Federal Reserve Reforms Also, not always clear that the entity is in fact too big to fail, or whether there is simply a perception that it is too big to fail Introduces classic moral hazard Whether it is feasible in a market and political sense in the future. Auto industry Banking industry Greece?

Federal Reserve Reforms Also, not always clear that the entity is in fact too big to fail, or whether there is simply a perception that it is too big to.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Federal Reserve Reforms

Also, not always clear that the entity is in fact too big to fail, or whether there is simply a perception that it is too big to fail

Introduces classic moral hazard Whether it is feasible in a market and political

sense in the future. Auto industry Banking industry Greece?

Limits to Reforms

Many institutions, public and private, have risk management strategies – not often followed for long

When times are good, firms are reluctant to take into accountant all risks out there

Problem is at both macro and micro level Very political

Micro level - US housing sector in 2000s - Fannie Mae and Freddie Mac

Macro international level - voting pressures on IMF right now

Steps taken over Past Year

Basel III provisions include new capital standards and rules to provide strong incentives to change their business models. Much tougher than existing regime.

- Tighter definition of Tier 1 capital and

- stricter definition of risk-adjusted assets.

Basel III – Dudley Conclusions

- “[E]asy access to credit that is underpriced because it is not backed by sufficient capital is not a sustainable route to prosperity.”

Issues to think about• US seeking to fix the banking and non-

banking financial system at same time as....

• Fixing health care, energy and the environment ...

• Fixing housing crisis by offering new loans to buyers – or continue with foreclosures

• Boost employment through more government spending and record budget deficits

• Coordinate with international financial community – where and to what extent?

6

Globalization Drivers

• Reductions in tariffs/quotas under WTO and FTAs

• Declines in sea/air transportation costs

• Dramatic declines in telecommunications costs

• Elimination of controls over short- and long-term capital flows

• Collapse of Soviet Union and the socialist model

7

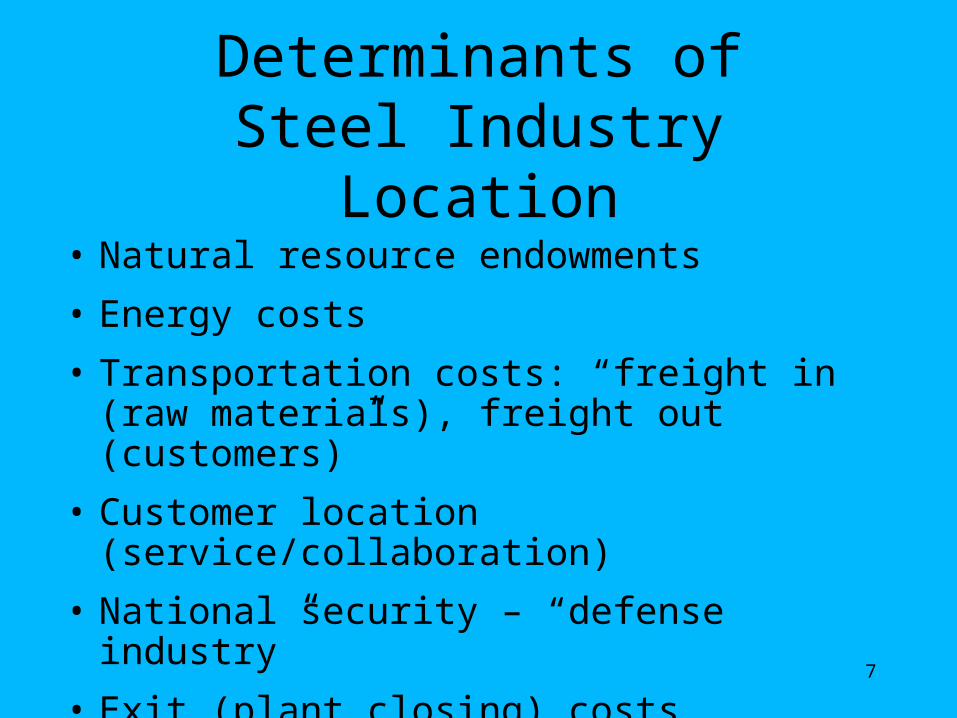

Determinants ofSteel Industry Location

• Natural resource endowments

• Energy costs

• Transportation costs: “freight in (raw materials), freight out (customers)”

• Customer location (service/collaboration)

• National security – “defense industry”

