Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Overall Industry Size (INR Bn)*

2008 2009 2010 2011 2012 2013 2014

Growth in 2014

over 2013

2015P 2016P 2017P 2018P 22019PCAGR(2014-2019P)

Television 241.0 257.0 297.0 329.0 370.1 417.2 474.9 13.8% 543.2 631.2 739.6 854.6 975.5 15.5%

Print 172.0 175.2 192.9 208.8 224.1 243.1 263.4 8.3% 284.5 307.1 331.9 358.0 386.8 8.0%

Film 104.4 89.3 83.3 92.9 112.4 125.3 126.4 0.9% 136.3 155.6 170.7 186.3 204.0 10.0%

Radio 8.4 8.3 10.0 11.5 12.7 14.6 17.2 17.6% 19.6 22.3 27.0 32.7 39.5 18.1%

Music 7.4 7.8 8.6 9.0 10.6 9.6 9.8 2.3% 10.4 12.0 14.2 16.9 18.9 14.0 %

Out of Home 16.1 13.7 16.5 17.8 18.2 19.3 22.0 14.0% 24.4 27.1 29.6 32.2 35.1 9.8 %

Animation and VFX

17.5 20.1 23.7 31.0 35.3 39.7 44.9 13.1% 51.0 58.7 68.5 80.6 95.5 16.3%

Gaming 7.0 8.0 10.0 13.0 15.3 19.2 23.5 22.4% 27.5 31.8 35.4 40.0 45.8 14.3%

Digital Advertising

6.0 8.0 10.0 15.4 21.7 30.1 43.5 44.5% 62.5 84.0 115.3 138.2 162.5 30.2%

Total 580 587 652 728 821 918 1,026 11.7% 1159 1330 1532 1740 1964 13.9%

Source: KPMG analysis and industry discussions

Indian Media and Entertainment : Industry size & Projections

Overall Industry Size (INR Bn)*

2008 2009 2010 2011 2012 2013 2014

Growth in 2014

over 2013

2015P 2016P 2017P 2018P 2019PCAGR(2014-2019P)

Television 82.0 88.0 103.0 116.0 124.8 135.9 154.9 14.0% 174.6 198.4 226.2 260.1 299.1 14.1%

Print 108.0 110.4 126.0 139.4 150.0 162.6 176.4 8.5% 192.6 211.8 232.9 255.2 280.0 9.7%

Radio 8.4 8.3 10.0 11.5 12.7 14.6 17.02 17.6% 19.6 22.3 27.0 32.7 39.5 18.1%

Out of Home(OOH)

16.1 13.7 16.5 17.8 18.2 19.3 22.2 14.0% 24.4 27.1 29.6 32.2 35.1 9.8%

Digital Advertising 6.0 8.0 10.0 15.4 21.7 30.1 43.5 44.5% 62.5 84.0 115.3 138.2 162.5 30.2%

