“The International Financial Crisis: Have the Roles of Finance Changed?”

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“The International Financial Crisis:Have the Roles of Finance Changed?”

OutlineOutline1. Introduction1. Introduction2. The Global Financial 2. The Global Financial Crisis of 2007-2009Crisis of 2007-2009

3. Crisis Prevention, 3. Crisis Prevention, Management and ResolutionManagement and Resolution

4. Recent Regulatory Reforms 4. Recent Regulatory Reforms to Address Systemic Riskto Address Systemic Risk

5. Conclusions5. Conclusions

1. Introduction1. Introduction• Failure to predict the current global financial crisis and to assess the severity of its impact

• Is there a playbook to contain a systemic financial crisis?

• All the crises in the past had major policy mistakes, leading to structural vulnerabilities and systemic risk, and were slow to unfold. They could have been “spotted” in early stages

• What is needed to make a playbook, if there is one, effective?

Why do we care? Output losses and Why do we care? Output losses and fiscal costs are staggering. A fiscal costs are staggering. A

crisis lasts long.crisis lasts long.

2. Global Financial Crisis, 2. Global Financial Crisis, 2007-092007-09

2.1 Policy mistakes behind the 2.1 Policy mistakes behind the crisiscrisis

• Failure of macroeconomic policy, particularly monetary policy, to contain the build up of domestic financial vulnerabilities and systemic risk

• Flaws in financial regulation and supervision

• Weak global financial architecture

IMF, “Initial Lessons of the Crisis for the Global Architecture and the IMF” (February 2009).

Major policy mistakes led to this crisis: rapid credit

growth, housing bubbles, etc.• Bernanke: “The Fed cannot reliably identify bubbles in asset prices…”- “Aftermath: Implications for Monetary Policy,” NBER Working Paper 8992, June 2002

• The Taylor rule ignored: “Getting off Track: How Government Actions and Interventions Caused, Prolonged, and Worsened the Financial Crisis

• Greenspan’s belief that monetary policy should not prick asset price bubbles, but should respond to the bursting of the bubble to mitigate its negative impact

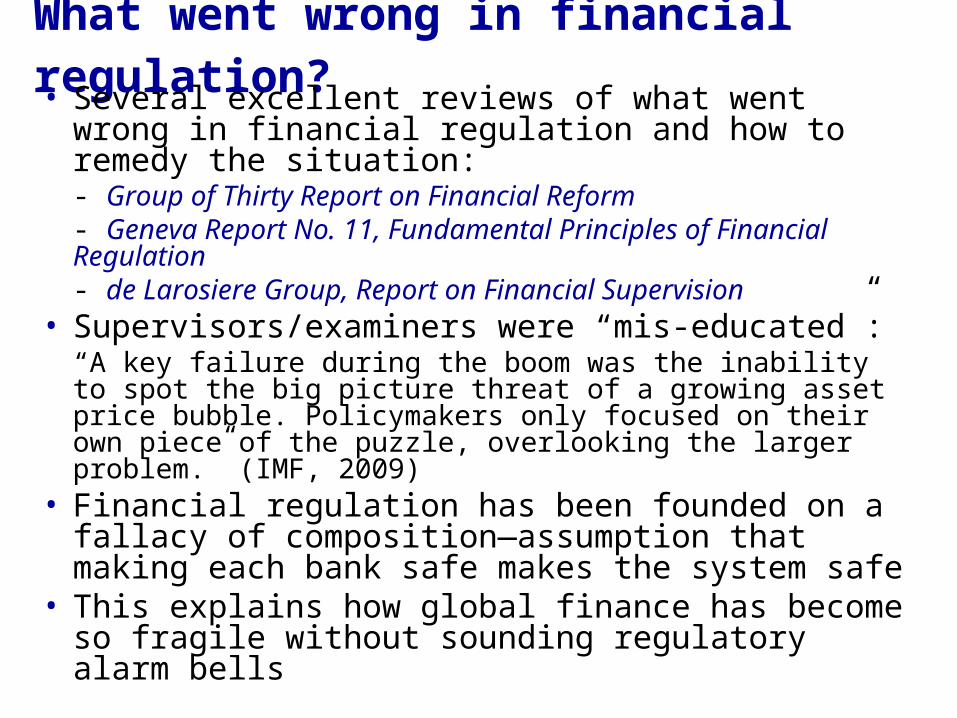

What went wrong in financial regulation? • Several excellent reviews of what went

wrong in financial regulation and how to remedy the situation: - Group of Thirty Report on Financial Reform - Geneva Report No. 11, Fundamental Principles of Financial Regulation- de Larosiere Group, Report on Financial Supervision

• Supervisors/examiners were “mis-educated”:“A key failure during the boom was the inability to spot the big picture threat of a growing asset price bubble. Policymakers only focused on their own piece of the puzzle, overlooking the larger problem.” (IMF, 2009)

• Financial regulation has been founded on a fallacy of composition—assumption that making each bank safe makes the system safe

• This explains how global finance has become so fragile without sounding regulatory alarm bells

Weak global financial architecture

• Failure of global institutions (IMF, BIS, FSF) to conduct effective macro-financial surveillance of systemically important economies (US, UK, the euro zone) and provide compelling warnings

• The discussion of “global payments imbalances” diverting attention away from the build up of US domestic financial vulnerabilities (towards China’s exchange rate policy)

• Ineffectiveness of fragmented international arrangements for regulation and supervision (and resolution) of internationally active financial institutions and markets

