FINANCIAL AID OFFICE Student Loans KNOW WHO YOU OWE AND HOW MUCH and……WHERE ARE YOU GOING???

FINANCIAL AID OFFICE Student Loans KNOW WHO YOU OWE AND HOW MUCH and……WHERE ARE YOU GOING???

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FINANCIAL AID OFFICE

Student Loans

KNOW WHO YOU OWE AND HOW MUCH and……WHERE

ARE YOU GOING???

Note

You MUST READ this complete presentation to be able to answer the related questions on the Federal Direct Loan Worksheet.

The purpose of this information is to benefit to YOU! We want you to have the information needed to be a responsible borrower and to understand your repayment obligations.

G o t o h t t p : / /w w w. b l a c k r i v e r t e c h . o r g / fi n a n c i a l - a i d / l o a n s f o r t h e f o r m s :

1. Loan Appl icat ion 2. Federal Direct Loan Worksheet3. Updated Contacts List

Go to w w w. s t u d e n t l o a n s . g o v) to Comple te :

4. Direct Loan Entrance Counsel ing5. Master promissory note (MPN)

Direct Loan Requirements

Do you really need a loan?

Almost 60% of BRTC students qualify for a Pell grant - if you qualify for at least $1700 Pell/semester, it is enough to cover Tuition, Fees, and $500 books for 12 credit hours -- No loans needed

Loans are NOT free! You have to pay them back.Borrow conservatively….think ahead…..plan ahead! .

Create a budget…and stick to it!

Review the loan payment schedule later in this presentation. Can you afford payments??

Can you decrease any of your current expenses? Try ALL other options before taking loans.

Pell Scholarships Family/Friend Loans Working at least one job!! (go to school 2 days/nights a week) (depending on program

demands)

CREATE A

BUDGET!!

Authorized Educational Expenses

Authorized educational expenses include: Tuition Room and board Institutional fees Books Supplies Equipment Dependent child care expenses Transportation and commuting expenses Rental or purchase of a personal computer Loan fees Other documented, authorized costs

What is your goal??

Think ahead and plan so that you are proactive in your own success! Are you planning on obtaining a Bachelor’s? Are you getting your

college“BASICS”? Do your courses at BRTC transfer to ???? Go to acts.adhe.edu/ Visit the

Registrar of the school you plan to attend and make sure they accept. How much will I need to complete Bachelor’s ($20,000) and/or Master’s

($20,000)? What will the total be if I take loans for a Technical Certificate/Associates????

If you have over 60 hours, get a degree audit NOW!! How close are you to graduating?

Am I close to reaching my 150% max hours limit at BRTC for my Financial Aid? Will every class I take transfer? MAKE EVERY CLASS COUNT toward your final educational goal!

Will I have Pell when I transfer?? CAN I PAY THE LOANS BACK with the education I am getting????

* Visit with a Financial Aid Officer or your Advisor if you can not answer these questions.

Where are you going and how do you get there?

acts.adhe.edu is the Arkansas Transfer Coursework Website

Bachelors degree programs in today’s educational fast tracks….

General Education requirements for your Bachelor’s program

Degree Plans

Know what you want to do.- KUDER test information is available in the Career Pathways Office in Administration Building.- DiscoverArkansas.net has occupations and salaries to help you decide what you want to do.

Know what degree you are working on and take ONLY the courses that will lead to completion of that program.

Don’t waste loan money on classes you don’t need! You are limited to how many credit hours you may attempt toward your chosen degree and still maintain Financial Aid eligibility.

Get advice from Financial Aid when changing degree plans, transferring to a university, dropping a class or getting close to 100 hours to understand the effects this will have on your eligibility to Title IV Funds. (Pell and Loans)

BRTC STUDENT EMAIL

We communicate with students primarily by BRTC email. Make sure you have set up your GMAIL account. Go go www.blackrivertech.edu and access Current Students to activate your account.

Make sure your inbox doesn’t fill up. Email cannot be delivered to a full inbox.

Check this EMAIL weekly, if not daily. This is how you will be notified of dates that Financial Aid REFUNDS are mailed.

Other departments will also expect you to check this account frequently. You’ve

GOT MAIL!

Campus Connect

https://connect.blackrivertech.org/cc3_scripts/cc_server.exe Link is at bottom of BRTC homepage

Student account access. Use it to:

View mid-term and final grades Register for classes View your Student Account and financial aid View your award letter View Holds If a new user, Log in using your

