FIAS/World Bank Study of Linkages in the Philippine ITES Industry June 27, 2005 F. Ted Tschang Lee Kong Chian School of Business Singapore Management University for the Foreign Investment Advisory Service (FIAS) A joint service of the IFC and the World Bank

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FIAS/World Bank

Study of Linkages in the Philippine ITES Industry

June 27, 2005

F. Ted TschangLee Kong Chian School of BusinessSingapore Management University

for the Foreign Investment Advisory Service (FIAS)A joint service of the IFC and the World Bank

Outline

IntroductionGeneral picture

why outsourcing occurs, constraintsCurrent Philippines situation

SWOTAn outsourcing model and a case

Firm Capability and Linkages: Domestic, MNCsPolicies

FIAS/World Bank ITES sector study

5 sectorsBusiness Process OutsourcingCall centersSoftware ServicesAnimationMedical transcription

Strengths, weaknesses, opportunities, threatsLinkages, foreign investment Policy guidance

FIAS/World Bank ITES sector study

No conventional (supply chain) linkages, consider ITES as one big engine (e.g. India)

Opportunity for Philippines to leap frogForeign investment

Is nature of investors, skills, capability different?

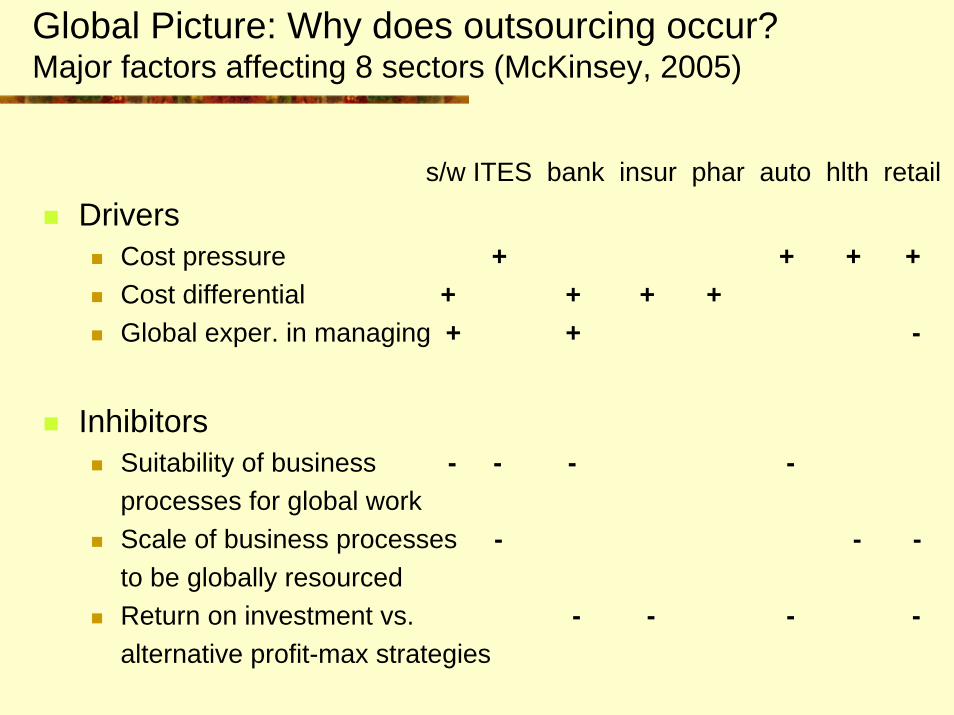

Global Picture: Why does outsourcing occur? Major factors affecting 8 sectors (McKinsey, 2005)

s/w ITES bank insur phar auto hlth retail

DriversCost pressure + + + +Cost differential + + + +Global exper. in managing + + -

InhibitorsSuitability of business - - - -processes for global workScale of business processes - - -to be globally resourcedReturn on investment vs. - - - -alternative profit-max strategies

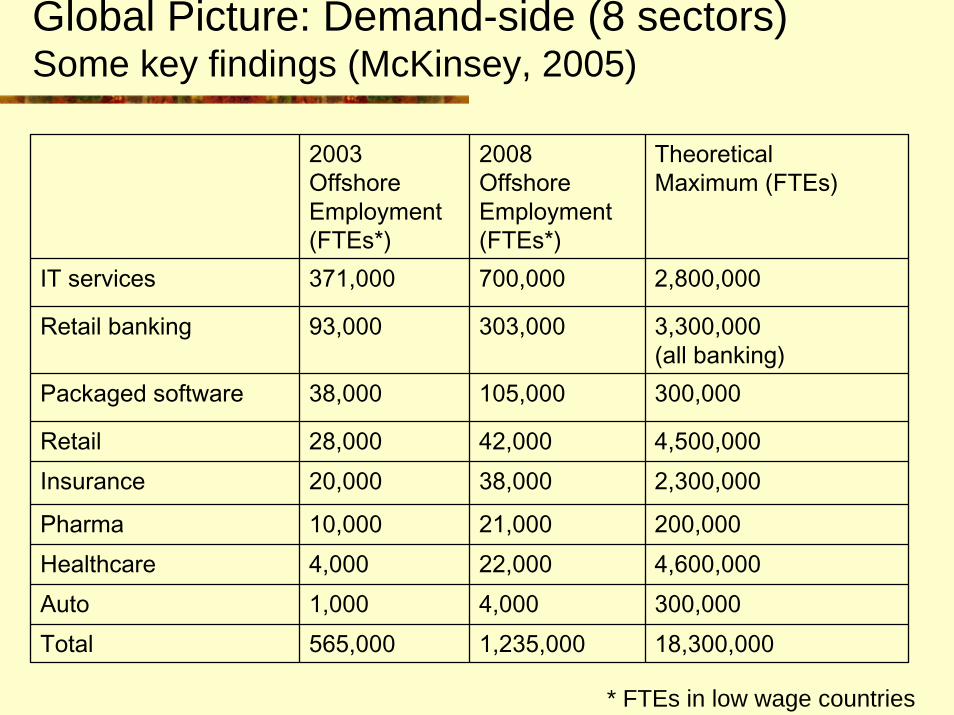

Global Picture: Demand-side (8 sectors)Some key findings (McKinsey, 2005)

2003OffshoreEmployment(FTEs*)

2008OffshoreEmployment(FTEs*)

TheoreticalMaximum (FTEs)

IT services 371,000 700,000 2,800,000

Retail banking 93,000 303,000 3,300,000 (all banking)

Packaged software 38,000 105,000 300,000

Retail 28,000 42,000 4,500,000Insurance 20,000 38,000 2,300,000

Pharma 10,000 21,000 200,000Healthcare 4,000 22,000 4,600,000Auto 1,000 4,000 300,000Total 565,000 1,235,000 18,300,000

