FAQs on recent amendments in Indian Stamp Act, 1899 ..................................... 4 Prelude ............................................................................................................... 4 Introduction........................................................................................................ 5 1. What was the intent behind amending the provisions of Indian Stamp Act? .............................. 5 2. What is effective date of the amendment? .................................................................................. 5 Constitutionality and Scope................................................................................................ 5 3. Levy of stamp duty is governed by which provision? ................................................................... 5 4. What do we mean by securities? .................................................................................................. 6 5. Who has the authority to levy stamp duty on issue and transfer of securities? .......................... 7 6. What kinds of instruments are subject to stamp duty? ............................................................... 7 7. What kinds of transactions in securities are covered within the ambit of the recent amendments in the Indian Stamp Act, 1899?....................................................................................... 8 8. What kinds of transactions are excluded from the ambit of the recent amendments in the Indian Stamp Act, 1899? ....................................................................................................................... 9 9. Post enforcement of the amendment, what will be the position of the States who have their respective Acts on stamp duty? ............................................................................................................ 9 10. Whether the Stamp duty amendment is also applicable on Unlisted Companies? ................. 9 Authority to collect Stamp duty ........................................................................ 10 11. Who has the authority to collect stamp duty? ....................................................................... 10 12. Which Government is entitled to receive the stamp duty in case of issue and transfer of securities? ........................................................................................................................................... 10 Framework for various kinds of securities ......................................................... 11 13. What do we mean by transactions ‘on delivery basis’ and ‘non-delivery basis’? .................. 11 Key Definitions................................................................................................................. 11 14. What do we mean by allotment list? ...................................................................................... 11 15. What do we mean by Market Value? ..................................................................................... 11 16. What do we mean by Settlement Day? .................................................................................. 12 17. What do we mean by clearing list? ......................................................................................... 12 18. What do we mean by domicile state? .................................................................................... 12 19. What is meant by ‘Debentures’? ............................................................................................ 12 Issue of Shares ................................................................................................................. 13

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FAQs on recent amendments in Indian Stamp Act, 1899 ..................................... 4

Prelude ............................................................................................................... 4

Introduction ........................................................................................................ 5

1. What was the intent behind amending the provisions of Indian Stamp Act? .............................. 5

2. What is effective date of the amendment? .................................................................................. 5

Constitutionality and Scope................................................................................................ 5

3. Levy of stamp duty is governed by which provision? ................................................................... 5

4. What do we mean by securities? .................................................................................................. 6

5. Who has the authority to levy stamp duty on issue and transfer of securities? .......................... 7

6. What kinds of instruments are subject to stamp duty? ............................................................... 7

7. What kinds of transactions in securities are covered within the ambit of the recent

amendments in the Indian Stamp Act, 1899?....................................................................................... 8

8. What kinds of transactions are excluded from the ambit of the recent amendments in the

Indian Stamp Act, 1899? ....................................................................................................................... 9

9. Post enforcement of the amendment, what will be the position of the States who have their

respective Acts on stamp duty? ............................................................................................................ 9

10. Whether the Stamp duty amendment is also applicable on Unlisted Companies? ................. 9

Authority to collect Stamp duty ........................................................................ 10

11. Who has the authority to collect stamp duty? ....................................................................... 10

12. Which Government is entitled to receive the stamp duty in case of issue and transfer of

securities? ........................................................................................................................................... 10

Framework for various kinds of securities ......................................................... 11

13. What do we mean by transactions ‘on delivery basis’ and ‘non-delivery basis’? .................. 11

Key Definitions ................................................................................................................. 11

14. What do we mean by allotment list? ...................................................................................... 11

15. What do we mean by Market Value? ..................................................................................... 11

16. What do we mean by Settlement Day? .................................................................................. 12

17. What do we mean by clearing list? ......................................................................................... 12

18. What do we mean by domicile state? .................................................................................... 12

19. What is meant by ‘Debentures’? ............................................................................................ 12

Issue of Shares ................................................................................................................. 13

20. What is the value on which stamp duty is payable in case of issue of shares? ...................... 13

21. What is the stamp duty payable on issue of shares in physical mode?.................................. 13

22. Who is required to pay the stamp duty and to whom? .......................................................... 13

23. What is the stamp duty payable on issue of shares in demat mode? .................................... 14

24. Who is required to pay the stamp duty and to whom? .......................................................... 14

25. What is the value on which stamp duty is payable in case of issue of shares pursuant to

exercise of ESOP? ................................................................................................................................ 14

26. What is the value on which stamp duty is payable in case of issue of bonus shares? ........... 15

Transfer of Shares ............................................................................................................ 15

27. What is the stamp duty payable on transfer of shares in physical mode? ............................. 15

28. Who is required to pay the stamp duty and to whom? .......................................................... 15

29. What is the stamp duty payable on transfer of shares in demat mode? ............................... 15

30. Who is required to pay the stamp duty and to whom? .......................................................... 15

31. What is the value on which stamp duty is payable in case of transfer of shares? ................. 16

32. Whether stamp duty is required to be paid in case of transfers, without change in beneficial

ownership? .......................................................................................................................................... 16

33. Whether stamp duty is payable on transfer of shares to IEPF? ............................................. 16

34. Whether stamp duty is payable on acquisition of shares pursuant to takeover, open offer,

buy-out? .............................................................................................................................................. 16

35. Whether stamp duty is payable on invocation of pledge? ..................................................... 17

36. Whether stamp duty is payable on sale subsequent to invocation of pledge? ...................... 17

Others ............................................................................................................................. 17

37. Whether a Company is required to stamp the letter of allotment? ....................................... 17

38. Whether stamp duty is payable on issue of duplicate share certificates? Can it be considered

as reissue of shares? ........................................................................................................................... 17

Issue/ Re-issue of Debentures .......................................................................................... 19

