BY HARSHA VARDHAN R IST MFA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BY HARSHA VARDHAN R IST MFA

INTRODUCTIONRetail banking is typical mass-market banking where individual customers use local branches of larger commercial banks. Services offered include: savings and checking accounts, mortgages, personal loans, debit cards,credit cards, and so

HISTORY• Organised banking services started in 15th and 16 century Europe, when banks began opening branches in commercial areas of large cities.

• By the last quarter of 19th century banks were consolidating their branch networks so that they could operate in a more integrated manner.

OBJECTIVE

The main objective of Retail Bank is to provide itstarget market customers a full range of financial products and banking services, giving the customer aone-stop window for all his/her banking requirements

THE FUTURE OF RETAIL BANKING: GLOBAL PERSPECTIVE

The accelerated retail growth has been on a historically low base

Penetration continues to be significantly low compared to global benchmarks

Share of retail credit expected to grow from 22% to 36%

Retail credit expected to grow to Rs.575,000 crs by 2010 at an annualgrowth rate of 25% Dramatic changes expected in the credit portfolio of Banks in the next5 years

Housing will continue to be the biggest growth segment, followed byAuto loans

Banks need to expand and diversify by focussing on non urbansegment as well as varied income and demographic groups

Rural areas offer tremendous potential too which needs to beexploited

Today’s reTail banking secTor is characterized into:

• Multiple products • Multiple channels of distribution• Multiple customer groups

MULTIPLE PRODUCTS

1. Savings Accounts 2. Current Accounts3. Mobile Banking4. Internet Banking 5. Fixed Deposits6. Trading accounts 7. ATM

CHANNELS

• Education loan• home loan• Loans against Securities • Vehicle Loans• Car Loans• Personal Loans

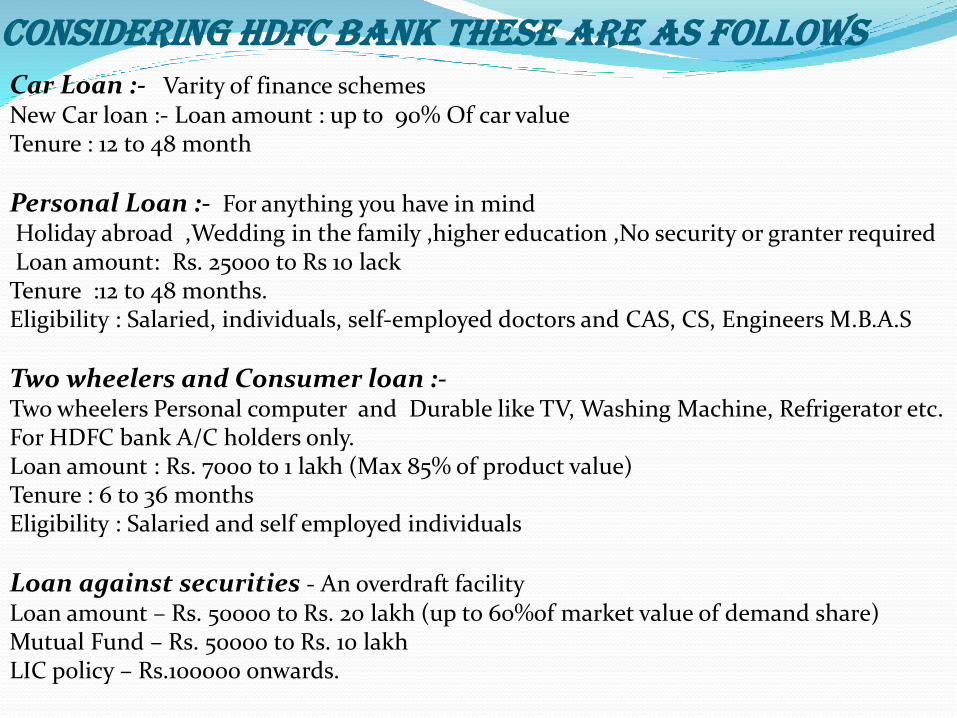

CONSIDERING HDFC BANK THESE ARE AS FOLLOWSCar Loan :- Varity of finance schemesNew Car loan :- Loan amount : up to 90% Of car value Tenure : 12 to 48 month

Personal Loan :- For anything you have in mind Holiday abroad ,Wedding in the family ,higher education ,No security or granter required Loan amount: Rs. 25000 to Rs 10 lackTenure :12 to 48 months.Eligibility : Salaried, individuals, self-employed doctors and CAS, CS, Engineers M.B.A.S

Two wheelers and Consumer loan :-Two wheelers Personal computer and Durable like TV, Washing Machine, Refrigerator etc.For HDFC bank A/C holders only.Loan amount : Rs. 7000 to 1 lakh (Max 85% of product value)Tenure : 6 to 36 monthsEligibility : Salaried and self employed individuals

Loan against securities - An overdraft facilityLoan amount – Rs. 50000 to Rs. 20 lakh (up to 60%of market value of demand share)Mutual Fund – Rs. 50000 to Rs. 10 lakhLIC policy – Rs.100000 onwards.

SOME OF THE INNOVATIVE PRODUCTSv Phone banking v Inter branch banking v Net bankingv Bill payablev Free phone banking v Free mobile banking v Free demand draftv Free International debit cardv Direct salary creditv Overdraft facilityv De MAT A/Cv Joint A/C facilityv Free Demand Draft

RISK INVOLVED IN RETAIL BUSINESS

(a) Databases on credit history are large.(b) Collection mechanisms are poor.(c) Investments in technology are large.(d) Operating efficiency level needs to be very high.(e) Unlike corporate banking, retail banking involves a

large number of small accounts.(f) Demands on processing capabilities are higher.(g) Retail segment is not something you can get into overnight.(h) The right systems and the right – architecture needs to be

put in place first

ADVANTAGES•The bank you are familiar with and which knows you can also offer you a wide range of other services, such as mortgages and insurance.

•Retail banks offer a variety of ways you can access your account and Manage your money

• Retail Banking focuses on individual and small units

•The risk is spread and the recovery is good.

• Surplus deployable funds can be put into use by the banks .

• Customize and wide ranging products are available

•Your money is much more secure than in a box under your bed

DISADVANTAGES

Banks are a business, and they need to make money from looking after yours. If the bank decides to apply charges to your account (within the terms of the account), you may only find out about it afterwards—for example if you accidentally go overdrawn without permission. If you disagree with a charge, you will need to contest it to recover the money.

Winning Strategy

The Bank That Best Addresses And

Anticipates Customers Needs, Delivers

Consistently Higher Quality Service And

Connects To The Customer Via Their

Channel Of Choice Wins

Y.Y.Chin, Ocbc Bank

Related Documents