the

setting up of an enterprise. It is concerned with raising of funds, deciding the cheapest source of finance, utilization of

funds raised, making provision for refund when money is not required in the business, deciding the most profitable

investment, managing the funds raised and paying returns to the providers of funds in proportion to the risks undertaken

by them. Therefore, it aims at acquiring sufficient funds, utilizing them properly, increasing the profitability of the

organization and maximizing the value of the organization and ultimately the shareholder‟s wealth.

Notes on:- Inter-relationship between Investment, Financing and Dividend Decisions

The finance functions are divided into three major decisions, viz., investment, financing and dividend decisions.

It is correct to say that these decisions are inter-related because the underlying objective of these three decisions is the

same, i.e. maximisation of shareholders‟ wealth. Since investment, financing and dividend decisions are all interrelated,

one has to consider the joint impact of these decisions on the market price of the company‟s shares and these decisions

should also be solved jointly. The decision to invest in a new project needs the finance for the investment. The financing

decision, in turn, is influenced by and influences dividend decision because retained earnings used in internal financing

deprive shareholders of their dividends. An efficient financial management can ensure optimal joint decisions. This is

possible by evaluating each decision in relation to its effect on the shareholders‟ wealth.

The above three decisions are briefly examined below in the light of their inter -relationship and to see how they

can help in maximising the shareholders‟ wealth i.e. market price of the company‟s shares.

CA- IPCC- Financial Management`

8

8

Investment decision: The investment of long term funds is made after a careful assessment of the various

projects through capital budgeting and uncertainty analysis. However, only that investment proposal is to be accepted

which is expected to yield at least so much return as is adequate to meet its cost of financing. This have an influence on

the profitability of the company and ultimately on its wealth.

Financing decision: Funds can be raised from various sources. Each source of funds involves different issues.

The finance manager has to maintain a proper balance between long-term and short-term funds. With the total volume of

long-term funds, he has to ensure a proper mix of loan funds and owner‟s funds. The optimum financing mix will

increase return to equity shareholders and thus maximise their wealth.

Dividend decision: The finance manager is also concerned with the decision to pay or declare dividend. He

assists the top management in deciding as to what portion of the profit should be paid to the shareholders by way of

dividends and what portion should be retained in the business. An optimal dividend pay-out ratio maximises

shareholders‟ wealth.

The above discussion makes it clear that investment, financing and dividend decisions are interrelated and are to

be taken jointly keeping in view their joint effect on the shareholders‟ wealth.

INTRODUCTION

Decisions relating to working capital and short term financing are referred to as Working Capital Management. These involve

managing the relationship between a firm.s short-term assets and its short-term liabilities. The goal of working capital

management is to ensure that the firm is able to continue its operations and that it has sufficient cash flow to satisfy both

maturing short-term debt and upcoming operational expenses.

MEANING AND CONCEPT OF WORKING CAPITAL

There are two concepts of working capital - gross and net. Gross working capital refers to the firm.s investment in current

assets. Current assets are those assets which can be converted into cash within an accounting year. Net working capital refers

to the difference between current assets and current liabilities. Current liabilities are those claims of outsiders which are

expected to mature for payment within an accounting year.

Current Assets include: Stocks of raw materials, Work-in-progress, Finished goods, Trade debtors, Prepayments, Cash

balances .

Current Liabilities include: Trade creditors, Accruals, Taxation payable, Bills Payables, Outstanding expenses, Dividends

payable, short term

Working capital is also known as operating capital. A most important value, it represents the amount of day-to-day operating

liquidity available to a business. A company can be endowed with assets and profitability, but short of liquidity if these assets

cannot readily be converted into cash. A positive working capital means that the company is able to payoff its short-term

liabilities. A negative working capital means that the company currently is unable to meet its short-term liabilities. From the

point of view of time, the term working capital can be divided into two categories viz., Permanent and temporary.

Permanent working capital refers to the hard core working capital. It is that minimum level of investment in the current assets

that is carried by the business at all times to carry out minimum level of its activities.

Temporary working capital refers to that part of total working capital, which is required by a business over and above

permanent working capital. It is also called variable working capital. Since the volume of temporary working capital keeps on

fluctuating from time to time according to the business activities it may be financed from short-term sources.

