Financial Information Management FINANCIAL INFORMATION MANAGEMENT Stefano Grazioli

Financial Information Management FINANCIAL INFORMATION MANAGEMENT Stefano Grazioli.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t

FINANCIAL INFORMATION MANAGEMENT

Stefano Grazioli

Critical Thinking Team submission possible from H17 email me with team name, members

(userids) and get the team # on collab.

Easy meter

The Hedge Tournament Questions? Team formation / paper / opting

out

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t HomeworkThe Spartan Trader

Suggestions Give yourself plenty of time Audit the numbers!

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t

FinancialStrategies:

BasicsStefano Grazioli

Payoff Curves

Profit & Loss

Going long / short =flipping horizontally the payoff curve

Profit & Loss

Stock price

Stock price

short

$10

long

$10

price at which you bought it

Call and Put Payoffs

Stock price

Profit & Loss

long call

Stock price

short call

Profit & Loss

strike strike

Stock price

Profit & Loss

long put

Stock price

Profit & Loss

strike

short put

strike

Transaction Costs (constant)

Stock price

Profit & Loss

TCs always lower your payoff curve

TC

long - TC

$10

Stock price

short - TC

Profit & Loss

TC $10

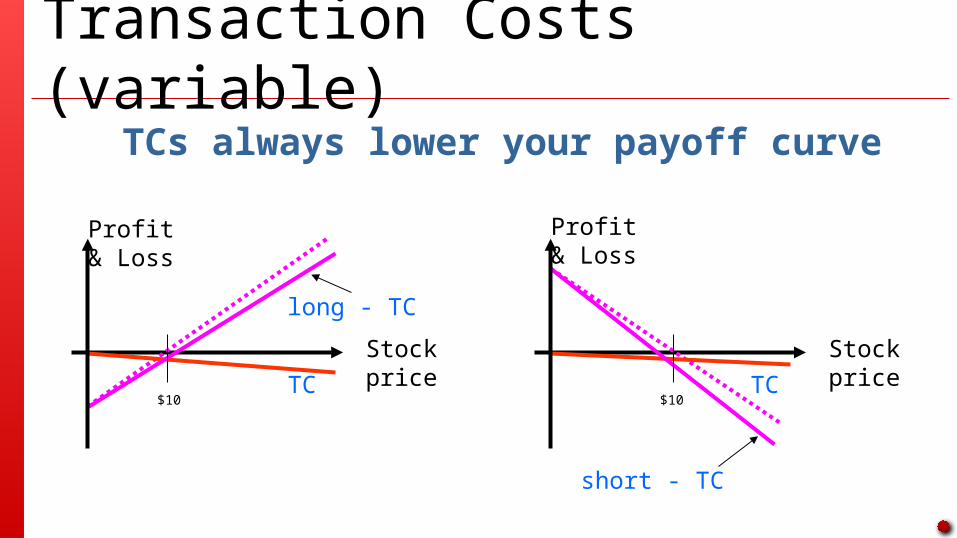

Transaction Costs (variable)

Stock price

Profit & Loss

long - TC

TCs always lower your payoff curve

Stock price

short - TC

Profit & Loss

TC TC $10 $10

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t WINITWhat Is New

In Technology?

Financial Strategies: Key idea Combine different types of

positions to obtain custom payoff curves.

Payoff curves can be designed to achieve many different objectives. Hedging is just one of them.

Hedging Strategies1. Offsetting the position (not applicable to the HT)

2. One to one3. One to many4. Dynamic approaches5. Synthetics (based on put/call parity)

6. Delta hedging (based on Black Scholes)

7. Delta + Gamma hedging (complex refinement)

Strategy #1: Offset the Position

Stock price

Long positionto hedge

Total Payoff

Profit & Loss

Short position

Perfect hedge, but guaranteed to lose money.Impossible do to when a position is illiquid

(i.e., you cannot do it in the HT)

Strategy #2 1:1 (e.g., Covered Calls)

Stock price

Profit & Losses

Total Payoff

long Stock

short call

strike

Very popular - Neutral to moderately bullish

Example 1:1 Strategies Table

A short call Go long on the stock

A long call Go short on the stock

A short put ...

A long put ...

A short stock ...

A long stock ...

If our position is... ...this is what we (the system) should do

…work well BUT are expensive

Strategy #3: Multiple options (e.g., collars)

Stock price

Profit & Losses

short call

long Stock

Way out of the money – Inexpensive means to protect wealth from sharp downturns

long put

Total Payoff

Strategy #4: Dynamic Approaches (e.g., “Stop Loss”)

Stock price

Profit & Losses

short call

Total Payoff

long on Stock

Buy the stockif its price raises above strike,and sell it back if falls below. Yes, there is a

catch....

Yes, there is a catch....

These were the Basics.... Typically useful for manually

managing your portfolio In the past:

Most teams did Delta Hedging Some of the better teams did their own mix of

Delta and Gamma hedging There is a dark horse…

Strategy #5: Offset the Positionwith a Synthetic Security

Stock price

Long positionto hedge

Total Payoff

Profit & Loss

Synthetic Short position

Perfect hedge, but costly.

Put-Call ParityFor European Ps and Cs that have the same strike K, and expire by the same time t:

P + S = C + K e-rt thus, we can solve for S, P, or C, effectively synthesizing a security with a combination of the other two and some interest-earning cash.