• Exit (plant closing) costs

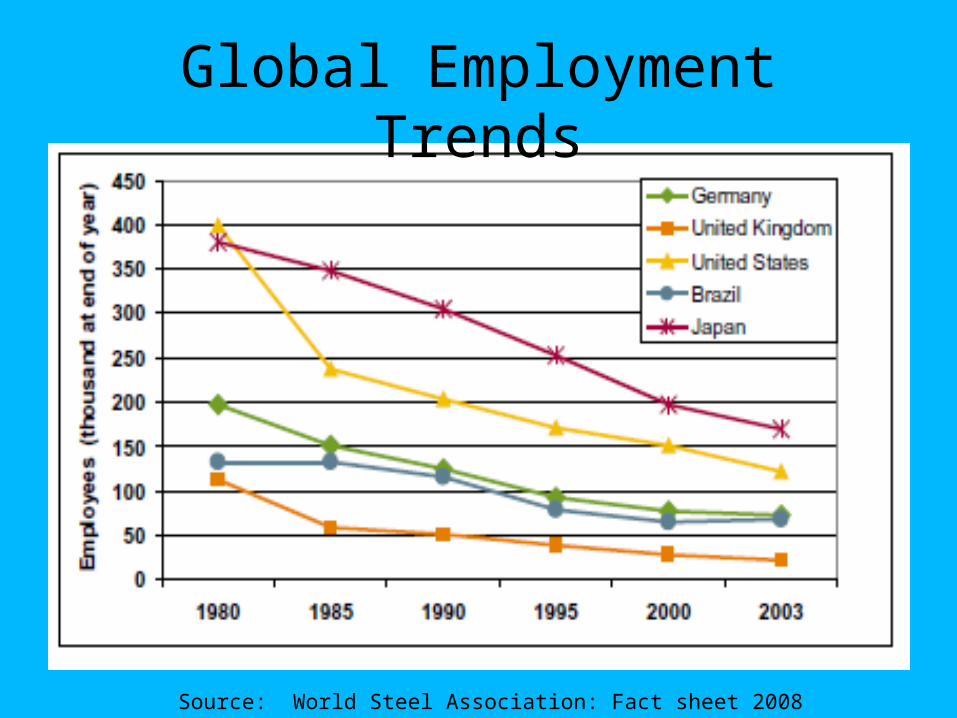

Global Employment Trends

Source: World Steel Association: Fact sheet 2008

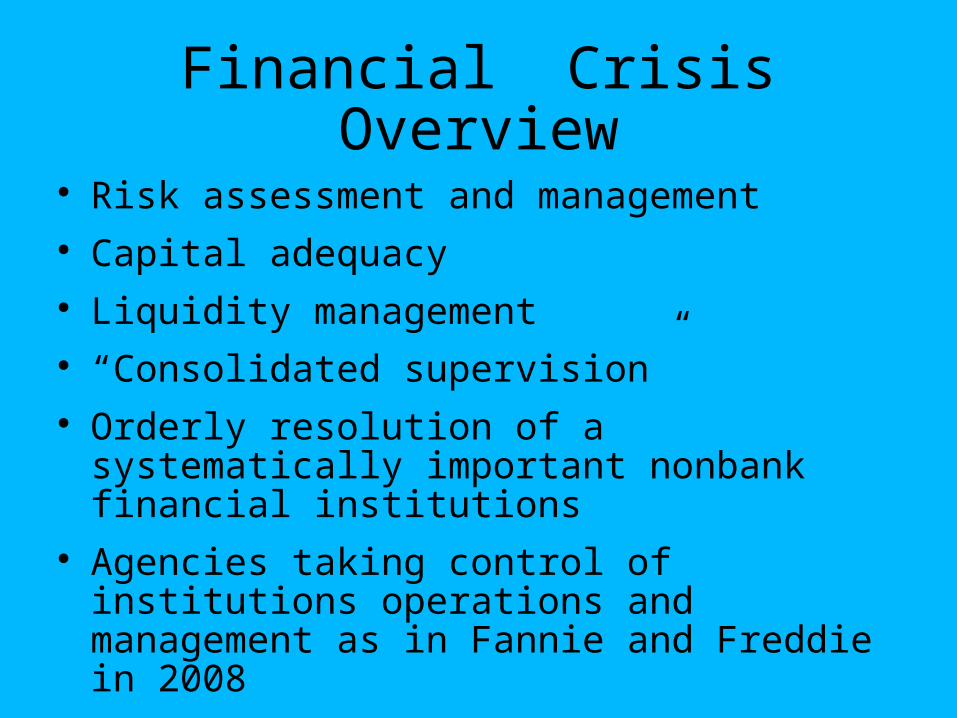

Financial Crisis Overview Risk assessment and management Capital adequacy Liquidity management “Consolidated supervision” Orderly resolution of a systematically important

nonbank financial institutions Agencies taking control of institutions operations

and management as in Fannie and Freddie in 2008

Federal Reserve: Financial Reform to Address

Sytemic RiskBernanke in spring of 2009 described elements to a strategy to deal with four key issues with international implications (BIS). Sought to address:

• “Too big to fail” problem

• Financial infrastructure (“plumbing”) – systems, rules and conventions that govern trading, payment, clearing and settlement

• Regulatory policies to avoid excessive “procyclicality”

• A new “risk assessment authority” to monitor and address systemic risks at “macroprudential” level

Federal Reserve Reforms - 1

Allowing “Too Big to Fail” institutions – results in too many distortions, according to Bernanke:

