CRISIL MFIGrading mfR5 Weaker Sections Development Society-Institute of Innovative Technology Transfer and Environment (WSDS Initiate) Date Assigned July 2, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CRISIL MFIGrading

mfR5

Weaker Sections Development Society-Institute of Innovative

Technology Transfer and Environment (WSDS Initiate)

Date Assigned July 2, 2013

1

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

DISCLAIMER

CRISIL's microfinance institution (MFI) Grading reflects CRISIL’s current opinion on the ability of an

MFI to conduct its operations in a scalable and sustainable manner. In the case of NGO-MFIs and

entities with multiple businesses, CRISIL’s MFI Gradings apply only to their microfinance programmes.

The MFI Grading is a one-time exercise and the Grading will not be kept under surveillance. This

grading is valid for a period of one year from the date of assignment. However, CRISIL reserves the

right to suspend, withdraw, or revise the MFI grading at any time, on the basis of any new information

or unavailability of information or any other circumstances brought to CRISIL’s notice, which CRISIL

believes may have an impact on the grading. CRISIL recommends that the user of the Grading seeks a

review of the Grading if the graded institution/microfinance programme experiences significant

changes/events during this period which could impact the graded institution/its grading.

CRISIL MFI Gradings are based on the information provided by the Institution, or obtained by CRISIL

from sources it considers reliable. CRISIL does not guarantee the completeness or accuracy of the

information on which the MFI Grading is based. CRISIL MFI Grading is not a recommendation to

purchase, sell or hold any financial instrument issued by the graded MFI, or to make loans and

donations / grants to the institution. The MFI Grading does not constitute an audit of the graded MFI by

CRISIL.

The MFI Grading Report and the information contained therein are the intellectual property of CRISIL.

The MFI Grading Report should not be reproduced or distributed or communicated directly or indirectly

in any form to any other person or published or copied in whole or in part, for any purpose or by any

means without the prior written permission of CRISIL. The MFI Grading should not be used for

mobilising deposits/savings/thrift/insurance funds/other funds (including equity) from their

members/clients or general public and should not be used in its external communications, promotional

materials or member/client passbooks. CRISIL is not responsible for any errors and especially states

that it has no financial liability, whatsoever, to the subscribers/ users/transmitters/distributors of its MFI

Gradings. For the latest information on any outstanding CRISIL MFI Gradings, please contact CRISIL

RATING DESK at [email protected] or at (+91-22)-3342 3047/3064.

2

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

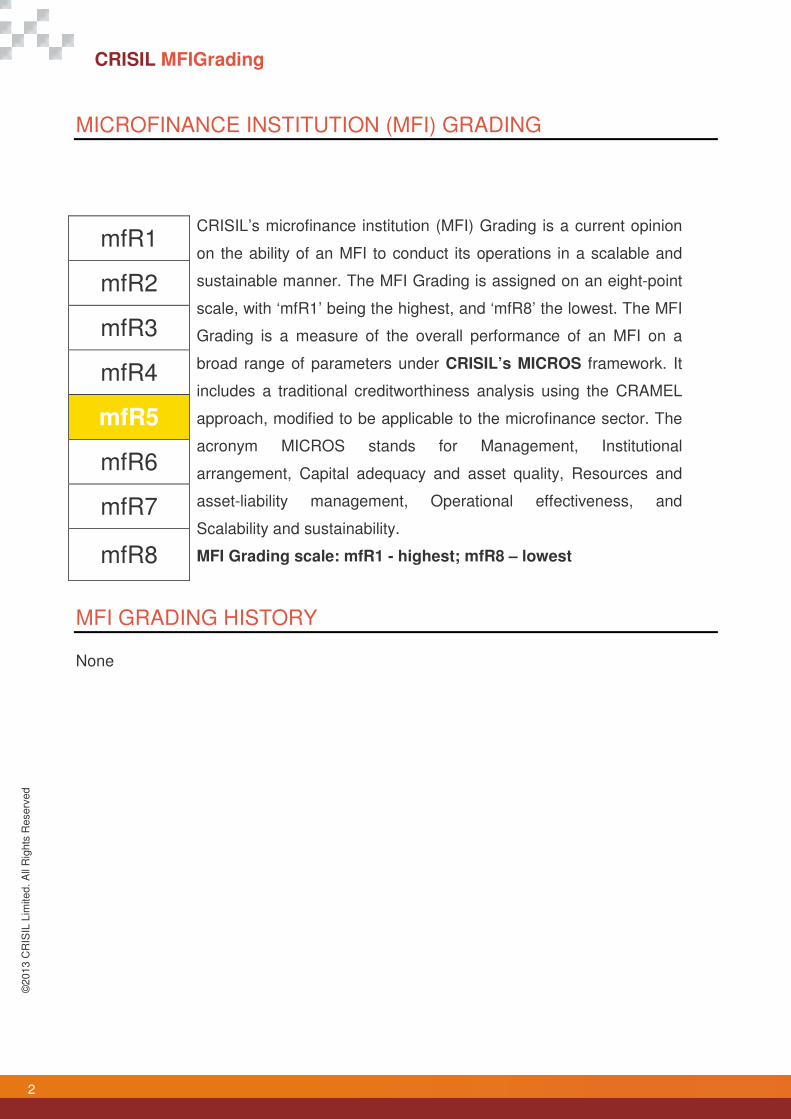

MICROFINANCE INSTITUTION (MFI) GRADING

MFI GRADING HISTORY None

mfR1 CRISIL’s microfinance institution (MFI) Grading is a current opinion

on the ability of an MFI to conduct its operations in a scalable and

sustainable manner. The MFI Grading is assigned on an eight-point

scale, with ‘mfR1’ being the highest, and ‘mfR8’ the lowest. The MFI

Grading is a measure of the overall performance of an MFI on a

broad range of parameters under CRISIL’s MICROS framework. It

includes a traditional creditworthiness analysis using the CRAMEL

approach, modified to be applicable to the microfinance sector. The

acronym MICROS stands for Management, Institutional

arrangement, Capital adequacy and asset quality, Resources and

asset-liability management, Operational effectiveness, and

Scalability and sustainability.