Importance of Adequate Working Capital:

The importance of adequate working capital in commercial undertakings can be judged from the fact that a

concern needs funds for its day-to-day running. Adequacy or inadequacy of these funds would determine the efficiency with

which the daily business may be carried on. Management of working capital is an essential task of the finance manager. He has

to ensure that the amount of working capital available with his concern is neither too large nor too small for its requirements.

A large amount of working capital would mean that the company has idle funds. Since funds have a cost, the company has to

pay huge amount as interest on such funds. The various studies conducted by the Bureau of Public Enterprises have shown that

one of the reason for the poor performance of public sector undertakings in our country has been the large amount of funds

locked up in working capital This results in over capitalization. Over capitalization implies that a company has too large funds

Chapter : Estimation of Working Capital

CA- IPCC- Financial Management`

9

9

for its requirements, resulting in a low rate of return a situation which implies a less than optimal use of resources. A firm has,

therefore, to be very careful in estimating its working capital requirements.

If the firm has inadequate working capital, it is said to be under-capitalised. Such a firm runs the risk of

insolvency. This is because, paucity of working capital may lead to a situation where the firm may not be able to meet its

liabilities. It is interesting to note that many firms which are otherwise prosperous (having good demand for their products and

enjoying profitable marketing conditions) may fail because of lack of liquid resources. If a firm has insufficient working

capital and tries to increase sales, it can easily over-stretch the financial resources of the business. This is called overtrading.

Early warning signs of

over trading include:

♦ Pressure on existing cash.

♦ Exceptional cash generating activities e.g., offering high discounts for early cash payment.

♦ Bank overdraft exceeds authorized limit.

♦ Seeking greater overdrafts or lines of credit.

♦ Part-paying suppliers or other creditors.

♦ Paying bills in cash to secure additional supplies.

♦ Management pre-occupation with surviving rather than managing.

♦ Frequent short-term emergency requests to the bank (to help pay wages, pending receipt of a cheque).

needs enough cash to pay wages and salaries as they fall due and to pay creditors if it is to keep its workforce engaged and

ensure its supplies. Maintaining adequate working capital is not just important in the short-term. Sufficient liquidity must be

maintained in order to ensure the survival of the business in the long-term as well. Even a profitable business may fail if it

does not have adequate cash flow to meet its liabilities as they fall due. Therefore, when business make investment decisions

they must not only

consider the financial outlay involved with acquiring the new machine or the new building, etc., but must also take account of

the additional current assets that are usually required with any expansion of activity. Increased production leads to hold

additional stocks of raw materials and work in progress. Increased sales usually means that the level of debtors will increase. A

general increase in the firm.s scale of operations tends to imply a need for greater levels of working capital. A question then

arises what is an optimum amount of working capital for a firm? We can say that a firm should neither have too high an

amount of working capital nor should the same be too low. It is the job of the finance manager to estimate the requirements of

working capital

carefully and determine the optimum level of investment in working capital.

Optimum Working Capital:

If a company.s current assets do not exceed its current liabilities, then it may run into trouble with creditors

that want their money quickly. The working capital ratio, which measures this ability to pay back can be calculated as current

assets divided by current liabilities.

Current ratio (current assets/current liabilities) has traditionally been considered the best indicator of the

working capital situation. It is understood that a current ratio of 2 (two) for a manufacturing firm implies that the firm has an

optimum amount of working capital. This is supplemented by Acid Test Ratio (Quick assets/Current liabilities) which should

be at least 1 (one). Thus it is considered that there is a comfortable liquidity position if liquid current assets are equal to current

liabilities. Bankers, financial institutions, financial analysts, investors and other people interested in financial statements have,

for years, considered the current ratio at, .two. and the acid test ratio at, .one. as indicators of a good working capital situation.

As a thumb rule, this may be quite adequate. However, it should be remembered that optimum working capital can be

determined only with reference to the particular circumstances of a specific situation. Thus, in a company where the

inventories are easily saleable and the sundry debtors are as good as liquid cash, the current ratio may be lower than 2 and yet

firm may be sound. An optimum working capital ratio is dependent upon the business situation as such and the nature and

composition of various current assets. A company having short conversion cycle (from cash to cash) my have a lower current

ratio.