• Reduces market discipline and encourages excessive risk taking by the firm

• Provides artificial incentive for firms to grow

• Creates un-level playing field with smaller firms

• Cost of bailing out too big to fail firms very, very expensive

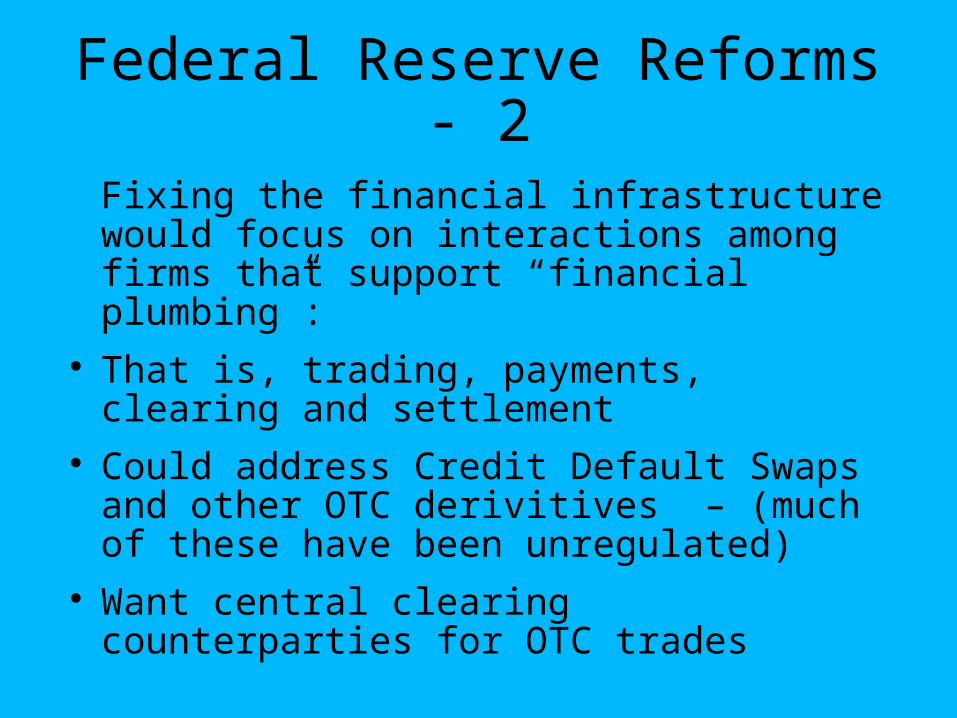

Federal Reserve Reforms - 2

Fixing the financial infrastructure would focus on interactions among firms that support “financial plumbing”:

That is, trading, payments, clearing and settlement

Could address Credit Default Swaps and other OTC derivitives – (much of these have been unregulated)

Want central clearing counterparties for OTC trades

Federal Reserve Reforms - 3Deal with “procyclicality” Current capital standards, accounting rules and

other regulations have made the financial sector excessively procyclical and . . . .

“Led financial institutions to ease credit in booms and tighten credit in downturns more than is justified by changes in the creditworthiness of borrowers”

Modify capital standards Improve disclosure and transparency Review standards governing valuation and loss

provisioning

Federal Reserve Reforms - 4

To address broad risk assessment strategy issues looked to create a Systemic Risk Authority – probably Fed (see 2010 Dodd-Frank Act)

Take a more “macroprudential” approach to the supervision and regulation of financial firms

Look at overall economic risks, not just market or credit risks

Steps Taken

Basel III

The Dodd-Frank Act

and

the Volcker Rule

Steps taken in Recent Years

Basel III is designed to address a number of issues that were recently identified by NY Fed President Dudley:

Many large financial firms “did not have enough high-quality capital to be able to retain access to private funding markets” during large losses.

Inadequate liquidity buffers – “widespread over-reliance on short-term funding to finance long-term illiquid assets”

Steps taken over Past Year

“Lack of transparency” – hard to value derivatives, such as CDS, etc.

“Inappropriate structure of incentives encouraged excessive risk taking.”

Lack of appreciation of how much the financial system was “interconnected so that shocks were transmitted broadly through the financial system...”

Basel III

- Standards emphasize banks to use more common equity in numerator by creating an explicit quantitative capital standard

- Tier 1 capital to include more common equity and that equity to be more narrowly defined as “tangible common equity”

- Ratio of that equity to rise to 4.5% of risk adjusted capital

- Also add 2.5 percent for “capital conservation buffer”

Basel III

- Much higher proportion of ratio is now met by common equity;

- that common equity is much better quality;

- the amount of risk-adjusted assets has increased and better reflects underlying risk;

- new capital conservation buffer is added;

- and much more.

