Feedstock competitiveness and olefins margins Ng Baoying Managing Editor Asia Petrochemicals

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

No content below the line No content below the line

Feedstock competitiveness and olefins margins

Ng Baoying

Managing Editor

Asia Petrochemicals

No content below the line No content below the line

Petrochemicals

Private & Confidential 2

• Europe maximizes flexibility

• Opportunities for Taiwan

Cracker margins

• Market fundamentals and margins

• Can the good times last? Ethylene

• Market fundamentals and margins

• Shaky margins, uncertain future Propylene

Agenda Feedstock competitiveness and olefins margins

No content below the line No content below the line

Petrochemicals

Private & Confidential 3

The principles call on PRAs to:

• Adopt robust internal quality control procedures applicable to the submission and evaluation of market data used in an assessment

• Commit to make available to market authorities audit trails and other related documentation

• Maintain robust and publicly available methodologies

• Give priority to concluded transactions and, if not, explain the reasons

• Institute a formal complaints process, which includes recourse to an independent third party

Highest level of IOSCO standards IOSCO issued formal Principles for Oil Price Reporting Agencies in 2012

No content below the line No content below the line

Petrochemicals

Private & Confidential 4

Transparent and rigorous assessments Trust and reliability

Details the specific

dimensions of our assessments

A living document

Backbone of Platts’ prices

No content below the line No content below the line

Private & Confidential 5

SGX-Platts swaps vols hits all-time high in July 254,000 mt swaps traded – that’s 25% of monthly physical PX volume into China

Petrochemicals

-

50,000

100,000

150,000

200,000

250,000

300,000

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

De

c-1

5

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

mt

Traded volumes of Platts-based SGX PX swaps triple

Source: SGX

Exchange-traded

contracts settle off

Platts prices

PX swaps contract volumes

surge amid volatility

Hedge with limited basis

risk

PX volumes tripled year

on year

More than 250 kt in July

That’s 25% of the monthly PX physical imports in

China

No content below the line No content below the line

Petrochemicals

Private & Confidential 6

• Europe maximizes flexibility

• Opportunities for Taiwan

Cracker margins

• Market fundamentals and margins

• Can the good times last? Ethylene

• Market fundamentals and margins

• Shaky margins, uncertain future Propylene

Agenda Feedstock competitiveness and olefins margins

No content below the line No content below the line

Petrochemicals

Private & Confidential 7

NEA naphtha still more expensive than most Despite naphtha price falls

-

100

200

300

400

500

600

700

800

900

1,000

- 20,000 40,000 60,000 80,000 100,000 120,000 140,000

$/MT

Cumulative Capacity ('000 MT)

Saudi Ethane US Ethane

US E/P Mix

WE Ethane

SE Asia Naphtha

NE Asia Naphtha

ME Ethane

US Ethylene Price

NW Europe Ethylene Price

NE Asia Ethylene Price

CTO/MTO

Source: Platts Analytics

Red oval: NEA naphtha producers VS

everyone else

Many producers at

lower cost

C2 NEA most expensive in the world, cost push a

factor

No content below the line No content below the line

Petrochemicals

Private & Confidential 8

Historical cost curve: Major landscape shifts Naphtha-based producers gains competitive edge against ethane-based producers