39. What is the stamp duty payable on issue of debentures in physical mode? ......................... 19

40. Who is required to pay the stamp duty and to whom? .......................................................... 19

41. What is the stamp duty payable on issue of debentures in demat mode? ............................ 19

42. Who is required to pay the stamp duty and to whom? .......................................................... 19

43. What is the value on which stamp duty is payable in case of issue of debentures? .............. 19

44. What is the rate and value on which stamp duty is payable in case of re-issue of

debentures? ........................................................................................................................................ 20

45. What is the value on which stamp duty is payable in case of issue of bonus debentures? ... 20

46. Whether only marketable i.e. transferable debentures would be levied with stamp duty? ..... 20

Transfer of Debentures .................................................................................................... 21

47. What is the stamp duty payable on transfer of debentures in physical mode? ..................... 21

48. Who is required to pay the stamp duty and to whom? .......................................................... 21

49. What is the stamp duty payable on transfer of debentures in demat mode? ....................... 21

50. Who is required to pay the stamp duty and to whom? .......................................................... 21

51. What is the value on which stamp duty is payable in case of transfer of debentures? ......... 21

Issue of Commercial Papers (CPs) ..................................................................................... 22

52. Whether stamp duty is payable on issue of CPs? ................................................................... 22

53. If answer to above question is yes, what is the rate of stamp duty payable on issue of CPs?

22

54. Who is required to pay the stamp duty in case of issue and transfer of CPs and to whom? . 22

55. What is the value on which stamp duty is payable in case of issue of CPs? ........................... 22

Other instruments............................................................................................................ 23

56. Whether stamp duty is payable on Options, Swaps and Repo? ............................................. 23

Penal provisions ................................................................................................ 24

57. In case of failure to collect duty? ............................................................................................ 24

58. In case of failure to transfer duty to State Government? ....................................................... 24

59. In case of failure to file return or failure to give correct details in the return? ..................... 24

FAQs on recent amendments in Indian Stamp Act, 1899 CS Vinita Nair, Aanchal Kaur Nagpal, Harshil Matalia

Date: December 31, 2019

Prelude Stamp duty is duty paid on instruments by way of stamp. Stamp means any mark, seal or endorsement by

any agency or person duly authorised by the State Government, and includes an adhesive or impressed

stamp, for the purposes of duty chargeable under Indian Stamp Act. Stamping the instrument provides

evidentiary value to such instruments whenever produced in Courts of Law.

Every transaction involves execution of some kind of instrument which results in creation or transfer of

extension or extinguishment or recording of some kind of right or liability. Every such instrument is

required to be stamped in accordance with applicable stamp rates.

Financial securities transactions also results in execution of instruments. In cases of securities falling in

the state list, parties tried to select jurisdiction to achieve arbitrage as differential duty rates existed in

different states. Eg. Maharashtra, Gujarat has higher stamp duty rates as compared to Tamil Nadu, Delhi

etc.

With the enforcement of amendments in Indian Stamp Act, 1899:

Jurisdictional arbitrage will be no longer available as all financial transactions will be chargeable

with a uniform rate of stamp duty;

Responsibility to collect stamp duty has been fixed on S.E, CC and Depository

The stock exchanges, clearing corporations and the depositories have been cast with the responsibility

of collecting stamp duty and remitting to the concerned State Government. The depositories are

required to collect the same before executing any transaction in the depository system and the stock

exchanges are required to collect the same on the settlement date. Failure to collect the same will

attract penal provisions.

We have discussed threadbare the constitutionality of the amendments, impact on issue and transfer of

securities, exempted instruments, exempted transactions in our FAQs. We will continue to update this

further by highlighting the insertions made.

Link to our ppt: http://vinodkothari.com/wp-content/uploads/2019/12/Recent-amendments-in-Stamp-

Act.pdf

Introduction

1. What was the intent behind amending the provisions of Indian Stamp Act?

As stated in the Budget speech1, the intent behind the amendment to Indian Stamp Act was to

harmonize stamp duty on financial securities transaction.

The intent was to bring about a streamlined system wherein stamp duties on financial securities would

be levied on one instrument relating to one transaction and get collected at one single place through

the stock exchanges or clearing corporation or depositories as the case may be.

The duty so collected will be shared with the State Governments seamlessly on the basis of domicile

of buying client.

2. What is effective date of the amendment?

The effective date of the amendment made vide Finance Act, 20192 is 9th January, 2020.3

Constitutionality and Scope

3. Levy of stamp duty is governed by which provision?

Article 246 of the Constitution of India4 empowers Central Government and State Government to

levy stamp duty.

Section 3 of the Indian Stamp Act, 18995 provides for instruments attracting stamp duty as per the

rates specified in Schedule I of the Act.

1 Speech for the Interim Budget 2019-2020 2 The Finance Act, 2019 3 Notification issued by Central Government dated 10th December, 2019 4 Constitution of India 5 Indian Stamp Act, 1899

