INTRODUCTION Finance is regarded as “THE LIFE BLOOD OF BUSINESS ENTERPRISE”. Finance function has become so impo rtant that it h as given bi rth to finan cia l man age ment as a separa te subj ect . So, this sub jec t is acquiring univ ersal applicabilit y. Financial Man agement is that managerial activity which is concerned with the planning and controlling of the firm’s financial resources. As a separate activity or dis cipline is of recent origin it was a branch of economics til l 1890. Still today it has n o unique knowled ge of its own, and it draws heavily on economy for its theoretical concepts. The subj ec t of fi nanc ia l mana ge ment is of immens e inte res t to both ac ad emic ia ns an d practi ci ng ma nag ers . It is of gre at in terest to aca demicians bec ause the sub jec t is still dev elo pin g, and the re are still certain areas where controversies exist for which no unanimous solutions have been reached as yet. Practicing Managers a re interested in t his subject because among the most crucial decisions of the firm are those which relate

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 1/38

INTRODUCTION

Finance is regarded as “THE LIFE BLOOD OF BUSINESS

ENTERPRISE”. Finance function has become so important that it has given

birth to financial management as a separate subject. So, this subject is

acquiring universal applicability. Financial Management is that managerial

activity which is concerned with the planning and controlling of the firm’s

financial resources. As a separate activity or discipline is of recent origin it

was a branch of economics till 1890. Still today it has no unique knowledge

of its own, and it draws heavily on economy for its theoretical concepts.

The subject of financial management is of immense interest to both

academicians and practicing managers. It is of great interest to

academicians because the subject is still developing, and there are still

certain areas where controversies exist for which no unanimous solutions

have been reached as yet. Practicing Managers are interested in this subject

because among the most crucial decisions of the firm are those which relate

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 2/38

to finance and an understanding of the theory of financial management

provides them with conceptual and analytical insights.

Scope of Finance Management:

Firms create manufacturing capacities for production for goods; some

provide services to customers. They sell their goods or services to earn

profits. They raise funds to acquire manufacturing and other facilities.

Thus, the three most important activities of a business firm are:

Production

Marketing

Finance

A firm secures whatever capital it needs and employees it

(finance activity) in activities that generate returns on invested capital

(production and marketing activities). A business firm thus is an entity

that engages in activities to perform the functions of finance, production

and marketing. The raising of capital funds and using them for

generating returns to the supplies of funds is called the finance function

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 3/38

of the firm.

FUNCTION OF FINANCIAL MANAGEMENT

Two significant contribution to the development of modern theory of

financial management are:

Theory of Portfolio Management developed by Harry Markowitz in

1950, which deals with portfolio selection with risky investment. This

theory uses statistical concepts to quantify the risk-return

characteristics of holding a group/portfolio of securities, investment or

assets.

The theory of Leverage and Valuation of Fire developed by

Modigliani and Miller in 1958. They have shown by introducing

analytical approach as to how the financial decision making in any

firm be oriented towards maximization of the value of the firm and the

maximization of the shareholders wealth.

Type of Financial Actions:

1. The Financial Management of trading or manufacturing firms

2. Financial Management of Financial Institutions.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 4/38

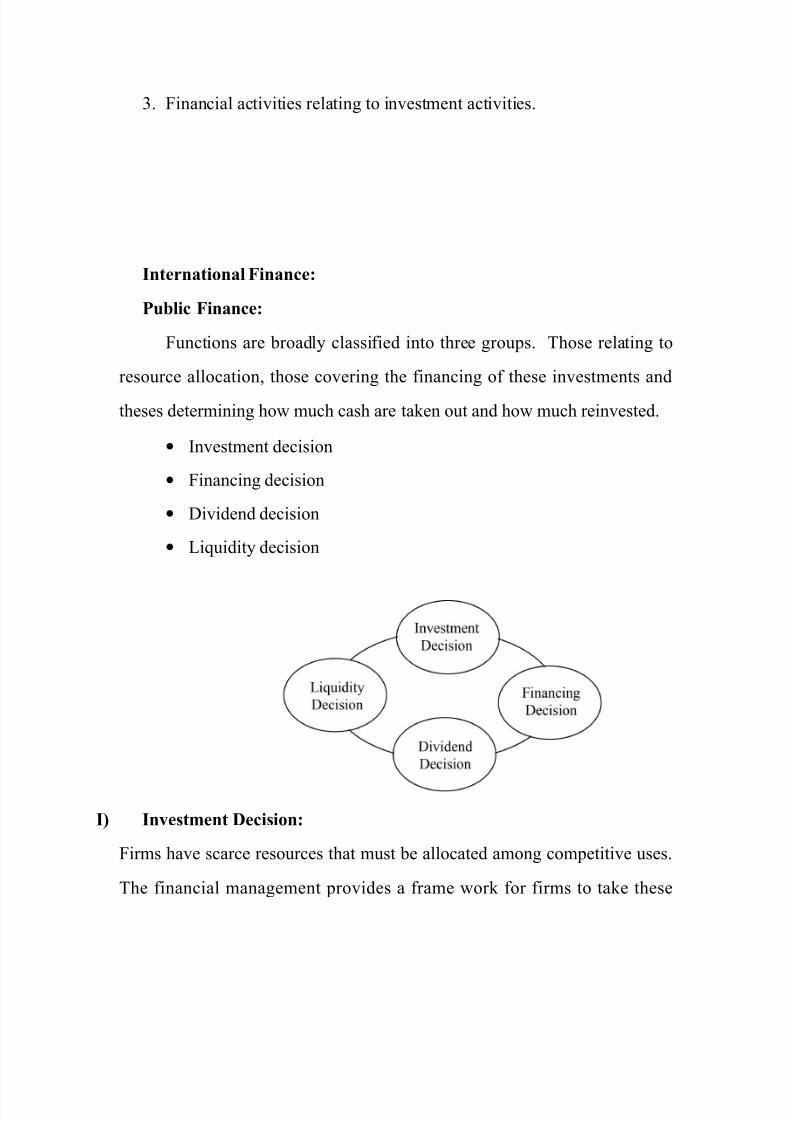

3. Financial activities relating to investment activities.

International Finance:

Public Finance:

Functions are broadly classified into three groups. Those relating to

resource allocation, those covering the financing of these investments and

theses determining how much cash are taken out and how much reinvested.

• Investment decision

• Financing decision

• Dividend decision

• Liquidity decision

I) Investment Decision:

Firms have scarce resources that must be allocated among competitive uses.

The financial management provides a frame work for firms to take these

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 5/38

decisions wisely. The investment decisions include not only those that

create revenues and profits (e.g. introducing a new product line) but also

those that save money.

So, the investment decisions are the decisions relating to assets composition

of the firm. Assets can be classified into fixed assets and current assets, and

therefore the investment decisions can also be bifurcated into Capital

Budgeting decisions and the Working Capital Management.

The Capital Budgeting decisions are more crucial for

any firm. A finance manager may be asked to decide about.

1. Which asset should be purchased out of different alternative options;

2. To buy an asset or to get it on lease;

3. To produce a part of the final product or to procure it from some other

supplier;

4. To by or not an other firm as a running concern;

5. Proposal of merger of other group firms to avail the synergies of consolidation.

Working Capital Management, on the other hand, deals with the

Management of current assets of the firm. Though the current assets do not

contribute directly to the earnings, yet their existence is necessitated for the

proper, efficient and optimum utilization of fixed assets. There are dangers

of both the excessive working capital as well as the shortage of working

capital. A finance manager has to ensure sufficient and adequate working

capital to the firm.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 6/38

II Financing Decisions:

As firms make decisions concerning where to invest these resources,

they have also to decide two they should raise resources. There are two

main sources of finance for nay firm, the shareholders funds and the

borrowed funds. The borrowed funds are always repayable and require

payment of a committed cost in the form of interest on a periodic basis.

The borrowed funds are relatively cheaper but always entail risk.

The risk is known as the financial risk i.e., the risk of insolvency

due to non-payment of interest or non-repayment of capital amount. The

shareholders fund is the main source of funds to any firm.

This may comprise of the equity share capital, preference share capital

and the accumulated profits. Firms usually adopt a policy of employing

both the borrowed funds as well as the shareholders funds to finance their

activities. The employment of these sources in combination is also

known as financial management.

II) Dividend Decisions:

Another major area of the decision marking by a finance manager is

known as the Dividend decisions which deal with the appropriation of after tax

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 7/38

profits. These profits are available to be distributed among the shareholders or

can be retained by the firm for reinvestment with in the firm. The profits which

are not distributed are impliedly retained in the firm. Al firms whether small or

big, have to decide how much of the profits should be reinvested back in the

business and how much should be taken out in form of dividends i.e., return on

capital. On one hand, paying out more to the owners may help satisfying their

expectations; on the other hand, doing so has other implications as a business

that reinvests less will tend to grow slower.

Reinvestment opportunities available to the firm,

The opportunity rate of the shareholders

The Identification of the relevant groups:

The various groups which may have stakes in the financial decisions

making of a firm and therefore required to be3 considered while taking

financial decisions are:

The shareholders

The debt investors,

The employees,

The customer and the suppliers,

The public,

The Government, and

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 8/38

The Management

Objective of the Financial Decision Making

The following two are often considered as the objectives of the financial

management.

The maximization of the profits of the firm, and

The maximization of the shareholders wealth

Maximization of the Profits of the firm:

For any business firm, the maximization of the profits is often

considered as the implied objective and therefore it is natural to retain the

maximization of profit as the goal of the financial also.