-

200

400

600

800

1,000

1,200

1,400

1,600

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

De

c-1

5

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

$/MT Ethylene production cost

NE Asia Naphtha

US Ethane

Delivered EthaneChinaCTO

Saudi Ethane

Asia Ethylene

Source: Platts Analytics

Source: Platts Analytics

Red line: Ethylene price has

been rocky

Other lines: Cost to produce

C2

Naphtha-based

costs have fallen

Margins have

widened

No content below the line No content below the line

Petrochemicals

Private & Confidential 9

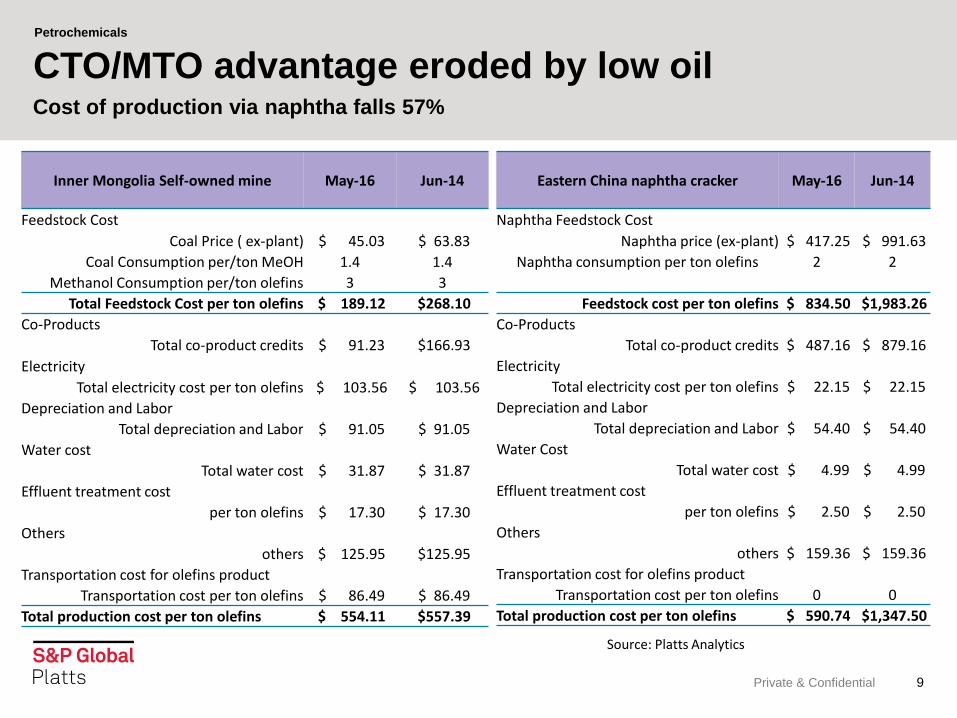

CTO/MTO advantage eroded by low oil Cost of production via naphtha falls 57%

Inner Mongolia Self-owned mine May-16 Jun-14

Feedstock Cost

Coal Price ( ex-plant) $ 45.03 $ 63.83

Coal Consumption per/ton MeOH 1.4 1.4

Methanol Consumption per/ton olefins 3 3

Total Feedstock Cost per ton olefins $ 189.12 $268.10

Co-Products

Total co-product credits $ 91.23 $166.93

Electricity

Total electricity cost per ton olefins $ 103.56 $ 103.56

Depreciation and Labor

Total depreciation and Labor $ 91.05 $ 91.05

Water cost

Total water cost $ 31.87 $ 31.87

Effluent treatment cost

per ton olefins $ 17.30 $ 17.30

Others

others $ 125.95 $125.95

Transportation cost for olefins product

Transportation cost per ton olefins $ 86.49 $ 86.49

Total production cost per ton olefins $ 554.11 $557.39

Eastern China naphtha cracker May-16 Jun-14

Naphtha Feedstock Cost

Naphtha price (ex-plant) $ 417.25 $ 991.63

Naphtha consumption per ton olefins 2 2

Feedstock cost per ton olefins $ 834.50 $1,983.26

Co-Products

Total co-product credits $ 487.16 $ 879.16

Electricity

Total electricity cost per ton olefins $ 22.15 $ 22.15

Depreciation and Labor

Total depreciation and Labor $ 54.40 $ 54.40

Water Cost

Total water cost $ 4.99 $ 4.99

Effluent treatment cost

per ton olefins $ 2.50 $ 2.50

Others

others $ 159.36 $ 159.36

Transportation cost for olefins product

Transportation cost per ton olefins 0 0

Total production cost per ton olefins $ 590.74 $1,347.50

Source: Platts Analytics

No content below the line No content below the line

Petrochemicals

Private & Confidential 10

Sup

ply

gro

wth

• U.S.

