Farebox and Bus Pass Revenues - Transit Division Follow-up Report March 5, 2015 Report No. 15-06 Office of County Auditor Evan A. Lukic, CPA County Auditor Exhibit 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Farebox and Bus Pass Revenues - Transit Division Follow-up Report

March 5, 2015 Report No. 15-06

Office of County Auditor Evan A. Lukic, CPA

County Auditor

Exhibit 1

Table of Contents Topic Page

Executive Summary ................................................................................1

Scope and Methodology ........................................................................2

Findings ...................................................................................................2

Recommendations ..................................................................................4

APPENDIX A

Executive Summary This report presents the results of our follow-up review of our Report 08-05, Review of Controls over Farebox and Bus Pass Revenues, dated March 3, 2008. The original objective of our current review was to report on the status of implementation of the recommendations in Report 08-05. However, our current review disclosed that although the Transit Division has taken steps to address some of the recommendations, significant deficiencies1 continue to exist in management controls over bus passes and cash handling activities. Because bus passes and cash are the two principal elements of Transit revenues, the continuing lack of controls are of the utmost concern. Therefore, we have limited the balance of this report to findings and recommendations relative to current observations of bus pass and cash handling activities. Current Findings:

• Basic controls over bus passes are inadequate due to lack of segregation of incompatible duties and failure to account for and reconcile bus pass inventory, purchases and sales.

• Controls at the Transit cash count rooms are inadequate due to limited supervision of count room operations, failure to establish and maintain basic controls over access to the count rooms and ineffective use of the surveillance camera system.

Given that the lack of controls greatly increase the potential for loss of revenues it is imperative that the Administration take immediate and appropriate steps to address the deficiencies over bus passes and cash handling. Therefore, we recommend the Board of County Commissioners direct the County Administrator, as a priority to:

1. Assign appropriate personnel to review cash handling practices and procedures across the entire Transit Division to ensure appropriate controls are in place and that the findings and recommendations from prior reviews have been completely addressed.

2. Provide the Board with a quarterly status update of recommendations in this report until fully implemented.

A copy of Report 08-05 is provided at Appendix A.

1 A significant deficiency is a deficiency, or a combination of deficiencies, in internal control important enough to merit attention by those charged with governance. Statement of Auditing Standards (SAS) No. 115

1

Scope and Methodology To accomplish our objective we:

• Requested a status update of the 18 recommendations from Report 08-05 as of October 1, 2013 from the Division’s management,

• Reviewed responses provided by management in November 2013, • Tested supporting documentation to confirm reported implementation status, • Interviewed staff at the Transit, Accounting, Records, Taxes and Treasury, and

Libraries Divisions, and • Observed current cash counting operations (including cameras and taped video

surveillance recordings) and bus pass sales processing at selected Transit sites in March and April 2014.

Findings Controls over bus passes and cash remain inadequate to prevent and detect losses In our report, Report 08-05, Review of Controls over Farebox and Bus Pass Revenues, we identified, among other things, significant control deficiencies over bus passes and cash handling. The report included eighteen recommendations. Our current review disclosed that although the Transit Division has taken steps to address some of the recommendations, significant deficiencies continue to exist in controls over bus passes and cash handling activities. Because bus passes and cash are the two principal elements of Transit revenues, the continuing lack of basic controls over bus passes and inadequate security over count rooms are of the utmost concern.

• Basic controls over bus passes are inadequate

o Employees with access to bus pass inventories performed the monthly and annual inventory counts2 and the Division did not perform periodic reconciliations of bus pass inventory counts to records and sales. Independent physical inventories and reconciliations are essential to ensure that all pass sales are being recorded.

o Bus pass sales at one location visited are processed without a cash register

or point of sale system and bus passes and cash are stored in an unlockable drawer. This site processes approximately $1.8 million in sales annually. Manual records are used to tally and reconcile sales to cash receipts. In addition, the location only accepts cash contrary to the County’s cash handling policy and customers are not provided receipts.