* Userid – SSN * Password - 1111

Change your password after first log-in

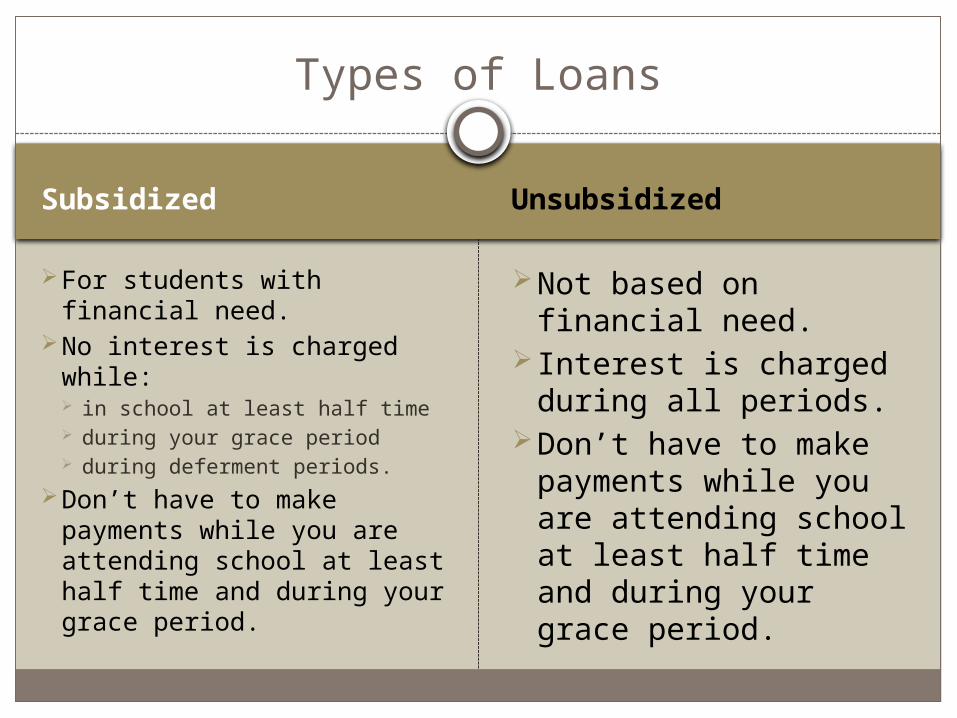

Subsidized Unsubsidized

For students with financial need.

No interest is charged while: in school at least half time during your grace period during deferment periods.

Don’t have to make payments while you are attending school at least half time and during your grace period.

Not based on financial need.

Interest is charged during all periods.

Don’t have to make payments while you are attending school at least half time and during your grace period.

Types of Loans

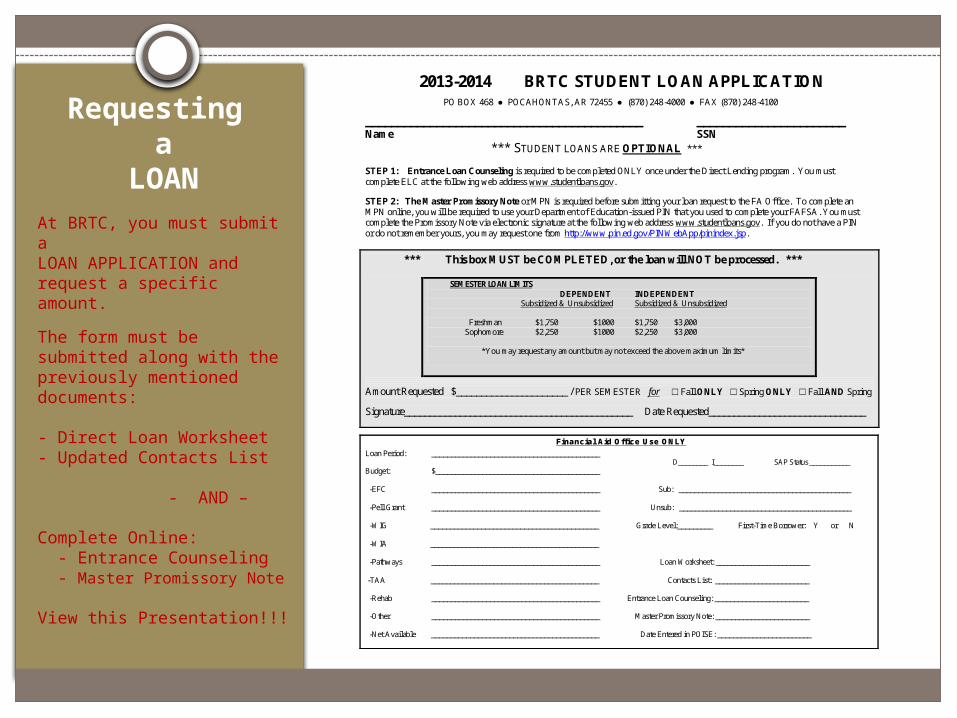

Requesting a

LOANAt BRTC, you must submit aLOAN APPLICATION and request a specific amount.

The form must be submitted along with the previously mentioned documents:

- Direct Loan Worksheet- Updated Contacts List - AND –

Complete Online: - Entrance Counseling - Master Promissory Note View this Presentation!!!

You accept or decline loans by clicking these boxes. If you want to decrease the amount, you click accept and the amount under the offered tab will allow you to type into it. When you are done, click submit.

2013-2014 BRTC STUDENT LOAN APPLICATION

PO BOX 468 ● POCAHONTAS, AR 72455 ● (870) 248-4000 ● FAX (870) 248-4100

___________________________________________ _______________________ Name SSN *** STUDENT LOANS ARE OPTIONAL *** STEP 1: Entrance Loan Counseling is required to be completed ONLY once under the Direct Lending program. You must complete ELC at the following web address www.studentloans.gov.

STEP 2: The Master Promissory Note or MPN is required before submitting your loan request to the FA Office. To complete an MPN online, you will be required to use your Department of Education-issued PIN that you used to complete your FAFSA. You must complete the Promissory Note via electronic signature at the following web address www.studentloans.gov. If you do not have a PIN or do not remember yours, you may request one from http://www.pin.ed.gov/PINWebApp/pinindex.jsp.

*** This box MUST be COMPLETED, or the loan will NOT be processed. ***

SEMESTER LOAN LIMITS DEPENDENT INDEPENDENT Subsidized & Unsubsidized Subsidized & Unsubsidized

Freshman $1,750 $1000 $1,750 $3,000 Sophomore $2,250 $1000 $2,250 $3,000 *You may request any amount but may not exceed the above maximum limits*

Amount Requested $______________________ / PER SEMESTER for □ Fall ONLY □ Spring ONLY □ Fall AND Spring

Signature_____________________________________________ Date Requested_______________________________

Financial Aid Office Use ONLY

Loan Period: ___________________________________________ D________ I________ SAP Status ___________ Budget: $__________________________________________

-EFC ___________________________________________ Sub: ____________________________________________

-Pell Grant ___________________________________________ Unsub: ____________________________________________

-WIG ___________________________________________ Grade Level:_________ First-Time Borrower: Y or N

-WIA ___________________________________________

-Pathways ___________________________________________ Loan Worksheet: ________________________

-TAA ___________________________________________ Contacts List: ________________________ -Rehab ___________________________________________ Entrance Loan Counseling: ________________________ -Other ___________________________________________ Master Promissory Note: ________________________