One instrument

One transaction

One place

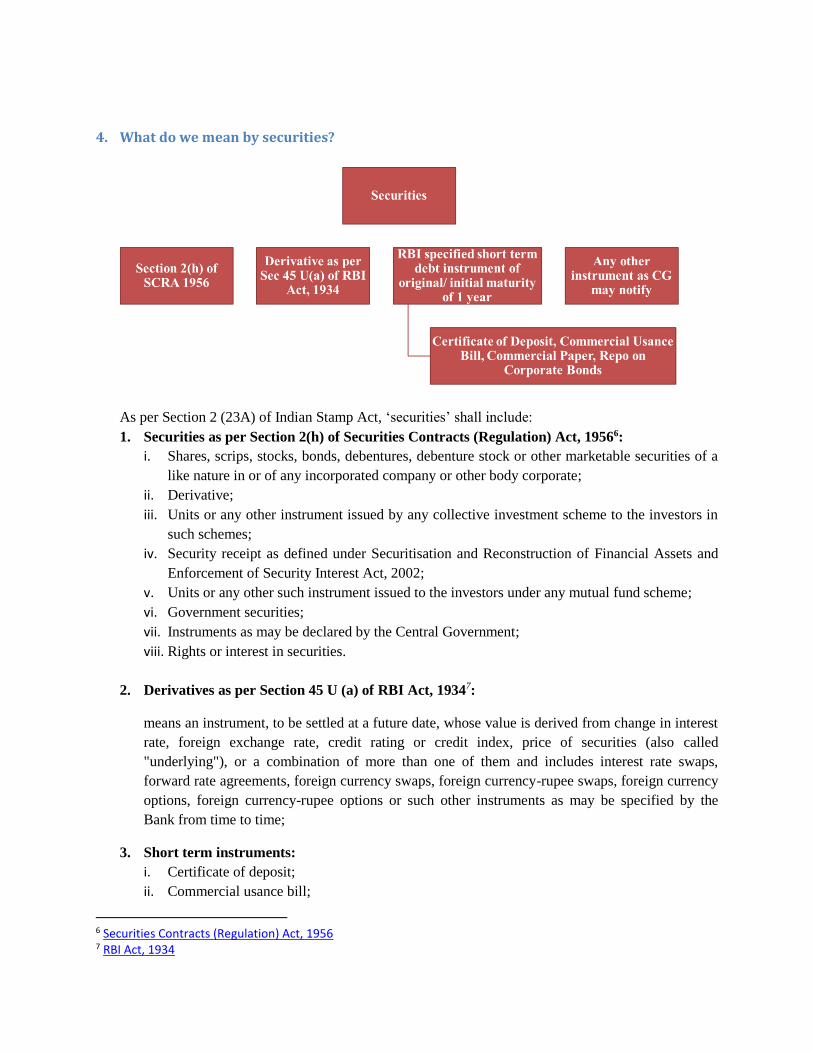

4. What do we mean by securities?

As per Section 2 (23A) of Indian Stamp Act, ‘securities’ shall include:

1. Securities as per Section 2(h) of Securities Contracts (Regulation) Act, 19566:

i. Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a

like nature in or of any incorporated company or other body corporate;

ii. Derivative;

iii. Units or any other instrument issued by any collective investment scheme to the investors in

such schemes;

iv. Security receipt as defined under Securitisation and Reconstruction of Financial Assets and

Enforcement of Security Interest Act, 2002;

v. Units or any other such instrument issued to the investors under any mutual fund scheme;

vi. Government securities;

vii. Instruments as may be declared by the Central Government;

viii. Rights or interest in securities.

2. Derivatives as per Section 45 U (a) of RBI Act, 19347:

means an instrument, to be settled at a future date, whose value is derived from change in interest

rate, foreign exchange rate, credit rating or credit index, price of securities (also called

"underlying"), or a combination of more than one of them and includes interest rate swaps,

forward rate agreements, foreign currency swaps, foreign currency-rupee swaps, foreign currency

options, foreign currency-rupee options or such other instruments as may be specified by the

Bank from time to time;

3. Short term instruments:

i. Certificate of deposit;

ii. Commercial usance bill;

6 Securities Contracts (Regulation) Act, 1956 7 RBI Act, 1934

iii. Commercial paper;

iv. Repo on corporate bonds;

v. Such other debt instrument of original or initial maturity up to 1 year as RBI may specify

from time to time.

4. Any other instrument declared by the Central Government, by notification in the Official

Gazette, to be securities for the purpose of stamp duty.

Negotiable instruments have been included under the definition of securities to be chargeable with

stamp duty. Additionally, the Central Government has been granted power to declare securities that

would be chargeable to stamp duty and thus can expand the definition of securities.

5. Who has the authority to levy stamp duty on issue and transfer of securities?

Entry 91 of the Union List:

“Rates of stamp duty in respect of bills of exchange, cheques, promissory notes, bills of lading,

letters of credit, policies of insurance, transfer of shares, debentures, proxies and receipts.”

Accordingly, Central Government has power to levy stamp duty on issue and transfer of debentures,

transfer of shares and bill of exchange. State Government has power to levy stamp duty on items not

covered in Union list. Therefore, the power to levy stamp duty on issue of shares vests with State

Government.

Finance Act, 2019 seems to bypass this distinction as Parliament has prescribed rates of stamp duty in

case of issue of shares as well.

6. What kinds of instruments are subject to stamp duty?

As per Section 2(14) of the Indian Stamp Act, 1899

Stamp Act mandates payment of duty on instruments, including those created for a transaction in a stock

exchange or depository.

The arrangement of sections in Chapter II of the Stamp Act is also split in accordance with the aforesaid

instruments, as depicted in the figure below:

Part A Part AA

7. What kinds of transactions in securities are covered within the ambit of the recent

amendments in the Indian Stamp Act, 1899?

Transactions covered under the recent amendments are in relation:

Securities not liable to stamp duty [Section 8A]

Sale of securities made through stock exchange [Sec 9A (1) (a)]

Open offer, tender offer, OFS made through stock exchange [Rule 3(2)]

Transfer of securities made by a depository [Sec 9A (1) (b)]

Transfer of securities in case of pledge [Rule 5 (7)]

Acquisition of securities under Section 236 [Rule 6 (4)]

Issue of securities in demat form [Sec 9A (1) (c)]

Transactions not attracting stamp duty [Rule 6 (3)]

8. What kinds of transactions are excluded from the ambit of the recent amendments in the

Indian Stamp Act, 1899?

Transactions expressly excluded from levy of stamp duty under these amendments are:

i. Stock split

ii. Stock consolidation

iii. Mergers and acquisitions

iv. Such other transactions

These corporate actions shall only be excluded if they do not involve a change in their beneficial

ownership. However, fresh issue to an investor as part of a corporate action shall be subject to

stamp-duty. [Rule 6(3) of Stamp Duty Rules, 2019]

v. Transfer of registered ownership of securities from a person to a depository

vi. Transfer of registered ownership of securities from a depository to a beneficial owner.

[Section 8A(b) of the Stamp Act, 1899]

9. Post enforcement of the amendment, what will be the position of the States who have

their respective Acts on stamp duty?

Considering the intent of the government to introduce single point collection mechanism for financial

securities transactions, State Governments cannot impose separate stamp duty on securities even if

the same falls exclusively under State List.

