FACTORS AFFECTING THE PERFORMANCE OF FINANCIAL SECTOR IN MALAYSIA Bong Lie Lin BG 173 B713 Corporate Master in Business Administration 2012 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FACTORS AFFECTING THE PERFORMANCE OF FINANCIAL SECTOR IN MALAYSIA

Bong Lie Lin

BG 173 B713 Corporate Master in Business Administration 2012 2012

Pu J ~ 4

UNJVERSJll - en ~ MALAy LA SARAWAK

PKHIOMAT MAKLUMAT AKAOEMIK

11111 nllfli~rlllllllill 1000246523

FACTORS AFFECTING THE PERFORMANCE OF FINANCIAL SECTOR IN MALAYSIA

BONG LIE LIN

A dissertation submitted in partial fulfillment of the requirements for the degree of Corporate Master in Business Administration

Faculty of Economics and Business UNIVERSITI MALAYSIA SARA W AK

2012

I

ABSTRACT

0his paper is to analyze and detennine the factors that affecting the financial sector

perfonnance in Malaysia for the period of five years from year 2006 to 2011 From

the study the result shows that the perfonnance of Malaysian financial sector is

stable and quite profitable because of systematic Malaysian financial systems

regulations and the strong financial capital However the global financial crisis

occurred during year 2008 to 2009 was affected the financial sector globally and

affected the financial institutions service qualit~ The study will use the financial

ratios and apply the CAMEL Model namely Capital adequacy Asset quality

Management Earnings and Liquidity to detennine the factors affecting the financial

sector perfonnance So in order to identify the detenninants of perfonnance of

Malaysian financial sector during 2006 to 2011 this study has chosen mUltiple

regression analysis Besides that the dependent variables are consisting profitability

ratio which Return on Assets (ROA) and Return on Equity (ROE) then independent

variables are the CAMEL Methods So from the study the results also shows that the

ROA and ROE are depends on the CAMEL Lastly there are a significant

relationship between the dependent variables and the independent variables

ACKNOWLEDGEMENT

My highest and more sincere appreciation goes to my beloved parents and my

families who have always encouraged and guided me to be independent never try to

limit my aspirations

I would like to express my great appreciation to my supervisor Dr Chu Ei Yet for his

understanding attention kindness and encouragement His supervision idea

guidance and critics of the research paper have been an enormous help Words alone

Icannot be expressed my greatest appreciation and thanks to him

I would like to express my high appreciation to my all lectures of Faculty Economics

and Business especially lecturers of Finance Thanks again to everyone including

those who I have probably forgotten to mention here

I

ii

Pusat Khidmat MakJumat Akademik UNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENT

ABSTRACT i

AKNOWLEDGEMENT ii

TABLE OF CONTENT iii

LIST OF FIGURES v

LIST OF TABLES v

LIST OF ABBREVIATIONS vi

1 INTRODUCTION

11 Background 1

111 Malaysian Gross Domestic Product (GDP) 4

112 Malaysian Financial System Challenges in Malaysian Financial

Sector 6

113 Challenges in Malaysian Financial Sector 9

12 Problem Statement 10

13 Theoretical Framework 12

131 Agency Theory 12

132 Characteristics ofAgency Problems in Financial Institutions 13

14 Conceptual Framework 15

15 Scope of the Study 16

16 Research Objectives 17

161 General Objective 17

162 Specific Objectives 18

17 Significance of the Study 18

18 Organization of the Study 19

19 Conclusion 20

2 LITERATURE REVIEW

21 Introduction 21

22 Literature review on CAMEL Approach 22

23 Financial Institutions Rating in Malaysia 24

231 Capital Adequacy 24

232 Asset Quality 26

233 Management 29

iii

234 Earnings 30

235 Liquidity 31

24 Empirical Literature Determinants of Financial Institutions

Profitability 32

3 METHODOLOGY

31 Introduction 34

32 Data 35

33 Sample 35

34 Variables used in the study 36

341 Dependent variables 36

342 Independent variables 36

35 Empirical Model 43

36 Concluding Remarks 44

37 Conclusions 45

4 FINDINGS AND CONCLUSION

41 Introduction 46

42 Descriptive Analysis 46

421 Descriptive Analysisor the Dependent and Independent

Variables 46

422 Trend Analysis 48

4221 Return on Asset (ROA) 48

4222 Return on Equity (ROE) 49

43 Correlation Analysis 49

44 Model Summary and coefficient Analysis 52

441 Model Summary 52

442 Coefficient Analysis 0ROA 53

45 Chapter summary 56

5 CONCLUSION AND RECOMMENDATIONS

51 Introduction 57

52 Summary of Findings 57

53 Recommendations and Suggestions 59

REFERENCES 61

iv

I

LIST OF FIGURE

Figure 1 Malaysia Real Growth Rate 5

Figure 2 Malaysia GDP Per Capita (US$) 5

Figure 3 The Conceptual Framework for Financial Sector Performance 16

Figure 4 Trend Analysis ofROA of Malaysian Financial Sector 48

Figure 5 Trend Analysis of ROE of Malaysian Financial Sector 49

LIST OF TABLES

Table 1 List of Financiallnstitutions as Public Listed in Bursa Saham Malaysia 4

Table 2 The Malaysian Financial System 8

Table 3 Independent Variables and their Proxies 42

Table 4 Descriptive Analysis for the Dependent and Independent Variables 47

Table 5 Correlation between ROA and all ratios 50

Table 6 Correlation between ROE and all ratios 51

Table 7 Summary of Analysis Return on Assets (ROA) and Return on

Equity (ROE) 52

Table 8 Coefficient Analysis and Collinearity Statistic (ROA) 54

Table 9 Coefficient Analysis and Collinearity Statistic (ROE) 55

v

ASST

BNMlGP8

CAP

CTD

EARN

FDI

FDIC

FIs

GDP

LIQ

LPI

LTD

MARC

MBSB

MNGT

MNRB

NPL

OLS

RHB

ROA

ROE

LIST OF ABBREVIATIONS

Asset Quality

Financial Reporting for Licensed Institutions

Capital Adequacy

Cash to Deposit

Earnings

Foreign Direct Investment

Federal Deposit Insurance Corporation

Financial Institutions

Malaysian Gross Domestic Product

Liquidity

Lonpac Insurance

Loan to Deposit

Malaysian Rating Corporation Berhad

Malaysia Building society Berhad

Management

Malaysian Reinsurance Berhad

Not Performing Loan

Ordinary Least Squares

Rashid Hussein Bank

Return on Assets

Return on Equity

vi

1

-==

I

RWCR Risk Weighted Capital Ratio

VIF Variance Inflation Factor

vii

CHAPTER 1

INTRODUCTION

11 Background

The global financial crisis from 2008 t02009 had brought huge impact for the world

economy due to the price of the assets which has been over inflated and caused the

sub-prime mortgage booming and exploding into housing and banking crisis with a

cascading effect on consumer and investment demand In addition the financial market

becomes panic due to the subprime mortgages and the failures of Lehman Brothers

and Washington Mutual in United States The government of United States had

implemented some solutions and actions to reduce the panics during the first half of

October by promoting the liquidity and the solvency of the financial sector reducing

the prices for the asset classes and the commodities the cost of the corporate and the

bank borrowing rose significantly and high volatility in financial market which

increasing infrequently In the case of Malaysian economy the countrys economy was

sheltered from the direct effects of financial exposure because the new derivatives were

not allowed into the country The global financial crisis may result the Governments

plans to achieve vision 2020 being interrupted because of decreasing in the exports and a

slowdown in foreign direct investment (FDI)

The financial services sector is the bedrock of any economy It is the key to the overall

economy by providing various fonns of capital to enable the growth of other

industries in the economy All large and successful economies require strong banks

system vibrant capital markets and well-functioning financial infrastructures

Moreover the sector is also a core component in a services-based economy and a key

growth engine in its own right As demonstrated by the emergence of international

1

___--==========-=-----------=---=------- ---_

II

shy

financial services centres worldwide the financial sector growth comes from serving

domestic businesses and consumers as well as tapping external markets and sources of

funds

Mansor (2007) states that financial liberalization and development has been the major

financial feature in many developing countries Malaysia is a highly open economic

country and it also witnesses a respectable economic growth and rapid financial

development since the introducing of Financial Sector Masterplan in 2001 the

Malaysian financial sector has undergone significant transformation and progress The

banking sector especially has undergone restructuring consolidation and

rationalization Moreover the flexibility and the performance of the financial

landscaping had been improved due to the transformation and deregulation and

liberalization Moreover a stable and effective financial sector will affect the

performance of the financial sector and it will become an important pillar of strength

in our economy

Schumpeter (1911) contends that the services provided by the financial intermediaries

are essential drivers for innovation and growth Well developed financial systems

channel financial resources to the most productive use Malaysias Prime Minister

Dato Sri Mohd Najib bin Tun Hj Abdul Razak states that financial sector in Malaysia

is expected to have a greater role in assisting the economic growth as Malaysia transit

towards achieving a developed economy status by year 2020 The financial sector is

able to assist the economy growth and encourage the economy transformation into the

next phase of development and provide the world class high value added financial

products and services at the competitive prices and speed up the new economic

sectors In order to enhance the economys expansion Government has taken the

2

initiatives to promote structural change within the economy and diversify the sources

of the financial sectors growth by offering liberalisation package from 2009 to 2012

