C/ CIRCULATING COPY TO BE RETURNED TO REPORTS DESK FILE buri fLt%fLvl' tTi-1 rI flfl Ttrr'v * AI'.r.t Aj T 3 p4x t run. nflfllt%Tfl'flf TflhfTfl'T I tTn "Tht ,r'y %lnl~ SnkrL IJI.AuiV I OF I1NTERUNPATIO"NA L BANK FOR ui.flLUN wKlRUIN AjNDJ DJE,vELOPMri;vrnT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use | \X h <t < '; W 2$' ;2'' ' 't U 'Report No. 38-BR l/ ' THE ECONOMIC AND SOCIAL DEVELOPMENT OF BRAZIL VOLUME VII INDUSTRY March 12, 19173 La-tin A mler4ca andu th'e CariLbubean D-epartrment This report was prepared for official use only by the Bank Group. It may not be published, quoted or cited without Bank Group authorization. The Bank Group does not accept responsibility for the accurac-y or conpleteness of the report, Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

C/CIRCULATING COPY

TO BE RETURNED TO REPORTS DESK

FILE burifLt%fLvl' tTi-1 rI flfl Ttrr'v * AI'.r.t Aj T 3 p4x t run. nflfllt%Tfl'flf TflhfTfl'T I tTn "Tht ,r'y %lnl~ SnkrL

IJI.AuiV I OF I1NTERUNPATIO"NA L BANK FOR ui.flLUN wKlRUIN AjNDJ DJE,vELOPMri;vrnT

INTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

| \X h <t < '; W 2$' ;2'' ' 't U 'Report No. 38-BR

l/ '

THE ECONOMIC AND

SOCIAL DEVELOPMENT

OF

BRAZIL

VOLUME VII

INDUSTRY

March 12, 19173

La-tin A mler4ca andu th'e CariLbubean D-epartrment

This report was prepared for official use only by the Bank Group. It may not be published, quoted

or cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccurac-y or conpleteness of the report,

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

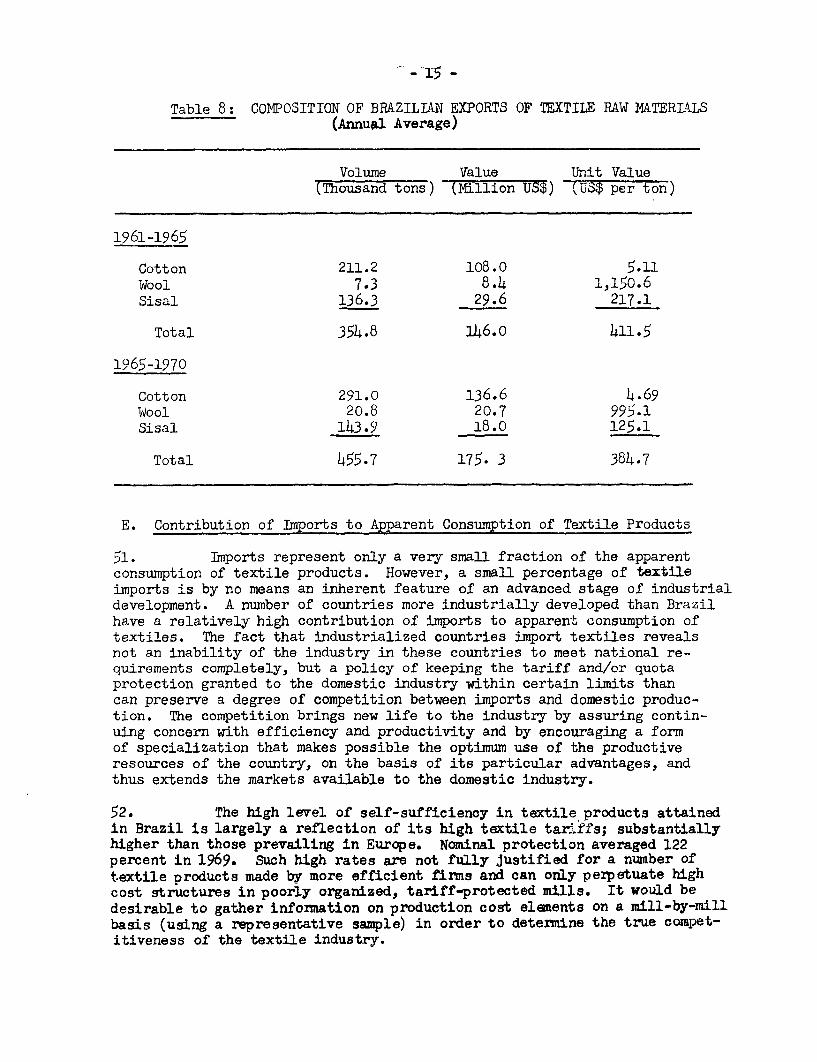

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

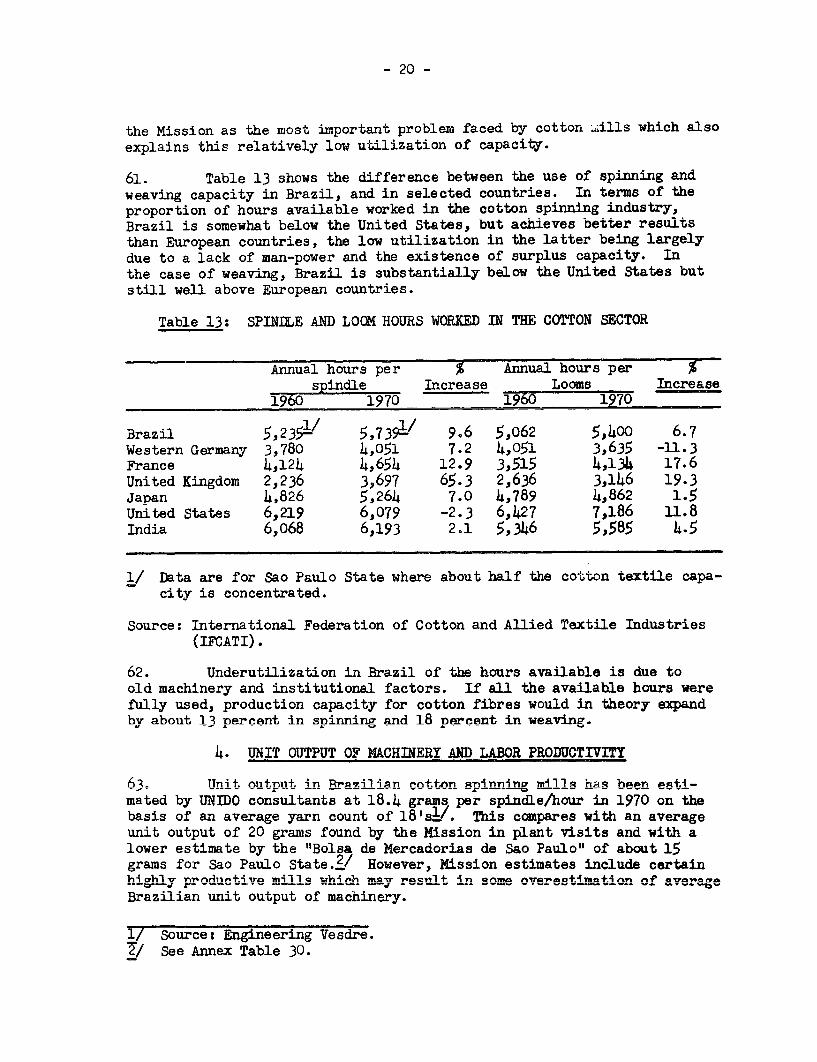

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENT

Currency Uvnet: Cruzeiro- (Prior to Mav 15j 1970; the eurrencyunit was called the "Cruzeiro Novo" or "NewCrUzeiro", the adjective was dropnPA in May, 1970;without any change involved.)

"Achange Rates Effecie L;L,LVW~ ^Ce -F be r 'I -7* 1972

Selling Hate:VS 'St.0L -VJ rtS

Buying Rate: US$1.00 = Cr$6,165

Average Exchange Rates

US$1.00 Cr$h.59 Cr$5.285US$1 million = Cr$4y594,000 Cr$5,285,000Cr$1 million US$217,675 US$189,215

This report is based on the findings of a mission inMay to June, 1972 to Brazil composed of:

Roger P. Hipskind (Chief of Mission);Lorne T. Sonley (Agricultural Economist);Donald Pickering (Consultant - Agricultural Economist);Bernard Decaux (Consultant - Industrial Econonist);Gerhard Thiebach (Industrial Economist)-Joaquin A. Martinez (Telecommunications 5 ;Sonia C. Hoehlein (Secretary)

TA nnD OF 0 WCi,vlyi EiS

Paure No.

I - THE TEXTILE INDUSTRY ................. 1

II - THE LEATHER INDUSTRY .*.... ...... *.... s..** .... ,.s..s. .o.. 73

III - THE SHOE MANUFACTURING INDUSrRY .. ........ ... 95

IV - THE FERTILIZER INDUSTRY ..... .*.*. 10O

I. THE TEXTILE INDUSTRY

1. DESCRIPTION OF TIE TEXTILE INDUSTRY

A. Significance of the Textile Industry in the Natioinal Econony

1. The textile industry is an important source of industrialemployment, providing work for about 3)40,000 operatives out of a totalof 2.3 j4lion persons employed in manufacturing (14.6 percent of thetota±, .0= Similarly, the wages paid by the textile industry, whichamounted to more than 1 billion cruzeiros in 1969, represented a signifi-cant proportion (about 11 percent) of the total wages paid by the manufac-turing industry. Gross value added in textile production was 3.5billion cruzeiros in 1969, i.e., 10 percent of total gross manufacturingproduct. As the latter contributes about 15 percent of GDP the textileindustry therefore supplies 1.5 percent of the GDP, apart from the In-direct contribution it makes by purchasing raw materials fram othersectors.

2, The recent evolution of the textile industry shows that it istending to develop at a much slower pace than the manufacturing industryas a whole, and is therefore contributing less than in the past. Forinstance, the number of persons employed in the textile industry, althoughrepresenting a substantial proportion of industrial employment (thelargest for any one branch of activity) is now less than in 1958, whennearly 20 percent of the operatives in the manufacturing industry wereworking in the textile sector. At the same time, the proportion of totalmanufacturing wages paid by the textile industry dropped from 17 percentin 1958 to 11 percent in 1969, and the value added declined from 13percent to 10 percent of the total for the whole manufacturing sector.The contribution made by the textile industry shrank as a result of therelatively slow growth of its production, which in the period in questionincreased by 73 percent, as against 120 percent for the manufacturingindustry as a whole.