Total 221 228 266 300 327 363 414.0 10.9% 474 544 631 718 816 14.5%

82

154.9

299.1

108

176.4

280

8.4

17.2

39.5

16.1

22

35.1

6

43.5

162.5

0

100

200

300

400

500

600

700

800

900

2008 2014 2018P

TelevisionPrintRadioOOHDigital Advertising

Source : KPMG analysis and industry interviews

Source: KPMG analysis and industry interviews

Percentage share of Advertising spend by Media

Advertising revenues and projections

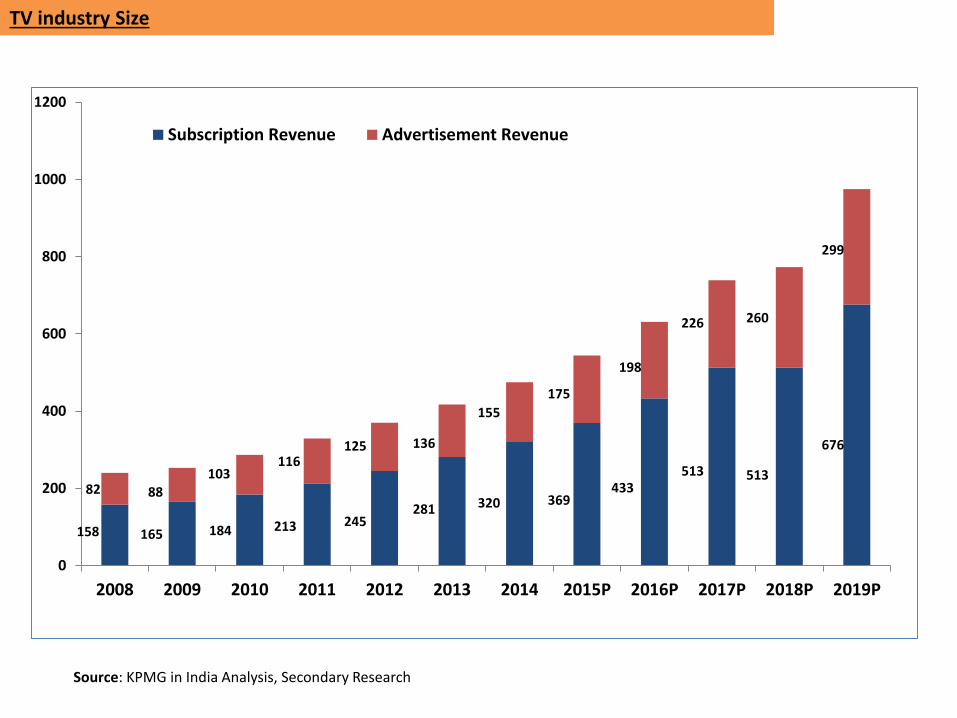

158 165 184 213 245281 320 369

433513 513

676

82 88103

116125 136

155

175

198

226 260

299

0

200

400

600

800

1000

1200

2008 2009 2010 2011 2012 2013 2014 2015P 2016P 2017P 2018P 2019P

Subscription Revenue Advertisement Revenue

Source: KPMG in India Analysis, Secondary Research

TV industry Size

Source: KPMG Analysis, Secondary Research

161

168

196

80%

82%

90%

74%

79%

84%

89%

94%

99%

0

50

100

150

200

250

2013 2014 2019p

TV House holds Paid C&S Penetration of Tv Household %2

INR

Bill

ion

Source: KPMG Analysis, Secondary Research

% P

erce

nta

ge

TV households and C&S penetration of TV households

65 74 69 68 7055

275

5 5

5

619 25

29

45

67

85 9094

28

31

3437

4048 61 72

7476

8

8

99

10

1111

1212

12

0

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014E 2015P 2016P 2017P 2018P 2019P

Analog Cable Digital cable DTH Other Digital

105119

C&S subscribers by platform

Source: KPMG Analysis, Secondary ResearchNote : (1)DTH figures are net of chum

(2) Figures are rounded to the nearest integer and may not add up exactly to column totals