-Net Available ___________________________________________ Date Entered in POISE: ________________________

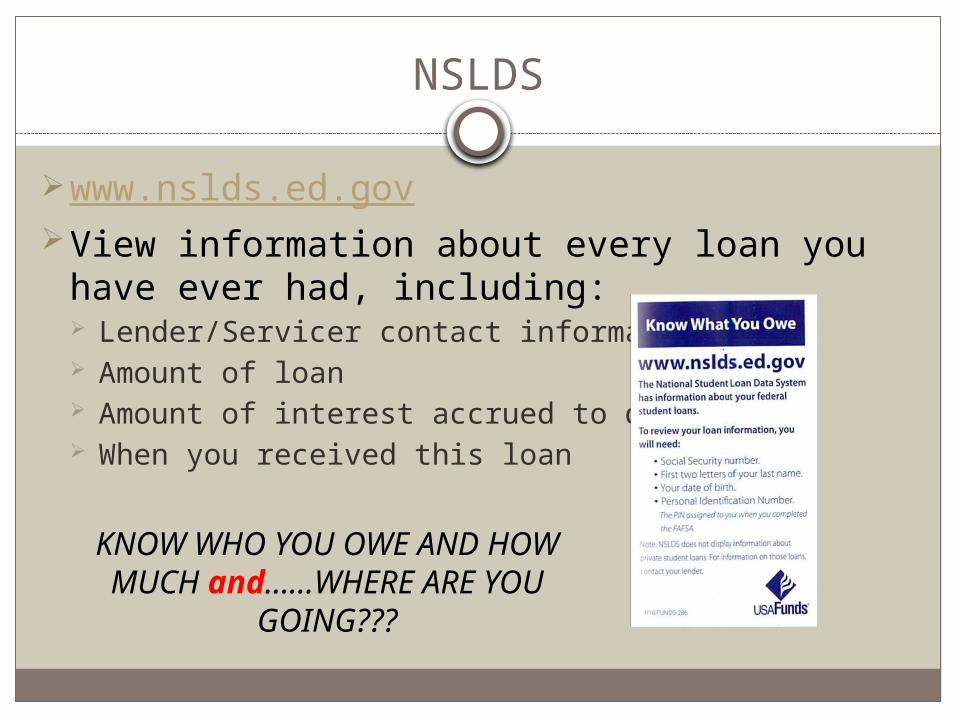

NSLDS

www.nslds.ed.govView information about every loan you have

ever had, including: Lender/Servicer contact information Amount of loan Amount of interest accrued to date When you received this loan

KNOW WHO YOU OWE AND HOW MUCH and……WHERE

ARE YOU GOING???

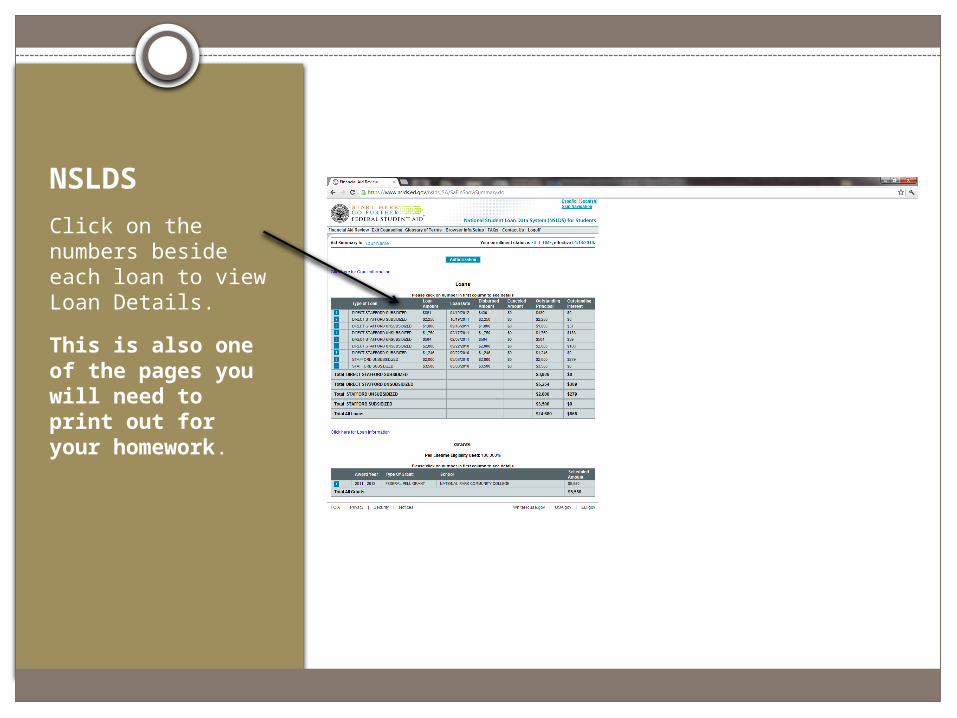

NSLDS

Click on the numbers beside each loan to view Loan Details.

This is also one of the pages you will need to print out for your homework.