The profit maximization as the objective of financial management has

a built in favour for its choice. The profit is regarded as yard stick for the

economic efficiency of any form. If all business

Firm of the society are working towards profit maximization then the

economic resources of the society as a whole would have been most

efficiently, economically and profitably used. The profit maximization

by one firm and if targeted by all, will ensure the maximization of the

welfare of the society. So, the profit maximization as objective of

financial management will result inefficient allocation of resources not

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 9/38

only from the point of view of the firm but also for the society as such.

It ignores the risk.

The profit maximization concentrates on the profitability only and

ignores the financing aspect of that decision and the risk associated

with that financing.

It ignores the timings of costs and returns and thereby ignores the time

value of money

The profit maximization as an objective is ague and ambiguous.

The profit maximization may widen the gap between the perception of

the management and that of the shareholders.

The profit maximization borrows the concept of profit from the field

of accounting and thus tends to concentrate on the immediate effect of

a financial decisions as reflected in the increase in the profit of that

year or in near future.

Maximization of Shareholder Wealth:

This objective is generally expressed in term of maximization of the

value of a share of a firm. It is necessary to know and determine as to

how the maximization of shareholders wealth is to be measured.

The measure of wealth which is used in financial management is the

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 10/38

concept of economic value. The economic value is defined as the present

value of the future cash flows generated by a decision, discounted as

appropriate rate of discount which reflects the degree of associated risk.

This measure of economic value is based on cash flows rather than profit.

The economic value concept is objective in its approach and also takes

into account the timing of cash flows and the level of risk through the

discounting process.

Profit Maximization Versus Wealth Maximization:

The objective of profit maximization measures the performance of a

firm by a looking at its total profit. The objective of maximization of the

shareholders wealth is operational and objective in its approach. A firm

that wishes to maximize the profits may opt to pay no dividend and to

reinvest the retained earnings, whereas a firm that wishes to maximize

the shareholders wealth may pay regular dividends.

THE CHANGING ROLE OF FINANCIAL MANAGEMENT:

Many changes in the contemporary world, financial management has

undergone significant changes over the years. The financial management

has a very limited role in business enterprise. Finance Manger is

responsible only for maintaining financial records, preparing reports of

the company’s status, performance and arranging funds recorded by

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 11/38

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 12/38

IMPORTANCE OF FINANCIAL MANGEMENT:

Finance Management is of greater importance on the present

corporate world. It is a science of money, which permits the authorizes

to go further.

SIGNIFICANCE OF FINANCIAL MANAGEMENT CAN BE

SUMMARISED AS:

It assists in the assessment of financial needs of industry large or

small and indicates the internal and external resources for meeting them.

It assesses the efficiency and effectiveness of the financial institution in

mobilizing individual or corporate science. It also prescribes various

means for such mobilization of savings into desirable investment

channels.

It assists the management while investing the funds in profitable

projects by analyzing the viability of that project through capital

budgeting techniques. It permits the management to safeguard against

the interest of shareholders by properly utilizing the funds procured from

different sources and it also regulates and controls the funds to get

maximize use.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 13/38

METHODOLOGY OF THE STUDY

This study is made through two sources.

1. Primary Data:

The primary data comprises information collected during discussions with

Head of finance Department and from the meeting with staff.

2. Secondary Data:

The secondary data has been collected from information through

Annual Reports, Public Report, Bulletins and other Printed Materials

supplied by the Company.

methods

primary secondary

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 14/38

Chap -- 3

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 15/38

NATURE OF RATIOS

Ratio analysis is a widely used tool of finance analysis. The

term ratio in it refers to the relation ship expressed in mathematical terms between individual figures of group of figures connected with each other in

some logical manner and are selected from financial statements of the

concern. The ratio analysis is based on the fact that a single accounting

figure by itself may not communicate any meaningful information but

when expressed as a relative to some other figure, it may definitely provide

some significant information. The relation between two or more

accounting figures/groups is called a FINANCIAL RATIO. A financial

ratio helps to express the relationship between two accounting figures in

such a way that users can draw conclusions about the performance,

strengths and weakness of a firm.

STANDARDS OF COMPARISON:

The ratio analysis involves comparison for a useful interpretation of the

financial statements. A single ratio in itself does not indicate favorable

or unfavorable condition. It should be compared with some standard.Standards of comparison may consist of:

Past ratios, i.e. ratios calculated from the financial statements of the same

firm.

Competitors ratios i.e. ratios of some selected firms, especially the most

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 16/38

progressive and successful competitor, at the same in time.

Industry ratios i.e. ratios of the industry to which the firm belongs.

ADVANTGAGES OF RATIOS

Useful for evaluating performance in terms of profitability and

financial stability

Useful for intra and inter firm comparison.