In nutshell, a firm needs to maintain a sound working capital position. It should have adequate working capital to run its

business operations. Both excessive as well as inadequate working capital positions are dangerous. Excessive working capital

means holding costs and idle funds which earn no profits for the firm. Paucity of working capital not only impairs the firm.s

profitability but also results in production interruptions, inefficiencies and sales disruptions. The management should therefore

maintain the right amount of working capital continuously.

MANAGEMENT OF WORKING CAPITAL

Working capital management is the functional area of finance that covers all the current accounts of its firm.

It is concerned with management of the level of individual current assets and the current liabilities or in other words the

management of total working capital. Managing Working Capital is a matter of balance. A firm must have sufficient cash on

hand to meet its immediate needs while ensuring that idle cash is invested to the organizations best possible advantage. To

avoid the difficulties, it is necessary to have clear and accurate reports on each of the components of working capital and an

awareness of the potential impact of likely influences. Sound financial and statistical techniques, supported by judgement

should be used to predict the quantum of working capital required at different times. Adequate provisions of working capital

mitigates risk. Working capital management entails short-term decisions generally, relating to its next one year period which

are .reversible.. Management will use a combination of policies and techniques for the management of working capital. These

CA- IPCC- Financial Management`

10

10

require managing the current assets . generally cash and cash equivalents, inventories and debtors. There are also a variety of

short term financing options which are considered. The various steps in the management of working capital involve:

♦ Cash management . Identify the cash balance which allows for the business to meet day to day expenses, but reduces cash

holding costs.

♦ Inventory management . Identify the level of inventory which allows for uninterrupted production but reduces the

investment in raw materials and hence increases cash flow;The techniques like Just In Time (JIT) and Economic order quantity

(EOQ) are used for this.

♦ Debtors management . Identify the appropriate credit policy, i.e., credit terms which will attract customers, such that any

impact on cash flows and the cash conversion cycle will be offset by increased revenue and hence Return on Capital (or vice

versa). The tools like Discounts and allowances are used for this.

♦ Short term financing . Inventory is ideally financed by credit granted by the supplier; dependent on the cash conversion

cycle, it may however, be necessary to utilize a bank loan (or overdraft), or to .convert debtors to cash. through .factoring. in

order to finance working capital requirements.

There are, however, certain constraints in the management of working capital such as:

(i) Non-realisation of the importance of working capital.

(ii) Continuous inflation in the economy.

(iii) The existence of seller.s market or monopoly conditions; and

(iv) High profitability.

Determinants of Working Capital: The following factors will generally influence the working capital requirements of the

firm:

(i) Nature of Business.

(ii) Market and demand conditions.

(iii) Technology and manufacturing Policies.

(iv) Credit Policy of the firm.

(v) Availability of credit from suppliers.

(vi) Operating efficiency.

(vii) Price Level Changes.

ISSUES IN THE WORKING CAPITAL MANAGEMENT

Working capital management entails the control and monitoring of all components of working capital i.e. cash, marketable

securities, debtors (receivables) and stocks (inventories) and creditors (payables). The finance manager has to determine the

levels and composition of current assets. He has to ensure a right mix of different current assets and that current

liabilities are paid in time. There are many aspects of working capital management which makes it important function of

financial management.

♦ Time: Working capital management requires much of the finance manager.s time.

♦ Investment: Working capital represents a large portion of the total investment in assets.

♦ Credibility: Working capital management has great significance for all firms but it is very critical for small firms.

♦ Growth: The need for working capital is directly related to the firm.s growth. It is advisable that the finance manager should

take precautionary measures for effective and efficient management of working capital. He has to pay particular attention to

the levels of current assets and their financing. To decide the levels and financing of current assets, the risk return trade off

must be taken into account.

Liquidity versus Profitability:

Risk return trade off − A firm may follow a conservative, aggressive or moderate policy as discussed above. However, these

policies involve risk, return trade off. A conservative policy means lower return and risk. While an aggressive policy produces

higher return and risk.

