Financial Holding Companies (Section 4(k) of the BHC Act) Section 3900.0 WHAT’S NEW IN THIS REVISED SECTION Effective January 2015, footnote 1 is revised to indicate that SR-12-17/CA-12-14 supersedes SR-99-15. See section 2124.05 of this manual. The Gramm-Leach-Bliley Act (the GLB Act) became effective on March 11, 2000. The GLB Act authorized affiliations among banks, securi- ties firms, insurance firms, and other financial companies. To further this goal, the GLB Act amended section 4 of the BHC Act to allow a bank holding company (BHC) or foreign bank that qualifies as a financial holding company (FHC) to engage in a broad range of activities that (1) the GLB Act defines as financial in nature or incidental to a financial activity, or (2) the Board, in consultation with the Secretary of the Treasury, determines to be financial in nature or incidental to a financial activity. Fur- thermore, section 4 of the BHC Act authorizes an FHC to engage in designated financial activi- ties, including insurance and securities under- writing and agency activities, merchant bank- ing, and insurance company portfolio investment activities. The GLB Act includes conditions that must be met for a BHC or a foreign bank to be deemed a ‘‘financial holding company’’ and engage in expanded activities. The GLB Act also allows an FHC to seek Board approval to engage in any activity that the Board determines (1) is complementary to a financial activity and (2) does not pose a substantial risk to the safety and soundness of depository institutions or the financial system generally. BHCs that do not qualify as FHCs are limited to engaging in those nonbanking activities that were permissible under section 4(c)(8) of the BHC Act before enact- ment of the GLB Act. The GLB Act provides that, in most cases, an FHC may engage in or acquire the shares of a company that is engaged in financial activities without obtaining prior approval from the Board. An FHC is instead required to provide a post- commencement notice to the Board within 30 days after commencing a financial activity or acquiring a company. See section 4(k) of the BHC Act. Prior approval from the Board is required to acquire or engage in the activities of a savings association. 3900.0.1 FHC SUPERVISORY OVERSIGHT AUTHORITY Under the GLB Act, the Federal Reserve has supervisory oversight authority and responsibil- ity for BHCs, including BHCs that operate as FHCs. The GLB Act sets forth parameters for operating relationships between the Federal Reserve and other regulators. The statute differ- entiates between the Federal Reserve’s relations with (1) depository institution regulators and (2) functional regulators, which include insur- ance, securities, and commodities regulators. There should be minimal, if any, noticeable change in the well-established relationships between the Federal Reserve as BHC (including FHC) supervisor and the bank and thrift supervi- sors (federal and state). The Federal Reserve’s relationships with functional regulators will, in practice, depend on the extent to which an FHC is engaged in functionally regulated activities; those relationships will also be influenced by existing working arrangements. The Federal Reserve’s supervisory oversight role is that of an umbrella supervisor concentrat- ing on a consolidated or group-wide analysis of an organization. Umbrella supervision is not an extension of more traditional bank-like supervi- sion throughout an FHC. The FHC framework is consistent with and incorporates principles that are well established for BHCs. The FHC supervisory policy focuses on addressing super- visory practice for and relationships with FHCs, particularly those that are engaged in securities or insurance activities. See SR-00-13. 3900.0.2 ROLES OF SUPERVISORS The Federal Reserve is responsible for the con- solidated supervision of FHCs. In this regard, the Federal Reserve will assess the holding com- pany on a consolidated or group-wide basis with the objective of ensuring that the holding com- pany does not threaten the viability of its deposi- tory institution subsidiaries. The manner in which the Federal Reserve fulfills this role will likely evolve along with the activities and structure of FHCs, and it may differ depending on the mix of banking, securities, and insurance activities of an FHC. Depository institution subsidiaries of FHCs are supervised by their appropriate primary bank BHC Supervision Manual January 2015 Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Holding Companies(Section 4(k) of the BHC Act) Section 3900.0

WHAT’S NEW IN THIS REVISEDSECTION

Effective January 2015, footnote 1 is revised toindicate that SR-12-17/CA-12-14 supersedesSR-99-15. See section 2124.05 of this manual.

The Gramm-Leach-Bliley Act (the GLB Act)became effective on March 11, 2000. The GLBAct authorized affiliations among banks, securi-ties firms, insurance firms, and other financialcompanies. To further this goal, the GLB Actamended section 4 of the BHC Act to allow abank holding company (BHC) or foreign bankthat qualifies as a financial holding company(FHC) to engage in a broad range of activitiesthat (1) the GLB Act defines as financial innature or incidental to a financial activity, or(2) the Board, in consultation with the Secretaryof the Treasury, determines to be financial innature or incidental to a financial activity. Fur-thermore, section 4 of the BHC Act authorizesan FHC to engage in designated financial activi-ties, including insurance and securities under-writing and agency activities, merchant bank-ing, and insurance company portfolio investmentactivities.

The GLB Act includes conditions that mustbe met for a BHC or a foreign bank to bedeemed a ‘‘financial holding company’’ andengage in expanded activities. The GLB Actalso allows an FHC to seek Board approval toengage in any activity that the Board determines(1) is complementary to a financial activity and(2) does not pose a substantial risk to the safetyand soundness of depository institutions or thefinancial system generally. BHCs that do notqualify as FHCs are limited to engaging in thosenonbanking activities that were permissible undersection 4(c)(8) of the BHC Act before enact-ment of the GLB Act.

The GLB Act provides that, in most cases, anFHC may engage in or acquire the shares of acompany that is engaged in financial activitieswithout obtaining prior approval from the Board.An FHC is instead required to provide a post-commencement notice to the Board within 30days after commencing a financial activity oracquiring a company. See section 4(k) of theBHC Act. Prior approval from the Board isrequired to acquire or engage in the activities ofa savings association.

3900.0.1 FHC SUPERVISORYOVERSIGHT AUTHORITY

Under the GLB Act, the Federal Reserve hassupervisory oversight authority and responsibil-ity for BHCs, including BHCs that operate asFHCs. The GLB Act sets forth parameters foroperating relationships between the FederalReserve and other regulators. The statute differ-entiates between the Federal Reserve’s relationswith (1) depository institution regulators and(2) functional regulators, which include insur-ance, securities, and commodities regulators.There should be minimal, if any, noticeablechange in the well-established relationshipsbetween the Federal Reserve as BHC (includingFHC) supervisor and the bank and thrift supervi-sors (federal and state). The Federal Reserve’srelationships with functional regulators will, inpractice, depend on the extent to which an FHCis engaged in functionally regulated activities;those relationships will also be influenced byexisting working arrangements.

The Federal Reserve’s supervisory oversightrole is that of an umbrella supervisor concentrat-ing on a consolidated or group-wide analysis ofan organization. Umbrella supervision is not anextension of more traditional bank-like supervi-sion throughout an FHC. The FHC frameworkis consistent with and incorporates principlesthat are well established for BHCs. The FHCsupervisory policy focuses on addressing super-visory practice for and relationships with FHCs,particularly those that are engaged in securitiesor insurance activities. See SR-00-13.

3900.0.2 ROLES OF SUPERVISORS

The Federal Reserve is responsible for the con-solidated supervision of FHCs. In this regard,the Federal Reserve will assess the holding com-pany on a consolidated or group-wide basis withthe objective of ensuring that the holding com-pany does not threaten the viability of its deposi-tory institution subsidiaries. The manner in whichthe Federal Reserve fulfills this role will likelyevolve along with the activities and structure ofFHCs, and it may differ depending on the mixof banking, securities, and insurance activitiesof an FHC.

Depository institution subsidiaries of FHCsare supervised by their appropriate primary bank

BHC Supervision Manual January 2015Page 1

or thrift supervisor (federal and state). The GLBAct did not alter the role of the Federal Reserve,as holding company supervisor, vis-a-vis theprimary supervisors of FHC-associated bankand thrift subsidiaries. Traditionally, the FederalReserve has relied to the fullest extent possibleon those supervisors.

Nonbank (or nonthrift) subsidiaries engagedin securities, commodities, or insurance activi-ties are supervised by their appropriate func-tional regulators. Such functionally regulatedsubsidiaries include a broker, dealer, investmentadviser, and investment company registered withand regulated by the Securities and ExchangeCommission (SEC) (or, in the case of an invest-ment adviser, registered with any state); aninsurance company or insurance agent subject tosupervision by a state insurance regulator; and anonbank subsidiary engaged in activities regu-lated by the Commodity Futures Trading Com-mission (CFTC).

