INITIATION | COMMENT JULY 24, 2012 Federated Investors, Inc. (NYSE: FII) Liquidity at a 'Buck', But for How Long? Underperform Above Average Risk Price: 19.69 Shares O/S (MM): 104.2 Dividend: 0.96 Price Target: 19.00 Implied All-In Return: 1% Market Cap (MM): 2,052 Yield: 4.9% Priced as of market close, July 24, 2012 ET. Investment Conclusion We view recent regulatory efforts to introduce new rules for money market funds as the biggest challenge the company has faced. Any of the new money market rules proposed by the Chairman of the SEC Ms. Schapiro — floating NAVs, capital buffers, or deterrents to redemptions — could lead to significant outflows, in our view. Sure, there have been encouraging developments with positive flows into Federated's equities business and continued strong flows into its fixed-income funds. However, the shares are trading at an in-line multiple with its peers despite facing a potential risk to its core money market franchise. We provide sensitivity tables to demonstrate the effect of outflows on our price target were the new rules adopted. The following lead us to our investment conclusion: • Federated is leveraged to money markets: With 75% of its total AuM in money market funds contributing to 40% of net revenues, we would expect an adoption of new rules as proposed by the SEC to affect earnings negatively. • Tougher money market rules could be introduced despite strong opposition: While there has been widespread resistance to new rules proposed by the SEC's Chairman, investors should not dismiss this initiative yet. Ms. Schapiro will put her proposal to a vote in late July. If the proposal fails, tougher rules could still be introduced with the Financial Stability Oversight Council (FSOC) gaining regulatory oversight over money market funds by declaring them to be 'systemically important'. • Large outflows a possibility: If passed, any of the proposals put forth by the SEC will make money market funds especially desirable and could lead to industry-wide outflows, we believe. The risk to Federated is not to be ignored. Federated's CEO has emphasized on various occasions that the money market industry could be changed significantly if the proposed rules were to pass. • Limited upside potential, fairly valued: With the stock trading at 12x 2013E P/E, which is in line with its peers, we see limited upside potential. Historically, Federated has traded at a discount to its peers. We see potential downside risk, should money market reforms be approved. We apply a 15% discount to the peer multiple. Priced as of prior trading day's market close, EST (unless otherwise noted). 125 WEEKS 12MAR10 - 23JUL12 16.00 18.00 20.00 22.00 24.00 26.00 28.00 M A M J J A S O N 2010 D J F M A M J J A S O N 2011 D J F M A M J J 2012 HI-28JAN11 28.57 HI/LO DIFF -49.74% CLOSE 20.44 LO-23DEC11 14.36 5000 10000 15000 PEAK VOL. 20787.9 VOLUME 838.0 60.00 70.00 80.00 90.00 100.00 Rel. S&P 500 HI-12MAR10 100.00 HI/LO DIFF -47.95% CLOSE 66.46 LO-23DEC11 52.05 RBC Capital Markets, LLC Bulent Ozcan, CFA (Associate Analyst) (212) 863-4818; [email protected] Eric N. Berg, CPA, CFA (Analyst) (212) 618-7593; [email protected] Kenneth S. Lee (Associate) (212) 905-5995; [email protected] FY Dec 2010A 2011A 2012E 2013E Adj EPS - FD 1.73 1.45 1.70 1.80 P/AEPS 11.4x 13.6x 11.6x 10.9x Net Flows (B) (35.8) 10.2 0.7 15.3 AUM (B) 358.2 369.7 375.4 395.2 Adj EPS - FD Q1 Q2 Q3 Q4 2010 0.38A 0.46A 0.42A 0.45A 2011 0.32A 0.41A 0.37A 0.36A 2012 0.41A 0.42E 0.43E 0.45E 2013 0.44E 0.45E 0.46E 0.46E Net Flows (B) 2010 (40.8)A 79.1A (89.3)A 15.2A 2011 (4.9)A (6.2)A 5.8A 15.4A 2012 (9.3)A 3.3E 3.3E 3.4E 2013 3.8E 3.8E 3.9E 3.9E AUM (B) 2010 349.9A 426.8A 341.3A 358.2A 2011 354.9A 349.4A 351.7A 369.7A 2012 363.6A 366.1E 370.9E 375.4E 2013 380.2E 385.1E 390.1E 395.2E All values in USD unless otherwise noted. For Required Conflicts Disclosures, see Page 35.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INITIATION | COMMENTJULY 24, 2012

Federated Investors, Inc. (NYSE: FII)

Liquidity at a 'Buck', But for How Long?

UnderperformAbove Average RiskPrice: 19.69

Shares O/S (MM): 104.2Dividend: 0.96

Price Target: 19.00Implied All-In Return: 1%Market Cap (MM): 2,052Yield: 4.9%

Priced as of market close, July 24, 2012 ET.

Investment Conclusion

We view recent regulatory efforts to introduce new rules for money market fundsas the biggest challenge the company has faced. Any of the new money marketrules proposed by the Chairman of the SEC Ms. Schapiro — floating NAVs,capital buffers, or deterrents to redemptions — could lead to significant outflows,in our view. Sure, there have been encouraging developments with positive flowsinto Federated's equities business and continued strong flows into itsfixed-income funds. However, the shares are trading at an in-line multiple with itspeers despite facing a potential risk to its core money market franchise. Weprovide sensitivity tables to demonstrate the effect of outflows on our price targetwere the new rules adopted.

The following lead us to our investment conclusion:

• Federated is leveraged to money markets: With 75% of its total AuM inmoney market funds contributing to 40% of net revenues, we would expect anadoption of new rules as proposed by the SEC to affect earnings negatively.

• Tougher money market rules could be introduced despite strongopposition: While there has been widespread resistance to new rules proposedby the SEC's Chairman, investors should not dismiss this initiative yet. Ms.Schapiro will put her proposal to a vote in late July. If the proposal fails,tougher rules could still be introduced with the Financial Stability OversightCouncil (FSOC) gaining regulatory oversight over money market funds bydeclaring them to be 'systemically important'.

• Large outflows a possibility: If passed, any of the proposals put forth by theSEC will make money market funds especially desirable and could lead toindustry-wide outflows, we believe. The risk to Federated is not to be ignored.Federated's CEO has emphasized on various occasions that the money marketindustry could be changed significantly if the proposed rules were to pass.

• Limited upside potential, fairly valued: With the stock trading at 12x 2013EP/E, which is in line with its peers, we see limited upside potential.Historically, Federated has traded at a discount to its peers. We see potentialdownside risk, should money market reforms be approved. We apply a 15%discount to the peer multiple.

Priced as of prior trading day's market close, EST (unless otherwise noted).

125 WEEKS 12MAR10 - 23JUL12

16.00

18.00

20.00

22.00

24.00

26.00

28.00

M A M J J A S O N2010

D J F M A M J J A S O N2011

D J F M A M J J2012

HI-28JAN11 28.57HI/LO DIFF -49.74%

CLOSE 20.44

LO-23DEC11 14.36

5000

10000

15000

PEAK VOL. 20787.9VOLUME 838.0

60.00

70.00

80.00

90.00100.00 Rel. S&P 500 HI-12MAR10 100.00

HI/LO DIFF -47.95%

CLOSE 66.46

LO-23DEC11 52.05

RBC Capital Markets, LLC

Bulent Ozcan, CFA (Associate Analyst)(212) 863-4818; [email protected]

Eric N. Berg, CPA, CFA (Analyst)(212) 618-7593; [email protected]

Kenneth S. Lee (Associate)(212) 905-5995; [email protected]

FY Dec 2010A 2011A 2012E 2013E

Adj EPS - FD 1.73 1.45 1.70 1.80

P/AEPS 11.4x 13.6x 11.6x 10.9x

Net Flows (B) (35.8) 10.2 0.7 15.3

AUM (B) 358.2 369.7 375.4 395.2

Adj EPS - FD Q1 Q2 Q3 Q4

2010 0.38A 0.46A 0.42A 0.45A

2011 0.32A 0.41A 0.37A 0.36A

2012 0.41A 0.42E 0.43E 0.45E

2013 0.44E 0.45E 0.46E 0.46ENet Flows (B)

2010 (40.8)A 79.1A (89.3)A 15.2A

2011 (4.9)A (6.2)A 5.8A 15.4A

2012 (9.3)A 3.3E 3.3E 3.4E

2013 3.8E 3.8E 3.9E 3.9EAUM (B)

2010 349.9A 426.8A 341.3A 358.2A

2011 354.9A 349.4A 351.7A 369.7A

2012 363.6A 366.1E 370.9E 375.4E

2013 380.2E 385.1E 390.1E 395.2E

All values in USD unless otherwise noted.

For Required Conflicts Disclosures, see Page 35.

2

Investment Summary

We are initiating coverage of Federated Investors Inc. with an Underperform, Above Average Risk rating,

and a $19 price target. We view the following favorably:

Opposition is increasing against money market reforms with the industry, trade organizations, and the

US Chamber of Commerce combating new rules. Chairman of the SEC, Ms. Shapiro, does not seem to

have a majority at this point. One possibility is that the SEC commissioners will not approve money

market rules and introduce new regulations that are acceptable to all parties.