2 Bus pass inventories exceeded $13 million in March 2014

2

A cash register/point of sale system is essential to providing basic control over sales and cash receipts. A register can provide customers with receipts (a key control), improve accuracy over cash handling (automatically calculate change due), allow acceptance of debit/credit cards, and aid in shift closeout and reconciliation of sales to cash receipts.

o At another location we noted checks from retail bus pass vendors were not

immediately restrictively endorsed upon receipt, contrary to County policy. Instead, the checks are sent to the Bus Pass Administrative Coordinator for endorsement and processing. Failure to immediately endorse checks could result in undetected theft.

o There is a lack of segregation of duties over the sale and accounting for bus passes and transit fare passes to state and local agencies and non-profit entities. One employee sells bus passes and is responsible for billing and collecting revenues from the sales. The employee also has complete control over the sales, revenue collection, purchases and inventory of transit fare passes. Lack of segregation of duties increases the risk of undetected errors and theft.

• Controls at the Transit cash count rooms are inadequate

o Management acknowledged limited supervision3 over cash count rooms staff and activities.

o Count room employees wear uniforms with pockets contrary to prior recommendations and industry best practice.

o Count room employees were observed entering and leaving the count room with pocketbooks and backpacks.

o Count room employees’ lockers are located inside one of the count room facilities in close proximity to the area used for counting activities.

o Surveillance cameras for one count room were not being viewed live to

observe staffs’ activities. Recordings at one count room are of poor picture quality and images buffered for extensive periods obscuring counting activities. As a result, the recordings4 are difficult to view and could prevent the reviewer from detecting potential wrongful activities inside the count room.

3 The employee responsible for supervision of the count room staff has other time consuming supervisory duties such as payroll and ERP 4 We noted better picture quality during live viewings

3

o The alarm coverages do not require5 the central monitoring station to contact Transit personnel during off hours if the alarms are not activated6 (connected to central monitoring). Connection to central monitoring is important to ensure that police are dispatched and Transit management is notified in the event of an emergency.

o Vault combinations for both count rooms were not changed7 after an employee transferred from the Division in June 2013.

o Farebox revenues are processed for deposit on alternate days.8 As a result,

the potential loss due to theft is increased.

o One of the farebox repair rooms has a camera that was not properly positioned to capture farebox repair activities. This is important because malfunctioning fareboxes may contain cash.

The above noted deficiencies, taken in their entirety, represent a fundamental lack of control over Transit revenues in that they severely limit management’s ability to:

• Ensure all revenues are accounted for and properly recorded, • Safeguard assets (cash and bus passes) against theft, and • Prevent or detect errors or misappropriation.

Recommendations We recommend the Board of County Commissioners direct the County Administrator as a priority to:

1. Assign appropriate personnel to review cash handling practices and procedures across the entire Transit Division to ensure appropriate controls over cash and bus passes are in place and that the findings and recommendations from prior reviews have been completely addressed.

2. Provide the Board with a quarterly status update of recommendations in this report

until fully implemented.

5 Currently the alarm system for one of the vaults sends a message to central monitoring regarding activation and deactivation but the monitoring company’s representative stated that they are not contractually required to take any action if the message is not received 6 We surveyed the Transit agency for Palm Beach and Miami-Dade counties and both confirmed that their alarm systems perform daily automatic check-ins to confirm connections to central monitoring 7 Vault combinations were changed in February 2014 8 The Division received an exception approved by the Director of Finance and Administrative Services Department; however given the amount of cash on hand receipts should be deposited daily

4

APPENDIX A Our Previous Report 08-05, Review of Controls over Farebox and Bus Pass Revenues Dated March 3, 2008

Compliance Review

Review of Controls over Farebox and Bus Pass Revenues - Office of Transportation March 3, 2008 Report No. 08-05

Office of the County Auditor

Evan A. Lukic, CPA County Auditor

Table of Contents Topic Page

Executive Summary ................................................................................3

Purpose and Scope ................................................................................4

Methodology ...........................................................................................4

Background .............................................................................................4

Findings and Recommendations ...........................................................7

Executive Summary Our review evaluated the effectiveness of controls over the custody and processing of farebox and bus pass revenues by the Office of Transportation (OT). Our objective was to determine whether controls are adequate to safeguard County assets and prevent or detect errors and irregularities. We found deficiencies with the OT’s internal controls that diminish its effectiveness to detect or prevent errors and irregularities, which include: • Deficient internal controls over bus pass sales and inventory:

o Lack of segregation of duties o Lack of supervisory oversight over the employee responsible for processing bus

pass sales totaling $4 million in FY 2007 o Inadequate controls over fiscal year 2007 year-end physical inventory of bus

passes valued at $5.7 million o Not maintaining separate accounting records for each custodian