Useful forecasting and budgeting.

It is just in a tabular form over a period of years indicates the trendof the business.

Simple to understand rather than the reading but the figures of

financial statement.

Key tool in the hand of modern financial management.

Enables outside parties to assess the strength and weakness of the

firm.

Ratio analysis is very useful for raking management decision and

also highlights the performance in the area of profitability, financial

stability and operational efficiency.

LIMITATIONS OF FINANCIAL RATIOS

The ratio analysis is widely used of technique to evaluate the

financial position and performance of business. But there are certain

problems in using ratios. The analyst should be aware of these

problems. The following are some of the limitations the ratio

analysis.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 17/38

It is difficult to decide on the proper basis of comparison.

The comparison is rendered difficult because of differences in

situations of two companies or of one company over years.

The price level changes make the interpretations of ratios invalid.

The difference in the definitions of items in the balance sheet and

the profit and loss statement make the interpretation of ratios

difficult.

The ratios calculated at a point of time are less informative and

defective as they suffer from short term changes.

Difference in accounting policies and accounting period make theaccounting data of two firms non-comparable as also the accounting

ratios.

It is very difficult to generalize whether a particular ratio is good or

bad. For example, a low current ratio may be said “bad” from the

point of view of low liquidity, but a high current ratio may not be

“good” as this may result from inefficient working capital

management.

Several ratios, calculated from the accounting date, can be grouped

into various classes according to financial activity or function to be

evaluated. As stated earlier, the parties interested in financial analysis are

short and long-term creditors, owners and management.

“Short-term creditors” main interest is in the liquidity position or the

short-term solvency of the firm. Long-term creditors, on the other hand, and

more interested in the long-term solvency and profitability of the firm.

Similarly, owners concentrate on the firms profitability and financial

condition. Management is interested on in evaluating every aspect of the

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 18/38

firms performance. They have to protect the interests of all parties and see

that the firm grows profitably. In view of the requirements of the various

users of ratios, we may classify them into the following four important

categories.

Types of Ratio:

Liquidity Ratios

Leverage Ratios

Activity Ratios

Profitability Ratios

I) Liquidity Ratio:

The liquidity refers to the maintenance of cash, bank balance

and those assets, which are easily convertible into cash in order to

meet the liabilities as and when arising. So, the liquidity ratios study

the firm’s short-term solvency and its ability to pay off the liabilities.

Current Ratio:

Current ratio is the ratio of current assets and current liabilities.Current assets are assets which can be covered into cash within one

year and include

cash in hand and at bank, bills receivable, net sundry debtors, stock of

raw materials, finished goods and work in progress, prepaid expenses,

outstanding and occurred incomes, and short term or temporary

investments.

Current liabilities are liabilities, which are to be repaid within a periodof 1 year and include Bills payable, Sundry Creditors, Bank

Overdraft, Outstanding Expenses, Incomes received in advanced,

proposed dividend, provision for taxation, unclaimed dividends and

short term loans and advances repayable within 1 year.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 19/38

Current Assets

Current Ratio= -----------------------------------

Current Liabilities

A Current ratio of 2:1 is considered as ideal: if a business has an

undertaking with its bankers to meet its working capital requirements

short notices, a current ratio of is adequate.

Quick Ratio :

Quick Assets

Quick Ratio = ----------------------------------------

Quick Liabilities

A quick ratio of 1 is considered as ideal. A quick ratio of less than 1is indicative of inadequate liquidity of the business. A very high quick

ratio is also not available, as funds can be more profitably employed.

Absolute Liquid Ratio

It is the ratio of Absolute Liquid Assets to Quick Liabilities.

However, for calculation purposes, it is taken as ratio of Absolute

Liquid Assets of Current Liabilities. Trade investment or Marketable

securities are equivalent of cash therefore, they may be included in thecomputation of absolute liquid ratio.

Absolute Liquid Assets

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 20/38

Absolute Quick Ratio = -------------------------------------

Current Liabilities

II) Leverage Ratios:

Leverage ratios indicate the relative interest of owners and creditors in a

business. It shows the proportions of debt and equity in financing the firm’s

assets the long-term solvency of a firm can be examined by using leverage

ratios. The long-term creditors like debenture holders, financial institutions

etc., are more concerned with the firms long-term financial strength.

There are two aspects of the long-term solvency of a firm ability to repay the principal when due, and regular payment of the interest they leverage ratio

are calculated to measure the financial rest and firms abilities of using debt.

TOTAL DEBT RATIO:

Total debt will include short and long-term borrowings from financial

institutions debentures bonds. Capital employed will include total debt

and net worth.

The firm may be interested in knowing the proportion of the interest

bearing debt in the capital structure by calculating total debt ratio. A

highly debt burdened firm will find difficulty in raising funds from

creditors and owners in future. Creditors treat the owner’s equities as

a margin of safety.