10. Whether the Stamp duty amendment is also applicable on Unlisted Companies? Stamp duty provisions do not distinguish on the basis of companies being listed or unlisted. Stamp

duty is levied on execution of instrument pursuant to which any right or liability is, or purports to be,

created, transferred, limited, extended, extinguished or recorded. Accordingly, the amendments are

applicable on unlisted companies as well.

Authority to collect Stamp duty

11. Who has the authority to collect stamp duty?

Accordingly, pursuant to the power granted under Section 73A of the Indian Stamp Act, the Central

Government notified the Indian Stamp (Collection of Stamp Duty through Stock Exchanges, Clearing

Corporations and Depositories) Rules, 2019 effective from January 9, 2020.

Further, the stock exchange or the clearing corporation authorised by it or the depository are entitled

to deduct 0.2 % of the stamp-duty collected, towards facilitation charges. [Rule 7 (4)]

12. Which Government is entitled to receive the stamp duty in case of issue and transfer of

securities?

Framework for various kinds of securities

13. What do we mean by transactions ‘on delivery basis’ and ‘non-delivery basis’?

Meaning

Delivery based transactions means those transactions where the securities are received by the Buyer.

Non-delivery based transactions means those transactions where the position is reversed by the Buyer

that results in settlement in cash for the gain or loss.

Distinction is crucial as different rates have been prescribed: [Section 9A(1)(a)(b) read with

Article 56A of Schedule I of the Indian Stamp Act]

Type of security (through stock exchange or

otherwise)

Rate of stamp duty per Rs. 1 crore transaction

Security, other than debenture, on delivery basis Rs. 1500

Transfer of security, other than debenture, on

non-delivery basis

Rs. 300

Determination of transaction

Whether a particular transfer of securities through a stock exchange or clearing corporations shall be

treated as on delivery basis or on non-delivery basis, would be determined by the clearing corporation

at the time of settlement, as per established principles governing delivery.

In case of inter-operability of clearing corporations

In case of inter-operability of clearing corporations, the trades of a client across the stock exchanges

shall be considered for determining whether the same would result in a delivery or not.

Key Definitions

14. What do we mean by allotment list?

A list containing details of allotment of the securities intimated by the issuer to the depository under

sub-section (2) of section 8 of the Depositories, Act, 1996

15. What do we mean by Market Value?

16. What do we mean by Settlement Day?

17. What do we mean by clearing list?

A list of transactions of sale and purchase relating to contracts traded on the stock exchanges

submitted to a clearing corporation in accordance with the law for the time being in force in this

behalf.

18. What do we mean by domicile state?

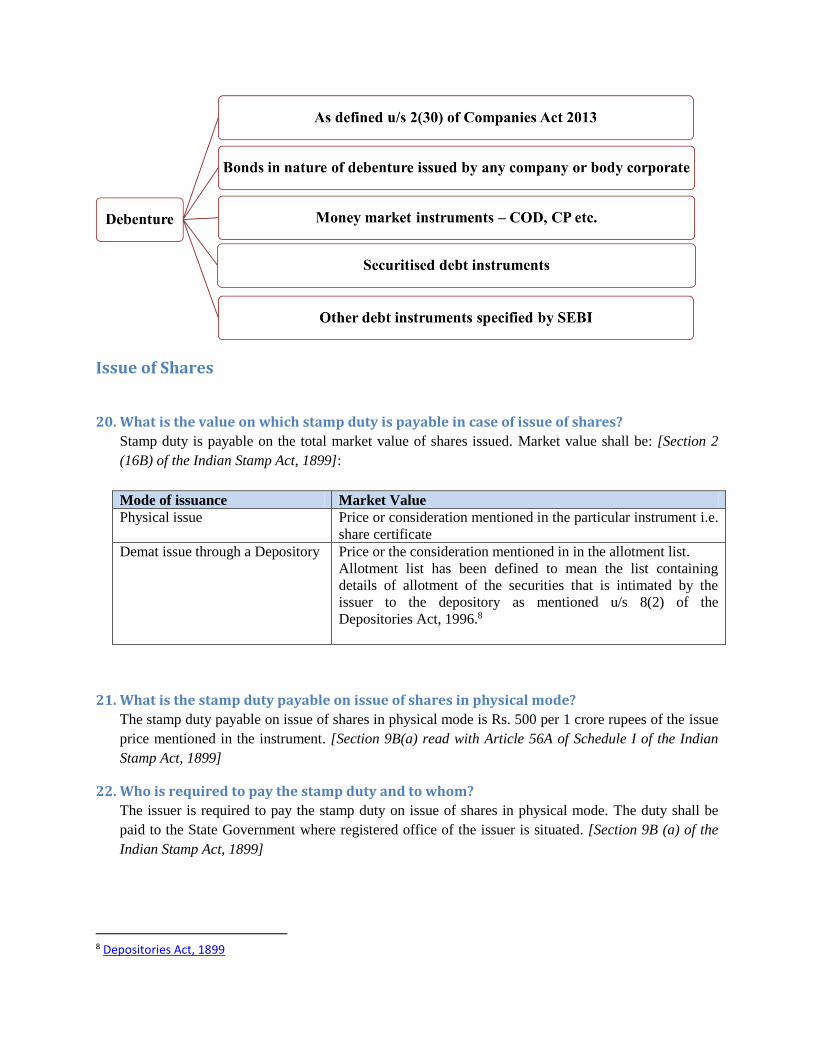

19. What is meant by ‘Debentures’?

In the erstwhile provision, debentures were included in the definition of Bonds but were provided

separately in Schedule I for the purposes of rate of stamp duty. Under the present amendment,

debentures have been excluded from the definition of bonds as a separate has been inserted, which is

different from the definition of debentures under Companies Act, 2013.

Issue of Shares

20. What is the value on which stamp duty is payable in case of issue of shares?

Stamp duty is payable on the total market value of shares issued. Market value shall be: [Section 2

(16B) of the Indian Stamp Act, 1899]:

Mode of issuance Market Value

Physical issue Price or consideration mentioned in the particular instrument i.e.

share certificate

Demat issue through a Depository Price or the consideration mentioned in in the allotment list.