MFI Grading scale: mfR1 - highest; mfR8 – lowest

mfR2

mfR3

mfR4

mfR5

mfR6

mfR7

mfR8

3

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

FACT SHEET

Name of the MFI : Weaker Sections Development Society-Institute of Innovative

Technology Transfer and Environment (WSDS Initiate)

Year of Incorporation : August, 2007

Year of commencement of microfinance programme

: August, 2007

Legal status : Registered under the Societies Registration Act 1860

Managing Director : Mr. Lamkhomang Kipgen

Office address : "Gollut Gens", New Lambulane,

Imphal East - 795 001, Manipur

Tel.: +91 385 2442 730

Mobile: +91 9862008741/+91 8794424451

Email: [email protected], [email protected]

Web: www.wsdsinitiate.org

Bankers and lenders : � Ananya Finance for Inclusive Growth Private Limited

� North Eastern Development Finance Corporation Limited (NEDFi)

� Friends of Women's World Banking (FWWB)

� Kiva International

� Kashi Vishwanath Vida Sama

Statutory Auditors : Kunjabi and Company, Imphal, Manipur

4

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

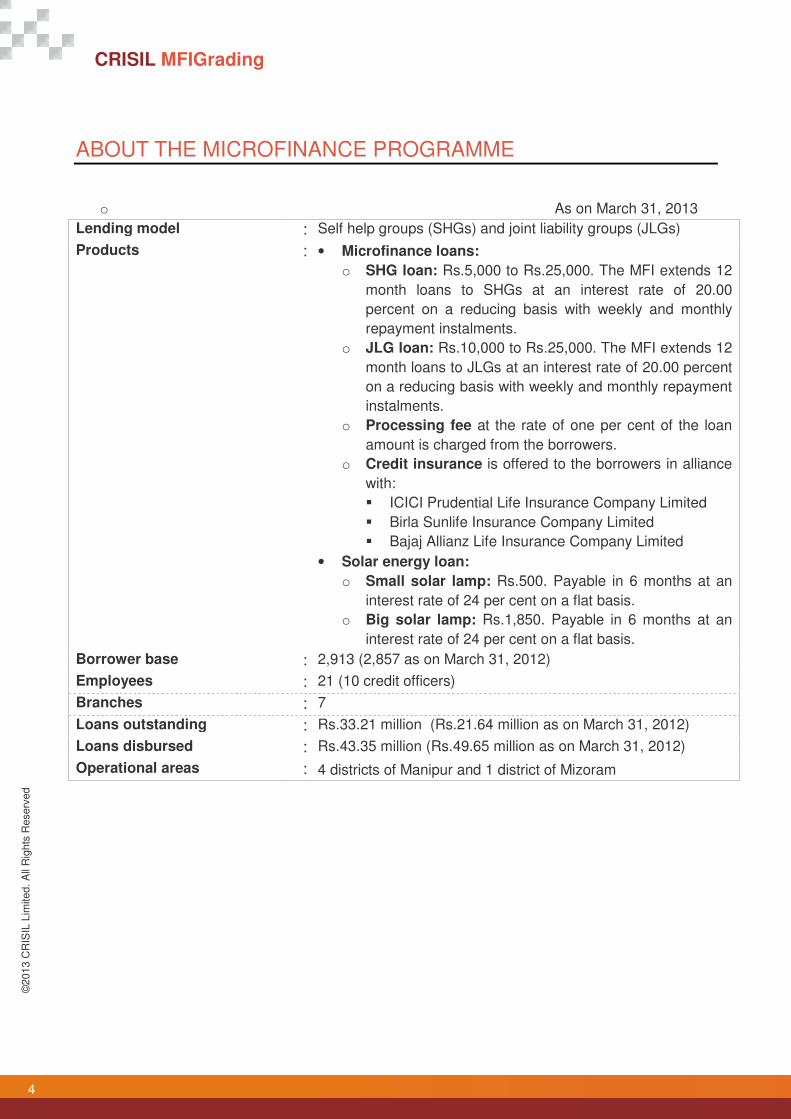

ABOUT THE MICROFINANCE PROGRAMME

o As on March 31, 2013

Lending model : Self help groups (SHGs) and joint liability groups (JLGs)

Products : • Microfinance loans:

o SHG loan: Rs.5,000 to Rs.25,000. The MFI extends 12

month loans to SHGs at an interest rate of 20.00

percent on a reducing basis with weekly and monthly

repayment instalments.

o JLG loan: Rs.10,000 to Rs.25,000. The MFI extends 12

month loans to JLGs at an interest rate of 20.00 percent

on a reducing basis with weekly and monthly repayment

instalments.

o Processing fee at the rate of one per cent of the loan

amount is charged from the borrowers.

o Credit insurance is offered to the borrowers in alliance

with:

� ICICI Prudential Life Insurance Company Limited

� Birla Sunlife Insurance Company Limited

� Bajaj Allianz Life Insurance Company Limited

• Solar energy loan:

o Small solar lamp: Rs.500. Payable in 6 months at an

interest rate of 24 per cent on a flat basis.

o Big solar lamp: Rs.1,850. Payable in 6 months at an

interest rate of 24 per cent on a flat basis.