• Atlantic basin

• Middle East

• Russia

• Iran?

Mo

re V

LGC

s • 48 new VLGCs in 2016

• Freight rates to ease

• Expanded Panama canal D

eman

d g

row

th

• Indonesia

• Thailand

• Brazil

• China

What about LPG? Spread to naphtha hits $70/mt

No content below the line No content below the line

Petrochemicals

Private & Confidential 11

Asia LPG-naphtha spread starts to widen Prices typically move somewhat in tandem – till now

200

400

600

800

1000

1200

1400

January-12 January-13 January-14 January-15 January-16

Naphtha C+F Japan Cargo

Propane Refrigerated CFR South China 20-35 days cargo

Butane Refrigerated CFR South China 20-35 days cargo

Diverging spread

between LPG and naphtha

LPG supply rose on US cargo flows

LPG now cheaper than naphtha - $50 difference is

the threshold

Impact: Formosa using more LPG as

cracker feedstock

(15% in May)

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 12

Asia LPG discount to naphtha gains a foothold Some producers switch

-400

-300

-200

-100

0

100

200

300

1/1/2012 1/1/2013 1/1/2014 1/1/2015 1/1/2016

Asia propane discount to naphtha

Asia butane discount to naphtha

$50

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 13

Europe LPG-naphtha spread widens time to time Unlike Asia, price don’t move in tandem and vary

0

200

400

600

800

1000

1200

1400

1/4/2010 1/4/2011 1/4/2012 1/4/2013 1/4/2014 1/4/2015 1/4/2016

Naphtha CIF NWE Cargo

Propane CIF NWE 7kt+

Butane CIF NWE 3kt+

From 2015, wide

spread more

entrenched

2014 spot cracker margin:

$265

2015 spot cracker margin:

$558

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 14

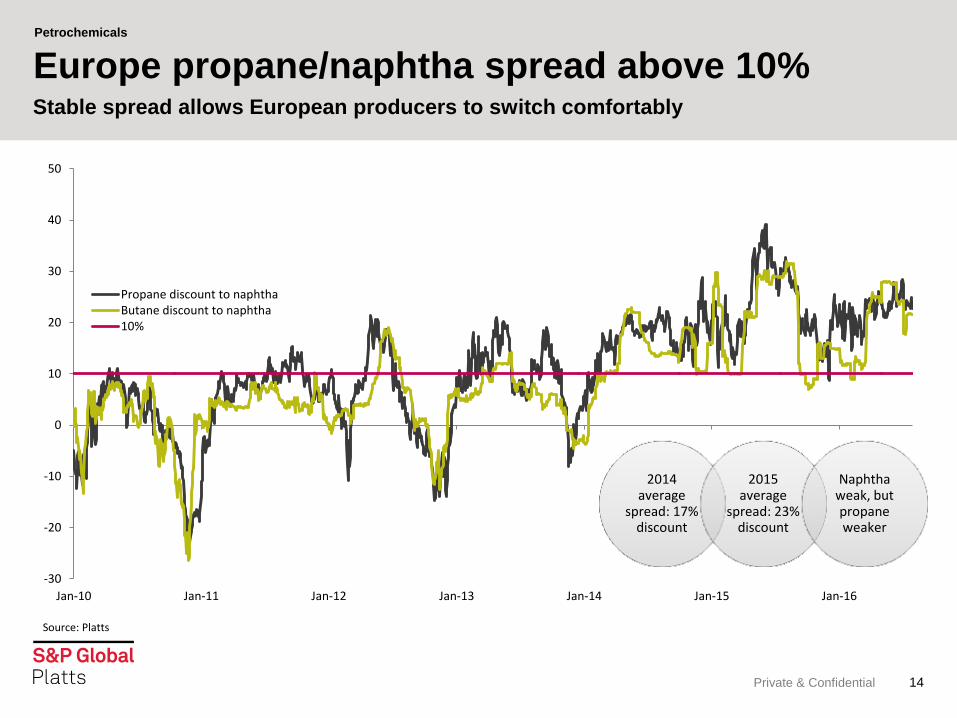

Europe propane/naphtha spread above 10% Stable spread allows European producers to switch comfortably

