PPACA Update Seth Perre.a Principal Groom Law Group, Chartered

Feb 2015 ppaca webinar seth perretta

Jul 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PPACA Update

Seth Perre.a Principal Groom Law Group, Chartered

2

Today’s Discussion

• What employers should be thinking about in 2015: • Employer mandate and related tax reporJng compliance

• Employer exchange noJces

• PiKalls for small employers, including new rules related to defined contribuJon health

• Expected Supreme Court decision on ACA subsidies

• Future of the high-‐cost “Cadillac” excise tax • Current legislaJve acJvity related to health care

3

Employer Mandate Compliance • Does it apply to you?

• Did you have 50+ FT/FTEs in 2014? • If yes and 50-‐99 FT/FTEs, are you eligible for transiJon relief?

• If yes, do you qualify for non-‐calendar year transiJon relief?

4

• Does it apply to you? • Did you have 50+ FT/FTEs in 2014? • If yes and 50-‐99 FT/FTEs, are you eligible for transiJon relief?

• If yes, do you qualify for non-‐calendar year transiJon relief?

Employer Mandate Compliance

5

Employer Mandate Compliance

• Does it apply to you? • Did you have 50+ FT/FTEs in 2014? • If yes and 50-‐99 FT/FTEs, are you eligible for transiJon relief?

• If yes, do you qualify for non-‐calendar year transiJon relief?

6

Employer Mandate Compliance

• Does it apply to you? • Did you have 50+ FT/FTEs in 2014? • If yes and 50-‐99 FT/FTEs, are you eligible for transiJon relief?

• If yes, do you qualify for non-‐calendar year transiJon relief?

7

Employer Mandate Compliance

• If the employer mandate applies to you, have you taken the steps to be compliant as of 1/1/15? • Which compliance method are you using (i.e., monthly or look-‐back)?

• Have you determined which employees must be treated as a full-‐Jme employee?

• Have you offered qualifying coverage to your full-‐Jme employees?

8

Employer Mandate Compliance

• If the employer mandate applies to you, have you taken the steps to be compliant as of 1/1/15? • Which compliance method are you using (i.e., monthly or look-‐back)?

• Have you determined which employees must be treated as a full-‐Jme employee?

• Have you offered qualifying coverage to your full-‐Jme employees?

9

Employer Mandate Compliance

• If the employer mandate applies to you, have you taken the steps to be compliant as of 1/1/15? • Which compliance method are you using (i.e., monthly or look-‐back)?

• Have you determined which employees must be treated as a full-‐Jme employee?

• Have you offered qualifying coverage to your full-‐Jme employees?

10

Employer Mandate Compliance

• If the employer mandate applies to you, have you taken the steps to be compliant as of 1/1/15? • Which compliance method are you using (i.e., monthly or look-‐back)?

• Have you determined which employees must be treated as a full-‐Jme employee?

• Have you offered qualifying coverage to your full-‐Jme employees?

11

Employer Mandate Compliance

• Have you considered your short-‐term employees and determined whether they may qualify as bona fide seasonal employees? • Note: If have lots of bona fide seasonal employees, should probably use look-‐back versus monthly compliance method

12

Employer Mandate Compliance

• If you are using the look-‐back method, have you documented which posiJons you do not reasonably expect to work a full-‐Jme schedule? • Otherwise, you may lack records on audit necessary to show that you didn’t just fail to offer coverage to a full-‐Jme employee

13

Employer Mandate Compliance

• Don’t forget about the new tax reporJng requirements

1. Evidence of MEC Enrollment (applies to all employers of any size)

• If insured MEC, obligaJon runs to carrier

• If self-‐funded, obligaJon runs to plan sponsor

2. Evidence of employer mandate compliance (only applies to employers subject to employer mandate)

• Tax reporJng occurs in 1Q of 2015 with respect to the 2014 calendar year

• Make sure you are keeping track of all payroll and hours data, as well as benefit eligibility and offers of coverage in order to be able to fully tax report, as required, in 2015

14

Employer Exchange NoJces

• ACA requires state or federal exchanges to send employers a noJce indicaJng that one of their employees has been condiJonally approved for federally-‐provided premium tax credits (PTCs)

• NoJces put employers on noJce that they be liable in the future for an employer mandate “B” penalty.