125 136155

175198

226260

2995769

7590

114

145

174

201

0

100

200

300

400

500

600

2012 2013 2014E 2015p 2016p 2017p 2018p 2019p

Ad Revenues Sub Revenues

INR

Bill

ion

Source: KPMG in India analysis, Industry discussions conducted by KPMG in India

% P

erce

nta

ge

Broadcaster Industry size

31.2%

17.9%

13.6%

7.3%

3.2%

3.7%

3.7%

3.7%

2.4% 1.8%

1.3%

0.9%0.1%

9.4%

Viewership share by genre - 2014

Hindi GEC

Regional GEC

Hindi Movies

Kids

Music

Regional News

Regional Movies

Hindi News

Sports

Regional Music

Infotainment

English Entertainment

English News

Other

Viewership share by genre - 2014

27.5%

15.9%

6.7%7.3%3.0%

8.3%

2.8%

8.4%

4.3%

1.4%

2.0% 4.6%

5.0%

6.4%

Adex share by genre - 2014

Hindi GEC

Regional GEC

Hindi Movies

Kids

Music

Regional News

Regional Movies

Hindi News

Sports

Regional Music

Infotainment

English Entertainment

English News

Other

Adex share by genre - 2014

Rank Genre Channel Average GVT

1 Diya Aur Baati Hum Star Plus 10,651

2 Jodha Akbar Zee TV 8,678

3 Ye Hai Mohabbatein Star Plus 8,519

4 Saathiya Saath Nibhana Star Plus 8,390

5 Yeh Rishta Kya Kehlata Hai Star Plus 7,377

6 Mahabharat Star Plus Star Plus 7,124

7 Taarak Mehta Ka Ooltah Chashma SAB TV 6,916

8 Kumkum Bhagya Zee TV 6,348

9 Sapne Suhane Ladakpan Ke Zee TV 4,355

10 Sasural Simar Ka Colors 5,489

Source: TAM; HSM 4+ Week 1 to 52, 2013; Copyright reserved with TAM MEDIA RESEARCH PRIVATE LIMITED; Any use of TAM data (or derivative thereof) mentioned herein without express permission of TAM shall be treated as illegal

Top 10 Fiction Serials on Hindi GECs - 2014

Rank Genre Channel Average GVT

1 Comedy Nights With Kapil Colors 7,090

2 India's Got Talent 5 Colors 6,829

3 Fear Factor Khatron Ke Khiladi Colors 6,107

4 Dance India Dance Little Masters 3 Zee TV 4,978

5 Bigg Boss 8 Colors 4,837

6 Jhalak Dikhhla Jaa Colors 4,521

7 Dance India Dance 4 Zee TV 4,095

8 Kaun Banega Crorepati Sony 3,511

9 Nach Baliye 6 Star Plus 1,470

10 Made In India Star Plus 1,315

Top 10 Non-Fiction Serials on Hindi GECs - 2014

Source: TAM; HSM 4+ Week 1 to 52, 2013; Copyright reserved with TAM MEDIA RESEARCH PRIVATE LIMITED; Any use of TAM data (or derivative thereof) mentioned herein without express permission of TAM shall be treated as illegal