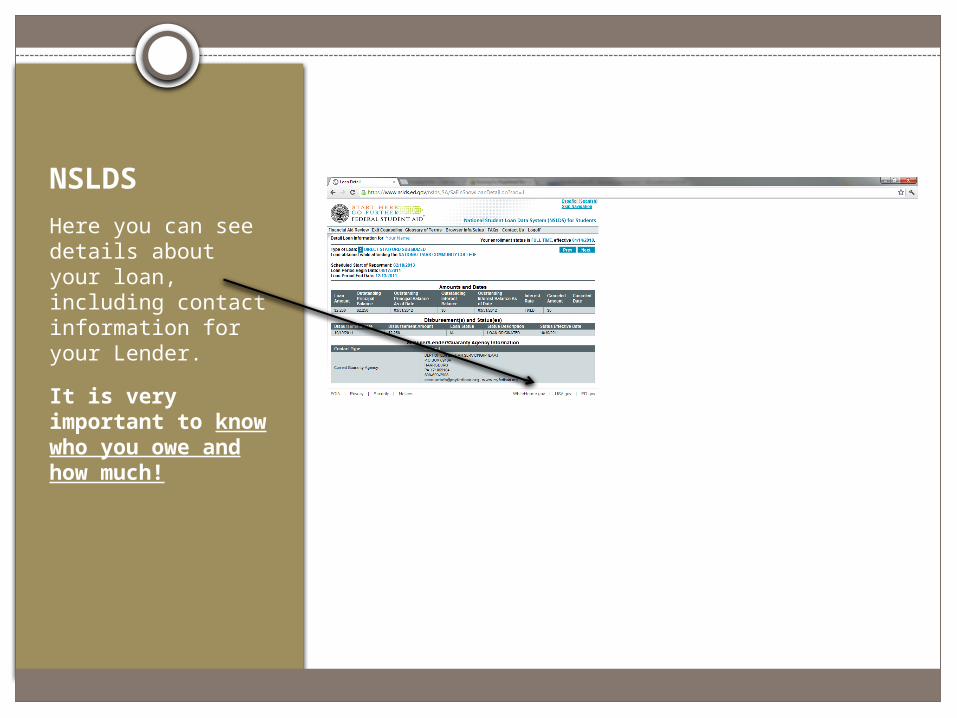

NSLDS

Here you can see details about your loan, including contact information for your Lender.

It is very important to know who you owe and how much!

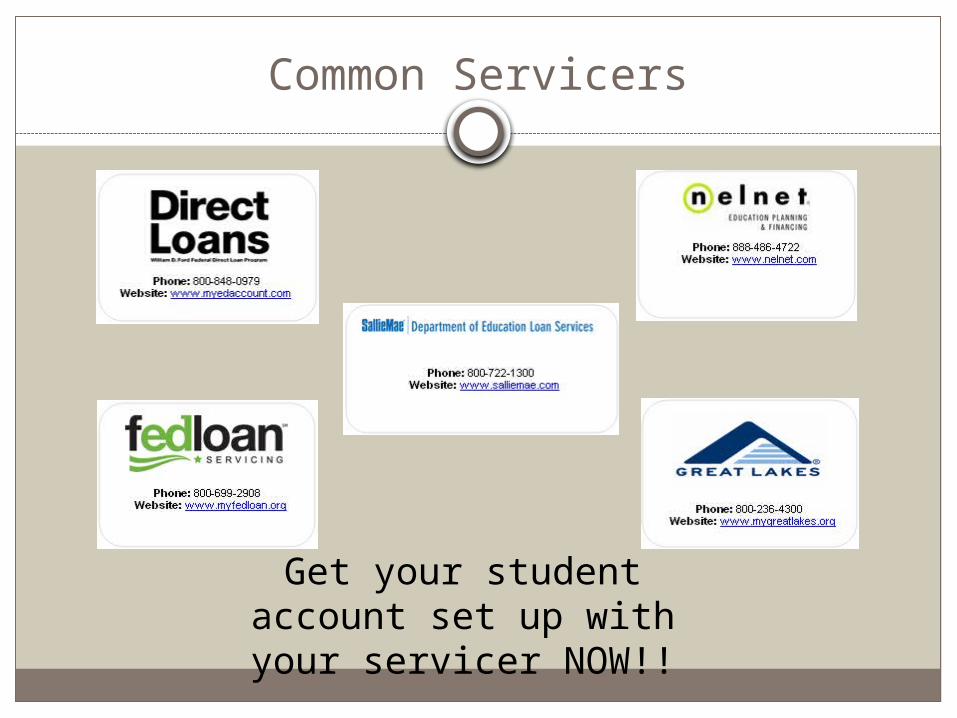

Common Servicers

Get your student account set up with your servicer

NOW!!

Entrance Counseling

www.studentloans.gov log in, then click “Complete Entrance Counseling”

A requirement for student loans Explains:

borrower responsibilities interest rates grace periods when to pay how much you’ll pay how/why to go into deferment or forbearance what happens if you don’t pay (default)

Takes about 30-45 minutes

Log in with your name, SSN, DOB,

and PIN from FAFSA

Master Promissory Notes

www.studentloans.gov log in, then click “Complete Master Promissory Note”

A legal document!When you sign it, you promise to repay your

loan(s) and any accrued interest and fees. It includes the terms and conditions of your

loan. It is required!Can complete online.