• Employers are invited/encouraged to provide informaJon to exchange if the employee was offered affordable, minimum value coverage, or is enrolled in minimum essenJal coverage (regardless of affordability of minimum value)

• States such as CT and NV have begun sending out the noJces. Nothing yet from HHS for federal exchange

15

PiKalls for Small Employers x Don’t forget the controlled group when determining whether the employer mandate applies

x Don’t think there is an automaJc one-‐year delay from the employer mandate for employers with 50-‐99 FT/FTEs (because there isn’t one!!)

x Don’t forget about the small business tax credit (but note: may need to purchase coverage via the SHOP if want to claim credit)

x Don’t run afoul of new rules prohibiJng an employer from using tax-‐free dollars or taxable wages to reimburse an employee for his/her OOP medical expenses or individual premiums (unless also enrolled in employer-‐sponsored major med)

16

PiKalls for Small Employers x Don’t forget the controlled group when determining whether the employer mandate applies

x Don’t think there is an automaJc one-‐year delay from the employer mandate for employers with 50-‐99 FT/FTEs (because there isn’t one!!)

x Don’t forget about the small business tax credit (but note: may need to purchase coverage via the SHOP if want to claim credit)

x Don’t run afoul of new rules prohibiJng an employer from using tax-‐free dollars or taxable wages to reimburse an employee for his/her OOP medical expenses or individual premiums (unless also enrolled in employer-‐sponsored major med)

17

PiKalls for Small Employers x Don’t forget the controlled group when determining whether the employer mandate applies

x Don’t think there is an automaJc one-‐year delay from the employer mandate for employers with 50-‐99 FT/FTEs (because there isn’t one!!)

x Don’t forget about the small business tax credit (but note: may need to purchase coverage via the SHOP if want to claim credit)

x Don’t run afoul of new rules prohibiJng an employer from using tax-‐free dollars or taxable wages to reimburse an employee for his/her OOP medical expenses or individual premiums (unless also enrolled in employer-‐sponsored major med)

18

PiKalls for Small Employers x Don’t forget the controlled group when determining whether the employer mandate applies

x Don’t think there is an automaJc one-‐year delay from the employer mandate for employers with 50-‐99 FT/FTEs (because there isn’t one!!)

x Don’t forget about the small business tax credit (but note: may need to purchase coverage via the SHOP if want to claim credit)

x Don’t run afoul of new rules prohibiJng an employer from using tax-‐free dollars or taxable wages to reimburse an employee for his/her OOP medical expenses or individual premiums (unless also enrolled in employer-‐sponsored major med)

19

PiKalls for Small Employers x Don’t forget the controlled group when determining whether the employer mandate applies

x Don’t think there is an automaJc one-‐year delay from the employer mandate for employers with 50-‐99 FT/FTEs (because there isn’t one!!)

x Don’t forget about the small business tax credit (but note: may need to purchase coverage via the SHOP if want to claim credit)

x Don’t run afoul of new rules prohibiJng an employer from using tax-‐free dollars or taxable wages to reimburse an employee for his/her OOP medical expenses or individual premiums (unless also enrolled in employer-‐sponsored major med)

20

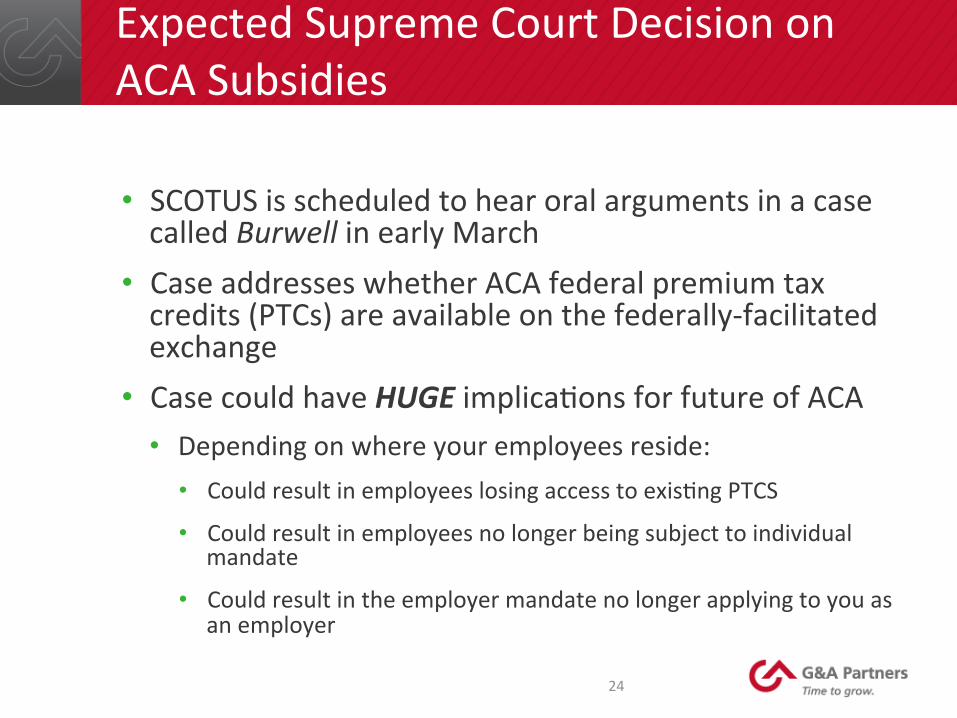

Expected Supreme Court Decision on ACA Subsidies

• SCOTUS is scheduled to hear oral arguments in a case called Burwell in early March

