Distribution: CLT Members Head of HR Strategy Head of Information Technology Head of Democratic Services Head of Legal Head of Audit & Risk Management Corporate Communications Manager Review undertaken by: Corporate Manager (Improvement) Lynda Baker – Audit Managers Member with Portfolio - Finance Member with Portfolio –Governance August 2006 Audit Manager – Audit Commission CORPORATE GOVERNANCE REVIEW SELF ASSESSMENT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Distribution: CLT Members Head of HR Strategy Head of Information Technology Head of Democratic Services Head of Legal Head of Audit & Risk Management Corporate Communications Manager Review undertaken by: Corporate Manager (Improvement) Lynda Baker – Audit Managers Member with Portfolio - Finance Member with Portfolio –Governance August 2006 Audit Manager – Audit Commission

CORPORATE

GOVERNANCE REVIEW

SELF ASSESSMENT

1

PREFACE The term “corporate governance” owes its origins to the “Report of the Committee on Financial Aspects of Corporate Governance”, which was commissioned by Cadbury-Schweppes in 1992 as a result of concern arising from the activities of companies such as BCCI and Maxwell Communications. The Cadbury Report, as it is sometimes referred to, looked at those aspects of corporate governance specifically related to financial reporting and accountability – specifically the control and reporting functions of PLC boards and the role of auditors. The Cadbury Report defined corporate governance as “the system by which organisations are directed and controlled”. After the publication of the Cadbury Report the public sector recognised its value – particularly as this was the time of the Nolan Committee and concerns of conduct in public life – and started to look at corporate governance but tended to focus more on the accountability and control aspects of governance. There followed a series of initiatives to improve corporate governance in the different services of the public sector, however there was no major work undertaken in local government. Much of the present Government’s modernising agenda – democratic renewal, community leadership, accountable and responsive services etc – concerns the need for authorities to review the various processes and systems they have for managing both their own internal affairs and their relationships with key stakeholders. Together, these systems comprise corporate governance and are directly relevant to councils and to the government’s aim of democratic renewal. As part of the modernising agenda councils will be subject to a “Comprehensive Performance Assessment” by the Audit Commission. It is anticipated that when making this judgement the Commission will take into account the outcomes of a corporate governance self-assessment – which will have been undertaken by the Council – and the content of a “corporate governance code” which will have been developed using the outcomes of the self-assessment. In anticipation of this an initial self-assessment of corporate governance at Milton Keynes Council is being undertaken as part of the Local Governance Overview and Scrutiny Committee review of corporate governance. The assessment uses the framework jointly developed by CIPFA and the Society of Local Authority Chief Executives. This report outlines the methodologies of the exercise, its outcomes and conclusions.

2

Contents Page

1. Introduction 3

2. Methodology 4

3. Dimension 1 – evaluation 6

4. Dimension 2 – evaluation 12

5. Dimension 3 – evaluation 16

6. Dimension 4 – evaluation 22

7. Dimension 5 – evaluation 26

8. Conclusions and action plan 29

9. Code of corporate governance 34

3

SECTION 1 INTRODUCTION

1. Corporate Governance is a framework, which sets out how a local authority directs and controls its functions and relates to its community. This framework :

• sets out the controls that an authority needs in order to function effectively;

• ensures a connection between the democratic process, strategy, policy and organisation;

• ensures probity, lawfulness, compliance with standards and sound ethics;

• ensures openness and inclusivity in dealing with stakeholders; • ensures the effective overall management of the authority including

performance monitoring.

2. CIPFA (Chartered Institute of Public Finance and Accountancy) and SOLACE (Society of Local Authority Chief Executives) have issued guidance relating to “corporate governance in local government”. They have sought to set out a framework which is intended to be followed as best practice for establishing a locally adopted code of corporate governance and for making adopted practice open and explicit.

3. The guidance indicates that an authority must be able to demonstrate that it is complying with the underlying principles of good governance which are:

• openness and inclusivity; • integrity; • accountability.

4. If we at Milton Keynes Council are to do this, then these principles need to be translated into a framework which seeks to ensure that they are fully integrated into the conduct of the authority’s business and so establish a means of demonstrating compliance. We need to demonstrate that our systems and processes are:

• monitored for their effectiveness in practice; • subject to review on a continuing basis to ensure that they are up

to date; • comply with the principles of corporate governance.

4

SECTION 2 METHODOLOGY The approach to this self assessment exercise was guided by best practice in corporate governance including the use of guidance notes and framework produced by CIPFA and Solace. There are five dimensions set out within this framework:

1) Community focus – the extent to which a council is devoting its efforts to the things that matter to local citizens.

2) Service delivery arrangements – the extent to which services

deliver what local people expect, and what the council itself requires.

3) Structures and process – the extent to which a council has the

right structure of decision making and business processes to conduct its affairs safely and effectively.

4) Risk management and internal control – the extent to which the

council has an adequate understanding of service and financial risk, and has made provision for it.

5) Standards of conduct – the extent to which the council has ways

of setting standards of conduct and regulating the behaviour of its members and officers to achieve them.

Additionally we looked at the following issues:

1) the extent to which the council complies with the principles and elements of corporate governance as set out in the framework;

2) the identification of systems, processes and documentation that provide evidence of compliance;

3) areas where improvements can be made.

5

The questionnaire framework The self-assessment questionnaire – has been designed taking into account the CIPFA/Solace guidance notes. For each dimension:

1) the questionnaire makes a number of statements which require evaluation – column 1

2) alongside each statement are listed source documents, processes and

documentation that provide evidence of compliance – column 2

3) some examples of current practice of compliance, although not an exhaustive list – column 3

4) suggestions for improvement – column 4

5) self assessment score – column 5

Scoring We scored the questionnaire by:

1) evaluating how well we thought the council complied with each statement and

2) identifying what evidence was available to confirm that evaluation

A numerical value was then assigned to each judgement to indicate how well it is thought the council performed. A score of 0 would indicate “very poor” and a score of 10 would indicate “best practice”. This review was undertaken during October and November 2005 by Lynda Baker, Audit Manager.

6

SECTION 3 : Dimension 1 - Community Focus The guidance states that through carrying out our general and specific duties and responsibilities and their ability to exert wider influence Milton Keynes Council should:

� work for and with their communities

� exercise leadership in their local communities, where appropriate

� undertake an “ambassadorial” role to promote the well-being of their area, where appropriate, through maintaining effective arrangements:

� for explicit accountability to stakeholders for the authority’s performance and its effectiveness in the delivery of services and sustainable use of resources;

� demonstrate integrity in the authority’s dealings in building effective relationships and partnerships with other public agencies and the private voluntary sectors;

� demonstrate openness in all their dealings;

� demonstrate inclusivity by communicating and engaging with all sections of the community to encourage active participation;

� develop and articulate a clear and up to date vision and corporate strategy in response to community needs.

Are we are addressing these issues?

1. Does the council have clear ambitions and a shared and realistic vision for the future of the area with a strategy to deliver it?

2. Does the council communicate clearly with the community and stakeholders about what it is doing and seeks and takes account of these views?