Borrower Responsibilities

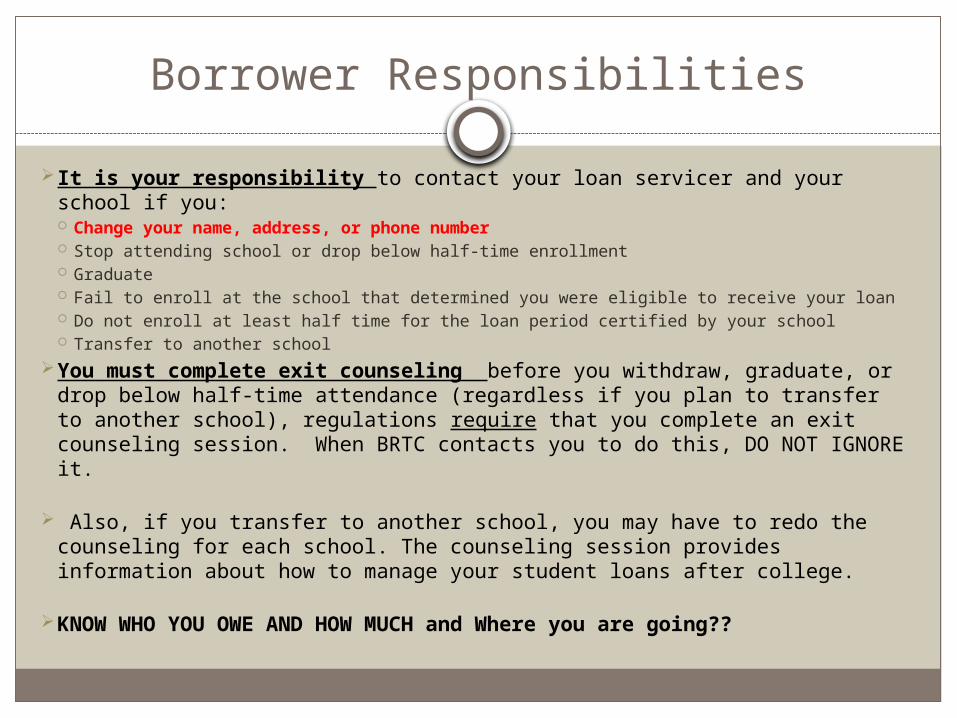

It is your responsibility to contact your loan servicer and your school if you: Change your name, address, or phone number Stop attending school or drop below half-time enrollment Graduate Fail to enroll at the school that determined you were eligible to receive your loan Do not enroll at least half time for the loan period certified by your school Transfer to another school

You must complete exit counseling before you withdraw, graduate, or drop below half-time attendance (regardless if you plan to transfer to another school), regulations require that you complete an exit counseling session. When BRTC contacts you to do this, DO NOT IGNORE it.

Also, if you transfer to another school, you may have to redo the counseling for each school. The counseling session provides information about how to manage your student loans after college.

KNOW WHO YOU OWE AND HOW MUCH and Where you are going??

Grace Period

Begins when you graduate, withdraw, or drop to less than half-time status

You only get one, and it only lasts 6 months. You will receive your repayment obligation,

which includes: Date payments are to begin (Payment is expected even if you do not receive a

payment booklet or monthly statement.) Monthly payment amount Repayment terms Current principal balance Interest rate

Things That Affect Eligibility for Financial Aid at BRTC

Completed Financial Aid file- do the FAFSA www.fafsa.ed.gov Submitting ALL required documents to BRTC Financial Aid Office.

Financial Aid Office will notify you by mail of missing documents and then you must remember to submit them to us. This may be veiwed on Campus Connect under the “Review Aid” option.

Previous attendance at other institutions- Must have ALL official transcripts from previously attended schools

before Financial Aid awards will be approved Satisfactory Academic Progress-(SAP) -- maintaining a 2.00 term &

cumulative GA and completing required minimum amount of courses each term

Maximum eligibility limits for Pell and Loans – on the Loan Application

SAP-REVIEW AND CHANGES

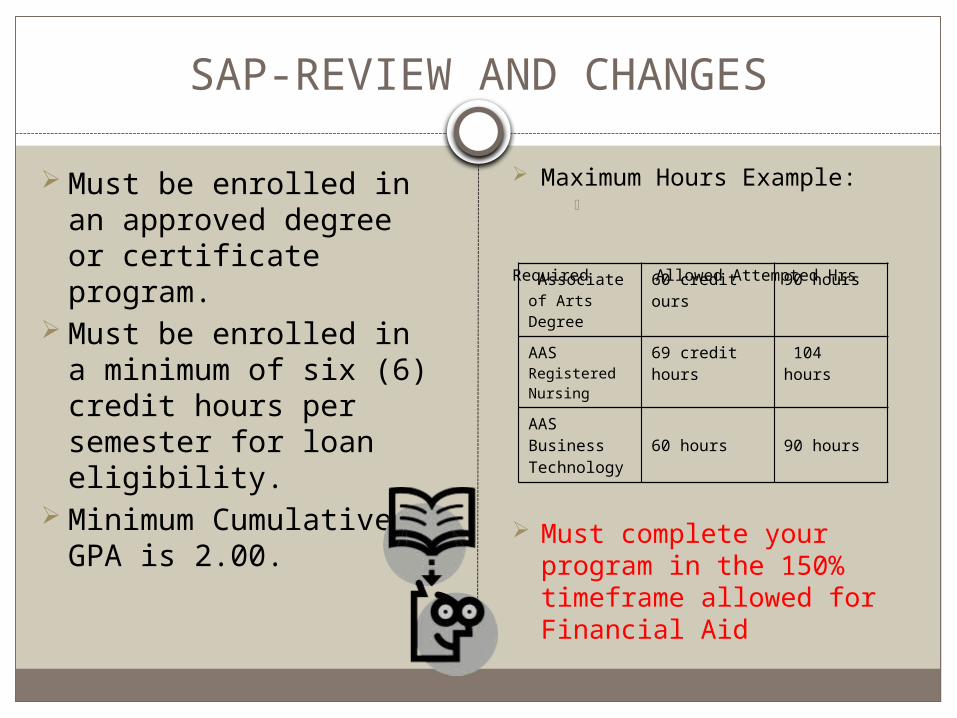

Must be enrolled in an approved degree or certificate program.

Must be enrolled in a minimum of six (6) credit hours per semester for loan eligibility.

Minimum Cumulative GPA is 2.00.

