5/22/2014 1 © Huron Consulting Group Inc. All Rights Reserved. Huron is a management consulting firm and not a CPA firm, and does not provide attest services, audits, or other engagements in accordance with the AICPA's Statements on Auditing Standards. Huron is not a law firm; it does not offer, and is not authorized to provide, legal advice or counseling in any jurisdiction. YOUR MISSION | OUR SOLUTIONS Federal Grants Compliance 101 June 4, 2014 Agenda • Introduction to Research Compliance • Regulations Governing Sponsored Awards • Compliance Focus Topics: • Direct Charging Practices – Service/Recharge Centers • Effort Reporting • Cost Sharing • Cost Transfers • Financial Management and Monitoring • Other Regulatory Topics (Non-Financial) • Best Practices for Compliance Programs 2 TODAY’S SESSION WILL INCLUDE THE FOLLOWING TOPICS….

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

5/22/2014

1

© Huron Consulting Group Inc. All Rights Reserved.Huron is a management consulting firm and not a CPA firm, and does not provide attest services, audits, or other engagements in accordance with the AICPA's Statements on Auditing Standards.

Huron is not a law firm; it does not offer, and is not authorized to provide, legal advice or counseling in any jurisdiction.

YOUR MISSION | OUR SOLUTIONS

Federal Grants Compliance 101June 4, 2014

Agenda

• Introduction to Research Compliance

• Regulations Governing Sponsored Awards

• Compliance Focus Topics:• Direct Charging Practices

– Service/Recharge Centers

• Effort Reporting

• Cost Sharing

• Cost Transfers

• Financial Management and Monitoring

• Other Regulatory Topics (Non-Financial)

• Best Practices for Compliance Programs2

TODAY’S SESSION WILL INCLUDE THE FOLLOWING TOPICS….

5/22/2014

2

Introduction to Research Compliance

Introduction to Research CompliancePERSPECTIVE ON THE CURRENT INDUSTRY LANDSCAPE

• The research administration environment grows increasingly complex with changing regulations, inconsistencies among agencies, lack of information (meaningful and timely reports), thus generating more risk than institutions recognize.

• There remains a vast disconnect between:• The award environment, during which the funding agency and the PI focus

primarily on the research itself

• The degree of flexibility that is perceived to exist while the research is being conducted

• The audit environment when an award is closed and subsequent audits take place

• Current environment will likely place increased emphasis on accountability during a time when many institutions are faced with significant financial pressures and pressures to reduce staff.

5/22/2014

3

Introduction to Research ComplianceCOMPLEXITY VIA DIVERSITY

Complexity is found in research and fiscal areas and in the diversity of constituents:

• Genomics• Stem cell research• Clinical trials• Technology transfer• Faculty owned start-ups• University equity interests• Conflict of interest• International collaborations• Interdisciplinary research• Subcontracts• Human subject protections• Electronic payment• Grants.gov• Cost accounting standards

• Investigators, research assistants, staff, technicians

• Students, grad students, parents of students

• Board members, taxpayers• Federal agencies, external auditors• Suppliers, donors, corporate sponsors,

investors• Human subjects, advocacy groups

(PETA, etc.)• University administration, college and

departmental administration

Research & Fiscal Areas Constituents

Introduction to Research ComplianceREGULATORY ENVIRONMENT

Results of audits and investigations include:• In the first half of FY 2009, financial penalties resulting from audits of sponsored

research totaled:• $274.8 million in audit receivables

• $2.2 billion in investigative receivables

• In the last decade the number of annual criminal convictions of individuals or entities that engaged in improper compliance activities nearly quadrupled, to:

• 222 criminal convictions (6 months of FY09)

• Additionally, there were 239 civil actions

• False claims/whistleblower (qui tam) suits allow an individual who knows about a person or entity submitting false claims to bring a suit on behalf of the government

• The individual may receive a portion (15-30%) of the damages recovered

:

5/22/2014

4

Introduction to Research ComplianceCONSEQUENCES OF NON-COMPLIANCE

• Exceptional status of awards

• Suspension/termination of award

• Special terms and conditions of award

• Greatly reduced flexibility in the management of federally provided resources

• Negative publicity

• Large financial settlements

• Audit findings

• Disallowance of costs

• Significant difficulty negotiating F&A rates

• Extrapolation to additional grants

Introduction to Research ComplianceSETTLEMENT LANDSCAPE

5/22/2014

5

Trends related to research compliance at universities include:

• Volume of activity

• Complexity

• Scrutiny

• Demand for accountability

• Large investments in facilities

• Pressure to maintain/reduce administrative cost

Introduction to Research ComplianceTRENDS IN FUNDING AND COMPLIANCE

The Perfect Storm

Introduction to Research ComplianceAREAS OF CURRENT COMPLIANCE EMPHASIS

• Cost transfers• Clinical trial billing• Cost sharing• Direct charging practices• Effort reporting• Financial reporting• Program income reporting• Recharge centers• Subrecipient monitoring• Unallowable costs

• Animal subject protections (IACUC)• Human subject protections (IRB)• Biosafety (IBC)• Conflicts of interest• Environmental health & safety• Export controls• Invention disclosure & reporting• International agreements• Data management• Scientific overlap• Scientific misconduct• Other support

Financial Technical/Research

BOLD topics will be covered in more depth, but first…

Key areas of federal compliance focus:

5/22/2014

6

Regulations Governing Sponsored Awards

Regulations Governing Sponsored AwardsOFFICE OF MANAGEMENT AND BUDGET (OMB)

• OMB's predominant mission is to assist the President in overseeing the preparation of the federal budget and to supervise its administration in Executive Branch agencies. In helping to formulate the President's spending plans, OMB evaluates the effectiveness of agency programs, policies, and procedures, assesses competing funding demands among agencies, and sets funding priorities. OMB ensures that agency reports, rules, testimony, and proposed legislation are consistent with the President's Budget and with Administration policies.

• In addition, OMB oversees and coordinates the Administration's procurement, financial management, information, and regulatory policies. In each of these areas, OMB's role is to help improve administrative management, to develop better performance measures and coordinating mechanisms, and to reduce any unnecessary burdens on the public.

5/22/2014

7

Regulations Governing Sponsored AwardsOMB CIRCULARS

• The OMB Circulars provide guidance for research institutions to administer, audit and charge federally funded sponsored programs.

OMB Circular Regulation Purpose

A-110 (Uniform Administrative Requirements for Grants and Agreements With Institutions of Higher Education, Hospitals, and Other Non-Profit Organizations)

• Obtain consistency and uniformity among Federal agencies in the administration of grants to and agreements with institutions of higher education, hospitals, and other non-profit organizations.

A-21 (Cost Principles for Educational Institutions)A-122 (Cost Principles for Non-Profit Institutions)A-87 (Cost Principles for State, Local, and Indian Tribal Governments)

• Provide principles for determining the costs applicable to research and development, training, and other sponsored work performed entitesunder grants, contracts, and other agreements with the Federal Government.

A-133 (Audits of States, Local Governments, and Non-Profit Organizations)

• Obtain consistency and uniformity among Federal agencies for the audit of non-Federal entities expending Federal awards

Regulations Governing Sponsored AwardsOMB CIRCULAR A-110

• This Circular sets forth standards for obtaining consistency and uniformity among Federal agencies in the administration of grants to and agreements with institutions of higher education, hospitals, and other non-profit organizations.

• Subpart A - General

• Subpart B – Preaward Requirements (forms for application, special award conditions, etc.)

• Subpart C – Postaward Requirements (financial management, cost sharing, allowable costs, period of availability of funds, etc.)

• Subpart D – After the Award Requirements

http://www.whitehouse.gov/omb/circulars/a110/a110.html

5/22/2014

8

Regulations Governing Sponsored AwardsOMB CIRCULARS A-21, A-122, A-87

• These Circulars establish principles for determining costs applicable to grants, contracts, and other agreements for the specific type of recipient entities

• Defines the financial framework for administering Federally sponsored research

• Describes the basis for calculating facilities and administrative (“F&A” or indirect) costs

• Provides a reference section for determining how to charge specific, common costs

http://www.whitehouse.gov/omb/circulars/a021/a021.html

http://www.whitehouse.gov/omb/circulars_a122_2004

http://www.whitehouse.gov/omb/circulars_a087_2004

Regulations Governing Sponsored Awards45 CFR APPENDIX E (OASC-3)

• Though not a circular, this regulation establishes principles for determining costs applicable to research and development under grants and contracts with hospitals

• Defines the financial framework for administering Federally sponsored research, specifically at hospitals

• Provides the same types of information includes in the related Circulars

• OASC-3 remains in effect even with the Uniform Guidance

http://www.gpo.gov/fdsys/granule/CFR-2010-title45-vol1/CFR-2010-title45-vol1-part74-appE/content-detail.html

5/22/2014

9

Regulations Governing Sponsored AwardsOMB CIRCULAR A-133

• This Circular sets forth standards for obtaining consistency and uniformity among Federal agencies for the audit of States, local governments, and non-profit organizations expending Federal awards

• Who is required to have an audit conducted?