The foreign equity limits of investment banks Islamic banks insurance companies

and Takaful operators had increased from 40 percent to 70 percent The alliances will

strengthen business potential and enhance the growth of the financial institutions

through international expertise and global network foreign shareholders The rapid

growth and the strong financial sector of the country will enable the consumers to get

more infonnation between the financial service providers the regulators and the

authorities will need to provide the conducive environment that raises the consumer

empowennent The more consumers can afford and able to buy the products or

services provided by of the financial institution such as commercial bank investment

company or insurances company will positively affect the perfonnance of the

financial sector

As a result the financial sector plays crucial role for the economic growth and the

countrys development From Table 1 it shows that then financial sector comprises of

26 institution consisting 4 commercial bank 6 insurance company 14 investment

holding companies stock broking companies finance companies and the exchange

holding companies The lists of the financial institutions in Table 1 are public listed

on the Bursa Saham Malaysia

3

_ _ _ ____ _

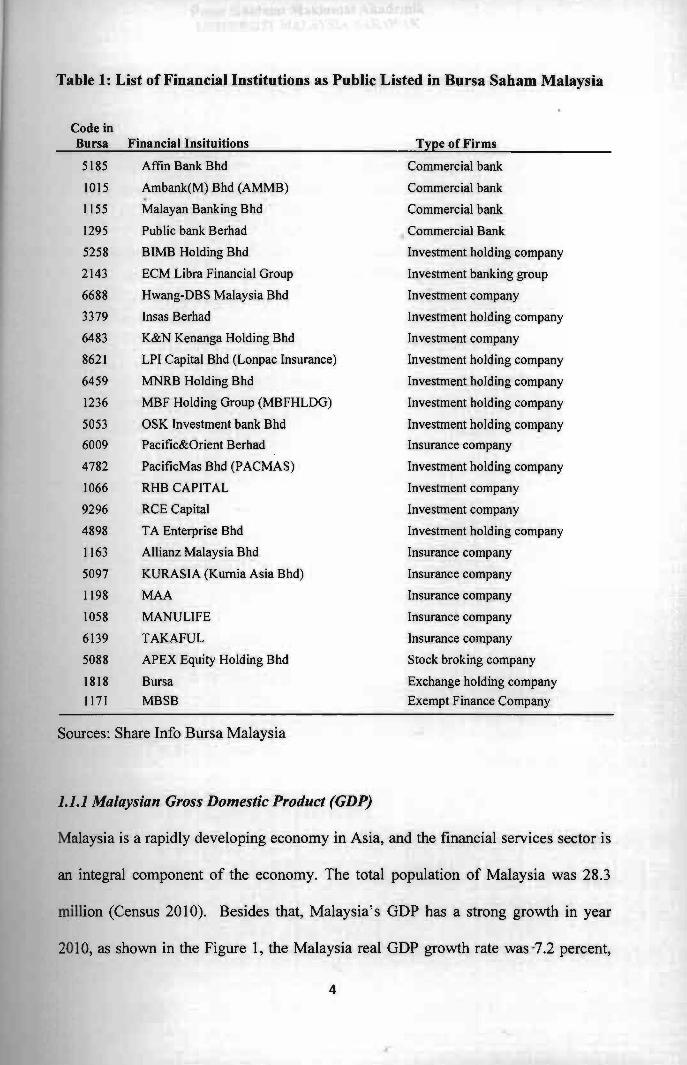

Table 1 List of Financial Institutions as Public Listed in Bursa Saham Malaysia

Code in Bursa

5185

1015

1155

1295

5258

2143

6688

3379

6483

8621

6459

1236

5053

6009

4782

1066

9296

4898

1163

5097

1198

1058

6139

5088

1818 1171

Financial Insituitions

Affin Bank Bhd

Ambank(M) Bhd (AMMB)

Malayan Banking Bhd

Public bank Berhad

BIMB Holding Bhd

ECM Libra Financial Group

Hwang-DBS Malaysia Bhd

Insas Berhad

KampN Kenanga Holding Bhd

LPI Capital Bhd (Lonpac Insurance)

MNRB Holding Bhd

MBF Holding Group (MBFHLDG)

OSK Investment bank Bhd

PacificampOrient Berhad

PacificMas Bhd (PACMAS)

RHB CAPITAL

RCE Capital

T A Enterprise Bhd

Allianz Malaysia Bhd

KURASIA (Kumia Asia Bhd)

MAA

MANULIFE

TAKAFUL

APEX Equity Holding Bhd

Bursa

MBSB

Sources Share Info Bursa Malaysia

111 Malaysian Gross Domestic Product (GDP)

Type of Firms

Commercial bank

Commercial bank

Commercial bank

Commercial Bank

Investment holding company

Investment banking group

Investment company

Investment holding company

Investment company

Investment holding company

Investment holding company

Investment holding company

Investment holding company

Insurance company

Investment holding company

Investment company

Investment company

Investment holding company

Insurance company

Insurance company

Insurance company

Insurance company

Insurance company

Stock broking company

Exchange holding company

Exempt Finance Company

Malaysia is a rapidly developing economy in Asia and the financial services sector is

an integral component of the economy The total population of Malaysia was 283

million (Census 2010) Besides that Malaysias GDP has a strong growth in year

2010 as shown in the Figure 1 the Malaysia real GDP growth rate was -72 percent

--==-o---===--=-----shy

4

$15000

$14000

$13000

S12OOO

Pu ot Khidmat Maklumat Akademik UNlVERSm MALAYSIA SARAWAK

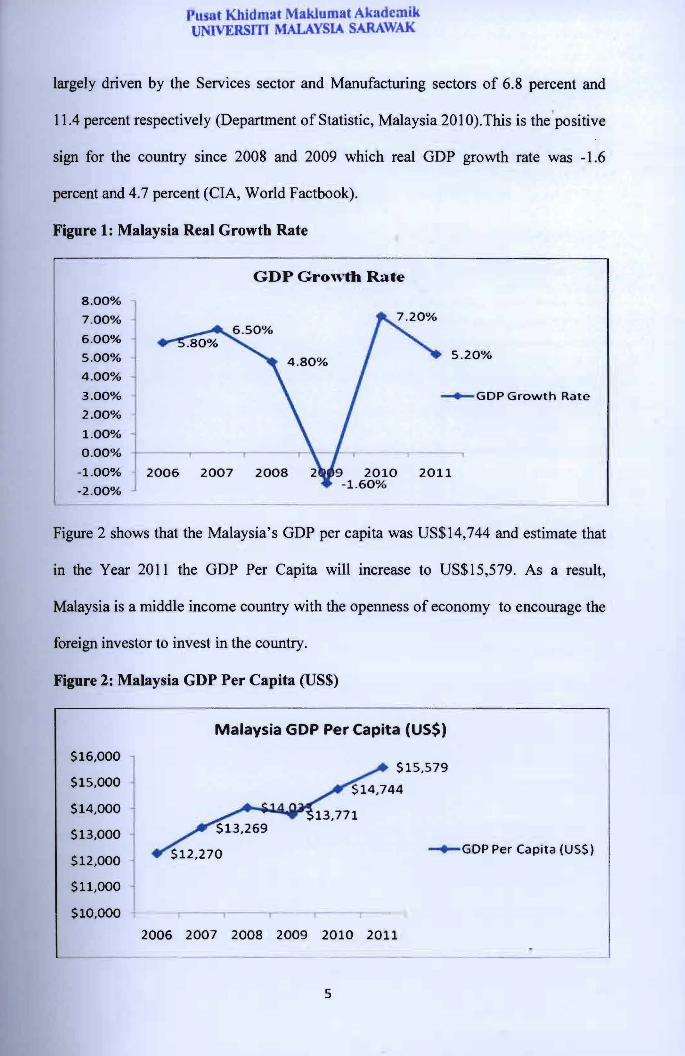

largely driven by the Services sector and Manufacturing sectors of 68 percent and

114 percent respectively (Department of Statistic Malaysia 201 O)This is the positive

sign for the country since 2008 and 2009 which real GDP growth rate was -16

percent and 47 percent (CIA World Factbook)