2.2 Crisis management not always 2.2 Crisis management not always effectiveeffective

• Collapse of Lehman Brothers• Troubled Asset Relief Program (TARP)• Blanket protection of deposits and guarantees of interbank loans

• Asset stress tests of US financial institutions

• Public-Private Investment Program (PPIP)2.3 Consequences of crisis2.3 Consequences of crisis • Financial sector impact• Output and employment losses• Central bank balance sheets• Fiscal costs• Moral hazard issues

3. Crisis Prevention, 3. Crisis Prevention, Management and ResolutionManagement and Resolution

3.1 Containing systemic risk3.1 Containing systemic risk• Systemic risk: the potential for an event or shock triggering a loss of economic value or confidence in a substantial portion of the financial system (through contagion effects), with resulting major adverse effects on the real economy

• The strategy to contain systemic risk involves oversight of the financial system as a whole, and not just its individual components, as potential events or shocks can affect the economy as a whole

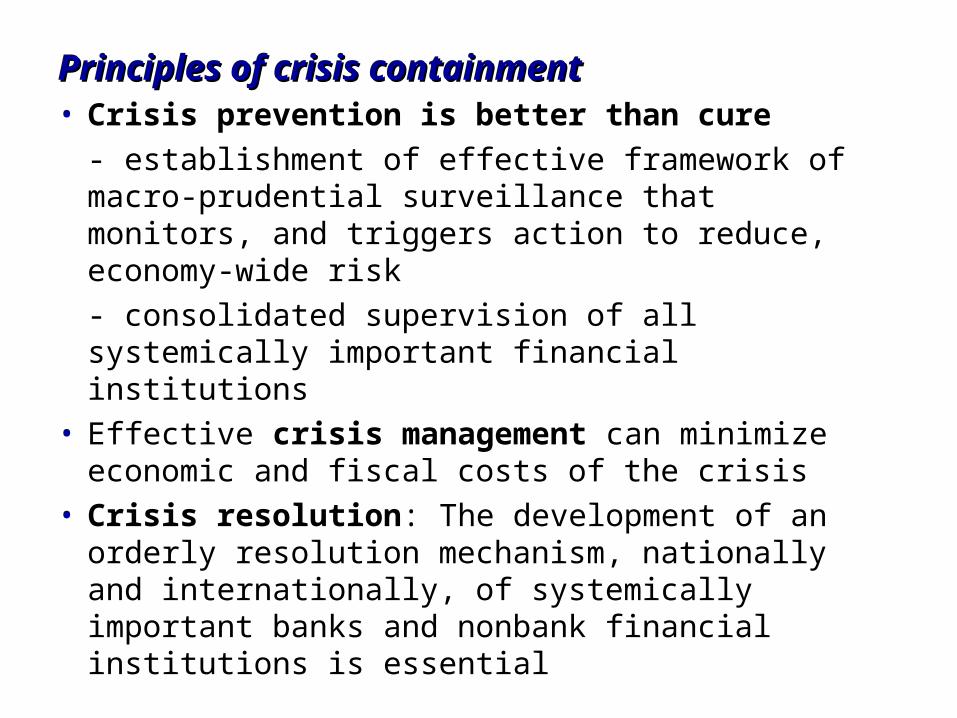

Principles of crisis containmentPrinciples of crisis containment• Crisis prevention is better than cure- establishment of effective framework of macro-prudential surveillance that monitors, and triggers action to reduce, economy-wide risk- consolidated supervision of all systemically important financial institutions

• Effective crisis management can minimize economic and fiscal costs of the crisis

• Crisis resolution: The development of an orderly resolution mechanism, nationally and internationally, of systemically important banks and nonbank financial institutions is essential