The two important aims of the working capital management are profitability and solvency. A liquid firm has less risk of

insolvency that is, it will hardly experience a cash shortage or a stock out situation. However, there is a cost associated with

maintaining a sound liquidity position. However, to have higher profitability the firm may have to sacrifice solvency and

maintain a relatively low level of current assets. This will improve firm.s profitability as fewer funds will be tied up in idle

current assets, but its solvency would be threatened and exposed to greater risk of cash shortage and stock outs. The following

illustration explains the risk-return trade off of various working capital management policies, viz., conservative, aggressive

and moderate etc.

OPERATING OR WORKING CAPITAL CYCLE

A useful tool for managing working capital is the operating cycle. The operating cycle analyzes the accounts

receivable, inventory and accounts payable cycles in terms of number of days. In other words, accounts receivable are

analyzed by the average number of days it takes to collect an account. Inventory is analyzed by the average number of days it

takes to turn over the sale of a product (from the point it comes in the store to the point it is converted to cash or an account

receivable). Accounts payable are analyzed by the average number of days it takes to pay a supplier invoice. Most businesses

cannot finance the operating cycle (accounts receivable days + inventory days) with accounts payable financing alone.

Consequently, working capital financing is needed. This shortfall is typically covered by the net profits generated internally or

by externally borrowed funds or by a combination of the two. Most businesses need short-term working capital at some point

CA- IPCC- Financial Management`

11

11

in their operations. For instance, retailers must find working capital to fund seasonal inventory build-up. But even a business

that is not seasonal occasionally experiences peak months when orders are unusually high. This creates a need for working

capital to fund the resulting inventory and accounts receivable build-up.

Some small businesses have enough cash reserves to fund seasonal working capital needs. However, this is

very rare for a new business. If your new venture experiences a need for short-term working capital during its first few years of

operation, you will have several potential sources of funding. The important thing is to plan ahead. If you get caught off guard,

you might miss out on the one big order. Cash flows in a cycle into, around and out of a business. It is the business.s life blood

and every manager.s primary task is to help keep it flowing and to use the cashflow to generate profits. If a business is

operating profitably, then it should, in theory, generate cash surpluses.

If it doesn.t generate surplus, the business will eventually run out of cash. The faster a business expands, the

more cash it will need for working capital and investment. The cheapest and best sources of cash exist as working capital right

within business. Good management of working capital will generate cash which will help improve profits and reduce risks.

Bear in mind that the cost of providing credit to customers and holding stocks can represent a substantial proportion of a firm.s

total profits. There are two elements in the business cycle that absorb cash . Inventory (stocks and workin- progress) and

Receivables (debtors owing you money). The main sources of cash are Payables (your creditors) and Equity and Loans.

Working Capital Cycle

Each component of working capital (namely inventory, receivables and payables) has two dimensions

..TIME ...and MONEY, when it comes to managing working capital then time is money. If you can get money to move faster

around the cycle (e.g. collect monies due from debtors more quickly) or reduce the amount of money tied up (e.g. reduce

inventory levels relative to sales), the business will generate more cash or it will need to borrow less money to fund working

capital. As a consequence, you could reduce the cost of bank interest or you will have additional free money available to

support additional sales growth or investment. Similarly, if you can negotiate improved terms with suppliers e.g. get longer

credit or an increased credit limit, you are effectively creating free finance to help fund future sales. Working capital cycle

indicates the length of time between a company.s paying for materials, entering into stock and receiving the cash from sales of

finished goods. It can be determined by adding the number of days required for each stage in the cycle. For example, a

company holds raw materials on an average for 60 days, it gets credit from the supplier for 15 days, production process needs

15 days, finished goods are held for 30 days and 30 days credit is extended to debtors. The total of all these, 120 days, i.e., 60 .

15 + 15 + 30 + 30 days is the total working capital cycle. The determination of working capital cycle helps in the forecast,

control and management of working capital. It indicates the total time lag and the relative significance of its constituent parts.

The duration of working capital cycle may vary depending on the nature of the business.

Effect of Double Shift Working on Working Capital requirements:

Increase in the number of hours of production has an effect on the working capital requirements. The

greatest economy in introducing double shift is the greater use of fixed assets-little or marginal funds may be required for

additional assets.

It is obvious that in double shift working, an increase in stocks will be required as the production rises.

