FIDUCIARY LIABILITY—PUBLIC SECTOR Hard Choices, Real Protection October 10, 2009 Robert D. Klausner Klausner & Kaufman, P.A. Esquire Daniel Aronowitz Ullico Casualty President Christine A. Dart Chubb & Son Vice President Brian L. Smith The Segal Company Senior Vice President

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FIDUCIARY LIABILITY—PUBLIC SECTOR

Hard Choices, Real Protection

October 10, 2009

Robert D. KlausnerKlausner & Kaufman, P.A.Esquire

Daniel AronowitzUllico CasualtyPresident

Christine A. DartChubb & SonVice President

Brian L. SmithThe Segal CompanySenior Vice President

Agenda

Indemnity protection Common misconceptions v. reality

Fiduciary “Standard of Care”

Fiduciary liability exposures Operational Statutory Other

Claim Examples

Fiduciary liability insurance Is it permitted? What does it cover?

3

Common Misconceptions

Trustees are not bound to fiduciary rules Plans are exempt from ERISA

Trustees are exempt from liability Sovereign immunity Statutory indemnification Governmental policy

4

The Reality

Trustees are subject to significant fiduciary obligations

Existing protections may be Very limited Non-existent

5

Possible “Gaps” in Your Liability Protection

“Good faith” standard Who determines?

– The attorney general, the board of trustees, or the courts

Indemnity contingent upon an evaluation of the underlying conduct

Liable for bad faith, willful, wanton or grossly negligent conduct

“Ultra virus” standard Indemnity not available for actions taken outside “the scope of employment” Conduct must be consistent with “statutory duties” or “applicable standard of care”

– “Breaches of fiduciary duty” may not be covered

6

Potential “Gaps” continued

No uniformity

Statues vary by state for indemnification of defense costs, judgments, penalties, and other expenses

“Triggers” also vary

No indemnity

At least eleven appear to limit indemnification to trustees No indemnity is available to other officers, agents or employees

7

Immunity

State “agent” immunity may be qualified Acts involving skill or judgment (Discretionary Acts) may not be eligible for

immunity Non-qualifying acts may include:

– Acts “inconsistent” with statutory duty– “Ultra Virus” acts– “Willful and wanton” negligence

The “independence” of Public Sector plans may void sovereign immunity protection

8

Indemnity/ImmunityOther Observations

State statutory law may mirror ERISA’s section 412 [or 410?]

Any indemnity agreement for a breach of fiduciary duty is void

State statutory law may specifically grant immunity

BE AWARE OF THE CAVEAT “That do not involve malicious or wanton misconduct…”

9

Critical Questions

Do you know your state’s statutory and other applicable laws that define your responsibilities and liabilities?

Do you have written opinions from legal counsel identifying the scope of any indemnification or immunity protections?

Do you understand the caveat language that may exist within these protections? For example, is indemnity available for: “Gross negligence” or “willful or wanton failure?” Any alleged criminal activity?

Are you protected if the Plan or a regulatory agency (e.g., the state attorney general) sues you for an alleged wrongdoing?

Will the indemnity or immunity be provided if the alleged wrongdoing has become a political “hot potato” or “public scandal”?

10

Fiduciary Standard of Care

The fiduciary standard adopted in most states is the ERISA standard applicable to most private sector plans.

Federal Standard

=Expert

Prudent Man

State Standard

= or ~Expert

Prudent Man

11

Fiduciary Standard of Care continued

The fiduciary…may owe affirmative duties…beyond those found in an ordinary case of fraud. See Jersey City v. Hague, 18 N.J. 584, 589-90 (1995)

A fiduciary agent is presumed to be acting with “absolute devotion”… See Jaclyn, Inc. v. Edison Bros. Stores, Inc., 1970 N.J. Super. 334, 369 (1979)

The public official may be considered a “constructive trustee” of assets gained through misconduct…or impose an “equitable lien”… The public employer may demand not only what was lost, but also gains…