3. Does the council have a clear focus on the services it provides and the community it provides them to?

7

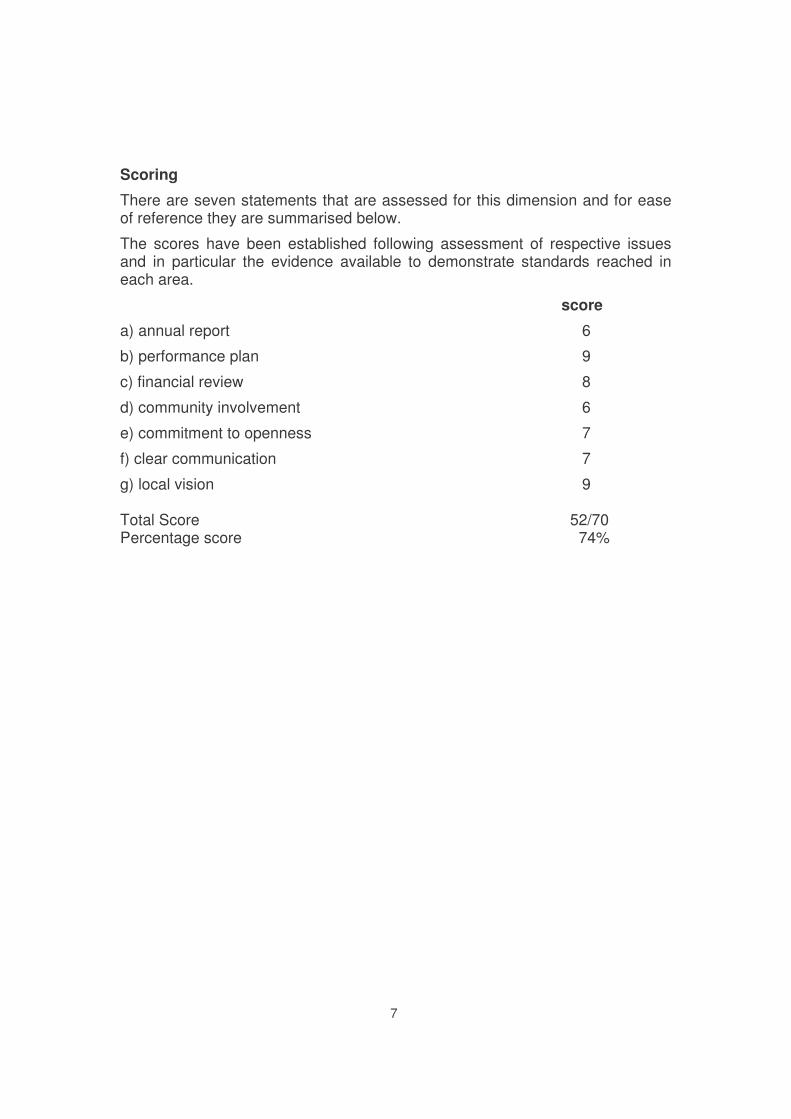

Scoring

There are seven statements that are assessed for this dimension and for ease of reference they are summarised below.

The scores have been established following assessment of respective issues and in particular the evidence available to demonstrate standards reached in each area.

score

a) annual report 6

b) performance plan 9

c) financial review 8

d) community involvement 6

e) commitment to openness 7

f) clear communication 7

g) local vision 9 Total Score 52/70 Percentage score 74%

8

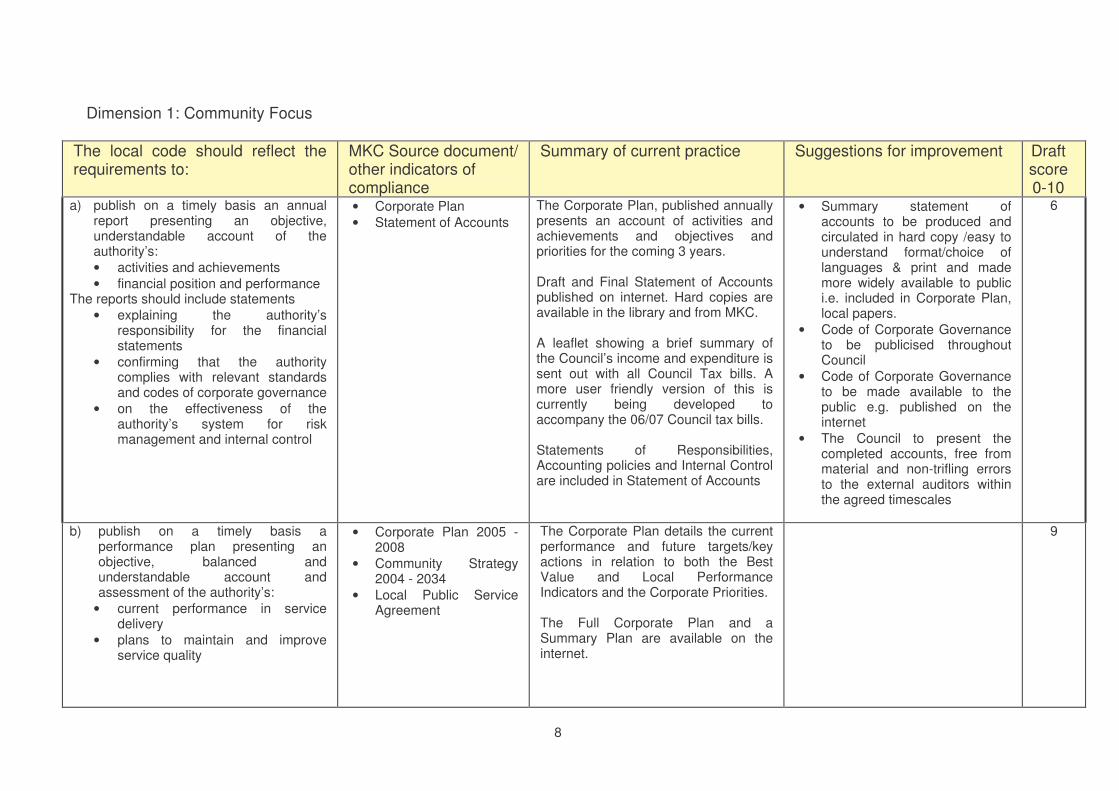

Dimension 1: Community Focus

The local code should reflect the requirements to:

MKC Source document/ other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

a) publish on a timely basis an annual report presenting an objective, understandable account of the authority’s: • activities and achievements • financial position and performance

The reports should include statements • explaining the authority’s

responsibility for the financial statements

• confirming that the authority complies with relevant standards and codes of corporate governance

• on the effectiveness of the authority’s system for risk management and internal control

• Corporate Plan • Statement of Accounts

The Corporate Plan, published annually presents an account of activities and achievements and objectives and priorities for the coming 3 years. Draft and Final Statement of Accounts published on internet. Hard copies are available in the library and from MKC. A leaflet showing a brief summary of the Council’s income and expenditure is sent out with all Council Tax bills. A more user friendly version of this is currently being developed to accompany the 06/07 Council tax bills. Statements of Responsibilities, Accounting policies and Internal Control are included in Statement of Accounts

• Summary statement of accounts to be produced and circulated in hard copy /easy to understand format/choice of languages & print and made more widely available to public i.e. included in Corporate Plan, local papers.

• Code of Corporate Governance to be publicised throughout Council

• Code of Corporate Governance to be made available to the public e.g. published on the internet

• The Council to present the completed accounts, free from material and non-trifling errors to the external auditors within the agreed timescales

6

b) publish on a timely basis a performance plan presenting an objective, balanced and understandable account and assessment of the authority’s:

• current performance in service delivery

• plans to maintain and improve service quality

• Corporate Plan 2005 - 2008

• Community Strategy 2004 - 2034

• Local Public Service Agreement

The Corporate Plan details the current performance and future targets/key actions in relation to both the Best Value and Local Performance Indicators and the Corporate Priorities. The Full Corporate Plan and a Summary Plan are available on the internet.

9

9

The local code should reflect the requirements to:

MKC Source document/ other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

c) put in place proper arrangements for the independent review of the financial and operational reporting processes

• Annual Audit Letter & other Audit reports

• Overview & Scrutiny reports

• Inspectorate reports • Internal Audit reports • Service plans • Medium Term Financial

Strategy

The Annual Audit letter from external audit reports on this other areas reviewed, and is reported to CLT and the Performance Review and Audit Panel, and published on the internet. Internal Audit report to the Performance Review and Audit Panel Inspectorate reports are reported to Leaders and relevant Committees. Overview and Scrutiny function in place All inspection reports are published on the internet

• A separate audit committee to be established, as opposed to the current duties of the committee being undertaken by the Performance Review and Audit Panel.

• Develop mechanisms to ensure the Council’s Medium Term Financial Strategy is communicated effectively to staff and stakeholders

8

d) put in place proper arrangements designed to encourage individuals and groups from all sections of the community to engage with, contribute to and participate in the work of the authority and put in place appropriate monitoring processes to ensure that they continue to work in practice.

• Community Strategy • Consultation Strategy • Consultation Toolkit • Tenant Participation

Compact • Area Consultative

Forums • Service Charters

Creating social inclusion is one of the specified Corporate Priorities MKC has recently introduced a Consultation Strategy and toolkit to ensure consultations are inclusive, of consistent standards, effective and impact on service provision. Community engagement through consultation activities, local media, Live MK,(Council paper), leaflets, Council website, range of leaflets, local Forums and Panels, surveys. MKC Listening Days – the public talk directly to Cabinet members and Officers.

• Improve publicity of ‘listening days’ e.g. posters in libraries.

• Include skills in supporting community involvement activities / consultation within the corporate training programme

• The consultation strategy and toolkit should be used throughout the Council whenever any formal consultation activities are undertaken throughout the Council to ensure a consistent and inclusive process is followed.

6

10

The local code should reflect the requirements to:

MKC Source document/ other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

Tenants Forums – tenants are actively involved in decisions relating to their properties / estates It is widely publicised that the public may ask questions and speak at Cabinet and Committee meetings.

e) make an explicit commitment to openness in all of their dealings, subject only to the need to preserve confidentiality in those specific circumstances where it is proper and appropriate to do so, and by their actions and communications deliver an account against that commitment.