3. The purchase of raw and related materials by the textileindustry is one of the prime spurs to several sectors of the eqonomy,especially agriculture, stock fanming and the chemical industry. In thelast decade, its average yearly purchases of cotton totalled 250,000 tonswhich was about 45 percent of domestic cotton production. In 1969, thesector as a whole consumer about 3.0 billion cruzeiros' worth of domesticraw materials, mainly cotton, wool, rayon, synthetics and jute. The

1/ Source: IBGE - Data are for 1969.

- 2 -

textile industry thus makes possible a large volume of employment inother sectors. estimated at about half a million workers in the agricul-tural sector alone.

B. Structure of the Textile Industryv

The Brazilian textile industry comnrises the following groupswithin the manufacturing sector: the processing and preparation of fibresfnr txYtiles purposes; the spinning; weAvina of yarn and fabricr nrocessingof cotton, wool, man-made fibres, jute and similar fibres, flax and ramie,and natural silk; the knitti.ng industry, and the mnanufacturaA of hnRivrvand knitted goods in general; the industry manufacturing trimmings, ribbons,t.ullp- feltjq lace and emhrnoiderv goodg. the industries nroducing rone;carpets and serving and emboidery thread; the hammock and fishing netindustry, arnr d som.e other arnninl tetile 1 rancrhes.

5. TIn all, the textile industry is c omosed of about 10QnOplantsV of every size excluding artisan units employing less than five persons.

6. The spinning and weaving sectors cover spinning, weaving,print+ing, +he dyeingr of nylar.n andd shbr4 n o+her Ae , procssving sec-

- .A.** tA.. SA~ ~ USS *J ~.A.- o - e-**- - - -†- - - .5

tions, including the finishing and packaging of sewing and embroiderycot-tons. nnlis is 4th-e p,t-ncipal sec4tor ir.-l -h 4-4ile indust-r;, - -rising

about 80 percent of the production in tons.

Ts.ble 1: STRUCTURE OF THE TEXTILE INDUSTRY

_~~~~~~~~~~~~~~~~~~ , . ~%%,UL1

(In.thousand tons) %

3pinning, weaving, and yarn and 298 77.6

AKJUtu.Lire ar-id hosiery 54 14.1

Trimming, ribbons, tulle, felts, etc. 18 4.7

Ropms, cords 14 3.6

TOTAL 384 100.0

Source: Engineering Vesdre (Belgium)

7. Next in importance is the knitting and hosiery industry, whichaccounts for 14 percent of the production. The industry is highly atom-ized. There are hundreds of manufacturers of knittear in the. country,and only a few have more than 10 machines. Traditional (flat) knittingmachinery is found in the areas around Porto Alegre, Blumenau and Petro-

17 lBGE Producao Industrial, 1969.

polis. The fully fashioned flat machines are concentrated wiLthin aroundt.en , 11X9 s -n Sao auo. rs-3ly, mlodern, c Irc-'ar 1-n-1 'In maL-l are_ _ -ItLI I.±LII i.i 0 r,.U.L r 2Ir&L.LY IIUU .Liuu.L" A&IWLL .LI16 hZiauLLLI1OS arelocated predominantly in Sao Paulo, except for the cotton knitting indus-t,ry of Santa Ca_aria. Hosiery i s also developed in the latter S-ate.

8. The other specialized branches of textile ma^nufacture play afairly minor part in the industry as a whole, except in the state of Riode Janeiro -where the manufactuwr Of t1Mmi ngs, lace, felts, anu otherspecialities is important.

Table 2: STRUCTURE OF THE TEXTILE INDUSTRY FOR THE DIFFEYENT STATES

Value Added C-L

(Cr million) Value Added

Sao Paulo 2,065.2 57.0Nordeste 354.9 9.8Guanabara 279.5 7.7Minas Gerais 243.5 6.7Rio de Janeiro 204.6 5.7Santa Catarina 200.6 5.5Rio Grande do Sul 114.6 3.2Parana 103.4 2.8Others 59.2 1.6

TOTAL 3,625.5 100e0

Source: Producao Industrial, 1969.

C. Distribution of Textile Production

The Textile Industry as a khole

9. In 1970, the output of the spinning industry was estimated at325,000 tons of yarn and 270,000 tons of fabrics. This compares with total,domestic output of 285,000 tons of yarn and 260,000 tons of fabric in 1960.Y/It is clear that in Brazilian textile production cotton predominates intenns of volume, followed by man-made fibres, wool and flax and ramie.

Cotton Sector

10. Total yarn production was estimated at 270 thousand tons in1970, i.e. 19 percent above the 1960 level. Production of fabrics was approxi-mately 1,200 million square meters against 1,171 million in 1960. Fabrics pro-duction has increased much less than yarn output due to the diversion of in-creased quantity of yarn to the knitting and hosiery industries which havegrown at a fast rate.

1/ ECLA survey.

-14.-

Table 3: STRuCTURE OF PROD-UCTION IN TIE TEXTILE INDUSTRY

Yarn Production Fabrics(Thousiard of tons) (Million square meters)

I1960-/ 1970_/ 1960 1970

Cotton 227.0 270.0 1,170.7 1,200.0

Wool 30.0 15.3 14.1 20.0

Artificial Fibres 13.0 14.6/ ( ((122.6 (300.0

Synthetic Fibres 1.2 15-02. (

Silk o.5 o.5 n.a. n.a.

Flax/ramie 9.0 9.0 22.8 i8.o

280.7 3214.8 1,359,2 1.558.OY

V/ ECLA survey7/ Engineering Vesdre

/ Excluding filaments, directly used in weaving, knitting, etc.z/ Mission estimates.

11. Cotton consumption represented 64 percent of total apparentconsumption of fibres in 1970 against 73 percent in 1960. Such a decreaseis due to inroads made by synthetics and artificial fibres. Data availablefor Sao Paulo State show that cotton consumption in spinning mills rose by6.3 percent from 1960 to 1971 while yarn production increased by 8.7 percent.

Wool Sector

12. Domestic consumntion of raw wool has decreased in the lastdecade from about 25,000 tons (including re-used wool) in 1960 to about15,000 tons in 1970. But while in 1960Q onlg 11 nercent of fibres usedin the wool spinning mills were artificials and synthetics, this propor-tion rose to L6 percent in 1970. Thus the total fibre consi ntion was

oUut the same in 1960 and in 1970, i.e. less than 30,000 tons. The useof woolen goods in annarel is very small in Brazil. noving to thle rclimates

Man-made Fibre setorl/

13. Cons'ampti on of man-made fibres has substantIally Increased in1/ n-made fibres refers to 11 fibre mater s c h-uman

.~~~ n alI,aha -- p r A..o d~ UU.I C -Uy' Ua

manipulation of natural resources. In other words, fibres which do nototi-hr natu.rall auch as cot+or., wTol "' ax 4 J et.. f'i .he u

synthetic fibres refers specifically to those fibrous materials producedfrom rolm-ers1 r The main -+'-.the,, YNks a-e the ,lon- polyester and acr) - lict, - 8 Ul j.v.. LV.LIJA, V1.LJ1i.L I1U vy ctypes, the other man-made fibres being the cellulosic type, namely rayonand acetate.

recent years. Sixty percent of fibres used in the textile indu3try arecontinuous filaments sLch as polyester, nylon; viscose and acetate. Themain end use is for knitting, hoseiry and cords.

Table 4: CONSIIMTION OF MAN-MADE FIBRES IN THE TEXTILE INDUSTRY

(In thousand tons)

1965 1970 % Increase

Artificial Fibres

Staple 11.0 16.8 52.7FIlMent 18.2 24.0 31.9r X lament,--

29.2 40.8 40.7

Synthetic Fr'bres

Duwl A.> 20.21.Filament 7.7 30.4 294..8

12.7 50.1 294.5

Total

Staple Ul.9 90.9 116.9Filament 16.0 37.5 134.4

25.9 54.4 110.0

11X. Production capacity of man-made fibres in Brazil in 1971 wasabout 41,000 ons for artificial fibres and 54,000 tons for synthetics usedin textiles.,/ Actual dcmestic production was 23,000 tons in 1970 forartificials and 43,000 tons for synthetics. Polyester, and yeny larothe main inported fibres.

D. Mill Size and Vertical Integration

15. In 1969, the average size mill in the textile industry as awhole was one with 150 persons employed. The average size mill in 1960

V/ There are also some industrial uses (acetate staple for cigarettefilters, nylon 6 and viscose for tires).

was 108 persons, thus revealing some increase in mi'l size in the lastdecade. In 1969 firms with 500 to 999 employees contributed 23.5 per-cent of value added and 27.5 percent of employment but represented only6.2 percent of the total number of mills. Also firms with more than1,000 employees contributed 26.8 percent of value added and 2415 percentof employment. These large mills represented only 2.4 percent of the totalnumber of mills.

16. The number of textile mills has also decreased from about2,900 in 1958 to 1,900 in 1969 (excluding units with less than 5 workers).This has been partly due to increasing integration of the mills. rnelargest proportion of man power is employed by the fully integrated mills(spinning, weaving and yarn and fabric processing, including printing anddyeing). In other words, the bigger establishments generally tend tocover the whole range of processing.

17. Admittedly, the lack of any tradition in the marketing of inter-mediate production has been a contributory factor. In this respect, thetextile economy of each state is practically a watertight compartment,trade among the different regions being in raw materials and end goodsonly. The vertical integration of the industry at the regional leveland the consequent limitation of the market for intermediate goods areleading to more and more integration at the mill level, and in some casesto production units that are not of economic size. It is reported thatin one state, mills with only 6,000 spindles have also finishing sections.:'This state of affairs is far from satisfactory, since it results in idlecapacity and a low level of specialization, factors which together withlow machine efficiency and labor productivity tend to raise costs.

18. It should be noted that in such countries as the United King-dom, the Federal Republic of Germany,and France, the textile industry ishighly specialized, and complete integration is found only in a fewexceptionally large mills. Consequently, except for such very large mills,the industrial integration of textile mills would not seemi justified oneconomic grounds. Specialization and standardization of production at themill would make for an overall improvement in industrial efficiency andproductivity.