Total Debt

Total Ratio = --------------------------------

Capital Employed

DEBT-EQUITY RATIO:

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 21/38

It reflects the relative claims of creditors and shareholders against the

assets of the business. Debt, usually, refers to long-term liabilities.

Equity includes preference share capital and reserves.

The relationship describing the lenders contribution for each refers of the owner’s contribution is called debt equity ratio.

A high ratio shows a large share of financing by the creditors

relatively to the owners and therefore, larger claim against the assets

of the firm. A low ratio implies a smaller claim of creditors. The debt

equity indicates the margin of satisfy to the creditors so, there is no

doubt the Beth High and Low debt equity ratios are not desirable.

What is needed is a ratio, which strikes a proper balance between debt

and equity.

Total Debt

Debt-Equity Ratio = ----------------------------

Net worth

Some financial experts opine that ‘debt’ should include current

liabilities also. However, this is not a popular practice. In case of

preference share capital, it is treated as a part of shareholders funds,

but if the preference shares are redeemable, they are taken as a part of

long-term debt shareholder funds are also known as proprietor funds

and it includes items equity share capital, reserves, and surplus. A

debt equity ratio of 3:1 is considered ideal.

PROPRIETORY RATIOS:

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 22/38

It expresses the relationship between net worth and total assets.

Net worth

Property ratio = ----------------------------

Total Assets

Net worth = Equity share capital + Preference share capital + reserves

– Fictitious assets.

Total Assets = Fixed assets + current assets (excluding fictitious

assets)

Reserves earmarked specifically for a particular purpose should not be

included in calculation of net worth. A high proprietor’s ratio is indicative of

strong financial position of the business. The higher the ratio, the better it is.

FIXED ASSETS RATIO:

Fixed Assets

Fixed Assets = ----------------------------------------

Capital employed

Capital employed – Equity share capital + preference share capital +

Reserves + long term liabilities – Fictitious assets.

This ratio indicates the mode of financing the fixed assets. A

financially well-managed company will have its fixed assets financed

by long-term funds. Therefore, the fixed assets ratio should never bemore than a ratio of 0.67 is considered idea

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 23/38

INTEREST COVERAGE RATIOS:

This interest coverage ratio is computed by dividing earnings before

interests and taxed by interest charges.

Debt

Interest Coverage Ratio = ------------------

Interest

The interest coverage ratio shows the number of times the interest

charges are covered by funds that are or demurely available for their

payment. A high ratio is desirable but too high ratio indicates that the firmis very conservative in using debt and that is not using credit to the debt

advantage of shareholder. A lower ratio indicates excessive use of debt or

inefficiency operations. The firm should make efforts to improve the

operating efficiency or to retire debt to have a comfortable coverage ratio.

III) ACTIVITY RATIOS:

Activity ratios measure the efficiency or effectiveness with

which a firm manages its resources or assets. They calculate thespeed with which various assets, in which funds are blocked up, get

converted into sales.

TOTAL ASSETS TURNOVER RATIOS:

The assets turnover ratio, measures the efficiency of a firm in

managing and utilizing its assets. The higher the turnover ratio, the

more efficiency the management and utilization of the assets while

low turnover ratio is indicative of under-utilization of available

resources and presence idle capacity. The total assets turnover ratio is

computed by dividing sales by total assets.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 24/38

S a l e s

Total assets turnover ratio = --------------------------

Total Assets

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 25/38

WORKING CAPITAL TURNOVER RATIOS:

Cost of goods sold

Working capital turnover ratio = ----------------------------------

Working Capital

Where if cost of goods sold is known. Net sales can be taken in

the numerator.

Working capital = Current Assets – Current liabilities.

A high working capital turnover ratio indicates efficiency

utilization of the firm’s funds. However, it should not result in

overtrading.

DEBTORS TURNOER RATIO:

Debtor’s turnover ratio expresses the relationship between

debtors and sales. It is calculated.

Net credit sales

Debtors Turnover Ratio = ------------------------------------

Average debtors

Net credit sales inspire credit sales after adjusting for salesreturns. In case information no credit sale is not available. “Sales”

can be taken in the numerator. Debtors include bills receivable.

Debtors should be taken at Gross Value, without adjusting provisions

for bad debts. In case, average debtors can’t be found; closing balance

of debtors should be taken in the denominator. A high debtors

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 26/38

turnover ratio or a low debt collection period is indicative of a sound

credit management policy. A debtors turnover collection period of

30-36 days is considered ideal.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 27/38

DEBT COLLECTION PERIOD:

The debt collection period measures the quality of debtors since it

indicates the speed of the collection. The shorter the average

collection period implies the prompt payment by debtors.