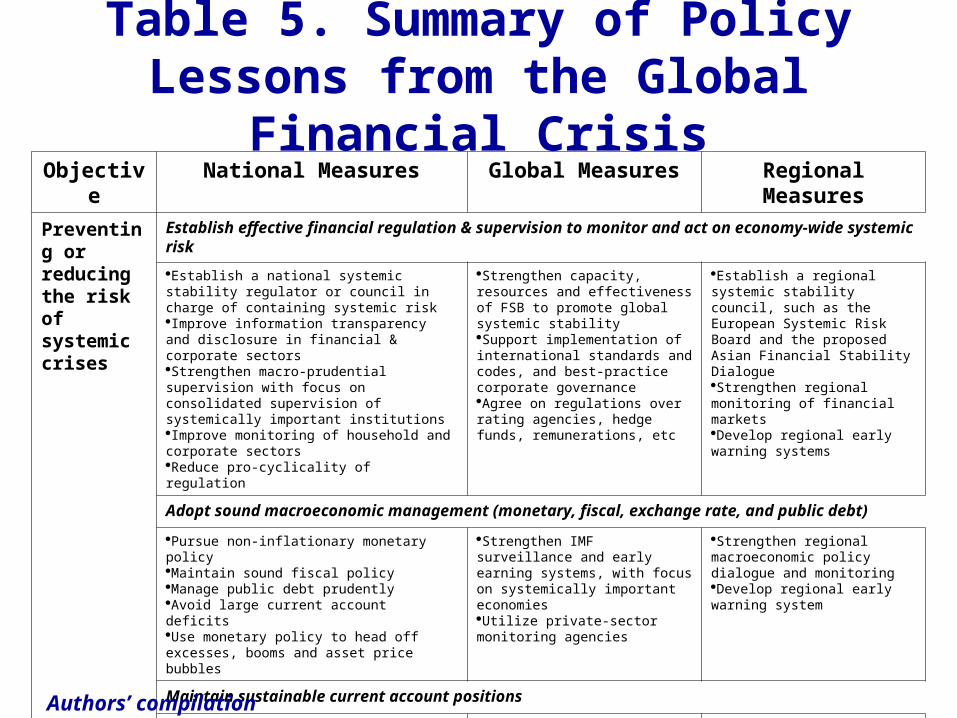

Table 5. Summary of Policy Lessons from the Global

Financial CrisisObjectiv

eNational Measures Global Measures Regional

MeasuresPreventing or reducing the risk of systemic crises

Establish effective financial regulation & supervision to monitor and act on economy-wide systemic riskEstablish a national systemic stability regulator or council in charge of containing systemic riskImprove information transparency and disclosure in financial & corporate sectorsStrengthen macro-prudential supervision with focus on consolidated supervision of systemically important institutionsImprove monitoring of household and corporate sectorsReduce pro-cyclicality of regulation

Strengthen capacity, resources and effectiveness of FSB to promote global systemic stabilitySupport implementation of international standards and codes, and best-practice corporate governanceAgree on regulations over rating agencies, hedge funds, remunerations, etc

Establish a regional systemic stability council, such as the European Systemic Risk Board and the proposed Asian Financial Stability DialogueStrengthen regional monitoring of financial marketsDevelop regional early warning systems

Adopt sound macroeconomic management (monetary, fiscal, exchange rate, and public debt)Pursue non-inflationary monetary policyMaintain sound fiscal policyManage public debt prudentlyAvoid large current account deficitsUse monetary policy to head off excesses, booms and asset price bubbles

Strengthen IMF surveillance and early earning systems, with focus on systemically important economiesUtilize private-sector monitoring agencies

Strengthen regional macroeconomic policy dialogue and monitoringDevelop regional early warning system

Maintain sustainable current account positionsAvoid excessive currency overvaluationAvoid persistent current account deficits and heavy reliance on ST capital inflows

Coordinate policies to avoid unsustainable global payments imbalances

Expand regional demand where savings rates are exceptionally high

Authors’ compilation

Table 5. (continued)Managing crises

Provide timely liquidity of sufficient magnitudeRestore market confidence through consistent policy packagesReduce moral hazard problems

Strengthen IMF liquidity support, including the new Flexible Credit Line

Strengthen a regional liquidity support facility to contain crises and contagion

Support the financial sector within a consistent frameworkExtend guarantees of bank obligationsConduct stress tests to identify losses and capital needs of financial institutionsEstablish a consistent framework for NPL removal and recapitalization

Establish a common international rule for public sector interventions in the distressed financial systemAvoid financial protectionism

Harmonize national interventions in the financial system—such as bank deposit guarantees—at the regional level

Adopt appropriate macroeconomic policies to mitigate the adverse feedback loop between financial and real sectorsAdopt an appropriate monetary and fiscal policy mix contingent on the specific conditions of the economyBe prepared for extraordinary policies

Streamline IMF conditionalityDesign international fiscal support programs for fiscally constrained economies

Strengthen regional capacity to formulate conditionality Create regional fiscal support systems

Resolving systemic crises

Establish frameworks for resolving financial institutions’ impaired assets and corporate & household debt Establish frameworks for resolving bad assets of financial institutions Introduce legal and out-of-court procedures for corporate debt workouts

Harmonize national frameworks for resolving bad assets of financial institutionsProvide international support

Finance regional programs to help accelerate bank and corporate restructuring

Introduce rules for exit of non-viable financial institutionsEstablish clear procedures for exits of financial institutions, and rehabilitation Establish legal & formal procedures for corporate insolvencies and workouts

Harmonize national resolution regimes for non-viable financial institutions

Harmonize insolvency procedures by adopting good practices

Introduce international insolvency mechanisms for resolving internationally active fin. institutionsStrengthen national insolvency procedures of banks, non-bank financial institutions and corporations

Introduce international procedures for cross-border insolvencies

Develop regional insolvency procedures to support the global effort

3.2 Crisis prevention3.2 Crisis prevention• Establish effective financial regulation and supervision to monitor and act on economy-wide systemic risk- focus on not only financial institutions, but also corporations and households (and their links with the financial system)

• Adopt sound macroeconomic management (monetary, fiscal, exchange rate, and public debt)- be ready to use monetary policy to reduce macro-financial instability

• Maintain sustainable current account position

Macro-prudential surveillance• A methodology that aims to preserve systemic financial stability by identifying vulnerabilities in a country’s financial system and triggering policy and regulatory actions in a timely and informed manner to prevent crises from occurring

• The focus is the system and therefore includes corporations and households, and does not rule out contained failures of individual institutions

• It is a “top-down” approach that focuses on the environment (e.g., macroeconomic, regulatory, legal) in which financial systems operate and helps assess sources of risks and incentives

• Micro-prudential supervision is a “bottoms-up” approach that focuses on the health and stability of individual institutions

3.3 Crisis management3.3 Crisis management• Provide timely liquidity of sufficient magnitude (to individual institutions and the market)

• Support the financial sector within a consistent framework of supporting viable institutions (NPL removal, recapitalization, etc.) and allowing exit of nonviable institutions

• Adopt appropriate macroeconomic policies to mitigate the adverse feedback loop between the financial system and the real sector