• Constitution • Provision for public to

attend Council meetings • Council Publication

scheme under FOI • Publication of Audit

Reports • Community Strategy • LiveMK

The Public Charter, published on the internet, states ’We want to be an open and transparent public body from which citizens can get the information they are entitled to without difficulty or delay. Access to information Procedure rules in the constitution. Publication scheme available on internet website. Council meetings are open to the public. The agenda, reports and minutes for meetings of full council, committees and scrutiny panels are made available to the public on the internet. Publication of Forward Plan for Cabinet Community involvement through consultation activities.

• Commitment to openness to be specifically stated in the Corporate Plan

• Publish Internal Audit reports on the internet unless specifically exempt under one of the criteria of the Freedom of Information Act or other statutory legislation. NB This process began in December 2005.

• The internet search facility should be improved to enable the public to obtain information from Council meetings, without the current requirement of knowing the date of the meeting and committee concerned to obtain relevant information.

7

11

The local code should reflect the requirements to:

MKC Source document/ other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

f) establish clear channels of communication with all sections of their community and other stakeholders and put in place proper monitoring arrangements to ensure that they operate effectively.

• Intranet • Mki Observatory • Live MK • Complaints Procedure • Consultation strategy • Website • LiveMK

The Council has a well-publicised and monitored complaints system which identifies learning outcomes Consultation strategy – emphasises need to include ‘hard to reach’ members of community. MKC publications have a corporate identity The Council is working to fully implement the LGA Reputation Programme. The Council has an internal communication strategy.

• All managers should ensure that the corporate templates are used for their documents and publications to reinforce the Councils corporate identity.

7

g) ensure that a vision for their local communities and their strategic plans, priorities and targets are developed through robust mechanisms and in consultation with the local community and other key stakeholders and that they are clearly articulated and disseminated.

• Community Strategy • Consultation Strategy • Consultation toolkit • Corporate Plan

Councils aims and objectives are published in the Corporate Plan and on several other Corporate documents as well as on the internet Working with the Local Strategic Partnership Progress in relation to Corporate Priorities is reported to Cabinet on a 6 monthly basis Annual publication of the Corporate Plan and Community Strategy Extensive consultation feeding into the strategic planning process

9

12

SECTION 4 :

Dimension 2 Service delivery arrangements This dimension looks at how well a council provides services and of their potential to improve. The framework states that a council should ensure that continuous improvement is sought. Agreed policies are implemented and decisions are carried out by maintaining arrangements which:

� discharge their accountability for service delivery at a local level

� ensure effectiveness through setting targets and measuring performance

� demonstrate integrity in dealings with service users and developing partnerships to ensure the ‘right’ provision of services locally

� demonstrate openness and inclusivity through consulting with key stakeholders, including service users

� are flexible so that they can be kept up to date and be adapted to accommodate change and meet user wishes

Are we are addressing these issues?

1. Has the council effectively implemented its legal obligations to secure service improvement?

2. Does the council procure appropriately to provide better service provision?

3. Does the council innovate and implement new initiatives and extend its ICT to improve service provision?

Scoring There are six statements that are assessed for this dimension and for ease of reference they are summarised as: Score

a) established targets and standards 7

b) management information systems 7

c) performance monitoring 6

d) resourcing of priorities 5

e) effective partnerships 8

f) response to auditors 7 Total score 40/60 Percentage sore 67%

13

Dimension 2: Service Delivery Arrangements

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

a) set standards and targets for performance in the delivery of services on a sustainable basis and with reference to equality policies

• Medium term plans • Medium Term Financial

Strategy • Service plans • Best Value and Local

Performance Indicators • Appraisals • SLA’s • A guide to Performance

Management • Corporate Equalities

plan • Comprehensive

Equalities Policy • Sustainable

Development Policy • Local Agenda 21

Strategy

All managers to attend Performance management training Annual staff appraisals result in individual action plans and targets E-learning package on equalities and diversity recently developed Equality policies are covered in Corporate Inductions Targets for services and performance against these are published in the Corporate Plan Medium Term Plans and Service Plans set specific objectives and targets for service areas. Progress against LA21 is monitored and actions identified to improve compliance. The Council is working towards achieving Level 3 Equality Standard by January 2007

• Revise Medium Term and Service Planning to be more simple and focused on the delivery of outcomes.

7

14

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

b) put in place sound systems for providing management information for performance measurement purposes

• Service Plans • Appraisals • Budget monitoring

reports • Client Officers • Local, statutory and

Best Value PI’s

Report to Performance Management and Audit Review Committee on a two-monthly basis All services have local performance indicators, recorded in the medium term plans, which are monitored and reported upon

• The central database of Performance indicators currently being developed should record both national and local performance indicators, and information from this made readily available to the public.

7

c) monitor and report performance against agreed standards and targets and develop comprehensive and understandable performance plans

• As above • Performance Review

and Audit Panel • Budget monitoring

Client Officers monitor performance of the HBS Partnership contract against SLA’s Cabinet, Performance Review and Audit Panel, CLT, DMT’s, team meetings all monitor performance at the respective levels. A monthly basket of performance indicators is published on the internet.

• Undertake a regular review of the Council’s local indicators to ensure that they measure the critical performance issues

• Map performance measures to the Corporate objectives and priorities

• Progress against priorities, as reported to Cabinet, to be published on the Internet.

6

d) put in place arrangements to allocate resources according to priorities

• Budget setting process • 3 year budget plan/

capital plan • Corporate Plan • Service plans • Medium Term Plans

Strategic Objectives and Corporate Priorities set Budget setting process Medium Term Planning Process The Medium Term Financial Strategy is a 3 year plan, updated annually, which aims to ensure that priorities are affordable and met. Service Planning process

• Review the links between the Council’s strategies and planning as part of the MTP process and improve the financial and activity analysis of the strategies

• Consider undertaking a zero-based budget setting process – review of budget setting process

5

15

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

e) foster effective relationships and partnerships with other public sector agencies and the private and voluntary sectors and consider outsourcing where it is efficient and effective to do so in delivering services to meet the needs of the local community and put in place processes to ensure that they operate effectively in practice.

• LSP • Community strategy • Inter Authority groups

The Council works in partnership with a wide range of statutory and community organisations to ensure that its services Are provided in the most efficient and effective ways and that its residents receive value for money. These partnerships include HBS, the PCT, the LSP, Central Buying Consortium Contractors performance is regularly reviewed by client officers and Directorates Internal Audit review contract monitoring.

• The success of partnerships, financially and with regard to the achievement of aims, should be formally monitored.

8

f) respond positively to the findings and recommendations of external auditors and statutory inspectors and put in place arrangements for the effective implementation of agreed actions.

• Annual audit letter and other Audit reports

• Inspectorate reports such as OFSTED

• Post inspection Action plans

Required actions are fed into the medium term planning process.

• Services should consolidate recommendations from all parties and produce Action Plans to address these issues. Copies of the Action Plans should be held centrally by ACE (S&P)

• Internal Audit should review implementation of these action plans as part of the internal audit process.

• External Audit should copy Internal Audit and the Performance Review and Audit Panel into every report.

7

16

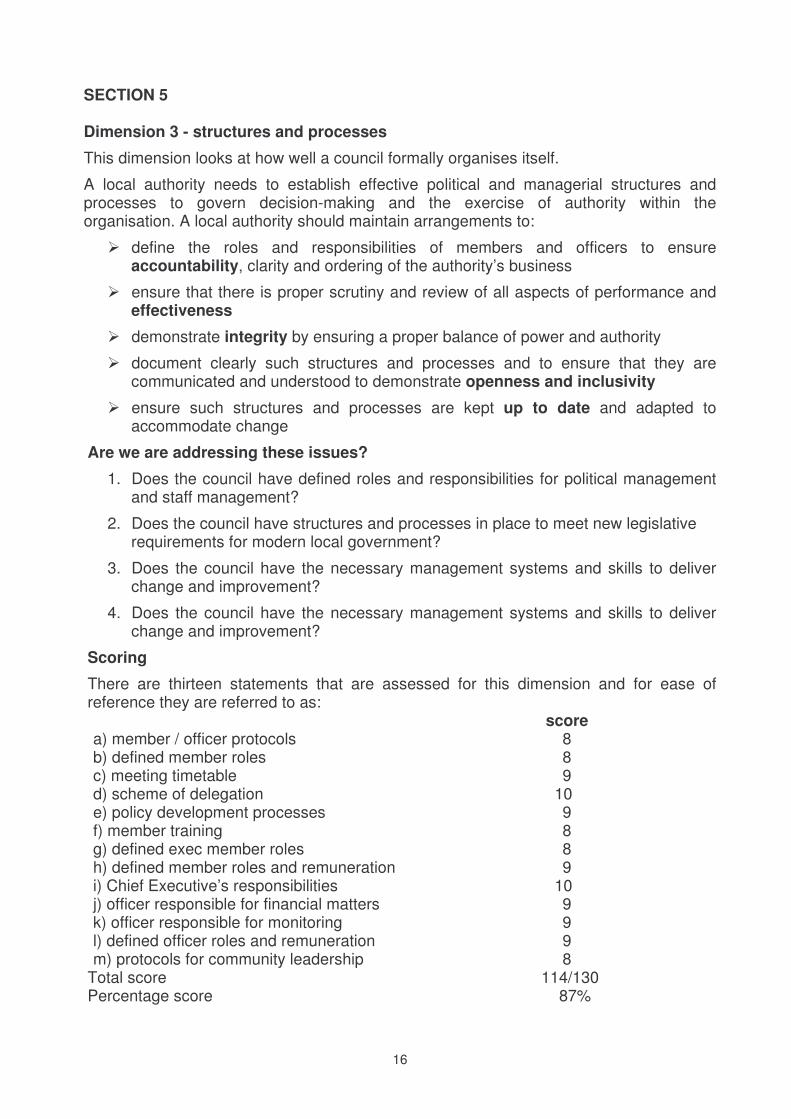

SECTION 5 Dimension 3 - structures and processes

This dimension looks at how well a council formally organises itself.