Borrower base : 2,913 (2,857 as on March 31, 2012)

Employees : 21 (10 credit officers)

Branches : 7

Loans outstanding : Rs.33.21 million (Rs.21.64 million as on March 31, 2012)

Loans disbursed : Rs.43.35 million (Rs.49.65 million as on March 31, 2012)

Operational areas : 4 districts of Manipur and 1 district of Mizoram

5

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

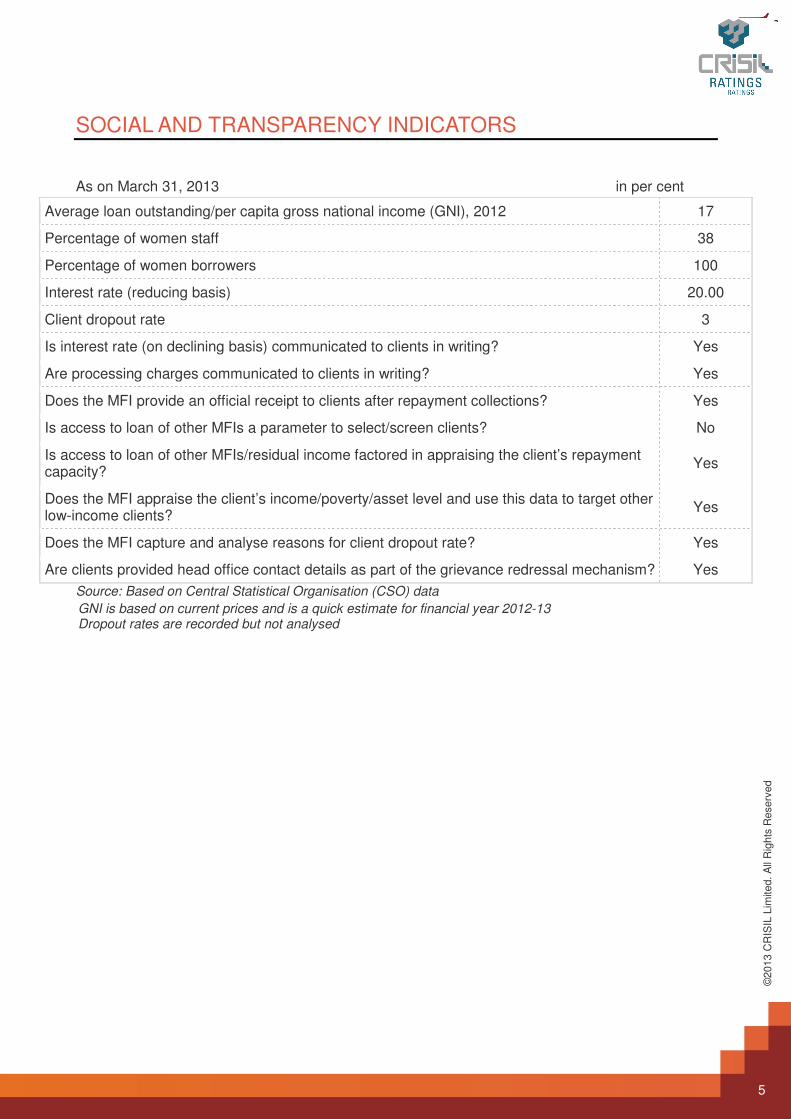

SOCIAL AND TRANSPARENCY INDICATORS

As on March 31, 2013 in per cent

Average loan outstanding/per capita gross national income (GNI), 2012 17

Percentage of women staff 38

Percentage of women borrowers 100

Interest rate (reducing basis) 20.00

Client dropout rate 3

Is interest rate (on declining basis) communicated to clients in writing? Yes

Are processing charges communicated to clients in writing? Yes

Does the MFI provide an official receipt to clients after repayment collections? Yes

Is access to loan of other MFIs a parameter to select/screen clients? No

Is access to loan of other MFIs/residual income factored in appraising the client’s repayment capacity?

Yes

Does the MFI appraise the client’s income/poverty/asset level and use this data to target other low-income clients?

Yes

Does the MFI capture and analyse reasons for client dropout rate? Yes

Are clients provided head office contact details as part of the grievance redressal mechanism? Yes

Source: Based on Central Statistical Organisation (CSO) data GNI is based on current prices and is a quick estimate for financial year 2012-13 Dropout rates are recorded but not analysed

6

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

GRADING RATIONALE CRISIL’s microfinance institution (MFI) grading on WSDS Initiate reflects the following strengths:

• Experienced board and senior management

• Above-average asset quality

• Average earnings profile

• Adequate MIS and loan monitoring software for current level of operation

The above mentioned grading strengths are offset by its:

• Small net worth and scale of operations

• Asset under management concentrated in one district

• Modest resource profile

• Weak cash management practices

Profile

Imphal-based WSDS Initiate was established in 2007 by Mr. Lamkhomang Kipgen. Its

microfinance programme is designed to help women entrepreneurs conduct income-generation

activities, such as running greengroceries, embroidery shops, eateries, cosmetic trading, and

tailoring establishments. In addition to financial inclusion, the NGO-MFI also undertakes social

development projects, delivering education, health awareness, and livelihood services to the rural

poor.

WSDS had 2,913 borrowers and a loan outstanding of Rs.33.21 million as on April 31, 2013.

Manipur can serve as India's gateway to Southeast Asia. WSDS has seven branches across four

districts of Manipur, namely, Senapati, Imphal East, Churachandpur, and Bishnupur. It also has a

branch in the Aizawl district of Mizoram and plans to expand operations to the other north-eastern

states as well. The organisation would also stand to benefit significantly from the proposed Trans-

Asian Railway Network (TARN). The line is expected pass through Manipur, connecting India to

Burma, Thailand, Malaysia, and Singapore.