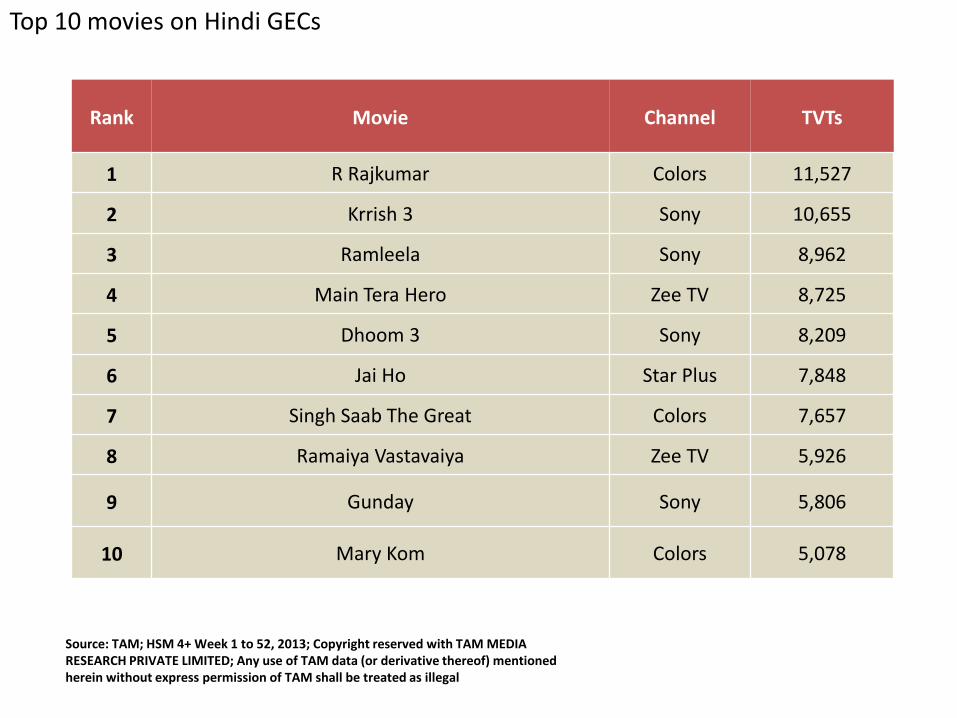

Rank Movie Channel TVTs

1 R Rajkumar Colors 11,527

2 Krrish 3 Sony 10,655

3 Ramleela Sony 8,962

4 Main Tera Hero Zee TV 8,725

5 Dhoom 3 Sony 8,209

6 Jai Ho Star Plus 7,848

7 Singh Saab The Great Colors 7,657

8 Ramaiya Vastavaiya Zee TV 5,926

9 Gunday Sony 5,806

10 Mary Kom Colors 5,078

Top 10 movies on Hindi GECs

Source: TAM; HSM 4+ Week 1 to 52, 2013; Copyright reserved with TAM MEDIA RESEARCH PRIVATE LIMITED; Any use of TAM data (or derivative thereof) mentioned herein without express permission of TAM shall be treated as illegal

24.0%

24.0%

14.1%

12.1%

11.7%

5.3%

1.2%

1.1% 0.6% 2.4%

Viewership share of regional channels

Tamil

Telegu

Marathi

Kannada

Bangali

Malyalam

Gujrathi

Oriya

Bhojpuri

Others

Viewership share of regional channels - 2014

28.3%

17.9%

16.0%

11.6%

11.1%

9.1%

2.0% 3.0% 1.0%

Viewership share of regional channels

Tamil

Telegu

Marathi

Kannada

Bangali

Malyalam

Gujrathi

Oriya

Bhojpuri

Adex share of regional channels - 2014

Source: KPMG India analysis and industry discussions

Print Industry Overview

Overall Industry Size (INR Bn)*

2010 2011 2012 2013 2014Growthin 2014 2015P 2016P 2017P 2018P 2019P

CAGR (2012,1

7)

Total Advertising 126 139 150 163 176 8.50% 193 212 233 255 275 9.70%

Total Circulation 67 69 75 81 87 7.90% 92 95 99 103 107 4.20%

Total Industry Size 193 209 224 243 263 8.30% 285 307 332 358 382 8.00%

Total News paper Revenue

181 196 211 230 249 8.50% 270 293 318 344 372 8.40%

Total Magazine Revenue

12 13 13 14 14 4.40% 14 14 14 14 14 0.30%

Total Industry size 193 209 224 243 263 8.30% 287 313 343 374 374 8.00%

Source: KPMG India analysis and industry discussions

Print Industry : Long term growth looks promising

INR billion 2010 2011 2012 2013 2014Growthin 2014

2015P 2016P 2017P 2018P 2019P CAGR

(2014,17)

English market 79 83 86 91 96 5.2% 101 105 109 113 118 4.2%

Advertising 53 57 59 62 65 4.8% 32 33 33 34 35 4.9%

Circulation 26 26 27 29 31 6.0% 69 72 76 80 83 2.4%

Hindi Market 58 62 68 75 83 10.5% 92 100 109 120 131 9.4%

Advertising 37 41 45 50 54 9.8% 60 67 75 83 92 11.2%

Circulation 21 22 24 26 29 12.0% 31 33 35 36 38 5.6%

Vernacular Market 56 63 69 76 84 9.8% 92 102 113 125 138 10.5%

Advertising 36 42 46 51 57 11.8% 64 72 82 92 104 13.0%

Circulation 20 21 24 26 27 6.0% 29 30 31 33 34 4.6%

Total Print Market 193 209 224 243 263 8.3% 284 307 332 358 387 8.0%

37%31%

32%35%

31% 34%

0%

20%

40%

60%

80%

100%

120%

2013 2018P

English Hindi Vernacular

Print advertising advertisement Volume Language (% share)

Source : KPMG Analysis, industry Discussions

63 65 67 67 67

37 35 33 33 33

0

20

40

60

80

100

120

2009 2010 2011 2012 2013

Advertising Circulation

Advertising and Circulation revenue share

Source : TAM Media Research PVT LTD &KPMG Analysis, industry Discussions

Correlation between GDP and print advertising revenue growth

Source : KPMG Analysis, industry Discussions

Note: While advertising revenue has been estimated for a calendar year, GDP growth has been calculated for the financial year