Maximum Hours Example:

Required Allowed Attempted Hrs

Must complete your program in the 150% timeframe allowed for Financial Aid

Associateof Arts Degree

60 credit ours

90 hours

AASRegistered Nursing

69 credit hours

104 hours

AASBusiness Technology

60 hours 90 hours

SAP-REVIEW AND CHANGES

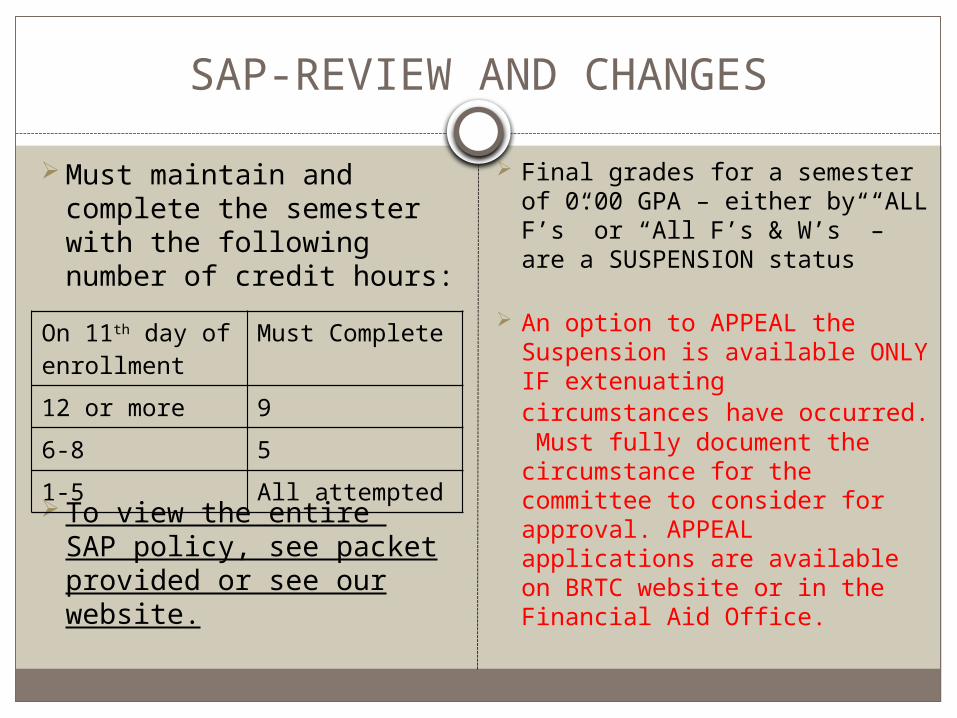

Must maintain and complete the semester with the following number of credit hours:

To view the entire SAP policy, see packet provided or see our website.

Final grades for a semester of 0.00 GPA – either by “ALL F’s” or “All F’s & W’s” – are a SUSPENSION status

An option to APPEAL the Suspension is available ONLY IF extenuating circumstances have occurred. Must fully document the circumstance for the committee to consider for approval. APPEAL applications are available on BRTC website or in the Financial Aid Office.

On 11th day of enrollment

Must Complete

12 or more 9

6-8 5

1-5 All attempted

Budget Allocation of Awards

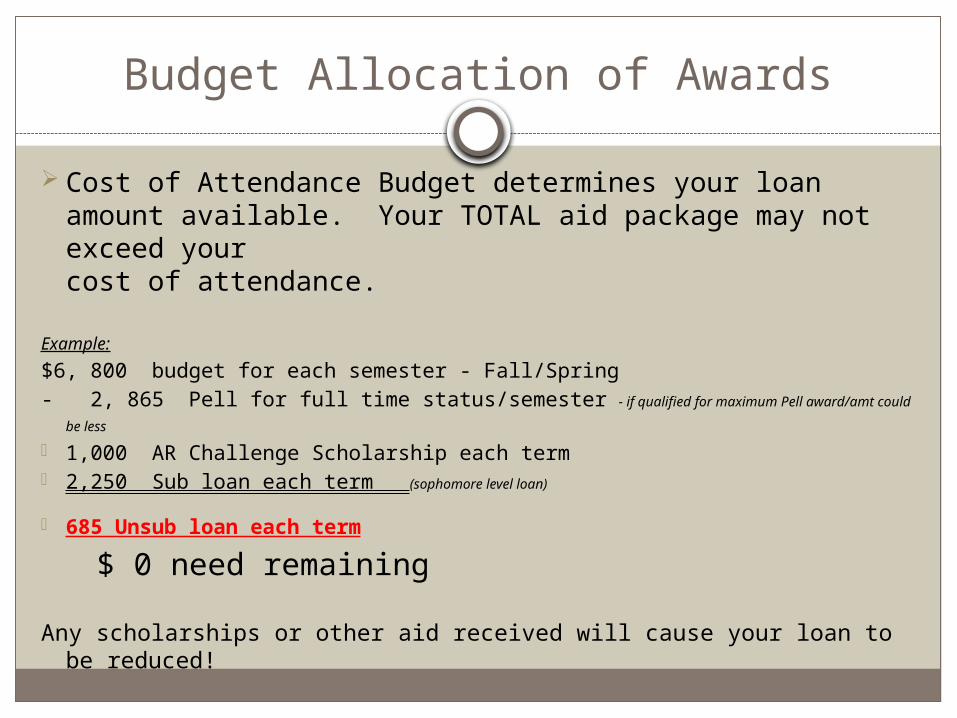

Cost of Attendance Budget determines your loan amount available. Your TOTAL aid package may not exceed your cost of attendance.

Example:

$6, 800 budget for each semester - Fall/Spring- 2, 865 Pell for full time status/semester - if qualified for maximum Pell award/amt could be

less

1,000 AR Challenge Scholarship each term 2,250 Sub loan each term (sophomore level loan)

685 Unsub loan each term

$ 0 need remaining

Any scholarships or other aid received will cause your loan to be reduced!

PELL Lifetime Limits

Federal guideline-600% Pell allowed 6 years of full-time Pell For years 2009-10 & 2010-2011, the regs were

different for Summer Pell – you may have used extra those years Review your Pell used on www.nslds.ed.gov

Do not take unnecessary classes (like let’s take this one so I can get full pell) and

Conserve your Pell refunds (FREE MONEY)……SAVE it for Bachelor’s program, if able. Use your Pell refund wisely!

Loan lifetime limits are coming in the future!!

150% Time Limit on Subsidized Loans

You have LIFETIME Limit on borrowing Subsidized Loans!