Federated remains determined to growing its business organically and through acquisitions. It

announced in late June that it has signed an agreement to roll up $903 million of fund assets of

Performance Funds Trust to Federated funds. About half of the assets are in money market funds.

Clearly, Federated remains focused on running its business.

Fund performance at Federated is improving. We like the fact that Federated‘s top-10 equity funds beat

60% of their peers, and top-10 fixed-income funds are in the top 41 percentile over a one-year

measurement period. The favorable effect on the three-year performance is noticeable.

However, the challenges Federated is facing are significant. While we would argue that none of the

problems the company is facing is self-created, Federated could be forced to operate in an environment in

which its largest offering—as measured by assets under management (AuM)—would lose its attractiveness.

This is how we arrive at our investment recommendation:

While resistance against Ms. Schapiro‘s rules is increasing, and we have included this as a positive for

Federated, we do not assign a high probability to this scenario. Instead, we think that tougher money

market rules could pass despite strong opposition. We believe that there are two potential paths as how

this could happen despite widespread resistance against new rules. One possibility could be that Luis

Aguilar, a Democratic SEC Commissioner, could change his stance and vote in favor of new rules. After

all, he is the only Democrat not supporting the proposals. This would give Ms. Schapiro the required

majority vote even with the remaining two Republican SEC Commissioners opposing the rules. The

SEC will put the proposal to vote in late July. Assuming that there is no majority vote, another

possibility would be that the Financial Stability Oversight Council (FSOC) could gain regulatory

oversight over money market funds by designating them as ‗systemically important‘. This would have

the Fed‘s support as the Fed Chairman publicly said that more needs to be done.

Federated, a top-five provider of money market funds, is highly leveraged to this asset class. With 75%

of its total AuM and 40% of net revenues tight to money market funds, we would expect an adoption of

new rules as proposed by the SEC to affect Federated‘s earnings negatively.

Large outflows are a possibility, if new money market rules pass. Any of the proposals put forth by the

SEC has the potential of leading to significant outflows. The proposals would make money market funds

a less desirable product. After all, investors use money market funds as a substitute to savings accounts

with the benefit of higher returns. Investors like the liquidity that these products provide and the implicit

guarantee that they will receive their capital back when requested. This is why some academics argue

that this product should not even exist because it violates the rule of risk-return trade-off. The risk to

Federated‘s business model is not to be ignored, in our opinion.

Limited potential upside: With the stock trading at 12x 2013 P/E, which is in line with its peers, we

believe that there is limited potential upside. Historically, Federated has traded at a 15% discount to

traditional asset managers. Given the regulatory overhang, we would have expected the stock to trade at

a larger discount to its peers. Clearly, investors are assigning a very low probability to money market

reforms passing. We disagree and recommend a cautious stance.

Federated Investors, Inc.July 24, 2012

3

Company Overview

Federated Investors Inc. is one of the larger domestic investment managers, managing $363.6 billion in

assets as of March 31, 2012. It has been in the investment management business since 1955. With 134

funds and a variety of separately managed account options, Federated provides comprehensive investment

management to approximately 4,800 institutions and intermediaries, including corporations, government

entities, insurance companies, foundations and endowments, banks, and broker-dealers. Federated is one of

the top-five money market fund providers in the United States. It also provides equity funds, fixed-income

funds, and manages liquidation portfolios, which are pools of distressed fixed-income securities that are

being run off over multiple years.

Exhibit 1: Federated Investors Snapshot

Federated Investors

Headquarters Pittsburgh, PA

Total AUM $363.6 bn

Major Brands Prudent Bear Fund, Kaufmann Funds, Federated

% retail funds AUM rated

4-5 stars by Morningstar28%

Signature Money market funds manager

Source: Company reports, RBC Capital Markets

Valuation

The asset managers are currently trading at 12.3x calendar-year 2013 estimated earnings. Over the past 10

years, Federated has been trading at a 15% discount to its peers. We believe that the discount is justified

given the regulatory overhang. We arrive at our price target using a price-to-earnings multiple of 10.5x,

which represents a 15% discount to the company‘s peers and our 2013 calendar-year earnings estimate of

$1.80 per share. Our price target is $19.

Exhibit 2: Federated’s Forward Looking P/E Relative to RBC Asset Managers Index

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Note: RBC Asset Managers Index includes BLK, EV, IVZ, LM, TROW, WDR, BEN, JNS, AB, ART, AMG, CNS, CLMS, GBL, PZN

Source: Bloomberg, RBC Capital Markets

Federated Investors, Inc.July 24, 2012

4

Ownership

Exhibit 3: Top-10 Holders

Position Mkt Val

Ultimate Holder ('000) (MM) % OS

Legg Mason, Inc. 13,264 281 12.7

Atlanta Life Financial Group 6,706 142 6.4

The Vanguard Group, Inc. 5,686 121 5.5

Virtus Investment Partners, Inc. 5,190 110 5.0

Bank of America Corp. 4,227 90 4.1

Invesco Ltd. 4,203 89 4.0

BlackRock, Inc. 4,152 88 4.0

State Street Corp. 3,168 67 3.0

Shapiro Capital Management Co., Inc. 2,627 56 2.5

Coop. Centr. Raiffeisen-Boerenleenbank BA 2,388 51 2.3

Source: FactSet

Exhibit 4: Ownership by Region

Position Mkt Val

Global Region ('000) (MM) % OS

North America 86,994 1,847 83.5

Europe 3,983 85 3.8

Asia 154 3 0.1

Pacific 47 1 0.0

Middle East 0 0 0.0

Source: FactSet

Federated Investors, Inc.July 24, 2012

5

Investment Thesis & Analysis

We are initiating coverage on Federated Investors with an Underperform and Above Average Risk rating.

We believe that the company is facing a significant threat to its business model and earnings, despite

progress in its equity and fixed-income businesses, and a continued push to grow organically and through

acquisitions. We believe that considerations such as the low interest rate environment, fee waivers, or

improving fund performance, i.e., fundamental value drivers, are inconsequential at this point. With the

backdrop of shares trading in line with its peers and the potential threat of new money market regulations

transforming the industry, we regard the push for new rules as the main driver of valuation. We see risks in

that respect. Thus, we made this subject the main topic of this initiation report because we believe that the

market has fully priced in positive developments, yet it seems to assign a low probability to new money

market rules being adopted.

We Believe that Tougher Rules are Coming Despite Strong Opposition

There are two potential paths as how this could happen despite widespread resistance against new regulations. One possibility could be that Luis Aguilar, a Democratic SEC Commissioner, votes in favor of new rules in late July. Another possibility would be that the FSOC could gain regulatory oversight over money market funds by designating them as

‘systemically important’.

We felt it necessary to provide some recent history to explain our view on the matter.

In our opinion, the events leading to the financial crisis have affected the money market industry

profoundly. Following the collapse of Lehman Brothers in the fall of 2008, one of the older money market

funds, the Reserve Primary Fund, with $62 billion of assets, faced $40 billion of redemption requests. The

fund had invested $785 million in commercial papers issued by Lehman Brothers, when the investment

bank filed for bankruptcy. This was only the second time in history that a money market fund had ‗broken

the buck‘, that is, net asset values fell below $1.00. Ironically, the Reserve Fund, the parent of the Reserve

Primary Fund, was the first money market fund to be sold. It was established in 1971 by Bruce Bent and

Henry Brown.

The other fund, which had ‗broken the buck‘, was the Community Bankers US Government Money Market

Fund in 1994. That fund had 25% of its assets in derivatives and was caught in the derivatives meltdown

that year.

Since money market funds are used as an alternative to savings accounts, the implications of ‗breaking the

buck‘ can be alarming. Clients who invest in the money market fund are likely to withdraw all their money

if a money market fund declares that it has suffered large losses on investments. The product design

incentivizes investors to redeem their share sooner rather than later. In a sense, an analogy would be with

musical chairs—no one wants to be left standing when the music stops playing.

Here is why: Since the first investors to withdraw their assets could get 100% of their investments, there

might not be any resources left to satisfy the funds obligation to the last investor. If the fund had to

liquidate its investments to meet redemption requests, then it might have to do so at depressed market

values and at a loss. Hence, at the first sign of a loss, investors try to get their capital out of the fund.

Before the financial crisis, there was a general perception that money market funds were superior to savings

accounts. Money market funds were preserving the value of an investment while providing overnight

liquidity. At the same time, money market funds were yielding more than savings account could. Investors

expected to receive 100 cents on the dollar when they redeemed them.

The events after Lehman Brothers‘ collapse were a wake up call to investors and regulators as the musical

chairs scenario played out. The President‘s Working Group on Financial Markets (PWG), tasked to prepare

a report on fundamental changes needed to address systemic risk and reduce the susceptibility to runs on

money market funds, found that investors withdrew $310 billion from prime money market funds during

the week of September 15, 2008—when the Reserve Primary Fund broke the buck. Within two weeks of

Lehman Brother‘s collapse, $400 billion was pulled out of money markets and invested into government

securities.