19. There are still several large 4yig houses specializing intollwork, the most important ones being located in Americana (Sao PaulaState) and in Sao Paulo. In general these large houses have a strongposition in the Dolyester field on account of the high investment requiire-rents of dyeing. The smaller houses, however, have 50 to 60 percent ofthe knitted goods finishing market. which also hapnens to be the fastergrowing sector. Small houses are more flexible as to minimum quantities.Large operatorsr' mIinimmn requiremrents exclude most of the Tit-wear factoriesand warp knitters. The larger houses, on the other hand, are being threatened

1/ Also independent spinners are being increasingly squeezed by the integratedm.ills For instance, integrated mills already spirn 70 percent of poly-

ester blends against only around 30 percent by unintegrated spinners.

- 7 -

by the gradual switch of the large cotton mills to polyester/cotton blends.This points to a growth of in-house finishing at the exnense of the customfinishers. Even so, custom finishers may continue to handle peak-shavingwork ev.n for the large nolvester/cotton weavers, aside from the outnutof the smaller mills. This overall impression is confirmed by the opinionof the larger houses; who complahin that their position has bhen eroded bvthe smaller dyers. This process will probably continue because of thehigh grnwth rate of thp knitting industry.

20. As to printing, t-llwork is spread amonga ach larger rnimherof small operations and thus more difficult to evaluate. There are aroundten larg1 e cuno stoQm printers, oing boetween them soma 1 m41 1 nma t/ h

This is probably around 60 percent of the printing tollwork total, whichis- +.hia aa+Amm+.t a+. 1.5 milliof n mff%v'a/1,,A4h o ut Or +a t+,l Toaz4lin

production of 4 5 million meters/month of printed cloth.

21. As regards weaving on a toll basis, it is estixaated that itApru,rinaQ l0-000 nnn rym n rinf' na4v+ Rn Ann 1OM -nnam 4in 7a41 Tr^0+lw 4tvr^ Z--- - - __v_-_ __-w . S~~..-.,, ,,,.,&, * yA.L

Americana where there is a large concentration of weaving mills havingless thann l00 looms which nve go-ne oter alost entirely +o +his fo ofoperation in order to stay in business at all. This would represent some10 crcena of +-o+.I cot+on fl%4n- --apac, -1h. h 48 I rea sonable ag,ree-ment with the ECLA survey, according to which in 1960 around 11 percentofL co-t't on weav4 ig capsacity was in mJ '" 10 of, le8a8 L"CLU _LVW L 0-s.

2. THE MARKET FOR TEXTILES

A. Evolution of Apparent Consumption

22. Total apparent consumption of textilesa/ in Brazil rose from302,000 tonv ia 1955 to 45U,000 ton& in i970, representing an increase of49 percent.

23. As Table 5 shows, the only year-to-year reduction in totalapparent consumption during une period was in i964-65. Most other yearsshow some increase, particularly from 1967 to 1968 when apparent consump-tion grew by 6.9 percent. However, in some years such as 1963 and 1969consumption remained stagnant.

24. The per capita series shows that after declining from 1961 to1965 consumption started rising regularly up to 1970 (with the only excep-tion of 1969). However, per capita consumption was still lower in 1970Uanl it was in i955 witn 4.82 kg compared to 5.02 kg in 1955 and 5.14 Kg

in 1961. This level of consumption is to be compared with 6 kg per capitaiLn Colombia, 10 kg in Argentina, 14 kg in uermany, 15 kg in France and 20kg in the United States._

1i, in ,ierms Of natural ana man-made fibres.T/ Source: IPEA draft study on the Textile Industry in Brazil.

- 8 -

Table t: TOTAL APPARENT CONSUMPTIONI. OF TEXTILES 1955-70

Total 3/Consumntion Consumption Per Clanita

Population 2/ (Thousand of Index ConsumptionYear (-m.i I1 io)n) tons) Oqqq5loo) T( Io,rs

1955 60.2 30l2.3 100 < 021956 62.2 306.5 102 4.961957 6I.2 312.1 103 4-861958 66.3 326.1 1o8 4.92195° AR *. c '-I.9 16 5. o

1960 71.0 362.2 120 5.10I (z)i 71 0 17? n n0.Cn1.J./ V-L D t. J e V- _. 1 v- v V- .L-. * J e w

1962 75.0 372.7 123 4.971C62 -77 1 370.A 1V23 -.

1964 79.3 357.7 118 4.51I9 O1.5 A6. 121 4. 501966 83.8 383.2 127 4.57-I oA pA f, -oI' 7) -7 O En

xL;l ~a 7v uv- . -L _71.7J . f U4.V

1968 88.5 423.2 140 4.78I AAA0 AlA1.) , AVL1969 91.0 U 4f-L2 14V 4.64

1970 93.2 450.0 149 4.82

1/' Production L imports ls or of natur a,-.dt .

5/ Population data interpolated on the basis of 1950, 1960, and 1970 censuses.v/, Consumption of cotton, wool, artificial and syn.thetic ibres, silk, lilne

and ramie excluding jute and sisal. Includes industrial uses for wThichdetailed yearly data a-e not a-vailable. In 1970, industrial uses (tirecord, bagging, tarpaulins, rope, etc.) have been estimated at about64,0oo tons. L?cl-uding such ind-ustrial uses, cons-wuption of fibresclassed as for personal use would thus be 386,ooo tons in 4.14 kg percapita.

25. The composition of apparent consumptioD by fibre underwent nomarked changes from 1955 until the early sixties .1 Consumption of cottontextiles predominated throughout that period, representing always a littleless than 3/4 of the total. The remaining consumption was of manufacturesof artificial fibres, wool, synthetic fibres and linon and ramie. However,in recent years, the share of cotton has decreased to less than 65 percentsL the total while synthetic fibres increased drastically, accounting for12 percent of total fibres consumption in 1970 (against only 1.4 percentin 1960). The share of artificial fibres has also slightly increased whilewool, linen and ramie registered some decline.

1/ See Annex Table 13.

26. This general picture of the composition of consumption can beregardedl a s r,o maL -,; sir.ce couttorn is produck, edI inJL "1%ab,dance "I theU cow,1.ty,it can be expected to still predominate over all other fibres consumed,particularly as cottor products meet rmost of 'the requirements of a countrywith extensive tropical areas. Artificial fibres, which can be used eitheralone or blended with other fibres, are also qualifieu to obtain a substan-tial share of the total consumption of textiles. However, the growth ofartificial fibres has and will remain small as compared with the mughfaster growing sector of synthetic fibres. The consumption of syntheticfibres has increased four-fold from 1965 to 1970. Tne significant changein the structure of consumption of textiles in Brazil which occurred inrecent years is generally expected to be continued in favor of syntheticsand at the expense of cotton.

27. Total textiles consumption increased at the low average annualrate of 2.7 percent from 1955 to 1970, cotton textiles consumption grewby 1.7 percent only while wool, linen and ramie stagnated. Consequentlyonly artificial and synthetic fibres have shown significant increases.

B. Marketing of Textile Products

28. Until about ten years ago, the bulk of the sales for each plantwere made through wholesalers. In the virtual absence of a garment industry,wholesalers bought the bulk of the entire output from the mills and resoldit to the piece goods stores, often through one or two fu't;her links inthe chain known as "grossistas". There is no doubt that in those somewholesalers were of greater individual importance than any of the mills.This type of organization however, is facing extinction, as in the urbancenters the mills increasingly sell direct not only to the garment indus-try but also to the chains of piece goods stores and even to individualoutlets.

29. Nevertheless mission interviews with some of the major cottonmills show that 50 percent or more of their sales are still typically madevia wholesalers. In the urban centers, the wholesale trade has evolvedin two ways. On the one hand, there still exist the purely textile whole-sale houses that more often can manage to survive only by evading taxes,selling a part of their throughput without invoicing. Others have movedinto different but related fields. There are garment wholesalers who alsohandle standard items such as hosiery, men's slacks and undergarments; andindustry oriented wholesalers catering to military, government, hospitalor other institutional markets and who survive thanks to "special rela-tionships" with the appropriate purchasing agents. These latter tradinghouses may have a future although their links with the industry proper arebecoming more and more tenuous.

30. In the interior, however, the wholesaler still exists and thisis what accounts for the high percentage mentioned by the mills. Theseare usually wholesalers-retailers, who buy directly from the mill to gainaccess to the goods at mill prices, but then sell part of their purchasesthey cannot channel to the public themselves to other, smaller retail stores.

- 10 -

31. The typical price structure of the cotton goods distributionchain is as follows:

Level Price Index

Mill 100Wholesaler 130'lrossista" 170Retail 220

32. There is thus a 30 percent mark-up at each level. Thisillust.rn+ates qni+.t cwlperly the adcivan+tnag of thp nhninec . bh alimintAtna +twn

stages, they are able to buy at 100 and to sell at around 190, undercuttingother stores in the area while ennoying agross margin three times higherthan that of any single one of the traditional channels.

33. The piece goods stores are a very important outlet for thetexti;- oindust". A nf :1 l .1 A+.; nr ._ar Q D D+.i1 1__~~J X _M __- ,*-- - r - ~-' Y ---~a~~~-sold as yard goods, although a portion of this may be going to cottage

34. rPh. lroI li.e of __t a-ivieaa (ofiresged. 4 v me+ers) of +he pstores has in the last ten years declined by 40 percent, while the number_of -,,+-le+. w 11 al b;r AO per ent -- neverL-eless, --- A n(rVo

'.~ ~ .A.L tLl CA. .J .L- -MS -J d" t.-flU * W j -U t CJ. UL* Q .OO D%AMV %1¼, ~%OJ~

stores left in Brazil that deal in piece goods. The degree of specializa-4tior. dimirishes zsa e4tne rRW w cent-rs Jncreases;-h-aU.L.'Ji A t .LJU J.ILC 0. ULLC %A-A. U0"..LIV .L4.Ltu VI=I &A.L10LA LCL IJCl. "J%.-OL Z WuC.Lfd.zin cities like Sao Paulo stores will deal only in yard goods, in the out-sL.r+ 4O Itey - '1 also st0ock remady madeI I c.U.JVUMIJUJ..JLVu-LLg .L) onU e U V V LoU4w

interior, cloth tends to be one of numerous itess sold by small "generalstores.'11

35. The dominant factor- if thiL field is tne chain, which accountsfor a share of the business that is out of all proportion to its numbers.Th-us, one very- large chain, with 700 stores in the country, sells around120 million meters per year. Two other chains have 180 and 200 outlets,respectively, and seil between them another 60 miilion meters. rnus, withless than 2 percent of the outlets, these three chains of stores move over15 percent of the estimated volume of yard goods sold in Brazil. Theirbuying power also allows the chains in many cases to act as wholesalers,

IZ±ing to other stores in their geographic area and undercutting thewholesaler with his traditional structure of travelling commission sales-men.