* FTEs in low wage countries

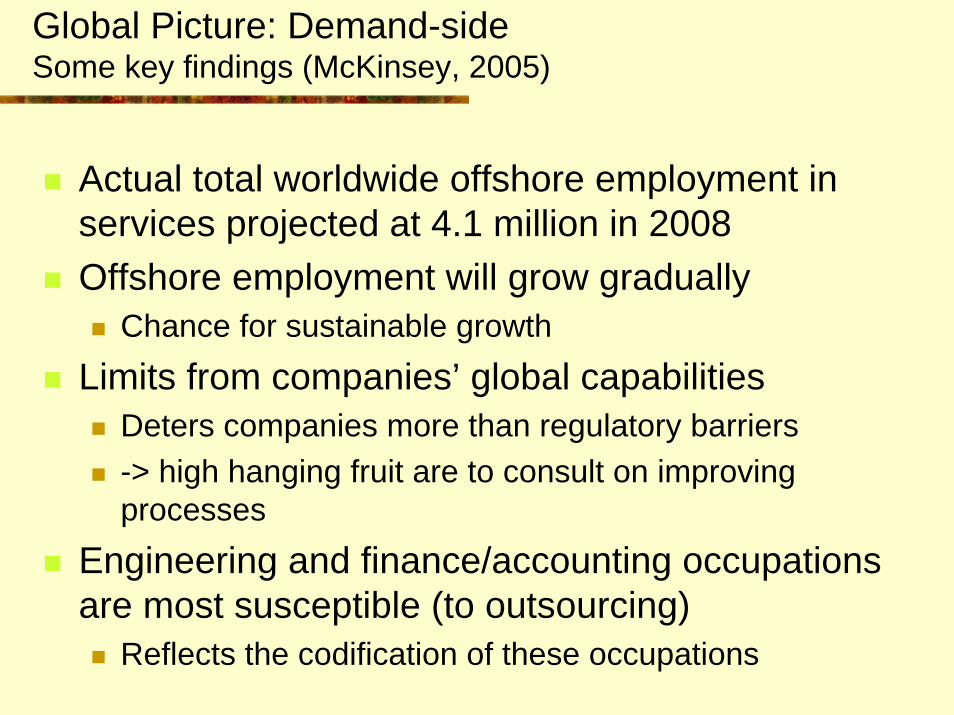

Global Picture: Demand-side Some key findings (McKinsey, 2005)

Actual total worldwide offshore employment in services projected at 4.1 million in 2008Offshore employment will grow gradually

Chance for sustainable growthLimits from companies’ global capabilities

Deters companies more than regulatory barriers-> high hanging fruit are to consult on improving processes

Engineering and finance/accounting occupations are most susceptible (to outsourcing)

Reflects the codification of these occupations

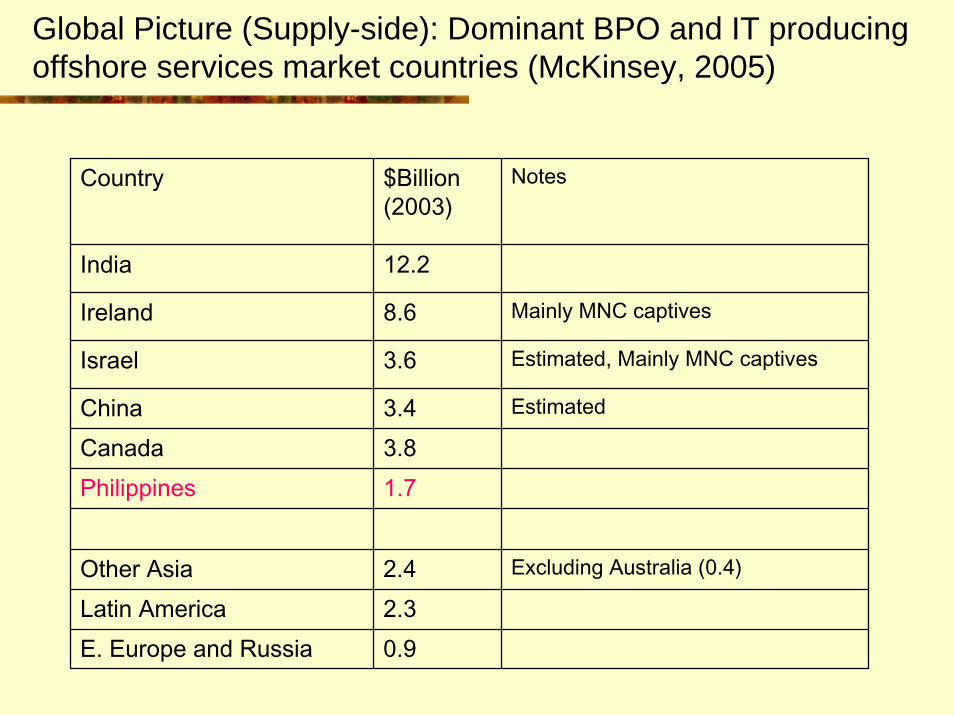

Global Picture (Supply-side): Dominant BPO and IT producing offshore services market countries (McKinsey, 2005)

Country $Billion (2003)

Notes

India 12.2

Ireland 8.6 Mainly MNC captives

Israel 3.6 Estimated, Mainly MNC captives

China 3.4 Estimated

Canada 3.8Philippines 1.7

Other Asia 2.4 Excluding Australia (0.4)

Latin America 2.3E. Europe and Russia 0.9

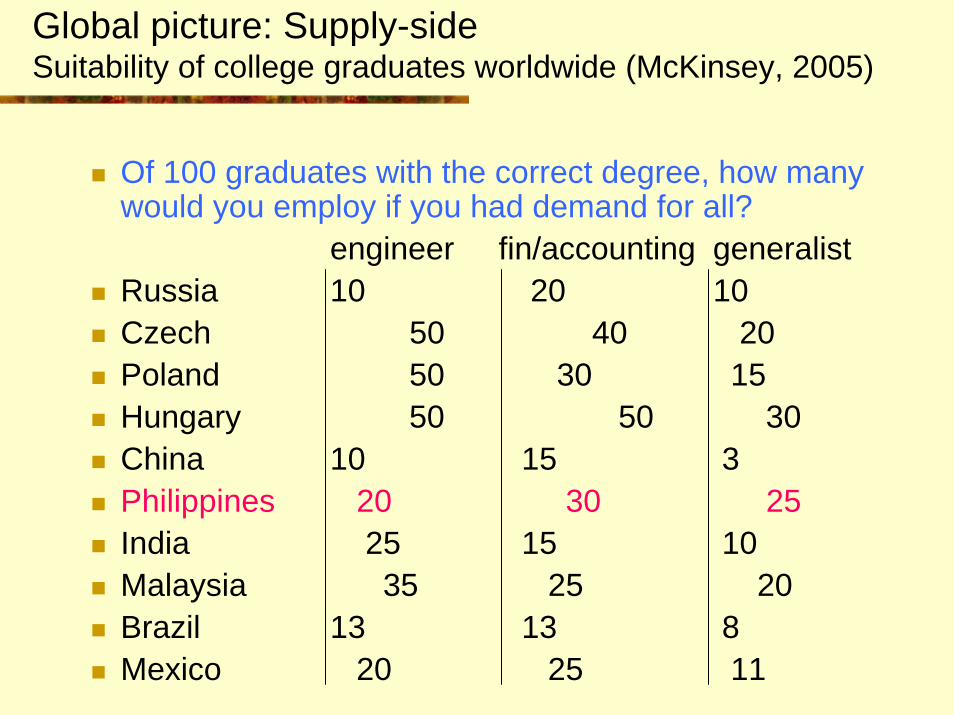

Global picture: Supply-side Suitability of college graduates worldwide (McKinsey, 2005)