Federated Investors, Inc.July 24, 2012

6

The commercial-paper market came to an abrupt stop with corporations struggling to meet their short-term

cash needs. The Federal Reserve and the US Treasury had to backstop the entire money market industry in

order to calm investors. The government promised that it would guarantee all money market funds against

losses of up to $50 billion per fund if a money market fund ‗broke the buck‘. This guarantee was kept in

place for one year, and both retail and institutional money market funds could participate in this insurance

program for a fee, which they did. Given recent history, we believe regulators could argue that money

market funds pose systemic risk.

Why would regulators care if there were only two failures since money markets were introduced? Because data suggest that it could have been more.

Of course, money market fund managers will suggest that there have been only two failures in the 40-year

history of money market funds and that implying money market funds pose systemic risk is wrong. We are

not convinced because recent data suggest that while there were only two cases of failures, the rate could

have been much higher if it were not for the fund managers stepping in or the government providing

guarantees.

Moody‘s estimated that at least 36 of the 100 largest US prime money market funds had to receive funding

from their parents to survive after Lehman Brothers collapse. According to Moody‘s, at least 20 firms that

manage money market funds in Europe and the US had to contribute more than $12 billion into their funds

so that these would not ‗break the buck‘. This was done either as direct capital contribution or by buying

troubled securities from the funds. Moody‘s estimated that from 1980 to 2010, about 200 funds had to rely

on their parents‘ aid in order not to ‗break the buck‘.

A recent SEC study, completed in June 2012, concluded that money market mutual funds have been

rescued from financial trouble by their parent company more than 300 times over the past 40 years and

raising Moody‘s estimates by another 100 funds. This was accomplished by the funds‘ parent company

buying troubled debt out of the fund or by getting support from a bank, according to the SEC.

We believe that regulators will disagree with the money market fund industry on this topic and argue that a

run on money market funds could happen again as it is not such a rare incident.

But have not existing rules been strengthened already? Why is there the need for additional rules? Because regulators will argue that these amendments have not addressed the main issue, namely product design flaw.

Sure, in response to the events of 2008 and 2009, the SEC made amendments to Rules 2a-7 and 17a-9 in

February 2010. Rule 2a-7 of the SEC‘s Investment Company Act of 1940 regulates the quality, maturity,

and diversity of investments while Rule 17a-9 deals with purchases of assets from a money market fund by

an affiliate or parent. A series of rules was adopted to make money markets less susceptible to a run, such

as tightened credit quality standards, shortened maturities of funds investments, and enhanced liquidity.

Federated Investors, Inc.July 24, 2012

7

Exhibit 5: Rule 2a-7 Amendments

Focus Enhancements

Credit Quality Reduced exposure limit for second-tier securities. *

Funds not permitted to acquire second-tier securities with remaining maturities of over 45 days.

Diversification More restrictive single-issuer limits.

More restrictive collateral requirements for repurchase agreements qualifying for ‘look through’ treatment.

Liquidity Reduced exposure limit for illiquid securities. **

At least 10% of total assets in Daily Liquid Assets *** (not applicable to tax-exempt funds).

At least 30% of total assets Weekly Liquid Assets. ****

Maturity Reduced Weighted Average Maturity (WAM) limit.

Weighted Average Life (WAL) calculated without reference to any provision that would permit a fund to shorten the maturity of an adjustable-rate security by reference to its interest rate reset dates.

Portfolio Stress Testing

Performance of stress testing (simulated shocks such as interest rate changes, higher redemptions, and changes in credit quality of the fund) as required by new policies and procedures adopted by the fund board.

Transparency Monthly disclosure of all portfolio holdings on the fund’s website.

Monthly filings of portfolio and additional information (‘shadow’ NAV) with SEC.

Additional Board Power

Fund board permitted to suspend redemptions and postpone payment of redemption proceeds if a fund will ‘break the buck’ and if the fund will irrevocably liquidate.

* A second-tier security is defined as a security rated in the second-highest short-term rating category by rating agencies. ** An illiquid security is defined as one that cannot be sold or disposed of within seven days at approximately the value ascribed to it by the fund. *** Daily liquid assets include cash, US Treasury securities, and securities readily convertible to cash within one business day. **** Weekly liquid assets include daily liquid assets (convertible to cash within five business days rather than one) as well as US government agency discount notes with remaining maturities of 60 days or less.

Source: BlackRock

While the money market fund industry argues that these amendments made in 2010 are sufficient to reduce

the risk of a run on money markets, Ms. Schapiro disagrees. She points out that further steps need to be

taken in order to prevent occurrences such as the one witnessed in 2008. Ms. Schapiro believes that more is

needed as current amendments have not addressed the main issue—namely structural flaws in product

design.

These are Ms. Schapiro‘s three suggestions to fix the product design problem:

1) Floating Net Asset Values: This proposal would eliminate the ‗stable NAV‘ rule, which allows funds

to carry investments at book value. Money market funds argue that they hold the securities until

maturity, and mark-to-market would create unnecessary noise. The current rule allows money market

fund shares to trade at $1, unless investment losses result in a decline of more than $0.005 in NAV.

Under the new proposal, NAV would be calculated using actual market values of assets held by the

fund; thus, the NAV would fluctuate.

2) Creation of a capital buffer to absorb fund losses to sustain a stable NAV: A small amount from

portfolio income would be set aside as a cushion. Regulators would establish this ‗fee‘ (three to five

basis points), which could be suspended once a predetermined minimum capital requirement has been

met. Shareholders would have rights to this cushion, which essentially results in higher NAV for funds.

3) Introduction of deterrents to redemptions: When an investor redeems money market fund shares, a

specified portion of the proceeds would remain in the fund and absorb first losses over the next 30

days. The hold-back provision has been very controversial within the money market industry. As a

result, and Ms. Schapiro proposed a fee that would be imposed on customers who take out their money

during a liquidity crisis instead of holding back assets.

Federated Investors, Inc.July 24, 2012

8

With so much opposition, why do we think new rules could be introduced? Because Ms. Schapiro has influential supporters.

To be sure, recent news flow would suggest that Ms. Schapiro‘s proposals would not succeed because a

large number of industry experts, trade groups, and, increasingly, politicians is arguing that a ‗run on the

bank‘ scenario would be more likely with the new proposals. For instance, Bloomberg published an article

on June 21, 2012, saying that the SEC faced ―skeptical lawmakers from both parties,‖ as Ms. Schapiro

defended her campaign to overhaul the regulation of money market funds the day that she appeared before

the Senate Banking Committee.

We would not write-off the possibility of Ms. Schapiro‘s ideas becoming new rules because she seems to

have influential supporters. Treasury Secretary Timothy Geithner and Federal Reserve Chairman Ben

Bernanke share her view that a future run on money market funds is a real threat. This could damage the

economy if it were to happen.

Likewise, former Treasury Secretary Henry Paulson, who served under President Bush from 2006 to 2009,

offered Ms. Schapiro the use of excerpts from his 2010 book titled On the Brink, if it helps push through

her proposals. The book provides Mr. Paulson‘s perspective on the financial crisis. He recounts that billions

in money market fund redemption requests were made by investors from solid institutions, such as Bank of

New York Mellon, BlackRock and Northern Trust.

Several Federal Reserve officials continue to raise the issue of a possible run on money market funds in

public forums, saying that money market funds remain vulnerable during a crisis despite steps to bolster the

industry in 2010. The Federal Reserve Bank of Richmond President, Jeffrey Lacker, said at a Bloomberg

event that the system is broken and that the money market fund product design ―provides an artificial

incentive to run fast for the exits if a fund gets in trouble.‖ Federal Reserve Board Governor, Daniel

Tarullo, expressed his support for Ms. Schapiro in a speech given in May 2012. He said that ―the

combination of fixed NAV, the lack of loss absorption capacity, and the demonstrated propensity for

institutional investors to run together make clear that Chairman Schapiro is right to call for additional

measures.‖

The fear is real, in our view. Current ICI data suggest that the size of the industry is about $2.6 trillion as of

May 2012. Concerns that money market funds could damage the economy if there were a run on money

market funds in the future are defensible, in our view. Some academics even suggest that this product

should not exist at all.

Money market funds provide the same degree of liquidity as cash in a saving account, yet money market

funds yield returns above what one could earn by depositing cash at a bank. We could see why these funds

ignore the relationship between risk and return. After all, money market fund assets were artificially

boosted through Regulation Q when saving accounts in the late 1970s and early 1980s were forbidden from

offering an interest rate above 5.25%. Money market funds successfully competed against banks for

deposits, since they were not ruled by Regulation Q and could offer double-digit yields. Exhibit 6 makes it

clear why money market funds were able to accumulate assets and to compete against savings accounts: It

is hard to attract assets for banks if the inflation rate is significantly in excess of inflation.