Basel III

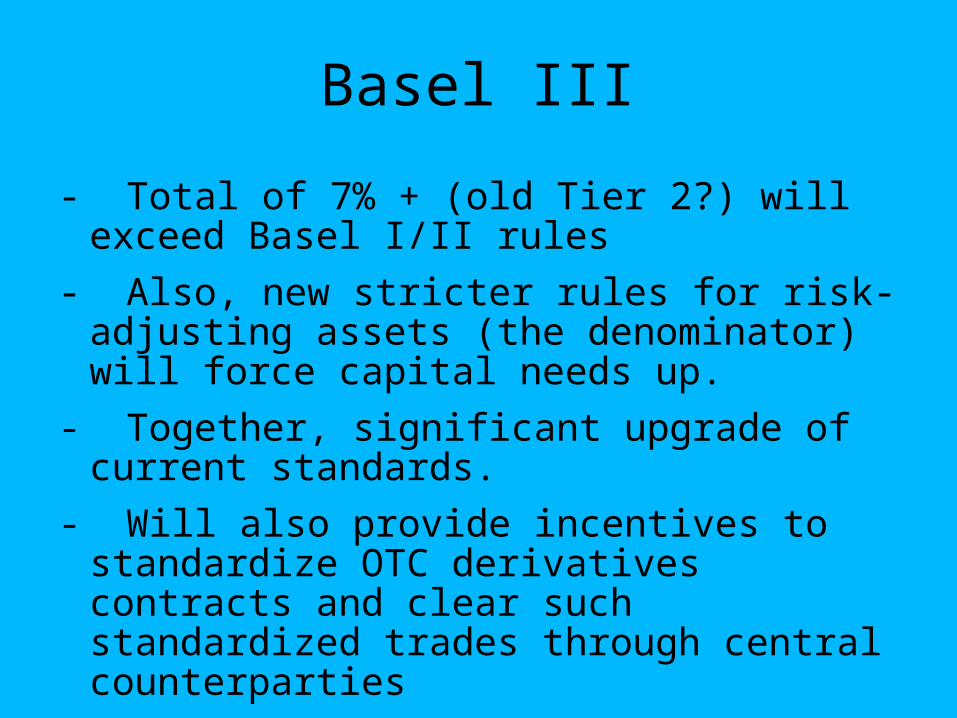

- Total of 7% + (old Tier 2?) will exceed Basel I/II rules

- Also, new stricter rules for risk-adjusting assets (the denominator) will force capital needs up.

- Together, significant upgrade of current standards.

- Will also provide incentives to standardize OTC derivatives contracts and clear such standardized trades through central counterparties

Dodd-Frank Act 2010

Well over 2000 pages Gave to Fed most authority = to at least 250

projects associated with implementing the act, including 50 rulemakings and sets of formal guidelines

Lots of coordination with lots of other USG agencies over the next few years

Overlays the existing regulatory structure Will generates tens of thousands of pages of

new rules

Dodd-Frank Act 2010

Designed to address not just the safety and soundness of each individual firm

But also the overall stability of the financial system and economy – the macroprudential approach

“The crisis demonstrated that a too narrow focus on the safety and soundness of individual firms can result in a failure to detect and thwart emerging threats to' financial stability that cut across many firms.” Bernanke

Federal Reserve Reforms Problems?

Implementation Financial innovations Moral Hazard Political pressures Integrate with extra-national rules and

regulations

25

The Global Steel Industry

26

Topics

• Globalization drivers - review

• The steelmaking process

• U.S. steel industry background and analysis

• The global steel industry today

• The road ahead

27

The Steel Making Process - I

28

The Steel Making Process - II

29

The Steel Making Process - III

30

Question: How to Measure the Health of the Industry?

• Employment

• Gross production

• Prices

• Net shipments

• Value added

• Industry profitability

• Share of global exports

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20090

50

100

150

T housands

T otal E m ployees P roduction workers

U S S teel Industry E m plo yees(Januar y)