Of 100 graduates with the correct degree, how many would you employ if you had demand for all?

engineer fin/accounting generalistRussia 10 20 10Czech 50 40 20Poland 50 30 15Hungary 50 50 30China 10 15 3Philippines 20 30 25India 25 15 10Malaysia 35 25 20Brazil 13 13 8Mexico 20 25 11

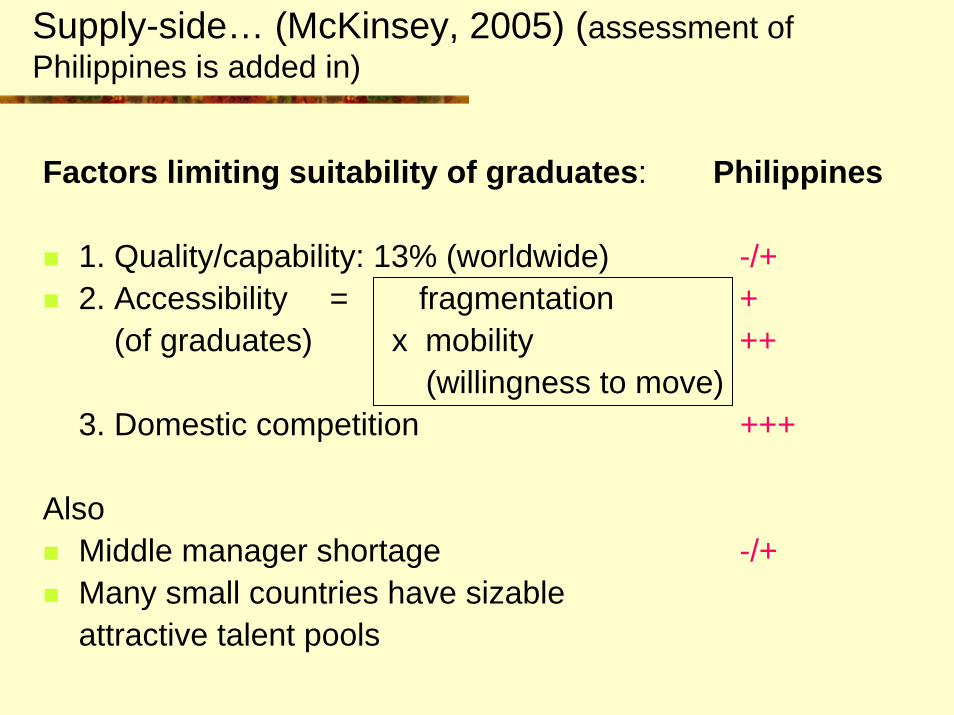

Supply-side… (McKinsey, 2005) (assessment of Philippines is added in)

Factors limiting suitability of graduates: Philippines

1. Quality/capability: 13% (worldwide) -/+2. Accessibility = fragmentation +

(of graduates) x mobility ++(willingness to move)

3. Domestic competition +++

AlsoMiddle manager shortage -/+Many small countries have sizableattractive talent pools

Issues that pertain to ITES

AT Kearney 2004 Overall: Philippines is 6th out of 25 People skills: Philippines is 11th (second pack)

(India is 1st, China 7th, S. Africa 10th, rest are DCs)Skills score is much closer to E. Europe than McKinsey’s

Business environment: Philippines is 22nd

Financial structure: Philippines is 3rd

IDCAsset advantage (tech, know-how): Philippines is 4th of 10 countries (after Canada, India, Ireland)Cost advantage: Philippines is 3rd after India, Jamaica

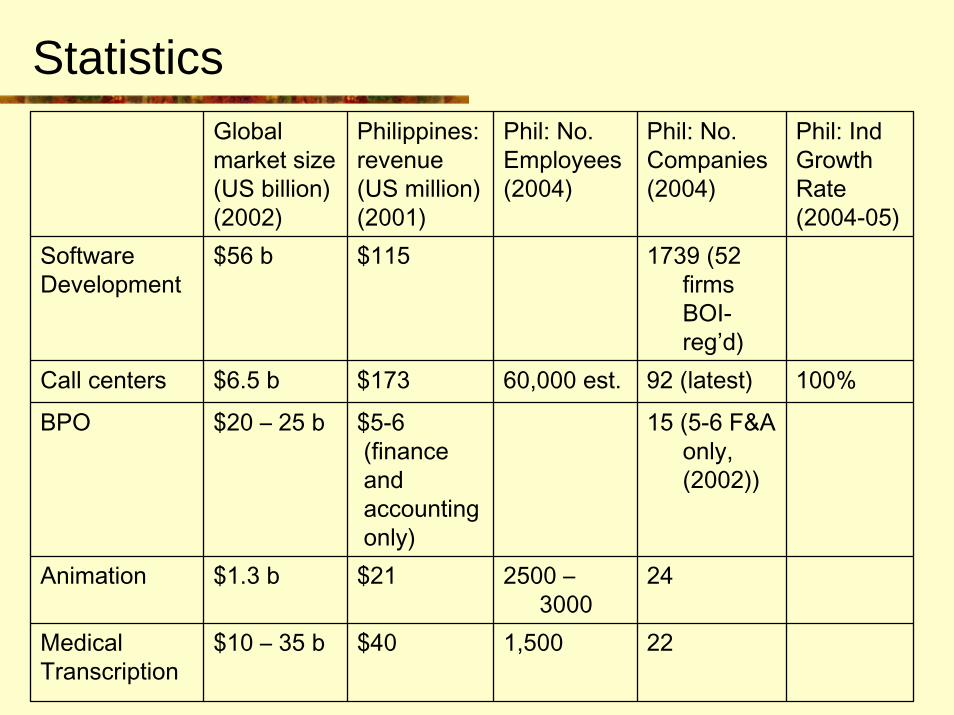

StatisticsGlobalmarket size(US billion)(2002)

Philippines:revenue(US million)(2001)

Phil: No.Employees(2004)

Phil: No.Companies(2004)

Phil: IndGrowthRate(2004-05)