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t Delta HedgingThe Greeks

Delta Hedging Objective: obtain the right

type and quantity of securities to counterbalance the movements of a security that we own.

DeltaNeutralPortfolio

What is Delta? Delta is a parameter. Roughly, it is the change in an option price

when the underlying stock price changes by a unit (e.g., one dollar).

O2 – O1

U2 – U1

Example1: a call option price goes down by $1.60 when a stock goes down by $2.Delta = -1.60 / -2.00 = +0.8

Example2: a put option is up by $0.5, when the stock is down by $1. Delta = 0.50 / -1.00 = -0.5

Delta =

Balancing a Position

I own 100,000 IBM stocks.

I am bearish - I think that the Stock price

may go down.

What kind andhow many options do I need, in order to counter-balance possible price changes and preserve my portfolio value?

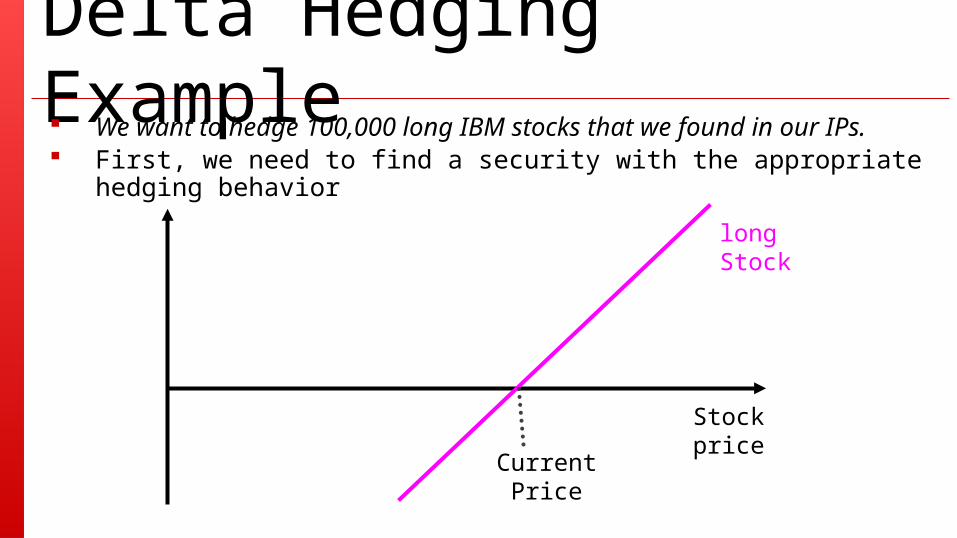

Delta Hedging Example We want to hedge 100,000 long IBM stocks that we found in our IPs. First, we need to find a security with the appropriate hedging behavior

Stock price

long Stock

Current Price

Hedging a Long Stock

Stock price

Profit & Loss long call

Stock price

short call

Profit & Loss

strike strike

Stock price

Profit & Loss

long put

Stock price

Profit & Loss

strike

short put

strike

Delta Hedging Example- Short calls have the right behavior (also long puts)- How many short calls?

Stock price

short call

long Stock

Strike

Current Price

How many calls are needed to make our position price-neutral?gain/loss from options = - gain/loss from stocks

Noptions * (O2-O1) = - Nstocks * (U2-U1)

Noptions = - Nstocks * (U2-U1)/(O2-O1)

Noptions = - Nstocks * 1/Deltacall

Noptions = - 100,000 * 1/0.8

Noptions = - 125,000 i.e., we need 125,000 short calls.

Numeric CheckSuppose that the IBM stock price decreases by $10. What happens to my portfolio?

by assumption:

Option price change / Underlier price change = 0.8

so: Option price change = 0.8 * (-$10) = -$8

Change in Portfolio value = 100,000 * (-$10) + (-125,000) * (-$8) =

= -1,000,000 + 1,000,000 = $0

We have a Delta neutral portfolio

Computing Delta Delta of a Call Option = N(d1)

Delta of a Put Option = N(d1) -1

d1 = {ln(S/X) + (r + s 2/2) t} s t

What Hedges What

1 Short call Delta long stock

1 Long call Delta short stock

1 Short put |Delta-1| short stock

1 Long put |Delta-1| long stock

1 Short stock 1/Delta long call or 1/|Delta-1| short put

1 Long stock 1/Delta short call or 1/|Delta-1| long put

If your position is... ...this is what you need

Need for Recalibration

There is a catch.Delta changes with time....

Dynamic Delta Hedging Delta changes with S, r, s and t. Since they all change in

time, the hedge needs to be periodically readjusted – a practice called rebalancing (r, s are fixed in the HT).

Example:Yesterday we wanted to hedge 100,000 long stock and so we shorted 125,000 calls. But now the delta is 0.9.

100,000 = - Noptions * 0.9

Noptions = - 111,111 so, we need to buy 13,889 calls

(=125,000-111,111) to maintain delta neutrality.

Next Time Balancing a whole portfolio Other types of hedging

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t WINITWhat Is New

In Technology?

Fin

anci

al In

form

ati

on

M

an

ag

em

en

t HomeworkThe Spartan Trader

Suggestions Give yourself plenty of time Test the numbers!

Critical Thinking Teams! Collab Why APPL_COCTB crashed your system After sunday posting, no more late credit.

Easy meter

The Hedge Tournament Questions? Team formation

Related Documents