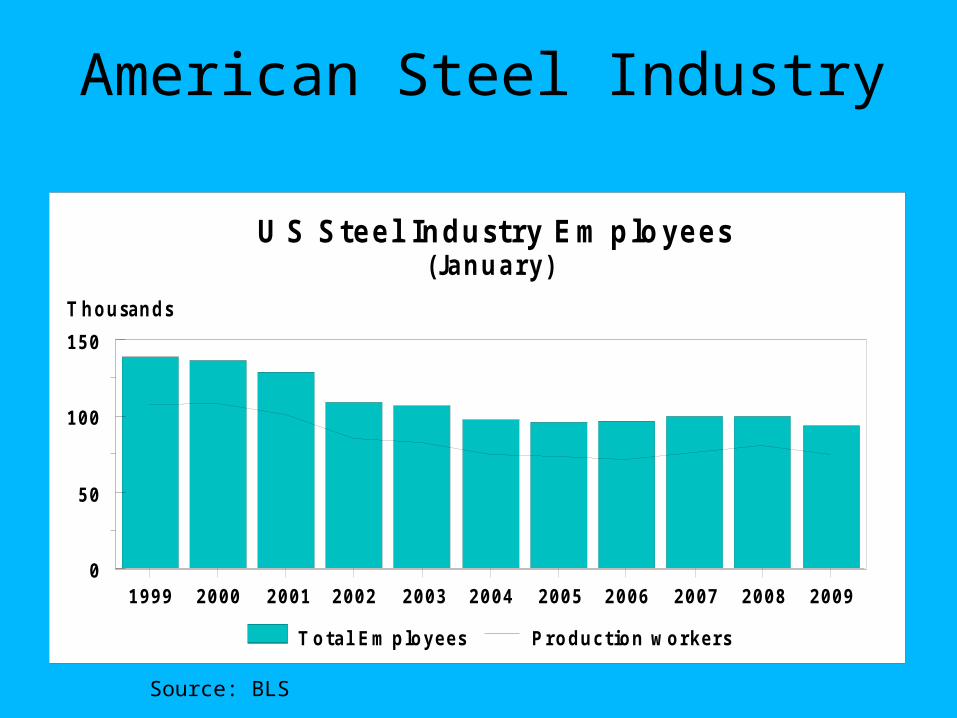

American Steel Industry

Source: BLS

US Steel Industry Employment by

Occupation

Source: World Steel Association: Fact sheet 2008

33

American Steel Industry

Source: US ITA: Steel Industry Executive Summary February 2012

Share of Global Steel Production

Source: US ITA: Steel Industry Executive Summary February 2012

2001 2002 2003 2004 2005 2006 2007 2008

X-Axis

0

2

4

6

8

10

12

14

Millions

W o rld Canada Ch ina

US E xports of S teel Mill P roductsQ uantity in Metric T ons

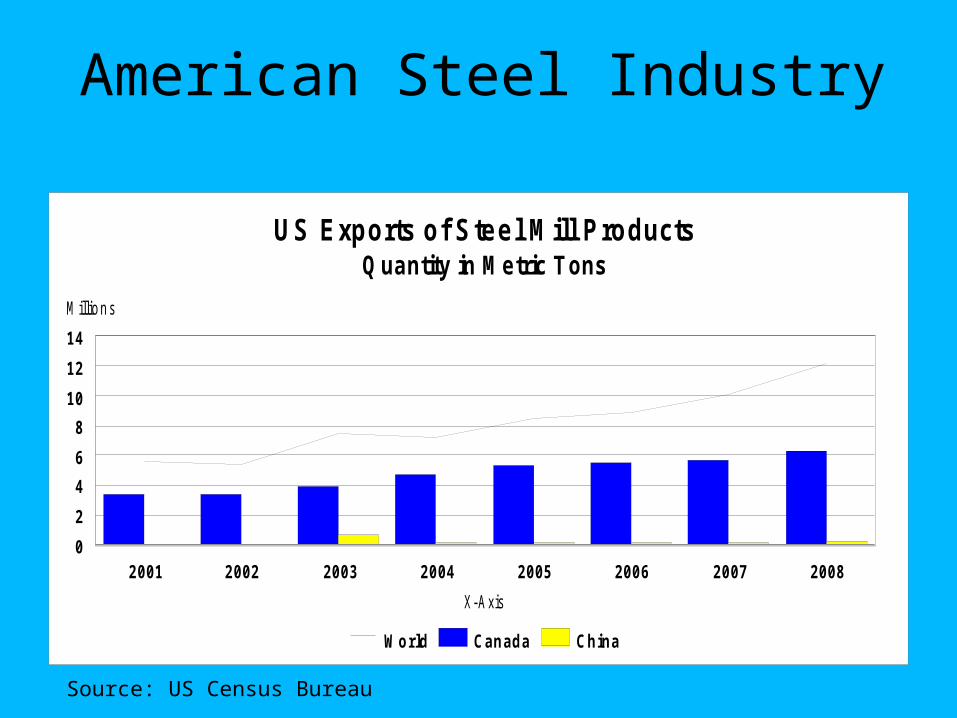

American Steel Industry

Source: US Census Bureau

2001 2002 2003 2004 2005 2006 2007 2008

X-Axis

$0

$5

$10

$15

$20

Billions of US dollars

W ORLDCANADA

MEXICO CHINA INDIA

U S Exports o f Steel Mill ProductsBy Valu e

American Steel Industry

Source: US Census Bureau

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20080

10

20

30

40

Billions US $

0

20

40

60

80

100

Millions metric tons

Qu an tity (rig h t scale) Valu e

U S S teel Im ports

American Steel Industry