The loan size varies from Rs.5,000 to Rs.25,000, depending on the repayment capacity of

individual clients, number of loan cycles, type of activity, and type of microfinance loan. The loans

are provided for a one year period with weekly and monthly repayment instalments, and are

offered at an interest rate of 20.00 per cent (reducing) per annum. In addition, a processing fee of

one per cent of the loan amount is collected from each borrower at the time of loan disbursement.

7

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

The NGO-MFI also has tie-up with ICICI Prudential Life Insurance Company Limited, Birla Sunlife

Insurance Company Limited, and Bajaj Allianz Life Insurance Company Limited to offer loan credit

insurance services for its borrowers, for which it collects an insurance fee of one percent of the

loan amount.

8

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

MANAGEMENT

Extensive microfinance experience

• The founders of WSDS have more than two decades of experience in

providing microfinance and social development services in the MFI’s

operational area. CRISIL expects the resultant operational expertise to

enable the MFI to expand to new areas while maintaining portfolio

quality.

Loan monitoring software in place

• The NGO-MFI has been using loan-monitoring software for about a

year. The software is integrated with the accounting package and can

generate various reports, including portfolio at risk (PAR) statement,

loan processing and disbursements, and demand and collection at

branch levels. However, only three of seven branches are

computerised, and the rest maintain manual documentation. This

affects productivity and poses the risk of data inaccuracy.

• The NGO-MFI has a loan monitoring software in place and it is

integrated with the accounting package. Thus, the MFI is generating

important reports on daily basis, which includes portfolio at risk (PAR)

statement, loan processing and disbursements, and demand and

collection at branch levels. However, only three out of seven branches

are computerised and are using the software to generate demand and

collection statements. The remaining branches are maintaining all the

documents manually; this poses risk of data inaccuracy and low

productivity levels. Further this could hinder the HO’s consolidation

process.

Adequate credit appraisal process

• The credit appraisal process at WSDS is decentralised. The branch

head sanctions the loans after proper due diligence, including

verification of data on the applicant’s household income and expenses.

• WSDS tied-up with a credit information bureau (High Mark) in June

2013 but is yet to begin data sharing. Thus it is currently unable to

assess the borrower’s credit and repayment history. CRISIL also

observed that there is no formal mechanism of assessing attendance

history of existing clients.

Moderate internal audit

• WSDS has appointed an employee to verify loan applications, demand

9

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

and collection sheets, and other documents at the branches. The audit

is conducted on a monthly basis at HO and branch levels, and the

findings are shared with the respective BMs. However, the branches

do not send compliance documentation to the HO. CRISIL believes

that the internal audit also has scope for improvement in terms of

capturing more details on operational deviations and field-level

findings.

Weak cash management practices

• WSDS branches follow the practice of next-day deposit of collections,

which results in high cash balance on a daily basis. WSDS has not

availed cash-in-transit and cash-in-safe insurance.

• Further, the branches that aren’t connected to the loan monitoring

system have an inadequate reconciliation system for due receivables

and actual collections. CRISIL thus believes that there is a scope of

theft/ misappropriation and ineffective cash utilisation at the branches.

Limited competition in area of operations

• WSDS’s microfinance operations are in hilly areas which have poor

infrastructure and connectivity. Thus, the NGO-MFI faces limited

competition from other national level large-sized MFIs in its area of

operations.

Social impact by providing credit services to clients having limited access to formal financial services

• WSDS has been operating for six years in hilly areas of Manipur,

where there is limited access to formal financial services. This has led

to financial literacy and empowerment of clients. The organisation

targets clients who have no access to formal financial services and

have not been served by other MFI players. Significant social impact

has been created by micro credit intervention by WSDS.

INSTITUTIONAL ARRANGEMENT

Experienced board and senior management

• WSDS has a seven-member board with over a decade of experience in

microfinance, social development, and the banking and financial

services (BFS) sectors. The senior management team also comprises

professionals with extensive microfinance and development experience.

• WSDS’s senior management comprises professionals with experience

in microfinance and social development activities. The experienced

senior management team would enable the organisation to steer the

10

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

microfinance programme in long term.

• The NGO-MFI has an agreement with Vittana Foundation (a

Washington-based non-profit organisation), under which the it provides

consulting and technical assistance for the education loan program.