36. A fairly prosperous sector of the piece goods business is insuitings, which are handled primarily by specialized chains. Around 75percent of all suits are stYULl tail or-made, although slacks are increasinglybeing bought off the rack._

1/ In Sao Paulo custom tailors make around 40 percent of the suits boughtor made in the city annually. But in the interior, the ready made suitdisappears almost entirely.

37. The only other channel of importance is the factory outlet.According to a study carried out on a sample of smaller mills, thisaccounts for around 8 percent of the total sales. If larger mills wereincluded, the overall percentage might be somewhat lower, but it is never-theless an important channel. Even among the middle classes, consumerstravel out to the various plants to buy textiles.

38. Lack of proper marketing organization is a problem for many tex-tile mills in Brazil. Only a small number of textile firms have a marketingsection, Among the mills visited by the mission, marketing was frequentlymentioned as an important problem.J-/ Areas where improvements were consideredas needed include increase in the number of salesmen, better training to beprovided for the latter, improved market research and quick collection ofinformation on consumers' taste and changing fashion. Also some manufacturerscomplained about the small size, poor management and lack of financial re-sources of garment manufacturers. The latter have substantially developedsince 1965 but largely remain at a semi-artisan level, often unable to cor-rectly process valuable material. Measures such as standardization and regionalmarket studies are needed to help garment manufacturers. In the meantime,chain stores would continue to be developed, in close association with the mills.

C. Evolution and Structure of Imoorts

Textile Products

39. Although small as compared to domestic production, importshave increased in the last decade from US$1.1 million in 1960 to US$12.2million in 1970._/ Imports of cotton fabrics rose from US$0,3 million in1960 to US$1.2 million in 1970. However. the largest increase has takenplace for artificial and synthetic fibres whose import value rose fror US$0.2million in 1960 to US$3.2 million in 1970. Tmnorts of fabrics consist mainlyof special process items for industrial uses, such as fabrics treated withrubber or other materials. The other manufactures consist either of itemsfor industrial use, such as rope and twine, or costly items such as linentowels, wool carpets, and even some knitted articles such as stockings.

ho. Wiile man-made fibres reoresented 15.5 percent of total imoortsin 1960 they rose to 36.4 percent in i968 but decreased to 26.3 percent in1970.3/

Textile Raw Materials

Lu. As in imnorts of finished oroducts. there was a shar_ increasein imports of textile raw materials (see Annex Table 22) and the value ofimports in 1970 was seven times hi8her than in 1960- rthith Thqkpl -819

17 In 18 mills questioned, marketing was mentioned 4 times as the secondmost important prohlTm a-d in most cases as one o tfhe fiv mostimportant problems of the company.

2/ 0. percen.t pt of total im porrt3/ About 0.8 percent of total imports,

- 12 -

million in the former vear 9 The relative imnortance of the variousfibres showed marked changes during the period, with decreased percentagesfor wool and flnr Tmrmnnrt.+ nf fflna practica1vy e-ased aq there was anoverall stagnation in the final consumption of flax products largely com-pensate hyr +'hp us of nr+ifii ml andi cnm+.hp+i fi'hrAq. ont.+.nn imnortq

were negligible and were attributable solely to occasional special importsof extra long stple fibre (38 or 39 millirneters) not prodMnno in the countr,vwhich are used for very fine yarns (100's and above) needed for the produc-I nn P' 4 mel nf h;~ Ar ov96 -nh; - Qw -- 1 - -6. 5 e> i ---

h2.* Artifi^cial an.d synthetic fibres imports rose from. about US$Tj0.3million in 1960 to US$20.3 million in 1970. In volume they grew from 136tons in 1965 to 11,4N0 tons in. 1970. Imports ere maInly for p(4,100 tons), acrylics (2,300 tons), nylon (1,100 tons) and polypropylene(1,000 + Xns. Schb. imports are foreca+st to decrease to about +.0 tr.sa

by 1975./ with growing domestic production capacity in particular forL. VfLwe iS i

D. Evolution and Composition of Exports

Textile Products

43. Textile exports rose from less than US$2 million in 1961 andU$7 MrLL.iLliun i-L 1J74 UU UOtPJ4 II"L.±-.UL irL. L7966.* jL.ej ±eaChULJ.U U04).LU o

million in 1970.Y Cotton textile products represented about 8 ercentof expor t va-lue, Jute a-na sisal products providnrg tle ba1arne.=' Of thecotton fabrics exported, the greater part is grey cloth (67 percent ofblLIt, V a.±U.- U. I ULAU LI[±aV idU.U±6 :Ap U1 -L UICU il 1 J rU ~flU a u U U -LI JJ I I T flUUMLLL.5 U

which is normal since grey cloth is heavier than other finer, higher qualityfabr-ic). There are no ex rs of syn-thetics or arici-'sal srince basic

raw materials are still importec'. and Brazil is now engaged in an importsubstitution process.

progress made by cotton textile exports in recent years hasbeen encouraging.

i5. In 1970, a trade agreement with the United Saates allowed Brazilan export quota of 75 million square meters for cotton textiles. The quotacovers yarn for 30 million square meters equivalent, cotton cloth for 39r-Lion and clothing for 6 million. The agreement provides for a 5 percentannual increase in the volume of authorized export, which would thus reach

1/ See Annex Table 22.2j See Annex Table 16.3/ About 0.7 percent of total exports.4/ 9See Annex Table 23.

1.968 1797 170 I 7 [. ±70 ±7 16 IX70

(In US$ million)

Cotton Yarn 1.75 2.82 5.77 6.81 1,806 2,960 5,781

Cotton Fabrics 1.83 4.14 9.04 11.04 808 3040 7,979

3.58 6.96 14.47 17.85 2,614 7,000 13,760

92 million square meters Dy 1974. As a result Brazilian exports to theUnited States increased in 1971 and should continue to grow in 1972 andsubsequent years.

46. Brazilian exports are also increasing to other countries.Already in the past some exports were made to Australia, South Africa,the United Kingdom and Switzerland. Efforts are now being made toexport to EEC countries. Part of wool yarn exports also go to the USSR.

47. So far, exports are made by a limited number of textile firms.Cacex (Carteira de Comercio Exterior of Banco do Brasil) has publisheda list of eight companies exporting cotton yarn while 19 other firms arelisted for cotton fabrics export and 11 to export clothing. About 25firms effectively export, of which 70 percent are in Sao Paulo. Exportsas a percentage of their sales range from less than 5 percent to 25percent. Most of the firms visited by the Mission had plans to substantiallyincrease their export sales in 1972 and 1973.

48. Government incentives provided to the industry play a decisiverole in enabling firms, who would not normally be in a position to exporta significant part of their production, to venture into foreign markets.Such incentives allow various tax exemptions and subsidies which permityarn and cloth to be sold f.o.b. Brazilian ports below domestic sellingprice.

49. It can be seen from the above table that cotton yarn may beexported c.i.f. at 97 percent of net domestic selling price (includingprofit) and cotton cloth at 86 percent of net domestic price if full ad-vantage is taken of existing incentives. When taking net domestic pricebefore profit, i.e., at cost, cotton cloth can still be exported belowcost after incentives are taken into account. This may explain whyexports of cloth have shown a faster rate of increase than exports ofyarn. In fact, a comparison between production costs and export pricesf.o.b. shows that in a number of cases mills do export cloth at pricesbelow cost.Y This clearly shows that without incentives the Brazilian

- 14 -

Table 7: INCENTIVES FOR TEXTILE EXPORT5i;'

Yarn Cloth

1. Gross domestic selling price (including10 percent profit margin, IPI, ICMand financial charges) 100.00 100.00

2. Net domestic selling price (excludingtaxes and financial charges) 71.24 66.78

3. Net domestic selline Drice(excluding profit) 64.12 60.10

4. Export incentives in percent of grossselling nrice 3.. 071/

5 f..o.b. Axnort pnrc.-k/ 63.22 .3l

6. c.i.f. export nrine&' 69.0o3 7.

1/ For detailed calculation see Annex Table 25.7/ Tnnl iiriPcz TPT irrpmnti.; n (),-70- Tr.M yomnsti nn tll <91a _ Tntrk +-Q-r-, __ _ _______ _-_ _ w _,;Z__ __r____,X__ ______

exemption (1,90), ICM credit (4,95), IPI credit (5106), financialinr-.Antves Resolutinn 71 (3TjY Tal tines -not inceA+. ie TPT credit

on insurance and freight (0,51).'A/ Tineiiidna TPT nmt....i nnc (10-71), Tr.M awpwmrni nw (IJi 49) T-n.em= +

exemption (1,54), ICM credit (7,04), IPI credit (7,70), financialiinon ivpr P.eouitioArn 71 (9 79). 'T'+n does not jinc1li TIT credi+

on insurance and freight (1,08).L/ +^c1 A-e by1 t. 1- r.g 6^Oas d-esfic se-"Ir. prc de-4-4tir eort-

incentives, and financial charges as export sales are made cash,~~ ~'~-- F6 k' r %,W. W ~ '.'J _

4IPJ.JJ W, .55.L . 6L U IJOAJ S CUJ.IJ- h=O11 IJIJ %;Uoko$Jau

and loading charges.,/fo. b. pri;c e pl us ocear freigh -. d 4 n-nem-8 a R tofreight and insurance.

textile industry would not be in a position to export its products dueto hi. p_4 r-odcto a" s.l

R,kaw ,atriL J

50. The main raw materials exported by Brazi are raw cotton, wooland sisal. For 1960-65, the annual average sales abroad are shown in Tableu. Theue a,-e 4ju tmpourts of uoer raw materials sucn as jute and ramie,but only in very small amounts.

1/ It must be recognized,however, that export prices have to be very compet-itive on the world market and that many countries other than Brazil alsoexport below cost. Brazil, now trying to open new markets, is alsoprobably obliged to sell at low prices in order to gain external markets.