However, it is quite possible that the increase may not be proportionate to the rise in production since the minimum level of

stocks may not be very much higher. Thus, it is quite likely that the level of stocks may not be required to be doubled as the

production goes up two-fold. The amount of materials in process will not change due to double shift working since work

started in the first shift will be completed in the second; hence, capital tied up in materials in process will be the same as with

single shift working. As such the cost of work-in-process, will not change unless the second shift.s workers are paid at a higher

rate. Fixed overheads will remain fixed whereas variable overheads will increase in proportion to the increased production.

Semi-variable overheads will increase according to the variable element in them.

CA- IPCC- Financial Management`

12

12

Important Questions

Que:- MNO Ltd. has furnished the following cost data relating to the year ending of 31st March, 2008.

Sales

Material Consumed

Direct wages

Factory overheads (100% variable)

Office and Administrative overheads (100% variable)

Selling overheads

Rs. (in lakhs)

450

150

30

60

60

50

The company wants to make a forecast of working capital needed for the next year and anticipates that:

Sales will go up 100%,

Selling expenses will be Rs. 150 lakhs,

Stock holdings for the next year will be-Raw material for two and half months, Work-in-progress for one month, Finished goods

for half month and Book debts for one and half months,

Lags in payment will be of 3 months for creditors, 1 month for wages and half month for Factory, Office and Administrative and

Selling overheads.

You are required to:

(i) Prepare statement showing working capital requirements for next year, and

(ii) Calculate maximum permissible bank finance as per Tandon Committee guidelines assuming that core current assets of the firm

are estimated to be Rs. 30 lakhs.

Que:- A company is considering its working capital investment and financial policies for the next year. Estimated fixed assets and current

liabilities for the next year are Rs. 2.60 crores and Rs. 2.34 crores respectively. Estimated Sales and EBIT depend on current assets

investment, particularly inventories and book-debts. The financial controller of the company is examining the following alternative Working

Capital Policies:

(Rs. in Crores)

Working Capital Policy Investment in Current Assets Estimated Sales EBIT

Conservative

Moderate

Aggressive

4.50

3.90

2.60

12.30

11.50

10.00

1.23

1.15

1.0

After evaluating the working capital policy, the Financial Controller has advised the adoption of the moderate working capital

policy. The company is now examing the use of long-term and short-term borrowings for financing its assets. The company will use Rs. 2.50

crores of the equity funds. The corporate tax rate is 35%. The Company is considering the following debt alternatives.

(Rs. in Crores)

Financing Policy Short-term Debt Long-term Debt

Conservative

Moderate

Aggressive

Interest Rate-Average

0.54

1.00

1.50

12%

1.12

0.66

0.16

16%

You are required to calculate the following:

(1) Working Capital Investment for each policy:

(a) Net Working Capital Position

(b) Rate of Return on Total Assets

(c) Current Ratio

(2) Financing for each policy:

(a) Net Working Capital position,

(b) Rate of return on Shareholders‟ equity.

(c) Current Ratio.

Que:- An engineering company is considering its working capital investment for the year end 2003-04. The estimated fixed assets and

current liabilities for the next year are Rs. 6.63 crore and Rs. 5.967 crore respectively. The sales and earnings before interest and taxes

(EBIT) depend on investment in its current assets- particularly inventory and receivables. The company is examining the following

alternative working capital policies:

(Rs. in crore)

Working capital policy

Conservative

Moderate

Aggressive

Investment in C. Assets

11.475

9.945

6.630

Estimated sales

31.365

29.325

25.500

EBIT

3.1365

2.9325

2.5500

You are required to calculate the following for each policy:

(i) Rate of return on total assets.

(ii) Net working capital position.

(iii) Current assets to fixed assets ratio.

(iv) Discuss the risk-return trade off of each working capital policy.

CA- IPCC- Financial Management`

13

13

Practical Questions:-

Q. 1. The selling price per unit of a product is computed as follows:

Cost per Unit

Raw Material Rs. 50

Direct Labour 20

Factory overheads (including depreciation of Rs. 10) 20

Admn. Overheads (including depreciation of Rs. 5) 10

Selling Overheads (including depreciation of Rs. 5) 10

Total 110

Profit per unit 20

Selling price per unit 130

Average raw material in stock for one month . Average material in work –in –progress in for half month .