3900.0.3 FHC SUPERVISIONOBJECTIVES

The Federal Reserve, as umbrella supervisor,will seek to determine that FHCs are operated ina safe and sound manner so that their financialcondition does not threaten the viability of affili-ated depository institutions. Oversight of FHCs(particularly those engaged in a broad range offinancial activities) at the consolidated level isimportant because the risks associated with thoseactivities can cut across legal entities and busi-ness lines. The purpose of FHC supervision is toidentify and evaluate, on a consolidated or group-wide basis, the significant risks that exist in adiversified holding company to assess how theserisks might affect the safety and soundness ofdepository institution subsidiaries.

Accordingly, the Federal Reserve will focuson the financial strength and stability of FHCs,their consolidated risk-management processes,and overall capital adequacy. The Federal Reservewill review and assess the internal policies,reports, and procedures and the effectiveness ofthe FHC consolidated risk-management pro-cess. The appropriate bank, thrift, or functionalregulator will continue to have primary respon-sibility for evaluating risks, hedging, and riskmanagement at the legal-entity level for theentity or entities that it supervises.

FHC supervision is not intended to imposebank-like supervision on FHCs, nor is it intended

to duplicate or replace supervision by the pri-mary bank, thrift, or functional regulators ofFHC subsidiaries. Rather, FHC supervision seeksto protect the depository institution subsidiariesof increasingly complex organizations with sig-nificant interrelated activities and risks, whilenot imposing an unduly duplicative or onerousburden on the subsidiaries of the organization.Effective financial holding company supervisionrequires—

1. strong, cooperative relationships between theFederal Reserve and primary bank, thrift,and functional regulators and foreign super-visors (these relationships respect the indi-vidual statutory authorities and responsibili-ties of the respective supervisors, but alsoallow for enhanced information flows andcoordination so that individual responsibili-ties can be carried out effectively withoutcreating duplication or excessive burden);

2. substantial reliance by the Federal Reserveon reports filed with or prepared by bank,thrift, and functional regulators, as well as onpublicly available information for both regu-lated and nonregulated subsidiaries; and

3. continued reliance on the risk-focused super-vision and examination process and on mar-ket discipline.

3900.0.4 FHC SUPERVISION INPRACTICE

The supervisory activities of the Federal Reservefall into three broad categories: (1) informationgathering, assessments, and supervisory coop-eration; (2) ongoing supervision; and (3) promo-tion of sound practices and improved disclosure.

3900.0.4.1 Information Gathering,Assessments, and SupervisoryCooperation

To fulfill its GLB Act responsibilities, the Fed-eral Reserve needs to interact closely andexchange information with the primary bank,thrift, and functional regulators. The FederalReserve will foster strong relationships withsenior management and the boards of directorsof FHCs, and have access to timely informa-tion from FHCs. These relationships will needto include heads of significant business linesand key internal-audit, control, and risk-management officials in order to understandhow risk-management and internal-control poli-cies and procedures established at the consoli-

Financial Holding Companies (Section 4(k) of the BHC Act) 3900.0

BHC Supervision Manual January 2015Page 2

dated level are being implemented and assessed.To achieve these objectives, Federal Reservesupervisory staff will take the following actions:

1. Regularly assess an FHC’s centralized risk-management and control processes. Suchassessments are necessary to understand anorganization’s overall risk profile, identifymaterial contributions to core risks, and deter-mine how such risks are being managed andcontrolled on a consolidated basis.

2. Perform limited, targeted transaction testing.The purpose of this transaction testing is toverify that the risk-management systems ofthe FHC are adequately and appropriatelymeasuring and managing areas of risk for theorganization, and to confirm that laws andregulations applicable to the FHC and withinthe jurisdiction of the Federal Reserve arebeing observed.

3. Have periodic discussions with FHC seniormanagement and boards of directors. Suchdiscussions will enable the Federal Reserveto build relationships with key personnel andto understand changing activities and theevolving risk profile of the consolidatedorganization. Periodic discussions also willprovide a forum for supervisory staff to pres-ent any findings or concerns related to theactivities of the group as a whole or to busi-ness lines that cut across legal entities.

4. Have periodic discussions with key person-nel. Discussions will be held with the person-nel responsible for corporate managementand control functions, such as heads of busi-ness lines, risk management, internal audit,and internal control.

When performing the above tasks, FederalReserve supervisory staff, to the extent possible,will coordinate their actions with those of theprimary bank, thrift, and functional regulators ofthe FHC’s subsidiaries. For example, to under-stand the risks and risk-management systems ofan FHC at the consolidated level, the FederalReserve will need information concerning assetsor liabilities booked in significant bank, thrift,and functionally regulated subsidiaries withinthe FHC group. The primary bank, thrift, andfunctional regulators of such subsidiaries alsomay need information from the FHC to performtheir respective statutory mandates. To assist insharing needed information, Federal Reservesupervisory staff should do the following:

1. Have periodic meetings with the primarybank, thrift, and functional regulators of anFHC’s subsidiaries. The purpose of these

meetings is to develop an understanding ofthe risk profiles of the individual regulatedlegal entities and their relation to the FHC’soverall risk profile. These meetings also shouldbe used, when appropriate, to share informa-tion regarding supervisory plans and to coor-dinate supervisory activities and follow-up,as needed.

2. Review the examination findings of primarybank, thrift, and functional regulators (andtheir self-regulatory organizations) togetherwith other relevant information. The purposeof this review is to develop a consolidatedpicture of the FHC’s financial condition andrisk profile, the effectiveness of risk-management and internal-control policies,and the implications for the affiliated deposi-tory institutions.

3. Make available to primary bank, thrift, andfunctional regulators, to the extent permis-sible, pertinent information regarding theFHC. Included is information on the finan-cial condition, risk-management policies, andoperations of an FHC that may have a mate-rial impact on individual regulated subsidi-aries, as well as information concerning trans-actions or relationships between the regulatedsubsidiaries and other subsidiaries within theFHC group. This process will assist supervi-sors in performing their statutory and super-visory responsibilities over regulatedsubsidiaries.

4. Participate in the sharing of informationamong international supervisors, consistentwith applicable law. The purpose of thisexchange is to ensure that an FHC’s globalactivities are supervised on a consolidatedbasis and to minimize material gaps insupervision.

5. Review internal-audit and managementreports and publicly available information(including market information on equity anddebt prices of the consolidated organiza-tion), as well as reports and statistics col-lected by other regulators, including regula-tors of depository institution subsidiaries. Tolimit regulatory burden, this informationshould be obtained, to the fullest extent pos-sible, from (1) the parent organization; (2) pri-mary bank, thrift, and functional regulatorsof the FHC’s regulated subsidiaries; and(3) publicly available sources, such as exter-nally audited financial statements.

Financial Holding Companies (Section 4(k) of the BHC Act) 3900.0

BHC Supervision Manual January 2015Page 3

3900.0.4.2 Ongoing Supervision

3900.0.4.2.1 FHC Structure,Management, and the ApplicationsProcess

The Federal Reserve is responsible for under-standing the consolidated organization’s legal,organizational, and risk-management structure;major business activities; and risk exposuresand risk-management systems. The FederalReserve needs to understand the nature anddegree of involvement of the board of directorsin overseeing their organization’s risk-management and control process at the consoli-dated group level. The Federal Reserve, whenconsidering any formal application, declaration,or notification at the FHC level, will coordinate,as appropriate, with primary bank, thrift, andfunctional regulators.

3900.0.4.2.2 Reporting and Examination

The Federal Reserve will rely, to the fullestextent possible, on reports that an FHC or itssubsidiaries are required to file with federal orstate authorities (or self-regulatory organiza-tions) or on reports that are prepared by thefederal or state authorities. The Federal Reservewill rely on routinely prepared managementreports, publicly reported information, andexternally audited financial statements. The Fed-eral Reserve also will rely to the fullest extentpossible on the examination of an FHC’s bankand nonbank subsidiaries by their appropriateprimary bank, thrift, and functional regulators(and their self-regulatory organizations).

If supervisory staff requires a specializedreport from a functionally regulated subsidiaryof an FHC, staff will first request it from thesubsidiary’s appropriate functional regulator. Inthe event that the report is not made available tothe Federal Reserve, supervisory staff may obtainthe report directly from the functionally regu-lated subsidiary if it is necessary to assess—

1. a material risk to the FHC or any of itsdepository institution subsidiaries;

2. compliance with any federal law that theFederal Reserve has specific jurisdiction toenforce against the FHC or a subsidiary; or

3. the FHC’s systems for monitoring and con-trolling financial and operational risks thatmay pose a safety-and-soundness threat to adepository institution subsidiary.