• Who is exempt from having an audit conducted?

• What is the frequency?

• Must comply with GAGAS (Generally Accepted Government Auditing Standards)

• Must comply with GAAP (Generally Accepted Accounting Principles)

• Must comply with regulations stated in OMB Circulars (e.g. A21, A122, A110)

http://www.whitehouse.gov/omb/circulars/a133/a133.html

Regulations Governing Sponsored AwardsOMB CIRCULAR A-133

Audits of States, Local Governments, and Non-Profit Organizations

• Applies to non-Federal entities that expend $500,000 or more in a year in Federal awards

• Required annually (or biennial in specific cases) and usually conducted with an institution’s Financial Statement audit

• Performed by an independent audit firm

• A-133 provides specific guidance to auditors – “Compliance Supplement”

http://www.whitehouse.gov/omb/circulars/a133/a133.html

5/22/2014

10

Regulations Governing Sponsored AwardsWHO ENSURES COMPLIANCE – A NATIONAL PRIORITY?

• An Office of Inspector General (OIG) is an entity created by Congress to be independent and act within each sponsoring governmental institution (NIH, NSF, etc.)

• The OIG within a sponsoring institution serves as an objective unit within the federal departments and agencies to review the administration of federal funds

• Primary OIG activities include:– Conducting an annual work-plan based on laws and regulations; specific

government concerns; significant management and performance challenges; and results of previous reviews

– Carrying out audits, evaluations, investigations, and legal activities

– Coordinating and recommending policies; prevents and detects fraud and abuse; keeps constituents informed about corrective actions

Regulations Governing Sponsored AwardsOTHER REGULATORY GUIDELINES

Federal Acquisition Regulations (FAR)

• The FAR was established to codify uniform policies for acquisition of supplies and services by agencies of the federal government.

• Website: http://www.acqnet.gov/far/

NIH Grants Policy Statement

• The National Institutes of Health Grants Policy Statement (NIHGPS) is intended to make available to NIH grantees, the policy requirements that serve as the terms and conditions of NIH grant awards.

• Website: http://grants.nih.gov/grants/policy/policy.htm#gps.

5/22/2014

11

Regulations Governing Sponsored AwardsOTHER REGULATORY GUIDELINES

NSF Grants Policy Manual

• The Grant Policy Manual (GPM) is a compilation of basic NSF policies and procedures for use by the grantee community and NSF staff. Its coverage includes the NSF award process, from issuance and administration of an award through closeout.

• Website: http://www.nsf.gov/pubs/manuals/gpm05_131/index.jsp

Regulations Governing Sponsored AwardsNEW! UNIFORM GUIDANCE

The OMB issued the Uniform Guidance in December 2013 to consolidate eight separate OMB circulars, each with its own unique rules and requirements, into a single regulation governing federal grants to IHEs, non-profits, and tribes.

The Uniform Guidance will go into effect at the end of 2014 includes:

• Current Language from Existing Circulars

• Revised Language Clarifying and Updating Current Requirements

• New Language Adding New Requirements

Reforms to Audit Requirements

• Merges and consistently aligns OMB Circular A‐133 and Circular A‐50.

Reforms to Cost Principles

• Merges and updates OMB cost principle Circulars A‐21, A‐87 and A‐122 and 45 CFR Part 75.

Reforms to Administrative Requirements

• Updates OMB Circulars A‐102, A‐110 and A‐89

5/22/2014

12

23

Section Regulation Requirement Institutional Impact

Section 200.204, 205, 207 (Merit and Risk)

• Merit and Risk must be Evaluated• Evaluation Criteria Must be Disclosed• Proposal Review Includes a Risk‐Based

Approach• Merit Based Selection vs. Eligibility Criteria

• Transparency in the award‐making process

Section 200.203 (Advanced Notice)

• Opportunities Must be Made Public• With Limited Exceptions, ALL Opportunities

Must be Open for 60 Days

• Requirement for 60‐day notice of funding opportunities

Section 200.203 (Standard Format)

• Standard Set of Data Elements• Agency Restriction on Additional Elements

• Standard format for announcements of funding opportunities

Section 200.210 (Standard Award Information)

Federal Awards MUST Include:• Award Information• General Terms and Conditions• Agency or Award Specific Terms and Conditions• ‘Performance Goals

• Provide a standard set of information in Federal Awards.

Regulations Governing Sponsored AwardsNEW! UNIFORM GUIDANCE: SUBPART C – PRE-AWARD REQUIREMENTS

24

Section Regulation Requirement Institutional Impact

Section 200.303 (Internal Controls)

• Non‐Federal Entities• Applicable Standards

• Establish and effectively utilize Internal Controls • Take prompt action when instances of

noncompliance are identified including noncompliance identified in audit findings.

Section 200.328 (Financial/Program Management)

• Agency Collection of Performance Data• Measurement of Performance• Institutional Accountability

Set standards for financial and program management.• Institutions are responsible for oversight.• Continue to use standard forms and tools.• Institutions will also be accountable to the federal

government to demonstrate responsible procurement and costing practices.

Section 200.306 (Cost Sharing)

• Voluntary Cost Sharing• Required Cost Sharing• Voluntary Committed Cost Sharing• Inclusion in Research Base for F&A Calculation

• Adds the OMB clarification in to Requirements• Does not include VUCS• Educate PI’s on the fact that cost sharing is not

required

Section 200.318‐322 (Procurement Standards)

• Federal Guidance Prevails• Small Purchase Threshold Changed to $150K• Avoidance of Unnecessary and Duplicative

Items• Procurement Methodologies

• P card and other small purchase guidelines should be reviewed based on the $3,000 federal limit

Section 200.331 (Sub recipient Monitoring)

• Financial and Performance Report Review• Pass‐Through Entity Management Decision• Pass‐Through Entity Follow‐up

• Institutions need to continue to emphasize accountability

• May be able to justify some administrative effort charged directly to awards

Regulations Governing Sponsored AwardsNEW! UNIFORM GUIDANCE: SUBPART D – POST-AWARD REQUIREMENTS

5/22/2014

13

25

Section Regulation Requirement Institutional Impact

Section 200.430 (Effort Reporting)

• High Standards for Internal Controls and Processes for Reviewing After‐The‐Fact Changes

• Consolidation of Standards for Documentation of Personnel Expenses

o Documented Policies and Procedureso Account for 100%o Cost Share

• Removal of Specific Guidance, References and Examples

• Effort reporting does not go away• Organization is the decision maker and doesn’t

have to follow the examples since they were removed

• Greater flexibility on the implementation side, but applicable standards remain

Section 200.413 (Direct Charges)

• Direct vs. Indirect Determination• Administrative and Clerical Salaries• Elimination of Major Project Example

• Consistency is a foundational element• Institutions will need to have specific definitions• Move staff from indirect to direct cost

Section 200.453 (Computing Devices)

• Computers, Associated Supplies and Accessories

• Impact on Administrative Requirements for Acquisition Costs < $5,000

• Capitalization Threshold

An institutional policy may be needed• Doesn’t have to be solely dedicated to research• Need to make sure the charge is essential and

allocable • Need sponsor approval

Section 200.453 (Unused Supplies)

• Residual Inventory• Determination of Funds to be Returned to

Federal Government

• Less than $5,000 can be kept

Section 200.XXX (Cost Studies)

• Operating Large Research Facilities• Elimination of Cost Studies Requirement

Reduction in administrative burden

Regulations Governing Sponsored AwardsNEW! UNIFORM GUIDANCE: SUBPART E – COST PRINCIPLES

26

Section Regulation Requirement Institutional Impact

Section 200.436 (Reimbursed Depreciation)

• Elimination of Restrictions on the Use of F&A Reduction in administrative burden associated with monitoring and accounting for depreciation or use allowances.

Section 200.449 (Lease/Purchase)

• Elimination of Lease/Purchase Analysis• ACO Notification

Reduction in administrative burden associated with undergoing the lease purchase analysis in order to justify the incurrence and charging of interest costs (as a direct or indirect charge) on federally sponsored programs..

Section 200.433 (Contingency Costs)

• Allowable When Causes are Indeterminable• Conditional Requirements

• Institutions may budget for contingency amounts in grantee proposed budgets and, if awarded, these amounts will be incorporated into the awarded amounts.

• Institutions must estimate these amounts using broadly‐accepted cost estimating methodologies and specify this practice in the budget documentation of the proposal.

Section 200.419 (Disclosure Statements)

• Change in DS‐2 Threshold• Streamlined Agency Review of Changes in

Accounting Practices

DS‐2 OIG strongly emphasized its importance of the DS‐2 so its importance may increase in the future

Section 200.414 (F&A Rate)

• Requirement to Accept Negotiated Rates• De minimis MTDC Rate• Four Year Extension• Sub Recipient F&A Rates

• De minimus rate will help small and new institutions• Automatic 4 year extension realities – does not apply

to hospitals and may not be a good strategy given the limitations

Regulations Governing Sponsored AwardsNEW! UNIFORM GUIDANCE: SUBPART E – COST PRINCIPLES

5/22/2014

14

27

Section Regulation Requirement Institutional Impact

Section 200.5XX • Single Audit Threshold Change• Designation of a Senior Accountable Official• Agency Cooperative Audit Resolution Practices• Internal Control/Material Weakness Emphasis• Timey Audit Reporting

Reduces the pool of audited entities and focuses audit attention on the highest risk areas of program oversight.