CAPITAL ADEQUACY AND ASSET QUALITY

Low capitalisation levels

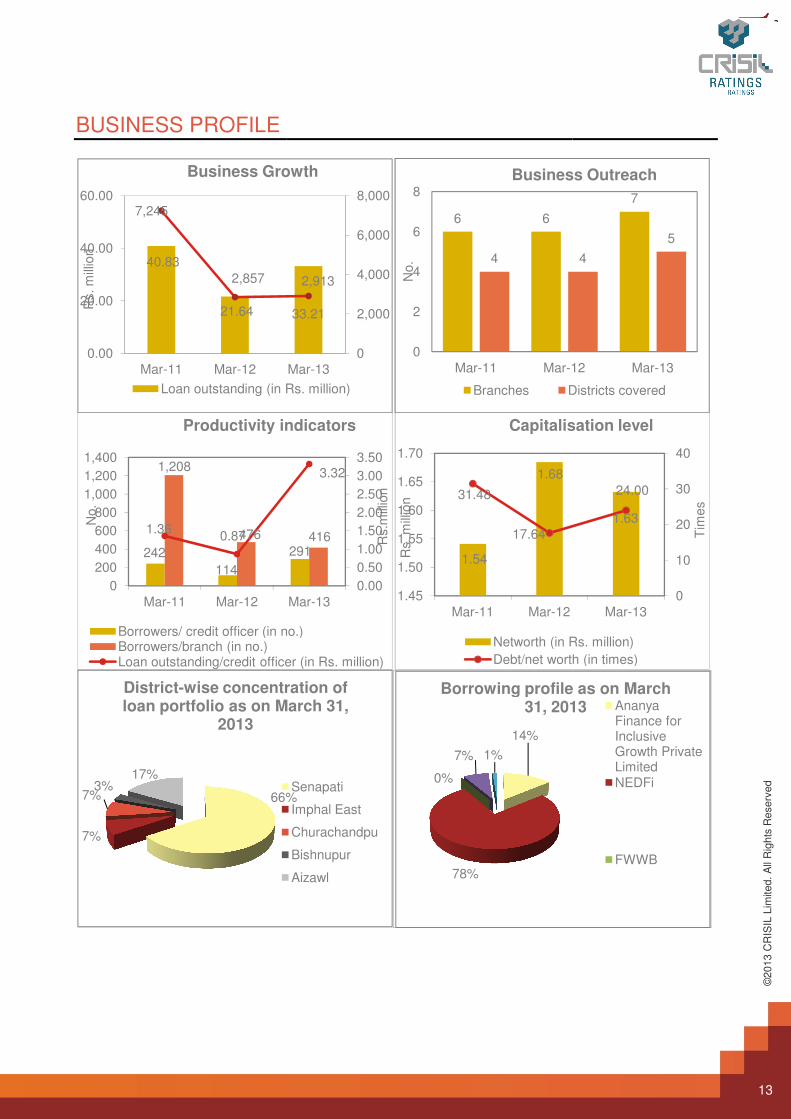

• Compared to the other CRISIL-rated MFIs, WSDS had a small corpus of

Rs.1.63 million as on March 31, 2013. CRISIL expects the corpus to

remain small in the midterm, as the organisation’s fundraising ability is

limited by its legal status as a society.

• The capital adequacy ratio (CAR) declined to 4.69 per cent as on March

31, 2013 from 6.09 per cent as on March 31, 2013, and the debt-to-equity

ratio also declined to 24.00 times from 17.64 times in the same period

due to increase in asset size without corpus infusion. CRISIL expects

gearing to deteriorate further with the planned growth in portfolio and

borrowings.

Above-average asset quality

• Though the MFI is operating in sparsely populated area, it maintained

above-average asset quality with an on-time repayment rate of 99.24 per

cent as on March 31, 2013 and portfolio at risk greater than 90 days

(PAR>90 days) of 0.56 per cent. CRISIL believes that the organisation’s

ability to extend repeat loans and meet credit demands on time will be an

important grading factor.

Significant geographic concentration

• The Senapati district of Manipur accounts for around 66 per cent of the

loan portfolio, which makes WSDS vulnerable to high credit and

operational risks.

• As operations are expected to remain concentrated over the near term,

any adverse credit event in the operational area could affect the MFI’s

capitalisation levels. Its ability to maintain delinquency at acceptable

levels while also pursuing growth remains a key grading sensitivity factor.

11

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

RESOURCES AND ASSET LIABILITY MANAGEMENT

Though it accessed funds from five lender it highly depend on single lender

• The NGO-MFI had outstanding borrowings from five lenders as on

March 31, 2013, out of which top lender accounted for about 77.38 per

cent (Rs.30.19 million) of overall borrowings, with no borrowings from

private and public sector banks.

Moderate resource profile

• CRISIL however expects an improvement in the MFI’s resource profile

as it received funding of Rs.69.60 million in 2012-13. Kashi

Vishwanatha Vidya Samasthe sanctioned Rs.1.00 million, while KIVA

International sanctioned a three-year, interest-free loan of Rs.1.10

million per month.

• The MFI’s average cost of borrowings was also low at 8.72 per cent in

2012-13. CRISIL expects costs to remain moderate as MFI plans to

raise around Rs.70.00 million in the near term to fund portfolio growth.

OPERATIONAL EFFECTIVENESS

Moderate earning profile

• As compared to the previous year, WSDS demonstrated an

improvement in its field-productivity indicators in 2012-13:

o Loans outstanding per credit officer increased to Rs.3.32 million

from Rs.0.87 million

o Loan outstanding per branch increased to Rs.4.74 million from

Rs.3.61 million

• The NGO-MFI has high operating efficiency, with opex improving to 6.69

per cent in 2012-13 from 14.37 per cent for 2011-12. Operational self-

sufficiency (OSS) also improved to 102.26 per cent as on March 31,

2013 from 100.69 per cent as on March 31. 2012.

• CRISIL expects the earnings profile to remain moderate despite an

increase in disbursements and productivity.

12

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

SCALABILITY AND SUSTAINABILITY

• In the six years that it has been operational, WSDS has demonstrated a

profitable track record in the fields of microfinance and social

development. Its experienced board and management team is expected

to help it steer the microfinance programme in long term.

• The key challenges faced by the organisation are weak cash

management practices, geographic concentration, undiversified

borrowings profile, small scale of operations, and small net worth size.

BUSINESS PROFILE

40.83

21.64

7,245

2,857

0.00

20.00

40.00

60.00

Mar-11 Mar-12

Rs. m

illio

n

Business Growth

Loan outstanding (in Rs. million)

242

114

1,208

476 1.360.87

0

200

400

600

800

1,000

1,200

1,400

Mar-11 Mar-12

No.

Productivity indicators

Borrowers/ credit officer (in no.)Borrowers/branch (in no.)Loan outstanding/credit officer (in Rs. million)

66%

7%

7%3%

17%

District-wise concentration of loan portfolio as on March 31,

2013

33.21

2,913

0

2,000

4,000

6,000

8,000

Mar-13

Business Growth

Loan outstanding (in Rs. million)

6 6

4

0

2

4

6

8

Mar-11 Mar-12

No.