The Indian print industry continuedits journey at a steady rate in 2014with most players strengtheningtheir presence in the existingmarkets, and consolidating theirexisting operations. The structure ofthe Indian print industry continuesto be highly fragmented with bothnational and regional players presentin the market.The industry’s growth is directlyrelated to the macroeconomicconditions prevailing in the country.Post general elections in 2014, theformation of a stable government atthe centre generated optimism inthe country. This boosted investors’confidence in the otherwise shakyeconomy. During the April – June2014 quarter, the FICCI BusinessConfidence Index (BCI) rose to a 15-quarter high of 72.7 points from 49points a year earlier. Themacroeconomic stability seems tohave facilitated the growth in theprint industry

Number of registered newspapers and periodical (in 000’)

Source: The Registrar of Newspaper for India, Annual report 2013-14

Percentage share of advertisement and circulation revenue in the Indian print industry

Source: KPMG in India analysis, Industry discussions conducted by KPMG in India

Revenue contribution from newspapers and magazines

New publications registered in FY14

Source: The Registrar of Newspaper for India, Annual report 2013-14

Big spenders on print

Source: Pitch Madison reports

Film industry performance

Revenue (INR Billion)*

2010 2011 2012 2013 2014 2015P 2016P 2017P 2018P 2019P2013-14

(YoY growth)

CAGR (2014,19

Domestic Theatrical 62 68.8 85.1 93.4 93.5 99.9 113.6 123.5 133.5 145.1 0.10% 9.20%

Overseas Theatrical 6.6 6.9 7.6 8.3 8.6 9.6 10.9 11.9 12.9 13.9 3.50% 10.10%

Home Video 2.3 2 1.7 1.4 1.2 1 0.9 0.8 0.7 0.7-

15.00%-

12.20%

Cable & Satellite rights 8.3 10.5 12.6 15.1 14.7 15.5 17.6 19.2 20.8 22.5 -2.70% 8.80%

Ancillary Revenue streams

4.1 4.7 5.4 7 8.4 10.3 12.5 15.4 18.3 21.8 19.70% 21.00%

Total 83.3 92.9 112.4 125.3 126.4 136.3 155.6 170.7 186.3 204 0.90% 10.00%

Box office performance of select regional films

Movie Language Budget Gross Box Office

Lingaa Tamil 800 1480

Kaththi Tamil 700 1240

Aranmanai Tamil 120 220

Vella Illa Pattathar Tamil 80 530

Bangalore Days Malayalam 90 500

Lai Bhaari Marathi 80 350

Chaar Sahibzaade Punjabi 200 700

Veeram Tamil 400 1300

Domestic Box Office revenue – India, China (in USD billion)

1.11

1.1

1.4

1.6

1.8

0.9

1.5

2

2.7

3.5

4.7

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2009 2010 2011 2012 2013 2014

India China

Source: Ent Group report, China film industry report 2013-2014, KPMG in India analysis

210

272

337

402469

528

20

22

25

27

30

32

0

100

200

300

400

500

600

2014E 2015P 2016P 2017P 2018P

Wireless connections Wireline Connections

Million Connections

India internet connections, 2014(E) – 2019 (P)

Note: TRAI restated the numbers for broadband and wired internet subscribers last year. In line with this we have restated our projections

Source: KPMG in India analysis

India internet vs. TV penetration, 2014 (E) – 2019 (P)

825857

886913

938960

281

348

420

494

570

640

0

200

400

600

800

1000

1200

2014E 2015p 2016p 2017p 2018p 2019p

Tv Viewers Internet users

Source: KPMG in India analysis

Fig in Million

Mobile internet users in India, 2014(E) – 2019(P )

173

232

286

342

399

475

0

50

100

150

200

250

300

350

400

450

500

2014E 2015p 2016p 2017p 2018p 2019p

Million users

Million users

Source: KPMG in India analysis

Fig in Million

Internet enabled smartphones in India, 2014(E) –2019(P)

116

188

249

299

369

435

0

50

100

150

200

250

300

350

400

450

500

2014E 2015p 2016p 2017p 2018p 2019p

Million

Million users

Source: KPMG in India analysis, IDC and eMarketer estimates, 2014

Projected smartphone sales in India, 2014 (E) - 2019(P) (in millions)