SoftwareDevelopment

$56 b $115 1739 (52 firms BOI-reg’d)

Call centers $6.5 b $173 60,000 est. 92 (latest) 100%

BPO $20 – 25 b $5-6(financeandaccountingonly)

15 (5-6 F&A only, (2002))

Animation $1.3 b $21 2500 –3000

24

MedicalTranscription

$10 – 35 b $40 1,500 22

Philippines: strengths and weaknesses

StrengthsGood skills (including IT)Language affinity (but…)A “western” countryBranding (at least in the short lists)

Weaknesses (conventional)#1 corruption (weakens perception of fairness) *#2 macroeconomic instability (weak environment for investments) *Poverty, social stability

* based on World Bank E Asia PREM ICA report

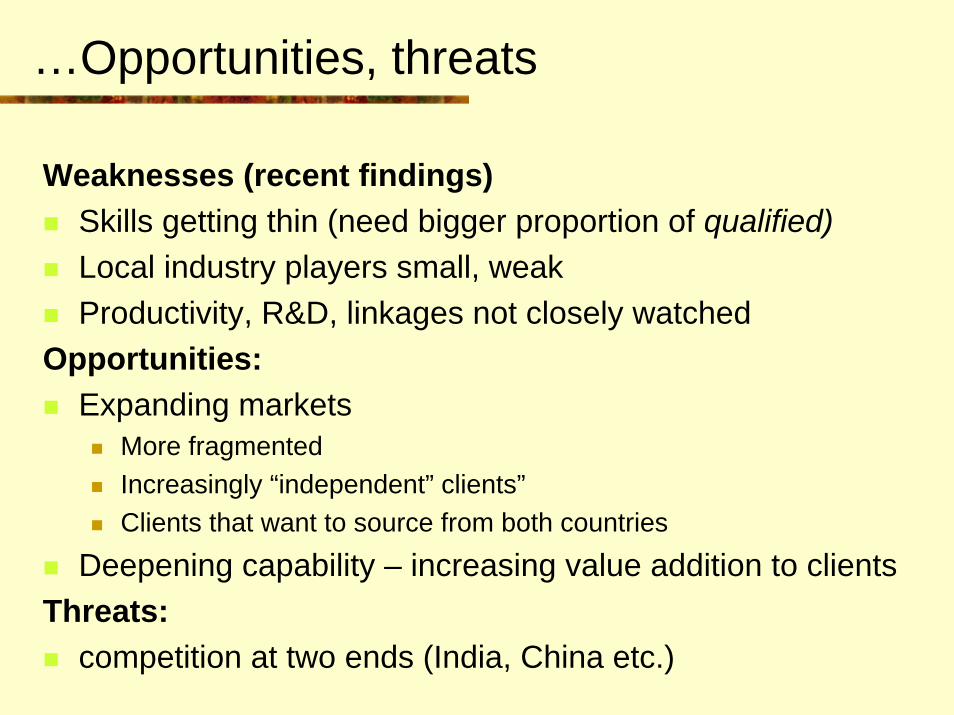

…Opportunities, threats

Weaknesses (recent findings)Skills getting thin (need bigger proportion of qualified)Local industry players small, weakProductivity, R&D, linkages not closely watched

Opportunities:Expanding markets

More fragmentedIncreasingly “independent” clients”Clients that want to source from both countries

Deepening capability – increasing value addition to clientsThreats:

competition at two ends (India, China etc.)

Issues

The significant problems we face cannot be solved at the same level of thinking we were at when we created them."

- Albert Einstein (1879-1955)

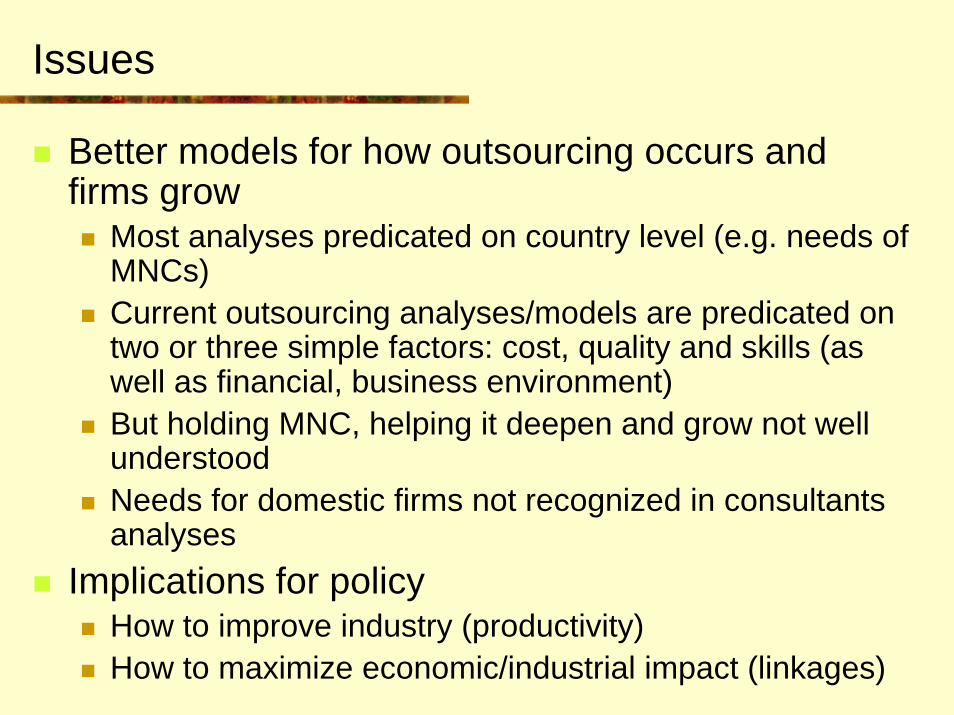

Issues

Better models for how outsourcing occurs and firms grow

Most analyses predicated on country level (e.g. needs of MNCs)Current outsourcing analyses/models are predicated on two or three simple factors: cost, quality and skills (as well as financial, business environment)But holding MNC, helping it deepen and grow not well understoodNeeds for domestic firms not recognized in consultants analyses

Implications for policyHow to improve industry (productivity)How to maximize economic/industrial impact (linkages)