Figure 1 Malaysia Real Growth Rate

GDP Growth Rate

800 1 700

6 00

5 00

j2006 2007 2008 2011

520~ 400

300 ~GDP Growth Rate

200

1 00

000

-100

-2 00

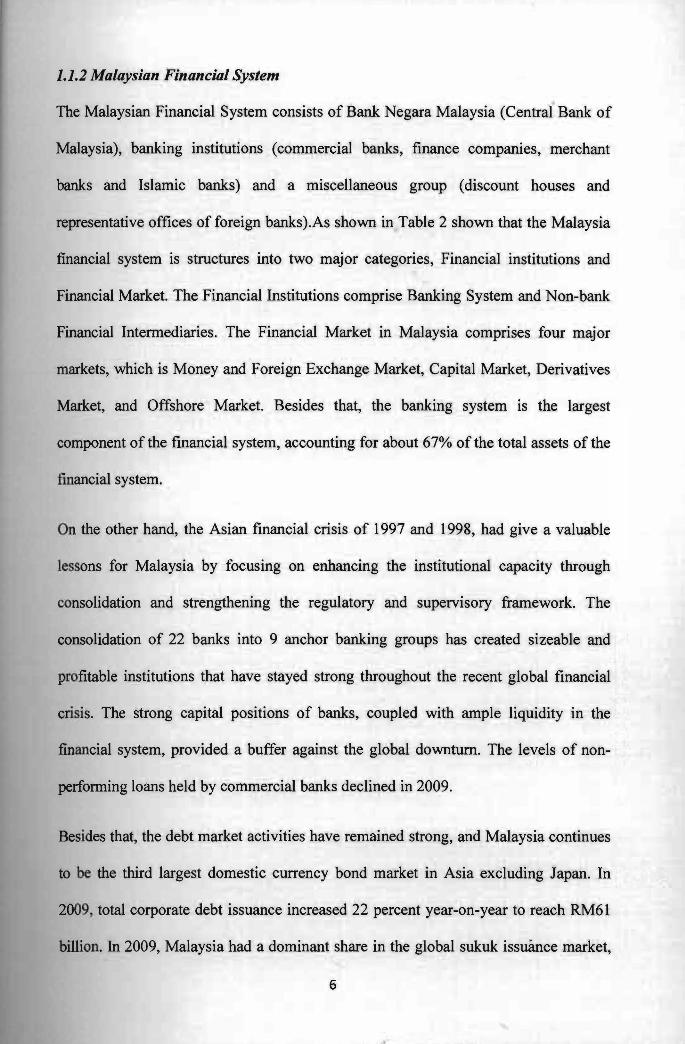

Figure 2 shows that the Malaysias GDP per capita was US$14744 and estimate that

in the Year 2011 the GDP Per Capita will increase to US$15579 As a result

Malaysia is a middle income country with the openness of economy to encourage the

foreign investor to invest in the country

Figure 2 Malaysia GDP Per Capita (US$)

Malaysia GOP Per Capita (US$)

$16000 $15579

-+-GDP Per Capita (USS)

$11000

$10000

2006 2007 2008 2009 2010 2011

5

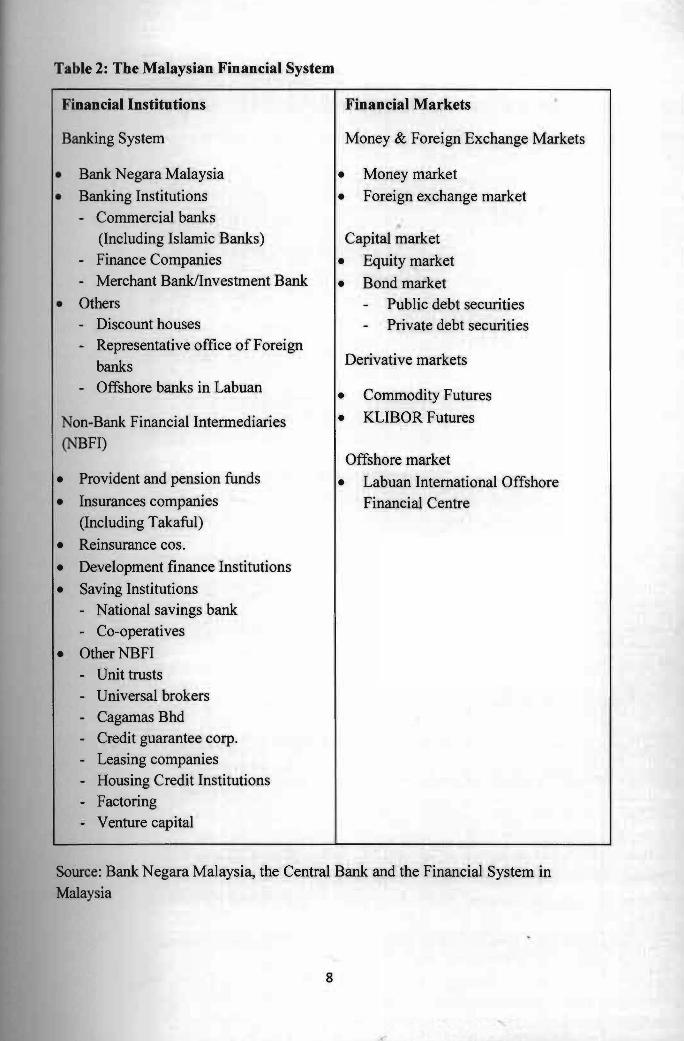

112 Malaysian Financial System

The Malaysian Financial System consists of Bank Negara Malaysia (Central Bank of

Malaysia) banking institutions (commercial banks finance companies merchant

banks and Islamic banks) and a miscellaneous group (discount houses and

representative offices of foreign banks)As shown in Table 2 shown that the Malaysia

fmancial system is structures into two major categories Financial institutions and

Financial Market The Financial Institutions comprise Banking System and Non-bank

Financial Intermediaries The Financial Market in Malaysia comprises four major

markets which is Money and Foreign Exchange Market Capital Market Derivatives

Market and Offshore Market Besides that the banking system is the largest

component of the financial system accounting for about 67 of the total assets of the

fmancial system

On the other hand the Asian financial crisis of 1997 and 1998 had give a valuable

lessons for Malaysia by focusing on enhancing the institutional capacity through

consolidation and strengthening the regulatory and supervisory framework The

consolidation of 22 banks into 9 anchor banking groups has created sizeable and

profitable institutions that have stayed strong throughout the recent global financial

crisis The strong capital positions of banks coupled with ample liquidity in the

financial system provided a buffer against the global downturn The levels of nonshy

perfonning loans held by commercial banks declined in 2009

Besides that the debt market activities have remained strong and Malaysia continues

to be the third largest domestic currency bond market in Asia excluding Japan In

2009 total corporate debt issuance increased 22 percent year-on-year to reach RM61

billion In 2009 Malaysia had a dominant share in the global sukuk issuance market