No. of days year

Debt collection period = ------------------------------------------------

Debtors turn over ratio

An excessively long collection period implies a very liberal and

inefficient credit and collection performance. This certainly delays thecollection of each and impairs the firm’s liquidity. The average no. of days

for which debtors remain outstanding is called debt collection period or

average collection period.

CREDITORS TURNOVER RATIO:

Creditors turnover ratio expresses the relationship between creditors

and purchases.

Net Credit Purchase

Creditors turnover Ratio = -----------------------------------------------

Average Creditors

Net credit purchases imply credit purchases after adjusting for

purchases returns. In case information on credit purchases is not

available purchase may be taken in the numerator. Creditors include bills payable. In case avenue creditors can’t be found, closing balance

of creditors should be taken in the denominator.

The creditors turnover ratio is 12 or more. However, very less

creditors turnover ratio, or a high debt payment period, may indicate

the firm’s inability in meeting its obligations in time.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 28/38

PAYMENT PERIOD RATIO:

Credit turnover rate can also be expressed in terms of number of days

taken by the business to pay off its debts. It is termed as debt payment

period which is calculated as:

Number of days in a year

Payment Period Ratio= --------------------------------------------

Creditor’s turnover ratio

FIXED ASSETS TURNOVER RATIO: It is defined as

Net Sales

Fixed Assets Turnover Ratio= ----------------------------

Fixed Assets

Fixed assets imply net fixed assets i.e. after depreciation.

A high fixed assets turnover ratio indicates better utilization of the

firm’s fixed assets. A ratio around 5 is considered ideal.

INVENTORY TURNOVER RATIO:

Stock turnover ratio indicates the number of times the stock has

turned over into sale sin the year. It is calculated as

Cost of goods sold

Inventory Turnover Ratio= --------------------------------------------

Average Inventory

Cost of goods sold = Sales Gross Profit

Average Stock = (Opening stock and closing stock ½)

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 29/38

In case, information regarding cost of goods sold is not

known. Sales may be taken in the numerator. Similarly, if average stock

can’t be calculated, closing stock should be taken in the denominator.

A stock turnover ratio of ‘8’ is considered ideal. A high stock turnover ratioindicates that the stocks are fast moving and get converted into sales

quickly. However, it may also be on account of holding low amount of

stocks and replenishing stocks in larger number of installments.

IV) PROFITABILITY RATIO:

It measures the overall performance and effectiveness of the

firm. Poor operational performance may indicate poor sales and hence poor

profits. A lower profitability may arise due to the lack of control over the

expenses. Bankers, financial institutions and other creditors look at the

profitability’s. Ratio as an indicator whether or not the firm earns

substantially more than it pays interest for the use of borrowed funds and

whether the ultimate repayment of their debt appear reasonably certain

owner are interested to know the profitability as it indicates the return which

they can get on this instruments. Profitability ratios measure the profitability

of a concern generally. They are calculated either in relation to sales or in

relation to investment.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 30/38

NET PROFIT RATIO:

It indicates the result of the overall operation of the firm.

The higher the ratio, per profitable is the business. The net

profit ratio is reassured by dividing net profit buy sales. The net profit

ratio indicates management efficiency in manufacturing

administrating and selling the products. This ratio is the overall firm’s

ability to turn each rupee of sale into net profit. If the net profit

margin is inadequate, the firm fails to achieve satisfactory return on

shareholder’s funds.

Profit After Tax

Net Profit Ratio = ------------------------------------

Net Sales

A firm with high net profit margin can make better use of

favorable conditions. Such as rising selling prices, falling cost of

products or increasing demand for the product. Such a firm will be

able to accelerate its profits at a faster rate than a firm with a low net

profit margin. This ratio also indicates the firm capacity to withstand

adverse economic conditions.

RETURN ON NETWORTH RATIO:

It indicates the return, which the shareholders are earning on

their resources invested in the business.

Profit after tax

Return on net worth ratio = -------------------------------------- Net Wroth

Net worth = Shareholders funds = Equity share capital + Preference

share capital + Reserves – Factious Assets.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 31/38