Exhibit 6: US Inflation Rate

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Source: InflationData

Federated Investors, Inc.July 24, 2012

9

Money market funds started losing share to banks after 1982, when banks were allowed to offer higher

interest rates on deposits. However, the money market fund industry reacted to increased competition by

convincing the SEC to let the industry adopt a new accounting rule that allowed it to show NAV of the

funds as a fixed NAV per share. With this, money market funds could value their investments at amortized

cost and would not have to mark the assets to market. Thus, the NAV remains around $1. Our point:

Fluctuating net asset values are not a new invention but were used before current accounting rules

changed that. Could we go back to floating NAVs? It is not inconceivable, in our opinion.

With the introduction of these accounting rules leading to fixed NAVs, investors may have had the

impression that their investments are as safe as holding cash. This proved to be a fallacy as the events of

2008 showed. Money market funds take risk, as we have seen in the case of the Reserve Prime Fund. The

erroneous belief that one will get back every dollar of investment was driven by the accounting changes of

1983.

Some question why money market funds should be treated differently from other 1940 Act funds, which

have to show their NAV at market prices. Floating NAVs would allow investors to realize that they could

lose money. Thus, having floating NAVs could eliminate the ‗run on the bank‘ risk because investors

would receive what their shares are worth when they surrender their shares. After all, a ‗run on the bank‘

risk arises when investors try to redeem their shares at $1, with investors remaining in the fund absorbing

the losses. A fixed NAV would give investors an incentive to surrender their shares when a money market

fund reports losses on investments—at an inopportune time.

And the Federal Reserve Bank might have its own reasons why a reform is needed. After all, if Ms.

Schapiro‘s proposal turns into new regulation, then banks should see an influx of deposits. Currently, while

money market funds are included in the Fed‘s M2 classification of the money supply because of the

checking privileges granted by money market funds to their investors, the Fed has limited control over

money markets. We have heard many individuals argue that making money market funds less attractive

would result in funds being reverted to savings accounts, effectively giving the Federal Reserve greater

control over the money supply. This begs the question of why the SEC would propose new regulation that

would shrink the size of the money market fund industry, which it currently controls. The verdict on this

argument is outstanding.

There are good arguments on both sides of the discussion as to why and why not Ms. Schapiro‘s proposals

should be accepted. Nonetheless, we believe that the proposed regulation, if accepted, would greatly reduce

demand for money market funds. Regulators are concerned about a potential run on money market funds.

We believe that there is systemic risk and that it is more likely than not that new regulations will be

introduced. Even if these new regulations are a less stringent than what Ms. Schapiro is proposing, we

could see potential outflows.

Our call is that if we were to assume that there would be no new regulations, then we believe that there

would be limited upside potential with the stock trading at 12x 2013E P/E. Historically, Federated‘s shares

have traded at a discount to its peers or about 15% on average over the past 10 years.

Given the risk of the industry, one would expect this discount to be larger not smaller. Potential rules could

significantly change the industry, thereby making the product offering unattractive. This could lead to

sizeable outflows. We provide a sensitivity analysis in the Valuation section that shows the effect of

outflows on our price target.

Our price target of $19 assumes no changes to the money market rules. We did not deem this necessary to

assign probabilities to various scenarios to arrive at our price target because the shares are currently trading

above our price target. This is why we initiate coverage with an Underperform and Above Average Risk

rating.

Federated Investors, Inc.July 24, 2012

10

With Shares Fully Priced, We see Potential Downside Risk

Our call is that given current valuation, we see little upside potential in owning the shares. The shares are trading at 12x 2013E P/E, which is in line with its peers. We believe the risk of potential regulatory changes could significantly transform the industry, thereby turning money market funds unattractive. This could lead to sizeable outflows, in our view. A quick analysis reveals that if rules, as suggested by Mary Schapiro, were implemented and investors, therefore, redeemed assets, Federated’s valuation could decline significantly. We provide various scenarios.

Some investors may have brushed aside the subject of potential money market reforms. This could be one

of the factors explaining the performance put forth by Federated, with its shares rising by 46% year to date.

As a comparison, the broader S&P 400 Mid Cap Asset Management and Custody Banks Index moved

‗only‘ 15% during the same period. Below, we will discuss what might have fueled the rally in Federated‘s

shares.

We believe that a sense of optimism may have been created by the media suggesting that it is very unlikely

that any new rules could be passed. Indeed, recent news, such as Call to Leave Money Market Funds Alone

Grows Louder, published by the Wall Street Journal on May 31, 2012, may have fostered this optimism.

Certainly, Ms. Schapiro does not seem to have managed to gain the support of the majority of SEC

commissioners yet. Their support is needed to pass her proposals into law. In a news release published by

Reuters on May 11, 2012, the author wrote that Democratic SEC Commissioner Luis Aguilar and

Republican SEC Commissioners Troy Paredes and Dan Gallagher issued a joint statement saying a report

critical of the money market fund industry did not reflect the views and inputs of a majority of the SEC

commissioners.

This report published by the International Organization of Securities Commissions (IOSCO) on April 27,

2012, analyzed the risk that money market funds pose to financial stability. The IOSCO report sought

comments on a number of potential regulatory options—including introducing a floating NAV, which is

part of Ms. Schapiro‘s suggested solution, as well.

Obviously, all three commissioners do not seem to have changed their opposition to Ms. Schapiro‘s

proposals. Investors‘ optimism that new rules would not be introduced was probably strengthened by the

commissioner‘s issued statement. Interestingly, the statement by the three commissioners was given on the

day the Investment Company Institute convened for its annual conference in Washington.

Then in late in May 2012, Ms. Schapiro indicated that she was open to a compromise on money market

rules, thereby giving the impression that she was willing to shy away from her agenda and find a middle

ground that would be acceptable to all—or at least, it might have been perceived as such by investors.

And more recently, the US Chamber of Commerce published a white paper that warned of the dangers of

money market fund reform in the current environment, because any new rule would ―undermine the utility

and effectiveness of money market mutual funds.‖ The concern is that issuers of commercial paper, in

which money market funds invest, could face significantly higher interest costs. The Chamber‘s view is

that new money market rules could affect corporations‘ ability to raise short-term debt and finance their

liquidity needs. The result would be the opposite of what regulators are trying to achieve, namely an

increase in systemic risk. There could potentially be a run on money market funds, as investors start

withdrawing their cash in search for alternatives to ‗unattractive‘ money market funds. This is the opposite

of what the reform intends to achieve.

Ultimately, corporations, as well as governments, could face higher financing costs. As usual, we believe

that these higher costs would most likely be borne by the end consumer. New money market rules would,

therefore, lead to higher prices and higher taxes, thereby curbing demand for goods and services at a time

when the economy is struggling to gain any meaningful momentum.

There is more. Another research report published in April 2012 by Treasury Strategies probed the level of

acceptance of new money market rules by corporate treasurers. In our view, its findings are sobering.

Money market funds would potentially suffer significant outflows if any of Ms. Schapiro‘s three proposals

were adopted. Here are the results of their survey:

If fund NAV were to float, Treasury Strategies estimates that money market fund assets held by

corporate, government, and institutional investors would see a net decrease of 61%.

Federated Investors, Inc.July 24, 2012

11

If money market funds were required to institute a 30-day holdback of 3% of all redemptions, there

could be a net decrease of 67% in money market fund assets held by corporate, government, and

institutional investors.

If a loss reserve or a capital buffer was required, 36% of respondents said they would either decrease the

use of money market funds or discontinue their use altogether. However, the other 64%, who said that

they would continue using money market funds, changed their answers when asked if they would be

willing to accept lower yields resulting from implementing a loss reserve or a capital buffer.

o About half of these respondents (53%) said they would decrease or stop using money market funds

if the loss reserve or capital buffer rule resulted in a cost of two basis points, and

o 92% would stop or decrease usage of money market funds if the costs were five basis points.

Thus, we believe that recent news and reports have raised hopes among investors that the likelihood of

enacting new rules is very low and that business will continue as usual. We think this has led to a strong

rally in Federated‘s shares.

Exhibit 7 shows the performance of Federated‘s stock over the past six months and compares the

performance versus the S&P 500 Mid Cap Asset Manager and Custody Bank Index.

Exhibit 7: Indexed Six Months Performance

80%

90%

100%

110%

120%

130%

140%

150%

160%

01/02/2012

01/16/2012

01/30/2012

02/13/2012

02/27/2012

03/12/2012

03/26/2012

04/09/2012

04/23/2012

05/07/2012

05/21/2012

06/04/2012

06/18/2012

FI I S&P Mid Cap 400 / AM & Custody Banks

Source: FactSet

Bottom line: While the broader index was up 15%, Federated‘s shares increased 46% year to date. The

shares are trading in line with its peer multiples, and we just do not see why the shares could be trading at a

premium to its peers. It has historically traded at a discount to its peers; therefore, we see limited potential

upside.

There could actually be some potential downside risk because earnings could come under pressure if new

money market rules were to be adopted. We will explain later why money market rules could be tightened.