-30

-20

-10

0

10

20

30

40

50

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Propane discount to naphthaButane discount to naphtha10%

2014 average

spread: 17% discount

2015 average

spread: 23% discount

Naphtha weak, but propane weaker

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 15

• Europe maximizes flexibility

• Opportunities for Taiwan

Cracker margins

• Market fundamentals and margins

• Can the good times last? Ethylene

• Market fundamentals and margins

• Shaky margins, uncertain future Propylene

Agenda Feedstock competitiveness and olefins margins

No content below the line No content below the line

Petrochemicals

Private & Confidential 16

NEA naphtha still more expensive than most Despite naphtha price falls

-

100

200

300

400

500

600

700

800

900

1,000

- 20,000 40,000 60,000 80,000 100,000 120,000 140,000

$/MT

Cumulative Capacity ('000 MT)

Saudi Ethane US Ethane

US E/P Mix

WE Ethane

SE Asia Naphtha

NE Asia Naphtha

ME Ethane

US Ethylene Price

NW Europe Ethylene Price

NE Asia Ethylene Price

CTO/MTO

Source: Platts Analytics

No content below the line No content below the line

Petrochemicals

Private & Confidential 17

Asia ethylene enjoy stable, firm margins Ethylene prices fall slower than naphtha

0

200

400

600

800

1000

1200

1400

1600

1800

1/4/2010 1/4/2011 1/4/2012 1/4/2013 1/4/2014 1/4/2015 1/4/2016

Ethylene-Naphtha spread

Ethylene CFR NE Asia

Naphtha C+F Japan Cargo

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 18

Bulk of ethylene investments in Asia, N. America Over 2015-2025

17%

2%

3%

37%

40%

1%

Global cracker additions by feedstock

CTO/MTOButanePropaneNaphthaEthane

28%

18% 14%

37%

3%

Global cracker additions by region

North AmericaMiddle EastEuropeAsiaAfrica

Source: Platts Analytics N. America, Asia most

new plants

Mid East already has

many

Ethane most

popular feedstock

(US)

No content below the line No content below the line

Petrochemicals

Private & Confidential 19

Eight steam crackers under construction in USGC More projects proposed

19 Total Petrochemicals, TX

Williams Geismar 2, LA

Badlands NGL, ND

PTT Global Chemical & Marubeni, OH

ChevronPhillips

ExxonMobil

Dow Sasol

Odebrecht/ Braskem, WV

Shell, PA

Under Construction

Formosa

Oxy

Axiall & Lotte

Proposed

Formosa Petrochemical, LA

Shintech

Source: Platts Analytics

No content below the line No content below the line

Petrochemicals

Private & Confidential 20

USGC exported ethane on oversupply First waterborne cargo left Marcus Hook in March 2016

20

Petchem Company

INEOS

Borealis

SABIC

Reliance

-

100

200

Mb

/d

US Ethane Exports

Marcus Hook Enterprise

Other Potential C2 Customers: • Versalis • BPCL (Asia) • GAIL (Asia) • Braskem • SP Chemical (Asia)

Source: Platts Analytics

No content below the line No content below the line

Petrochemicals

Private & Confidential 21

• Europe maximizes flexibility

• Opportunities for Taiwan

Cracker margins

• Market fundamentals and margins

• Can the good times last? Ethylene

• Market fundamentals and margins

• Shaky margins, uncertain future Propylene

Agenda Feedstock competitiveness and olefins margins

No content below the line No content below the line

Petrochemicals

Private & Confidential 22

Asia propylene margin shrinks on 2016 Largely due to excess supply in market

R² = 0.8307

R² = 0.7809

0

200

400

600

800

1000

1200

1400

1600

Jan-13 Jan-14 Jan-15 Jan-16

Naphtha C+F Japan Cargo

Propylene Poly Grade CFR China

Poly. (Naphtha C+F Japan Cargo)