Source: US Census Bureau

39

Steel Plants 1978:BOF and EAF Operating Capacity

EAF Capacity BOF Capacity

BOF 97.6EAF 20.3 117.9

million tonsper year

Source: Steel Plant Database

Copyright 2003, University of Pittsburgh

40

EAF Capacity BOF Capacity

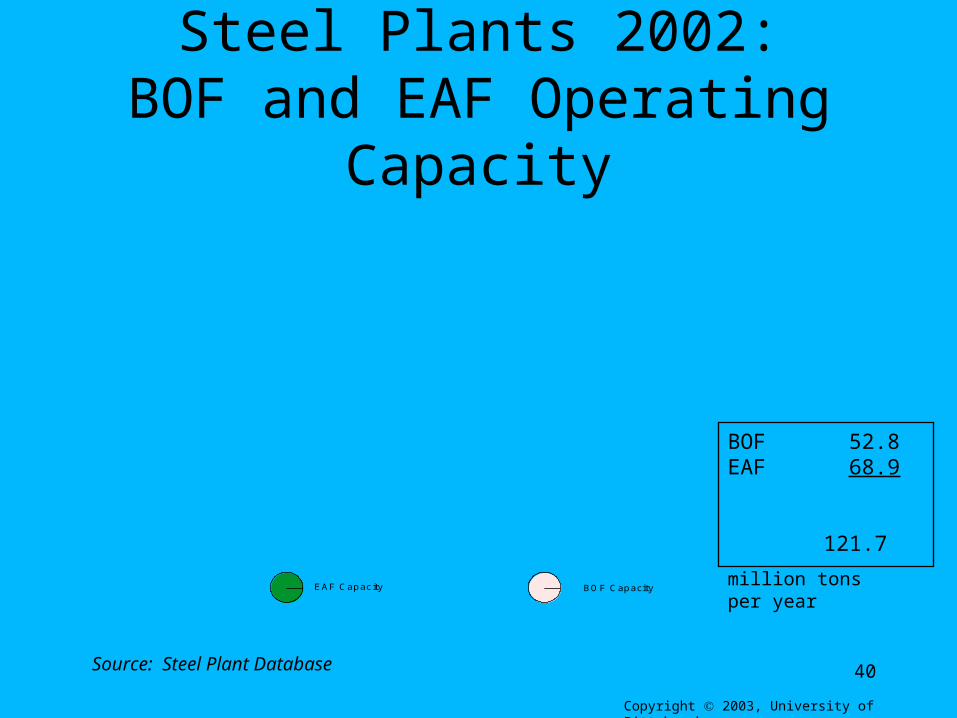

BOF 52.8EAF 68.9 121.7

million tonsper year

Source: Steel Plant Database

Copyright 2003, University of Pittsburgh

Steel Plants 2002:BOF and EAF Operating Capacity

41

U.S. Management Mindsets:1950-1980

• Taylorism: “scientific management”

• Economies of scale: bigger is better

• Vertical integration

• Ignore the Japanese

42

Emergence of Japanese Competition for US: 1970s+

• Underestimating the Japanese

• Misreading customers’ sensitivity to price v. availability

• Mismanaging technology: “followers”

43

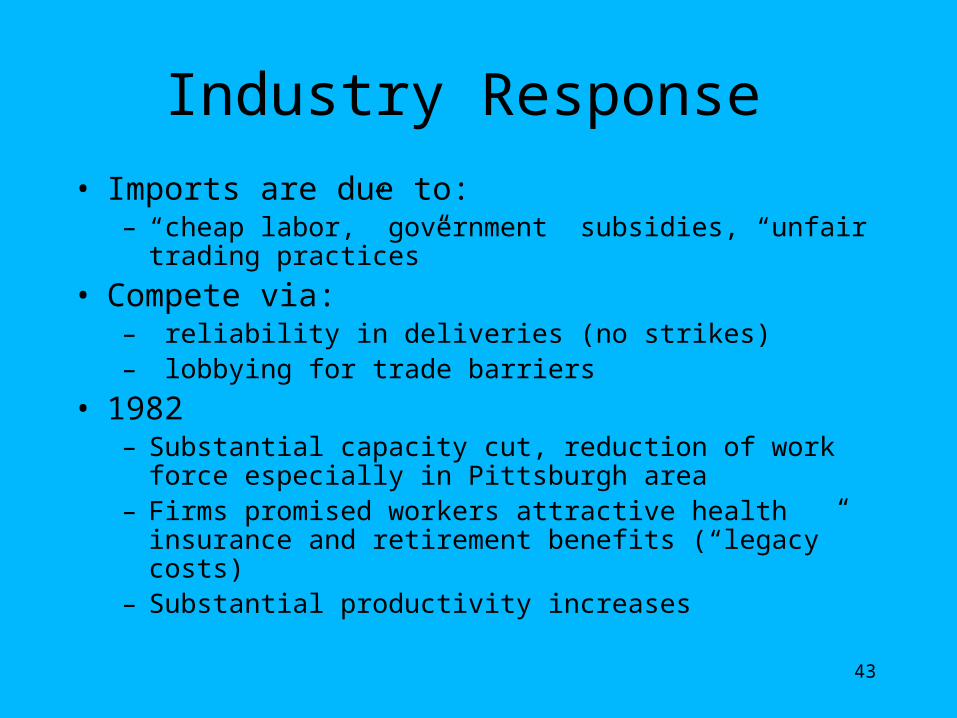

Industry Response

• Imports are due to: – “cheap labor,” government subsidies, “unfair trading

practices”

• Compete via:– reliability in deliveries (no strikes)– lobbying for trade barriers