Table 8: CONPOSITION OF BRAZILIAN EXPORTS OF TEXTILE RAW MATERIALS

Volume Value Unit Valueu tionusO.LALLU1 ,.) (rJ ,'±L±Lio UYT) '4 UtJy YI UUe I)

1961-1965

Cotton 211.2 108.0 5.1117 11 D I. , -Iff *wool I v. 1 .6

Sisal 136.3 29.6 217.1

Total 354.8 146.0 411.5

1965-1970

Cotton 291.0 136.6 4.69n fl C~n AH -

Wool 2u.o 0u.7 yy>±Sisal 143.9 18.0 125.1

Total 455.7 175. 3 384.7

E. Contribution of Imports to Apparent Consumption of Textile Products

51. Imports represent only a very small fraction of the apparentconsumption of textile products. However, a small percentage of textileimports is by no means an inherent feature of an advanced stage of industrialdevelopment. A number of countries more industrially developed than Brazilhave a relatively high contribution of imports to apparent consumption oftextiles. The fact that industrialized countries import textiles revealsnot an inability of the industry in these countries to meet national re-quirements completely, but a policy of keeping the tariff and/or quotaprotection granted to the domestic industry within certain limits thancan preserve a degree of competition between imports and domestic produc-tion. The competition brings new life to the industry by assuring contin-uing concern with efficiency and productivity and by encouraging a formof specialization that makes possible the optimum use of the productiveresources of the country, on the basis of its particular advantages, andthus extends the markets available to the domestic industry.

52. The high level of self-sufficiency in textile products attainedin Brazil is largely a reflection of its high textile tariffs; substantiallyhigher than those prevailing in Europe. Nominal protection averaged 122percent in 1969. Such high rates are not fully Justified for a number oftextile Droducts made by more efficient firms and can only perpetuate highcost structures in poorly organized, tariff-protected mills. It would bedesirable to gather information on production cost elements on a mill-by-millbasis (using a representative sample) in order to determine the true compet-itiveness of the textile industry.

- 16 -

Table 9: BRAZILIAN TEXTILE EXPORTS AND IMpORTS OFTEXTILE MANUFACTIUES, 1968-70

Foreign / Domestic Ratio of inportsImPorts Exports Trade Balance Consumption to Domestic------------- (Thousands of tons)---------------- Consumption(%)

1968 2.5 24.8 + 22.3 423.2 o.61969 2.6 27.1 + 2h.5 Lll.9 0.61970 3.9 27.3 + 23.4 150.0 0.9

Table 10: FOREIGN TRADE AND APPARENT CONSUMTION OF TEXTILEFA_RRTC ITN Sn.RECTED CG0NTRTES (1970?

Foreign Ratio of ImportsTrade Annarent to Annarant

IrPorts Exports Balance Consumption Consumption--------------(ThAU9anl nf' tOns) --------------- (PerCentageA)

EEC 2.822 3i063 -+2J 11 8.h82 33n3UK 644 257 -387 1,991 32.3US 1/ 870 -426 i6AWorld= 10,650 9,652 -998 56,838 18.7

1/ ExcludIng i TSSR Easter.n. Eu rope, Ghi ,na.

So"lce:. The Tertjil Gour.nil, Mnr..hs+oer, Uv1.tew Kt,ndc,rn

3. PRODUCTION CAPACITY IN THE TEXTILE INDUSTRY

53. In 1970, the basic equipment in the Brazilian spinning andxa.ir4 n6, -4 ,iiery far' -ha prensnr4 ofn c- or,, -nfl 3 .,--..dA P4 ib-n -a

flax was estimated to consist of 3.2 million spindles.17 The number ofcotton v-.piAnles was 2 0/ r,llAion .na the e,number of cott-on Alon s about 76thousand. This inrentory puts Brazil in the first place in Latin America.r-j7 a.. pos4.ition of. isUSme J.hILpJrta n U 1J nt.LU na ti%aU LsAM.L.LjV *.Z .LI .. 7%JVj, JL.L4V 11urnLIMJ

of spindles was 4.2 million and the number of locms 127,000.

1/ See Annex Table 27.wc/ This large num,ber of spindles installed. includes, hev-evr, substa-ntial

obsolete equipment with the result that much lower production is achievedwdith a very large machine inventory.

- 17 -

Table 1l: SPINNING AND WEAV1NG MACHINERiKY (COTTON SYSIr.mJIN SELECTED COUNTRIES

Spindles Looms(In millions) (In thousands)

Italy 4.1 70Western Germany 4.0 52France 3.5 56United Kingdom 3.5 75Belgium 0.9 19Netherlands 0.5 10Brazil 2.9 76

Source: Cotton industries EEC Comm,ittee and Textile Council, Manchester,United Kingdom.

Table 12: COTTON SPINDLES AND LOOMS INSTALLED CAPACITY

Thousand Spindles Looms1960 1970- 1960 1970

Sao Paulo 1,412 1,40221 31,008 33,900Rio-Guanabara 830 44O 20.159 11,730Nordeste 642 4i1 22,476 11,500Minas Gerais 532 400 16,630 13,720Santa Catarina 102 170 2,1445 3,600Others/_ 19 25 771 2.000

Total 3764- 2.878 93,I89 76.L60

Percentar'e PAre!n ta519600 1970

Sao Paulo 39.9 48.7 33.2 44.3Rio-nuanabara 2 13 21.6 1Nordeste 18.2 15.3 24.0 15.0Minas rfrais 15 0 13-9 17.8 18.0Santa Catarina 2.9 5.9 2.6 4.7Others n- 09 n0. 2.6

Total 100.0 100.0 10(0. 100.0

1/ Mainly Rio Grande do Sul.2/ Including 49,000 inactive spindles.J/ Total number of cotton spindles estimated at 3,840 in 1970 by ECLA.

Above number of 3,357 relates to industries surveyed for which onlya geographical breakdown is available.

4/ Total number of cotton looms estimated at 102, 760 in 1970 by ECLA.Same remark as in note (3).

Source: ECLA and SUDENE surveYs for 1960; Engineering Ves&Le for 1970.

54. The uneven distribution of textile equipment inventory amongthe different regions of Brazil is a close reflection of the difference inthe levels of industrial development of the various states. Table 12 showsthat the cotton textile industry is centered in the state of Sao Paulo,which has 49 percent of installed cotton weaving capacity. The correspondingfigures for the states with the bulk of the remaining capacity are: Rio-Guanabara, 15 percent both for spinning and weaving; Northeast states l5percent; and Minas Gerais, 14 and 18 percent.

55. In cotton spinning, capacity decreased by 19 percent duringthe period (while the increase in cotton yarn production was also 19 percent).The 47 percent decrease in the number of spindles in Rio-Guanabara and the31 percent decrease in the Northeast region was due to the shutting downof several mills whose severe shortage of technical facilities and lack ofadministrative organization resulted in high production costs that made itimpossible to compete in the market with manufacturers of other regions.However, in several instances, existing mills have also replaced oldequipment by modern spindles with higher unit output. These factors explainhow Brazilian average yarn output per spindle grew from 6L kg in 1960 to9h kw in 1970. i.e.. by L7 percent. The sizaificant increase in capacityin Santa Catarina can be attributed to the specialization of productionthere (towels, coverlets, etc.) and to the proximity of the major textileconsumer centers and cotuon growers (Sao Paulo and Parana). The develop-ment of the industry in Sao Paulo is undoubtedly due to the proximity ofa large market, the existence of facilities for the purchase of raw materials,nnd suihsfantial external enonomies. The same remarks applv to the cottonweaving industry.

56. In every country weaving mills are converting more and more toautnmatic lonms, bhreause of thelr higher And more uniform output andthe smaller labor force required. In Brazil the share of automatic loomsin the total has neteased frnm ahouit 2P pereent in 1960 to h4 -nercent in1970. However, this increase has been achieved mainly as the result of thepr~oga..+ress; sispp>^.c of nnwpv l1nOmq znn th- i-adhntion in tntal numbArof looms. It is estimated that the absolute number of automatic loomshas riser. from 9A0n0 in 1io to +n 0,00 in lQ70. Iho rrhrnm of nntorRtil

looms range from 100 percent in the United States to 80 percent in Western

Eur j A 1, . 4-n- ,,, 'I ' 4- m"+. -4

r-m.v4 T 4 Ain4M ~ "v -pe, 70 perent -. Pa kitar ar. 18 I cr. in. 1

-_ J I

t' A sub+ 1ta opr -io ofP the ~ " Aqir ita e 4t=n

,.id, and another appreciable proportion is between 10 and 15 years old._/T>'e SU4A11S i4sited, 1- +16e )ssio had n vr^ o-4dOetettn

over 15 years old. However, certain modern mills, particularly those newly

-LTh J.11e ULLOssi.Lon ..S.LIVU. A^U.L.LJ wLJe a. suLv 5ual A.Lr kJ.L VkofOAL 01 loMws f re30 to 40 years old. However, these looms were operated although evidently

__ A. _4 - - _ _ _ 'I*| A 4.. Al 'I - - - - - - -_ , x, k . - - _- - - -Pr VALAV.1 Vel J L , Iv . aiL tUU'vurU LAvJvD IW.L 4 L-LAU Us 1jJVKO -IUOu .LV. UX%_- V

years, they became obsolete as compared with more modern machinery. In-. J.L. TV_4Le.2 S~.LL.. ' -- I..L .. 4-.. !' J.. f

E-rope andu u'-e VuILi St,aue loomOs are cui -udlU uobsoleteu afual 5 to 6

years.

- 19 -

established in the Northeast, have a high proportion of machinery less than

5 years old. In the Northeast the proportion of looms above 30 years hasdecreased fram 81 percent of tht total in 1959 to 35 percent in 1969,whereas the proportion of looms below 10 yearphas increased from about 10

percent to 35 percent during the same period.±' Detailed data are lackingas regards the various types and age of machinery existing in Brazil. An

inventory of textile equipment should be made in order to detenmine theexact degree of obsolescence of machinery.

58. Production capacity is determined partly by the number anxltypes of machines available and partly by the level of utilization,which depends both on technical conditions and on institutional factors(such as the number of hours worked per shift, number of days of leave perworker. relative importance of women in total staff, etc.) partly or wholly

outside the industry's control. Although most existing machinery is utilized,not all available hours and shifts are turned to account. The proportionof machinery utilized is satisfactory, but the number of hours and shifts

worked is rather less than it might be; not only because of legal andinstitutional factors, but also because the age of machinery results ina high proportion of stoppage time for repairs and upkeep.