• Case addresses whether ACA federal premium tax credits (PTCs) are available on the federally-‐facilitated exchange

• Case could have HUGE implicaJons for future of ACA • Depending on where your employees reside:

• Could result in employees losing access to exisJng PTCS

• Could result in employees no longer being subject to individual mandate

• Could result in the employer mandate no longer applying to you as an employer

21

Expected Supreme Court Decision on ACA Subsidies

• SCOTUS is scheduled to hear oral arguments in a case called Burwell in early March

• Case addresses whether ACA federal premium tax credits (PTCs) are available on the federally-‐facilitated exchange

• Case could have HUGE implicaJons for future of ACA • Depending on where your employees reside:

• Could result in employees losing access to exisJng PTCS

• Could result in employees no longer being subject to individual mandate

• Could result in the employer mandate no longer applying to you as an employer

22

Expected Supreme Court Decision on ACA Subsidies

• SCOTUS is scheduled to hear oral arguments in a case called Burwell in early March

• Case addresses whether ACA federal premium tax credits (PTCs) are available on the federally-‐facilitated exchange

• Case could have HUGE implicaJons for future of ACA • Depending on where your employees reside:

• Could result in employees losing access to exisJng PTCS

• Could result in employees no longer being subject to individual mandate

• Could result in the employer mandate no longer applying to you as an employer

23

Expected Supreme Court Decision on ACA Subsidies

• SCOTUS is scheduled to hear oral arguments in a case called Burwell in early March

• Case addresses whether ACA federal premium tax credits (PTCs) are available on the federally-‐facilitated exchange

• Case could have HUGE implicaJons for future of ACA • Depending on where your employees reside:

• Could result in employees losing access to exisJng PTCs

• Could result in employees no longer being subject to individual mandate

• Could result in the employer mandate no longer applying to you as an employer

24

Expected Supreme Court Decision on ACA Subsidies

• SCOTUS is scheduled to hear oral arguments in a case called Burwell in early March

• Case addresses whether ACA federal premium tax credits (PTCs) are available on the federally-‐facilitated exchange

• Case could have HUGE implicaJons for future of ACA • Depending on where your employees reside:

• Could result in employees losing access to exisJng PTCS

• Could result in employees no longer being subject to individual mandate

• Could result in the employer mandate no longer applying to you as an employer

25

Future of the High-‐Cost “Cadillac” Excise Tax

• 40% nondeduc3ble excise tax • Doesn’t take effect unJl 2018. However, the tax is likely to affect the type

and extent of benefits that are offered by employers in 2018 • Applies on a per enrollee basis and looks at enrolled coverage

• If the coverage exceeds $10,200 for self-‐only coverage or $27,500 for other coverage, then any excess is subject to the tax (with limited adjustments for certain high-‐risk professions, age and gender)

• Also this excise tax and the employer mandate provisions appear to be on a collision course whereby employers may need to eventually choose which one to comply with

• Strange bedfellows – all stakeholders (employer groups, unions, elder rights groups, etc.) appear to want the tax repealed or modified

• Many open quesJons; no regulaJons issued yet; regulators are just now beginning the rulemaking process

• LegislaJve acJvity likely with respect to the tax – but when and will it make it into law?

26

Current and Expected LegislaJve AcJvity

• Republicans are likely to conJnue to introduce ACA repeal legislaJon

• Depending on Burwell outcome, Republicans (and maybe Democrats) may need to legislate to gap fill

• We will likely conJnue to see limited bi-‐parJsan acJvity on the margins • Medical device tax repeal

• Changes to full-‐Jme employee definiJon from 30-‐40 hours/week

• Cadillac tax changes? • Unclear/unlikely that any of this legislaJve acJvity will result in actual laws/changes to the benefit of employers and employees

QUESTIONS?

G&A Partners [email protected]

(800) 253-‐8562

*This webinar has been recorded and will be posted on the G&A website by Friday

Related Documents