Business Outreach

Branches Districts covered

291416

3.32

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Mar-13

Rs.m

illio

n

Productivity indicators

Borrowers/ credit officer (in no.)

Loan outstanding/credit officer (in Rs. million)

1.54

1.68

31.48

17.64

1.45

1.50

1.55

1.60

1.65

1.70

Mar-11 Mar-12

Rs. m

illio

n

Capitalisation level

Networth (in Rs. million)

Debt/net worth (in times)

66%

wise concentration of loan portfolio as on March 31,

Senapati

Imphal East

Churachandpu

Bishnupur

Aizawl

14%

78%

0%

7% 1%

Borrowing profile as on March 31, 2013

13

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

7

4

5

12 Mar-13

Business Outreach

Districts covered

1.63

24.00

0

10

20

30

40

Mar-13

Tim

es

Capitalisation level

Networth (in Rs. million)

Debt/net worth (in times)

Borrowing profile as on March 31, 2013 Ananya

Finance for Inclusive Growth Private LimitedNEDFi

FWWB

14

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

FINANCIAL INDICATORS Income and expenditure statement Rs. million For the year ended March 31, 2015 2014 2013 2012 2011

MFI’s Projections Provisional Audited

Fund based income 17.70 8.98 5.06 10.17 12.23

Interest and finance charges 8.45 3.42 3.00 5.14 5.86

Gross spread 9.25 5.56 2.06 5.03 6.38

Fee based income - - 0.43 0.42 0.73

Total income 17.70 8.98 5.50 10.59 12.96

Gross surplus 9.25 5.56 2.49 5.45 7.11

Personnel expenses 3.11 2.14 1.21 3.28 3.63

Administrative expenses 1.86 1.54 0.98 1.81 1.99

Total expenses 4.97 3.68 2.19 5.09 5.62

Provision for loan loss 1.39 1.17 - 0.04 0.16

Other provisions - - - - 0.06

Total provisions 1.39 1.17 - 0.04 0.23

Depreciation 0.30 0.29 0.18 0.24 0.28

Profit/loss before tax 2.59 0.43 0.12 0.07 0.99

Tax 0.71 - - 0.02 0.20

Profit/loss before revenue grants 1.88 0.43 0.12 0.05 0.78

Grants and donations - - - 0.09* -

Net surplus 1.88 0.43 0.12 0.14 0.78

*Donation for administrative expenses

15

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

Balance sheet Rs. million

As on March 31, 2015 2014 2013 2012 2011

Liabilities MFI’s Projections Provisional Audited

Net worth 2.56 0.68 1.63 1.68 1.54

Borrowings 92.60 40.11 39.17 29.72 48.51

Provision for loan loss - - - 0.13 0.16

Other liabilities and provisions 12.41 10.51 0.28 0.47 0.88

Total current liabilities 12.41 10.51 0.28 0.60 1.05

Total liabilities 107.57 51.30 41.08 32.00 51.10

Assets

Loans and advances 106.48 50.16 33.21 21.79 40.98

Cash and bank balances 0.35 0.16 5.76 3.78 3.49

Total funds deployed 106.84 50.32 39.46 26.13 44.73

Other current assets & advances - - 0.53 4.74 5.06

Net fixed assets 0.73 0.97 1.10 1.13 1.31

Total assets 107.57 51.30 41.08 32.00 51.10

16

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

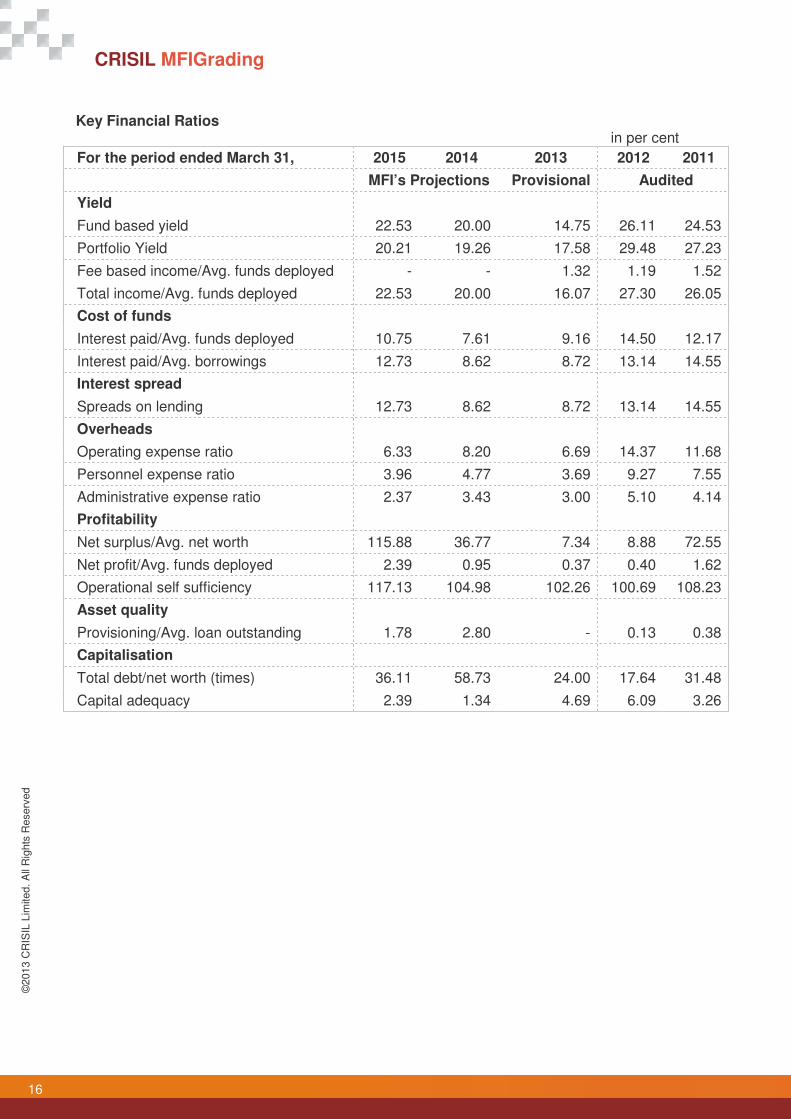

Key Financial Ratios in per cent

For the period ended March 31, 2015 2014 2013 2012 2011

MFI’s Projections Provisional Audited

Yield

Fund based yield 22.53 20.00 14.75 26.11 24.53

Portfolio Yield 20.21 19.26 17.58 29.48 27.23

Fee based income/Avg. funds deployed - - 1.32 1.19 1.52

Total income/Avg. funds deployed 22.53 20.00 16.07 27.30 26.05

Cost of funds

Interest paid/Avg. funds deployed 10.75 7.61 9.16 14.50 12.17

Interest paid/Avg. borrowings 12.73 8.62 8.72 13.14 14.55

Interest spread

Spreads on lending 12.73 8.62 8.72 13.14 14.55

Overheads

Operating expense ratio 6.33 8.20 6.69 14.37 11.68

Personnel expense ratio 3.96 4.77 3.69 9.27 7.55

Administrative expense ratio 2.37 3.43 3.00 5.10 4.14

Profitability

Net surplus/Avg. net worth 115.88 36.77 7.34 8.88 72.55

Net profit/Avg. funds deployed 2.39 0.95 0.37 0.40 1.62

Operational self sufficiency 117.13 104.98 102.26 100.69 108.23

Asset quality

Provisioning/Avg. loan outstanding 1.78 2.80 - 0.13 0.38

Capitalisation

Total debt/net worth (times) 36.11 58.73 24.00 17.64 31.48

Capital adequacy 2.39 1.34 4.69 6.09 3.26

17

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

Annexure

1.1 Outreach summary ................................................................................................... 18

1.2 Human resource and productivity summary .............................................................. 18

1.3 Asset quality ............................................................................................................. 18

1.4 District-wise loan outstanding ................................................................................... 19