Appendix XI • Compliance Supplement• Future Updates

• No changes were made to the Compliance Supplement process at this time.

• Future changes to the Compliance Supplement may be made

Section 200.511 and 200.521

• Valid Reasons for No Further Action• Management Decisions• Expeditious Corrective Action

• Auditees must review and respond to and address all audit findings as quickly as possible, and not wait until audit reports are submitted.

Section 200.512 and 200.513

• Reliance on Federal Audit Clearinghouse• ACO Coordination• Pass‐Through Entity Verification

• Multiple agency audits and additional agency audits should be better coordinated and in line with each other.

• The requirements for subrecipient monitoring are substantively unchanged from existing guidance.

Regulations Governing Sponsored AwardsNEW! UNIFORM GUIDANCE: SUBPART F – AUDIT REQUIREMENTS

Compliance Focus:Direct Charging

5/22/2014

15

Compliance Focus: Direct ChargingLINK TO OMB CIRCULAR A-21, A-122, A-87: COST ACCOUNTING STANDARDS

The Cost Accounting Standards include four requirements:

• 501: Consistency in estimating, accumulating and reporting costs

• 502: Consistency in allocating costs incurred for the same purpose

• 505: Accounting for unallowable costs

• 506: Consistency in using the same cost accounting period

The CAS outline the framework for charging costs to federally sponsored projects. In order to be charged to a sponsored project, a cost must be:

• Reasonable

• Allowable

• Allocable

• Consistently Treated

Compliance Focus: Direct ChargingCOST ACCOUNTING STANDARDS: REASONABLE

A cost is reasonable if:

• The nature of the goods or services acquired or applied, and the amount involved therefore, reflect the action that a prudent person would have taken under the circumstances prevailing at the time the decision to incur the cost was made (OMB Circular A-21)

Considerations in determining reasonableness:

• Cost is necessary for the operation of the institution or performance of an award

• Cost is consistent with institutional policies

5/22/2014

16

Compliance Focus: Direct ChargingCOST ACCOUNTING STANDARDS: ALLOWABLE

A cost is allowable if:

• It conforms to any limitations or exclusions set forth in the regulations that govern the award (e.g. A-21, A-110, institution or system policies, etc.) or in the sponsored award.

Considerations in determining allowability:

• What is allowable per the notice of award or award document?

• What are the sponsor terms and conditions available via the website or other location?

• What are your institutional policies (e.g. travel policies)?

• How does cost-reimbursable versus fixed price (as in Clinical Trials) impact allowability?

Compliance Focus: Direct ChargingCOST ACCOUNTING STANDARDS: ALLOCABLE

A cost is allocable if:

• The goods or services involved are chargeable or assignable to such cost objectives in accordance with relative benefits received

• Incurred for the benefit of only one project or can be readily assigned to multiple projects which benefit from cost

Considerations in determining if the cost is allocability:

• It is incurred solely to advance the work under the sponsored award

• It benefits both the sponsored award and other work of the institution

• It is necessary to the overall operation

5/22/2014

17

Compliance Focus: Direct ChargingCOST ACCOUNTING STANDARDS: CONSISTENTLY TREATED

A cost is treated consistently if:

• The costs incurred for the same purpose, in like circumstances, are either direct costs only or F&A costs only with respect to final cost objectives. This assures that the same types of costs are not charged to awards both as direct costs AND as F&A costs.

Considerations in determining if the cost is consistently treated:

• How has this cost been classified on other sponsored awards?

• How was this cost classified when calculating our F&A rate?

• Is the an “unlike circumstance”?– “A sponsored project or activity, due to its size and nature, requires administrative

or clerical services, supplies, postage and/or telecommunications costs that are well beyond the core of departmental support routinely provided for departmental activities.”

Compliance Focus: Direct ChargingDIRECT OR INDIRECT COST?

–NO – Not allocable to a specific award.

–General research administrative cost.

–Charges are for copying of journal articles of general interest in the PI’s field.

–Scenario 2

Copying Charges

–YES – Able to be charged directly to the award.

–Unique to the scope of work.

–Charges are for copying and dissemination of research materials created as part of the scope of work on the award.

–Scenario 1

5/22/2014

18

Compliance Focus: Direct ChargingDIRECT OR INDIRECT COST?

–NO – Not allocable to a specific award.

–General research administrative cost.

–Typing of correspondence, journal articles, expense reimbursements, etc.

–Scenario 2

Administrative Support

–YES – Able to be charged directly to the award.

–Unique to the scope of work.

–A large volume of research data needs to be entered for a federal award.

–Scenario 1

Compliance Focus: Direct ChargingDIRECT OR INDIRECT COST?

–NO – Not allocable to a specific award.

–General research administrative cost.

–A software program (such as Microsoft Office) must be purchased in order to type technical reports.

–Scenario 2

Software Purchase

–YES – Able to be charged directly to the award.

–Unique to the scope of work.

–A specific software program must be purchased in order to develop and run analysis for a research project.

–Scenario 1

5/22/2014

19

Compliance Focus: Direct ChargingIMPACT OF THE UNIFORM GUIDANCE

Major Impact Area: Clerical and Administrative Salaries

• OLD: Generally considered indirect costs – previously allowed as direct charges only when the project fit the definition of a “major project”

• NEW: – There are no further references in “major projects”

– Administrative and clerical salaries, as well as other items of cost, can be charged directly to a federal award when it is appropriate, allocable and meets the conditions outlined in the federal guidance.

– These costs must be included in the original budget or institutions must have prior approval for rebudgeting for these costs

Compliance Focus: Direct ChargingIMPACT OF THE UNIFORM GUIDANCE

Major Impact Area: Computing Devices (computers, laptops, software)

• OLD: Generally considered indirect costs – as allocability of these major purchases was difficult to assign with a high degree of accuracy

• NEW: – Computing devices are now considered “supplies” and can be allocated directly to

sponsored awards as long as consistent, supported allocation methodologies are used

5/22/2014

20

Compliance Focus: Direct ChargingWHAT IS A SERVICE/RECHARGE CENTER (2 TYPES)

Definition: Specialized Service Facilities (SSF):

• Animal facilities

• Linear accelerators

• Magnetic centers

• Cell sorters

• Flow cytometers

• Air testing labs

- Material costs must be directly charged based on actual service usage and established rates- If the costs of the SSF are immaterial, they may be allocated as indirect costs

Compliance Focus: Direct ChargingWHAT IS A SERVICE/RECHARGE CENTER (2 TYPES)

Definition: Recharge Centers:

• Institution Wide: Non-SSF centers that are operated by the institution to provide support internal and external to the institution, including:– Telecommunications

– Copy centers

– Publication services

– Mail services

– Facility repair and maintenance services

• Department Wide: Centers operating within an academic division or department to provide support to the division or department activities. Copy center– Mail services

– Electrical shops

– Mechanical shops or Equipment fabrication facilities

5/22/2014

21

Compliance Focus: Direct ChargingSERVICE/RECHARGE CENTERS: MAJOR COMPLIANCE CONSIDERATIONS

• Rates should recover no more than the cost of the good or service

• Rates must break-even over time

• Rates don’t discriminate between users

• Note that you can still charge less to non-federal users but must ensure that federal users are not subsidizing or paying more than actual cost

• Surplus from service center shouldn’t be used to fund unrelated activities

• Rates may include depreciation expense only, not the full cost of equipment

• Depreciation included in SC rates can’t also be in the F&A rate

Compliance Focus:Effort Reporting

5/22/2014

22

Compliance Focus: Effort ReportingWHAT IS EFFORT?

Definition: Effort is the proportion of time spent on any activity and expressed as a percentage of the total professional activity for which an individual is employed by the institution.

Effort must be:

• A reasonable estimate

• Equal 100%

• Not based on a 40 hour week

Compliance Focus: Effort ReportingWHY IS EFFORT IMPORTANT?

Effort reporting provides support for salary charged to sponsored programs:

• Labor expenses represent ~2/3 of direct research costs

• Salary expense is often the first area reviewed by auditors

• Reports document that effort commitments have been met

• Reports supports both salary charging and salary cost sharing

Salary is charged to sponsored projects based on an estimate of how effort will be expended. Effort reports are used to document how effort was actually expended in order to verify that charges are appropriate

• Alternative = timecards (!)

5/22/2014

23

Compliance Focus: Effort ReportingEFFORT VERSUS PAYROLL

Effort reports often present total percentages of payroll distributions across sources (sponsored projects and non-sponsored funds) to be used as a starting point.

• It is often assumed that payroll distribution is monitored and revised based on effort expended/changes to workplans.