The Federal Reserve may examine a function-ally regulated subsidiary under certain circum-stances. Before examining a functionally regu-lated subsidiary, supervisory staff should firstseek to obtain the necessary information fromthe appropriate functional regulator. If an exami-nation is determined to be necessary, the FederalReserve should coordinate its actions with theappropriate functional regulator. An examina-tion may be conducted when the Federal Reservehas reasonable cause to believe (or reasonablydetermines) that—

1. the subsidiary is engaged in an activity thatposes a material risk to an affiliated deposi-tory institution,

2. the examination is necessary to be adequatelyinformed about the FHC’s systems for moni-toring and controlling the financial andoperational risks that may pose a safety-and-soundness risk to a depository institutionsubsidiary; or

3. the subsidiary is not in compliance with anyfederal law that the Board has specific juris-diction to enforce (and the Board cannotdetermine compliance by examining the FHCor its affiliated depository institutions).

The Federal Reserve, consistent with its cur-rent practice, will continue relying to the fullestextent possible on the work performed by bank,thrift, and functional regulators to validate thatmaterial risks are measured and managedadequately at the regulated subsidiary level.Where necessary and appropriate, and consis-tent with (1) through (3) immediately above, theFederal Reserve may conduct or participate inreviews at banks, thrifts, or functionally regu-lated subsidiaries to validate that risk-management and internal-control policies estab-lished at the consolidated level are beingimplemented effectively.

For an FHC subsidiary that is not supervisedby a bank, thrift, or functional regulator, theFederal Reserve will obtain information fromthe subsidiary, as appropriate and necessary, toassess the financial condition of the FHC as awhole. In addition, the Federal Reserve willconduct examinations of such subsidiaries, ifnecessary, to be informed about (1) the nature ofthe subsidiary’s operations and financial condi-tion, (2) the subsidiary’s financial and opera-tional risks that may pose a threat to the safetyand soundness of any depository institution sub-sidiary of the FHC, and (3) the systems formonitoring and controlling such risks. Underthe GLB Act, the Federal Reserve may notexamine any subsidiary of an FHC that is an

Financial Holding Companies (Section 4(k) of the BHC Act) 3900.0

BHC Supervision Manual January 2015Page 4

investment company registered with the SECand that is not itself a BHC.

3900.0.4.2.3 Capital Adequacy

The Federal Reserve is responsible for assessingconsolidated capital adequacy for FHCs, withthe ultimate objective of protecting the insureddepository subsidiaries from the effects of dis-ruptions in the nonbank portions of the organi-zation. Capital adequacy will be assessed inrelation to the risk profile of the consolidatedorganization. The Federal Reserve will reviewthe FHC’s internal risk assessment and relatedcapital-analysis process for determining theadequacy of its overall capital position. Such areview will include consideration of current andfuture economic conditions, business-development plans for the future, possible stressscenarios, and internal risk-control and auditprocedures. As BHCs, FHCs are subject to theFederalReserve’sholdingcompanycapitalguide-lines, which set forth minimum capital ratiosthat serve as tripwires for additional supervisoryscrutiny and corrective action. The FederalReserve will review these requirements as theyapply to FHCs and may, if warranted, adapt themanner in which they apply to FHCs that engagein a broad range of financial activities.

Although the Federal Reserve is responsiblefor assessing the consolidated capital adequacyof FHCs, the primary bank, thrift, or functionalregulators of FHC subsidiaries will continue toset and enforce applicable capital requirementsfor the regulated entities within their jurisdic-tion. Under the GLB Act, the Federal Reservemay not establish separate capital adequacyrequirements for an FHC subsidiary that is incompliance with the capital requirements of itsfunctional regulator.

Consistent with current practice, the FederalReserve will continue to place significant reli-ance on the primary bank, thrift, or functionalregulator’s analysis of the capital adequacy of aregulated subsidiary. That analysis will be asignificant input in the Federal Reserve’s assess-ment of an FHC’s consolidated capital adequacy,especially when a securities broker-dealer orinsurance company is a predominant part of anFHC.

Several issues become particularly importantwhen assessing the consolidated capital adequacyof FHCs with functionally regulated subsidi-aries. The capital adequacy requirements thathave been established for banking, securities,and insurance entities by their respective regula-tors reflect varying definitions of the elements

of capital and varying approaches to asset andliability valuations. Yet techniques for assessingcapital adequacy must be able to identify situa-tions such as double or multiple leverage ordouble-gearing. In such cases, the actual capitalprotection may be overstated.

3900.0.4.2.4 Intra-Group Exposures andConcentrations

Intra-group exposures, including servicingarrangements and risk concentrations, have thepotential to threaten the condition of regulatedentities. Intra-group exposures may be signifi-cant at large, complex FHCs, especially thosethat operate their businesses on global lines thatcut across legal entities within the firm. TheFederal Reserve’s focus in this area is the poten-tial impact of intra-group exposures and concen-trations on insured depository institution subsid-iaries of an FHC.

Risk concentrations can take many forms,including exposures to one or more counterpar-ties or related entities, industry sectors, and geo-graphic regions. For risk concentrations, theholding company supervisor is uniquely posi-tioned to understand the combinations of expo-sures within an organization across all legalentities. This understanding is critical at thegroup level—risk concentrations that are pru-dent on a legal-entity basis may aggregate to anunsafe level for the consolidated organization.The Federal Reserve will monitor intra-groupexposures and risk concentrations as follows:

1. The appropriate primary bank and thrift regu-lators will continue to monitor and enforcesection 23A and 23B restrictions at the bankor thrift level. The Federal Reserve will focuson assessing whether the FHC monitors andensures compliance with these statutoryrequirements. The Federal Reserve plans tobegin collecting data from each depositoryinstitution subsidiary of BHCs, includingFHCs, on their covered transactions withaffiliates that are subject to sections 23A and23B and will share that data with primarybank and thrift regulators.

2. Functional regulators will continue to moni-tor and enforce any intra-group exposurerestrictions that may apply to the regulatedentities under their jurisdictions.

3. The Federal Reserve will focus on under-standing and monitoring related-party expo-

Financial Holding Companies (Section 4(k) of the BHC Act) 3900.0

BHC Supervision Manual January 2015Page 5

sures at the group level (including areas suchas servicing agreements, derivatives expo-sures, and payments-system exposures). Animportant emphasis will be the extent towhich risk management in a group’s subsidi-ary depository instutions depends on transac-tions with affiliates.

4. The Federal Reserve will focus on manage-ment’s effectiveness in monitoring and con-trolling intra-group exposures and risk con-centrations. The Federal Reserve will considerhow an organization’s risk-management pro-cesses measure and manage group-wide riskconcentrations.

3900.0.4.2.5 Enforcement Powers

The Federal Reserve is authorized generally totake enforcement action against FHCs and theirnonbank subsidiaries. The primary bank andthrift supervisors have the authority to takeenforcement action against the banks and thriftsunder their respective jurisdictions. Under theGLB Act, the Federal Reserve may takeenforcement action against a functionally regu-lated subsidiary of an FHC, but only when suchaction is necessary to prevent or redress anunsafe or unsound practice or breach of fidu-ciary duty that poses a material risk either to(1) the financial safety, soundness, or stability ofan affiliated depository institution or (2) thedomestic or international payments system. Insuch circumstances, the Federal Reserve mayonly take the action if it is not reasonably pos-sible to protect effectively against the materialrisk through an action directed at or against anaffiliated depository institution.

Under any circumstances, the Board may takeenforcement action against a functionally regu-lated subsidiary to enforce compliance with anyfederal law that the Federal Reserve has specificjurisdiction to enforce against the subsidiary. Ifthe Federal Reserve believes that an enforce-ment action against a functionally regulatedentity is necessary, the Federal Reserve willnotify the entity’s appropriate functional regula-tor and, whenever practical, will coordinate suchan action with any action taken by the func-tional regulator. It is expected that the FederalReserve will not take an enforcement actionagainst a functionally regulated subsidiary (or aperson associated with the subsidiary) if theproblem involves factors and statutes that are

the primary responsibility of the functional regu-lator.

Under the existing bank holding companyframework, the Federal Reserve coordinatesenforcement actions with the primary bank andthrift regulators, possibly with some adaptationof the action for the holding company context(such as limitations on parent company debt ordividends). The Federal Reserve will continueto coordinate enforcement actions with theseregulators. Similarly, the Federal Reserve willcoordinate with functional regulators when for-mulating and issuing enforcement actions thatinvolve or may have an impact on functionallyregulated subsidiaries.