– See Dobbs, Law of Remedies

RICO provisions and remedies may also be available

12

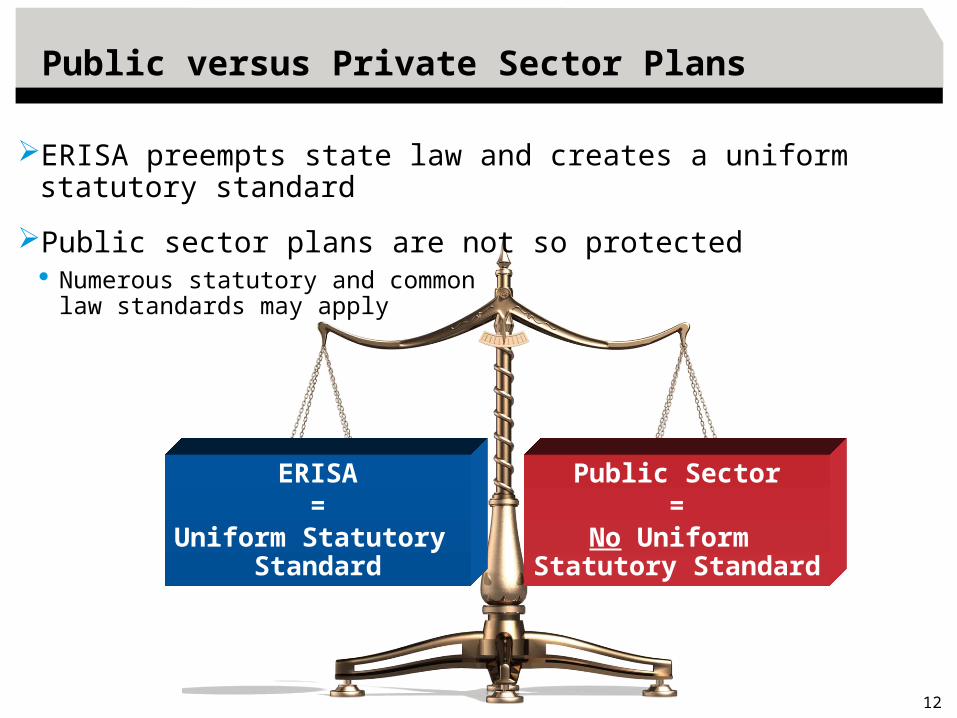

Public versus Private Sector Plans

ERISA preempts state law and creates a uniform statutory standard

Public sector plans are not so protected Numerous statutory and common

law standards may apply

ERISA=

Uniform Statutory Standard

Public Sector=

No Uniform Statutory Standard

13

Delegation of Fiduciary Duty

ERISA permits the avoidance of fiduciary liability by delegation Trustees’ exposure is

essentially limited to monitoring

Government plan fiduciaries do not transfer their liability by delegation of their duties to service providers Trustees’ exposure