• Payroll percentages should be in line with dedicated effort and may need to be revised based on actual expended effort.

The new Uniform Guidance has some important impacts on effort reporting requirements – the terms

“effort reporting” and “certification” are not used.

Compliance Focus: Effort ReportingIMPACT OF THE UNIFORM GUIDANCE

The Uniform Guidance moves away from prescriptive effort reporting procedures.

• No specific requirements for activity reports or personnel action forms

• No specific rules regarding effort reporting frequency

• No guidance on who may document (certify?) compensation costs

Institutions have flexibility to implement appropriate internal to document/support compensation costs.

Wait and see…. How will auditors review internal controls?

5/22/2014

24

Compliance Focus: Effort ReportingMAJOR COMPLIANCE CONSIDERATIONS

Managing Commitments:

• Investigators and other research personnel commit effort during the proposal stage

• Commitment of an individual’s effort must be < 100% – Cost share included

• Total distribution of effort dedicated to all institutional activities for an individual must not be greater than 100%– Cost share included

• 100%, or nearly 100% research effort, is not realistically possible for individuals with significant non-research obligations to the institution – (administrative, clinical or teaching)

• Key personnel must request prior approval to reduce their effort on sponsored programs by more than 25%

Compliance Focus: Effort ReportingMAJOR COMPLIANCE CONSIDERATIONS

100% Effort:

• Effort reporting is not based on a standard work week for faculty and exempt staff– The hours will vary from individual to individual

• Effort should be consistent with the expectations of the individual’s institutional appointment(s)

• Effort should include “all compensated activities” – no “unpaid” hours

• Be consistent in considering effort during proposal and effort reporting

5/22/2014

25

Compliance Focus: Effort ReportingMAJOR COMPLIANCE CONSIDERATIONS

Institutional Base Salary (IBS):

• Definition: The annual compensation paid by an institution for an employee's appointment, whether that individual's time is spent on research, teaching, patient care, or other activities. The base salary excludes any income that an individual is permitted to earn outside of duties for the applicant/grantee organization.

• IBS should not change as the number of grants a PI has increases or decreases.

• Payments that may or may not be considered IBS:– Additional appointments (Department chair; formal committee members)

– Temporary additional responsibilities (e.g., teaching additional classes)

– Consulting (internal, external)

Compliance Focus: Effort ReportingMAJOR COMPLIANCE CONSIDERATIONS

Summer Effort and Summer Salary:

• Charges for summer sponsored research activities must be consistent with the level of effort provided during that time period.

• It is not compliant for an individual who is absent from research for a substantial period of the summer session (vacation?) to charge full salary to sponsored research and report 100% research activity on effort reports.

• NSF Regulations: Limits salary compensation for senior project personnel to no more than two months of their regular salary in any one year (regardless of summer vs. academic year)

5/22/2014

26

Compliance Focus: Effort ReportingMAJOR COMPLIANCE CONSIDERATIONS

Salary Cap:

• NIH and certain other sponsors limit the salary that can be charged on awards– NIH cap assumes a 12-month, full-time commitment, so if the appointment is

anything less, need to pro-rate the applicable cap

– Other caps – NIH K award

• Cap must be considered when charging salary

• Cap cost sharing needs to be reflected on the effort report

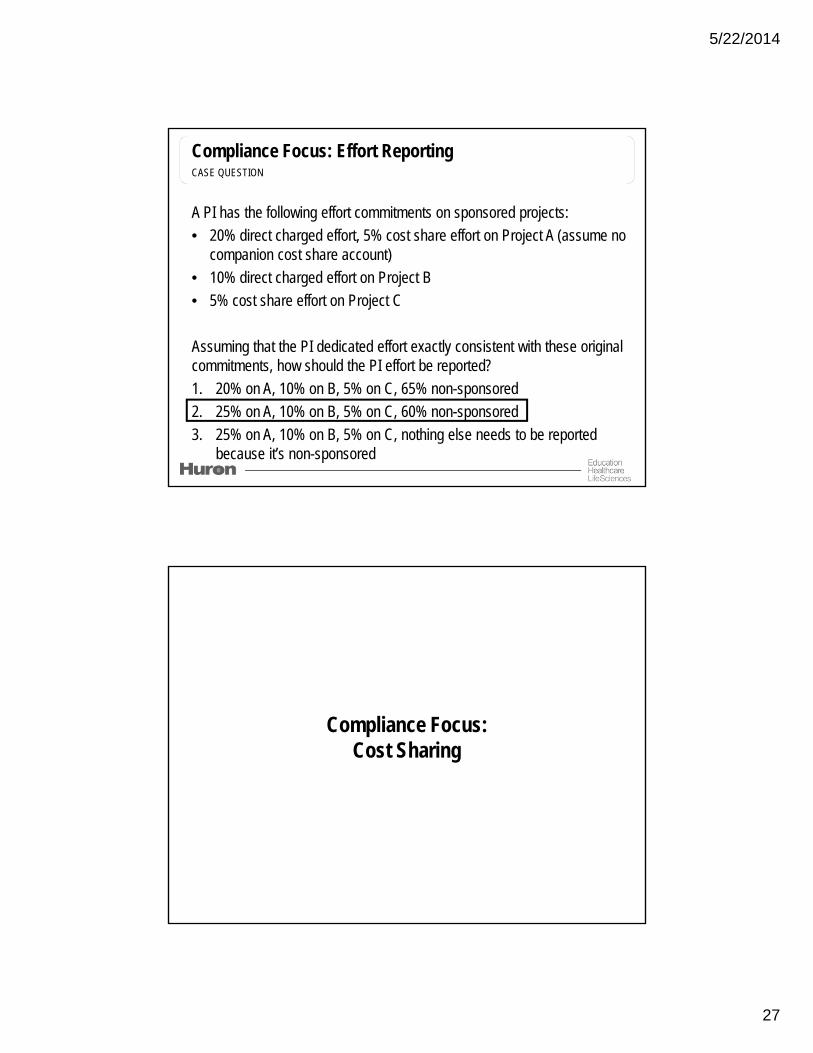

Compliance Focus: Effort ReportingCASE QUESTION

A PI has the following effort commitments on sponsored projects:

• 20% effort charged, 5% effort cost shared on Project A (assume no companion cost share account)

• 10% effort charged on Project B

• 5% effort cost shared on Project C

Assuming that effort ends up being consistent with commitments, how should the effort be reported?

1. 20% on A, 10% on B, 5% on C, 65% non-sponsored

2. 25% on A, 10% on B, 5% on C, 60% non-sponsored

3. 25% on A, 10% on B, 5% on C, nothing else needs to be reported because it’s non-sponsored

5/22/2014

27

Compliance Focus: Effort ReportingCASE QUESTION

A PI has the following effort commitments on sponsored projects:

• 20% direct charged effort, 5% cost share effort on Project A (assume no companion cost share account)

• 10% direct charged effort on Project B

• 5% cost share effort on Project C

Assuming that the PI dedicated effort exactly consistent with these original commitments, how should the PI effort be reported?

1. 20% on A, 10% on B, 5% on C, 65% non-sponsored

2. 25% on A, 10% on B, 5% on C, 60% non-sponsored

3. 25% on A, 10% on B, 5% on C, nothing else needs to be reported because it’s non-sponsored

Compliance Focus:Cost Sharing

5/22/2014

28

Compliance Focus: Cost SharingWHAT IS COST SHARING?

Total Project Costs

Sponsor Paid Costs

Shared Costs

Recipient Org. Cost Share

Third Party Cost

Share

Compliance Focus: Cost SharingTYPES OF COST SHARING

Definition: The portion of project costs not born by the sponsor. These costs are either born by the institution or potentially a third party.

Cost Share Type Definition

Matching Matching is generally used to refer to a statutorily specified percentage of program or project costs that must be contributed by a grantee in order to be eligible for Federal funding.

Mandatory Cost share based on sponsor stipulations that cost sharing or matching funds are required as a condition of receiving an award.

Voluntary Cost share offer by an institution in a proposal when the sponsor does not stipulate that cost sharing is required but the grantee incurs costs (e.g. additional effort, supplies) not reimbursed by the sponsor.• Voluntary Committed• Voluntary Uncommitted (VUCS)

5/22/2014

29

Compliance Focus: Cost SharingTYPES OF COST SHARING

Voluntary Uncommitted Cost Sharing (VUCS):

• Costs of the project are quantified in the project proposal (including the budget narrative) but not included in the costs to be borne by the sponsor

• Cost Share is committed 9and this commitment must be met) when that proposal is accepted by the sponsor

• VUCS must be documented and accounted for just like mandatory cost sharing.