Ms. Schapiro is preparing to set a vote by late July; after which, all commissioners have to take a public

position on money market rules. While some investors might have hoped that Ms. Schapiro was backing

away from her initiative to reform the sector, her testimony at the Senate Banking Committee hearing in

June 2012 should be a clear signal that she continues to view money market funds as a source of systemic

risk.

Federated Investors, Inc.July 24, 2012

12

Financial Analysis

Fund Performance

In order to assess performance at Federated Investors, we decided to focus on the asset manager‘s top-10

funds since performance at the largest funds will affect earnings the most. Using Morningstar Direct, we

downloaded data for all funds offered and split the universe into two categories: equity funds and fixed-

income funds. We then eliminated ETFs, indexed funds, alternative funds, commodities funds, money

market, and funds with investments in properties only. Our focus was on the core equity and fixed-income

products. We decided to eliminate funds from our analysis that are part of an insurance product offering

because the asset management company has little control over the ultimate cost structure of the variable

annuity or the variable life product that is being offered.

We then weighted the ranking of the funds versus their peers using the individual rankings of the

underlying share classes offered within the top-10 funds by their NAV. Essentially, we weighted the

rankings by the size of the share class within the subgroup of 10 funds. Exhibit 8–10 plot the ranking for

the one-, three-, and five-year periods. While investors in general and consultants and advisors specifically

are focused on the three- and five-year performances, we deemed it necessary to look at the one-year

performance because it can serve as an indication as to where the three- and five-year performances will

head.

We would summarize performance at Federated as follows: While performance is improving, Federated is

struggling to beat its peers meaningfully. On a three-year basis, both equity and fixed-income funds are

trailing the majority of their peers. And despite decent performance generated by fixed-income funds,

equity funds are still trailing their peers on a five-year basis.

Exhibit 8: One-Year Performance for the Top-10 Funds

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11

Equities Fixed Income Top 50%

Source: Morningstar, RBC Capital Markets

Funds performance had clearly been improving at Federated going into the financial crisis. Both equity and

fixed-income funds included in our analysis were seeing strong performance. However, with the onset of

the financial crisis, performance has deteriorated, hitting lows in 2010. Both asset classes started beating

their peers just as recently as January 2012. While we like the trend, it will take continued improvement in

performance to have a meaningful effect on the three-year performance.

Good

Bad

Federated Investors, Inc.July 24, 2012

13

Exhibit 9: Three-Year Performance for the Top-10 Funds

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11

Equities Fixed Income Top 50%

Source: Morningstar, RBC Capital Markets

On a three-year basis, the company‘s top-10 fixed-income and equity funds are underperforming the

majority of their peers. We would expect a few more challenging periods before equity and fixed-income

funds start ranking higher as the improvement in recent performance will be offset by the performance in

2010.

Exhibit 10: Five-Year Performance for the Top-10 Funds

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

May-03 May-04 May-05 May-06 May-07 May-08 May-09 May-10 May-11

Equities Fixed Income Top 50%

Source: Morningstar, RBC Capital Markets

Good

Bad

Good

Bad

Federated Investors, Inc.July 24, 2012

14

As for the five-year performance, we see a clear bifurcation, with fixed-income funds doing much better

than equity funds. One could argue that, being a money manager, the company has a tendency to pick the

winners on the credit side of the business. However, this would not do the performance displayed prior to

2010 any justice.

Recent Results

Once again, questions around proposed money market reform remained the top priority in the quarter.

However, putting the important issue about the effect of the rules proposed by the SEC aside, one cannot

help but notice that Federated seems to be doing fundamentally well. The company reported earnings of

$0.52 (normalized), handily exceeding consensus estimates of $0.38. Sequential growth in average AuM of

3.3% combined with a reduction of the effect of fee waivers in the March quarter helped produce solid

results.

While up from the year-ago quarter, the fee waiver posed less of a drag on earnings in this quarter

compared to the December quarter. Higher rates on repurchase agreements backed by Treasuries and

mortgages helped lift average yields on investments and lower the effect of fee waivers. The company

disclosed that the average yield on investments in its money funds had moved from the single digits to the

high teens. Clearly, while average US dollar overnight repurchase rates had been around 0.08% in the

fourth quarter of 2011, rates climbed into the mid-teens in the first quarter of 2012 and have further

improved since the March quarter. This should further dampen the effect of fee waivers in the June quarter.

The company also reported organic growth of 1.3% annualized in the quarter, one of the better March

quarters in recent memory. Overall, net flows of $1.3 billion improved 14% year over year. In equities, the

company reported its third consecutive quarter of positive flows, following a long period of outflows.

Federated saw solid demand for its ‗Value & Income‘ products, such as the Strategic Value Dividend fund

(domestically and internationally). The Capital Income fund reported positive flows in the quarter after

having experienced outflows in the December quarter. Likewise, the company reported positive flows into

its ‗value‘ funds such as Clover Value and Clover Small Value. Performance of the Small Value fund has

been improving over the past months with the fund beating 75% of its peers on a trailing one-year basis.

And while the Prudent Bear and Kaufman funds are still reporting outflows, performance at Kaufman

seems to be improving, and management stated that the Prudent Bear fund has actually seen outflows

declining. Based on Morningstar, this fund has had outflows of $12.6 million in April 2012 versus outflows

of $186 million in the March quarter. We like the trend. However, while improving, performance is still an

issue at Federated.

Federated Investors, Inc.July 24, 2012

15

Exhibit 11: Performance of US Equity funds – Percentage of funds beating 50% of peers

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q04 3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11

1 Year 3 Year 5 Year

Source: Company reports, Lipper

Exhibit 11 shows the percentage of funds (asset weighted) in the top half of the respective Lipper

categories. While the one-year performance is improving, the company is still struggling to improve the

three- and five-year performances. The trend in performance for these vintages has been deteriorating, but

recent performance should help. Nonetheless, we do not expect flows to improve significantly from here

onward.

As for the fixed-income business, we saw a similar trend but not to the same extent. Despite its origins as

an equity fund manager, Federated seems to be doing a better job selecting fixed-income securities than

equity securities. While there were performance issues in the latter half of 2009, the company has clearly

put these issues behind it. The performance is not great, but it is good.

Good

Bad

Federated Investors, Inc.July 24, 2012

16

Exhibit 12: Performance of fixed-income funds – Percentage of funds beating 50% of peers

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q04 3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11

1 Year 3 Year 5 Year

Source: Company reports, Lipper

Given the recent performance in the one-year category, we expect the company to add to its fixed-income

AuM. Federated reported net flows of $775 million into its fixed-income funds. While the in flows are less

than what we saw in the March quarter of 2010 and 2009, the current quarter‘s net flows are still better on a

year-over-year comparison. The company reported that RFP (request for proposal) activity was up in the

first quarter, with institutional investors showing interest in the company‘s fixed-income products.

Federated recently added three new consultant relationship positions, which seem to have affected activity

in the institutional channel in a positive way.

Finally, flows into money market products, while positive, have declined over the previous two March

quarters. While there is seasonality due to the fact that tax collections have declined—states are a big user

of money market funds—there is also the possibility that clients could be looking for alternatives in

preparation for new regulations which might be passed. Nonetheless, looking at the quarter, one can see

that the earning power of the money market business has improved. Higher yields on repo rates helped

reduce the effect of fee waivers. Current data suggest that the June quarter could be even better than the

March quarter. While each money market fund has its own yield curve that will determine investment

income, the trend should be similar for all. We included the yield curve for US dollar overnight repurchase

rates in Exhibit 13 to show the improvement in the rates.

Good

Bad

Federated Investors, Inc.July 24, 2012

17

Exhibit 13: US Dollar Repo Rates

-0.05%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

May-09 Nov-09 May-10 Nov-10 May-11 Nov-11 May-12

Source: FactSet

Again, the trend over the past few months is positive because rates have increased. While it is difficult to

predict where rates will settle toward the end of the quarter, we remain optimistic that the average rate will

be in the high teens.

Overall, this was a good quarter. However, investors‘ focus will probably remain on what will happen on

the regulatory front, and we believe that politics will continue to dominate any discussion that investors are

having with management.

Exhibit 14: Recent Net Flows Have Been Positive ($ in billion)

($0.55)

($0.79)

($0.40) ($0.48)($0.38) ($0.42)

$0.56$0.74

$0.61

$1.34

$2.14

$1.11$0.94

$0.71

$0.13 $0.07

$1.50

$0.78

($1.0)

($0.5)

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12

Equity Fixed income

Note: Equity and Fixed Income include mutual funds and separate accounts. Source: Company reports, RBC Capital Markets

Federated Investors, Inc.July 24, 2012

18

Financial Projections

We expect Federated Investors to increase its total AuM at year-end 2011 from $369.7 billon to $375.4

billion in 2012 and $395.2 billon in 2013, driven mainly by growth in equity and fixed-income mutual fund

assets. We expect client interest in the fixed-income asset class to continue, with fixed-income AuM (which

includes assets within fixed-income mutual funds and separate accounts) increasing from $44.8 billion in

2011 to $48.7 billon in 2012 and $52.2 billion in 2013. We expect equity AuM (which includes mutual

funds and separate accounts AuM) to increase from $30.9 billion in 2011 to $35.8 billion in 2012 and $40.3

billion in 2013.