79

114

142

178

222

256

0

50

100

150

200

250

300

2014E 2015p 2016p 2017p 2018p 2019p

Million

Million users

Source: KPMG in India analysis

Fig in Million

Market Share: Smartphone vs Feature Phone

28% 29% 32% 35%

72% 71% 68% 65%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q 1 2014 Q 2 2014 Q 3 2014 Q 4 2014

Smartphone Feature phone

Source: IDC Asia Pacific Quarterly Mobile Phone Tracker Q4 2014

Digital advertising market in India, 2014 (E) – 2019(P) (in INR billions)

38

54.80

72.40

98.60

116.10

135.40

5

7.70

11.60

16.80

22.10

27.10

0

20

40

60

80

100

120

140

160

180

2014 E 2015 P 2016 P 2017 P 2018 P 2019 P

Desktop Advertising Mobile Advertising

Source: IDC Asia Pacific Quarterly Mobile Phone Tracker Q4 2014

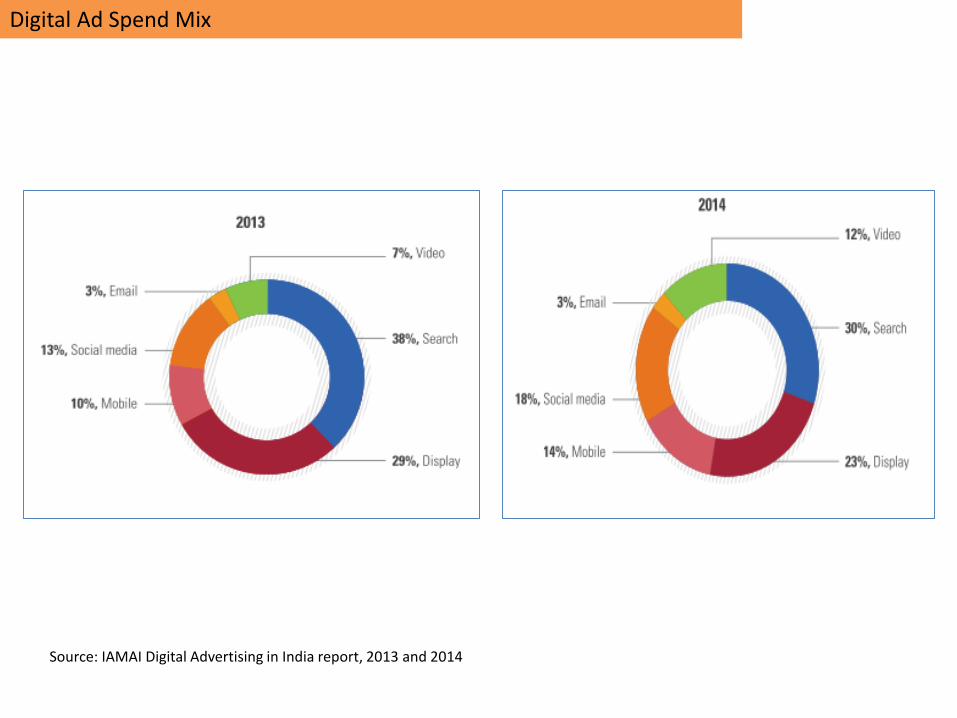

Digital Ad Spend Mix

Source: IAMAI Digital Advertising in India report, 2013 and 2014

113

316

362

271 271294

158181

294

495

413

385

303 303

275

193

220

165

0

100

200

300

400

500

600

E-Commerce Telecom FMCG &ConsumerDurables

BFSI Travel Auto Education IT/ITeS Others

FY. 2013 FY. 2014

Industry wise Digital Ad spends (INR Cr)

Source: IAMAI Digital Advertising in India report, 2014

Percentage of adults using social media platforms globally

Global gender-wise distribution of adults using social media platforms

Source: Pew Research Center’s combined omnibus survey, September 2014

Source: Pew Research Center’s combined omnibus survey, September 2014

22.8

28.8

35.1

42.5

50.6

59.4

0

10

20

30

40

50

60

70

2014E 2015P 2016P 2017P 2018P

INR in billions

Indian online classifieds market, 2014 (E) to 2019 (P)

Note: TRAI restated the numbers for broadband and wired internet subscribers last year. In line with this we have restated our projections