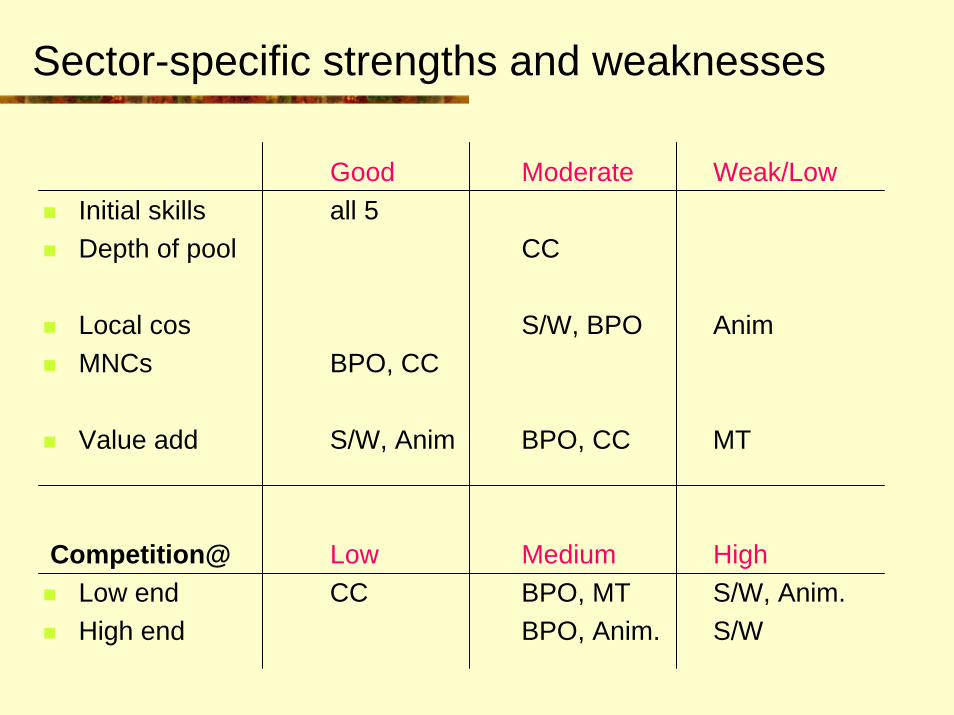

Sector-specific strengths and weaknesses

Good Moderate Weak/LowInitial skills all 5Depth of pool CC

Local cos S/W, BPO AnimMNCs BPO, CC

Value add S/W, Anim BPO, CC MT

Competition@ Low Medium HighLow end CC BPO, MT S/W, Anim.High end BPO, Anim. S/W

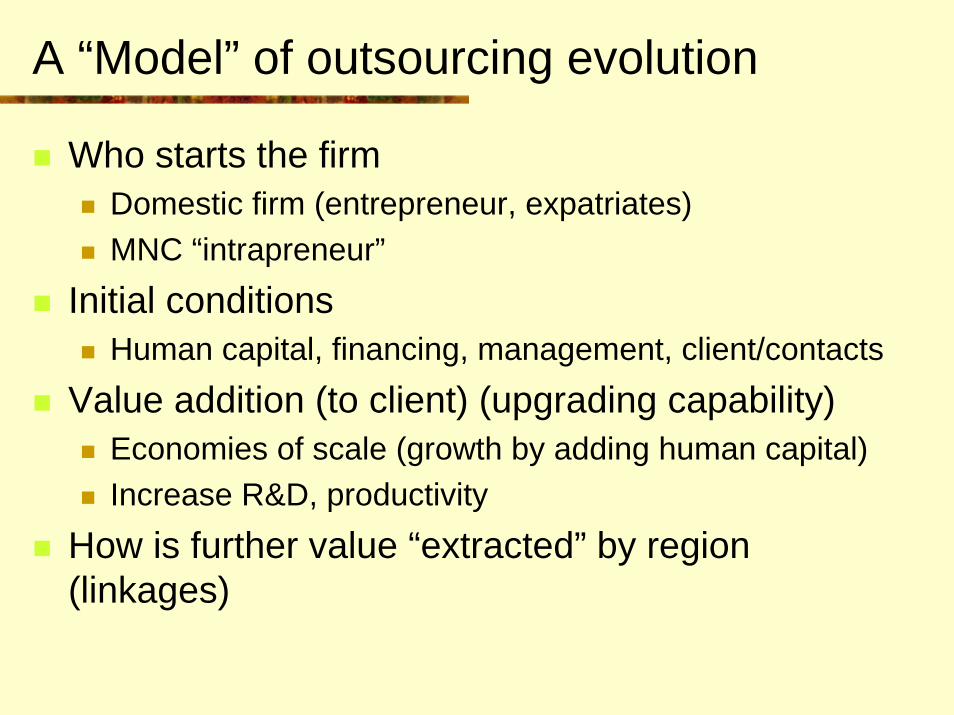

A “Model” of outsourcing evolution

Who starts the firmDomestic firm (entrepreneur, expatriates)MNC “intrapreneur”

Initial conditionsHuman capital, financing, management, client/contacts

Value addition (to client) (upgrading capability)Economies of scale (growth by adding human capital)Increase R&D, productivity

How is further value “extracted” by region (linkages)

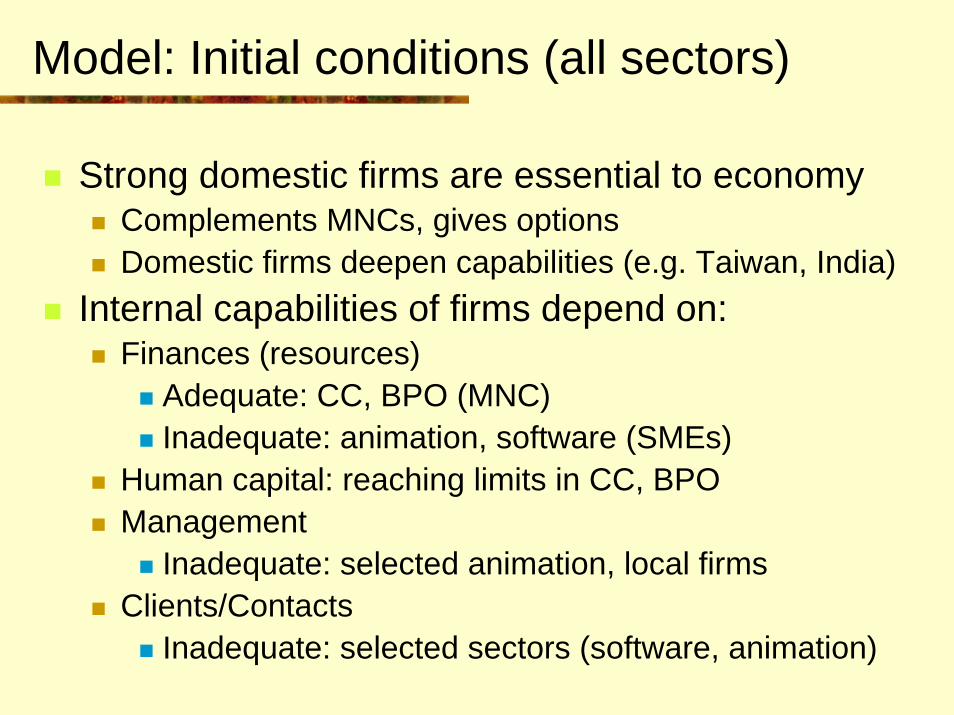

Model: Initial conditions (all sectors)