• Inadequate security controls in the cash rooms and at Central Terminal: o Cameras in the cash rooms have blind spots and are not routinely monitored by

authorized personnel o Cash box repair areas do not have camera surveillance o Area used for storage of the camera recording equipment and server is not

locked to prevent unauthorized access o Alarm systems were not tested since installation and are subject to unauthorized

deactivation o Alarm access codes were shared o Safe and door access combinations were not changed when employees with

access were terminated or reassigned

• Farebox and bus pass revenues were not timely deposited and entered into the County’s accounting system: o Farebox revenues were processed on alternate days which resulted in

increased security risks o Bus Pass revenues were not timely deposited, and o Cash Receipts Vouchers (CRV) were not timely processed into the Advantage

Financial System • Foreign coins were not stored in a secured area and were sold non-competitively

without concurrence of the Director of Purchasing in violation of the Purchasing Division rules.

To correct these deficiencies, we have included specific recommendations on pages 8 through 14.

3

Purpose and Scope Our objective was to determine whether controls over the custody and processing of farebox and bus pass revenues by the Office of Transportation (OT) are adequate to safeguard County assets and prevent or detect errors and irregularities. Our review covered the six month period ended September 30, 2007. Methodology To accomplish our objectives, we:

• Toured the transit facilities at Ravenswood Road, Central Terminal, and Copans Road. • Reviewed:

o Chapter 1 of the Revenue Collection Division Internal Control Handbook (ICH) o Chapter 15.B. of the Purchasing Division’s ICH o Chapter 22.80.d of the Administrative Code of Broward County o Selected OT Numbered Procedures Memorandum (NPM) o OT cash receipts process documentation

• Tested selected controls and attributes • Observed video tapes of cash handling activities in the cash rooms • Interviewed staff at:

o Office of Transportation, o Accounting Division, o Revenue Collection Division, o Libraries Division, and