Credit allowed by suppliers is one month and credit allowed to debtors is one month. Average time lag in payment of

wages is 10 days. Average time lag in payment of overheads is 30 days. 25% of the sales are on cash basis. Cash

balance is approximately maintained at Rs. 1,00,000. The finished goods lie in the warehouse for one month.

You are required to prepare a statement of working capital requirement to finance a level of activity of

54,000 units of output.

Q. 2. A company is presently operating at 60% capacity, producing 36,000 units per annum,. It is now decided to operate at

90% capacity. The following information is available:

(1) Existing cost price structure per unit is as follows:

Raw Material Rs. 4

Wages Rs. 2

Variable Overheads Rs. 2

Fixed overheads Re. 1

Profit Re. 1

Rs.10

(2) It is expected that the cost of raw material, wages, expenses and selling price per unit will remain unchanged

in 1997.

(3) Raw material remain in store for 2 months and in production for 1 month.

(4) Finished goods remain in godown for 2 months.

(5) Credit allowed to debtors is 2 months and credit allowed by creditors is 3 months.

(6) Lag in wages and overheads payment is one month.

Required: (a) Prepare Profit Statement at 90% capacity level.

(b) Calculate the working capital requirement at 90% capacity level.

Q. 3. Ess Ltd. sells goods at a gross profit of 25% considering depreciation as part of the cost of production. Its annual figures

are as follows: Rs.

Sales at two months credit 18,00,000

Materials consumed (suppliers extend two months‟ credit) 4,50,000

Wages paid (monthly in arrear) 3,60,000

Manufacturing expenses outstanding at the end of the year 40,000

(cash expenses are paid one month in arrear)

Total Administrative Expenses, paid as above 1,20,000

Sales promotion expenses paid quarterly in advance 60,000

The company keeps one month‟s stock each of raw materials and finished goods, and believes in keeping Rs.

1,00,000 in cash. Assuming a 15% safety margin ascertain the requirements of working capital requirement of the

company on cash costs basis. Ignore work-in-progress.

Q. 4. BS Ltd. has been operating its manufacturing facilities till 31:03:1999 on single shift-working with the following cost

structure: Per Unit

Rs,

Cost of Materials 6.00

Wages (40% fixed) 5.00

Overheads (80% fixed) 5.00

Profit 2.00

Selling Price 18.00

Sales during 1998-1999 – Rs. 4,32,000. As at 31;03:1999 the company held:

Rs.

CA- IPCC- Financial Management`

14

14

Stock of raw materials (at cost) 36,000

Work-in-progress (valued at prime cost) 22,000

Finished goods (valued at total cost) 72,000

Sundry debtors 1,08,000

In view of increased market demand, it is proposed to double production by working an extra shift. It is

expected that a 10% discount will be available from suppliers of raw materials in view of increased volume of business.

Selling price will remain the same. The credit period allowed to customers will remain unaltered. Credit availed of from

suppliers will continue to remain at the present level i.e. 2 months. Lag in payment of wages and expenses will continue

to remain half a month.

You are required to assess the additional working capital requirement, if the policy to increase output is implemented.

Q. 5. The following are the extracts from Balance Sheet of a company as on 31.12.1999.

Fixed Assets:

Land & Building Rs. 5,00,000

Plant & Machinery 3,00,000 Rs. 8,00,000

Working Capital:

Current Assets:

Stock 8,00,000

Debtors 3,00,000

Cash 2,00,000

13,00,000

Current Liabilities:

Creditors 3,40,000

Provision for tax 80,000

Bank Overdraft 1,40,000

Outstanding

Liabilities 1,60,000 7,20,000 5,80,000

Total 13,80,000

Additional Information:-

(1) Sales will increase by 25% next. Year

(2) Maximum Bank Overdraft Rs. 1,60,000

(3) No increase in tax liability for next year.

(4) Period of credit allowed to customers and stock turnover will remain unchanged.

(5) Period of credit allowed by creditors will also remain same.

(6) Outstanding liabilities will remain at the same relative position.

(7) There will be no increase in cash balance.

You are required to computes the additional and total working capital required by the company for the next year.

Q. 6. At the beginning of the year, a company wants to know the working capital that will be required to meet the programme

of activity they have planned for the year. The following information is available

(1) Paid up Share Capital Rs. 2,00,000.