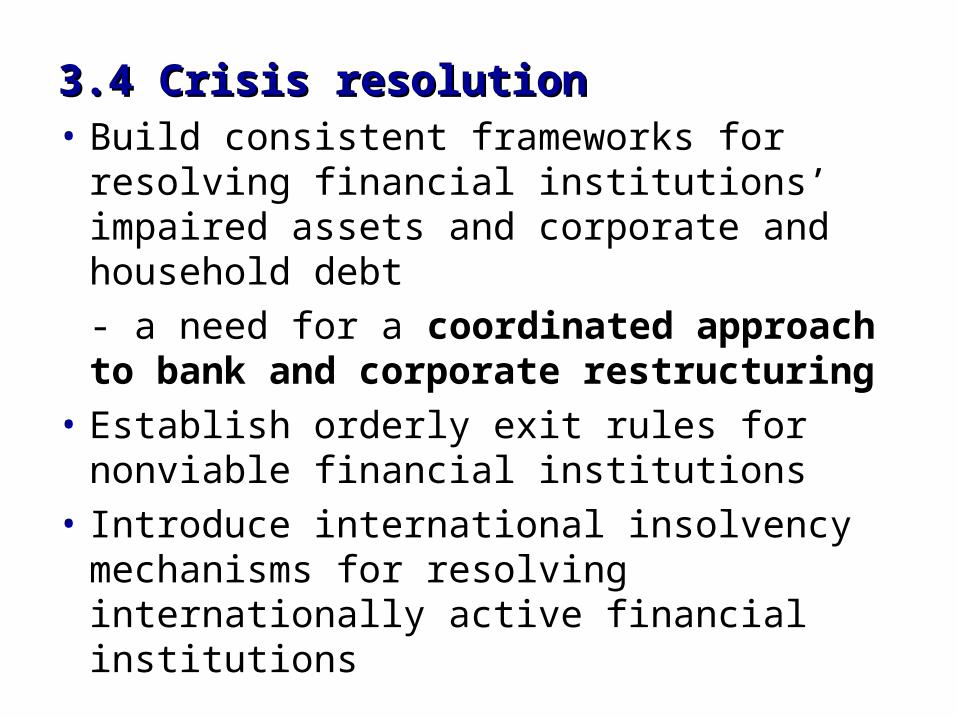

3.4 Crisis resolution3.4 Crisis resolution• Build consistent frameworks for resolving financial institutions’ impaired assets and corporate and household debt- a need for a coordinated approach to bank and corporate restructuring

• Establish orderly exit rules for nonviable financial institutions

• Introduce international insolvency mechanisms for resolving internationally active financial institutions

3.5 Systemic stability regulator3.5 Systemic stability regulator• Clear regulatory objectives and mandates (crisis prevention, management and resolution)

• Effective regulatory structure (a single agency vs. a council)

• Sufficient regulatory resources (political backing, and legal, human and financial resources)

• Effective regulatory implementation (instruments and tools)

Clear objectives and mandates of a systemic stability regulator• Monitoring systemic risks—such as large or growing

credit exposure to real estate—across firms and markets

• Assessing the potential for deficiencies in risk-management practices, broad-based increases in financial leverage, or changes in financial markets/products, creating systemic risk

• Analyzing possible spillovers between financial firms or between firms and markets—for example through the mutual exposures of highly interconnected firms

• Identifying possible regulatory gaps, including gaps in the protection of consumers and investors, that pose risks for the system as a whole

• Curtailing systemic risks across the entire financial system—through legislative action, prudential measures, advising on monetary policy, intervention in individual institutions

• Issuing periodic reports on the stability of the financial system

Effective organization of a systemic stability

regulator• Independent, credible and transparent- Nick Stern: “Any forthright, disinterested assessment of the global economic system’s stability requires two sorts of independence.. must not have anything other than its own reputation riding on its assessment… It must be independent of the G-7.”-The systemic stability regulator should complement, not displace, micro-prudential supervision

• A single agency approach- a fully consolidated model (Singapore, pre-1998 Japan)- a central bank-led model- a new national agency in charge of systemic stability

• A “council” approach: a coordinated framework with the central bank, financial regulator(s) and supervisor(s), and finance ministry, supported by a powerful working group

Sufficient regulatory resources to fulfill responsibilities• Adequate authority and powers backed up

by legal and legislative support • Staffing

– Requires knowledge and experience across a wide range of financial institutions and markets to offer a comprehensive and multi-faceted approach to systemic risk

– Substantial analytical resources to identify the types of information needed and to analyze the information obtained, and

– Supervisory expertise to develop and implement the necessary supervisory response

• Broad authority to obtain information– Rely on the information, assessments, and supervisory and regulatory programs of existing financial supervisors and regulators whenever possible; however,

– Broad authority to obtain information—through data collection and reports, or when necessary, examinations—from a range of financial market participants, including banking organizations, securities firms, and key financial market intermediaries

Effective implementation by a systemic stability regulator• Macro-prudential measures - Warnings of signs of built-up vulnerabilities- Sector targeted tools (tightening loan and underwriting standards, limiting loan-to-value ratios, limiting debt-to-income ratios)- Stress tests- Higher capital ratios and provisioning

• Monetary policy as a last-resort tool against a build up of systemic risk through the market (in a non-inflationary environment)

• Legislative initiatives such as insolvency regimes for non-viable banks and nonbank financial institutions

Stress testing & scenario analysis• Stress testing is a technique to assess the vulnerability of the financial system (and macro “top-down” on the entire economic system) to exceptional but plausible shocks

• Stress tests impose a coherent structure in which to discuss risks and can add rigor to systemic analyses