Strong domestic firms are essential to economy Complements MNCs, gives optionsDomestic firms deepen capabilities (e.g. Taiwan, India)

Internal capabilities of firms depend on:Finances (resources)

Adequate: CC, BPO (MNC)Inadequate: animation, software (SMEs)

Human capital: reaching limits in CC, BPOManagement

Inadequate: selected animation, local firmsClients/Contacts

Inadequate: selected sectors (software, animation)

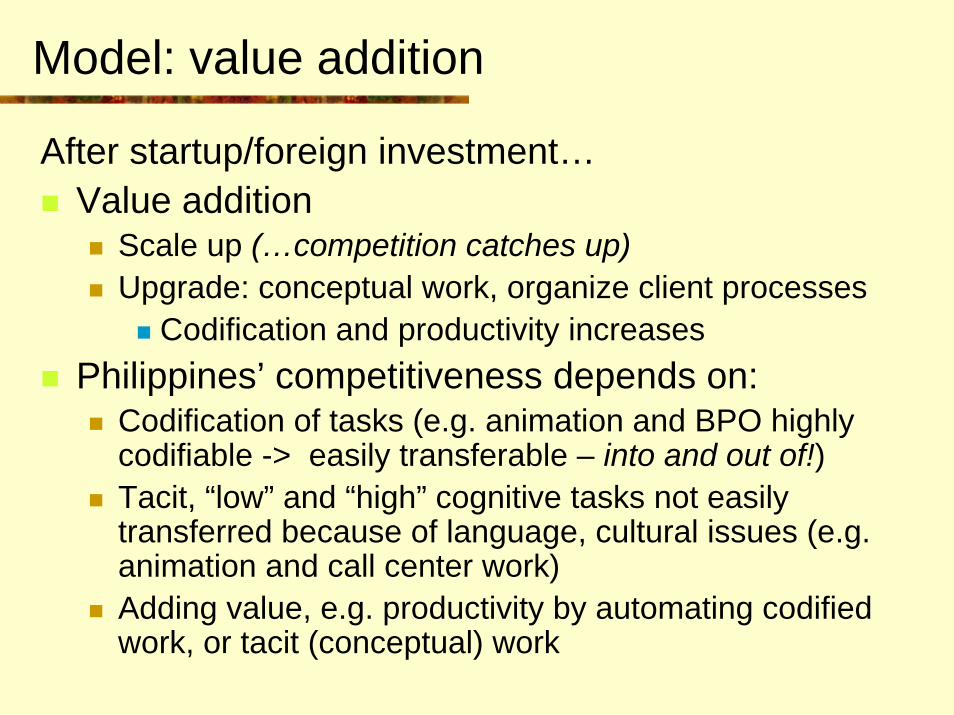

Model: value addition

After startup/foreign investment…Value addition

Scale up (…competition catches up) Upgrade: conceptual work, organize client processes

Codification and productivity increasesPhilippines’ competitiveness depends on:

Codification of tasks (e.g. animation and BPO highly codifiable -> easily transferable – into and out of!)Tacit, “low” and “high” cognitive tasks not easily transferred because of language, cultural issues (e.g. animation and call center work)Adding value, e.g. productivity by automating codified work, or tacit (conceptual) work

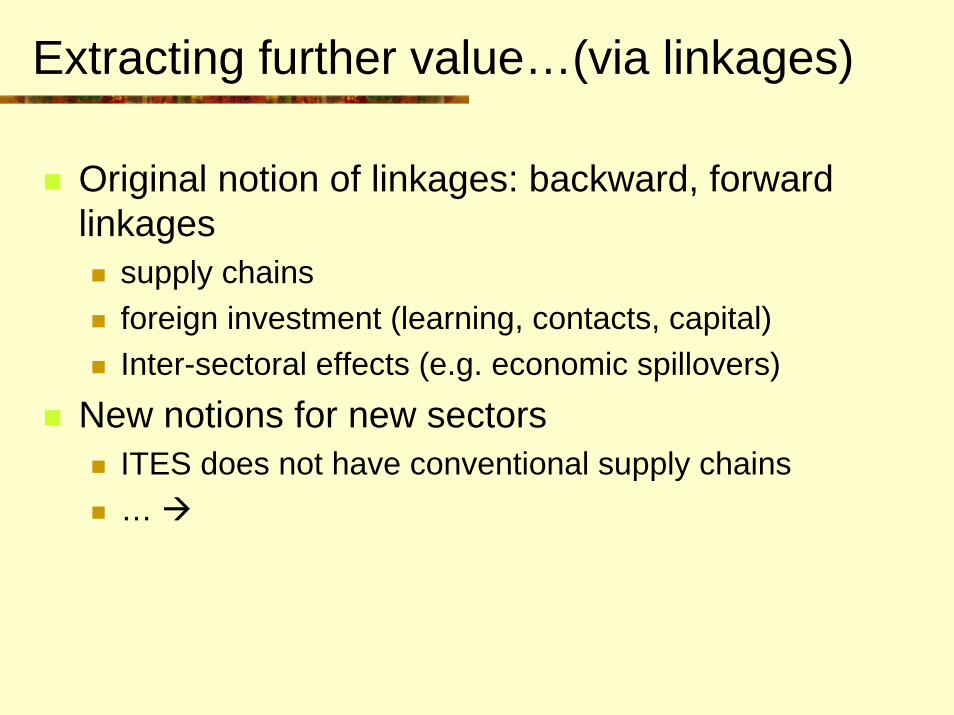

Extracting further value…(via linkages)

Original notion of linkages: backward, forward linkages

supply chainsforeign investment (learning, contacts, capital)Inter-sectoral effects (e.g. economic spillovers)