A local authority needs to establish effective political and managerial structures and processes to govern decision-making and the exercise of authority within the organisation. A local authority should maintain arrangements to:

� define the roles and responsibilities of members and officers to ensure accountability, clarity and ordering of the authority’s business

� ensure that there is proper scrutiny and review of all aspects of performance and effectiveness

� demonstrate integrity by ensuring a proper balance of power and authority

� document clearly such structures and processes and to ensure that they are communicated and understood to demonstrate openness and inclusivity

� ensure such structures and processes are kept up to date and adapted to accommodate change

Are we are addressing these issues?

1. Does the council have defined roles and responsibilities for political management and staff management?

2. Does the council have structures and processes in place to meet new legislative requirements for modern local government?

3. Does the council have the necessary management systems and skills to deliver change and improvement?

4. Does the council have the necessary management systems and skills to deliver change and improvement?

Scoring

There are thirteen statements that are assessed for this dimension and for ease of reference they are referred to as:

score a) member / officer protocols 8 b) defined member roles 8 c) meeting timetable 9 d) scheme of delegation 10 e) policy development processes 9 f) member training 8 g) defined exec member roles 8 h) defined member roles and remuneration 9 i) Chief Executive’s responsibilities 10 j) officer responsible for financial matters 9 k) officer responsible for monitoring 9 l) defined officer roles and remuneration 9 m) protocols for community leadership 8

Total score 114/130 Percentage score 87%

17

Dimension 3: Structures and Processes

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

Balance of Power and Authority a) put in place clearly documented

protocols governing relationships between members and officers

• Constitution- • Code of conduct (3.1)

Protocol on member – officer relationships included in Constitution Membership responsibilities and decision making is included in the Constitution

• Corporate inductions to include reference to Protocol on member officer relations as contained within the Constitution

• Code of conduct to be reviewed annually by standards Committee.

8

b) ensure that the relative roles and responsibilities of executive and other members, members generally and senior officers are clearly defined

• Constitution • Records of decisions • Job descriptions

Scheme of delegation, roles, responsibilities and functions are defined in the Constitution Clear records of Council/Committee/ Cabinet Decisions are maintained

• A generic job description to be produced for members and specific job descriptions for those with special responsibilities

8

Rules and Responsibilities – Members c) ensure that members meet on a formal

basis regularly to set the strategic direction of the authority and to monitor service delivery

• Calendar of Council meetings

• Forward Plan – Key decisions

• Agenda / minutes • Corporate plan • Strategic Objectives • Corporate Priorities • Financial Regulations

There is a planned and published Calendar of Council, Cabinet and Committee meetings Forward plan of key decisions is published Regular meetings are held between CLT and Cabinet to address strategic planning Performance Review & Audit Panel monitors service delivery The capital strategy is linked to the Corporate Objectives

• Develop mechanisms for reporting key financial health indicators to Members.

9

18

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

d) develop and maintain a scheme of delegated or reserved powers which should include a formal schedule of those matters specifically reserved for the collective decision of the authority

• Constitution – scheme of delegation

Comprehensive scheme of delegation in place – adopted and amended by Full Council The scheme of delegation is reviewed as any changes to the structure occur

10

e) put in place clearly documented and understood management processes for policy development implementation and review and for decision making, monitoring, and control and reporting and formal procedural and financial regulations to govern the conduct of the authority’s business

• Constitution • Overview

Committees/ Panels • Policy Development

Committees

The Business Management Group monitor and review the operation of the Constitution. The Constitution includes several documents relating to procedural rules e.g. financial procedures, contracts procedures, business management procedures Constitution documents Terms of Reference of Committees Members receive training on their ’role in policy development’ Pre-decision scrutiny of all Policy Framework and other major policy documents undertaken by the relevant Policy Development Committee.

• Regular reviews of significant Corporate Policies should be undertaken to ensure that they are relevant, up-to-date and reflect the Council’s culture. Each service area should timetable a review date for all policies for which they have responsibility.

9

f) put in place arrangements to ensure that members are properly trained for their roles and have access to all relevant information advice and resource as necessary to enable them to carry out their roles effectively

• Members Training • Members induction • Members handbooks • Reports to

committees

Members provided with IT training and resources. New members are provided with booklets and induction training Members are provided with a ‘Members Booklet’

• The budget for member training should be maintained.

• The training programme should include key officer views.

8

19

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

Programme for training members based on IdeA modules All members have a personal development plan and the opportunity of a 360° appraisal High member training budget when compared to other LA’s

g) ensure that the role of the executive

member(s) is/are formally defined in writing to include responsibility for providing effective strategic leadership to the authority and for ensuring that the authority successfully discharges its overall responsibilities for the activities of the organisation as a whole.

• Constitution The roles of Cabinet and Committees are defined in Part 2 of the Constitution. Part 3 of the Constitution defines the responsibilities for functions – unless functions are specifically allocated to bodies other than the Cabinet, all of the functions are allocated to the Cabinet.

• A formal succession process to facilitate the change of executive members should be documented

• A generic job description to be produced for members and specific job descriptions for those with special responsibilities

8

h) ensure that the roles and responsibilities of all members of the local authority, together with the terms of their remuneration and its review, are defined clearly in writing

• Constitution • Members Allowance

Scheme

Roles and responsibilities are defined in the Constitution An independent review of the scheme of allowances is undertaken. The scheme of allowances is published on the internet

• Align members allowances with JNC increases as recommended in the Audit Report

9

Roles and Responsibilities – Officers i) ensure that a chief executive or

equivalent is made responsible to the authority for all aspects of operational management

• Job description – Chief Exec

• Constitution (Article 13.1)

The Chief Executive is designated as Head of Paid Service and has responsibility for all aspects of operational management.

10

20

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

j) ensure that a senior officer is made responsible to the authority for ensuring that appropriate advice is given to it on all financial matters for keeping proper financial records and accounts and for maintaining an effective system of internal financial control

• Job description – Head of Finance

• Constitution (13.3) • Financial Regulations

- Strategic

The Constitution states the functions of the Chief Finance Officer include ‘administration of financial affairs’ ‘providing advice’ and ‘giving financial information’ The job description includes the provision of support and advice to both officers and members and to ‘maintain strong financial management underpinned by effective financial controls and secure systems’ Budgets & accounts are completed in accordance with CIPFA standards and checked annually by Audit Commission.

• The job description of the Head of Finance to specifically include responsibility for ‘keeping proper financial records and accounts.’

9

k) ensure that a senior officer is made responsible to the authority for ensuring that agreed procedures are followed and that all applicable statues, regulations and other relevant statements of good practice are complied with

• Job description - Monitoring Officer

• Constitution (13.2)

Head of Legal Services is the designated Monitoring Officer with responsibilities defined in the Constitution and job description. The job description states “to be Council’s Monitoring officer for purpose of S5 LG&H Act 1989 & subsequent legislation”. All staff have responsibilities to ensure that good practice is maintained and proper procedures followed.

• The job description for the Head of Legal Services to include responsibility for ensuring that all applicable statues and regulations and other relevant are complied with.

• A nominated Senior Officer (or CLT) to be specifically responsible for ensuring agreed procedures and relevant statements of good practice are complied with

9

21

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

l) ensure that the roles and responsibilities of all senior officers together with the terms of their remuneration and its review are defined clearly in writing

• Job descriptions of Senior Officers

• Pay scale chart • Contract of

employment / terms & conditions

• Appraisals

Roles and responsibilities of Senior Officers are defined in their job descriptions and in the Constitution where applicable. Pay rises of Senior Officers are dependent on performance review Pay scales applicable to Senior Officers are published on the internet.