Exhibit 15: AuM Roll Forward

AuM Roll Forward

($ in billion) 2010A 2011A 2012E 2013E

Mutual funds and liquidation portfolios

Beginning assets $76.1 $82.2 $84.6 $92.3

Sales 27.9 30.2 n/a n/a

Redemptions (26.5) (29.1) n/a n/a

Net sales (redemptions) $1.4 $1.1 $2.8 $3.8

Net exchanges (0.0) 0.0 (0.1) -

Acquisition-related - 0.6 - -

Market gains and lossess/reinvestments 4.8 0.7 5.0 4.5

Ending assets $82.2 $84.6 $92.3 $100.6

Beginning money market fund assets $313.3 $276.0 $285.1 $283.0

Net sales (redemtions) and other (37.2) 9.1 (2.1) 11.5

Ending money market fund assets $276.0 $285.1 $283.0 $294.5

Total assets $358.2 $369.7 $375.4 $395.2

Source: Company data, RBC Capital Markets estimates

Given our expectations for increasing AuM in the next few years, we forecast net revenues to increase,

from $809.7 million in 2011 to $834.9 million in 2012 and $992.8 million in 2013, due mainly to

increasing investment advisory fees revenues. We believe net pre-tax margins (net of distribution expenses)

will be largely unchanged at the end of the next two-year period, going from 30.4% in 2011 to 34.9% in

2012 and 30.6% in 2013. We expect Federated Investors to generate $295.0 million in operating income in

2012 and $306.9 million in 2013, compared to operating income of $257.5 million in 2011.

Our diluted EPS estimate for 2012 and 2013 is $1.70 per share and $1.80 per share, respectively. This

compares to diluted EPS of $1.45 in 2011.

Federated Investors, Inc.July 24, 2012

19

Valuation

Exhibits 16–18 show how Federated Investors has traded: On an absolute P/E basis, on a basis of

Federated‘s P/E relative to that of the S&P 500, and on a basis that looks at Federated‘s P/E relative to that

of a broad valuation index we constructed for asset managers in general.

On an absolute P/E basis, Federated‘s shares trade at a premium to historical levels over the past five and a

half years.

Exhibit 16: Federated’s Forward Looking P/E multiples

0x

2x

4x

6x

8x

10x

12x

14x

16x

18x

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Source: Bloomberg, RBC Capital Markets

On a relative basis, Federated has been trading at a discount to the S&P 500. While the last two years have

seen some volatility in the company‘s share price, recent data show that the stock is now trading in line

with the S&P 500 index.

Exhibit 17: Federated’s Forward Looking P/E Relative to S&P 500 Index

0.4x

0.5x

0.6x

0.7x

0.8x

0.9x

1.0x

1.1x

1.2x

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Source: Bloomberg, RBC Capital Markets

More recently, the company has been trading at above historical forward looking P/E multiples relative to

traditional asset managers.

Federated Investors, Inc.July 24, 2012

20

Exhibit 18: Federated’s Forward Looking P/E Relative to RBC Asset Managers Index

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Note: RBC Asset Managers Index includes BLK, EV, IVZ, LM, TROW, WDR, BEN, JNS, AB, ART, AMG, CNS, CLMS, GBL, PZN

Source: Bloomberg, RBC Capital Markets

The asset managers are currently trading at 12.3x calendar-year 2013 estimated earnings. Over the past 10

years, Federated Investors has been trading at a 15% discount to its peers. We believe that the discount is

justified given the regulatory overhang. We arrive at our price target using a price-to-earnings multiple of

10.5x, which represents a 15% discount to the company‘s peers and our 2013 calendar-year earnings

estimate of $1.80 per share. Our price target is $19.

Market Sensitivity Analysis

Our EPS sensitivity analysis to equity market movements starts with our published estimates as the base

case. Our base case assumes uniform market appreciation, with equity markets appreciating 2%

sequentially and fixed-income markets appreciating 1% sequentially, starting in calendar fourth quarter of

2012 or the December quarter. For simplification, we assume that the alternative asset classes appreciate at

the same rate as the equity markets and thus assign an appreciation rate of 2% sequentially. We believe

these assumptions are in line with long-term historical average returns. For the bull case scenario, we

assume equity markets and alternative asset classes appreciate 4% sequentially, with fixed-income

appreciation unchanged from the base case scenario. For the bear case, we assume zero appreciation within

the equity markets and alternative asset classes. We apply these assumed appreciation rates uniformly

starting in the calendar December quarter (the fourth quarter of 2012) and throughout calendar 2013.

Exhibit 19: EPS Sensitivity to Equity Market Movements

Scenario 2013 P/E

2013

Peer P/E

(Discount)/

Premium 2013 EPS PT

Base Case 10.5x 12.3x -15% $1.80 $19

Bear Case 10.5x 12.3x -15% $1.79 $19

Bull Case 10.5x 12.3x -15% $1.82 $19

Source: RBC Capital Markets estimates

Federated Investors, Inc.July 24, 2012

21

Sensitivity to Money Market Fund Outflows

In order to provide some sense of the downside risk, we compiled Exhibit 20. It shows the sensitivity of our

price target based on various premiums and discounts to the 2013 price-to-earnings multiple of 12.3x and

various money market fund retention rates. For instance, if we assumed that the Federated lost half of its

money market assets as of the beginning of 2013, and a 12.3x 2013 P/E multiple, our price target would be

$11—all else being the same.

Exhibit 20: Price Target in Various Outflow Scenarios

Money Market Assets Retention Rate

90% 80% 70% 60% 50% 40% 30%

20% $23.99 $21.37 $18.74 $16.12 $13.49 $10.87 $8.24

15% $22.99 $20.48 $17.96 $15.45 $12.93 $10.42 $7.90

10% $21.99 $19.59 $17.18 $14.78 $12.37 $9.96 $7.56

5% $20.99 $18.70 $16.40 $14.10 $11.81 $9.51 $7.21

0% $20.00 $17.81 $15.62 $13.43 $11.24 $9.06 $6.87

-5% $19.00 $16.92 $14.84 $12.76 $10.68 $8.60 $6.53

-10% $18.00 $16.03 $14.06 $12.09 $10.12 $8.15 $6.18

-15% $17.00 $15.14 $13.28 $11.42 $9.56 $7.70 $5.84

-20% $16.00 $14.25 $12.50 $10.75 $9.00 $7.25 $5.50Pre

miu

m /

(D

iscount)

to P

eer

P/E

Mult

iple

Source: RBC Capital Markets estimates

We then compared how our price target would change if we assumed various probabilities to money market

reforms passing and money market assets declining as a result of this. Our base case is that Federated will

earn $1.80 per share in 2013. We weighted each scenario by various probabilities. These are the resulting

price targets:

Exhibit 21: Effect on Price Target Assuming 10% Probability that Reforms Pass

Money Market Assets Retention Rate

90% 80% 70% 60% 50% 40% 30%

20% $26.36 $26.09 $25.83 $25.57 $25.31 $25.04 $24.78

15% $25.26 $25.01 $24.76 $24.50 $24.25 $24.00 $23.75

10% $24.16 $23.92 $23.68 $23.44 $23.20 $22.96 $22.72

5% $23.06 $22.83 $22.60 $22.37 $22.14 $21.91 $21.68

0% $21.96 $21.75 $21.53 $21.31 $21.09 $20.87 $20.65

-5% $20.87 $20.66 $20.45 $20.24 $20.03 $19.83 $19.62

-10% $19.77 $19.57 $19.37 $19.18 $18.98 $18.78 $18.59

-15% $18.67 $18.48 $18.30 $18.11 $17.93 $17.74 $17.55

-20% $17.57 $17.40 $17.22 $17.05 $16.87 $16.70 $16.52Pre

miu

m /

(D

iscount)

to P

eer

P/E

Mult

iple

Source: RBC Capital Markets estimates

Federated Investors, Inc.July 24, 2012

22

Exhibit 22: Effect on Price Target Assuming 30% Probability that Reforms Pass

Money Market Assets Retention Rate

90% 80% 70% 60% 50% 40% 30%

20% $25.83 $25.04 $24.26 $23.47 $22.68 $21.89 $21.11

15% $24.76 $24.00 $23.25 $22.49 $21.74 $20.98 $20.23

10% $23.68 $22.96 $22.24 $21.51 $20.79 $20.07 $19.35

5% $22.60 $21.91 $21.22 $20.54 $19.85 $19.16 $18.47

0% $21.53 $20.87 $20.21 $19.56 $18.90 $18.24 $17.59

-5% $20.45 $19.83 $19.20 $18.58 $17.96 $17.33 $16.71

-10% $19.37 $18.78 $18.19 $17.60 $17.01 $16.42 $15.83

-15% $18.30 $17.74 $17.18 $16.62 $16.07 $15.51 $14.95

-20% $17.22 $16.70 $16.17 $15.65 $15.12 $14.60 $14.07Pre

miu

m /

(D

iscount)