6

~~~-~------------- ---shy

accounting for 47 percent of the global market Malaysia also has the largest Islamic

fund management industry in the world in terms of number of funds and is

recognised as a centre for product innovation in the realm of Islamic finance The

growth of Islamic finance owes much to the strong legal and regulatory framework

that has been established here In addition Malaysia has been recognised

internationally for its regulatory environment

Overall Malaysias financial services sector has enhanced its domestic

competitiveness and broadened its activities However some segments like banking

are maturing With a population of 28 million people the domestic market lacks the

necessary critical mass to further develop these segments Going forward there is a

need to look externally for growth and to develop new engines of growth

7

Table 2 The Malaysian Financial System

Financial Institutions

Banking System

bull Bank Negara Malaysia

bull Banking Institutions - Commercial banks

(Including Islamic Banks) - Finance Companies - Merchant BankInvestment Bank

bull Others - Discount houses bull Representative office of Foreign

banks - Offshore banks in Labuan

Non-Bank Financial Intermediaries (NBFI)

I

bull Provident and pension funds

bull Insurances companies (Including Takaful)

bull Reinsurance cos bull Development finance Institutions

bull Saving Institutions bull National savings bank - Co-operatives

bull OtherNBFI - Unit trusts - Universal brokers - Cagamas Bhd - Credit guarantee corp bull Leasing companies - Housing Credit Institutions - Factoring - Venture capital

Financial Markets

Money amp Foreign Exchange Markets

bull Money market bull Foreign exchange market

Capital market

bull Equity market

bull Bond market Public debt securities Private debt securities

Derivative markets

bull Commodity Futures

bull KUBOR Futures

Offshore market

bull Labuan International Offshore Financial Centre

Source Bank Negara Malaysia the Central Bank and the Financial System in Malaysia

8

113 Challenges in Malaysian Financial Sector

There are some challenges that being faced by the Malaysia financial sectors First

the industry has gone through a phase of consolidation the segment such as

investment banking and brokerage remain fragmented Besides that many of the

Malaysian banks are still significantly smal1er than regional powerhouses Apart from

this there is lack critical mass to attract significant levels of investment in Malaysian

capital market

Second Malaysias financial markets are lack of liquidity and diversity in capital

markets Before the Asian financial crises in 1997 and 1998 the capital markets have

lost some of their vitalities Moreover Malaysias liquidity ranking in Asia has

dropped from 3rd in 1996 to 14th in 2010 (The World Factbook) Between there is

also limited diversity in the market in tenns of investors products or currency

Third the level of personal financial literacy is low thus the growing consumerism as

well as changing in customer expectations There is a need to reinforce better

management towards their personal finances in order to achieve high income

economy Lastly the competition from other regional financial centres will affect the

performance of the local financial services sector Malaysia continues to face negative

perception issues due to the capital control measurement implemented during the

Asian financial crisis In addition the foreign financial centres have developed their

reputations as being open and pro-business As a result the foreign investor interest is

currently directed towards North Asia

Hence this study is to investigate and analyze the factors that affecting the financial

sector performance for the period 2006 to 2011 A question appeal from the study is

how the financial sectors services performs during the 2008 to 2009 and then after the

9

financial crisis A large number of studies on the banking sectors examme the

profitability cost efficiency and market performances of banks

The study investigates the performance of Malaysian financial services sector during

2006 to 2011 period The study focuses largely in the context of CAMEL which are

related to the capital assets management earnings and liquidity considerations

This chapter will proceed with the description of the problem statement and research

objective The significance of research will end with the research scope assumption

and limitation Chapter 2 will be focusing on the literature that related to performance

of financial sectors in Malaysia and South East Asia by various authors the definition

of CAMEL components and the relationship between the CAMEL and the

performance of the financial sectors Chapter 3 describes data and methodology

where it begins with the description of data sources and follows with the explanation

on the analysis of data As well as the components of the CAMEL and the financial

ratios used to evaluate the performances of the financial services sectors Chapter 4

represents and discusses the findings It includes analysis of data for the financial ratio

variables derived from CAMEL assumptions such as capital asset quality

management earnings and liquidity Chapter 5 concludes the research findings and

some suggestions to further refine future research on the international financial

sectors and performances of Malaysian financial sectors

12 Problem Statement

The Malaysian financial sector plays a crucial role in the economy Therefore the

instability of the financial sector will affect the economy development and overall

countrys development Mansor (2007) states that financial liberalization has been a

financial feature in many nations to develop and liberalize financial markets This

10

follows the argument that the development of the financial sector can promote growth

The economic growth will encourage more financial institutions financial products

and services emerge in the markets in response to the higher demand of financial

services

However the presence financial institutions in the Malaysia financial sector raised

some challenges which are lack of scale lack of liquidity and diversity in capital

market low levels of financial literacy and competitions from other regional financial

centre Lensik R amp Hennes N (2004) claims that the entrance of foreign investors

had increased the market competitions and improves the quality and the availability of

foreign financial institution and motivate the local financial institutions to enhance

their efficiency and increase the diversity and quality of financial services The

restructuring of the financial system policy by the Malaysian government after the

economic recession during had brought the important of the growth for local financial

development

As a result it is important to analyze the important of financial services sector in

Malaysia because of the stability of the financial services sector will encourage

economic growth and fast growing for a country development Apart from that

different structure and characteristics of financial institutions and the different

influence of external factors on these financial institutions will lead to differences

perfonnances between the financial services for instance the differences of

performances among commercial bank investment companies insurance companies

and stock broker In order to evaluate the financial sectors perfonnances the CAMEL

method was applied and as supervision tool and measure the banks current overall

financial managerial operational and compliance perfonnance The empirical

11

analysis will assists the financial institutions expand their financial services to the

international market to gain greater profit

The study is to identify what kind of factors will affect the performance of the

financial sector Besides that the relationship between the performance of the

fmancial sectors and the factors will be examined and analyzed in this study

Although there are many study had been done to analyze the financial sector around

the world based on the economic development and the financial indicators However

the study will use the financial ratios to analyze the performance of financial

institution as shown in the Table 1 based on the CAMEL approach on 26 financial

institutions comprising 4 commercial bank 6 insurance companies 13 investment

holding companies stock broking company finance company and the exchange

holding company

13 Theoretical Framework

131 Agency Theory

Agency theory or agency relationship is the theory which concern to the relationships

between the owners of the company in the form of shareholders (equity investors) and

those appointed to in charge for the company management which is a director of the

company The agency theory plays a crucial role for every aspects of the business

activity especially for the decision-making by directors which included executive and

non-executive directors) In addition the agency concepts had became more important

due to the global financial crisis especially the corporate collapses of the major

multinational companies for instance Enron 2001 WorldCom 2001 and Lehman

brothers 2008 and nationalization of many financial institutions

12

The theory stated that the owner of the company assigns the day to day decision

making to the directors who are shareholders agent Besides that the agents are no

necessary to make decisions according to best interest of the principal The personal

interests of companys senior managers can differ from the company shareholders

The manager and the owner of the company are differing to each other As a result

the board of director of the company plays a crucial role in balancing and control the

action of the senior management who control day to day operation of the company

and on the shareholders behalf

Apart from that the agency relationship occurred because of the different goals and

interests among the agents and the principals Bohren (1998) assumed that the

individual agents and principal that involved in the agency relationship are

opportunistic due to they are aiming to maximize their own interest Thus there is no

guarantee that agents will always act in the best interest for their principals Therefore

if the company unable to manage their agency problem in their company so it will

affect the company performance due to agents will only aim to maximize their own

interest from the company

132 Characteristics ofAgency Problems in Financial Institutions

According to the theory of the firm which views a firm as a nexus of contract

between parties and with conflicting interests (Jensen and Mekling 1976) the agency

problem may occurred among all stacks holders within the company However the

agency problem generally refers to conflicts of interest between firms management

(agent) and its owner (principal) Also the corporate governance is widely accepted

as a mechanism that makes the management (agent) operate the firms not for him own

sake but for the interest of the owner (principal) According to the work Fama and

13

Jensen (1983) which views an owner as a residual risk bearer and residual

claimholder a shareholder generally refers to the owner as who bears the residual

risk There is a substantial research studying the agency problem focusing on the

problems between companys shareholders and management

However the agency problem is not limited to the shareholders and management but

extends to the companys stakeholders One of the most critical is the conflicts of

interest between shareholders and debtholders In a company only after interest and

other payments are paid to its debtholders then shareholders hold unlimited claims

for the remainder On the other hand debtholders have fixed size senior claims to the

companys cash flows This arrangement creates incentives for shareholders to pursue

high-risk-high-return businesses to raise the expected value of residual claims This

may transfer wealth from debtholders to shareholders which goes against the

debtholders interest

The agency problem between the shareholders and debtholders is more important in

financial institutions because they hold their customers funds as debt and therefore

customers are debtholders This distinguishes the agency problem in financial

institutions form other types of firms for instances ordinary manufacturing

companies In a commercial bank fixed claims are widely dispersed among many

small deposit holders In this situation due to the well-known free rider problem

each deposit holder has little incentive to monitor and control business decisions made

by shareholders or managements In addition the protection for deposited principal

exacerbates this type of moral hazard Therefore potential agency costs incurred

between shareholders and debtholders can be significantly large

14

Therefore for the sake of corporate governance of a financial institution it is not

sufficient to align only the interests of shareholders or management It is also

important to align the interest of shareholders or management and customers by

preventing from institutions the venturing excess high-risk-high-retum businesses

with customer deposit A possible solution is found in market discipline from

competition where customers pay enough attention when choosing a financial

institution or product However the complexity and information asymmetry which lie

in financial products can hamper the effective operation of market discipline The

other possible option is to strengthen the monitoring and discipline of managements

decision making by customers However this is not realistic considering the

customers lack of expertise and the aforementioned free rider problem In the end

the government may have to step in and represent the interest of customers and

taxpayers by monitoring and disciplining the decision making at financial firms In

todays market this takes the form of regulations and supervision over financial firms

lIDs provides partial explanation why regulations and supervision over the financial

industry are generally stronger than those over the general manufacturing industry

14 Conceptual Framework

Figure 3 shows that the diagram of the determinants for the performance of the

financial sector in Malaysia The independent variables comprise the financial

institutions capital adequacy asset quality management earning and liquidity

Furthermore the dependent variables are Return on Asset (ROA) and Return on

Equity (ROE) The performance of the financial sector will evaluate by using the

financial ratio The capital adequacy is related to the overall financial leverage of the

firms The high financial leverage will experience more volatile earni~g behavior As

15

Pu J ~ 4

UNJVERSJll - en ~ MALAy LA SARAWAK

PKHIOMAT MAKLUMAT AKAOEMIK

11111 nllfli~rlllllllill 1000246523

FACTORS AFFECTING THE PERFORMANCE OF FINANCIAL SECTOR IN MALAYSIA

BONG LIE LIN

A dissertation submitted in partial fulfillment of the requirements for the degree of Corporate Master in Business Administration

Faculty of Economics and Business UNIVERSITI MALAYSIA SARA W AK