Compliance Focus: Cost SharingCOST SHARE REQUIREMENTS

A-110 (Current):

• Provided for in the budget when required by the federal agency

• Conforms to other A-110 provisions

• May include un-recovered F&A, with agency approval

• Verifiable from institutional records

• Not included as a contribution for any other federally assisted program

• Costs considered cost share must be allowable under the cost principles, and necessary and reasonable to accomplish program objectives

• Not paid under another federal award (except where authorized by statute)

5/22/2014

30

Compliance Focus: Cost SharingIMPACT OF THE UNIFORM GUIDANCE

Uniform Guidance (Upcoming):

• Only to be considered in making an award decision if a requirement and the assessment/evaluation criteria is outlined in the funding announcement

• Required only in special circumstances and when approved by sponsor agency leadership

Compliance Focus: Cost SharingMAJOR COMPLIANCE CONSIDERATIONS

Salary Cap:

• While not referred to as “cost share,” the salary cap, in fact, imposes cost share

• Example:– PI annual salary is $300,000; if salary cap is $199,700, difference is $100,300

– PI budgets 15% effort to the project

– Budget shows salary to grant at $29,955 for PI salary (15%)

– PI certifies 15% effort to the project

– Cost share is $15,045 ($100,300 x 15%)

• As cost share, salary over the cap is included in the F&A base

5/22/2014

31

Compliance Focus: Cost SharingMAJOR COMPLIANCE CONSIDERATIONS

Equipment Cost Share:

• Institution receives donated equipment to be used as cost share Fair Market Value of the equipment at time of donation is $80,000

• Equipment has a useful life of 10 years

• Institution may claim $8,000/yr as cost share

Waived Indirect Costs:

• Sponsor requires $25,000 in cost sharing as an eligibility criteria for submission of an application with a $100,000 direct cost cap

• The institution wants to match using the F&A cost rate

• Institution (current F&A rate of 50%) proposes to charge F&A at 25% to the sponsor

• Unrecovered F&A results in $25,000 cost sharing

Compliance Focus: Cost SharingCASE STUDY EXERCISE

Example:

• PI annual salary is $120,000

• PI proposes (commits) 50% effort to project

• Budget shows PI salary to grant at $30,000

• Charged 25% but PI certifies 50% to the project

• $120,000 x 50% = $60,000

• Less paid from grant = ($30,000)

• Cost Share = $30,000 or 25%

5/22/2014

32

Compliance Focus:Cost Transfers

Compliance Focus: Cost TransfersWHAT IS A COST TRANSFER?

Definition: A cost transfer is an after-the-fact reallocation of an expense, either salary or non-salary costs, associated with a sponsored program after the expense was initially charged to another sponsored program or non-sponsored program

Cost transfer requirements:

• Timely

• Supported

• Reasonable

• Allocable

• Allowable

5/22/2014

33

Compliance Focus: Cost TransfersWHAT IS A COST TRANSFER?

Cost transfer processes, for identified, processing review and approval must have adequate internal controls to enable monitoring.

Frequent, tardy, and inadequately supported transfers, particularly if they involve projects with

significant cost overruns or unexpended fund balances, raise serious questions about the

appropriateness of the transfers and the overall reliability of the university's accounting system and

internal controls.

Compliance Focus: Cost TransfersCOST TRANSFER EXAMPLES

• Differences between certified effort (%) and salary charged (%) may require a redistribution of payroll (cost transfer)– Important to ensure that a review and follow-up procedure occurs at your institution

• Correction of an error of mis-keying the account number when providing a sponsored fund to be charged

• Recategorization of a charge from one expenditure type to another

Under no circumstances may a Cost Transfer be made with the sole intent of using up the unexpended

balance in a federal award account

5/22/2014

34

Compliance Focus: Cost TransfersCOST TRANSFER REQUIREMENTS

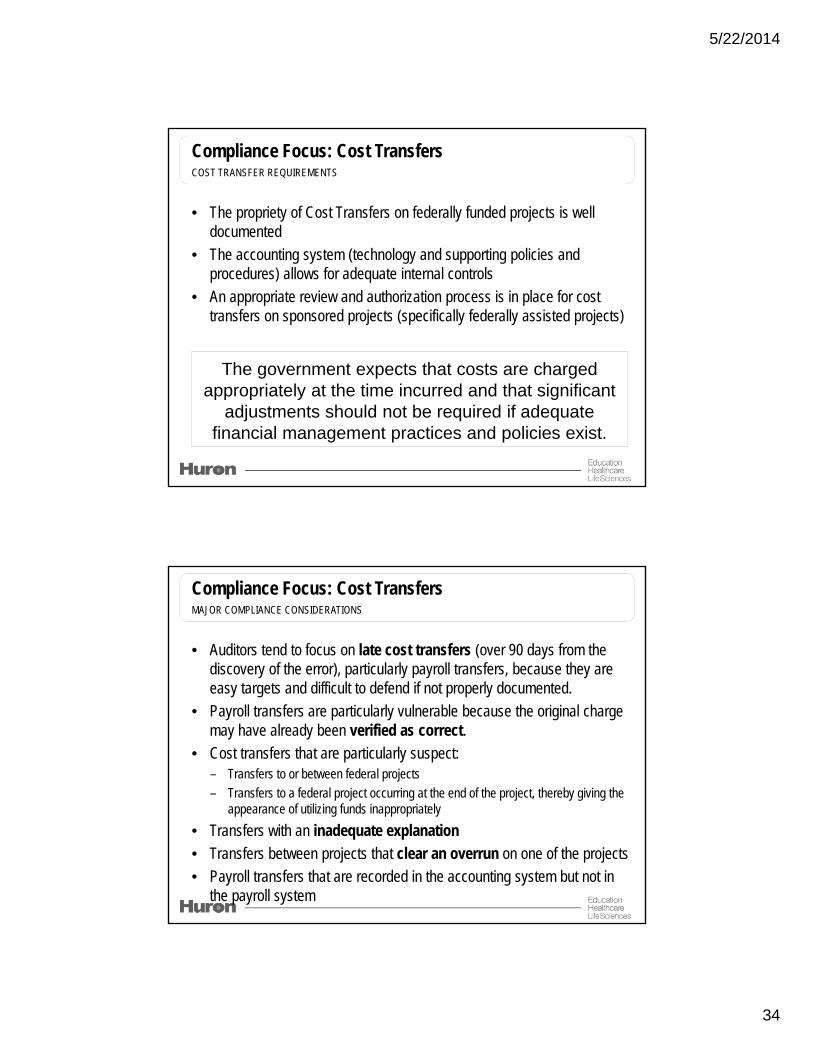

• The propriety of Cost Transfers on federally funded projects is well documented

• The accounting system (technology and supporting policies and procedures) allows for adequate internal controls

• An appropriate review and authorization process is in place for cost transfers on sponsored projects (specifically federally assisted projects)

The government expects that costs are charged appropriately at the time incurred and that significant

adjustments should not be required if adequate financial management practices and policies exist.

Compliance Focus: Cost TransfersMAJOR COMPLIANCE CONSIDERATIONS

• Auditors tend to focus on late cost transfers (over 90 days from the discovery of the error), particularly payroll transfers, because they are easy targets and difficult to defend if not properly documented.

• Payroll transfers are particularly vulnerable because the original charge may have already been verified as correct.

• Cost transfers that are particularly suspect:– Transfers to or between federal projects

– Transfers to a federal project occurring at the end of the project, thereby giving the appearance of utilizing funds inappropriately

• Transfers with an inadequate explanation

• Transfers between projects that clear an overrun on one of the projects

• Payroll transfers that are recorded in the accounting system but not in the payroll system

5/22/2014

35

Compliance Focus: Cost TransfersMAJOR COMPLIANCE CONSIDERATIONS: RED FLAGS

Despite being a compliance issue in and of itself, cost transfers are often the symptom for other post award compliance and management issues

Observed Activity Potential Root Issue

Frequent cost transfers at the start of projects, especially late cost transfers

Late award setups, “Parking” charges

Late or high volume of cost transfers coinciding with effort report due dates

Labor distributions not being monitored; Effort reports used to manage labor

High volume of cost transfers through the life of the award

Bad management of funds or accounting practices

High volume of cost transfers near the end of an award or after

Surpluses or shortfalls being transferred on or off of federal awards

Compliance Focus: Cost TransfersCASE STUDY EXERCISE: THE GOOD, THE BAD AND THE UGLY

Cost Transfer Request FormANY University

Section 2 – Justification for TransferSpecifically, explain why the expense(s) was not originally charged to the correct project.

Section 4 – CertificationI certify that the above-mentioned costs are appropriate charges to the project and project to which the costs are being transferred.

Dept Grants Admin Date

Section 3 – EXCEPTION – Late Cost Transfer RequestComplete this section in the space provided only if you are requesting the transfer of expenses older than 90 days.

Please transfer the $100 charge for lab equipment.

I incorrectly charged fund 12345 instead of 12354. This was a data-keying error that I noted once the month closed and

we reconciled our accounts.

Personnel CostsNon-Personnel Costs

Section 1 – Identification of Cost:

5/22/2014

36

Compliance Focus: Cost TransfersCASE STUDY EXERCISE: THE GOOD, THE BAD AND THE UGLY

Cost Transfer Request FormANY University

Section 2 – Justification for TransferSpecifically, explain why the expense(s) was not originally charged to the correct project.

Section 4 – CertificationI certify that the above-mentioned costs are appropriate charges to the project and project to which the costs are being transferred.