18

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

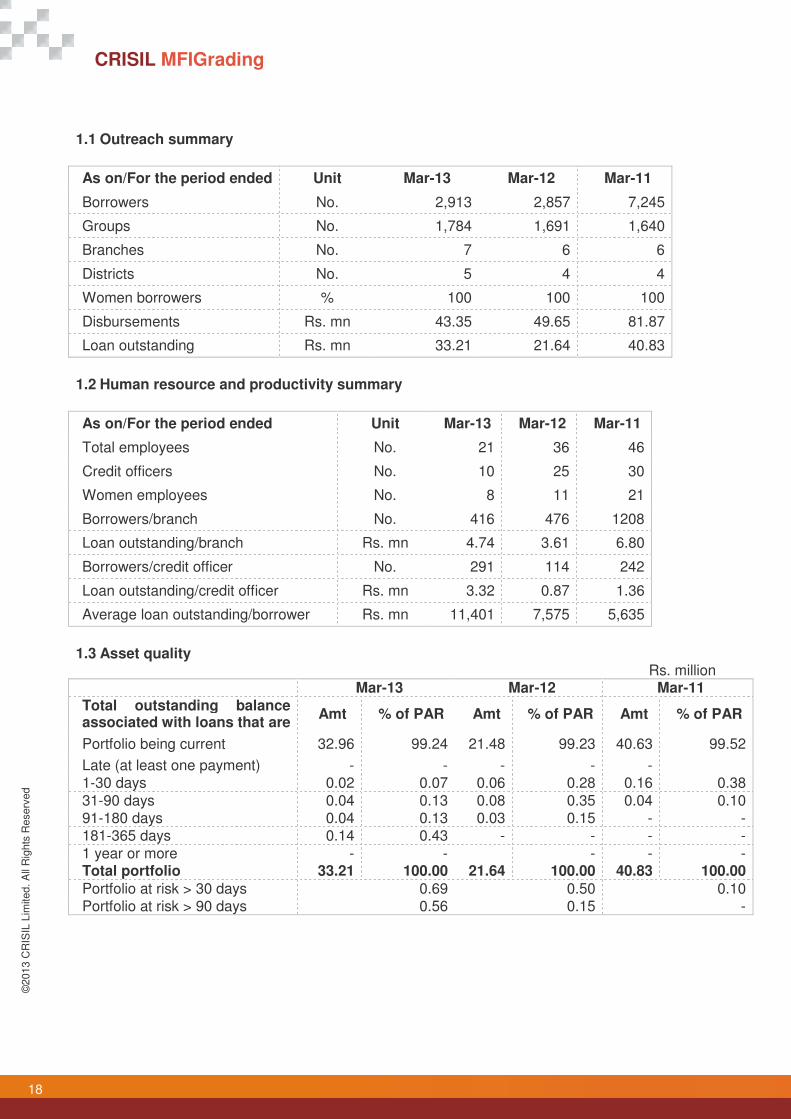

1.1 Outreach summary

As on/For the period ended Unit Mar-13 Mar-12 Mar-11

Borrowers No. 2,913 2,857 7,245

Groups No. 1,784 1,691 1,640

Branches No. 7 6 6

Districts No. 5 4 4

Women borrowers % 100 100 100

Disbursements Rs. mn 43.35 49.65 81.87

Loan outstanding Rs. mn 33.21 21.64 40.83

1.2 Human resource and productivity summary

As on/For the period ended Unit Mar-13 Mar-12 Mar-11

Total employees No. 21 36 46

Credit officers No. 10 25 30

Women employees No. 8 11 21

Borrowers/branch No. 416 476 1208

Loan outstanding/branch Rs. mn 4.74 3.61 6.80

Borrowers/credit officer No. 291 114 242

Loan outstanding/credit officer Rs. mn 3.32 0.87 1.36

Average loan outstanding/borrower Rs. mn 11,401 7,575 5,635

1.3 Asset quality

Rs. million

Mar-13 Mar-12 Mar-11

Total outstanding balance associated with loans that are

Amt % of PAR Amt % of PAR Amt % of PAR

Portfolio being current 32.96 99.24 21.48 99.23 40.63 99.52

Late (at least one payment) - - - - -

1-30 days 0.02 0.07 0.06 0.28 0.16 0.38

31-90 days 0.04 0.13 0.08 0.35 0.04 0.10 91-180 days 0.04 0.13 0.03 0.15 - - 181-365 days 0.14 0.43 - - - -

1 year or more - -