9

m) adopt clear protocols and codes of conduct to ensure that the implications for supporting community political leadership for the whole council are acknowledged and resolved.

• Constitution • Protocol on officer-

member relations • Code of conduct –

Officers and Members

• Pecuniary Interest registers

Member-Officer Protocol seeks to acknowledge the political aspects of the Council’s workings without compromising the activities of Officers or Members.

• Consideration should be given to developing a resolution process where the protocols are not followed

8

22

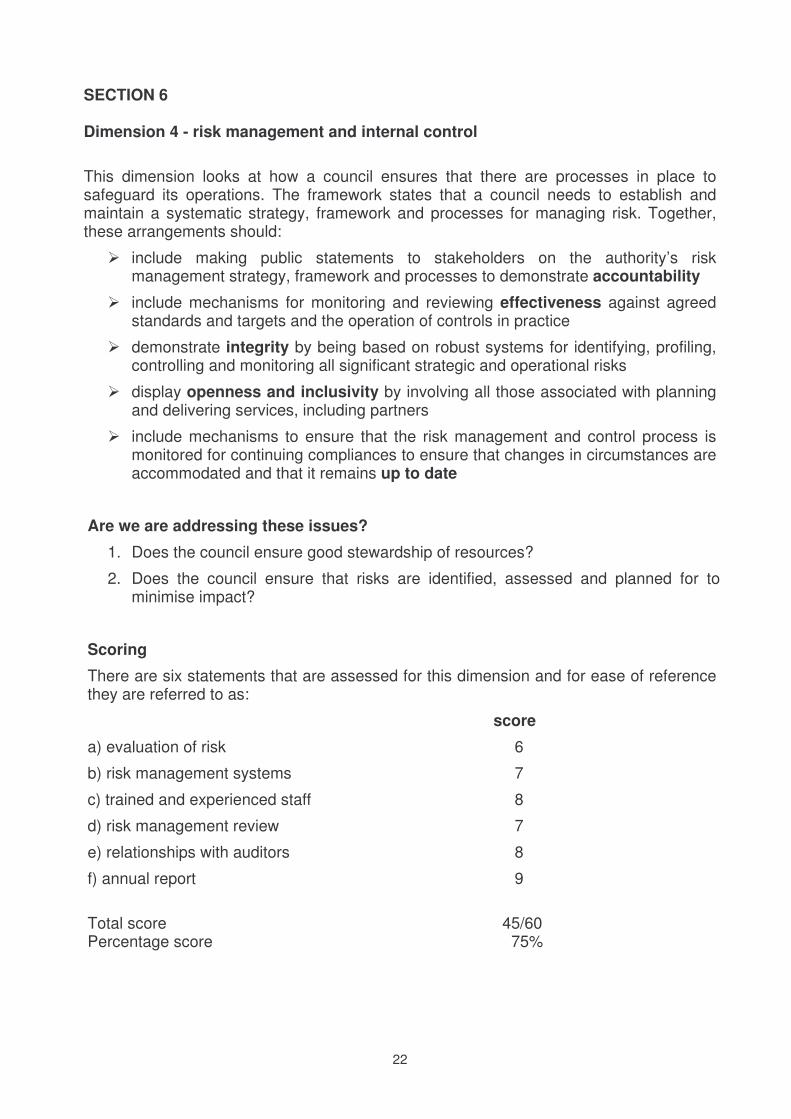

SECTION 6 Dimension 4 - risk management and internal control

This dimension looks at how a council ensures that there are processes in place to safeguard its operations. The framework states that a council needs to establish and maintain a systematic strategy, framework and processes for managing risk. Together, these arrangements should:

� include making public statements to stakeholders on the authority’s risk management strategy, framework and processes to demonstrate accountability

� include mechanisms for monitoring and reviewing effectiveness against agreed standards and targets and the operation of controls in practice

� demonstrate integrity by being based on robust systems for identifying, profiling, controlling and monitoring all significant strategic and operational risks

� display openness and inclusivity by involving all those associated with planning and delivering services, including partners

� include mechanisms to ensure that the risk management and control process is monitored for continuing compliances to ensure that changes in circumstances are accommodated and that it remains up to date

Are we are addressing these issues?

1. Does the council ensure good stewardship of resources?

2. Does the council ensure that risks are identified, assessed and planned for to minimise impact?

Scoring

There are six statements that are assessed for this dimension and for ease of reference they are referred to as:

score

a) evaluation of risk 6

b) risk management systems 7

c) trained and experienced staff 8

d) risk management review 7

e) relationships with auditors 8

f) annual report 9

Total score 45/60 Percentage score 75%

23

Dimension 4: Risk Management and Internal Control

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

a) develop and maintain robust systems for identifying and evaluating all significant risks which involve the proactive participation of all those associated with planning delivering services

• Corporate Risk Register • Risk Management

Strategy • Internal /external Audit

reviews • Service plans • Financial Procedures • Overview and Scrutiny

Panels

Corporate risk register in place Risk Management Strategy has been approved by Members and adopted. The Council has a Risk Management Group Risk Management workshops held with most departments

• Risk register to be completed to ensure all service areas have been considered and all significant risks identified.

• Managers to take proactive ownership for risks within their areas – to include a programme for risk self-assessment and its regular review

• Disaster Recovery and Business Continuity Plan to be completed and approved

• Member involvement in the risk management process via workshop training

• A methodology should be communicated to ensure risk assessments are undertaken for all major projects and strategic policy decisions.

6

b) put in place effective risk management systems including systems of internal control and an internal audit function. These arrangements need to ensure compliance with all applicable statutes, regulations and relevant statements of best practice and need to ensure that public funds are properly safeguarded and are used economically, efficiently and effectively and in accordance with the statutory and other authorities that govern their use.

• Risk workshops • Internal Audit Plan • External audit reviews • Financial regulations • VFM reviews • Best Value reviews • Scheme of delegation • RIPA • Performance Appraisals • Performance

management System • SIC • Budget Monitoring

Systems of Internal Control in place and reviewed by Internal Audit on a cyclical basis Internal Audit governed by CIPFA standards and reports to Performance Review and Audit Panel The external auditors review the work of Internal Audit annually. Corporate training programme includes training on Financial Regulations

• Risk register to inform the Audit Plan

• Promote risk management throughout the Council educating managers to identify and take ownership for the risks in their area and to proactively up date the risk registers

• Risk Management system to be fully implemented

• Internal Audit Strategy to be adopted and approved by Cabinet

7

24

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

c) ensure that services are delivered by

trained and experienced people

• Job Descriptions • Appraisals • Training – internal and

external • CPD • Performance

Management Training

Appraisal process highlights individual’s training requirements, which are communicated to the Corporate training department, although this process needs strengthening. Recruitment and selection policies are in place ensuring that staff of a suitable calibre are employed. Corporate training programme reviewed annually to meet users needs Induction programme for new starters

• Directorates to identify training Co-ordinators for each directorate to consolidate training needs within their areas.

8

d) put in place effective arrangements for an objective review of risk management and internal control including internal audit.

• Performance management system

• Performance Review and Audit Panel

• Audit Commission

Internal Audit monitored by Performance Review and Audit Panel and reviewed annually by external audit Internal Audit undertake an annual review of the Risk Management Service Annual review process leading to the Statement of Internal Control. ALARM Toolkit adopted as standard approach to Risk Management.

• A separate audit committee to be established, as opposed to the current duties of the committee being undertaken by the Performance Review and Audit Panel.

• Risk Management reports to be presented to Performance Review and Audit Panel Audit Committee at least quarterly, and annually to full Council

7

e) maintain an objective and professional relationship with their external auditors and statutory inspectors

• Inspectorate reports • Annual audit letter &

reports • Internal Audit strategy

Internal Audit meets with Audit Commission on a two monthly basis All final Internal Audit reports copied to external audit for information.

• Internal Audit to monitor and report on progress of recommendations made by the external audit and other independent review bodies

8

25

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

f) publish on a timely basis within the annual report an objective balanced and understandable statement and assessment of the authority’s risk management and internal control mechanisms and their effectiveness in practice.

• Annual report Statement of Internal Control, produced in line with CIPFA/SOLACE requirements, accompanies Statement of Financial Accounts External Audit statement on the financial accounts and processes

• A summary assessment of the Authority’s internal control and risk management mechanisms to be included in the Corporate Plan.

• The Statement of Internal Control to be reported to Members as an agenda item independent of the accounts.