4. Recent Regulatory 4. Recent Regulatory Reforms to Address Systemic Reforms to Address Systemic

RiskRisk4.1 Global financial architecture4.1 Global financial architecture• With sweeping mandates, can the FSB be effective?- weak political commitments by the G20 to make the FSB a credible and powerful global institution- lack of capacity to provide “high-powered” analytical surveillance

• What can be done to make the FSB effective?- need for a full support by the US & UK in expanding the number of experts, providing independent assessment, and compelling member countries to take necessary actions

Financial Stability Board: Mandate • Assess vulnerabilities affecting the financial

system; • Identify and oversee action needed to address them;

• Promote coordination and information exchange among authorities responsible for financial stability;

• Monitor and advise on market developments and their implications for regulatory policy;

• Advise on and monitor best practice in meeting regulatory standards;

• Undertake joint strategic reviews of the policy development work of the international standards setting bodies;

• Set guidelines for and support the establishment of supervisory colleges;

• Manage contingency planning for cross-border crisis management; and

• Collaborate with the IMF to conduct Early Warning Exercises

4.2 National efforts to 4.2 National efforts to establish a systemic establish a systemic stability regulatorstability regulatorUS stability reform plan

• The Federal Reserve would become the nation’s most powerful financial overseer.

• The Fed would win power to monitor risks across the financial system, and sweeping authority to examine any firm that could threaten financial stability, even if the Fed wouldn't normally supervise the institution.

• The nation’s systemically important financial institutions (“Tier 1 institutions”), whether or not they are banks in the old-fashioned sense, will be more tightly regulated by the Fed.

• A proposed “rapid resolution plan” requires systemically important financial companies to regularly file a “funeral plan”: a set of instructions for how the institution could be quickly dismantled should the need to do so arise.

• A new insolvency regime will cover all such firms, modeled on the scheme run by the FDIC for ordinary banks

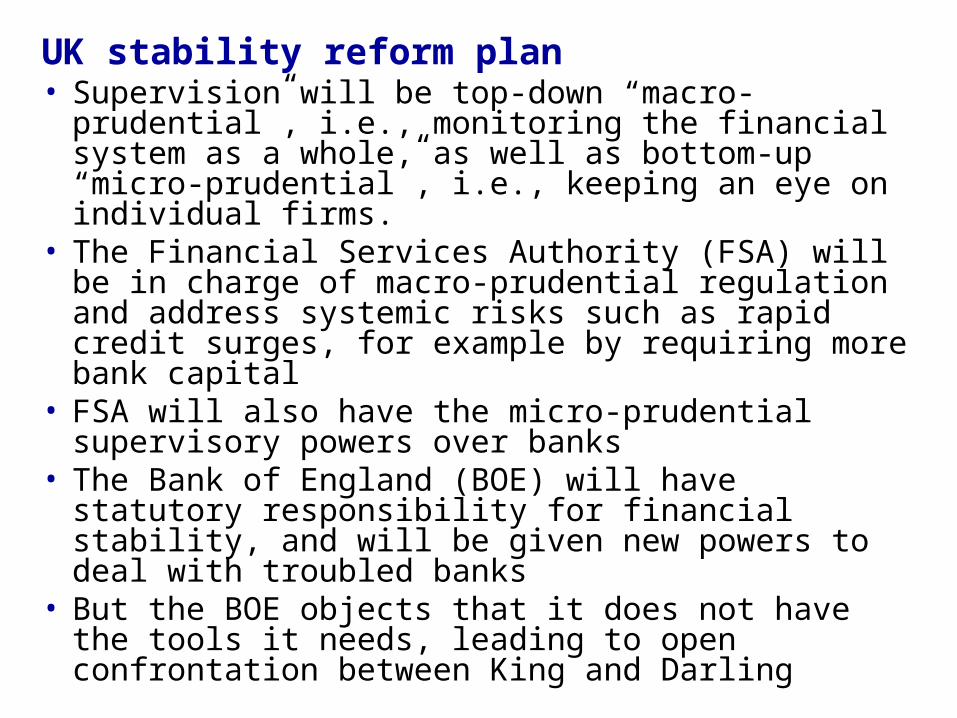

UK stability reform plan• Supervision will be top-down “macro-prudential”, i.e., monitoring the financial system as a whole, as well as bottom-up “micro-prudential”, i.e., keeping an eye on individual firms.

• The Financial Services Authority (FSA) will be in charge of macro-prudential regulation and address systemic risks such as rapid credit surges, for example by requiring more bank capital

• FSA will also have the micro-prudential supervisory powers over banks

• The Bank of England (BOE) will have statutory responsibility for financial stability, and will be given new powers to deal with troubled banks

• But the BOE objects that it does not have the tools it needs, leading to open confrontation between King and Darling