2012

I

ABSTRACT

0his paper is to analyze and detennine the factors that affecting the financial sector

perfonnance in Malaysia for the period of five years from year 2006 to 2011 From

the study the result shows that the perfonnance of Malaysian financial sector is

stable and quite profitable because of systematic Malaysian financial systems

regulations and the strong financial capital However the global financial crisis

occurred during year 2008 to 2009 was affected the financial sector globally and

affected the financial institutions service qualit~ The study will use the financial

ratios and apply the CAMEL Model namely Capital adequacy Asset quality

Management Earnings and Liquidity to detennine the factors affecting the financial

sector perfonnance So in order to identify the detenninants of perfonnance of

Malaysian financial sector during 2006 to 2011 this study has chosen mUltiple

regression analysis Besides that the dependent variables are consisting profitability

ratio which Return on Assets (ROA) and Return on Equity (ROE) then independent

variables are the CAMEL Methods So from the study the results also shows that the

ROA and ROE are depends on the CAMEL Lastly there are a significant

relationship between the dependent variables and the independent variables

ACKNOWLEDGEMENT

My highest and more sincere appreciation goes to my beloved parents and my

families who have always encouraged and guided me to be independent never try to

limit my aspirations

I would like to express my great appreciation to my supervisor Dr Chu Ei Yet for his

understanding attention kindness and encouragement His supervision idea

guidance and critics of the research paper have been an enormous help Words alone

Icannot be expressed my greatest appreciation and thanks to him

I would like to express my high appreciation to my all lectures of Faculty Economics

and Business especially lecturers of Finance Thanks again to everyone including

those who I have probably forgotten to mention here

I

ii

Pusat Khidmat MakJumat Akademik UNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENT

ABSTRACT i

AKNOWLEDGEMENT ii

TABLE OF CONTENT iii

LIST OF FIGURES v

LIST OF TABLES v

LIST OF ABBREVIATIONS vi

1 INTRODUCTION

11 Background 1

111 Malaysian Gross Domestic Product (GDP) 4

112 Malaysian Financial System Challenges in Malaysian Financial

Sector 6

113 Challenges in Malaysian Financial Sector 9

12 Problem Statement 10

13 Theoretical Framework 12

131 Agency Theory 12

132 Characteristics ofAgency Problems in Financial Institutions 13

14 Conceptual Framework 15

15 Scope of the Study 16

16 Research Objectives 17

161 General Objective 17

162 Specific Objectives 18

17 Significance of the Study 18

18 Organization of the Study 19

19 Conclusion 20

2 LITERATURE REVIEW

21 Introduction 21

22 Literature review on CAMEL Approach 22

23 Financial Institutions Rating in Malaysia 24

231 Capital Adequacy 24

232 Asset Quality 26

233 Management 29

iii

234 Earnings 30

235 Liquidity 31

24 Empirical Literature Determinants of Financial Institutions

Profitability 32

3 METHODOLOGY

31 Introduction 34

32 Data 35

33 Sample 35

34 Variables used in the study 36

341 Dependent variables 36

342 Independent variables 36

35 Empirical Model 43

36 Concluding Remarks 44

37 Conclusions 45

4 FINDINGS AND CONCLUSION

41 Introduction 46

42 Descriptive Analysis 46

421 Descriptive Analysisor the Dependent and Independent

Variables 46

422 Trend Analysis 48

4221 Return on Asset (ROA) 48

4222 Return on Equity (ROE) 49

43 Correlation Analysis 49

44 Model Summary and coefficient Analysis 52

441 Model Summary 52

442 Coefficient Analysis 0ROA 53

45 Chapter summary 56

5 CONCLUSION AND RECOMMENDATIONS

51 Introduction 57

52 Summary of Findings 57

53 Recommendations and Suggestions 59

REFERENCES 61

iv

I

LIST OF FIGURE

Figure 1 Malaysia Real Growth Rate 5

Figure 2 Malaysia GDP Per Capita (US$) 5

Figure 3 The Conceptual Framework for Financial Sector Performance 16

Figure 4 Trend Analysis ofROA of Malaysian Financial Sector 48

Figure 5 Trend Analysis of ROE of Malaysian Financial Sector 49

LIST OF TABLES

Table 1 List of Financiallnstitutions as Public Listed in Bursa Saham Malaysia 4

Table 2 The Malaysian Financial System 8

Table 3 Independent Variables and their Proxies 42

Table 4 Descriptive Analysis for the Dependent and Independent Variables 47

Table 5 Correlation between ROA and all ratios 50

Table 6 Correlation between ROE and all ratios 51

Table 7 Summary of Analysis Return on Assets (ROA) and Return on

Equity (ROE) 52

Table 8 Coefficient Analysis and Collinearity Statistic (ROA) 54

Table 9 Coefficient Analysis and Collinearity Statistic (ROE) 55

v

ASST

BNMlGP8

CAP

CTD

EARN

FDI

FDIC

FIs

GDP

LIQ

LPI

LTD

MARC

MBSB

MNGT

MNRB

NPL

OLS

RHB

ROA

ROE

LIST OF ABBREVIATIONS

Asset Quality

Financial Reporting for Licensed Institutions

Capital Adequacy

Cash to Deposit

Earnings

Foreign Direct Investment

Federal Deposit Insurance Corporation

Financial Institutions

Malaysian Gross Domestic Product

Liquidity

Lonpac Insurance

Loan to Deposit

Malaysian Rating Corporation Berhad

Malaysia Building society Berhad

Management

Malaysian Reinsurance Berhad

Not Performing Loan

Ordinary Least Squares

Rashid Hussein Bank

Return on Assets

Return on Equity

vi

1

-==

I

RWCR Risk Weighted Capital Ratio

VIF Variance Inflation Factor

vii

CHAPTER 1

INTRODUCTION

11 Background

The global financial crisis from 2008 t02009 had brought huge impact for the world

economy due to the price of the assets which has been over inflated and caused the

sub-prime mortgage booming and exploding into housing and banking crisis with a

cascading effect on consumer and investment demand In addition the financial market

becomes panic due to the subprime mortgages and the failures of Lehman Brothers

and Washington Mutual in United States The government of United States had

implemented some solutions and actions to reduce the panics during the first half of

October by promoting the liquidity and the solvency of the financial sector reducing

the prices for the asset classes and the commodities the cost of the corporate and the

bank borrowing rose significantly and high volatility in financial market which

increasing infrequently In the case of Malaysian economy the countrys economy was

sheltered from the direct effects of financial exposure because the new derivatives were

not allowed into the country The global financial crisis may result the Governments

plans to achieve vision 2020 being interrupted because of decreasing in the exports and a

slowdown in foreign direct investment (FDI)

The financial services sector is the bedrock of any economy It is the key to the overall

economy by providing various fonns of capital to enable the growth of other

industries in the economy All large and successful economies require strong banks

system vibrant capital markets and well-functioning financial infrastructures

Moreover the sector is also a core component in a services-based economy and a key

growth engine in its own right As demonstrated by the emergence of international

1

___--==========-=-----------=---=------- ---_

II

shy

financial services centres worldwide the financial sector growth comes from serving

domestic businesses and consumers as well as tapping external markets and sources of

funds

Mansor (2007) states that financial liberalization and development has been the major

financial feature in many developing countries Malaysia is a highly open economic

country and it also witnesses a respectable economic growth and rapid financial

development since the introducing of Financial Sector Masterplan in 2001 the

Malaysian financial sector has undergone significant transformation and progress The

banking sector especially has undergone restructuring consolidation and

rationalization Moreover the flexibility and the performance of the financial

landscaping had been improved due to the transformation and deregulation and

liberalization Moreover a stable and effective financial sector will affect the

performance of the financial sector and it will become an important pillar of strength

in our economy

Schumpeter (1911) contends that the services provided by the financial intermediaries

are essential drivers for innovation and growth Well developed financial systems

channel financial resources to the most productive use Malaysias Prime Minister

Dato Sri Mohd Najib bin Tun Hj Abdul Razak states that financial sector in Malaysia

is expected to have a greater role in assisting the economic growth as Malaysia transit

towards achieving a developed economy status by year 2020 The financial sector is

able to assist the economy growth and encourage the economy transformation into the

next phase of development and provide the world class high value added financial

products and services at the competitive prices and speed up the new economic

sectors In order to enhance the economys expansion Government has taken the

2

initiatives to promote structural change within the economy and diversify the sources

of the financial sectors growth by offering liberalisation package from 2009 to 2012

The foreign equity limits of investment banks Islamic banks insurance companies

and Takaful operators had increased from 40 percent to 70 percent The alliances will

strengthen business potential and enhance the growth of the financial institutions

through international expertise and global network foreign shareholders The rapid

growth and the strong financial sector of the country will enable the consumers to get

more infonnation between the financial service providers the regulators and the

authorities will need to provide the conducive environment that raises the consumer

empowennent The more consumers can afford and able to buy the products or

services provided by of the financial institution such as commercial bank investment

company or insurances company will positively affect the perfonnance of the

financial sector

As a result the financial sector plays crucial role for the economic growth and the

countrys development From Table 1 it shows that then financial sector comprises of

26 institution consisting 4 commercial bank 6 insurance company 14 investment

holding companies stock broking companies finance companies and the exchange

holding companies The lists of the financial institutions in Table 1 are public listed

on the Bursa Saham Malaysia

3

_ _ _ ____ _

Table 1 List of Financial Institutions as Public Listed in Bursa Saham Malaysia

Code in Bursa

5185

1015

1155

1295

5258

2143

6688

3379

6483

8621

6459

1236

5053

6009

4782

1066

9296

4898

1163

5097

1198

1058

6139

5088

1818 1171

Financial Insituitions

Affin Bank Bhd

Ambank(M) Bhd (AMMB)

Malayan Banking Bhd

Public bank Berhad

BIMB Holding Bhd

ECM Libra Financial Group

Hwang-DBS Malaysia Bhd

Insas Berhad

KampN Kenanga Holding Bhd

LPI Capital Bhd (Lonpac Insurance)

MNRB Holding Bhd

MBF Holding Group (MBFHLDG)

OSK Investment bank Bhd

PacificampOrient Berhad

PacificMas Bhd (PACMAS)

RHB CAPITAL

RCE Capital

T A Enterprise Bhd

Allianz Malaysia Bhd

KURASIA (Kumia Asia Bhd)

MAA

MANULIFE

TAKAFUL

APEX Equity Holding Bhd

Bursa

MBSB

Sources Share Info Bursa Malaysia

111 Malaysian Gross Domestic Product (GDP)

Type of Firms

Commercial bank

Commercial bank

Commercial bank

Commercial Bank

Investment holding company

Investment banking group

Investment company

Investment holding company

Investment company

Investment holding company

Investment holding company

Investment holding company

Investment holding company

Insurance company

Investment holding company

Investment company

Investment company

Investment holding company

Insurance company

Insurance company

Insurance company

Insurance company

Insurance company

Stock broking company

Exchange holding company

Exempt Finance Company

Malaysia is a rapidly developing economy in Asia and the financial services sector is

an integral component of the economy The total population of Malaysia was 283

million (Census 2010) Besides that Malaysias GDP has a strong growth in year

2010 as shown in the Figure 1 the Malaysia real GDP growth rate was -72 percent

--==-o---===--=-----shy

4

$15000

$14000

$13000

S12OOO

Pu ot Khidmat Maklumat Akademik UNlVERSm MALAYSIA SARAWAK

largely driven by the Services sector and Manufacturing sectors of 68 percent and

114 percent respectively (Department of Statistic Malaysia 201 O)This is the positive

sign for the country since 2008 and 2009 which real GDP growth rate was -16

percent and 47 percent (CIA World Factbook)

Figure 1 Malaysia Real Growth Rate

GDP Growth Rate

800 1 700

6 00

5 00

j2006 2007 2008 2011

520~ 400

300 ~GDP Growth Rate

200

1 00

000

-100

-2 00

Figure 2 shows that the Malaysias GDP per capita was US$14744 and estimate that

in the Year 2011 the GDP Per Capita will increase to US$15579 As a result

Malaysia is a middle income country with the openness of economy to encourage the

foreign investor to invest in the country

Figure 2 Malaysia GDP Per Capita (US$)

Malaysia GOP Per Capita (US$)

$16000 $15579

-+-GDP Per Capita (USS)

$11000

$10000

2006 2007 2008 2009 2010 2011

5

112 Malaysian Financial System

The Malaysian Financial System consists of Bank Negara Malaysia (Central Bank of

Malaysia) banking institutions (commercial banks finance companies merchant

banks and Islamic banks) and a miscellaneous group (discount houses and

representative offices of foreign banks)As shown in Table 2 shown that the Malaysia

fmancial system is structures into two major categories Financial institutions and

Financial Market The Financial Institutions comprise Banking System and Non-bank

Financial Intermediaries The Financial Market in Malaysia comprises four major

markets which is Money and Foreign Exchange Market Capital Market Derivatives

Market and Offshore Market Besides that the banking system is the largest

component of the financial system accounting for about 67 of the total assets of the

fmancial system

On the other hand the Asian financial crisis of 1997 and 1998 had give a valuable

lessons for Malaysia by focusing on enhancing the institutional capacity through

consolidation and strengthening the regulatory and supervisory framework The

consolidation of 22 banks into 9 anchor banking groups has created sizeable and

profitable institutions that have stayed strong throughout the recent global financial

crisis The strong capital positions of banks coupled with ample liquidity in the

financial system provided a buffer against the global downturn The levels of nonshy

perfonning loans held by commercial banks declined in 2009

Besides that the debt market activities have remained strong and Malaysia continues

to be the third largest domestic currency bond market in Asia excluding Japan In

2009 total corporate debt issuance increased 22 percent year-on-year to reach RM61

billion In 2009 Malaysia had a dominant share in the global sukuk issuance market

6