Allotment list has been defined to mean the list containing

details of allotment of the securities that is intimated by the

issuer to the depository as mentioned u/s 8(2) of the

Depositories Act, 1996.8

21. What is the stamp duty payable on issue of shares in physical mode?

The stamp duty payable on issue of shares in physical mode is Rs. 500 per 1 crore rupees of the issue

price mentioned in the instrument. [Section 9B(a) read with Article 56A of Schedule I of the Indian

Stamp Act, 1899]

22. Who is required to pay the stamp duty and to whom?

The issuer is required to pay the stamp duty on issue of shares in physical mode. The duty shall be

paid to the State Government where registered office of the issuer is situated. [Section 9B (a) of the

Indian Stamp Act, 1899]

8 Depositories Act, 1899

23. What is the stamp duty payable on issue of shares in demat mode?

The stamp duty payable on issue of shares in demat mode is Rs. 500 per 1 crore rupees of their total

market value. [Section 9A(1)(c) read with Article 56A of Schedule I of the Indian Stamp Act, 1899]

24. Who is required to pay the stamp duty and to whom?

The issuer shall pay the required stamp duty and the Depository will collect the same on behalf of the

State Government of the State as mentioned below[Section 9A (1)(a) and (4) of the Indian Stamp Act,

1899]:

Participant has been defined under the Rules to mean a participant of the depository as defined u/s 2

(1) (g) of the Depositories Act, 1996.

25. What is the value on which stamp duty is payable in case of issue of shares pursuant to

exercise of ESOP?

The amendment will not result in departure from the existing practice, where the issuer used to stamp

the shares on the basis of the consideration received i.e. the exercise price as the same will be

mentioned as consideration received in the allotment list.

State Government to whom the stamp duty shall be transferred by the Depository

If the buyer is in India

Where the residence of the buyer of shares is

located

If the buyer is outside India

Trading has been done through a trading member or broker

where registered office of trading

member or broker is located

Trading has not been done through a trading

member or broker

where registered office of the participant*is

located

26. What is the value on which stamp duty is payable in case of issue of bonus shares?

In case of issue of bonus shares through stock exchange or depository, stamp duty shall be payable on

the total market value as contained in the allotment list, in the manner payable in case of issue of

shares.

In case of bonus shares issued otherwise than through stock exchange or depository, stamp duty shall

be payable on the total market value of the securities so issued.

Transfer of Shares

27. What is the stamp duty payable on transfer of shares in physical mode?

The stamp duty payable of transfer of shares in physical form shall be Rs. 300 per 1 crore rupees of

the total market value of the shares. [Section 9B(b) read with Article 56A of Schedule I of the Indian

Stamp Act, 1899]

28. Who is required to pay the stamp duty and to whom?

The stamp duty will be payable by the transferor to the State Government having domicile of the

buying client (Not expressly provided, on the basis of rationale provided for demat transfers).

[Section 9B(b) of the Indian Stamp Act, 1899]

29. What is the stamp duty payable on transfer of shares in demat mode?

The rate of stamp duty in case of transfer of shares in demat mode would depend on whether the

transfer is made on a delivery or non-delivery basis. [Section 9A(b) read with Article 56A of Schedule

I of the Indian Stamp Act, 1899]

Nature of transfer Rate of stamp duty

Delivery basis Rs. 1500 per 1 core rupees of the market value

Non-delivery basis Rs. 300 per 1 core rupees of the market value

30. Who is required to pay the stamp duty and to whom?

The liability to pay as well as collect stamp duty is bifurcated as follows: [Section 9A(1)(a) and (b) of

the Indian Stamp Act, 1899]

Liability to pay stamp duty Responsibility to collect of stamp duty

Sale of shares through the stock exchange

Buyer of shares Stock exchange or a clearing corporation

Transfer of shares made by depository otherwise than above

Transferor of shares Depository

31. What is the value on which stamp duty is payable in case of transfer of shares?

Stamp duty shall be payable on the total market value of the shares to be transferred as given below:

[Section 16B of the Indian Stamp Act, 1899]

Mode of transfer Market Value

Physical transfer

Offer price i.e. actual sale consideration mentioned in the

particular instrument.

Shares transferred through stock

exchange

[Rule 3(3) of Stamp Rules, 2019]

Trading price of shares

Even if payment is made in part or on installment basis, stamp

duty shall be collected on the entire sale consideration. [Rule

3(4) of Stamp Rules 2019]

Shares transferred through

depository but not traded in stock

exchange

[Rule 5(2) of Stamp Act Rules,

2019]

Consideration amount specified by the transferor in the delivery

instruction slip (electronic or otherwise)

32. Whether stamp duty is required to be paid in case of transfers, without change in

beneficial ownership?

If the transfer results in debit to the demat account of the transferor i.e. there is a change in beneficial

ownership, then stamp duty will be required to be paid.

For example, in case of pledge of securities, the securities gets locked in the demat account. There is

no change in the beneficial owner of securities. The change occurs only on invocation of pledge.

However, in case the securities are transferred to the broker account for margin facility, there is a

change in the beneficial ownership of securities. In those cases, stamp duty will be payable.

33. Whether stamp duty is payable on transfer of shares to IEPF?

Section 9A(1)(b) and 9(B)(b) provides for payment of stamp duty in case of transfer of securities for

a consideration.

Transfer of shares to IEPF is pursuant to statutory provisions of law. While there is a change in

beneficial ownership of shares, the IEPF Authority holds the shares in trust capacity till the actual

beneficial owner claims the shares. The transfer does result in transfer of any right or liability. The

shares are not permitted to be dealt in any manner by IEPF. The benefits on those shares are also

transferred to IEPF and held on behalf of the claimant.

Therefore, stamp duty should not be payable in case of transfer of shares to IEPF and on transfer of

shares back to the claimant.

34. Whether stamp duty is payable on acquisition of shares pursuant to takeover, open offer,

buy-out?