• 1982– Substantial capacity cut, reduction of work force especially in

Pittsburgh area– Firms promised workers attractive health insurance and

retirement benefits (“legacy” costs)– Substantial productivity increases

44

Emergence of Global Competition

1980s:• Japanese establish leadership• Others (Korea, Taiwan) follow Japanese

model• European Union forces industry-

rationalization1990s:• Collapse of Soviet Union brings

Russian/Ukrainian producers into world market

45

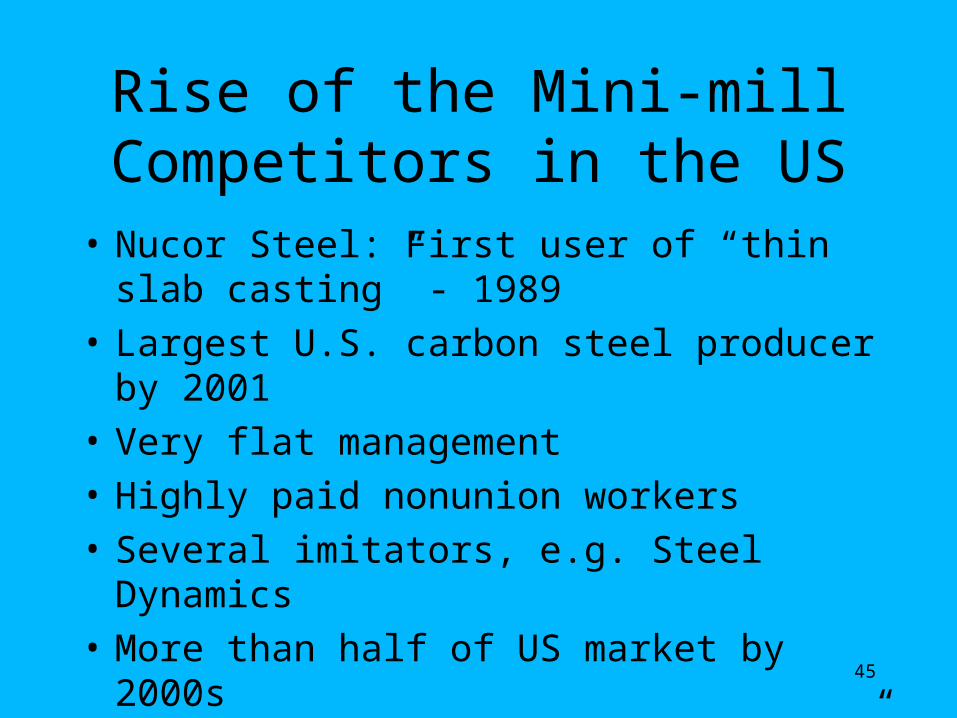

Rise of the Mini-mill Competitors in the US

• Nucor Steel: First user of “thin slab casting” - 1989

• Largest U.S. carbon steel producer by 2001• Very flat management• Highly paid nonunion workers• Several imitators, e.g. Steel Dynamics• More than half of US market by 2000s• Not competitive in very “high end” products

46

State of Industry Today

• Continuous technological change in the presence of competition driving costs down

• Consolidation of industry within countries– In U.S.: U.S. Steel, ISG/Mittal and Nucor

• Emergence of multinational steel companies– Mittal/Arcelor– Tata/Corus– U.S. Steel (Slovakia, Serbia)

47

State of Industry (cont)

• Reduction in U.S. capacity at older producers, frequently via bankruptcies and Wilbur Ross/Mittal

• Temporary tariffs 2002-2003 helped process of consolidation

• Substantial reduction in company “legacy” costs– $8.2 billion in steelworker pension liabilities

assumed by federal government– USW retirees’ health benefits cut

• Substantial investment by foreign companies in U.S.

48

State of Industry (cont)

• Severstal acquisition of Oregon Steel for $2.3 billion (11/06); Sparrows Point with 3.6 million tons capacity (5/08); Wheeling-Pittsburgh (9/08)

• US Steel acquisition of Lone Star Steel for $2.3 billion (3/07)

• IPSCO acquired by Svensk Stal for $7.7 billion (5/07)

• Thyssen building 4.0 million ton $3.4 billion integrated works in Alabama (5/07)– will use imported slabs from Brazil

• U.S. Steel rebuild of Clairton Cokeworks on hold

Import Rules for the American Steel Industry

• “Steel Import Monitoring and Analysis System” under US Commerce Department

• Created in 2003 along with the imposition of tariffs on foreign steel imports

• US based companies must obtain a license and report in detail all imports of foreign steel

• System was extended in March 2009 for four years to 2013

• Likely will be made permanent

The World Steel Industry

50

Carbon Steel Price Index

(USD/Tonne)