Source: KPMG in India analysis

Gaming market in India, 2014(E) – 2019(P)

9.20 9.70 10.20 10.70 11.20 11.80

10.7013.40

16.1018.40

21.80

26.20

3.60

4.40

5.50

6.30

7.00

7.80

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

2014 E 2015 P 2016 P 2017 P 2018 P 2019 P

Console Mobile PC & Digital TV

INR billions

Source: IDC Asia Pacific Quarterly Mobile Phone Tracker Q4 2014

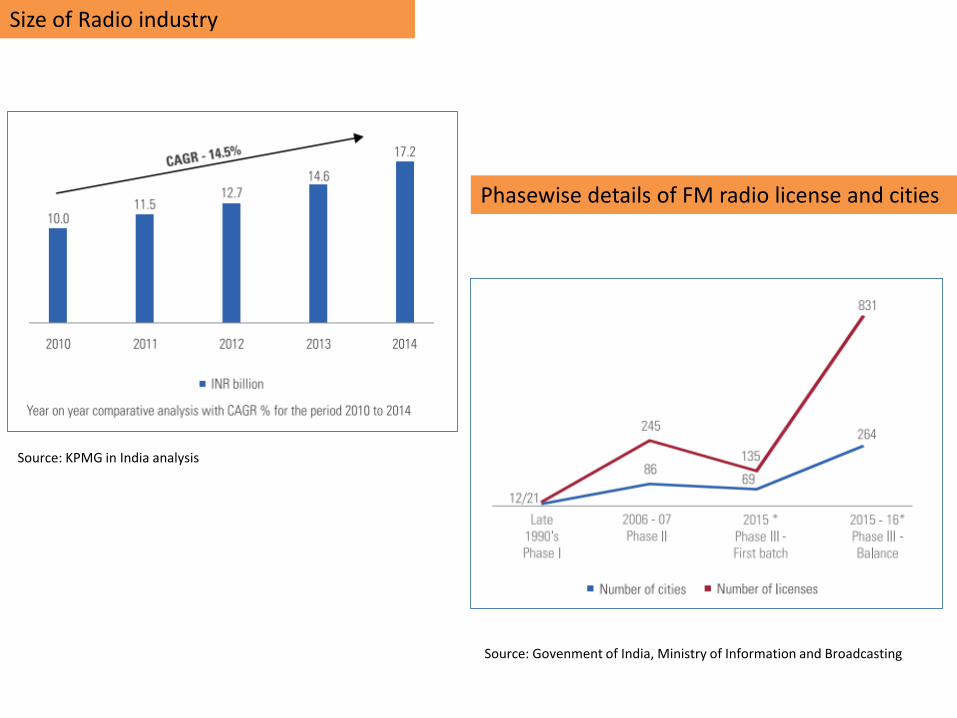

Size of Radio industry

Phasewise details of FM radio license and cities

Source: Govenment of India, Ministry of Information and Broadcasting

Source: KPMG in India analysis

Geographical expansion

Source: Industry discussions conducted by KPMG in India, KPMG in India analysis

Listernership on the go & Time spent on radio

Source: Copyright reserved with TAM MEDIA RESEARCH PVT. LTD. any use of TAM Data or (derivative thereof) mentioned herein without express permission of TAM shall be treated as illegal. RAM covers 4 metros only (Mum, Delhi, Kol & Bglr). TG : Persons, 12yrs+, All SECs’; Markets : 4 Metros

Size of Animation, VFX and Post production industry in India

Source: KPMG in India analysis and Industry discussions conducted by KPMG in India

Indian animation industry… the race begins

Number of Indian animation theatrical releases over the years

Indian animated movies with production budget and box office collections in 2014 and 2013

Countrywise animated shows on Indian TV

Top 10 favourite kids’ characters

Source: Oramax – Small wonder report, November 2014 for rank, show and channel.

Top 10 Bollywood grossers (domestic collection net) of 2014 and 2013 with number of VFX shots

Source: Industry discussions conducted by KPMG in India, KPMG in India analysis

Thank YouSource: FICCI-KPMG Indian Media and Entertainment Industry Report 2015

Prepared By: Vaibhav Dalvi

Contact: 9004786586Email: [email protected]

Related Documents