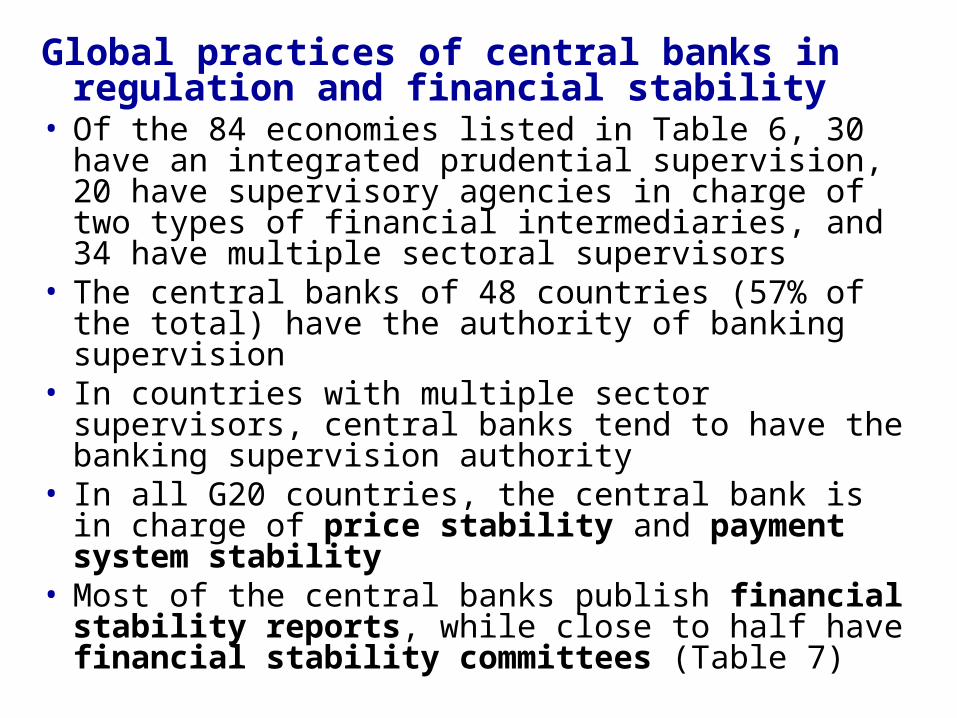

Global practices of central banks in regulation and financial stability

• Of the 84 economies listed in Table 6, 30 have an integrated prudential supervision, 20 have supervisory agencies in charge of two types of financial intermediaries, and 34 have multiple sectoral supervisors

• The central banks of 48 countries (57% of the total) have the authority of banking supervision

• In countries with multiple sector supervisors, central banks tend to have the banking supervision authority

• In all G20 countries, the central bank is in charge of price stability and payment system stability

• Most of the central banks publish financial stability reports, while close to half have financial stability committees (Table 7)

Table 6. Economies with Single, Semi-Integrated, and

Sectoral Prudential Supervisory Agencies, 2009 Single Prudential

Supervisorfor the Financial System(year of establishment)

Agency Supervising Two Types of

Intermediaries

Multiple Sectoral

Supervisors(at least one each for banks, securities firms

& insurers)

Banks and

securities

firms

Banks and insurers

Securities firms

and insurers

Australia (1998)Austria (2002)Bahrain* (2002)Belgium (2004)Bermuda* (2002)Cayman Islands*

(1997)Denmark (1988)Estonia (1999)Germany (2002)Gibraltar (1989)Guernsey (1988)Hungary (2002)Iceland (1988)Ireland* (2002)Japan (2001)Kazakhstan* (1998)Korea, Rep. (1997)Latvia (1998)Maldives* (1998)

Malta* (2002)Netherlands* (2004)Nicaragua* (1999)Norway (1986)Singapore* (1984)South Africa* (1990)Sweden (1991)Taipei,China (2004)United Arab Emirates*

(2000)United Kingdom (1997)Uruguay (1993)Total - 30

FinlandLuxembour

gMexicoSwitzerla

ndUruguayTotal - 5

CanadaColumbiaEcuadorEl SalvadorGuatemalaMalaysia*PeruVenezuela,

Rep. Bolivariana de

Total - 8

BoliviaBulgaria*ChileJamaica*Mauritius*Slovak

Rep.* (b)

Ukraine*Total - 7

Albania*Argentina*Bahamas, The*Barbados*Botswana*Brazil*Croatia*Cyprus*Czech

Republic (b)

Dominican Rep*

Egypt*France *Greece *Hong Kong SAR

*India *Indonesia *Israel *Italy *Jordan*

Lithuania*New

Zealand*

PanamaPhilippine

s*People’s

Republic of China (PRC)

Poland*Portugal*Russia*Slovenia*Sri Lanka*Spain *Thailand *Tunisia *Uganda *United

States *

Total - 34

Table 7: Mandates for the Major Central Banks

De jure independenc

e

Price stability

Financial system stability

Payment system

regulation &

supervision

Regulation and supervision of Macro

prudential

surveillance

Financial

stability

committee

Financial system

stability analysis/repor

tCountry/Region

Banking

Securities

Insurance

Argentina Yes Yes Yes Yes -- -- --- -- YesAustralia Yes Yes Yes -- -- -- -- Yes YesBrazil Yes Yes Yes Yes Yes -- -- -- YesCanada No Yes Yes -- -- -- -- -- YesChina (PRC) No Yes Yes -- -- -- -- Yes YesEuro Zone Yes Yes Yes -- -- -- -- Yes**** YesHong Kong No Yes Yes Yes -- -- -- Yes**** YesIndia No Yes Yes Yes Yes Yes -- Yes*** YesIndonesia Yes Yes Yes Yes -- -- -- -- YesJapan Yes Yes Yes Yes* -- -- -- -- YesMalaysia No Yes Yes Yes Yes Yes -- -- YesMexico Yes Yes Yes -- -- -- -- -- YesPhilippines Yes Yes Yes Yes -- -- -- Yes --Russia Yes Yes Yes Yes -- -- -- Yes**** --Saudi Arabia No Yes Yes Yes Yes Yes Yes Yes YesSingapore No Yes Yes Yes Yes Yes Yes Yes YesSouth Africa Yes Yes Yes Yes -- -- -- -- YesSouth Korea Yes Yes Yes -- -- -- -- -- YesSwitzerland Yes Yes Yes Yes** Yes** -- -- -- YesThailand No Yes Yes Yes Yes Yes -- Yes*** --Turkey Yes Yes Yes -- -- -- -- -- YesUnited