9

26

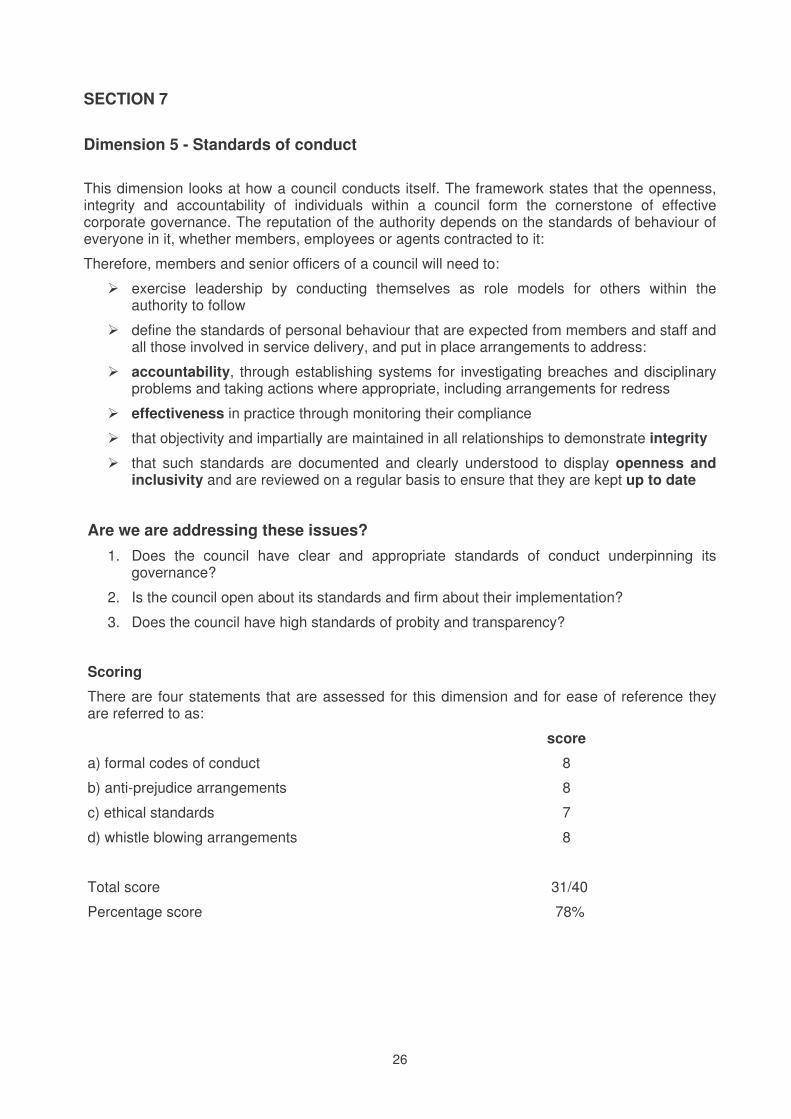

SECTION 7

Dimension 5 - Standards of conduct This dimension looks at how a council conducts itself. The framework states that the openness, integrity and accountability of individuals within a council form the cornerstone of effective corporate governance. The reputation of the authority depends on the standards of behaviour of everyone in it, whether members, employees or agents contracted to it:

Therefore, members and senior officers of a council will need to:

� exercise leadership by conducting themselves as role models for others within the authority to follow

� define the standards of personal behaviour that are expected from members and staff and all those involved in service delivery, and put in place arrangements to address:

� accountability, through establishing systems for investigating breaches and disciplinary problems and taking actions where appropriate, including arrangements for redress

� effectiveness in practice through monitoring their compliance

� that objectivity and impartially are maintained in all relationships to demonstrate integrity

� that such standards are documented and clearly understood to display openness and inclusivity and are reviewed on a regular basis to ensure that they are kept up to date

Are we are addressing these issues?

1. Does the council have clear and appropriate standards of conduct underpinning its governance?

2. Is the council open about its standards and firm about their implementation?

3. Does the council have high standards of probity and transparency?

Scoring

There are four statements that are assessed for this dimension and for ease of reference they are referred to as:

score

a) formal codes of conduct 8

b) anti-prejudice arrangements 8

c) ethical standards 7

d) whistle blowing arrangements 8

Total score 31/40

Percentage score 78%

27

Dimension 5: Standards of Conduct

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

a) develop and adopt formal codes of conduct defining the standards of personal behaviour to which individual members officer and agents of the authority are required to subscribe and put in place appropriate systems and processes to ensure that they are complied with.

• Anti Fraud Policy • Members code of

Conduct • Officers Code of

Conduct • Complaints procedure • Whistle-blowing policy • Disciplinary and

Capability policies • IT Security Policy • Employment Contract

Human Resources policies reviewed and updated 2005 All policies available on the intranet and communicated to employees during the induction process. Annual staff appraisals complemented by regular supervision/ 1-1 meetings

• Anti Fraud and Corruption Policy and Code of Conduct to be reviewed annually.

• Code of Conduct to be updated in line with the National Code when it is published.

8

b) put in place arrangements to ensure that members and employees of the authority are not influenced by prejudice, bias or conflicts of interest in dealing with different stakeholders and put in place appropriate processes to ensure that they continue to operate in practice.

• Pecuniary Interest registers

• Financial Regulations • Rules of Procedure

(Constitution) • Protocol on member –

officer relationships • Contracts Procedures • Equalities Policy

Through the Codes of Conduct, Standing Orders, financial regulations, policies on partnership working. Code of good practice for planning matters within the Constitution. Equalities policy in place Equalities and diversity e-learning package available to employees Corporate induction includes covers equality issues. All Members and Officers should complete the register of interests annually Standards Committee have a protocol for investigation.

• Undertake Internal Audit to assess how effectively Members are complying with the Code of Conduct and that appropriate action is taken with regard to complaints

• Completion of Pecuniary Interest forms and consideration of register of gifts and hospitality by employee to be undertaken alongside and within the same timeframe as the annual appraisal process

8

28

The local code should reflect the requirements to:

Source document/ Other indicators of compliance

Summary of current practice Suggestions for improvement Draft score 0-10

c) put in place arrangements to ensure that their procedures and operations are designed in conformity with appropriate ethical standards and to monitor their continuing compliance in practice.

• AC Ethical Gov diagnostic

• Comprehensive Equalities Policy

• Corporate Equalities Plan

• Equalities standard • Standards Committee • Whistle-blowing Policy • Reports to standards

Committee • Equalities consultative

group • Corporate Equalities

group

HR Policies updated July 2005 Ethical Governance Audit undertaken in 2005 by Audit Commission Regular monitoring of minorities within MKC. Currently working to achieve level 3 of Equality Standard by January 2007

7

d) put in place arrangements for whistle blowing to which staff and all those contacting the council have access.

• Whistle-blowing Policy Whistle blowing policy is on the intranet and all staff receive a copy of the policy at Corporate Induction training.

• Undertake review of the impact/effectiveness of the Whistle Blowing Policy

• Ensure that the Whistle Blowing Policy is communicated to those partners contracting with the Council.

8

29

SECTION 8 CONCLUSIONS AND ACTION PLAN

In this section we look at the overall score against the framework and, as a result of the exercise and summarise the actions recommended (referenced to the relevant dimension) to improve the Council’s Corporate Governance framework.

Overall Score To arrive at an overall score we have calculated the average score for each dimension. Dimension Total

score Average score

% score

1 Community focus 52 / 70 7.4 74 2 Service delivery arrangements 40 / 60 6.7 67 3 Structure and processes 114 / 130 8.7 87 4 Risk management and internal control 45 / 60 7.5 75 5 Standards of conduct 31 / 40 7.7 77 Overall Total 281 / 360 7.8 78

This table shows that the procedures in place in relation to structure and process within Milton Keynes Council provide assurance of strong governance. Greatest improvements can be made in respect of service delivery arrangements. In many cases the building blocks to improve corporate governance in this area are already in place, but all services throughout the Council need to take advantage of relevant work already done and procedures and frameworks that have been drawn up. The overall score of 78% is good, and provides evidence that in many areas the Council is complying with the principles of good governance which include; integrity; accountability, openness and inclusivity.