includes investment decision, performance, and monitoring

ERISA Delegation Permitted

Liability Transferred

Public SectorDelegation Permitted

Liability Not Transferred

14

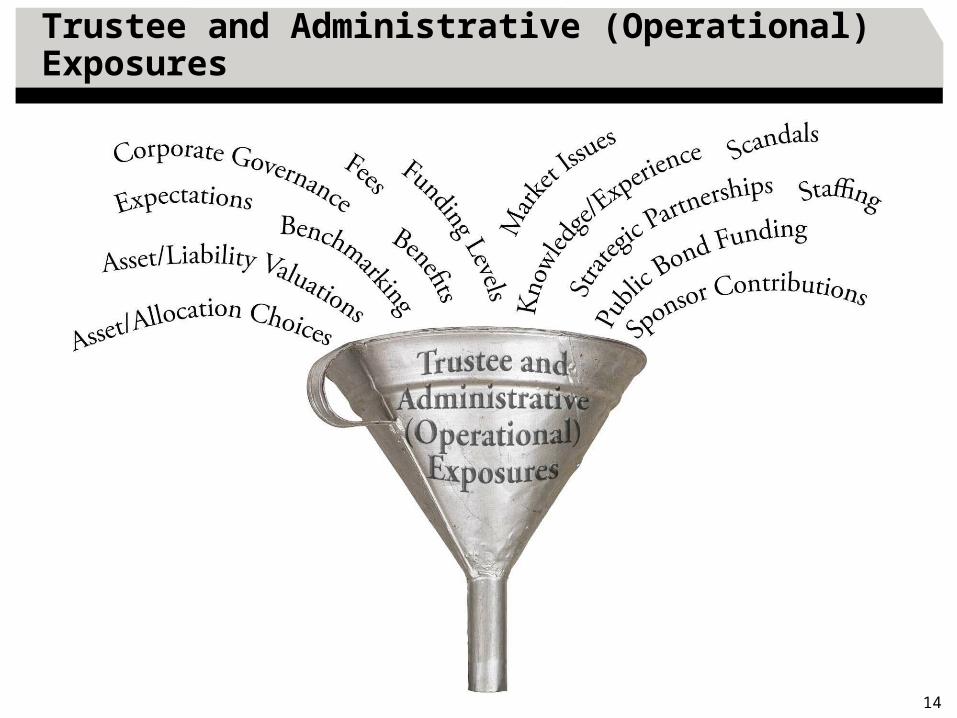

Trustee and Administrative (Operational) Exposures

15

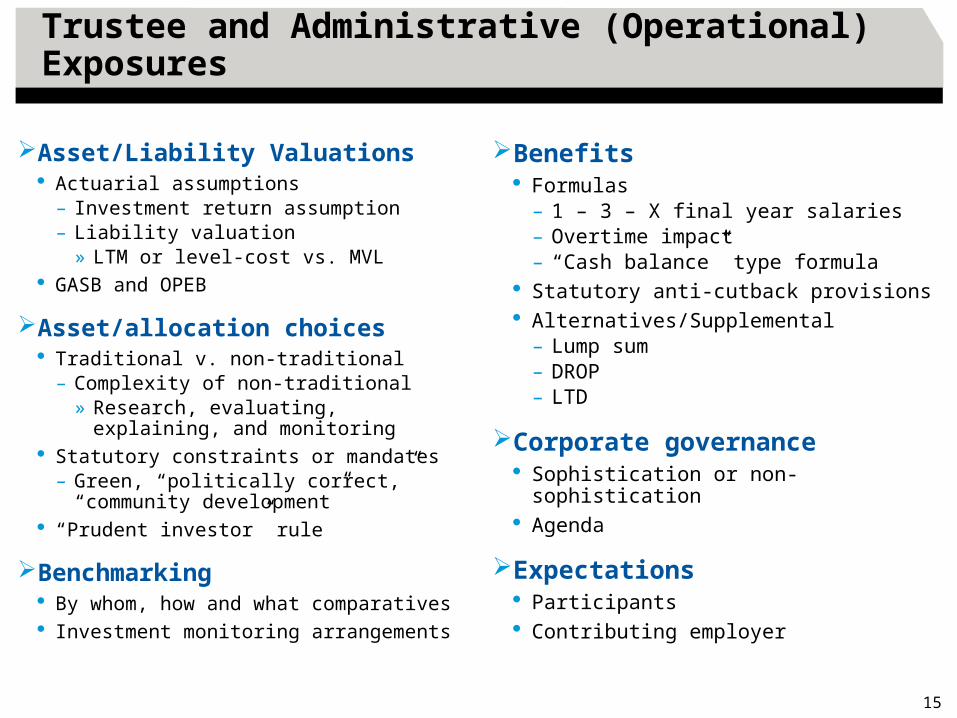

Trustee and Administrative (Operational) Exposures

Asset/Liability Valuations Actuarial assumptions

– Investment return assumption– Liability valuation

» LTM or level-cost vs. MVL GASB and OPEB

Asset/allocation choices Traditional v. non-traditional

– Complexity of non-traditional» Research, evaluating, explaining, and

monitoring Statutory constraints or mandates

– Green, “politically correct,” “community development”

“Prudent investor” rule

Benchmarking By whom, how and what comparatives Investment monitoring arrangements