to P

eer

P/E

Mult

iple

Source: RBC Capital Markets estimates

Exhibit 23: Effect on Price Target Assuming 50% Probability that Reforms Pass

Money Market Assets Retention Rate

90% 80% 70% 60% 50% 40% 30%

20% $25.31 $23.99 $22.68 $21.37 $20.06 $18.74 $17.43

15% $24.25 $22.99 $21.74 $20.48 $19.22 $17.96 $16.70

10% $23.20 $21.99 $20.79 $19.59 $18.38 $17.18 $15.98

5% $22.14 $20.99 $19.85 $18.70 $17.55 $16.40 $15.25

0% $21.09 $20.00 $18.90 $17.81 $16.71 $15.62 $14.53

-5% $20.03 $19.00 $17.96 $16.92 $15.88 $14.84 $13.80

-10% $18.98 $18.00 $17.01 $16.03 $15.04 $14.06 $13.07

-15% $17.93 $17.00 $16.07 $15.14 $14.21 $13.28 $12.35

-20% $16.87 $16.00 $15.12 $14.25 $13.37 $12.50 $11.62Pre

miu

m /

(D

iscount)

to P

eer

P/E

Mult

iple

Source: RBC Capital Markets estimates

Exhibit 24: Effect on Price Target Assuming 80% Probability that Reforms Pass

Money Market Assets Retention Rate

90% 80% 70% 60% 50% 40% 30%

20% $24.52 $22.42 $20.32 $18.22 $16.12 $14.02 $11.92

15% $23.50 $21.48 $19.47 $17.46 $15.45 $13.43 $11.42

10% $22.48 $20.55 $18.63 $16.70 $14.78 $12.85 $10.92

5% $21.45 $19.62 $17.78 $15.94 $14.10 $12.27 $10.43

0% $20.43 $18.68 $16.93 $15.18 $13.43 $11.68 $9.93

-5% $19.41 $17.75 $16.09 $14.42 $12.76 $11.10 $9.44

-10% $18.39 $16.81 $15.24 $13.66 $12.09 $10.51 $8.94

-15% $17.37 $15.88 $14.39 $12.90 $11.42 $9.93 $8.44

-20% $16.35 $14.95 $13.55 $12.15 $10.75 $9.35 $7.95Pre

miu

m /

(D

iscount)

to P

eer

P/E

Mult

iple

Source: RBC Capital Markets estimates

While we do not see upside potential for the stock, we believe that there is some risk to the downside.

Based on our assumptions and analysis, the shares could drop to $11 if Federation should lose half of its

assets. As a reference, the stock had hit a low of $14 in December 2011.

Federated Investors, Inc.July 24, 2012

23

Exhibit 25: Valuation Matrix

Market Current 52-week Div. Enterprise YTD YTD

Company Ticker Cap ($m) Price High Low Yield Value ($m) 2012E 2013E 2012E 2013E 2011A 2012E 2013E EV/AuM P/AuM Price Perf. Total Return

Traditional Asset Managers

BlackRock BLK $24,213 $173.31 $209.37 $137.00 3.46% $33,397.86 $13.08 $14.59 13.2x 11.9x 9.2x 9.1x 8.2x 0.009x 0.007x (2.8%) (1.1%)

T.Rowe Price TROW 15,681 61.47 $66.00 $44.68 2.21% $15,111.57 3.27 3.76 18.8x 16.3x 11.6x 10.4x 9.2x 0.027x 0.028x 7.9% 9.1%

INVESCO IVZ 9,655 21.54 $26.94 $14.52 3.20% $10,680.89 1.82 2.10 11.9x 10.2x 9.2x 9.0x 8.0x 0.016x 0.014x 7.2% 8.6%

Legg Mason LM 3,616 25.61 $32.58 $22.36 1.72% $3,499.53 1.67 2.27 15.4x 11.3x 7.3x 6.7x 6.1x 0.005x 0.006x 6.5% 7.2%

Franklin Resources BEN 23,746 110.35 $135.21 $87.71 0.98% $19,075.69 8.92 9.74 12.4x 11.3x 6.7x 6.7x 6.2x 0.026x 0.033x 14.9% 15.4%

Waddell & Reed WDR 2,457 28.46 $38.73 $22.85 3.51% $2,023.61 2.21 2.44 12.9x 11.6x 6.5x 6.2x 5.6x 0.022x 0.026x 14.9% 16.8%

Janus Capital Group Inc. JNS 1,361 7.22 $9.70 $5.36 3.32% $1,401.99 0.57 0.68 12.7x 10.6x 4.0x 5.0x 4.6x 0.009x 0.008x 14.4% 16.1%

Eaton Vance Corp. EV 3,054 26.43 $29.64 $20.07 2.88% $3,642.09 1.83 2.04 14.4x 13.0x 8.0x 8.7x 8.3x 0.018x 0.015x 11.8% 13.4%

Federated Investors, Inc. FII 2,158 20.71 $23.89 $14.36 4.64% $2,115.35 1.64 1.76 12.6x 11.8x 7.7x 7.1x 6.7x 0.006x 0.006x 36.7% 40.0%

AllianceBernstein AB 1,260 11.98 $18.76 $11.55 8.68% $1,220.60 1.04 1.17 11.5x 10.3x 2.5x 2.6x 2.5x 0.003x 0.003x (8.4%) (5.9%)

Artio Global Investors ART 187 3.14 $11.22 $2.83 2.55% $164.13 0.16 0.04 19.8x n/m 1.2x 10.0x n/m 0.006x 0.007x (35.7%) (34.4%)

Affiliated Manager Group AMG 5,528 107.63 $115.66 $70.27 0.00% $7,276.03 7.28 8.58 14.8x 12.5x 14.9x 13.3x 11.3x 0.020x 0.015x 12.2% 12.2%

Cohen & Steers CNS 1,377 31.91 $40.93 $23.79 2.26% $1,242.58 1.63 1.93 19.5x 16.5x 15.3x 10.9x 9.5x 0.028x 0.031x 10.4% 11.7%

Calamos CLMS 221 10.85 $14.66 $9.40 3.50% $113.22 0.92 0.89 11.9x 12.3x 0.7x 0.9x 0.8x 0.003x 0.006x (13.3%) (11.9%)

GAMCO GBL 1,214 45.57 $52.98 $35.81 0.35% $1,169.06 3.13 3.30 14.6x 13.8x 9.2x 8.4x 7.8x 0.032x 0.033x 4.8% 5.6%

Pzena Investment Mgmt PZN 266 4.11 $7.39 $3.18 2.92% $268.93 0.33 0.39 12.3x 10.5x 6.2x 6.8x 6.5x 0.018x 0.018x (5.1%) (1.3%)

Mean 2.89% 14.3x 12.3x 7.5x 7.6x 6.7x 0.016x 0.016x 4.8% 6.3%

Median 2.90% 13.1x 11.8x 7.5x 7.8x 6.7x 0.017x 0.015x 7.6% 8.9%

Min 0.00% 11.5x 10.2x 0.7x 0.9x 0.8x 0.003x 0.003x (35.7%) (34.4%)

Max 8.68% 19.8x 16.5x 15.3x 13.3x 11.3x 0.032x 0.033x 36.7% 40.0%

Alternative Asset Managers

Och-Ziff OZM $2,920 $7.05 $13.23 $6.56 5.67% $2,493.47 $0.48 $1.15 6.2x 5.4x 8.9x 3.6x 3.3x 0.083x 0.097x (16.2%) (14.8%)

Apollo Global Manager APO 1,696 13.41 $17.94 $8.85 7.46% $7,415.10 (0.86) 2.22 6.0x 4.6x -24.3x 7.8x 6.1x 0.086x 0.020x 8.1% 14.9%

Blackstone BX 6,727 13.15 $17.78 $10.51 3.04% $23,469.76 (0.57) 1.47 9.0x 6.4x 46.7x 38.3x 28.3x 0.123x 0.035x (6.1%) (4.0%)

KKR KKR 3,253 14.00 $16.10 $8.95 4.29% $43,312.58 0.73 2.06 6.8x 6.4x 73.7x 156.8x 102.3x 0.695x 0.052x 9.1% 12.7%

Fortress Investment Group FIG 1,950 3.79 $4.79 $2.67 5.28% $2,518.22 0.46 0.41 9.2x 6.9x 11.0x 10.4x 7.6x 0.054x 0.042x 12.1% 15.3%

Mean 5.15% 7.4x 5.9x 23.2x 43.4x 29.5x 0.208x 0.049x 1.4% 4.8%

Median 5.28% 6.8x 6.4x 11.0x 10.4x 7.6x 0.086x 0.042x 8.1% 12.7%

Min 3.04% 6.0x 4.6x -24.3x 3.6x 3.3x 0.054x 0.020x (16.2%) (14.8%)

Max 7.46% 9.2x 6.9x 73.7x 156.8x 102.3x 0.695x 0.097x 12.1% 15.3%

S&P 500 SP50 $12,316,922 $1,362.66 $1,422.38 $1,074.77 2.21% $96.42 $104.26 14.1x 13.1x 8.4% 8.4%