Dept Grants Admin Date

Section 3 – EXCEPTION – Late Cost Transfer RequestComplete this section in the space provided only if you are requesting the transfer of expenses older than 90 days.

Request for these expenditures on an overspent sponsored project to be

transferred to another sponsored project that still has an available balance.

Her sponsored project (fund 11111) overlapped a great deal with her other sponsored project (fund 22222) and so costs can justifiably be transferred to

fund 22222.

Personnel CostsNon-Personnel Costs

Section 1 – Identification of Cost:

Compliance Focus: Cost TransfersCASE STUDY EXERCISE: THE GOOD, THE BAD AND THE UGLY

Cost Transfer Request FormANY University

Section 2 – Justification for TransferSpecifically, explain why the expense(s) was not originally charged to the correct project.

Section 4 – CertificationI certify that the above-mentioned costs are appropriate charges to the project and project to which the costs are being transferred.

Dept Grants Admin Date

Section 3 – EXCEPTION – Late Cost Transfer RequestComplete this section in the space provided only if you are requesting the transfer of expenses older than 90 days.

Request for a cost transfer of revenue from an expired cost-reimbursable fund. Expenses had already been transferred

off the fund resulting in a cash surplus on the fund.

“I spoke with Joe this morning, and wanted to formally request that we move the balance of fund 12345 to the Dept.

Special Purpose Fund. It would allow us more flexibility in expending the funds if we could move them. Thanks for your

consideration.”

Personnel CostsNon-Personnel Costs

Section 1 – Identification of Cost:

5/22/2014

37

Compliance Focus:Financial Management and Monitoring

Compliance Focus: Financial Management and MonitoringFINANCIAL MANAGEMENT AND MONITORING TOPICS

Billions of federal dollars are awarded every year to institutions in the form of grants and contracts. Considering the level of (tax-payer!) dollars at stake – financial management is a key are of compliance focus.

Key topics related to the financial management and monitoring of sponsored projects include:

• Sponsored Project Billing

• Overdrafts

• Subrecipient Monitoring

• Financial Reporting

• Award Closeout

5/22/2014

38

Compliance Focus: Financial Management and MonitoringSPONSORED PROJECT BILLING

Sponsored projects can be billed via a variety of methods depending on the sponsor and the terms included in the award documents.

Billing Terms Method

Cost-Reimbursable Institution uses its own funds, incurs the expense and requests reimbursement from the sponsor only after disbursements have been made.• Letter of Credit: Reimbursement is requested and received via a “Draw Down.”• Non-Letter of Credit: Reimbursement is requested via an invoice.

Fixed Fee The institution will be paid a set amount for completion of the project, regardless of the cost incurred to do so.• Scheduled: Payments are made for a pre-established amount on a defined

timeline• Advance Payments: The full amount of the award if paid in full up-front

Milestone-Based The amount and timing of payments are based on technical milestones or deliverables throughout the life of the project (samples analyzed, patients enrolled, etc.)

Compliance Focus: Financial Management and MonitoringSPONSORED PROJECT BILLING: FEDERAL REGULATIONS

OMB Circular A-110 (and Uniform Guidance):

• Recipients are to be paid in advance, provided they maintain or demonstrate the willingness to maintain: (1) written procedures that minimize the time elapsing between the transfer of funds and disbursement by the recipient, and (2) financial management systems that meet the standards for fund control and accountability as established in Section.

• Reimbursement is the preferred method when the requirements in paragraph (b) cannot be met.

5/22/2014

39

Compliance Focus: Financial Management and MonitoringSPONSORED PROJECT BILLING: FEDERAL REGULATIONS

OMB Circular A-110 (and Uniform Guidance):

• Unless otherwise required by statute, Federal awarding agencies shall not withhold payments for proper charges made by recipients at any time during the project period unless (1) or (2) apply.– (1) A recipient has failed to comply with the project objectives, the terms and

conditions of the award, or Federal reporting requirements.

– (2) The recipient or subrecipient is delinquent in a debt to the United States.

Compliance Focus: Financial Management and MonitoringSPONSORED PROJECT BILLING: SPOTLIGHT ON LETTER OF CREDIT BILLING

LOC is the most common billing and payment method used by federal government sponsors.• The LOC mechanism is intended to minimize the time elapsing between

the transfer of funds from the Federal Government and disbursement by a grantee.

• LOC also minimizes the time between expenditure being incurred and when funds are transferred.

• Frequency of draws is usually determined by the institution.• Reimbursement should NOT be requested for:

– Charges that don’t meet the direct cost criteria (allowable, allocable, reasonable, consistent)

– Charges over the approved budget

– Charges outside of the approved budget period

– Charges incurred in advance of the receipt of the award document

5/22/2014

40

Compliance Focus: Financial Management and MonitoringSPONSORED PROJECT BILLING: SPOTLIGHT ON LETTER OF CREDIT BILLING

Best practices and requirements for managing the LOC Draw:• Ensure that the funds are fully disbursed within three business days of

receipt• Immediately returning all undisbursed Federal funds to the sponsor• Reconciling the amount drawn and cash on hand for each quarter by

completing the quarterly FFR (as required by certain sponsors)• Draw actual expenditures rather than relying on estimates

Compliance Focus: Financial Management and MonitoringSPONSORED PROJECT BILLING: SPOTLIGHT ON ADVANCED FEDERAL PAYMENTS

Requirements for advanced payments for federal awards:• Advance payments must be kept in an interest-bearing account.

– This practice mandated by sponsor agencies

– Interest earned should be returned to sponsor or applied against future expenses • Unspent funds are generally required to be returned to the federal

sponsor– Review the award documents to determine proper treatment

5/22/2014

41

Compliance Focus: Financial Management and MonitoringOVERDRAFTS: WHAT IS AN OVERDRAFT?

Definition: An overdraft occurs on a sponsored award when the expenditures, both direct and indirect, incurred by the PI exceed the authorized budget provided by the sponsor.

Some institutions use other terms:

• Account Deficit or Deficit Account

• Overspent Account

• Budget Overdraft

Compliance Focus: Financial Management and MonitoringOVERDRAFTS: ROOT CAUSES

Sponsored project overdrafts result from a variety of circumstances, many of which can be avoided:

• Delayed account set-up

• Subcontract execution delays

• Encumbrances or obligations are not considered.

• Projections not included in financial system

• Cycle time for payroll or non-payroll cost transfers

• No systematic control over recharge center charges that post to an account or fund automatically

• Lack of review of budget statements

• No consequences for lack of compliance

5/22/2014

42

Compliance Focus: Financial Management and MonitoringSUBRECIPIENT MONITORING: WHAT IS A SUBRECIPIENT, WHY ARE THEY MONITORED?

Definition: A subrecipient is “… a non-Federal entity that expends Federal awards received from a pass-through entity to carry out a Federal program, but does not include an individual that is a beneficiary of such a program. A subrecipient may also be a recipient of other Federal awards directly from a Federal awarding agency.”

Definition: Subrecipient Monitoring is the process of providing oversight on subawards throughout their lifecycle including:

• Obtaining the appropriate information prior to submitting the proposal Reviewing appropriateness of subawardee

• Executing an agreement consistent with A-133 requirements

• Acquiring signed A-133 certification statements (from other A-133 institutions)

Compliance Focus: Financial Management and MonitoringSUBRECIPIENT MONITORING: COMPLIANCE CONSIDERATIONS

Prime Awardees (Pass-Through Entities) are responsible for:

• Ensuring that federal funds are used for authorized purposes in accordance with laws, regulations and provisions of the prime recipient

• Ensuring that performance goals are met

• Monitoring the activities of the subrecipient to ensure compliance (e.g., request organization’s financial statement, documentation of expenditures invoiced, and/or limited scope audits)

• Ensuring that subrecipients expending $500K ($750 K under the Uniform Guidance) or more annually have met the audit requirements for that fiscal year (e.g. request audit certification)

• Issuing a management decision on audit findings within 6 months of receipt of the subrecipient’s audit report

5/22/2014

43

Compliance Focus: Financial Management and MonitoringSUBRECIPIENT MONITORING: COMPLIANCE CONSIDERATIONS (CONTINUED)

Prime Awardees (Pass-Through Entities) are responsible for:

• Ensuring that the subrecipient takes appropriate and timely corrective action

• Considering whether subrecipient audits necessitate adjustment of the pass-through entity’s own records

• Requiring each subrecipient to permit the pass-through entity and auditors to have access to records and financial statements as necessary

• On-going review and oversight are expected and may include:– Reviewing financial and performance reports

– Performing site visits to review information and observe operations

– Regularly communicating with the subawardee and conducting appropriate inquires

Compliance Focus: Financial Management and MonitoringSUBRECIPIENT MONITORING: COMPLIANCE CONSIDERATIONS (CONTINUED)

Prime Awardees (Pass-Through Entities) are responsible for:

• Federal Funding Accountability and Transparency Act (FFATA) reporting – when applicable– When the prime award qualified for FFATA reporting, the prime awardee must

report on data related to first-tier subgrants of $25,000 or more

– Report data via FSRS (FFATA Sub-award Reporting System)

5/22/2014

44

Compliance Focus: Financial Management and MonitoringSUBRECIPIENT MONITORING: IMPACT OF THE UNIFORM GUIDANCE

As updated in the new Uniform Guidance, Prime Awardees (Pass-Through Entities) are responsible for:

• Prime awardees are only required to monitor and follow-up on subrecipeint responses and corrective actions to audit findings that specifically relate to the subaward granted by the prime awardee

Compliance Focus: Financial Management and MonitoringFINANCIAL REPORTING: WHAT IS A FINANCIAL REPORT?