Benefits Formulas

– 1 – 3 – X final year salaries– Overtime impact– “Cash balance” type formula

Statutory anti-cutback provisions Alternatives/Supplemental

– Lump sum– DROP– LTD

Corporate governance Sophistication or non-sophistication Agenda

Expectations Participants Contributing employer

16

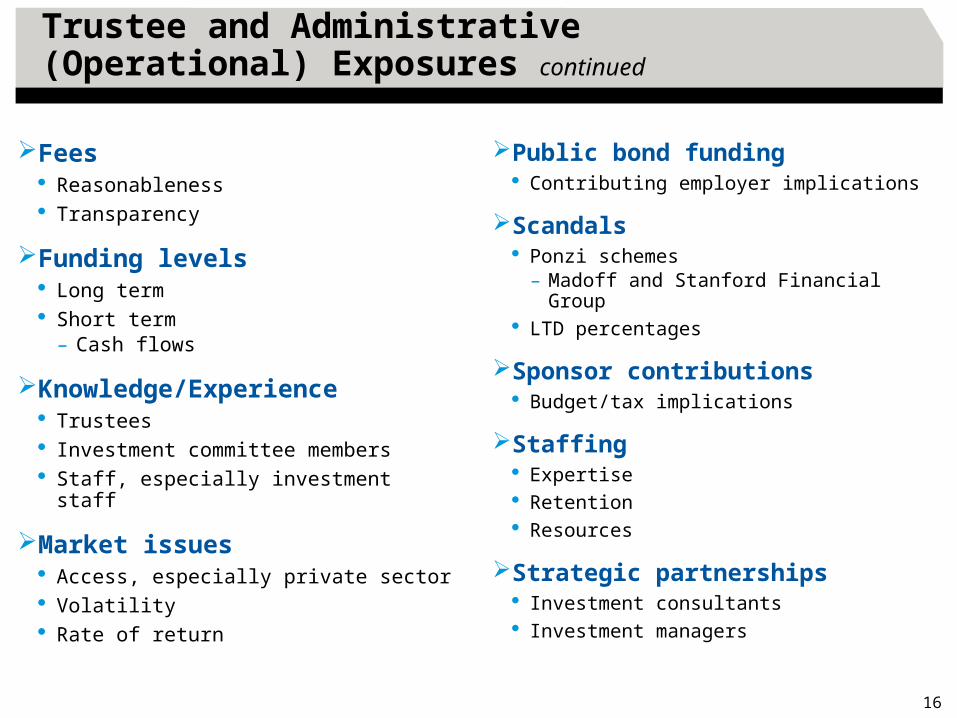

Trustee and Administrative (Operational) Exposures continued

Fees Reasonableness Transparency

Funding levels Long term Short term

– Cash flows

Knowledge/Experience Trustees Investment committee members Staff, especially investment staff