In case of the transactions arising from acquisition of shares pursuant to takeover through tender offer

or open offer or any offer for sale executed through stock exchange or through the depository, the

stamp-duty shall be collected from the offeror, on the total market value of the security being

acquired or sold out, at the offer price, once the offer is successfully completed.

35. Whether stamp duty is payable on invocation of pledge?

In case of transfer of securities pursuant to an invocation of pledge, stamp duty shall be payable by

the pledgee on the market value of the shares. Refer here for definition of market value.

As per SEBI’s guidance note9 on insider trading, for the purpose of calculation of threshold for

disclosures relating to pledge under Chapter III of the Regulations, the market value on the date of

pledge/revoke transaction should be considered.

36. Whether stamp duty is payable on sale subsequent to invocation of pledge?

When the pledged shares are subsequently sold, it would amount to transfer of shares and change in

beneficial ownership. Therefore, stamp duty will be payable on sale subsequent to invocation of

pledge.

Others

37. Whether a Company is required to stamp the letter of allotment?

In terms of Section 4 (3) of the Indian Stamp Act, in case of any issue, sale or transfer of securities,

where the duty has been paid on the principal instrument chargeable under Section 9A i.e. instrument

chargeable with duty for transactions in stock exchanges and depositories, no stamp duty is required

to be charged on any other instrument relating to such transaction.

In all other cases, stamp duty will be paid in accordance with Section 4 (1) read with Schedule 1 to

Indian Stamp Act.

38. Whether stamp duty is payable on issue of duplicate share certificates? Can it be

considered as reissue of shares?

Issue of duplicate share certificate is not a case of re-issuance. Issue of duplicate share certificates is

relevant in case of issue of shares in physical (governed by Section 9B) or where the issue of shares

was made through depository (governed by Section 9A) and shareholder rematerialized the shares and

eventually lost the certificate.

Post amendment, in terms of Section 4 (3) of the Indian Stamp Act, in case of any issue, sale or

transfer of securities, where the duty has been paid on the principal instrument chargeable under

Section 9A i.e. instrument chargeable with duty for transactions in stock exchanges and depositories,

no stamp duty is required to be charged on any other instrument relating to such transaction.

Issue of duplicate share certificates is neither a case of issue or sale or transfer of securities.

Accordingly, stamp duty on duplicate share certificate is applicable in accordance with the duty

provided in respective state stamp act.

9 Guidance note on SEBI(Prohibition of Insider Trading) Regulations, 2015

Issue/ Re-issue of Debentures

39. What is the stamp duty payable on issue of debentures in physical mode?

The stamp duty payable on issue of debentures in physical mode is Rs. 500 per 1 crore rupees of the

total market value on each issue. [Section 9B(a) read with Article 27 of Schedule I of the Indian

Stamp Act, 1899]

40. Who is required to pay the stamp duty and to whom?

The issuer is required to pay the stamp duty on issue of debentures in physical mode. The duty shall

be paid to the State Government of the State where registered office of the issuer is situated. [Section

9B (a) of the Indian Stamp Act, 1899]

41. What is the stamp duty payable on issue of debentures in demat mode?

The stamp duty payable on issue of debentures in demat mode is Rs. 500 per 1 crore rupees of their

total market value. [Section 9A(1)(c) read with Article 27 of Schedule I of the Indian Stamp Act,

1899]

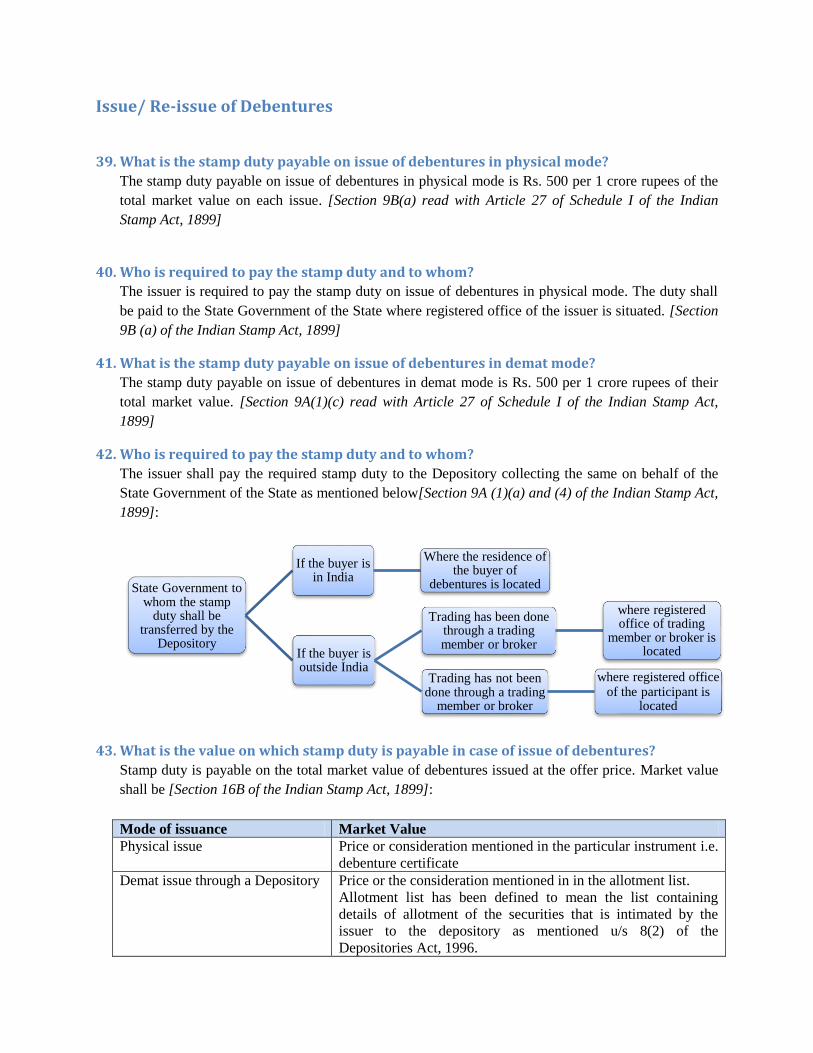

42. Who is required to pay the stamp duty and to whom?

The issuer shall pay the required stamp duty to the Depository collecting the same on behalf of the

State Government of the State as mentioned below[Section 9A (1)(a) and (4) of the Indian Stamp Act,

1899]:

43. What is the value on which stamp duty is payable in case of issue of debentures?

Stamp duty is payable on the total market value of debentures issued at the offer price. Market value

shall be [Section 16B of the Indian Stamp Act, 1899]:

Mode of issuance Market Value

Physical issue Price or consideration mentioned in the particular instrument i.e.

debenture certificate

Demat issue through a Depository Price or the consideration mentioned in in the allotment list.