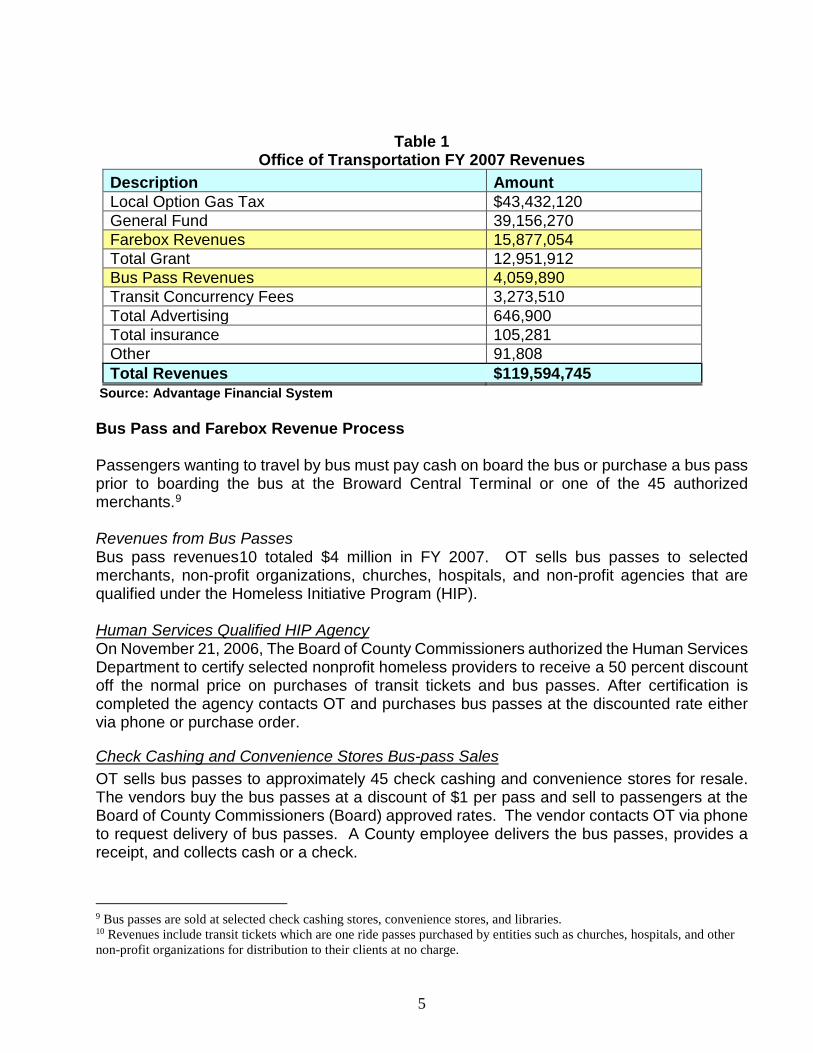

• Surveyed four large Florida mass transit systems Background The Office of Transportation’s mission is to provide clean, safe, reliable and efficient transit services to Broward County residents and visitors. OT provides fixed-route, paratransit, and community bus services, which covers 410 square miles, providing access to work, schools, shopping and other community destinations. Annually OT provides approximately 13.4 million bus service miles, and approximately 37.5 million passenger trips. Fixed-Route Services As of September 30, 2007, OT operated a fleet of 290 fixed route buses on 41 scheduled bus routes. Fixed-route buses operate daily from 4:30 a.m. until approximately 12:40 a.m., except for major holidays and Sundays. Fixed-route services extend into Palm Beach and Miami-Dade counties with additional connections to Tri-Rail services. Office of Transportation’s Revenues The OT received revenues totaling $119,594,745 in Fiscal Year 2007 which are detailed in Table 1 below. Our review focused on fare box and bus pass revenues received from fixed route buses, which totaled $19.9 million ($15.9 and $4.0 million respectively) in FY 2007.

4

Table 1 Office of Transportation FY 2007 Revenues

Description Amount Local Option Gas Tax $43,432,120 General Fund 39,156,270 Farebox Revenues 15,877,054 Total Grant 12,951,912 Bus Pass Revenues 4,059,890 Transit Concurrency Fees 3,273,510 Total Advertising 646,900 Total insurance 105,281 Other 91,808 Total Revenues $119,594,745

Source: Advantage Financial System Bus Pass and Farebox Revenue Process Passengers wanting to travel by bus must pay cash on board the bus or purchase a bus pass prior to boarding the bus at the Broward Central Terminal or one of the 45 authorized merchants.9 Revenues from Bus Passes Bus pass revenues10 totaled $4 million in FY 2007. OT sells bus passes to selected merchants, non-profit organizations, churches, hospitals, and non-profit agencies that are qualified under the Homeless Initiative Program (HIP). Human Services Qualified HIP Agency On November 21, 2006, The Board of County Commissioners authorized the Human Services Department to certify selected nonprofit homeless providers to receive a 50 percent discount off the normal price on purchases of transit tickets and bus passes. After certification is completed the agency contacts OT and purchases bus passes at the discounted rate either via phone or purchase order.

Check Cashing and Convenience Stores Bus-pass Sales OT sells bus passes to approximately 45 check cashing and convenience stores for resale. The vendors buy the bus passes at a discount of $1 per pass and sell to passengers at the Board of County Commissioners (Board) approved rates. The vendor contacts OT via phone to request delivery of bus passes. A County employee delivers the bus passes, provides a receipt, and collects cash or a check.

9 Bus passes are sold at selected check cashing stores, convenience stores, and libraries. 10 Revenues include transit tickets which are one ride passes purchased by entities such as churches, hospitals, and other non-profit organizations for distribution to their clients at no charge.

5

Broward Central Terminal and Libraries Sales Bus passes are consigned to the Central Bus Terminal and the Libraries Division for sale to the public. Cash from sales are deposited and booked as revenue to OT. Farebox Revenues (Bus Fares) Farebox revenues totaled $15.9 million in FY 2007. Upon boarding, passengers without bus passes can purchase either an all-day pass11 or pay for the single trip with cash. Passengers requiring an all-day pass, pay the appropriate fare and the farebox issues and validates a day pass. There are four fare types: adult, youth, elderly, and disabled12. Bus passes and cash fares are processed by the computerized GFI fare box onboard the buses while the driver selects the appropriate fare rate from a keypad on the farebox. Pre-purchased bus passes are swiped through the farebox each time the customer boards. The farebox saves the transaction to memory and updates the card accordingly. The machine will not process a card that has already been swiped within the previous two minutes. When used for the first time, seven-day and thirty-one day passes (passes having an expiration date) must first be inserted into a separate slot in the farebox machine before being swiped. This activates the pass and programs and prints the expiration date onto the pass. The GFI fare box automatically saves the revenue information, type of fare (adult, youth, senior, disabled), and tracks passenger count. Transfer of Farebox Revenues to the Cash Rooms Each evening, fareboxes are processed at one of the two bus depots. A computerized probe is inserted into each GFI fare box which performs two functions:

• downloads transaction data such as total revenues, the number of passengers by fare type, etc. from the GFI farebox and saves it on the probe, then

• unlocks the sealed cash box from the farebox. The sealed cash box is then placed in a vault compartment of the cash room where it is emptied. Security cameras are positioned to monitor this process. After all buses are probed and the cash boxes are emptied, the information stored on the probe is uploaded into the main GFI computer system. This system produces a daily fare box report showing the total revenues collected and ridership data by fare type for each bus. Deposit and Revenue Recording Process Cashiers in the cash room count and prepare the cash for deposit via an armored car service. Simultaneously a Cash Receipts Voucher13 (CRV) is prepared and forwarded to the Accounting Division along with a copy of the deposit slip and other supporting documents. An Account Clerk in the Accounting Division records the CRV in the Advantage Financial System

11 For $3.00 the passenger gets unlimited trips for one day. 12 Passengers must show proper identification for youth, elderly, and disabled fares. 13 CRV is a voucher document used to record revenues in Advantage.

6

(Advantage) and OT reconciles the total revenues deposited to the Fare Box Report for the same dates. Findings and Recommendations Finding 1 Internal controls are deficient over bus pass sales and inventories. Controls over bus pass sales and inventory are deficient because of inadequate segregation of duties, poor inventory controls and a lack of supervisory oversight. A. Duties performed by an Administrative Coordinator lack segregation and

supervisory oversight: Auditing literature14 defines “segregation of duties” as a preventive control designed to preclude improper activity and is essential to ensure that errors or irregularities are detected timely during the normal course of business. Segregation of duties (SOD) require more than one individual to be responsible for completing a process and one individual should not have control over more than one phase of a transaction. SOD makes it difficult for intentional wrongdoing because it requires collusion of two or more individuals.

1. An Administrative Coordinator has control of all phases of the bus pass activities such as:

• Inventory custodian • Inventory accounting • Sales invoices preparation • Billing and collection of sales on credit • Cash receipts • Year-end physical inventory • Expired bus pass destruction

2. In addition to the lack of segregation of duties there was no evidence of supervisory oversight of the Administrative Coordinator with respect to:

• Processing sales transactions • Issuing bus passes at no charge • Replacing expired bus passes • Destroying expired bus passes, and • Counting the year-end physical inventory

B. Independent monthly and year-end inventory and reconciliation were not

performed: Chapter 1 of the Revenue Collection Division ICH requires that a monthly inventory is performed for documents of value by someone other than the custodian and person maintaining the inventory records. A bus pass is a document of value and should

14 Sawyer’s Internal Auditing, The Practice of Modern Internal Auditing, Fifth Edition, Institute of Internal Auditors.

7

be counted and reconciled monthly to reduce the risk of errors and shortages. We noted that:

• OT did not perform monthly inventory counts and reconciliation; • The bus pass inventories on September 30, 2007, held by the Broward County

branch libraries, were performed by custodians; and • Bus passes counted on September 30, 2007, valued at $5.7 million, were not

reconciled to OT’s inventory records.

Lack of segregation and supervisory oversight, failure to conduct monthly independent physical inventories, and failure to reconcile physical inventory counts to the perpetual inventory records could result in undetected inventory errors and concealment of shortages.

C. Separate accounting records were not maintained to reconcile bus passes issued

to two employees for sale to authorized merchants and at the Central Terminal. A total of approximately $570,000 in passes were issued to the two employees during the six months reviewed. We found that separate accounting records were not kept for each employee to track bus pass sales and on hand inventory, as a result shortages can go undetected.

Recommendations We recommend the Board of County Commissioners direct the County Administrator to: 1. Enforce chapter 1 of Revenue Collections Division ICH to require monthly and annual

physical inventories of bus passes by someone other than the custodians.

2. Require monthly and annual reconciliation of physical inventories to the accounting records for bus passes.

3. Review the duties performed by the Administrative Coordinator responsible for bus passes and establish appropriate segregation of duties.

4. Establish supervision over the duties performed by the Administrative Coordinator responsible for bus passes.

5. Establish separate accounting controls over bus passes transferred to the Central

Terminal and to the employee responsible for sales to authorized merchants.

Finding 2 Security controls in the cash rooms and at the Central Terminal are inadequate.

Security controls are safeguards or countermeasures to avoid, counteract or minimize security risks.