30

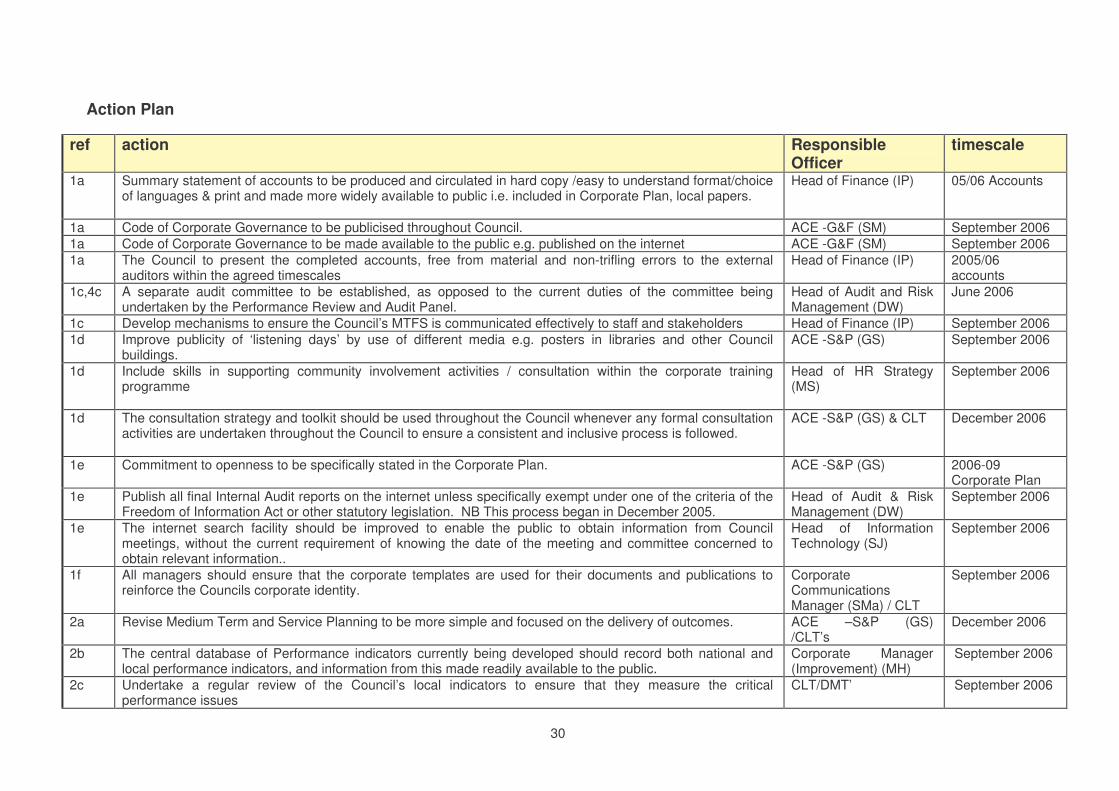

Action Plan

ref action Responsible Officer

timescale

1a Summary statement of accounts to be produced and circulated in hard copy /easy to understand format/choice of languages & print and made more widely available to public i.e. included in Corporate Plan, local papers.

Head of Finance (IP) 05/06 Accounts

1a Code of Corporate Governance to be publicised throughout Council. ACE -G&F (SM) September 2006 1a Code of Corporate Governance to be made available to the public e.g. published on the internet ACE -G&F (SM) September 2006 1a The Council to present the completed accounts, free from material and non-trifling errors to the external

auditors within the agreed timescales Head of Finance (IP) 2005/06

accounts 1c,4c A separate audit committee to be established, as opposed to the current duties of the committee being

undertaken by the Performance Review and Audit Panel. Head of Audit and Risk Management (DW)

June 2006

1c Develop mechanisms to ensure the Council’s MTFS is communicated effectively to staff and stakeholders Head of Finance (IP) September 2006 1d Improve publicity of ‘listening days’ by use of different media e.g. posters in libraries and other Council

buildings. ACE -S&P (GS) September 2006

1d Include skills in supporting community involvement activities / consultation within the corporate training programme

Head of HR Strategy (MS)

September 2006

1d The consultation strategy and toolkit should be used throughout the Council whenever any formal consultation activities are undertaken throughout the Council to ensure a consistent and inclusive process is followed.

ACE -S&P (GS) & CLT December 2006

1e Commitment to openness to be specifically stated in the Corporate Plan. ACE -S&P (GS) 2006-09 Corporate Plan

1e Publish all final Internal Audit reports on the internet unless specifically exempt under one of the criteria of the Freedom of Information Act or other statutory legislation. NB This process began in December 2005.

Head of Audit & Risk Management (DW)

September 2006

1e The internet search facility should be improved to enable the public to obtain information from Council meetings, without the current requirement of knowing the date of the meeting and committee concerned to obtain relevant information..

Head of Information Technology (SJ)

September 2006

1f All managers should ensure that the corporate templates are used for their documents and publications to reinforce the Councils corporate identity.

Corporate Communications Manager (SMa) / CLT

September 2006

2a Revise Medium Term and Service Planning to be more simple and focused on the delivery of outcomes. ACE –S&P (GS) /CLT’s

December 2006

2b The central database of Performance indicators currently being developed should record both national and local performance indicators, and information from this made readily available to the public.

Corporate Manager (Improvement) (MH)

September 2006

2c Undertake a regular review of the Council’s local indicators to ensure that they measure the critical performance issues

CLT/DMT’ September 2006

31

ref action Responsible Officer

timescale

2c Map performance measures to the Corporate objectives and priorities CLT September 2006 2c Progress against priorities, as reported to Cabinet, to be published on the Internet. ACE -S&P (GS) September 2006 2d Review the links between the Council’s strategies and planning as part of the MTP process and improve the

financial and activity analysis of the strategies Head of Finance (IP) September 2006

2d Undertake a review of budget setting process –to include consideration of zero based budgeting

Head of Finance (IP) September 2006

2e The success of partnerships, financially and with regard to the achievement of aims, should be formally monitored.

ACE - S&P (GS) /CLT September 2006

2f Services should consolidate recommendations from all parties and produce Action Plans to address these issues. Copies of the Action Plans should be held centrally by ACE (S&P)

ACE –S&P (GS) /CLT’s

September 2006

2f Internal Audit should review implementation of the consolidated action plans as part of the internal audit process

Head of Audit and Risk Management (DW)

September 2006

2f External Audit should copy Internal Audit and the Performance Review and Audit Panel into every report. Head of Audit and Risk Management (DW)

September 2006

3a Corporate inductions to include reference to Protocol on member officer relations as contained within the Constitution

Head of Democratic Services (JM)

September 2006

3a Code of conduct to be reviewed annually by standards Committee. Head of Democratic Services (JM)

September 2006

3b,3g A generic job description to be produced for members and specific job descriptions for those with special responsibilities

Head of Democratic Services (JM)

September 2006

3c Develop mechanisms for reporting key financial health indicators to Members. Head of Finance (IP) September 2006 3e Regular reviews of the Councils significant Corporate Policies should be undertaken to ensure that they are

relevant, up-to-date and reflect the Council’s culture. Each service area should timetable a review date for all policies for which they have responsibility.

CLT’s September 2006

3f The budget for member training should be maintained.

Head of Democratic Services (JM)

September 2006

3f The Member training programme should include key officer views. Head of Democratic Services (JM)

September 2006

3g A formal succession process to facilitate the change of executive members should be documented. Head of Democratic Services (JM)

September 2006

3h Align members allowances with JNC increases as recommended in the Audit Report. Head of Democratic Services (JM)

September 2006

3j The job description of the Head of Finance to specifically include responsibility for ‘keeping proper financial records and accounts.’

Head of Finance (IS) December 2006

3k The job description for the Head of Legal Services to include responsibility for ensuring that all applicable statues and regulations and other relevant are complied with.

Head of Legal (PM) December 2006

3k A nominated Senior Officer (or CLT) to be specifically responsible for ensuring agreed procedures and CLT December 2006

32

ref action Responsible Officer

timescale

relevant statements of good practice are complied with. 3m Consideration should be given to developing a resolution process where the protocols are not followed. Head of Democratic

Services (JM) September 2006

4a Risk register to be completed to ensure all service areas have been considered and all significant risks identified

Head of Audit & Risk Management (DW)

December 2006

4a Managers to take proactive ownership for risks within their areas – to include a programme for risk self-assessment and its regular review.

Head of Audit & Risk Management (DW)

September 2006

4a Disaster Recovery and Business Continuity Plan to be completed and approved. Head of Audit & Risk Management (DW)

September 2006

4a Member involvement in the risk management process via workshop training.

Head of Democratic Services (JM) & Head of Audit & Risk Management (DW)

September 2006

4a A methodology should be communicated to ensure risk assessments are undertaken for all major projects and strategic policy decisions.

Head of Audit & Risk Management (DW)

September 2006

4b Risk register to inform the Audit Plan. Head of Audit & Risk Management (DW)

September 2006

4b Promote risk management throughout the Council educating managers to identify and take ownership for the risks in their area and to proactively up date the risk registers.

Head of Audit & Risk Management (DW)

December 2006

4b Internal Audit Strategy to be adopted and approved by Cabinet Head of Audit & Risk Management (DW)

December 2005

4c Directorates to identify training Co-ordinators and implement training liaiason mechanisms. for each directorate to consolidate training needs within their areas.