Allotment list has been defined to mean the list containing

details of allotment of the securities that is intimated by the

issuer to the depository as mentioned u/s 8(2) of the

Depositories Act, 1996.

State Government to whom the stamp

duty shall be transferred by the

Depository

If the buyer is in India

Where the residence of the buyer of

debentures is located

If the buyer is outside India

Trading has been done through a trading member or broker

where registered office of trading

member or broker is located

Trading has not been done through a trading

member or broker

where registered office of the participant is

located

44. What is the rate and value on which stamp duty is payable in case of re-issue of

debentures?

Physical mode:

In case of re-issue in physical mode, stamp duty on each re-issue shall be payable by issuer at the rate

of Rs. 10 per 1 crore rupees of the consideration amount specified in the instrument.

Demat Mode: Same as above.

45. What is the value on which stamp duty is payable in case of issue of bonus debentures?

In case of issue of bonus debentures through stock exchange or depository, stamp duty shall be

payable on the total market value as contained in the allotment list, in the manner payable in case of

issue of debentures.

In case of bonus debentures issued otherwise than through stock exchange or depository, stamp duty

shall be payable on the total market value of the securities so issued.

Accordingly, stamp duty will be payable on the face value of the debentures.

46. Whether only marketable i.e. transferable debentures would be levied with stamp duty?

Erstwhile Article 27 of Schedule I to Indian Stamp Act, 1899 levied stamp duty on debentures that

were a marketable security and were transferrable.

The terms ‘marketability’ or ‘marketable’ can be understood by referring to the judicial precedents in

this regard. Apex Court in Bhagwati Developers v Peerless General Finance has considered some

important questions relating to the interpretation of the term marketable security and also applicability

of SCRA to public unlisted companies. The Court stressed on the fact that marketability is based on

transferability. It held as below:

“…As is evident from the dictionary meaning set out above, the expression “marketable” has been

equated with the word saleable. In other words, whatever is capable of being bought and sold in a

market is marketable. The size of the market is of no consequence. In other words, the number of

persons willing to purchase such shares would not be decisive. One cannot lose sight of the fact that

there may not be any purchaser even for the listed shares. In such a case can it be said that even

listed shares are not marketable? In our opinion what is required is free transferability. Subject to

certain limited statutory restrictions, the shareholders possess the right to transfer their shares, when

and to whom they desire. It is this right which satisfies the requirement of free transferability.

However, when the statute prohibits or limits transfer of shares to a specified category of people with

onerous conditions or restrictions, right of shareholders to transfer or the free transferability is

jeopardized and in that case those shares with these limitations cannot be said to be marketable…”

In view of the above landmark judgement, the Apex Court was clear on the point that where a

security is non- transferable, it ceases to be a “security”. Further, it is pertinent to mention here that,

in case of public companies, Section 58 (2) of Act, 2013 also provides that securities of such

companies shall be freely transferable. In our view, the basic difference between a loan and a

debenture is premised on the transferability of a debenture by way of a secondary market transaction,

whereas a loan is a contractual relationship. A non-transferable debenture comes closer to a

contractual debt between the issuer and the holder – hence, it is akin to a loan.

Accordingly, debentures that fall within the definition of security, would be levied with stamp duty.

Transfer of Debentures

47. What is the stamp duty payable on transfer of debentures in physical mode?

The stamp duty payable of issue of debentures in physical form shall be Rs. 10 per 1 crore rupees of

the total market value of the debentures to be transferred. [Section 9B(b) read with Article 56A of

Schedule I of the Indian Stamp Act, 1899]

48. Who is required to pay the stamp duty and to whom?

While this is not expressly provided, on the basis of rationale provided for demat transfers, the stamp

duty will be payable by the transferor to the respective State Government that represents domicile of

the buying client.

49. What is the stamp duty payable on transfer of debentures in demat mode?

The rate of stamp duty in case of transfer of debentures in demat mode shall be Rs. 10 per 1 crore

rupees of the total market value of the debentures to be transferred. [Section 9A(b) read with Article

27 of Schedule I of the Indian Stamp Act, 1899]

50. Who is required to pay the stamp duty and to whom?

The liability to pay as well as collect stamp duty is bifurcated as follows: [Section 9A(1)(a) and (b) of

the Indian Stamp Act, 1899]

Liability to pay stamp duty Responsibility to collect of stamp duty

Sale of debentures through the stock exchange

Buyer of debentures Stock exchange or a clearing corporation

Transfer of debentures made by depository otherwise than above

Transferor of debentures Depository

51. What is the value on which stamp duty is payable in case of transfer of debentures?

Stamp duty shall be payable on the total market value of the debentures to be transferred as given

below: [Section 16B of the Indian Stamp Act, 1899]

Mode of transfer Market Value

Physical transfer Offer price i.e. actual sale consideration mentioned in the

particular instrument.

Debentures transferred through Trading price of debentures

Mode of transfer Market Value

stock exchange

[Rule 3(3) of Indian Stamp Rules,

2019]

Even if payment is made in part or on installment basis, stamp

duty shall be collected on the entire sale consideration. [Rule

3(4) of Stamp Rules 2019]

Debentures transferred through

depository but not traded in stock

exchange

[Rule 5(2) of Stamp Act Rules,

2019]

Consideration amount specified by the transferor in the delivery

instruction slip (electronic or otherwise)

Issue of Commercial Papers (CPs)

52. Whether stamp duty is payable on issue of CPs?

As per FIMMDA guidelines, CPs being a kind of a negotiable instrument were chargeable with stamp

duty as a usance promissory note.