Maximum eligibility period to receive Direct Subsidized Loans

There is a limit on the maximum period of time (measured in academic years) that you can receive Direct Subsidized Loans. In general, you may not receive Direct Subsidized Loans for more than 150% of the published length of your program. This is called your “maximum eligibility period”. You can usually find the published length of any program of study in your school’s catalog. For example, if you are enrolled in a 4-year bachelor’s degree program, the maximum period for which you can receive Direct Subsidized Loans is 6 years (150% of 4 years = 6 years). If you are enrolled in a 2-year associate degree program, the maximum period for which you can receive Direct Subsidized Loans is 3 years (150% of 2 years = 3 years). Your maximum eligibility period is based on the published length of your current program. This means that your maximum eligibility period can change if you change programs. Also, if you receive Direct Subsidized Loans for one program and then change to another program, the Direct Subsidized Loans you received for the earlier program will generally count against your new maximum eligibility period.

150% Time Limit on Subsidized Loans (continued)

Periods that count against your maximum eligibility period

The periods of time that count against your maximum eligibility period are periods of enrollment (also known as “loan periods”) for which you received Direct Subsidized Loans.

For example, if you are a full-time student and you receive a Direct Subsidized Loan that covers the fall and spring semesters (a full academic year), this will count as one year against your maximum eligibility period.

If you receive a Direct Subsidized Loan for a period of enrollment that is shorter than a full academic year, the period that counts against your maximum usage period will generally be reduced accordingly.

For example, if you are a full-time student and you receive a Direct Subsidized Loan that covers the fall semester but not the spring semester, this will count as one-half of a year against your maximum eligibility period.

With one exception, the amount of a Direct Subsidized Loan you receive for a period of enrollment does not affect how much of your maximum eligibility period you have used. That is, even if you receive a Direct Subsidized Loan in an amount that is less than the full annual loan limit, that lesser amount does not reduce the amount of your maximum eligibility period you have used. The one exception applies if you receive the full annual loan limit for a loan period that does not cover the whole academic year. In that case, the loan will count as one year against your maximum eligibility period regardless of your enrollment status (half-time, three-quarter time, or full-time).

150% Time Limit on Subsidized Loans (continued)

Regaining eligibility for Direct Subsidized Loans

If you become ineligible for Direct Subsidized Loans because you have received Direct Subsidized Loans for your maximum eligibility period, you may again become eligible to receive Direct Subsidized Loans if you enroll in a new program that is longer than your previous program.

If you regain eligibility to receive additional Direct Subsidized Loans because you enrolled a program that is longer than your prior program and you previously became responsible for paying all of the interest that accrues on your Direct Subsidized Loans, we will pay the interest that accrues on your new loans..

Multiple Disbursements

ALL student loans will be made in multiple disbursements each semester - 2 equal disb’s for Fall 2 equal disb’s for Spring 2 equal disb’s for Summer (1 in Summer I /1 in Summer II)

*** Disbursement Date Schedules are always posted on the FA page of BRTC website ***

Will not get full amount all at once. Loans and Pell are based on ATTENDANCE. If you do

not attend, you will not earn the funds. If you take the funds and did not earn them…….you will

owe a bill with BRTC and/or the Federal Government.

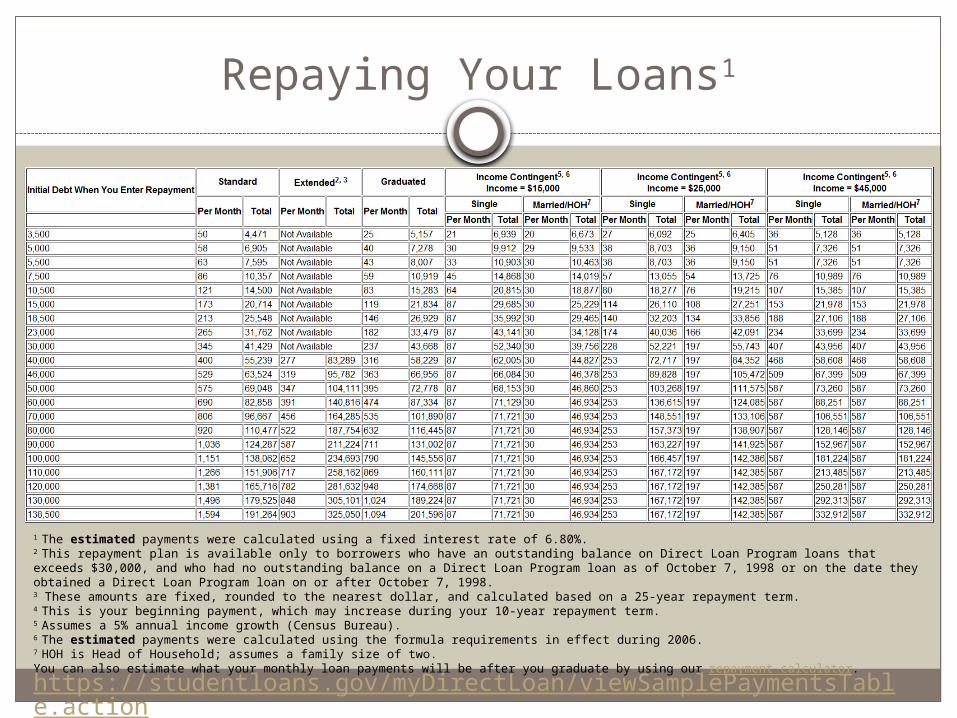

Repaying Your Loans1

1 The estimated payments were calculated using a fixed interest rate of 6.80%.2 This repayment plan is available only to borrowers who have an outstanding balance on Direct Loan Program loans that exceeds $30,000, and who had no outstanding balance on a Direct Loan Program loan as of October 7, 1998 or on the date they obtained a Direct Loan Program loan on or after October 7, 1998.3 These amounts are fixed, rounded to the nearest dollar, and calculated based on a 25-year repayment term.4 This is your beginning payment, which may increase during your 10-year repayment term.5 Assumes a 5% annual income growth (Census Bureau).6 The estimated payments were calculated using the formula requirements in effect during 2006.7 HOH is Head of Household; assumes a family size of two.You can also estimate what your monthly loan payments will be after you graduate by using our repayment calculator.

https://studentloans.gov/myDirectLoan/viewSamplePaymentsTable.action

Student Loan Repayment

Income-Based Repayment (IBR)---A repayment plan available to a borrower who has partial financial hardship. The IBR monthly payment amount is determined by income, family size, and applicable loan debt and may be adjusted annually depending on these factors.