~~~-~------------- ---shy

accounting for 47 percent of the global market Malaysia also has the largest Islamic

fund management industry in the world in terms of number of funds and is

recognised as a centre for product innovation in the realm of Islamic finance The

growth of Islamic finance owes much to the strong legal and regulatory framework

that has been established here In addition Malaysia has been recognised

internationally for its regulatory environment

Overall Malaysias financial services sector has enhanced its domestic

competitiveness and broadened its activities However some segments like banking

are maturing With a population of 28 million people the domestic market lacks the

necessary critical mass to further develop these segments Going forward there is a

need to look externally for growth and to develop new engines of growth

7

Table 2 The Malaysian Financial System

Financial Institutions

Banking System

bull Bank Negara Malaysia

bull Banking Institutions - Commercial banks

(Including Islamic Banks) - Finance Companies - Merchant BankInvestment Bank

bull Others - Discount houses bull Representative office of Foreign

banks - Offshore banks in Labuan

Non-Bank Financial Intermediaries (NBFI)

I

bull Provident and pension funds

bull Insurances companies (Including Takaful)

bull Reinsurance cos bull Development finance Institutions

bull Saving Institutions bull National savings bank - Co-operatives

bull OtherNBFI - Unit trusts - Universal brokers - Cagamas Bhd - Credit guarantee corp bull Leasing companies - Housing Credit Institutions - Factoring - Venture capital

Financial Markets

Money amp Foreign Exchange Markets

bull Money market bull Foreign exchange market

Capital market

bull Equity market

bull Bond market Public debt securities Private debt securities

Derivative markets

bull Commodity Futures

bull KUBOR Futures

Offshore market

bull Labuan International Offshore Financial Centre

Source Bank Negara Malaysia the Central Bank and the Financial System in Malaysia

8

113 Challenges in Malaysian Financial Sector

There are some challenges that being faced by the Malaysia financial sectors First

the industry has gone through a phase of consolidation the segment such as

investment banking and brokerage remain fragmented Besides that many of the

Malaysian banks are still significantly smal1er than regional powerhouses Apart from

this there is lack critical mass to attract significant levels of investment in Malaysian

capital market

Second Malaysias financial markets are lack of liquidity and diversity in capital

markets Before the Asian financial crises in 1997 and 1998 the capital markets have

lost some of their vitalities Moreover Malaysias liquidity ranking in Asia has

dropped from 3rd in 1996 to 14th in 2010 (The World Factbook) Between there is

also limited diversity in the market in tenns of investors products or currency

Third the level of personal financial literacy is low thus the growing consumerism as

well as changing in customer expectations There is a need to reinforce better

management towards their personal finances in order to achieve high income

economy Lastly the competition from other regional financial centres will affect the

performance of the local financial services sector Malaysia continues to face negative

perception issues due to the capital control measurement implemented during the

Asian financial crisis In addition the foreign financial centres have developed their

reputations as being open and pro-business As a result the foreign investor interest is

currently directed towards North Asia

Hence this study is to investigate and analyze the factors that affecting the financial

sector performance for the period 2006 to 2011 A question appeal from the study is

how the financial sectors services performs during the 2008 to 2009 and then after the