Post amendment, CPs has been specifically included in the definition of debentures and securities,

thereby attracting similar stamp duty as in case of debentures. [Section 2 (10A) of the Indian Stamp

Act, 1899]

53. If answer to above question is yes, what is the rate of stamp duty payable on issue of CPs?

As per RBIs Commercial Paper Directions, 2017 the CPs can be held in dematerialized form only.

Accordingly, the stamp duty payable will be similar to issue of debentures in dematerialized form i.e.

Rs. 500 per 1 crore rupees of the market value.

54. Who is required to pay the stamp duty in case of issue and transfer of CPs and to whom?

Mode of transfer Transaction undertaken Liability to pay Paid to

Demat Issue of CPs Issuer Depository

Demat Transfer of CPs through stock

exchange

Buyer Stock exchange/ clearing

corporation

Demat Transfer or sale of CPs

otherwise than through a

stock exchange

Seller/

Transferor

Depository

55. What is the value on which stamp duty is payable in case of issue of CPs?

CPs are issued at discount and redeemed at Par. The stamp duty is payable on the market value as

contained in the allotment list. As per FIMMDA’s operational guidelines, stamp duty is payable on

total face value.

Other instruments

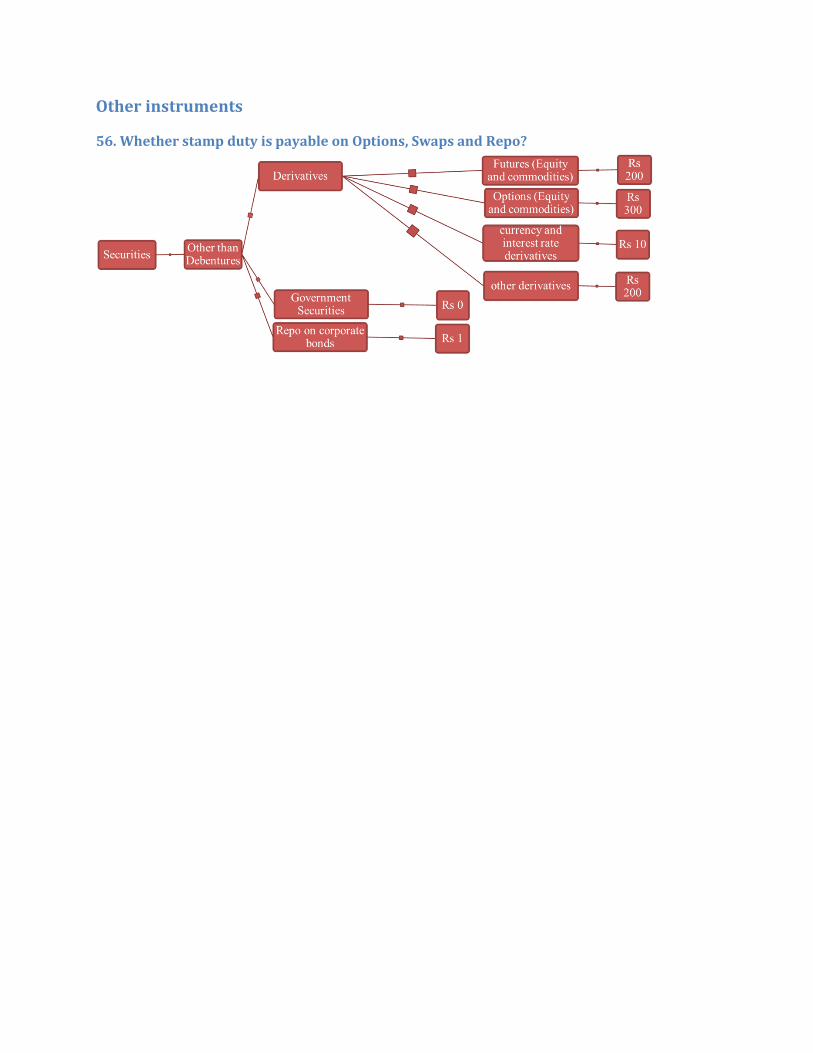

56. Whether stamp duty is payable on Options, Swaps and Repo?

Penal provisions

57. In case of failure to collect duty?

In case of failure to collect stamp duty within the time specified, such person shall be punishable with

a minimum fine of Rs. 1 lakh but which may extend up to 1% of the amount to be collected.

58. In case of failure to transfer duty to State Government?

In case a person fails to transfer the duty amount to the respective State Government, a fine of

minimum Rs. 1 lakh but which may extend up to 1% of the amount to be transferred shall be levied.

59. In case of failure to file return or failure to give correct details in the return?

Any person who-

i. Fails to file return with the State Government or

ii. Submits incorrect details

shall be punishable with fine of one lakh Rs.1 lakh for each day during which such failure continues

or Rs.1 crore, whichever is less.

Related Documents

![THE INDIAN STAMP ACT, 1899 [ACT NO. II OF 1899] As …agraredco.com/wp-content/uploads/2013/02/INDIAN-STA… · · 2013-02-25As amended in its application in Uttar Pradesh. AN ACT](https://static.cupdf.com/doc/110x72/5b06719e7f8b9a5c308cfbb0/the-indian-stamp-act-1899-act-no-ii-of-1899-as-amended-in-its-application-in.jpg)

![INDIAN STAMP ACT, 1899 - Andhra Pradeshregistration.ap.gov.in/.../ACT/Stamp/StampAct.pdfINDIAN STAMP ACT, 1899 [ACT NO. II OF 1899] As Applicable in State of Andhra Pradesh. (1 April,](https://static.cupdf.com/doc/110x72/5ad98afa7f8b9a52528baaa5/indian-stamp-act-1899-andhra-stamp-act-1899-act-no-ii-of-1899-as-applicable.jpg)