S&P 500 / Asset Mgmt & Custody Banks SPT30 134,632 120 138.27 94.63 2.53% 9.84 10.32 12.7x 12.1x 5.3% 5.3%

S&P Comp. 1500 / Asset Mgmt & Custody Banks SPT29 154,759 131 149.00 102.23 2.59% 10.56 11.04 12.8x 12.3x 6.3% 6.3%

S&P Mid Cap 400 / Asset Mgmt & Custody Banks SPT31 16,977 225 245.14 168.41 2.50% 16.40 16.85 14.0x 13.6x 14.7% 14.7%

S&P 500 / Financials SP621 1,737,330 $193.42 215.37 151.85 2.07% 14.57 17.63 13.5x 11.2x 10.4% 10.4%

Current P/EConsensus CY EPS EV/EBITDA Consensus

Asset Management Research

Source: FactSet (Priced as of market close July 20, 2012 ET)

Federated Investors, Inc.July 24, 2012

24

Company Description

Founded in 1955 and headquartered in Pittsburgh, Pennsylvania, Federated Investors Inc. (NYSE:FII) is a

global-investment manager. It provides investment-management products and related financial services

through its subsidiaries with US$363.6 billion of total managed assets as of March 31, 2012. Investment

offerings include domestic and international equities, fixed-income, and alternative strategies. However, the

company is best known for its money market products.

Out of the 134 Federated-sponsored funds the company provides, 48 are money market funds, 51 are fixed-

income funds, and 35 are equity funds. Federated markets these funds to banks, broker-dealers, registered

investment advisors, and other financial intermediaries. The company maintains relationships with some

4,700 client institutions. The ultimate clients include retail investors, corporations, and retirement plans. In

addition to advising and administrating Federated mutual funds and separate accounts, the company derives

its earnings from other mutual fund-related services such as distribution, shareholder servicing, and

retirement plan recordkeeping services.

All Federated-sponsored funds are domiciled in the US, except for the Federated International Funds Plc

and Federated Unit Trust, which are domiciled in Dublin, Ireland. Federated earned revenue worth $878.5

million from domestic operations and a mere $16.6 million from its foreign operations in the financial year

ended December 2011. The domestic market continues to be the main driver of Federated‘s revenues.

Exhibit 26: Revenue by Region

Revenues by Region (Dec 31, 2011)

Domestic

98%

Foreign

2%

Source: Company reports

Federated Investors, Inc.July 24, 2012

25

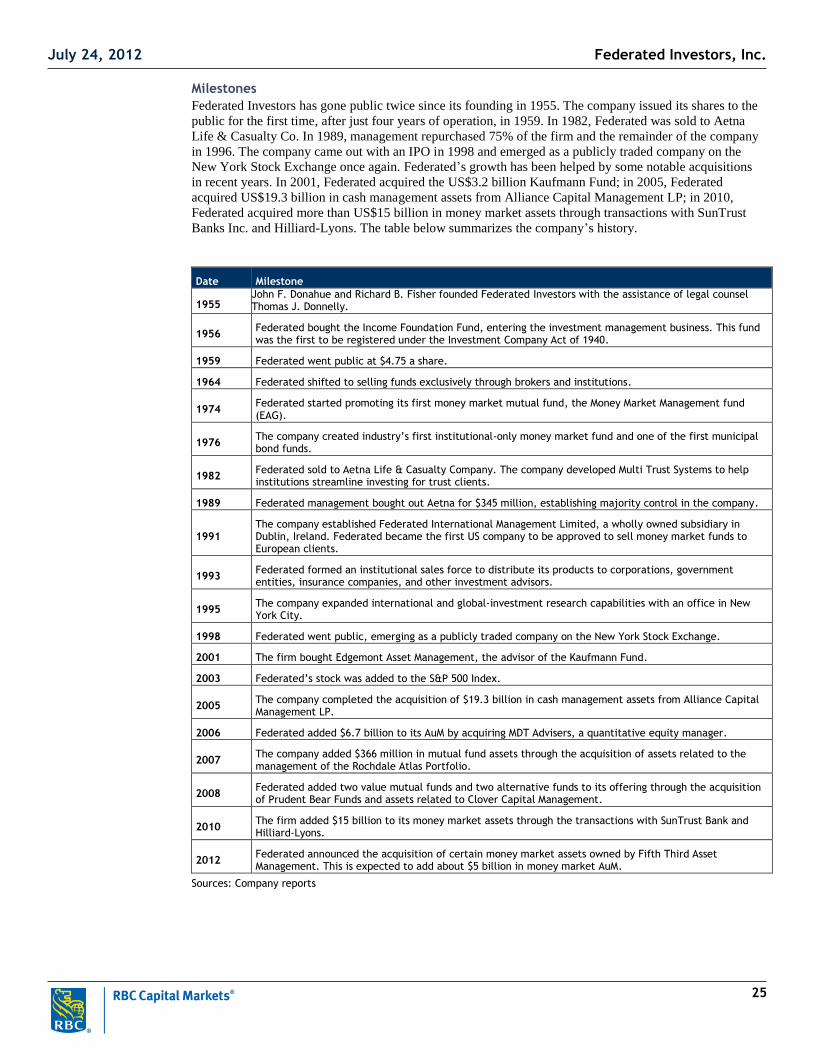

Milestones

Federated Investors has gone public twice since its founding in 1955. The company issued its shares to the

public for the first time, after just four years of operation, in 1959. In 1982, Federated was sold to Aetna

Life & Casualty Co. In 1989, management repurchased 75% of the firm and the remainder of the company

in 1996. The company came out with an IPO in 1998 and emerged as a publicly traded company on the

New York Stock Exchange once again. Federated‘s growth has been helped by some notable acquisitions

in recent years. In 2001, Federated acquired the US$3.2 billion Kaufmann Fund; in 2005, Federated

acquired US$19.3 billion in cash management assets from Alliance Capital Management LP; in 2010,

Federated acquired more than US$15 billion in money market assets through transactions with SunTrust

Banks Inc. and Hilliard-Lyons. The table below summarizes the company‘s history.

Date Milestone

1955 John F. Donahue and Richard B. Fisher founded Federated Investors with the assistance of legal counsel Thomas J. Donnelly.

1956 Federated bought the Income Foundation Fund, entering the investment management business. This fund was the first to be registered under the Investment Company Act of 1940.

1959 Federated went public at $4.75 a share.

1964 Federated shifted to selling funds exclusively through brokers and institutions.

1974 Federated started promoting its first money market mutual fund, the Money Market Management fund (EAG).

1976 The company created industry’s first institutional-only money market fund and one of the first municipal bond funds.

1982 Federated sold to Aetna Life & Casualty Company. The company developed Multi Trust Systems to help institutions streamline investing for trust clients.

1989 Federated management bought out Aetna for $345 million, establishing majority control in the company.

1991 The company established Federated International Management Limited, a wholly owned subsidiary in Dublin, Ireland. Federated became the first US company to be approved to sell money market funds to European clients.

1993 Federated formed an institutional sales force to distribute its products to corporations, government entities, insurance companies, and other investment advisors.

1995 The company expanded international and global-investment research capabilities with an office in New York City.

1998 Federated went public, emerging as a publicly traded company on the New York Stock Exchange.

2001 The firm bought Edgemont Asset Management, the advisor of the Kaufmann Fund.

2003 Federated’s stock was added to the S&P 500 Index.

2005 The company completed the acquisition of $19.3 billion in cash management assets from Alliance Capital Management LP.

2006 Federated added $6.7 billion to its AuM by acquiring MDT Advisers, a quantitative equity manager.

2007 The company added $366 million in mutual fund assets through the acquisition of assets related to the management of the Rochdale Atlas Portfolio.

2008 Federated added two value mutual funds and two alternative funds to its offering through the acquisition of Prudent Bear Funds and assets related to Clover Capital Management.

2010 The firm added $15 billion to its money market assets through the transactions with SunTrust Bank and Hilliard-Lyons.

2012 Federated announced the acquisition of certain money market assets owned by Fifth Third Asset Management. This is expected to add about $5 billion in money market AuM.

Sources: Company reports

Federated Investors, Inc.July 24, 2012

26

Strategy

Despite its origin as an equity fund, Federated has always been a strong fixed-income manager. While

others wrestled during the financial crisis with bond prices that fell sharply in value—the more extreme

examples included bonds of Lehman and Fannie Mae—Federated says it had hardly any major credit issues

during the crisis. It says there were no allegations leveled against it that Federated‘s fixed-income portfolio

managers were departing from the mandates in their prospectuses. To this day, while Federated has some

well known equity funds, including the Kaufmann Funds and the Prudent Bear fund, it is our sense that the

company is best known for its bond funds, including Federated Total Return Bond fund and Federated

Muni Ultra-short fund.

If Federated has been a leader in fixed-income investing, it is a reflection of the company‘s culture and

history. Centered in Pittsburgh, with hardly any fixed-income professionals working outside that city, the