Poly. (Propylene Poly Grade CFR China)

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 23

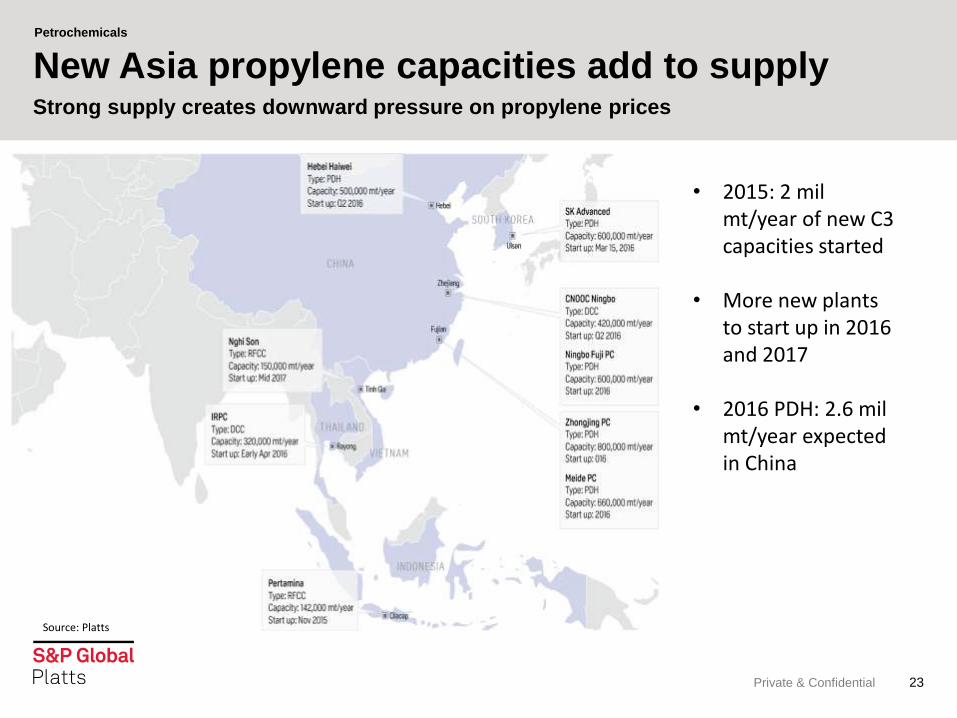

New Asia propylene capacities add to supply Strong supply creates downward pressure on propylene prices

• 2015: 2 mil mt/year of new C3 capacities started

• More new plants to start up in 2016 and 2017

• 2016 PDH: 2.6 mil mt/year expected in China

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 25

2.6 mil mt new China PDH capacity in 2016 Propylene faces supply pressures with new supply, after 2.9 mil mt added in 2014-15

Source: Platts

No content below the line No content below the line

Petrochemicals

Private & Confidential 26

PDH profitable after early 2016 struggle Despite price pressures from new supply

(350.00)

(150.00)

50.00

250.00

450.00

650.00

850.00

1050.00

1250.00

1450.00

1650.00

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16

Estimated Profit margin (Actual price VS cost)

Propane Refrigerated CFR South China 20-35 days cargo

Propylene Poly Grade CFR China

Breakeven cost to produce propylene

Source: Platts

No content below the line No content below the line

Petrochemicals

27

Ng Baoying

Managing Editor

Asian Petrochemicals

D: +65 6530 6588

M: +65 9105 5221

Thank you

Related Documents

![Final report - pdf version...b) Ethylene production by source. c) Propylene production by source [6] In a steam cracking plant, the process from feedstock to olefins involves many](https://static.cupdf.com/doc/110x72/6141006783382e045471cfce/final-report-pdf-version-b-ethylene-production-by-source-c-propylene-production.jpg)