Market issues Access, especially private sector Volatility Rate of return

Public bond funding Contributing employer implications

Scandals Ponzi schemes

– Madoff and Stanford Financial Group LTD percentages

Sponsor contributions Budget/tax implications

Staffing Expertise Retention Resources

Strategic partnerships Investment consultants Investment managers

17

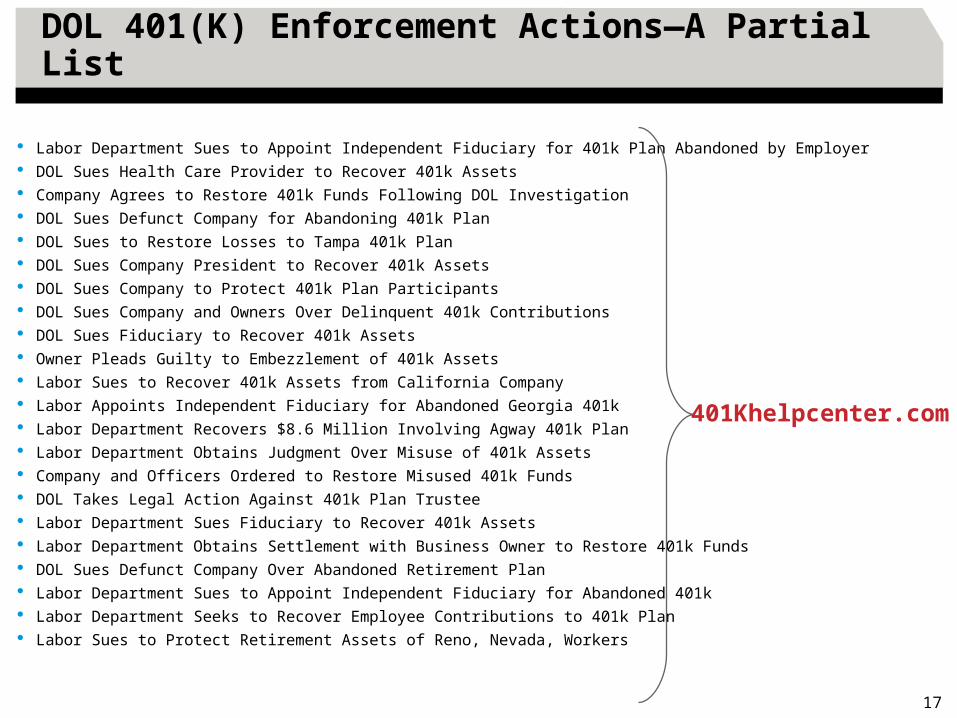

DOL 401(K) Enforcement Actions—A Partial List

Labor Department Sues to Appoint Independent Fiduciary for 401k Plan Abandoned by Employer DOL Sues Health Care Provider to Recover 401k Assets Company Agrees to Restore 401k Funds Following DOL Investigation DOL Sues Defunct Company for Abandoning 401k Plan DOL Sues to Restore Losses to Tampa 401k Plan DOL Sues Company President to Recover 401k Assets DOL Sues Company to Protect 401k Plan Participants DOL Sues Company and Owners Over Delinquent 401k Contributions DOL Sues Fiduciary to Recover 401k Assets Owner Pleads Guilty to Embezzlement of 401k Assets Labor Sues to Recover 401k Assets from California Company Labor Appoints Independent Fiduciary for Abandoned Georgia 401k Labor Department Recovers $8.6 Million Involving Agway 401k Plan Labor Department Obtains Judgment Over Misuse of 401k Assets Company and Officers Ordered to Restore Misused 401k Funds DOL Takes Legal Action Against 401k Plan Trustee Labor Department Sues Fiduciary to Recover 401k Assets Labor Department Obtains Settlement with Business Owner to Restore 401k Funds DOL Sues Defunct Company Over Abandoned Retirement Plan Labor Department Sues to Appoint Independent Fiduciary for Abandoned 401k Labor Department Seeks to Recover Employee Contributions to 401k Plan Labor Sues to Protect Retirement Assets of Reno, Nevada, Workers

401Khelpcenter.com

18

Asset allocation choices

Funding Issues NJ—Considers bill deferring ½ of municipalities annual pension funding requirements. PA—Employer contributions may increase from 4% of payroll to 28% in 2012. MI—Employer contributions for Detroit’s police and fire pension plans may increase to 50% of payroll in 2011.

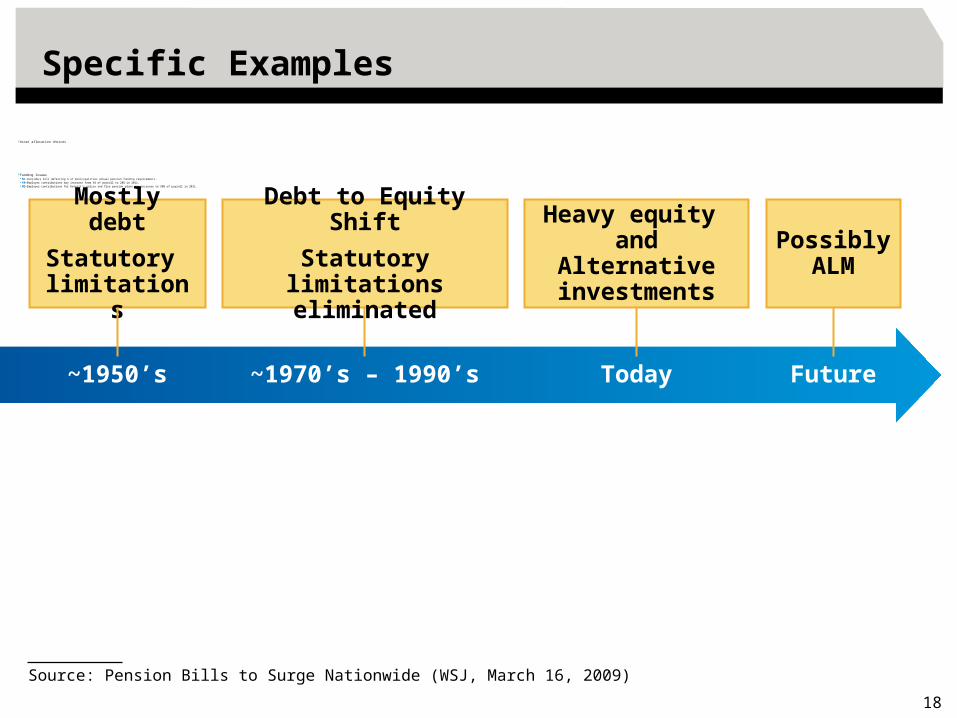

Source: Pension Bills to Surge Nationwide (WSJ, March 16, 2009)

Specific Examples

~1950’s ~1970’s – 1990’s Today

Mostly debt

Statutory limitations

Debt to Equity Shift

Statutory limitationseliminated

Heavy equity and Alternative

investments

PossiblyALM

Future

19

Specific Examples continued

Favorable benefit provisions For example, in at least one municipal plan

– The minimum retirement age = 50– 100% benefits after 25 years of service

Performance disclosure 13 states have secrecy laws

Real estate investments—risk adjusted performance In 2007, one large fund held $213 billion in commercial real estate equity,

leveraged 70% on average.– Rarely do internal rates of return account for leverage.– In a down market, leverage turns average performance into a disaster.