Definition: A financial report is a statement of expenditures for any individual award as required by the sponsor.

Financial reporting provides official documentation of the financial status of expenditures charged to the sponsored award, as required by the Notice of Award or sponsor regulations.

Recipients must ensure that the information submitted is:– Accurate

– Complete

– Consistent with the recipient’s accounting system

5/22/2014

45

Compliance Focus: Financial Management and MonitoringFINANCIAL REPORTING

Federal sponsors require a variety of financial report formats/frequenciesFederal Agency

Reporting Requirements

DHHS • The Federal Financial Report (FFR or SF-425) as the DHHS reporting format.• Quarterly/Semi-Annual interim reports are due 30 days after the end of each reporting

period. Annual/Final reports are due are due 90 days after the end of each reporting period.

• Quarterly cash reconciliation reports are submitted electronically on a quarterly basis.

NSF • NSF does not require grantees to submit final financial status reports for purposes of final grant accountability.

• However, final financial reporting information is extracted from the financial data provided as part of the LOD draw.

USDE • USDE requires financial reporting as a component of the Grant Performance Report (Ed 524B form).

• Annual reports should include expenditures for the entire previous budget period as well as the expenditures for the current reporting period.

• Final reports will include the above as well as expenditures through the entire project period. These reports are due within 90 days of the project period end.

• Must also provide an explanation if reported funds have not been drawn down from the G5 System and if funds have not been expended at expected rate.

90

Expanded Authorities Considerations

• Operating authorities provided to grantees that waive the requirement for prior approval for specified actions.

• EA Allows:– One-time One-Year No Cost Extension– Carryover of un-obligated balances without prior approval.

• Carryover of >25% Award should be justified to the sponsor

• EA Does Not Allow:– Change in scope of work– Significant re-budgeting (>25% of current year’s award)– Significant change in effort/status of PI– Change in grantee organization (transfers)

• The Federal Demonstration Partnership (FDP) is a cooperative effort among federal research agencies and universities aimed at streamlining and improving the federal/university research support relationship and reducing administrative burden on Principal Investigators. FDP members are eligible for Expanded Authorities (as are other institutions).

Compliance Focus: Financial Management and MonitoringFINANCIAL REPORTING: FEDERAL REGULATIONS

Expanded Authorities and the impact on financial reporting….

5/22/2014

46

91

Allowable

Financial reports must be filed in a timely manner!1. Reporting deadlines are specified in the award documents of a grant or

contract2. Due at the end of both the budget and project period within 90 days of

the expiration date of the award3. If more frequent reporting is required, the NOA will specify both the

frequency and due date

Include allowable activity supported by general ledger documentation

Follow requirements specified in the Notice of Grant Award

Timely

Award Reqmts

Compliance Focus: Financial Management and MonitoringFINANCIAL REPORTING: MAJOR COMPLIANCE CONSIDERATIONS

92

Allowable

Presence of & adherence to the institution’s policy requiring review and written approval

Documented reconciliation of the FSR must tie out to the G/L

Failure to submit complete, accurate, and timely reports may result in:1. Penalties or enforcement actions2. Closer monitoring by the sponsor3. Delayed sponsor payments4. New, Supplemental, and Continuation awards delayed5. Loss of administrative flexibility

Risks

Compliance Focus: Financial Management and MonitoringFINANCIAL REPORTING: MAJOR COMPLIANCE CONSIDERATIONS

Policy

Reconciled

5/22/2014

47

Compliance Focus: Financial Management and MonitoringAWARD CLOSEOUT: WHAT DOES IT MEAN?

In theory: The project has concluded and all required deliverables (financial and technical) have been submitted and the institutional account have been closed.

In practice:

• The Department and PI cease using the project/account number

• Transactions are no longer approved by units outside of the department

• The financial system blocks expenditures from posting to the project

Primary Objective: TOTAL EXPENDITURES = TOTAL BUDGET = TOTAL CASH

Compliance Focus: Financial Management and MonitoringAWARD CLOSEOUT: FEDERAL REGULATIONS

OMB A-110 (and Uniform Guidance):

• Submit all sponsor required reports and liquidate all obligations within 90 calendar days

• Refund any balances of unobligated cash that was paid by the sponsor

• Disclose information on any property acquired with funds or received from the sponsoring agency

5/22/2014

48

Compliance Focus: Financial Management and MonitoringAWARD CLOSEOUT: MAJOR COMPLIANCE CONSIDERATIONS

• Unallowable expenditures posted (and continue to post!) to the project that should have been removed

• Debits or credits posted that were not captured on the financial report or final invoice

• Sponsors may withhold incremental funding or final payments until all outstanding financial and progress or technical reports are received

• Awards not issued under FDP or Expanded Authorities could lose carryover funds

• Awards that are not closed out will continue to incur expenditures after funding is deobligated

• Indirect Costs, or F&A, may not calculate correctly in the financial system, which would prevent the institution from recovering all costs

Compliance Focus:Other Regulatory Topics

5/22/2014

49

Compliance Focus: Other Regulatory TopicsOTHER REGULATORY AND COMPLIANCE TOPICS

A variety of social issues, and concern for the broader well being also drives a focus on non-financial compliance and regulatory topics related to sponsored projects administration.

Additional compliance topics related to sponsored projects include:

• Human Subjects Research

• Animal Subjects Research

• Biosafety

• Conflict of Interest

Compliance Focus: Other Regulatory TopicsHUMAN SUBJECTS RESEARCH: WHAT IS A HUMAN SUBJECT?

DHHS Definition: A living individual about whom an investigator obtains data AND based on how the investigator gathers the data:

– The data about that individual are obtained through intervention or interaction with that individual.

OR

– The type of data gathered: The data are identifiable and private.

– Application to projects based on funding. Institutional decision as to whether to apply to non-federally funded studies.

5/22/2014

50

Compliance Focus: Other Regulatory TopicsHUMAN SUBJECTS RESEARCH: WHAT IS A HUMAN SUBJECT?

FDA Definition:

• Individual who gets a test article– Drugs, biologics, devices, food with a health claim, food additives, nutrients, infant

formula

• Individual who serves as a control– This research does not have to involve a test article

– Could be a comparison to another study involving a test article

• For medical device research: Human specimens– Specimens may be unidentified

– Specimens may be from deceased individuals

Does it matter which?

Compliance Focus: Other Regulatory TopicsHUMAN SUBJECTS RESEARCH: WHAT IS A HUMAN SUBJECT?

Why? What’s different?

• Activities subject to regulation

• Informed consent disclosures

• Waivers of consent

• Waivers of consent documentation

• Exemptions

• Reporting requirements

In Summary....There are multiple overlapping laws and to be compliant one needs to know which laws apply.

YES!

5/22/2014

51

Compliance Focus: Other Regulatory TopicsHUMAN SUBJECTS RESEARCH: INSTITUTIONAL REVIEW BOARDS

Universities that perform research on human subjects are required to obtain the review and approval of the university’s Institutional Review Board (IRB).

• Definition: The IRB is an administrative body established to protect the rights and welfare of human research subjects recruited to participate in research activities conducted under the auspices of the institution with which it is affiliated.

• The IRB approves the protocol, which is the outline or plan for use of an experimental procedure or experimental treatment. Review and approval must include all protocols involving humans, including externally and internally-funded research

Compliance Focus: Other Regulatory TopicsHUMAN SUBJECTS RESEARCH: OTHER MAJOR COMPLIANCE CONSIDERATIONS

• Protocols for continuing research not reviewed and approved at least once per year

• Quorum is not present at meetings

• Mandatory training for key research personnel not performed

• Protocols for externally or internally funded research involving human subjects not reviewed

• Documentation of IRB policies and procedures not sufficient

• Informed consent forms confusing or unused

• Meeting minutes incomplete

• Inadequate HIPAA compliance

• Inadequate consideration of special populations (children, prisoners)

5/22/2014

52

Compliance Focus: Other Regulatory TopicsHUMAN SUBJECTS RESEARCH: FEDERAL AWARD COMPLIANCE CONSIDERATIONS

• Costs incurred to conduct human subjects research, including:– Subject reimbursements

– Salaries/supplies for studies

are charged to federal awards when full approval has not been granted or when approval has lapsed.

• Human subjects research not originally identified in the project scope of work is conducted without obtaining prior approval for the change in scope.

Compliance Focus: Other Regulatory TopicsANIMAL SUBJECTS RESEARCH: WHAT IS AN ANIMAL SUBJECT?