(2) 5% Debentures Rs. 50,000

(3) Fixed Assets Rs. 1,25,000 (at the beginning of year).

(4) Production during the last year was 60,000 units. It is to be maintained during the current year.

(5) Raw Material, Direct Wages and Overheads are 60% ,10% and 20% of selling price.

(6) Each unit is expected to be in production process for one month.

(7) Finished units will stay in warehouse for three months.

(8) Creditors allow credit of two months.

(9) Credit allowed to debtors is 3 months.

(10) Raw Material remains in store for 2 months.

(11) Selling price per unit = Rs. 5.

Prepare: (i) Working Capital requirement forecast.

(ii) An estimated Profit and Loss Account and Balance Sheet as at the end of the year.

Q.7. A company provided the following data:

Cost Per units (Rs.)

Raw materials 52.00

Direct labour 19,50

Overhead 39.00

Total 110.50

Profit 19.50

Selling price 130.00

The following additional information is available:

CA- IPCC- Financial Management`

15

15

1. Average raw materials in stock: one month;

2. Average raw materials in process: half-a-moth;

3. Average finished goods in stock: one month;

4. Credit allowed by suppliers: one month;

5. Credit allowed to debtors: two months;

6. Time lag in payment of wages: one and a half weeks;

7. Overheads; one month;

One-fourth of sales are on cash basis. Cash balance is expected to be Rs. 1.20.000.

You are required to prepare a statement showing the working capital needed to finance a level of activity of 70,000

units of annual output. The production is carried throughout the year on even basis and wages and overheads accrue

similarly. (Calculation be made on the basis on 30 days a months and 52 weeks a year.)

Q.8 Determine the working capital requirement from the following particulars:

Annual budget figures for: (Rs. Lakhs)

Raw materials 360

Supplies and components 120

Manpower 240

Factory expenses 60

Administration 90

Sales 1190

You are given thee following additional information:

(1) Stock- levels planned:

Raw materials 30 days

Supplies and components 90 days

(2) 50% of the sales is for cash; for the remaining, 20 days credit is normal.

(3) Finished goods are held in stock for a period of seven days before they are released for sale.

(4) Goods remain in process for 5 days.

(5) The company enjoys 30 days‟ credit facilities on 20% of the purchase.

(6) Cash/bank balance had been planned to be kept at the rate of half month‟s budgeted expenses.

Q.9. Prepare an estimate of net working capital requirement for the WCM Ltd. Adding 10% for contingencies from the

information given below.

Estimate cost per unit of production Rs. 170, includes raw materials rs.80, direct labour Rs. 30 and overheads

(exclusive of depreciation) Rs. 60. Selling price is Rs.200 per unit. Level of activity per annum 1,04,000 units. Raw

material in stock: average 4 weeks: work-in-progress (assume 50% completion stage) : average 2 weeks; 4 weeks;

credit allowed to debtors: average 8 weeks; lag in payment of wages: average 1.5 weeks, and cash at bank is expected

to be Rs. 25,000. You may assume that production is carried on evenly throughout the year (52 weeks) and wages and

overhead accrue similarly. All dales are on credit basis only. You may state wages and overheads accrue similarly.

All sales are on credit basis only. You may state your assumptions, if any.

Q. 10. On 1st January, the Managing director of A Ltd. wishes to know the amount of working capital that will be required during the year.

From the following information, prepare the working capital requirement forecast:

Production during the previous year was 60,000 units. It is planned that this level of activity would be maintained during the present

year. The expected ratios of the cost to selling prices are Raw Material 60%. Direct Wages 10% and Overheads 20%, Raw Material is

expected to be in store for average of 2 months before issue to production. Each unit is expected to be in process for one month, the

raw material being fed into the pipeline immediately and labour and overheads cost accruing evenly during the month. Finished

goods will stays in the warehouse awaiting dispatch to customers for approximately 3 months credit allowed by creditors is 2 months

from the date of delivery of raw material. Credit allowed to debtors is 3 months from the date of dispatch. The selling price is Rs. 5

per unit. There is regular production and sales cycle. Wages and overheads are paid after one month. The company normally keep

cash in hand to the extent of Rs. 20,000.