- - - Total portfolio 33.21 100.00 21.64 100.00 40.83 100.00

Portfolio at risk > 30 days 0.69 0.50 0.10 Portfolio at risk > 90 days 0.56 0.15 -

19

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

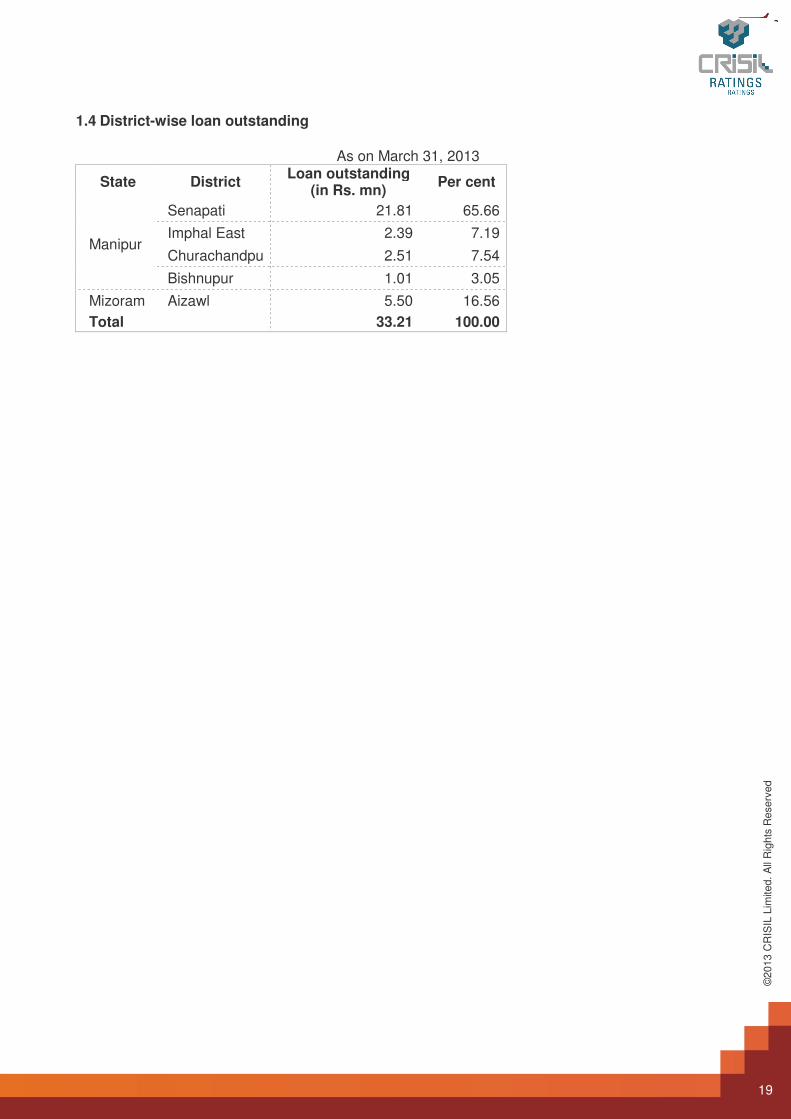

1.4 District-wise loan outstanding

As on March 31, 2013

State District Loan outstanding

(in Rs. mn) Per cent

Manipur

Senapati 21.81 65.66

Imphal East 2.39 7.19

Churachandpu 2.51 7.54

Bishnupur 1.01 3.05

Mizoram Aizawl 5.50 16.56

Total 33.21 100.00

20

©2013 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

This page is intentionally left blank

Contact Us

Analytical Contacts

Mr. Yogesh Dixit Director

[email protected] +91 22 3342 3037

Mr. T Raj Sekhar Associate Director

[email protected] +91 44 4226 3614

CRISIL House, Central Avenue, Hiranandani Business Park Powai, Mumbai 400 076 Phone: + 91 22 3342 3000 Fax: + 91 22 3342 3001 Email: [email protected] www.crisil.com

Related Documents

![Arohan Grading RR · 2019. 8. 1. · I p.]. Annexure~1 Arohan Financial Services Pvt. ltd MFI Grading Report Year of incorporation 2006 as NBFC Legal status NBFC.MFI 'MFI2+' Year](https://static.cupdf.com/doc/110x72/610b811e1b27231d361b0f6b/arohan-grading-rr-2019-8-1-i-p-annexure1-arohan-financial-services-pvt.jpg)