52

Global Steel Industry Production

Source: US ITA: Steel Industry Executive Summary February 2012

53

Global Steel Production by Major Producers

Source: US ITA: Steel Industry Executive Summary February 2012

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20080%

20%

40%

60%

80%

100%

Percent of Total

US China All Asia

Share o f W orld Production

World Steel Industry

Source: World Steel Association

55

World Crude Steel Production

World Steel Association

World Steel Production 2008

Source: World Steel Association

China

EU

Japan

US

Russia

India

South Korea

Germany

Ukraine

Brazil

Italy

Turkey

Taiwan

France

Spain

Mexico

Canada

UK

Belgium

Poland

Iran

0 100 200 300 400 500 600

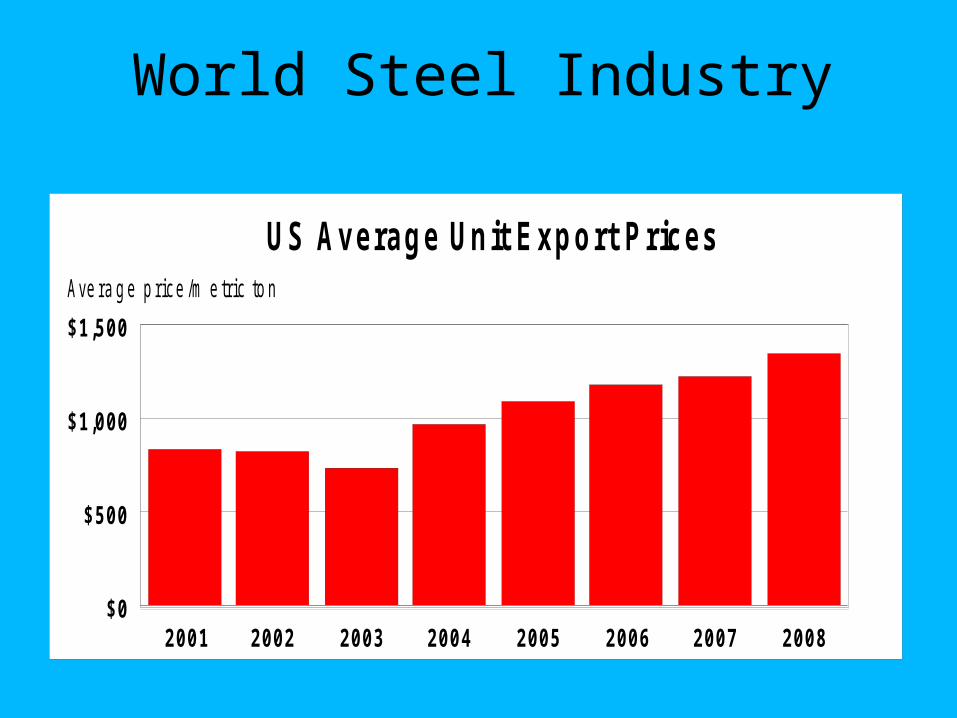

2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8$ 0

$ 5 0 0

$ 1 ,0 0 0

$ 1 ,5 0 0

Ave ra g e p rice /m e tric to n

U S A v e r a g e U n it E x p o r t P r ic e s

World Steel Industry

58

Global Concentration Ratios

59

Industry Concentration Ratios

60

Continuous Adjustment Ahead

• Global vertical specialization in production facilities

• Continued consolidation of companies

• A three sector steel industry?

61

Global Vertical Specialization

“Relying on subsidiaries or suppliers in different countries at each stage of adding value to take advantage of each country’s strengths.”Facilitated by low or nonexistence tariffs and reliable and low cost:

• Transportation• Telecommunications

62

Global Vertical Specialization

• Example: cell phones: – Design end products in Sweden (Ericsson)

or Finland (Nokia)– Design key components (e.g. chips) in U.S.– Produce key components in Taiwan/Korea– Assemble them in China – Distribute them in the U.S. – Provide technical assistance for customers

out of India

63

A Three Sector Industry?

• Integrated producers: ore to hot metal in coke-fired furnaces to finished steel (“automobile grade”)

• “Minimill” producers: scrap/reduced ore in electric furnaces to finished steel

• “De-integrated model:” Why ship ore and coal instead of slabs across oceans?

– Transportation costs v. Customer service/collaboration

– Roll imported slabs/bars into products for near-by customers

– India, Russia, Ukraine, Brazil as slab providers

64

Summary

• Global recession likely to accelerate the final stages of completing a long-delayed consolidation/globalization of the steel industry worldwide

• China becoming a major factor in global markets – depends on domestic demand

• The global organization of production and processing relative to customer location remains in flux due to energy cost trends and environmental considerations

Arcelor Mittal: #1 ProducerDutch/British/US/World . . .

65

66

Top 15 Global Steel Producers 2007

(By million metric tons of crude steel)

Source: World Steel Association

68

Steel Industry Employment(1,000 Workers)

Source: Bureau of Labor Statistics

BLS forecasts a 25% drop

69

LEADING EXPORTERS/IMPORTERS2006

World Steel Association

70

Brazilian Player

71

American Steel Industry

Related Documents