8

Cash handling functions in the cash rooms and at the Central Terminal which process over $15.9 million in cash annually are not supervised. However, camera systems were installed to tape employee activities. Management indicated that the camera systems were installed at a cost of approximately $45,600 in lieu of direct supervision. A. The use of cameras is deficient because the camera systems have blind spots and

were not routinely monitored by authorized personnel:

• We reviewed the camera system access logs for an eighteen day period and noted that the system was accessed three times by authorized personnel to observe the cash room activities for a total of 95 minutes. One of these times was to demonstrate the system to the auditors.

• One of the three employees authorized to view cash room activities was out sick for

approximately three months and retired from the County in October 2007. His camera viewing function was not reassigned during his extended absence.

• We reviewed camera activities during a fifteen day period and noted the following

deficiencies:

o The main camera in the Ravenswood cash room was broken and activities were not taped from September 15 to September 28, 2007. The broken camera was discovered September 18 and was fixed ten days later.

o One employee was in the cash room with the sealed cash bags awaiting pickup by

the armor security company. This was in violation of OT Cash Handling policy which requires a minimum of two employees in the cash room until the deposit is picked up.

o Blind spots were observed in both cash room locations; as a result the handling

and processing of cash could not be fully viewed. o We noted seven instances when the cashiers’ activities could not be observed

when working in areas outside of the fixed camera’s range. The areas may have been viewed by the camera if a special zoom camera feature was utilized at the time of taping. The administrator of the camera system stated that if the cameras were observed live, the viewer could have utilized the special feature to zoom in on the activity; however this feature cannot be activated after the event is taped.

o Cashier duties included emptying trash receptacles. These duties should be

segregated because cash could be concealed with trash and retrieved when the receptacle is taken out of the cash room and camera view.

Failure to view camera activities reduced security controls over cash handling and could permit the concealment of cash to go undetected.

9

B. Cash Box Repair area does not have camera surveillance: The area used for repair of cashboxes at both transit locations are not under camera surveillance. Repair technicians have access to the cash in the cash boxes during some repairs.

C. Area used for storage of the camera recording equipment and server is not locked

to prevent unauthorized access: The cameras in the cash room are connected to equipment that records activities 24 hours daily. The recording equipment is connected to a server and activities taped are stored on the server for approximately 50 days. We noted that the area used for storage of camera recording equipment and server was not locked; therefore employees could gain unauthorized access and disconnect the recording equipment and/or server and prevent the storage or recording of cash room activities.

D. Controls over the alarm systems in the cash rooms are deficient:

The former Mass Transit Division installed alarm systems in 2006 at three cash handling locations. We noted that:

• The alarm systems were not tested since installation to ensure continued connection to central monitoring. Connection to central monitoring would automatically dispatch police/law enforcement, and notify OT Management in an emergency.

• The Administrator of the alarm systems for both cash rooms is also one of the

cashiers. As administrator, the cashier is authorized to program the systems to add and deactivate access codes. This function combined with the cashiering duties creates a conflict that should be segregated because security can be compromised by unauthorized deactivation.

• All thirteen Transit Service Agents that perform cashiering duties at the Central

Terminal and five supervisory staff that have access to bus passes and cash shared the same alarm code. The alarm code was also not deactivated after three Transit Service Agents terminated employment. OT staff told us that the alarm code was deactivated October 15, 2007, and each Transit Agent was assigned a unique alarm code.

E. Safe and door access combinations were not changed when employees with access were terminated or reassigned.

Revenue Collection Division Internal Control Handbook (ICH) Chapter 1. Section V.B.2, requires safe combinations or locks to be changed annually and upon the termination or reassignment of employees who have had previous access. The combination to safes and door access codes to cash receipts areas in the agency were changed in November 2006. Subsequently, three employees with access were terminated or reassigned and the combinations and door access codes were not changed.

10

Failure to change combination and access codes could result in unauthorized access and increase the risk of theft or loss.

Recommendations We recommend the Board of County Commissioners direct the County Administrator to:

6. Evaluate coverage provided by the camera system and ensure that blind spots within the cash rooms are eliminated.

7. Require monitoring of cameras by authorized personnel. 8. Repair defective cameras timely.

9. Install cameras at all locations used for cashbox repairs.

10. Ensure at least two cashiers are in the cash room until all deposits are picked up by

the armored security company.