9

financial crisis A large number of studies on the banking sectors examme the

profitability cost efficiency and market performances of banks

The study investigates the performance of Malaysian financial services sector during

2006 to 2011 period The study focuses largely in the context of CAMEL which are

related to the capital assets management earnings and liquidity considerations

This chapter will proceed with the description of the problem statement and research

objective The significance of research will end with the research scope assumption

and limitation Chapter 2 will be focusing on the literature that related to performance

of financial sectors in Malaysia and South East Asia by various authors the definition

of CAMEL components and the relationship between the CAMEL and the

performance of the financial sectors Chapter 3 describes data and methodology

where it begins with the description of data sources and follows with the explanation

on the analysis of data As well as the components of the CAMEL and the financial

ratios used to evaluate the performances of the financial services sectors Chapter 4

represents and discusses the findings It includes analysis of data for the financial ratio

variables derived from CAMEL assumptions such as capital asset quality

management earnings and liquidity Chapter 5 concludes the research findings and

some suggestions to further refine future research on the international financial

sectors and performances of Malaysian financial sectors

12 Problem Statement

The Malaysian financial sector plays a crucial role in the economy Therefore the

instability of the financial sector will affect the economy development and overall

countrys development Mansor (2007) states that financial liberalization has been a

financial feature in many nations to develop and liberalize financial markets This

10

follows the argument that the development of the financial sector can promote growth

The economic growth will encourage more financial institutions financial products

and services emerge in the markets in response to the higher demand of financial

services

However the presence financial institutions in the Malaysia financial sector raised

some challenges which are lack of scale lack of liquidity and diversity in capital

market low levels of financial literacy and competitions from other regional financial

centre Lensik R amp Hennes N (2004) claims that the entrance of foreign investors

had increased the market competitions and improves the quality and the availability of

foreign financial institution and motivate the local financial institutions to enhance

their efficiency and increase the diversity and quality of financial services The

restructuring of the financial system policy by the Malaysian government after the

economic recession during had brought the important of the growth for local financial

development

As a result it is important to analyze the important of financial services sector in

Malaysia because of the stability of the financial services sector will encourage

economic growth and fast growing for a country development Apart from that

different structure and characteristics of financial institutions and the different

influence of external factors on these financial institutions will lead to differences

perfonnances between the financial services for instance the differences of

performances among commercial bank investment companies insurance companies

and stock broker In order to evaluate the financial sectors perfonnances the CAMEL

method was applied and as supervision tool and measure the banks current overall

financial managerial operational and compliance perfonnance The empirical

11

analysis will assists the financial institutions expand their financial services to the

international market to gain greater profit

The study is to identify what kind of factors will affect the performance of the

financial sector Besides that the relationship between the performance of the

fmancial sectors and the factors will be examined and analyzed in this study

Although there are many study had been done to analyze the financial sector around

the world based on the economic development and the financial indicators However

the study will use the financial ratios to analyze the performance of financial

institution as shown in the Table 1 based on the CAMEL approach on 26 financial

institutions comprising 4 commercial bank 6 insurance companies 13 investment

holding companies stock broking company finance company and the exchange

holding company

13 Theoretical Framework

131 Agency Theory

Agency theory or agency relationship is the theory which concern to the relationships

between the owners of the company in the form of shareholders (equity investors) and

those appointed to in charge for the company management which is a director of the

company The agency theory plays a crucial role for every aspects of the business

activity especially for the decision-making by directors which included executive and

non-executive directors) In addition the agency concepts had became more important

due to the global financial crisis especially the corporate collapses of the major

multinational companies for instance Enron 2001 WorldCom 2001 and Lehman

brothers 2008 and nationalization of many financial institutions

12

The theory stated that the owner of the company assigns the day to day decision

making to the directors who are shareholders agent Besides that the agents are no

necessary to make decisions according to best interest of the principal The personal

interests of companys senior managers can differ from the company shareholders

The manager and the owner of the company are differing to each other As a result

the board of director of the company plays a crucial role in balancing and control the

action of the senior management who control day to day operation of the company

and on the shareholders behalf

Apart from that the agency relationship occurred because of the different goals and

interests among the agents and the principals Bohren (1998) assumed that the

individual agents and principal that involved in the agency relationship are

opportunistic due to they are aiming to maximize their own interest Thus there is no

guarantee that agents will always act in the best interest for their principals Therefore

if the company unable to manage their agency problem in their company so it will

affect the company performance due to agents will only aim to maximize their own

interest from the company

132 Characteristics ofAgency Problems in Financial Institutions

According to the theory of the firm which views a firm as a nexus of contract

between parties and with conflicting interests (Jensen and Mekling 1976) the agency

problem may occurred among all stacks holders within the company However the

agency problem generally refers to conflicts of interest between firms management

(agent) and its owner (principal) Also the corporate governance is widely accepted

as a mechanism that makes the management (agent) operate the firms not for him own

sake but for the interest of the owner (principal) According to the work Fama and

13

Jensen (1983) which views an owner as a residual risk bearer and residual

claimholder a shareholder generally refers to the owner as who bears the residual

risk There is a substantial research studying the agency problem focusing on the

problems between companys shareholders and management

However the agency problem is not limited to the shareholders and management but

extends to the companys stakeholders One of the most critical is the conflicts of

interest between shareholders and debtholders In a company only after interest and

other payments are paid to its debtholders then shareholders hold unlimited claims

for the remainder On the other hand debtholders have fixed size senior claims to the

companys cash flows This arrangement creates incentives for shareholders to pursue

high-risk-high-return businesses to raise the expected value of residual claims This

may transfer wealth from debtholders to shareholders which goes against the

debtholders interest

The agency problem between the shareholders and debtholders is more important in

financial institutions because they hold their customers funds as debt and therefore

customers are debtholders This distinguishes the agency problem in financial

institutions form other types of firms for instances ordinary manufacturing

companies In a commercial bank fixed claims are widely dispersed among many

small deposit holders In this situation due to the well-known free rider problem

each deposit holder has little incentive to monitor and control business decisions made

by shareholders or managements In addition the protection for deposited principal

exacerbates this type of moral hazard Therefore potential agency costs incurred

between shareholders and debtholders can be significantly large

14

Therefore for the sake of corporate governance of a financial institution it is not

sufficient to align only the interests of shareholders or management It is also

important to align the interest of shareholders or management and customers by

preventing from institutions the venturing excess high-risk-high-retum businesses

with customer deposit A possible solution is found in market discipline from

competition where customers pay enough attention when choosing a financial

institution or product However the complexity and information asymmetry which lie

in financial products can hamper the effective operation of market discipline The

other possible option is to strengthen the monitoring and discipline of managements

decision making by customers However this is not realistic considering the

customers lack of expertise and the aforementioned free rider problem In the end

the government may have to step in and represent the interest of customers and

taxpayers by monitoring and disciplining the decision making at financial firms In

todays market this takes the form of regulations and supervision over financial firms

lIDs provides partial explanation why regulations and supervision over the financial

industry are generally stronger than those over the general manufacturing industry

14 Conceptual Framework

Figure 3 shows that the diagram of the determinants for the performance of the

financial sector in Malaysia The independent variables comprise the financial

institutions capital adequacy asset quality management earning and liquidity

Furthermore the dependent variables are Return on Asset (ROA) and Return on

Equity (ROE) The performance of the financial sector will evaluate by using the

financial ratio The capital adequacy is related to the overall financial leverage of the

firms The high financial leverage will experience more volatile earni~g behavior As

15

I

ABSTRACT

0his paper is to analyze and detennine the factors that affecting the financial sector

perfonnance in Malaysia for the period of five years from year 2006 to 2011 From

the study the result shows that the perfonnance of Malaysian financial sector is

stable and quite profitable because of systematic Malaysian financial systems

regulations and the strong financial capital However the global financial crisis

occurred during year 2008 to 2009 was affected the financial sector globally and

affected the financial institutions service qualit~ The study will use the financial

ratios and apply the CAMEL Model namely Capital adequacy Asset quality

Management Earnings and Liquidity to detennine the factors affecting the financial

sector perfonnance So in order to identify the detenninants of perfonnance of

Malaysian financial sector during 2006 to 2011 this study has chosen mUltiple

regression analysis Besides that the dependent variables are consisting profitability

ratio which Return on Assets (ROA) and Return on Equity (ROE) then independent

variables are the CAMEL Methods So from the study the results also shows that the