Kingdom Yes Yes Yes -- -- -- -- Yes YesUnited

States Yes Yes Yes Yes -- -- -- Yes**** --

The “council” approach to systemic stability regulation

• US, UK and Japan: possible to expand the existing framework of crisis management to broader crisis containment, including crisis prevention

• UK government’s proposal to create a “Council for Financial Stability” to bring together the BOE, FSA and HM Treasury

• Australia: Council of Financial Regulators, with RBA as chair, APRA, ASIC and Treasury

• Korea: Financial policy coordination by the Finance Ministry as chair, BOE and Financial Supervisory Commission

• For the council approach to be successful, it needs- clear mandates and division of labor- analytical resources and capacity collectively- all the necessary macro-prudential tools

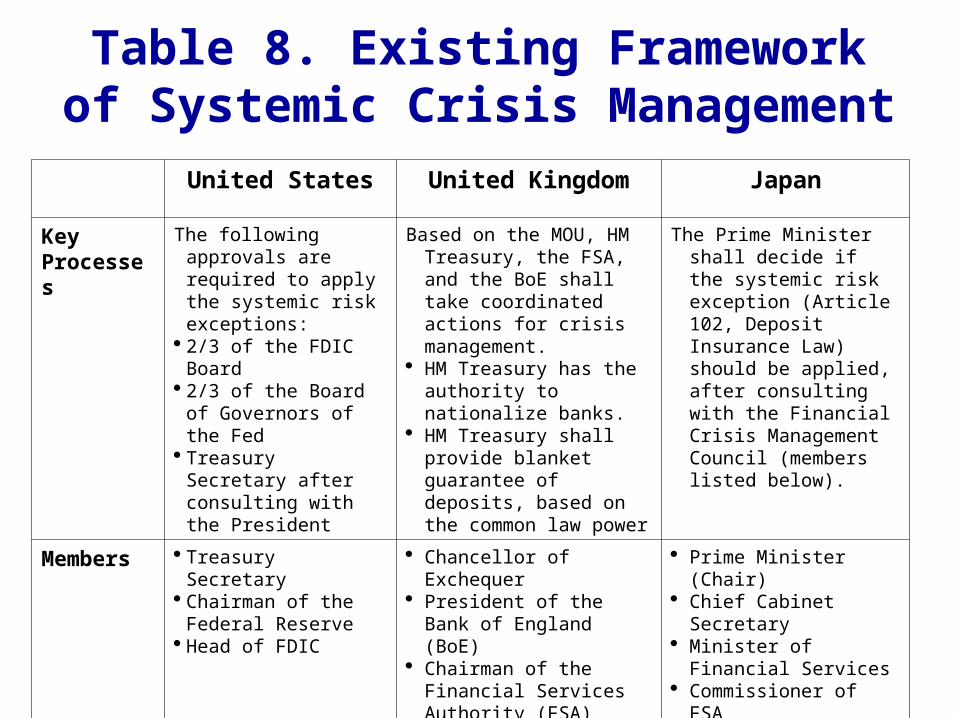

Table 8. Existing Framework of Systemic Crisis Management

United States United Kingdom Japan

Key Processes

The following approvals are required to apply the systemic risk exceptions:

2/3 of the FDIC Board

2/3 of the Board of Governors of the Fed

Treasury Secretary after consulting with the President

Based on the MOU, HM Treasury, the FSA, and the BoE shall take coordinated actions for crisis management.

HM Treasury has the authority to nationalize banks.

HM Treasury shall provide blanket guarantee of deposits, based on the common law power

The Prime Minister shall decide if the systemic risk exception (Article 102, Deposit Insurance Law) should be applied, after consulting with the Financial Crisis Management Council (members listed below).

Members Treasury Secretary

Chairman of the Federal Reserve

Head of FDIC

Chancellor of Exchequer

President of the Bank of England (BoE)

Chairman of the Financial Services Authority (FSA)

Prime Minister (Chair)