3900.0.4.3 Promotion of Sound Practicesand Improved Disclosure

The Federal Reserve can promote sound prac-tices in a number of ways, such as by monitor-ing trends in risk exposures and risk-management practices across the FHC populationthrough a combination of efforts, including—

1. regular discussions, centered on specific issuesand emerging risks, with FHC management;

2. regular meetings with primary bank, thrift,and functional regulators to explore and dis-cuss issues of mutual interest or concern;

3. interagency working groups or specialty teamsto gain early insight into risks that cut acrossthe various entities of a conglomerate orgroups of conglomerates; and

4. industry conferences on relevant topics ofinterest.

These initiatives will contribute to the develop-ment of sound practices that the Federal Reserveand the primary bank, thrift, and functionalregulators can communicate to the senior man-agement and boards of directors of the FHCs, aswell as to the senior management of their bankand nonbank subsidiaries.

Improved transparency and public disclosurecan meaningfully supplement the efforts ofsupervisors to monitor the increasingly complexand global activities of diversified banking orga-nizations. Consistent with sound accounting prin-ciples, practices, and depository institution safety-and-soundness practices, the Federal Reservewill participate in efforts to enhance disclosuresthat will illuminate group-wide activities, riskexposures, risk management, controls, and intra-group exposures.

Financial Holding Companies (Section 4(k) of the BHC Act) 3900.0

BHC Supervision Manual January 2015Page 6

3900.0.4.4 Supervisory Response toChallenges Posed by FHCs

The Federal Reserve’s response to the supervi-sory challenges of FHCs has been in the contextof the consolidated supervision of BHCs.1

Examples include greater reliance on risk-focused supervision; strengthening relationshipswith senior management; improving coordina-tion with other federal, state, and internationalregulatory and supervisory authorities; greaterreliance on specialty teams, sound-practicespapers, and public disclosures; and simplifica-tion of the applications process.

The more diversified FHCs present newsupervisory challenges. To address these chal-lenges, the Federal Reserve will continue tostrengthen—

1. cooperative arrangements with bank and thriftregulators, the SEC, the CFTC, state insur-ance and securities regulators, and foreignsupervisors;

2. relationships with the FHC management andpersonnel responsible for significant risk-management functions and, when necessary,the management of the organization’s non-bank subsidiaries;

3. information flows that provide supervisorswith relevant, up-to-date information withoutimposing an unwarranted burden on financialorganizations;

4. techniques for evaluating capital adequacyfor FHCs engaged in an expanded range ofnonbank financial activities;

5. public disclosures and market discipline;6. techniques for assessing the overall risk pro-

file of FHCs and the implications for affili-ated depository institutions; and

7. incentives for FHCs to continually reviewand improve their risk-management pro-cesses, internal controls, and audit practices.

The Federal Reserve is committed to workingconstructively and cooperatively with all regula-tors involved in overseeing the activities ofFHCs and their bank and nonbank subsidiaries.

1. The Federal Reserve’s framework for supervising large

complex banking organizations (LCBOs) is described in

SR-12-17/CA-12-14, “Consolidated Supervision for Large

Financial Institutions.” See section 2124.05.

Financial Holding Companies (Section 4(k) of the BHC Act) 3900.0

BHC Supervision Manual January 2015Page 7

U.S. Bank Holding Companies Operating as Financial HoldingCompanies (Section 4(k) of the BHC Act) Section 3901.0

To become a financial holding company (FHC),a domestic bank holding company (BHC) mustfile a written declaration with the appropriateFederal Reserve Bank. This declaration shouldcontain the following information:

1. A statement that the BHC elects to be anFHC.

2. The name and head-office address of thecompany and each depository institution con-trolled by the company. For purposes of theelection process for both domestic BHCs andforeign banks, the term ‘‘depository institu-tion’’ here means any national bank, state-chartered bank, federal branch of a foreignbank, insured branch of a foreign bank, sav-ings association, savings bank, and industrialbank. It also includes any trust company thatengages in the business of receiving depositsother than trust funds. (See 12 U.S.C. 1813.)A depository institution does not have tohave FDIC insurance.

3. A certification that all depository institutionscontrolled by the company are well capital-ized as of the date the company files itsdeclaration.

4. The capital ratios for all relevant capital mea-sures (as defined in section 38 of the FederalDeposit Insurance Act), as of the close of theprevious quarter, for each depository institu-tion controlled by the company on the datethe company files its declaration.

5. A certification that all depository institutionscontrolled by the company are well managedas of the date the company files its declara-tion.

A depository institution is well managed if, atthe most recent inspection or examination orsubsequent review by its appropriate federalbanking agency, the institution received (1) atleast a satisfactory composite rating and (2) atleast a satisfactory rating for management, ifsuch a rating is given. In the case of a deposi-tory institution that has not received an inspec-tion or examination rating, a depository institu-tion is well managed if the Board has determined,after a review of the depository institution’smanagerial and other resources and after con-sulting with the depository institution’s appro-priate federal and state banking agency, that theinstitution is well managed. In addition, a deposi-tory institution that results from the merger oftwo or more depository institutions that are wellmanaged will be considered to be well managedunless the Board determines otherwise after

consulting with the appropriate federal bankingagency for each depository institution involvedin the merger.

A depository institution that results from themerger of a depository institution that is wellmanaged with one or more depository institu-tions that are not well managed or that have notbeen examined will be considered to be wellmanaged, if the Board determines that the result-ing institution is well managed. The Boardmakes this determination after a review of themanagerial and other resources of the resultinginstitution and after consulting with the appro-priate federal and state banking agencies for theinstitutions involved in the merger, asapplicable.

The Gramm-Leach-Bliley Act (the GLB Act)also requires that all the insured depository insti-tutions controlled by the FHC at the time of thedeclaration must be rated satisfactory or betterunder the Community Reinvestment Act (CRA).When determining whether the insured deposi-tory institutions controlled by a BHC meet theCRA requirement, the Federal Reserve excludesan institution that was acquired during the 12months preceding the date the company filed itsdeclaration. To qualify for this exception, (1) thecompany must have submitted the depositoryinstitution’s affirmative correction plan to theappropriate federal banking agency and (2) theagency must have accepted the plan.

A BHC must file its declaration to become anFHC with the appropriate responsible ReserveBank. A BHC’s election to become an FHC iseffective on the thirty-first day after the date thata complete declaration was received, unless theBoard notifies the company before that time thatthe election is ineffective. The Board or theappropriate Federal Reserve Bank also maynotify a BHC in writing that its election tobecome an FHC is effective before the thirty-first day after the date that a complete declara-tion was filed.

When an FHC’s declaration becomes effec-tive, it may engage in the expanded financialactivities available to such companies. If, how-ever, the Board has timely notified a BHC thatits declaration is ineffective, the BHC will notbe considered an FHC and may not begin toengage in any expanded activities.

A company that is not a BHC may simulta-neously submit an application under section3(a)(1) of the Bank Holding Company Act (BHC

BHC Supervision Manual July 2009Page 1

Act) to become a BHC and to request to becomean FHC on consummation of that transaction.The company must (1) state that it seeks tobecome an FHC on consummation of its section3 proposal to become a BHC and (2) certify thateach depository institution that would be con-trolled by the company on consummation of thesection 3 proposal will be both well capitalizedand well managed on the date of consummation.To coordinate action on these two requests, theacceptance of the declaration as complete doesnot occur until the date the company lawfullyconsummates its section 3 proposal and becomesa BHC. A simultaneous declaration will not beeffective if the Board notifies the company atany time before consummation that (1) anydepository institution that would be controlledby the company on consummation will not bewell capitalized and well managed or (2) anyinsured depository institution that would be con-trolled by the company on consummation hasnot achieved at least a satisfactory rating at itsmost recentCRAexamination.An insureddeposi-tory institution that is controlled or would becontrolled by a company filing a simultaneousdeclaration and section 3(a)(1) application tobecome a BHC may not be excluded for thepurposes of evaluating the CRA performancerecord under this provision or the general FHCcertification requirements of section 225.82(d)of Regulation Y.