ROA and ROE are depends on the CAMEL Lastly there are a significant

relationship between the dependent variables and the independent variables

ACKNOWLEDGEMENT

My highest and more sincere appreciation goes to my beloved parents and my

families who have always encouraged and guided me to be independent never try to

limit my aspirations

I would like to express my great appreciation to my supervisor Dr Chu Ei Yet for his

understanding attention kindness and encouragement His supervision idea

guidance and critics of the research paper have been an enormous help Words alone

Icannot be expressed my greatest appreciation and thanks to him

I would like to express my high appreciation to my all lectures of Faculty Economics

and Business especially lecturers of Finance Thanks again to everyone including

those who I have probably forgotten to mention here

I

ii

Pusat Khidmat MakJumat Akademik UNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENT

ABSTRACT i

AKNOWLEDGEMENT ii

TABLE OF CONTENT iii

LIST OF FIGURES v

LIST OF TABLES v

LIST OF ABBREVIATIONS vi

1 INTRODUCTION

11 Background 1

111 Malaysian Gross Domestic Product (GDP) 4

112 Malaysian Financial System Challenges in Malaysian Financial

Sector 6

113 Challenges in Malaysian Financial Sector 9

12 Problem Statement 10

13 Theoretical Framework 12

131 Agency Theory 12

132 Characteristics ofAgency Problems in Financial Institutions 13

14 Conceptual Framework 15

15 Scope of the Study 16

16 Research Objectives 17

161 General Objective 17

162 Specific Objectives 18

17 Significance of the Study 18

18 Organization of the Study 19

19 Conclusion 20

2 LITERATURE REVIEW

21 Introduction 21

22 Literature review on CAMEL Approach 22

23 Financial Institutions Rating in Malaysia 24

231 Capital Adequacy 24

232 Asset Quality 26

233 Management 29

iii

234 Earnings 30

235 Liquidity 31

24 Empirical Literature Determinants of Financial Institutions

Profitability 32

3 METHODOLOGY

31 Introduction 34

32 Data 35

33 Sample 35

34 Variables used in the study 36

341 Dependent variables 36

342 Independent variables 36

35 Empirical Model 43

36 Concluding Remarks 44

37 Conclusions 45

4 FINDINGS AND CONCLUSION

41 Introduction 46

42 Descriptive Analysis 46

421 Descriptive Analysisor the Dependent and Independent

Variables 46

422 Trend Analysis 48

4221 Return on Asset (ROA) 48

4222 Return on Equity (ROE) 49

43 Correlation Analysis 49

44 Model Summary and coefficient Analysis 52

441 Model Summary 52

442 Coefficient Analysis 0ROA 53

45 Chapter summary 56

5 CONCLUSION AND RECOMMENDATIONS

51 Introduction 57

52 Summary of Findings 57

53 Recommendations and Suggestions 59

REFERENCES 61

iv

I

LIST OF FIGURE

Figure 1 Malaysia Real Growth Rate 5

Figure 2 Malaysia GDP Per Capita (US$) 5

Figure 3 The Conceptual Framework for Financial Sector Performance 16

Figure 4 Trend Analysis ofROA of Malaysian Financial Sector 48

Figure 5 Trend Analysis of ROE of Malaysian Financial Sector 49

LIST OF TABLES

Table 1 List of Financiallnstitutions as Public Listed in Bursa Saham Malaysia 4

Table 2 The Malaysian Financial System 8

Table 3 Independent Variables and their Proxies 42

Table 4 Descriptive Analysis for the Dependent and Independent Variables 47

Table 5 Correlation between ROA and all ratios 50

Table 6 Correlation between ROE and all ratios 51

Table 7 Summary of Analysis Return on Assets (ROA) and Return on

Equity (ROE) 52

Table 8 Coefficient Analysis and Collinearity Statistic (ROA) 54

Table 9 Coefficient Analysis and Collinearity Statistic (ROE) 55

v

ASST

BNMlGP8

CAP

CTD

EARN

FDI

FDIC

FIs

GDP

LIQ

LPI

LTD

MARC

MBSB

MNGT

MNRB

NPL

OLS

RHB

ROA

ROE

LIST OF ABBREVIATIONS

Asset Quality

Financial Reporting for Licensed Institutions

Capital Adequacy

Cash to Deposit

Earnings

Foreign Direct Investment

Federal Deposit Insurance Corporation

Financial Institutions

Malaysian Gross Domestic Product

Liquidity

Lonpac Insurance

Loan to Deposit

Malaysian Rating Corporation Berhad

Malaysia Building society Berhad

Management

Malaysian Reinsurance Berhad

Not Performing Loan

Ordinary Least Squares

Rashid Hussein Bank

Return on Assets

Return on Equity

vi

1

-==

I

RWCR Risk Weighted Capital Ratio

VIF Variance Inflation Factor

vii

CHAPTER 1

INTRODUCTION

11 Background

The global financial crisis from 2008 t02009 had brought huge impact for the world

economy due to the price of the assets which has been over inflated and caused the

sub-prime mortgage booming and exploding into housing and banking crisis with a

cascading effect on consumer and investment demand In addition the financial market

becomes panic due to the subprime mortgages and the failures of Lehman Brothers

and Washington Mutual in United States The government of United States had

implemented some solutions and actions to reduce the panics during the first half of

October by promoting the liquidity and the solvency of the financial sector reducing

the prices for the asset classes and the commodities the cost of the corporate and the

bank borrowing rose significantly and high volatility in financial market which

increasing infrequently In the case of Malaysian economy the countrys economy was

sheltered from the direct effects of financial exposure because the new derivatives were

not allowed into the country The global financial crisis may result the Governments

plans to achieve vision 2020 being interrupted because of decreasing in the exports and a

slowdown in foreign direct investment (FDI)

The financial services sector is the bedrock of any economy It is the key to the overall

economy by providing various fonns of capital to enable the growth of other

industries in the economy All large and successful economies require strong banks

system vibrant capital markets and well-functioning financial infrastructures

Moreover the sector is also a core component in a services-based economy and a key

growth engine in its own right As demonstrated by the emergence of international

1

___--==========-=-----------=---=------- ---_

II

shy

financial services centres worldwide the financial sector growth comes from serving

domestic businesses and consumers as well as tapping external markets and sources of

funds

Mansor (2007) states that financial liberalization and development has been the major

financial feature in many developing countries Malaysia is a highly open economic

country and it also witnesses a respectable economic growth and rapid financial

development since the introducing of Financial Sector Masterplan in 2001 the

Malaysian financial sector has undergone significant transformation and progress The

banking sector especially has undergone restructuring consolidation and

rationalization Moreover the flexibility and the performance of the financial

landscaping had been improved due to the transformation and deregulation and

liberalization Moreover a stable and effective financial sector will affect the

performance of the financial sector and it will become an important pillar of strength

in our economy

Schumpeter (1911) contends that the services provided by the financial intermediaries

are essential drivers for innovation and growth Well developed financial systems

channel financial resources to the most productive use Malaysias Prime Minister

Dato Sri Mohd Najib bin Tun Hj Abdul Razak states that financial sector in Malaysia

is expected to have a greater role in assisting the economic growth as Malaysia transit

towards achieving a developed economy status by year 2020 The financial sector is

able to assist the economy growth and encourage the economy transformation into the

next phase of development and provide the world class high value added financial

products and services at the competitive prices and speed up the new economic

sectors In order to enhance the economys expansion Government has taken the

2

initiatives to promote structural change within the economy and diversify the sources

of the financial sectors growth by offering liberalisation package from 2009 to 2012

The foreign equity limits of investment banks Islamic banks insurance companies

and Takaful operators had increased from 40 percent to 70 percent The alliances will

strengthen business potential and enhance the growth of the financial institutions

through international expertise and global network foreign shareholders The rapid

growth and the strong financial sector of the country will enable the consumers to get

more infonnation between the financial service providers the regulators and the

authorities will need to provide the conducive environment that raises the consumer

empowennent The more consumers can afford and able to buy the products or

services provided by of the financial institution such as commercial bank investment

company or insurances company will positively affect the perfonnance of the

financial sector

As a result the financial sector plays crucial role for the economic growth and the

countrys development From Table 1 it shows that then financial sector comprises of

26 institution consisting 4 commercial bank 6 insurance company 14 investment

holding companies stock broking companies finance companies and the exchange

holding companies The lists of the financial institutions in Table 1 are public listed

on the Bursa Saham Malaysia

3

_ _ _ ____ _

Table 1 List of Financial Institutions as Public Listed in Bursa Saham Malaysia

Code in Bursa

5185

1015

1155

1295

5258