Head of HR Strategy (MS) /CLT

September 2006

4d Risk Management reports to be presented to Performance Review and Audit Panel at least quarterly, and annually to full Council

Head of Audit & Risk Management (DW)

September 2006

4e Internal Audit to monitor and report on progress of recommendations made by external audit and other independent review bodies

Head of Audit & Risk Management (DW)

September 2006

4f A summary assessment of the authority’s internal control and risk management mechanisms to be included in Corporate Plan.

ACE – G&F (SM) 2006-09 Plan

4f The Statement of Internal Control to be reported to Members as an agenda item independent of the accounts. Head of Finance (IP) June 2006 5a Anti Fraud and Corruption Policy and Code of Conduct to be reviewed annually. Head of Audit & Risk

Management (DW) September 2006

5a Code of Conduct to be updated in line with the National Code when it is published. Head of Democratic Services (JM)

September 2006

5b Undertake an Internal Audit to assess how effectively Members are complying with the Code of Conduct and Head of Audit & Risk September 2006

33

ref action Responsible Officer

timescale

that appropriate action is taken with regard to complaints Management (DW) 5b Completion /of Pecuniary Interest forms and consideration of register of gifts and hospitality by employee to be

undertaken alongside and within the same timeframe as the annual appraisal process Head of HR Strategy (MS) & CLT

September 2006

5d Undertake a review of the impact/effectiveness of the Whistle Blowing Policy. Head of Audit & Risk Management (DW

September 2006

5d Ensure that the Whistle Blowing Policy is communicated to those partners contracting with the Council. Head of Audit & Risk Management (DW)

September 2006

34

SECTION 9

Code of Corporate Governance Introduction The Council is responsible for ensuring that its business is conducted in accordance with the law and proper standards, that public money is safeguarded and properly accounted for, and used economically, efficiently, effectively and equitably. In discharging this accountability, members and senior officers are responsible for putting in place proper arrangements for the governance of the Council’s affairs and the stewardship of the resources at its disposal. To this end, the Council has adopted this code of corporate governance. The Council will seek to ensure that the following principles underpin the operation of the Council in working for the people of Milton Keynes:

� openness and inclusivity � accountability � integrity

The Council in carrying out its business will seek to aspire to the standards and aspirations set out below under the following headings;

� Community Focus � Service Delivery Arrangements � Structure and Processes � Risk Management and Internal Control � Standards of Conduct

Community Focus The Council will focus on the services it provides and the communities it provides them to. It will set out ambitions for the area based on a shared and realistic vision for the future, along with a strategy to deliver it. The Council’s plans will be clearly communicated with the community and stakeholders and take account of feedback received. The Council in the exercise of its powers and duties will always seek to:

� work for and with local communities, especially within the context of growth, through the Local Strategic Partnership, Parish and Town Councils, our consultative forums, Political processes and our service provision.

� exercise leadership, in the local communities, where appropriate � undertake an’ ambassadorial role’ to promote the well-being of the community

35

The Council will maintain effective arrangements:

� for explicit accountability to stakeholders for the authority's performance and its effectiveness in the delivery of services and the sustainable use of resources, amongst other things by reporting and monitoring through Overview and Scrutiny Committees, and progress reports on implementing the Community Strategy

� to demonstrate integrity in the authority's dealings in building effective relationships and partnerships with other public agencies and the private/ voluntary sectors

� to demonstrate openness in all their dealings, particularly through the Local Strategic Partnership

� to demonstrate inclusivity by communicating and engaging with all sections of the community to encourage active participation with reference to the Council’s Consultation Strategy and consultation toolkit

� to develop and articulate a clear and up-to-date vision and corporate strategy in response to community needs by the setting and publication of both strategic and corporate priorities, following consultation where appropriate, and reporting on the progress against these priorities.

Service Delivery Arrangements The Council will strive to achieve continuous improvement in all its services by:

� ensuring all areas of service provision are subjected to best value review; � procuring appropriately to secure better service provision; � innovate and implement new initiatives and extend Information

Communication Technology opportunities to improve service provision. The Council will ensure that agreed policies are implemented and decisions carried out by maintaining arrangements which:

� discharge the Council’s accountability for service delivery at a local level in accordance with the Corporate Plan, Medium Term Plans and Service Plans.

� ensure effectiveness through setting targets and measuring performance through the Council's Corporate Plan

� demonstrate integrity in-dealing with service users and developing partnerships to ensure the 'right' provision of services locally with special reference to the Local Strategic Partnership and the encouragement of community involvement and customer focus to determine and define services and by ensuring transparency and openness with regard to the decision making process

� demonstrate openness and inclusivity through consulting with key stakeholders, including service users by following guidance given in the consultation strategy and toolbox

� are flexible and regularly reviewed so that they can be kept up to date and adapted to accommodate change and meet user wishes

� are underpinned by the Council's Business Planning process.

36

Structures and Processes The Council will establish effective political and managerial structures and processes to govern decision-making and the exercise of authority within the organisation and will:

� define the roles and responsibilities of members and officers to ensure accountability, clarity and good ordering of the Council’s business though the Constitution and job profiles

� deliver change and improvement through open and transparent decision-making by the Cabinet

� ensure that there is proper scrutiny and review of all aspects of performance and effectiveness through the use of Scrutiny Panels and the Overview and Scrutiny Committee

� demonstrate transparency by promoting the effective use of the Call-in process by the community and by making the access to information procedure rules publicly available

� demonstrate integrity by ensuring a proper balance of power and authority and promoting and ensuring adherence to both the members and officers Codes of Conduct.

� document clearly such structures and processes within the Constitution and ensure that they are communicated and understood both internally through training and externally by publication on the internet.

� ensure such structures and processes are kept up to date to meet operational and legislative requirements and adapted to accommodate change by undertaking regular reviews.

Risk Management and Internal Control To ensure good management of resources and that risks are identified, assessed and addressed to minimise impact. The Council will establish and maintain a strategy, framework and processes for managing risk which will:

� include making public statements to stakeholders on the authority's risk management strategy, framework and processes to demonstrate accountability within the annual Statement of Internal Control which accompanies the Financial Accounts

� include mechanisms for monitoring and reviewing effectiveness against agreed standards and targets and the operation of controls in practice by promoting both internal and external inspections

� demonstrate integrity by being based on robust systems for identifying, profiling, controlling and monitoring all significant strategic and operational risks, by continual review and monitoring of the Corporate Risk Register

� display openness and inclusivity by involving all those associated with planning and delivering services, including partners

� include mechanisms to ensure that the risk management and control process is monitored for continuing compliance to ensure that changes in circumstances are accommodated and that it remains up to date, by undertaking regular internal audit reviews and risk workshops.

37

Standards of Conduct The Council believes that openness, integrity and accountability of individuals within the Council form the cornerstone of effective corporate governance and that the reputation of the Council depends on the standards of behaviour of everyone in it, whether members, employees or agents contracted to it. The Council will try to ensure that members and senior officers:

� exercise leadership by conducting themselves as role models for others within the authority to follow by ensuring awareness and compliance with the Codes of Conduct for Members and Employees.

� define the standards of personal behaviour that are expected from members and staff and all those involved in service delivery, and put in place arrangements to ensure:

� accountability, through establishing systems for investigating breaches and disciplinary problems and taking action where appropriate, including arrangements for redress, in accordance with the Councils disciplinary process and the requirements of the Standards Board

� effectiveness in practice through monitoring their compliance and putting in place procedures by which concerns can be raised such as the Confidential Reporting Policy.

� that objectivity and impartiality are maintained in all relationships to demonstrate integrity, in accordance with the protocol on member officer relationships and the Codes of Conduct.

� ensure that such standards are documented within the Constitution and clearly understood to display openness and inclusivity and are reviewed on a regular basis to ensure that they are kept up to date.

Management of this Code of Corporate Governance The Council is determined that the effectiveness of this Code is embedded and owned by the whole of the organisation. It will review and update the Code, though Cabinet and the Council’s Performance Review and Audit Panel, on an annual basis in order to ensure that the principles of openness and inclusivity, accountability and integrity that underpin the operation of the Council in working for the people of Milton Keynes is maintained. This Code of Corporate Governance is consistent with the principles and requirements of the Framework prepared by the Chartered Institute of Public Finance and Accountancy (CIPFA) and the Society of Local Authority Chief Executives and Senior Managers (SOLACE) and set out in the publication Corporate Governance in Local Government: A Keystone for Community Governance (CIPFA) - 2001.

Related Documents

![Corporate Governance Manualpaisalo.in/pdf/corporate-governance-en.pdf · [ 1 ] DEFINITIONS Corporate Governance Corporate Governance is the system of internal controls and procedures](https://static.cupdf.com/doc/110x72/60457b037dc32d128b177c66/corporate-governance-1-definitions-corporate-governance-corporate-governance.jpg)