59. The number of hours available with three shifts is theoreticallyeight hours per shift and 300 days a year, or 7,200 hours/year. But as the

third shift is usually shorter than the others because of the time neededto clean machines and the compulsory rest period halfway through the thirdShift which is required by social legislation, production estimates arebased on a third shift of only six hours, which reduces the daily workinghours to 22, and gives an annual total of 6,600 hours. In Brazil', theactual number of hours worked in cotton weaving has been estimated at 5,400hours/yea-r in. 1970n,/ i0e.- 82 nercent of theoretical work time. This

compares with 5,062 hours in 1960y, i.e., a 6.7 percent increase from 1960so 170.

6o. Lil+4izat-ion of Gapacitv is higher in spinning than in weaving.

Data for Sao Paulo State show that the number of hours worked in spinningwas ,739 in. 1970 against 5,235 in 1960. i.e., a 9.6 percent increase.Hours worked in 1970 represented 87 percent of theoretical work time. Thenmrber of pindlle hours is higher than that of weaving hours because the

spinning mills have to supply intermediate products to other textile groupsmakine kn4tted goods, carpets, rs-pe; sewing thread , etc. Furthermore, there

is a preponderance of small weaving establishments run on family lines,and there are institutional difficulties in having a three shift working

day in mills of this kind that are unconnected with the big manufacturingsectors. i'4naly,r lnck of mnarket for cotton cloth has been mentioned to

J./ toeU Ann I Ta9U 31.Source: Engineering Vesdre.

. s Sources ECLA.

- 20 -

the Mission as the most important problem faced by cotton -ills which alsoexplains this relatively low utilization of capacity.

61. Table 13 shows the difference between the use of spinning andweaving capacity in Brazil, and in selected countries. In terms of theproportion of hours available worked in the cotton spinning industry,Brazil is somewhat below the United States, but achieves better resultsthan European countries, the low utilization in the latter being largelydue to a lack of man-power and the existence of surplus capacity. Inthe case of weaving, Brazil is substantially below the United States butstill well above European countries.

Table 13: SPINDE AND LOOK HOURS WORKED IN THE COTTON SECTOR

Annual hours per Annual hours per %spindle Increase Looms Increase

1960 1970 1960 _ __ _ 1970

Brazil 5,235 -/ 5,73#/ 9.6 5,062 5s40o 6.7Western Germany 3,780 4,051 7.2 4,051 3,635 -11.3France 4,124 4,654 12.9 3,515 4,134 17.6United Kingdom 2,236 3,697 65.3 2,636 3,146 19.3Japan 4,826 5,264 7.0 4,789 4,862 1.5United States 6,219 6,079 -2.3 6,427 7,186 11.8India 6,068 6,193 2.1 5,346 5,585 4.5

1/ Data are for Sao Paulo State where about half the cotton textile capa-city is concentrated.

Source: International Federation of Cotton and Allied Textile Industries(IFCATI).

62. Underutilization in Brazil of the hours available is due toold machinerv and institutional factors. If all the available hours werefully used, production capacity for cotton fibres would in theory expandby about 13 nereAnt in spinning and 18 narcent in weaving.

4. NTTT nfTPPT OW MA(RTtNJRY ANn T.AROR PROMDTITVTY

63. Unit outpnt, in 3rail ian cottnn Rninning milTh has bhpn esti-

mated by UNDO consultants at 18.4 grams per spindle/hour in 1970 on theh1-qii of an average yvrn eo-nnt of 1RI l/- This C-mYuiar-A viti an Rverage

unit output of 20 grams found by the Mission in plant visits and with a1ower esmicte~ hi the I'n1ors An eis nrlador nA e Sa P lo eof abnhnt I

grams for Sao Paulo State.& However, Mission estimates include certainbJ lar npnAllrtitr -millct wh;-h mn-r wowmlt in Qnmn nvrdavgct

Brazilian unit output of machinery.

1/ Source: Engineering Vesdre.2/ See Annex Table 30.

- 21 -

64. A unit output of 18.4 grams per spindle/hour is to becomr%ny.aA wi +h nn naloaga eri i+v..+. ofv I Is ierl 4ne 19hn, Oi.A 'I an ss+ov.i

increase of about 30 percent. Such output remains, however, below the

This shows that unit output is still low in the Brazilian cotton spinninga-C*' yV U. °o.w'e V Wr 3 U,U L%.. U %OL= LO soWe exceed thAe 0 adUope ILVU UVU UY

ECLA testify to the feasibility of a reorganization program designed topromotJ e eUA0 wiLe U.LL-e J.LiVftisLUL Vo. FCU%;VUW 5U s MVU 'w.ALCS Vof W'rL Watare already in full use in some mills.

65. Labor productivity is not known with precision for the whole ofDr-azil. nowever, a study by SUDEN shnows AT output in grama per mian

hours was 3,435 gr in the Northeast in 1970..~/ Estimates for Santa CatarinaState coverj.u-g 5u percent of the installed spindles capacity snow anaverage output of 2,956 gr per man/hour. Assuming conservatively thataverage Brazilian la-bor productivity was 3,uuu gr per man/nour in 1970,this would represent a 50 percent increase over the 1960 average of 1,996grams per man/hnurs anc a reauction in te number or workers ror 1,0U0spindles from 7 to 6.3/ Despite such progress, Brazil remains below theLatin America standard set by EGLA of 4,300 grams per man/hour and of5 workers for 1,000 spindles.

66. As regards cotton weavin7 the average output was estimated at5.40 meters per loom/hour in 1970,YV against 2.93 meters per locm/hours in1960. This represents an 84 percent increase in unit output, largely dueto the increase in the proportion of automatic looms in total installedcapacity (from 25 to 45 percent). The number of hours/year where spindlesand looms are in operation has evolved as follows from 1960 to 1970:

Latin Amerip1960 1970' % Increasie StandardZ/

Hours/spindle/year 5,235 5,739 9.6Hours/loom/year 5,062 5,400 6.6 6,600

1/ The Latin American standard was based on a unit output of 22 gr perspindle/hour for carded yarn of count 18. The standard workload adoptedwas five workers (of all ages) to 1,000 spindles, which represented 200spindles to each spinning operative. Output for 1,000 spindles wastaken as 22 kg per hour and output per man/hour as 4,400 gr (22 k2/5workers). In Brazil, as in othei Latin American countries, about 80percent of the yarn produced is carded and about 20 percent combed.Combing involves the use of more machinery and hence a greater numberof operatives, estimated at about 10 percent more than those needed forcarding. To allow for this difference, the standard output adoptedfor carded cotton yarn was reduced by 2 percent, giving an output of4,300 gr per man/hour as the average standard output for Zarn of count18 (both carded and combed).

2/ On the basis of an average yarn count of 18's._/ Unit output per spindle loom divided by output in grams per man/hour.i~/ Engineering Vesdre.5/ As set bv ECLA: RAP naraf anph 59 4, 4for ,-.4l. A4e..-av.

- 22 -

67. Above figures represent only approximate averages and do notgive a full picture of the extremely large variations existing amongmills. Some mills may have obsolete equipment and be of small size, butthere is also a nunber of relatively small mills (i.e., about 200 looms)which have attained a good level of productivity and which have a fairlyhigh portion of old machinery, Similarly large cotton mills show vastdifferences in productivity with about the same equipment. Consequently,after studying the limited data available, it must be concluded that theexplanation of that part of the variation in productivity not attributableto physical factors involved must be looked for in the human factors inthe production process. The most important is mill management, includingthe whole concept of the entrepreneur's or manager's responsibility asregards use of satisfactory raw material, careful machinery maintenance,manpower training, etc. The question arises whether manpower training isthe direct responsibility of the entrepreneur or whether he siould make useof the services of existing training institutions. The plain fact is thatlabor productivity in some mills is many times that in others, and theexplanation of such very different results in the same country would appearto be the concern of the entrepreneur. Differences in productivity, giventhe same conditions of obsolescence, mill size and type of product, callfor a more searching analysis, which is beyond the scope of the presentreport. Nevertheless, a more thorough knowledge of the reasons for thissituation and of the role played therein by the entrepreneur will contributeto the more efficient operation of Brazil' s textile industry.

68. The existence in one country of mills working efficientlyside-by-side with others where conditions are sadly deficient proves thatefficiency can be attained even under existing conditions* For theinefficient mills, attaining these standards might require some time, andprobably pravision of appropriate incentives and financin-g but there donot appear to be any insuperable difficulties since the moreprogressivemills have been able to reach their present standard with the resourcesnow available. The foregoing implies also that Brazil possesses sufficientknow-how to attain pr-oductivitv levels comnarable with those of Europe,and that this kind of knowledge,whether administrative or technical couldwell be channelled into an effort to reorganize the 1ndu try on a rationalrbasis to meet future requirements.

5 PRODlUCTTON COSTS

A. Labor Costs

69. Labor in terms of wages paid is relatively cheap in Brazil,even with the payroll taxes, paid holidays, 13S h month bonus and otherbenefits which represent about three-fourths pereent of the hourly wagelevel, O. the other hard, l1w "roduc it&V1y means that labor accounts fora relatively high share of production costs.

- 23 -

70. The average monthly wage in the textile industry in Sao PauloState was about Cr$260 in May 1972, i.e., about Cr$1.08 per hour (US$0.18).2!In the weaving mills with automatic loms, one operative can handle a greaternunber than where the looms are mechanical. The wage paid in such cases ishither bv about 20 nercent.

71. The different social securitv-related navroll taxes should beadded to the wage as should the cost of the 13th month bonus, weekly timeoff; legal naid holidavy and the annual naid vacations -- ueuallv 20 davB --all of which are required by law.

72. The incidence of all of these changes in the case of Sao Paulote,lt.ile millq i9q skwn in Annr,r 'Pnh.- 32. Vno thes A ,A 11q non-waue laborcosts represent 77 percent of basic wage costs, i.e., in the case of anhoil-lg A" wair ofvA MI,83 +he varieus socriol c.>12&A Mes ar.d be-Nits Z1Tnn1"tPd

to Cr$O,838, giving a total cost of Cr$1,921 per hour.