Source: The Next Meltdown, Forbes, July 21, 2008

20

Other Statutory Exposures

Federal

ERISA’s “exclusive benefit” rule Tax exempt status is subject to plan assets not being used for or diverted to non-

participants– Does this indirectly impose ERISA’s “fiduciary standards”?

» See H.R. Conf. Rep. No. 93-1280

ADEA, PPA’06, and WRERA Crediting interest in cash balance plans

– What is a market rate? Non-spousal rollovers Temporary waiver of required minimum distributions Self-funded plans eligible for special tax exclusion

IRS

See Segal’s April, 2009 Bulletin for details

21

Other Statutory Exposures continued

State and local laws

“Mirror” ERISA’s fiduciary standards

Statutory “prudent investor” rules Investment analysis “per investment” versus “overall portfolio”

Trust law

Common law

Duty of loyalty and “prudent investment” rule may create additional liability

22

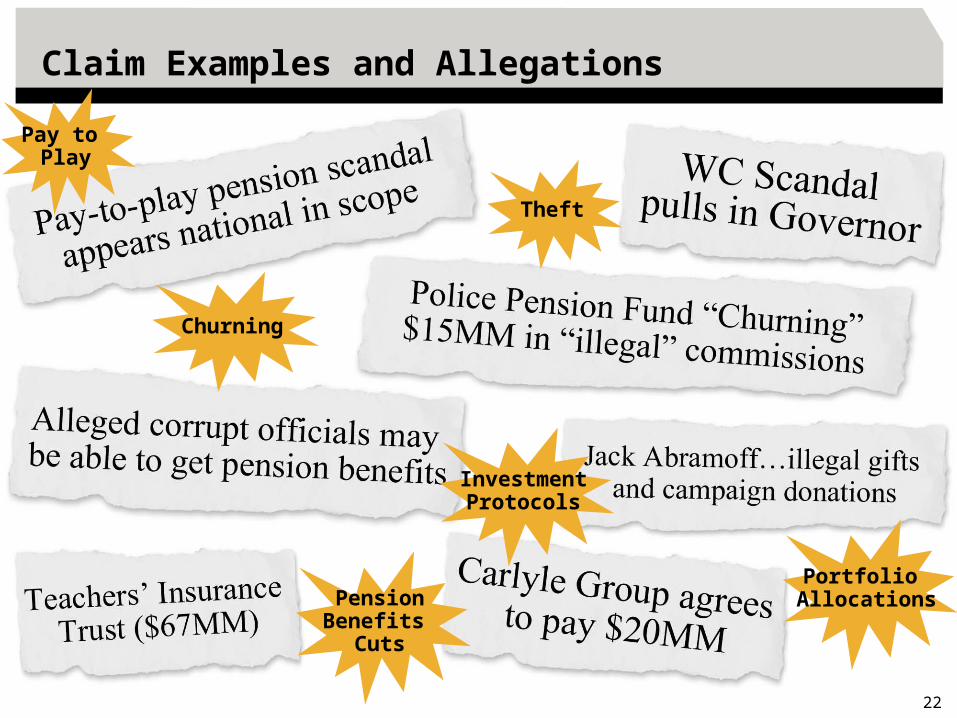

Claim Examples and Allegations

Churning

Theft

InvestmentProtocols

Portfolio Allocations

Pay to Play

PensionBenefits

Cuts

23

Allegations versus Final Impact

Fee increases for poor performance

Churning—unusually high number of transactions

Inappropriate investments— insufficient liquidity

Theft of funds

Pay to play

Reduced benefits

New benefit “tiers”

Increased taxes

Greater contributions

Insolvency

FINAL IMPACTALLEGATION

24

Public Scandals are Not New

History repeats itselfHistory repeats itself

Ancient Roman writing tablets suggest public officials were involved in expenses scandals 2,000 years ago.