In most cases, an FHC may, without provid-ing prior notice to or obtaining prior approvalfrom the Board, conduct an activity that is finan-cial in nature or incidental to a financial activity(a financial activity). (See section 225.85(a)(1)of Regulation Y.) An FHC may conduct a finan-cial activity by engaging directly in the activityor by acquiring and retaining the shares of anycompany that is engaged exclusively in one ormore financial activities. An FHC may conducta financial activity at any location inside oroutside of the United States, subject to the lawsof the jurisdiction in which the activity is con-ducted. A company acquired or to be acquiredby an FHC also may engage in other activitiesthat are permissible for an FHC, in accordancewith any applicable notice, approval, or otherrequirements.

An FHC may acquire more than 5 percent ofthe voting shares or control of a company that isnot engaged exclusively in activities that arefinancial in nature, incidental to financial activi-ties, or otherwise permissible for the acquiringFHC. (See section 225.85(a)(3) of Regulation

Y.) To do so, the acquisition must meet threerequirements:

1. The company to be acquired must be sub-stantially engaged in activities that are finan-cial in nature, incidental to a financial activ-ity, or otherwise permissible for the FHCunder section 4(c) of the BHC Act. A com-pany is considered to be substantially engagedin permissible activities if at least 85 percentof the company’s consolidated total annualgross revenues is derived from and at least85 percent of the company’s consolidatedtotal assets is attributable to the conduct ofactivities that are financial in nature, inciden-tal to a financial activity, or otherwise per-missible for an FHC under section 4(c) of theBHC Act. An FHC’s management shouldconsult with Board staff if they are uncertainwhether a proposed acquisition meets thisstandard.

2. The FHC must comply with the noticerequirements of section 225.87 of RegulationY. The acquired company must conform, ter-minate, or divest, within two years of thedate the FHC acquires shares or control ofthe company, all activities that are not finan-cial in nature, incidental to a financial activ-ity, or otherwise permissible for the FHCunder section 4(c) of the BHC Act. Althoughan FHC may acquire any percentage of sharesor control of a company engaged in limitedimpermissible activities, the FHC needs onlyto provide a post-transaction notice if suchanacquisition results incontrolof thecompany.

3. After being acquired by an FHC, the com-pany engaged in impermissible activities maynot engage in or acquire a company engagedin any activity that is not permissible for theFHC.

Section 225.85(c) of Regulation Y identifiestwo circumstances in which Board approval isstill required to engage in financial activities.First, prior approval in accordance with section4(j) of the BHC Act and section 225.24 ofRegulation Y is required to acquire more than5 percent of the voting shares or control of asavings association or any company that owns,operates, or controls a savings association. Sec-ond, the Board may, in the exercise of its super-visory authority, require an FHC to provide itwith prior notice or obtain prior Board approvalif circumstances warrant. The GLB Act did notchange in any way the requirement that a com-pany receive prior Board approval under section3 of the BHC Act before acquiring shares orcontrol of a bank.

U.S. Bank Holding Companies Operating as Financial Holding Companies 3901.0

BHC Supervision Manual July 2009Page 2

Section 225.87(a) of Regulation Y requiresan FHC that commences an activity, or thatacquires control or shares of a company engagedin an activity under section 225.86 of Regula-tion Y, to provide written notice to the appropri-ate Reserve Bank within 30 calendar days aftercommencing the activities or consummating theacquisition. The notice must be provided on theFR Y-10 form, obtained from the Board or anyReserve Bank. This requirement also applies toan activity that the FHC may engage in undersection 4(c)(8) of the BHC Act that is incorpo-rated under section 4(k) of the act.

There are two circumstances in which noticeto the Board is not required to engage in anactivity: (1) when an FHC acquires shares of acompany without acquiring control of the com-pany, or (2) when an FHC is engaged in securi-ties underwriting, dealing, or market-makingactivities described in section 4(k)(4)(E), mer-chant banking investment activities conductedpursuant to section 4(k)(4)(H), or insurancecompany investment activities conducted pursu-ant to section 4(k)(4)(I) of the BHC Act, andhas provided the System with the appropriatenotice regarding the relevant activity. (See sec-tion 225.87(b) of Regulation Y.) Under thesecircumstances, the FHC must provide writtennotice to the Board within 30 days after acquir-ing, as part of a merchant banking activity undersection 4(k)(4)(H) or an insurance companyinvestment activity under section 4(k)(4)(I) ofthe BHC Act, more than 5 percent of any com-pany at a cost that exceeds 5 percent of theFHC’s tier 1 capital or $200 million, whicheveris less.

3901.0.1 SUPERVISORY CONCERNS

In some instances, a U.S. BHC or a foreign bankmay meet the statutory requirements to be anFHC, but its capital strength and managerialresources are less than satisfactory on a consoli-dated basis. In this situation, the Federal Reservemay have supervisory concerns about the con-solidated entity although it technically qualifiesas an FHC. The Federal Reserve may, in theexercise of its supervisory authority, restrict orlimit the conduct of new activities or futureacquisitions of an FHC, or take other appropri-ate action, if it finds that the FHC does not havethe financial or managerial resources to conductthe activity or make the acquisition. This super-visory action could be based, for example, on adetermination that the company does not haveadequate capital or risk-management systems toconduct a specific activity in a safe and sound

manner and may involve the issuance of cease-and-desist orders, the execution of written agree-ments, or other appropriate supervisory action.

3901.0.2 HOLDING COMPANY FAILSTO CONTINUE MEETING FHCCAPITAL AND MANAGEMENTREQUIREMENTS

If a domestic bank holding company has madean effective election to be an FHC, and theBoard finds that any depository institution sub-sidiary owned or controlled by the companyceases to be well capitalized or well managed,the company must execute an agreement accept-able to the Federal Reserve Board to complywith all applicable capital and managementrequirements. This agreement should be executedwithin 45 days after the Board notifies the com-pany that it is not in compliance with the appli-cable requirements for an FHC. (See section225.83 of Regulation Y.)

At the request of the bank holding company,the Federal Reserve Board may extend the 45-day period. The request should state why anextension is necessary. The agreement mustexplain the specific actions that the bank hold-ing company will take to correct all areas ofnoncompliance, provide a schedule for all suchactions, and provide any other information theBoard may require, and be acceptable to theBoard.

During the period of noncompliance, the Fed-eral Reserve Board may impose limitations orconditions on the activities of the company. Inaddition, the company must obtain the Board’sapproval before conducting any of the activitiesthat are newly authorized for FHCs by the GLBAct. Section 225.83 of Regulation Y also setsforth the consequences of failing to correct thenoncompliance within a period of 180 days.Such consequences may include divestiture ofownership or control of any depository institu-tion the company owns or controls, or the cessa-tion of the expanded activities permitted forFHCs.

3901.0.3 DEPOSITORY INSTITUTIONSUBSIDIARY FAILS TO MAINTAIN ASATISFACTORY OR BETTER CRARATING

The Federal Reserve Board prohibits an FHC

U.S. Bank Holding Companies Operating as Financial Holding Companies 3901.0

BHC Supervision Manual December 2001Page 3

from engaging in any additional activity1 oracquiring control of a company engaged in anyactivity under section 4(k) and 4(n) of the BHCAct if any insured depository institution con-

trolled by the FHC fails to maintain a satisfac-tory or better CRA rating.

3901.0.4 LAWS, REGULATIONS, INTERPRETATIONS, AND ORDERS

Subject Laws 1 Regulations 2 Interpretations 3 Orders

BHCs and foreign banks that qualifyas FHCs can engage in financialactivities and those incidental thereto

1843

Definition of an FHC 225.81 4-056

Election to become an FHC 225.82 4-056.1

Failure to meet applicable capital andmanagement requirements

225.83 4-056.2

Consequences of the failure to main-tain at least a satisfactory CRA rating

225.84 4-056.3

Notices or approvals for FHCs toengage in financial activities

225.85 4-056.4

Activities permissible for FHCs 228.86 4-056.5

Post-commencement notice for FHCto engage in a financial activity

225.87 4-056.6

Board determination that an FHCactivity is financial in nature or inci-dental thereto

225.88 4-056.7

Board approval for an FHC to engagein an activity that is complementary toa financial activity

225.89 4-056.8

1. 12 U.S.C., unless specifically stated otherwise.2. 12 C.F.R., unless specifically stated otherwise.