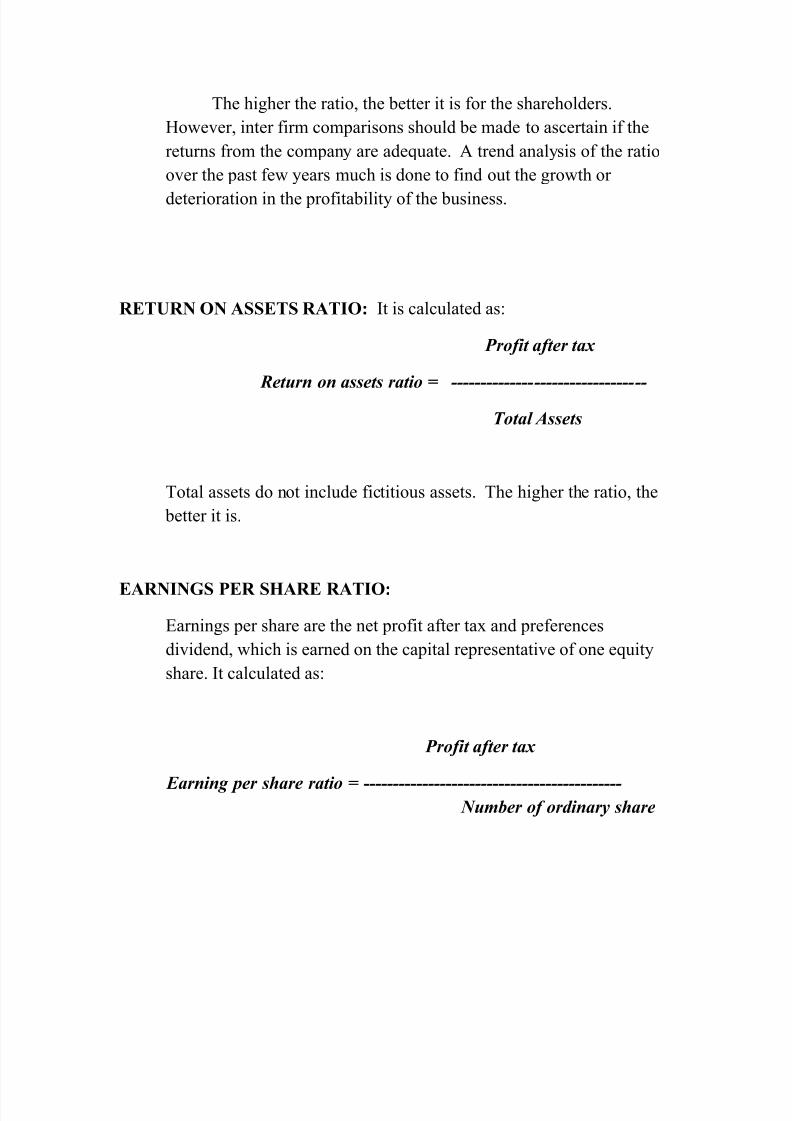

The higher the ratio, the better it is for the shareholders.

However, inter firm comparisons should be made to ascertain if the

returns from the company are adequate. A trend analysis of the ratio

over the past few years much is done to find out the growth or

deterioration in the profitability of the business.

RETURN ON ASSETS RATIO: It is calculated as:

Profit after tax

Return on assets ratio = ---------------------------------

Total Assets

Total assets do not include fictitious assets. The higher the ratio, the

better it is.

EARNINGS PER SHARE RATIO:

Earnings per share are the net profit after tax and preferences

dividend, which is earned on the capital representative of one equity

share. It calculated as:

Profit after tax

Earning per share ratio = -------------------------------------------- Number of ordinary share

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 32/38

FUNDS FLOW STATEMENT

Definition of Funds:

Funds may mean change in financial resources, arising from

changes in working capital items and from financing and investing activities

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 33/38

of the enterprise, which may involve only non-current items.

The funds flow statement analyses only the causes of changes in

the firm’s working capital position. The cash flow statement is prepared to

analyze changes in the flow of cash only. These statements fail to consider the changes in the firm’s total financial resources. They do not reveal some

significant items that do not affect the firm’s cash or working capital

position, but considerably influence the financing and asset mix of the firm.

But funds or cash flow statement will not include this transaction, as it does

not involve any change in cash or working capital. A comprehensive

statement of changes in financial position would disclose this information

along with information on cash or working capital changes.

The statement of changes in financial position is an extension of the funds flow statement or the cash flow statement. It is more informative

and comprehensive in indicating the changes in the firm’s financial position.

However, the analysis of changes in the firm’s cash position or working

capital is still very significant. Therefore, to get better insights, a firm may

prepare a comprehensive, all- Inclusive, statement of changes in financial

position incorporating changes in the firm’s cash and working capital

position. The preparation and use of the statement of changes in financial

position involving:

• Changes in the firm’s working capital position,

• Changes in the firm’s cash position, and

• Changes in the firm’s total financial resources.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 34/38

Funds flow statement:

The statement of changes in financial position, prepared to

determine only the sources and uses of working capital between dates of two

balance sheets, is known as the funds flow statement.

Working capital is defined as the difference between current

assets and current liabilities. Working capital determines the liquidity

position of the firm.

As historical analysis, the statement of changes in working

capital reveals to management the way in which working capital was

obtained and used. With this insight, management can prepare the estimates

of working capital flows. A statement reporting the changes in workingcapital is useful in addition to the financial statements. A projected statement

of changes in working capital is immensely useful in the firm’s long-range

planning. Management, for example, wants to anticipate the working capital

flows in order to plan the repayment schedules of its long-term debt. For a

fast growth and expansion, a fir needs larger amount of working capital.