25

Fiduciary Liability Insurance

At least one state mandates its purchase

Approximately twenty states expressly authorize its purchase

26

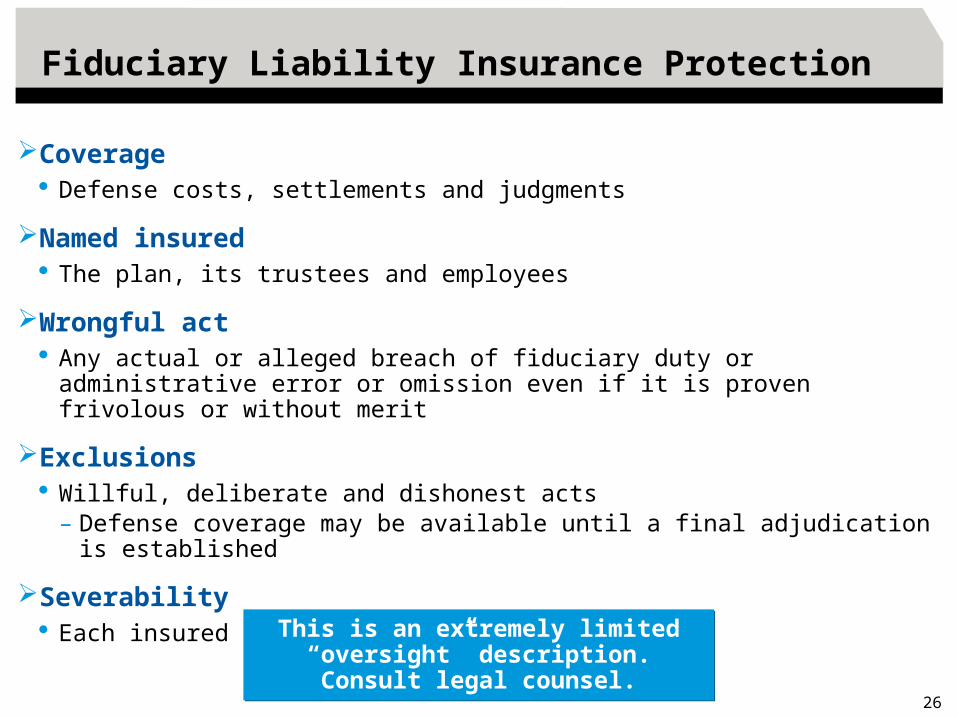

Fiduciary Liability Insurance Protection

Coverage Defense costs, settlements and judgments

Named insured The plan, its trustees and employees

Wrongful act Any actual or alleged breach of fiduciary duty or administrative error or omission

even if it is proven frivolous or without merit

Exclusions Willful, deliberate and dishonest acts

– Defense coverage may be available until a final adjudication is established

Severability Each insured individually protected

This is an extremely limited “oversight” description. Consult legal counsel.

This is an extremely limited “oversight” description. Consult legal counsel.

27

Fiduciary Liability Insurance Protection continued

It is a legal, insurance contract with a third party, professional insurance company

The insurance carrier will either provide or pay for independent legal counsel

A qualified insurance carrier knows public sector claims

The insurance carrier has an objective, financial rather than emotional investment

The insurance carrier has been paid to be on your side

28

Conclusion

Recent economic events: Spotlight trustees’ actions and responsibilities Are potentially redefining trustees’ standard

of care

Historical experience is not an indicator of future experience

Relying on indemnification and immunity may be a false security

Fiduciary liability insurance is an established, proven “safety net”

29

Contacts

One Park AvenueNew York, NY 10016-5895www.segalco.com

Brian L. SmithSenior Vice Presidentemail: [email protected]

Bus: (212) 251-5333Mobile: (347) 423-3452Bus Fax: (212) 726-5518

10059 Northwest 1st CourtPlantation, Florida33324

Robert D. [email protected]

Bus: 954-916-1202Bus Fax: 954-916-1232

82 Hopmeadow Street Simsbury, CT 06070-7683

Christine DartVice President [email protected]

1625 Eye Street, NWWashington, DC 20006

Daniel Aronowitz [email protected]

Bus: 202-682-4992Mobile: (415) 254-4031Bus Fax: 202-962-8853

Phone: 203-222-9625 Mobile: 203-451-3431

Related Documents