73. The labor cost per kilogram of yarn resulting from the pro-ducttiity leegl e1ti.ted abe at I,+ 0 r0 pert --- -- a--

64) is Cr9 . Cr$0,640 i.e., US¢10.9 per kg of yarn produced.

countries.2/

Table 14: LABOR COSTS IN SELECTED COUNTRIES

A.ZV . V D / 4 Z 1 4 I

Hour US$/Kg Yarn Hour Hours/Years- ( ~~~~~~~TUIOW

Bai .7 10.9A 30 ^eAll

West Germany 132.0 12.5 10,530 1,906France 98.0 10.3 9,490 2,0United States 242.0 13.6 17,775 2,400Japan 42.9 7.2 5,920 2,232Hong Kong 32.3 7.2 4,500 2,464

Inuia 19.0 ~~9.5 2,000 2,304

75. The above estimates clearly show that the level of laborproductivity wnich is still rather low in Brazil is an essential factorin determining the cost of labor per unit of output. Although Brazilianwages remain low, they are to a large extent offset by lower labor pro-ductivity, thus resulting in a relatively high labor cost per unit of output.

1/ See Annex Table 32.6/ Sourcet Werner Associates, Inc. New York.

B. Cost of Raw Materials

76. Two main ty es of cotton are used: Paulistal/ and NordestinomTedAim, ale otton+._/ Bot+bi are of fan4 l r t% nnlinl i +%, wit +h a,iea a

fibre strength, but their classification leaves a good dpal to be desiredrhie'nh mnsvia +.In+ +.3h m4ill ewr,nir' hnzra afna+A.mrna +.n Tc.r'1naaif'ir le-&.- my47,4v

at their warehouses. The lots are mixed, consisting of fibres of different1 --nths; ofter. they are not cleanr enr.o ng1, -.n ^"MIMl s"artards, ardthis leads to a relatively high proDortion of wastage. This is particularlythe cas-.e for NoTdtir.o+A . .st..n stpl cottor..l M,ng of' various fibre-length cottons is one of the causes of inefficiency and low productivity insp mi n rinn a.d results in production l,oses. rt I n a to al^ +naetheamount of wastage, and to lower the quality of the yarn, a defect thatultim.a4

el r affects weae.g o1+put+ *T i9 h,wsr, -^+rtd- 0 A 4h1na+&5 _ p _ LW ~~~~~~~~~~~~~~~~~~~~ .&Y"WW-A, ._JJ_- _ W-W~~~~~~~~~~~~~~~~~~~~~~~~, *..~,~* *u ~ v

progress has been made in recent years in reducing wastage.

77. The cost of Paulista cotton no. 5 (1-Y6 inches), which is themost4 c oam,,or nZS US30J Ie o,--^ 9073.re 4cvnoLiA~J~ U t~ VMS 1fi!AA, UsJf 1)' -)J I - -A~L1J -1 . IC '-q7 / f .- * .4, J~UU UJ

similar quality produced by other countries w,ere generally more expensiveas Shown in Table L5. Thus, BraZil i8 ,n a f.arly good position as regardsits supply of raw cotton, subject to reservations as to cleaning and classi-ficationL, Which cause wastage and er-lntal the expense Of'I 'eLaSsif'CatiOnIn addition, the marketing system entails the tying up of large aum9 ofmoney, Since th;e whole yearly -"uP'4Y O' et,uux,-UO ly hs to be boughbduring the months of the crop season, and the indumtrialtsts who have tobuy 1n advanUce are forced to pa-y the Undt4.-y aig prices aaked on the currentmarket for some of the scarcer types of cotton.

Table 15: PRICES OF COTTON IN SELECTED COUNTRIES .

1970/ ?71(Average)

Brazil SP Tip o 5 30, 31Mexico aI, l, -/l6. '; J,12United States ,M, 1-1/16" (Memphia) 31,77Turkey - Izmir 3a, 1-1/16"1 30,67Syria SM, 1-1/16 " 31,11z.caragua 94, 1-1/16" 30.,98Soviet Union SM, 1-1/16", 33,30

Source: Bolsa de Mercadorias do Sao Paulo.

1/ 1-1/6 inches or 30/32 mm.7/ 30/32 and 32/34 mm.3/ 12 month average.

- 25 -

78. Brazil is in a much less favorable position as regards syntheticfibre supplies part of which are imported and part of which are producedlocally by two of Brazil's existing synthetics producers (of which one hasabout 90 percent of the domestic production capacity). For example, theBrazilian price of polyester staple is US$1.98/kg while it is only US$0.80/kgin the United States (but was US$2.00 in 1964).1'

C. Machinery Costs

79. Most of the machinery in use is old and is generally not properlymaintained. The units are of almost every type, make and origin. and arealready fully amortized, with the exception of a certain number of machinesimported in recent years. To this last group must be added the machinesproduced domestically (see text Table 16). No estimate of amortization canbe made, as neither the value of the machinery as a whole nor that of theas yet unamortized machinery is known.

80. Domestic production covers only a portion of the machinery requiredfor the spinning and weaving of cotton and artificial fibres. for prepara-tion and conditioning of yarns and for dyeing and processing in general.Thus, in the existing- circumstances it is necessary to imnort many tvnes ofmachinery that are not produced or produced only on an insufficient scale,by domestic manufacturers. Tn brief; the conditionks governing imnnrts c.fmachinery are:

(i) where no similar machinery is produced domestically,eAuipnment is generally ijnortAd wit.hoult c-i+o.mnduty;

(ii) where similar machinery is produced domesvically,iforfts +te bJay-= CI r+o iMn^ortAIMD Auies of1- An t

percent. The mission did not hear substantialcomplaints reqa"eijv%" +the applij+jto.w" ^ +o,tprinciple of "similarity' by administrativeauthor±ties.

81. The yst--em governing import-s of pa-ts a" accessories is thesame as for machinery, but most of the items needed are already beingrodAucedlA 4 t- +he c^',,+w * " A , e -1 n-O+. -4 . 1 I - 41- I -- - - ---- -*v-v^-g * ^ v- --J * -- - EVW La ' WO

have their own factories and workshop and produce many of the parts andaccessories needed th.emssel-vues, &-d &-e of+er. abl to -recor.ditior.4- or ever.manufacture certain machines. Thus, lack of spares is not considered aproblem of 4y r tn 4n B r 4n

1/ Polyester staple prices have continuously declined in the lastter. v as

- 26 -

Table 1% O1 TTIN OT ^V TT I r-rMIWI'r%Ti? N MV1VTI' T?w1J

(.In p.eLcenitage Of val-ue of m.u.LplWuInU)

-17 n -1 %V 17 1 79 17.L >VU L7V f L7V J7V 7 U7t

1. Brazilian Finns

T _ _ s _ I ~~r ]_ _ _1M I 0-t r ^ 0 1oI inporteu Equipment 95.4 8u.7 69.2 84.9 807.Local Equipment 4o6 18.3 30.8 15.1 12.1

Total 100.0 100.0 100.0 100.0 100.0

2. Foreign Firms

Imported Equipment 96.0 63.5 89.8 54.3 66.7Local Equipment 4.0 f0. lO 45.7 34.3

Total 100.0 100.0 100.0 100.0 100.0

3. Total (1 + 2)

Imported Equipment 95.5 79.8 70.5 75.8 82.9Local Equipment 4.5 20.2 29.5 24.2 17.1

Total 100.0 100.0 100.0 100.0 100.0

Source: IPEA - Study covering 156 firms.

D. Cavital Co.ts

82. In recent years, textile industrialists have financed abouthalf of their investments through their own resources and half throughloans, the latter about equally divided between domestiG and foreign credits.

83. The profitability of the textile industry is not particularlyhigh. An analysis of balance sheets of 33 textile companies shows an averagenet profit on capital and reserves of 12.6 percent (see Annex Table 34).Hoiwen-3r, 10 out of 33 companies show net profits of less than 8 percentand 15 less than 10 percent. Some highly efficient fires show very highprofits, i.e. around 25 percent. This reflects the wide dispersion betweenfirms of different productivity already noted above.

84. The number of firms which have engaged in modernization, ex-pansion or opened new plants is relatively small. One hundred and twenty tex-tile firms were given investment incentives by the government's IndustrialDevelopment Council (CDI) in 1971 (see Annex Table 35). This number probablyrepresents most of the firms having effected substantial investment during

- 27 -

Table 17: SOURCES OF FINANCING - TEXTILE INDUSTRY

(Average 1966-70, in percentage)

1. Company's Own Resources

Capital and Reserves 9.8Retained E.arnings 3u .Fiscal Incentives 3.4Others 0.1

Total 47.7

2. Other Resources 52.3

i. Domestic

Regional Development Banks 9.0Commercial Banks 3.4BNDE/FIPEME 5.3Domestic Suppliers 2.5Bank of Brazil 0.8BNDE/FRE 0.5BNDE/FINAME 0.3Others 2.1

Sub-Total 25.1

ii. External

Suppliers'Credits 18.9Financial Credits 8.3Direct Investment 0.0

Sub-Total 27.2

TOTAL (1+2i+2ii) 100.0

Source: IPEA - Study covering 156 enterprises.

- 28 -

1971. However, enterprises procuring small amounts of equipment onlyprob-ably did r.o+ soii G,.I 4e.ivs-

AC Tle Ie e a.of N - -1 - m t t4-^ 4 | A- 4---*41_ .V>.).L A-, W. _ - W. J .1 J- ^' - -�� . IL W.JW UA. W .W 4LULLU u41 UtL a OD en

relatively high in recent years, i.e., around US$100 million per annum inI969/71. Thi4s com,-ares with only abot- US$50 o-41"ior in 1967 and In 1968 2/It must be noted, however, that in the total of US$100 million are includedsome exceptionall.y large nvesQtmLents. For example, in 1971, about 20 per-cent of the total was for two new plants to produce synthetic fibres andfor.L a vet large LC.L-,.ode.. .izatior.L-6 Crog&..

86. ,The national and regional development banks are the most impor-tant source of domestic long-term loan capital. The Bank of the NortheastkDnv) proviUeUj Ub LLoLVd16- 4rU± sorW k -Uxlu ZL.LUt:1 lor LMextle inaustries inthe Northeast. Several modern plants have come to that region in recentyears. Entrepreneurs have had access to subsidized resources in tne formof 34/18 funds. These resources, while normally not available to financethe cost of imported equipment, release their own resources for that pur-pose. In several instances, SUDENE has permitted project sponsors to con-vert 34/i8 funds into foreign exonange.