New notions for new sectorsITES does not have conventional supply chains…

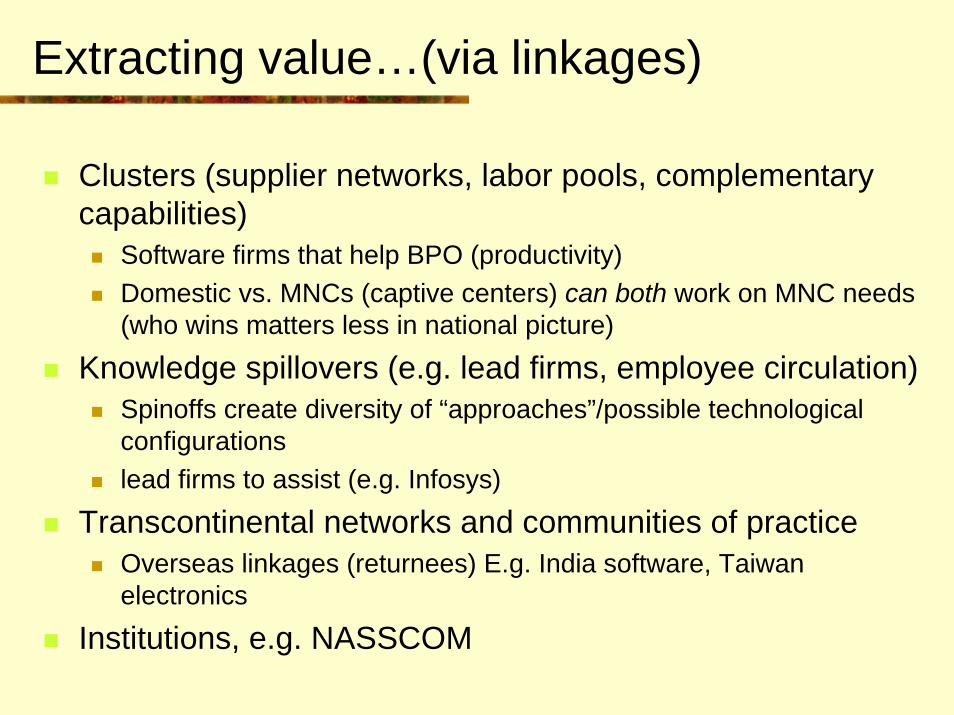

Extracting value…(via linkages)

Clusters (supplier networks, labor pools, complementary capabilities)

Software firms that help BPO (productivity)Domestic vs. MNCs (captive centers) can both work on MNC needs (who wins matters less in national picture)

Knowledge spillovers (e.g. lead firms, employee circulation)Spinoffs create diversity of “approaches”/possible technological configurationslead firms to assist (e.g. Infosys)

Transcontinental networks and communities of practiceOverseas linkages (returnees) E.g. India software, Taiwan electronics

Institutions, e.g. NASSCOM

Case: Animation industry

Global market: US 45 bill now, 50+ billion by 2005 worldwide (NASSCOM)

High value added industry, unstableApplication areas (“products”):

Conceptual hi end: Feature films, and 3D (US-based)Codified low end: series (cartoons), Movie CG effects, commercials, 2D (most of Philippines’ work)

Market (supply)Japan (430 studios) e.g. Toei with 400, many smallerKorea (200)Philippines (24): small studios - people pool: 2500-3000India (15): large diversified studiosChina - new policies to encourage domestic programsSingapore – government funding, coordination

A story using the model: animation sector

Who starts, upgrades the firmDomestic firm (expatriates), “MNCs” (e.g. Disney)

Initial conditions/capabilityStrong: Human capital, cultural advantages (initially)Weak: Finance and management (domestic firms), networks

How is value added (to client), capability upgradedLittle upgrading, no R&D, some increase in efficiency (see technology)No scale economies (average co. is small)Linkages (personal)No local investments, investments in productivity

How is further value “extracted” (further linkages)No spinoffs, spillovers minimallead firms in some areas (e.g. training)

External conditions: Industry’s downturn broke many firmsTechnology: codification of processes reduced jobs

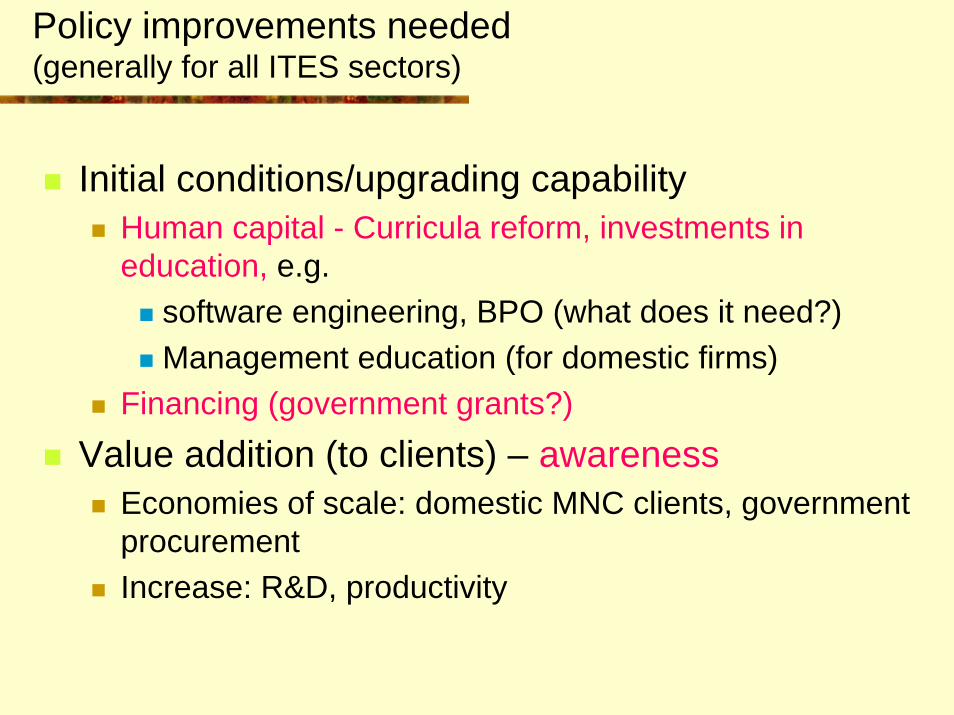

Policy improvements needed (generally for all ITES sectors)

Initial conditions/upgrading capabilityHuman capital - Curricula reform, investments in education, e.g.

software engineering, BPO (what does it need?) Management education (for domestic firms)

Financing (government grants?)Value addition (to clients) – awareness

Economies of scale: domestic MNC clients, government procurementIncrease: R&D, productivity