3. Federal Reserve Regulatory Service reference.

1. With respect to engaging in any additional activities, seesection 225.84 of Regulation Y for the exceptions.

U.S. Bank Holding Companies Operating as Financial Holding Companies 3901.0

BHC Supervision Manual December 2001Page 4

Foreign Banks Operating as Financial HoldingCompanies (Section 4(k) of the BHC Act) Section 3903.0

3903.0.1 FINANCIAL HOLDINGCOMPANY QUALIFICATIONREQUIREMENTS FOR FOREIGNBANKS

A foreign bank that owns or controls a U.S.bank (and any company that controls the foreignbank) must comply with the same requirementsas a domestic bank holding company (BHC)that elects to be treated as a financial holdingcompany (FHC). Either entity is thus able toengage in authorized financial activities underthe Gramm-Leach-Bliley Act (GLB Act). If aforeign bank does not own a subsidiary bank inthe United States, but instead operates through abranch, agency, or commercial lending com-pany located in the United States, the foreignbank (and any company that controls the foreignbank) is subject to the Bank Holding CompanyAct (BHC Act) as if the foreign bank or com-pany were a BHC. Such foreign banks may, likeU.S. BHCs, also elect to be treated as FHCs.Foreign banks electing to be treated as FHCsmust meet ‘‘well-capitalized’’ and ‘‘well-managed’’ standards comparable to those thatare applicable to U.S. depository institutions.Futher, any U.S. branches of the foreign bankthat are FDIC-insured must be rated satisfactoryor better under the Community ReinvestmentAct (CRA).1 (See section 225.90 of RegulationY.)

To be treated as an FHC, a foreign bank (or acompany that owns or controls a foreign bank)that operates in the United States only throughU.S. branches, agencies, or commercial lendingsubsidiaries must file a written declaration withthe appropriate Reserve Bank. This declarationmust contain items 1 through 6 below. Foreignbanks or companies that operate in the UnitedStates through U.S. branches, agencies, or com-mercial lending companies and through a U.S.subsidiary bank are not required to provide item1, but they must provide the items domesticBHCs are to provide.

1. a statement that the foreign bank or companyelects to be treated as an FHC

2. the risk-based capital ratios and the amountsof tier 1 capital and total assets of the foreignbank as of the close of the most recent quar-

ter, and as of the close of the most recentaudited reporting period

3. a certification that the foreign bank meets thestandards to be well capitalized that are setout in section 225.90(b)(1)(i) and (ii) or sec-tion 225.90(b)(2) of Regulation Y, as of thedate the foreign bank or company files itselection

4. a certification that the foreign bank is wellmanaged, as defined in section 225.90(c)(1)of Regulation Y, as of the date the foreignbank or company files its election

5. a certification that all U.S. depository institu-tions controlled by the foreign bank or com-pany (including thrifts and nonbank trustcompanies) are well capitalized and wellmanaged as of the date the foreign bank orcompany files its election

6. the capital ratios and all relevant capital mea-sures (as defined in section 38 of the FederalDeposit Insurance Act) for all U.S. deposi-tory institution subsidiaries of the foreignbank or company as of the end of the previ-ous quarter

The well-capitalized and well-managed tests initems 2, 3, and 4 above apply to each foreignbank that has U.S. operations in the form of abranch, agency, or commercial lending com-pany subsidiary that is part of a foreign bankingorganization seeking certification as an FHC.

For those foreign banks whose home-countrysupervisors have adopted risk-based capital stan-dards consistent with the Basel Accord, theirtier 1 and total risk-based capital ratios, as calcu-lated under the home-country standard, must beat least 6 percent and 10 percent, respectively.The Board will determine the comparability ofthe foreign bank’s capital under the listed com-parability factors in section 225.92(e) of Regula-tion Y. Among these factors are the compositionof the foreign bank’s capital, accounting stan-dards, long-term debt ratings, the ratio of tier 1capital to total assets, reliance on governmentsupport to meet capital requirements, the for-eign bank’s anti–money laundering procedures,whether the foreign bank is subject to compre-hensive consolidated supervision, and other fac-tors that may affect the analysis of capital andmanagement.2 For those foreign banks whose

1. Under the GLB Act, the capital and management stan-dards the Board must apply to foreign banking organizationsthat elect to become FHCs should be comparable to thestandards applied to domestic institutions, giving due regardto the principle of national treatment and equality of competi-tive opportunity.

2. The Board may consider whether the overall level of theforeign bank’s capital and other factors indicate that addi-

BHC Supervision Manual December 2001Page 1

home-country supervisors have not adopted theBasel Accord and for any other foreign bankingorganizations that otherwise do not meet thecapital standards noted above, the foreign bankmay be considered well capitalized by obtainingfrom the Board a prior determination that itscapital is otherwise comparable to the capitalthat would be required of a U.S. banking organi-zation to become an FHC. The pre-clearanceprocess provided by section 225.91(c) of Regu-lation Y can be used to obtain this determina-tion.

A foreign bank will be considered well man-aged if—

1. the branches, agencies, and commercial lend-ing subsidiaries of the foreign bank havereceived at least a satisfactory composite rat-ing at their most recent examination;3

2. the home-country supervisor of the foreignbank consents to the foreign bank expandingits activities in the United States to includeFHC activities;4 and

3. the Board determines that the managementof the foreign bank meets standards compa-rable to those required of a U.S. bank ownedby an FHC.

The Board believes that, as a general rule, thetop tier foreign bank in a foreign banking groupthat requests an FHC determination should besubject to comprehensive consolidated supervi-sion by the home-country supervisor.

As a general matter, a foreign bank will notbe determined to be well capitalized and wellmanaged when it is not subject to comprehen-sive consolidated supervision. When a foreignbank has not been determined by the Board tobe subject to comprehensive consolidated super-vision, and the Board has not deemed any otherbank from the country where the foreign bank ischartered to be subject to comprehensive con-solidated supervision, the foreign bank must usethe pre-clearance process provided by section225.91(c) of Regulation Y—even if it otherwisemeets the objective screening criteria. The Boardmay review a foreign bank’s home-countrysupervision through the pre-clearance processand make a comprehensive consolidated super-vision determination in that context. The Boardwill try to make a determination on pre-clearance requests within 30 days of receipt.5

There may be limited situations when anexceptionally strong bank from a country thathas not yet fully implemented comprehensiveconsolidated supervision should be consideredfor FHC status. Such a foreign bank can qualifyfor FHC status if (1) the home-country supervi-sor has made significant progress in adoptingand implementing arrangements for the consoli-dated supervision of its banks, and (2) the for-eign bank demonstrates significant financialstrength, such as through high levels of capitalor exceptional asset quality. The Board antici-pates, however, that a foreign bank that is notsubject to comprehensive consolidated supervi-sion will be granted FHC status only in rareinstances.

As in the case of domestic BHCs, each U.S.depository institution subsidiary of a foreignbank is required to meet all the well-capitalizedand well-managed standards in order for theforeign bank or company to obtain FHC statusin the same manner as required for U.S. BHCs.In addition, all the U.S. insured depository insti-tutions controlled by the foreign bank or com-pany must be rated satisfactory or better underthe CRA. If the foreign bank operates a U.S.branch that is FDIC-insured, the branch must berated satisfactory or better under the CRA.

tional analysis should be undertaken to assess comparability.The Board will not impose a specific standard for the foreignbank’s ratio of tier 1 capital to total assets (the leverage ratio),but a foreign bank’s leverage ratio may be among the factorstaken into account in the comparability review.

3. The Federal Reserve’s foreign bank examination pro-cess includes the assignment of a combined assessment (thecombined ROCA rating) of a foreign banking organization’s(FBO’s) U.S. branch, agency, and commercial lending opera-tions through the regular examination cycle. (See SR-00-14.)The combined ROCA rating will be factored into the FBO’soverall combined U.S. operations rating, which will continueto be a single composite rating that reflects the U.S. supervi-sors’ collective assessment of all operations (that is, bankingand nonbanking) of the FBO in the United States. If a foreignbank wishes to obtain FHC status, but does not have theassignment of a combined U.S. banking assessment as part ofthe regular examination cycle, the foreign bank can contact itsresponsible Federal Reserve Bank or engage in the pre-clearance process. If a foreign banking group contains morethan one foreign bank with U.S. banking offices, each suchforeign bank in the group must have a satisfactory compositeU.S. banking assessment in order for the foreign bankinggroup or any of its subsidiaries to obtain FHC status.

4. The home-country supervisor should consider the FBO’sconsolidated capital and management before providing itsconsent to the expansion. If the home country has no formalconsent process, the Board will consult with the supervisor toassure itself that the supervisor considers the capital andmanagement of the bank to satisfy its home-country standardsand that the supervisor has no objections to the expansion.

5. If the Board makes an affirmative comprehensive con-solidated supervision determination through the FHC pre-clearance process, the determination will be relied on for theforeign bank to establish additional branches and agenciesunder the Foreign Bank Supervision Enhancement Act.