Definition: Any live or dead dog, cat, nonhuman primate, guinea pig, hamster, rabbit, or any warmblooded animal used for research, teaching, testing, experimentation, or exhibition purposes, or as a pet.

• By definition, coldblooded species (amphibians and reptiles) are exempt from coverage under the Animal Welfare Act.

• Birds, rats, and mice bred for use in research

• Horses not used for research purposes

• Farm animals, including livestock and poultry, used or intended for use as food or fiber or in agricultural research

• Fish and Invertebrates (crustaceans, insects)

5/22/2014

53

Compliance Focus: Other Regulatory TopicsANIMAL SUBJECTS RESEARCH: MAJOR COMPLIANCE CONSIDERATIONS

• Protocols for continuing research not reviewed and approved when required

• Animal research taking place without protocol approval

• Documentation of IACUC policies and procedures not sufficient

• Animal charges not properly allocated to benefiting research projects

• Animal per diem rates not representative of the actual cost

Compliance Focus: Other Regulatory TopicsANIMAL SUBJECTS RESEARCH: INSTITUTIONAL ANIMAL CARE AND USE COMMITTEE

Universities that perform research on animal subjects are required to obtain the review and approval of the university’s Institutional Animal Care and Use Committee (IACUC).

Responsibilities of the IACUC include:

• Reviewing and approving protocols for the humane care and use of animals in research

• Inspecting the animal facilities and investigator laboratories semiannually

• Reporting findings and recommendations to the IO.

• Ensuring compliance with federal regulations

5/22/2014

54

Compliance Focus: Other Regulatory TopicsANIMAL SUBJECTS RESEARCH: FEDERAL AWARD COMPLIANCE CONSIDERATIONS

• Costs incurred to conduct animal subjects research, including:– Animal husbandry charges

– Animal purchases

– Salaries/supplies for studies

are charged to federal awards when full approval has not been granted or when approval has lapsed.

• Animal subjects research, or animal models (mice, rabbits, etc.) not originally identified in the project scope of work is conducted without obtaining prior approval for the change in scope.

• Charges for animal husbandry, studies or per diem charges are not tracked and allocated based on approved protocols and animal usage (Protocol to Account match).

Compliance Focus: Other Regulatory TopicsBIOSAFETY: WHAT IS BIOSAFETY? WHAT IS A BIOHAZARD?

• Biohazard Definition: An agent of biological origin that has the capacity to produce deleterious effects on humans, animals, plants and insects. – These include microorganisms, toxins and allergens derived from those organisms;

and allergens and toxins derived from insects, animals and plants.

• Biosafety Definition: Safety measures taken with respect to the effects of biological research on humans, animals, plants and the environment.

• Biosafety Level Definition: Description of the degree of physical containment being employed to confine organisms containing recombinant DNA molecules and to reduce the potential for exposure of laboratory workers, persons outside of the laboratory, and the environment.

5/22/2014

55

Compliance Focus: Other Regulatory TopicsBIOSAFETY: INSTITUTIONAL BIOSAFETY COMMITTEE

Institutional Biosafety Committee: An institutional committee created under the NIH Guidelines to review research involving recombinant DNA.

The IBC is responsible for:

• Reviewing rDNa research for completeness, consistency

• Suggesting changes to PI (as necessary)

• Performing biosafety audits

• Researching/documenting particular issues– i.e., 3rd generation retro-viral vectors

• Coordinate with IRB & IACUC

Compliance Focus: Other Regulatory TopicsCONFLICT OF INTEREST: WHAT IS A CONFLICT OF INTEREST?

Definition (pertaining to the design, conduct, or reporting of research):

• A situation in which financial or other considerations have the potential to compromise or bias professional judgment and objectivity

• Involves the use of authority for financial or other gain

• May involve both individuals and institutions

• Not a statement of wrongdoing

A conflict of interest is not inherently problematic. Each COI must be reviewed and managed appropriately by the institution and researcher.

5/22/2014

56

Compliance Focus: Other Regulatory TopicsCONFLICT OF INTEREST: WHAT IS A CONFLICT OF INTEREST?

An apparent or potential conflict of interest may develop into an actual conflict:

• Conflict of interest implies that there is a potential for COI, but it does not imply a likelihood

• Conflict of interest may exist regardless of whether decisions are driven by personal interest

• Conflict of interest is not misconduct in research

The institution, not the federal government or the sponsor, has the primary responsibility to develop its own internal policies and procedures.

Compliance Focus: Other Regulatory TopicsCONFLICT OF INTEREST: WHAT CAN HAVE A CONFLICT?

Individuals:

• Investigators (PI, Co-PI, Post-Docs, Students)

• Study Coordinators

• Research technicians, data analysts

• IRB members

• Anyone involved in technology transfer

• Anyone involved in procurement, education, healthcare

Institutions:

• Financial holdings of the institution

• Allocation of resources for research

5/22/2014

57

Compliance Focus: Other Regulatory TopicsCONFLICT OF INTEREST: MAJOR COMPLIANCE CONSIDERATIONS

• Institution does not have a conflict of interest policy or procedures

• Institution does not have effective procedures for reviewing the financial conflict of interest disclosures received from the investigators

• Institution does not properly maintain records of all financial disclosures and all actions taken by the Institution with respect to each conflicting interest for at least three years from the date of submission of final expenditures report

• Conflicts were not appropriately identified and communicated to the sponsor

• Conflicts were identified and communicated but were not properly managed

Compliance Focus: Other Regulatory TopicsCONFLICT OF INTEREST: FEDERAL AWARD COMPLIANCE CONSIDERATIONS

• Identification of “investigators” - individuals responsible for the design, conduct and reporting of research.

• Confirmed SFI disclosures on file prior to proposal submission (NIH).

• Reviewed SFI and fully managed COI prior to expenditure of federal funds (NIH).

• Made COI publically available through a website and/or upon request.

• Resolution of non-compliance issues and timely, accurate reporting of instances of non-compliance.

• Uniform Guidance will require agencies beyond NIH and NSF to develop COI policies – Stay Tuned!

5/22/2014

58

Best Practices for Compliance Programs

Best Practices for Compliance ProgramsMITIGATING RISK

Each of the topics we have been discussed is a top area of federal focus…

What can institutions do to minimize their risk in each of these areas and ensure they are doing everything they can to remain in compliance?

The right types of internal controls will help you and your institution mitigate risk.

5/22/2014

59

Best Practices for Compliance ProgramsBENEFITS OF AN EFFECTIVE COMPLIANCE PROGRAM

• A proactive approach to creating a compliance program will allow an institution to manage its compliance risk without imposing unnecessary constraints on the institution’s operations

• Strong compliance programs benefit research institutions by reducing the risk of significant non-compliance

• Compliance programs reduce the negative impact of having non-compliance discovered by regulators or funding agencies

• The accountability, clarity, and information requirements of a strong compliance program are often beneficial in terms of institutional management

Best Practices for Compliance ProgramsKEY ELEMENTS OF EFFECTIVE COMPLIANCE PROGRAMS

The DHHS Office of the Inspector General (OIG) identified the following eight elements considered as necessary for a comprehensive compliance program.

8 Elements How Institutions Should Respond

• Compliance Leadership: Designating a compliance officer and compliance oversight committees

• Policies and Procedures: Implementing written policies and procedures that foster an institutional commitment to stewardship and compliance

• Roles and Responsibilities: Defining roles and responsibilities across the institution and assigning oversight responsibility

• Training: Conducting effective training and education

• Adequate institutional and Board-level oversight of the compliance function

• Designation of a responsible institutional official with appropriate authority and expertise

• Explicit written policies, institutional codes of ethics and conduct

• Training programs supported by leadership

• Adoption of adequate procedures, resources, and systems to permit compliance

5/22/2014

60

Best Practices for Compliance ProgramsKEY ELEMENTS OF EFFECTIVE COMPLIANCE PROGRAMS (CONT.)

The DHHS Office of the Inspector General (OIG) identified the following eight elements considered as necessary for a comprehensive compliance program.

8 Elements How Institutions Should Respond

• Communication: Developing effective lines of communication

• Monitoring: Conducting internal monitoring, quality review, auditing, and assurance

• Enforcement: Enforcing standards through well-publicized disciplinary guidelines

• Corrective Response: Responding promptly to detected problems, undertaking corrective action, and reporting to the appropriate agencies

• Maintenance of a process to allow anonymous reporting of alleged non-compliance

• Protection of employees who file reports

• Regular monitoring and quality review audits to test compliance

• Mechanisms to enforce rules and discipline rule violators, take corrective action and communicate results

Best Practices for Compliance ProgramsBALANCING COMPLIANCE AND SERVICE

Not surprisingly, strong customer service (i.e. doing what a PI wants) can conflict with compliance requirements (institutional and sponsor based).

Research administrators are faced with a variety of challenges:

• Internal and external customers • Finding middle ground

• Little empowerment • Different points of view

• Institutional politics and culture • Vague language and grey areas in federal regulations