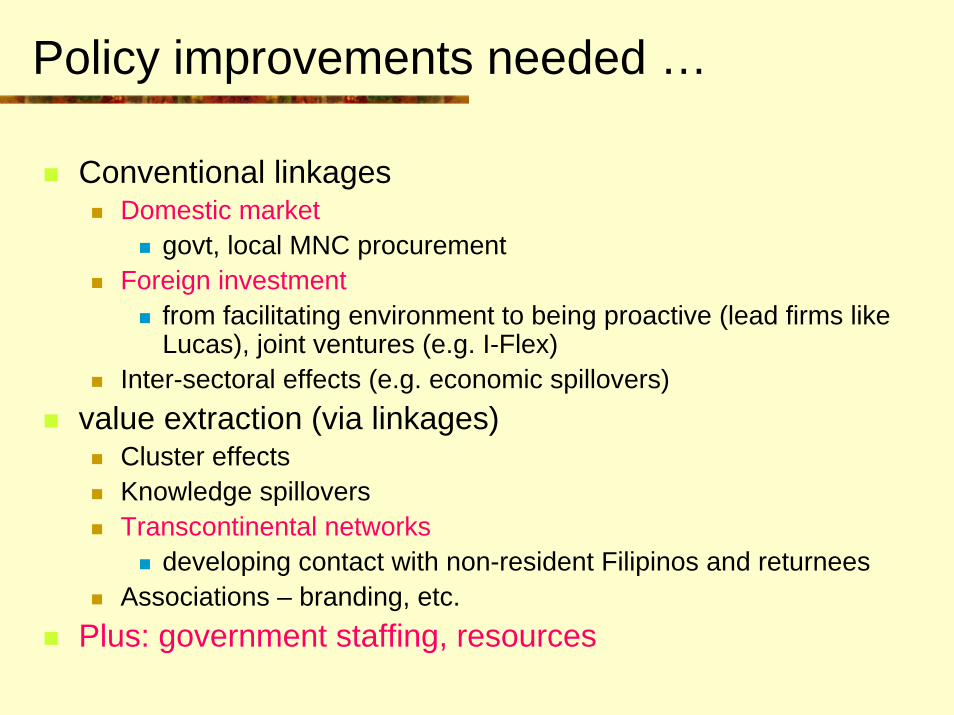

Policy improvements needed …

Conventional linkagesDomestic market

govt, local MNC procurementForeign investment

from facilitating environment to being proactive (lead firms like Lucas), joint ventures (e.g. I-Flex)

Inter-sectoral effects (e.g. economic spillovers)value extraction (via linkages)

Cluster effectsKnowledge spillovers Transcontinental networks

developing contact with non-resident Filipinos and returneesAssociations – branding, etc.

Plus: government staffing, resources

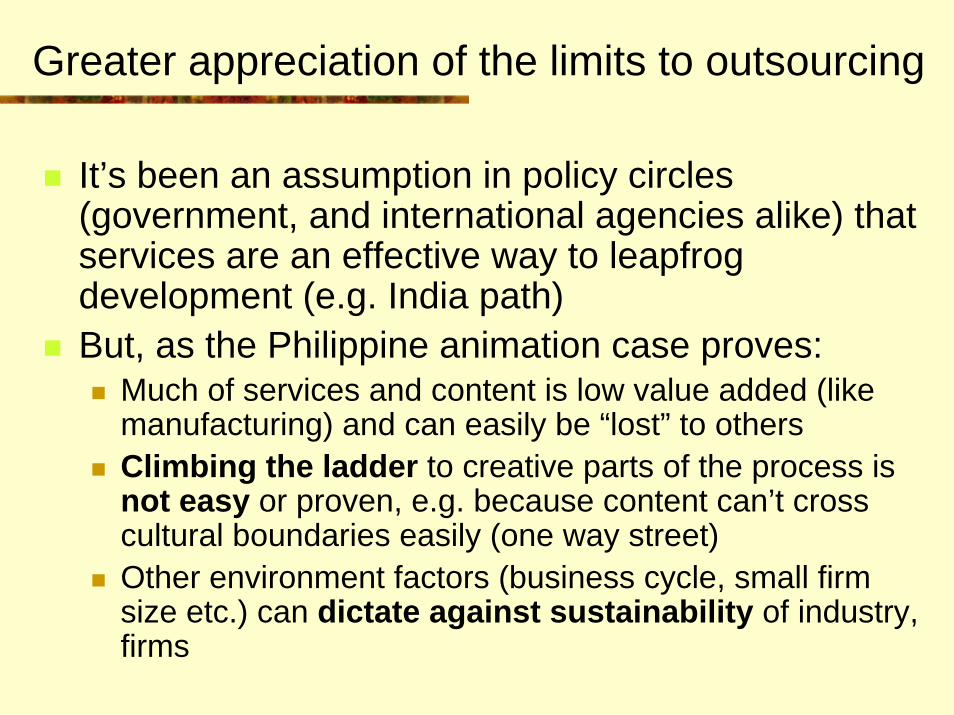

Greater appreciation of the limits to outsourcing

It’s been an assumption in policy circles (government, and international agencies alike) that services are an effective way to leapfrog development (e.g. India path)But, as the Philippine animation case proves:

Much of services and content is low value added (like manufacturing) and can easily be “lost” to othersClimbing the ladder to creative parts of the process is not easy or proven, e.g. because content can’t cross cultural boundaries easily (one way street)Other environment factors (business cycle, small firm size etc.) can dictate against sustainability of industry, firms

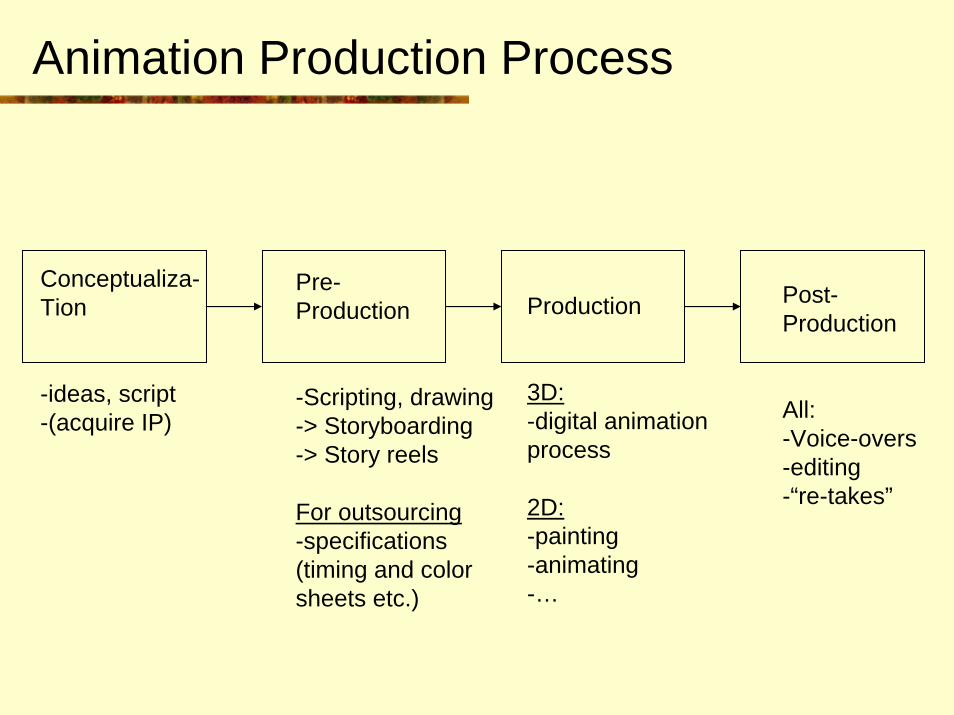

Animation Production Process

Conceptualiza-Tion

-ideas, script-(acquire IP)

Post-Production

All: -Voice-overs-editing -“re-takes”

Pre-Production

-Scripting, drawing-> Storyboarding-> Story reels

For outsourcing-specifications(timing and color sheets etc.)

Production

3D:-digital animationprocess

2D:-painting-animating-…

Source: McKinsey, 2005

Source: McKinsey, 2005

Source: McKinsey, 2005

Related Documents