Foreign Banks Operating as Financial Holding Companies 3903.0

BHC Supervision Manual December 2001Page 2

An election by a foreign bank or company tobe treated as an FHC will become effective onthe thirty-first day after the date that an electionwas received by the appropriate Reserve Bank,unless the Board notifies the foreign bank orcompany before that time that the election isineffective or unless the period for the Board’sdetermination is extended with the consent ofthe foreign bank or company making the elec-tion. The date the Federal Reserve Bank receivesthe declaration should be considered the firstday of the 30-day review period. The Board orthe Reserve Bank also may notify a foreignbank or company in writing that its election tobecome an FHC is effective before the thirty-first day after the election was filed. A foreignbank or company should file the declaration (orpre-clearance request) with the responsibleReserve Bank.

If the election is determined to be effective,the foreign bank or company may engage in thefinancial activities available to FHCs. The GLBAct requires that an FHC that engages in anactivity, or that acquires control or shares of acompany engaged in an activity, under section4(k) of the BHC Act provide written notice tothe appropriate Reserve Bank within 30 calen-dar days after commencing the activities oracquisition.Thenotice shoulddescribe theactivitycommenced or identify the name of the com-pany acquired and describe its activities.

3903.0.2 FOREIGN BANK FAILS TOCONTINUE MEETING FHC CAPITALAND MANAGEMENTREQUIREMENTS

If a foreign bank or company has made aneffective election, and the Board finds that theforeign bank; any foreign bank that is controlledby the foreign bank and maintains a U.S. branch,agency, or commercial lending company; or anyU.S. depository institution owned or controlledby the foreign bank or company ceases to bewell capitalized or well managed, the foreignbank or company must execute an agreementacceptable to the Federal Reserve Board to com-

ply with all applicable capital and managementrequirements. This agreement should be executedwithin 45 days after the Board notifies the for-eign bank or company that it is not in compli-ance with the applicable requirements for anFHC. (See section 225.93 of Regulation Y.) Atthe request of the foreign bank or company, theBoard may extend the 45-day period. (The requestshould state why an extension is necessary.) Theagreement must explain the specific actions thatthe foreign bank or company will take to correctall areas of noncompliance, provide a schedulefor all such actions, provide any other informa-tion the Board may require, and be acceptable tothe Board. During the period of non-compliance, the Board also may impose limita-tions or conditions on the U.S. activities of theforeign bank or company. Section 225.93 ofRegulation Y also sets forth the consequencesof failing to correct the noncompliance within aperiod of 180 days. Such consequences mayinclude termination of the foreign bank’s U.S.branches and agencies and divestiture of itscommercial lending company subsidiaries, orcessation of the expanded activities permittedfor FHCs. The foreign bank may also choose tocease engaging in activities not permitted for aforeign bank under sections 2(h) and 4(c) of theBHC Act.

3903.0.3 INSURED BRANCH FAILSTO MAINTAIN A SATISFACTORY ORBETTER CRA RATING

When an insured branch of a foreign bank, or aninsured depository institution controlled by aforeign bank, fails to maintain a satisfactory orbetter CRA rating, section 225.94 of RegulationY applies the provisions of section 225.84 to theforeign bank and to any company that owns orcontrols the foreign bank. For these purposes,the insured branch is treated as an ‘‘insureddepository institution.’’ An FHC is thus prohib-ited by the Board from engaging in any addi-tional activity or acquiring control of a companyengaged in activities under section 4(k) or 4(n)of the BHC Act.( See section 225.84 of Regula-tion Y.)

Foreign Banks Operating as Financial Holding Companies 3903.0

BHC Supervision Manual December 2001Page 3

3903.0.4 LAWS, REGULATIONS, INTERPRETATIONS, AND ORDERS

Subject Laws 1 Regulations 2 Interpretations 3 Orders

BHCs and foreign banks that qualifyas FHCs can engage in financialactivities and those incidental thereto

1841(h)1843(c)

Election of a foreign bank to becomean FHC

225.91 4-057.2

How elections by foreign banks to bean FHC become effective

225.92 4-057.3

Foreign bank fails to satisfy capitaland management requirements

225.93 4-057.4

Foreign branch fails to retain a satis-factory CRA rating

225.94225.84

4-057.74-056.5

1. 12 U.S.C., unless specifically stated otherwise.2. 12 C.F.R., unless specifically stated otherwise.

3. Federal Reserve Regulatory Service reference.

Foreign Banks Operating as Financial Holding Companies 3903.0

BHC Supervision Manual December 2001Page 4

Permissible Activities for FHCs(Section 4(k) of the BHC Act) Section 3905.0

WHAT’S NEW IN THIS REVISEDSECTION

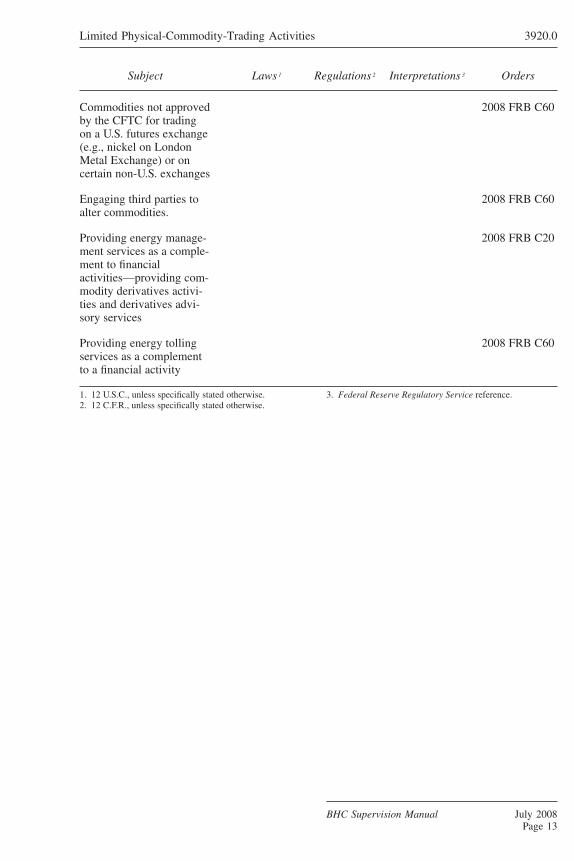

Effective July 2008, this section was revised to

include the Board’s September 7, 2007, determi-

nation, by order, at the FDIC’s request, that

disease management and mail-order pharmacy

activities complement the financial activity of

underwriting and selling health insurance; per-

missible for an FHC under section 4 (k) of the

BHC Act, as amended by the Gramm-Leach-

Bliley (GLB) Act (see 2007 FRB C133). (An

applicant had filed an application with the FDIC

for deposit insurance for a proposed de novo

industrial loan company.) The Board determined

the activities to be financial in nature under

section 4(k) of the BHC Act and complementary

to a financial activity. The Board’s determina-

tion is conditioned and based on the limitations

it placed on the activities in the aggregate (that

is, the specified percentages of the applicants’

consolidated total assets, consolidated total

annual revenues, and total capital).

The section is also amended for the Board’s

approvals of FHC notices, under section 4 of

the BHC Act, to provide energy management

services under energy management agreements

and also, energy tolling. On December 4, 2007,

the Board determined, by order, that an FHC’s

provision of energy management services is

complementary to the financial activities of

engaging as principal in physical commodity

derivatives and the providing of financial and

investment advisory services for derivative trans-

actions. (See 2008 FRB C20.) On March 27,

2008, the Board also determined, by order, that

an FHC’s providing energy tolling is comple-

mentary to the financial activity of engaging in

commodity derivatives activities (see 2008 FRB

60).

The section has been revised to also delete a

reference to an interim Board rule that is final.

See 225.4(g) of Regulation Y (12 C.F.R. 225.4(g)).

This rule pertains to nonbank activities involv-

ing the underwriting and dealing in, or making

a market in, bank-ineligible securities under

section 4(k)(4)(E) of the BHC Act.