Income-Sensitive Repayment---Payments are based on a percentage of your gross monthly income but must cover the interest that accrues each month.

Income-Contingent Repayment (ICR)---Eligibility is based on income (or combined income with spouse, if married), family size, and total federal Direct Loan debt.

Loan Consolidation Reduce your monthly payments by extending your repayment period. Combine all of you student loans with various lenders into one monthly

payment. Benefit from a fixed interest rate.Do your homework to determine what repayment option is most beneficial for you! Go to www.Studentloans.gov and click Complete IBR/Pay as you earn/ICR Repayment

Plan Request – it is the easiest way to submit for one of these repayment plans!

Student Loan Forgiveness

Loan Forgiveness Programs Loan forgiveness programs promote employment in certain fields by forgiving part or all of

you loan debts, provided you fulfill certain work-related requirements.

Federal Loan Forgiveness Programs Teacher Loan Forgiveness Program – 5 years - $5,000 or $17,500 Public Service Loan Forgiveness Program – 10 years – remaining principal & interest Federal Employee Student Loan – Minimum 3 years required service – up to $10,000 annually

– up to $60,000 maximum

State loan forgiveness programs vary. Please check with the individual state.

*** For Arkansas residents, you may go to ADHE.edu and inquire the detail of a loan forgiveness program.

WHAT IS DELINQUENCY??

Delinquency

Failing to make your scheduled monthly loan payments will negatively affect your credit.

Late payments stay on your credit history for 7 years. Your lender, loan servicer, and school will begin contacting you

via letters and phone calls, which will continue until you resolve the delinquency.

KNOW WHO YOU OWE AND HOW MUCH and……WHERE ARE YOU GOING???

WHAT IS DEFAULT???

DefaultIf a loan remains delinquent, you will default. If you default, the entire unpaid balance and any accrued collection fees on the applicable loans will become immediately due and payable.

Consequences of default may include any or all of the following: Damage to your credit rating Garnishment of your wages Legal action against you Collection charges (including attorney fees) being assessed against you Loss of deferment eligibility Loss of your professional license An increase in the interest rate on your loan Withholding of your federal and state income tax refunds Loss of eligibility for state and federal financial aid Loss of other state or federal payments

Can’t make your payment?

If you're having trouble making payments on your loans, contact your loan servicer or your school loan advisors (Drew Garland, BRTC Default

Management Coodrinator) as soon as possible to discuss options that may help you.

Options include: Changing repayment plans Deferment, if you meet certain requirements (for example, if you are unable to find

full-time employment, or are experiencing an economic hardship). A deferment allows you to temporarily stop making payments on your loan.

Forbearance, if you don't meet the eligibility requirements for a deferment but are temporarily unable to make your loan payments. Forbearance allows you to temporarily stop making payments on your loan, temporarily make smaller payments, or extend the time for making payments.

If you stop making payments and don't get a deferment or forbearance, your loan could go into default, which has serious consequences!

You must be aware that a deferment or forbearance is for a limited time, and it must be renewed if eligible.

Deferment Criteria

Types of Deferment

In-SchoolGraduate FellowshipRehabilitation

Training ProgramUnemploymentEconomic HardshipMilitary

Length of Deferment

No time limitNo time limitNo time limit

Up to 36 monthsUp to 36 monthsNo time limit

Forbearance Criteria

Discretionary Forbearance

For discretionary forbearances, your lender decides whether to grant forbearance or not.

You can request a discretionary forbearance for the following reasons:

Financial hardship Illness

Mandatory Forbearance

in a medical or dental internship or residency program & meet requirements

Total owed is 20% or more of your total monthly gross income

National service position which you received a national service award

Teaching service that qualifies for teacher loan forgiveness

Qualify for partial payment under U.S Department of Defense SLRP

National Guard but not activated by governor, but not eligible for a military deferment

Financial Literacy

Come to the financial aid office for additional information on Pell and Loans.

Prepare yourself for repayment! Start making a habit of good finances now by

making better financial decisions regarding your student loans. Set a budget and stick to it. Plan your educational goals and be looking at what your total

student loans may be when completed. Do not get loans just to support you and your family! KNOW WHAT YOU ARE DOING HERE AND PLANS FOR

FUTURE KNOW WHO YOU OWE AND HOW MUCH!!

www.nslds.ed.gov

Resources

www.nslds.ed.gov www.direct.ed.gov www.studentloans.gov www.npcc.edu/FinancialAid/fa_conditions.ht

m http://www.consumerfinance.gov/payingforco

llege/costcomparison/ http://www2.ed.gov/offices/OSFAP/DirectLoa

n/BudgetCalc/budget.html http://studentaid.ed.gov/PORTALSWebApp/st

udents/english/IBRPlan.jsp https://studentloans.gov/myDirectLoan/viewS

amplePaymentsTable.action www.discoverar.net

R EMEMBER : YOU AR E OU R STU DEN T EVEN I F YOU GO TO AN OTHER SCHOOL OR STOP

ATTEN DI NG. WE AR E HER E TO HELP YOU !

Questions about your LOANS? Drew Garland Default Management Coordinator

Pocahontas Campus [email protected] (870) 248-4000, Ext. 4022

ForFor other Financial Aid questions, contact the BRTC Financial Aid Office @ (870) 248-4000.

Misty Bradley [email protected] Natasha Rush [email protected]

Jenny Weaver [email protected] (Paragould Campus) Brandi Chester [email protected]

Related Documents