11. Prohibit the removal of trash or other containers from the cash rooms by cashiers.

12. Store the server for camera system and recording equipment in a locked area. 13. Periodically test the alarm systems to ensure that they are operating effectively and

are connected to central monitoring. 14. Ensure the alarm codes, safe and door access combinations are changed when

employees with access are terminated. 15. Promulgate security procedures.

Finding 3 Farebox and bus pass revenues are not timely deposited and entered into the County’s accounting system.

Farebox and bus pass revenues which totaled $19.9 million in Fiscal Year 2007 were not deposited daily and not recorded timely in the Accounting records. As a result, security risks are increased and the Office of Transportation does not earn the optimum investment revenues. A. Farebox revenues were processed on alternate days, which resulted in increased

security risks: Farebox revenues totaling $15.9 million in FY 2007 were processed and deposited on alternate days. Revenue Collection Division Internal Control Handbook (ICH) requires that revenues are deposited by 10:30 AM of the following business day.

11

The ICH permits agencies to request exception from this rule. On September 25, 1995, Revenue Collection approved the then Mass Transit Division’s request to deposit farebox revenues on alternate days.

We reviewed farebox revenue transactions for August 2007 totaling approximately $1.4 million and noted that the deposits were processed on alternate days in accordance with the approved exception. Agency personnel stated that farebox revenues are processed on alternate days at each transit location so that the number of cashiers can be kept to a minimum. The current policy exposes the County to larger losses in the event of theft.

B. Bus Pass revenues were not timely deposited: OT did not comply with the County’s policy requiring deposit by 10:30 AM of the following business day for 47% of transactions reviewed.

We reviewed 60 bus pass sales transactions, totaling $230,601 to determine timeliness of deposits. We found that cash and checks were stored in safes by a Special Projects Coordinator and an Administrative Coordinator and were not deposited daily, as a result 28 (47%) of the 60 transactions totaling $50,297 were deposited 3 to 23 days after the sale dates, which is not in compliance with Revenue Collection’s rules.

C. Cash Receipts Vouchers (CRV) were not timely recorded into the Advantage

Financial System: Chapter 22.80.d of the Administrative Code requires that interest earned on pooled cash is allocated to participants in the pooled-cash fund. The earnings are allocated based on each member’s average equity balance, and are distributed on the last business day of each calendar month. Delays in recording revenues therefore result in reduced investment earnings to OT. We reviewed 83 Cash Receipts Vouchers for farebox and bus pass revenues totaling $1,590,000 processed by OT and noted that all 83 were processed into Advantage 4 to 28 days after the transaction dates. OT requires that CRVs are sent to an Account Clerk in the Accounting Division to be recorded in the Advantage Financial system. In some instances, OT prepares a Cash Receipt Journal15 which is sent to an Account Clerk in the Accounting Division to prepare and record the CRV.

Recommendations We recommend the Board of County Commissioners direct the County Administrator to take steps to ensure that:

16. Farebox and bus pass revenues are deposited daily. 17. Cash Receipts Vouchers are recorded daily at the Office of Transportation.

Finding 4

15 Cash receipts journals are used to summarize revenues and used to prepare the Cash Receipts Voucher.

12

Foreign coins were not stored in a secured area and were sold non-competitively without concurrence of the Director of Purchasing in violation of the Purchasing Division rules. Chapter 15.B.1 of the Purchasing Division’s ICH requires that non-consumable County property may be declared surplus and sold at auction, by competitive sealed bid, or sold in any other manner approved as to legal compliance by the County Attorney in accordance with State Statutes, and/or County Laws, Rules, or Regulations, and deemed advantageous by the Purchasing Director. Chapter 15.B.2 states that disposal of surplus property requires the concurrence of the Director of Purchasing. We observed that foreign coins are stored in an unlocked box in the payroll office accessible by all three payroll staff and found that 151.50 pounds of foreign coins were sold during FY 2007 non-competitively at $2 per pound. We surveyed five other large mass transit systems in Florida to determine how they handled sales of foreign coins. We noted:

• one transit system sells coins based on a percentage of the exchange rate, • two transit systems sell by the pound, and • two transit systems utilized more advanced GFI fareboxes16 that reject foreign coins and return them to passengers.

Recommendations We recommend the Board of County Commissioners direct the County Administrator to:

18. Enforce Purchasing Division rules to require competitive sales of foreign coins.

16 54 of 290 buses in the County’s fleet have fareboxes that can be programmed to return foreign coins.

13

Related Documents