3905.0.1 NONBANK ACTIVITYAUTHORIZATIONS FOR FHCS

The Gramm-Leach-Bliley Act (the GLB Act)amended the Bank Holding Company Act (theBHC Act) to allow a BHC or foreign bank thatqualifies as a financial holding company (FHC)

to engage in a broad range of activities that theGLB Act defines as ‘‘financial in nature.’’ Sec-tion 4(k)(4)(A)–(E) of the BHC Act defines thefollowing activities as financial in nature:

1. lending, exchanging, transferring, investingfor others, or safeguarding money orsecurities

2. insuring, guaranteeing, or indemnifyingagainst loss, harm, damage, illness, disabil-ity, or death, or providing and issuing annu-ities, and acting as principal, agent, or brokerfor purposes of the foregoing, in any state

3. providing financial, investment, or economicadvisory services, including advising aninvestment company (as defined in section 3of the Investment Company Act of 1940)

4. issuing or selling instruments representinginterests in pools of assets permissible for abank to hold directly

5. underwriting, dealing in, or making a marketin securities

The Board had previously determined that someof these activities were impermissible for BHCs,such as acting as principal, agent, or broker forpurposes of insuring, guaranteeing, or indemni-fying against loss, harm, damage, illness, dis-ability, or death, and issuing annuity products.Permissible insurance activities as principalinclude reinsuring insurance products.

An FHC acting under section 4(k)(4)(B) ofthe BHC Act may conduct insurance activitieswithout regard to the restrictions on the insur-ance activities imposed on BHCs under section4(c)(8).

Providing claims-administration and risk-

management services. Legal counsel represent-ing an FHC sought an opinion as to whether aninsurance agency owned by an FHC may engagein certain insurance claims activities, as describedbelow, under section 4(k)(4)(B) of the BHCAct. In particular, it was asked whether such aninsurance agency may engage in the followingclaims-administration activities in connectionwith its insurance sales activities: (1) collectinginsurance premiums; (2) holding insurance pre-miums in trust; (3) establishing an insuranceclaims–paying account; (4) adjusting insuranceclaims (which would include obtaining factsabout claims, investigating the veracity of claims,and estimating losses relating to claims);

BHC Supervision Manual July 2008Page 1

(5) negotiating with insureds and their represen-tatives concerning insurance claims; and (6) pay-ing and settling insurance claims. A representa-tion was made that insurance agents typicallyperform these claims-administration services foran insurance underwriter in connection withinsurance policies sold by the agents on behalfof an insurance underwriter.

With respect to the insurance risk-management activities provided in connectionwith insurance sales activities, a legal opinionwas requested as to whether an insurance agencyor broker owned by an FHC could engage in thefollowing activities: (1) assessing the risks of aclient seeking insurance and identifying the cli-ent’s exposures to loss; (2) designing programs,policies, and systems (such as workplace safetyprograms) to reduce the client’s risks; (3) advis-ing clients about risk-management alternativesto insurance (such as self-insurance, securitiza-tion, or derivatives); and (4) negotiating insur-ance coverages, deductibles, and premiums foran insurance client. It was represented thatinsurance agents and brokers provide these risk-management services to their customers in con-nection with the sale of insurance products,including, in particular, commercial propertyand casualty insurance, and other insuranceactivities. It also was understood that the pro-posed risk-management services would (1) berelated to managing insurable risks, (2) be advi-sory in nature, and (3) not allow the risk man-ager to control or perform operations of itsclients.

Board staff noted that most states require aperson performing one or more of the insuranceclaims–administration services listed above tobe licensed by, or registered with, the appropri-ate insurance authority of the state as an insur-ance company, an insurance agent, or a third-partyadministrator (TPA).1 The legislativehistoryof the GLB Act also suggests that the Congress

believed that insurance-related claims-administration services are a necessary part ofthe insurance sales and underwriting activitiesauthorized by section 4(k)(4)(B).2

State insurance laws generally do not requirecompanies that provide insurance risk-management services to obtain a special insur-ance license. However, states generally do requirea license of any person who negotiates insur-ance coverages, deductibles, and premiums foranother.3

In a legal opinion dated July 10, 2002, Boardstaff opined that the specific insurance claims–administration services listed above are encom-passed within the insurance activities authorizedby section 4(k)(4)(B) of the BHC Act and thatthe services may be conducted by an FHC whenthey are provided by an insurance agent orbroker in connection with its other insurancesales activities. In addition, Board staff believesthat the specific insurance risk-management ser-vices listed above are encompassed within sec-tion 4(k)(4)(B) insurance activities and that theservices may be conducted by an FHC if they(1) are provided by an insurance agent or brokerin connection with its other insurance salesactivities, (2) involve managing insurable risks,(3) are advisory in nature, and (4) do not allowthe FHC to control, or perform operations of,the person to whom the services are provided.4

Acting as a third-party administrator. Otherlegal counsel representing a BHC that had electedto become an FHC requested an opinion onwhether acting as a TPA on behalf of an insur-ance company is an activity that is permissiblefor an FHC under the BHC Act. The BHCproposed to invest in a company that acts as aTPA for licensed insurance companies thatunderwrite and sell credit life insurance. A TPAprovides one or more insurance companies withadministrative and related services that supportand assist the sale of insurance products by the

1. For example, the Model Third Party Administrator Stat-ute adopted by the National Association of Insurance Com-missioners (NAIC) requires a person who collects premiumsor adjusts or settles claims for an insurer in connection withthe sale of life or health insurance policies or annuities toregister with the relevant state insurance authority as a TPA ifthe person is not already registered with the state as aninsurance company, agent, or broker. See the NAIC ModelThird Party Administrator Statute, sections 1.A and 11 (1996).

The NAIC’s Model Managing General Agents Act alsorequires a person to register with the relevant state insuranceauthority if the person adjusts or pays claims for an insurerand engages in certain other activities on behalf of an insurer.See NAIC Model Managing General Agents Act, sections 2.Cand 3 (1993).

2. See H.R. Rep. No. 106-74, part I, p. 122 (1999) (‘‘Activitiessuch as administering, marketing, advising or assisting with . .. claim administration or similar programs shall be deemed tobe incidental to insurance activities as described in [section4(k)(4)(B)].’’).

3. See NAIC Producer Licensing Model Act, sections 2.Kand 3 (2000).

4. A BHC or an FHC may provide advice to customersconcerning financial matters, including insurance, self-insurance, securitizations, and derivatives, under 12 C.F.R.225.28(b)(6), and may provide management consulting adviceto customers regarding nonfinancial equity matters, such asworkplace safety, subject to Regulation Y’s limits and restric-tions. See 12 C.F.R. 225.28(b)(9) (management consultingactivities permissible for all bank holding companies) and225.86(b)(1) (management consulting activities permissiblefor all FHCs).

Permissible Activities for FHCs 3905.0

BHC Supervision Manual July 2008Page 2

insurance company. A TPA may provide someor all of the following services to an insurancecompany: (1) assisting the insurance companyin designing its insurance programs (which wouldinclude policy and certificate development andissuance); (2) determining whether a prospec-tive insured meets the insurance company’sestablished underwriting guidelines; (3) collect-ing and processing insurance premiums; (4) pro-cessing, adjudicating, and paying claims onbehalf of the insurance company; (5) investingexcess cash and maintaining bank accounts forthe insurance company; (6) establishing riskreserves for the insurance company; (7) advis-ing on, and arranging for, reinsurance or stop-loss insurance for the insurance company; (8) pre-paring and filing tax returns and regulatoryreports for the insurance company and provid-ing other related services designed to ensurethat the insurance company remains properlylicensed and in compliance with applicable gov-ernment regulations; (9) providing accountingand recordkeeping services to the insurancecompany in connection with its insurance activi-ties; and (10) providing insurance-product salestraining to employees of the insurance company.It was represented that the BHC may engage insome, but not all, of the activities in its capacityas a TPA.

The Board’s staff noted that the activitieslisted above are directly related to the provisionand sale of insurance by a third-party insurancecompany and constitute an integral part of theregulated insurance activities of the third-partyinsurance company. Consequently, most statesrequire a person performing one or more ofthese services for an insurance company to belicensed by, or registered with, the appropriateinsurance authority of the state either as aninsurance company or agent or as a TPA. Inaddition to the previously stated requirements,the Model Third Party Administrator Statute(Model TPA Statute) requires a person to regis-ter as a TPA if the person accepts insurancecontracts for an insurer that meet the insurer’sunderwriting guidelines, assists an insurer in theoverall planning and coordination of its insur-ance program, or collects premiums or adjustsclaims for an insurer.5

In a legal opinion dated July 10, 2002, theBoard staff opined that the above-listed servicesare encompassed within the insurance activitiesauthorized by section 4(k)(4)(B) of the BHCAct when provided to, or on behalf of, an insur-ance company in connection with the sale orunderwriting of insurance. Staff concluded thatan FHC could, under section 4(k)(4)(B) of theBHC Act, provide these services to a third-partyinsurance company.