Therefore, estimates of working capital on a long-term basis are also

required to determine whether or not adequate working capital will be

generated to meet the firm’s expansion. If not, the firm can makearrangements in advance to procure funds from outside to meet its needs.

Concept of working capital flow:

The working capital flow or fund arises when the net effect

of a transaction is to increase or decrease the amount of working capital.

Normally, a firm will have some transactions that will change net working

capital and some that will cause no change in net working capital.

Transactions that change net working capital include most of the items of the profit and loss account and those business events that simultaneously affect

both current and non-current balance sheet items. On the order hand,

transactions that do not increase or decrease working capital include those

that affect only current accounts or only non current accounts.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 35/38

The concept of working capital flow may be summarized as follows:

• The net working capital increases or decreases when a

transaction involves a current account and non-current

account.

• The net working capital remains unaffected when a

transaction involves only current accounts.

• The net working capital remains unaffected when a

transaction involves only non-current accounts.

Sources of working capital:

The typical sources of working capital are summarized below:

1. funds from operation(adjusted net income)

2. sale of non-current assets:

• Sale of long-term investments (shares, bonds/debentures etc.)

• Sale of tangible fixed assets like land. Building, plant, or

copyrights.

3. long-term financing:

• long term borrowings(institutional loans, debentures,

bonds ,etc)

• Issuance of equity and preference shares.

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 36/38

4. Short-term financing such as bank borrowings.

Uses of working capital:

The typical uses of working capital are as follows:

1. Adjusted net loss from operation

2. Purchase of non-current assets:

• Purchase of long-term investments like shares,

bonds/debentures etc.

• Purchase of intangible fixed assets, like goodwill, patents,

copyrights etc.

• Purchase of tangible fixed assets, like land, building, plant,

machinery, equipments etc.

3. Repayment of long-term debt(debentures or bonds) and short-term

debt(bank borrowing)

4. Redemption of redeemable preference shares

5. Payment of cash dividend.

Forms of Funds Flow Statement:

The statement of changes in working capital or funds flow is the

summary of sources and uses of working capital. This statement may be

presented in two parts.

The first part explains the causes of the change in amount of

working capital from the end of one period to another. It gives a list of

sources which provide working capital was applied.

The second part of the statement contains an analysis of the

changes in the working capital items. This part of the statement shows items

of current assets and current liabilities at the beginning and at the end of the

accounting period and the effect of their changes between two periods on the

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 37/38

working capital.

Significance of Funds Flow Statement:

The utility of the funds flow statement stems from the fact that itenables shareholders, creditors and other interested in the enterprise to

evaluate the uses of funds by the enterprise and to determine how these uses

are financed. Thus, the outside parties can have clear knowledge about the

financial policies that the company has pursued. In the light of the

information so supplied by statement, the outsiders can decide whether or

not to invest in the enterprise and on what terms funds have to be invested.

The funds statement provides an insight into the financial operations of a

business enterprise- an insight immensely valuable to the financial manager in analyzing the past and future expansion plans of the enterprise and the

impact of these plans on the enterprise liquidity. He can detect imbalances in

the uses of funds and undertake remedial actions.

With the help of the funds statement the analyst can evaluate the

financing pattern of the enterprise. An analysis of the major sources of funds

in the past reveals what portion of the growth was financed internally and

what portion externally. The statement is also meaningful in judging

whether the company has grown at too fast a rate and whether financing is

strained.

Comparative statements

A simple method of tracing periodic changes in the financial

performance of a company is to prepare comparative statements.

Comparative financial statements will contain items at least for two periods.

Changes----increases and decreases----in income statement and balance

8/8/2019 Financial Analysis Raw Info First Copy

http://slidepdf.com/reader/full/financial-analysis-raw-info-first-copy 38/38

sheet over period can be shown in two ways: (1) aggregate changes and

(2) proportional changes.

Drawing special columns for aggregate amount or percentage, or

both, of increases and decreases, can indicate aggregate changes. Recording percentage calculated in relation to a common base in special columns, on

the other hand, shows relative, or proportional, changes. For example, in the

case of profit and loss statement, sales figure is assumed to be common base

and all other items are expressed as percentage of sales. Similarly, the

balance sheet items are expressed as percentage of total assets or total funds.

The financial statements prepared in terms of common base percentage are

called common size statements. This kind of analysis is called vertical

analysis and it indicates static relationships since relative changes are

studied at a specific date.

An investigation of the Comparative financial statements helps to

highlight the significant facts and points out the items which need further

analysis. The published balance sheets and profit and loss accounts of joint-

stock companies in India are presented in two-year comparative form. Some

of the companies also report to shareholders condensed comparative

statements covering an extended period of years. From analytical point of

view, such statements are quite useful to investors.

Related Documents