Chief Cabinet Secretary

Minister of Financial Services

Commissioner of FSA

Minister of Finance

Governor of the BOJ

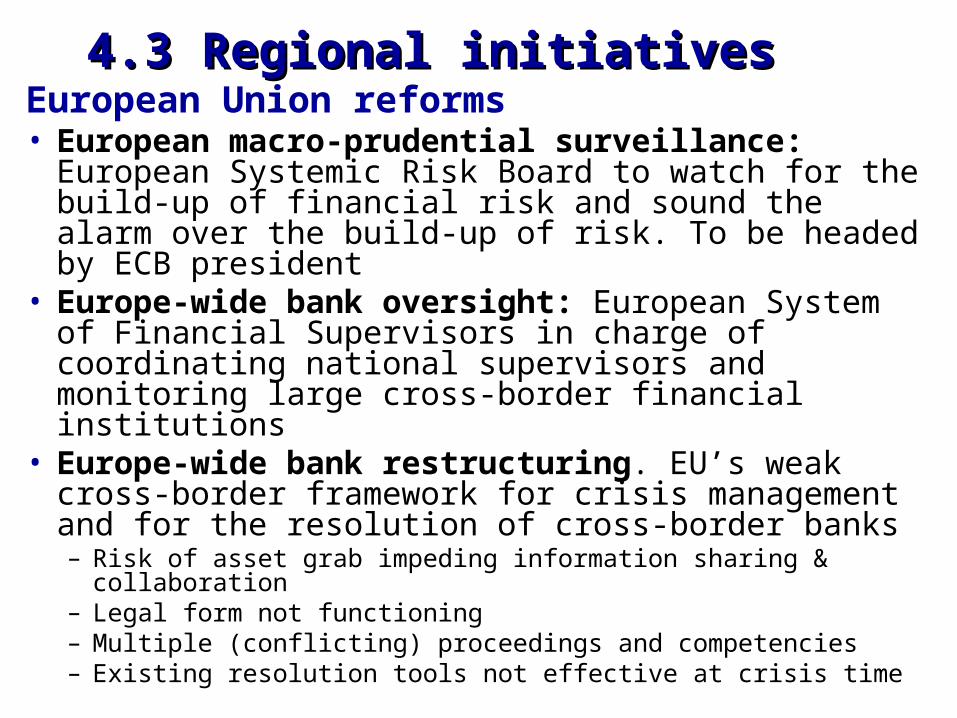

4.3 Regional initiatives4.3 Regional initiativesEuropean Union reforms• European macro-prudential surveillance: European Systemic Risk Board to watch for the build-up of financial risk and sound the alarm over the build-up of risk. To be headed by ECB president

• Europe-wide bank oversight: European System of Financial Supervisors in charge of coordinating national supervisors and monitoring large cross-border financial institutions

• Europe-wide bank restructuring. EU’s weak cross-border framework for crisis management and for the resolution of cross‐border banks – Risk of asset grab impeding information sharing & collaboration

– Legal form not functioning– Multiple (conflicting) proceedings and competencies– Existing resolution tools not effective at crisis time

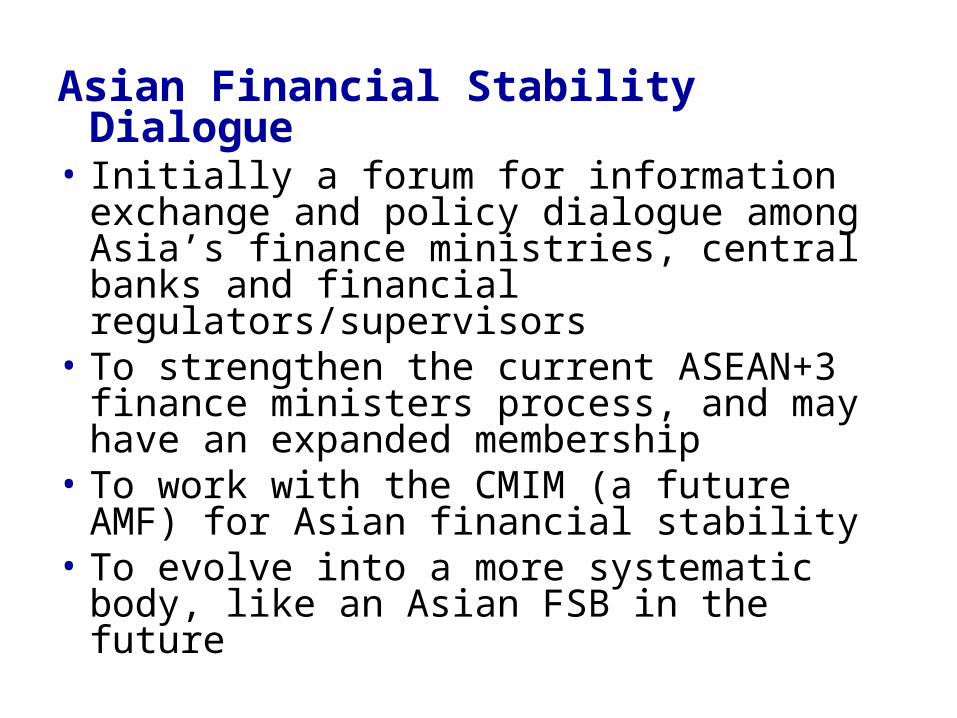

Asian Financial Stability Dialogue

• Initially a forum for information exchange and policy dialogue among Asia’s finance ministries, central banks and financial regulators/supervisors

• To strengthen the current ASEAN+3 finance ministers process, and may have an expanded membership

• To work with the CMIM (a future AMF) for Asian financial stability

• To evolve into a more systematic body, like an Asian FSB in the future

4.4 An international 4.4 An international framework for the 21framework for the 21stst

centurycenturyWho is going to do the heavy-lifting?• The present voluntary cooperative efforts at the international level are not adequate

• The FSF (FSB) and IMF have done little more than issue statements of principles since the start of the crisis

• The Westphalian principles governing international financial oversight (sovereignty of states) are not suited to address today’s global financial system

• The international financial community needs to make progress with a binding global financial order.

5. Conclusions5. Conclusions• A playbook to contain a systemic financial crisis does exist

• The best way is to prevent a crisis by identifying and acting on sources of instability

• A systemic stability regulator should be created at the national and regional levels, and support the global efforts

• For effective crisis management and resolution, there is a need to create a binding cross-border resolution regime for internationally active financial institutions

• The US and the UK need to commit themselves to effective financial stability regulation

For More Information:For More Information:Dr. Masahiro Kawai

Dean & CEO Asian Development Bank

[email protected] +81 3 3593 5527www.adbi.org

Related Documents