87. BDE an- its specilized subsidiaries such as F1NAME and FIPEMEis also a significant source of finance. FINAME finances purchases ofdomestic equipment. It covers '0 percent of the cost of equipment; privatefinancial intermediaries are expected to finance 30 percent and the sup-pliers, 20 percent. FThAME !enas on terms up to 15 years and at 3 to 8percent interest plus monetary correction. The objective is to assistdomestic equipment producers, who are not in a position to compete withforeign suppliers in providing credit to their customers. However, asnoted above, this objective is limited by the need to import most of therequired textile machinery. FIPEME is a special fund designed to assistmedium-size industries, and seems to be the second most important source ofdomestic borrowings for the textile industry. These funds utilize pri-marily tax resources and external credit as well as repayment of earlierloans.

88. The Fund for Modernization and Reorganization of Industry (FMRI)is another specialized agency of BNDE for the financing of investment and/orworking capital to firms facing financial reorganization problems or wantingto merge. Terms are up to 4 to 5 years. For mergers, interest rate of 6percent and for other cases, 8 percent (both plus monetary correction. ThroughMay 21, 1972 FMRI lending totalled Cr$229 million (about US$38 million). Loans

1/ CDI data do not cover fixed investment in the Northeast.

2/ The above-mentioned IPEA survey covering 156 textile firms gives anaverage annual fixed investment during the period 1966-70 of US$40.8million. (1966 = US$4.1 million; 1967 = US$16.1 million; 1968 = US$38-4million; 1969 = US$65.4 million; 1970 US$79.8 million.)

- 29 -

were made to 25 finns out of which 7 were for textiles. FMRI's source offunds is the BNDE. External credits play as important a role in textileindustry investment finance as domestic borrowings. The largest amountis represented by suppliers' credits, the balance by financial credits.The cost of financial credits is somewhat less than of most official domes-tic financing and much lower than that of private domestic financing.

Table 18: TERMS OF EXTERNAL FINANCIAL CREDITS

Borrower's InterestRate

Nominal Real _Mat urity _

Commercial and InvestmeitBanks (Resolution 63)i/ 24% 8% 6 months to 10 years

Other External Financial Credits(Instruction 289)2/ 22% 6% 6 months to 1 year

Law 4131-2/ 22% 6% 6 months to 10 years

1/ Borrowing abroad on behalf of Brazilian clients.2/ Firms allowed to contract directly with external lenders for working

capital finance. Usually the lenders are parent companies of theBrazilian borrower.

3/ Law 4131 covers a variety of transactions including some import financingbut like both Resolution 63 and Instruction 289 categories, it is usedprimarily as a source of cruzeiro denominated investment and workingcapital finance.

89. Reasons which have motivated recourse to this tvne of credit bythe textile industry include: (a) limits on and -- in some cases -- thehizh cost of domestic credit; and, (b) the fact that foreign nrincinalq canmaximize capital income extracted from Brazil if they make capital availableas loans rather than equity participation.

90. The 2h and 22 percent borrowers' cruzeiro interest rates on thesefinancial credits quoted above assume: (i) a 7 to 8 percent dollar interestrate plus withheld income tax at 33 nircent of the interest nnvmant;. s(iJ A2 percent Brazilian intermediary's charge in the case of Resolution 63 fin-ancine: and (iii) 10 percent annual xychange rate devAluAztIon ao pranyingan internal inflation rate of 15 percent. Were the authorities to devaluethe cruzeiro at annual rates eaunl to the rate of inteArnnl i nfl Ati on ratherthan to that rate measuring internal inflation, the borrowers' cost of thiscross currency financino would mAke it much leAas cnmtnaiti1?lJ

1/ "Current Economic PoatI+oAns nd PD"mr of %P M uml4e if paragr>ah161, IBRD, September 30, 1971.

-3r-

9i. Thu5-9s, despite rapidd expansiion uI du1moestic sources oI inwestmenzfinance (at least as compared with the situation prevailing in the earlysixties) the hign cost Of dome stic borrowing makes investment finance neavilydependent on retained earnings and external credit. Regional developmentbanks and B-uEJ make medium-term loans but their contribution to total invest-ment remains limited (about 15 percent).

92. W.i'h respect to working capital to meet the need for ii-int inventories,conditions in the raw materials markets oblige the industrialist to buy farin advance; during the four months of the crop season he generally buysenough to meet all his needs for a whole production year. Thus, the 60 to120 credit available from commercial banks to finance working capital re-quirements is inadequate. Tne industrialist must finance his productionfrom the point of maturity of such credit up to the time when he invoiceshis own customers.

93. Considering that the industrialist must bear a large part of thefinancial burden involved in carrying large stocks of raw materials and thatthe nominal rate of interest on working capital finance now averages about34 percent, it can be concluded that the textile industry faces seriousproblems as regards working capital. This problem was mentioned to themission (together with lack of demand) as the most important problem metby textile mills. The situation is made even more difficult when weakerfirms, lacking access to long-teim finance, resort to short-term borrowingto finance purchase of machinery.

94. These financial problems tend to perpetuate the relatively poorstate of the present machinery inventory, with considerable adverse effectson production costs.

E. International Comparison

95. A comparison of labor and raw material costs per unit ofoutput between various countries shows that raw materials costs are relativelylow and labor costs relatively high in Brazil' s cotton spinning and weavingindustry. The result of these two contrary factors is a joint input oflabor and raw materials per unit of output (fabric of a given tgne) some-what higher in value term than that found in the United States and lower thanthat found in Western Germany.

96. As regards labor costs, differences are due to low productivitvin spinning and weaving, particularly the latter. The number of man-hoursrequired to produce cotton fabrics is much higher in Brazil than in theUnited States and therefore productivity in weaving in Brazil is much lowerthan that for spinning. This fact calls attention to the need for thorouahsteps to improve operating conditions in weaving.

97. As noted above, the cost of raw material (Brazilian cotton) isabout equivalent to that of the United States; takina into annnurlht t.hna. inBrazil the low price of raw cotton is offset by higher wastage.

Table 19: COMPARISON OF COSTS OF COTTON AND LABOR FOR THEDDAfnlTrT90TTA?T AP A UZPLID Al;l fArv-l%YT WAODD(r.LL%L 0UV-.Lu%1 V; £r L- raU vL w-L . * vj* .Ls1 rjXE ± v..

IN SEICTED COUNTRIESY

(US¢/meter)

ui twd -Brazil States Japan Germany Hong Kong Iran

Raw Materials 7.18 7.18 7.42 7.63 7.25 7.19

Labor 6.50 4.80 3.75 7.43 3.75 6.36

TOTAL 13.68 11.78 10.17 15.06 11.00 13.55

_/ Cotton print cloth - 100 cm wide. Cotton counts 20's.

Source: Brazil - Mission estimates. Other countries: IBRD Report PI---,June 10, 1971.

98. This brief comparison leads to the conclusion that if Brazilused a better quality cotton, leading to a lower percentage of wastage, andif the number of man-hours to produce cotton fabrics were substantiallyreduced, Brazil could compete successfully in the world market. In fact,this is already the case for certain Brazilian firms whose productivity levelsare appreciably higher than the national average.

99. Nevertheless, it must be borne in mind that this comparison relatesonly to the cost of two inputs. If the others are taken into account, Brazil'srelative position wodild probably be less favorable since the prices of relatedmaterials (such as dyes) and machinery are higher than those in the UnitedStates, Japan and Germany. However, the incidence of the other components inthe cost of production should not represent more than a tLird of the totalcost, and if this is so, the price differences referred to would not have anappreciable effect.

100. It should be borne in mind, however, that the amortization of asubstantial modernization of the machinery would constitute an importantcomponent of the cost of the product. Consequently it would be necessary toreduce to the minimum the portion represented by other costs (mainly generaland administrative costs).

6. REORGANIZATION AND REEQUIPMENT OF THE TEXTILE INDUSTRY

101. The conclusions drawn in the previous sections give a pictureof imnrovned hbut. sQ+ti1ll un.san+t.ifac+.nrtr ynnn+.lnA opeattin.cnditlnn is +.hnt Pr:a7.i1inn

textile industry. Not only is the machinery old (despite the coming up of

- 32 -

some new plants and some modernization in recent years) but the low levelsof unit output, comiparedt-u WJL± WLMU %-;UL"IA wa coUGL."AW%L .'d.LW WAAV J.A .epst.L'JLL0,

show that even the existing machinery is not being fully utilized. Laborproductivityu is equally- low, reflecting inefficien,t tainn4g (lack of pr-oper-skil ls was mentioned by industrialists to the Mission as one key problem),inadequate internal orgaLizationL ad poor di.strb-utioU of workloads.

102 racr other tba- machinery- obsolesenc ___3 iu2-- at ls-1 1.LU.C. Fac'oors oi,ijev IaUli U DCLJ.±IiLy ULJU.U±C e4IUI .l.lu ..U 4LLcquaC .LaWUL

force training and utilization contributing to the inefficiency of theBrazilian textile industry include the poor quality of the raw material,lack of balanced output and good plant layout, and human factors such aspoor management and the lack oI qualified technicians and supervisors.

103. This indicates the complexity of the problem and the impossibilityof solving it on a piecemeal basis by remedying only one of the factors in-volved. Modernization of the equipment alone, which according to theabove analysis is the most marked single factor in keeping efficiency andproductivity low, Ls not likely to produce good results unless it is carriedout in conjunction with other improvements. For example, even the mostmodern machinery cannot produce the output of which it is capable if thepoor quality of the raw material continues to cause a large number of yarnbreaks and a high percentage of wastage. Moreover, withou-, proper training,the labor force would not be able to operate such machines. These areonly two examples which show the importance of a coordinated program con-templating both equipment and administrative reorganization.

104. Nevertheless, the main element in such a program would be modern-ization of the machinery and the improvement of its operating conditions,aimed at remedying the part of the overall operational efficiency of themachinery due to obsolescence. In practice, it would be difficult to under-take action in other respects (internal organization, planning of production,manpower training, quality of the raw material, etc.) without reequipmentsince internal reorganization involving a basic change in methods could noteasily be introduced without a parallel basic change in the characteristicsand composition of the machinery. In other words, reequipment is by itsvery nature a dynamic element, which is closely linked with action in theother fields and would provide an impetus that would undoubtedly be lackingif action were confined to the administrative aspects or just providingworking capital in isolation. Reequipment must therefore be the nucleus ofan overall program of modernization, but it cannot be fully effective inachieving higher levels of productivity in the Brazilian textile industryun' r o it goes hand in hand with a series of measures to improve wide organ-ization and manpower training. Only an integrated program combining thetwo elements, reequipment and overall reorganization, can provide an effectivesolution to the industry's problems.